Embed Size (px)

Citation preview

Great Political and Economic Thinkers:Theory and Reality

Lectures by Robert M. CoenEmeritus Professor of Economics

Northwestern University

November 11 and 18, 2014

Web site: faculty.wcas.northwestern.edu/~rcoen

Email: [email protected]

November 11

20th Century Revolution in Economic Thinking: John Maynard Keynes

November 18

Counterrevolution to Keynes

and Critiques of Activist Economic Policies:

Hayek, Friedman, Lucas, and Others

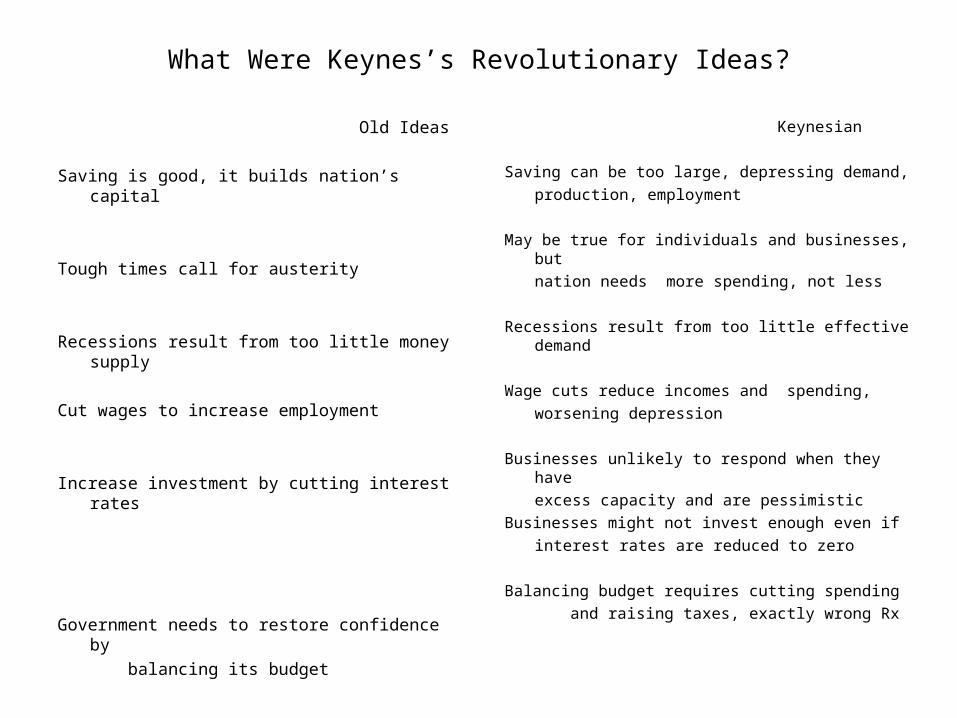

What Were Keynes’s Revolutionary Ideas?

Old Ideas

Saving is good, it builds nation’s capital

Tough times call for austerity

Recessions result from too little money supply

Cut wages to increase employment

Increase investment by cutting interest rates

Government needs to restore confidence by

balancing its budget

Keynesian

Saving can be too large, depressing demand,

production, employment

May be true for individuals and businesses, but

nation needs more spending, not less

Recessions result from too little effective demand

Wage cuts reduce incomes and spending,

worsening depression

Businesses unlikely to respond when they have

excess capacity and are pessimistic

Businesses might not invest enough even if

interest rates are reduced to zero

Balancing budget requires cutting spending

and raising taxes, exactly wrong Rx

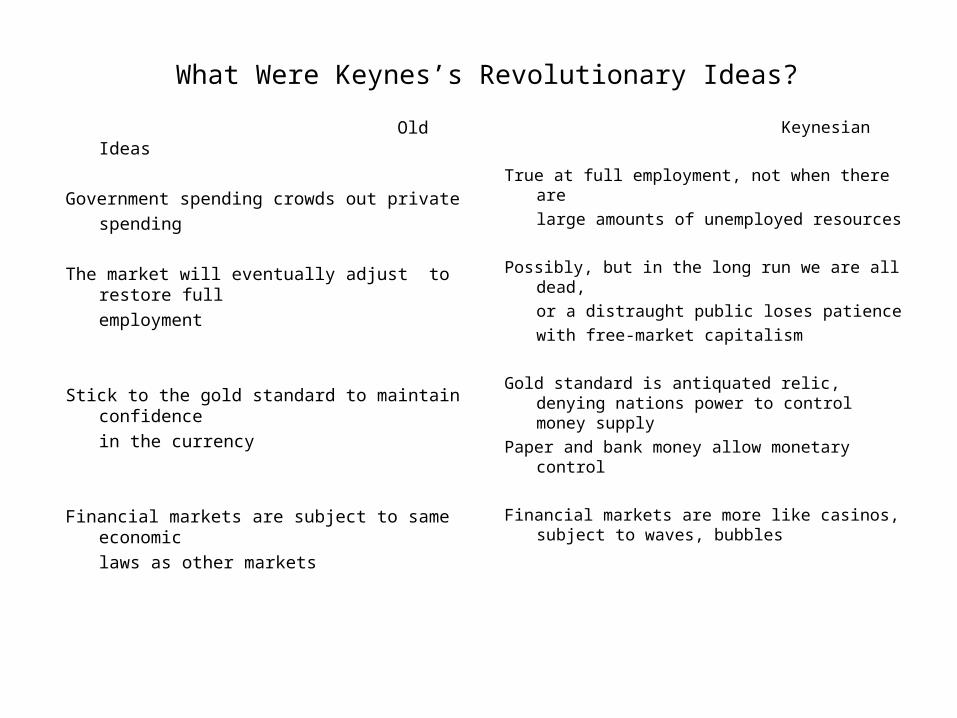

What Were Keynes’s Revolutionary Ideas?

Old Ideas

Government spending crowds out private

spending

The market will eventually adjust to restore full

employment

Stick to the gold standard to maintain confidence

in the currency

Financial markets are subject to same economic

laws as other markets

Keynesian

True at full employment, not when there are

large amounts of unemployed resources

Possibly, but in the long run we are all dead,

or a distraught public loses patience

with free-market capitalism

Gold standard is antiquated relic, denying nations power to control money supply

Paper and bank money allow monetary control

Financial markets are more like casinos, subject to waves, bubbles

Member of the cultured British elite, widely admired

Why was Keynes such an effective revolutionary leader?

