Embed Size (px)

Citation preview

SUMATRA COPPER & GOLD plc ABN 14 136 694 267

Ground Floor, 20 Kings Park Road, West Perth WA 6005 Australia

P +61 8 9389 2111 F +61 8 9389 2199 E [email protected] W www.sumatracoppergold.com

Registered in England and Wales Registered Number 5777015 Registered address: 39 Parkside, Cambridge CB1 1PN United Kingdom

SUMATRA COPPER & GOLD PLC

REGISTERED NUMBER 5777015 ABN 14 136 694 267

INTERIM FINANCIAL REPORT FOR THE HALF YEAR ENDED

30 JUNE 2013

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

CORPORATE DIRECTORY DIRECTORS

Stephen Daniel Robinson (Non-Executive Chairman)

Julian Peter Ford (Managing Director)

Adi Adriansyah Sjoekri (Executive Director)

Jocelyn Severyn de Warrenne Waller (Non-Executive Director)

Warwick George Morris (Non-Executive Director) COMPANY SECRETARY Alison Barr (United Kingdom) Graeme Smith (Australia) REGISTERED OFFICE 39 Parkside Cambridge CB1 1PN United Kingdom AUSTRALIAN OFFICE Level 1, 5 Ord Street West Perth WA 6005 Australia Phone: +61 8 6298 6200 BANKERS HSBC Bank plc 69 Pall Mall London SW17 5EY United Kingdom National Australia Bank 1238 Hay Street West Perth WA 6872 Australia STATUTORY AUDITORS PricewaterhouseCoopers LLP Abacus House Castle Park Cambridge CB3 0AN United Kingdom SHARE REGISTRY Computershare Investor Services Pty Limited

Level 2, 45 St George’s Terrace PERTH WA 6000 Phone: 1300 552 270 (within Australia) Phone: +61 3 9415 4000 (outside Australia) WEBSITE www.sumatracoppergold.com F

or p

erso

nal u

se o

nly

SUMATRA COPPER & GOLD PLC

0

CONTENTS

Directors’ Report 1 Consolidated Statement of Comprehensive Income 10 Consolidated Statement of Financial Position 11 Consolidated Statement of Changes in Equity 12 Consolidated Statement of Cash Flows 13 Notes to the Consolidated Financial Statements 14 Independent Auditor’s Review Report 22

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

11

Your Directors have pleasure in submitting their report together with the consolidated financial statements of the Group, being Sumatra Copper & Gold plc ('Sumatra' or the 'Company') and its controlled entities, for the half year ended 30 June 2013 and the review report thereon.

Directors

The names of the Directors of the Company in office during or since the end of the half year are: Mr Stephen Daniel Robinson B.Sc. Independent and Non-Executive Chairman

Steve Robinson is an experienced Australian mining executive and a Rhodes Scholar. He is the founding Director of independent corporate advisory firm Lincoln Capital Pty Ltd and has extensive international experience at senior executive levels within the mining industry.

He was previously a Director of Barrick (Australia Pacific) Limited and Bulletin Resources Ltd, Group Manager Planning with the leading Australian mineral sands producer Iluka Resources Ltd and a senior manager in the gold business unit at WMC Resources Ltd.

Mr Robinson is currently a Non-Executive Director of ASX-listed Orrex Resources Ltd. Mr Julian Peter Ford BSc (Eng), BCom, Grad Dip (Bus. Mgt) Managing Director

Julian Ford is an experienced mining professional with a career spanning more than 25 years within the global resources industry. He has held senior positions within several major resource companies including Alcoa, British Gas London and Western Metals Limited and co-founded copper and gold focused exploration and development company Zambezi Resources Ltd in 2004.

Mr Ford holds a degree in Chemical Engineering from the University of Natal, a Bachelor of Commerce from the University of South Africa and a Graduate Diploma in Business Management from the University of Western Australia. Mr Adi Adriansyah Sjoekri BSc, MSc, MBA (Management) Executive Director

Adi Sjoekri is an Indonesian national who graduated with a degree and a Master of Science in Geology from the Colorado School of Mines in the U.S.A. He completed his further education with an MBA in management at Monash University in Jakarta.

Mr Sjoekri has more than 17 years’ experience working for major companies such as CSR and Newmont throughout Indonesia and more recently as a successful consultant to the mining industry. He was instrumental in recognising the opportunity to acquire mineral tenements in Indonesia in 2006. Mr Jocelyn Severyn de Warrenne Waller MA (Hons) (Cantab) Non-Executive Director

Jocelyn Waller is a British national who is a founding shareholder and Director of the Company. Mr Waller graduated from Churchill College, Cambridge with a Master of Arts in History in 1965 and has since spent his entire career in the mining industry. For 22 years he worked for the Anglo American group and was involved variously with tin mining (Malaysia and Thailand), copper/cobalt (Zaire), potash (UK), tungsten (Portugal), exploration and metal sales (London).

In 1989 he set up Avocet Mining plc ('Avocet') and as CEO developed the Penjom gold mine in Malaysia and listed Avocet on the London Stock Exchange. In 2000 he set up Trans-Siberian Gold plc ('TSG') to develop gold projects in Eastern Russia listing TSG on the AIM market of the LSE in 2003. Mr Warwick George Morris BSc (Hons), MSc, MAusIMM Non-Executive Director

Warwick Morris is an Australian national who was appointed to the Board of the Company in March 2008 and shortly afterwards took over as Chairman. Mr Morris graduated from Sydney University in 1974 with a B.Sc (Hons) in Geology and in 1977 with a Master of Science in Geochemistry. He is a member of the Australasian Institute of Mining and Metallurgy and has more than 30 years' experience in the resources

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

22

industry.

Prior to mid-2007 Mr Morris was an Executive Director of Macquarie Bank Limited ('Macquarie'), where he had been both Chairman of the Metals and Energy Capital Division and head of Metals and Mining. In addition, he was co-founder of the Macquarie Energy Capital business, centred in Houston USA. Mr Morris has also held a directorship with Wine Planet Holdings Ltd, and was, before joining Macquarie, manager of the Mining Division of Minproc Engineers in Perth.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

33

REVIEW OF OPERATIONS

Sumatra Copper & Gold Plc (the “Company” or “Sumatra”) is an emerging gold and silver producer focused on the Indonesian island of Sumatra. The Company’s most advanced project is its 100%-owned Tembang Project which is currently under development and is scheduled to commence production during 2014.

Additional in-fill drilling and an Optimisation Study on the Stage 1 production plan was initiated during the reporting period as a response to the reduction in gold price. The purpose of the Optimisation Study is to enhance project economics in the lower gold price environment and enable completion of funding for the Tembang Project.

Highlights

The activities of the Group during and since the half year ended 30 June 2013 include the following highlights:

Tembang Project Permitting

Final Borrow & Use (Pinjam Pakai) Forestry Permit awarded in April 2013.

Significant progress achieved with other project permitting, with no other permit issues expected to be a critical path activity to achieving production.

Tembang Project Construction

Selected equipment orders placed for the processing plant with the first key offshore equipment component completed ahead of schedule and dispatched from Australia to Indonesia.

Early construction progress at site included commencement of on-site plant construction following the delivery of leach tank plate steel and construction of the 300-man camp, now 80% complete.

The Optimisation Study and revised Stage 1 mining plan is well advanced.

Tembang Exploration

A new zone of high-grade mineralisation named “Bitu” was discovered adjacent to the Belinau

underground deposit at Tembang. The mineralisation is expected to be readily and

economically accessed from the planned decline at Belinau.

Drilling resumed at Bitu in late July 2013 to test the potential of the high-grade zone, which remains open both along strike and at depth.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

44

Tandai Joint Venture - Exploration

The Tandai Joint venture was substantially scaled down during the half year with most staff demobilised.

A modest exploration campaign commenced at the Asa Prospect with encouraging results.

Corporate

A placement of 38,000,000 CDI’s to raise A$8.36 million was completed.

The proceeds of the equity raising were used to repay a $5M debt facility with Macquarie Bank.

