Embed Size (px)

Citation preview

THE COOEPRATION COUNCIL FOR THE ARAB STATES OF THE GULF

SECRETARIAT GENERAL

TECHNICAL SECRETARIAT FOR ANTI-INJURIOUS PRACTICES IN INTERNATIONAL TRADE

ANTIDUMPING QUESTIONNAIRE

Intended for foreign exporters/producers

Product under investigation :

Country(ies) concerned :

From (xx/xx/xxxx to xx/xx/xxxx)Period of Investigation :

PLEASE NOTE THAT THIS QUESTIONNAIRE HAS TO BE COMPLETED AND PROVIDED IN FOUR COPIES:

TWO AS CONFIDENTIAL VERSION

AND TWO AS PUBLIC VERSION

1

INDEX

INTRODUCTION...................................................................................................................................3

GENERAL INSTRUCTIONS................................................................................................................4

SECTION 1-GENERAL DATA.............................................................................................................7

1.IDENTITY OF THE COMPANY:..............................................................................................................72.LEGAL REPRESENTATIVE:...................................................................................................................73.LEGAL ENTITY:...................................................................................................................................74.ACTIVITIES:.........................................................................................................................................8

SECTION 2-THE PRODUCT UNDER INVESTIGATION...............................................................9

SECTION 3-FINANCIAL STATEMENT AND ACCOUNTING SYSTEM..................................11

SECTION 4-SALES..............................................................................................................................13

TURNOVER..........................................................................................................................................13EXPORT SALES OF THE PRODUCT UNDER INVESTIGATION TO THE GCC STATES............................13DOMESTIC SALES OF THE LIKE PRODUCT.........................................................................................16EXPORT SALES OF THE LIKE PRODUCT TO THIRD COUNTRIES........................................................18

SECTION 5-PURCHASES AND STOCKS........................................................................................21

PURCHASES..........................................................................................................................................21STOCKS................................................................................................................................................21

SECTION 6-PRODUCTION AND COST OF PRODUCTION.......................................................21

PRODUCTION.......................................................................................................................................21COST OF PRODUCTION........................................................................................................................22

SECTION 7-ATTACHMENTS............................................................................................................24

SECTION 9-ANNEXS...........................................................................................................................49

ANNEX 1: CERTIFICATE......................................................................................................................49ANNEX 2: GLOSSARY...........................................................................................................................50ANNEX 3: GUIDELINES FOR COMPLETING THE NON-LIMITED DATA...............................................53

2

INTRODUCTION

With reference to the GCC Common Law on Antidumping, Countervailing and

Safeguard Measures and its Rules of Implementation, this questionnaire aims to

obtain the necessary information to carry out the antidumping investigation of the

Public Notice issued in Volume (--) of the Official Gazette for the GCC-Bureau of the

Technical Secretariat of Anti-Injurious Practices in International Trade (GCC-TSAIP)

due to the complaint presented by the GCC domestic Industry of the product

“-------------------------------------------------------, (hereinafter referred to as the

“product under investigation") . It is in your own interest to reply to this questionnaire

as accurately and completely as possible and to attach all supporting documents.

It is imperative for the continuation of the proceeding to reply to all questions in

the formats requested and within the time limits specified by the GCC-TSAIP as

indicated in the general notes therein. All documents attached to this questionnaire

should be signed and stamped by or on behalf of your company.

If you have any problems completing the questionnaire, please contact the GCC-

TSAIP officials in charge of the proceedings who will provide you with any

explanation on any question contained in this questionnaire.

3

GENERAL INSTRUCTIONS

1. Before completing the questionnaire you are requested to read

and review carefully all instructions therein and the glossary of

dumping terminology attached as Annex2.

2. This questionnaire is intended for the foreign exporting

producers exporting the product under investigation classified

within the following HS codes :---------------------------------------.

3. The purpose of this questionnaire is to permit the GCC-TSAIP to

obtain the necessary information to carry out the investigation

and on the basis of which preliminary and final determinations

will be made with reference to the GCC common Law and its

Rules of Implementation.

4. The response to this questionnaire must be completed in English

on the official paper of your company.

5. Please put your answers in the order presented in this

questionnaire. In order to do this, rewrite the question to which

you are responding in your narrative submission and put your

answer directly below it. If for any reason because of the nature

of the response required, it is impractical to be able to do this,

please attach more attachments for more details indicating

clearly to which question they relate and indicate the extent of

confidentiality whenever it is required.

6. Any methodology used in allocation of costs and revenue to

different types of the product concerned… etc, should be clearly

explained.

7. The responses to the questionnaire must be based on sufficient

evidence supporting the data contained therein, which requires

identifying sources of data submitted.

8. Please respect the deadline specified for replying this

questionnaire. Any interested party may request, upon proper

4

justification, an extension of the deadline before the ending of

the initial deadline.

9. All cost and pricing information should be provided for the

period of investigation for dumping ( POI) from xx/xx/xxxx to

xx/xx/xxxx. If your company’s financial year differs from the

POI, please give a detailed explanation of how the information

was compiled for the POI.

10. The GCC-TSAIP may carry out on-spot visits to examine

the records of your company and to verify the information

provided in this questionnaire. For this reason, all worksheets,

documents and records used in answering this questionnaire must

be retained.

11. The confidentiali ty will be fully respected in the

proceeding. Therefore, where appropriate, certain information

and supporting evidence may be given on a confidential basis.

Any information or document provided as confidential must be

labelled as ‘’l imited’’. These limited data will not be made

available to any other interested party.

12. Moreover, any party providing such ‘’l imited’’ information is

required to provide a non-confidential summary thereof which is

open for consultation by interested parties. Such summaries shall

be in sufficient detail to permit a reasonable understanding of the

data submitted as ‘’limited’’.

13. The questionnaire with its tables and attachments should be

submitted (limited and non-confidential copies) in hard copy and

soft copy (using WORD or PDF for text and EXCEL for data).

14. Identify clearly all units of measurement and currencies used in

all submitted data.

5

15. All documents submitted in reply to this questionnaire must be

accompanied by an English or Arabic translation.

16. All correspondence must be sent by mail service or presented

personally to the following address:

Bureau of Technical Secretariat For

Anti-Injurious Practices in International Trade

Riyadh – The Kingdom of Saudi Arabia

P.O Box: 7153

Code: 11462

Tel: 00966112551388

Fax : 00966112810093

Email: [email protected]

6

1. GENERAL DATA

1. Identity of the company:

Legal entityName

Place of Export/ProductionDate of establishment

CapitalDate of beginning of export/production

WebsiteAddress

Tel/Fax

2. Legal representative:

If you have appointed a legal representative to represent you, please provide the original power of attorney in Attachment (1-1) with the following details:

Name of legal representative:

Nature of the legal representative work:

Address: ………………………… Fax: ………………………………

Tel: ………………………………... Website: ………………………….

