Embed Size (px)

Citation preview

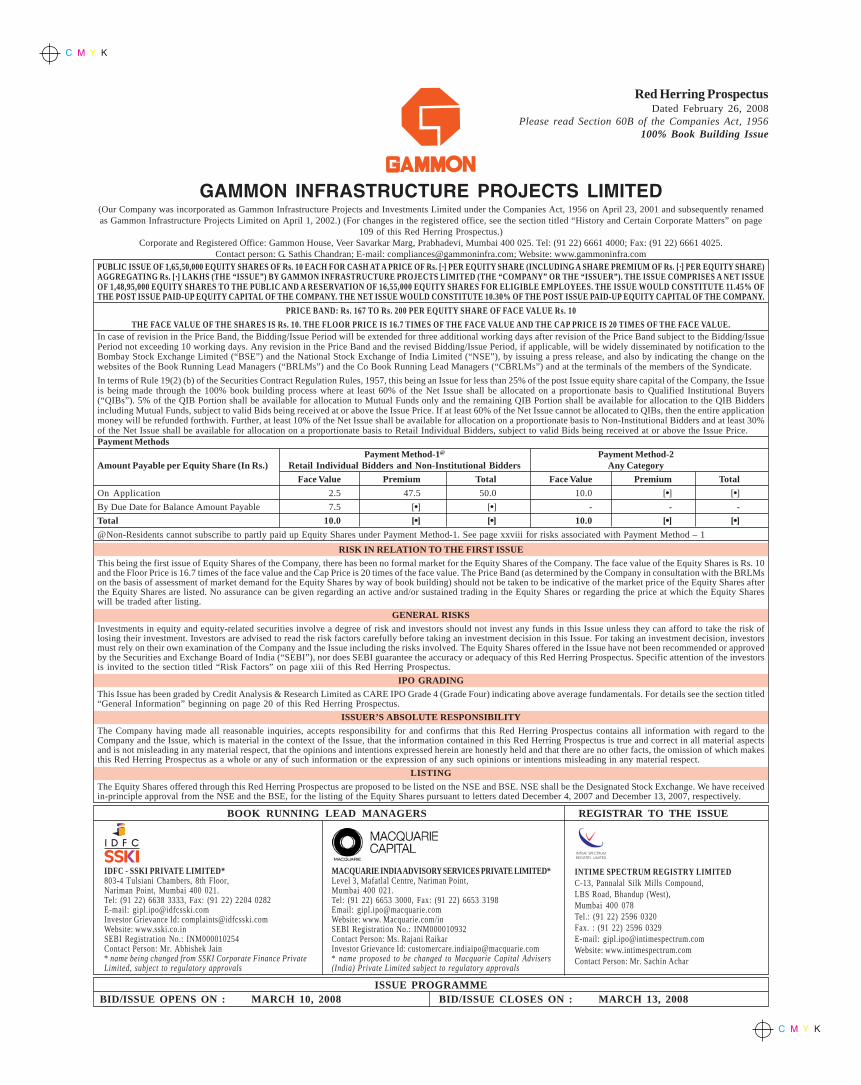

Red Herring ProspectusDated February 26, 2008

Please read Section 60B of the Companies Act, 1956100% Book Building Issue

GAMMON INFRASTRUCTURE PROJECTS LIMITED(Our Company was incorporated as Gammon Infrastructure Projects and Investments Limited under the Companies Act, 1956 on April 23, 2001 and subsequently renamedas Gammon Infrastructure Projects Limited on April 1, 2002.) (For changes in the registered office, see the section titled “History and Certain Corporate Matters” on page

109 of this Red Herring Prospectus.)Corporate and Registered Office: Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025. Tel: (91 22) 6661 4000; Fax: (91 22) 6661 4025.

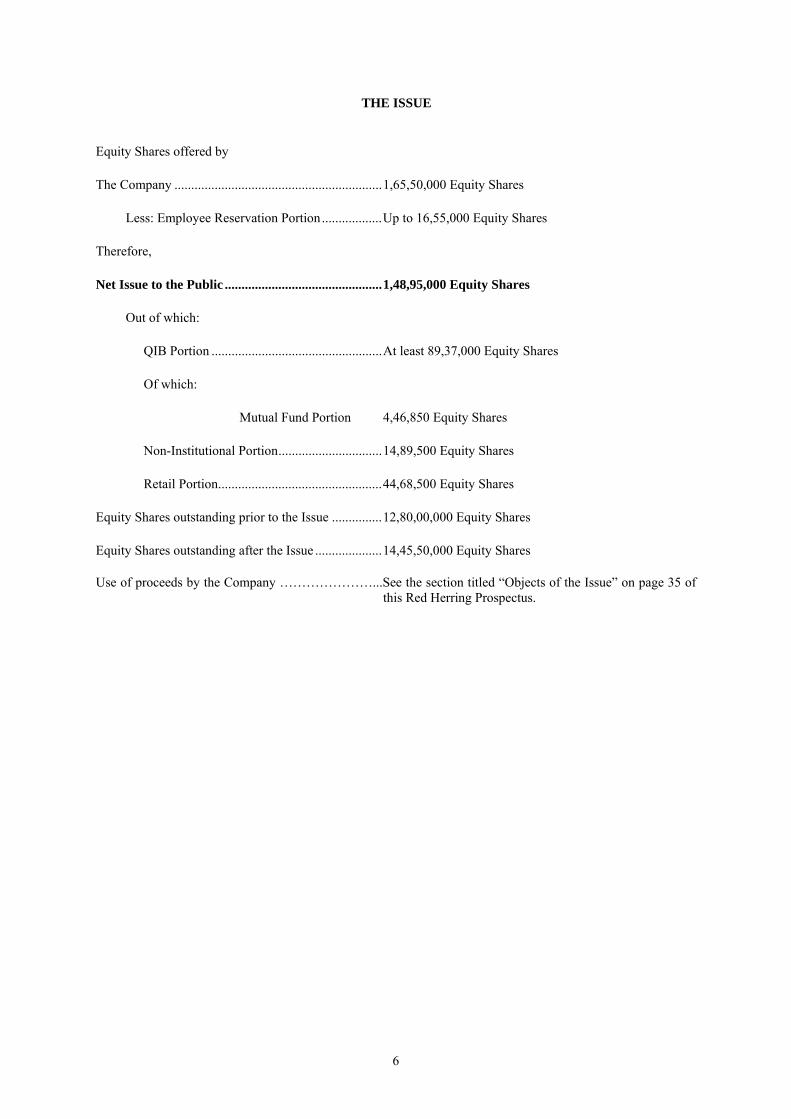

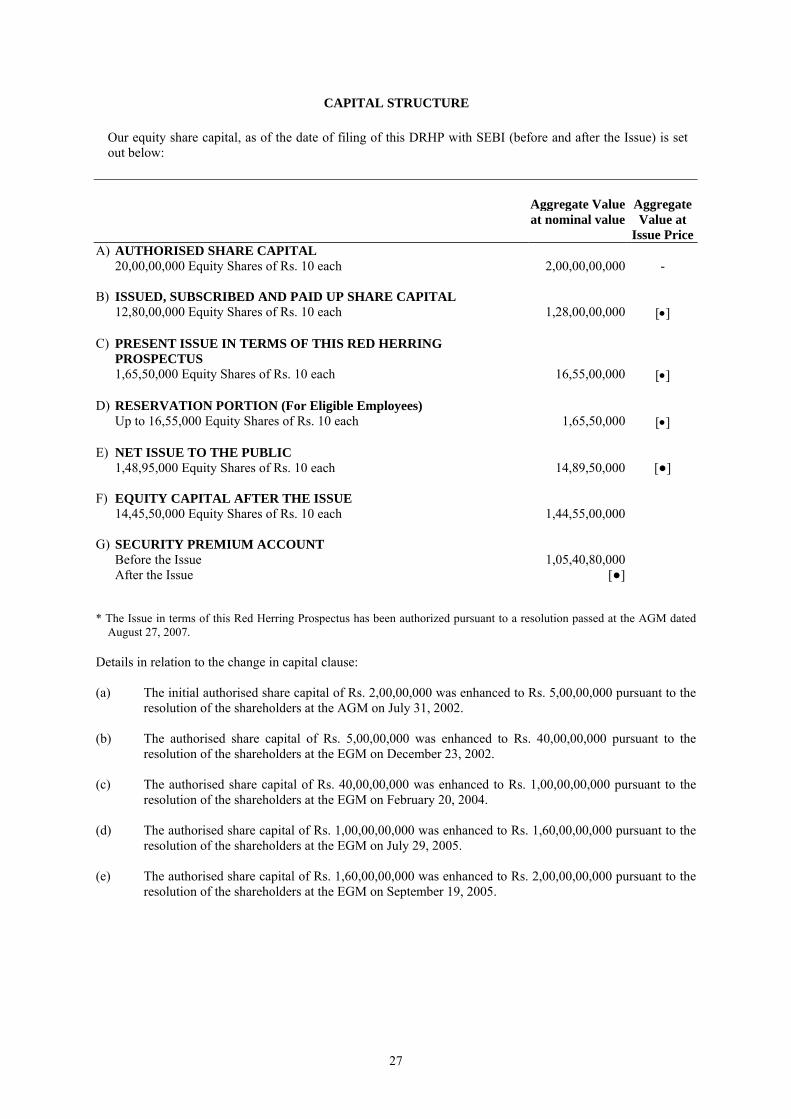

Contact person: G. Sathis Chandran; E-mail: [email protected]; Website: www.gammoninfra.comPUBLIC ISSUE OF 1,65,50,000 EQUITY SHARES OF Rs. 10 EACH FOR CASH AT A PRICE OF Rs. [·] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF Rs. [·] PER EQUITY SHARE)AGGREGATING Rs. [·] LAKHS (THE “ISSUE”) BY GAMMON INFRASTRUCTURE PROJECTS LIMITED (THE “COMPANY” OR THE “ISSUER”). THE ISSUE COMPRISES A NET ISSUEOF 1,48,95,000 EQUITY SHARES TO THE PUBLIC AND A RESERVATION OF 16,55,000 EQUITY SHARES FOR ELIGIBLE EMPLOYEES. THE ISSUE WOULD CONSTITUTE 11.45% OFTHE POST ISSUE PAID-UP EQUITY CAPITAL OF THE COMPANY. THE NET ISSUE WOULD CONSTITUTE 10.30% OF THE POST ISSUE PAID-UP EQUITY CAPITAL OF THE COMPANY.

PRICE BAND: Rs. 167 TO Rs. 200 PER EQUITY SHARE OF FACE VALUE Rs. 10THE FACE VALUE OF THE SHARES IS Rs. 10. THE FLOOR PRICE IS 16.7 TIMES OF THE FACE VALUE AND THE CAP PRICE IS 20 TIMES OF THE FACE VALUE.

In case of revision in the Price Band, the Bidding/Issue Period will be extended for three additional working days after revision of the Price Band subject to the Bidding/IssuePeriod not exceeding 10 working days. Any revision in the Price Band and the revised Bidding/Issue Period, if applicable, will be widely disseminated by notification to theBombay Stock Exchange Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”), by issuing a press release, and also by indicating the change on thewebsites of the Book Running Lead Managers (“BRLMs”) and the Co Book Running Lead Managers (“CBRLMs”) and at the terminals of the members of the Syndicate.In terms of Rule 19(2) (b) of the Securities Contract Regulation Rules, 1957, this being an Issue for less than 25% of the post Issue equity share capital of the Company, the Issueis being made through the 100% book building process where at least 60% of the Net Issue shall be allocated on a proportionate basis to Qualified Institutional Buyers(“QIBs”). 5% of the QIB Portion shall be available for allocation to Mutual Funds only and the remaining QIB Portion shall be available for allocation to the QIB Biddersincluding Mutual Funds, subject to valid Bids being received at or above the Issue Price. If at least 60% of the Net Issue cannot be allocated to QIBs, then the entire applicationmoney will be refunded forthwith. Further, at least 10% of the Net Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and at least 30%of the Net Issue shall be available for allocation on a proportionate basis to Retail Individual Bidders, subject to valid Bids being received at or above the Issue Price.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

INTIME SPECTRUM REGISTRY LIMITEDC-13, Pannalal Silk Mills Compound,LBS Road, Bhandup (West),Mumbai 400 078Tel.: (91 22) 2596 0320Fax. : (91 22) 2596 0329E-mail: [email protected]: www.intimespectrum.comContact Person: Mr. Sachin Achar

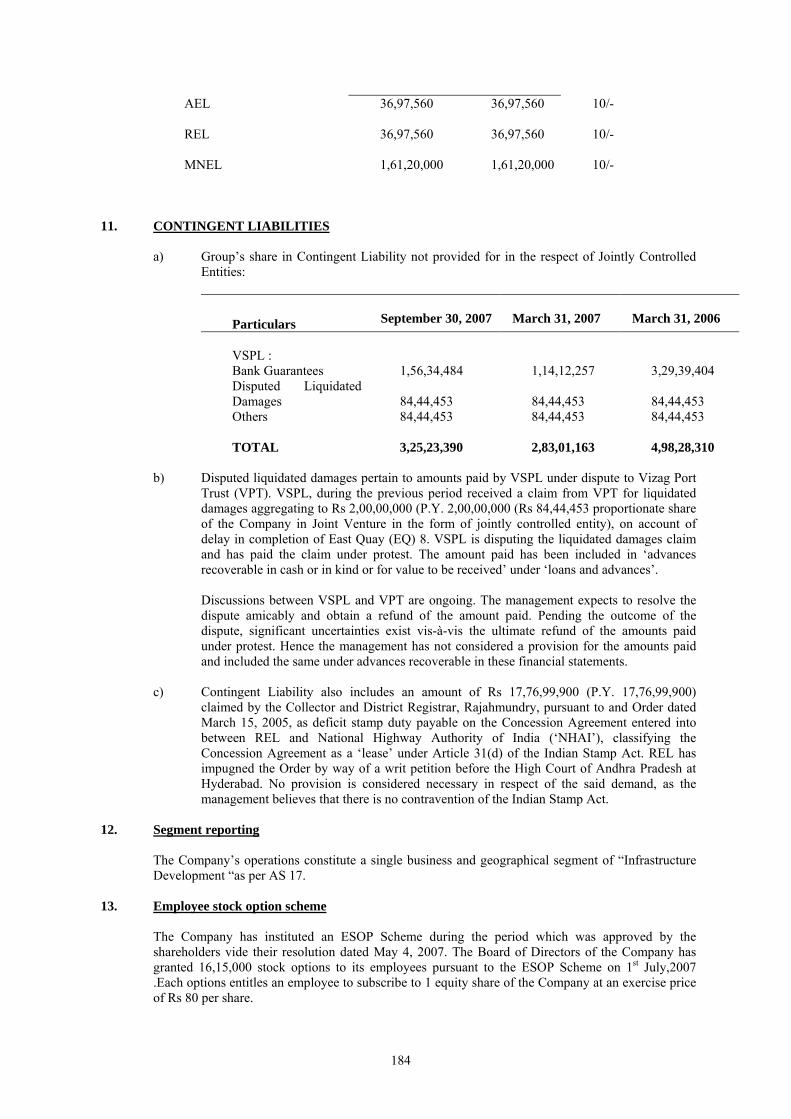

C M Y K

C M Y K

IDFC - SSKI PRIVATE LIMITED*803-4 Tulsiani Chambers, 8th Floor,Nariman Point, Mumbai 400 021.Tel: (91 22) 6638 3333, Fax: (91 22) 2204 0282E-mail: [email protected] Grievance Id: [email protected]: www.sski.co.inSEBI Registration No.: INM000010254Contact Person: Mr. Abhishek Jain* name being changed from SSKI Corporate Finance PrivateLimited, subject to regulatory approvals

MACQUARIE INDIA ADVISORY SERVICES PRIVATE LIMITED*Level 3, Mafatlal Centre, Nariman Point,Mumbai 400 021.Tel: (91 22) 6653 3000, Fax: (91 22) 6653 3198Email: [email protected]: www. Macquarie.com/inSEBI Registration No.: INM000010932Contact Person: Ms. Rajani RaikarInvestor Grievance Id: [email protected]* name proposed to be changed to Macquarie Capital Advisers(India) Private Limited subject to regulatory approvals

