Embed Size (px)

Citation preview

Gas Customer ForumTransmission Update

Chris Logue

9th July 2007

Items

Gas Quality Web Site

Introduction to MIPI Winter Outlook

Gas Quality

Commenced UNC Workshops to work up the requirements of Ofgem’s previous consultation process.

NG invest to provide service User commitment to send investment signal to NG

Process currently stalled pending a new consultation document from Ofgem

Market Information Provision Initiative

Market Information Provision

Content of presentation:

Evolution of current system (IE3) Current Presentation of Information Drivers for Change Market Information Provision Initiative (MIPI) MIPI presentation Concepts MIPI future communications

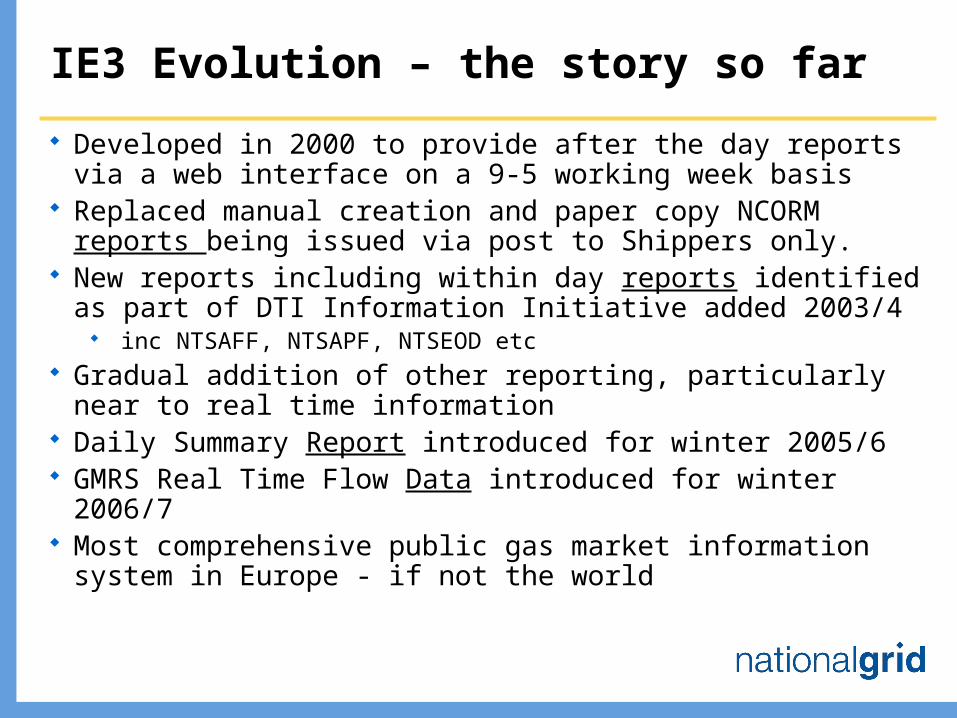

IE3 Evolution – the story so far

Developed in 2000 to provide after the day reports via a web interface on a 9-5 working week basis

Replaced manual creation and paper copy NCORM reports being issued via post to Shippers only.

New reports including within day reports identified as part of DTI Information Initiative added 2003/4

inc NTSAFF, NTSAPF, NTSEOD etc Gradual addition of other reporting, particularly near to real

time information Daily Summary Report introduced for winter 2005/6 GMRS Real Time Flow Data introduced for winter 2006/7 Most comprehensive public gas market information system

