Embed Size (px)

Citation preview

Fundamentals of Starting Fundamentals of Starting a Businessa Business

What we do …What we do … Building Better BusinessesBuilding Better BusinessesConsulting – No ChargeConsulting – No Charge• Assistance available to startup & existing businessesAssistance available to startup & existing businesses• Comprehensive Individualized Consulting – Business Comprehensive Individualized Consulting – Business

planning, growth strategies, financing options, financial planning, growth strategies, financing options, financial analysis, market analysis, etc.analysis, market analysis, etc.

Training Training • AffordableAffordable• ClassroomClassroom• Online – www.ksbdc.orgOnline – www.ksbdc.org

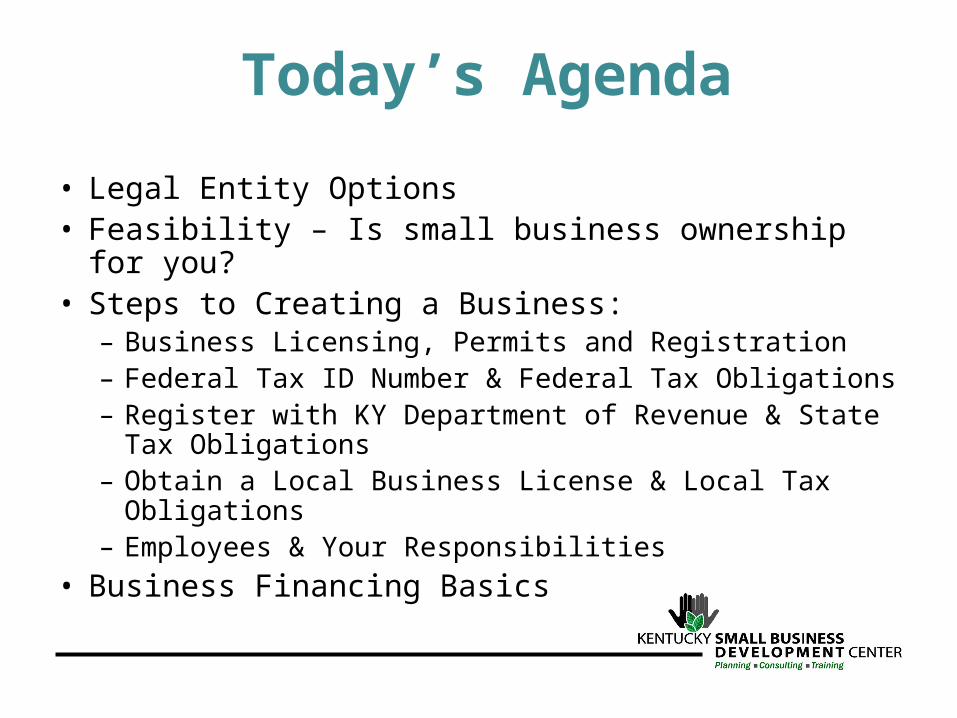

Today’s Agenda

• Legal Entity Options• Feasibility – Is small business ownership for you?• Steps to Creating a Business:

– Business Licensing, Permits and Registration– Federal Tax ID Number & Federal Tax Obligations– Register with KY Department of Revenue & State Tax