An in-principle US$35 million debt finance package from Credit Suisse AG was signed as part of the Tembang Project’s funding plan.

An A$20 million rights issue was completed with a strong take-up of more than 60% (A$12 million) by shareholders. The issue was fully sub-underwritten by the Company’s major shareholder and cornerstone investor, Provident Capital Partners Pte Ltd.

The UK Panel on Takeovers and Mergers confirmed that Sumatra is not subject to the UK City Code on Takeovers and Mergers, clearing the way for SUM investors to increase their interest in the Company to 30% or more without having to make a mandatory offer for the Company.

Board and senior management team further strengthened with the appointment of former Barrick Gold (Australia) Director of Business Development Steve Robinson as a Non-Executive Director (and then appointed Non-Executive Chairman on 22 August 2013), and experienced corporate executive David Fowler as Chief Financial Officer.

Financial

The Group loss for the period was US$ 7,368,533 including a provision for impairment relating to exploration assets of US$ 4,635,528.

At end of the period the Group’s cash position was US$ 18,300,609.

The Group’s expenditure on exploration and evaluation costs in the period was US$ 3,435,311.

During the half, share capital issues raised US$ 27,811,854.

Loan repayments during the period were US$ 5,117,000.

Operational Activities

The focus of activities in the half was to progress the development of the Tembang project. A key milestone was achieved with the final Pinjam Pakai permit for Tembang being received. This allowed construction and development of the Company’s flagship project to commence.

Permitting

The Company was granted a “Borrow and Use” (Pinjam Pakai) Forestry Permit for its wholly owned subsidiary, PT. Dwinad Nusa Sejahtera (DNS). The permit is valid for 19 years or until 4 April 2032.

Following the grant of the Pinjam Pakai, a team of Planology Forestry Officers from the Department of Forestry in Jakarta carried out a forestry inspection at the Tembang Project site. The site inspection related to the fulfilment and obligations of the Borrow and Use (Pinjam Pakai) Forestry Permit.

Over the past 6 months the Company was also granted the following permits: Access Road Permit; Custom Registration Permit; Environmental Permit in Principle for de-watering according to the agreed planned activities; and a work permit for the planned expatriate component of the Tembang development plan.

The Dinas of Mines has issued an explosive storage location permit. This has allowed the Company to commence the construction of the explosive storage building prior to further obtaining

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

55

initial Explosive Permit for Storage Location by the Bupati of Musi Rawas, and the approval of Explosive purchase by the Police Department.

Optimised Mine Plan

Sumatra has initiated additional infill drilling and a series of optimisation studies.

In light of the fall in the gold price during the half, the Company decided to investigate a revised mining strategy based on mining the Buluh and Asmar open pit deposits in the Stage 1 Development. In addition, as a result of favourable geotechnical results, the Company intends to progress Belinau as an underground mine from the outset rather than commencing with an initial higher cost pit cutback.

The key benefits of the revised mine plan are expected to be improved cash flow in the first two years of production and lower cash costs, which would in turn translate into an improvement in project economics at current gold and silver prices compared to the current Stage 1 plan. The Company has completed the environmental, geotechnical and geo-hydrological assessment of the Buluh deposit required to upgrade the deposit to Bankable Feasibility Study (BFS) status. The assessment has confirmed that the Buluh mine plan will meet these higher technical standards required for BFS status.

As a result of more stringent debt funding conditions an in-fill drilling programme is also being completed to upgrade the Inferred Resource at Belinau, Buluh and Asmar to Measured and Indicated status to allow a fully optimised Ore Reserve and mine plan to be developed. In addition, composite and additional variability samples have been despatched for metallurgical assessment. As Buluh was partially mined during the previous production period at Tembang with excellent metallurgical performance, no adverse metallurgical results are expected.

A new high-grade gold discovery (Bitu) adjacent to the Belinau deposit at Tembang has highlighted the significant exploration upside at the project. The new zone should be accessible from the planned underground infrastructure at Belinau and further drill testing of the discovery will commence during the September Quarter.

Tembang - Detailed Engineering Design & Construction

The detailed design of the process plant is progressing on schedule and electrical design has commenced. The civil, structural, mechanical and piping areas are on schedule for completion in the September Quarter. The EPCM contractor mobilised to site to begin supervision of the CIL tank plate work erection. The construction site was cleared back to its original levels and installation of the hard stand and drainage is underway.

The reinstatement of access roads to the project site has largely been completed, enabling the mobilisation of construction materials and equipment. The expansion of the accommodation village is also well advanced, with most of the proposed 300 rooms completed. This has enabled key sub-contractors to be mobilised to site, allowing commencement of the CIL tank erection. The erection of the SCG construction office was completed and the EPCM office substantially completed. Pre-fabrication of the steel structure for the Magazine has commenced in Jakarta. Corporate Activities

Equity Capital Raising

In February 2013, Sumatra completed a placement of 38 million Sumatra CDI’s to the Company’s major shareholder and cornerstone investor, Provident Minerals Pte Ltd, to raise gross proceeds of A$ 8.36 million. Provident subsequently allocated some of these shares to Saratoga, Mr Garibaldi Thohir and Mr Yaw Chee Siew, pursuant to the agreement between Provident and the Company.

In June 2013, Sumatra completed a rights issue, undertaken on a two-for-five basis, following the award of the Final Forestry Permit for Tembang in April 2013. The issue was fully sub-underwritten by the Company’s major shareholder and cornerstone investor, Provident Capital Partners Pte Ltd. The Offer opened on 22 May 2013 and closed on 5 June 2013 with a strong take-up by

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

66

shareholders of more than 60 per cent. At the closing date, Sumatra received applications for approximately A$ 12.1 million (71.1 million CDI’s) from shareholders. A total of 117.8 million CDI’s were offered under the rights issue. The Company arranged for the balance of the underwritten amount (A$7.9 million or 46.8 million CDI’s) to be taken up by the Underwriter, Patersons Securities Limited. Sumatra subsequently allotted and dispatched the remaining shortfall CDI’s to the underwriters, resulting in gross proceeds to the Company of A$ 20 million. Holding statements for the new securities were dispatched on 13 June and trading of the new CDI’s commenced on 14 June 2013. Following completion of the rights issue, Sumatra has 414,467,651 shares and 52,381,332 unquoted options on issue.

Debt Finance

The Company used the proceeds of the February placement to repay principal and capitalised interest for the 1 year Macquarie Bank loan. The A$5 million facility was put in place when the company share price was trading below 12 cents per share.

On 21 February, Sumatra received credit approval from Credit Suisse AG (“Credit Suisse”) for US$30 million in senior debt finance facilities to fund the commercial development of the Tembang Project, as well as up to US$5 million of cost overrun funding. Credit Suisse was appointed following a competitive process conducted by Sumatra’s debt advisors, Optimum Capital Pty Ltd.

Provision of the US$30 million senior debt facilities is subject to completion of the project finance documentation and conditions precedent customary for a financing of this nature. These include final approval of the company’s Forestry Permit, which was received on 26 April 2013, and the completion of the entitlements issue component of the funding package outlined above. Documentation of the facility is well advanced.

The fall in the gold price subsequent to the signing of the original letter agreement with Credit Suisse has resulted in a downward revision of the prices used by Credit Suisse to evaluate the debt carrying capacity of the Tembang project. As a result of this the Company initiated a process to re-optimise its mine plan at lower gold prices and complete additional drilling and technical studies to improve the certainty of the mine plan in the lower gold price environment. While the decision to take these initiatives has delayed completion of the debt facility, the Company remains confident that the debt facility will be available for drawdown in the fourth quarter of the 2013 calendar year. However the final funding plan for the project will only be confirmed upon finalisation of the updated mine plan and review by Credit Suisse, and will be also predicated by the gold price at the time.

People

Subsequent to the end of the half-year, the Company announced two key appointments, further strengthening its board and senior management team in the lead-up to production. Mr Steve Robinson, an experienced mining executive, joined the Board as a Non-Executive Director. Mr David Fowler, an experienced corporate executive, joined the Company as its Chief Financial Officer.