in Europe - if not the world

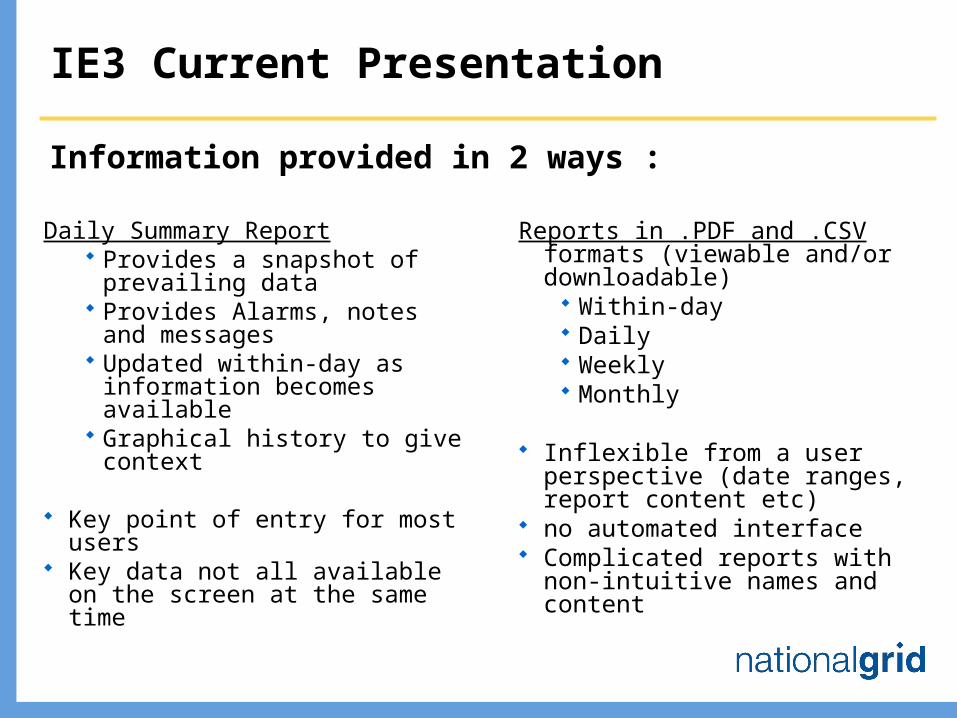

IE3 Current Presentation

Daily Summary Report Provides a snapshot of

prevailing data Provides Alarms, notes and

messages Updated within-day as

information becomes available

Graphical history to give context

Key point of entry for most users Key data not all available on the

screen at the same time

Reports in .PDF and .CSV formats (viewable and/or downloadable)

Within-day Daily Weekly Monthly

Inflexible from a user perspective (date ranges, report content etc)

no automated interface Complicated reports with non-

intuitive names and content

Information provided in 2 ways :

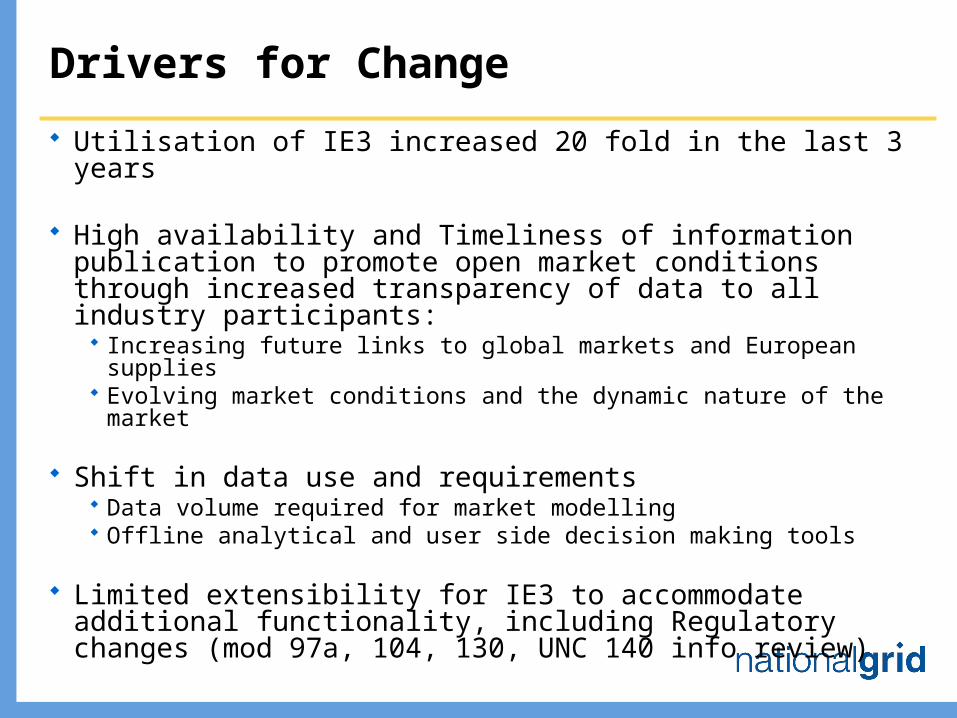

Drivers for Change

Utilisation of IE3 increased 20 fold in the last 3 years

High availability and Timeliness of information publication to promote open market conditions through increased transparency of data to all industry participants:

Increasing future links to global markets and European supplies Evolving market conditions and the dynamic nature of the market

Shift in data use and requirements Data volume required for market modelling Offline analytical and user side decision making tools

Limited extensibility for IE3 to accommodate additional functionality, including Regulatory changes (mod 97a, 104, 130, UNC 140 info review)

