Embed Size (px)

Citation preview

Footloose and Fancy Free: A Field Survey of Walkable Urban Places in the Top 30 U.S. Metropolitan Areas

Christopher B. Leinberger

The post-World War II era has witnessed the nearly exclusive building of low density suburbia, here termed “drivable sub-urban” development, as the American metropolitan built environment.. However, over the past 15 years, there has been a gradual shift in how Americans have created their built environment (defined as the real estate, which is generally privately owned, and the infrastructure that supports real estate, majority publicly owned), as demonstrated by the success of the many downtown revitalizations, new urbanism, and transit-oriented development. This has been the result of the re-introduction and expansion of higher density “walkable urban” places. This new trend is the focus of the recently published book, The Option of Urbanism: Investing in a New American Dream (Island Press, November, 2007).

This field survey attempts to identify the number and location of “regional-serving” walkable urban places in the 30 largest American metropolitan areas in the U.S, where 138 million, or 46 percent, of the US population lives. This field survey determines where these walkable urban places are most prevalent on a per capita basis, where they are generally located within the metro area, and the extent to which rail transit service is associated with walkable urban development.

The first section defines the key concepts used in the survey, providing relevant background information for those who have not read The Option of Urbanism. The second section outlines the methodology. The third section, which is the heart of the report, outlines the findings and conclusions of the survey.

Key Concepts

There are a number of key concepts and background information critical to understanding the rise of walkable urban places today. There is a more in-depth discussion of these terms in the book:

• Types of Built Environment Patterns. The built environment is generally marked by two kinds of development patterns—drivable sub-urban and walkable urban. Drivable sub-urban is very low density (floor-area-ratio of between 0.05 and 0.30), modular in nature, uses significantly more land relative to population growth and can generally only be accessed by car or truck. It is conventional suburban development. Walkable urban is:

- at least five times as dense as drivable sub-urban (floor-area-ratio of between 0.8 and upwards to 40.0),

- mixed-use (residential, office, retail, cultural, educational, etc.), - compact (regional-serving walkable urban places, as defined below, are generally between 100

and 500 acres in size), - generally accessible by multiple transportation means (transit, bike, car and walking), and - walkable for nearly every destination once in the place.

Christopher Leinberger is a visiting fellow at the Brookings Institution Metropolitan Policy Program, professor at the University of Michigan, and partner, Arcadia Land Company. He is also the author of The Option of Urbanism: Investing in A New American Dream published by Island Press in November, 2007, on which this field survey is based. He can be contacted at [email protected].

• Functions of Walkable Urban Places. There are two kinds of walkable urban places—local-serving and regional-serving. Local-serving places are primarily bedroom neighborhoods. They are residential in nature with limited commercial venues and instead serve everyday needs (grocery, drug store, etc.). Regional-serving places provide uses that have regional significance, such as employment, retail, medical, entertainment, cultural, higher education, etc., and generally integrates residential as well. This survey focuses only on regional-serving walkable urban places. For ease of usage, the term walkable urban as used in this survey means regional-serving walkable urban places.

• Types of Regional Walkable Urban Places. The book points out that five types of regional-serving walkable urban places have emerged in the country to date and these categories are used in the survey. These include:

- Downtown—the original center city of the largest city in the metropolitan area, though many metropolitan areas are so large that one could argue that there are multiple “original” downtowns, such as the case with downtown Brooklyn and Jersey City in the New York metropolitan area.

- Downtown Adjacent—Immediately adjacent to the original downtown or one or two transit stops away.

- Suburban Town Center—18th or 19th century towns that have been swept up in the growth of the metropolitan area but were laid out before the advent of the car.

- Suburban Redevelopment—failed drivable sub-urban commercial strips or regional malls that have been redeveloped into walkable urbanism.

- Greenfield—a walkable urban place developed on a greenfield site, such as the current trend of developing mixed-use “lifestyle centers” (note: not retail-only lifestyle centers).

• Critical Mass. The walkable urban places named in this survey are at or near “critical mass”. In this survey, critical mass is defined as places where new development projects do not need significant public or private subsidies to proceed with the next new project. There are many more walkable urban places in these 30 metro areas that are not yet at critical mass but probably will be over the next decade. Examples of places that are not yet at critical mass include Mid-Wilshire in Los Angeles, Crossroads in Kansas City, Royal Oak in the Detroit metropolitan area, Columbia Heights in Washington, DC, and nearly every downtown not listed in this field survey.

• Other Walkable Places Not Included in Survey. There are institutions within a metropolitan area that are regional-serving and walkable by their very nature. These include medical campuses, university and college campuses, large corporate headquarters campuses, theme parks, etc. Examples include the Texas Medical Center in Houston, University of California at Santa Cruz, General Motors Tech Center in Warren, Michigan, and Disney World in Orlando. These have not been listed as walkable urban places in this survey unless they have connected to the area immediately around their campuses, acting as an anchor in sparking walkable urban development on adjacent property.

• Maturity of Rail Transit System. The definition of the extent of a metropolitan rail transit system (which includes heavy rail, light rail, commuter rail and street car) in the survey is divided into four categories, using the judgment of the author:

- Full—The bulk of the inner suburbs and center city is served by a rail transit system, connecting many walkable urban places.

- Partial—A significant portion of the inner suburbs and center city is served by rail transit, connecting some walkable urban places.

- Starter—An initial transit line or two lines have been built serving a small portion of the inner suburbs and center city, connecting a few walkable urban places.

- None—no rail transit, though there may be rail circulator systems within a walkable urban place (the Las Vegas Strip monorail, Detroit’s downtown people mover, etc.), which is not counted due to the limited geography served.

Methodology

The walkable urban places identified in this field survey are based on the experience and observations of the author, who has been active as a real estate consultant, researcher, and developer for the past 30 years. He has worked in every one of these metropolitan areas. Those observations have been supplemented by the managing directors of Robert Charles Lesser & Co, an international consulting firm, Brookings Institution scholars, public officials, real estate developers, architectural critics, downtown business improvement managers, public officials, and academics, among others. This experience has been further complemented by web-based searches.

This field survey represents only a first step at understanding the breadth of walkable urban development in the country, which requires a more rigorous, systemic review. The most important caveat which needs to be corrected in future surveys relates to the lack of a meaningful measure of the size of each walkable urban place. The walkable urban places in New York are among the largest in the country; for example, Midtown Manhattan has over 300 million square feet of office space, tens of thousands of residential units and hotel rooms and millions of square feet of retail; by far the largest walkable urban place in the country. Yet in the survey calculation of the number of walkable urban places per capita, Midtown Manhattan is weighed the same as Reston Town Center in Washington, DC, which probably has around 1/30th of the office, residential, hotels and retail space. Therefore, size criteria need to be incorporated into the survey in the future.

A more rigorous definition of a regional-serving walkable urban place also needs to be developed. Still unclear is the best street-by-street definition to use to demarcate walkable urban place. For example, what are the discrete boundaries of Midtown Manhattan versus Chelsea, as defined by the market?

The definition of “critical mass” needs more rigorous definition. It has always been a concept somewhat like the judicial understanding of pornography; one knows it when one sees it. This survey applied the notion that critical mass is being near or past the point in time when the next real estate development project does not need government or private gap financing to make it financially feasible. This is a good first step but requires much more rigor and standardized measures in future research.