ISSUE PROGRAMMEBID/ISSUE OPENS ON : MARCH 10, 2008 BID/ISSUE CLOSES ON : MARCH 13, 2008

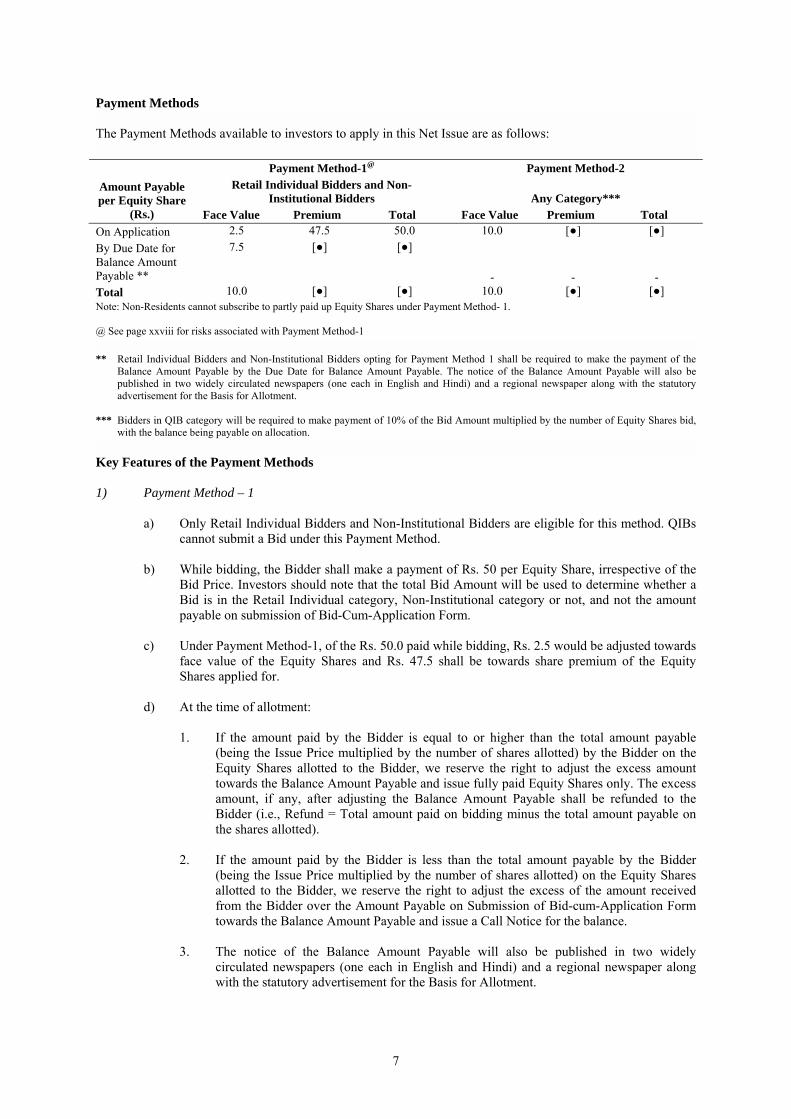

Payment MethodsPayment Method-1@ Payment Method-2

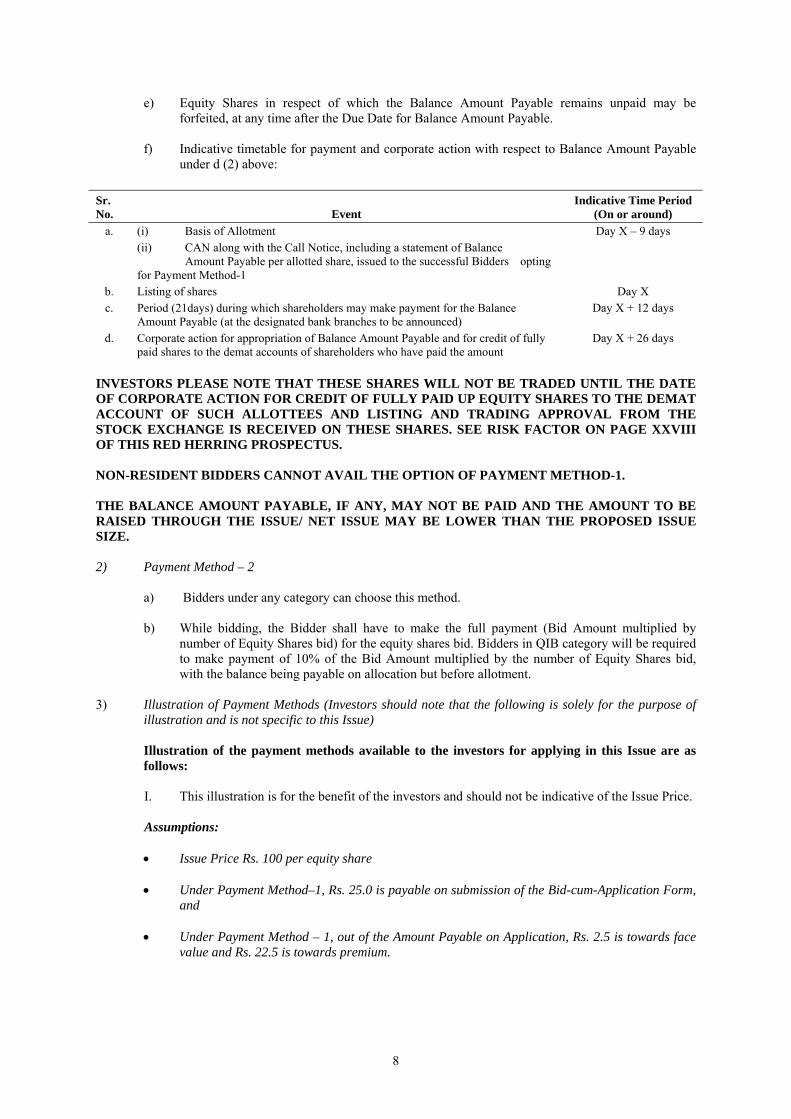

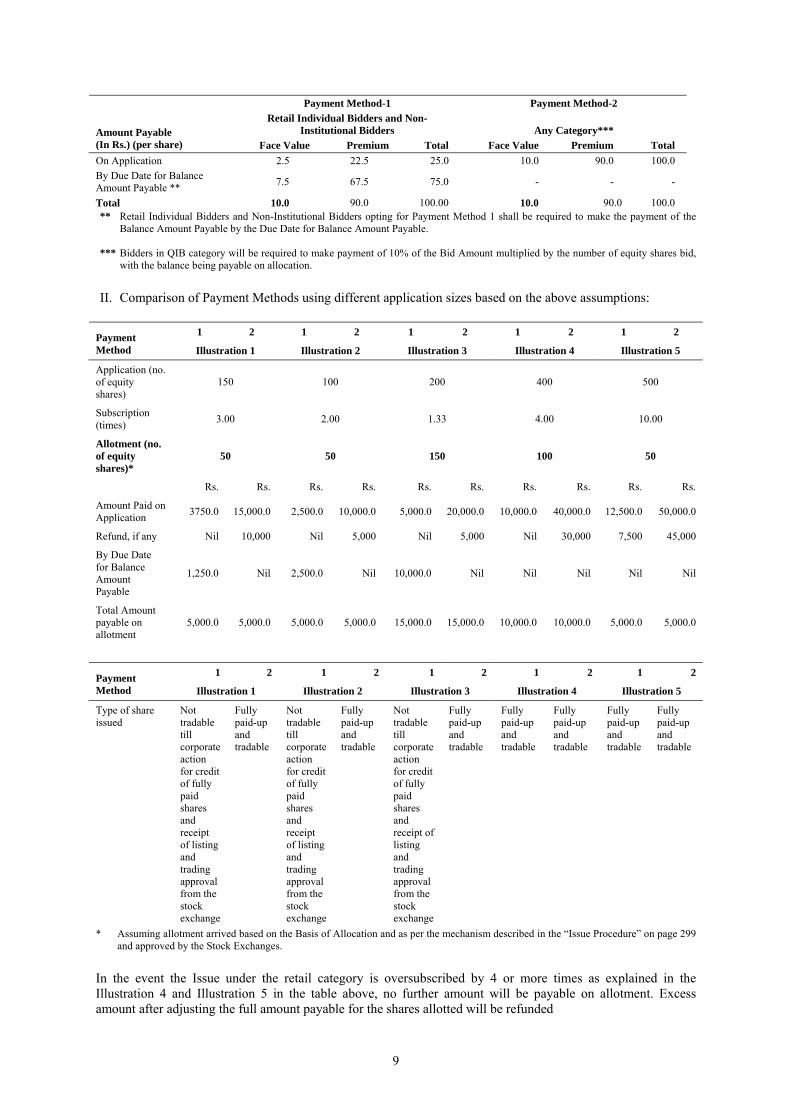

Amount Payable per Equity Share (In Rs.) Retail Individual Bidders and Non-Institutional Bidders Any CategoryFace Value Premium Total Face Value Premium Total

On Application 2.5 47.5 50.0 10.0 [•] [•]By Due Date for Balance Amount Payable 7.5 [•] [•] - - -Total 10.0 [•] [•] 10.0 [•] [•]@Non-Residents cannot subscribe to partly paid up Equity Shares under Payment Method-1. See page xxviii for risks associated with Payment Method – 1

RISK IN RELATION TO THE FIRST ISSUEThis being the first issue of Equity Shares of the Company, there has been no formal market for the Equity Shares of the Company. The face value of the Equity Shares is Rs. 10and the Floor Price is 16.7 times of the face value and the Cap Price is 20 times of the face value. The Price Band (as determined by the Company in consultation with the BRLMson the basis of assessment of market demand for the Equity Shares by way of book building) should not be taken to be indicative of the market price of the Equity Shares afterthe Equity Shares are listed. No assurance can be given regarding an active and/or sustained trading in the Equity Shares or regarding the price at which the Equity Shareswill be traded after listing.

GENERAL RISKSInvestments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk oflosing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. For taking an investment decision, investorsmust rely on their own examination of the Company and the Issue including the risks involved. The Equity Shares offered in the Issue have not been recommended or approvedby the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of this Red Herring Prospectus. Specific attention of the investorsis invited to the section titled “Risk Factors” on page xiii of this Red Herring Prospectus.

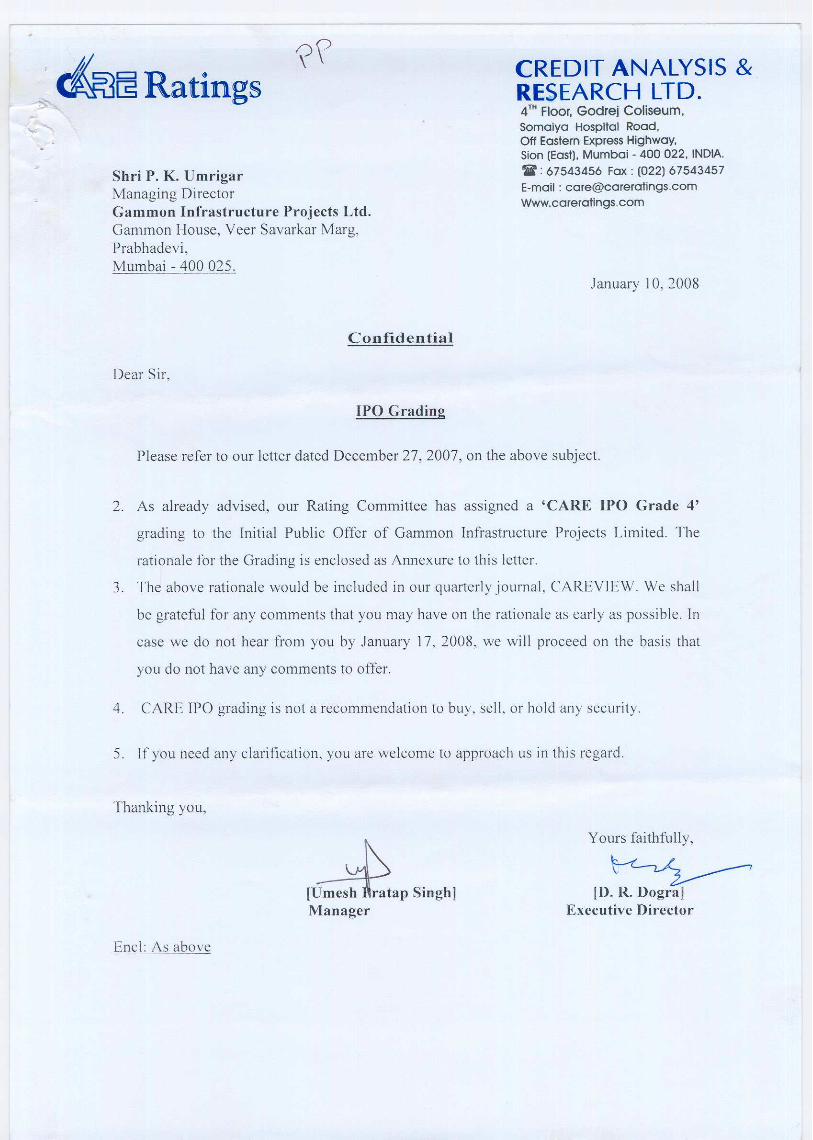

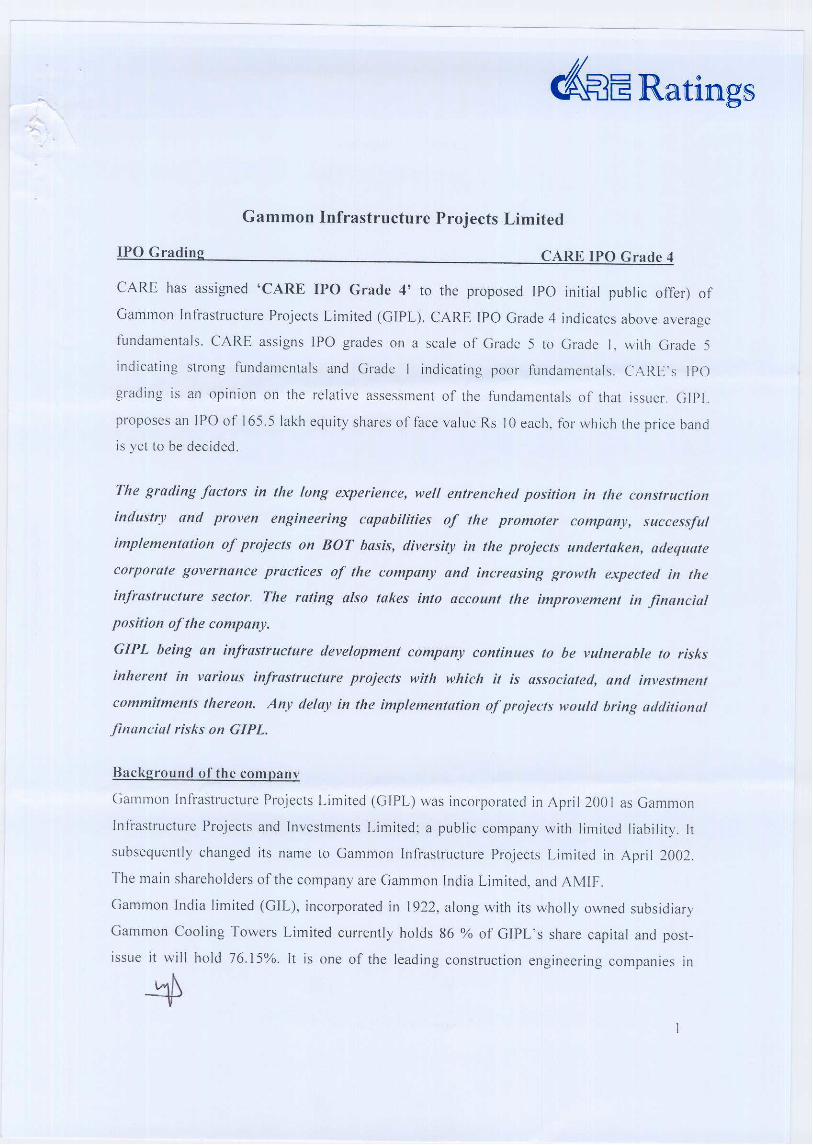

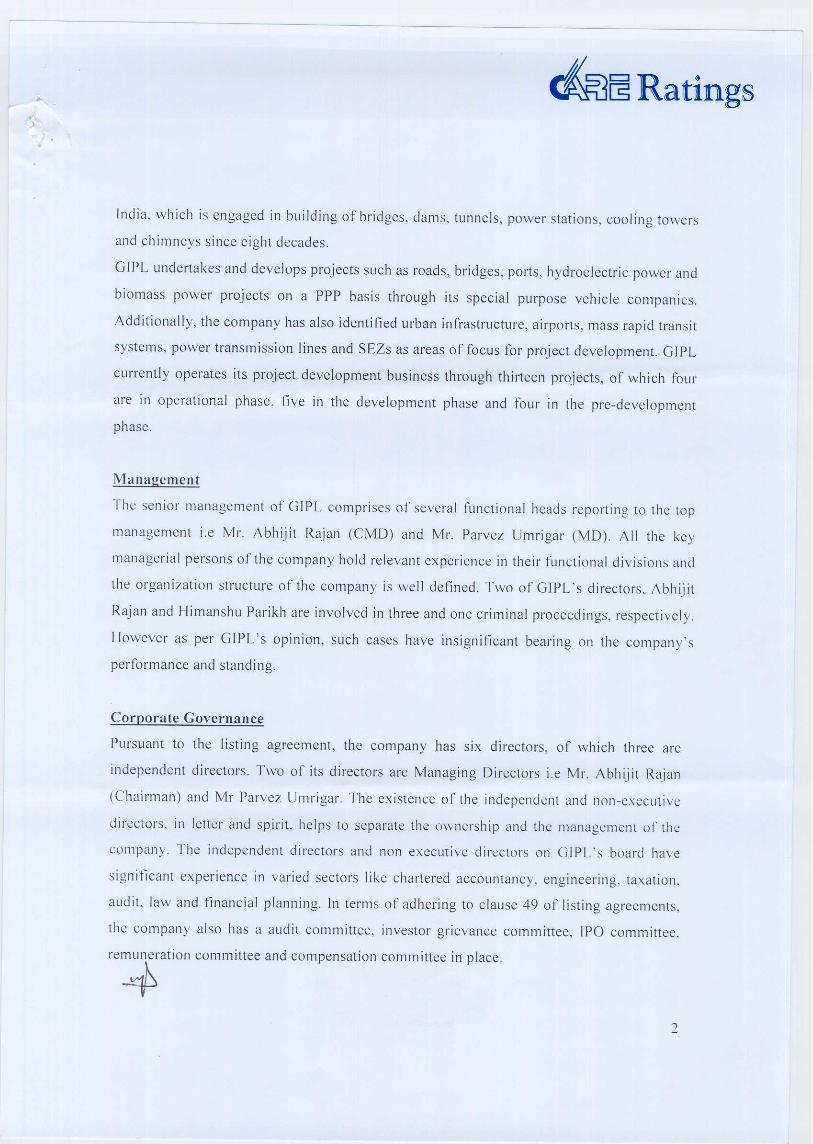

IPO GRADINGThis Issue has been graded by Credit Analysis & Research Limited as CARE IPO Grade 4 (Grade Four) indicating above average fundamentals. For details see the section titled“General Information” beginning on page 20 of this Red Herring Prospectus.

ISSUER’S ABSOLUTE RESPONSIBILITYThe Company having made all reasonable inquiries, accepts responsibility for and confirms that this Red Herring Prospectus contains all information with regard to theCompany and the Issue, which is material in the context of the Issue, that the information contained in this Red Herring Prospectus is true and correct in all material aspectsand is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makesthis Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

LISTINGThe Equity Shares offered through this Red Herring Prospectus are proposed to be listed on the NSE and BSE. NSE shall be the Designated Stock Exchange. We have receivedin-principle approval from the NSE and the BSE, for the listing of the Equity Shares pursuant to letters dated December 4, 2007 and December 13, 2007, respectively.