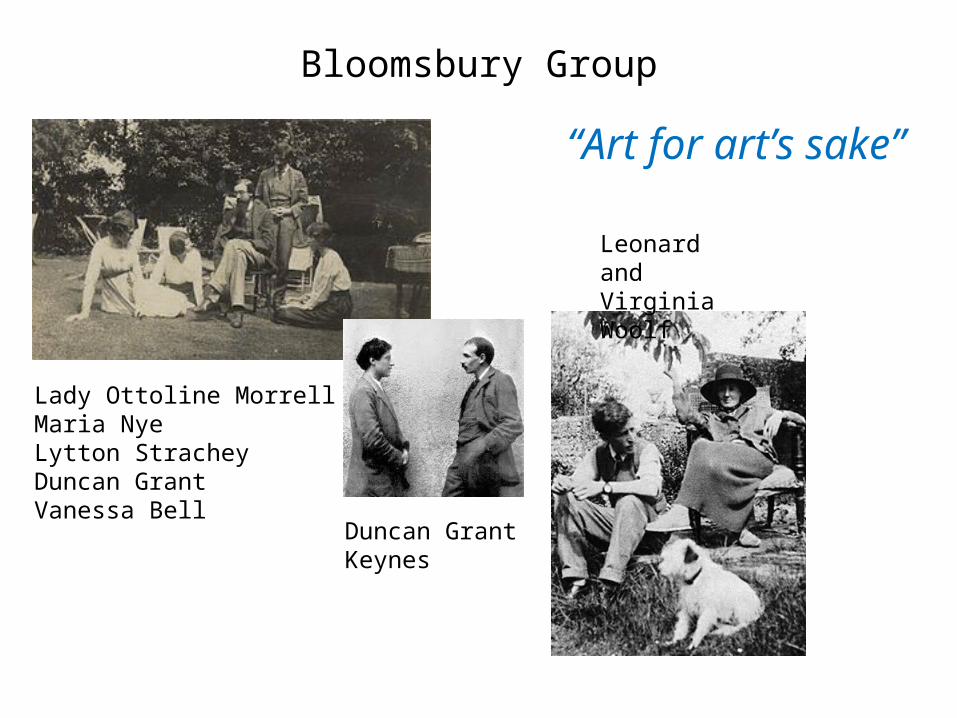

Bloomsbury Group

Lady Ottoline MorrellMaria NyeLytton StracheyDuncan GrantVanessa Bell

Duncan GrantKeynes

Leonard andVirginia Woolf

“Art for art’s sake”

Member of the cultured British elite, widely admired

Leader of the academic economic establishmentBest student of the world’s leading economist, Alfred MarshallEditor of the major international professional publication in

economics, the Economic Journal

A highly successful investor

Why was Keynes such an effective revolutionary leader?

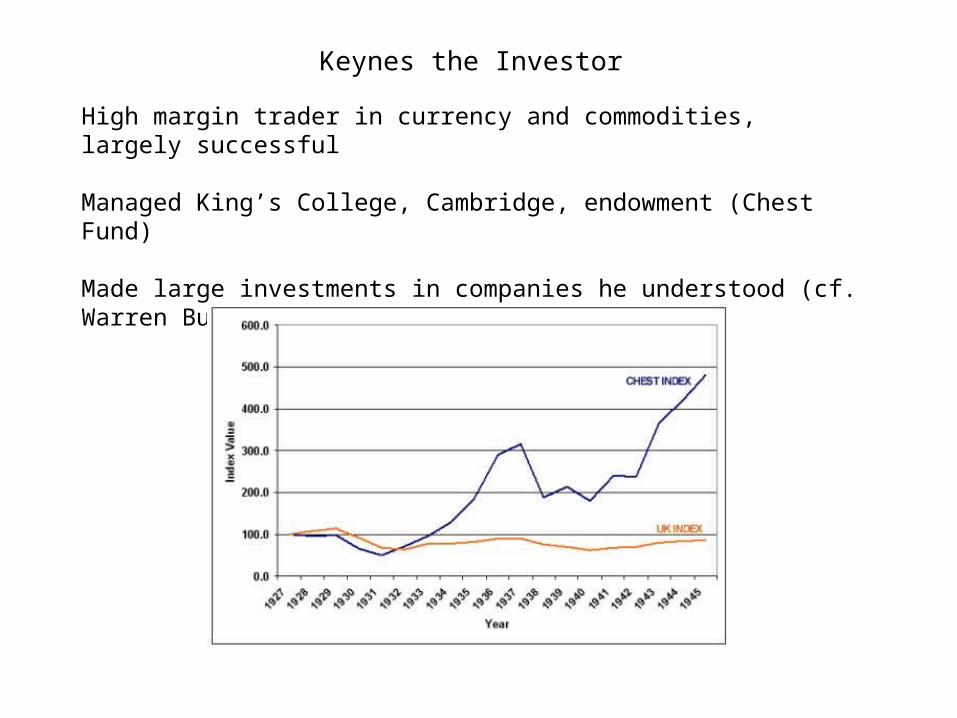

Keynes the Investor

High margin trader in currency and commodities, largely successful

Managed King’s College, Cambridge, endowment (Chest Fund)

Made large investments in companies he understood (cf. Warren Buffett)

Member of the cultured British elite, widely admired

Leader of the academic economic establishmentBest student of the world’s leading economist, Alfred MarshallEditor of the major international professional publication in

economics, the Economic Journal

A highly successful investor

Eloquent writer/expositor/debater

Man of affairs: Active in government service and as policy critic

Analyses of current problems on the markForesaw that Treaty of Versailles was a disasterPredicted UK return to gold in 1924 would abort economic recoverySaw that government austerity would worsen depression

Wanted to preserve capitalism, not destroy it

Why was Keynes such an effective revolutionary leader?

Triumph of Keynesianism

Massive debt-financed spending in World War II restores full employment

Alvin Hansen introduces Keynesian at Harvard in late 1930’s

Congress passes Employment Act of 1946

In 1948, Paul Samuelson (Nobel Prize, 1970), one of Hansen’s students, publishes first intro text incorporating Keynesian ideas, a best seller

Jan Tinbergen (Nobel Prize, 1969), Lawrence Klein (Nobel Prize, 1980), build first Keynesian-oriented macro-econometric models

In 1963, President Kennedy proposes large income tax cuts to promote recovery

In 1971, President Nixon takes US completely off gold standard, floats dollar (depreciates), declares, “I am now a Keynesian in economics.”

Time magazine, Dec. 31, 1965

Today, some 20 years after his death, [Keynes’s] theories are a prime influence on the world's free economies, especially on America's … In Washington the men who formulate the nation's economic policies have used Keynesian principles not only to avoid the violent cycles of prewar days but to produce a phenomenal economic growth and to achieve remarkably stable prices. In 1965 they skillfully applied Keynes's ideas … to lift the nation through the fifth, and best, consecutive year of the most sizable, prolonged and widely distributed prosperity in history.