Obligations– Obtain a Local Business License & Local Tax

Obligations– Employees & Your Responsibilities

• Business Financing Basics

Legal Entity Options And Tax Considerations

When Starting A Business

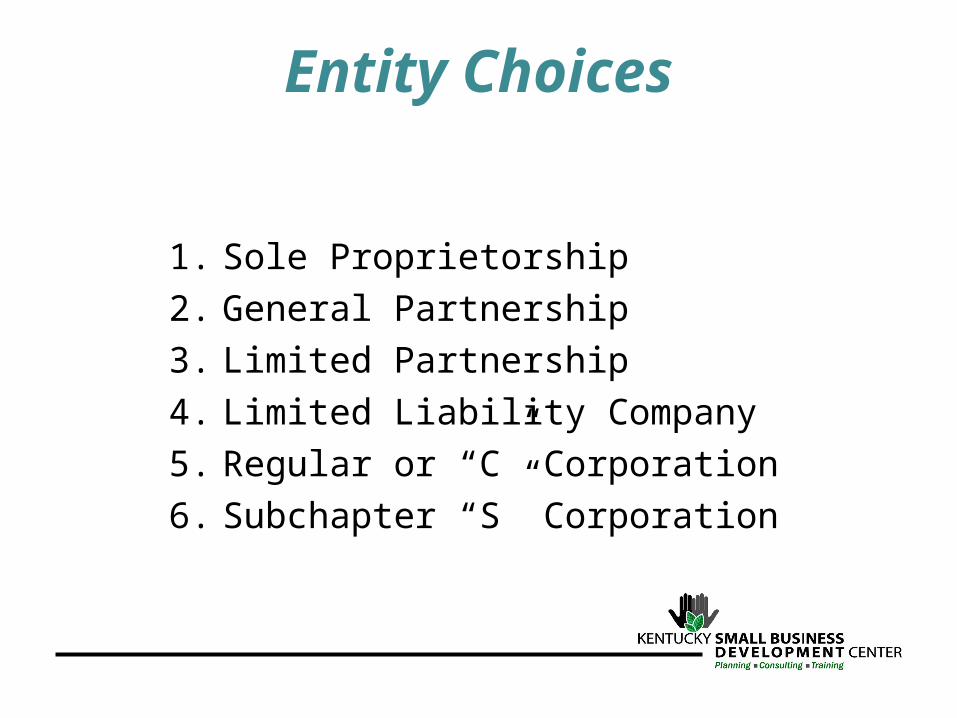

Entity Choices

1. Sole Proprietorship

2. General Partnership

3. Limited Partnership

4. Limited Liability Company

5. Regular or “C” Corporation

6. Subchapter “S” Corporation

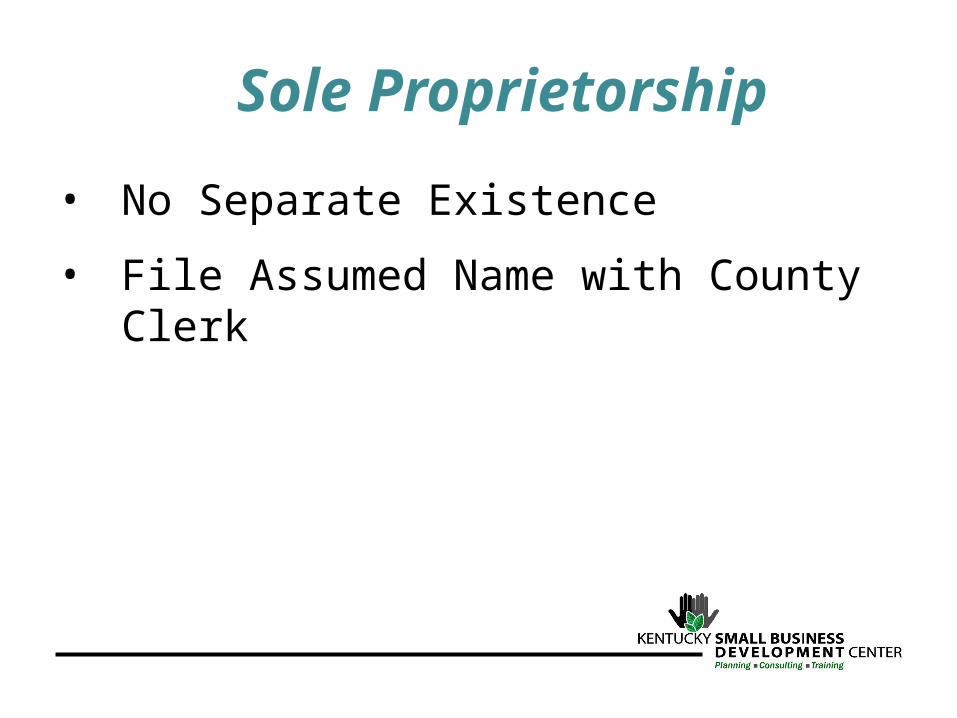

Sole Proprietorship

• No Separate Existence

• File Assumed Name with County Clerk

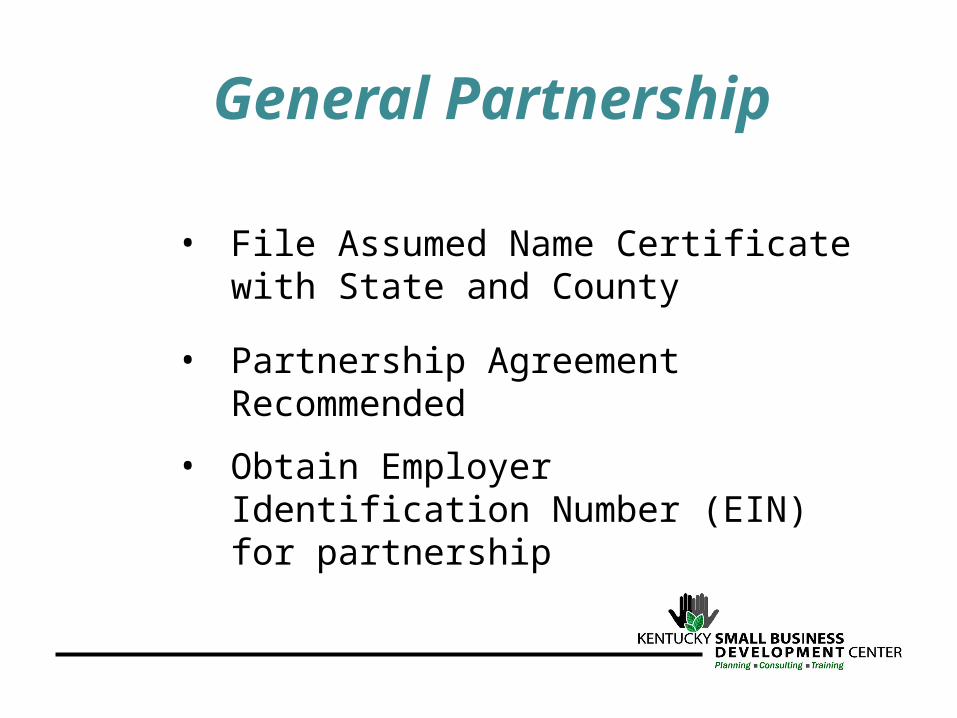

General Partnership

• File Assumed Name Certificate with State and County

• Partnership Agreement Recommended

• Obtain Employer Identification Number (EIN) for partnership

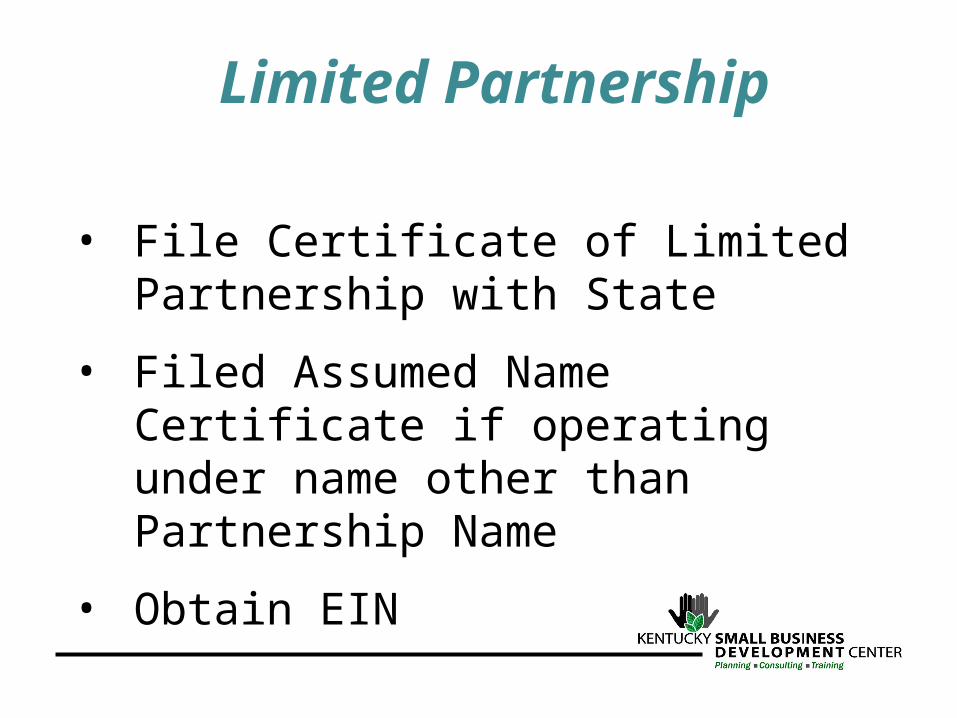

Limited Partnership

• File Certificate of Limited Partnership with State

• Filed Assumed Name Certificate if operating under name other than Partnership Name