TABLE OF CONTENTS

SECTION I – GENERAL ......................................................................................................................................................................... i i i

DEFINITIONS AND ABBREVIATIONS ................................................................................................................................................ iii

CERTAIN CONVENTIONS; USE OF MARKET DATA ....................................................................................................................... xi

FORWARD-LOOKING STATEMENTS .................................................................................................................................................. xii

SECTION II – RISK FACTORS ............................................................................................................................................................. xiii

SECTION III – INTRODUCTION ......................................................................................................................................................... 1

SUMMARY ................................................................................................................................................................................................ 1

THE ISSUE ................................................................................................................................................................................................. 6

SELECTED FINANCIAL INFORMATION ........................................................................................................................................... 11

GENERAL INFORMATION .................................................................................................................................................................... 20

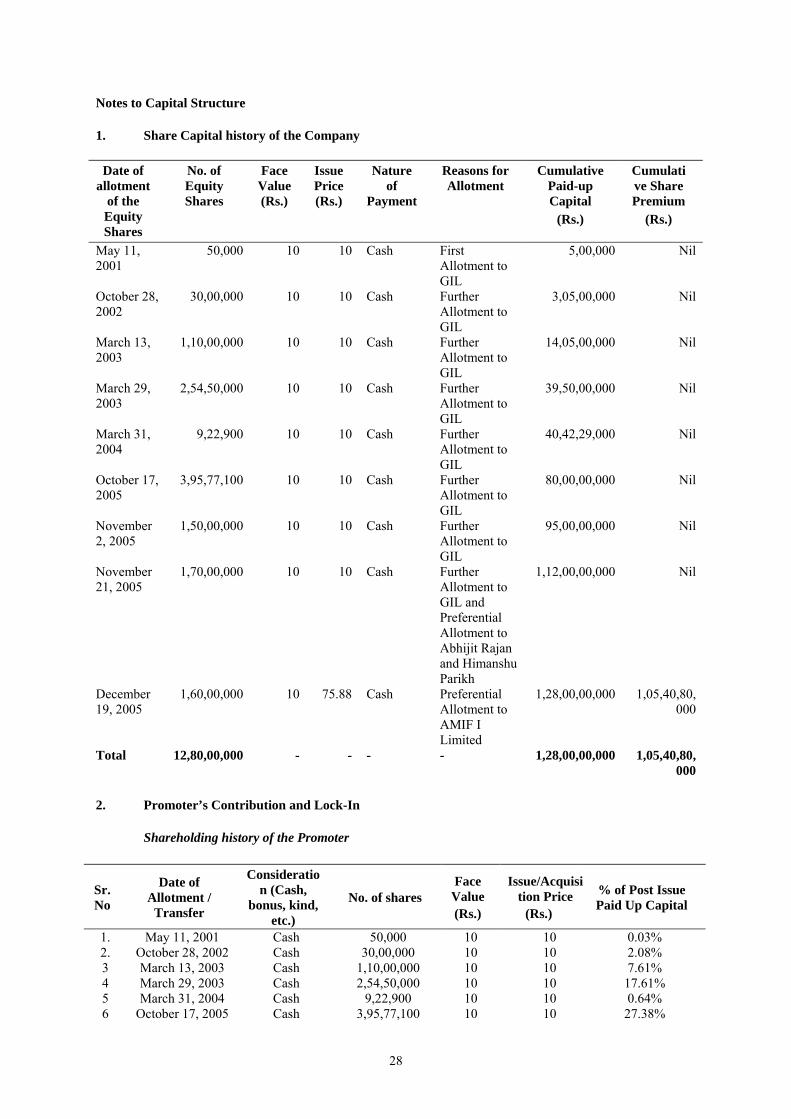

CAPITAL STRUCTURE ........................................................................................................................................................................... 27

OBJECTS OF THE ISSUE ........................................................................................................................................................................ 35

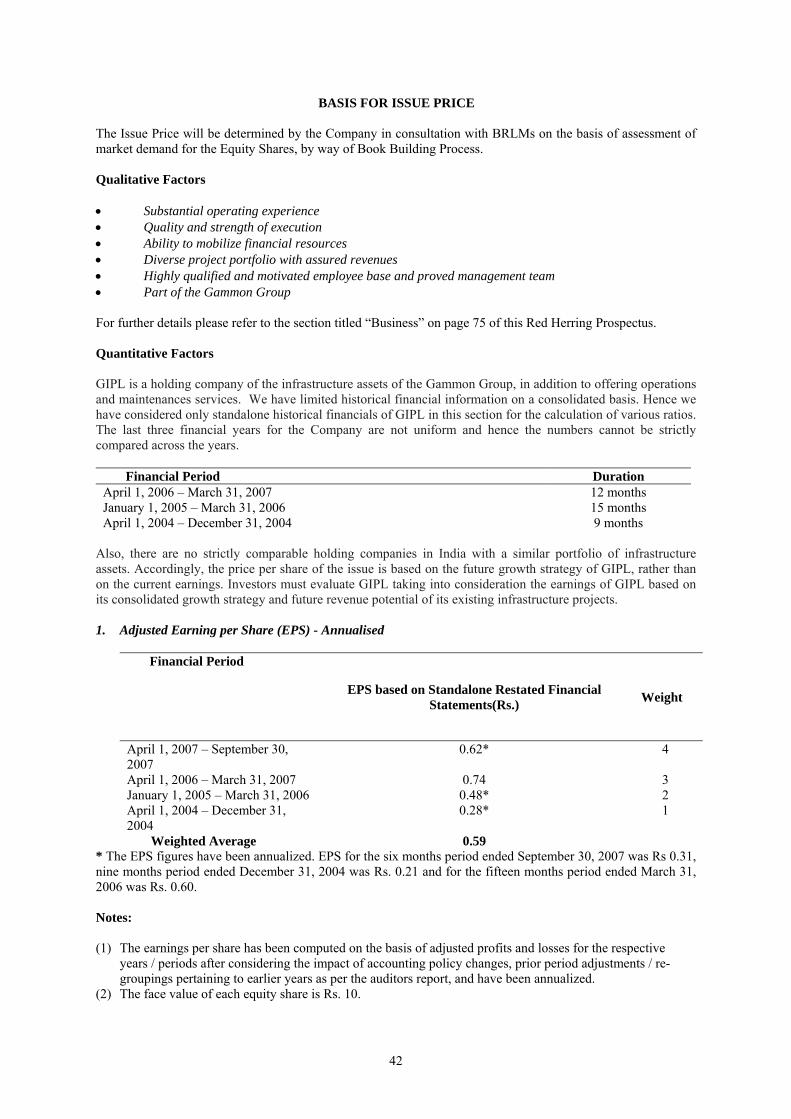

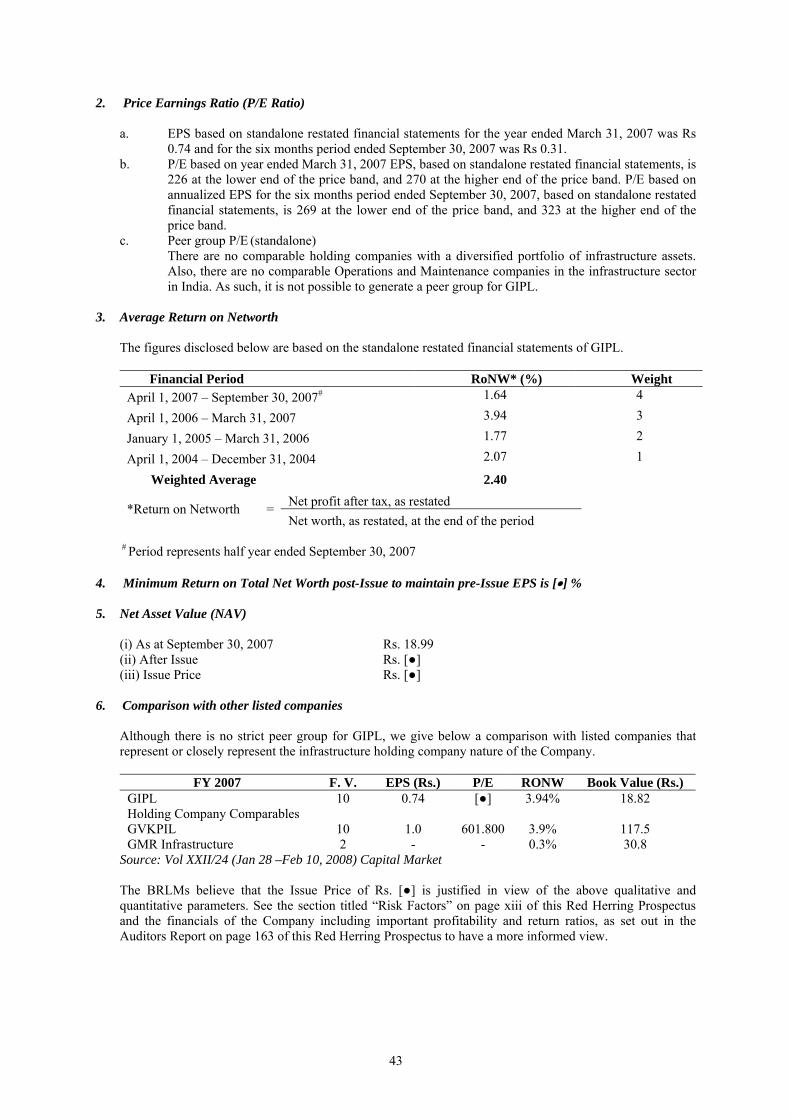

BASIS FOR ISSUE PRICE ........................................................................................................................................................................ 42

STATEMENT OF GENERAL TAX BENEFITS ..................................................................................................................................... 44

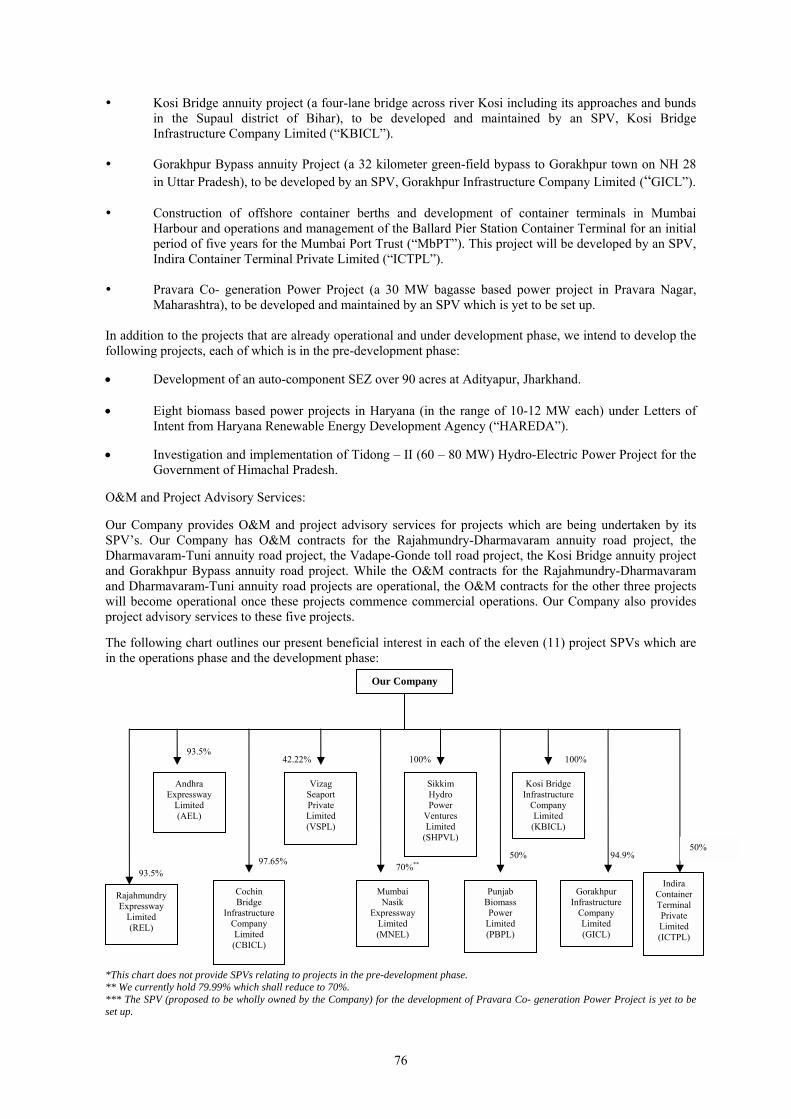

SECTION IV – ABOUT US ..................................................................................................................................................................... 52

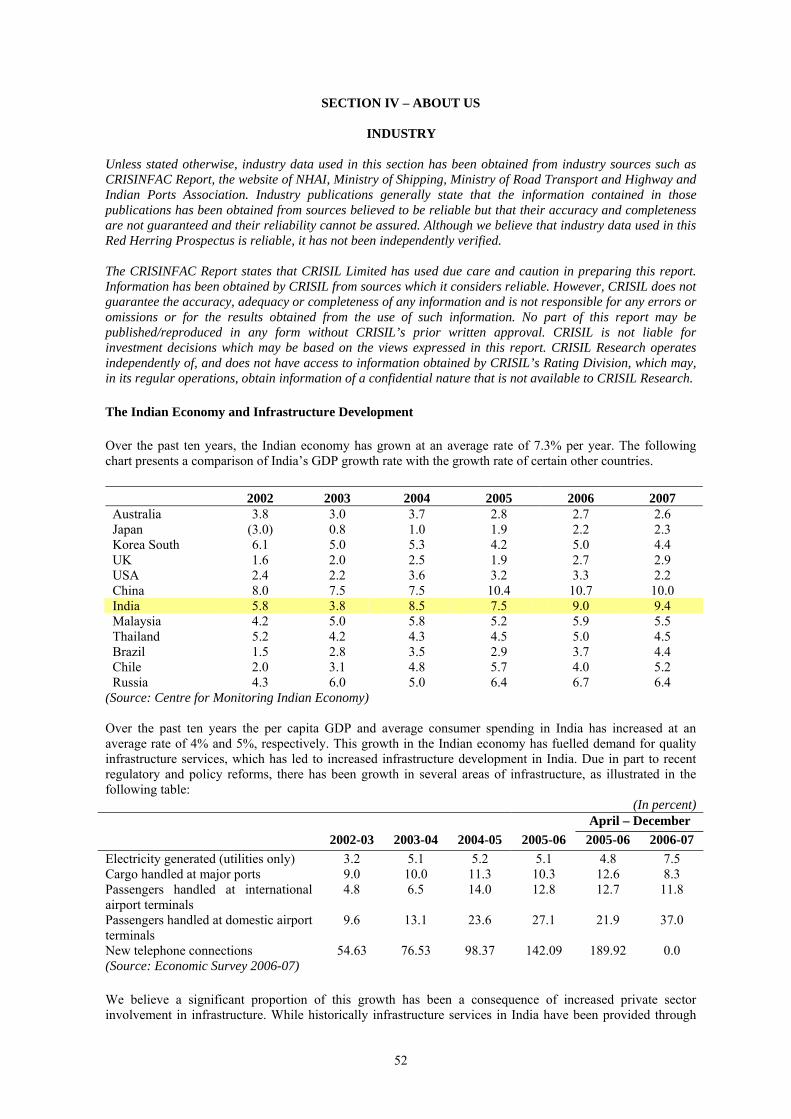

INDUSTRY ................................................................................................................................................................................................. 52

BUSINESS .................................................................................................................................................................................................. 75

REGULATIONS AND POLICIES ............................................................................................................................................................ 103

HISTORY AND CERTAIN CORPORATE MATTERS .......................................................................................................................... 109

OUR SUBSIDIARIES AND ASSOCIATES .............................................................................................................................................. 121

OUR MANAGEMENT ............................................................................................................................................................................. 138

OUR PROMOTERS .................................................................................................................................................................................. 147

RELATED PARTY TRANSACTIONS ..................................................................................................................................................... 159

DIVIDEND POLICY .................................................................................................................................................................................. 162

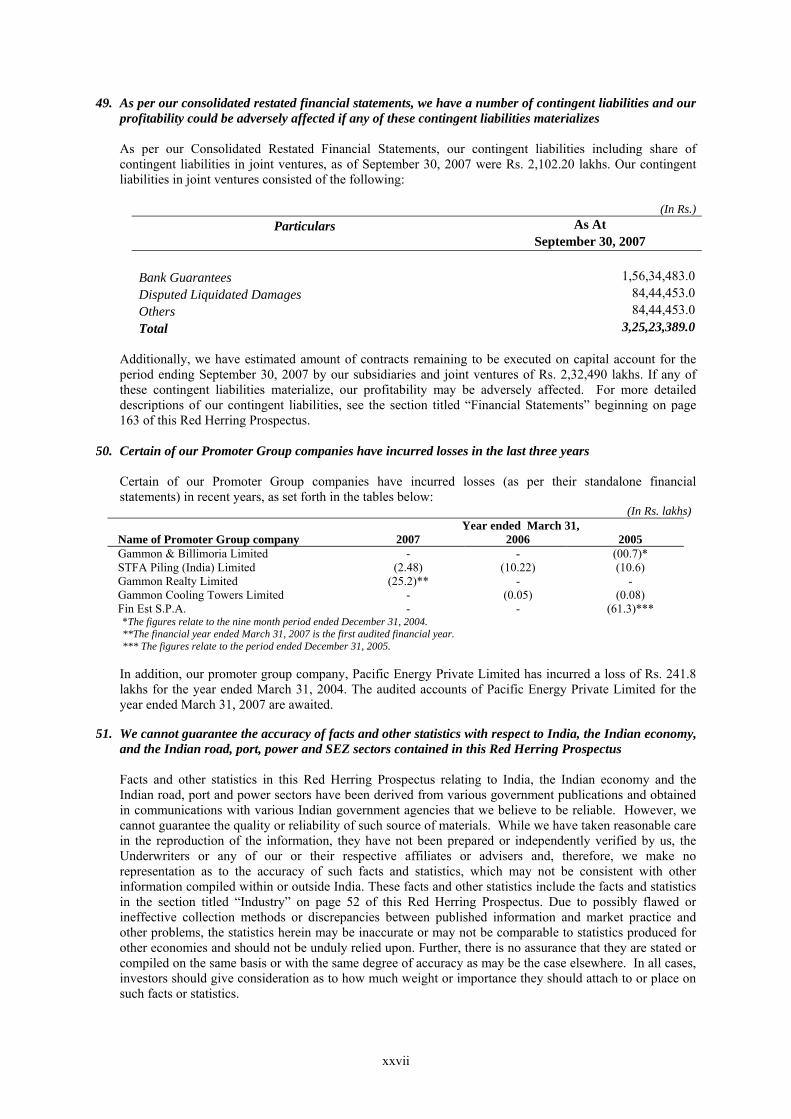

SECTION V – FINANCIAL INFORMATION ....................................................................................................................................... 163

FINANCIAL STATEMENTS ................................................................................................................................................................... 163