Email: …………………………….

Official in charge: ……………………….

(Name and responsibility)…………. Tel: ……………………………….

Email: …………………………… Fax: ………………………………

3. Legal entity:

State the legal form of your company:

Individual/private company□Limited company□

Limited partnership by shares□Limited partnership□

Other (specify) ……………□partnership□

7

corporation□

Provide copies of the following documents (in original language and in

English):

Articles of Association and all related documents to be attached in

Attachment (1-2). Provide details regarding changes in these Articles of

Association since the original establishment.

Business License in Attachment (1-3)

4. Activities:

Please indicate the activities of your company:

Producer□Importer□

Exporter□Retailer□

Wholesaler□Distributor□

Other (if any)□

5. Indicate the date of establishment of your company. Please attach any catalogues

or brochures issued by your company in Attachment (1-4).

6. Supply a diagram outlining the overall organizational structure of your company

in Attachment (1-5). Show all units involved in any way with the product under

investigation.

7. Identify your parent company/ies if applicable. Provide the names & addresses

and detail the extent of its ownership in your company.

8. Provide a list of all affiliated companies and their addresses. Describe the

relationship between your company and its affiliated companies and provide

details of the percentage of ownership held by your company and its affiliates.

9. Complete the Attachment (1-6) concerning the affiliated companies of your

company which are involved in any way with the product under investigation

and/or the like product.

8

10. Complete the Attachment (1-7) concerning the shareholders of your company

who own individually more than 5% of the shares in the capital and provide

details regarding any changes in these shares during the period of investigation.

1.

9

2. THE PRODUCT UNDER INVESTIGATION

The product under investigation is the imported product to the GCC as

described in the notice of initiation of the investigation Volume no.(XX),

which is currently classified within the GCC unified tariff schedule under H.S.

Heading items XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX.

11. Describe the product under investigation produced, sold domestically and/or

exported by your company in terms of:

Technical characteristics of the product End-uses HS Code when exporting Summary of the main stages of the production process and raw

materials used in production. Attach a complete flowchart of the production cycle, including

descriptions of each stage in the process. Distribution channels Periods in which the production and sales of the product under

investigation are increased. Other

12. Provide in Attachment (2-1) all documents related to the product under

investigation such as catalogues and brochures clarifying the detailed description

of the product under investigation.

13. In order to ensure a fair comparison between the export prices to the GCC and the

normal value in the domestic market during the period of investigation, it is

important that you and your related companies create a consistent code or Product

Control Number (PCN) for each type/size/model of the product under

investigation produced, exported to the GCC, and sold domestically. This PCN

will be used throughout the response to this questionnaire. It is especially

important that the PCN be detailed as much as possible and also be used in all

electronic files used in reply to this questionnaire, even if the company code(s)

used for domestic sales or in production are different from the PCN. Furthermore,

10

the PCN has to be provided in Excel table and each PCN has to be provided in

one cell/row without spaces, commas or other separators. Moreover, provide an

example on how to read the PCN.

14. Provide a list of the different types (Models/size) of the product under

investigation produced by your company. If your company uses coding system

for its production and sales of the product under investigation, please describe in

details your company’s product coding system for each (Type/Model/Size) of the

product under investigation in correlation with each PCN in Attachment (2-2).

15. In case your company does not use the same product codes in the production,

sales and invoicing department, or does not use the same code depending on the

sales market, provide a cross-reference table linking the codes used in the

production department with those used in the sales department on the invoices

and with the PCN.

16. If sales to independent customers in GCC or on your domestic market are made

via a related company, provide a cross-reference table between your production

codes and the codes on the invoices of the related company.

17. Indicate if the product under investigation is subject to any duties or restrictions.

18. Complete the Attachment (2-3) relating to the differences, if applicable, among

the exported product to the GCC (product under investigation), the like product

you sell in your domestic market (domestic like product), and the like product

you export to a third country (exported like product).

19. Regarding the units to be used in your reply to this questionnaire, you should

normally apply the same measurement consistently throughout your questionnaire

response. Unless otherwise specified, where we request “quantity/volume” you

should report the unit of measurement used in your sales and accounting records.

Furthermore, all sales prices and values, should be expressed in the currency in

which your accounts are kept.

11

3. FINANCIAL STATEMENT AND ACCOUNTING SYSTEM

20. Identify your company’s Accounting year. If any changes have occurred

regarding this accounting year during the period of investigation, please explain

these changes.

21. State whether your accounting practices comply with the generally accepted

accounting principles (GAAP) in your country. If the principles employed by

your company vary from the GAAP, explain the nature of the difference, and the

reason a different principle was adopted.

22. Describe all accounting principles related to inflation, which have a significant

impact on the measurement of current costs of the product. If the principles

employed by your company related to inflation vary from the GAAP, explain the

nature of the difference, and the reason a different principle was adopted.

23. Provide your company’s method for treatment of fixed assets and the related

depreciation expense. Describe whether these assets are revalued periodically. If

your company does revalue assets, provide a description of the process, including

the accounting entries that are recorded and the frequency of the adjustments.

Identify the indices used for revaluation adjustments and provide index tables

covering the POI and the past three years.

24. Describe the accounting methods used in preparing your financial statements, and

all principles which have a significant impact on the cost of production, including

the explanations of the following:

- Inventory evaluation (FIFO,LIFO,AVERAGE.) for each of (RM, WIP,

Finished Goods);

- Average useful life for each class of production equipment and

depreciation method and rate used for each including any accelerated

methods;

- Whether standard or actual costing methods are used.

12

25. In the event that any of the accounting methods used by your company changed

over the last three financial years, provide a detailed explanation of the changes,

the date of change and the reasons for it.

26. Attach copies (with English translation) of the audited financial statements

including all auditors’ reports, notes and opinion in Attachment (3-1) for the last

three fiscal years including the POI for your company as well as for those

companies related to you that are involved in production, marketing and sales of

the product under investigation.

27. If you keep separate books for each department/division in the company please

provide balance sheets and income statements for each of them before

consolidation for the last three fiscal years including the POI.

28. Provide full details on your company’s Auditors (i.e. name, address, telephone,

fax, email, and website)

29. Provide a copy of your company’s chart of accounts including the numbers and

names of the accounts used in Attachment (3-2).