Results of the Survey

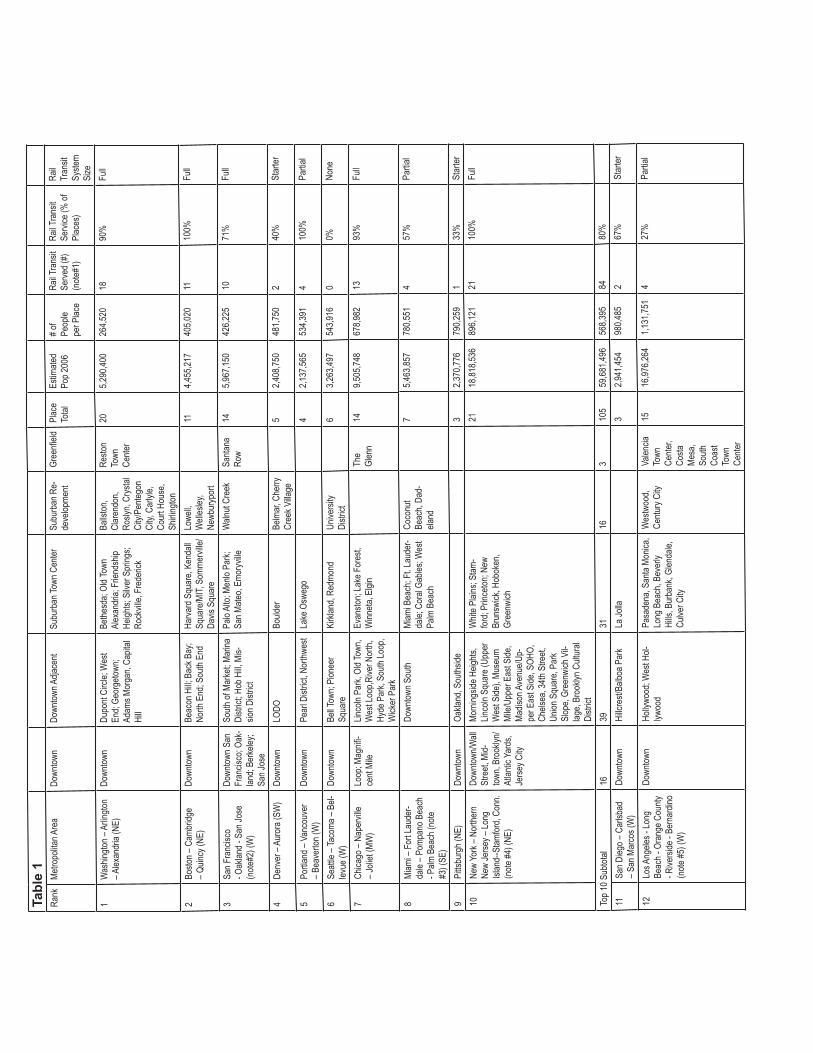

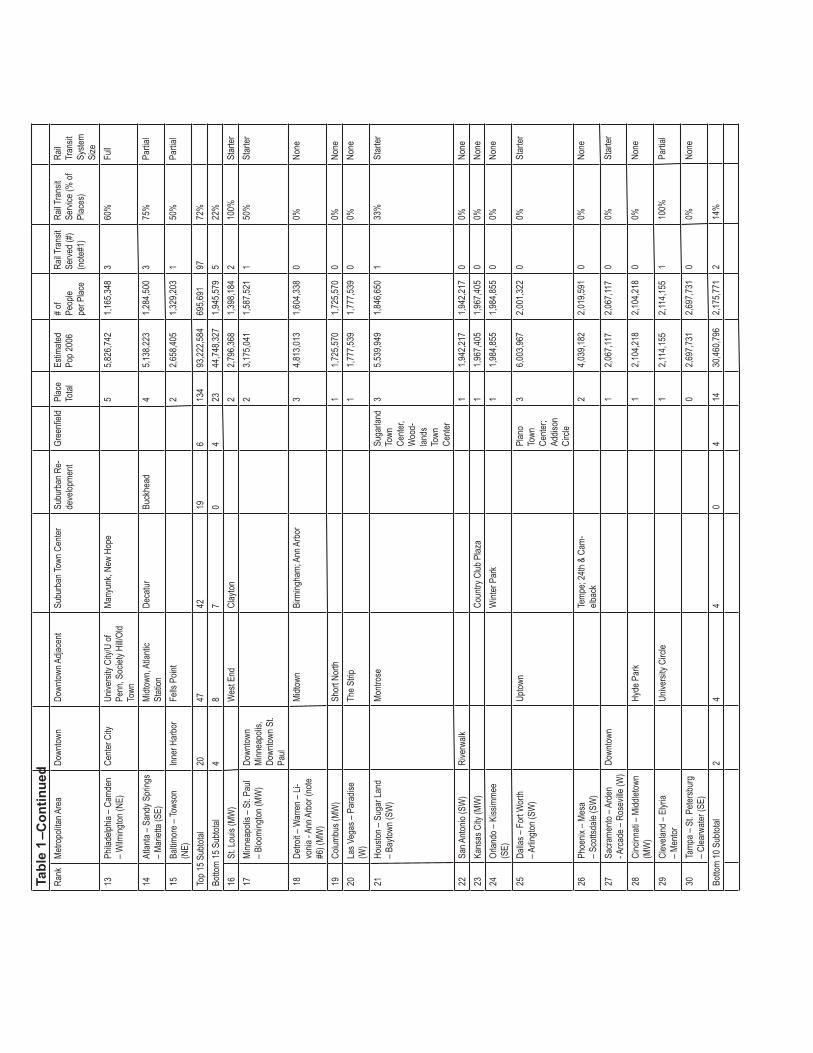

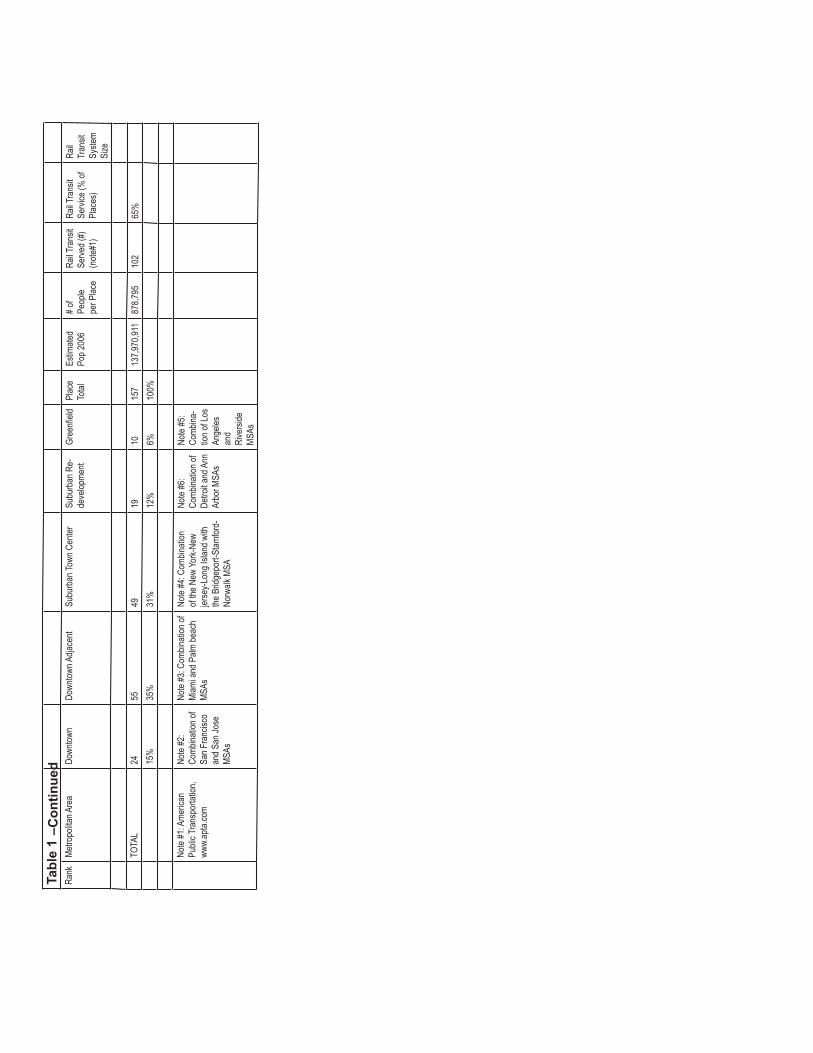

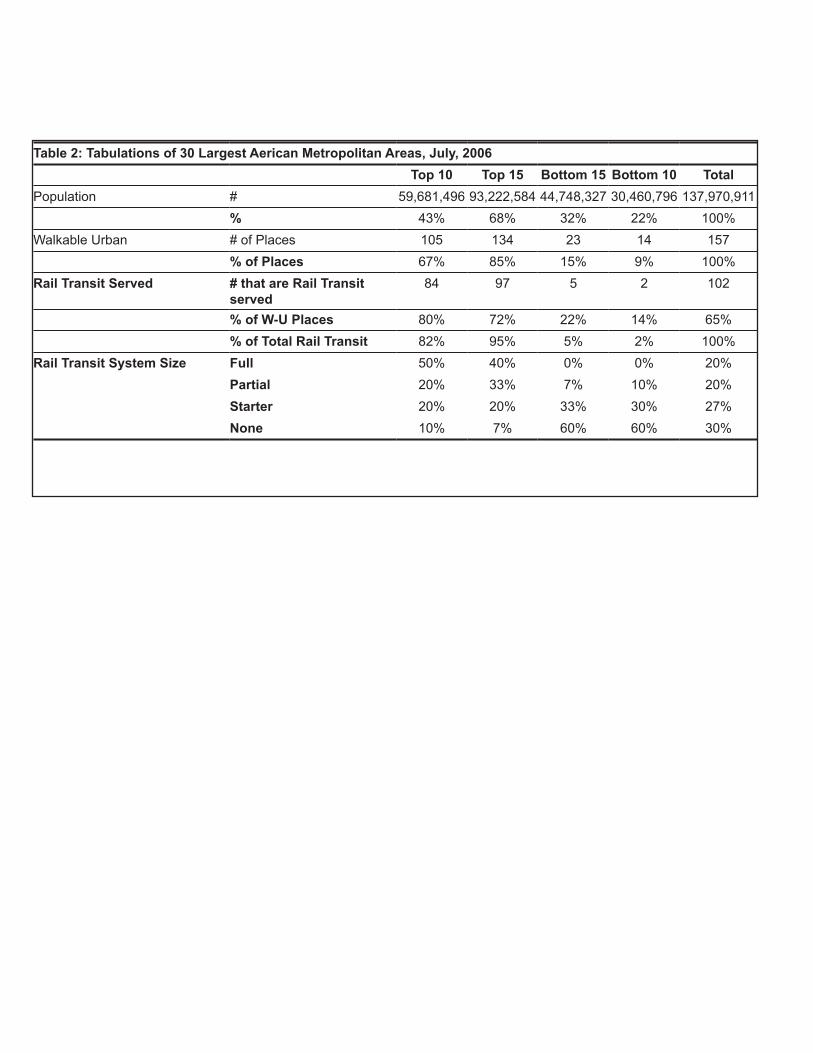

The survey results for the 30 largest metropolitan areas are found in Table 1. The metropolitan areas are ranked according to the number of people in the metropolitan area per regional-serving walkable urban place. Thus, the metro area with the lowest number of people needed to support a walkable urban place is the most advanced in developing walkable urbanism; the equivalent of the most walkable urban places per capita. The summary tabulations are in Table 2, which ranks the 30 metro areas by their ratio of walkable urban places to total population. This divides the 30 metropolitan areas into clusters of the top 10 most walkable urban, top 15, bottom 15 and bottom 10 for comparative purposes.