• Obtain EIN

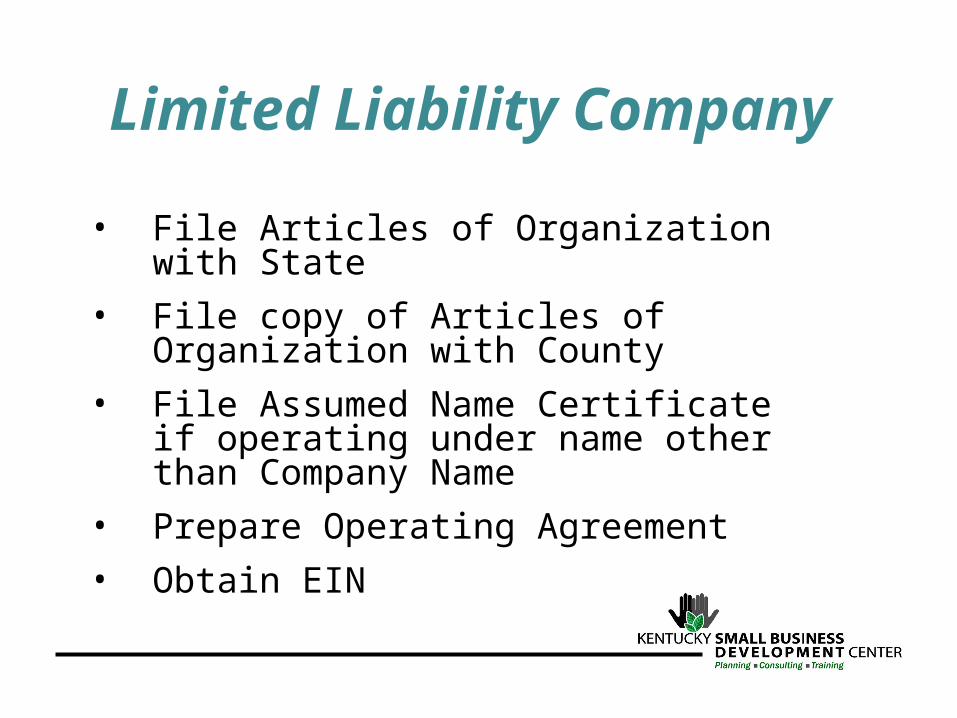

Limited Liability Company

• File Articles of Organization with State

• File copy of Articles of Organization with County

• File Assumed Name Certificate if operating under name other than Company Name

• Prepare Operating Agreement

• Obtain EIN

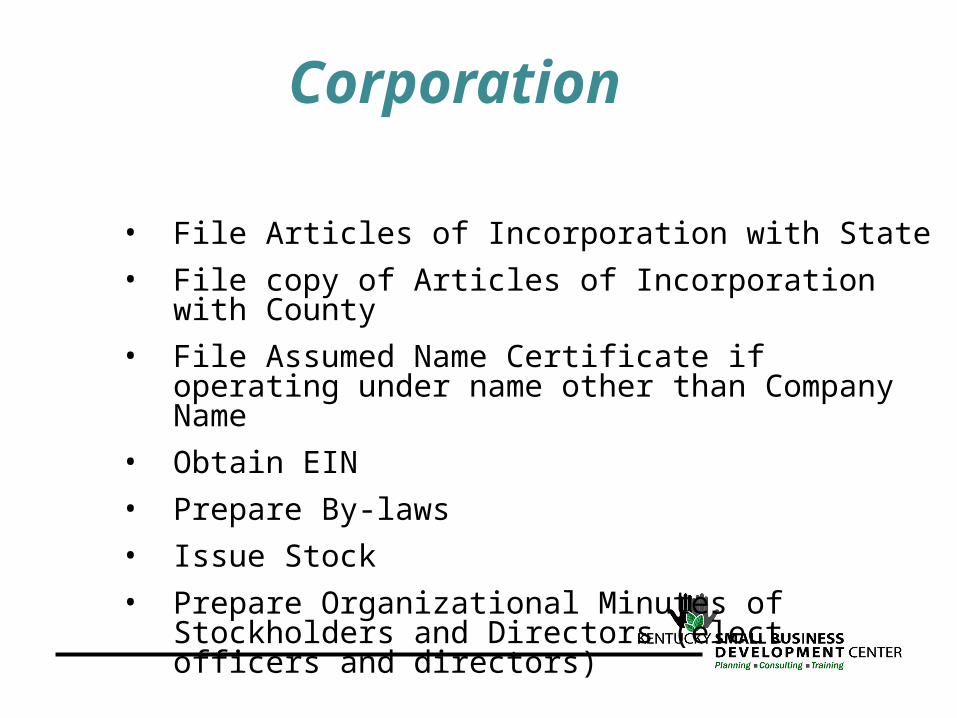

Corporation

• File Articles of Incorporation with State

• File copy of Articles of Incorporation with County

• File Assumed Name Certificate if operating under name other than Company Name

• Obtain EIN