From Time cover story, Dec. 31, 1965

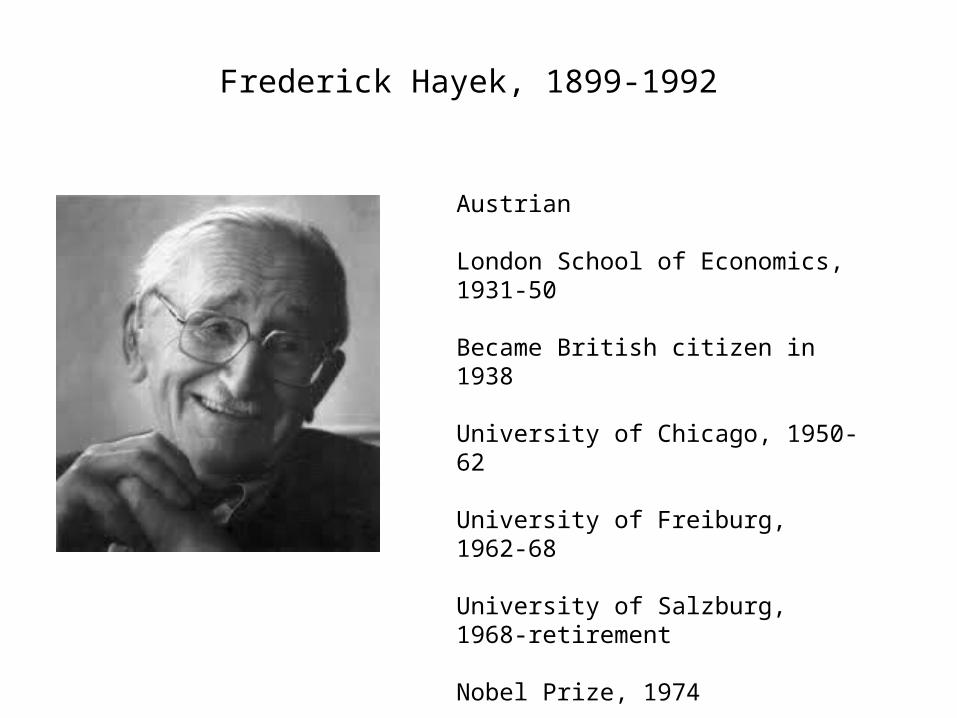

Frederick Hayek, 1899-1992

Austrian

London School of Economics, 1931-50

Became British citizen in 1938

University of Chicago, 1950-62

University of Freiburg, 1962-68

University of Salzburg, 1968-retirement

Nobel Prize, 1974

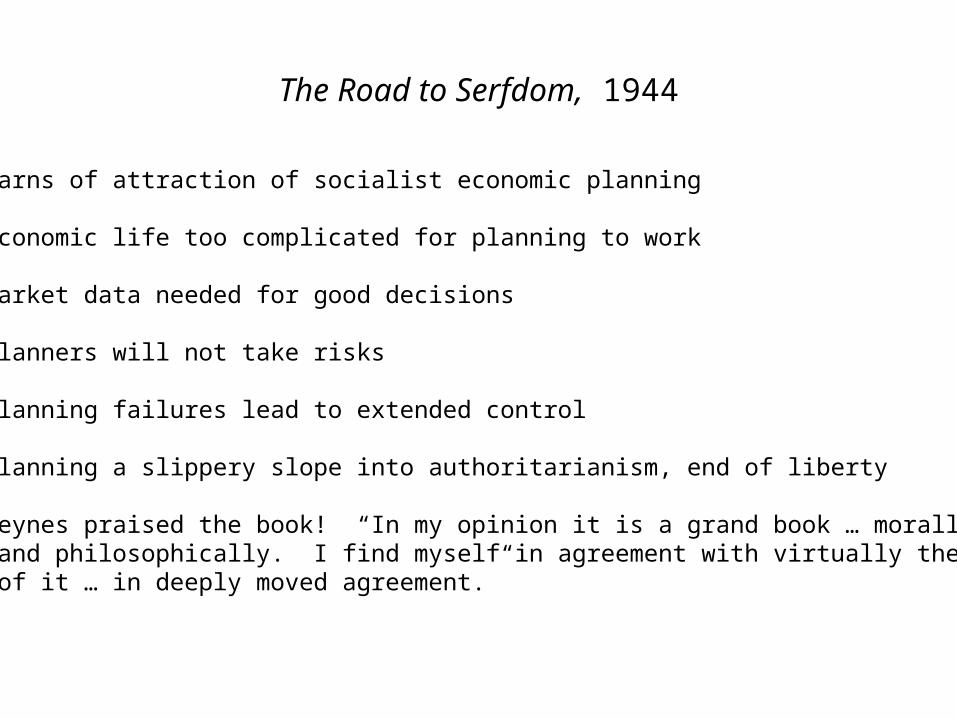

The Road to Serfdom, 1944

The Road to Serfdom, 1944

Warns of attraction of socialist economic planning

Economic life too complicated for planning to work

Market data needed for good decisions

Planners will not take risks

Planning failures lead to extended control

Planning a slippery slope into authoritarianism, end of liberty

Keynes praised the book! “In my opinion it is a grand book … morally and philosophically. I find myself in agreement with virtually the whole of it … in deeply moved agreement.”

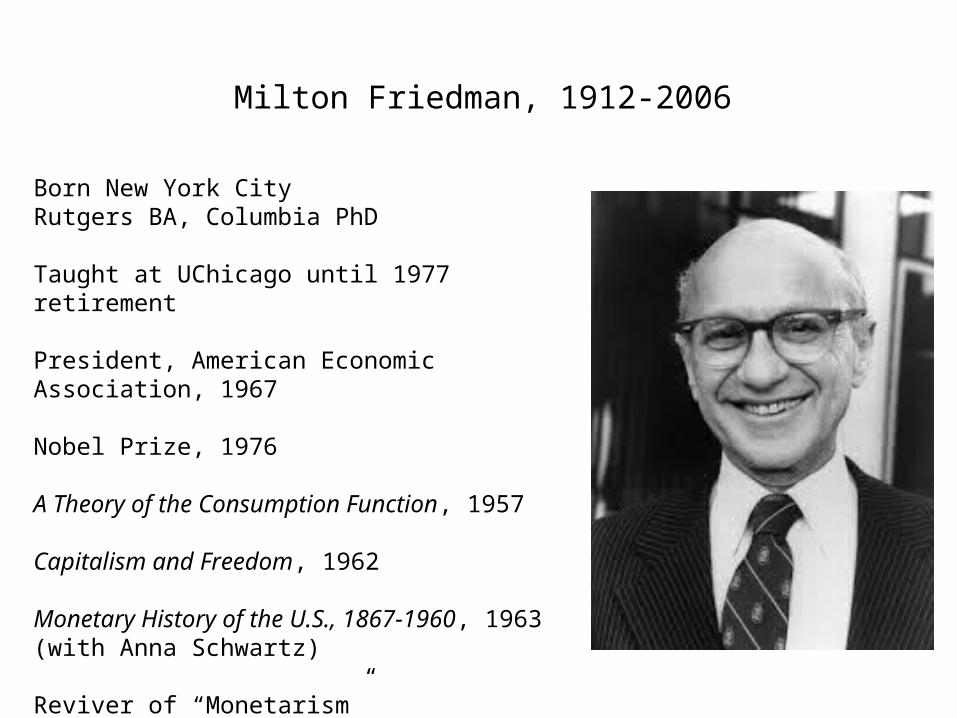

Milton Friedman, 1912-2006

Born New York CityRutgers BA, Columbia PhD

Taught at UChicago until 1977 retirement

President, American Economic Association, 1967

Nobel Prize, 1976

A Theory of the Consumption Function, 1957

Capitalism and Freedom, 1962

Monetary History of the U.S., 1867-1960, 1963 (with Anna Schwartz)

Reviver of “Monetarism”

