Embed Size (px)

Citation preview

Global changes and their impact on the chemical industry

René van Sloten

Trade policy today and tomorrow

SCHP ČR conference , Prague, 23 May 2006

2

European Chemical Industry Council (Cefic)

• about 28,000 small, medium and big chemical companies in Europe

• about 1.2 million employees

• about 32% of worldwide chemical production (2004)

• headquarters of Cefic is Brussels, Belgium

• homepage: www.cefic.be

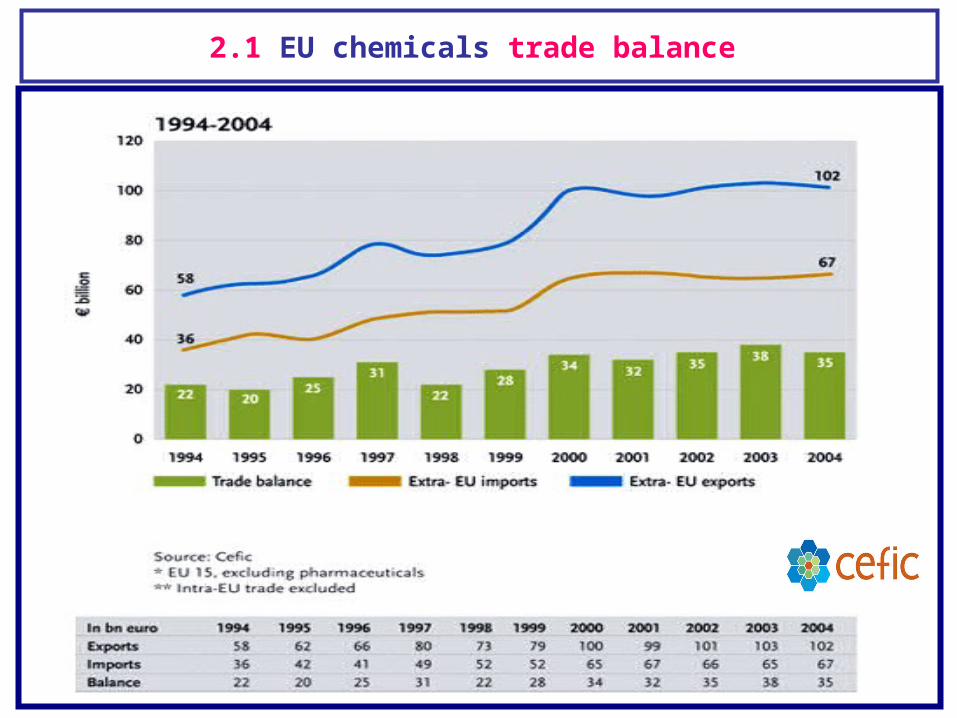

2.1 EU chemicals trade balance

4

The Challenges for Europe:Structural Shifts

• Transformation from Industry Society into Service Society

• Changes by Information and CommunicationTechnologies

• Demographic Trends• Sustainable Development• Global Competition• EU Enlargement• EU Governance

The Challenges for Europe:Structural ShiftsThe Challenges for Europe:Structural Shifts

5

Chances and Risks for the European Chemical Industry

European Chemical Industry 2015

Market& CustomerOrientation

Sustainability

Asian Competitors

Middle EastCompetitors

GlobalGlobalEconomyEconomy

CustomerCustomerIndustriesIndustries

European Authorities

BalancedChemical Policy

Incentives forInnovation

Non-bureaucraticregulations

NewTechnologies

(Opportunities&Threats)