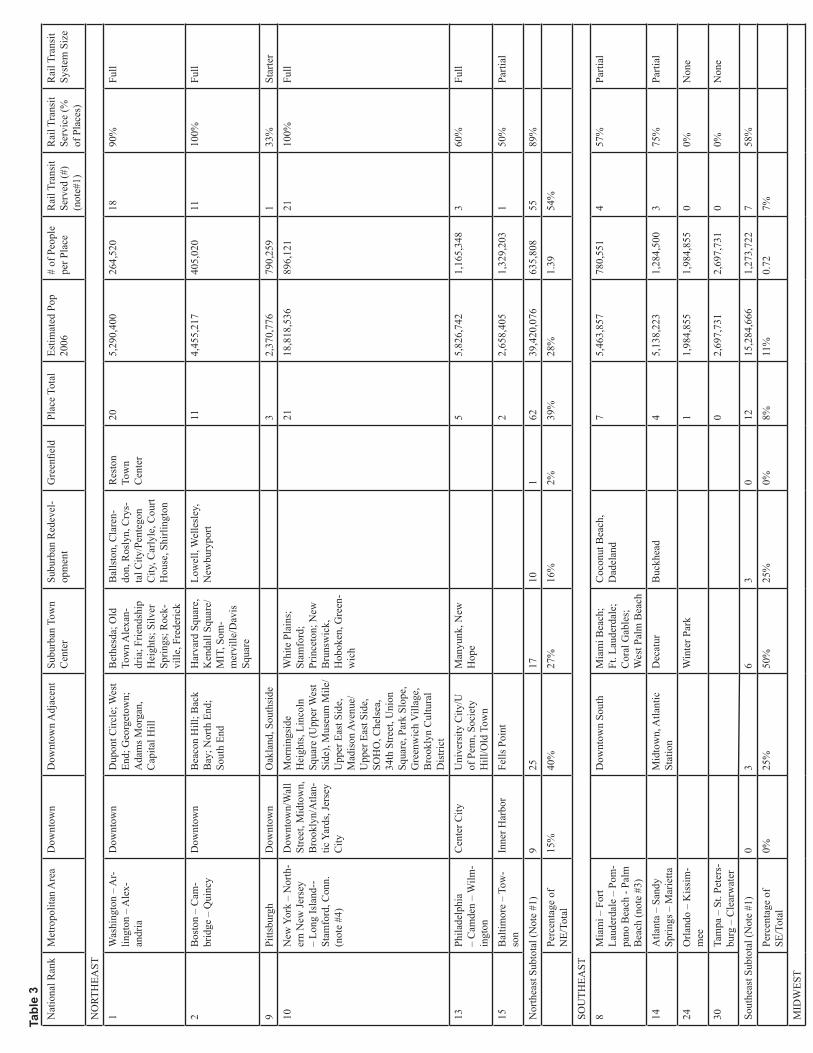

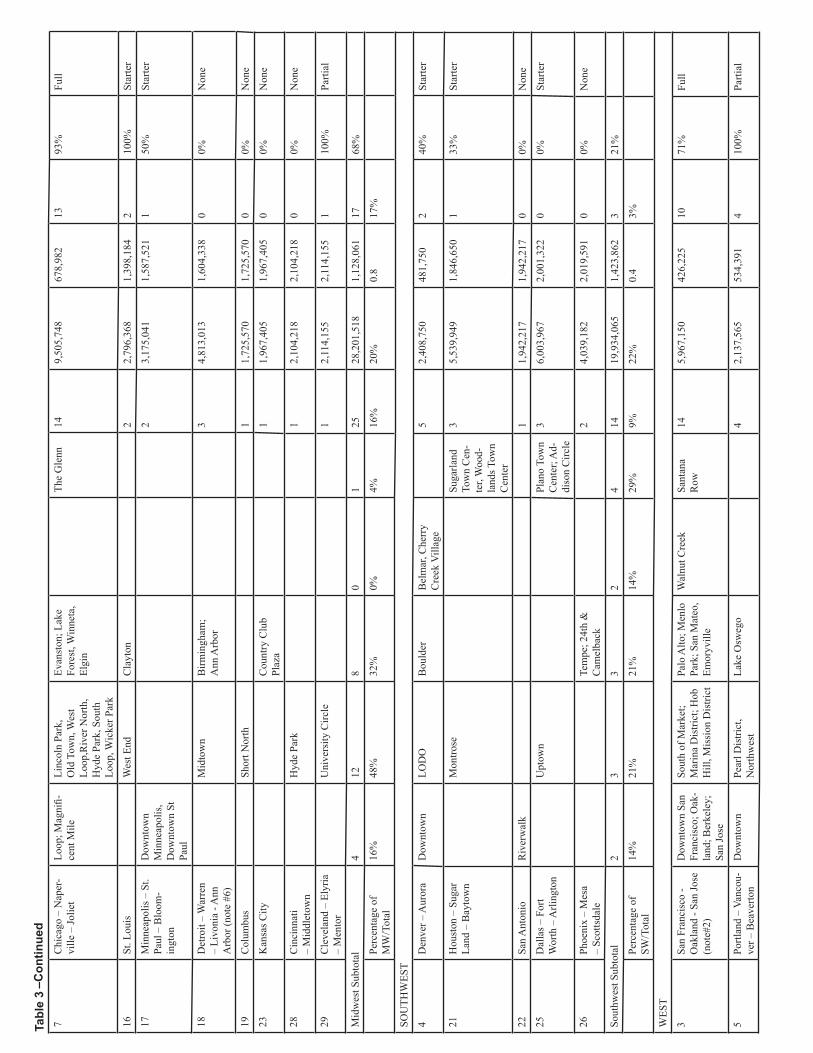

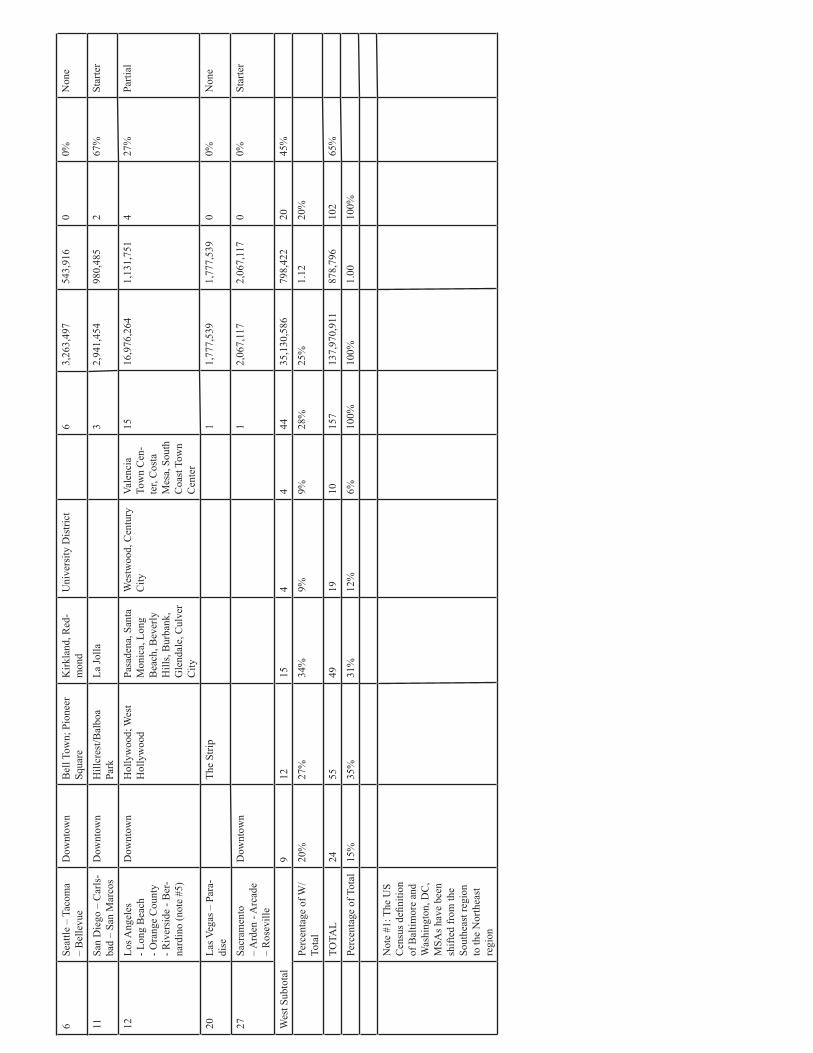

The base data is re-tabulated by region (Northeast, Southeast, Midwest, Southwest and West) in Table 3.

The key survey findings are:

1. There are 157 Walkable Urban Places in the Largest 30 Metro Areas in the Country—There are regional-serving walkable urban places at or near critical mass in nearly every surveyed metro area (29 of the 30). This is significant as the best way of encouraging the development of walkable urban places is to have hometown examples to demonstrate their function and market acceptance. While comparisons over time can be only impressionistic, one can safely assume that these 30 metropolitan areas probably had very few walkable urban places 20 years ago. For example, the Denver metropolitan area did not exhibit any regional-serving walkable urban places as of 1987; downtown was an office-only place with few residents, cultural attractions, or retail while the rest of the region was basically drivable sub-urban in nature. This survey identifies five regional-serving walkable urban places in the Denver region today. Many times that number are in the planning stages due to a

comprehensive new rail transit system that is funded and in the construction planning stage, building on an existing starter system.

2. There Are an Equal Number of Walkable Urban Places in the Center Cities and the Suburbs—While there has been much attention on the revival of American downtowns over the past 10 years, the revival of suburban downtowns, the redevelopment of failed regional malls and strip centers, and the recent emergence of lifestyle centers appears to be an equally dynamic trend. Today, walkable urban places are just as likely to be found in the suburbs as in center cities.

3. The Largest Number by Type of Walkable Urban Places are Those That are Downtown Adjacent— There are more examples of downtown adjacent walkable urban place than any other type in the largest 30 metropolitan areas; 55 of 157 or 35%. It is too soon since the beginning of the walkable urban development trend to determine why this is the situation. It may be a reflection of the market appeal of this specific type of walkable urban place. For example, it may be that a downtown adjacent place can offer more housing and commercial product options than the downtown, thus appealing to broader market segments. In Midtown Manhattan, stacked flats are the predominate residential offering. Yet the downtown adjacent Lincoln Square/Upper Westside offers stacked flats and townhouses. Some downtown adjacent places, such as Midtown in Atlanta, also offers single family housing in addition to higher density product.

4. Washington, DC, Could be the National Model of Walkable Urban Growth—The Washington, DC, metropolitan area has the most regional-serving walkable urban places per capita in the country, having one for every 264,000 people, and one of each of the five types of walkable urban places. Washington also has the second highest absolute number of walking urban places with 20 (compared to two in 1987, Georgetown and Old Town Alexandria, both tourist dependent at the time). The Washington metro area also has at least another 10 regional-serving walkable urban places emerging that could reach critical mass over the next five toten years. Twenty years ago, the Washington metro area only had two walkable urban places. The two major reasons for the high number of walkable urban places in Washington are (1) the success of the Metro rail system and (2) the aggressive use of “overlay zoning districts” that allow and promote walkable urbanism around Metro stations. Other reasons include the region’s strong economic growth over the past 15 years when the trend toward walkable urban development began, the high educational level of the population (the highest percentage of college graduates of all metro areas in the country according to the US Census in 2006), given the apparent, though not yet proven, propensity of the highly educated to prefer walkable urban development. It is also assisted by the large percentage of younger adults in their 20s and 30s that migrate to the region for employment opportunities and for the walkable urban lifestyle. Younger adults appear to have a higher propensity, though not proven, for walkable urbanism as well. The result is that the Washington region could be the probable model for the direction the country’s other metro areas are heading over the next generation.