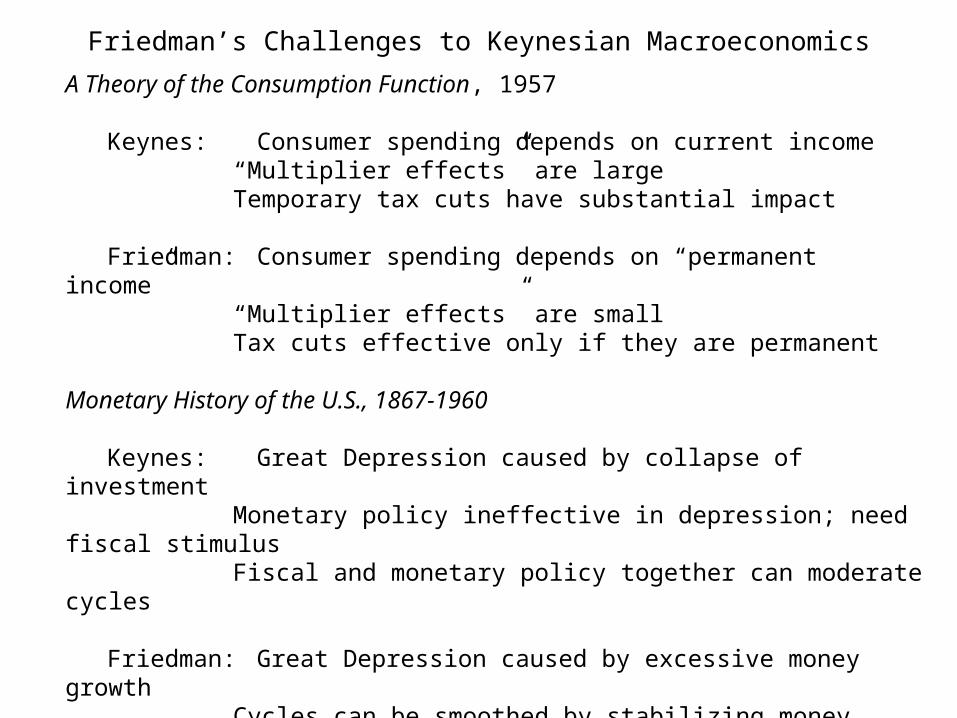

Friedman’s Challenges to Keynesian Macroeconomics

A Theory of the Consumption Function, 1957

Keynes: Consumer spending depends on current income“Multiplier effects” are largeTemporary tax cuts have substantial impact

Friedman: Consumer spending depends on “permanent income”“Multiplier effects” are smallTax cuts effective only if they are permanent

Monetary History of the U.S., 1867-1960

Keynes: Great Depression caused by collapse of investmentMonetary policy ineffective in depression; need fiscal stimulusFiscal and monetary policy together can moderate cycles

Friedman: Great Depression caused by excessive money growthCycles can be smoothed by stabilizing money growthPut Fed on “automatic pilot” – no discretionFiscal stimulus ineffective, crowds out private spending,

except when financed by printing moneyBut allow automatic fiscal stabilizers to operate

Time magazine, Dec. 19, 1969

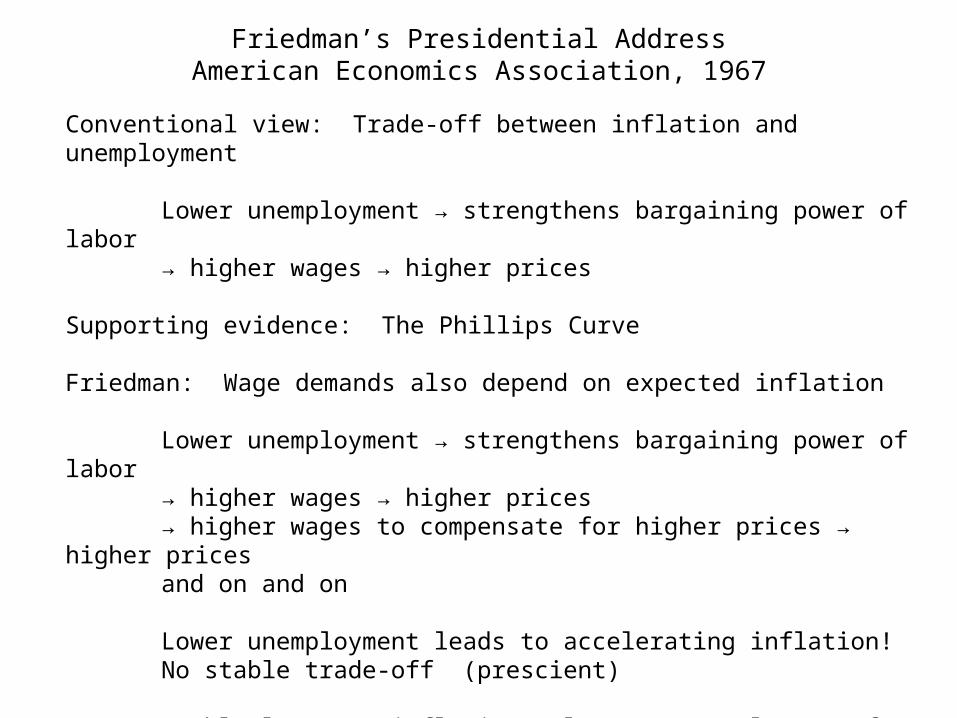

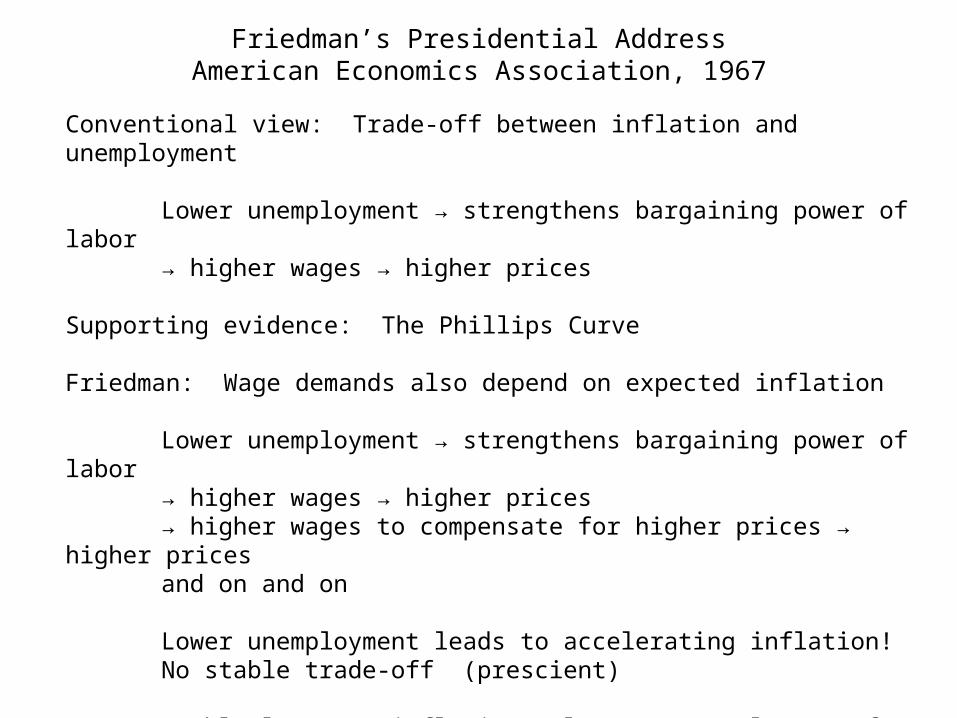

Friedman’s Presidential AddressAmerican Economics Association, 1967

Conventional view: Trade-off between inflation and unemployment

Lower unemployment → strengthens bargaining power of labor → higher wages → higher prices

