Embed Size (px)

Citation preview

FSTAR 101:FSTAR 101:The Coast Guard’s Audit The Coast Guard’s Audit

Readiness PlanReadiness Plan

RDML K. Taylor | DHS CFO Brief | 25 JAN 2010

Assistant Assistant CommandantCommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

2

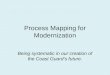

Coast Guard Financial Management

Principle Issues

CG accounting operations policies, procedures and processes which are not in accordance with Generally Accepted Accounting Principals (GAAP) standards

Multiple General Ledgers General Ledgers non-US Standard General Ledger (USSGL) Compliant Lack of a standard line of accounting

Unable to address the following major functional gaps in a cost-effective manner in the current environment: Centralized funds control Three-way matching of good receipt Payment management Automated processing of Intergovernmental Payments and Collections

(IPACs)

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

3

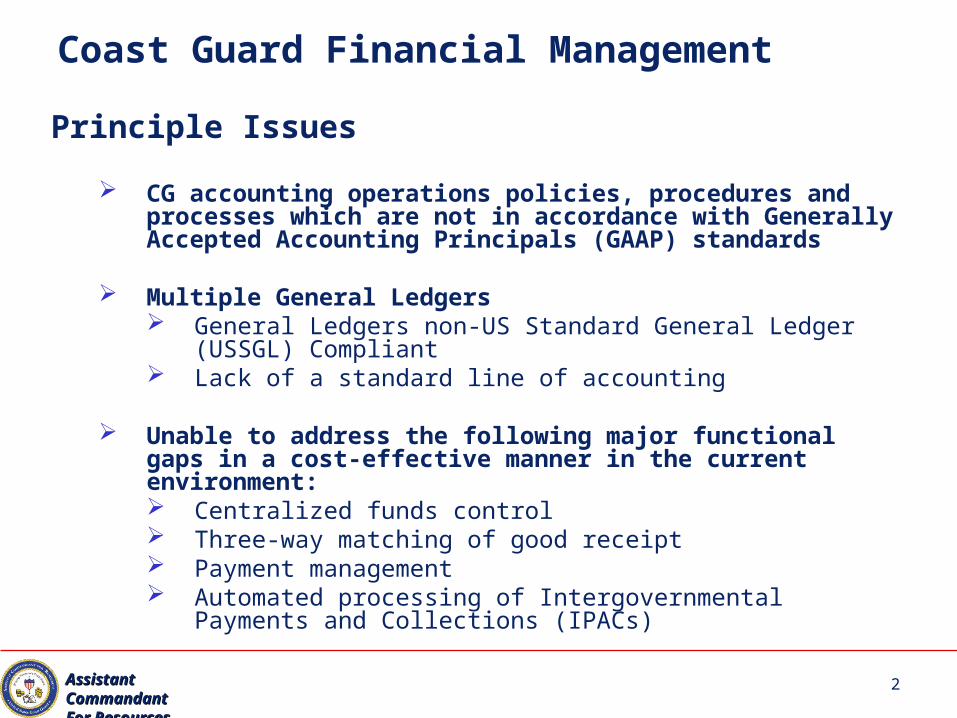

Size (Materiality) Matters

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

3

CG in DOT CG in DHS in 2010CG is 18% of DHS AssetsCG is 41% of DHS Liabilities

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

4

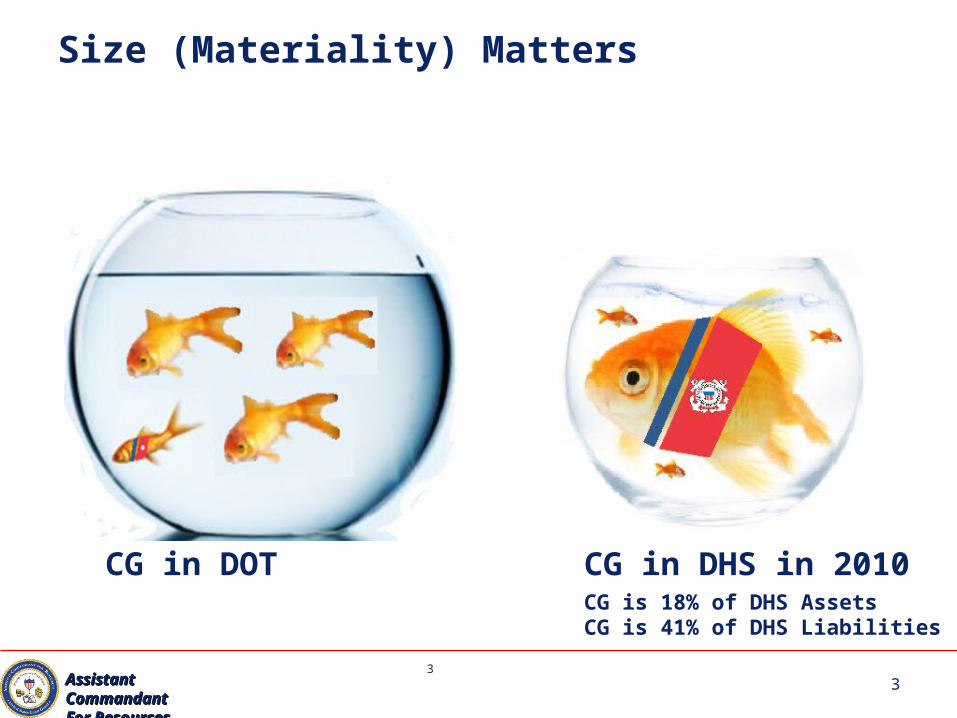

