Embed Size (px)

Citation preview

Financial Statement Financial Statement AnalysisAnalysis

Financial Statement Financial Statement AnalysisAnalysis

© Pearson Education Limited 2004Fundamentals of Financial Management, 12/e

Created by: Gregory A. Kuhlemeyer, Ph.D.Carroll College, Waukesha, WI

Financial Financial Statement AnalysisStatement AnalysisFinancial Financial Statement AnalysisStatement Analysis

Financial Statements

A Possible Framework for Analysis

Balance Sheet Ratios

Income Statement and Income Statement/Balance Sheet Ratios

Trend Analysis

Common-Size and Index Analysis

Financial Statements

A Possible Framework for Analysis

Balance Sheet Ratios

Income Statement and Income Statement/Balance Sheet Ratios

Trend Analysis

Common-Size and Index Analysis

Examples of External Uses Examples of External Uses of Statement Analysisof Statement AnalysisExamples of External Uses Examples of External Uses of Statement Analysisof Statement Analysis

Trade CreditorsTrade Creditors -- Focus on the liquidity of the firm.

BondholdersBondholders -- Focus on the long-term cash flow of the firm.

ShareholdersShareholders -- Focus on the profitability and long-term health of the firm.

Trade CreditorsTrade Creditors -- Focus on the liquidity of the firm.

BondholdersBondholders -- Focus on the long-term cash flow of the firm.

ShareholdersShareholders -- Focus on the profitability and long-term health of the firm.

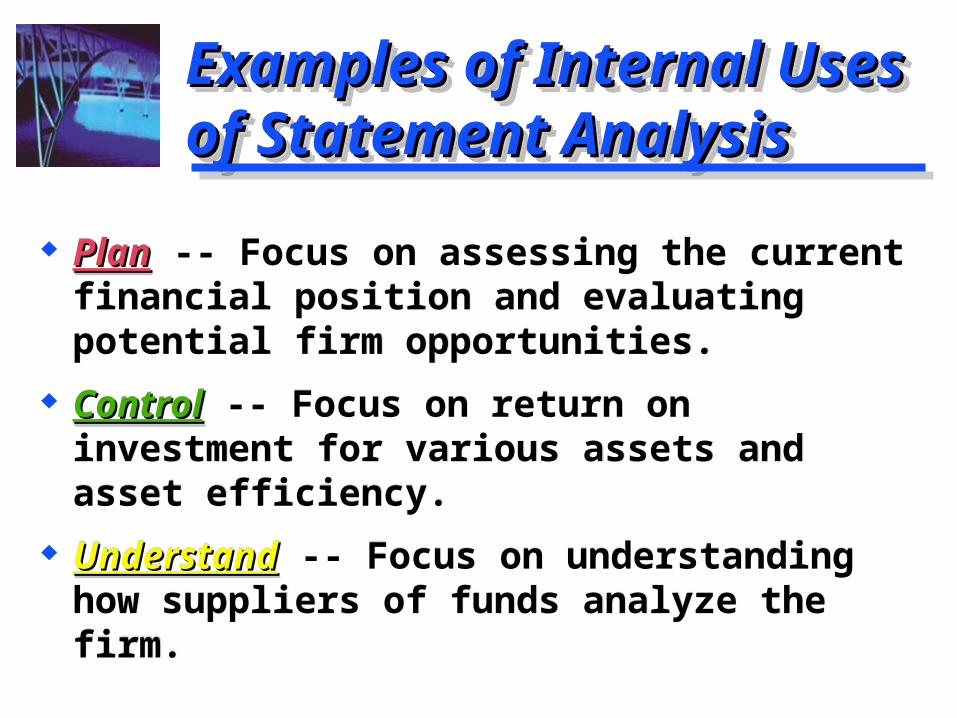

Examples of Internal Uses Examples of Internal Uses of Statement Analysisof Statement AnalysisExamples of Internal Uses Examples of Internal Uses of Statement Analysisof Statement Analysis

PlanPlan -- Focus on assessing the current financial position and evaluating potential firm opportunities.

ControlControl -- Focus on return on investment for various assets and asset efficiency.

UnderstandUnderstand -- Focus on understanding how suppliers of funds analyze the firm.

PlanPlan -- Focus on assessing the current financial position and evaluating potential firm opportunities.

ControlControl -- Focus on return on investment for various assets and asset efficiency.

UnderstandUnderstand -- Focus on understanding how suppliers of funds analyze the firm.

