Embed Size (px)

Citation preview

Sept. 21-23, 2011 • Ft. Lauderdale

2010 - 2011 Accounting Shows Committee

Christine Moreno - ChairLynn H. Clements - Vice Chair

26th Annual Accounting Show September 21-23, 2011

Ft. Lauderdale

12:45-1:35pm Keynote Address: Blue Ribbon Panel on ...................1Private Company Accounting

Keynote Address: Blue Ribbon Panel on Private Company

Accounting

Hubert D. Glover, CRISC, CMA, CIA, CPA, PhD

Hubert D. Glover, CRISC, CIA, CMA, CPA, PhD Clinical Associate Professor / Senior Partner

Drexel University / REDE Inc. Dr. Glover recently joined the faculty at Drexel University LeBow College of Business as a Clinical Associate Professor. Dr. Glover also serves as Chairman and co-founder of REDE Inc. (www.rede-inc.com) established in 1998 and provides institutional support and consulting services to federal agencies including NASA, USDA, Commerce, EPA and Department of Energy. REDE has an employee base of more than 250 employees providing IT and administrative support services from California to Florida. REDE was recognized in 2010 as the Houston Minority Supplier Development Council Strategic Teaming Company of the Year, and recognized in 2010 as NASA Kennedy Space Center Small Prime Contractor of the Year, recognized in 2007 and 2009 as the NASA Johnson Space Center Minority Contractor of the Year and 2007 and 2009; Texas A&M # 1 Aggie 100 Winner based on three year compound growth and in 2008 one of the Houston Minority Business Council Emerging 10 Business Winners. Dr. Glover has more than 30 years experience in management and leadership. This includes both the private sectors where his leadership roles included tenure as a CEO of a joint venture with Shell Oil and as a CEO for a subsidiary of PricewaterhouseCoopers. Dr. Glover’s leadership portfolio also included the public sectors serving as the chair of the accounting department for the School of Business at Howard University (both accredited by the AACSB) and leading small businesses to provide services for major federal agencies such as DOE and NASA. Dr. Glover currently serves on the Board of Directors for the Institute of Management Accountants (IMA) (www.imanet.org). He also recently completed service on the Blue Ribbon Panel for Private Company Standard Setting (AICPA/FAF/NASBA) which presented its recommendations to FAF in February 2011. Dr. Glover just completed terms as a member of the Board of Directors for the American Institute of Certified Public Accountants (AICPA) (www.aicpa.org) and IMA’s Foundation for Applied Research, and a terms as Council-at-large for the American Accounting Association (AAA) (http://aaahq.org/). Dr. Glover also served as the Chair of Audit Committee for a publicly traded company, Modavox (www.modavox.com) from 2003 to 2008 and for the Emmaus Services for the Aging (www.emmausservices.org) from 2007 to 2009. Dr. Glover has written more than 35 articles for trade publications, professional organizations and academic journals in the areas of organizational change, auditing and business education. Dr. Glover is also a Certified in Risk Information Systems Control, Certified Internal Auditor, Certified Management Accountant and Certified Public Accountant.

26th Annual Accounting ShowSeptember 21, 2011

Blue Ribbon Panel Recommendations

Presented by Hubert D. Glover, CRISC, CIA, CMA, CPA, Ph.D.Clinical Associate Professor at Drexel University

&Senior Partner at REDE Inc.

AGENDA

Blue Ribbon Panel RecommendationsHistorical concerns of privately held companiesPerfect storm for Blue Ribbon PanelBlue Ribbon Panel OverviewRecommendationsNext steps

Commentary – Open Discussion

HISTORY OF PRIVATE COMPANY REPORTING

Historically accounting standards and instruction reflected the nature of the economy during the early 1990s which was in the midst of the industrial revolutionThe passage of the Securities Acts of 1933 and 1933 led to the formalization and growth of the public accounting profession and initiated efforts toward a more comprehensive standard setting processHowever, the focus of the Securities Acts was publicly traded companies which was in response—no different than Sarbanes Oxley Act seventy years later—to the crash of 1929The agreement to transition after the Wheat Committee from the Accounting Principles Board to FASB in 1973 allowed the retention of the self regulatory model but the emphasis was on capital marketsThe backgrounds of the FASB board has been dominated by financial experts with a public company experience and only in 2011 the appointments of two new board members had emphasis on private company experience

OVERVIEW OF PREPARER MARKET

15,000 issuers vs. 28.5 million private companies, but GAAP driven by public company issues.Small businesses employ more than half of all private sector workers.Private companies and their financial statement users have information needs different from public companies.

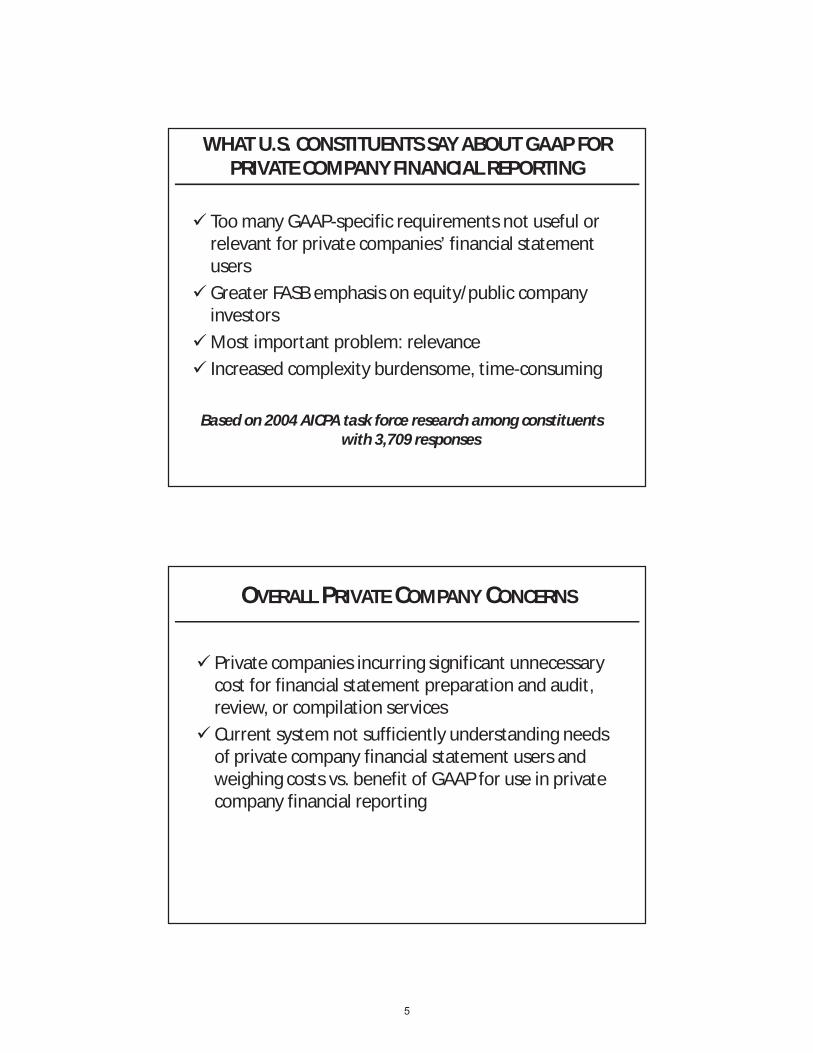

WHAT U.S. CONSTITUENTS SAY ABOUT GAAP FOR PRIVATE COMPANY FINANCIAL REPORTING

Too many GAAP-specific requirements not useful or relevant for private companies’ financial statement usersGreater FASB emphasis on equity/public company investorsMost important problem: relevanceIncreased complexity burdensome, time-consuming

Based on 2004 AICPA task force research among constituents with 3,709 responses

OVERALL PRIVATE COMPANY CONCERNS

Private companies incurring significant unnecessary cost for financial statement preparation and audit, review, or compilation servicesCurrent system not sufficiently understanding needs of private company financial statement users and weighing costs vs. benefit of GAAP for use in private company financial reporting

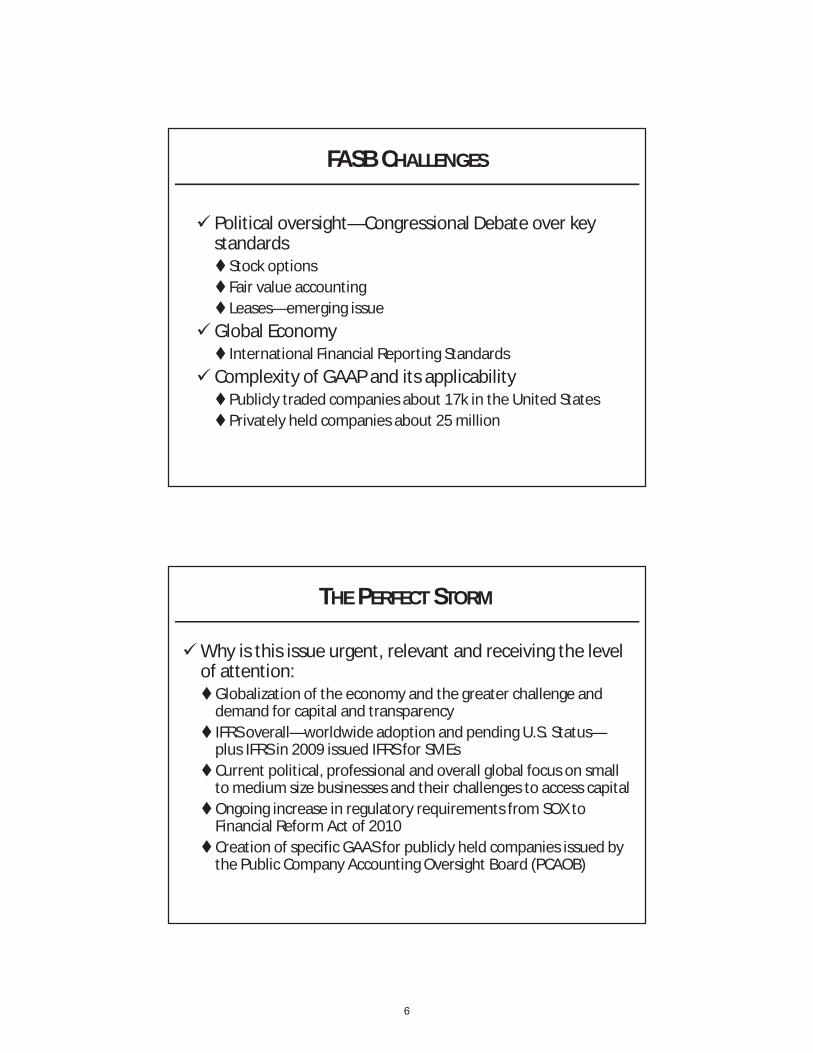

FASB CHALLENGES

Political oversight—Congressional Debate over key standards

Stock optionsFair value accountingLeases—emerging issue

Global EconomyInternational Financial Reporting Standards

Complexity of GAAP and its applicabilityPublicly traded companies about 17k in the United StatesPrivately held companies about 25 million

THE PERFECT STORM

Why is this issue urgent, relevant and receiving the level of attention:

Globalization of the economy and the greater challenge and demand for capital and transparencyIFRS overall—worldwide adoption and pending U.S. Status—plus IFRS in 2009 issued IFRS for SMEs Current political, professional and overall global focus on small to medium size businesses and their challenges to access capitalOngoing increase in regulatory requirements from SOX to Financial Reform Act of 2010 Creation of specific GAAS for publicly held companies issued by the Public Company Accounting Oversight Board (PCAOB)

WHAT DO YOU THINK?

Should there be a separate GAAP for Not for Profits, Government, Publicly Owned Companies and Privately Owned Companies?What is the appropriate oversight model?

Separate boards all under FAF like FASB and GASBSeparate organizationsOne size fits all GAAP under FASB or GASBOther models

COLLABORATING PARTNERS OF BLUE RIBBON PANEL

AICPA www.aicpa.org

Financial Accounting Foundation (www.accountingfoundation.org )

NASBA, (www.nasba.org)

Financial Accounting Foundation (FAF)National Association of State Boards of Accounting (NASBA)American Institute of Certified Public Accountants (AICPA)

OVERVIEW OF BLUE RIBBON PANEL

MissionAddress how accounting standards can best meet the needs of users of U.S. private company financial statements

GoalProvide recommendation on private company standard setting to the Financial Accounting Foundation (FAF)

ObjectivesReview prior studies, models in other countries and listen to comments from private company representatives on Panel as well as from regulatory agencies and key users such as banks and venture capital funds and surety companies

PANEL REPRESENTATION & OBSERVERS

18 panel members representing a cross section of large, medium and small private companies, accounting firms, professional accounting organizations, community banks, larger banks and venture capital fundsSeveral guest speakers and observers representing an array of federal regulatory agencies as well as key financial institutions who provided input but did not have a vote on recommendations—observers also included members from FASB including the new chair, Leslie Seidman

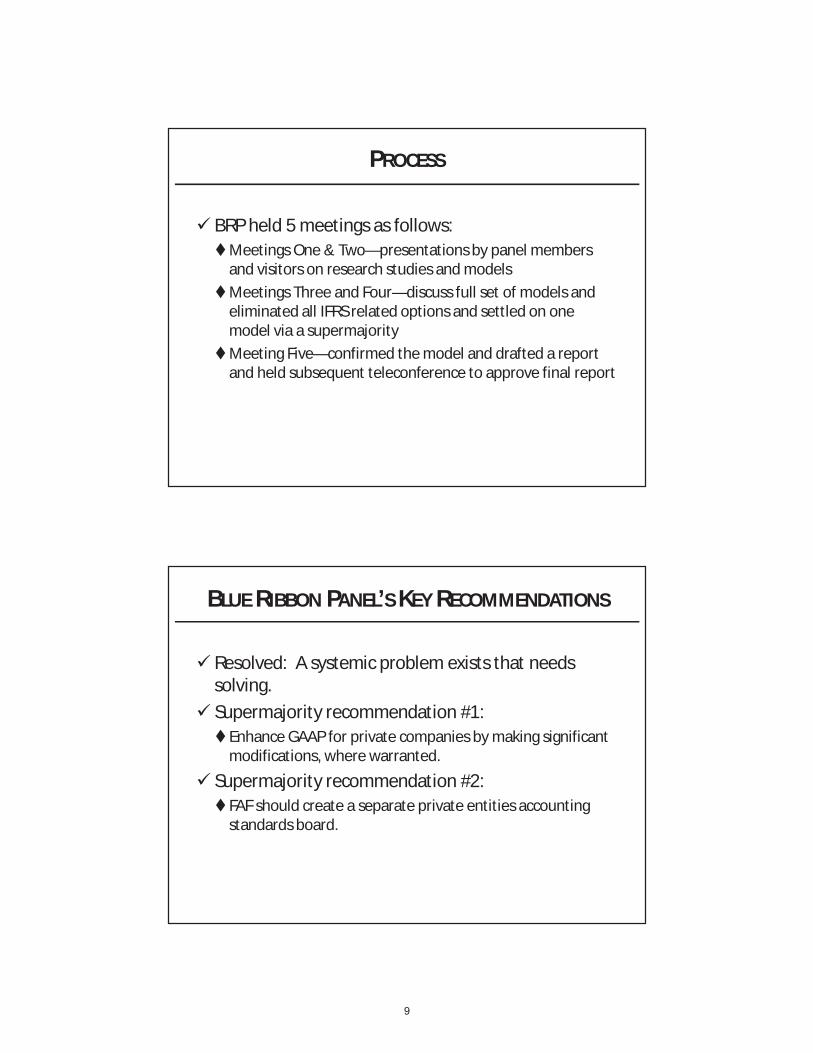

PROCESS

BRP held 5 meetings as follows:Meetings One & Two—presentations by panel members and visitors on research studies and modelsMeetings Three and Four—discuss full set of models and eliminated all IFRS related options and settled on one model via a supermajorityMeeting Five—confirmed the model and drafted a report and held subsequent teleconference to approve final report

BLUE RIBBON PANEL’S KEY RECOMMENDATIONS

Resolved: A systemic problem exists that needs solving.Supermajority recommendation #1:

Enhance GAAP for private companies by making significant modifications, where warranted.

Supermajority recommendation #2:FAF should create a separate private entities accounting standards board.

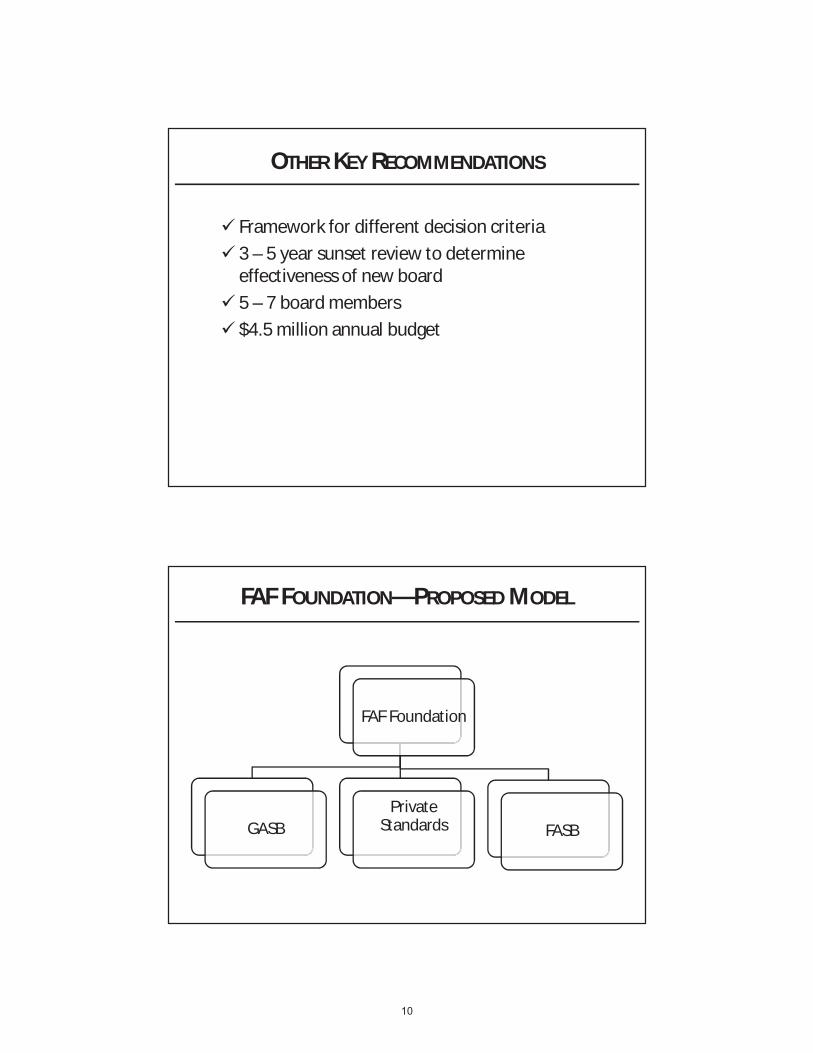

OTHER KEY RECOMMENDATIONS

Framework for different decision criteria3 – 5 year sunset review to determine effectiveness of new board5 – 7 board members$4.5 million annual budget

FAF FOUNDATION—PROPOSED MODEL

FAF Foundation

FASBPrivate

StandardsGASB

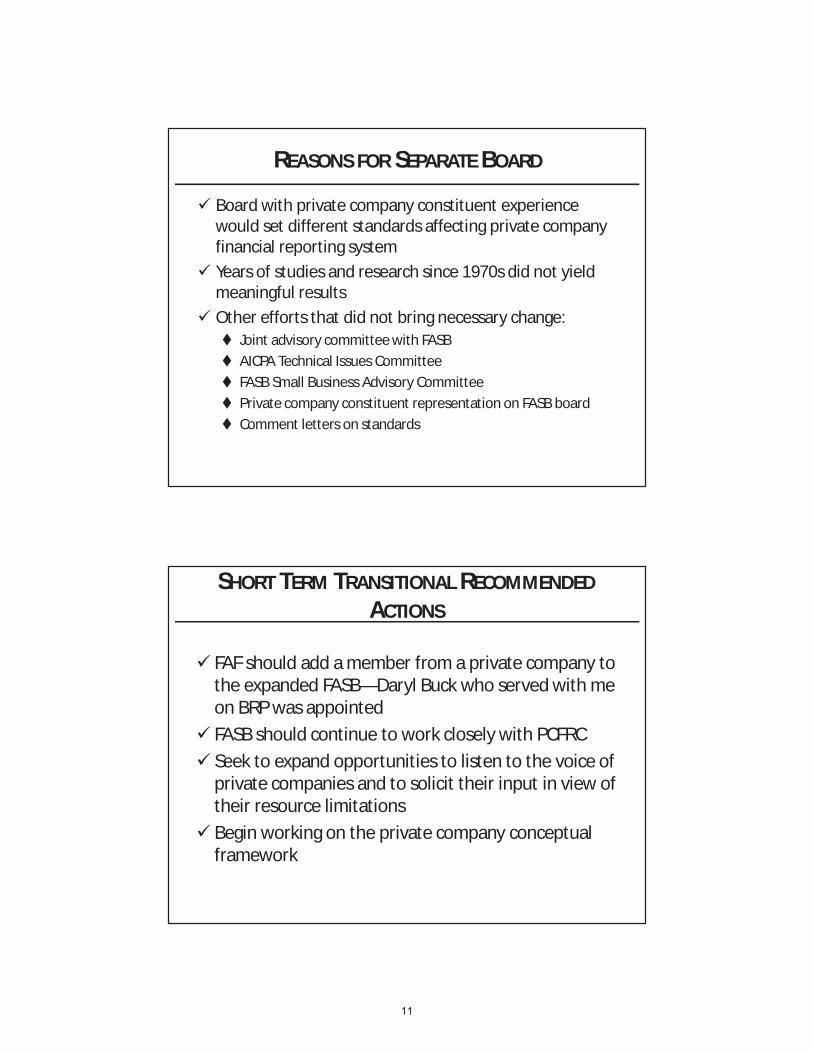

REASONS FOR SEPARATE BOARD

Board with private company constituent experience would set different standards affecting private company financial reporting systemYears of studies and research since 1970s did not yield meaningful results Other efforts that did not bring necessary change:

Joint advisory committee with FASBAICPA Technical Issues CommitteeFASB Small Business Advisory CommitteePrivate company constituent representation on FASB boardComment letters on standards

SHORT TERM TRANSITIONAL RECOMMENDEDACTIONS

FAF should add a member from a private company to the expanded FASB—Daryl Buck who served with me on BRP was appointedFASB should continue to work closely with PCFRCSeek to expand opportunities to listen to the voice of private companies and to solicit their input in view of their resource limitationsBegin working on the private company conceptual framework

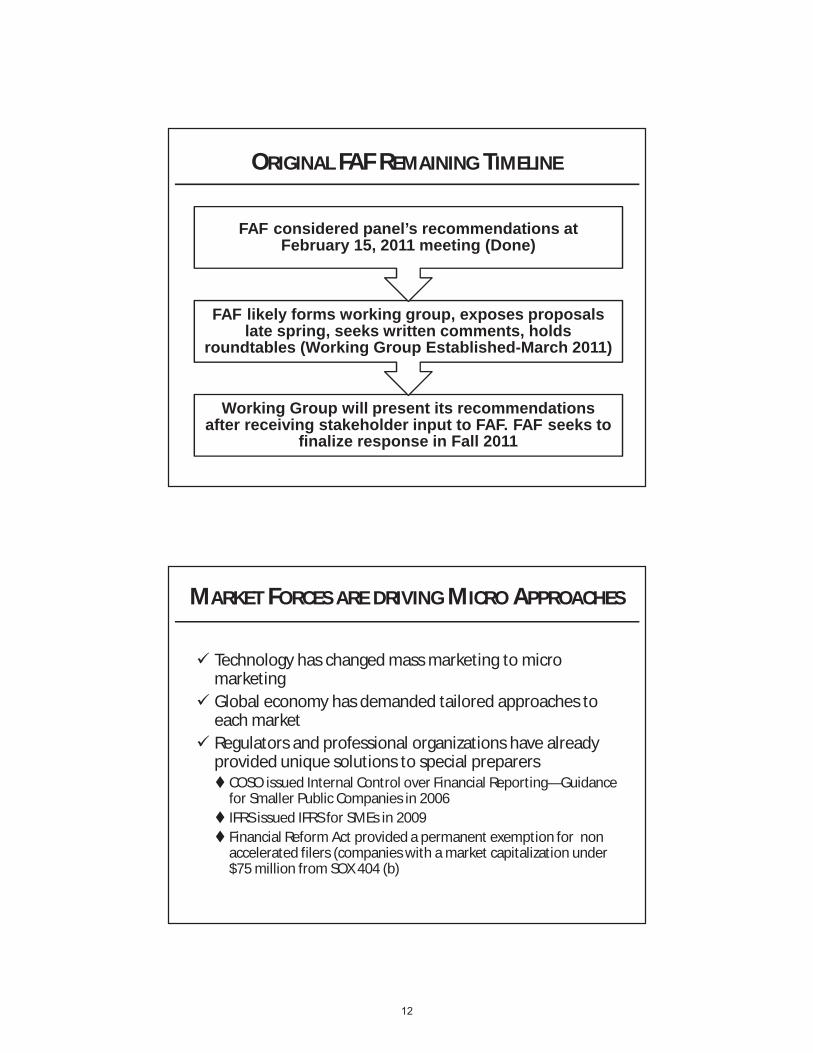

ORIGINAL FAF REMAINING TIMELINE

Working Group will present its recommendations after receiving stakeholder input to FAF. FAF seeks to

finalize response in Fall 2011

FAF likely forms working group, exposes proposals late spring, seeks written comments, holds

roundtables (Working Group Established-March 2011)

FAF considered panel’s recommendations at February 15, 2011 meeting (Done)

MARKET FORCES ARE DRIVING MICRO APPROACHES

Technology has changed mass marketing to micro marketingGlobal economy has demanded tailored approaches to each marketRegulators and professional organizations have already provided unique solutions to special preparers

COSO issued Internal Control over Financial Reporting—Guidance for Smaller Public Companies in 2006IFRS issued IFRS for SMEs in 2009Financial Reform Act provided a permanent exemption for non accelerated filers (companies with a market capitalization under $75 million from SOX 404 (b)

RESOURCES

Blue Ribbon Panel FAF www.financialaccountingfoundation.org

Learn more about membership. | [email protected] | www.ficpa.org(800) 342-3197 (in Florida) | (850) 224-2727

“ I renew because of the invaluable networking opportunities that being a member of the F ICPA provides. From being involved with your local chapter to attending networking events, the F ICPA is an organization that is

known and respected across many industries.”

Monica Ospina, CPA, ABV, CFF Cherry, Bekaert & Holland, LLP

Coral Gables Member since 2007

“ I renew my F ICPA membership because of the signif icant access to education, current events, and the

networking it provides.”

Ray Monteleone, CPA President, Paladin Global Partners

Fort Lauderdale Member since 1979

“ Ibeced

“ I’m renewing my F ICPA membership because it keeps me professionally and socia lly connected to my fellow peers in the profession.”

David White, CPA Carr Riggs & Ingram LLC

Tallahassee Member since 2010

FICPA Membership: Connect, Learn and ThriveProud to be a Member

FLA

Who We AreThe FICPA has teamed up with the Business Learning Institute (BLI), a one stop shop that helps you to develop a custom learning solution which blends traditional classroom settings with modern tools such as webcasts, webinars and on-line classes.

This combination of traditional and modern training venues will allow your employees – from the highest level to entry level – the opportunity to participate in programs that cover everything from technical content to leadership, performance skills and technology.

The company that learns together,

earns together...

Let Us Show You How!

What We DoLet us guide you through the process of selecting the right curriculum for

identify topics that will be the next hot issue.

Have you heard about XBRL, Lean Accounting, International Financial Reporting

Why Us?

Who Uses Our Services? BLI has coordinated and tailored programs for the following international organizations:

For more information

Contact Carol Kearney at (800) 342-3197 (in Florida) or (850) 224-2727, Ext. 271

or e-mail .

(PLACE ON YOUR COMPANY’S LETTERHEAD)

Attention: Business Editor Contact: (CONTACT NAME) (CONTACT’S TITLE) (FIRM NAME) For Immediate Release Phone ____________________

E-Mail ____________________ (WEB ADDRESS, IF APPLICABLE)

(MEMBER’S NAME), CPA, Completes course on (SUBJECT AREA)

(MEMBER’S CITY), (DATE), 2011 -- _______(MEMBER’S FULL NAME___________,

CPA, of _____(FIRM NAME)______ in ________(CITY)______________________, completed a course,

“________(COURSE TITLE)______,” on ____(DATE) ____. This continuing-education course covered

the topic of_____________________(SUBJECT AREA)______________________.

___(MEMBER’S LAST NAME)_________ is a ______(POSITION TITLE)___________ practicing in the

area of (MEMBER’S AREA OF PRACTICE – TAS, AUDIT, ETC.) with the firm.

In addition to (MEMBER’S LAST NAME)’S professional responsibilities, HE/SHE is also active in (LIST

ANY OTHER PROFESSIONAL/CIVIC/ VOLUNTEER/COMMUNITY ACTIVIES – OPTIONAL). HE/SHE is

an active member of the Florida Institute of Certified Public Accountants, the professional association

representing the interests of more then 18,400 CPAs with over 4,400 offices throughout Florida.

(MEMBER NAME) can be reached by telephone at _____(PHONE NUMBER)____, or via e-mail at

_______(E-MAIL ADDRESS)_______.

###