• Prepare By-laws

• Issue Stock

• Prepare Organizational Minutes of Stockholders and Directors (elect officers and directors)

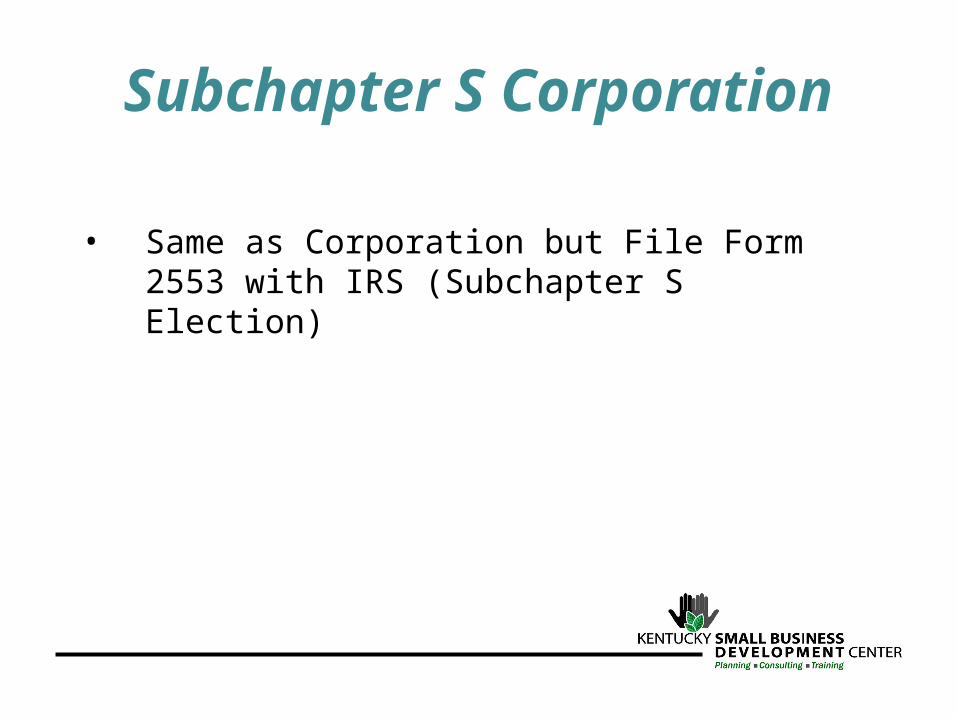

Subchapter S Corporation

• Same as Corporation but File Form 2553 with IRS (Subchapter S Election)

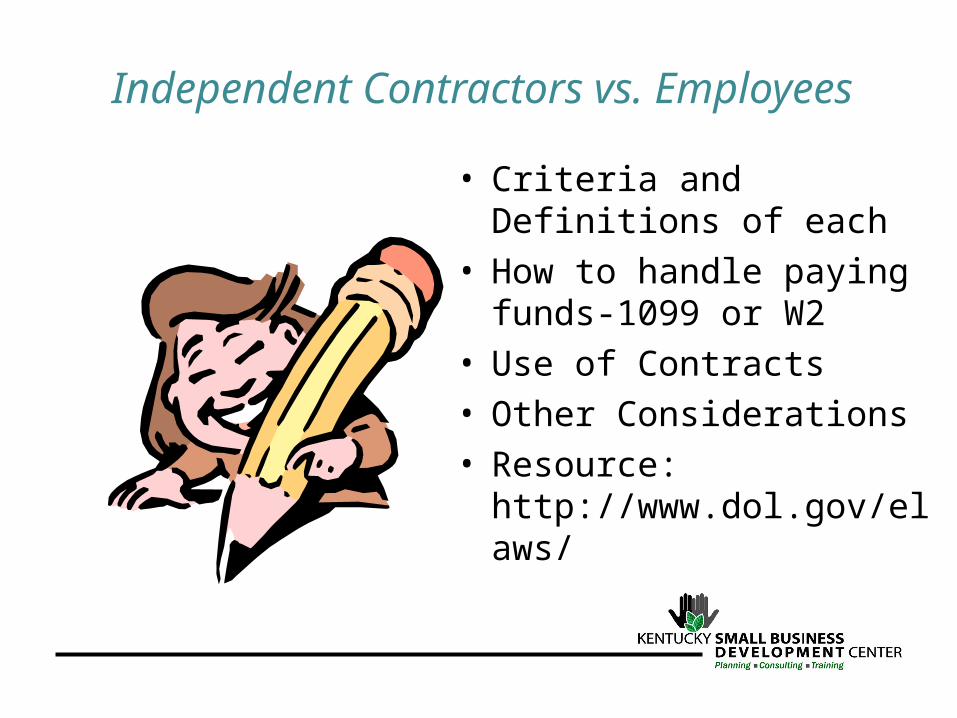

Independent Contractors vs. Employees

• Criteria and Definitions of each

• How to handle paying funds-1099 or W2

• Use of Contracts

• Other Considerations

• Resource: http://www.dol.gov/elaws/

Feasibility

Is Small Business

Ownership for You?