On 22 August 2013 Mr Warwick Morris elected to step down as Non-Executive Chairman and was replaced by Mr Steve Robinson. Exploration

During the half-year, drilling focused on the Tembang project at Belinau and Buluh. At Belinau infill drilling was performed on the main orebody and a new ore shoot Bitu.

At Buluh, development drilling is ongoing and comprised two components: a geotechnical and hydrological drilling program and an in-fill program designed to confirm existing resources.

Exploration under the Tandai joint venture focused on the Asa prospect. During the half, exploration comprised soil sampling and creek mapping to outline the zone of significant gold and base metals mineralisation originally discovered in the Kokoi River. Exploration has been

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

77

successful in defining a NE-SW corridor of silicification and quartz veining over 2km. Locally, the structure appears quite complex with the best zones of mineralisation most likely occurring at intersections with NNW trending structures.

The relatively large exploration team at Tandai project was reduced during the half with some staff being redeployed to the Tembang Project.

The Company understands that Newcrest are currently reviewing their participation in the Tandai Joint Venture. Under the terms of the joint venture agreement, in the event that Newcrest withdraws from the Tandai Joint Venture, then Sumatra must acquire the 70% Newcrest interest in the Joint Venture Company for a nominal consideration

The Company’s relinquishment proposals for the Jambi, Musi Rawas and Bengkulu Utara IUP’s, are currently being processed by the government. The Company expects to provide additional information to the market once the relinquishment process has been completed.

Limited work occurred on the Sontang project during the reporting period and the Company was unable to identify a joint venture partner as the financing market for early stage exploration projects has become more challenging. While the company continues to consider Sontang a prospective property and the Company maintain its exploration titles in good standing the Company has decided to book an impairment for all exploration expenditure related to Sontang. This decision also reflects the Company’s intention to focus its exploration programs over the next 18 months on the Tembang project where exploration discovery has the potential to incrementally improve cash-flows. Financial

During the half the Group recorded a loss of US$ 7,368,533 after income tax including a loss of US$ 4,635,528 relating to a provision for impairment of exploration expenditure on the Sontang project. Total General administrative expenses increased to US$ 1,910,961 as less expenditure was capitalised to exploration during the current half year when compared to the prior reporting period.

At the end of the half the Groups cash position was US$ 18,300,609 after raising US$ 26,544,830 (net of expenses) in new equity and repaying US$ 5,117,000 of debt. Expenditure on exploration and evaluation was US$ 3,435,311 with a further US$ 5,449,780 spent on property plant and equipment related to the construction of the Tembang project.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

88

Going Concern

In considering the appropriate basis on which to prepare the financial statements, the directors are required to consider whether the Group can continue in operational existence for the foreseeable future. The directors have prepared detailed cash flow forecasts for the period to 31 December 2014, which show that the Group has sufficient working capital for the forecast period. The cash flow forecast includes funding being received from share issues, or other sources, following the anticipated granting of the permits required to progress to production at the group’s Tembang Project. At the time of approving the financial statements, such funding is not committed.

The Feasibility Study prepared by the Group anticipates that the Group will spend $ 38.5 million to construct the Tembang mine over the period to 30 June 2014. At 30 June 2013, the Group had cash and cash equivalents of $18,300,609 and the Directors have a reasonable expectation that the Group will be able to raise the required funds to complete construction and achieve cashflow from production. However the requirement to complete debt funding indicates the existence of material uncertainty which may cast significant doubt as to the group’s ability to fund the construction of the Tembang project and ultimately continue as a going concern. In the event that some combination of the above events fails to occur as expected, the Group may be unable to realise its assets and discharge its liabilities in the normal course of business.

The financial statements do not include the adjustments that would result if the group was unable to continue as a going concern.

Competent Person’s Statement – Exploration Results

The information in this report that relates to Exploration Results is based on information compiled by Mr Matthew Farmer, geologist, who is a Member of the Australasian Institute of Mining and Metallurgy. Mr Farmer is an employee of the Company who has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the 'Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves'. Matthew Farmer has consented to the inclusion in this report of the matters based on his information in the form and context in which they appear. Competent Person’s Statement – Mineral Resources

The information relating to Mineral Resources is based on information compiled by Mr David Stock MAusIMM who is an independent Geological Consultant to the Company and is a Competent Person as defined in the 2004 Edition of the 'Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves' and has consented to the inclusion in this report of the matters based on his information in the form and context in which they appear. In addition, the Mineral Resource estimates were reviewed by Mr Robert Spiers who is a member of AIG and a full time employee of Hellman & Schofield Pty Ltd. Mr Spiers has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the 'Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves'. Competent Person’s Statement – Ore Reserves The information in this report that relates to Open Pit and Underground Ore Reserves is based on information compiled by Mr Shane McLeay of Entech Pty Ltd, who is a Fellow of the Australasian Institute of Mining and Metallurgy. Mr McLeay has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the 'Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves'. Mr McLeay consents to the inclusion in this report of the matters based on his information in the form and context in which it appears.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD plc

DIRECTORS’ REPORT

99

Events Occurring after the Balance Sheet Date Nil

Signed in Perth this 13th day of September 2013 in accordance with a resolution of the Board of Directors:

Julian Ford Managing Director

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

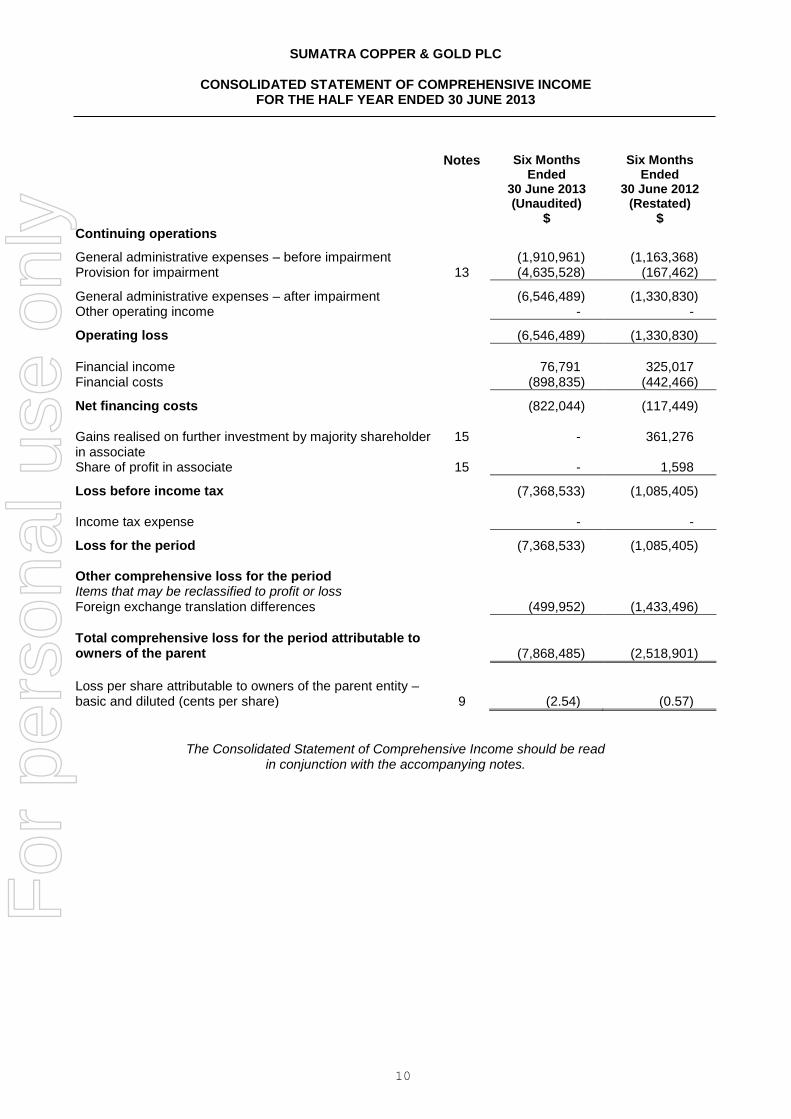

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE HALF YEAR ENDED 30 JUNE 2013