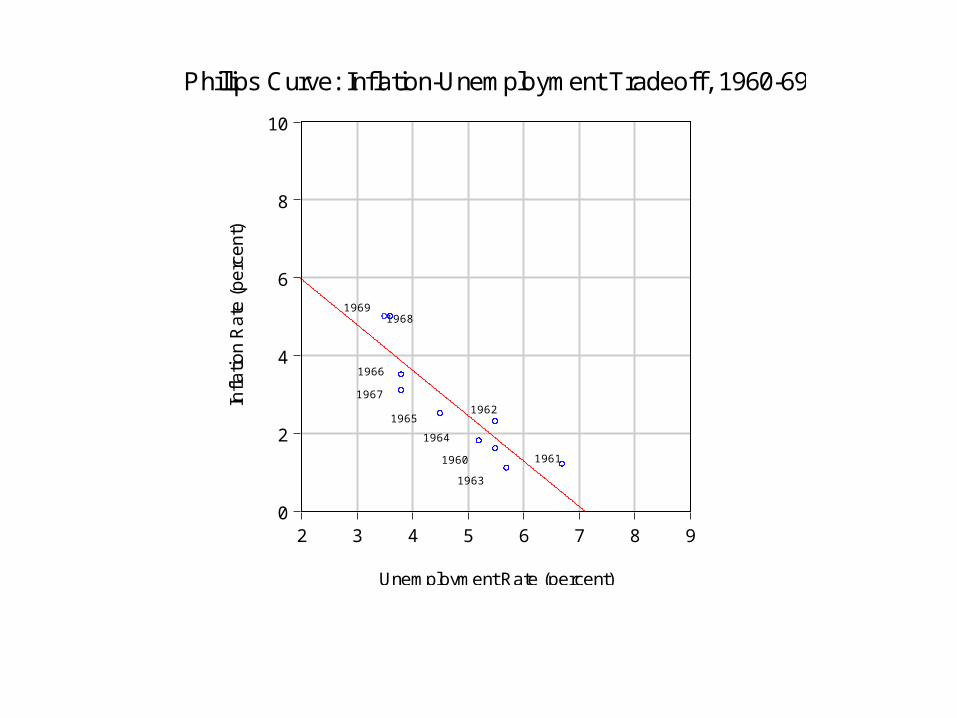

Supporting evidence: The Phillips Curve

Friedman: Wage demands also depend on expected inflation

Lower unemployment → strengthens bargaining power of labor → higher wages → higher prices→ higher wages to compensate for higher prices → higher pricesand on and on

Lower unemployment leads to accelerating inflation!No stable trade-off (prescient)

Stable long-run inflation only at “natural rate of unemployment”

Employment policy should seek to reduce the “natural rate”

0

2

4

6

8

10

2 3 4 5 6 7 8 9

Unemployment Rate (percent)

Infla

tion

Ra

te (

pe

rce

nt)

Phillips Curve: Inflation-Unemployment Tradeoff, 1960-69

19611960

1963

1962

1964

1965

1967

1966

19681969

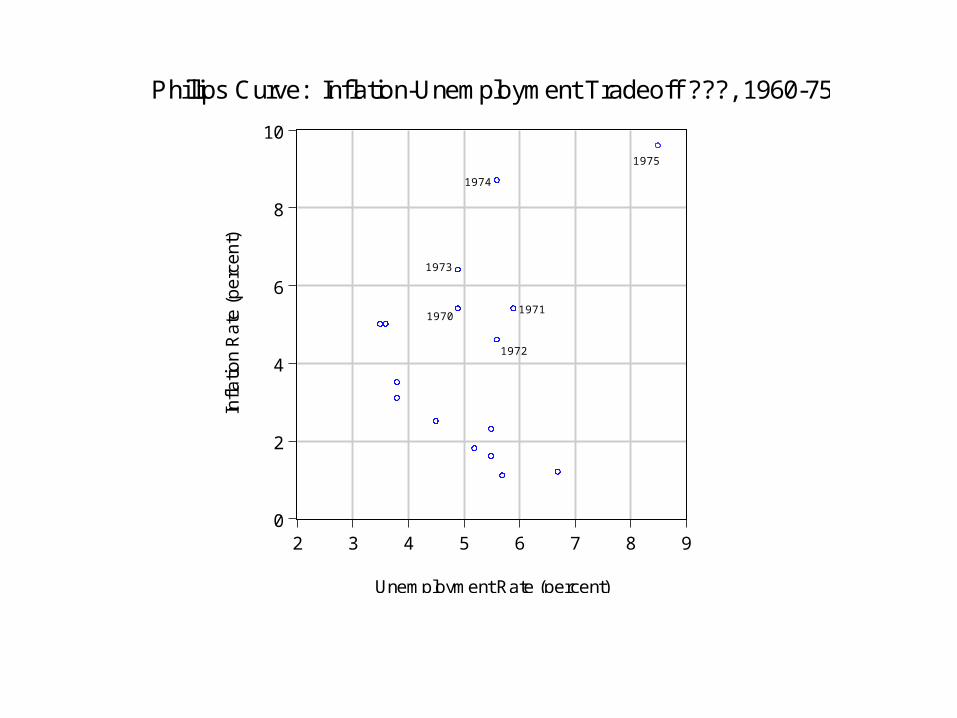

Friedman’s Presidential AddressAmerican Economics Association, 1967

Conventional view: Trade-off between inflation and unemployment

Lower unemployment → strengthens bargaining power of labor → higher wages → higher prices

Supporting evidence: The Phillips Curve

Friedman: Wage demands also depend on expected inflation

Lower unemployment → strengthens bargaining power of labor → higher wages → higher prices→ higher wages to compensate for higher prices → higher pricesand on and on

Lower unemployment leads to accelerating inflation!No stable trade-off (prescient)

Stable long-run inflation only at “natural rate of unemployment”

Employment policy should seek to reduce the “natural rate”

0

2

4

6

8

10

2 3 4 5 6 7 8 9

Unemployment Rate (percent)

Infla

tion

Ra

te (

pe

rce

nt)