5. New York Metro Area Has the Highest Number of Most Walkable Urban Places--The New York metro area, generally considered to be the most walkable urban metro area in the country, has the most discrete number of places that are walkable urban (21). However, it is ranked as the 10th most number of walkable urban places on a per capita basis. This lower ranking is due to its nearly 19 million population base (for example, compared to Washington’s 5.3 million population), resulting in one walkable urban place for every 896, 000 people (though the major caveat mentioned above in the methodology section needs to be taken into consideration). The extent and availability of drivable sub-urban development, as demonstrated by the metro area’s huge physical size stretching over four states (New York, New Jersey, Pennsylvania and Connecticut), belies its image as the leading walkable urban metro area in the country. However, the New York metro area has the largest walkable urban places in size as measured by any criteria. As mentioned above, Midtown Manhattan is the largest walkable urban place in the country regarding office square footage and probably many other kinds of real estate product types. For all of the walkable urbanism that Manhattan is justly known for, the bough is only 8.5 percent of the total population of the metro area.

6. Rail Transit Seems to Play a Significant Role in Catalyzing Walkable Urban Development—The relationship between rail transit and the existence of walkable urban places is very strong with 65 percent of the walkable urban places being served by rail transit service. In the top 10 metro areas for per capita walkable urban places, 80 percent (84 of 105) of these places have rail transit service. In the bottom 10 metro areas, only 14 percent (2 of 14) of the walkable urban places have rail transit service. In addition, the top 10 metro areas for per capita walkable urban places have five of the six full service rail systems and nine of the 10 have some level of rail transit service. The bottom 10 metro areas include six with no rail transit, one partial system and three starter systems. That 18 of 20 walkable urban places in Washington and 21 of 21 in New York have rail transit is rather convincing that having it is extremely beneficial for the emergence of walkable urbanism. However, rail transit is not absolutely essential for walkable urbanism to emerge since 35 percent of the walkable urban places do not have rail transit. For example, Reston Town Center, Valencia Town Center, Plano Town Center, etc., are walkable urban places identified in the survey, but do not have rail transit, relying nearly completely on car and truck transportation. However, many of the non-rail served walkable urban places in the survey (for example, Reston Town Center) have plans to be rail-served in the short-term; a condition referred to as being “transit-ready.”

7. Metro Areas with Old Rail Transit Systems Have a Greater Likelihood of Walkable Urbanism May be a Myth—Much less than half of the top 15 per capita walkable urban metro areas in the survey contain the nation’s oldest rail transit systems. Specifically, four of the top 15 are characterized by old rail transit systems, generally built in the early 20th century (Boston, Chicago,, New York, Philadelphia). However, of this top tier, one does not have rail transit (Seattle) and the remaining ten have the most recent rail transit systems, built since the 1970s. Most of the top ranked metro areas in walkable urbanism have recent rail transit systems (Washington, San Francisco, Denver, Portland, Pittsburgh, Miami, among others). This could indicate that a metro area with a newer rail transit system can catch up with and even pass the older rail transit metro areas in walkable urban development on a per capita basis.

8. Regional Differences Show that the Northeast and West Coast Have a Greater Prevalence of Walkable Urban Development—The Northeast and West Coast metropolitan areas, as shown in table #3, have a higher likelihood to have walkable urban places than the national average and the other three sections of the country, the Southeast, Midwest and Southwest. The Northeast has the highest likelihood; 39 percent greater propensity than the average for the surveyed metro areas. The Northeast and Midwest have a higher likelihood to have downtown and downtown adjacent places to be walkable urban than their suburbs; 57 percent of their walkable urban places are in the central city versus a national average of 50 percent, as mentioned above. The Southeast and Southwest are more likely to have suburban walkable urban places; 59 percent of these region’s walkable urban places are in the suburbs versus a national average of 50 percent. The West is at about the national average; it has 47 percent of its walkable urban places in the center city versus a national average of 50 percent. Note that this report has made some changes regarding the US Census regional boundaries; Baltimore and Washington, DC, MSAs have been considered in the Northeast region, not the Southeast region.

9. There is the Potential for the Development of Many Additional Walkable Urban Places—There is a wide range of population that currently supports each regional-serving walkable urban place in the survey in the different metropolitan areas. The top 10 metro areas have one walkable urban place per 568,000 people while the bottom 10 metro areas have one per 2,156,000 people, nearly four times the ratio. If the bottom 10 metropolitan areas developed as many walkable urban places on a per capita basis as the top 10 have done to date, there would be approximately 40 additional walkable urban places developed in these metro areas, probably representing tens of billions of dollars of real estate development.

10. A Tale of Two Kinds of Metropolitan Areas May be Evolving: Those Metros Benefiting from the Trend Toward Walkable Urbanism and Those Out of Position—There appears to be a wide gap between metropolitan areas that have many walkable urban places and those that have only one or two. The top 15 in the survey have 134 of the 157 walkable urban places identified; 85 percent of the total for the 30 largest metro areas, even though they are home to 68 percent of the population. The top 15 metro areas also have the preponderance of full or partial rail transit systems and thus 95 percent of the rail transit-served walkable urban places, which re-enforces the apparent connection between rail transit and walkable urbanism as discussed above. It may be possible that if action is not taken with regard to rail transit, a “have” versus “have not” gap may appear in American metropolitan areas. Additionally, those metro areas that do not have high level of walkable urban development nor extensive rail transit seem to fall into two categories. Many of the metropolitan areas near the bottom of the survey that have experienced some of the fastest population growth in the nation (e.g., Phoenix, Dallas-Ft. Worth, Houston) have starter transit systems and/or plans for extensive rail transit. These metro areas seem to be positioning themselves to take advantage of walkable urban demand even if they have not fully done so as of yet. It appears that these fast growth metros are emulating highly ranked walkable urban metros like Denver, Portland, and San Diego that built rail systems over the past 10–15 years. Metropolitan areas that are not seriously committed to building rail transit systems—such as Cincinnati, Detroit, and Kansas City—may not have the option of walkable urban development due to slower economic growth and weak tax base. These slow growing metropolitan areas without rail transit today may be at a competitive disadvantage regarding future economic growth. This will especially be the case if crude oil prices continue to rise as they have since 2002 (increasing nearly three fold). These metropolitan areas may have “painted themselves into a corner”, due to both rising energy costs and the market opportunity of walkable urban development.

Conclusion

The number and growth of regional-serving walkable urban places is significant in many metropolitan areas in the country and is clearly emerging in both cities and suburbs. The probable correlation between walkable urban development and rail transit, while not definitively proven by this field survey, supports the intuitive relationship between them. This field survey also points out the need to gather real estate and transit data in a different manner; distinguishing between walkable urban and drivable sub-urban places. As the research in the book, The Option of Urbanism; Investing in a New American Dream, points out, these two kinds of places appear to perform fundamentally differently in how they lay out on the ground and how they perform regarding market acceptance, financial performance, rental rates/sales prices, tax revenue generation, and environmental sustainability. Finally, infrastructure investment, particularly in rail transit, and revised zoning regulations should be seriously considered by metropolitan area governments that are not seeing growth in this type of development pattern.