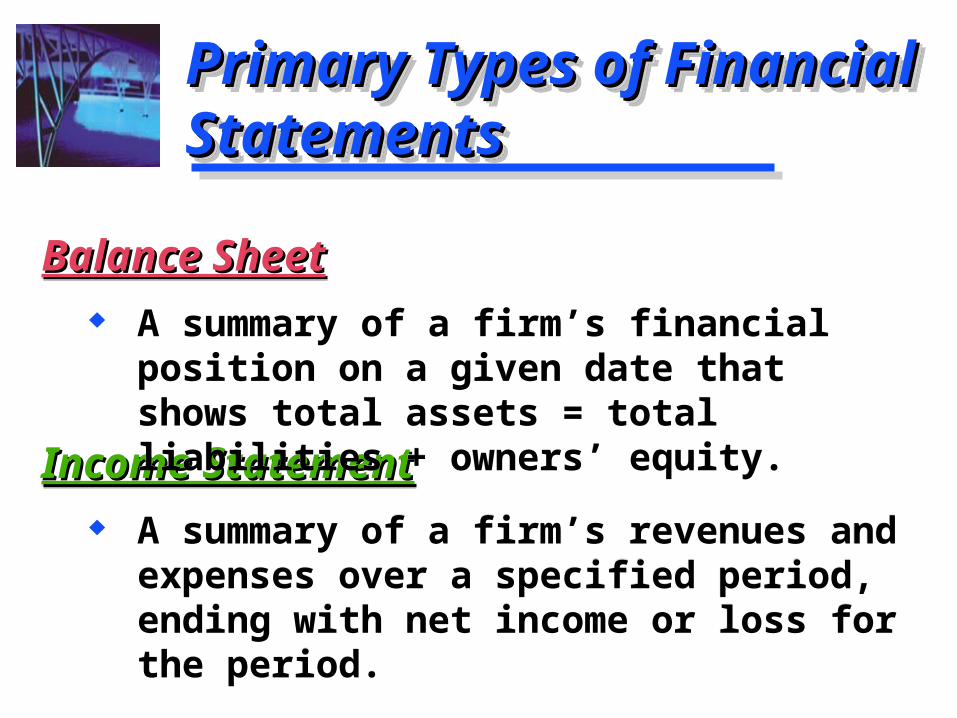

Primary Types of Primary Types of Financial StatementsFinancial StatementsPrimary Types of Primary Types of Financial StatementsFinancial Statements

Income StatementIncome Statement A summary of a firm’s revenues and

expenses over a specified period, ending with net income or loss for the period.

Income StatementIncome Statement A summary of a firm’s revenues and

expenses over a specified period, ending with net income or loss for the period.

Balance SheetBalance Sheet A summary of a firm’s financial position on

a given date that shows total assets = total liabilities + owners’ equity.

Balance SheetBalance Sheet A summary of a firm’s financial position on

a given date that shows total assets = total liabilities + owners’ equity.

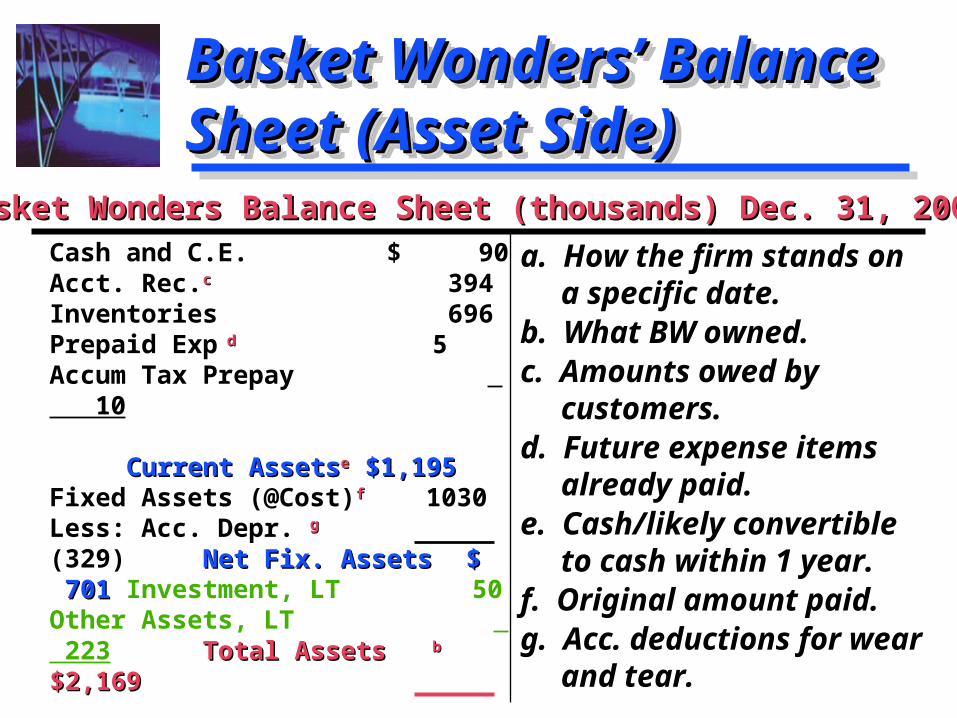

Basket Wonders’ Balance Basket Wonders’ Balance Sheet (Asset Side)Sheet (Asset Side)Basket Wonders’ Balance Basket Wonders’ Balance Sheet (Asset Side)Sheet (Asset Side)

a. How the firm stands on a specific date.

b. What BW owned.c. Amounts owed by

customers.d. Future expense items

already paid.e. Cash/likely convertible

to cash within 1 year.f. Original amount paid.g. Acc. deductions for

wear and tear.

a. How the firm stands on a specific date.

b. What BW owned.c. Amounts owed by

customers.d. Future expense items

already paid.e. Cash/likely convertible

to cash within 1 year.f. Original amount paid.g. Acc. deductions for

wear and tear.