Personal Considerations

• Access your readiness to be a business owner

• Take the SBA Readiness Assessment http://web.sba.gov/sbtn/sbat/index.cfm?Tool=4

• Develop a household budget to examine how the business will effect personal finances

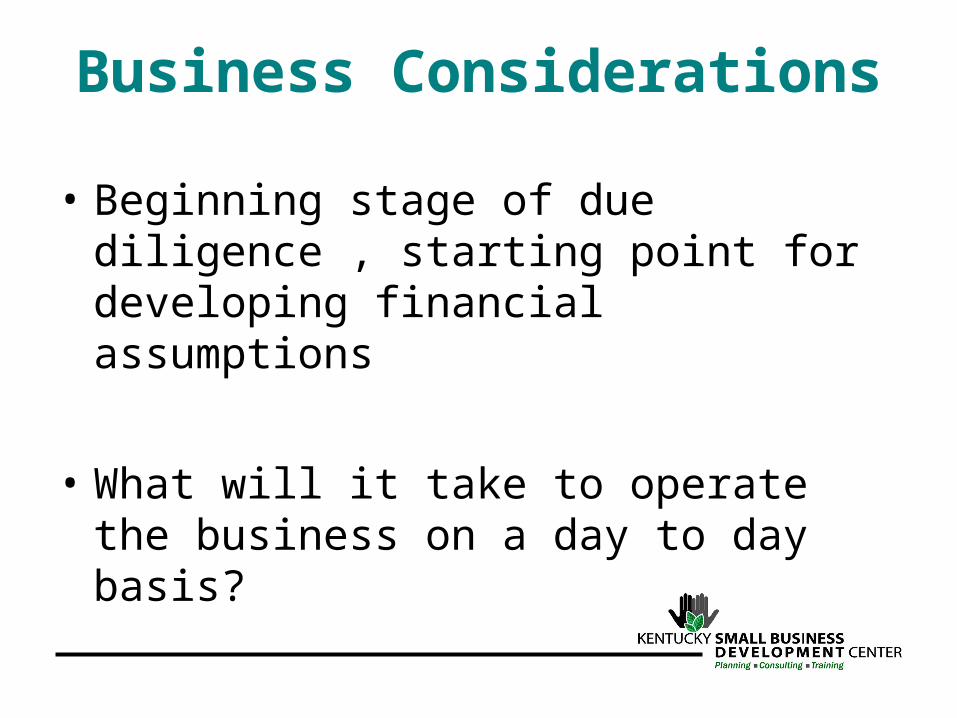

Business Considerations

• Beginning stage of due diligence , starting point for developing financial assumptions

• What will it take to operate the business on a day to day basis?

Market Factors Market Factors

Research and be able to answer:

1.Who is your target customer?

2.Who are your competitors?

3.What trends are taking place in your industry?

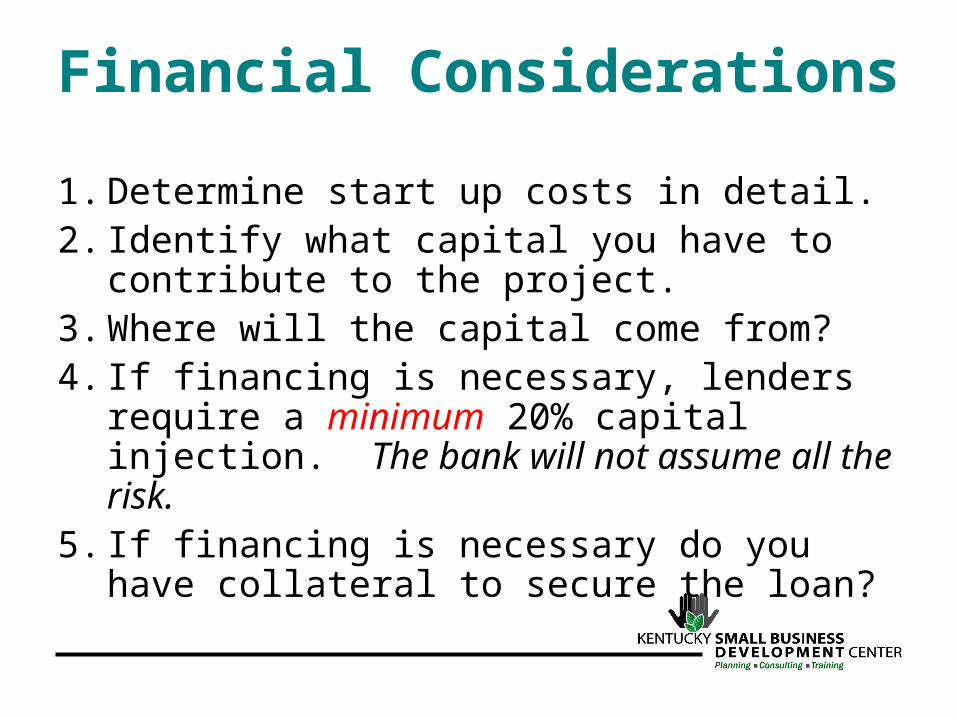

Financial Considerations

1. Determine start up costs in detail.2. Identify what capital you have to contribute

to the project. 3. Where will the capital come from? 4. If financing is necessary, lenders require a

minimum 20% capital injection. The bank will not assume all the risk.