30. If your company uses an accounting software, provide the following:

- Name of the accounting software

- The beginning date of use.

- Is the company still using the manual accounting system beside the

software?

31. Provide a list of exchange rates for your domestic currency against the U.S. dollar

(or any other currency of exportation to the GCC) in Attachment (3-3) for the

period of investigation (POI) and identify the source of the information.

32. Provide a list of inflation rates on a monthly basis for the period of investigation

in Attachment (3-4) and identify the sources of the information.

13

4. SALES

TURNOVER

33. Complete the table in Attachment (4-1) concerning total sales during the period

of investigation.

34. Complete the table in Attachment (4-2) concerning sales to (unrelated

customers) of the product under investigation, domestic like product, exported

like product to third countries during the period of investigation.

35. Complete the table in Attachment (4-3) concerning sales to (subsidiaries and

other related customers) of the product under investigation, domestic like

product, exported like product to third countries during the period of

investigation.

36. Provide any studies about the product under investigation or the like product in

Attachment (4-4).

EXPORT SALES OF THE PRODUCT UNDER INVESTIGATION TO THE GCC STATES

37. Explain how the selling prices are set (pricing methods) of the product under

investigation by providing all the information relating to the terms and conditions

of sale of the product under investigation in terms of:

Delivery Terms: FOB, CIF,C&F ..... etc.

Payment: In advance, upon delivery, Credit (specify no. of days).

Policy of granting discounts and rebates: quantity discount, value/cash

discount, .....

After-sales: Warranty, Maintenance contract, ...etc.

Other (if any)

38. Provide in Attachment (4-5) price lists issued by your company for export to the

GCC Countries during the period of investigation.

14

39. Complete the table in Attachment (4-6) for all sales of the product under

investigation to the GCC Countries during the period of investigation (POI).

Provide clear (PDF-format and hard) copies for all export invoices for each

export shipments to the GCC Countries of the product under investigation. Attach

clear (PDF-format and hard) copies of all export sales related documents for 5

export shipments of the product under investigation.

40. Complete the table in Attachment (4-6) relating to the breakdown of all the

charges incurred after the ex-factory price on export sales to the GCC of the

product under investigation during the POI (prices adjustments). Provide

evidence and working papers to explain each adjustment for 5 invoices.

Please ensure that all the price adjustments should be made where prices and

price comparability are affected. For this purpose you must claim adjustments

where it can be demonstrated that the factor concerned is one that has resulted

in a different price being charged to your customers.

An adjustment can only be made for expenses that are directly related to the

sales of the product under investigation. For example, advertising expenses

can be related to several activities but only advertising expenses that are

directly related to the sales of the product under investigation can be adjusted

such as when such expenses are assumed by the seller on behalf of the buyer

and directed toward the product under investigation.

41. Explain your company’s channels of distribution to the GCC member states for

the product under investigation starting from the factory gate up to the first resale

to independent customer. Describe the sales process for each method or channel

of distribution described and provide a detailed flow chart indicating all details

(i.e. terms of sale, pricing, customers) in Attachment (4-7).

The description you provide on your distribution and sales processes is

intended to provide the GCC-TSAIP with the information necessary to make

appropriate comparisons of sales at the same level of trade.

15

42. Explain the relationship between your company and your customers

(exporter/importers) mentioned in your reply to Attachment (4-6) and provide

enough details for that in Attachment (4-8) including list of customers’

categories (i.e. OEM’s, Distributors, Retailers, End-users), selling activities

performed in details.

Refer to definition of "affiliated person" in Annex 2.

43. Explain the sales negotiation process of the product under investigation starting

from contacting with the customer (purchase order) up to the delivery of the

product under investigation to this customer. Provide flow chart indicating all

details in Attachment (4-9).

44. Clarify whether a change occurred in the distribution channels or in the sales

negotiation process described above during the period of investigation and the

reasons for that.

45. Please provide copies of contracts (with English translation) between your

company and your customers for export sales to GCC (either long-term or short-

term), describe in detail the process by which the contracts, the prices, expenses,

and quantities therein, are agreed to. Describe each type of contracts applicable

to the product under investigation, including the terms, the requirements for a

price change or re-negotiation by either side, etc.

46. Were the prices of the product under investigation that were exported to the GCC

member states during the POI:

i) Subject to any direct or indirect reimbursement to your customers (e.g.,

sales promotion, advertising, warranty, etc)? Or,

ii) Influenced by a commercial agreement or relationship including

mutual corporate affiliations and / or common shareholders.

iii) Inclusive of any consideration other than price.

Refer to definition of “Arms-length transactions” in Annex 2).

16

DOMESTIC SALES OF THE LIKE PRODUCT IN THE COUNTRIES

47. Explain how the selling prices are set (pricing methods) for the like product in the

domestic market by providing all the information relating to the terms and

conditions of sale in terms of:

Delivery Terms: OEM’s, Wholesaler, Retailer, .....etc.

Payment: In Advance, upon delivery, credit (specify no. of days) ......

Policy of granting discounts and rebates: quantity discount, value/cash

discount, .....

After-sales: Warranty, Maintenance contract, ....

Other (if any)

48. Provide in Attachment (4-10) price lists issued by your company for sales in

domestic market during the period of investigation.