Cash and C.E. $ 90 Acct. Rec.cc 394 Inventories 696 Prepaid Exp dd 5 Accum Tax Prepay 10 Current AssetsCurrent Assetsee $1,195 $1,195 Fixed Assets (@Cost)ff 1030 Less: Acc. Depr. gg (329)

Net Fix. AssetsNet Fix. Assets $ 701 $ 701 Investment, LT 50 Other Assets, LT 223

Total AssetsTotal Assetsbb $2,169 $2,169

Basket Wonders Balance Sheet (thousands) Dec. 31, 2007Basket Wonders Balance Sheet (thousands) Dec. 31, 2007a

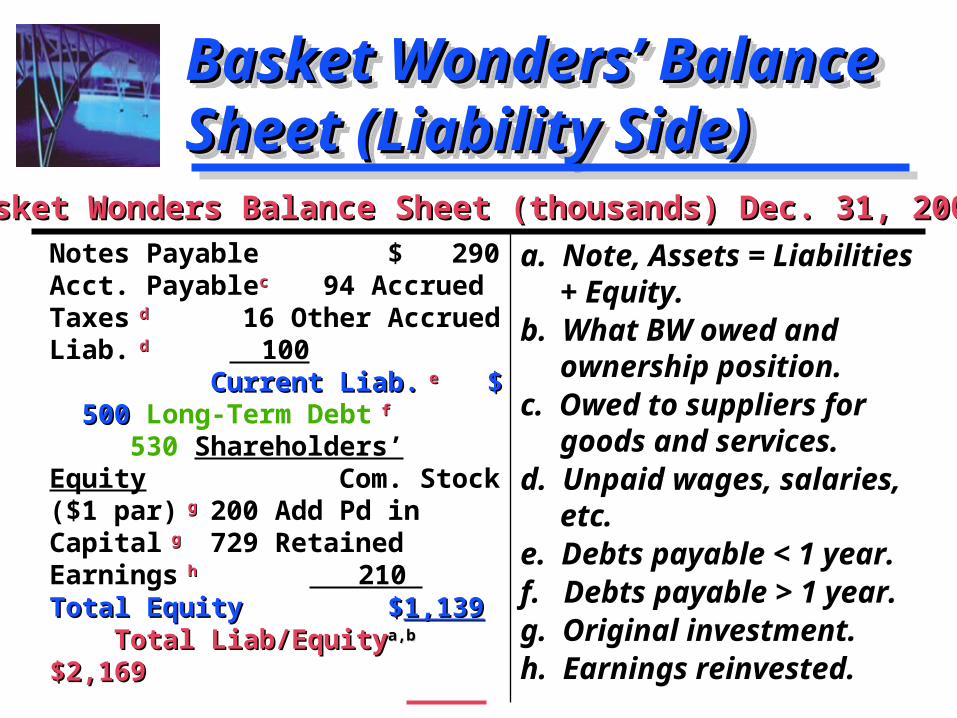

Basket Wonders’ Balance Basket Wonders’ Balance Sheet (Liability Side)Sheet (Liability Side)Basket Wonders’ Balance Basket Wonders’ Balance Sheet (Liability Side)Sheet (Liability Side)

a. Note, Assets = Liabilities + Equity.

b. What BW owed and ownership position.

c. Owed to suppliers for goods and services.

d. Unpaid wages, salaries, etc.

e. Debts payable < 1 year.f. Debts payable > 1 year.g. Original investment. h. Earnings reinvested.

a. Note, Assets = Liabilities + Equity.

b. What BW owed and ownership position.

c. Owed to suppliers for goods and services.

d. Unpaid wages, salaries, etc.

e. Debts payable < 1 year.f. Debts payable > 1 year.g. Original investment. h. Earnings reinvested.

Notes Payable $ 290 Acct. Payablecc 94 Accrued Taxes dd 16 Other Accrued Liab. dd 100 Current Liab.Current Liab. ee $ $ 500 500 Long-Term Debt ff

530 Shareholders’ Equity Com. Stock ($1 par) gg 200 Add Pd in Capital gg

729 Retained Earnings hh 210 Total Total EquityEquity $ $1,1391,139 Total Liab/EquityTotal Liab/Equitya,ba,b $2,169 $2,169

Basket Wonders Balance Sheet (thousands) Dec. 31, 2007Basket Wonders Balance Sheet (thousands) Dec. 31, 2007