1972

19711970

1973

1974

1975

Phillips Curve: Inflation-Unemployment Tradeoff ???, 1960-75

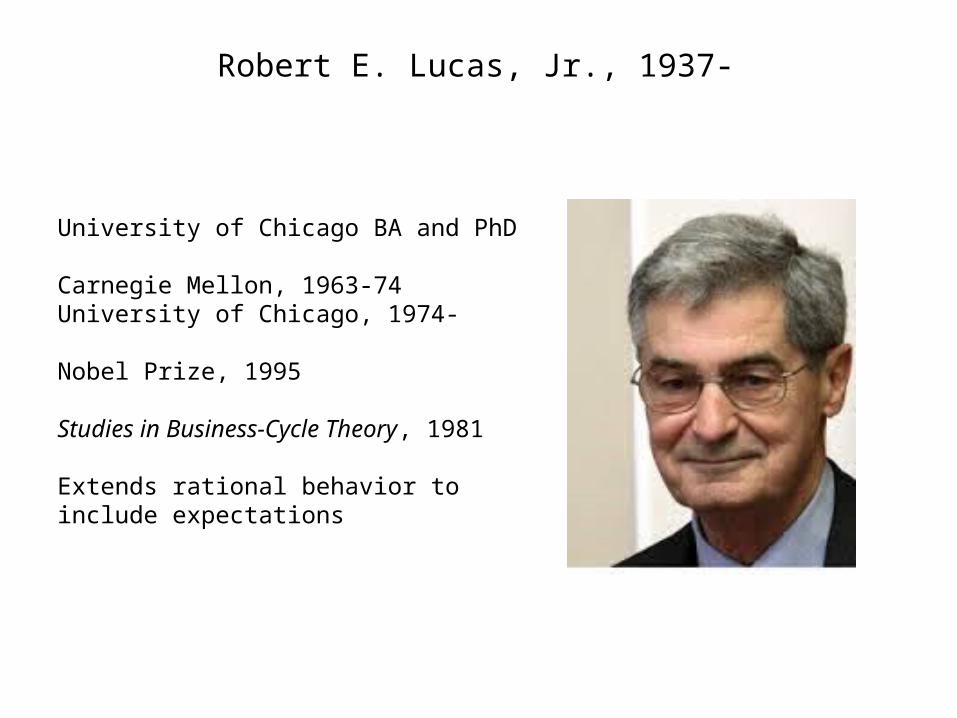

Robert E. Lucas, Jr., 1937-

University of Chicago BA and PhD

Carnegie Mellon, 1963-74University of Chicago, 1974-

Nobel Prize, 1995

Studies in Business-Cycle Theory, 1981

Extends rational behavior to include expectations

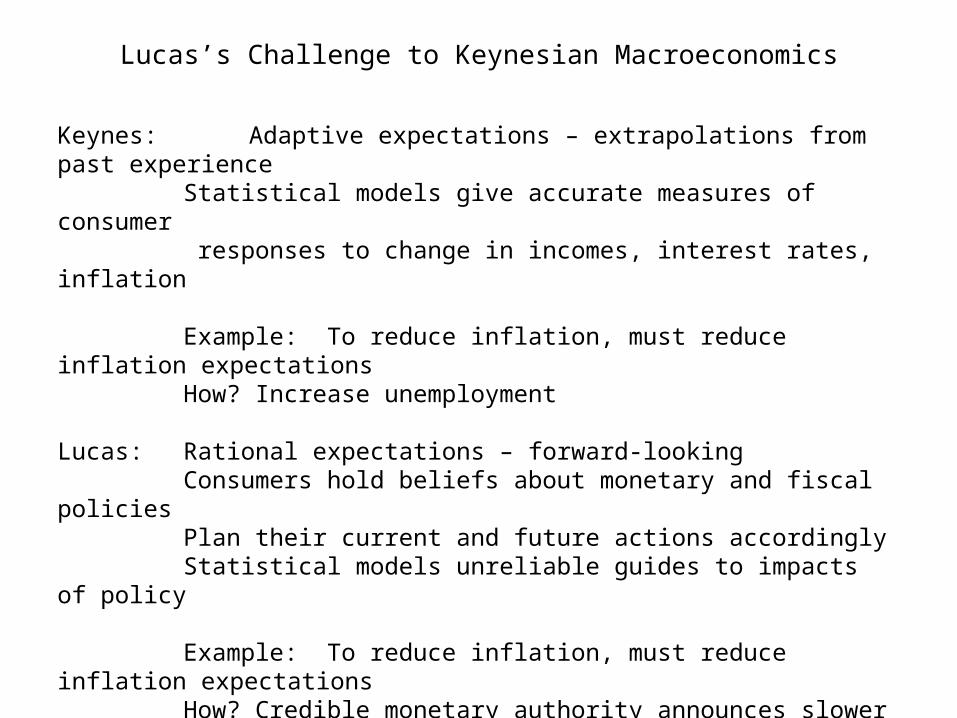

Lucas’s Challenge to Keynesian Macroeconomics

Keynes: Adaptive expectations – extrapolations from past experienceStatistical models give accurate measures of consumer responses to change in incomes, interest rates, inflation

Example: To reduce inflation, must reduce inflation expectationsHow? Increase unemployment

Lucas: Rational expectations – forward-lookingConsumers hold beliefs about monetary and fiscal policiesPlan their current and future actions accordinglyStatistical models unreliable guides to impacts of policy

Example: To reduce inflation, must reduce inflation expectationsHow? Credible monetary authority announces slower growth of

money supply

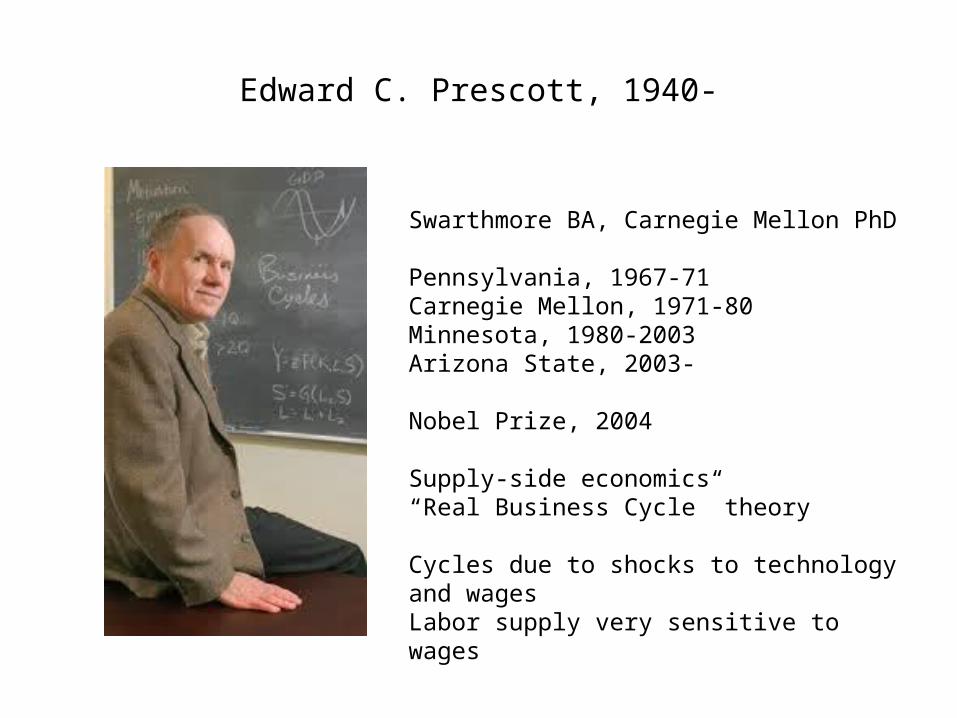

Edward C. Prescott, 1940-

Swarthmore BA, Carnegie Mellon PhD

Pennsylvania, 1967-71Carnegie Mellon, 1971-80Minnesota, 1980-2003Arizona State, 2003-

Nobel Prize, 2004

Supply-side economics“Real Business Cycle” theory

Cycles due to shocks to technology and wagesLabor supply very sensitive to wages

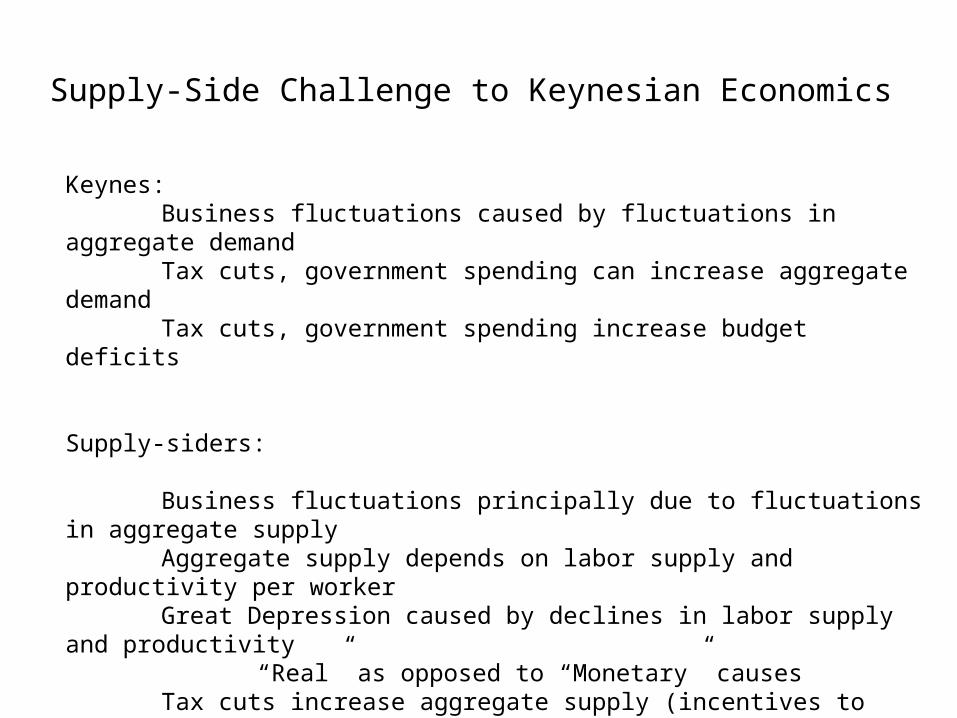

Supply-Side Challenge to Keynesian Economics

Keynes:Business fluctuations caused by fluctuations in aggregate demandTax cuts, government spending can increase aggregate demandTax cuts, government spending increase budget deficits