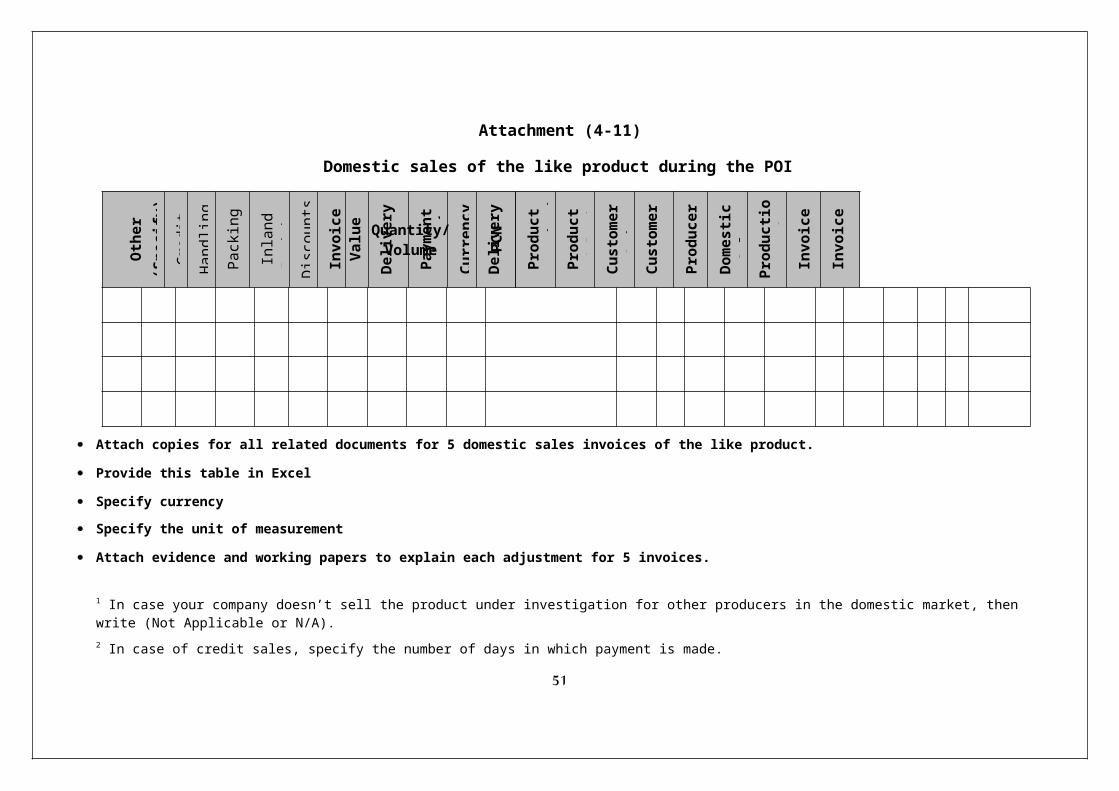

49. Complete the table in Attachment (4-11) for all domestic sales of the like

product during the period of investigation. Provide clear (PDF-format and hard)

copies for all domestic invoices for each domestic shipment of the like product.

Attach clear (PDF-format and hard) copies of all domestic sales related

documents for 5 domestic invoices of the like product.

50. Complete the table in Attachment (4-11) relating to the breakdown of all the

charges incurred after the ex-factory price on domestic sales in the countries

concerned. Provide evidence and working papers to explain each adjustment for 5

invoices.

Please ensure that all the price adjustments should be made where prices and

price comparability are affected. For this purpose you must claim adjustments

where it can be demonstrated that the factor concerned is one that has resulted

in a different price being charged to your customers.

An adjustment can only be made for expenses that are directly related to the

sales of the like product. For example, advertising expenses can be related to

several activities but only advertising expenses that are directly related to the

sales of the like product can be adjusted such as when such expenses are 17

assumed by the seller on behalf of the buyer and directed toward the like

product.

51. Explain your company’s channels of distribution on the domestic market for the

like product starting from the factory gate up to the first resale to independent

customer. Describe the sales process for each method or channel of distribution

described and provide a detailed flow chart indicating all details (i.e. terms of

sale, pricing, customers) in Attachment (4-12).

The description you provide on your distribution and sales processes is

intended to provide the GCC-TSAIP with the information necessary to make

appropriate comparisons of sales at the same level of trade.

52. Explain the relationship between your company and your customers (OEM’s,

wholesalers, retailers,..etc) mentioned in the reply to Attachment (4-11) and

provide enough details for that in Attachment (4-13) including list of customers’

categories (i.e. OEM’s, Distributors, Retailers, End-users), selling activities

performed in details.

Refer to definition of "affiliated person" in Annex 2.

53. Explain each step in the sales negotiation process of the like product starting from

contacting with the domestic customer (purchase order) up to the delivery of the

like product to this customer. Provide flow chart indicating all details in

Attachment (4-14).

54. Clarify whether a change occurred in the distribution channels or in the sales

negotiation process described above during the period of investigation in

Attachment (4-15) and the reasons for that.

55. Please provide copies of contracts (with English translation) between your

company and your domestic customers for domestic sales in the countries

concerned (either long-term or short- term), describe in detail the process by

which the contracts, the prices, expenses, and quantities therein, are agreed to.

Describe each type of contracts applicable to the like product, including the

terms, the requirements for a price change or re-negotiation by either side, etc.18

56. Are the prices of the like product that your company charges in the countries

concerned:

i) Subject to direct or indirect reimbursement to your domestic market

customers (e.g. sales promotion, advertising, warranty, etc)? or

ii) Influenced by a commercial agreement or relationship (including

mutual corporate affiliations and/or common shareholding)? or

iii) Inclusive of any consideration other than price?

If the answer to (i), (ii) or (iii) above is “yes”, please provide details.

EXPORT SALES OF THE LIKE PRODUCT TO THIRD COUNTRIES

57. Select a third country to which you export the like product and which is

comparable to GCC market in terms of: export volume, market size, distribution

channels, conditions of sales, techniques used in the production process.

58. Explain how the selling prices are set (pricing methods) for export sales to third

countries by providing all the information in terms of:

Delivery Terms: FOB, CIF, .....

Payment: in advance, upon delivery, credit (specify no. of days).....

Policy of granting discounts and rebates: quantity discount, value/cash

discount, .....

After-sales: Warranty, Maintenance contract, ....

Other (if any)

59. Provide in Attachment (4-16) price lists issued by your company for export sales

to third countries during the period of investigation.

60. Complete the table in Attachment (4-17) for all export sales of the like product

to third countries during the period of investigation. Provide clear (PDF-format

and hard) for all export invoices of the like product exported to third country

similar to the GCC and copies of the related export documents for 5 export

shipments of the like product to third country.

61. Complete the table in Attachment (4-17) relating to the breakdown of all the

charges incurred after the ex-factory price on export sales to third countries. 19

Provide evidence and working papers to explain each adjustment for 5 export

invoices of the like product to third country.

Please ensure that all the price adjustments should be made where prices and

price comparability are affected. For this purpose you must claim adjustments

where it can be demonstrated that the factor concerned is one that has resulted

in a different price being charged to your customers.

An adjustment can only be made for expenses that are directly related to the

sales of the like product. For example, advertising expenses can be related to

several activities but only advertising expenses that are directly related to the

sales of the like product can be adjusted such as when such expenses are

assumed by the seller on behalf of the buyer and directed toward the like

product.

62. Explain your company’s channels of distribution to third countries for the like

product starting from the factory gate up to the first independent customer in third

countries. Describe the sales process for each method or channel of distribution

described and provide a detailed flow chart indicating all details in Attachment

(4-18).