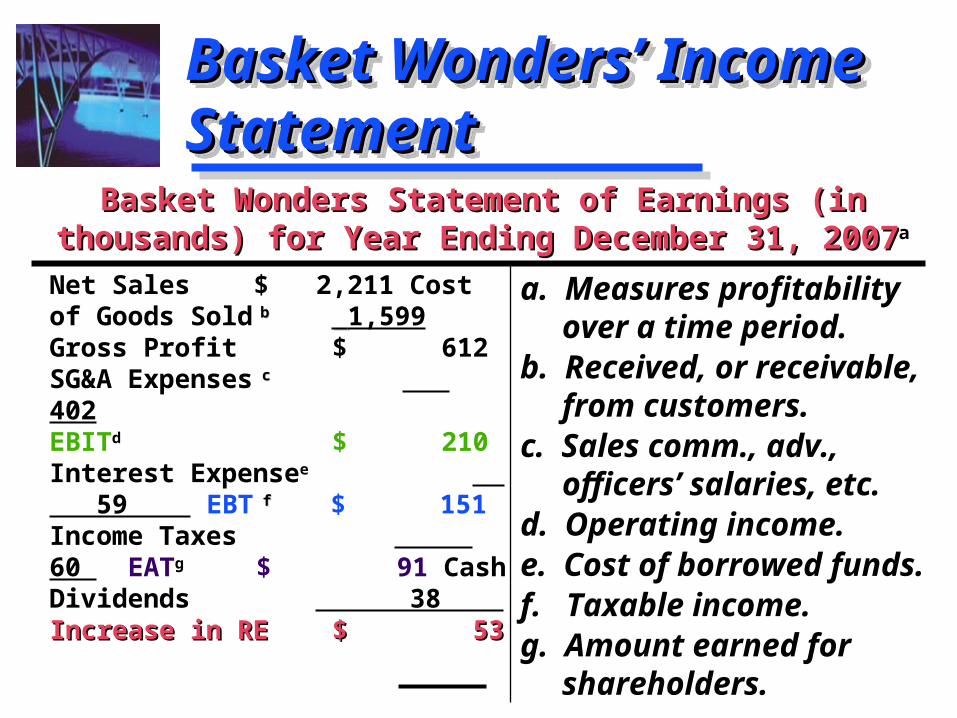

Basket Wonders’ Basket Wonders’ Income StatementIncome StatementBasket Wonders’ Basket Wonders’ Income StatementIncome Statement

a. Measures profitability over a time period.

b. Received, or receivable, from customers.

c. Sales comm., adv., officers’ salaries, etc.

d. Operating income.e. Cost of borrowed funds.f. Taxable income.g. Amount earned for

shareholders.

a. Measures profitability over a time period.

b. Received, or receivable, from customers.

c. Sales comm., adv., officers’ salaries, etc.

d. Operating income.e. Cost of borrowed funds.f. Taxable income.g. Amount earned for

shareholders.

Net Sales $ 2,211 Cost of Goods Sold bb 1,599

Gross Profit $ 612 SG&A Expenses c c 402 EBITd $ 210 Interest Expensee 59 EBT f f $ 151 Income Taxes 60 EATg $ 91 Cash Dividends 38 Increase in REIncrease in RE $ 53 $ 53

Basket Wonders Statement of Earnings (in thousands) Basket Wonders Statement of Earnings (in thousands) for Year Ending December 31, 2007for Year Ending December 31, 2007a

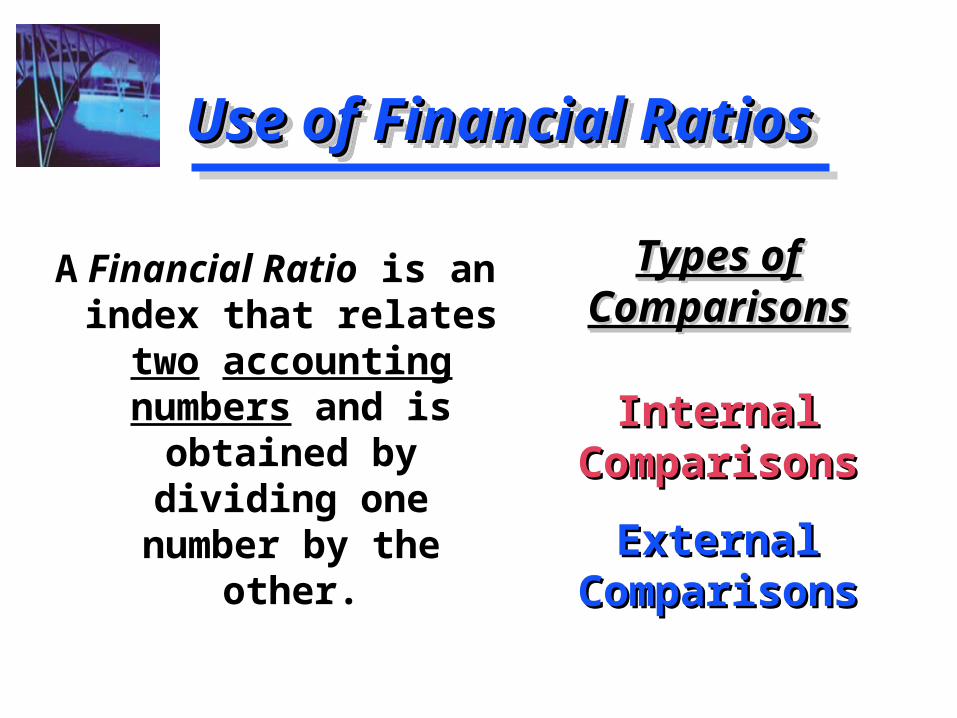

Use of Financial RatiosUse of Financial RatiosUse of Financial RatiosUse of Financial Ratios

Types of Types of ComparisonsComparisons

Internal Internal ComparisonsComparisons

External External ComparisonsComparisons

Types of Types of ComparisonsComparisons

Internal Internal ComparisonsComparisons

External External ComparisonsComparisons

A Financial Ratio is an index that relates

two accounting numbers and is

obtained by dividing one number by the

other.

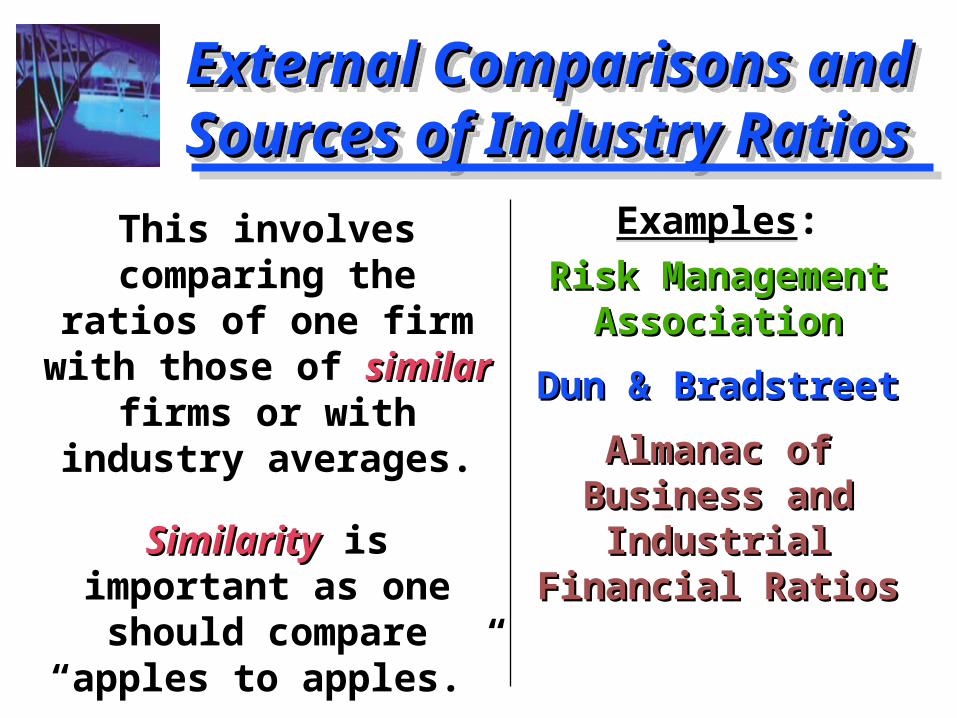

External Comparisons and External Comparisons and Sources of Industry RatiosSources of Industry RatiosExternal Comparisons and External Comparisons and Sources of Industry RatiosSources of Industry Ratios

Examples:

Risk Management Risk Management AssociationAssociation

Dun & BradstreetDun & Bradstreet

Almanac of Almanac of Business and Business and

Industrial Industrial Financial RatiosFinancial Ratios

Examples:

Risk Management Risk Management AssociationAssociation

Dun & BradstreetDun & Bradstreet

Almanac of Almanac of Business and Business and

Industrial Industrial Financial RatiosFinancial Ratios

This involves comparing the ratios of one firm with those of similarsimilar firms or with

industry averages.

SimilaritySimilarity is important as one should

compare “apples to apples.”

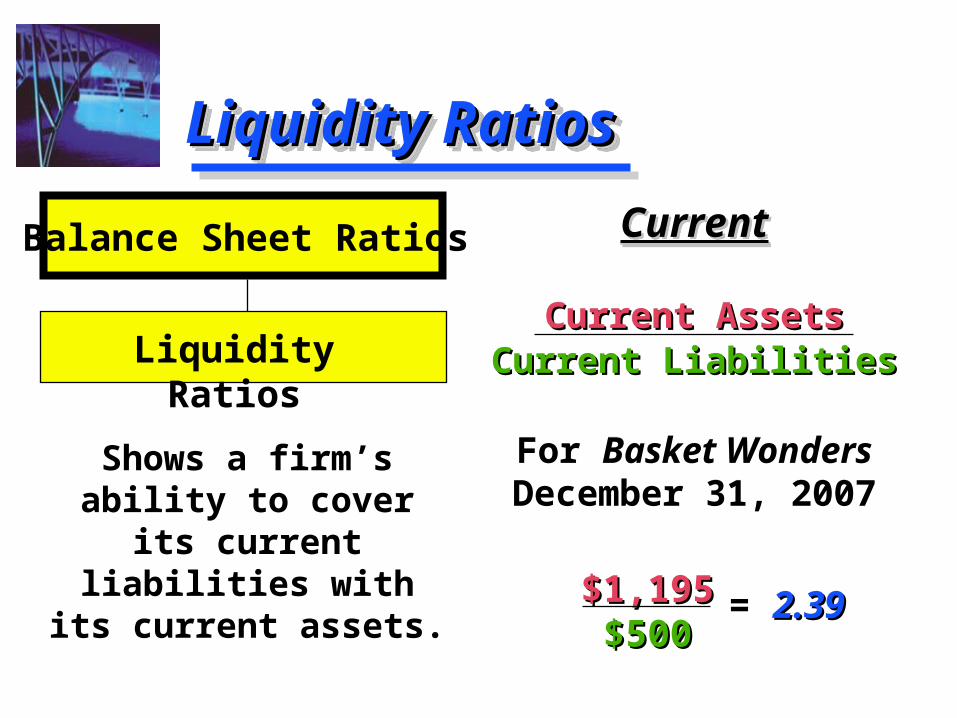

Liquidity RatiosLiquidity RatiosLiquidity RatiosLiquidity Ratios

CurrentCurrent

Current AssetsCurrent AssetsCurrent LiabilitiesCurrent Liabilities

For Basket Wonders December 31, 2007

CurrentCurrent

Current AssetsCurrent AssetsCurrent LiabilitiesCurrent Liabilities

For Basket Wonders December 31, 2007

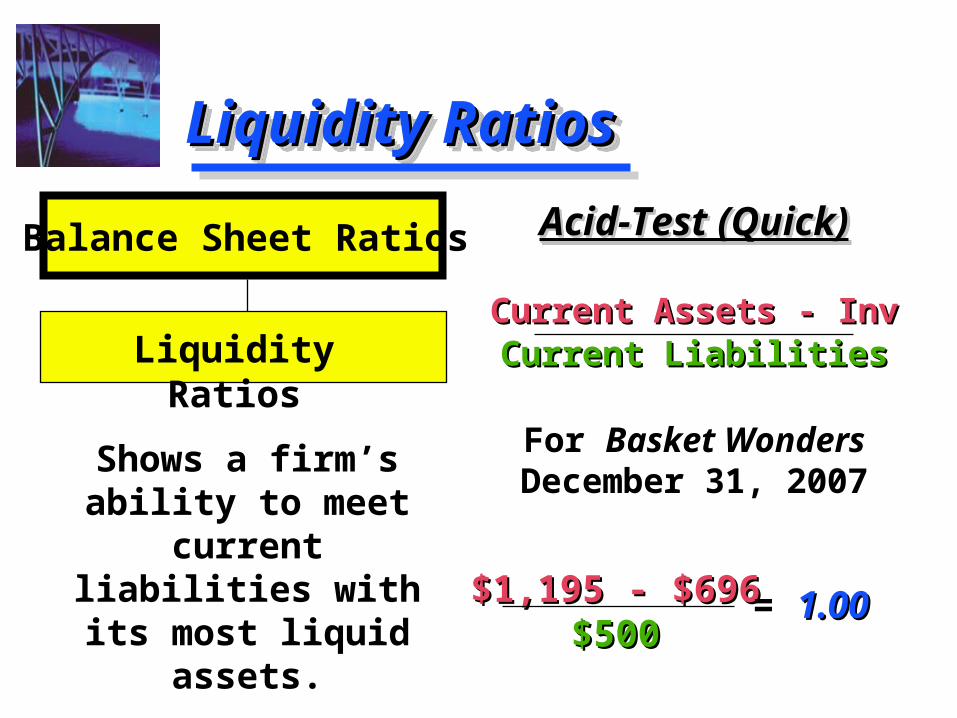

Shows a firm’s ability to cover its current liabilities with its current

assets.

Balance Sheet Ratios

Liquidity Ratios

$1,195$1,195$500$500

= 2.392.39

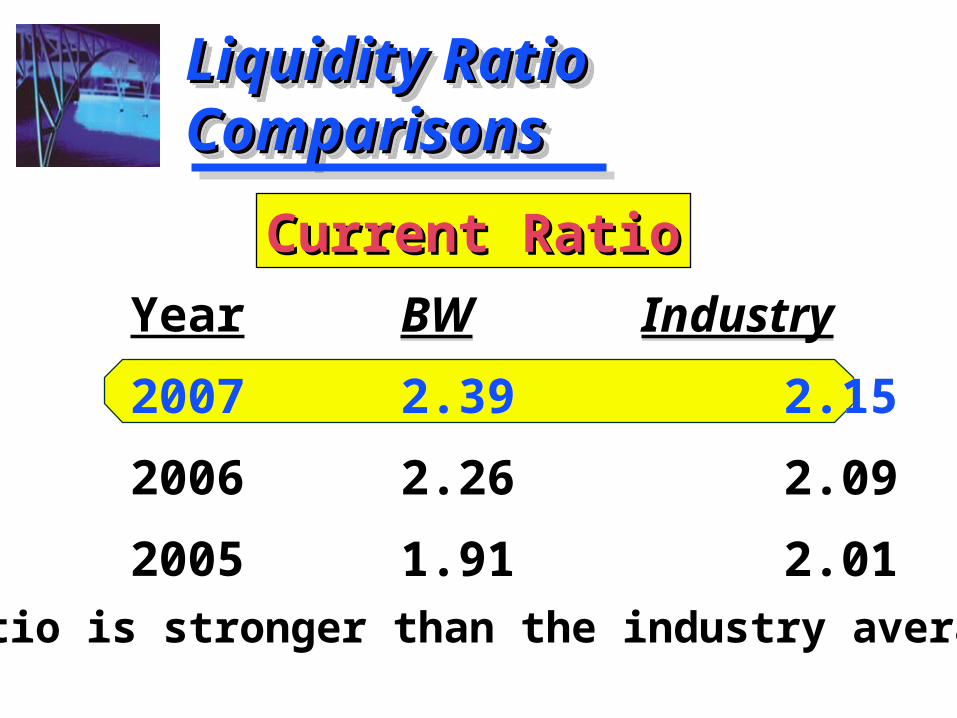

Liquidity Ratio Liquidity Ratio ComparisonsComparisonsLiquidity Ratio Liquidity Ratio ComparisonsComparisons

BW Industry

2.39 2.15

2.26 2.09

1.91 2.01

BW Industry

2.39 2.15

2.26 2.09

1.91 2.01

Year

2007

2006

2005

CurrentCurrent RatioRatio

Ratio is stronger than the industry average.

Liquidity RatiosLiquidity RatiosLiquidity RatiosLiquidity Ratios

Acid-Test (Quick)Acid-Test (Quick)

Current Assets - InvCurrent Assets - InvCurrent LiabilitiesCurrent Liabilities

For Basket Wonders December 31, 2007

Acid-Test (Quick)Acid-Test (Quick)

Current Assets - InvCurrent Assets - InvCurrent LiabilitiesCurrent Liabilities

For Basket Wonders December 31, 2007

Shows a firm’s ability to meet

current liabilities with its most liquid

assets.

Balance Sheet Ratios

Liquidity Ratios

$1,195 - $696$1,195 - $696$500$500

= 1.001.00

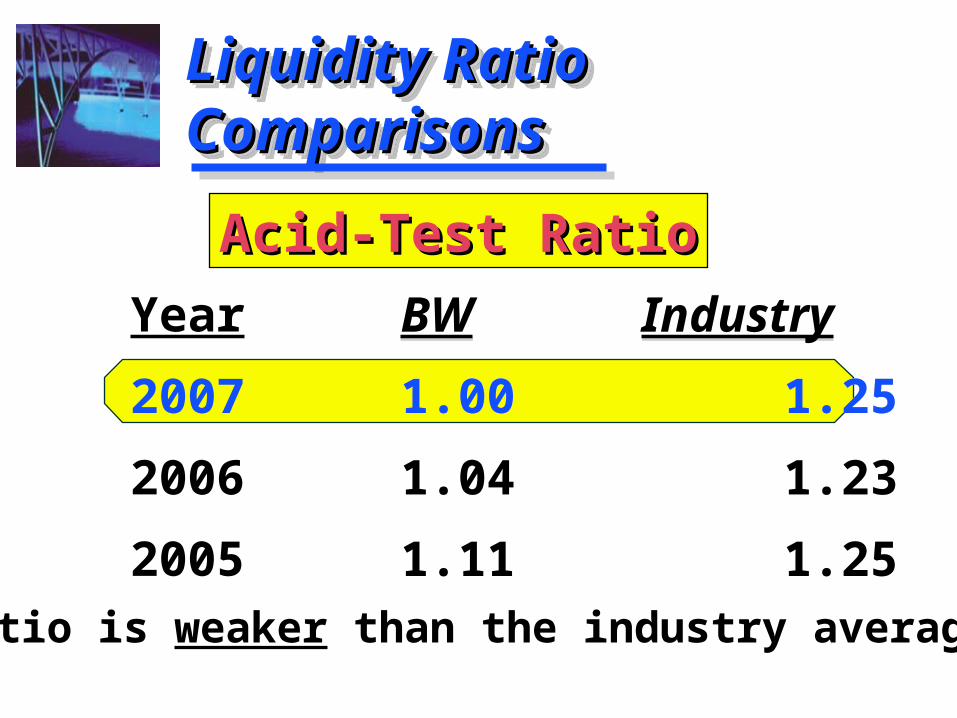

Liquidity Ratio Liquidity Ratio ComparisonsComparisonsLiquidity Ratio Liquidity Ratio ComparisonsComparisons

BW Industry

1.00 1.25

1.04 1.23

1.11 1.25

BW Industry

1.00 1.25

1.04 1.23

1.11 1.25

Year

2007

2006

2005

Acid-Test RatioAcid-Test Ratio

Ratio is weaker than the industry average.

Summary of the Liquidity Summary of the Liquidity Ratio ComparisonsRatio ComparisonsSummary of the Liquidity Summary of the Liquidity Ratio ComparisonsRatio Comparisons

Strong current ratio and weak acid-test ratio indicates a potential problem in the inventories account.

Note that this industry has a relatively high level of inventories.

Strong current ratio and weak acid-test ratio indicates a potential problem in the inventories account.

Note that this industry has a relatively high level of inventories.

RatioRatio BWBW IndustryIndustry

Current 2.39 2.15

Acid-Test 1.00 1.25

Current Ratio -- Trend Current Ratio -- Trend Analysis ComparisonAnalysis ComparisonCurrent Ratio -- Trend Current Ratio -- Trend Analysis ComparisonAnalysis Comparison