Supply-siders:

Business fluctuations principally due to fluctuations in aggregate supplyAggregate supply depends on labor supply and productivity per workerGreat Depression caused by declines in labor supply and productivity

“Real” as opposed to “Monetary” causes Tax cuts increase aggregate supply (incentives to work and invest)Reducing tax rates can increase tax revenue and reduce deficitsOther prominent supply-siders, influential in 1970s-1980s:

Paul Craig Roberts, Norman Ture, Arthur Laffer

Dale T. Mortensen, 1939-2014

Willamette BA, Carnegie Mellon PhD

Northwestern, 1965-2013

Nobel Prize, 2010

Search theory of markets

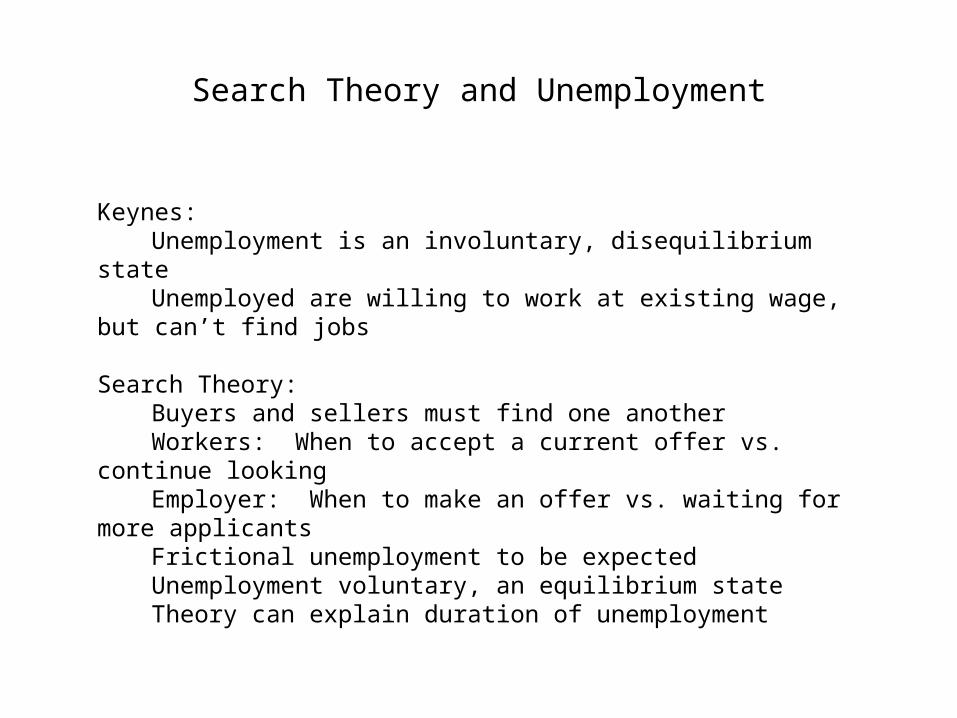

Search Theory and Unemployment

Keynes:Unemployment is an involuntary, disequilibrium stateUnemployed are willing to work at existing wage, but can’t find jobs

Search Theory:Buyers and sellers must find one anotherWorkers: When to accept a current offer vs. continue lookingEmployer: When to make an offer vs. waiting for more applicantsFrictional unemployment to be expectedUnemployment voluntary, an equilibrium stateTheory can explain duration of unemployment