MIPI

Market Information Provision Initiative

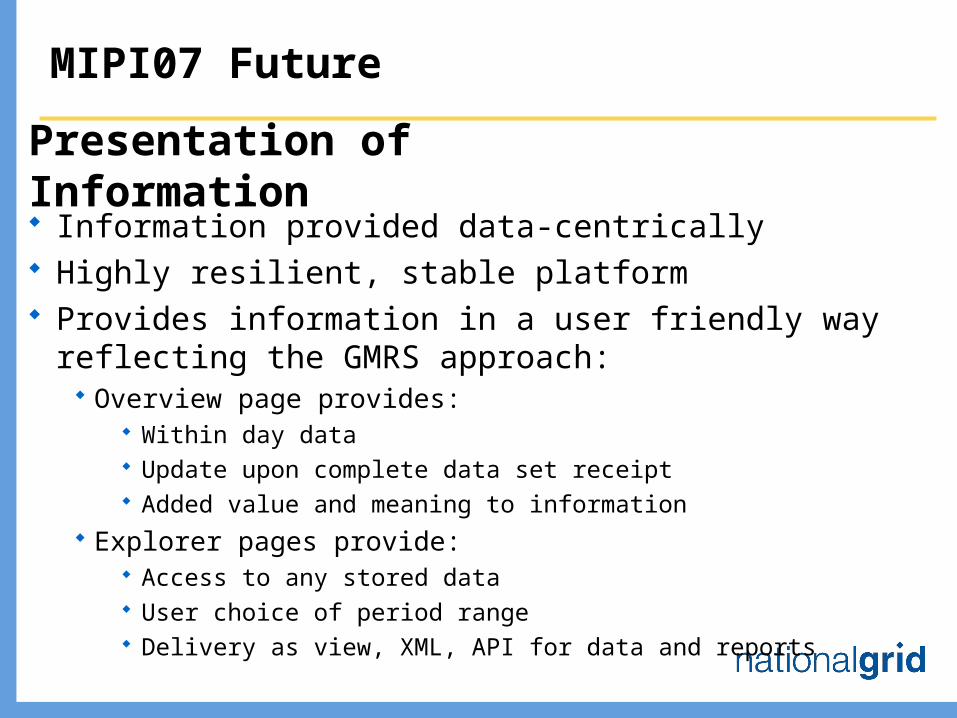

MIPI07 Future

Information provided data-centrically Highly resilient, stable platform Provides information in a user friendly way reflecting the

GMRS approach: Overview page provides:

Within day data Update upon complete data set receipt Added value and meaning to information

Explorer pages provide: Access to any stored data User choice of period range Delivery as view, XML, API for data and reports

Presentation of Information

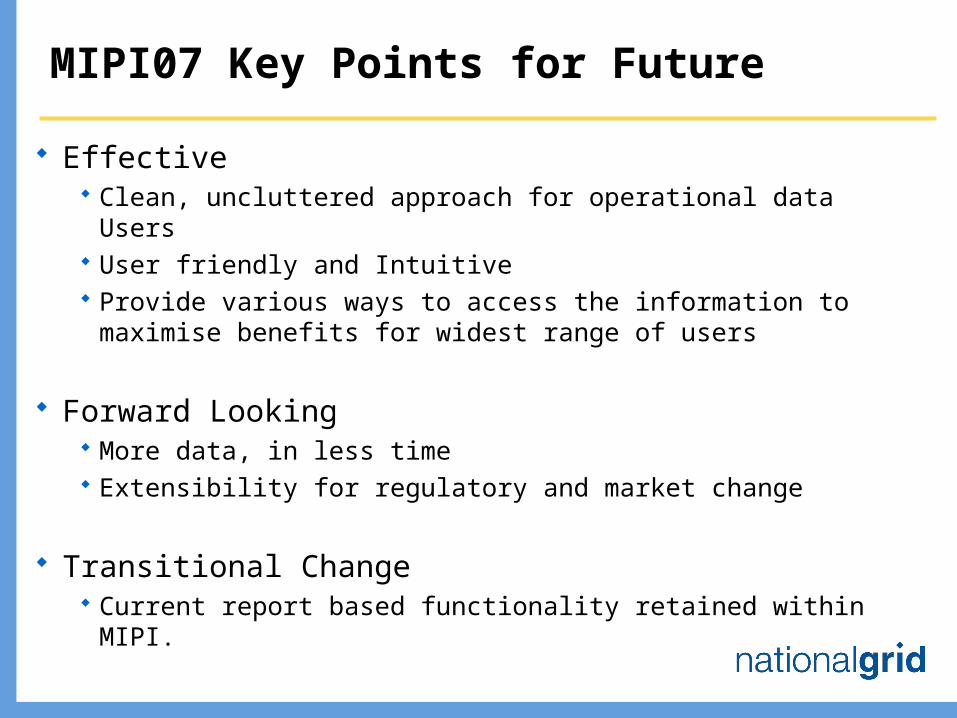

MIPI07 Key Points for Future

Effective Clean, uncluttered approach for operational data Users User friendly and Intuitive Provide various ways to access the information to maximise

benefits for widest range of users

Forward Looking More data, in less time Extensibility for regulatory and market change

Transitional Change Current report based functionality retained within MIPI.