Coast Guard Audit Readiness Approach

Financial Management Modernization is the backbone of the Coast Guard Modernization Efforts are inextricably linked Marks a turning point for the USCG to achieve timely, accurate, reliable, visible and

transparent financial information Critical to decision makers

Must actively transform our financial management processes and systems using a deliberate phased approach.

We must: Consolidate financial management activities to create centers of expertise and

reduce potential internal control issues Establish a preeminent culture of internal controls Institutionalize a governance architecture to:

Enhance advocacy Provide optimal resource allocation Enable an enduring audit readiness posture

4Assistant CommandantAssistant CommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

5

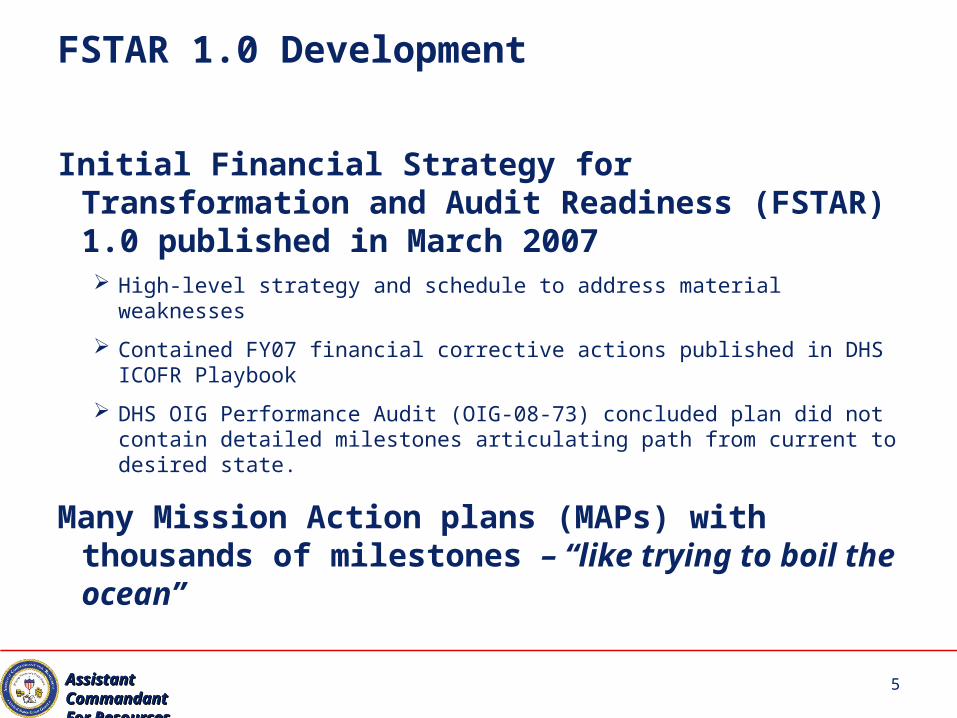

FSTAR 1.0 Development

Initial Financial Strategy for Transformation and Audit Readiness (FSTAR) 1.0 published in March 2007 High-level strategy and schedule to address material weaknesses

Contained FY07 financial corrective actions published in DHS ICOFR Playbook

DHS OIG Performance Audit (OIG-08-73) concluded plan did not contain detailed milestones articulating path from current to desired state.