1010

Notes Six Months Ended

30 June 2013 (Unaudited)

$

Six Months Ended

30 June 2012 (Restated)

$ Continuing operations

General administrative expenses – before impairment (1,910,961) (1,163,368) Provision for impairment 13 (4,635,528) (167,462)

General administrative expenses – after impairment (6,546,489) (1,330,830) Other operating income - -

Operating loss (6,546,489) (1,330,830)

Financial income 76,791 325,017 Financial costs (898,835) (442,466)

Net financing costs (822,044) (117,449) Gains realised on further investment by majority shareholder in associate

15 - 361,276

Share of profit in associate 15 - 1,598

Loss before income tax (7,368,533) (1,085,405) Income tax expense

- -

Loss for the period (7,368,533) (1,085,405) Other comprehensive loss for the period

Items that may be reclassified to profit or loss Foreign exchange translation differences (499,952) (1,433,496)

Total comprehensive loss for the period attributable to owners of the parent

(7,868,485) (2,518,901)

Loss per share attributable to owners of the parent entity – basic and diluted (cents per share) 9 (2.54) (0.57)

The Consolidated Statement of Comprehensive Income should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

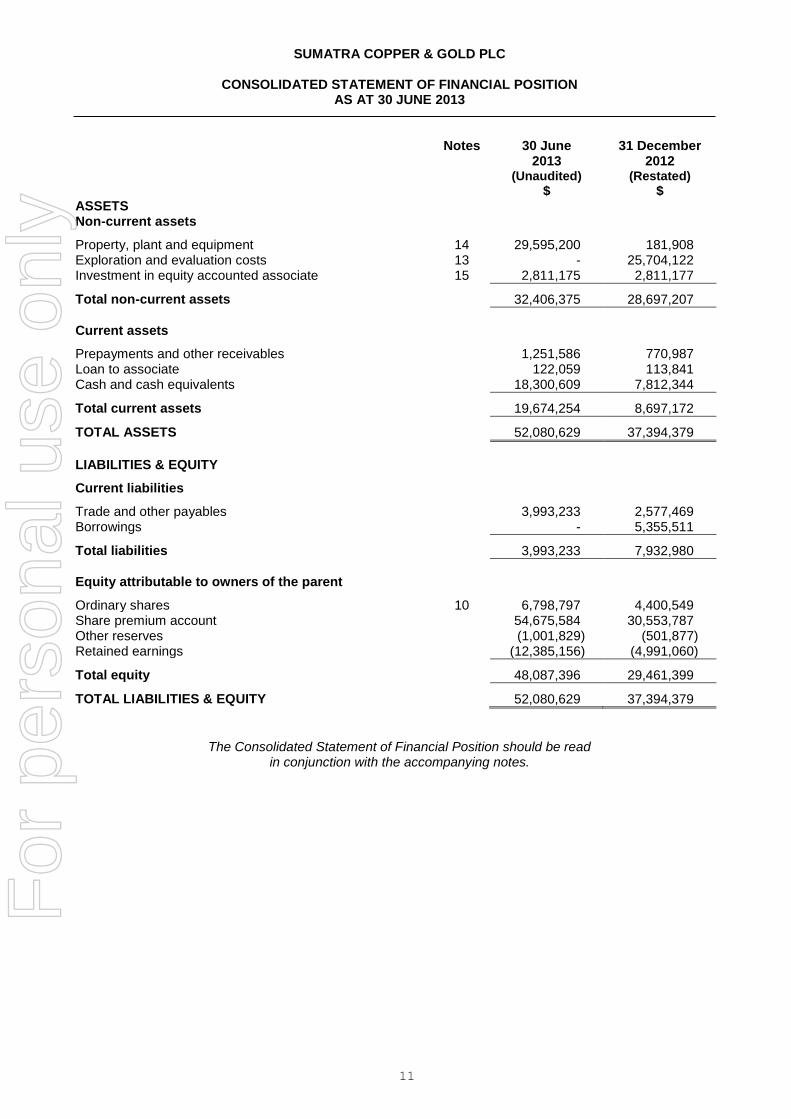

SUMATRA COPPER & GOLD PLC

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2013

1111

Notes 30 June 2013

(Unaudited)

$

31 December 2012

(Restated)

$ ASSETS Non-current assets

Property, plant and equipment 14 29,595,200 181,908 Exploration and evaluation costs 13 - 25,704,122 Investment in equity accounted associate 15 2,811,175 2,811,177

Total non-current assets

32,406,375 28,697,207

Current assets

Prepayments and other receivables 1,251,586 770,987 Loan to associate 122,059 113,841 Cash and cash equivalents 18,300,609 7,812,344

Total current assets

19,674,254 8,697,172

TOTAL ASSETS

52,080,629 37,394,379

LIABILITIES & EQUITY

Current liabilities

Trade and other payables 3,993,233 2,577,469 Borrowings - 5,355,511

Total liabilities

3,993,233 7,932,980

Equity attributable to owners of the parent

Ordinary shares 10 6,798,797 4,400,549 Share premium account 54,675,584 30,553,787 Other reserves (1,001,829) (501,877) Retained earnings (12,385,156) (4,991,060)

Total equity

48,087,396 29,461,399

TOTAL LIABILITIES & EQUITY

52,080,629 37,394,379

The Consolidated Statement of Financial Position should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

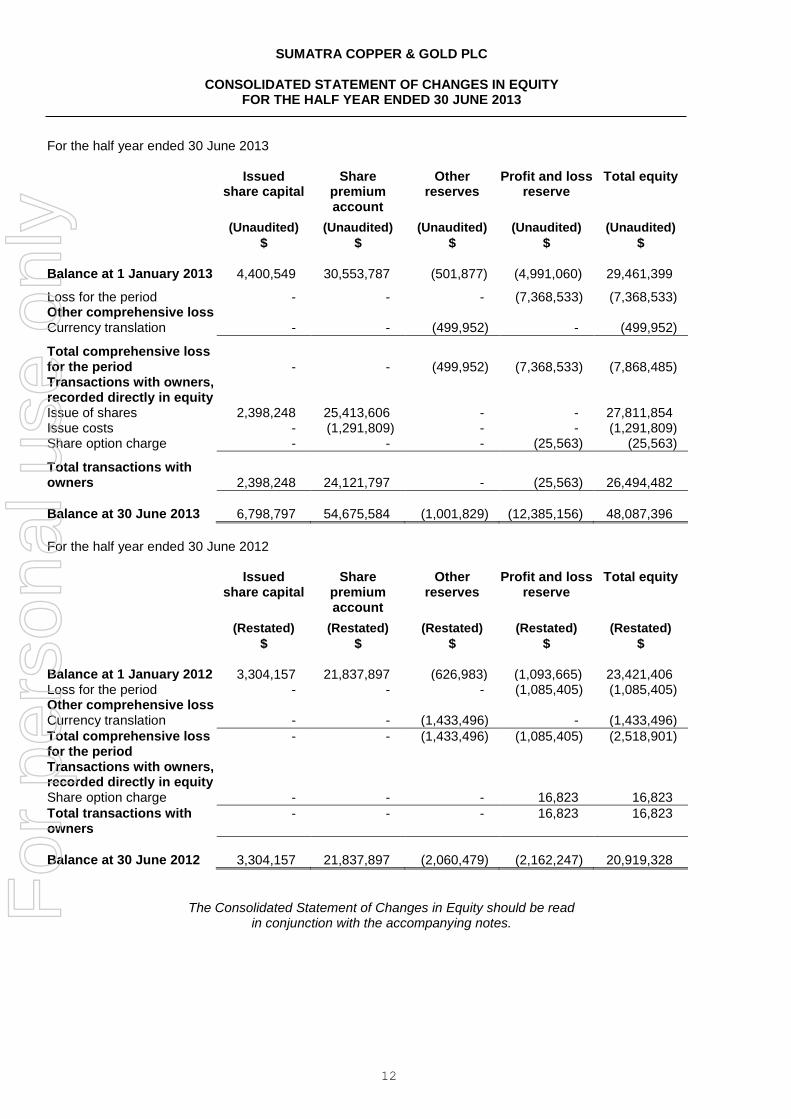

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE HALF YEAR ENDED 30 JUNE 2013