Presentation Concepts

Three Tier

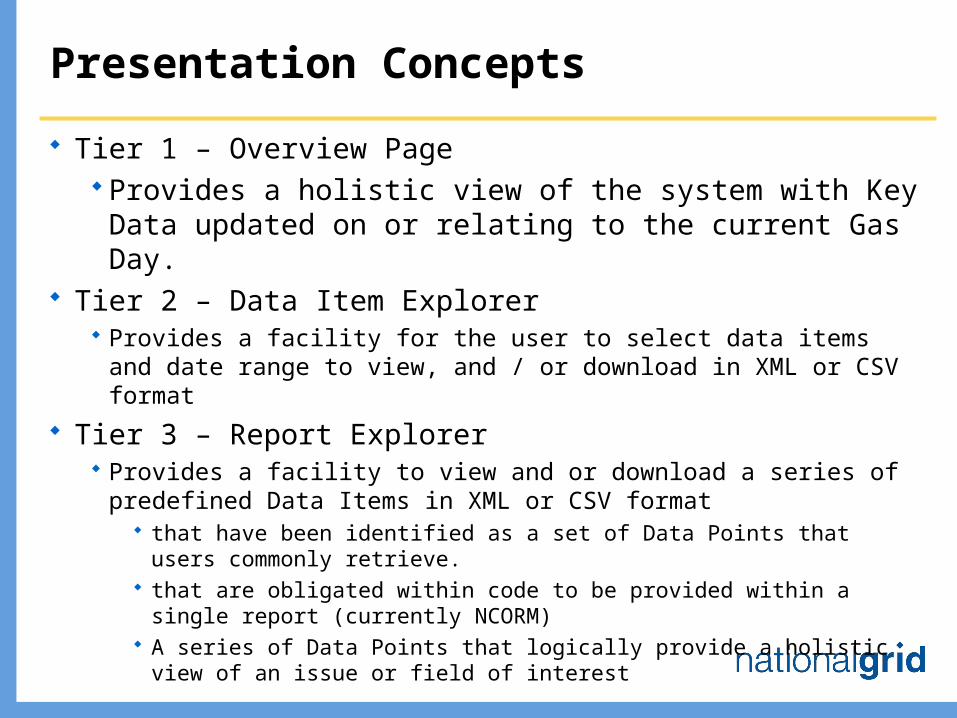

Presentation Concepts

Tier 1 – Overview Page Provides a holistic view of the system with Key Data

updated on or relating to the current Gas Day. Tier 2 – Data Item Explorer

Provides a facility for the user to select data items and date range to view, and / or download in XML or CSV format

Tier 3 – Report Explorer Provides a facility to view and or download a series of predefined

Data Items in XML or CSV format that have been identified as a set of Data Points that users commonly

retrieve. that are obligated within code to be provided within a single report

(currently NCORM) A series of Data Points that logically provide a holistic view of an issue

or field of interest

MIPI future communications

Planned communications for MIPI include:

Web News (July) Regional Seminars (August / September) API specific seminar (August) API Documentation (August) Trade journalist seminar (August / September) Industry Groups presentations (September) Go-Live October

Winter Consultation Report – June 2007

Gas Demand

Now updated, similar to 2006 forecast for 2007/8 Marginally higher due to lower gas price increasing

demand in power generation sector Power generation forecasts are now forecast on a

quarterly basis with Jan – March using gas as the marginal fuel with the rest of the year as the preferred fuel

Historical assessment of demands continues to provide sound validation of techniques used

Power generation assessment

Average Cold Spell (ACS) 60.8 GW Plant margin 23% Average plant availability 86% (CCGTs 90%) Demand side response from CCGTs is limited at

peak demands as coal is already assumed as the preferred generating source

At lower demands 10 – 20 mcm/d of additional gas could be made available to the market

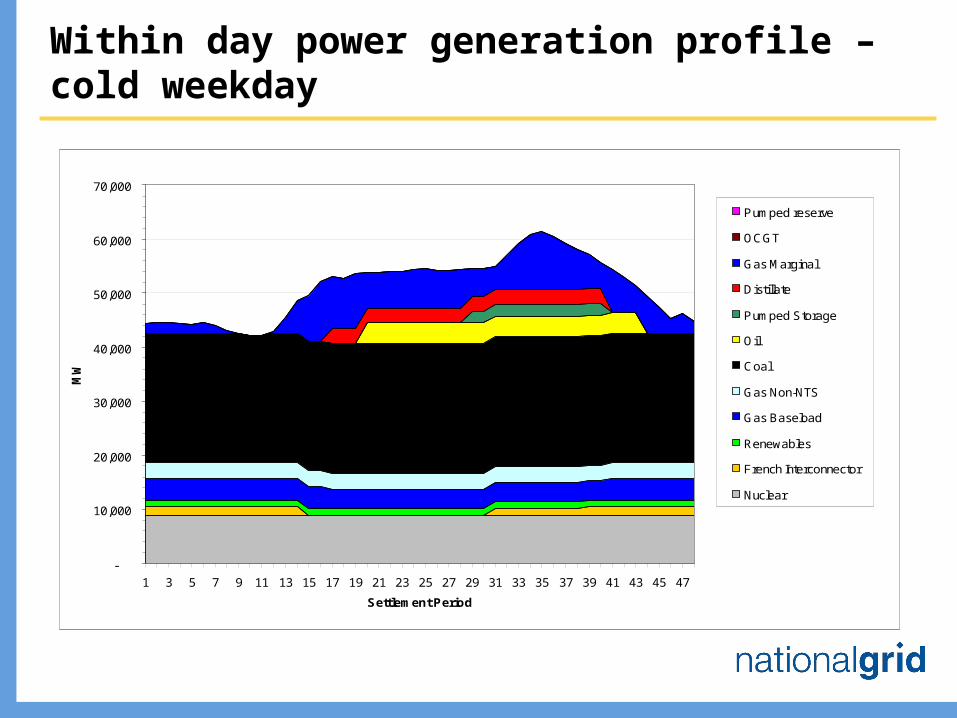

Within day power generation profile – cold weekday

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47

Settlement Period

MW

Pumped reserve

OCGT

Gas Marginal

Distillate

Pumped Storage

Oil

Coal

Gas Non-NTS

Gas Baseload

Renewables

French Interconnector

Nuclear

Transportation Issues

Interruption for capacity management is available to transporters but not expected at material levels