The description you provide on your distribution and sales processes is

intended to provide the GCC-TSAIP with the information necessary to make

appropriate comparisons of sales at the same level of trade.

63. Explain the relationship between your company and your customers (OEM’s,

wholesalers, retailers,..etc) mentioned in the reply to Attachment (4-17) and

provide enough details for that in a similar attachment as indicated in

attachments (4-13 & 4-8) including list of customers’ categories (i.e. OEM’s,

Distributors, Retailers, End-users), selling activities performed in details.

Refer to definition of "affiliated person" in Annex 2.

64. Explain each step in the sales negotiation process of the export sales of the like

product to third countries starting from contacting with the customer in the third

20

country (purchase order) up to the delivery of the like product to this customer.

Provide flow chart indicating all details in Attachment (4-19).

65. Clarify whether a change occurred in the distribution channels or in the sales

negotiation process described above during the period of investigation and the

reasons for that in Attachment (4-20).

66. Please provide copies of contracts between your company and your customers for

export sales to third country similar to GCC (either long-term or short- term),

describe in detail the process by which the contracts, and the prices, expenses,

and quantities therein, are agreed to. Describe each type of contracts applicable

to the like product, including the terms, the requirements for a price change or re-

negotiation by either side, etc.

67. If you have any information about exporting your product to the GCC countries

through third countries, please inform the investigation authority within 2 weeks

from the receipt of this questionnaire.

21

5. PURCHASES AND STOCKSPURCHASES

68. In case your company purchased the product under investigation or the like

product from other origins, please indicate in Attachment (5-1) the names of the

suppliers and the reasons for these purchases.

69. Provide invoices’ statement for the purchases of the product under investigation

or the like product and copies of purchase invoices in Attachment (5-2).

70. In case your company purchased raw materials or energy or other services related

to manufacturing from related companies or from companies in which capital you

contribute, please provide a list of the names of those companies with a

description of the nature of the relationship between your company and its

associated companies included all inter-companies transactions, indicating how

purchase prices of raw materials from these companies are determined.

Furthermore, please provide invoices’ statement for the purchases of these

materials from related companies.

71. Please complete Attachment (5-3) regarding the purchase of raw materials.

STOCKS

72. Provide a description of the stock of Raw materials, Semi-finished, and Finished

goods for the period of investigation related to the product under investigation

and the domestic like product and the exported like product to third countries in

Attachment (5-4).

6. PRODUCTION AND COST OF PRODUCTION

6-1 PRODUCTION

73. Complete the table in Attachment (6-1) related to the actual production in

volume for the product under investigation and the like product during the period

of investigation. In case your company manufactures the product under 22

investigation and the like product in more than one factory, please complete this

table separately for each factory.

74. Indicate in Attachment (6-2) the number and the names of your company’s

factories which produce the product under investigation or the like product.

75. Indicate the main inputs’ materials of the production process, whether such

materials were imported, and whether the input value includes import charges and

indirect taxes for both exported and domestic types.

6-2 COST OF PRODUCTION

76. Describe the cost accounting system used by your company to record and allocate

the production cost of the product under investigation (e.g. job costing, process

costing).

77. If your company uses a standard cost system state whether standard costs were

used in your response and whether all variances between standard and actual

costs have been allocated. Explain in detail the allocation method used, as well as

any significant or unusual cost variances that occurred during the investigation

period.

78. Please indicate the cost centers (direct & indirect) and the allocation methods

used regarding the product under investigation.

79. Describe the method used under your company's cost accounting system to

account for byproducts and scrap generated at each stage of the production

process.

80. Does your company receive, either directly or indirectly, any consideration from

a central or provincial Government or other organization (e.g., subsidies export

incentives, etc.) for the products you manufacture and sell? If so, please provide

details of any assistance on a per annum basis or on per unit basis, as appropriate.

81. Provide a copy of the income statement for the product under investigation for the

last 2 financial years including the period of investigation in Attachment (6-3).

Please provide full details of any allocation method used.

23

82. Please provide the cost of production of the product under investigation for

Domestic sales, Export sales to GCC, and exports to countries other than GCC in

Attachments (6-4), (6-5) and (6-6) respectively.

a- Separate schedules should be provided showing the cost structure for

each Model/Size of the product under investigation and the like product

for the period of investigation. This should include the following:

1- Identify and quantify the main raw material components and labour costs, and the basis of distribution/allocation of these costs to the product under investigation and like product during the POI.

2- Identify and quantify the indirect factory overhead costs and the basis of distribution/allocation of these costs to the product under investigation and the like product during the POI.

3- Identify and quantify the elements of SG&A costs, and the methods your company has used to allocate these costs to the product under investigation and the like product during the POI.

b- Attachments (6-4), (6-5), and (6-6) should be provided for each

type/model/Size (PCN) of the product under investigation and the like

product.

c- Supporting documentation for the cost items and working papers

demonstrating the allocation of costs and expenses should be

attached.

24

7. ATTACHMENTS

Attachment N0. Description Remark

1-1 Original power of attorney1-2 Articles of Association and related documents1-3 Business licence1-4 Catalogues or Brochures about your company1-5 Overall organizational structure of your company

1-6 Related companies of your companyTable is attached

1-7 Shareholders of your companyTable is attached

2-1 Catalogues or brochures for the product under investigation

2-2 Types of the product under investigation Table is attached

2-3Differences between the product under investigation and the like products

Table is attached

3-1Audited Financial Accounts for the last 3 years including the POI for the company

3-2 Copy of Chart of Accounts3-3 List of Exchange Rate for domestic currency against US$3-4 list of inflation rates on a monthly basis for the POI

4-1 Total sales during the period of investigation Table is attached

4-2Sales of the product under investigation to unrelated customers

Table is attached

4-3Sales of the product under investigation to subsidiaries and related customers

Table is attached

4-4Studies about the product under investigation or the like product

4-5 Price lists for export to the GCC Countries during the POI

4-6Export sales of the product under investigation to the GCC Countries during the POI

Table is attached

4-7 Flow chart of Distribution Channels for exports to GCC

4-8Customers for the product under investigation to GCC during the POI

Table is attached

4-9 Flow chart of sales negotiation process for exports to GCC4-10 Price Lists for domestic sales4-11 Domestic sales of the like product during the POI Table is

25

attached4-12 Domestic Flow chart of Sales process& Distribution Channels

4-13Domestic customers who sell the like product in your domestic market during the POI

Table is attached

4-14 Domestic flow chart of sales negotiation process4-15 Changes in distribution channels & sales negotiation process4-16 Price lists for export to third countries during the POI

4-17 Export sales to third countries during the POI Table is attached

4-18 Flow chart of distribution channels for sales to third countries

4-19Flow chart of sales negotiation process for sales to third countries

4-20Changes in distribution channels & sales negotiation process in third country.