1212

For the half year ended 30 June 2013

Issued share capital

Share premium account

Other reserves

Profit and loss reserve

Total equity

(Unaudited) (Unaudited) (Unaudited) (Unaudited) (Unaudited)

$ $ $ $ $ Balance at 1 January 2013 4,400,549 30,553,787 (501,877) (4,991,060) 29,461,399

Loss for the period - - - (7,368,533) (7,368,533) Other comprehensive loss Currency translation - - (499,952) - (499,952)

Total comprehensive loss for the period - - (499,952) (7,368,533) (7,868,485) Transactions with owners, recorded directly in equity Issue of shares 2,398,248 25,413,606 - - 27,811,854 Issue costs - (1,291,809) - - (1,291,809) Share option charge - - - (25,563) (25,563)

Total transactions with owners 2,398,248 24,121,797 - (25,563) 26,494,482

Balance at 30 June 2013 6,798,797 54,675,584 (1,001,829) (12,385,156) 48,087,396

For the half year ended 30 June 2012

Issued share capital

Share premium account

Other reserves

Profit and loss reserve

Total equity

(Restated) (Restated) (Restated) (Restated) (Restated)

$ $ $ $ $ Balance at 1 January 2012 3,304,157 21,837,897 (626,983) (1,093,665) 23,421,406 Loss for the period - - - (1,085,405) (1,085,405) Other comprehensive loss Currency translation - - (1,433,496) - (1,433,496)

Total comprehensive loss for the period

- - (1,433,496) (1,085,405) (2,518,901)

Transactions with owners, recorded directly in equity Share option charge - - - 16,823 16,823

Total transactions with owners

- - - 16,823 16,823

Balance at 30 June 2012 3,304,157 21,837,897 (2,060,479) (2,162,247) 20,919,328

The Consolidated Statement of Changes in Equity should be read in conjunction with the accompanying notes. For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

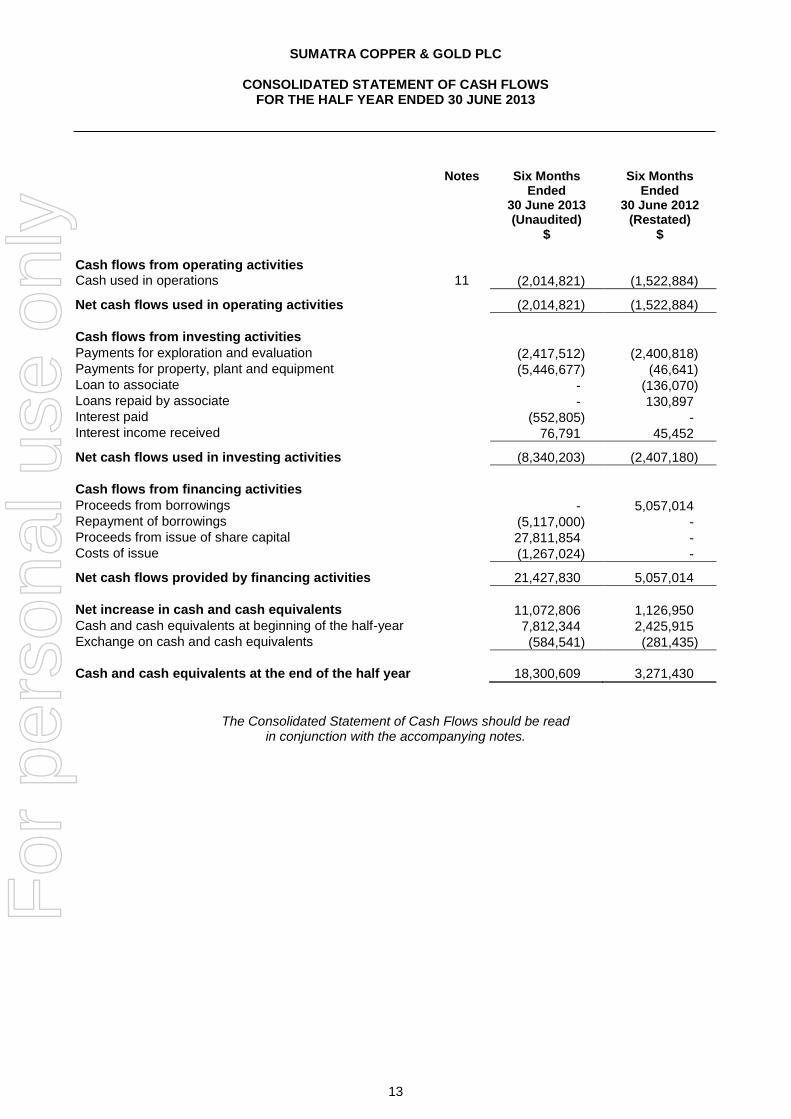

CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE HALF YEAR ENDED 30 JUNE 2013

13

Notes Six Months

Ended 30 June 2013 (Unaudited)

$

Six Months Ended

30 June 2012 (Restated)

$ Cash flows from operating activities

Cash used in operations 11 (2,014,821) (1,522,884)

Net cash flows used in operating activities (2,014,821) (1,522,884)

Cash flows from investing activities Payments for exploration and evaluation (2,417,512) (2,400,818) Payments for property, plant and equipment (5,446,677) (46,641) Loan to associate - (136,070) Loans repaid by associate - 130,897 Interest paid (552,805) - Interest income received 76,791 45,452

Net cash flows used in investing activities (8,340,203) (2,407,180)

Cash flows from financing activities Proceeds from borrowings - 5,057,014 Repayment of borrowings (5,117,000) - Proceeds from issue of share capital 27,811,854 - Costs of issue (1,267,024) -

Net cash flows provided by financing activities 21,427,830 5,057,014

Net increase in cash and cash equivalents 11,072,806 1,126,950 Cash and cash equivalents at beginning of the half-year 7,812,344 2,425,915 Exchange on cash and cash equivalents (584,541) (281,435)

Cash and cash equivalents at the end of the half year

18,300,609 3,271,430

The Consolidated Statement of Cash Flows should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

14

1. General information

The registered number of Sumatra Copper & Gold plc (the ‘Company’) is 5777015. The Company was incorporated in England on 11 April 2006 in the form of a company limited by shares and was later changed to a public limited company. It is domiciled in the United Kingdom. The Company’s shares are traded in the form of CHESS Depositary Interests on the Australian Stock Exchange.

The Company acts as the parent company of the Group.

The Company’s registered address is 39 Parkside, Cambridge CB1 1PN United Kingdom.

These condensed interim financial statements do not comprise statutory accounts within the meaning of section 434 of the Companies Act 2006. Statutory accounts for the year ended 31 December 2012 were approved by the Board of Directors on 29 March 2013 and delivered to the Registrar of Companies. The report of the auditors on those accounts was unqualified and did not contain any statement under section 498 of the Companies Act 2006. The report of the auditors contained an emphasis of matter paragraph in relation to going concern.

These condensed interim financial statements have been reviewed, not audited. 2. Basis of preparation

These condensed interim financial statements have been prepared on an historical cost basis. The financial statements are presented in United States Dollars and all values are rounded to the nearest Dollar except when otherwise indicated.

