Embed Size (px)

Citation preview

BASF UK Group Pension Scheme Group & BPP DC Section (the “Scheme”)

Factsheet 7 Aug 2016 - updated Oct 2019

Using your DC Account to target cash

Why should I read this factsheet?After age 55, you broadly have three different choices for how you use your defined contribution (DC) Account: Secure a guaranteed income (annuity)

Take a cash lump sum

Take a flexible income (also known as an adjustable income, ‘drawdown’or‘flexi-accessdrawdown’)

You can choose any combination of these options and can usually take up to 25% of your DC Account as a tax-free lump sum. This factsheet explains the process if you want to take your DC Account as cash .

Note: Where you see a word in italicsthistermisexplainedinyourDCBooklet.

What is this option? You can take all of your DC Account as a single cash lump sum (the first 25% tax-free, the rest subject to income tax). If your DC Account is worth more than £5,000, you can choose to take it as two cash lumpsumsovertwoconsecutivetaxyears(providedyouhaveatleast£1,500leftforthesecondpayment25%ofeachpaymentistax-free,therestsubjecttoincometax).

This applies to your DC Account in the Scheme and any Scheme Additional Voluntary Contributions (AVCs)investedwithoneofourexternalproviders,e.g.Prudential.

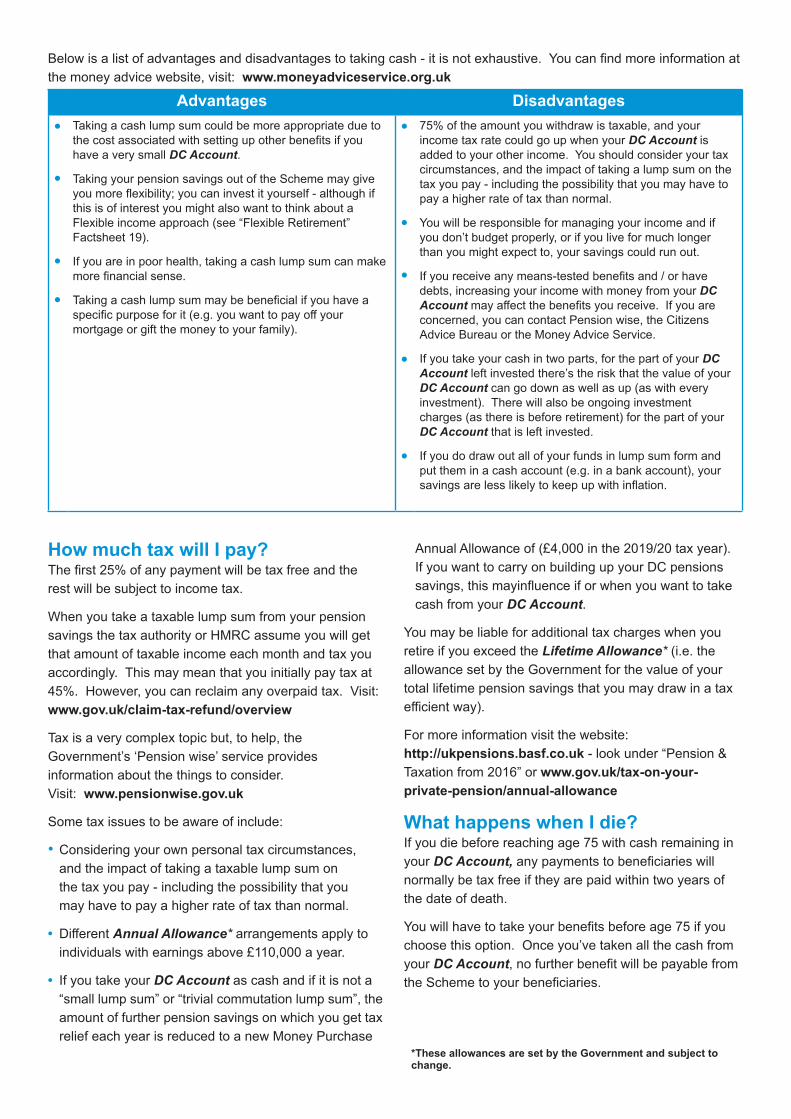

Advantages Disadvantages●

●

●

●

Takingacashlumpsumcouldbemoreappropriateduetothecostassociatedwithsettingupotherbenefitsifyouhave a very small DC Account.