5. If financing is necessary do you have collateral to secure the loan?

Development of a business plan to test overall feasibility is strongly

advised!

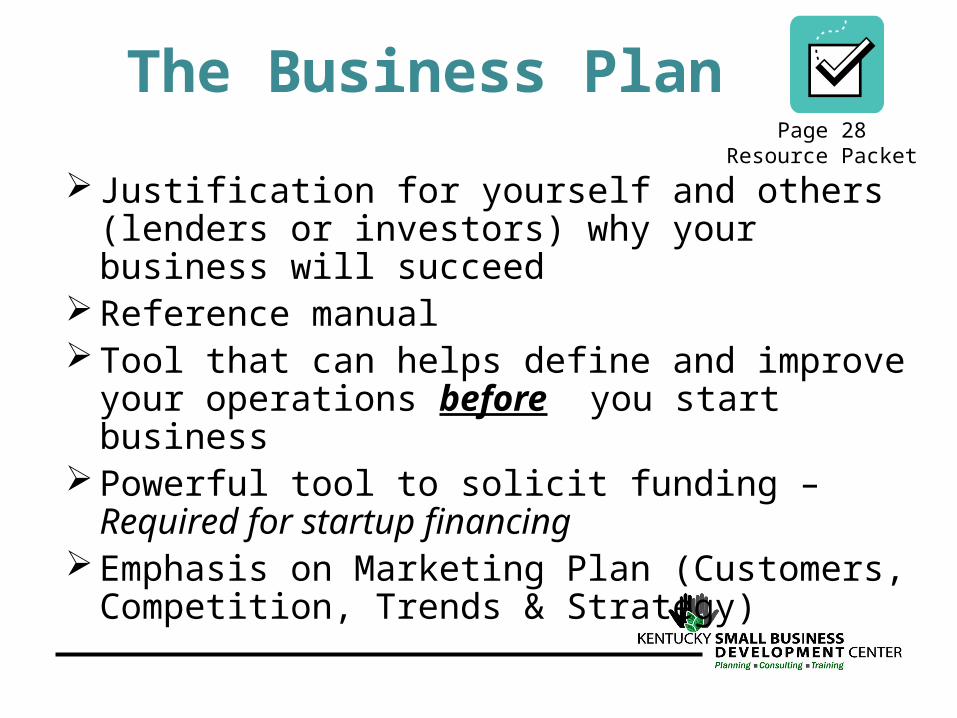

The Business Plan

Justification for yourself and others (lenders or investors) why your business will succeed

Reference manual Tool that can helps define and improve your

operations before you start business Powerful tool to solicit funding – Required for

startup financing Emphasis on Marketing Plan (Customers,

Competition, Trends & Strategy)

Page 28Resource Packet

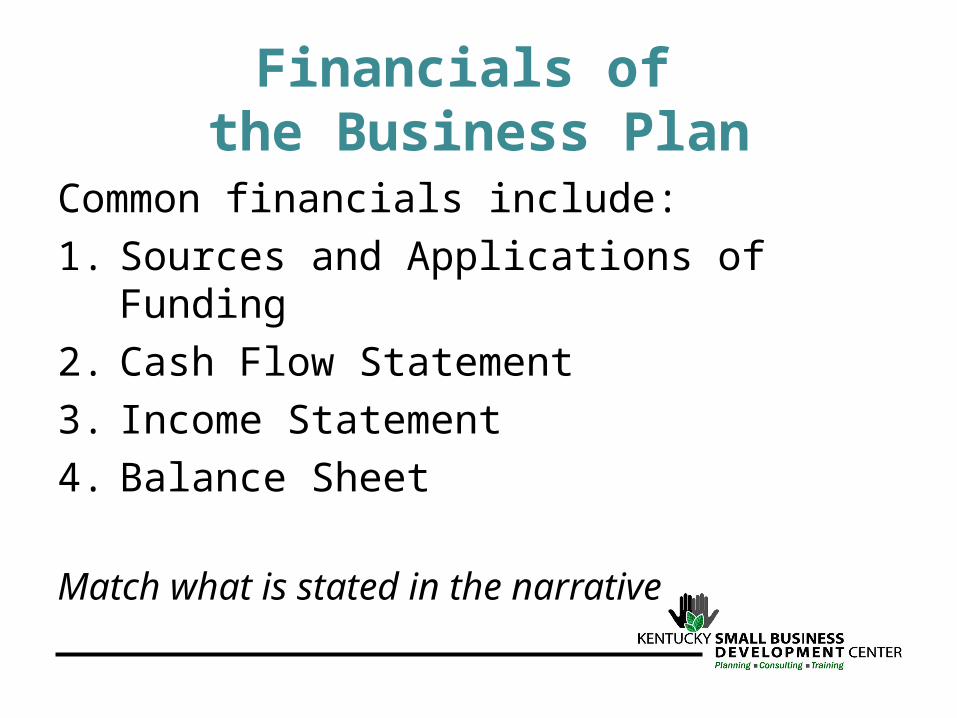

Financials of the Business Plan

Common financials include:

1. Sources and Applications of Funding

2. Cash Flow Statement

3. Income Statement

4. Balance Sheet

Match what is stated in the narrative

Steps to Creating a Business

The “How”