The Directors acknowledge their responsibly for the condensed interim financial statements and confirm that, to the best of their knowledge, the condensed interim financial statements for the six months ended 30 June 2013 have been prepared in accordance IAS 34 'Interim financial reporting', as adopted by the European Union. These condensed interim financial statements do not include all the notes of the type normally included in annual financial statements. Accordingly, these condensed interim financial statements should be read in conjunction with the annual financial statements for the year ended 31 December 2012, which have been prepared in accordance with IFRSs as adopted by the European Union. Going concern basis

In considering the appropriate basis on which to prepare the financial statements, the directors are required to consider whether the Group can continue in operational existence for the foreseeable future. The directors have prepared detailed cash flow forecasts for the period to 31 December 2014, which show that the Group has sufficient working capital for the forecast period. The cash flow forecast includes funding being received from share issues, or other sources, following the anticipated granting of the permits required to progress to production at the group’s Tembang Project. At the time of approving the financial statements, such funding is not committed.

The Feasibility Study prepared by the Group requires that the Group spends $ 38.5 million to move the Tembang mine to production over the period to 30 June 2014. At 30 June 2013, the Group had cash and cash equivalents of $18,300,609 and the Directors have a reasonable expectation that the Group will be able to raise the required funds to complete construction and achieve cashflow from production. However the requirement to complete debt funding indicates the existence of material uncertainty which may cast significant doubt as to the group’s ability to fund the construction of the Tembang project and ultimately continue as a going concern. In the event that some combination of the above events fails to occur as expected, the Group may be unable to realise its assets and discharge its liabilities in the normal course of business.

The financial statements do not include the adjustments that would result if the group was unable to continue as a going concern.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

15

3. Accounting policies

The accounting policies adopted are consistent with those of the previous financial year except as described below.

Functional and presentation currency

As the Group has progressed in to the development and construction phase of the Tembang project major cash outflows are now denominated in US Dollars. Future revenue from the Tembang project will be denominated in US Dollars, and it is anticipated that future debt and capital raisings will be denominated in US Dollars. On this basis, the parent entity and PT Dwinad Nusa Sejahtera have changed their functional currency to US Dollars, and the Group and the parent entity have changed their presentation currency from Pounds Sterling to US Dollars, effective 1 January 2013.

Financial information for prior periods has been restated from Pounds Sterling to US Dollars in accordance with IAS 21. Assets and liabilities were translated into US Dollars using the closing rate at the 2012 reporting date. Income, expenses and cashflows recognised in the period were translated at an average US Dollar exchange rate for the period. Resulting exchange differences were reflected as currency translation adjustments and included in the cumulative currency translation reserve.

Equity and share capital items were translated using the historic rate applicable at the date of the transaction and were not re-translated at each subsequent reporting date.

The applicable exchange rates used for 2012 were: Period Ended 01/01/2011 31/12/2011 31/12/2012 Average Rate - 1.60436 1.58513 Closing Rate 1.54710 1.54560 1.61680 New and amended standards

New standards that are applicable for the first time for the June 2013 interim financial statements are:

IAS 1 ‘Financial statement presentation’;

IFRS 10 ‘Consolidated financial statements’;

IFRS 11 ‘Joint Arrangements’;

IFRS 12 ‘Disclosures of interests in other entities’; and

IFRS 13 ‘Fair value measurement’.

These standards have introduced new disclosures for the interim financial statements but did not affect the Group’s accounting policies or any of the amounts recognised in the financial statements. 4. Estimates

The preparation of interim financial statements requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, income and expenses. Actual results may differ from these estimates.

In preparing these condensed interim financial statements, the significant judgements made by management in applying the Group’s accounting policies and the key sources of estimation uncertainty were the same as those that applied to the consolidated financial statements for the year ended 31 December 2012. 5. Financial risk management

Financial risk factors

The Group’s activities expose it to a variety of financial risks: liquidity risk, foreign currency risk and credit risk.

The condensed interim financial statements do not include all financial risk management information and disclosures required in the annual financial statements; they should be read in conjunction with the Group’s annual financial statements as at 31 December 2012. There have been no changes in any financial risk management policies since the year end.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

16

Liquidity risk

Compared to the year end there has been no material change to the Group’s liquidity risk.

Fair value estimation The Group had no assets or liabilities that were required to be fair valued (2012: none). 6. Segment information

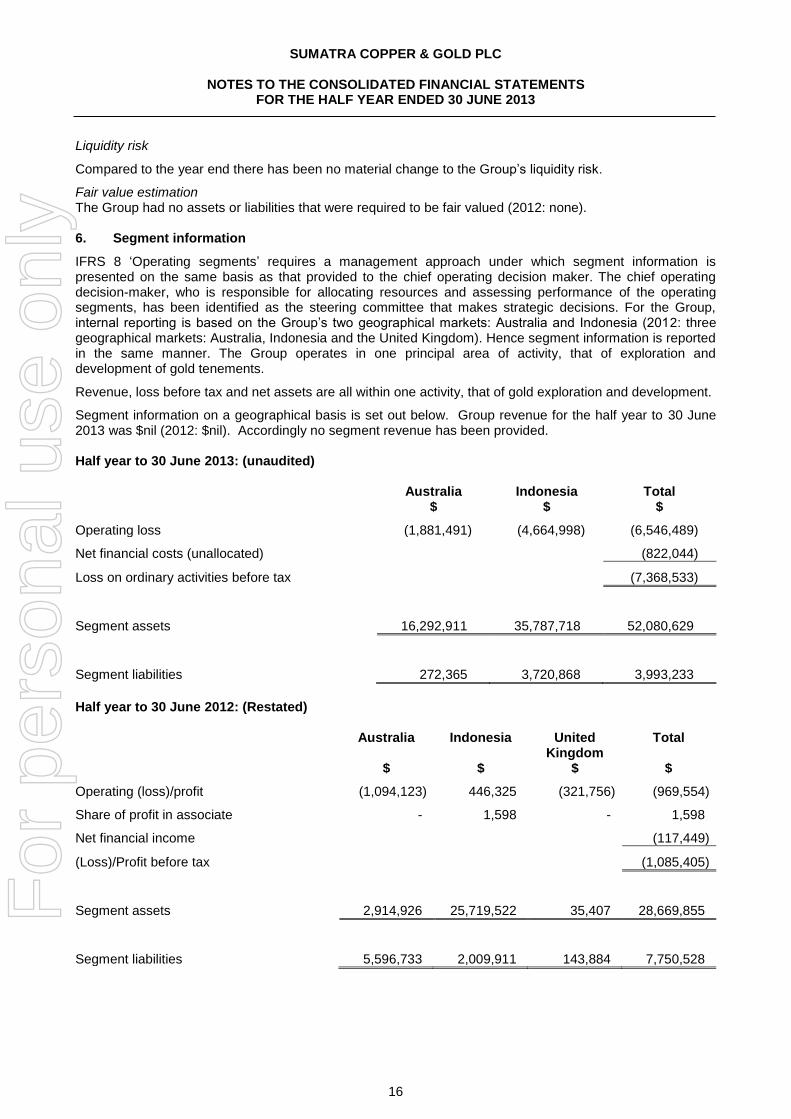

IFRS 8 ‘Operating segments’ requires a management approach under which segment information is presented on the same basis as that provided to the chief operating decision maker. The chief operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the steering committee that makes strategic decisions. For the Group, internal reporting is based on the Group’s two geographical markets: Australia and Indonesia (2012: three geographical markets: Australia, Indonesia and the United Kingdom). Hence segment information is reported in the same manner. The Group operates in one principal area of activity, that of exploration and development of gold tenements.

Revenue, loss before tax and net assets are all within one activity, that of gold exploration and development.