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS .......... 245

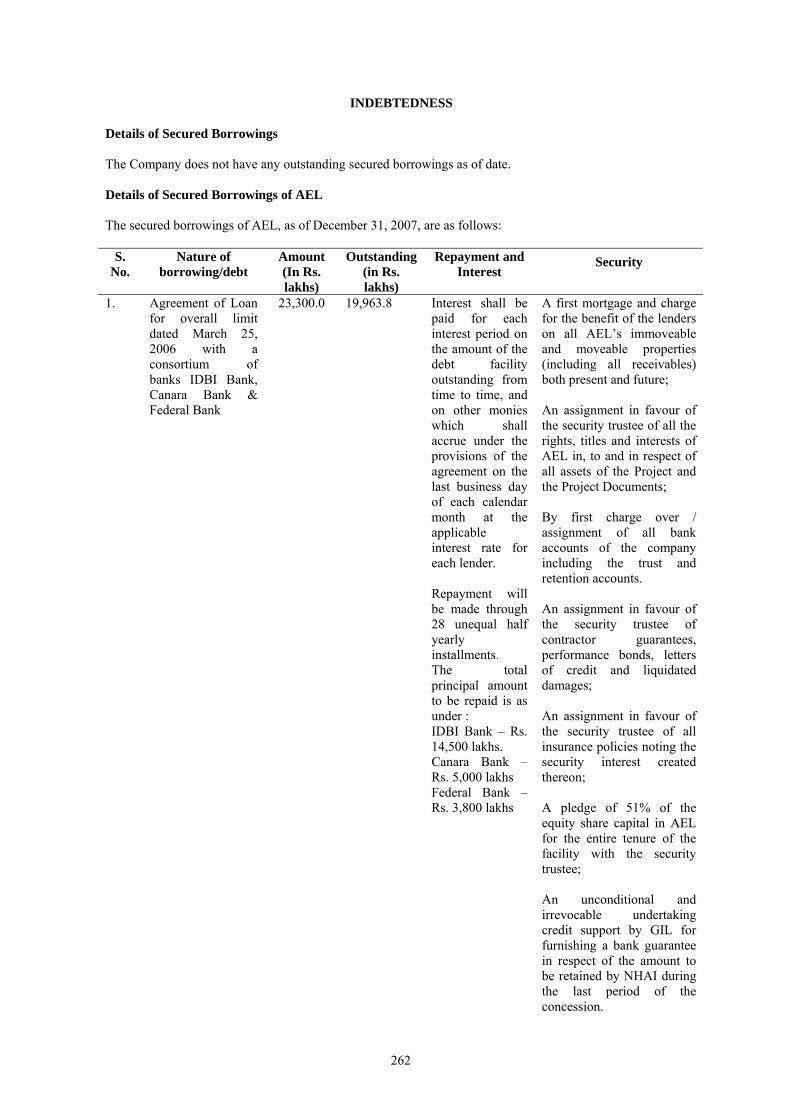

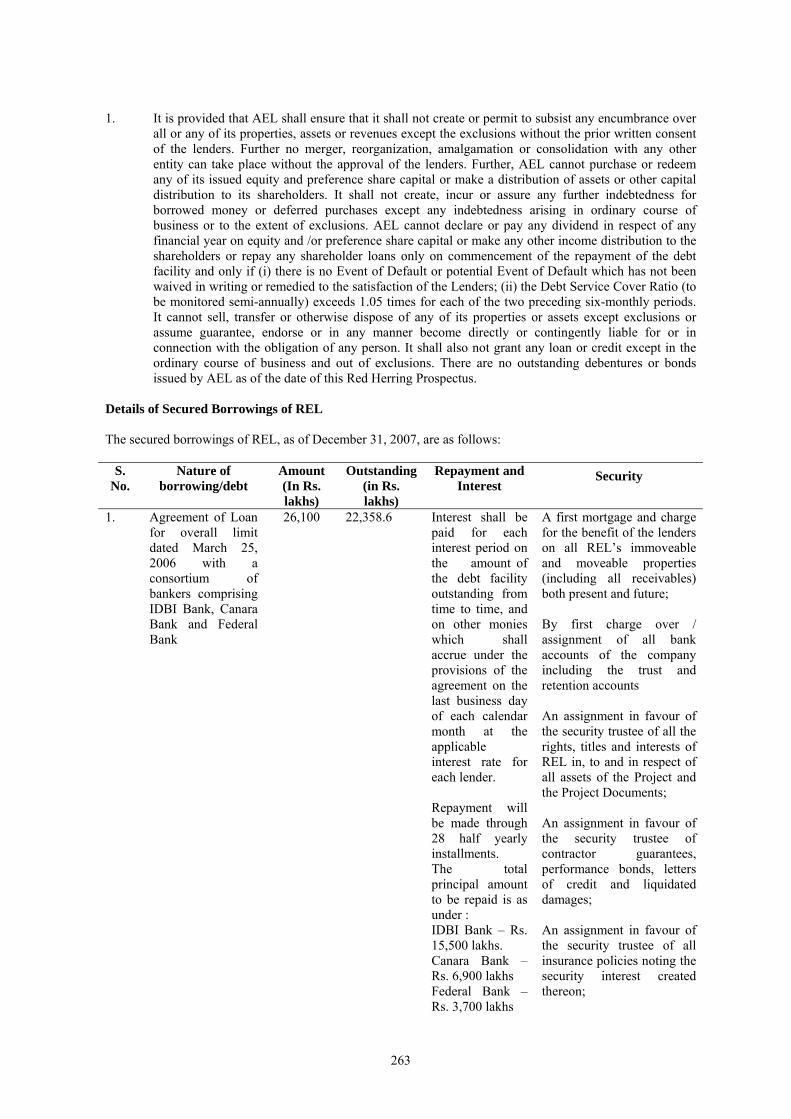

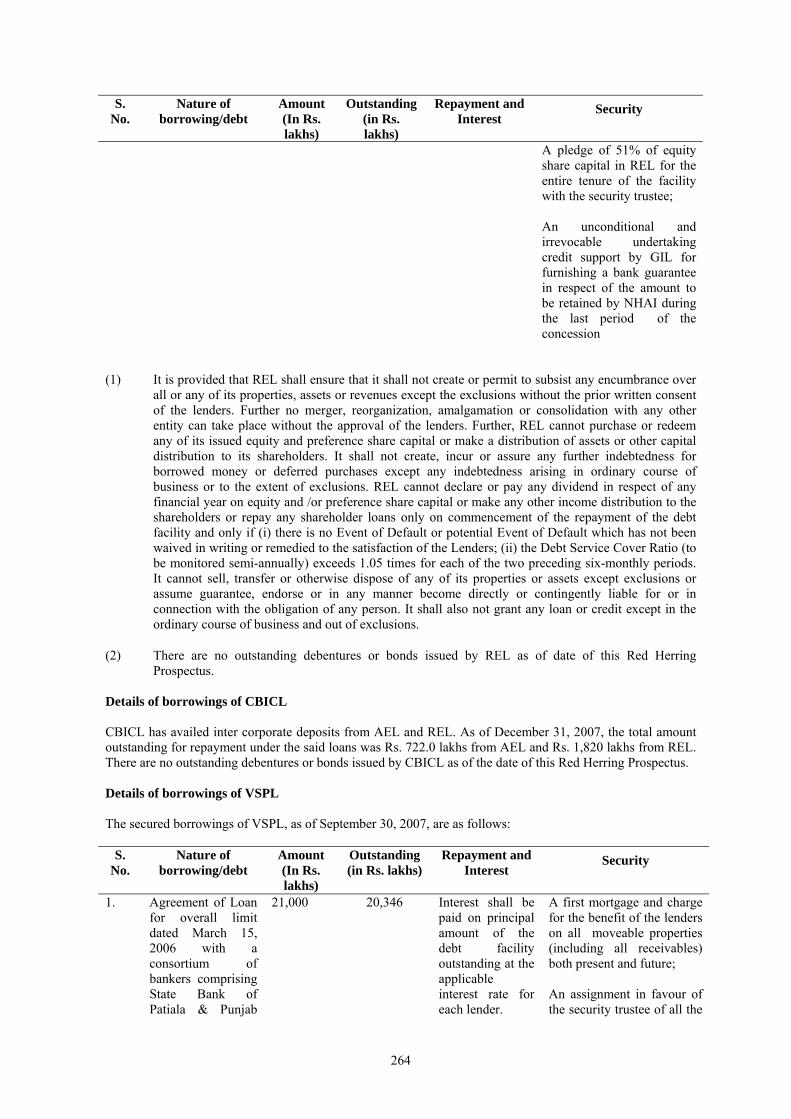

INDEBTEDNESS ....................................................................................................................................................................................... 262

SECTION VI – LEGAL AND REGULATORY INFORMATION ......................................................................................................... 271

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS ............................................................................................. 271

LICENSES AND APPROVALS ................................................................................................................................................................. 276

OTHER REGULATORY AND STATUTORY DISCLOSURES ............................................................................................................. 285

SECTION VII – ISSUE RELATED INFORMATION ........................................................................................................................... 293

TERMS OF THE ISSUE ............................................................................................................................................................................ 293

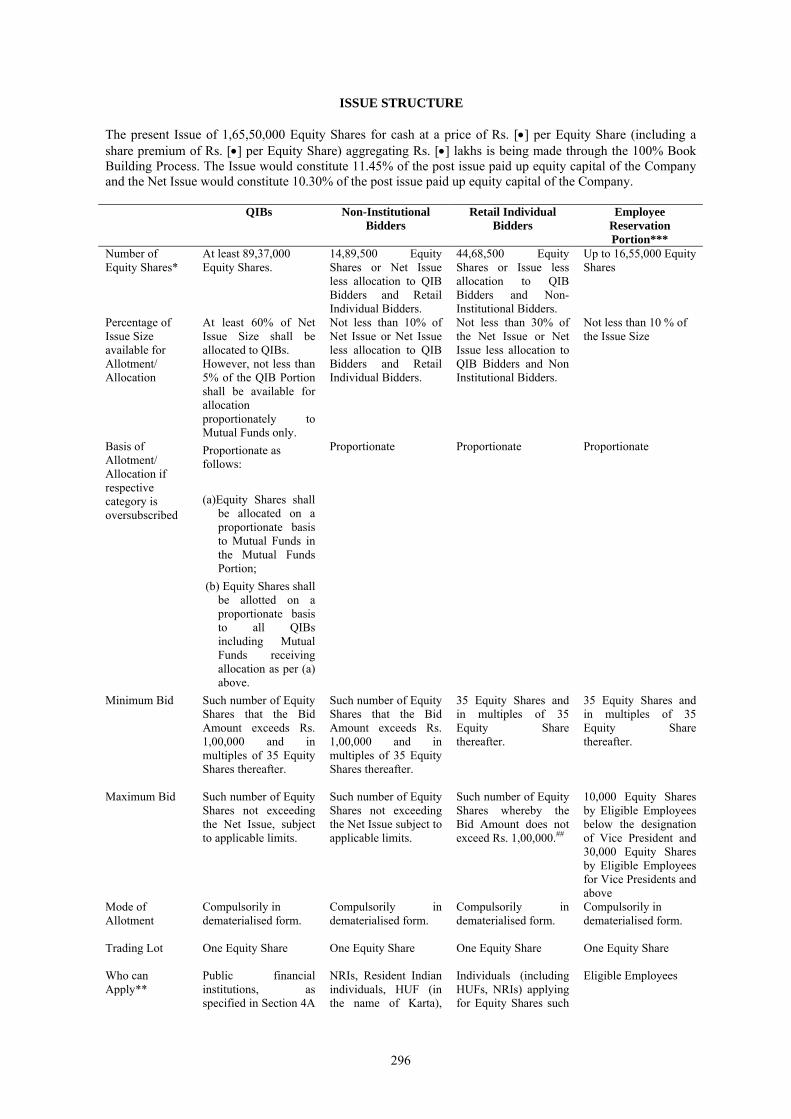

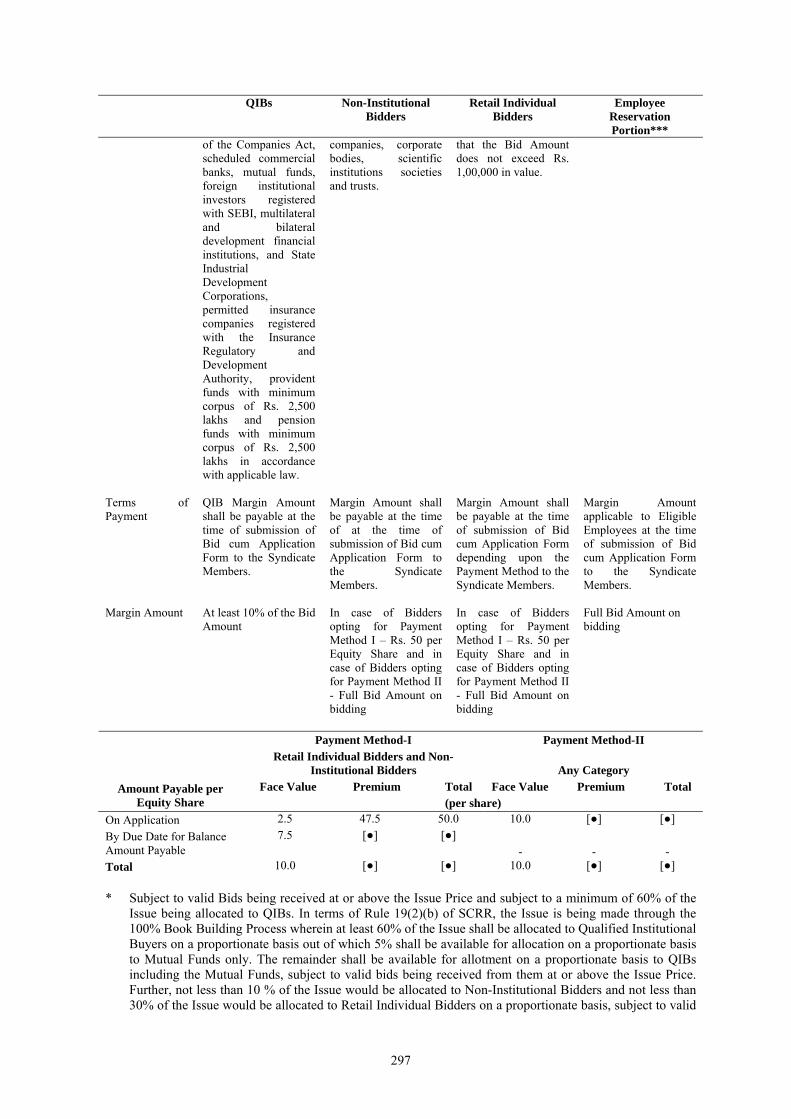

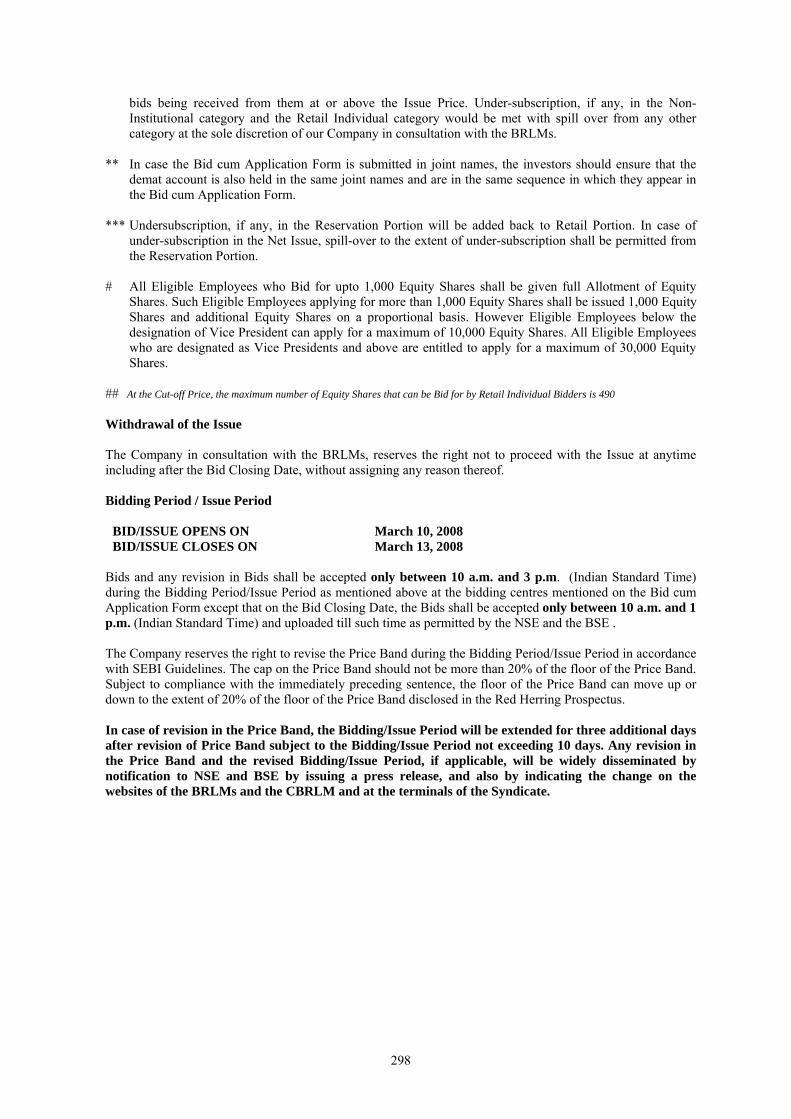

ISSUE STRUCTURE ................................................................................................................................................................................. 296

ISSUE PROCEDURE ................................................................................................................................................................................. 299

RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES ........................................................................................ 327

SECTION VIII – MAIN PROVISIONS OF THE ARTICLES OF ASSOCIATION ........................................................................ 329

SECTION IX – OTHER INFORMATION ............................................................................................................................................. 367

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ............................................................................................... 367

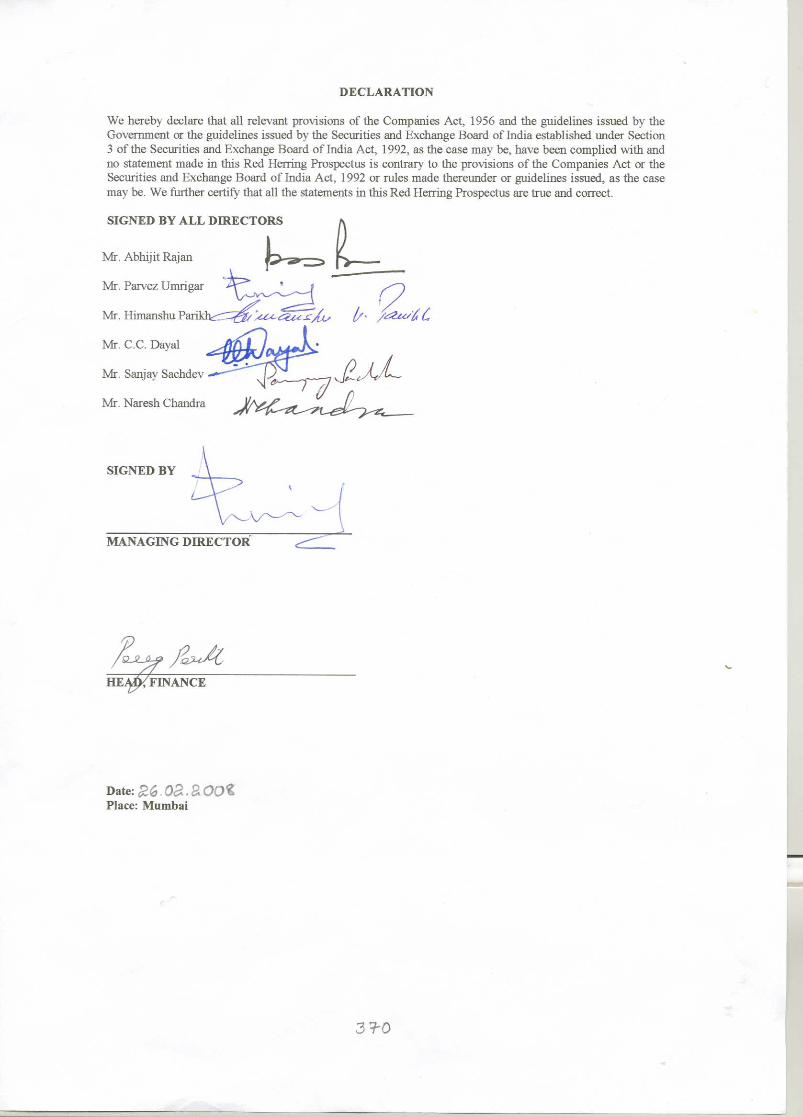

DECLARATION ........................................................................................................................................................................................ 370

ANNEXURE ...............................................................................................................................................................................................

iii

SECTION I – GENERAL

DEFINITIONS AND ABBREVIATIONS

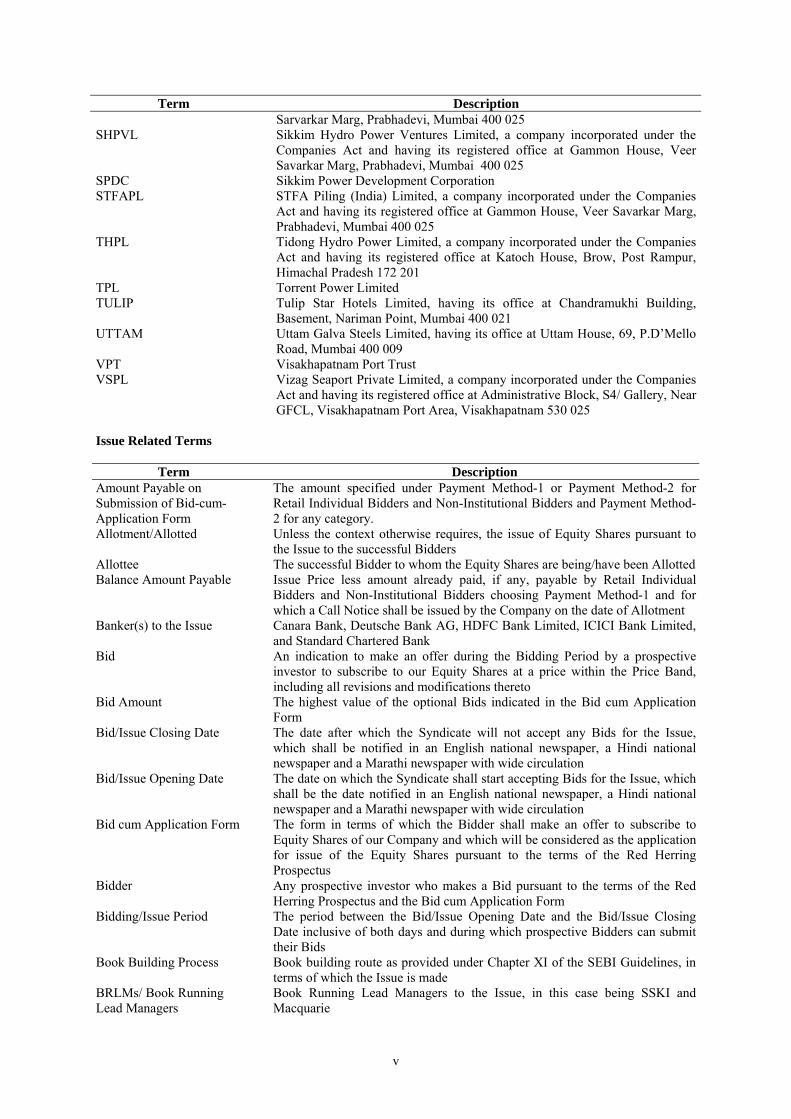

Term Description The �Company� or �our Company� or �GIPL� or �we� or �our� or �us�

Unless the context otherwise requires refers to Gammon Infrastructure Projects Limited on a consolidated basis, a company incorporated under the Companies Act

Company Related Terms

Term Description AEL Andhra Expressway Limited, a company incorporated under the Companies

Act and having its registered office at Alhuwalia Chambers, 16/17 LSC, Madangir, New Delhi 110 062

AIPL ATSL Infrastructure Projects Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025.