Tabl

e 1

Rank

Metro

polita

n Are

aDo

wntow

nDo

wntow

n Adja

cent

Subu

rban

Town

Cen

terSu

burb

an R

e-de

velop

ment

Gree

nfield

Plac

e To

tal

Estim

ated

Pop 2

006

# of

Peop

le pe

r Plac

e

Rail T

rans

it Se

rved (

#)

(note

#1)

Rail T

rans

it Se

rvice

(% of

Pl

aces

)

Rail

Tran

sit

Syste

m Si

ze

1W

ashin

gton –

Arlin

gton

– Alex

andr

ia (N

E)Do

wntow

nDu

pont

Circl

e; W

est

End;

Geor

getow

n; Ad

ams M

orga

n, Ca

pital

Hill

Bethe

sda;

Old T

own

Alex

andr

ia; F

riend

ship

Heigh

ts; S

ilver

Spr

ings;

Rock

ville,

Fre

deric

k

Balls

ton,

Clar

endo

n, Ro

slyn,

Crys

tal

City/

Pente

gon

City,

Car

lyle,

Cour

t Hou

se,

Shirli

ngton

Resto

n To

wn

Cente

r

205,2

90,40

026

4,520

1890

%Fu

ll

2Bo

ston –

Cam

bridg

e – Q

uincy

(NE)

Down

town

Beac

on H

ill; B

ack B

ay;

North

End

; Sou

th En

dHa

rvard

Squ

are,

Kend

all

Squa

re/M

IT, S

omme

rville

/Da

vis S

quar

e

Lowe

ll, W

elles

ley,

Newb

uryp

ort

114,4

55,21

740

5,020

1110

0%Fu

ll

3Sa

n Fra

ncisc

o - O

aklan

d - S

an Jo

se

(note

#2) (

W)

Down

town S

an

Fran

cisco

; Oak

-lan

d; Be

rkeley

; Sa

n Jos

e

South

of M

arke

t; Mar

ina

Distr

ict; H

ob H

ill, M

is-sio

n Dist

rict

Palo

Alto;

Men

lo Pa

rk;

San M

ateo,

Emor

yville

Waln

ut Cr

eek

Santa

na

Row

145,9

67,15

042

6,225

1071

%Fu

ll

4De

nver

– Au

rora

(SW

)Do

wntow

nLO

DOBo

ulder

Belm

ar, C

herry

Cr

eek V

illage

52,4

08,75

048

1,750

240

%St

arter

5Po

rtland

– Va

ncou

ver

– Bea

verto

n (W

)Do

wntow

nPe

arl D

istric

t, Nor

thwes

tLa

ke O

sweg

o4

2,137

,565

534,3

914

100%

Partia

l

6Se

attle

– Tac

oma –

Bel-

levue

(W)

Down

town

Bell T

own;

Pion

eer

Squa

reKi

rklan

d, Re

dmon

dUn

iversi

ty Di

strict

63,2

63,49

754

3,916

00%

None

7Ch

icago

– Na

pervi

lle

– Joli

et (M

W)

Loop

; Mag

nifi-

cent

Mile

Linco

ln Pa

rk, O

ld To

wn,

Wes

t Loo

p,Rive

r Nor

th,

Hyde

Par

k, So

uth Lo

op,

Wick

er P

ark

Evan

ston;

Lake

For

est,

Winn

eta, E

lgin

The

Glen

n14

9,505

,748

678,9

8213

93%

Full

8Mi

ami –

For

t Lau

der-

dale

– Pom

pano

Bea

ch

- Palm

Bea

ch (n

ote

#3) (

SE)

Down

town S

outh

Miam

i Bea

ch; F

t. Lau

der-

dale;

Cor

al Ga

bles;

Wes

t Pa

lm B

each

Coco

nut

Beac

h, Da

d-ela

nd

75,4

63,85

778

0,551

457

%Pa

rtial

9Pi

ttsbu

rgh (

NE)

Down

town

Oakla

nd, S

ouths

ide3

2,370

,776

790,2

591

33%

Star

ter

10Ne

w Yo

rk – N

orthe

rn

New

Jerse

y – Lo

ng

Islan

d--S

tamfor

d, Co

nn.

(note

#4) (

NE)

Down

town/W

all

Stre

et, M

id-tow

n, Br

ookly

n/At

lantic

Yar

ds,

Jerse

y City

Morn

ingsid

e Heig

hts,

Linco

ln Sq

uare

(Upp

er

Wes

t Side

), Mu

seum

Mi

le/Up

per E

ast S

ide,

Madis

on A

venu

e/Up-

per E

ast S

ide, S

OHO,

Ch

elsea

, 34th

Stre

et,

Union

Squ

are,

Park

Slop

e, Gr

eenw

ich V

il-lag

e, Br

ookly

n Cult

ural

Distr

ict

Whit

e Plai

ns; S

tam-

ford;

Princ

eton;

New

Brun

swick

, Hob

oken

, Gr

eenw

ich

2118

,818,5

3689

6,121

2110

0%Fu

ll

Top 1

0 Sub

total

1639

3116

310

559

,681,4

9656

8,395

8480

%

11Sa

n Dieg

o – C

arlsb

ad

– San

Mar

cos (

W)

Down

town

Hillc

rest/

Balbo

a Par

kLa

Jolla

32,9

41,45

498

0,485

267

%St

arter

12Lo

s Ang

eles -

Long

Be

ach -

Ora

nge C

ounty

- R

iversi

de -

Bern

ardin

o (n

ote #5

) (W

)

Down

town

Holly

wood

; Wes

t Hol-

lywoo

dPa

sade

na, S

anta

Monic

a, Lo

ng B

each

, Bev

erly

Hills

, Bur

bank

, Glen

dale,

Cu

lver C

ity

Wes

twoo

d, Ce

ntury

City

Valen

cia

Town

Ce

nter,

Costa

Me

sa,

South

Co

ast

Town

Ce

nter

1516

,976,2

641,1

31,75

14

27%

Partia

l

Tabl

e 1

Rank

Metro

polita

n Are

aDo

wntow

nDo

wntow

n Adja

cent

Subu

rban

Town

Cen

terSu

burb

an R

e-de

velop

ment

Gree

nfield

Plac

e To

tal

Estim

ated

Pop 2

006

# of

Peop

le pe

r Plac

e

Rail T

rans

it Se

rved (

#)

(note

#1)

Rail T

rans

it Se

rvice

(% of

Pl

aces

)

Rail

Tran

sit

Syste

m Si

ze13

Phila

delph

ia – C

amde

n – W

ilming

ton (N

E)Ce

nter C

ityUn

iversi

ty Ci

ty/U

of Pe

nn, S

ociet

y Hill/

Old

Town

Many

unk,

New

Hope

55,8

26,74

21,1

65,34

83

60%

Full

14At

lanta

– San

dy S

pring

s – M

ariet

ta (S

E)Mi

dtown

, Atla

ntic

Stati

onDe

catur

Buck

head

45,1

38,22

31,2

84,50

03

75%

Partia

l

15Ba

ltimor

e – To

wson

(N

E)Inn

er H

arbo

rFe

lls P

oint

22,6

58,40

51,3

29,20

31

50%

Partia

l

Top 1

5 Sub

total

2047

4219

613

493

,222,5

8469

5,691

9772

%Bo

ttom

15 S

ubtot

al4

87

04

2344

,748,3

271,9

45,57

95

22%

16St

. Lou

is (M

W)

Wes

t End

Clay

ton2

2,796

,368

1,398

,184

210

0%St

arter

17Mi

nnea

polis

– St

. Pau

l – B

loomi

ngton

(MW

)Do

wntow

n Mi

nnea

polis

, Do

wntow

n St.