Segment information on a geographical basis is set out below. Group revenue for the half year to 30 June 2013 was $nil (2012: $nil). Accordingly no segment revenue has been provided. Half year to 30 June 2013: (unaudited) Australia Indonesia Total $ $ $

Operating loss (1,881,491) (4,664,998) (6,546,489)

Net financial costs (unallocated) (822,044)

Loss on ordinary activities before tax (7,368,533)

Segment assets 16,292,911 35,787,718 52,080,629

Segment liabilities 272,365 3,720,868 3,993,233

Half year to 30 June 2012: (Restated) Australia Indonesia United

Kingdom Total

$ $ $ $

Operating (loss)/profit (1,094,123) 446,325 (321,756) (969,554)

Share of profit in associate - 1,598 - 1,598

Net financial income (117,449)

(Loss)/Profit before tax (1,085,405)

Segment assets 2,914,926 25,719,522 35,407 28,669,855

Segment liabilities 5,596,733 2,009,911 143,884 7,750,528

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

17

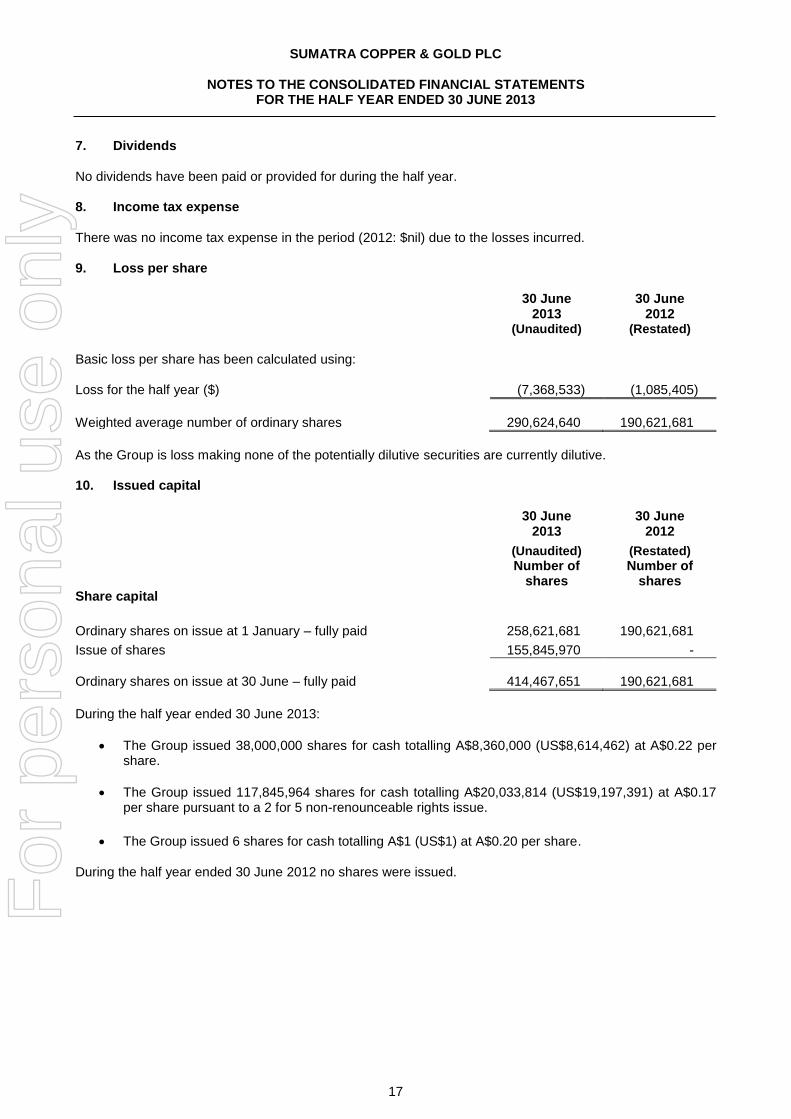

7. Dividends No dividends have been paid or provided for during the half year. 8. Income tax expense There was no income tax expense in the period (2012: $nil) due to the losses incurred. 9. Loss per share

30 June 2013

(Unaudited)

30 June 2012

(Restated) Basic loss per share has been calculated using:

Loss for the half year ($) (7,368,533) (1,085,405)

Weighted average number of ordinary shares 290,624,640 190,621,681

As the Group is loss making none of the potentially dilutive securities are currently dilutive. 10. Issued capital

30 June

2013 30 June

2012

(Unaudited) (Restated)

Number of

shares Number of

shares Share capital

Ordinary shares on issue at 1 January – fully paid 258,621,681 190,621,681

Issue of shares 155,845,970 -

Ordinary shares on issue at 30 June – fully paid 414,467,651 190,621,681

During the half year ended 30 June 2013:

The Group issued 38,000,000 shares for cash totalling A$8,360,000 (US$8,614,462) at A$0.22 per share.

The Group issued 117,845,964 shares for cash totalling A$20,033,814 (US$19,197,391) at A$0.17 per share pursuant to a 2 for 5 non-renounceable rights issue.

The Group issued 6 shares for cash totalling A$1 (US$1) at A$0.20 per share. During the half year ended 30 June 2012 no shares were issued. F

or p

erso

nal u

se o

nly

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

18

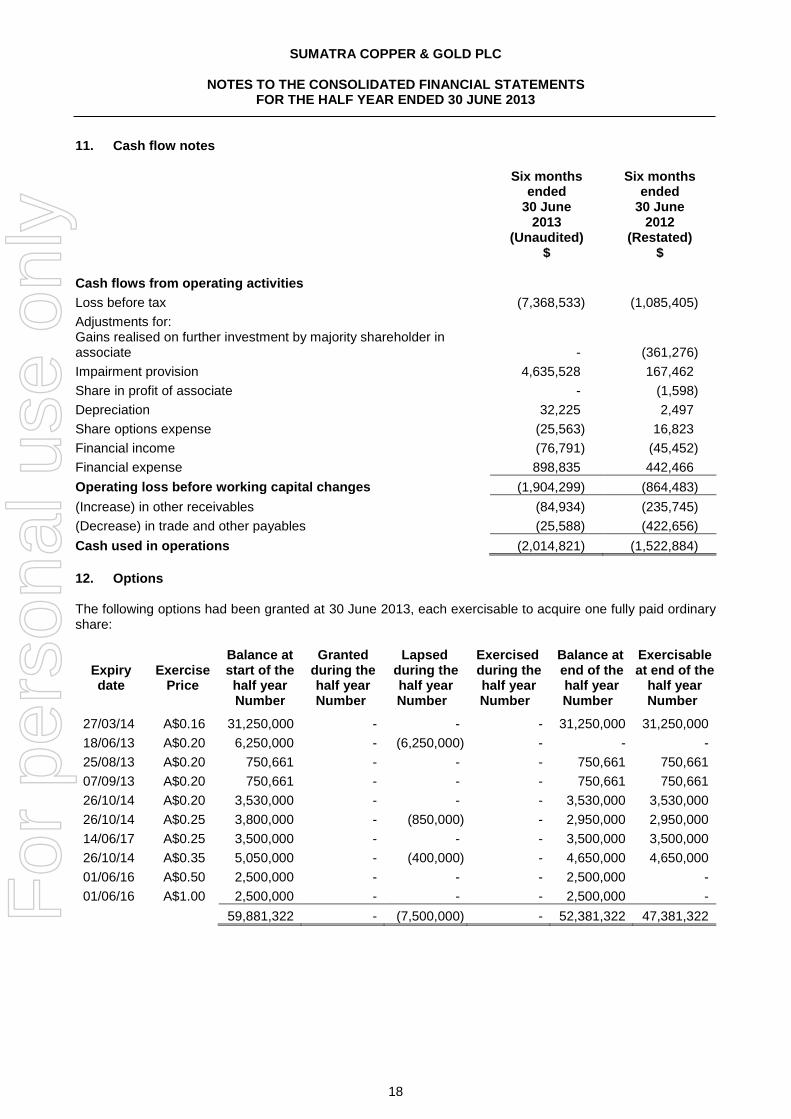

11. Cash flow notes

Six months ended

30 June 2013

(Unaudited) $

Six months ended

30 June 2012

(Restated) $

Cash flows from operating activities

Loss before tax (7,368,533) (1,085,405)

Adjustments for: Gains realised on further investment by majority shareholder in associate - (361,276)

Impairment provision 4,635,528 167,462

Share in profit of associate - (1,598)

Depreciation 32,225 2,497

Share options expense (25,563) 16,823

Financial income (76,791) (45,452)

Financial expense 898,835 442,466

Operating loss before working capital changes (1,904,299) (864,483)

