Embed Size (px)

Citation preview

GLOBAL STATUS OF CCS 2015an overview of existing and future CCS/EOR projects globally

Guido Magneschi – Global CCS Institute

Bellona EOR forum, Kiev, 24th November 2015

The Global CCS Institute

We are an international membership

organisation.

Offices in Washington DC, Brussels,

Beijing and Tokyo. Headquarters in

Melbourne.

Our diverse international

membership consists of:

o governments,

o global corporations,

o small companies,

o research bodies, and

o non-government organisations.

Specialist expertise covers the

CCS/CCUS chain.

OUR MISSIONTo accelerate the

development,

demonstration and

deployment of CCS

globally.

1Fact-based,

influential

advice and

advocacy

2Authoritative

knowledge

sharing

Our Vision for CCS:

CCS is an integral part of a low-carbon future

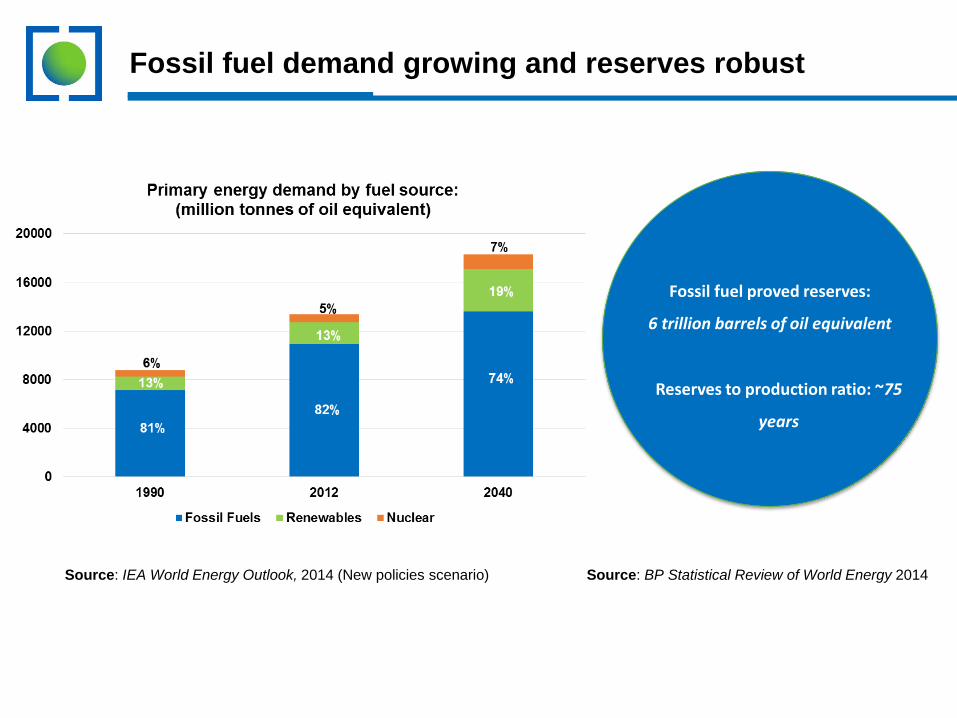

Fossil fuel demand growing and reserves robust

Source: BP Statistical Review of World Energy 2014

Fossil fuel proved reserves:

6 trillion barrels of oil equivalent

Reserves to production ratio: ~75

years

Source: IEA World Energy Outlook, 2014 (New policies scenario)

Non-OECD

OECD

~ 95 Gt CO2

Power

Industry

~95

Gt CO2

Source: IEA, Energy Technology Perspectives (2015).