Restructuring

Innovation

6

Market Trends Globalization

• “World-scale” plants

• High degree of standardization

• Increase in trade volume

• Production in non-traditional countries

• Sourcing, production and trade is global

7

$505.8

$101.1

$650.3$70.8

$74.9

$541.5

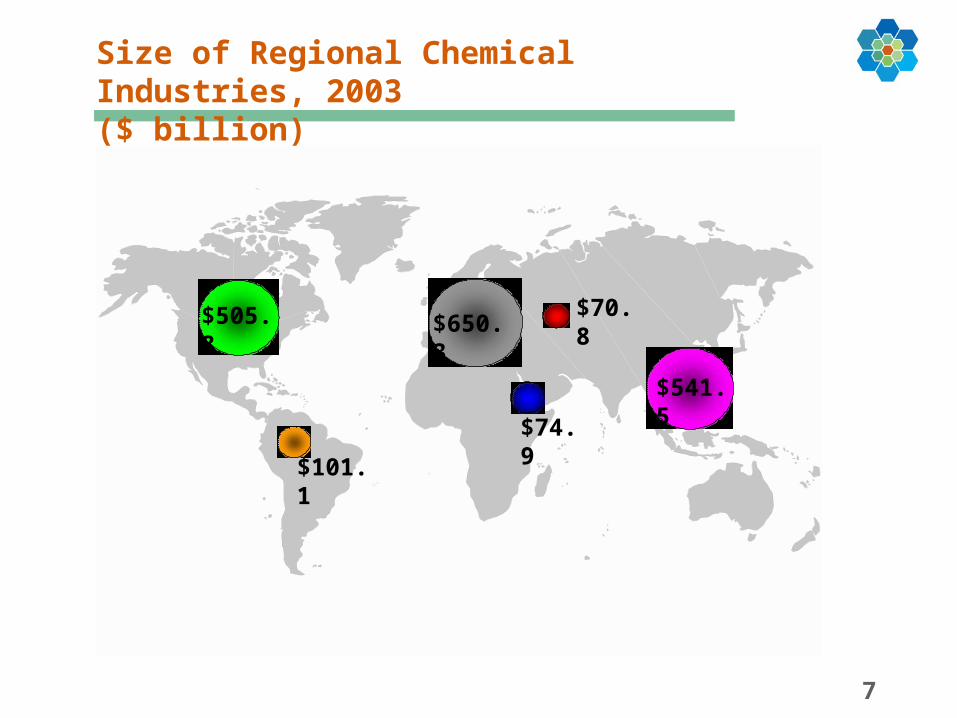

Size of Regional Chemical Industries, 2003($ billion)

8

World Chemical Sales & Trade (euro billion)

700

800

900

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

Sa

les

200

300

400

500

600

700

800

Ex

po

rts

Output Exports

Average growth p.a. (1991-2004)Output: 5%, Export 8.2%

Source: Cefic, ACC, VCI and Global Insight

9

1990 2000

Developed countries’ share of world chemical exports

83.5% 79.3%

Developing countries’ share of

world chemical exports16.5% 20.7%

World chemical exports

(billions)$308.8 $570.2

Source: UNCTAD

Change in Share of World Chemicals Exports

10

Objectives Cefic

Provide a favourable trading environment to

European Chemical Industry by

• Improving market access to third country markets• Ensuring a balanced trade-regulatory