5-1Suppliers for purchase of the product under investigation or the like product

Table is attached

5-2Invoices statement for the purchases of the product under investigation or the like product

Table is attached

5-3 Purchase of Raw materials Table is attached

5-4 Stock of raw materials, work-in-process, and finished goods Table is attached

6-1Actual production in volume for the product under investigation and the like product during the POI

Table is attached

6-2Your company’s factories producing the product under investigation

Table is attached

6-3 Income statement for the product under investigation the POI Table is attached

6-4Factory Cost and Profit for Domestic Sales of the Like Product.

Table is attached

6-5Factory Cost and Profit for Export Sales of Product under Investigation to the GCC.

Table is attached

6-6Factory Cost and Profit for Export Sales of the Like Product to Third Countries (same country as reported in Att.4-17)

Table is attached

26

Attachment (1-6)

Affiliated companies

Name, address, phone, fax, email, and website of

related company

Please tick (√)

if involved in any way with the product

under investigation or

the like product

List

activities

Percentage of share-

holding in related

company

%

Percentage of share-holding

of related company in

your company

%

27

Attachment (1-7)

Shareholders of your company

websiteEmailFaxTelJob

title

Share in the capital

AddressNameSeries

28

Attachment (2-2)

Types of the product under investigation

RemarksPCNExport

sales code

Domestic

sales code

Productio

n code

Type/Model/

Size

Provide this table in Excel

29

Attachment (2-3)

Differences between the product under investigation and the like products

Like product

exported to third

countries

Like product in

the domestic

market

Product under

investigation

exported to GCC

Difference

Provide this table in Excel

30

Attachment (4-1)

Total Sales during the period of investigation

Year xxxx

ValueVolumeData

Total Sales (as in income statements)

Domestic sales for all products

Export sales for all products

Specify currency

Specify the unit of measurement

Provide this table in Excel

31

Attachment (4-2)

Sales of the product under investigation to unrelated customers

during the POI

Year xxxx

ValueVolumeData

Domestic sales to (unrelated customers) for the Like product

Export sales to (unrelated customers) in the GCC for the

product under investigation

Export sales to (unrelated customers) in all third countries

for the like product

Specify currency

Specify the unit of measurement

Provide this table in Excel

32

Attachment (4-3)

Sales of the product under investigation to subsidiaries and related customers during the POI

Year xxxx

ValueQuantity/VolumeData

Domestic sales to (related customers) for the Like product

Export sales to (related customers) in the GCC for the product under

investigation

Export sales to (related customers) in all third countries for the like

product

Specify currency Specify the unit of measurement Provide this table in Excel.

33

Attachment (4-6)

Export sales of the product under investigation to the GCC Countries during the POI

Oth

er (S

peci

fy)

Ban

k ch

arge

s

Cre

dit C

ost

com

mis

sion

s

Inla

nd F

reig

ht

Pack

ing

Han

dlin

gD

isco

unt

Insu

ranc

e O

cean

Fre

ight

Paym

ent t

erm

1

Cur

renc

y

Del

iver

y te

rms

Invo

ice

Val

ue

Quantity/Volume PC

N

Prod

uct

Des

crip

tion

Prod

uct

Mod

el/S

ize

Exp

ort S

ales

C

ode

Prod

uctio

n C

ode

Impo

rter

C

ount

ryIm

port

er C

ode

Impo

rter

Nam

e

Exp

orte

r C

ode2

Exp

orte

r N

ame3

Arr

ival

Por

t

Ship

ping

Por

t

Ship

ping

Dat

e

Invo

ice

Dat

e

Invo

ice

No.

Provide this table in Excel Specify currency Specify the unit of measurement Attach copies of export documents for 5 export invoices for the product under investigation. Attach evidence and working papers to explain each adjustment for 5 invoices.

1 In case of credit sales, specify the number of days in which payment is made.2 In case your company is the exporting producer for the product under investigation, then write (Not Applicable or N/A).3

34

Attachment (4-8)

Customers of the product under investigation exported to GCC during the POI

Website

Em

ail

Fax

Tel

Add

ress

Value of annual transactions for the

product under investigation

35

Attachment (4-11)

Domestic sales of the like product during the POI

Oth

er

(Spe

cify

)

Cre

dit C

ost

Han

dlin

g

Pack

ing

Inla

nd

Frei

ght

Dis

coun

ts

Invo

ice

Val

ue

Del

iver

y da

teT

erm

s1

Cur

renc

y

Del

iver

y te

rmsQuantity/

Volume PCN

Prod

uct

Des

crip

tion

Prod

uct

Mod

el/S

ize

Cus

tom

er

Cod

eC

usto

mer

N

ame

Nam

e2

Dom

estic

Sa

les c

ode

Prod

uctio

n co

de

Invo

ice

date

Invo

ice

No.

Attach copies for all related documents for 5 domestic sales invoices of the like product.

Provide this table in Excel

Specify currency

Specify the unit of measurement

Attach evidence and working papers to explain each adjustment for 5 invoices.

1 In case your company doesn’t sell the product under investigation for other producers in the domestic market, then write (Not Applicable or N/A).2 In case of credit sales, specify the number of days in which payment is made.

36

Attachment (4-13)

Domestic customers who sell the like product in your domestic market during the POI

Site webEmailFaxTelAddressValue of annual transactions for the Like product

Nature of relationship

(i.e. affiliated, subsidiary, …

etc)

Category (OEM,

Distributor,

wholesaler, Retailer, end-user)

ActivityCountry

Customer Name

and Code

Specify currency

37

Attachment (4-17)

Export sales of the like product to third countries during the POIPa

ckin

g

Oce

an F

reig

htPa

ymen

t ter

m1

Cur

renc

y

Del

iver

y te

rms

Invo

ice

Val

ue

Quantity/Volume PC

N

Prod

uct

Des

crip

tion

Prod

uct

Mod

el/S

ize

Exp

ort S

ales

C

ode

Prod

uctio

n C

ode

Impo

rter

C

ount

ryR

elat

ions

hip

with

Impo

rter

or

exp

orte

rIm

port

er N

ame

Exp

orte

r C

ode

Nam

e2

Arr

ival

Por

t

Ship

ping

Por

t

Ship

ping

Dat

e

Invo

ice

Dat

e

Invo

ice

No.