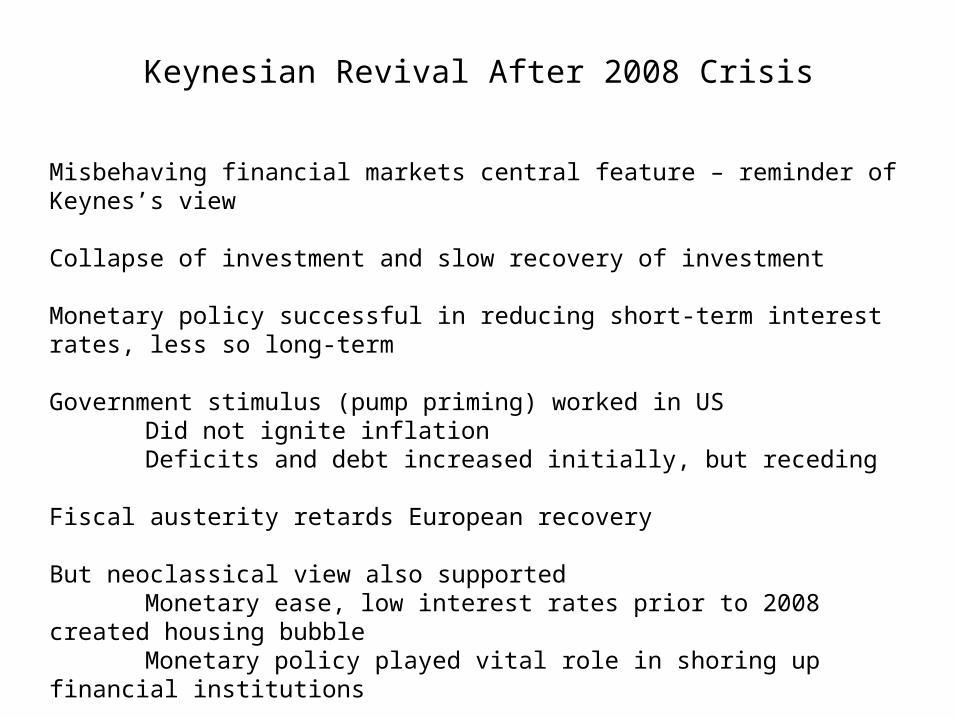

Keynesian Revival After 2008 Crisis

Misbehaving financial markets central feature – reminder of Keynes’s view

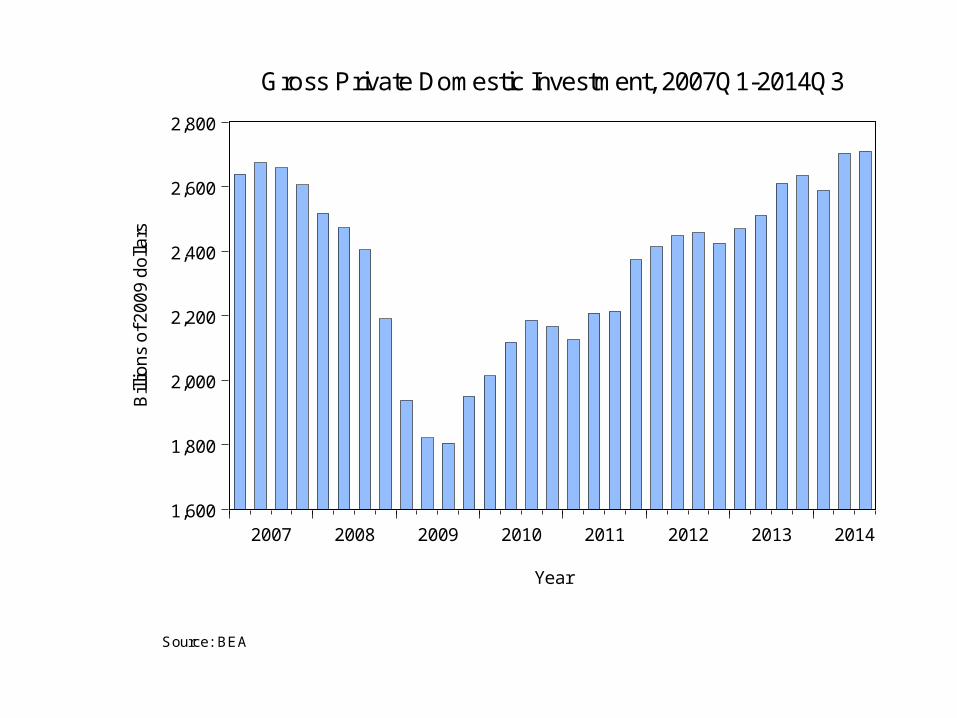

Collapse of investment and slow recovery of investment

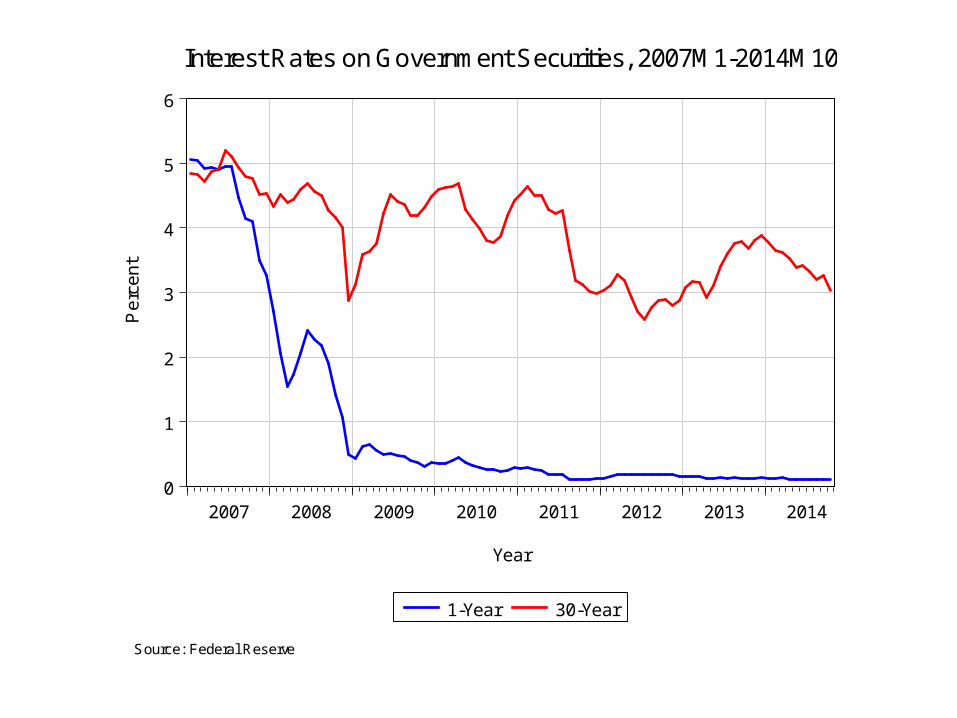

Monetary policy successful in reducing short-term interest rates, less so long-term

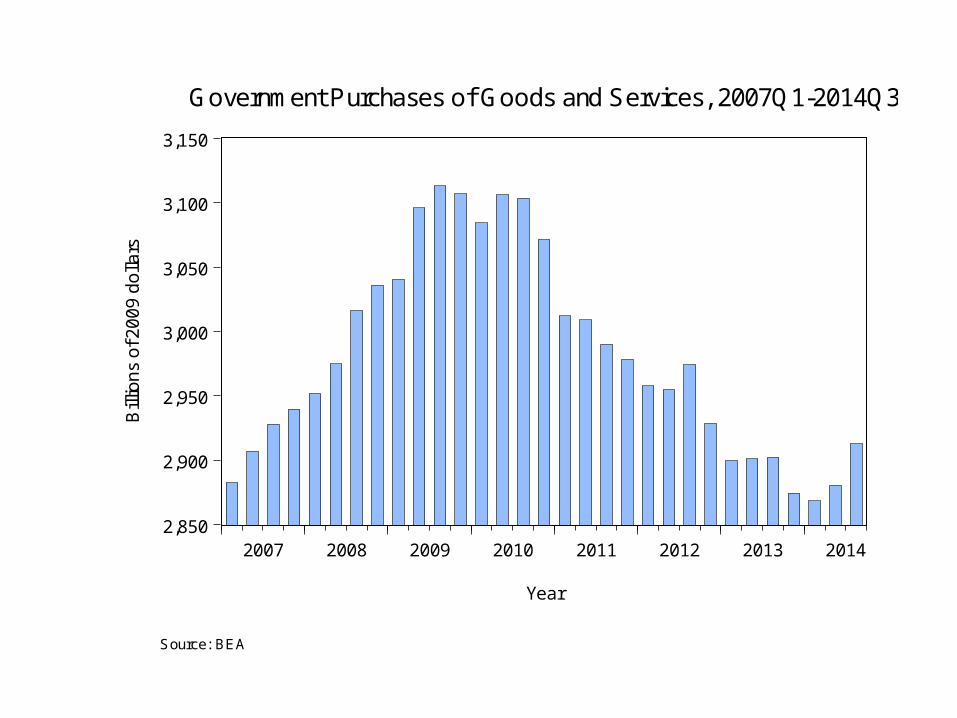

Government stimulus (pump priming) worked in USDid not ignite inflationDeficits and debt increased initially, but receding

Fiscal austerity retards European recovery

But neoclassical view also supportedMonetary ease, low interest rates prior to 2008 created housing bubbleMonetary policy played vital role in shoring up financial institutions

1,600

1,800

2,000

2,200

2,400

2,600

2,800

2007 2008 2009 2010 2011 2012 2013 2014

Gross Private Domestic Investment, 2007Q1-2014Q3

Year

Bill

ion

s o

f 20

09

do

llars

Source: BEA

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014

1-Year 30-Year

Interest Rates on Government Securities, 2007M1-2014M10

Year

Pe

rce

nt

Source: Federal Reserve

2,850

2,900

2,950

3,000

3,050

3,100

3,150

2007 2008 2009 2010 2011 2012 2013 2014

Government Purchases of Goods and Services, 2007Q1-2014Q3

Year

Bill

ion

s o

f 20

09

do

llars

Source: BEA

Reflections

Monetary and fiscal policies are powerful, potentially effective tools to achieve stability

Hayek correct that complexity of economy makes it difficult to set policy correctly

Even if policy could be set correctly, will it be? Will government leaders not use tools to further their own power and reelection?

Complexity or politicians’ self-interest leads to misuse – greater instability!

Today’s conservatives would limit discretion by imposing rules:Balance (small) budgetSet money growth on automatic pilot

Is large government not inescapable for national security?

Without improved quality of government, market capitalism not likely to survive

END