environment• Ensuring fair trade

11

Improving market access

Multilateral in the Doha Round• Reduction of tariffs

• Reduction of non-tariff barriers

• Negotiations on trade facilitation

• Improvement of the WTO dispute settlement system

Bilateral and regional trade negotiations• EU-GCC, EU-Mercosur

WTO Accession negotiations

12

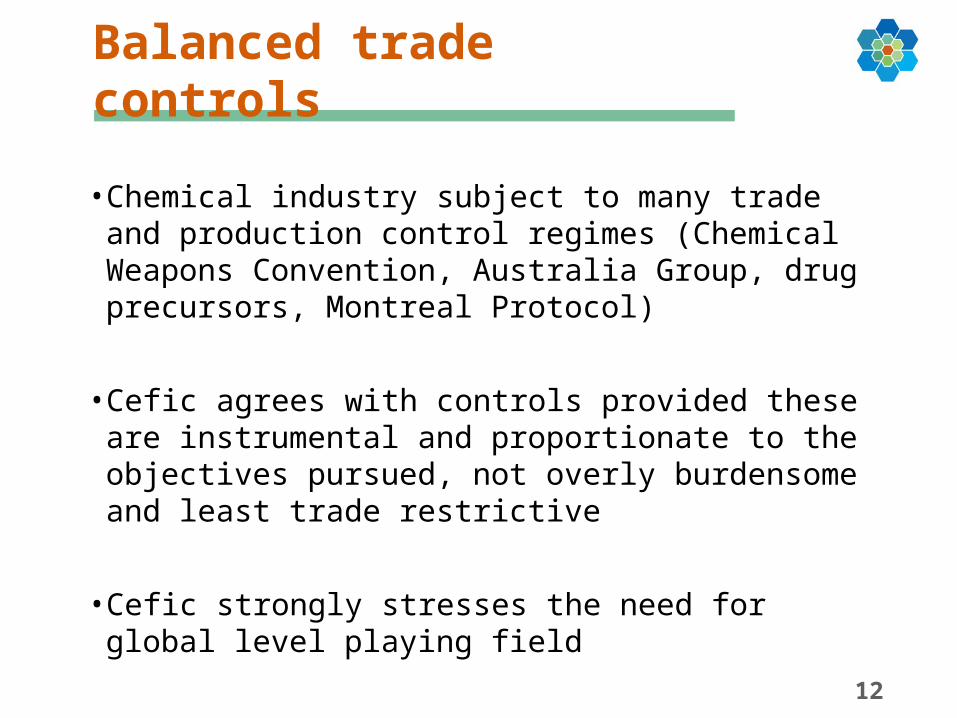

Balanced trade controls

• Chemical industry subject to many trade and production control regimes (Chemical Weapons Convention, Australia Group, drug precursors, Montreal Protocol)

• Cefic agrees with controls provided these are instrumental and proportionate to the objectives pursued, not overly burdensome and least trade restrictive

• Cefic strongly stresses the need for global level playing field

13

Ensuring fair trade

Cefic positions: • Cefic fully supports the principles of free and fair trade

• Industry needs trade instruments against unfair trade practices

• The WTO rules should be implemented in a more uniform and harmonised manner

• EU Chemical Industry should seek support from Cefic if internationally agreed trade rules are breached (Cefic trade policy service)