Supply patterns expected to shift to reflect new imports, considerable investment has been made for these to honour Baselines

If implemented, trades and transfers Modifications may impact Baselines

Easington – Pannel to Nether Kellet on schedule, primarily for Aldbrough but will provide capacity to Easington area when Hornsea or Aldbrough flows are reduced

Milford Haven – both connecting pipelines (MH to Aberdulais & Felindre to Tirley) still target completion for next winter

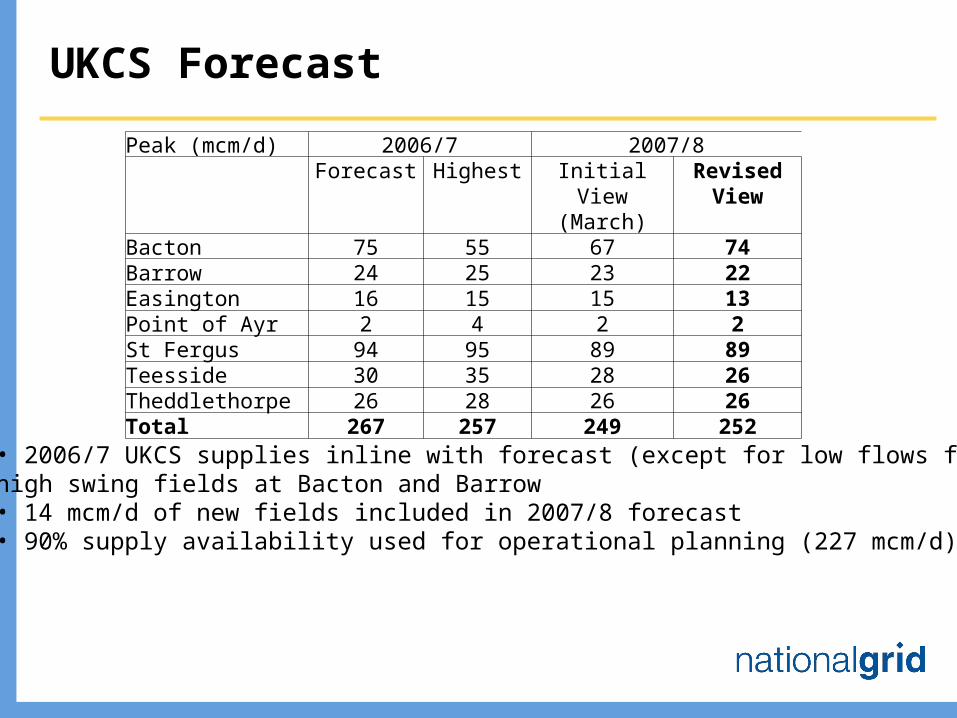

UKCS Forecast

Peak (mcm/d) 2006/7 2007/8Forecast Highest Initial View

(March)Revised

ViewBacton 75 55 67 74Barrow 24 25 23 22Easington 16 15 15 13Point of Ayr 2 4 2 2St Fergus 94 95 89 89Teesside 30 35 28 26Theddlethorpe 26 28 26 26Total 267 257 249 252

• 2006/7 UKCS supplies inline with forecast (except for low flows fromhigh swing fields at Bacton and Barrow • 14 mcm/d of new fields included in 2007/8 forecast• 90% supply availability used for operational planning (227 mcm/d)

Imports (1)

IUK Further expansion planned to 74 mcm/d Expected to operate as marginal source of supply, following price

differentials Expected to have higher import potential post December

BBL Expected to flow at near uniform 25 mcm/d to satisfy Centrica contract (3

bcm summer, 5 bcm winter) Norway

Ormen Lange still reported to be on schedule for October delivery High volumes expected through Langeled & Vesterled with low volumes

through newly completed Tampen Link Langeled imports assumed at 45 mcm/d to enable near full volumes from