TakingyourpensionsavingsoutoftheSchememaygiveyoumoreflexibility;youcaninvestityourself-althoughifthisisofinterestyoumightalsowanttothinkabouta Flexibleincomeapproach(see“FlexibleRetirement” Factsheet19).

Ifyouareinpoorhealth,takingacashlumpsumcanmakemorefinancialsense.

Takingacashlumpsummaybebeneficialifyouhaveaspecificpurposeforit(e.g.youwanttopayoffyour mortgageorgiftthemoneytoyourfamily).

●

●

●

●

●

75%oftheamountyouwithdrawistaxable,andyour incometaxratecouldgoupwhenyourDC Account is addedtoyourotherincome.Youshouldconsideryourtaxcircumstances,andtheimpactoftakingalumpsumonthetaxyoupay-includingthepossibilitythatyoumayhavetopayahigherrateoftaxthannormal.

Youwillberesponsibleformanagingyourincomeandifyoudon’tbudgetproperly,orifyouliveformuchlongerthanyoumightexpectto,yoursavingscouldrunout.

Ifyoureceiveanymeans-testedbenefitsand/orhavedebts,increasingyourincomewithmoneyfromyour DC Accountmayaffectthebenefitsyoureceive.Ifyouareconcerned, you can contact Pension wise, the Citizens AdviceBureauortheMoneyAdviceService.

If you take your cash in two parts, for the part of your DC Account left invested there’s the risk that the value of your DC Accountcangodownaswellasup(aswithevery investment).Therewillalsobeongoinginvestmentcharges(asthereisbeforeretirement)forthepartofyourDC Accountthatisleftinvested.

If you do draw out all of your funds in lump sum form and puttheminacashaccount(e.g.inabankaccount),yoursavingsarelesslikelytokeepupwithinflation.

Belowisalistofadvantagesanddisadvantagestotakingcash-itisnotexhaustive.Youcanfindmoreinformationatthe money advice website, visit: www.moneyadviceservice.org.uk

How much tax will I pay? Thefirst25%ofanypaymentwillbetaxfreeandthe restwillbesubjecttoincometax.

WhenyoutakeataxablelumpsumfromyourpensionsavingsthetaxauthorityorHMRCassumeyouwillgetthatamountoftaxableincomeeachmonthandtaxyouaccordingly.Thismaymeanthatyouinitiallypaytaxat45%.However,youcanreclaimanyoverpaidtax.Visit:www.gov.uk/claim-tax-refund/overview

Taxisaverycomplextopicbut,tohelp,the Government’s ‘Pension wise’ service provides informationaboutthethingstoconsider. Visit: www.pensionwise.gov.uk

Sometaxissuestobeawareofinclude:

• Consideringyourownpersonaltaxcircumstances, andtheimpactoftakingataxablelumpsumon thetaxyoupay-includingthepossibilitythatyou mayhavetopayahigherrateoftaxthannormal.

• DifferentAnnual Allowance*arrangementsapplyto individualswithearningsabove£110,000ayear.

• If you take your DC Account as cash and if it is not a “small lump sum” or “trivial commutation lump sum”, the amountoffurtherpensionsavingsonwhichyougettax relief each year is reduced to a new Money Purchase

AnnualAllowanceof(£4,000inthe2019/20taxyear). IfyouwanttocarryonbuildingupyourDCpensions savings,thismayinfluenceiforwhenyouwanttotake cash from your DC Account.

Youmaybeliableforadditionaltaxchargeswhenyou retireifyouexceedtheLifetime Allowance*(i.e.the allowance set by the Government for the value of your totallifetimepensionsavingsthatyoumaydrawinataxefficientway).

For more information visit the website: http://ukpensions.basf.co.uk -lookunder“Pension&Taxationfrom2016”orwww.gov.uk/tax-on-your- private-pension/annual-allowance

What happens when I die? Ifyoudiebeforereachingage75withcashremaininginyour DC Account,anypaymentstobeneficiarieswill normallybetaxfreeiftheyarepaidwithintwoyearsofthedateofdeath.