CCS contributes 13% of cumulative reductions required through 2050 in a 2DS world compared to ‘business as usual’

CCS is critical in a portfolio of low-carbon technologies

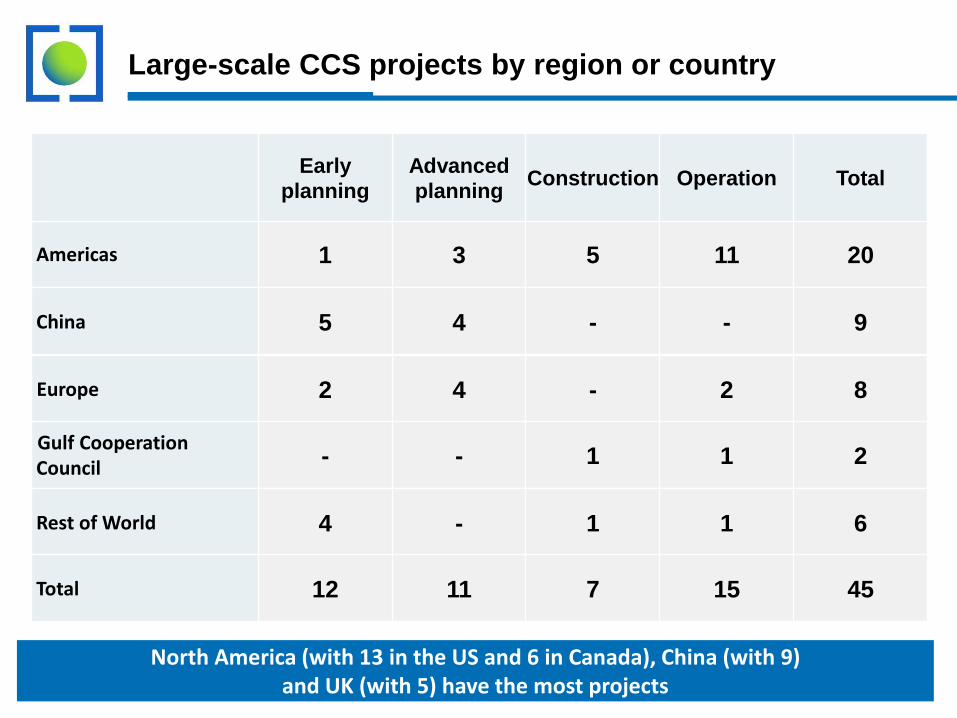

Large-scale CCS projects by region or country

North America (with 13 in the US and 6 in Canada), China (with 9) and UK (with 5) have the most projects

Americas 1 3 5 11 20

China 5 4 - - 9

Europe 2 4 - 2 8

Gulf Cooperation Council

- - 1 1 2

Rest of World 4 - 1 1 6

Total 12 11 7 15 45

Early

planning

Advanced

planningConstruction Operation Total

A significant task within one generation

45 large-scale CCS projects -

combined capture capacity of

80 Mtpa*:

• 22 projects in operation or

construction (40 Mtpa)

• 11 projects in advanced

planning, five nearing FID

(15 Mtpa)

• 12 projects in earlier stages

of planning (25 Mtpa)

OECDNon-OECD

4,000 Mtpa of CO2

captured by CCS by 2040 (IEA 450 Scenario)**

40 Mtpa

Global Status

of CCS: 2015

*Mtpa = million tonnes per annum **Source: IEA, Energy Technology Perspectives (2015).