Many Mission Action plans (MAPs) with thousands of milestones – “like trying to boil the ocean”

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

6

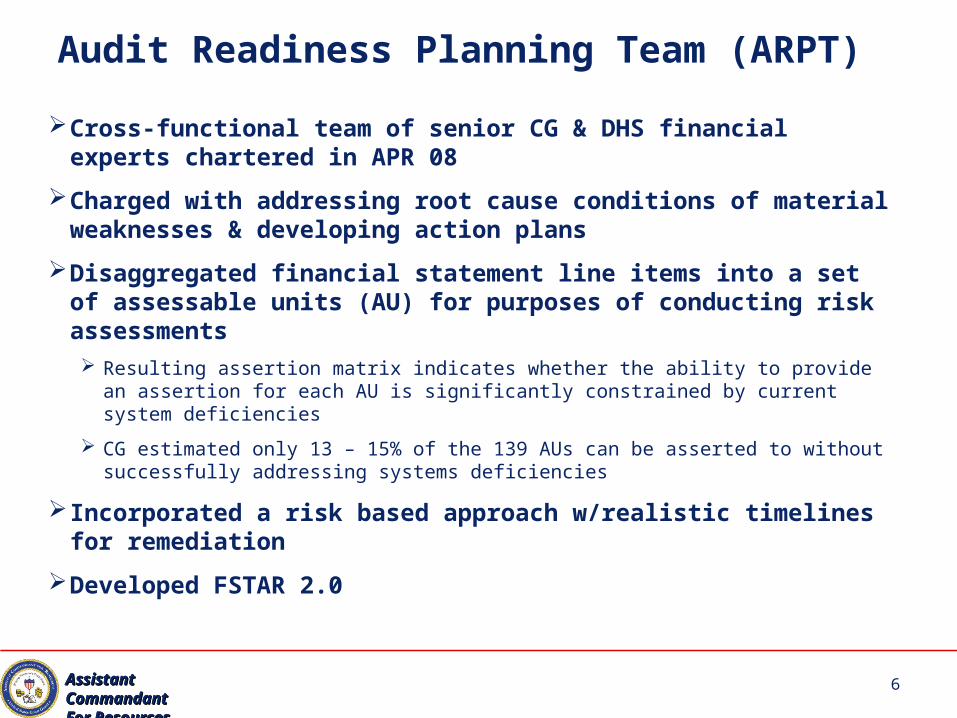

Audit Readiness Planning Team (ARPT)

Cross-functional team of senior CG & DHS financial experts chartered in APR 08

Charged with addressing root cause conditions of material weaknesses & developing action plans

Disaggregated financial statement line items into a set of assessable units (AU) for purposes of conducting risk assessments Resulting assertion matrix indicates whether the ability to provide an assertion for each AU

is significantly constrained by current system deficiencies

CG estimated only 13 – 15% of the 139 AUs can be asserted to without successfully addressing systems deficiencies