Attach copies of export documents for 5 invoices for the exported like product Provide this table in Excel Specify currency Specify the unit of measurement Attach evidence and working papers to explain each adjustment for 5 invoices.

1 In case of credit sales, specify the number of days in which payment is made.

2 In case your company is the exporting producer for the product under investigation, then write (Not Applicable or N/A).

38

Attachment (5-1)

Suppliers

Reasons for

purchase

Site webEmailFaxTelAddress

Value of annual

transactions for the

product under investigation

Nature of relationship

(i.e. affiliated, subsidiary, …

etc)

ActivityCountryName

Specify currency

39

Attachment (5-2)

Invoices statement for the purchases of the product under investigation or the like product

Country of origin

Customer codeRelationCustomer

namePayment

termsDelivery

termsInvoice ValueQuantity/

VolumeInvoice

dateInvoice

No.PCNProduct Description

Product Model/Size

Sales code

Provide this table in Excel Specify currency Specify the unit of measurement Attach copies of purchase invoices

40

Attachment (5-3)

Purchase of Raw Materials

Purchased domestically Imported with dutiesTOTAL

Raw Materials

Country of origin

Supplier Name Relation Value Quantity Duty paid

(if any)

Value

CIFQuantity Duty paid

(if any)Value Quantity Average cost per

unit

a)

b)

c)

d)

….etc

TOTAL

Provide this table in Excel Specify currency and unit of measurement.

41

Attachment (5-4)

Year xxxxDataValueVolume

Stock of raw materialsOpening stock:

Raw material 1Raw material 2………etcClosing stock:

Raw material 1Raw material 2………etc

Stock of Semi-finished GoodsOpening stock:

Semi-finished product (model/Size) 1Semi-finished product (model/Size) 2………etcClosing stock:

Semi-finished product (model/Size) 1Semi-finished product (model/Size) 2………etc

Stock of Finished GoodsOpening stock:

Product (Model/ Size) 1Product (Model/ Size) 2………etcClosing stock:

Product (Model/ Size) 1Product (Model/ Size) 2………etc

Stock during the POI related to the product under investigation and the domestic like product and the exported like product to third countries

Provide this table separately for the product under investigation and domestic like product and exported like product to third countries.

Provide these Table in Excel

Specify Currency

Specify the unit of measurement

42

Attachment (6-1)

Actual production during the POI

Year xxxxDataProduction

CostVolume

Total production of all products

Total production of the product under investigation

Total production of the exported product under

investigation to the GCC

Total production of the like product for domestic

sales

Total production of the like product for exports to

all third countries

Provide this Table in Excel

Provide this Table for each factory.

Specify the currency

Specify the unit of measurement

43

Attachment 6-2

Your company’s factories producing the product under investigation

Production in volumeTelCountryCityAddressFactory name

Provide this table in Excel

Specify the unit of measurement

44

Attachment 6-3

Income statement for the product under investigation in the last two years including the POI

Precedent yearPOIDataAll

products

Product under investigationAll products

Product under investigation

Export sales to third

countries

Export sales

to GCC

Domestic sales

Export sales to third

countries

Export sales

to GCC

Domestic sales

Sales revenueLess (Sales returns,

discount, allowances)

Net sales revenueLess

Cost of Goods SoldBeginning Inventory

+ Cost of Production

- Ending Inventory

Gross ProfitSelling Expense

Administrative and General expenses

Financing Expenses

Net profit / loss before tax

TaxNet profit / loss

Specify the Currency

Provide these Tables in Excel.

45

Attachment 6-4

Factory Cost and Profit for Domestic Sales of the Like Product during the POI

Cost Element Product (1) /Size/Model

Product (2) /Size/Model

Product (3) /Size/Model

PCN (1) PCN (2) PCN (3)1) Direct Materials

a) ………b) ……….c) ……....d) Others (Please Specify)

2) Direct Labour

3) Manufacturing Overhead

- Indirect materials- Indirect labour- Energy costs- Depreciation- Maintenance and repairs- Packaging Costs- Packaging Costs1

- Others (Please Specify)4) Total Manufacturing Cost

(1+2+3)5) Selling, General and Administrative

Expenses (SGA)- Insurance- Inland freight- Commissions- Advertising- R&D- Others (Please Specify)

6) Financing Expenses

TOTAL COST OF PRODUCTION (4+5+6)Net Profit/Loss before Tax

Selling Price Ex-Factory

Lines may be added to reflect the company’s cost structure. The cost data above must be provided for each Model/Size of the domestic like product. This information must also be provided in Excel. Specify Currency. Specify the unit of measurement

- Packaging Costs

1 If the packing process is part of the manufacturing process detail it here, otherwise it should be included in the selling expense.

46

Attachment 6-5

Factory Cost and Profit for Export Sales of Product under Investigation to the GCC during the POI

Cost Element Product (1) /Size/Model

Product (2) /Size/Model

Product (3) /Size/Model

PCN (1) PCN (2) PCN (3)1) Direct Materials

a) ………b) ……….c) ……....d) Others (Please Specify)

2) Direct Labour

3) Manufacturing Overhead

- Indirect materials- Indirect labour- Energy costs- Depreciation- Maintenance and repairs- Packaging Costs- Packaging Costs1

- Others (Please Specify)4) Total Manufacturing Cost

(1+2+3)5) Selling, General and Administrative

Expenses (SGA)- Insurance- Inland freight- Commissions- Advertising- R&D- Others (Please Specify)

6) Financing Expenses

TOTAL COST OF PRODUCTION (4+5+6)Net Profit/Loss before Tax

Selling Price Ex-Factory

Lines may be added to reflect the company’s cost structure. The cost data above must be provided for each Model/Size of the domestic like product. This information must also be provided in Excel. Specify Currency. Specify the unit of measurement

- Packaging Costs

1 If the packing process is part of the manufacturing process detail it here, otherwise it should be included in the selling expense.

47

Attachment 6-6 **

Factory Cost and Profit for Export Sales of the Like Product to Third Countries during the POI

Cost Element Product (1) /Size/Model

Product (2) /Size/Model

Product (3) /Size/Model

PCN (1) PCN (2) PCN (3)1) Direct Materials

a) ………b) ……….c) ……....d) Others (Please Specify)

2) Direct Labour3) Manufacturing Overhead

- Indirect materials- Indirect labour- Energy costs- Depreciation- Maintenance and repairs- Packaging Costs- Packaging Costs1

- Others (Please Specify)4) Total Manufacturing Cost

(1+2+3)5) Selling, General and Administrative

Expenses (SGA)- Insurance- Inland freight- Commissions- Advertising- R&D- Others (Please Specify)

6) Financing ExpensesTOTAL COST OF PRODUCTION (4+5+6)Net Profit/Loss before Tax

Selling Price Ex-FactoryLines may be added to reflect the company’s cost structure.