Rough. Higher volumes may impact other Easington deliveries

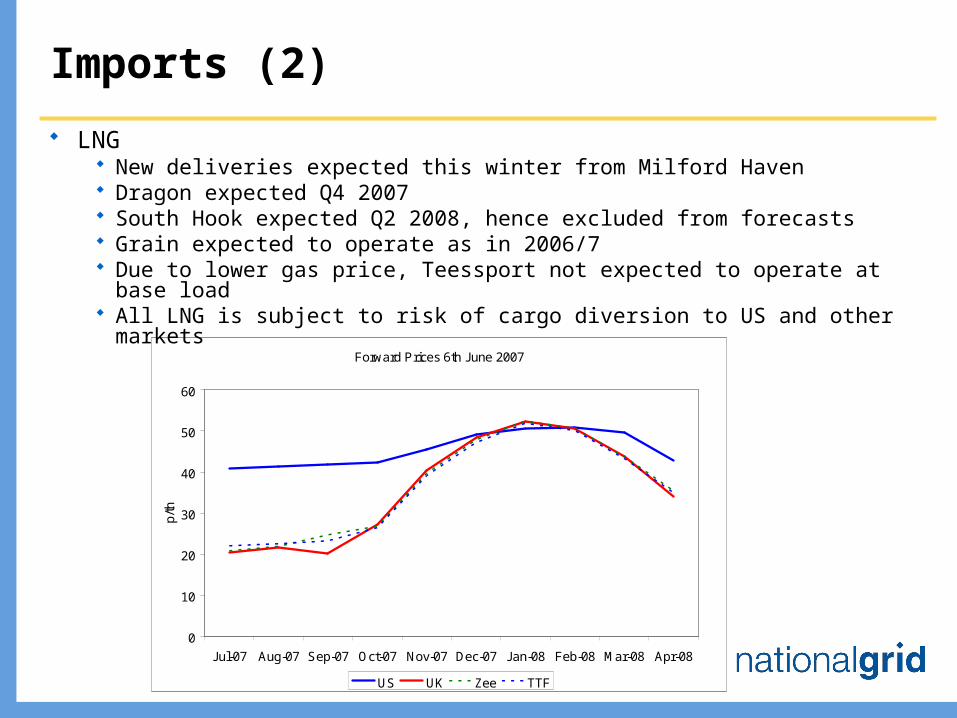

Imports (2)

LNG New deliveries expected this winter from Milford Haven Dragon expected Q4 2007 South Hook expected Q2 2008, hence excluded from forecasts Grain expected to operate as in 2006/7 Due to lower gas price, Teessport not expected to operate at base load All LNG is subject to risk of cargo diversion to US and other markets

Forward Prices 6th June 2007

0

10

20

30

40

50

60

Jul-07 Aug-07 Sep-07 Oct-07 Nov-07 Dec-07 Jan-08 Feb-08 Mar-08 Apr-08

p/th

US UK Zee TTF

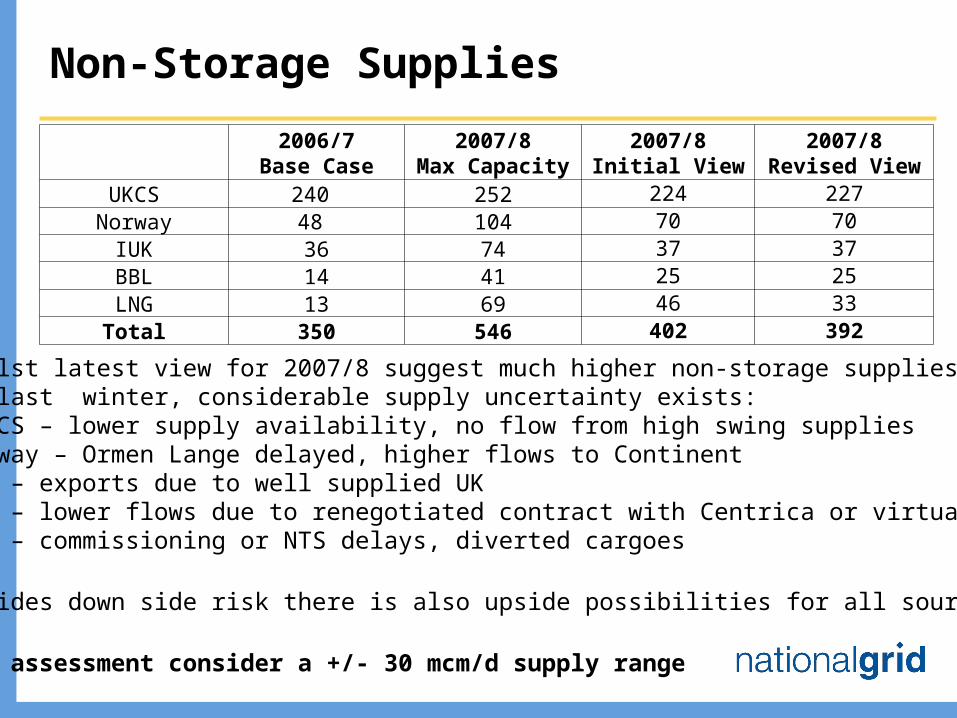

Non-Storage Supplies

2006/7Base Case

2007/8Max Capacity

2007/8Initial View

2007/8Revised View

UKCS 240 252 224 227Norway 48 104 70 70

IUK 36 74 37 37BBL 14 41 25 25LNG 13 69 46 33Total 350 546 402 392

•Whilst latest view for 2007/8 suggest much higher non-storage supplies thanfor last winter, considerable supply uncertainty exists:• UKCS – lower supply availability, no flow from high swing supplies•Norway – Ormen Lange delayed, higher flows to Continent•IUK – exports due to well supplied UK•BBL – lower flows due to renegotiated contract with Centrica or virtual exports•LNG – commissioning or NTS delays, diverted cargoes

•Besides down side risk there is also upside possibilities for all sources

•For assessment consider a +/- 30 mcm/d supply range

Storage

For next winter we anticipate higher storage availability through:

Hole House Farm – increased deliverability Aldbrough – new salt cavity storage, phased build-up of

capacity expected

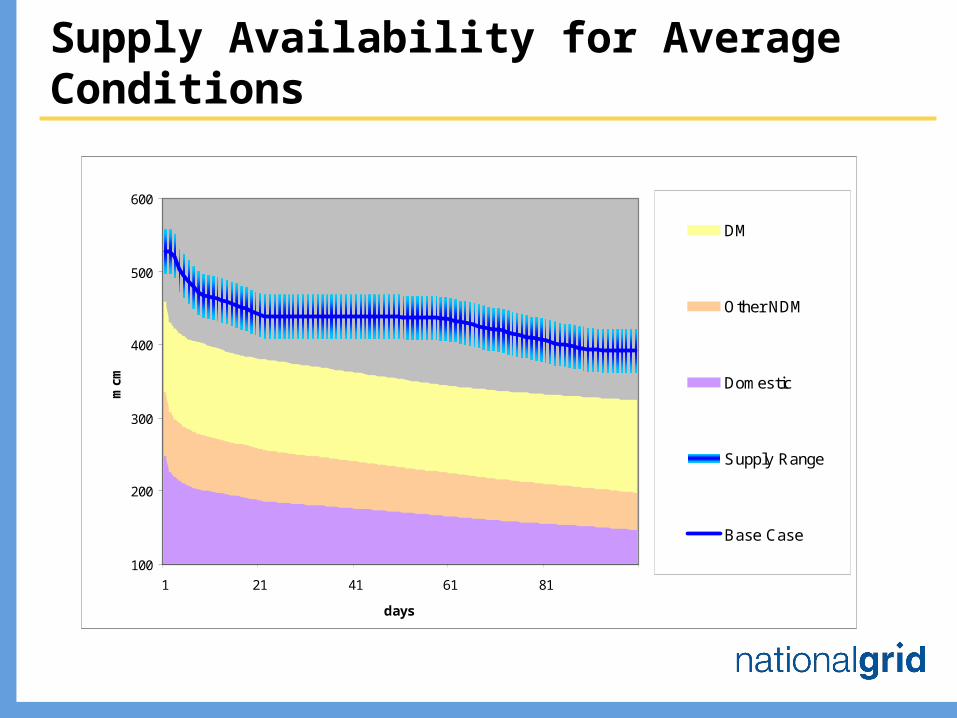

Supply Availability for Average Conditions

100

200

300

400

500

600

1 21 41 61 81

days

mcm

DM

Other NDM

Domestic

Supply Range

Base Case

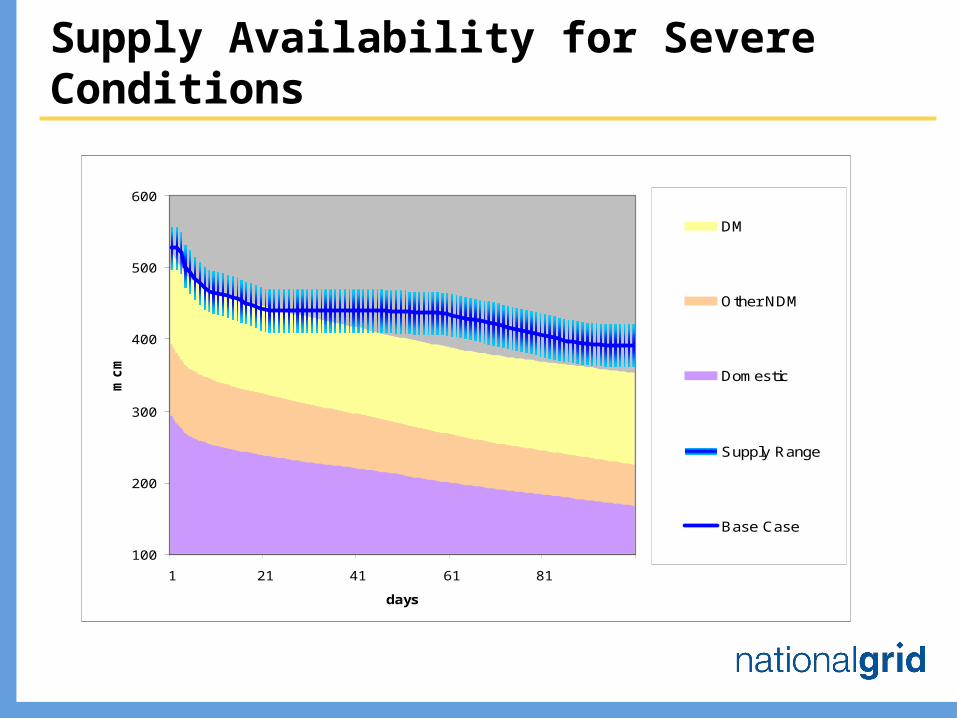

Supply Availability for Severe Conditions

100

200

300

400

500

600

1 21 41 61 81

days

mc

m

DM

Other NDM

Domestic

Supply Range

Base Case

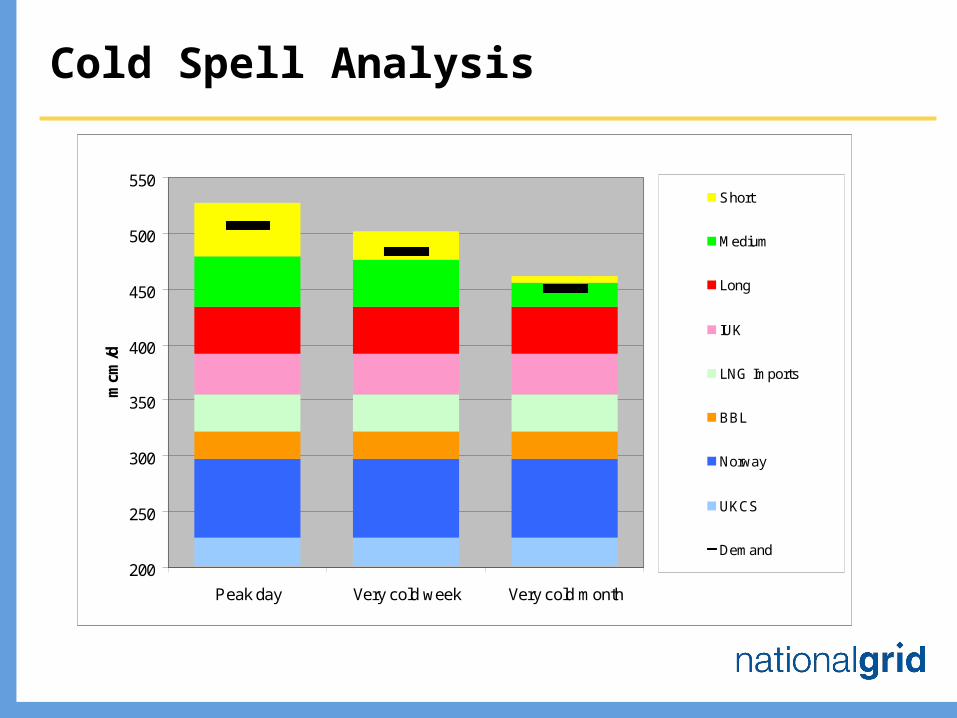

Cold Spell Analysis

200

250

300

350

400

450

500

550

Peak day Very cold week Very cold month