Incorporated a risk based approach w/realistic timelines for remediation

Developed FSTAR 2.0

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

7

Coast Guard Audit Readiness Strategy

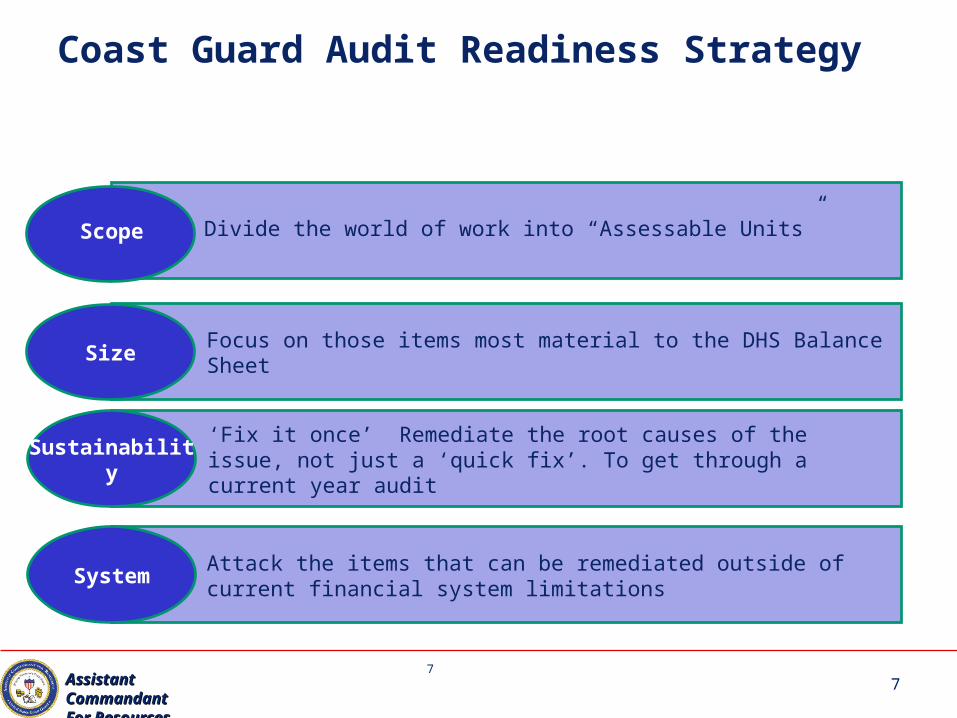

Size

Scope

System

Sustainability

Focus on those items most material to the DHS Balance Sheet

Attack the items that can be remediated outside of current financial system limitations

‘Fix it once’ Remediate the root causes of the issue, not just a ‘quick fix’. To get through a current year audit

7

Divide the world of work into “Assessable Units”