** same country as used in Attachment (4-17) The cost data above must be provided for each Model/Size of the domestic like product. This information must also be provided in Excel. Specify Currency. Specify the unit of measurement

- Packaging Costs

1 If the packing process is part of the manufacturing process detail it here, otherwise it should be included in the selling expense.

48

4- ANNEXS

ANNEX 1: CERTIFICATE

The undersigned on behalf of (name of company) certifies that all information

supplied in this questionnaire is correct and complete accordingly to records of the

company,

And in case of differences between the information submitted and those recorded in

you company, the GCC-TSAIP has the right to disregard this information,

And understands that the information submitted in this questionnaire or any

information submitted during the investigation proceeding may be subject to audit and

verification by the GCC-TSAIP.

Date signature of authorized official

Company stamp name and title of authorized official

49

ANNEX 2: GLOSSARY

WTO Agreement on Implementation of Article VI of the General Agreement on Tariffs and Trade 1994

Antidumping agreement

The GCC Common Law on Anti-Dumping, Countervailing and safeguard measures

The GCC Common Law

Exporting a product to GCC Member States at less than its normal value in the ordinary course of trade for the like product in the exporting country.

Dumping

Injury shall mean material injury to a GCC industry, threat of material injury to a GCC industry or material retardation of the establishment of such an industry.

Injury

Causal relationship between the dumped imports and the injury to the GCC industry. It should be determined on the basis of examination of all relevant evidence. The investigation authority will take actions only against the dumped imports which cause injury to the GCC industry. The injury caused by other factors must not be attributed to dumped imports.

Causal link

The price paid or payable for the product under investigation when sold for export from the exporting country to the GCC market

Export price:

The price paid or payable, for the like product in the ordinary course of trade when destined for consumption in the exporting country

Normal value:

The difference between the normal value and the export price during the period of investigation

Dumping amount:

Percentage of dumping amount relatively to the export priceDumping margin

A fair comparison has to be made between the export price and the normal value. Due allowances have to be made in each case, on its merits, for differences which affect price comparability, including discounts, rebates and quantities, transport, insurance, handling, loading and ancillary costs, packing, credit, after-sales costs, commissions.

Adjustments

It shall be considered to be de minimis if the dumping margin is less than two percent (2), expressed as a percentage of the export price. In this case the investigation shall be terminated

De minimis

The imported product as described in the notice of initiation of the investigation.

Product under investigation

50

GCC products which are identical or alike in all respects to the product under investigation, or in the absence of such a product, another product which, although not alike in all respects, has characteristics closely resembling those of the product under investigation

Like products:

GCC Industry: Member States’ producers as a whole of the like products or those of them whose collective output of the products constitutes a major proportion of the total domestic production of those products. For the purpose of safeguard investigations, the term GCC industry shall mean total Member States producers as a whole of the like or directly competitive products operating within the territory of Member states, or those whose collective output of the like or directly competitive products constitutes a major proportion of the total domestic production of those products.

GCC Industry:

Bureau of the Technical Secretariat of Anti-injurious Practices in International Trade

GCC Competent authority

Combined markets of the GCC Member States.GCC market:

Buyer(s) without association, and without a commercial or production partnership with the importer in the importing country or with the exporter or producer in the exporting country, and without any relationship with them, or where both of them are not controlled by a third party directly or indirectly and where neither of them are members of same family.

Independent buyer(s):

Under relevant trade laws, transactions between affiliated persons are subject to particular scrutiny. Affiliated persons (affiliates) include (1) members of a family, (2) an officer or director of an organization and that organization, (3) partners, (4) employers and their employees, and (5) any person or organization directly or indirectly owning, controlling, or holding with power to vote, five percent or more of the outstanding voting stock or shares of any organization and the organization. In addition, affiliates include (6) any person who controls any other person and the other person, and (7) any two or more persons who directly control, are controlled by, or are under common control with, any person. “Control” exists where one person or organization is legally or operationally in a position to exercise restraint or direction over the other person or organization.

Affiliated Person(s):

An arms-length transaction is a voluntary sale involving two parties who are independent of each other. In such a transaction no special consideration, such as preferred pricing arrangements, special services, etc., is made because of one party’s relationship

Arm’s-Length Transaction:

51

to the other. Sales within a company, or other transactions between two parties having some legal, financial, or other common connection, are not considered to be arm’s length transactions.

In order to establish whether differences in levels of trade exist, the GCC-TSAIP reviews distribution systems, including categories of customers, selling activities, and levels of selling expenses for each type of sale. Different levels of trade are typically characterized by purchasers at different stages in the chain of distribution and sellers performing qualitatively and/or quantitatively different selling activities. Different levels of trade necessarily involve differences in selling activities, although differences in selling activities alone are not sufficient to establish differences in levels of trade. Similarly, customer categories such as OEM’s, distributor, wholesaler, retailer, and end-user are often useful in identifying levels of trade, although they, too, are insufficient in themselves to establish differences in levels of trade. Rather, the GCC-TSAIP evaluates differences in levels of trade based on a seller’s entire marketing process.

A level of trade adjustment may be granted where a company can show that your domestic sales of the like product are being made at a level of trade different from the level of trade of its export sales and that such difference has affected price comparability. For this purpose, any claims should clearly identify the domestic and export levels of trade by demonstrating that functions and prices for the sales in question are shown to be appropriate to the alleged levels of trade on both markets.

Level of Trade

Period of investigation during which should be determined the existence of dumping, injury and causal link between them.

POI

The GCC-TSAIP may carry out on-spot visits to examine the records of the company and to verify the information provided in this questionnaire

On-spot visit

The commitment given by the interested party that information submitted in the questionnaire are correct and complete

Certificate

52

ANNEX 3: GUIDELINES FOR COMPLETING THE NON-LIMITED DATA

To protect confidential information, the following instructions show you how to complete the non-limited data:

When the information concerns numbers for various years you can use indices.Example of limited information:

2014 2015 201630000 60000 80000

The non-limited version could be as follows:2014 2015 2016100 200 267

When the limited information concerns text you can either summarize it or eliminate the names of parties by indicating their function.

53