ATSL Associated Transrail Structures Limited, a company incorporated under the Companies Act and having its registered office at Neptune House, 7th Floor, Productivity Road, Alkapuri, Baroda 390 007.

Articles/ Articles of Association

The Articles of Association of the Company

Auditors The joint statutory auditors of the Company are Natvarlal Vepari & Co., Chartered Accountants and S. R. Batliboi & Associates, Chartered Accountants

BEB B. E. Billimoria & Company Limited, Shiv Sagar Estate, �A� Block, 2nd Floor, Dr. Annie Besant Road, Worli, Mumbai 400 018

Bermaco Bermaco Energy Systems Limited Board of Directors/ Board The board of directors of our Company or a committee constituted thereof CBICL Cochin Bridge Infrastructure Company Limited, a company incorporated

under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

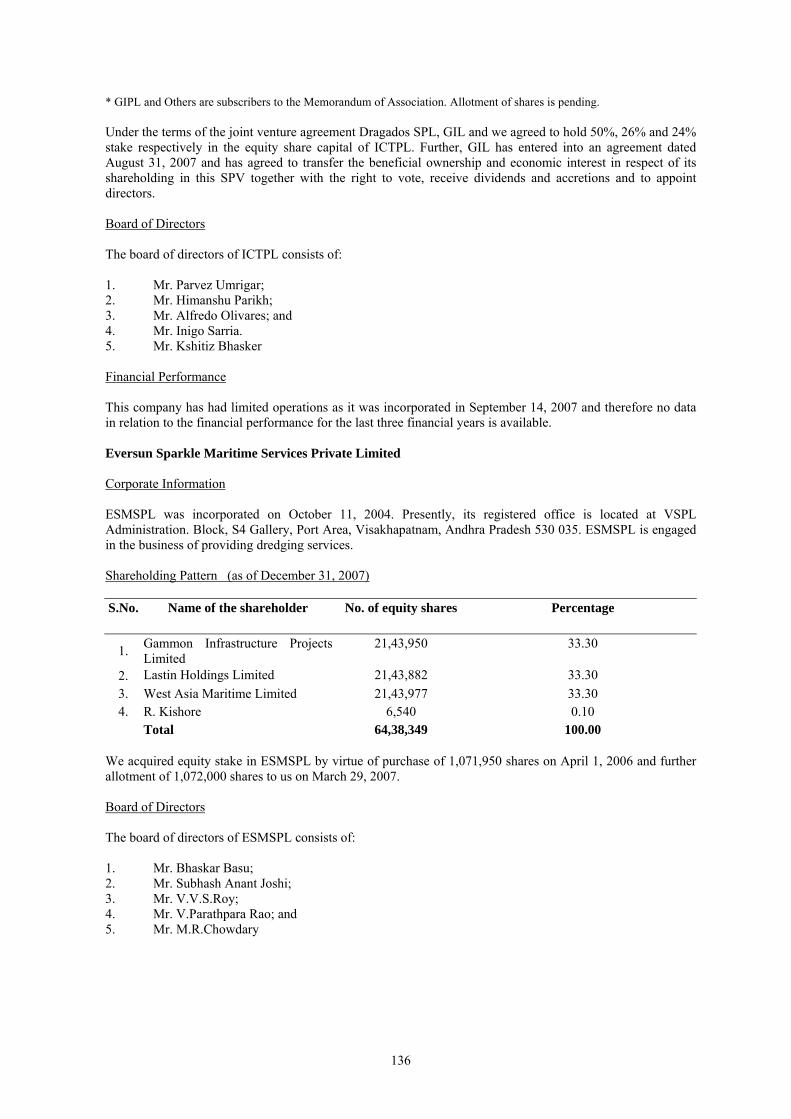

Director(s) Director(s) of our Company, unless otherwise specified ESMSPL Eversun Sparkle Maritime Services Private Limited, a company incorporated

under the Companies Act and having its registered office at S 4, Gallery Near GFCL, Visakhapatnam Port Area, Visakhapatnam 530 035

ESOPS Employees Stock Option Scheme as approved by the shareholders in the meeting dated May 4, 2007

Equity Shares Equity shares of the Company of face value Rs. 10 each Gammon Group GIL, GIPL Group and other companies forming part of the Promoter Group

Companies GBL Gammon & Billimoria Limited, a company incorporated under the Companies

Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

GCTL Gammon Cooling Towers Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

GICL Gorakhpur Infrastructure Company Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

GIL Gammon India Limited, a company incorporated under the Companies Act, 1913 and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

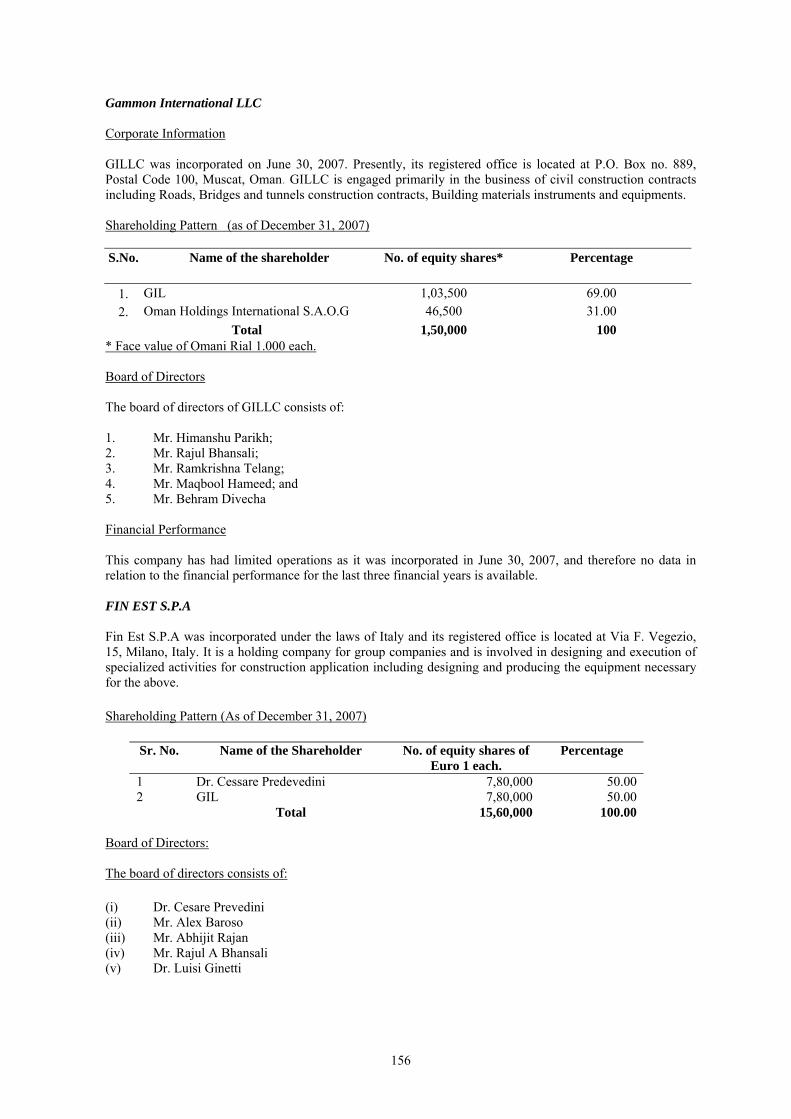

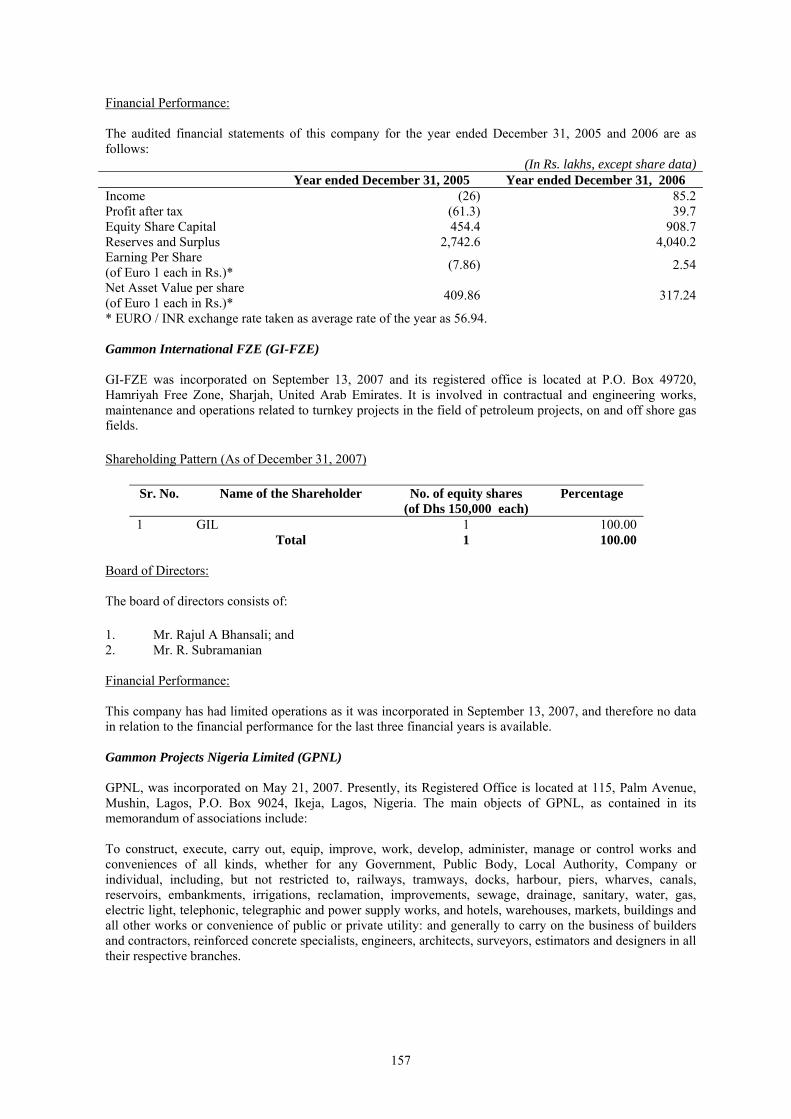

GILLC Gammon International LLC, a company incorporated under the Law of Commercial Companies, Sultanate of Oman and having its office at P. O. Box No. 889, Postal Code 100 Muscat, Oman

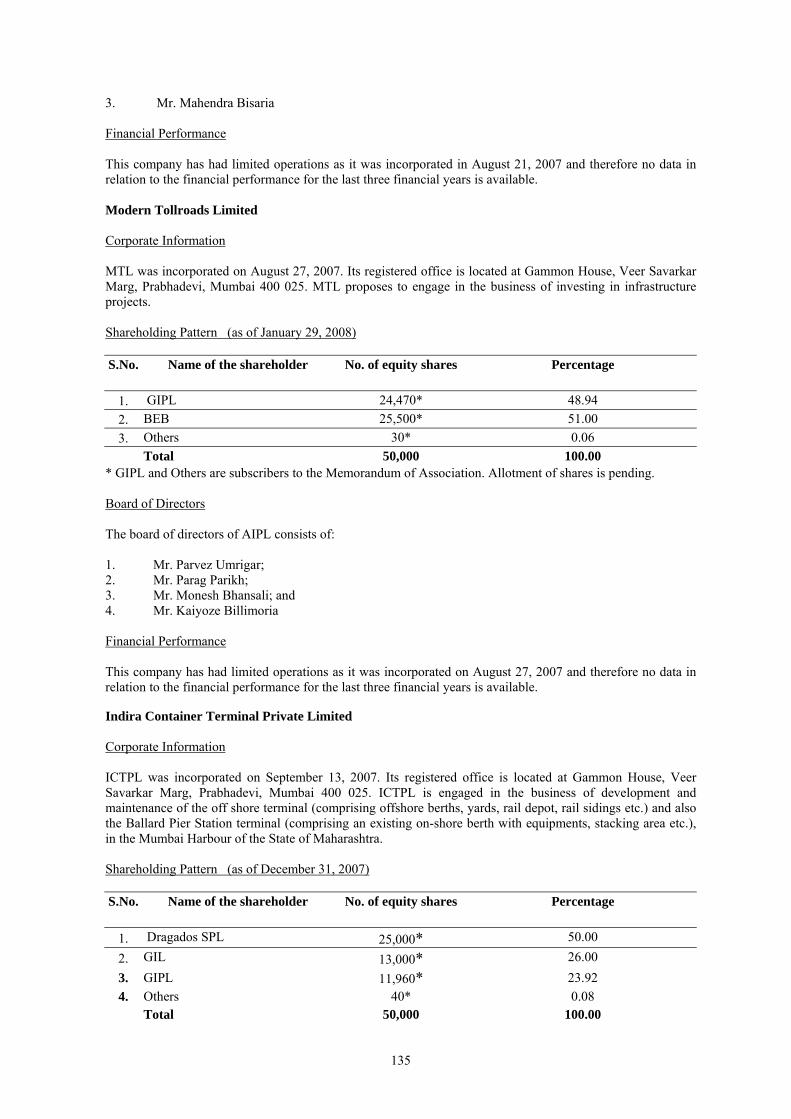

GIPL Group GIPL, AEL, AIPL, CBICL, GICL, GLIML, GPDL, GLL, HBPL, ICTPL, KBICL, MNEL, MPSL, MTL, PBPL, REL, SEZAL, SHPVL, THPL, MTL,

iv

Term Description ESMSPL and VSPL

GLIML Gammon-L&T Infra MRTS Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

GLL Gammon Logistics Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

GPDL Gammon Projects Developers Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

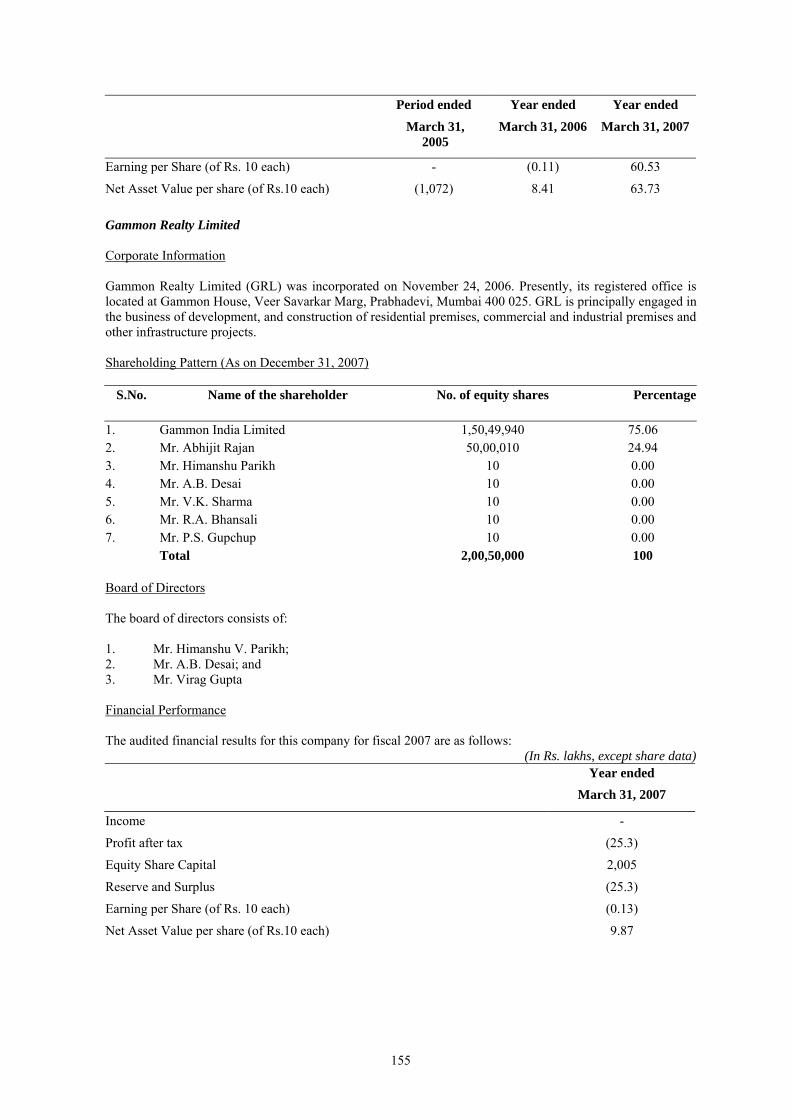

GRL Gammon Realty Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

GQ Golden Quadrilateral HBPL Haryana Biomass Power Limited, a company incorporated under the

Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

ICTPL Indira Container Terminal Private Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

IPS International Port Services JUSCO Jamshedpur Utilities and Services Company Limited KBICL Kosi Bridge Infrastructure Company Limited, a company incorporated under

the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

Memorandum/ Memorandum of Association

The Memorandum of Association of the Company

MNEL Mumbai Nasik Expressway Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

MPSL Marine Project Services Limited, a company incorporated under the Companies Act and having its registered office is located at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

MTCPL Moreshwar Trading Company Private Limited, having its office at Datta Bhavan, Gokhale Road, Vijay Manjrekar Lane, Dadar (West), Mumbai 400 028

MTL Modern Toll Roads Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

PBPL Punjab Biomass Power Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

PEPL Pacific Energy Private Limited, a company incorporated under the Companies Act and having its registered office at 301, Capri, Greenfields Estate, A.B. Nair Road, Juhu, Mumbai 400 049

PLL Punj Lloyd Limited PMS Portia Management Services Limited, UK REL Rajahmundry Expressway Limited, a company incorporated under the

Companies Act and having its registered office at Alhuwalia Chambers, 16/17 LSC, Madangir, New Delhi 110 062

RINL Rashtriya Ispat Nigam Limited Registered Office The registered office of the Company being Gammon House, Veer Savarkar

Marg, Prabhadevi, Mumbai 400 025 SEZAL SEZ Adityapur Limited a company incorporated under the Companies Act and

having its registered office at Sakchi Boulevard Road, Northern Town, Jamshedpur, Jharkhand 831 001

SGSL Satyagiri Shipping Company Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer

v

Term Description Sarvarkar Marg, Prabhadevi, Mumbai 400 025

SHPVL Sikkim Hydro Power Ventures Limited, a company incorporated under the Companies Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

SPDC Sikkim Power Development Corporation STFAPL STFA Piling (India) Limited, a company incorporated under the Companies

Act and having its registered office at Gammon House, Veer Savarkar Marg, Prabhadevi, Mumbai 400 025

THPL Tidong Hydro Power Limited, a company incorporated under the Companies Act and having its registered office at Katoch House, Brow, Post Rampur, Himachal Pradesh 172 201

TPL Torrent Power Limited TULIP Tulip Star Hotels Limited, having its office at Chandramukhi Building,

Basement, Nariman Point, Mumbai 400 021 UTTAM Uttam Galva Steels Limited, having its office at Uttam House, 69, P.D�Mello

Road, Mumbai 400 009 VPT Visakhapatnam Port Trust VSPL Vizag Seaport Private Limited, a company incorporated under the Companies

Act and having its registered office at Administrative Block, S4/ Gallery, Near GFCL, Visakhapatnam Port Area, Visakhapatnam 530 025

Issue Related Terms

Term Description

Amount Payable on Submission of Bid-cum-Application Form

The amount specified under Payment Method-1 or Payment Method-2 for Retail Individual Bidders and Non-Institutional Bidders and Payment Method-2 for any category.

Allotment/Allotted Unless the context otherwise requires, the issue of Equity Shares pursuant to the Issue to the successful Bidders

Allottee The successful Bidder to whom the Equity Shares are being/have been Allotted Balance Amount Payable Issue Price less amount already paid, if any, payable by Retail Individual

Bidders and Non-Institutional Bidders choosing Payment Method-1 and for which a Call Notice shall be issued by the Company on the date of Allotment

Banker(s) to the Issue Canara Bank, Deutsche Bank AG, HDFC Bank Limited, ICICI Bank Limited, and Standard Chartered Bank

Bid An indication to make an offer during the Bidding Period by a prospective investor to subscribe to our Equity Shares at a price within the Price Band, including all revisions and modifications thereto

Bid Amount The highest value of the optional Bids indicated in the Bid cum Application Form

Bid/Issue Closing Date The date after which the Syndicate will not accept any Bids for the Issue, which shall be notified in an English national newspaper, a Hindi national newspaper and a Marathi newspaper with wide circulation

Bid/Issue Opening Date The date on which the Syndicate shall start accepting Bids for the Issue, which shall be the date notified in an English national newspaper, a Hindi national newspaper and a Marathi newspaper with wide circulation

Bid cum Application Form The form in terms of which the Bidder shall make an offer to subscribe to Equity Shares of our Company and which will be considered as the application for issue of the Equity Shares pursuant to the terms of the Red Herring Prospectus

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring Prospectus and the Bid cum Application Form

Bidding/Issue Period The period between the Bid/Issue Opening Date and the Bid/Issue Closing Date inclusive of both days and during which prospective Bidders can submit their Bids

Book Building Process Book building route as provided under Chapter XI of the SEBI Guidelines, in terms of which the Issue is made

BRLMs/ Book Running Lead Managers

Book Running Lead Managers to the Issue, in this case being SSKI and Macquarie

vi

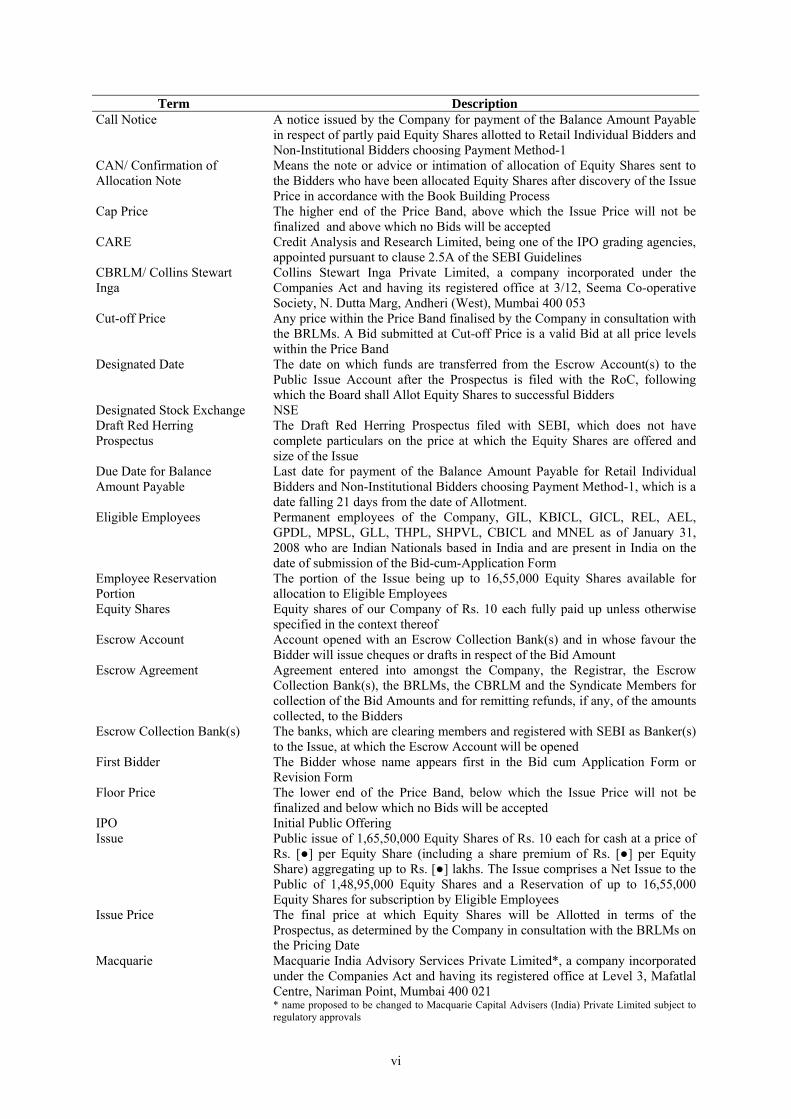

Term Description Call Notice A notice issued by the Company for payment of the Balance Amount Payable

in respect of partly paid Equity Shares allotted to Retail Individual Bidders and Non-Institutional Bidders choosing Payment Method-1

CAN/ Confirmation of Allocation Note

Means the note or advice or intimation of allocation of Equity Shares sent to the Bidders who have been allocated Equity Shares after discovery of the Issue Price in accordance with the Book Building Process

Cap Price The higher end of the Price Band, above which the Issue Price will not be finalized and above which no Bids will be accepted

CARE Credit Analysis and Research Limited, being one of the IPO grading agencies, appointed pursuant to clause 2.5A of the SEBI Guidelines

CBRLM/ Collins Stewart Inga

Collins Stewart Inga Private Limited, a company incorporated under the Companies Act and having its registered office at 3/12, Seema Co-operative Society, N. Dutta Marg, Andheri (West), Mumbai 400 053

Cut-off Price Any price within the Price Band finalised by the Company in consultation with the BRLMs. A Bid submitted at Cut-off Price is a valid Bid at all price levels within the Price Band

Designated Date The date on which funds are transferred from the Escrow Account(s) to the Public Issue Account after the Prospectus is filed with the RoC, following which the Board shall Allot Equity Shares to successful Bidders

Designated Stock Exchange NSE Draft Red Herring Prospectus

The Draft Red Herring Prospectus filed with SEBI, which does not have complete particulars on the price at which the Equity Shares are offered and size of the Issue

Due Date for Balance Amount Payable

Last date for payment of the Balance Amount Payable for Retail Individual Bidders and Non-Institutional Bidders choosing Payment Method-1, which is a date falling 21 days from the date of Allotment.

Eligible Employees Permanent employees of the Company, GIL, KBICL, GICL, REL, AEL, GPDL, MPSL, GLL, THPL, SHPVL, CBICL and MNEL as of January 31, 2008 who are Indian Nationals based in India and are present in India on the date of submission of the Bid-cum-Application Form

Employee Reservation Portion

The portion of the Issue being up to 16,55,000 Equity Shares available for allocation to Eligible Employees

Equity Shares Equity shares of our Company of Rs. 10 each fully paid up unless otherwise specified in the context thereof

Escrow Account Account opened with an Escrow Collection Bank(s) and in whose favour the Bidder will issue cheques or drafts in respect of the Bid Amount

Escrow Agreement Agreement entered into amongst the Company, the Registrar, the Escrow Collection Bank(s), the BRLMs, the CBRLM and the Syndicate Members for collection of the Bid Amounts and for remitting refunds, if any, of the amounts collected, to the Bidders

Escrow Collection Bank(s) The banks, which are clearing members and registered with SEBI as Banker(s) to the Issue, at which the Escrow Account will be opened

First Bidder The Bidder whose name appears first in the Bid cum Application Form or Revision Form

Floor Price The lower end of the Price Band, below which the Issue Price will not be finalized and below which no Bids will be accepted

IPO Initial Public Offering Issue Public issue of 1,65,50,000 Equity Shares of Rs. 10 each for cash at a price of

Rs. [●] per Equity Share (including a share premium of Rs. [●] per Equity Share) aggregating up to Rs. [●] lakhs. The Issue comprises a Net Issue to the Public of 1,48,95,000 Equity Shares and a Reservation of up to 16,55,000 Equity Shares for subscription by Eligible Employees

Issue Price The final price at which Equity Shares will be Allotted in terms of the Prospectus, as determined by the Company in consultation with the BRLMs on the Pricing Date

Macquarie Macquarie India Advisory Services Private Limited*, a company incorporated under the Companies Act and having its registered office at Level 3, Mafatlal Centre, Nariman Point, Mumbai 400 021 * name proposed to be changed to Macquarie Capital Advisers (India) Private Limited subject to regulatory approvals

vii

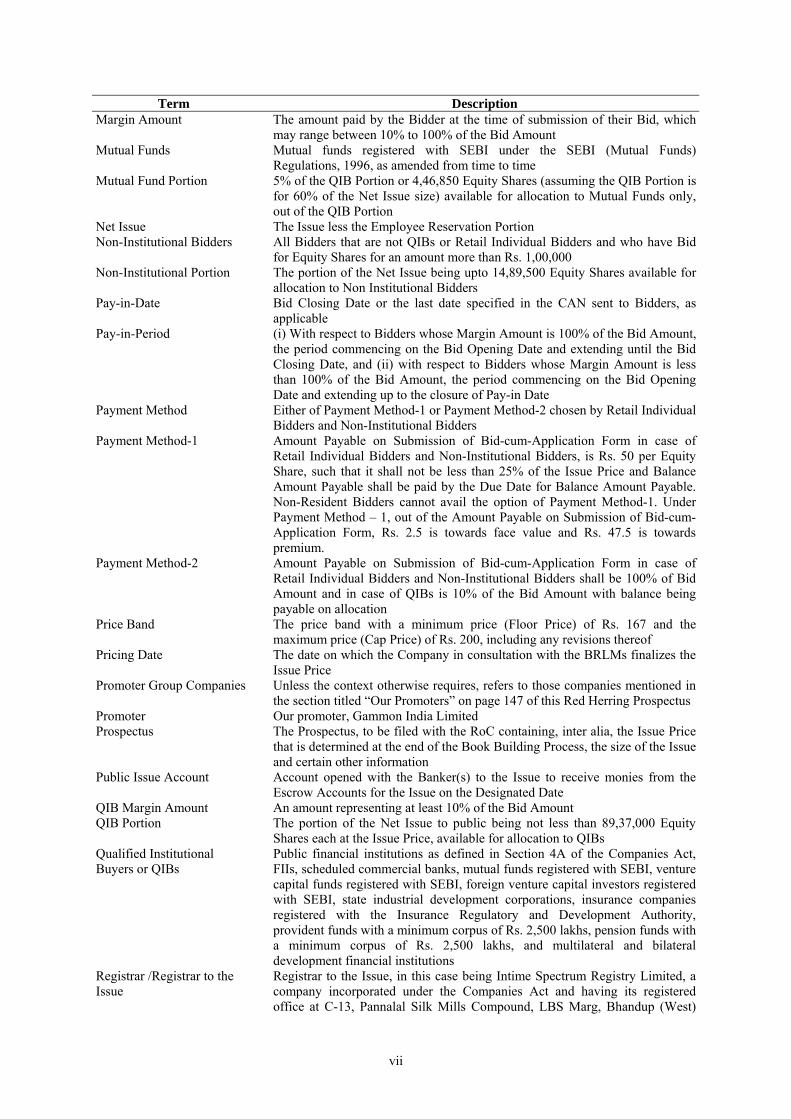

Term Description Margin Amount The amount paid by the Bidder at the time of submission of their Bid, which

may range between 10% to 100% of the Bid Amount Mutual Funds Mutual funds registered with SEBI under the SEBI (Mutual Funds)

Regulations, 1996, as amended from time to time Mutual Fund Portion 5% of the QIB Portion or 4,46,850 Equity Shares (assuming the QIB Portion is

for 60% of the Net Issue size) available for allocation to Mutual Funds only, out of the QIB Portion

Net Issue The Issue less the Employee Reservation Portion Non-Institutional Bidders All Bidders that are not QIBs or Retail Individual Bidders and who have Bid

for Equity Shares for an amount more than Rs. 1,00,000 Non-Institutional Portion The portion of the Net Issue being upto 14,89,500 Equity Shares available for

allocation to Non Institutional Bidders Pay-in-Date Bid Closing Date or the last date specified in the CAN sent to Bidders, as

applicable Pay-in-Period (i) With respect to Bidders whose Margin Amount is 100% of the Bid Amount,

the period commencing on the Bid Opening Date and extending until the Bid Closing Date, and (ii) with respect to Bidders whose Margin Amount is less than 100% of the Bid Amount, the period commencing on the Bid Opening Date and extending up to the closure of Pay-in Date

Payment Method Either of Payment Method-1 or Payment Method-2 chosen by Retail Individual Bidders and Non-Institutional Bidders

Payment Method-1 Amount Payable on Submission of Bid-cum-Application Form in case of Retail Individual Bidders and Non-Institutional Bidders, is Rs. 50 per Equity Share, such that it shall not be less than 25% of the Issue Price and Balance Amount Payable shall be paid by the Due Date for Balance Amount Payable. Non-Resident Bidders cannot avail the option of Payment Method-1. Under Payment Method � 1, out of the Amount Payable on Submission of Bid-cum-Application Form, Rs. 2.5 is towards face value and Rs. 47.5 is towards premium.

Payment Method-2 Amount Payable on Submission of Bid-cum-Application Form in case of Retail Individual Bidders and Non-Institutional Bidders shall be 100% of Bid Amount and in case of QIBs is 10% of the Bid Amount with balance being payable on allocation

Price Band The price band with a minimum price (Floor Price) of Rs. 167 and the maximum price (Cap Price) of Rs. 200, including any revisions thereof

Pricing Date The date on which the Company in consultation with the BRLMs finalizes the Issue Price

Promoter Group Companies Unless the context otherwise requires, refers to those companies mentioned in the section titled �Our Promoters� on page 147 of this Red Herring Prospectus

Promoter Our promoter, Gammon India Limited Prospectus The Prospectus, to be filed with the RoC containing, inter alia, the Issue Price

that is determined at the end of the Book Building Process, the size of the Issue and certain other information

Public Issue Account Account opened with the Banker(s) to the Issue to receive monies from the Escrow Accounts for the Issue on the Designated Date

QIB Margin Amount An amount representing at least 10% of the Bid Amount QIB Portion The portion of the Net Issue to public being not less than 89,37,000 Equity

Shares each at the Issue Price, available for allocation to QIBs Qualified Institutional Buyers or QIBs

Public financial institutions as defined in Section 4A of the Companies Act, FIIs, scheduled commercial banks, mutual funds registered with SEBI, venture capital funds registered with SEBI, foreign venture capital investors registered with SEBI, state industrial development corporations, insurance companies registered with the Insurance Regulatory and Development Authority, provident funds with a minimum corpus of Rs. 2,500 lakhs, pension funds with a minimum corpus of Rs. 2,500 lakhs, and multilateral and bilateral development financial institutions