Youwillhavetotakeyourbenefitsbeforeage75ifyouchoosethisoption.Onceyou’vetakenallthecashfromyour DC Account,nofurtherbenefitwillbepayablefromtheSchemetoyourbeneficiaries.

*These allowances are set by the Government and subject to change.

How and when can I take my DC Account as cash? Ifyouwanttotakeadvantageofthisoption,contactBuck.

If you have more than £5,000 in your DC Account and would like to take it as two cash lump sums over two consecutivetaxyears,youcanselectanyamountforthefirstpayment,providedyouhaveatleast£1,500leftforthesecondpayment.Allrelevantdetailsforyoursecondpayment would need to be provided to Buck at the time of arrangingyourfirstpayment.Buckwillsendyoua payslipatthetimeofeachpayment.

OnceallofthemoneyinyourDC Account has been paid toyou,youwillstopbeingamemberoftheSchemeandyouandyourprospective/nominatedbeneficiarieswillthenhavenofurtherlegalconnectionwithorentitlementunder the BASF UK Group Pension Scheme in respect of your DC Account.

Theprocesswillautomaticallybeginaroundsevenmonths before your Normal Pension Age (NRA) or, if you have one, your Target Pension Date (TPD), Buck willautomaticallysendyouaretirementpack.Ifyouwishtotakeyourbenefitsearlierorlateryoucanrequesta retirementpackfromBuck.

Your retirement pack will contain:

• Afundvaluestatement,tellingyouthevalueofyour DC Account,howmuchyoucouldtakeasatax-free cashlumpsumandthevariousbenefitoptionsyou have.

• Contactdetailsfortheindependentfinancialadviser appointedbyBASF(currentlyOrigenFinancial Services),whocanhelpyouconsideryouroptions;and

• Allrelevantformsyouwillneedtocomplete.

Please note:

• Theminimumretirementageiscurrentlyfromage55 butitisexpectedtoincreasetoage57by2028.

• Youdon’thavetotakeyourbenefitsfromage55;you can take them at any time after this, but no later than age75fromtheScheme.

• Restrictionsmayapplytoyourbenefitoptionsifyou have an entitlement to a Guaranteed Minimum Pension.Allbenefitoptionsaresubjecttochangesin legislationandthetaxstatuscurrentlyaffordedto pensionssavings.

Scammersmayoperateinpensionmarkets.Youcanfindoutmoreabouthowtoavoidscamsat: www.pensionwise.gov.uk/scams!

Don’t get stung. www.pension-scams.com

Scam: Convincing marketing materials that promise you guaranteed high returns on your investment

Scam: Offers of a free pension review, a one-off investment opportunity, the chance to cash in or release your pension early, pension loans or upfront pension cash

Scam: Unsolicited contact via call, text, email or in person claiming to be from The Pensions Advisory Service, Pension Wise or government-endorsed. Such contact would always be

initiated by you first, never by those organisations.

Scam: Pension access offered before age 55 and you are not in ill health

Scam: Overseas investment opportunities in property, green energy plantations, scratchcards where all your money is in one place

Scamproof: Checking a financial adviser is personally authorised by the FCA at www.fca.org.uk/register

Scamproof: Check the list of known investment scams at www.fca.org.uk/scamsmart

Scamproof: Seeking professional independent financial advice

Scamproof: Not allowing yourself to be rushed into a decision by time limited offers or delivery of previously unseen paperwork by courier

Scamproof: Not signing anything you don’t completely understand

Scamproof: Arming yourself with the facts at www.pension-scams.com

F R E E!

F R E E!

Scamproof: Taking advantage of free support and guidance offered by The Pensions Advisory Service and Pension Wise

scammable or scamproof?Are you

Buck can be contacted at:

TelNo:03301230647

Email:[email protected]

or write to:

BASF Buck (Bristol) POBox319 Mitcheldean GL149BF

Investing your DC Account to target cash WhereyouinvestyourDCpensionsavingscanhaveamaterialimpactonthebenefitsyoureceiveatretirement.Asyougetclosertoretirementyoumaywishtochangewhereyouare invested to reduce risk and protect the value of your pension savings.