14

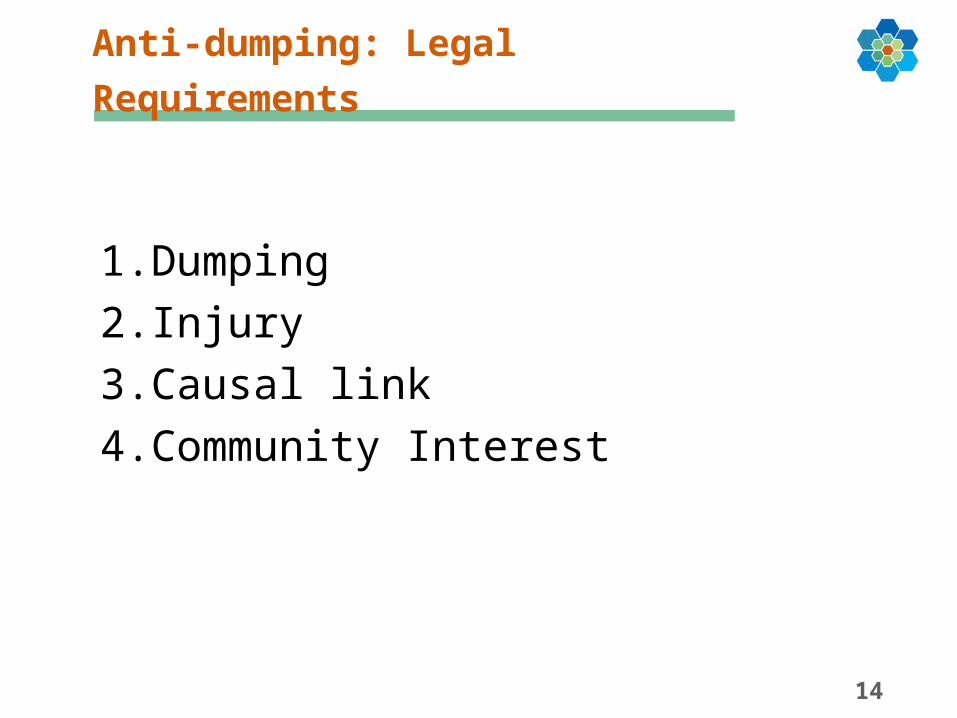

1. Dumping

2. Injury

3. Causal link

4. Community Interest

Anti-dumping: Legal Requirements

15

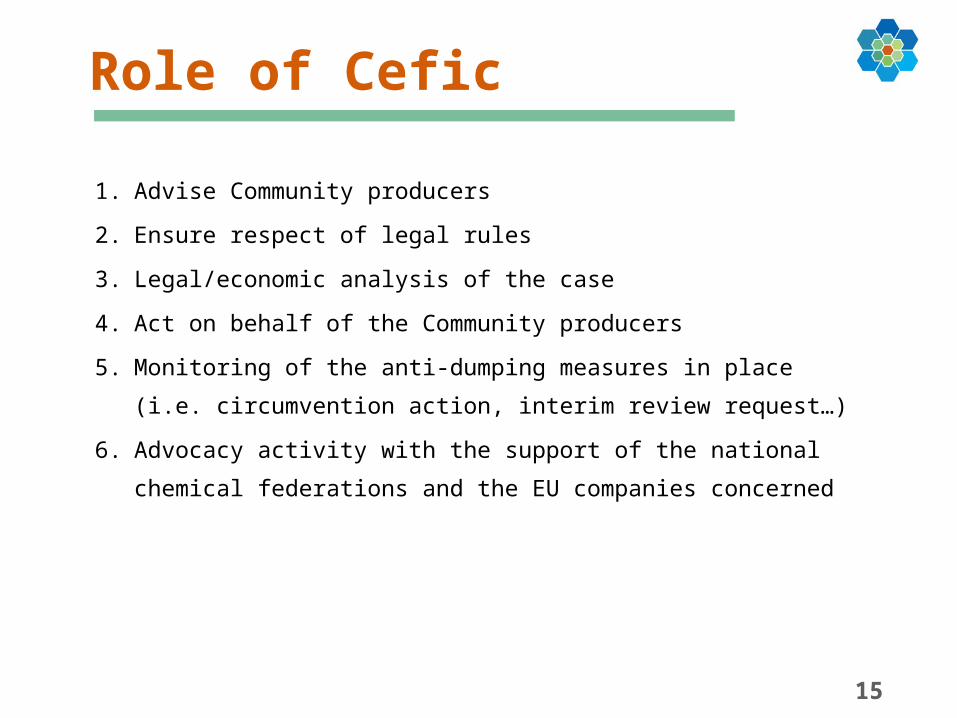

Role of Cefic

1. Advise Community producers

2. Ensure respect of legal rules

3. Legal/economic analysis of the case

4. Act on behalf of the Community producers

5. Monitoring of the anti-dumping measures in place (i.e.

circumvention action, interim review request…)

6. Advocacy activity with the support of the national chemical

federations and the EU companies concerned

16

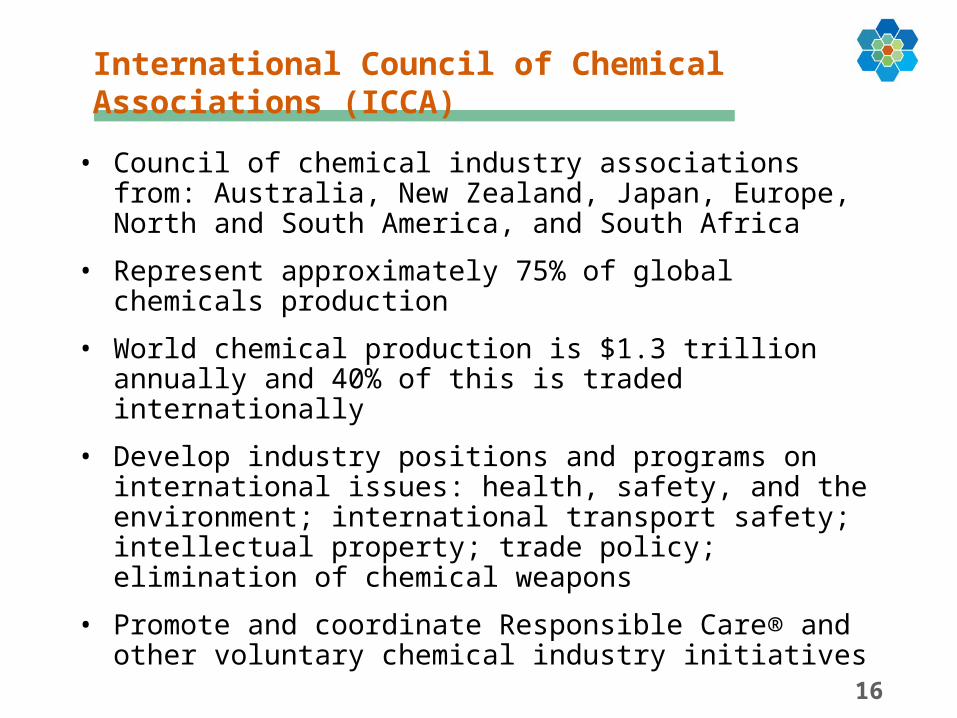

International Council of Chemical Associations (ICCA)

• Council of chemical industry associations from: Australia, New Zealand, Japan, Europe, North and South America, and South Africa

• Represent approximately 75% of global chemicals production

• World chemical production is $1.3 trillion annually and 40% of this is traded internationally