Paul

23,1

75,04

11,5

87,52

11

50%

Star

ter

18De

troit –

War

ren –

Li-

vonia

- Ann

Arb

or (n

ote

#6) (

MW)

Midto

wnBi

rming

ham;

Ann

Arb

or3

4,813

,013

1,604

,338

00%

None

19Co

lumbu

s (MW

)Sh

ort N

orth

11,7

25,57

01,7

25,57

00

0%No

ne20

Las V

egas

– Pa

radis

e (W

)Th

e Strip

11,7

77,53

91,7

77,53

90

0%No

ne

21Ho

uston

– Su

gar L

and

– Bay

town (

SW)

Montr

ose

Suga

rland

To

wn

Cente

r, W

ood-

lands

To

wn

Cente

r

35,5

39,94

91,8

46,65

01

33%

Star

ter

22Sa

n Anto

nio (S

W)

Rive

rwalk

11,9

42,21

71,9

42,21

70

0%No

ne23

Kans

as C

ity (M

W)

Coun

try C

lub P

laza

11,9

67,40

51,9

67,40

50

0%No

ne24

Orlan

do –

Kiss

imme

e (S

E)W

inter

Par

k1

1,984

,855

1,984

,855

00%

None

25Da

llas –

For

t Wor

th – A

rlingto

n (SW

)Up

town

Plan

o To

wn

Cente

r; Ad

dison

Ci

rcle

36,0

03,96

72,0

01,32

20

0%St

arter

26Ph

oenix

– Me

sa

– Sco

ttsda

le (S

W)

Temp

e; 24

th &

Cam-

elbac

k2

4,039

,182

2,019

,591

00%

None

27Sa

crame

nto –

Arde

n - A

rcade

– Ro

sevil

le (W

)Do

wntow

n1

2,067

,117

2,067

,117

00%

Star

ter

28Ci

ncinn

ati –

Midd

letow

n (M

W)

Hyde

Par

k1

2,104

,218

2,104

,218

00%

None

29Cl

evela

nd –

Elyri

a – M

entor

Unive

rsity

Circl

e1

2,114

,155

2,114

,155

110

0%Pa

rtial

30Ta

mpa –

St. P

etersb

urg

– Clea

rwate

r (SE

)0

2,697

,731

2,697

,731

00%

None

Botto

m 10

Sub

total

24

40

414

30,46

0,796

2,175

,771

214

%

–Con

tinue

d

Tabl

e 1

Rank

Metro

polita

n Are

aDo

wntow

nDo

wntow

n Adja

cent

Subu

rban

Town

Cen

terSu

burb

an R

e-de

velop

ment

Gree

nfield

Plac

e To

tal

Estim

ated

Pop 2

006

# of

Peop

le pe

r Plac

e

Rail T

rans

it Se

rved (

#)

(note

#1)

Rail T

rans

it Se

rvice

(% of

Pl

aces

)

Rail

Tran

sit

Syste

m Si

ze

TOTA

L24

5549

1910

157

137,9

70,91

187

8,795

102

65%

15%

35%

31%

12%

6%10

0%

Note

#1: A

meric

an

Publi

c Tra

nspo

rtatio

n, ww

w.ap

ta.co

m

Note

#2:

Comb

inatio

n of

San F

ranc

isco

and S

an Jo

se

MSAs

Note

#3: C

ombin

ation

of

Miam

i and

Palm

beac

h MS

As

Note

#4: C

ombin

ation

of

the N

ew Yo

rk-Ne

w jer

sey-L

ong I

sland

with

the

Brid

gepo

rt-St

amfor

d-No

rwalk

MSA

Note

#6:

Comb

inatio

n of

Detro

it and

Ann

Ar

bor M

SAs

Note

#5:

Comb

ina-

tion o

f Los

An

geles

an

d Ri

versi

de

MSAs

–Con

tinue

d

Table 2: Tabulations of 30 Largest Aerican Metropolitan Areas, July, 2006Top 10 Top 15 Bottom 15 Bottom 10 Total

Population # 59,681,496 93,222,584 44,748,327 30,460,796 137,970,911% 43% 68% 32% 22% 100%

Walkable Urban # of Places 105 134 23 14 157% of Places 67% 85% 15% 9% 100%

Rail Transit Served # that are Rail Transit served

84 97 5 2 102

% of W-U Places 80% 72% 22% 14% 65%% of Total Rail Transit 82% 95% 5% 2% 100%

Rail Transit System Size Full 50% 40% 0% 0% 20%Partial 20% 33% 7% 10% 20%Starter 20% 20% 33% 30% 27%None 10% 7% 60% 60% 30%

Table 2: Tabulations of 30 Largest Aerican Metropolitan Areas, July, 2006Top 10 Top 15 Bottom 15 Bottom 10 Total

Population # 59,681,496 93,222,584 44,748,327 30,460,796 137,970,911% 43% 68% 32% 22% 100%

Walkable Urban # of Places 105 134 23 14 157% of Places 67% 85% 15% 9% 100%

Rail Transit Served # that are Rail Transit served

84 97 5 2 102

% of W-U Places 80% 72% 22% 14% 65%% of Total Rail Transit 82% 95% 5% 2% 100%

Rail Transit System Size Full 50% 40% 0% 0% 20%Partial 20% 33% 7% 10% 20%Starter 20% 20% 33% 30% 27%None 10% 7% 60% 60% 30%

Nat

iona

l Ran

kM

etro

polit

an A

rea

Dow

ntow

nD

ownt

own

Adj

acen

tSu

burb

an T

own

Cen

ter

Subu

rban

Red

evel

-op

men

tG

reen

field

Plac

e To

tal

Estim

ated

Pop

20

06#

of P

eopl

e pe

r Pla

ceR

ail T

rans

it Se

rved

(#)

(not

e#1)

Rai

l Tra

nsit

Serv

ice

(%

of P

lace

s)

Rai

l Tra

nsit

Syst

em S

ize

NO

RTH

EAST

1W

ashi

ngto

n –

Ar-

lingt

on –

Ale

x-an

dria

Dow

ntow

nD

upon

t Circ

le; W

est

End;

Geo

rget

own;

A

dam

s Mor

gan,

C

apita

l Hill

Bet

hesd

a; O

ld

Tow

n A

lexa

n-dr

ia; F

riend

ship

H

eigh

ts; S

ilver

Sp

rings

; Roc

k-vi

lle, F

rede

rick

Bal

lsto

n, C

lare

n-do

n, R

osly

n, C

rys-

tal C

ity/P

ente

gon

City

, Car

lyle

, Cou

rt H

ouse

, Shi

rling

ton

Res

ton

Tow

n C

ente

r

205,

290,

400

264,

520

1890

%Fu

ll

2B

osto

n –

Cam

-br

idge

– Q

uinc

yD

ownt

own

Bea

con

Hill

; Bac

k B

ay; N

orth

End

; So

uth

End

Har

vard

Squ

are,

K

enda

ll Sq

uare

/M

IT, S

om-

mer

ville

/Dav

is

Squa

re

Low

ell,

Wel

lesl

ey,

New

bury

port

114,

455,

217

405,

020

1110

0%Fu

ll

9Pi

ttsbu

rgh

Dow

ntow

nO

akla

nd, S

outh

side

32,

370,

776

790,

259

133

%St

arte

r

10N

ew Y

ork

– N

orth

-er

n N

ew Je

rsey

–

Long

Isla

nd--

Stam

ford

, Con

n.

(not

e #4

)

Dow

ntow

n/W

all

Stre

et, M

idto

wn,

B

rook

lyn/

Atla

n-tic

Yar

ds, J

erse

y C

ity

Mor

ning

side

H

eigh

ts, L

inco

ln

Squa

re (U

pper

Wes

t Si

de),

Mus

eum

Mile

/U

pper

Eas

t Sid

e,

Mad

ison

Ave

nue/

Upp

er E

ast S

ide,

SO

HO

, Che

lsea

, 34

th S

treet

, Uni

on

Squa

re, P

ark

Slop

e,

Gre

enw

ich

Vill

age,

B

rook

lyn

Cul

tura

l D

istri

ct

Whi

te P

lain

s;

Stam

ford

; Pr

ince

ton;

New

B

runs

wic

k,

Hob

oken

, Gre

en-

wic

h

2118

,818

,536

896,

121

2110

0%Fu

ll

13Ph

ilade

lphi

a –

Cam

den

– W

ilm-

ingt

on

Cen

ter C

ityU

nive

rsity

City

/U

of P

enn,

Soc

iety

H

ill/O

ld T

own

Man

yunk

, New

H

ope

55,

826,

742

1,16

5,34

83

60%

Full

15B

altim

ore

– To

w-

son

Inne

r Har

bor

Fells

Poi

nt2

2,65

8,40

51,

329,

203

150

%Pa

rtial

Nor

thea

st S

ubto

tal (

Not

e #1

)9

2517

101

6239

,420

,076

635,

808

5589

%

Perc

enta

ge o

f N

E/To

tal

15%

40%

27%

16%

2%39

%28

%1.