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

8

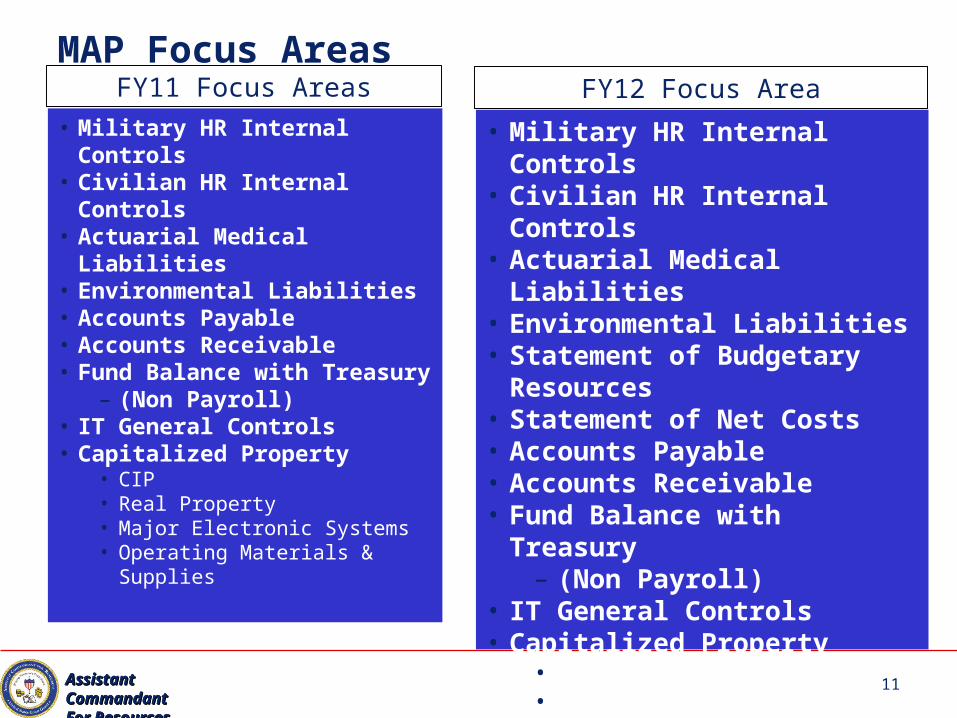

MAP Focus Areas

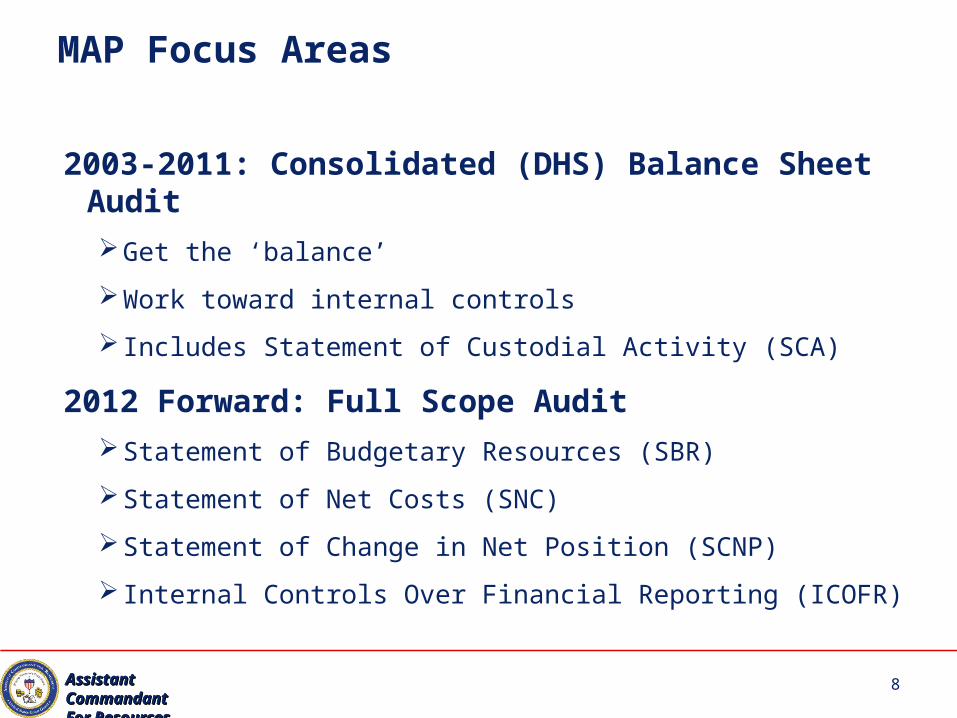

2003-2011: Consolidated (DHS) Balance Sheet Audit

Get the ‘balance’

Work toward internal controls

Includes Statement of Custodial Activity (SCA)

2012 Forward: Full Scope Audit

Statement of Budgetary Resources (SBR)

Statement of Net Costs (SNC)

Statement of Change in Net Position (SCNP)

Internal Controls Over Financial Reporting (ICOFR)