• Develop industry positions and programs on international issues: health, safety, and the environment; international transport safety; intellectual property; trade policy; elimination of chemical weapons

• Promote and coordinate Responsible Care® and other voluntary chemical industry initiatives

17

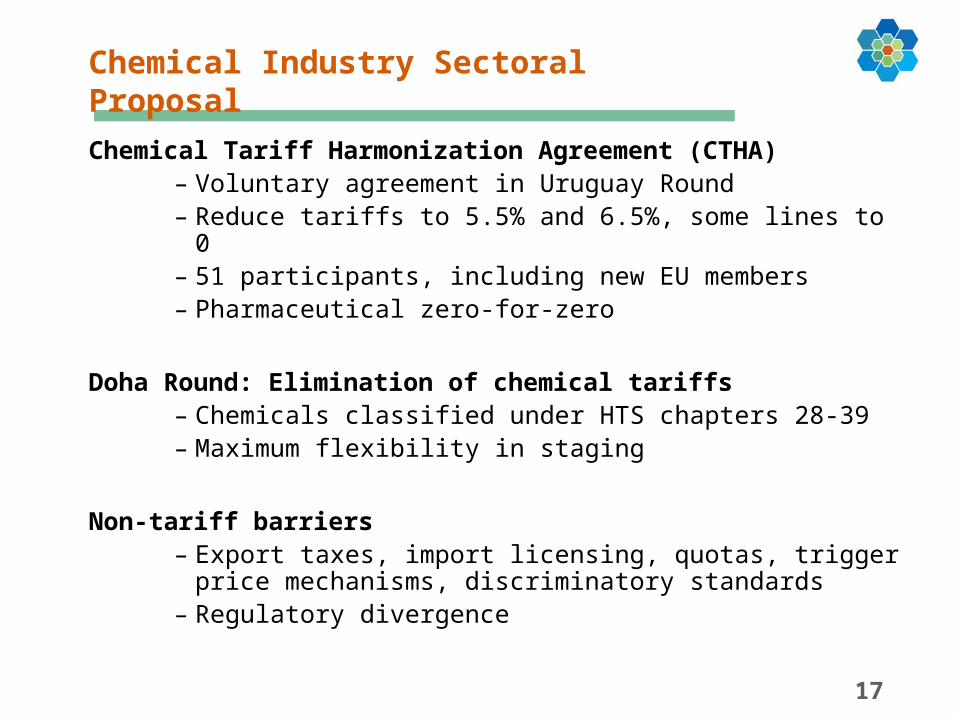

Chemical Industry Sectoral Proposal

Chemical Tariff Harmonization Agreement (CTHA)– Voluntary agreement in Uruguay Round– Reduce tariffs to 5.5% and 6.5%, some lines to 0– 51 participants, including new EU members– Pharmaceutical zero-for-zero

Doha Round: Elimination of chemical tariffs– Chemicals classified under HTS chapters 28-39– Maximum flexibility in staging