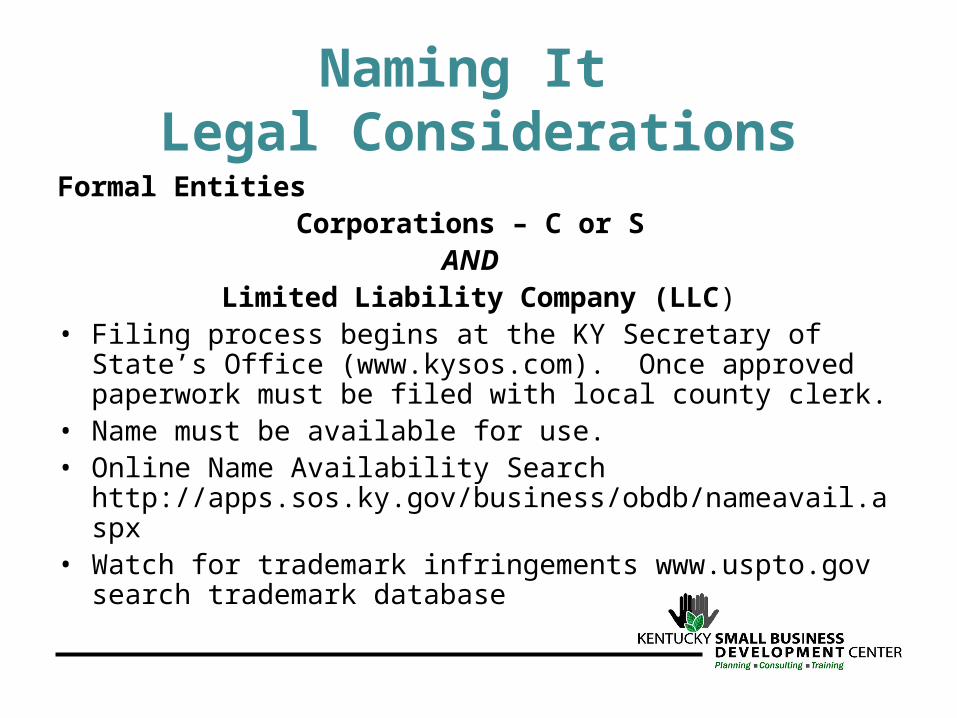

Naming It Legal Considerations

Formal EntitiesCorporations – C or S

AND Limited Liability Company (LLC)

• Filing process begins at the KY Secretary of State’s Office (www.kysos.com). Once approved paperwork must be filed with local county clerk.

• Name must be available for use. • Online Name Availability Search

http://apps.sos.ky.gov/business/obdb/nameavail.aspx • Watch for trademark infringements www.uspto.gov search

trademark database

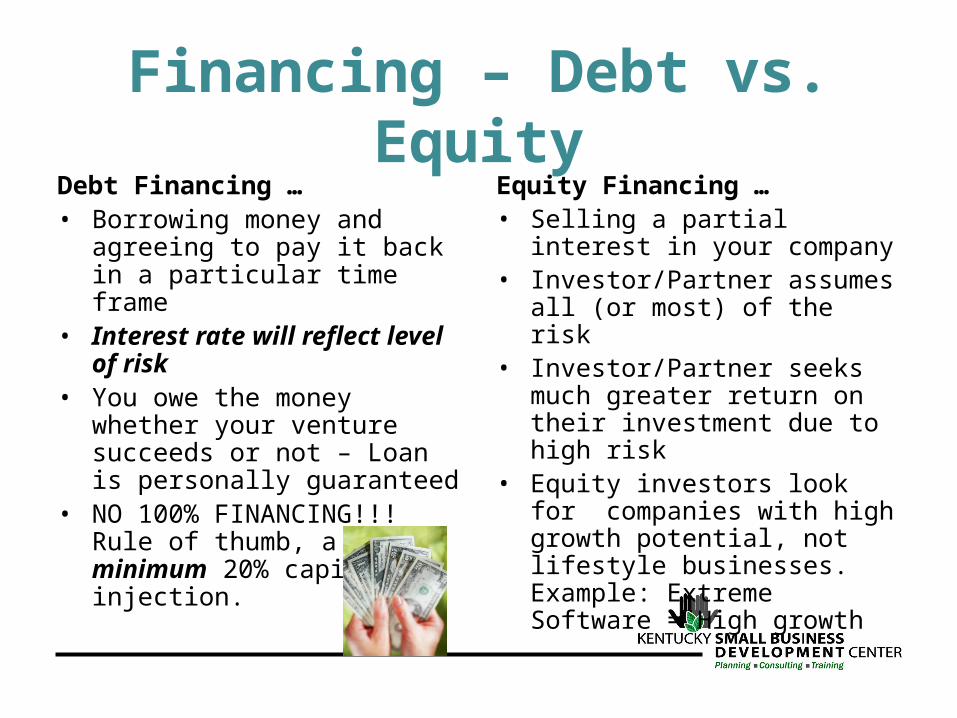

Financing – Debt vs. Equity

Debt Financing …• Borrowing money and

agreeing to pay it back in a particular time frame

• Interest rate will reflect level of risk

• You owe the money whether your venture succeeds or not – Loan is personally guaranteed

• NO 100% FINANCING!!! Rule of thumb, a minimum 20% capital injection.

Equity Financing …• Selling a partial interest in

your company• Investor/Partner assumes

all (or most) of the risk• Investor/Partner seeks

much greater return on their investment due to high risk

• Equity investors look for companies with high growth potential, not lifestyle businesses. Example: Extreme Software = High growth

What the bank looks for … 5 c’s + experience

1. Conditions – Market conditions, industry trends

2. Character/Credit – Personal credit history (know your score)

3. Capital – Cash you are willing to invest 4. Cash Flow Capacity – Repayment ability of

the business5. Collateral – Assets to secure the loan6. Experience – Industry experience

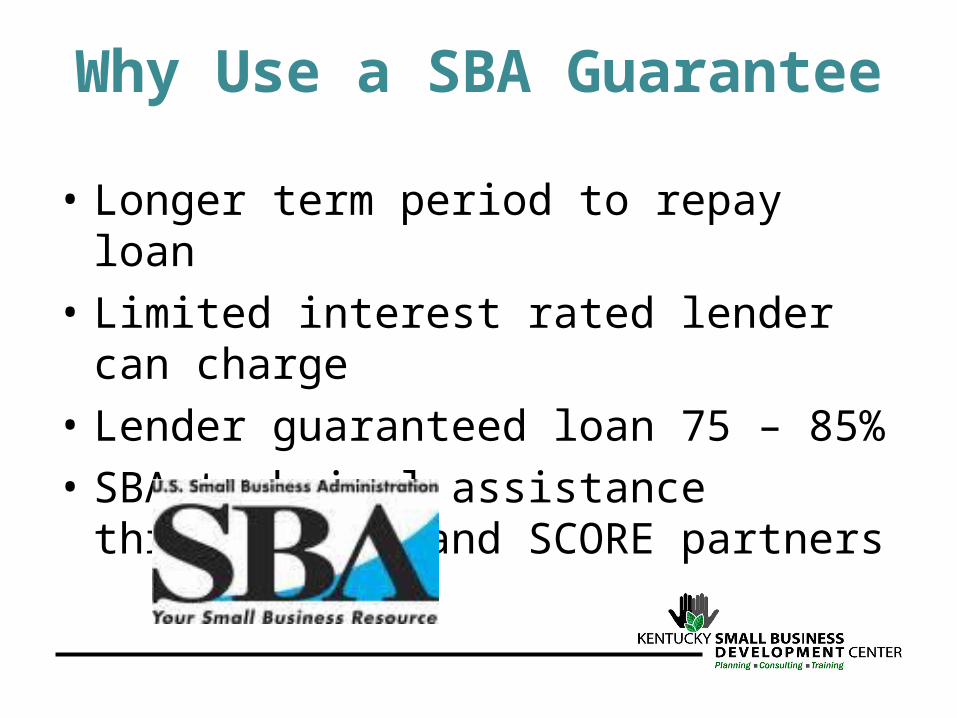

Why Use a SBA Guarantee

• Longer term period to repay loan

• Limited interest rated lender can charge

• Lender guaranteed loan 75 – 85%

• SBA technical assistance through SBDC and SCORE partners

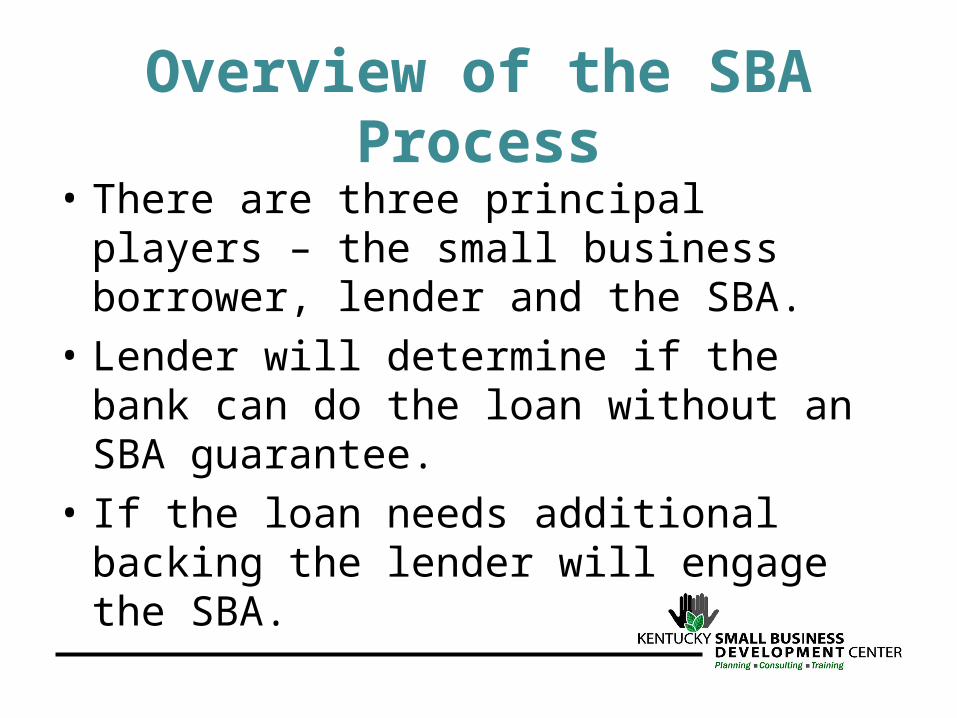

Overview of the SBA Process

• There are three principal players – the small business borrower, lender and the SBA.

• Lender will determine if the bank can do the loan without an SBA guarantee.

• If the loan needs additional backing the lender will engage the SBA.

Overview of SBA Products

Depending on your need there is a guarantee program to fit your needs. Commonly used programs at a glance.

1. 7(a) Guarantee Program

2. Community Express

3. 504 Program

4. Patriot ExpressNOTE: Other programs exists.

Page 37Resource Packet

Our service areaOur service areaAnderson , Bourbon , Boyle , Clark , Fayette , Franklin , Anderson , Bourbon , Boyle , Clark , Fayette , Franklin ,

Harrison , Jessamine , Mercer , Nicholas , Powell , Scott , WoodfordHarrison , Jessamine , Mercer , Nicholas , Powell , Scott , Woodford

Bluegrass SBDCBluegrass SBDC330 East Main Street, Suite 210330 East Main Street, Suite 210

Lexington, KY 40507Lexington, KY 40507Phone: 859.257.7666 or 1.888.475.SBDCPhone: 859.257.7666 or 1.888.475.SBDC

[email protected] [email protected] www.ksbdc.org www.ksbdc.org