If you take your DC Account as Cash, there are three LifePlan optionsavailabletohelpyoudothis-theAdventurousCash LifePlan, Moderate Cash LifePlan and Cautious Cash LifePlan.

Please refer to the Investment Guide for full details and if you wish to change your investment choices, you can do so by logging on to the Pension Portal (see overleaf).

Note: If you have AVCs invested with one of our external providers, they will have different investment options that apply. You can contact Buck for further details on:

+44 (0) 330 123 0647 email: [email protected]

Choosing your investment route in the BASF Scheme

If you are planning ahead (forexample,morethan5-10yearsfromretirement)

If you are getting ready to retire

(lessthan5-10yearsfromretirement)

LogontothePension Portal and take a look at your investment choices

LogontothePension Portal account and use the RetirementModellertoconsiderthetypeofbenefits

you’d like to take

CheckandupdateyourTargetPensionAgeif necessary

Update your investment choices to suit the type of benefitsyouwanttotakeatretirement

Keepyourinvestmentchoicesunderregularreview

CheckandupdateyourTargetPensionAgeif necessary

ConsiderusingthePensionwiseservicefromage50,fortailoredguidanceonyouroptions.

Buck will contact you seven months beforeyourTargetPensionAgetostartyourretirement

planning

Get support with your decisions Weknowthatchoosingyourbenefitsisareallyimportantdecision.Wewanttomakesureyouareprovidedwiththerightlevelofsupport,fromsourcesthatyoucantrust.

Use your the Pension Portal - A simple way to manage your DC Account The Pension Portalallowsyoutoviewandchangea number of details about your DC Account.Thereisa RetirementModellerwhichshowshowmuchyour DC Accountmightprovideasaguaranteed income (annuity), cash lump sum or flexible income.

Visit:https://www.buckhrsolutions.co.uk/basf Ifyouneedhelplogginin,pleaserefertothePensionPortalFactsheet, which can be found on the Scheme website (see below)

.

Use the Scheme website The BASF UK Group Pension Scheme website is dedicatedtoourmembersandgivesyouacentralplacetogowhenmanagingyourSchemebenefits. Visit: http://ukpensions.basf.co.uk

Pre-retirement Workshop IfyouarestillworkingforBASF,youcanattenda Pre-retirementWorkshop.FulldetailsareavailableonthePlanningforRetirementfactsheetwhichcanbefoundonthe Scheme website http://ukpensions.basf.co.uk under‘GettingreadyforRetirement’.

Pension wise - free Guidance There is a lot of information available about options at retirement and it’s important that you only rely on reputablesourcesofinformationtoavoidbeingtargetedbyscammers.Tohelp,theGovernmenthaslaunchedanew‘Pensionwise’servicetogivefreeimpartialguidanceto anyone with a DC Account,aimedatanyoneaged50orover.Wereccomendthatyougetguidancetohelpwithyourretirementplanningdecisions.Thewebsite offersyouguidanceonyourpensionoptions,orifyou’d prefertotalktoaspecialist,youcanarrangeatelephoneorface-to-faceappointment.Ifyouareinterestedinthis service visit: www.pensionwise.gov.uk

Origen Financial Services The BASF Scheme has appointed an independent company to help you with your retirement choices and to helpyoumaximiseyourretirementincome.Contact [email protected]

Buck Ifyouareapproachingretirementandwanttodiscussyouroptions,contactBuckwhowillbeabletoexplainyour options in more detail and provide a retirement benefitestimate.PleasenotethatBuckcan only provide information on your retirement options they cannotgiveindividualadvice.Call+44(0)3301230647or email: [email protected]

Independent Financial Advice InadditiontoorinsteadofOrigen,youcanusean IndependentFinancialAdviser(IFA).Theywillbeable togiveyouadviceinrelationtoyourpersonal circumstances, but please be aware that you may be chargedforthisadvice.TofinddetailsofalocalIFAvisitwww.moneyadviceservice.org.uk or unbiased.co.uk

Get support with your decisions

This factsheet provides a brief overview of your benefit options available from the Scheme. Details of how the Scheme benefits are calculated and paid are set out in the Trust Deed and Rules, which take precedence over the content of this factsheet should there be any discrepancies. Neither the Trustee nor the Company can provide financial advice to you and nothing in this factsheet should be treated as such advice.