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

9

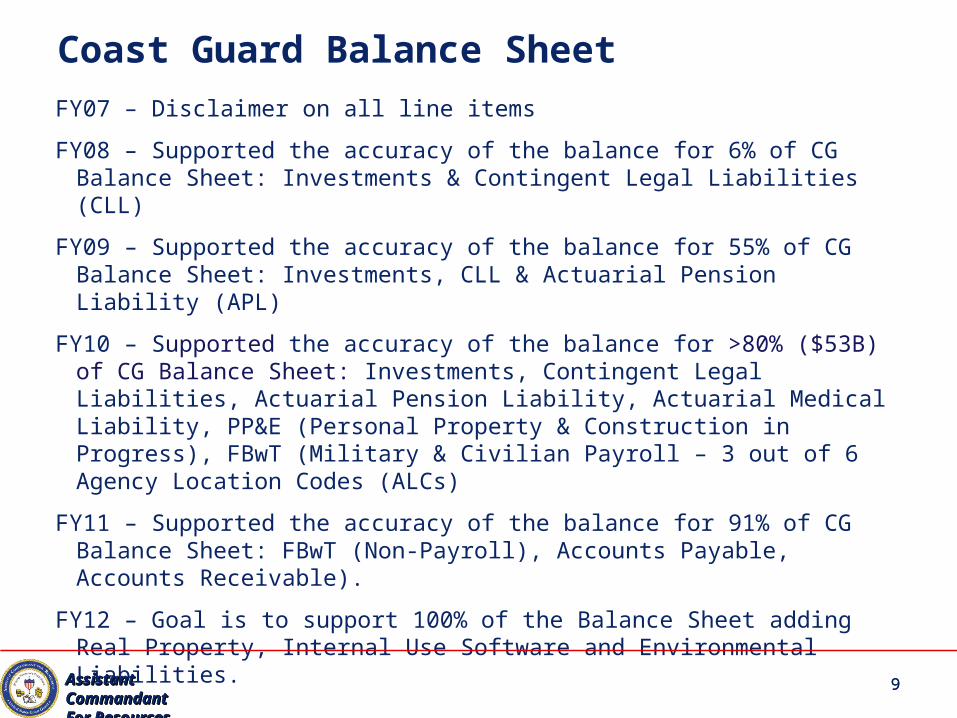

Coast Guard Balance Sheet

FY07 – Disclaimer on all line items

FY08 – Supported the accuracy of the balance for 6% of CG Balance Sheet: Investments & Contingent Legal Liabilities (CLL)

FY09 – Supported the accuracy of the balance for 55% of CG Balance Sheet: Investments, CLL & Actuarial Pension Liability (APL)

FY10 – Supported the accuracy of the balance for >80% ($53B) of CG Balance Sheet: Investments, Contingent Legal Liabilities, Actuarial Pension Liability, Actuarial Medical Liability, PP&E (Personal Property & Construction in Progress), FBwT (Military & Civilian Payroll – 3 out of 6 Agency Location Codes (ALCs)

FY11 – Supported the accuracy of the balance for 91% of CG Balance Sheet: FBwT (Non-Payroll), Accounts Payable, Accounts Receivable).

FY12 – Goal is to support 100% of the Balance Sheet adding Real Property, Internal Use Software and Environmental Liabilities.

9Assistant CommandantAssistant CommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

10

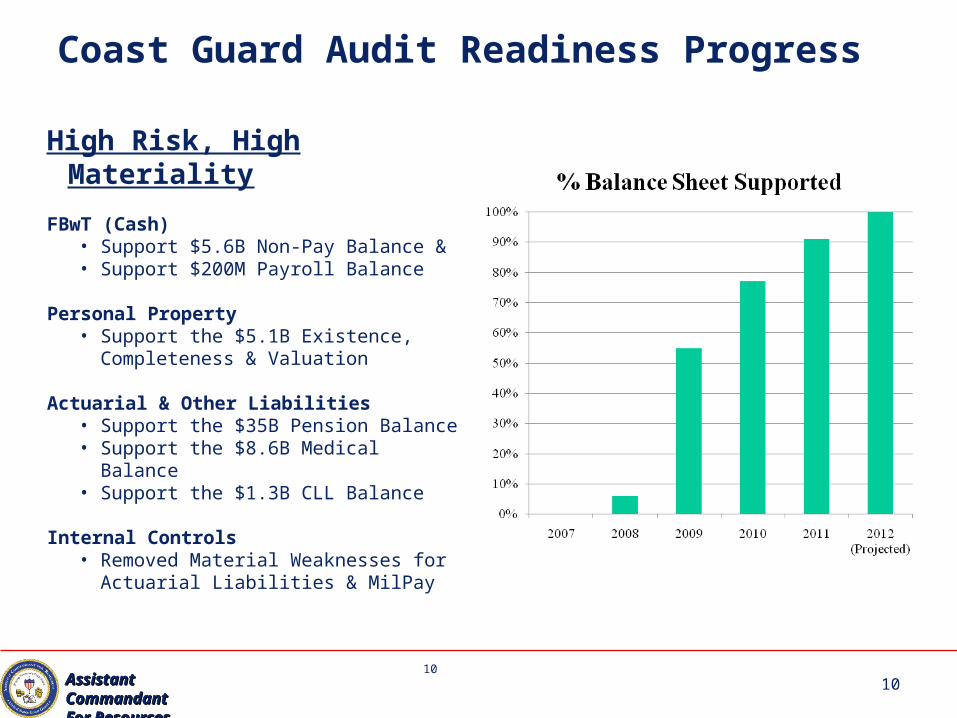

Coast Guard Audit Readiness Progress

High Risk, High Materiality

FBwT (Cash)• Support $5.6B Non-Pay Balance &• Support $200M Payroll Balance

Personal Property• Support the $5.1B Existence,

Completeness & Valuation

Actuarial & Other Liabilities• Support the $35B Pension Balance• Support the $8.6B Medical Balance• Support the $1.3B CLL Balance