2015

EOR

Dedicated Geological

Power

Generation

*** Institute estimate

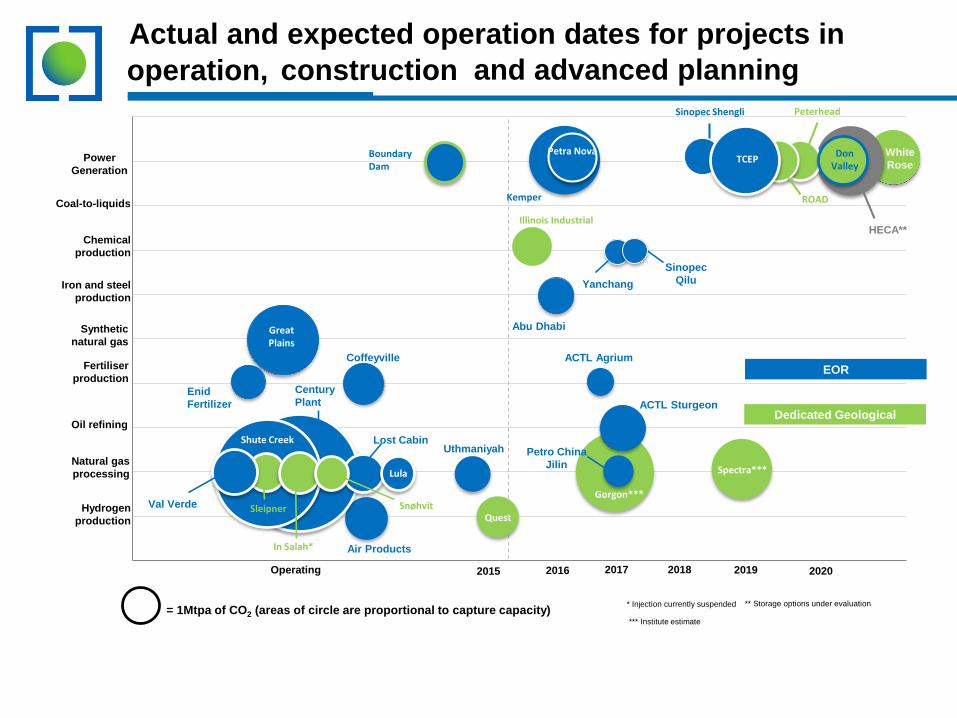

Actual and expected operation dates for projects in

Operating 20172016

Hydrogen

production

Natural gas

processing

Chemical

production

Iron and steel

production

Synthetic

natural gas

Fertiliser

production

Oil refining

2018 2019 2020

= 1Mtpa of CO2 (areas of circle are proportional to capture capacity)

Coal-to-liquids

* Injection currently suspended

Boundary Dam

Kemper

Petra Nova

ROAD

Sargas Texas

Sinopec Shengli Peterhead

HECA**Illinois Industrial

Yanchang

Sinopec

Qilu

Abu Dhabi

ACTL Agrium Coffeyville

Century

Plant Enid

Fertilizer

Val Verde

Air Products

Lost Cabin

Lula

SnøhvitSleipner

Shute Creek

In Salah*

Uthmaniyah

Quest

Gorgon***

Spectra***

ACTL Sturgeon

Petro China

Jilin

Great Plains

operation, construction and advanced planning

Don Valley

White

Rose

** Storage options under evaluation

TCEP

2015-2016: a year of action

ROAD

QuestUthmaniyah

Shaanxi YanchangPeterheadWhite Rose

Abu Dhabi CCS Kemper County

Execute2016

FID2015/16

Operational2015

Petra NovaDecatur

EOREOR

EOR

EOR

EOR

EOR projects globally

- More than 40 years of experience

- 11 operational large scale EOR projects globally

- EOR projects represent the largest share in the CCS portfolio

- EOR development generated significant learnings to be leveraged

in CCS applications

- EOR are attractive for high purity CO2 sources (gas processing,

ammonia plants, bio-ethanol facilities)

EOR in Europe

- No EOR operations in Europe:

- Relatively high cost for off-shore location of North sea oil fields

- Missing CO2 transport network

- Growing interest in EOR operations (UK, NO, NL)

- There are potential synergies between the development of CO2

hubs & cluster and EOR fields in the North sea.

Global CCS status – a recap to guide future action

CCS is indispensable in a least-cost approach to global

decarbonisation

The task is enormous – the urgency of CCS deployment is

only increasing

Deployment is not a technology challenge

Significant cost reduction and strong political support are

necessary to speed up the uptake of CCS

EOR projects would help to enlarge and diversify the

European CCS portfolio

The Global Status of CCS: 2015

The Institute’s key publication

Summary Report, Key Findings and other

advocacy materials can be found at:

www.globalccsinstitute.com

Full report is available online at the Institute’s

Members Portal.

If you have questions: