Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the

instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-

926-7926 ext. 10.

FLSA Administrative and Executive Exemptions:

Avoiding, Auditing and Correcting Misclassifications

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, AUGUST 5, 2015

Presenting a live 90-minute webinar with interactive Q&A

Robert M. Hale, Partner, Goodwin Procter, Boston

Janet A. Hendrick, Of Counsel, Fisher & Phillips, Dallas

Staci Ketay Rotman, Partner, Franczek Radelet, Chicago

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-370-2805 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your participation in this

webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive

immediately following the program.

For additional information about CLE credit processing call us at 1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

Overview

What does the FLSA require?

What are the requirements for the executive exemption?

What are the requirements for the administrative exemption?

What are the key considerations for self-audits and correcting misclassifications?

5

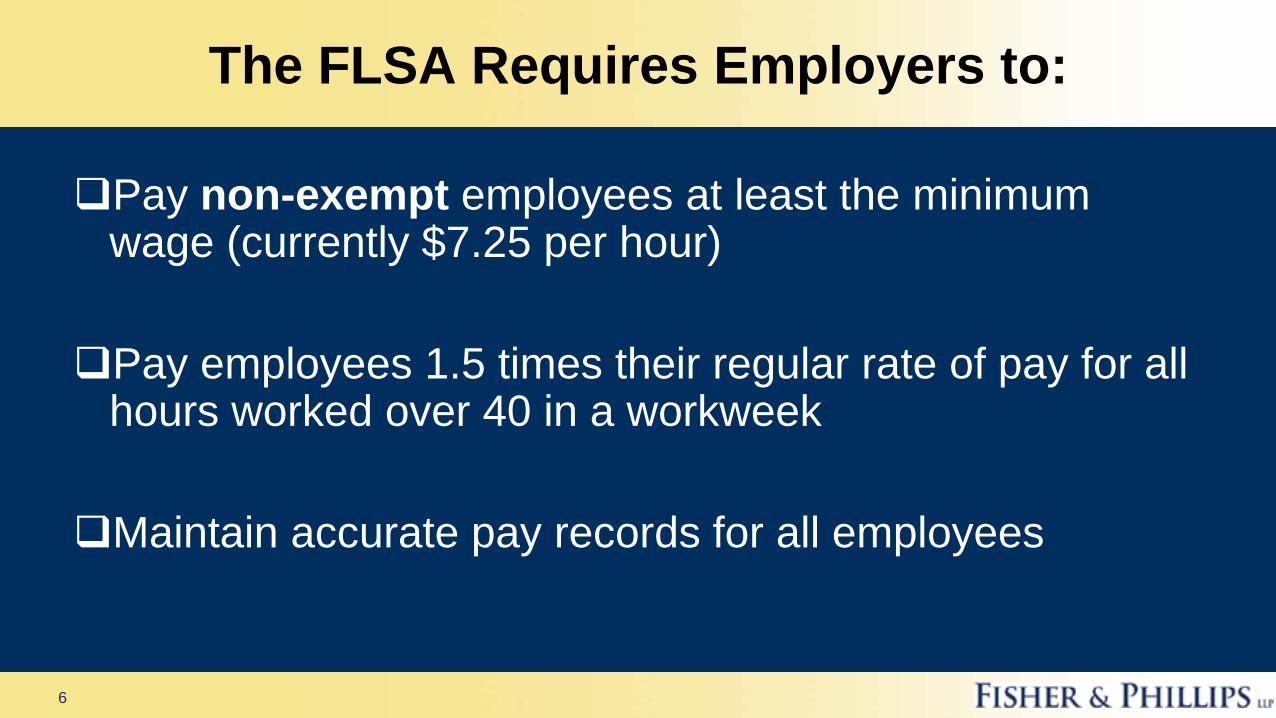

The FLSA Requires Employers to:

Pay non-exempt employees at least the minimum wage (currently $7.25 per hour)

Pay employees 1.5 times their regular rate of pay for all hours worked over 40 in a workweek

Maintain accurate pay records for all employees

6

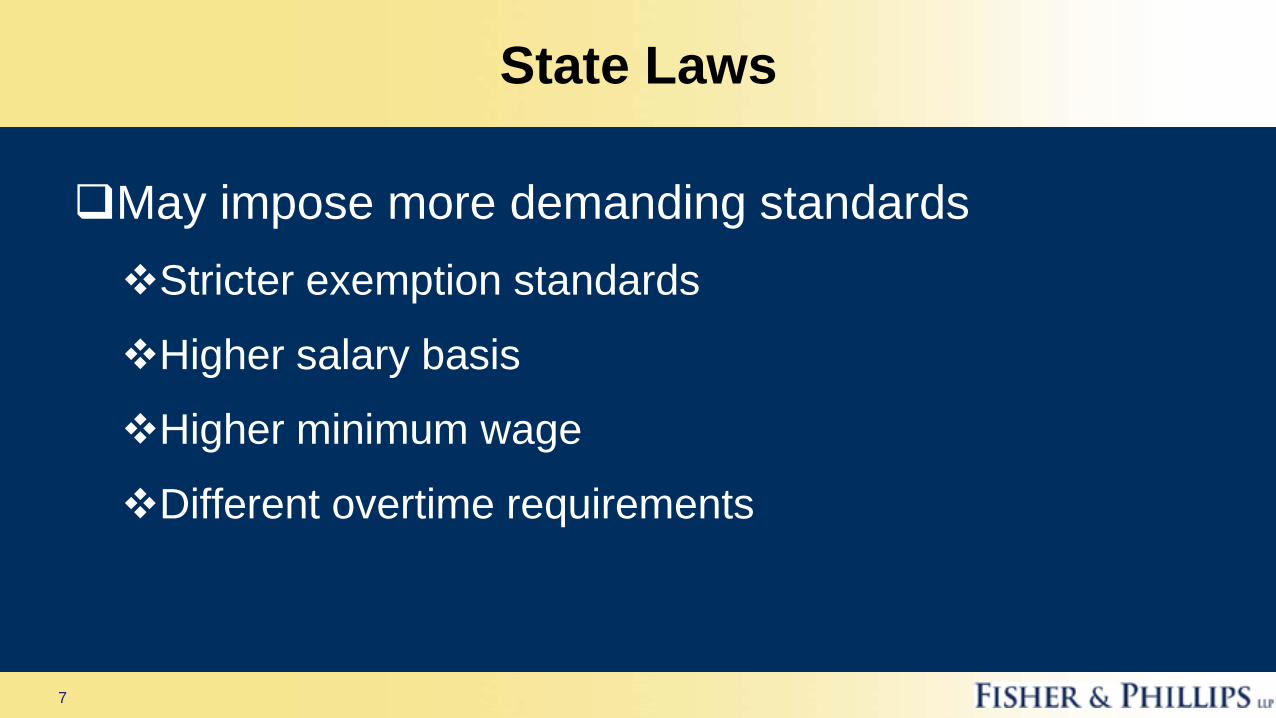

State Laws

May impose more demanding standards

Stricter exemption standards

Higher salary basis

Higher minimum wage

Different overtime requirements

7

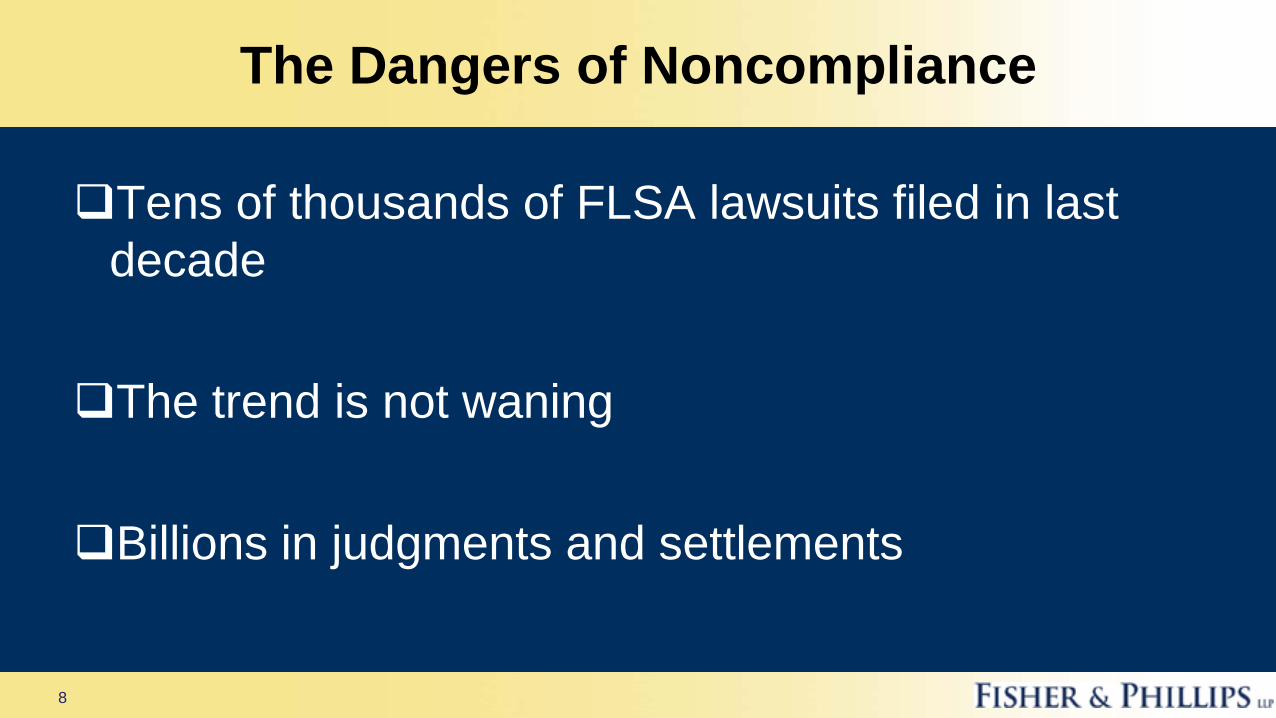

The Dangers of Noncompliance

Tens of thousands of FLSA lawsuits filed in last

decade

The trend is not waning

Billions in judgments and settlements

8

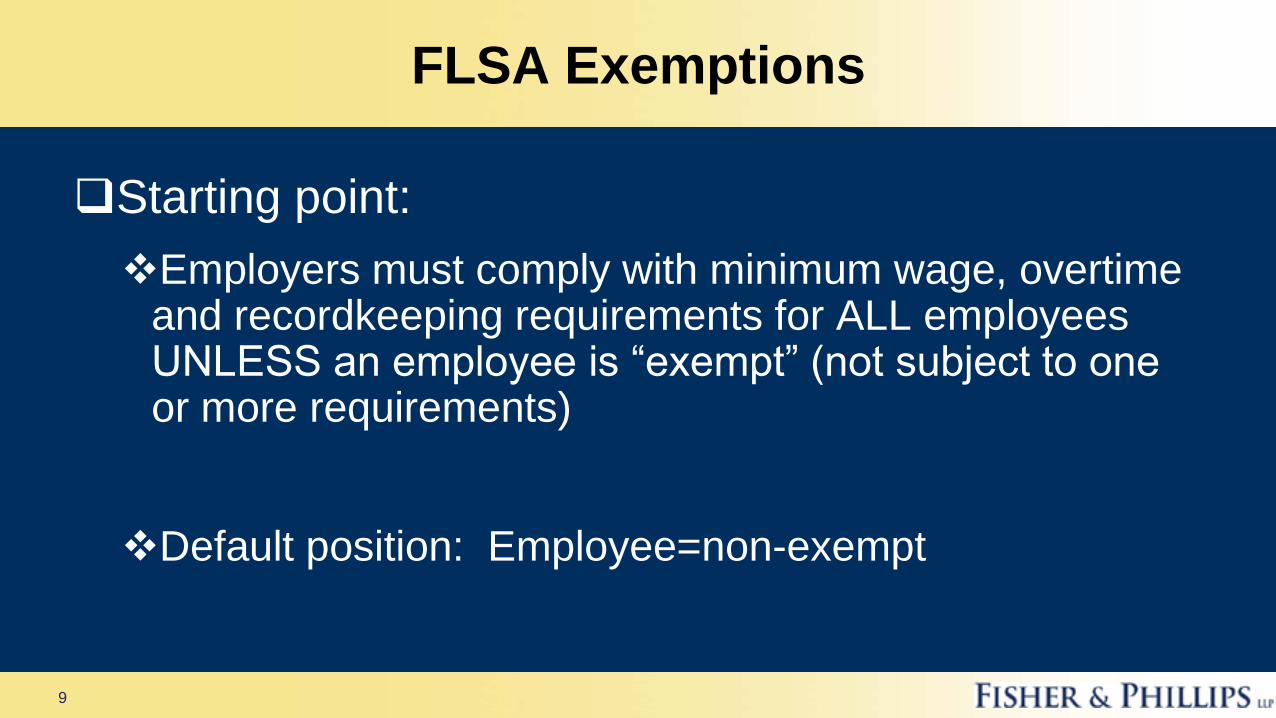

FLSA Exemptions

Starting point:

Employers must comply with minimum wage, overtime and recordkeeping requirements for ALL employees UNLESS an employee is “exempt” (not subject to one or more requirements)

Default position: Employee=non-exempt

9

Exemptions Generally

Exemptions are

defined by law, not by agreement, job descriptions,

or parties’ intentions

strictly interpreted

If an exemption is disputed, the employer has the

burden to prove that each requirement is met

(otherwise, the employer loses)

10

Exemptions Generally

Exemptions relate to individuals

Detailed, accurate, current job information is essential

Based upon actual work, real facts

Job descriptions do not “make employees exempt"

USDOL, plaintiffs’ lawyers will dig into the work the

employees actually do

11

Three Criteria For Exemption

Salary Level

Salary Basis

Job Duties

12

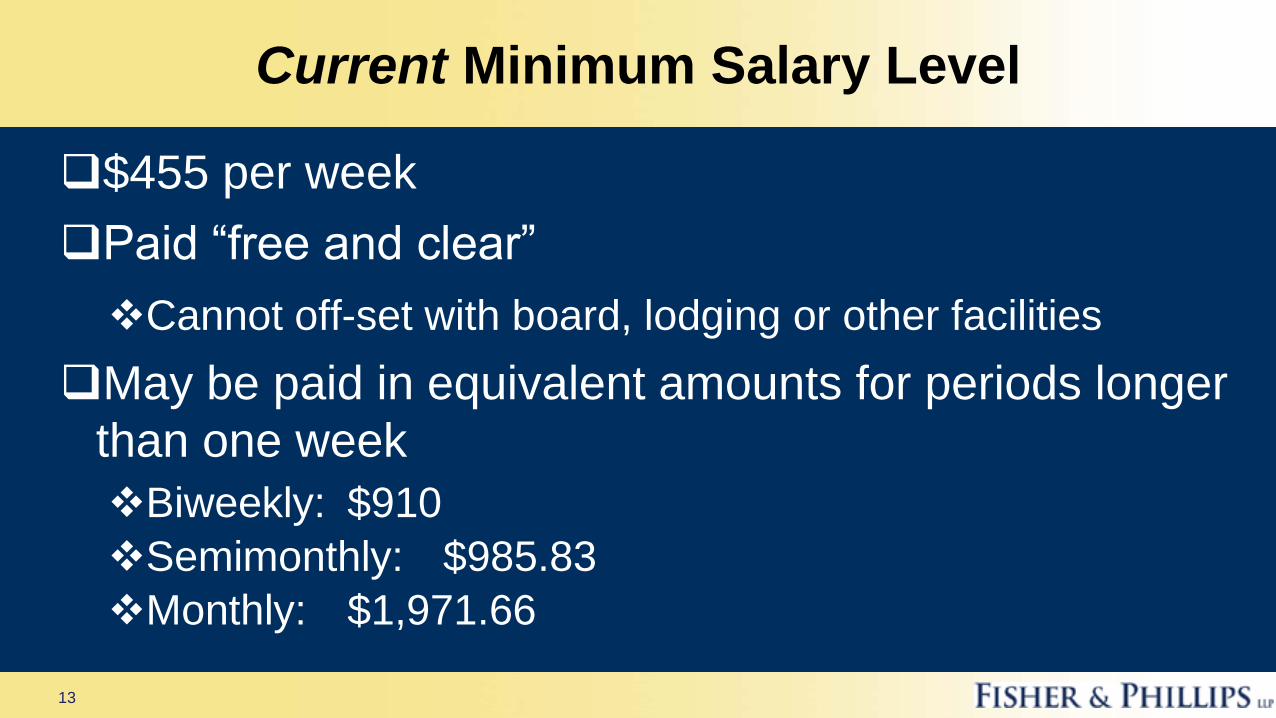

Current Minimum Salary Level

$455 per week

Paid “free and clear”

Cannot off-set with board, lodging or other facilities

May be paid in equivalent amounts for periods longer

than one week

Biweekly: $910

Semimonthly: $985.83

Monthly: $1,971.66

13

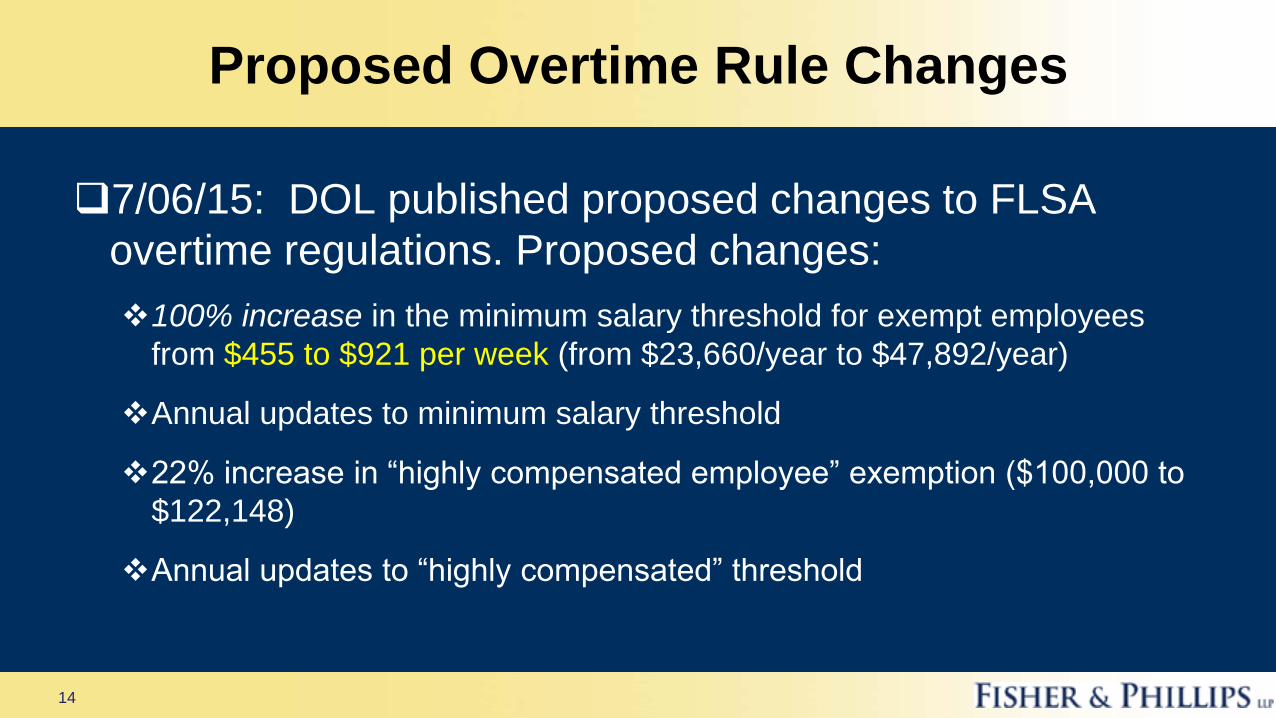

Proposed Overtime Rule Changes

7/06/15: DOL published proposed changes to FLSA

overtime regulations. Proposed changes:

100% increase in the minimum salary threshold for exempt employees

from $455 to $921 per week (from $23,660/year to $47,892/year)

Annual updates to minimum salary threshold

22% increase in “highly compensated employee” exemption ($100,000 to

$122,148)

Annual updates to “highly compensated” threshold

14

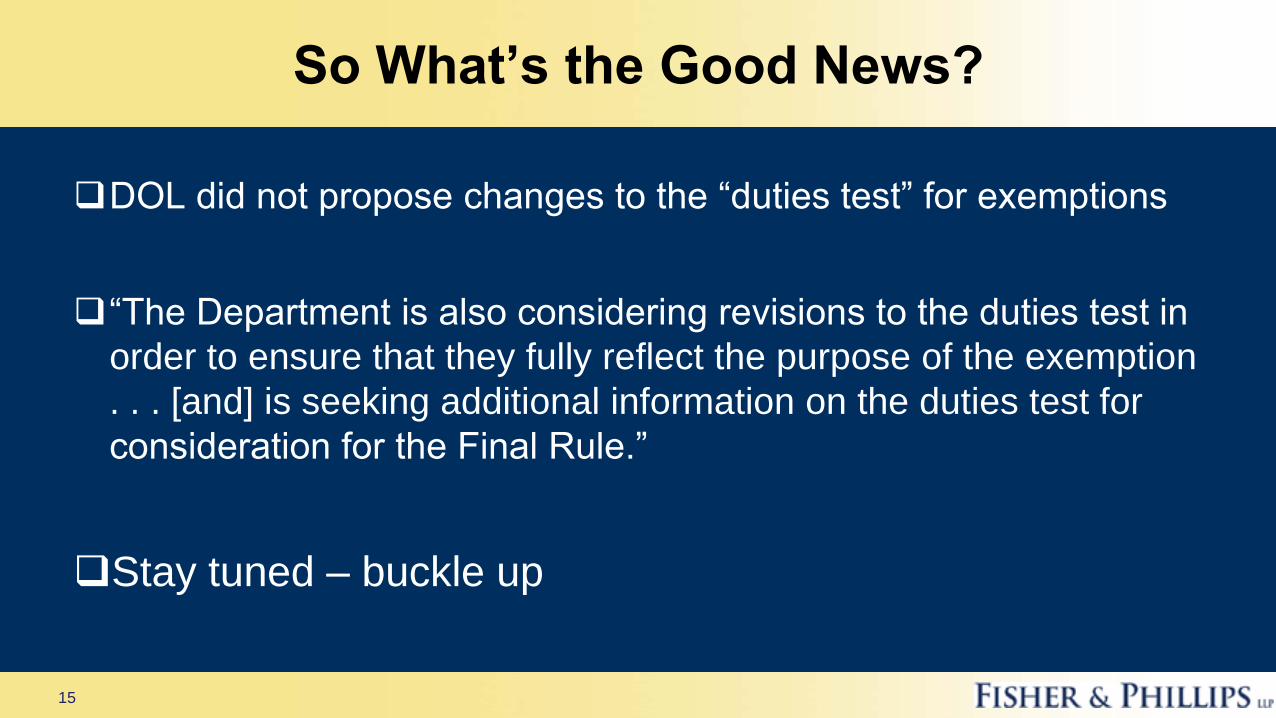

So What’s the Good News?

DOL did not propose changes to the “duties test” for exemptions

“The Department is also considering revisions to the duties test in

order to ensure that they fully reflect the purpose of the exemption

. . . [and] is seeking additional information on the duties test for

consideration for the Final Rule.”

Stay tuned – buckle up

15

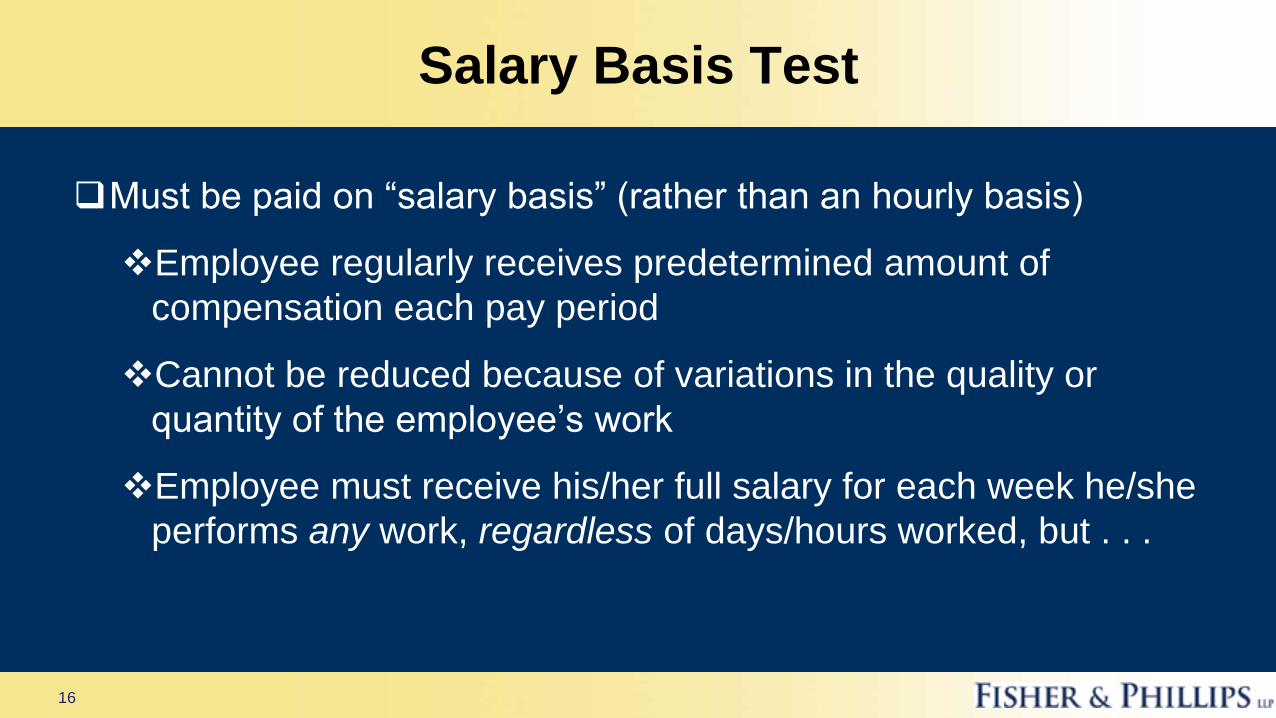

Salary Basis Test

Must be paid on “salary basis” (rather than an hourly basis)

Employee regularly receives predetermined amount of

compensation each pay period

Cannot be reduced because of variations in the quality or

quantity of the employee’s work

Employee must receive his/her full salary for each week he/she

performs any work, regardless of days/hours worked, but . . .

16

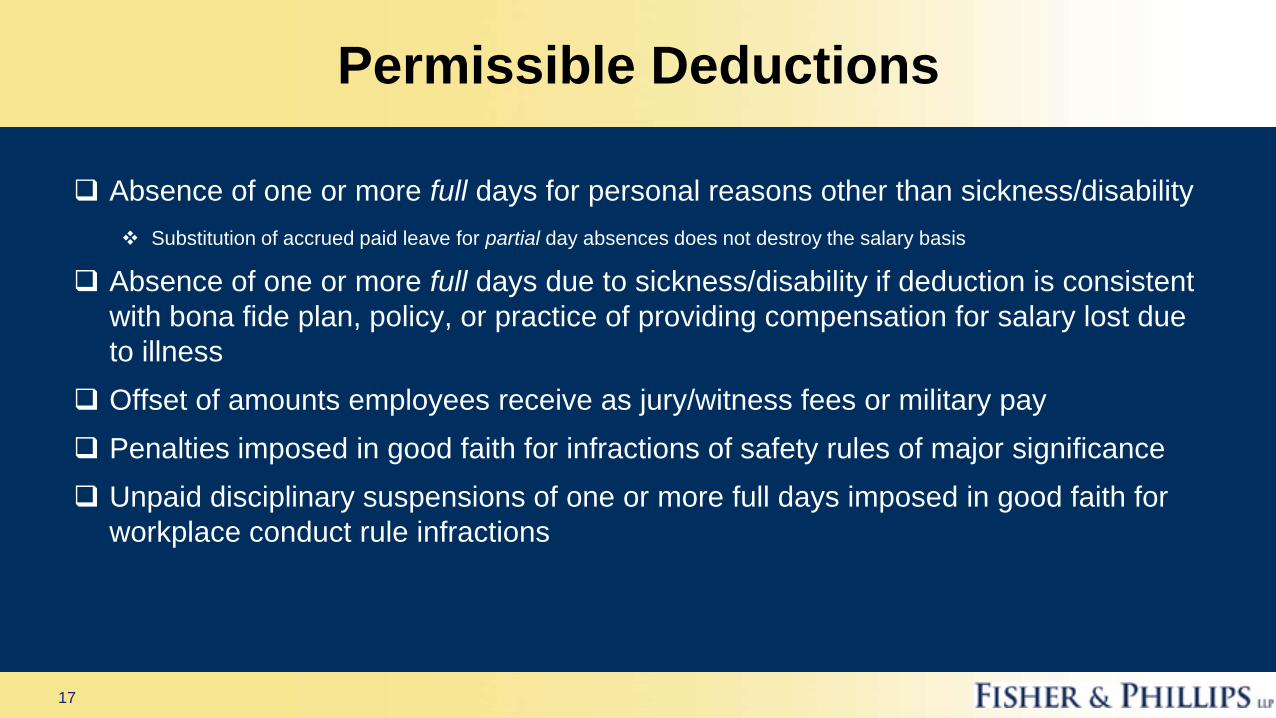

Permissible Deductions

Absence of one or more full days for personal reasons other than sickness/disability

Substitution of accrued paid leave for partial day absences does not destroy the salary basis

Absence of one or more full days due to sickness/disability if deduction is consistent

with bona fide plan, policy, or practice of providing compensation for salary lost due

to illness

Offset of amounts employees receive as jury/witness fees or military pay

Penalties imposed in good faith for infractions of safety rules of major significance

Unpaid disciplinary suspensions of one or more full days imposed in good faith for

workplace conduct rule infractions

17

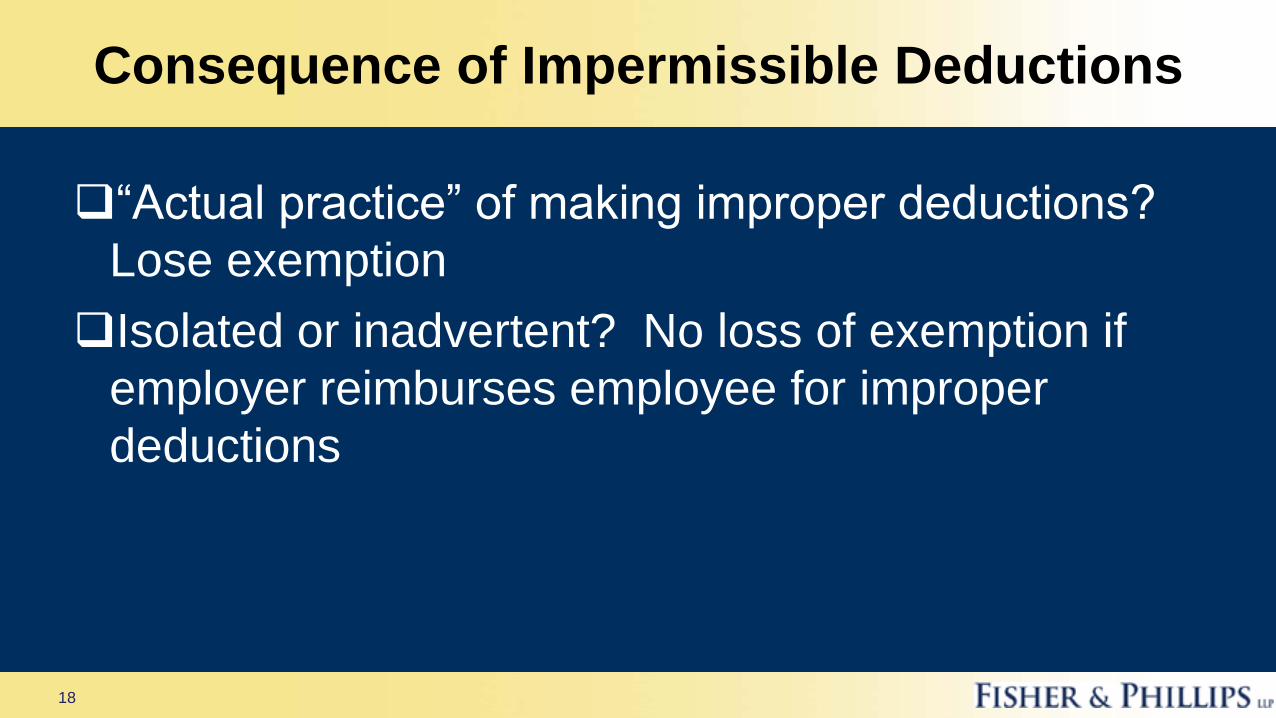

Consequence of Impermissible Deductions

“Actual practice” of making improper deductions?

Lose exemption

Isolated or inadvertent? No loss of exemption if

employer reimburses employee for improper

deductions

18

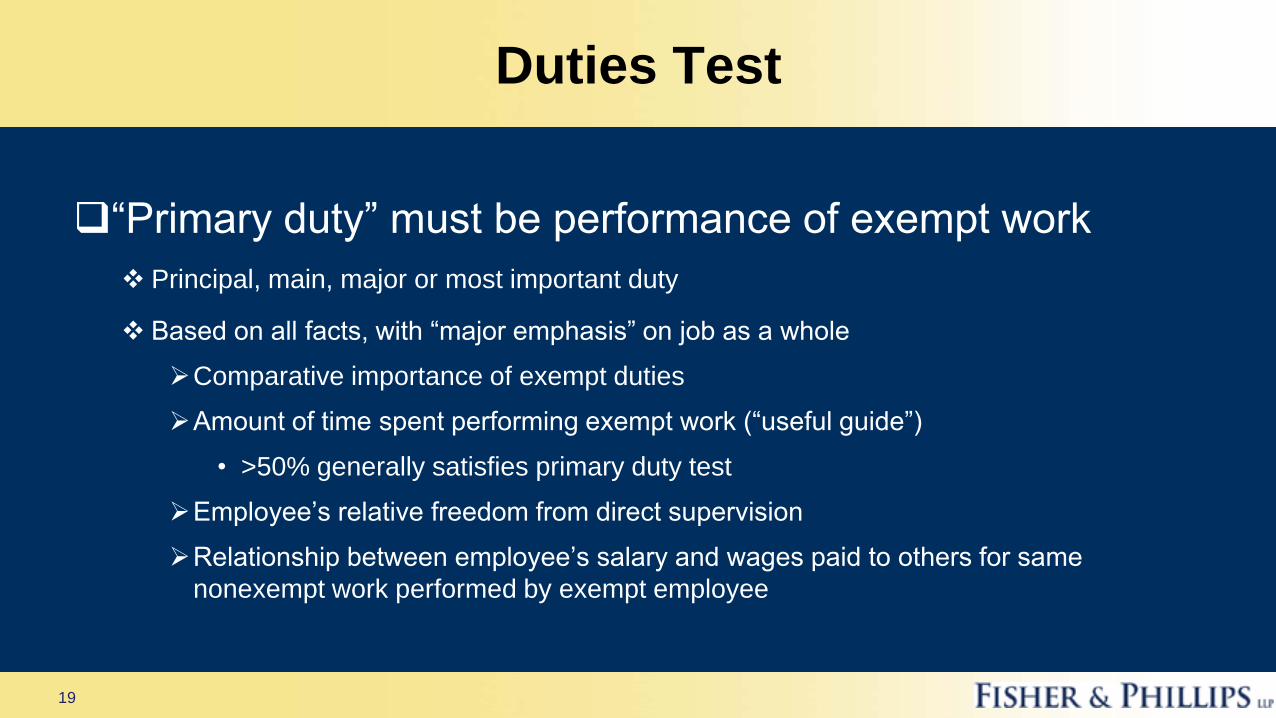

Duties Test

“Primary duty” must be performance of exempt work

Principal, main, major or most important duty

Based on all facts, with “major emphasis” on job as a whole

Comparative importance of exempt duties

Amount of time spent performing exempt work (“useful guide”)

• >50% generally satisfies primary duty test

Employee’s relative freedom from direct supervision

Relationship between employee’s salary and wages paid to others for same

nonexempt work performed by exempt employee

19

Copyright © 2015, Franczek Radelet P.C. All Rights Reserved. Disclaimer: Attorney Advertising. This presentation is a publication of Franczek Radelet P.C.

This presentation is intended for general informational purposes only and should not be construed as legal advice.

White Collar Exemptions:

The Executive Exemption

Staci Ketay Rotman

www.franczek.com

21

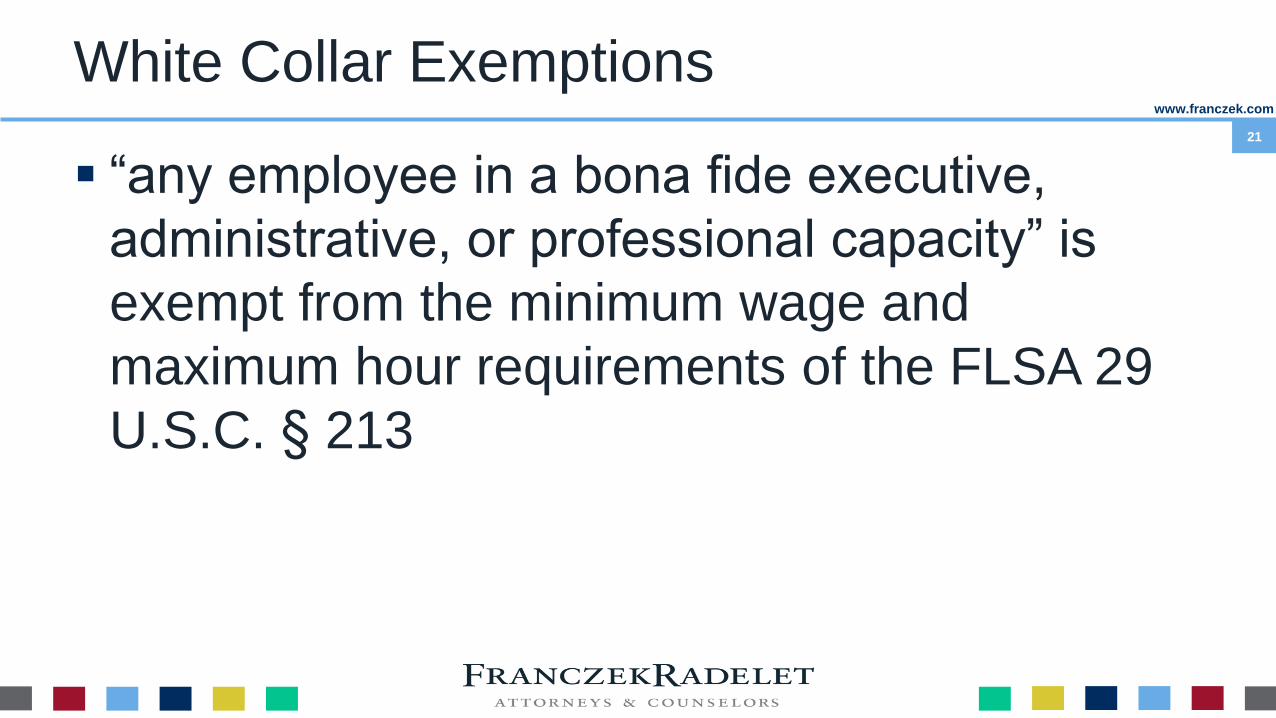

White Collar Exemptions

“any employee in a bona fide executive,

administrative, or professional capacity” is

exempt from the minimum wage and

maximum hour requirements of the FLSA 29

U.S.C. § 213

www.franczek.com

22

Exempt v. Non-Exempt:

That is the Question!

www.franczek.com

23

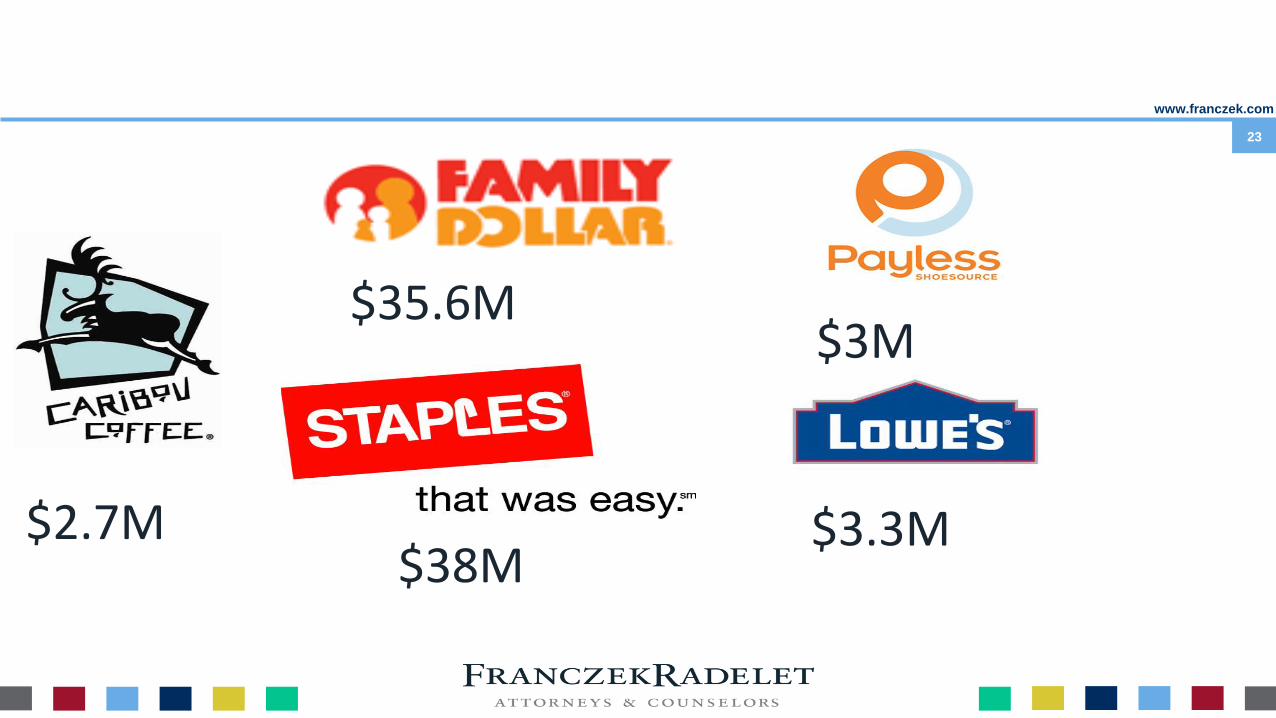

$2.7M $38M

$35.6M $3M

$3.3M

www.franczek.com

24

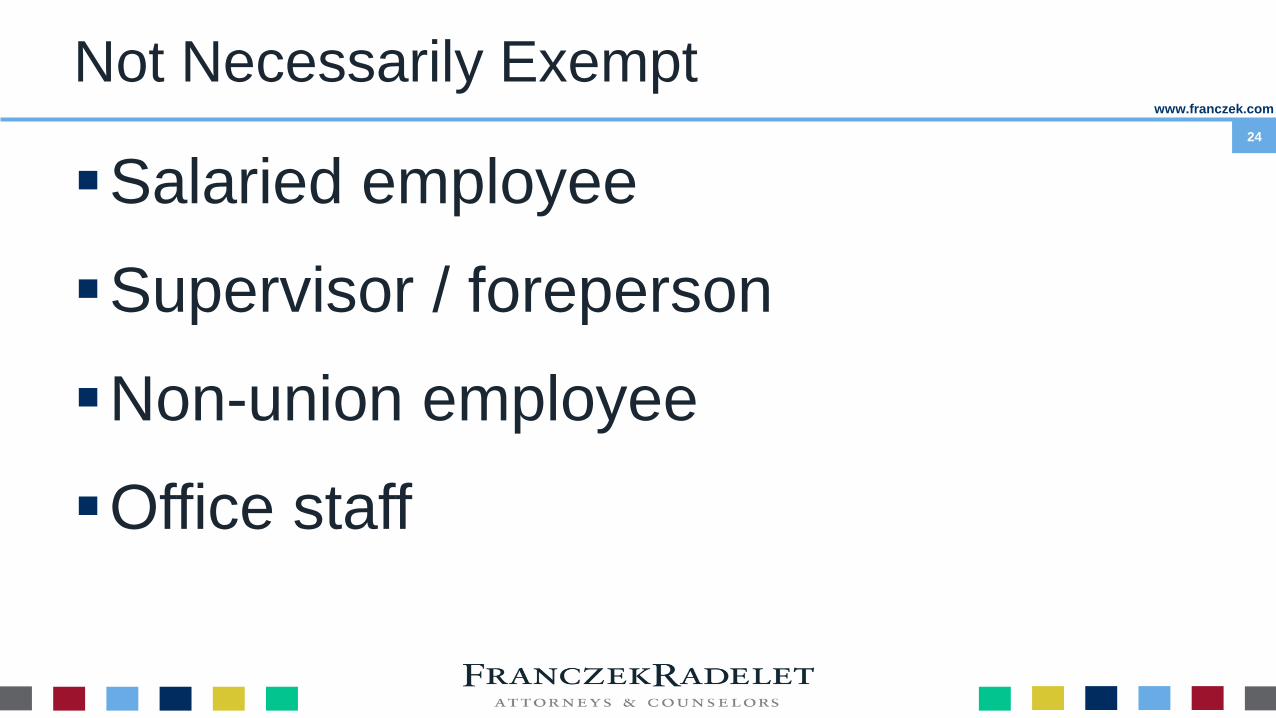

Not Necessarily Exempt

Salaried employee

Supervisor / foreperson

Non-union employee

Office staff

www.franczek.com

25

Executive Exemption

Currently must be compensated on a salary basis at not less than $455 per week (pending increase with the DOL’s proposed rules)

Primary duty: managing enterprise or customarily recognized department or subdivision

Customarily and regularly directs at least 2 FTEs or equivalent

Authority to hire / fire, or recommendations as to hiring, firing, advancement, promotion, or change of status carry “particular weight”

25

www.franczek.com

26

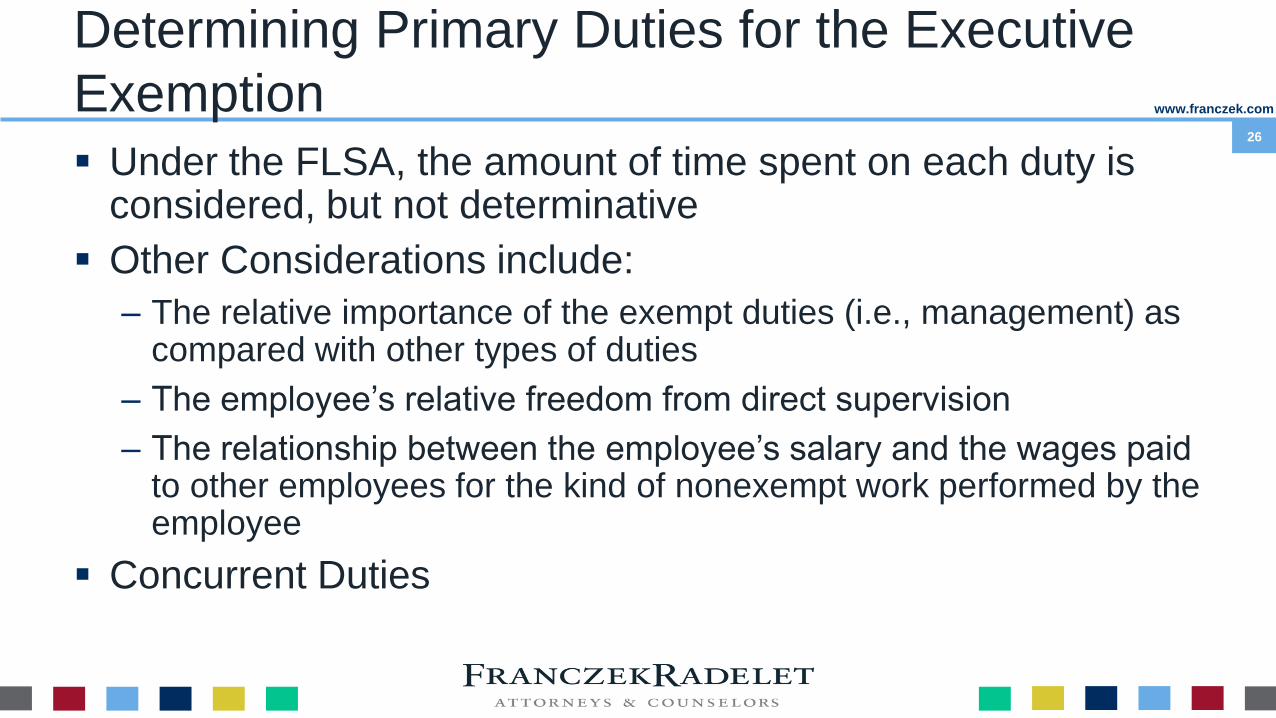

Determining Primary Duties for the Executive

Exemption

Under the FLSA, the amount of time spent on each duty is considered, but not determinative

Other Considerations include:

– The relative importance of the exempt duties (i.e., management) as compared with other types of duties

– The employee’s relative freedom from direct supervision

– The relationship between the employee’s salary and the wages paid to other employees for the kind of nonexempt work performed by the employee

Concurrent Duties

www.franczek.com

27

What May Constitute Management?

Interviewing, selecting, and training employees;

Setting rates of pay and hours of work;

Maintain production or

sales records (beyond

merely clerical

maintenance);

www.franczek.com

28

What May Constitute Management?

Appraising employee productivity and efficiency;

Handling employee complaints;

Disciplining employees;

www.franczek.com

29

Other Management Activities

Planning the work;

Determining the techniques to be used;

Apportioning work among the employees;

Determining the types equipment to be used in performing the

work;

Planning budgets for work;

Monitoring work for legal or regulatory compliance;

Providing for the safety and security of the workplace

www.franczek.com

30

Management Rule of Thumb

Ask who is “in charge” of a department or

subdivision of the company

www.franczek.com

31

Who is a Supervisor?

Mere supervision is not enough; it must constitute a

primary duty of the employee’s job

Supervision of non-employees is not included

A supervisor must supervise at least two full-time

employees

– An equivalent number of part-time employees is sufficient

32

www.franczek.com

32

Compare Example 1 to…

Store Manager supervises an

Assistant Manager & Clerks

Performs non-managerial work 80%

of the time

Is only paid $2.21 per hour more

than the Assistant Manager

33

www.franczek.com

33

…Example 2

Store Manager with

supervisory authority

Spends 75-80% of his time

performing non-managerial

tasks

Is paid 18-30% more per hour

than the next highest paid

employee

www.franczek.com

34

Dollar General Litigation

Both examples involved Store Managers, but resulted in different

outcomes

– Example 1: the court found in favor of the employee [SJ Denied]

– Example 2: the court found in favor of Dollar General [SJ Granted]

But:

– Employees had same job title

– Both were paid 18-30% more than the next highest paid employee in the store

– Both spent the overwhelming majority of their time performing non-managerial

tasks

So why the different decisions?

35

www.franczek.com

35

Information You Need

What does the job

description say?

If different, what does the

employee do?

How is the employee paid?

36

www.franczek.com

36

Job Titles to Watch For

Assistant Manager

Executive Assistant

Office Manager

Paraprofessionals

©2015 Goodwin Procter LLP

FLSA Administrative and Executive Exemptions:

Avoiding, Auditing and Correcting

Misclassifications

Robert M. Hale, Esq.

Goodwin Procter LLP

August 5, 2015

Goodwin Procter LLP 38

Administrative Employees – Duties Test Overview

The primary duty must consist of office or non-manual work

That work must directly relate to the management or general business operations of:

› the employer or

› the employer’s customers

The primary duty must include:

› the exercise of discretion and independent judgment

› with respect to matters of significance

Goodwin Procter LLP 39

Administrative Employees – Office or

Non-Manual Work

Manual work – work involving “repetitive operations with . . . hands.” 29 C.F.R. § 541.3(a)

Non-Manual work includes:

› fieldwork by a union organizer. Rincon v. AFSCME (N.D. Cal. 2013)

› piloting an aircraft. McCoy v. North Slope Borough (D. Alaska 2013)

Goodwin Procter LLP

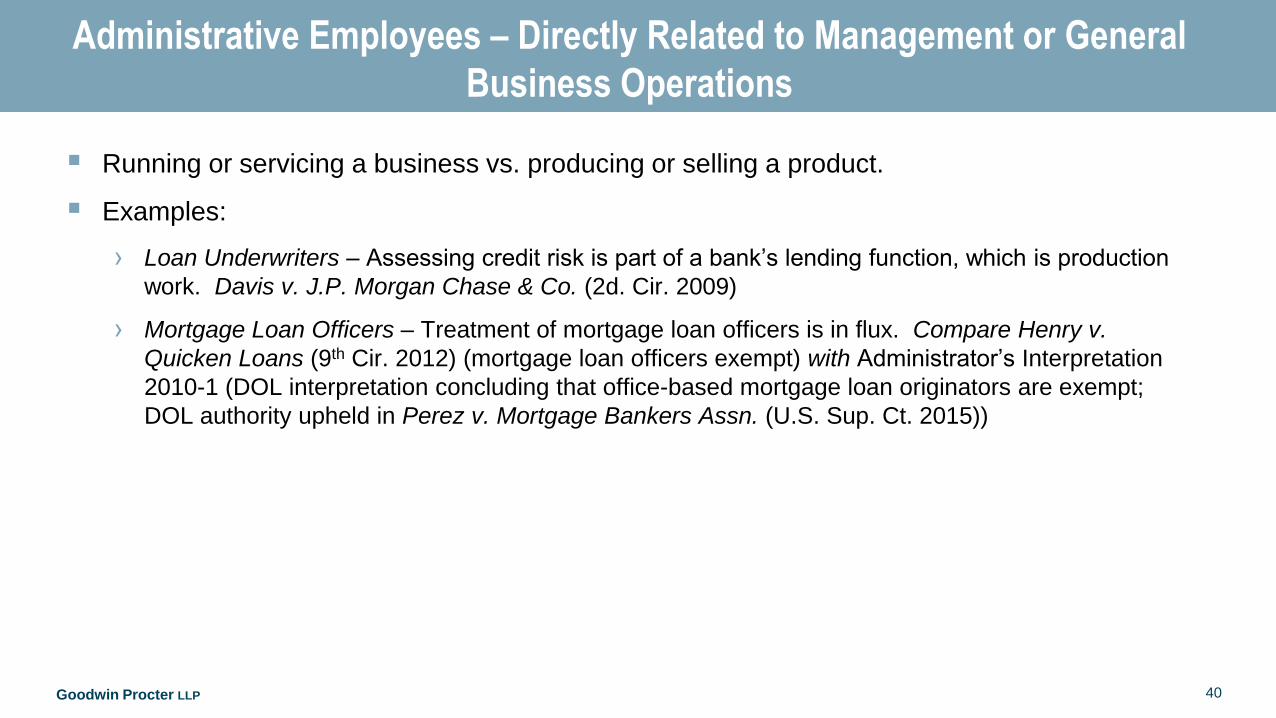

Administrative Employees – Directly Related to Management or General

Business Operations

Running or servicing a business vs. producing or selling a product.

Examples:

› Loan Underwriters – Assessing credit risk is part of a bank’s lending function, which is production

work. Davis v. J.P. Morgan Chase & Co. (2d. Cir. 2009)

› Mortgage Loan Officers – Treatment of mortgage loan officers is in flux. Compare Henry v.

Quicken Loans (9th Cir. 2012) (mortgage loan officers exempt) with Administrator’s Interpretation

2010-1 (DOL interpretation concluding that office-based mortgage loan originators are exempt;

DOL authority upheld in Perez v. Mortgage Bankers Assn. (U.S. Sup. Ct. 2015))

40

Goodwin Procter LLP

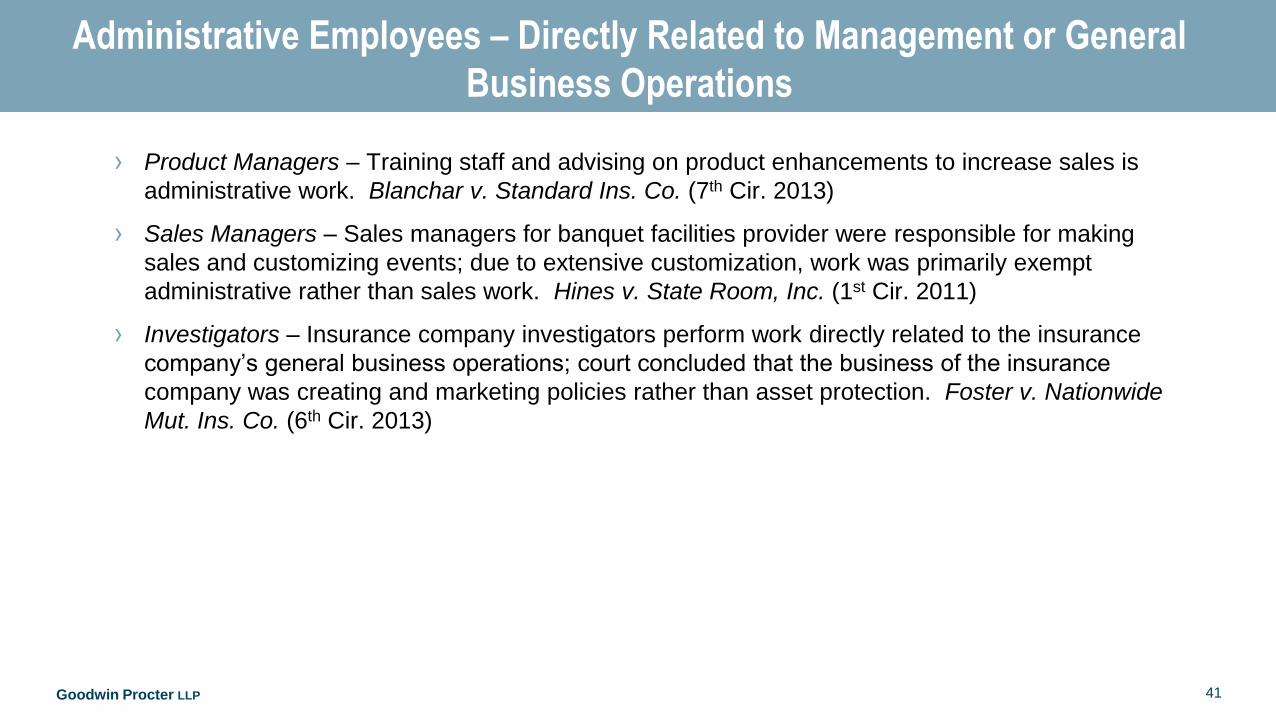

Administrative Employees – Directly Related to Management or General

Business Operations

› Product Managers – Training staff and advising on product enhancements to increase sales is

administrative work. Blanchar v. Standard Ins. Co. (7th Cir. 2013)

› Sales Managers – Sales managers for banquet facilities provider were responsible for making

sales and customizing events; due to extensive customization, work was primarily exempt

administrative rather than sales work. Hines v. State Room, Inc. (1st Cir. 2011)

› Investigators – Insurance company investigators perform work directly related to the insurance

company’s general business operations; court concluded that the business of the insurance

company was creating and marketing policies rather than asset protection. Foster v. Nationwide

Mut. Ins. Co. (6th Cir. 2013)

41

Goodwin Procter LLP

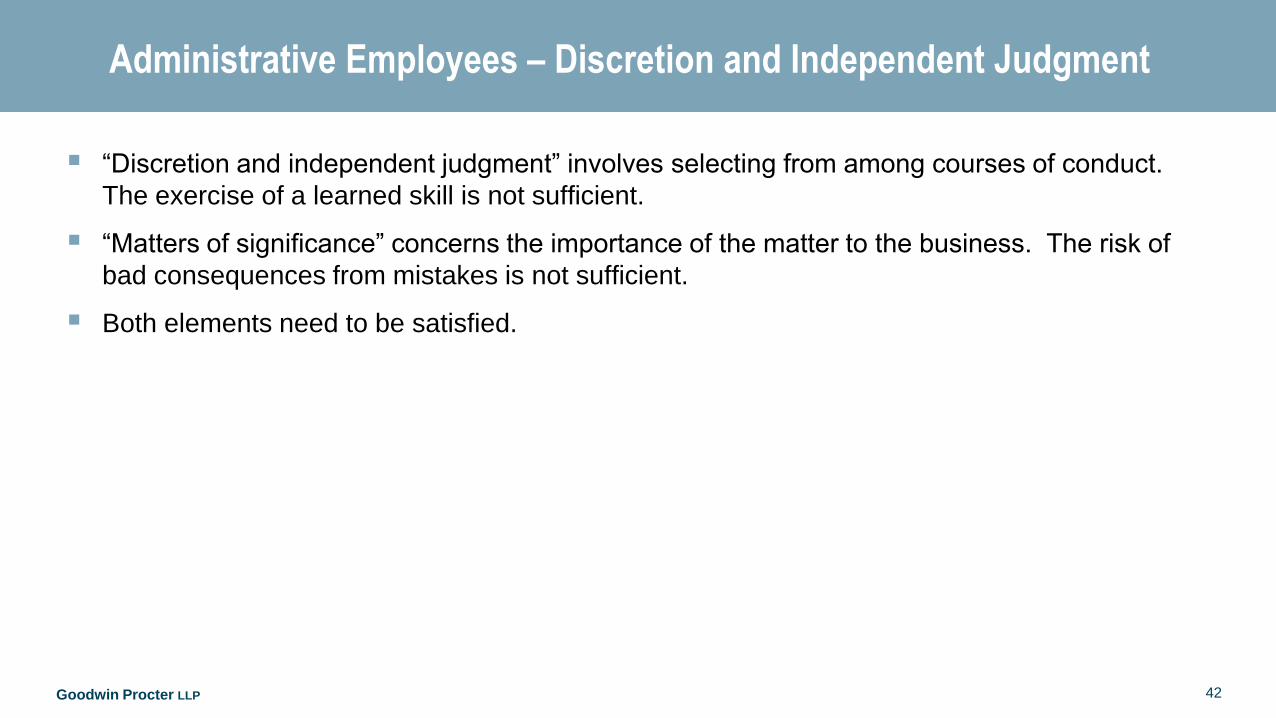

Administrative Employees – Discretion and Independent Judgment

“Discretion and independent judgment” involves selecting from among courses of conduct.

The exercise of a learned skill is not sufficient.

“Matters of significance” concerns the importance of the matter to the business. The risk of

bad consequences from mistakes is not sufficient.

Both elements need to be satisfied.

42

Goodwin Procter LLP

Administrative Employees – Discretion and Independent Judgment

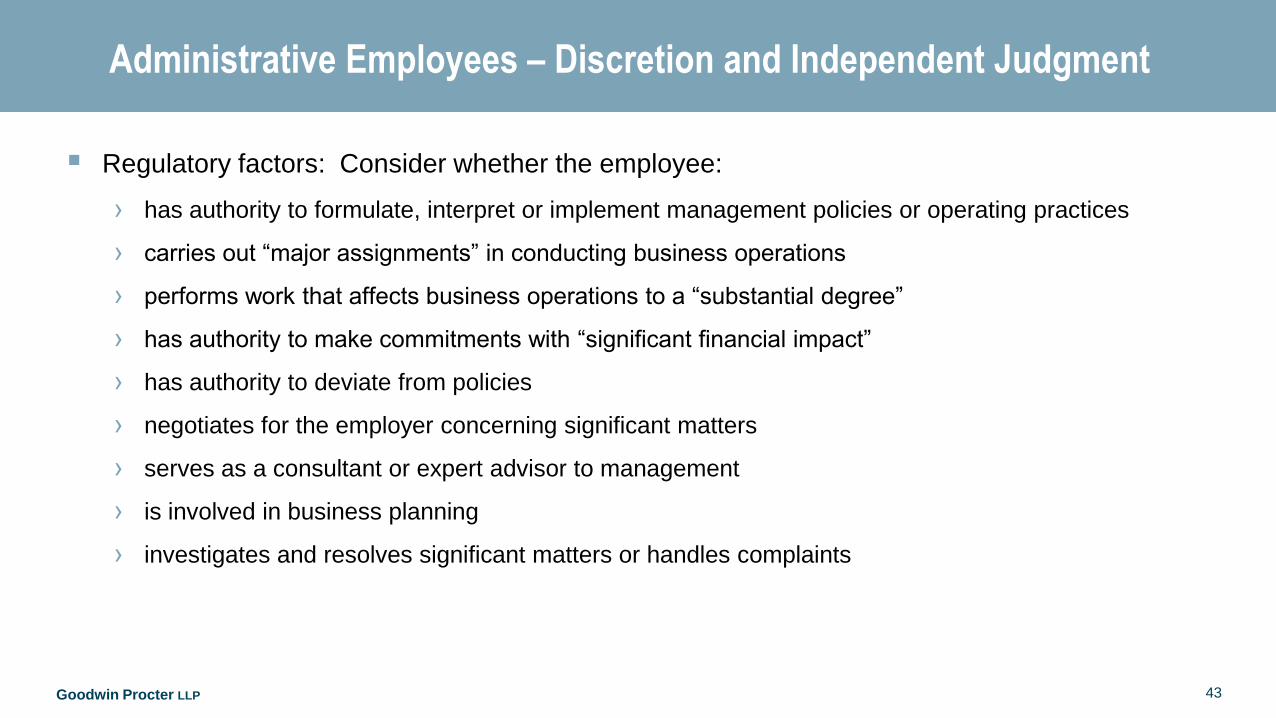

Regulatory factors: Consider whether the employee:

› has authority to formulate, interpret or implement management policies or operating practices

› carries out “major assignments” in conducting business operations

› performs work that affects business operations to a “substantial degree”

› has authority to make commitments with “significant financial impact”

› has authority to deviate from policies

› negotiates for the employer concerning significant matters

› serves as a consultant or expert advisor to management

› is involved in business planning

› investigates and resolves significant matters or handles complaints

43

Goodwin Procter LLP

Administrative Employees – Discretion and Independent Judgment

Examples:

› Investigators – Treatment depends on whether employees are limited to gathering facts following

established procedures or whether they are expected to use judgment in planning, conducting and

concluding investigations. Compare Calderon v. GEICO Gen. Ins. Co. (D. Md. 2012), Ahle v.

Veracity Research Co. (D. Minn. 2010) (investigators were non-exempt) and Fenton v. Farmers

Ins. Exchange (D. Minn. 2009) with Foster v. Nationwide Mut. Ins. Co. (6th Cir. 2013) and Mullins v.

Target Corp. (N.D. Ill. 2011) (investigators were exempt)

44

Goodwin Procter LLP

Administrative Employees – Discretion and Independent Judgment

› Field Inspectors – Field inspectors at construction sites who rely on manuals to guide the

inspection process were not exempt. Blotzer v. L-3 Communications Corp. (D. Ariz. 2012)

› Account Managers – Persons managing customer accounts under limited supervision exercise

discretion and independent judgment with respect to matters of significance. Verkuilen v.

MediaBank LLC (7th Cir. 2011) and Hines v. State Room, Inc. (1st Cir. 2011)

› Bookkeepers - Bookkeepers who made improvements in accounting systems and tax compliance

exercised discretion and independent judgment with respect to matters of significance. Fox v.

Lovas (W.D. Ky. 2012)

45

Exemption Disputes

Exemption Disputes Can Arise In Different Ways:

• Complaint To USDOL,

• Random Audit By USDOL,

• Lawsuit By One Or More Employees, Former

Employees

46

47

www.franczek.com

47

Warning Signs of Misclassification

Everyone in the office is

salaried

This is how it’s done in this

industry

Docking / deductions from

salary

48

www.franczek.com

48

Mitigating Risk

Offer Letter / Handbook: Salary

covers all hours worked

Handbook: “Safe Harbor”

language for improper

deductions

Best Practices

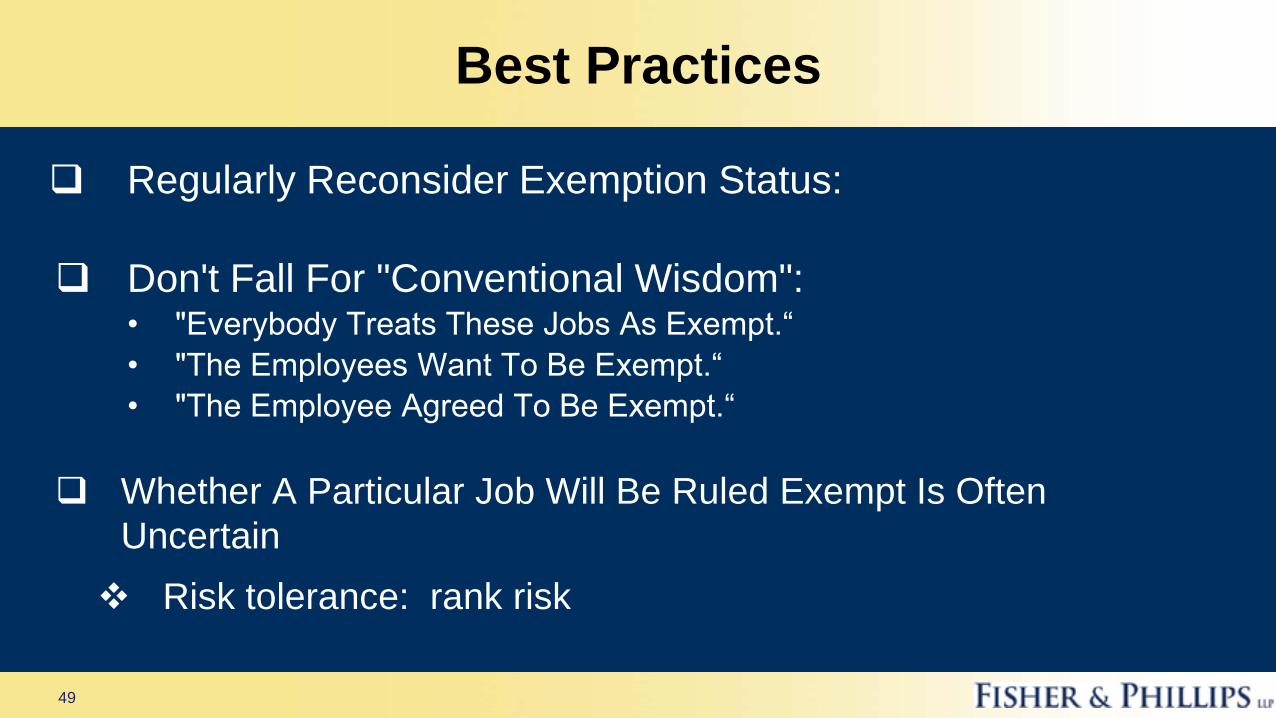

Regularly Reconsider Exemption Status:

Don't Fall For "Conventional Wisdom": • "Everybody Treats These Jobs As Exempt.“

• "The Employees Want To Be Exempt.“

• "The Employee Agreed To Be Exempt.“

Whether A Particular Job Will Be Ruled Exempt Is Often

Uncertain

Risk tolerance: rank risk

49

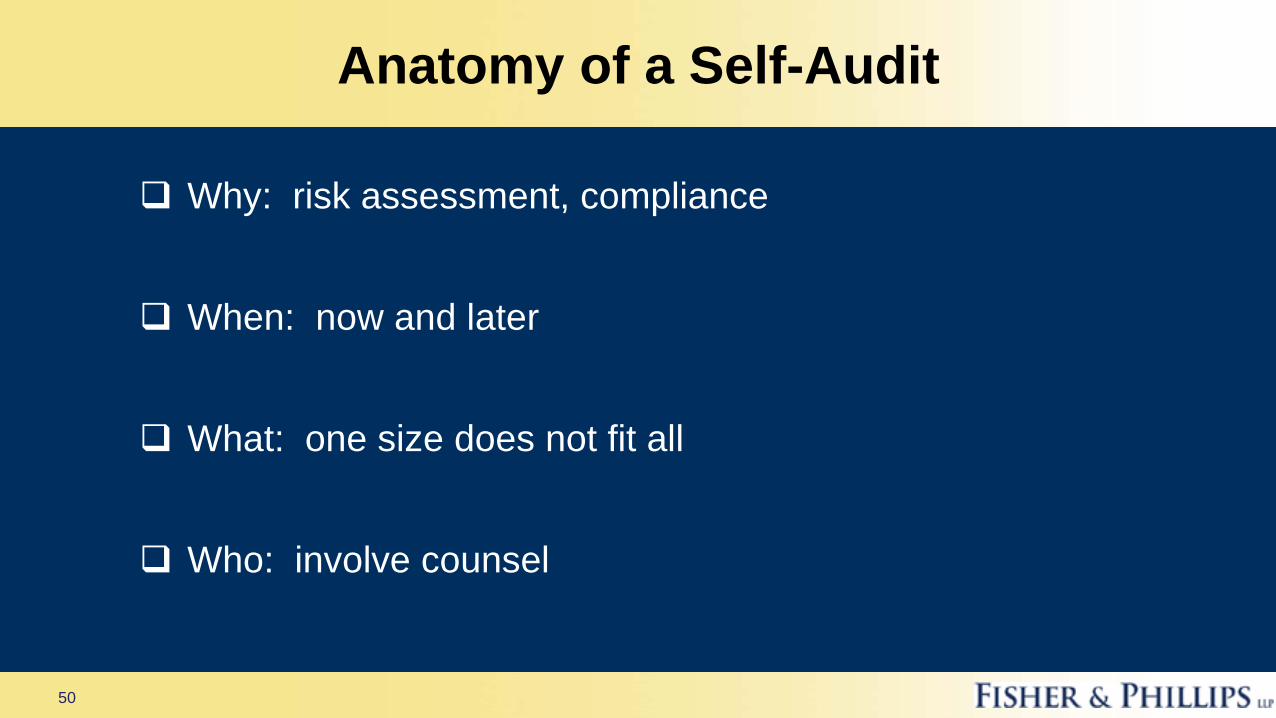

Anatomy of a Self-Audit

Why: risk assessment, compliance

When: now and later

What: one size does not fit all

Who: involve counsel

50

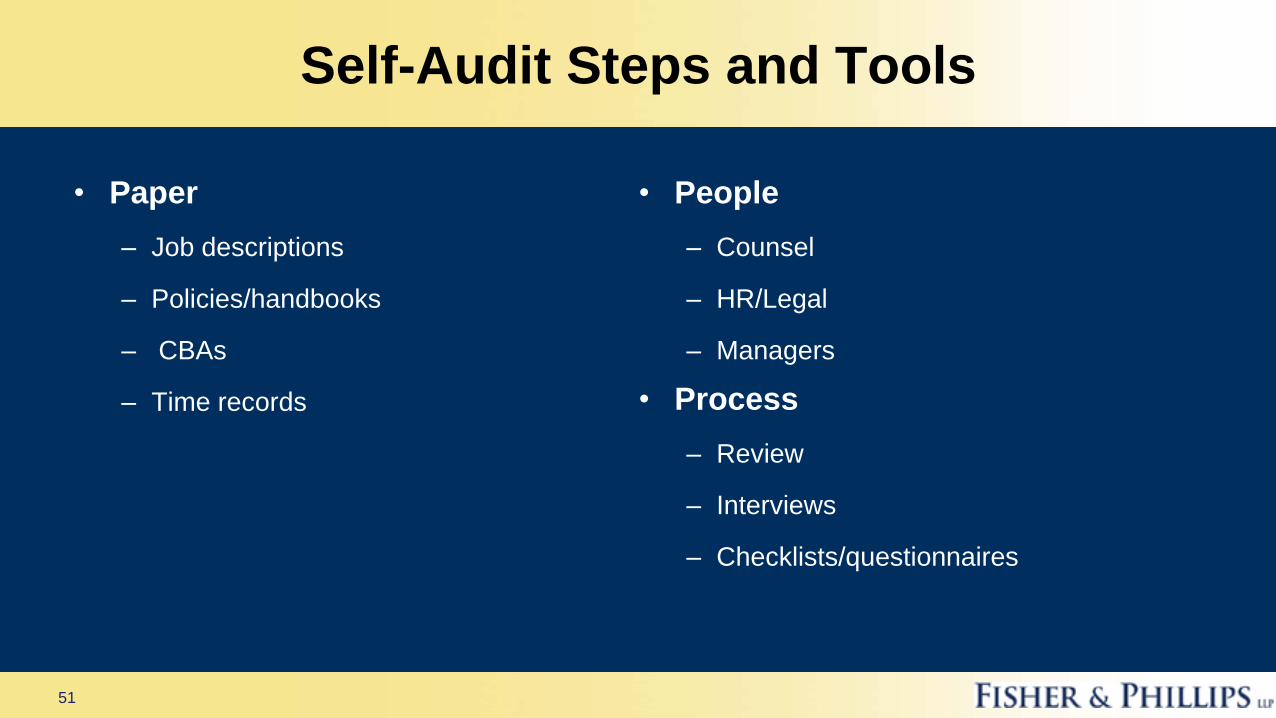

Self-Audit Steps and Tools

• Paper

– Job descriptions

– Policies/handbooks

– CBAs

– Time records

• People

– Counsel

– HR/Legal

– Managers

• Process

– Review

– Interviews

– Checklists/questionnaires

51

Goodwin Procter LLP

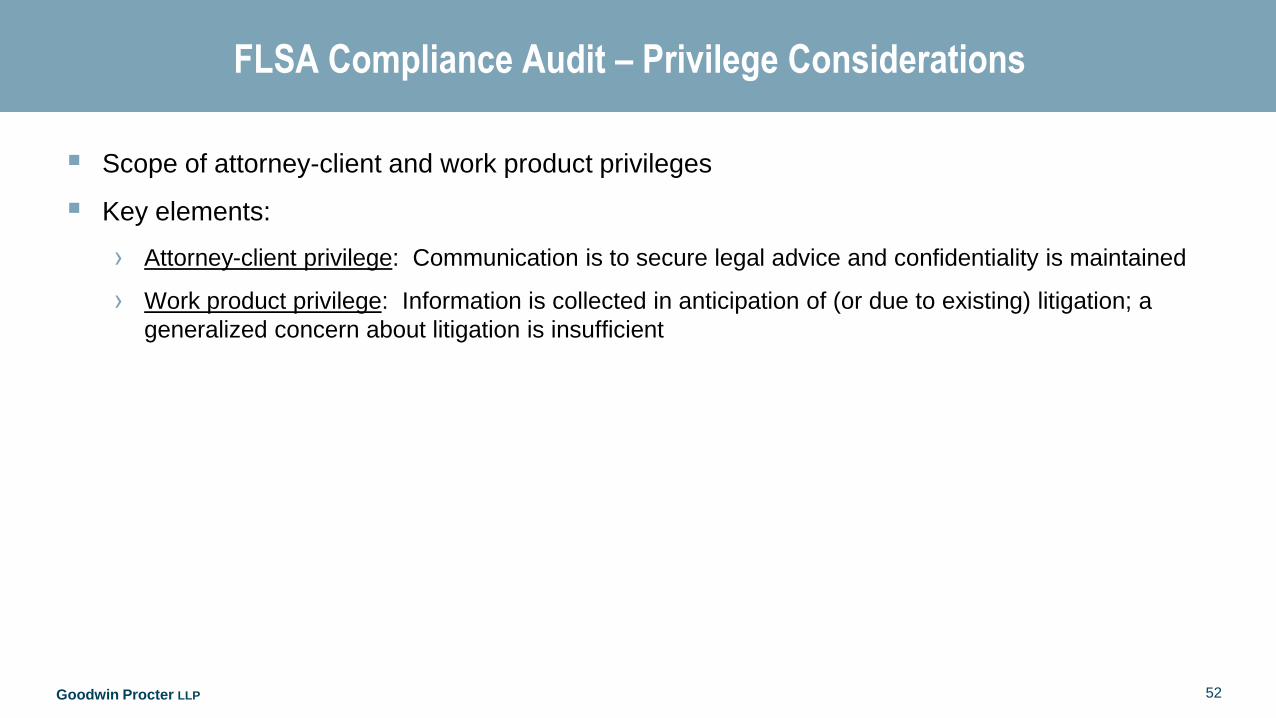

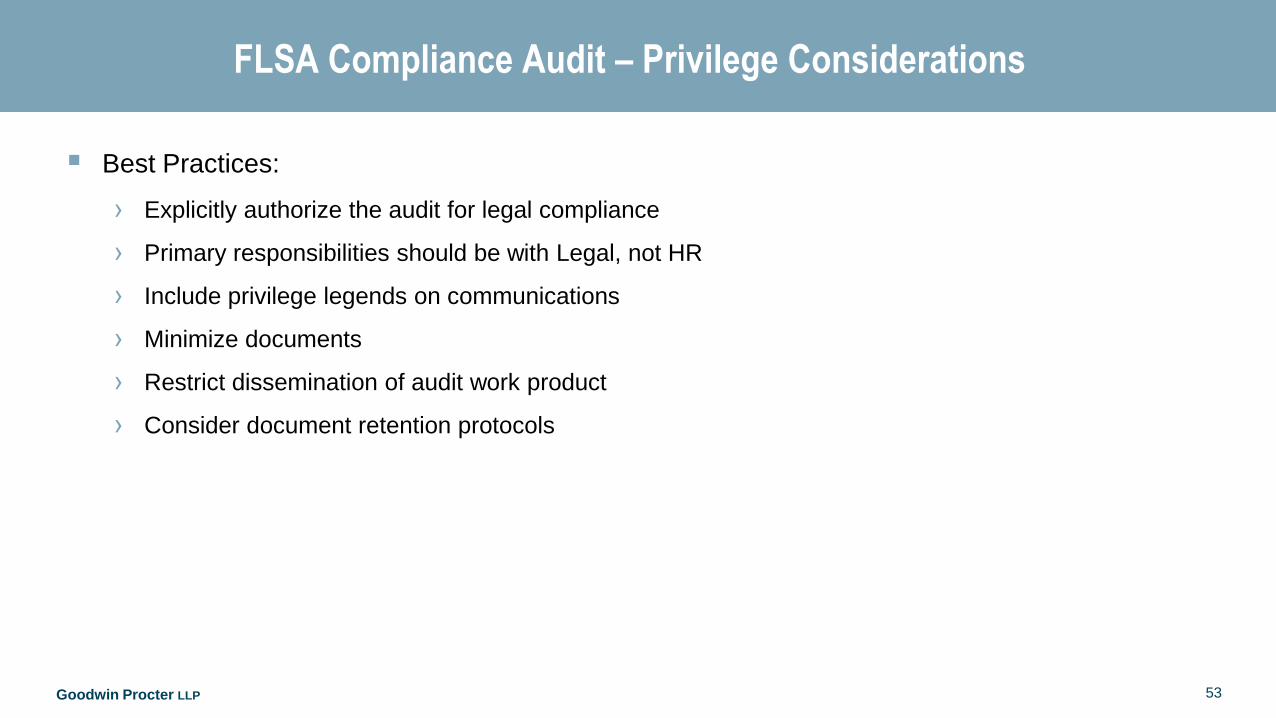

FLSA Compliance Audit – Privilege Considerations

Scope of attorney-client and work product privileges

Key elements:

› Attorney-client privilege: Communication is to secure legal advice and confidentiality is maintained

› Work product privilege: Information is collected in anticipation of (or due to existing) litigation; a

generalized concern about litigation is insufficient

52

Goodwin Procter LLP

FLSA Compliance Audit – Privilege Considerations

Best Practices:

› Explicitly authorize the audit for legal compliance

› Primary responsibilities should be with Legal, not HR

› Include privilege legends on communications

› Minimize documents

› Restrict dissemination of audit work product

› Consider document retention protocols

53

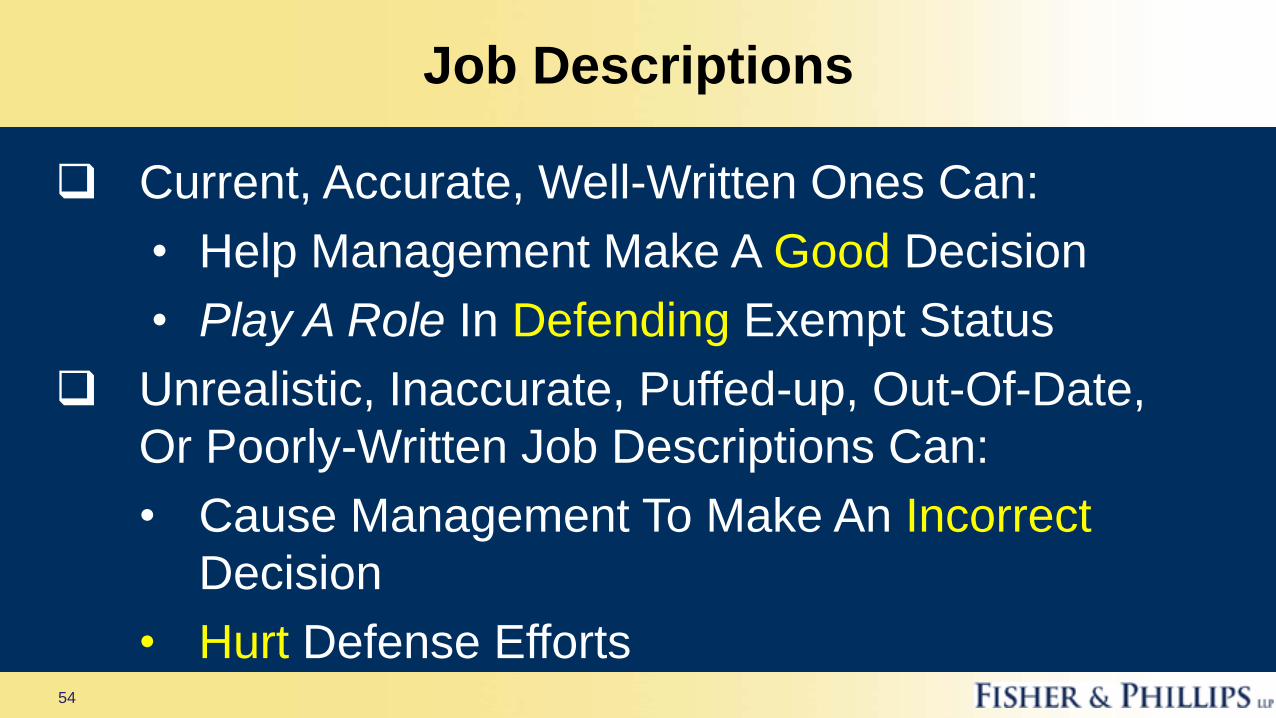

Job Descriptions

Current, Accurate, Well-Written Ones Can:

• Help Management Make A Good Decision

• Play A Role In Defending Exempt Status

Unrealistic, Inaccurate, Puffed-up, Out-Of-Date,

Or Poorly-Written Job Descriptions Can:

• Cause Management To Make An Incorrect

Decision

• Hurt Defense Efforts 54

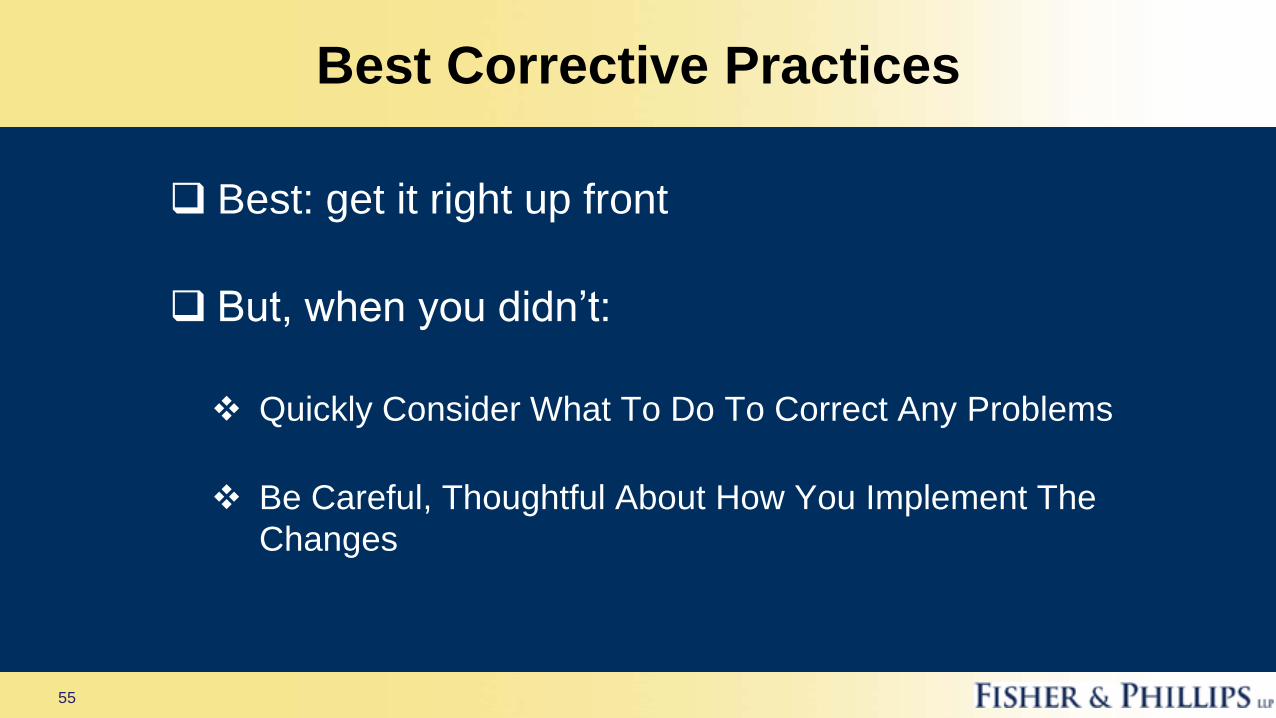

Best Corrective Practices

Best: get it right up front

But, when you didn’t:

Quickly Consider What To Do To Correct Any Problems

Be Careful, Thoughtful About How You Implement The

Changes

55

Goodwin Procter LLP

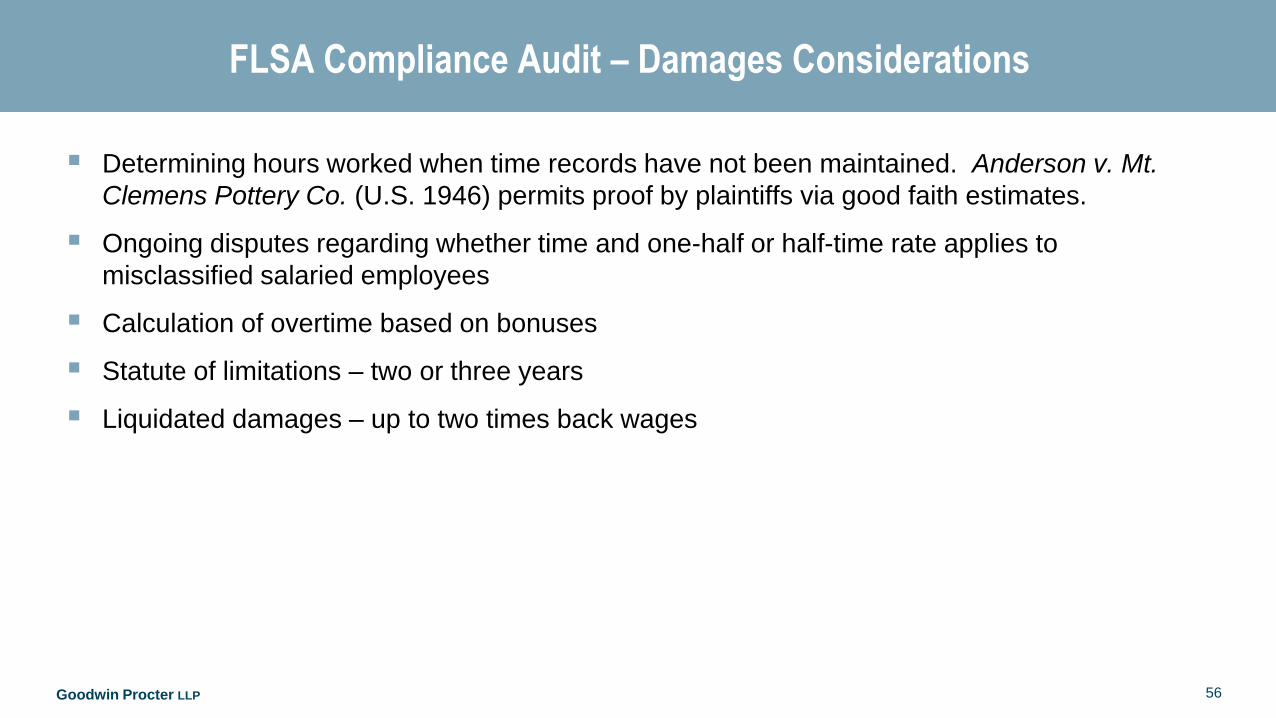

FLSA Compliance Audit – Damages Considerations

Determining hours worked when time records have not been maintained. Anderson v. Mt.

Clemens Pottery Co. (U.S. 1946) permits proof by plaintiffs via good faith estimates.

Ongoing disputes regarding whether time and one-half or half-time rate applies to

misclassified salaried employees

Calculation of overtime based on bonuses

Statute of limitations – two or three years

Liquidated damages – up to two times back wages

56

www.franczek.com

57

Rectifying a Misclassification

Prospective or retroactive?

How far back?

How many employees?

Self-Report?

What to communicate to employees?

www.franczek.com

58

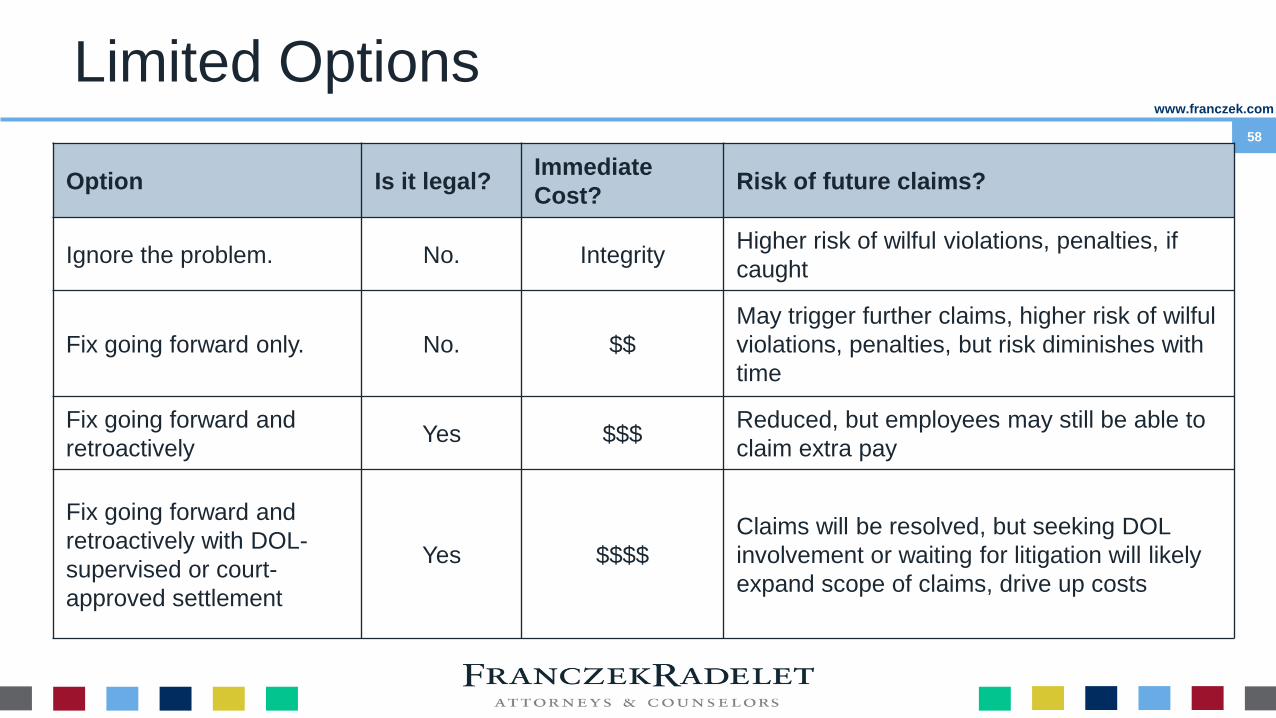

Limited Options

Option Is it legal? Immediate

Cost? Risk of future claims?

Ignore the problem. No. Integrity Higher risk of wilful violations, penalties, if

caught

Fix going forward only. No. $$

May trigger further claims, higher risk of wilful

violations, penalties, but risk diminishes with

time

Fix going forward and

retroactively Yes $$$

Reduced, but employees may still be able to

claim extra pay

Fix going forward and

retroactively with DOL-

supervised or court-

approved settlement

Yes $$$$

Claims will be resolved, but seeking DOL

involvement or waiting for litigation will likely

expand scope of claims, drive up costs

www.franczek.com

59

Retroactive Payments

Calculate amount owed and document calculation

If amount is uncertain (e.g., because hours were not tracked)

seek employee’s agreement

Obtain signed acknowledgement from employee

Consider requesting a release in appropriate cases, but

understand it may not be enforceable.

www.franczek.com

60

Can FLSA Claims be Waived?

Waiver and Release

Acknowledgement

www.franczek.com

61

[COMPANY LETTERHEAD]

ACKNOWLEDGEMENT

The ABC Corporation (the “Company”) employee named below (“Employee”) has been advised as of this date that her job as a Customer Services Account Manager with the Company is being

modified effective September 1, 2015 (“Effective Date”). As of the Effective Date, Employee’s new job title will be (Senior) Customer Service Representative and will thereafter be categorized as “non-

exempt” for purposes of the overtime pay provisions of applicable state and federal wage/hour laws. Employee acknowledges that the basis for this action as been fully explained by the Company and

Employee concurs with this action.

The Company has calculated the amount of additional pay that Employee would have earned if the Employee had been eligible for overtime over the last three years, which equals the payment listed

below. Employee represents that she does not know exactly how may overtime hours she worked but that she worked no more than overtime hours during this period. Employee acknowledges and

agrees that she has analyzed the number of hours she worked during this period and that the payment amount listed is accurate and represent s full compensation for any overtime hours worked during

the three year period. Employee further acknowledges and agrees that the Company has no obligation to make this payment.

Employee agrees that, in exchange for the payment listed below, Employee waives any and all claims for additional unpaid wages, salary, overtime pay or other compensation for work performed for

the Company to date. Employee represents that she has been paid in full for all hours worked fro the Company to day.

Payment to Employee: $___________ (minus applicable withholdings)

Employee has read this acknowledgement and agrees that all statements contained in this document are accurate.

________________________ ABC Corporation

Employee Name (Please Print) By: ______________________ Date: __________________

_________________________

Employee Signature

_________________________

Date

www.franczek.com

62

Thank You

Robert M. Hale

Goodwin Procter

Janet A. Hendrick

Fisher & Phillips

Staci Ketay Rotman

Franczek Radelet

![Litigating under the New USDOL Companionship Rules · 12/3/2015 · New York overtime level pegged to federal exemptions “…employees subject to section 13(a)(2) and (4) of [FLSA],](https://img.pdfslide.us/doc/110x75/5f63ad23f07da806ab1372ab/litigating-under-the-new-usdol-companionship-rules-1232015-new-york-overtime.jpg)

![LeadingAge Financial Managers PowerPoint [Read-Only] Your... · With few exceptions, New York law generally follows the overtime provisions and exemptions set forth by the FLSA. See](https://img.pdfslide.us/doc/110x75/5fe378617e83dc59094cfa8b/leadingage-financial-managers-powerpoint-read-only-your-with-few-exceptions.jpg)