Internal Controls• Removed Material Weaknesses for

Actuarial Liabilities & MilPay

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

10

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

11

MAP Focus Areas

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

• Military HR Internal Controls• Civilian HR Internal Controls• Actuarial Medical Liabilities• Environmental Liabilities• Accounts Payable• Accounts Receivable• Fund Balance with Treasury

– (Non Payroll)• IT General Controls• Capitalized Property

• CIP• Real Property• Major Electronic Systems• Operating Materials &

Supplies

FY11 Focus Areas

• Military HR Internal Controls• Civilian HR Internal Controls• Actuarial Medical Liabilities• Environmental Liabilities• Statement of Budgetary Resources• Statement of Net Costs• Accounts Payable• Accounts Receivable• Fund Balance with Treasury

– (Non Payroll)• IT General Controls• Capitalized Property

• Personal Property• CIP• Real Property• Major Electronic Systems• Operating Materials & Supplies

FY12 Focus Area

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

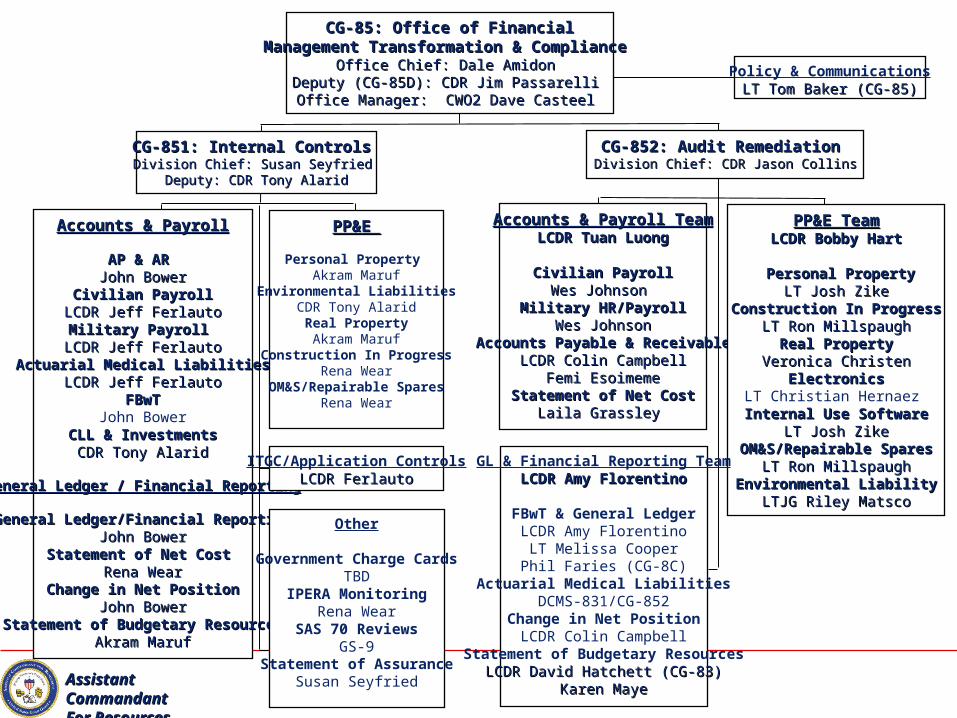

CG-85: Office of FinancialCG-85: Office of FinancialManagement Transformation & Compliance Management Transformation & Compliance

Office Chief: Dale Amidon Office Chief: Dale Amidon Deputy (CG-85D): CDR Jim Passarelli Deputy (CG-85D): CDR Jim Passarelli Office Manager: CWO2 Dave Casteel Office Manager: CWO2 Dave Casteel

CG-851: Internal Controls CG-851: Internal Controls Division Chief: Susan Seyfried Division Chief: Susan Seyfried

Deputy: CDR Tony AlaridDeputy: CDR Tony Alarid

CG-852: Audit Remediation CG-852: Audit Remediation Division Chief: CDR Jason CollinsDivision Chief: CDR Jason Collins

Accounts & Payroll TeamAccounts & Payroll TeamLCDR Tuan LuongLCDR Tuan Luong

Civilian PayrollCivilian PayrollWes Johnson Wes Johnson

Military HR/PayrollMilitary HR/PayrollWes JohnsonWes Johnson

Accounts Payable & ReceivableAccounts Payable & ReceivableLCDR Colin CampbellLCDR Colin Campbell