Registrar /Registrar to the Issue

Registrar to the Issue, in this case being Intime Spectrum Registry Limited, a company incorporated under the Companies Act and having its registered office at C-13, Pannalal Silk Mills Compound, LBS Marg, Bhandup (West)

viii

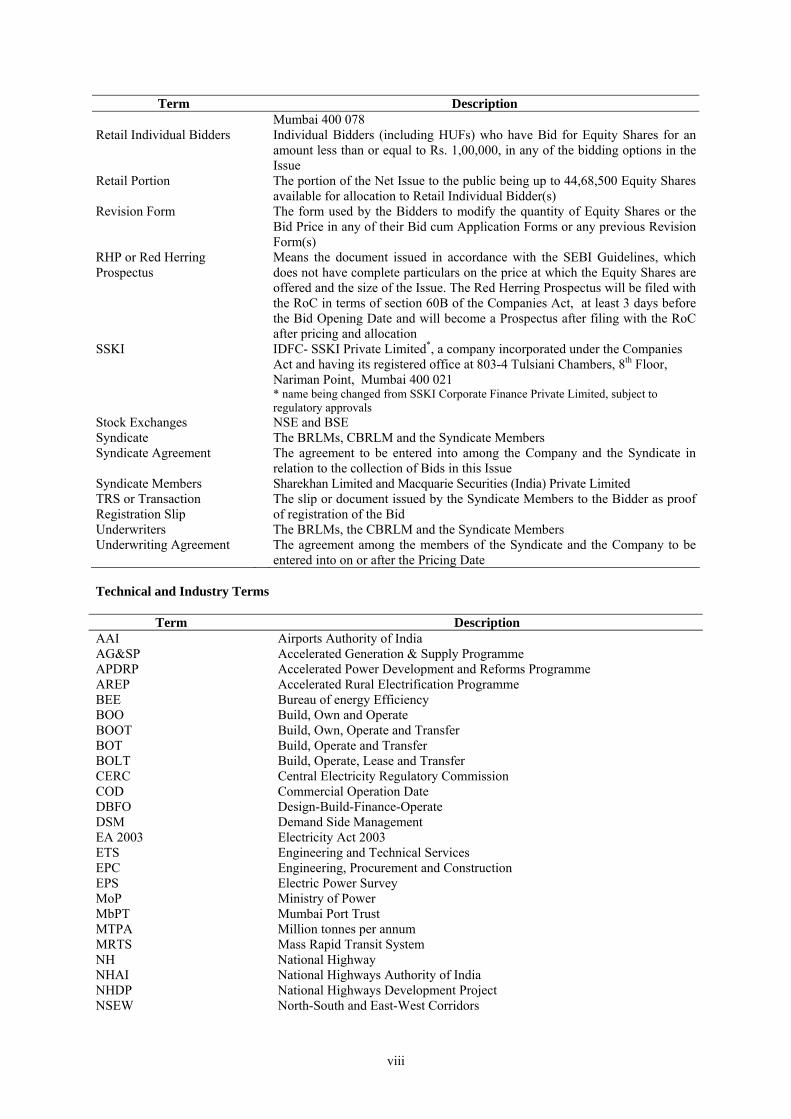

Term Description Mumbai 400 078

Retail Individual Bidders Individual Bidders (including HUFs) who have Bid for Equity Shares for an amount less than or equal to Rs. 1,00,000, in any of the bidding options in the Issue

Retail Portion The portion of the Net Issue to the public being up to 44,68,500 Equity Shares available for allocation to Retail Individual Bidder(s)

Revision Form The form used by the Bidders to modify the quantity of Equity Shares or the Bid Price in any of their Bid cum Application Forms or any previous Revision Form(s)

RHP or Red Herring Prospectus

Means the document issued in accordance with the SEBI Guidelines, which does not have complete particulars on the price at which the Equity Shares are offered and the size of the Issue. The Red Herring Prospectus will be filed with the RoC in terms of section 60B of the Companies Act, at least 3 days before the Bid Opening Date and will become a Prospectus after filing with the RoC after pricing and allocation

SSKI IDFC- SSKI Private Limited*, a company incorporated under the Companies Act and having its registered office at 803-4 Tulsiani Chambers, 8th Floor, Nariman Point, Mumbai 400 021 * name being changed from SSKI Corporate Finance Private Limited, subject to regulatory approvals

Stock Exchanges NSE and BSE Syndicate The BRLMs, CBRLM and the Syndicate Members Syndicate Agreement The agreement to be entered into among the Company and the Syndicate in

relation to the collection of Bids in this Issue Syndicate Members Sharekhan Limited and Macquarie Securities (India) Private Limited TRS or Transaction Registration Slip

The slip or document issued by the Syndicate Members to the Bidder as proof of registration of the Bid

Underwriters The BRLMs, the CBRLM and the Syndicate Members Underwriting Agreement The agreement among the members of the Syndicate and the Company to be

entered into on or after the Pricing Date Technical and Industry Terms

Term Description AAI Airports Authority of India AG&SP Accelerated Generation & Supply Programme APDRP Accelerated Power Development and Reforms Programme AREP Accelerated Rural Electrification Programme BEE Bureau of energy Efficiency BOO Build, Own and Operate BOOT Build, Own, Operate and Transfer BOT Build, Operate and Transfer BOLT Build, Operate, Lease and Transfer CERC Central Electricity Regulatory Commission COD Commercial Operation Date DBFO Design-Build-Finance-Operate DSM Demand Side Management EA 2003 Electricity Act 2003 ETS Engineering and Technical Services EPC Engineering, Procurement and Construction EPS Electric Power Survey MoP Ministry of Power MbPT Mumbai Port Trust MTPA Million tonnes per annum MRTS Mass Rapid Transit System NH National Highway NHAI National Highways Authority of India NHDP National Highways Development Project NSEW North-South and East-West Corridors

ix

Term Description O&M Operations and Maintenance PPA Power Purchase Agreement PPP Public Private Partnership R&M Renovation & Modernization REST Rural Electricity Supply Technology RFQ Request for Qualification RFP Request for Proposal RIDF Rural Infrastructure Development Fund SAIL Steel Authority of India Limited SERC State Electricity Regulatory Commissions SPV(s) Special Purpose Vehicle(s) T&D Transmission and Distribution TEU Twenty Feet Equivalent Unit Conventional/General Terms

Term Description AGM Annual General Meeting AS Accounting Standards as issued by the Institute of Chartered Accountants of

India BIFR Board for Industrial and Financial Reconstruction BSE Bombay Stock Exchange Limited CAG Comptroller and Auditor General CAGR Compounded Annual Growth Rate CDSL Central Depository Services (India) Limited Companies Act The Companies Act, 1956, as amended from time to time Debt Equity Ratio Secured and Unsecured debt divided by Net Worth Depositories Act The Depositories Act, 1996, as amended from time to time Depository A body corporate registered under the SEBI (Depositories and Participants)

Regulations, 1996, as amended from time to time Depository Participant A depository participant as defined under the Depositories Act ECS Electronic Clearing Service EGM Extraordinary General Meeting EPS Earnings per share EPZ Export Processing Zone Electronic Transfer of Funds Refunds through ECS, Direct Credit or RTGS as applicable FDI Foreign direct investment FEMA Foreign Exchange Management Act, 1999, as amended from time to time, and

the regulations framed thereunder FII Foreign Institutional Investor (as defined under Foreign Exchange Management

(Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000) registered with SEBI under applicable laws in India

FIPB Foreign Investment Promotion Board Financial Year/fiscal year/ FY/fiscal

Period of twelve months ended March 31 of that particular year, unless otherwise stated

GCDA Greater Cochin Development Authority Government/ GOI The Government of India GOK Government of Kerala GOS Government of Sikkim HUF Hindu Undivided Family I.T. Act The Income Tax Act, 1961, as amended from time to time Indian GAAP Generally Accepted Accounting Principles in India NAV/Net Asset Value Net Worth divided by number of shares. For subsidiaries net worth is defined

as shareholders funds less miscellaneous expenditure, to the extent not written off as per its audited financial statements

NMDP National Maritime Development Programme NOC No Objection Certificate Non-Residents/ NR Non-Resident is a Person resident outside India, as defined under FEMA and

includes a Non-Resident Indian

x

Term Description NRE Account Non-Resident External Account NRI/Non-Resident Indian Non-Resident Indian, is a Person resident outside India, who is a citizen of

India or a Person of Indian origin and shall have the same meaning as ascribed to such term in the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000

NRO Account Non-Resident Ordinary Account NSDL National Securities Depository Limited NSE National Stock Exchange of India Limited OCB/Overseas Corporate Body

A company, partnership, society or other corporate body owned directly or indirectly to the extent of at least 60% by NRIs, including overseas trusts in which not less than 60% of beneficial interest is irrevocably held by NRIs directly or indirectly as defined under Foreign Exchange Management (Deposit) Regulations, 2000. OCBs are not allowed to invest in this Issue.

p.a. / P.A. Per annum P/E Ratio Price/Earnings Ratio PAN Permanent Account Number Person/Persons Any individual, sole proprietorship, unincorporated association, unincorporated

organization, body corporate, corporation, company, partnership, limited liability company, joint venture, or trust or any other entity or organization validly constituted and/or incorporated in the jurisdiction in which it exists and operates, as the context requires

PIO/ Person of Indian Origin Shall have the same meaning as is ascribed to such term in the Foreign Exchange Management (Investment in Firm or Proprietary Concern in India) Regulations, 2000

Re. One Indian Rupee RBI The Reserve Bank of India RoC The Registrar of Companies, Maharashtra at Mumbai located at Everest House,

Marine Lines, Mumbai 400 020 Rs. Indian Rupees RTGS Real Time Gross Settlement Process SCRR Securities Contract Regulation Rules, 1957, as amended SEBI The Securities and Exchange Board of India constituted under the SEBI Act,

1992 SEBI Guidelines SEBI (Disclosure and Investor Protection) Guidelines, 2000 issued by SEBI on

January 27, 2000, as amended, including instructions and clarifications issued by SEBI from time to time

SEBI Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 1997, as amended from time to time

SEZ Special Economic Zone SICA Sick Industrial Companies (Special Provisions) Act, 1995 TAMP The Tariff Authority for Major Ports U.S. GAAP Generally accepted accounting principles in the United States of America UNCITRAL United Nations Commission on International Trade Law

xi

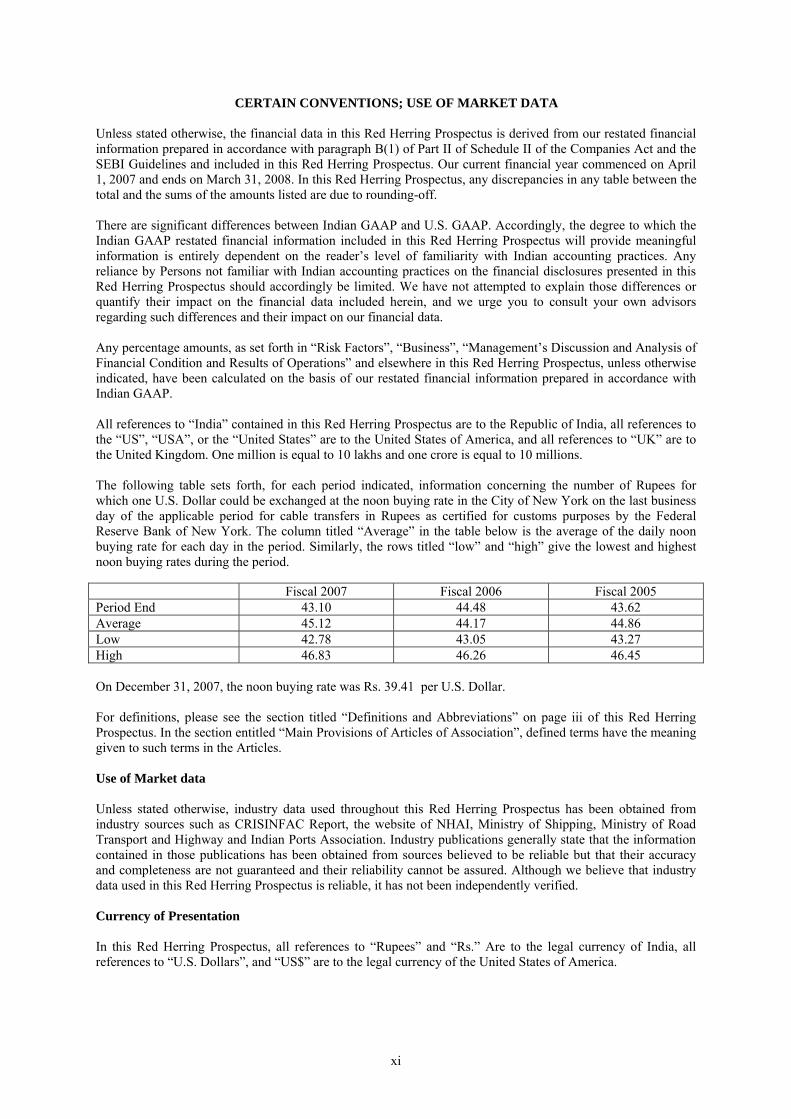

CERTAIN CONVENTIONS; USE OF MARKET DATA Unless stated otherwise, the financial data in this Red Herring Prospectus is derived from our restated financial information prepared in accordance with paragraph B(1) of Part II of Schedule II of the Companies Act and the SEBI Guidelines and included in this Red Herring Prospectus. Our current financial year commenced on April 1, 2007 and ends on March 31, 2008. In this Red Herring Prospectus, any discrepancies in any table between the total and the sums of the amounts listed are due to rounding-off. There are significant differences between Indian GAAP and U.S. GAAP. Accordingly, the degree to which the Indian GAAP restated financial information included in this Red Herring Prospectus will provide meaningful information is entirely dependent on the reader�s level of familiarity with Indian accounting practices. Any reliance by Persons not familiar with Indian accounting practices on the financial disclosures presented in this Red Herring Prospectus should accordingly be limited. We have not attempted to explain those differences or quantify their impact on the financial data included herein, and we urge you to consult your own advisors regarding such differences and their impact on our financial data. Any percentage amounts, as set forth in �Risk Factors�, �Business�, �Management�s Discussion and Analysis of Financial Condition and Results of Operations� and elsewhere in this Red Herring Prospectus, unless otherwise indicated, have been calculated on the basis of our restated financial information prepared in accordance with Indian GAAP. All references to �India� contained in this Red Herring Prospectus are to the Republic of India, all references to the �US�, �USA�, or the �United States� are to the United States of America, and all references to �UK� are to the United Kingdom. One million is equal to 10 lakhs and one crore is equal to 10 millions. The following table sets forth, for each period indicated, information concerning the number of Rupees for which one U.S. Dollar could be exchanged at the noon buying rate in the City of New York on the last business day of the applicable period for cable transfers in Rupees as certified for customs purposes by the Federal Reserve Bank of New York. The column titled �Average� in the table below is the average of the daily noon buying rate for each day in the period. Similarly, the rows titled �low� and �high� give the lowest and highest noon buying rates during the period. Fiscal 2007 Fiscal 2006 Fiscal 2005 Period End 43.10 44.48 43.62 Average 45.12 44.17 44.86 Low 42.78 43.05 43.27 High 46.83 46.26 46.45 On December 31, 2007, the noon buying rate was Rs. 39.41 per U.S. Dollar. For definitions, please see the section titled �Definitions and Abbreviations� on page iii of this Red Herring Prospectus. In the section entitled �Main Provisions of Articles of Association�, defined terms have the meaning given to such terms in the Articles. Use of Market data Unless stated otherwise, industry data used throughout this Red Herring Prospectus has been obtained from industry sources such as CRISINFAC Report, the website of NHAI, Ministry of Shipping, Ministry of Road Transport and Highway and Indian Ports Association. Industry publications generally state that the information contained in those publications has been obtained from sources believed to be reliable but that their accuracy and completeness are not guaranteed and their reliability cannot be assured. Although we believe that industry data used in this Red Herring Prospectus is reliable, it has not been independently verified. Currency of Presentation In this Red Herring Prospectus, all references to �Rupees� and �Rs.� Are to the legal currency of India, all references to �U.S. Dollars�, and �US$� are to the legal currency of the United States of America.

xii

FORWARD-LOOKING STATEMENTS We have included statements in this Red Herring Prospectus, that contain words or phrases such as �will�, �aim�, �will likely result�, �believe�, �expect�, �will continue�, �anticipate�, �estimate�, �intend�, �plan�, �contemplate�, �seek to�, �future�, �objective�, �goal�, �project�, �should�, �will pursue� and similar expressions or variations of such expressions that are �forward-looking statements�.

All forward-looking statements are subject to risks, uncertainties and assumptions that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement. Important factors that could cause actual results to differ materially from our expectations include, among others:

• Implementation risks involved in our projects; • Political and regulatory environment; • Our ability to raise capital for our future projects; • Our ability to service our debt service obligations; • Continuation of tax benefits available to us; • Our ability to successfully implement our strategy, growth and expansion plans; • Our exposure to market risks; • Changes in the value of the Rupee and other currencies; • The monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest

rates; • Changes in the foreign exchange control regulations in India; • Foreign exchange rates, equity prices or other rates or prices; and • The performance of the financial markets in India. For further discussion of factors that could cause our actual results to differ, see the section titled �Risk Factors� on page xiii of this Red Herring Prospectus. By their nature, certain risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated. We, the members of the Syndicate and their respective affiliates do not have any obligation to, and do not intend to, update or otherwise revise any statements reflecting circumstances arising after the date hereof or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to fruition. In accordance with SEBI requirements, we and the BRLMs and the CBRLM will ensure that investors in India are informed of material developments until such time as the grant of listing and trading permission by the Stock Exchanges.

xiii

SECTION II – RISK FACTORS An investment in Equity Shares involves a high degree of risk. You should consider all information in this red herring prospectus before making an investment in Equity Shares. If any of the following risks or any of the other risks and uncertainties discussed in this Red Herring Prospectus actually occur, our business, financial condition and results of operations could suffer, the trading price of our Equity Shares could decline, and you may lose all or part of your investment. Unless specified or quantified in the relevant risk factors below, we are not in a position to quantify the financial or other implication of any of the risks described in this section. Internal Risk Factors 1. There are outstanding litigations against us, our Directors, our Promoter and the Promoter Group

Companies

We, our Promoter and the Promoter Group Companies are defendants in legal proceedings incidental to our business and operations. These legal proceedings are pending at different levels of adjudication before various courts, tribunals and statutory authorities, brief details of which are set out below: Litigation involving the Company

SEBI related matter

Please refer to Risk Factor No. 2 below.

Arbitration matters

There are two arbitration petitions in which Company is a co-respondent in relation to the �Passenger Water Transport System for the West Coast of Mumbai�.

Litigation involving our Directors

Criminal Cases

There are three criminal complaints involving our director Abhijit Rajan in relation to equity shares delivered by Prashant Glass Works (P) Limited pursuant to the public offer made by Pacific Energy Private Limited to the shareholders of GIL, non-maintenance of register under Section 8 of the Equal Remuneration Act, 1976 at a worksite and for employing unregistered security agency at one of the premises belonging to GIL respectively.

SEBI related matter

Please refer to Risk Factor No. 2 below.

Consumer related cases

There is one consumer complaint filed against our director Abhijit Rajan in relation to delivery of equity shares of GIL. No monetary claims have been made.

Litigation involving Our Associates and Subsidiaries

Civil matters VSPL There are three writ petitions pending involving our Associate company, VSPL in

relation to deployment of Harbour Mobile Crane on General Cargo Berth of Visakhapatnam Port and engagement of private workers at the dock respectively by VSPL.

REL There is one civil suit involving our subsidiary REL in relation to deficient payment of stamp duty of Rs. 17,76,99,900.

CBICL There is one writ petition involving our subsidiary CBICL in relation to extension of concession period and grant of annuity. We have also initiated arbitration proceedings in relation to the aforesaid matter.

THPL There is one writ petition involving our subsidiary THPL in relation to execution of MOU for Tidong (II) Hydro Electric Power Project.

xiv

Arbitration matters

VSPL There is an arbitration petition involving our subsidiary, VSPL with respect to alleged delay in completion of construction of project facilities and the amount involved is Rs. 200 lakhs.

Litigation involving our Promoter

Criminal matters

There are three criminal matters filed against GIL in relation to non-maintenance of register under Section 8 of the Equal Remuneration Act, 1976 at a worksite and for employing unregistered security agency and non compliance with ESI Act.

SEBI related matter

Please refer to Risk Factor No. 2 below.