(Increase) in other receivables (84,934) (235,745)

(Decrease) in trade and other payables (25,588) (422,656)

Cash used in operations (2,014,821) (1,522,884)

12. Options The following options had been granted at 30 June 2013, each exercisable to acquire one fully paid ordinary share:

Expiry date

Exercise Price

Balance at start of the half year

Granted during the half year

Lapsed during the half year

Exercised during the half year

Balance at end of the half year

Exercisable at end of the

half year Number Number Number Number Number Number

27/03/14 A$0.16 31,250,000 - - - 31,250,000 31,250,000

18/06/13 A$0.20 6,250,000 - (6,250,000) - - -

25/08/13 A$0.20 750,661 - - - 750,661 750,661

07/09/13 A$0.20 750,661 - - - 750,661 750,661

26/10/14 A$0.20 3,530,000 - - - 3,530,000 3,530,000

26/10/14 A$0.25 3,800,000 - (850,000) - 2,950,000 2,950,000

14/06/17 A$0.25 3,500,000 - - - 3,500,000 3,500,000

26/10/14 A$0.35 5,050,000 - (400,000) - 4,650,000 4,650,000

01/06/16 A$0.50 2,500,000 - - - 2,500,000 -

01/06/16 A$1.00 2,500,000 - - - 2,500,000 -

59,881,322 - (7,500,000) - 52,381,322 47,381,322

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

19

There were no options issued or granted during the half year ended 30 June 2013.

During the half year ended 30 June 2012:

31,250,000 options were issued with an exercise price of 16 cents, vesting immediately and expiry date of 27 March 2014, to Macquarie Bank Limited as part of a convertible debt finance facility.

2,500,000 performance options were issued with an exercise price of 50 cents, an expiry date of 1 June 2016, to the Managing Director, as part of Mr Ford’s employment package. The options are subject to the Performance Condition of the completion of the first post-commissioning calendar month of gold production at the Tembang project with gold at or above budgeted gold production for that month. If the Performance Condition is not met by 30 June 2014 the options will lapse.

3,000,000 options were issued with an exercise price of 25 cents, vesting immediately and expiry date of 14 June 2017, to Directors Julian Ford and Adi Sjoekri.

13. Exploration and evaluation costs 30 June

2013 (Unaudited)

$

31 December 2012

(Restated) $

Opening balance 1 January 25,704,122 20,653,565 Additions 3,435,311 5,690,090 Provision for impairment (4,635,528) (272,519) Exchange movements (437,137) (367,014) Transfer to development assets (refer note 14) (24,066,768) -

Closing balance at period end - 25,704,122

During the half year ended 30 June 2013 the Directors wrote off the carrying value of exploration and evaluation costs totalling $4,635,528. These costs were associated with the Company’s Sontang, Jambi, Madina 1, Madina 2 and Musi Rawas projects as the Directors believed that whilst further exploration was on-going at each of these projects there did not exist at present enough significant mineralisation targets or drilling results to warrant the carry forward of exploration and evaluation costs at these projects. 14. Property Plant & Equipment 30 June

2013 (Unaudited)

$

31 December 2012

(Restated) $

Opening balance 1 January 181,908 196,101 Additions 5,449,780 73,160 Transfer from exploration and evaluation costs 24,066,768 - Depreciation charge for the period (32,225) (74,734) Exchange movements (71,031) (12,619)

Closing balance at period end 29,595,200 181,908

During the half year ended 30 June 2013 the exploration and evaluation costs associated with the Group’s Tembang project were reclassified as development assets following receipt of the final government approvals. Additions during the half year relate to construction activities associated with the Tembang project.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

20

15. Investment in equity accounted associate 30 June

2013 (Unaudited)

$

31 December 2012

(Restated) $

Opening balance 1 January 2,811,177 1,776,183 Gain realised on further investment by majority shareholder - 907,555 Share of profit in associate - 101,316 Foreign exchange gain (2) 26,123

Closing balance at period end 2,811,175 2,811,177

In March 2011 the Company completed joint venture arrangements with Newcrest Mining Limited ('Newcrest') in respect of PT Bengkulu Utara Gold ('PT BUG'), the holder of the exploration IUP covering the Tandai project. As part of this transaction a subsidiary of Newcrest subscribed $1.75 million for new shares in PT BUG for a 70% interest.

The $1.75 million subscription constitutes the minimum spend commitment by Newcrest over 18 months (‘Minimum Spend Period’). After the Minimum Spend Period, Newcrest may make further equity investments up to a total of $12 million to maintain a 70:30 ownership ratio of PT BUG. If Newcrest elects not to complete the full $12 million subscription over a 5 year period, Sumatra has the right to buy back Newcrest’s 70% interest in PT BUG for a nominal consideration. As a result of this transaction, the Company now accounts for PT BUG as an equity accounted associate, rather than a subsidiary, and has deconsolidated the net assets of PT BUG, including the carrying value of exploration and evaluation costs for the Tandai project. 16. Related party transactions

During the half year ended 30 June 2013, the Company sub-leased office space for its Perth office from Karen Ford, wife of Managing Director Julian Ford. The charge covered rental accommodation, utilities and office expenses. Fees paid to Karen Ford, which were in the ordinary course of business and on normal terms and conditions, amounted to A$23,378 (US$24,381) (2012: A$69,075 (US$70,893)). At 30 June 2013 there was an amount outstanding of A$nil (2012: A$10,390 (US$10,559)).

During the half year the Group received US$nil (2012: US$137,500) from PT Bengkulu Utara Gold, which the company has a 30% interest in, in respect of a management fee. At 30 June 2013 there was an amount outstanding of US$nil (2012: US$55,000).

During the half year ended 30 June 2012, Peter Nightingale, a Director at that time, had an interest in an entity, Mining Services Trust, which provided full administrative services, including rental accommodation, administrative staff, services and supplies, to the Group. Fees paid to Mining Services Trust during the half year ended 30 June 2012, which were in the ordinary course of business and on normal terms and conditions, amounted to A$88,221 (US$90,543). At 30 June 2012 there was no amount outstanding.

17. Contingencies

On 12 February 2013, following the receipt of “borrow and use” permits, PT Dwinad Nusa Sejahtera received notification from the forestry services department advising the maximum contingent liability on the Company’s limited production forest area that will be expected to arise from deforestation in the amount of Indonesian Rp 1.5 billion and $US 223,000. This contingent liability requires a bank guarantee of Indonesian Rp 387 million and $US 58,000, equivalent to approximately 25% of the maximum contingent liability.

As part of the permitting process for the Tembang project PT Dwinad Nusa Sejahtera submitted its reclamation plan for Tembang to the Government. This plan estimates that future remediation liabilities for the mine will be $US 1,500,000. PT Dwinad Nusa Sejahtera is required to progressively deposit funds to support this remediation liability over the mine life. Such deposits to support mine reclamation will commence in the second year of production.

For

per

sona

l use

onl

y

SUMATRA COPPER & GOLD PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 30 JUNE 2013

21

18. Commitments 30 June

2013 (Unaudited)

$

31 December 2012

(Restated) $

Expenditure commitments

The Group has certain commitments in relation to orders made for capital equipment. Outstanding commitments are as follows:

Within one year 10,300,000 - Later than one year but not later than five years - -

10,300,000 -

19. Events occurring after the balance sheet date No matter or circumstance has arisen since 30 June 2013 that has significantly affected or may significantly affect the operations, results or state of affairs of the Consolidated Entity in the following or future periods.

For

per

sona

l use

onl

y

For

per

sona

l use

onl

y

For

per

sona

l use

onl

y

![CHAMPION BEER OF SHOW Simon Bourman (Qld.)aabc.org.au/stateresults/AABC2019FullResults.pdf · Julian Robinson VIC Baltic Porter [BJCP 9C] 57 Simon Tongs TAS American Porter [BJCP](https://img.pdfslide.us/doc/110x75/60205775c3833e501c5223f5/champion-beer-of-show-simon-bourman-qldaabcorgaustateresults-julian-robinson.jpg)