3954

%

SOU

THEA

ST

8M

iam

i – F

ort

Laud

erda

le –

Pom

-pa

no B

each

- Pa

lm

Bea

ch (n

ote

#3)

Dow

ntow

n So

uth

Mia

mi B

each

; Ft

. Lau

derd

ale;

C

oral

Gab

les;

W

est P

alm

Bea

ch

Coc

onut

Bea

ch,

Dad

elan

d7

5,46

3,85

778

0,55

14

57%

Parti

al

14A

tlant

a –

Sand

y Sp

rings

– M

arie

tta

Mid

tow

n, A

tlant

ic

Stat

ion

Dec

atur

Buc

khea

d4

5,13

8,22

31,

284,

500

375

%Pa

rtial

24O

rland

o –

Kis

sim

-m

ee

Win

ter P

ark

11,

984,

855

1,98

4,85

50

0%N

one

30Ta

mpa

– S

t. Pe

ters

-bu

rg –

Cle

arw

ater

0

2,69

7,73

12,

697,

731

00%

Non

e

Sout

heas

t Sub

tota

l (N

ote

#1)

03

63

012

15,2

84,6

661,

273,

722

758

%

Perc

enta

ge o

f SE

/Tot

al0%

25%

50%

25%

0%8%

11%

0.72

7%

MID

WES

T

Tabl

e 3

–Con

tinue

d7

Chi

cago

– N

aper

-vi

lle –

Jolie

t Lo

op; M

agni

fi-ce

nt M

ileLi

ncol

n Pa

rk,

Old

Tow

n, W

est

Loop

,Riv

er N

orth

, H

yde

Park

, Sou

th

Loop

, Wic

ker P

ark

Evan

ston

; Lak

e Fo

rest

, Win

neta

, El

gin

The

Gle

nn14

9,50

5,74

867

8,98

213

93%

Full

16St

. Lou

is

Wes

t End

Cla

yton

22,

796,

368

1,39

8,18

42

100%

Star

ter

17M

inne

apol

is –

St.

Paul

– B

loom

-in

gton

Dow

ntow

n M

inne

apol

is,

Dow

ntow

n St

Pa

ul

23,

175,

041

1,58

7,52

11

50%

Star

ter

18D

etro

it –

War

ren

– Li

voni

a - A

nn

Arb

or (n

ote

#6)

Mid

tow

nB

irmin

gham

; A

nn A

rbor

34,

813,

013

1,60

4,33

80

0%N

one

19C

olum

bus

Shor

t Nor

th1

1,72

5,57

01,

725,

570

00%

Non

e

23K

ansa

s City

C

ount

ry C

lub

Plaz

a1

1,96

7,40

51,

967,

405

00%

Non

e

28C

inci

nnat

i –

Mid

dlet

own

Hyd

e Pa

rk1

2,10

4,21

82,

104,

218

00%

Non

e

29C

leve

land

– E

lyria

–

Men

tor

Uni

vers

ity C

ircle

12,

114,

155

2,11

4,15

51

100%

Parti

al

Mid

wes

t Sub

tota

l4

128

01

2528

,201

,518

1,12

8,06

117

68%

Perc

enta

ge o

f M

W/T

otal

16%

48%

32%

0%4%

16%

20%

0.8

17%

SOU

THW

EST

4D

enve

r – A

uror

a D

ownt

own

LOD

OB

ould

erB

elm

ar, C

herr

y C

reek

Vill

age

52,

408,

750

481,

750

240

%St

arte

r

21H

oust

on –

Sug

ar

Land

– B

ayto

wn

Mon

trose

Suga

rland

To

wn

Cen

-te

r, W

ood-

land

s Tow

n C

ente

r

35,

539,

949

1,84

6,65

01

33%

Star

ter

22Sa

n A

nton

io

Riv

erw

alk

11,

942,

217

1,94

2,21

70

0%N

one

25D

alla

s – F

ort

Wor

th –

Arli

ngto

n U

ptow

nPl

ano

Tow

n C

ente

r; A

d-di

son

Circ

le

36,

003,

967

2,00

1,32

20

0%St

arte

r

26Ph

oeni

x –

Mes

a –

Scot

tsda

le

Tem

pe; 2

4th

&

Cam

elba

ck2

4,03

9,18

22,

019,

591

00%

Non

e

Sout

hwes

t Sub

tota

l2

33

24

1419

,934

,065

1,42

3,86

23

21%

Perc

enta

ge o

f SW

/Tot

al14

%21

%21

%14

%29

%9%

22%

0.4

3%

WES

T

3Sa

n Fr

anci

sco

- O

akla

nd -

San

Jose

(n

ote#

2)

Dow

ntow

n Sa

n Fr

anci

sco;

Oak

-la

nd; B

erke

ley;

Sa

n Jo

se

Sout

h of

Mar

ket;

Mar

ina

Dis

trict

; Hob

H

ill, M

issi

on D

istri

ct

Palo

Alto

; Men

lo

Park

; San

Mat

eo,

Emor

yvill

e

Wal

nut C

reek

Sant

ana

Row

145,

967,

150

426,

225

1071

%Fu

ll

5Po

rtlan

d –

Vanc

ou-

ver –

Bea

verto

n D

ownt

own

Pear

l Dis

trict

, N

orth

wes

tLa

ke O

sweg

o4

2,13

7,56

553

4,39

14

100%

Parti

al

Tabl

e 3

6Se

attle

– T

acom

a –

Bel

levu

e D

ownt

own

Bel

l Tow

n; P

ione

er

Squa

reK

irkla

nd, R

ed-

mon

dU

nive

rsity

Dis

trict

63,

263,

497

543,

916

00%

Non

e

11Sa

n D

iego

– C

arls

-ba

d –

San

Mar

cos

Dow

ntow

nH

illcr

est/B

albo

a Pa

rkLa

Jolla

32,

941,

454

980,

485

267

%St

arte

r

12Lo

s Ang

eles

- L

ong

Bea

ch

- Ora

nge

Cou

nty

- Riv

ersi

de -

Ber

-na

rdin

o (n

ote

#5)

Dow

ntow

nH

olly

woo

d; W

est

Hol

lyw

ood

Pasa

dena

, San

ta

Mon

ica,

Lon

g B

each

, Bev

erly

H

ills,

Bur

bank

, G

lend

ale,

Cul

ver

City

Wes

twoo

d, C

entu

ry

City

Vale

ncia

To

wn

Cen

-te

r, C

osta

M

esa,

Sou

th

Coa

st T

own

Cen

ter

1516

,976

,264

1,13

1,75

14

27%

Parti

al

20La

s Veg

as –

Par

a-di

se

The

Strip

11,

777,

539

1,77

7,53

90

0%N

one

27Sa

cram

ento

–

Ard

en -

Arc

ade

– R

osev

ille

Dow

ntow

n1

2,06

7,11

72,

067,

117

00%

Star

ter

Wes

t Sub

tota

l9

1215

44

4435

,130

,586

798,

422

2045

%

Perc

enta

ge o

f W/

Tota

l20

%27

%34

%9%

9%28

%25

%1.

1220

%

TOTA

L24

5549

1910

157

137,

970,

911

878,

796

102

65%

Perc

enta

ge o

f Tot

al15

%35

%31

%12

%6%

100%

100%

1.00

100%

Not

e #1

: The

US

Cen

sus d

efini

tion

of B

altim

ore

and

Was

hing

ton,

DC

, M

SAs h

ave

been

sh

ifted

from

the

Sout

heas

t reg

ion

to th

e N

orth

east

re

gion

1775 Massachusetts Avenue, NWWashington, D.C. 20036-2188telephone 202.797.6000fax 202.797.6004web site www.brookings.edu

telephone 202.797.6139fax 202.797.2965web site www.brookings.edu/metro