Femi EsoimemeFemi EsoimemeStatement of Net CostStatement of Net Cost

Laila Grassley Laila Grassley

PP&E TeamPP&E TeamLCDR Bobby HartLCDR Bobby Hart

Personal PropertyPersonal PropertyLT Josh ZikeLT Josh Zike

Construction In ProgressConstruction In ProgressLT Ron MillspaughLT Ron Millspaugh

Real PropertyReal PropertyVeronica ChristenVeronica Christen

ElectronicsElectronicsLT Christian Hernaez Internal Use SoftwareInternal Use Software

LT Josh ZikeLT Josh ZikeOM&S/Repairable SparesOM&S/Repairable Spares

LT Ron MillspaughLT Ron MillspaughEnvironmental LiabilityEnvironmental Liability

LTJG Riley MatscoLTJG Riley Matsco

Accounts & PayrollAccounts & Payroll

AP & AR AP & AR John BowerJohn Bower

Civilian PayrollCivilian PayrollLCDR Jeff FerlautoLCDR Jeff FerlautoMilitary Payroll Military Payroll

LCDR Jeff FerlautoLCDR Jeff FerlautoActuarial Medical LiabilitiesActuarial Medical Liabilities

LCDR Jeff FerlautoLCDR Jeff FerlautoFBwTFBwT

John BowerCLL & InvestmentsCLL & Investments

CDR Tony AlaridCDR Tony Alarid

General Ledger / Financial ReportingGeneral Ledger / Financial Reporting

General Ledger/Financial ReportingGeneral Ledger/Financial ReportingJohn BowerJohn Bower

Statement of Net Cost Statement of Net Cost Rena WearRena Wear

Change in Net PositionChange in Net PositionJohn BowerJohn Bower

Statement of Budgetary ResourcesStatement of Budgetary ResourcesAkram MarufAkram Maruf

PP&E PP&E

Personal Property Akram Maruf

Environmental LiabilitiesCDR Tony Alarid

Real PropertyAkram Maruf

Construction In ProgressRena Wear

OM&S/Repairable SparesRena Wear

GL & Financial Reporting TeamLCDR Amy FlorentinoLCDR Amy Florentino

FBwT & General LedgerLCDR Amy Florentino

LT Melissa CooperPhil Faries (CG-8C)

Actuarial Medical LiabilitiesDCMS-831/CG-852

Change in Net PositionLCDR Colin Campbell

Statement of Budgetary ResourcesLCDR David Hatchett (CG-83)LCDR David Hatchett (CG-83)

Karen MayeKaren Maye

Policy & CommunicationsLT Tom Baker (CG-85)LT Tom Baker (CG-85)

ITGC/Application ControlsLCDR FerlautoLCDR Ferlauto

Other

Government Charge CardsTBD

IPERA MonitoringRena Wear

SAS 70 ReviewsGS-9

Statement of AssuranceSusan Seyfried

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

13

Why Do I Care?

• It’s not about Passing the Audit, it’s about doing our jobs IAW Federal Standards.

• The audit is merely a trigger

• It’s not extra work, it’s work we’ve been required to do, but failed to do

• You can’t know what you need if you don’t know what you have

• From the OMB Reviewer: the CG is not a candidate for budget growth until they can pass the audit (paraphrasing)

• Auditors heading your way…..

13Assistant CommandantAssistant CommandantFor ResourcesFor Resources

Assistant CommandantAssistant CommandantFor ResourcesFor Resources

14

Questions?

CDR Jim Passarelli

CG-85D

(202) 372-3459

Learn more about Auditing, Internal Controls and Financial Statements at:

https://collab.uscg.mil/lotus/mypoc?uri=dm:0d33288048f0ed30b0e9baea03115258&verb=view

14Assistant CommandantAssistant CommandantFor ResourcesFor Resources

![WELCOME [] · 2019-08-30 · Marksmanship Proficiency System CAPABILITY + Live, Virtual, Constructive Development and ... TEST & EVALUATION Carl Lee RDML G. Mays CNRSE RDML W. Dillon](https://img.pdfslide.us/doc/110x75/5f96c43b03cd97570e70a8f2/welcome-2019-08-30-marksmanship-proficiency-system-capability-live-virtual.jpg)