Departmental Inquiry

An Expert Committee has been constituted by Government of Andhra Pradesh to enquire into the collapse of a flyover at Hyderabad. The committee has recommended penal action of 10% of the total project costs and all costs direct and indirect concerned with loss to individual, private and public property.

Civil matters There are 34 civil matters filed against GIL, comprising 25 matters in which the total claim is Rs. 7,000 lakhs and nine matters, in which, the claim amount is not ascertainable. There are 29 civil matters filed by GIL, comprising 12 matters in which the total claim made by GIL is approximately Rs. 3,700 lakhs and seventeen matters in which the amount is not ascertainable.

Income Tax matters

There are eight income tax related cases involving GIL.

Sales Tax matters

There are 42 sales tax related cases and the total amount which is the subject matter of these litigations is Rs. 940 lakhs.

Services Tax matters

There are thirteen service tax notices/disputes comprising two matters in which the cumulative liability against GIL is expected to be Rs. 366 lakhs and eleven matters in which the amount involved is not ascertainable.

Excise/Custom Duty matters

There are three excise/customs related cases in which total amount of claims of over Rs. 213 lakhs may arise.

Arbitration matters

There are five arbitration references made against GIL wherein a total amount of approximately Rs. 1,470 lakhs has been claimed against GIL. GIL has filed counter claim of approximately Rs. 320 lakhs in these references. There are twenty two arbitration references made by GIL in which GIL has claimed approx. Rs. 29,600 lakhs. Counter claims of approx. Rs. 5,050 lakhs have been made against GIL in these references.

Labour matters There are 18 labour matters filed against GIL, comprising two matters in which the total claim is Rs. 12.5 lakhs and 16 matters in which the amount is not ascertainable. There are five labour matters filed by GIL.

Litigation involving our Promoter Group Companies

Civil matters PEPL A civil suit relating to recovery of an amount of Rs. 389.50 lakhs is pending. ATSL

There are seven civil cases involving ATSL in which a total amount of Rs. 4.60 lakhs has been claimed by ATSL and a total claim of Rs. 9.50 lakhs has been raised by ATSL.

xv

STFAPL A recovery suit for an outstanding amount of Rs. 5,53,446 has been decreed against

STFA Piling (India) Limited. Labour matters

ATSL There are eight labour cases pending against ATSL. The nature of claims in these cases is such that no financial value can be ascertained

Income Tax matters

ATSL There are four income tax matters pending against ATSL before the Income Tax Appellate Tribunal, Ahmedabad wherein the amount involved in Rs. 45.50 lakhs.

Should any new developments arise, such as a change in Indian law or rulings against us by appellate courts or tribunals, we may need to make provisions in our financial statements, which could increase our expenses and our current liabilities. Furthermore, if significant claims are determined against us and we are required to pay all or a portion of the disputed amounts, it could have a material adverse effect on our business and profitability. For more information regarding litigation involving us and the Promoter Group Companies, see the section titled �Outstanding Litigation and Material Developments� beginning on page 271 of this Red Herring Prospectus.

2. SEBI passed an order prohibiting GIL, our Promoter, Mr. Abhijit Rajan, our Chairman and Managing

Director and two other companies, controlled by Mr. Abhijit Rajan from accessing the capital markets, directly or indirectly

SEBI by way of its order dated December 21, 2006 prohibited our Promoter, GIL, Mr. Abhijit Rajan, our Chairman and Managing Director and two other companies from accessing the capital markets, directly or indirectly for a period of one year from the date of the order. Further, in terms of the order, GIL, Mr. Abhijit Rajan and the two others companies are also prohibited from divesting, transferring, selling or alienating in any way their shareholding in our Company for a period of three years from the date of allotment in the proposed IPO. The Securities Appellate Tribunal (�SAT�) on March 23, 2007 admitted two appeals filed by GIL and Mr. Rajan and two others against the SEBI order. In light of the above order, SEBI passed a further order dated February 2, 2007 and prohibited our Company from accessing the capital market for a period of one year from December 21, 2006.

SAT, by its order dated March 23, 2007 admitted the appeal filed by our Company against the order dated February 2, 2007 and has also granted an interim relief by directing SEBI to reopen and process the file pertaining to the earlier draft red herring prospectus dated March 28, 2006. In the event that the interim relief is reversed, this Issue may be significantly delayed and it may also result in adverse publicity, which could adversely impact our business. Further, the restriction on GIL in relation to divestment, transfer or sale of its entire shareholding for a period of three years from the date of allotment in the proposed IPO may also restrict our ability to raise financing through the pledge of these Equity Shares. The next hearing in the matter is scheduled on March 13, 2008.

3. The government order granting extension of the concession period and annuity to CBICL is under

challenge and may affect our revenues

A writ petition has been filed by the Kerala State Private Bus Owners Federation before the Kerala High Court challenging the government order dated January 24, 2005 granting extension of the concession period and annuity to CBICL. The petition has direct bearing on the concession period and our revenues from the bridge earned in terms of fees. Further, the revised concession agreement has not been formalized. CBICL has initiated arbitration proceedings against the Government of Kerala and Greater Cochin Development Authority for entering into the amended concession agreement incorporating the terms of the restructured concession. In the event of an adverse order under the writ petition by the Kerala High Court, our Company may suffer shortfall in revenues which will have an adverse effect on our results of operations.

xvi

4. Given the long-term nature of the projects we undertake, we face various kinds of implementation risks

All infrastructure development projects involve agreements that are long-term in nature. As of the date of this Red Herring Prospectus, we derive a substantial portion of our revenues from long-term concession or license agreements that range from 15 to 90 years. All long-term agreements have inherent risks associated with them that may not necessarily be within our control. Accordingly we are exposed to a variety of implementation and other risks, including construction delays, material shortages, unanticipated cost increases, cost overruns, inability to negotiate satisfactory arrangements with joint venture partners and disagreements with our joint venture partners.

For example, business circumstances may materially change over the life of one or more of our agreements and we may not have the ability to modify our agreements to reflect these changes. Further, being committed under these agreements may restrict our ability to implement changes to our business plan. This limits our business flexibility, exposes us to an increased risk of unforeseen business and industry changes and could have a material adverse effect on our business, financial condition and results of operations.

As our revenue structure under each such agreement is set over the life of the agreement (and fluctuates subject to the built-in adjustment mechanisms contained in such agreement), our profitability is largely a function of how effectively we are able to manage our costs during the terms of our agreements. If we are unable to effectively manage costs, our business, financial condition and results of operations may be materially and adversely affected.

5. We rely substantially on government-owned and government-controlled entities for our revenues.

Political or financial pressures could cause these entities to force us to renegotiate our agreements and could also adversely affect their ability to pay us

All infrastructure development projects under public private partnership in India, including all of our projects, have been awarded by government-owned or government-controlled entities and, therefore, may be subject to political or financial pressures that may lead to such agreements being restructured or renegotiated by these entities, which could materially and adversely affect our business and results of operations.

Additionally, our projects are government-owned or government-controlled projects and these are often subject to delay. Such delays could be on account of a change in the central and/or state government, changes in policies impacting the public at large, scaling back of government policies or initiatives, changes in governmental or external budgetary allocation, or insufficiency of funds, which can significantly and adversely affect our business, financial condition and results of operations.

6. Our flexibility in managing our operations is limited by the regulatory environment in which we operate

The infrastructure business in India is highly regulated. Our businesses are regulated by various authorities and state governments, including the Ministry of Shipping, Road Transport and Highways, the NHAI, the GOK, the VPT, the Ministry of Power and the Government of Sikkim. We may be restricted, in our ability to, among other things, increase prices, sell our interests to third parties, undertake expansions and contract with certain customers. These restrictions may limit our flexibility in operating our business, which could have a material adverse effect on our business, prospects, financial condition and results of operations.

7. We operate in an industry that is capital intensive in nature and we may not be able to raise the required

capital for future projects which may have an adverse effect on our business and results of operations

Infrastructure projects are typically capital intensive and may require high levels of financing. We have so far been able to arrange for the financing of all our projects. However, we cannot assure you that market conditions and other factors would permit us to obtain financing on terms acceptable to us. Our ability to arrange financing on a substantially non-recourse basis and the costs of capital of such financing are dependant on numerous factors, including general economic and capital market conditions, credit availability from banks, investor confidence, the continued success of our current projects and other laws that are conducive to our raising capital in this manner. Our attempts to complete future financings may not be successful or on favourable terms and failure to obtain financing on terms favourable to us could have an adverse effect on our business and results of operations.

xvii

8. We have substantial indebtedness and will continue to have substantial indebtedness and debt service obligations following the Issue

We have substantial indebtedness at the SPV level. As of September 30, 2007, on a consolidated basis, the SPVs had a total indebtedness of Rs. 79,937 lakhs, which was secured by their assets. As of September 30, 2007, our consolidated Debt to Equity Ratio was 2.81. The high degree of leverage in the SPVs (i) renders them more vulnerable to downturns in their businesses, which are subject to general economic conditions in India, inflation and other factors; (ii) limits their ability to obtain additional financing, if required and (iii) limits their ability to refinance existing indebtedness on terms favorable to them. Any of these could have significant consequences to the business and results of operations of the SPVs, and consequently to our shareholders to the extent of our holding in each of the SPVs.

For more information regarding our indebtedness, see the section titled �Indebtedness� beginning on page 262 of this Red Herring Prospectus.

9. Increases in interest rates may materially impact our results of operations

As our businesses are capital intensive, we are exposed to interest rate risk. Any increase in interest expense may have a material adverse effect on our business prospects and results of operations. Our current debt facilities carry interest at fixed rates with the provision for periodic reset of interest rates.

Although we may decide to engage in interest rate hedging transactions or exercise the right available to us to terminate the current debt financing arrangement on the respective reset dates and enter into new financing arrangements, there can be no assurance that we will be able to do so on commercially reasonable terms, that our counter-parties will perform their obligations, or that these agreements, if entered into, will protect us fully against interest rate risk.

10. Our growth strategy depends upon the award of new contracts

The growth of our business depends on us winning new contracts. Generally, it is very difficult to predict whether and when we will be awarded a new contract since many potential contracts involve a lengthy and complex bidding and selection process that may be affected by a number of factors, including changes in existing or assumed market conditions, financing arrangements, governmental approvals and environmental matters. Because the growth of our business will be derived primarily from these contracts, our future results of operations and cash flows can fluctuate materially from period to period depending on the timing of contract awards.

11. Demand for infrastructure services in India depends on domestic and regional economic growth

The infrastructure development business is dependent on the level of domestic, regional and global economic growth, international trade and consumer spending. The rate of growth of India�s economy and of the demand for infrastructure services in India may fluctuate over the years. During periods of strong economic growth, demand for such services may grow at a rate equal to, or even greater than, that of the GDP. Conversely, during periods of slow GDP growth, such demand may exhibit slow or even negative growth. There can be no assurance that future fluctuations in economic or business cycles, or other events that could influence GDP growth, will not have a material adverse effect on our business and results of operations.

12. We face margin pressure as a large number of infrastructure-related contracts are awarded by the GOI

and state governments following competitive bidding processes

Most of the infrastructure-related contracts are awarded by the GOI, state governments or their respective authorized agencies through competitive bidding processes and satisfaction of other prescribed pre-qualification criteria. Once the prospective bidders clear the technical requirements of the tender, the contract is usually awarded to the most competitive financial bidder. We face competition from domestic and international companies, some of whom may operate on a larger scale than us and thus may be able to achieve better economies of scale than us. The nature of the bidding process may cause us and our competitors to accept lower margins in order to be awarded the contract, which may have a material adverse effect on our business, financial condition and results of operations.

xviii

13. Certain government interests as our regulator, customer, joint venture partner and direct or indirect competitor may give rise to conflicts of interest that may harm us

We have entered into agreements with government entities, including NHAI, GCDA, PSEB and the Board of Trustees of VPT. In cases like REL and AEL, NHAI is our sole client, in PBPL, PSEB is our sole customer and in some cases, such as VPT, they are our competitors. We may face or suffer potential conflicts of interest, which may arise from the fact that such government authorities play multiple roles in our business model. We cannot assure you that potential conflict of interest situations will not continue to arise in the future or that any disputes arising in relation thereto will be resolved in a manner favorable to us. Any such situation may have a material adverse effect on our business, financial condition and results of operations.

14. We currently enjoy certain tax benefits, and any change in tax policies applicable to us may affect our

results of operations

Presently, infrastructure development projects enjoy certain benefits under Section 80IA of the Income Tax Act, 1961. As a result of these incentives, most of our projects are subject to relatively low tax liabilities. Our income tax exemptions for various projects expire at various points of time. There is no assurance that the infrastructure projects will continue to enjoy the tax benefits under Section 80IA in future. When our tax incentives expire or terminate, our tax expense will materially increase, reducing our profitability. Further, the GOI could enact laws in the future that may adversely impact our tax incentives and consequently, our tax liabilities and profits.

15. Forward looking information may prove inaccurate

This Red Herring Prospectus contains certain forward-looking statements and information relating to us that is based on the beliefs of our management as well as assumptions made by, and information currently available to, our management. When used in this document, the words �anticipate�, �believe�, �estimate�, �expect�, �going forward� and similar expressions, as they relate to us or our management, are intended to identify forward-looking statements. Such statements reflect the current views of our management with respect to future events and are subject to certain risks, uncertainties and assumptions, including the risk factors described in this prospectus. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove to be incorrect, our business, financial condition and results of operations may be adversely affected and may vary materially from those described herein as anticipated, believed, estimated or expected.

16. We may encounter problems relating to the operations of our joint ventures

As a consequence of client requirements and to mitigate risks associated with projects, many of our current operations are conducted through subsidiaries and joint venture companies. Currently, we own a 42.22% interest in VSPL, which owns two multi-purpose berths at Visakhapatnam Port. In our road business, we own a 49.0% equity interest and a further beneficial interest in 44.50% of the equity of REL and AEL, the companies that own our two operational road projects. We also have a controlling interest in REL and AEL due to our right to appoint directors on their boards. This trend is likely to continue in the future. In case we are unable to forge alliances with other companies to meet the pre-qualification requirements, we may lose the opportunity to bid.

Where we have been awarded the project, revenues from the project will be that of the joint venture. We can derive revenue only to the extent of our share in the joint venture, as agreed in the applicable joint venture arrangements. Further, if we are unable to successfully manage relationships with our joint venture partners, such projects and therefore our profitability may suffer.

If our joint venture partners fail to perform their obligations satisfactorily, the joint venture may be unable to perform adequately or deliver its contracted services. In this case, we may be required to make additional investments and/or provide additional services to ensure the adequate performance and delivery of the contracted services because we are subject to joint and several liability as a member of the joint venture in most of our projects. These additional obligations could result in reduced profits or, in some cases, significant losses for us. The inability of a joint venture partner to continue with a project due to financial or legal difficulties could mean that we may be required to bear increased and possibly sole responsibility for the completion of the project and bear a correspondingly greater share of the financial risk of the project.

xix

In the event of any disagreements between us and our various joint venture partners regarding the business and operations of the joint ventures, we cannot assure you that we will be able to resolve them in a manner that will be in our best interests, which could have a material adverse effect on our business, financial condition and results of operations.

17. Delays in the completion of current and future projects could have adverse effects on our operating

results

We provide performance guarantees to our clients which require us to complete projects within a specified time frame. If we fail to complete a project as scheduled, we may generally be held liable for penalties in the form of agreed liquidated damages, which would ordinarily range between 5% to 10% of the total project cost or, in some cases, the client may be entitled to appoint, at our expense, a third party to complete the work. To the extent that this happens and is not otherwise covered by the escalations clause in the relevant contracts, the total cost of a project would exceed our original estimates and we could experience reduced profit or a loss on that project.

18. Our operations are, and will continue to be, primarily dependent on a small number of operating assets.

If the operation of one or more of these assets is disrupted, it would have a material adverse effect on our financial condition and results of operations

Our revenues are currently dependent largely on the operation of four assets: the roads under REL, AEL and CBICL; and the port facilities under VSPL. As per the concession agreements of the Mumbai-Nasik road project, Gorakhpur by-pass project, Kosi Bridge project and the Rangit II hydroelectric power project, we are required to begin full commercial operation by April 2009, October 2009, April 2010 and December 2011, respectively, on these projects. Consequently, we expect that for the next two fiscal years, our revenues will depend principally on these four operating assets. If one or more of these four assets is damaged and our losses are not adequately covered by the relevant insurance policies, or if any such asset undergoes maintenance for a longer period than was estimated, our business, financial condition and results of operations could be materially adversely affected.

19. Our revenues are highly dependent on a few major clients. The loss of any of these clients may adversely

impact our revenues and profitability

We derive a significant portion of our revenues from a limited number of clients. We currently generate our road revenues from REL, AEL and CBICL where our clients are NHAI in case of AEL and REL and GOK in case of CBICL. NHAI is also our client in two annuity and one toll projects being developed by us. In addition, the revenues from our port project is expected to come from long-term take-or-pay agreement with SAIL for the duration of the license agreement between VSPL and VPT. The loss of business from these clients may adversely impact our business, revenues and profitability.

20. Our clients may default on their payment obligations to us, which would have a materially adverse effect

on our results of operations

In REL and AEL, the NHAI pays us a fixed annuity at pre-determined intervals. The REL project commenced operations 70 days before schedule for which, under the terms of the agreement with NHAI, REL was to receive a bonus of Rs. 1,151.9 lakhs (net of TDS Rs. 1,084.9 lakhs, outstanding as on September 30, 2007) for achieving the commencement date ahead of schedule. This amount has not been paid by NHAI and REL has issued a notice to NHAI for the payment of such amount. The AEL project commenced operations 30 days before schedule for which, under the terms of the agreement with NHAI, AEL was to receive a bonus of Rs. 465.2 lakhs for achieving the commencement date ahead of schedule. This amount has also not been paid by NHAI. Failure on the part of NHAI to fulfill its obligations under its agreements, such as non payment of the bonus amount accrued to REL, would have an adverse effect on our revenues, ability to service our debt, business, financial condition and results of operations.

The annuity portion of revenues in CBICL is approximately 30% of its current total revenues as of September 30, 2007 and we have yet to sign the supplementary concession agreement and receive the annuity from the GOK for the past 2 years. Any material failure on the part of the GOK to fulfill its

xx

obligations would have a material adverse effect on our revenues, ability to service our debt, business, financial condition and results of operations.

Our port project company, VSPL, has entered into a long-term take-or-pay agreement with SAIL for the duration of the license agreement between VSPL and VPT. When the facilities at the port and the take-or-pay agreement become fully operational, this agreement is expected to account for a substantial portion of the total revenues of the project. Any material failure on the part of our company / SAIL to fulfill its obligations under the take-or-pay agreement may have an adverse effect on our revenues, ability to service our debt, business, financial condition and results of operations.

21. Projects sub-contracted can be delayed on account of the principal or sub-contractor’s performance,

resulting in delayed payments

We sub-contract work on all our projects and payments may depend on the sub-contractor�s performance. A delay in completion on the part of a sub-contractor, for any reason, could result in delayed payment. In addition, we may be liable to the client due to failure on the part of a sub-contractor to maintain the required performance standards or insufficiency of a sub-contractor�s performance guarantees.