mcm

/d

Short

Medium

Long

IUK

LNG Imports

BBL

Norway

UKCS

Demand

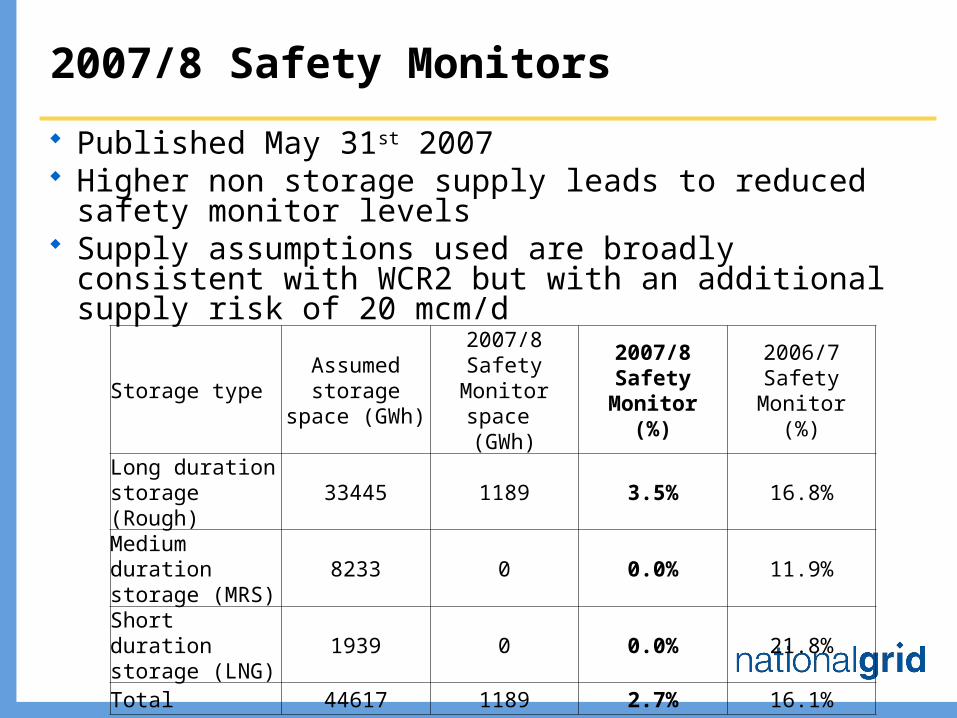

2007/8 Safety Monitors

Published May 31st 2007 Higher non storage supply leads to reduced safety monitor

levels Supply assumptions used are broadly consistent with

WCR2 but with an additional supply risk of 20 mcm/d

Storage typeAssumed

storage space (GWh)

2007/8 Safety Monitor space

(GWh)

2007/8 Safety Monitor

(%)

2006/7 Safety Monitor

(%)

Long duration storage (Rough)

33445 1189 3.5% 16.8%

Medium duration storage (MRS)

8233 0 0.0% 11.9%

Short duration storage (LNG)

1939 0 0.0% 21.8%

Total 44617 1189 2.7% 16.1%