Non-tariff barriers– Export taxes, import licensing, quotas, trigger price

mechanisms, discriminatory standards – Regulatory divergence

18

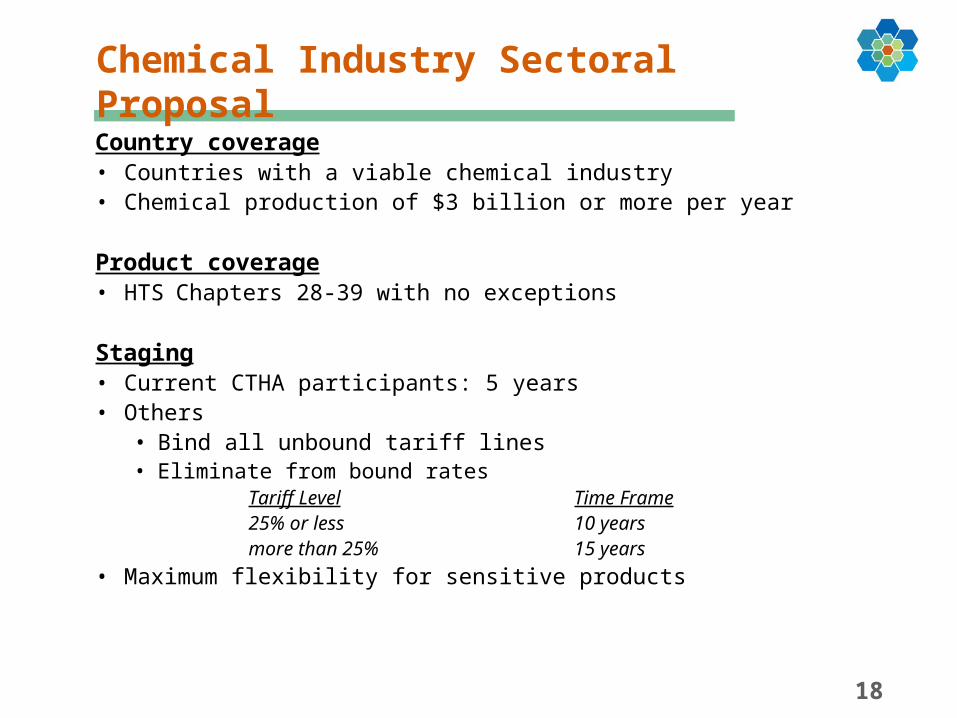

Chemical Industry Sectoral Proposal

Country coverage• Countries with a viable chemical industry• Chemical production of $3 billion or more per year

Product coverage• HTS Chapters 28-39 with no exceptions

Staging• Current CTHA participants: 5 years• Others

• Bind all unbound tariff lines• Eliminate from bound rates

Tariff Level Time Frame25% or less 10 yearsmore than 25% 15 years

• Maximum flexibility for sensitive products

19

Why Chemical Tariff Elimination?

Tariff liberalization benefits chemical industriesworldwide• Due to the globalized and capital intensive nature of this

sector, chemical industries are globally competitive wherever they are located

• Competitive chemical industries rely on chemical inputs. Countries with low chemical tariffs make themselves more attractive for investment in the chemicals sector

Tariff liberalization benefits all sectors• Chemicals are inputs into all manufacturing and agricultural

production. Lower chemical tariffs reduce input costs and prices of intermediate and finished goods.

20

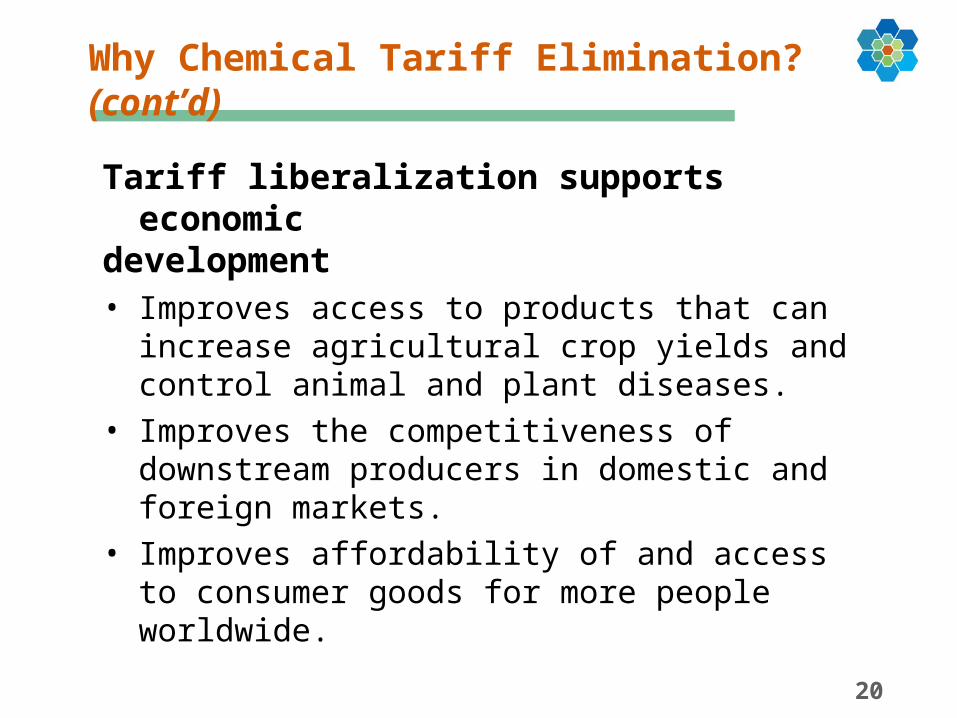

Why Chemical Tariff Elimination? (cont’d)

Tariff liberalization supports economicdevelopment• Improves access to products that can increase

agricultural crop yields and control animal and plant diseases.

• Improves the competitiveness of downstream producers in domestic and foreign markets.

• Improves affordability of and access to consumer goods for more people worldwide.