Trend Analysis of Current Ratio

1.5

1.7

1.9

2.1

2.3

2.5

2005 2006 2007

Analysis Year

Rat

io V

alu

e

BW

Industry

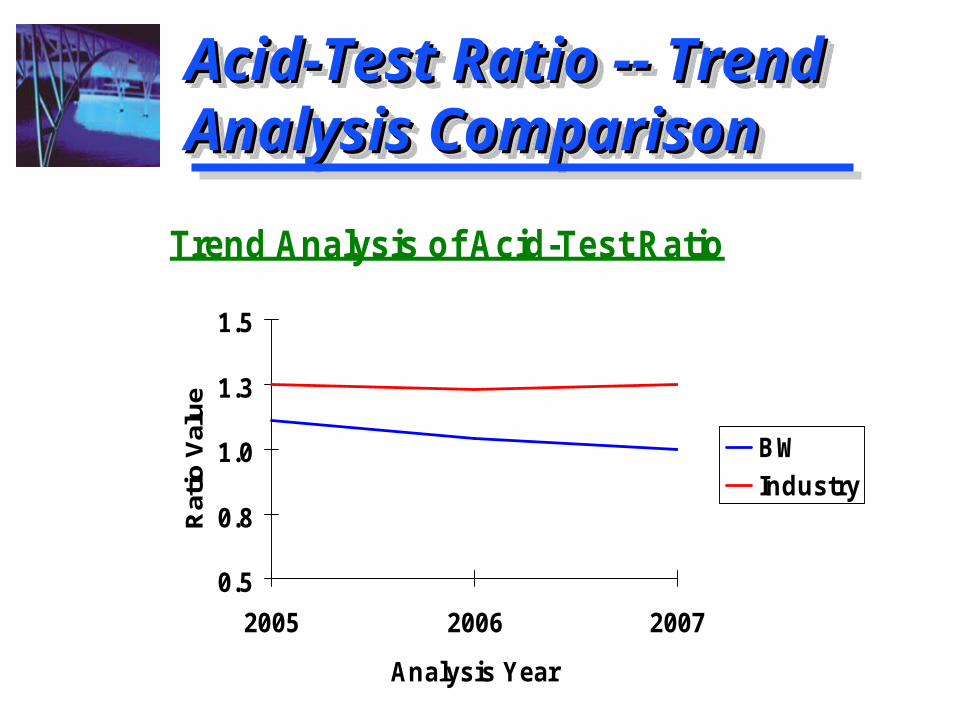

Acid-Test Ratio -- Trend Acid-Test Ratio -- Trend Analysis ComparisonAnalysis ComparisonAcid-Test Ratio -- Trend Acid-Test Ratio -- Trend Analysis ComparisonAnalysis Comparison

Trend Analysis of Acid-Test Ratio

0.5

0.8

1.0

1.3

1.5

2005 2006 2007

Analysis Year

Rat

io V

alu

e

BW

Industry

Summary of the Liquidity Summary of the Liquidity Trend AnalysesTrend AnalysesSummary of the Liquidity Summary of the Liquidity Trend AnalysesTrend Analyses

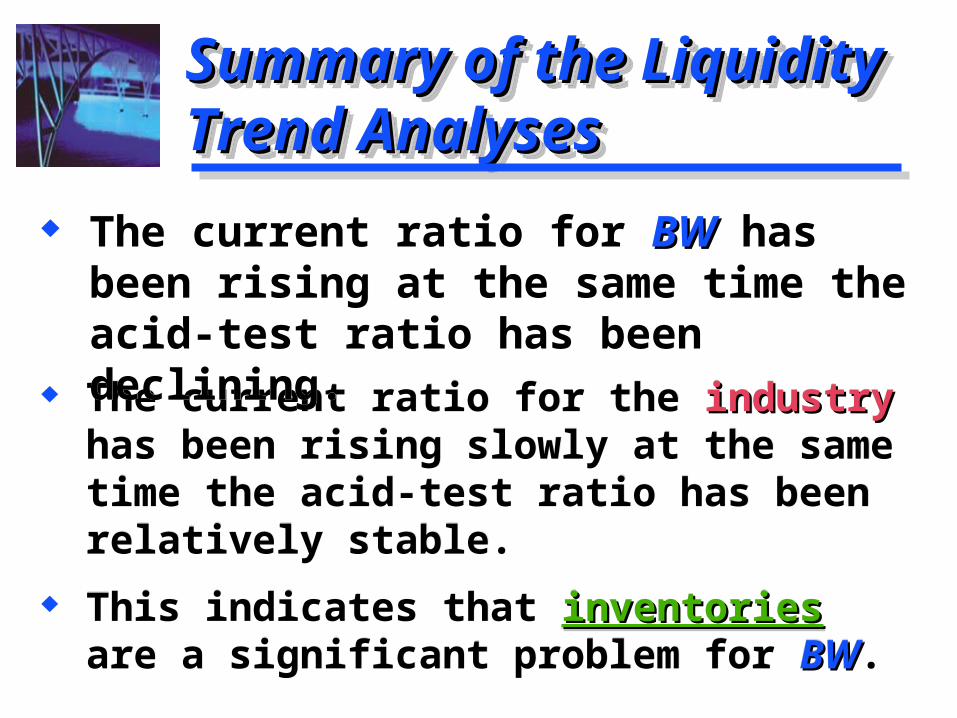

The current ratio for the industryindustry has been rising slowly at the same time the acid-test ratio has been relatively stable.

This indicates that inventoriesinventories are a significant problem for BWBW.

The current ratio for the industryindustry has been rising slowly at the same time the acid-test ratio has been relatively stable.

This indicates that inventoriesinventories are a significant problem for BWBW.

The current ratio for BWBW has been rising at the same time the acid-test ratio has been declining.

The current ratio for BWBW has been rising at the same time the acid-test ratio has been declining.

Financial Leverage RatiosFinancial Leverage RatiosFinancial Leverage RatiosFinancial Leverage Ratios

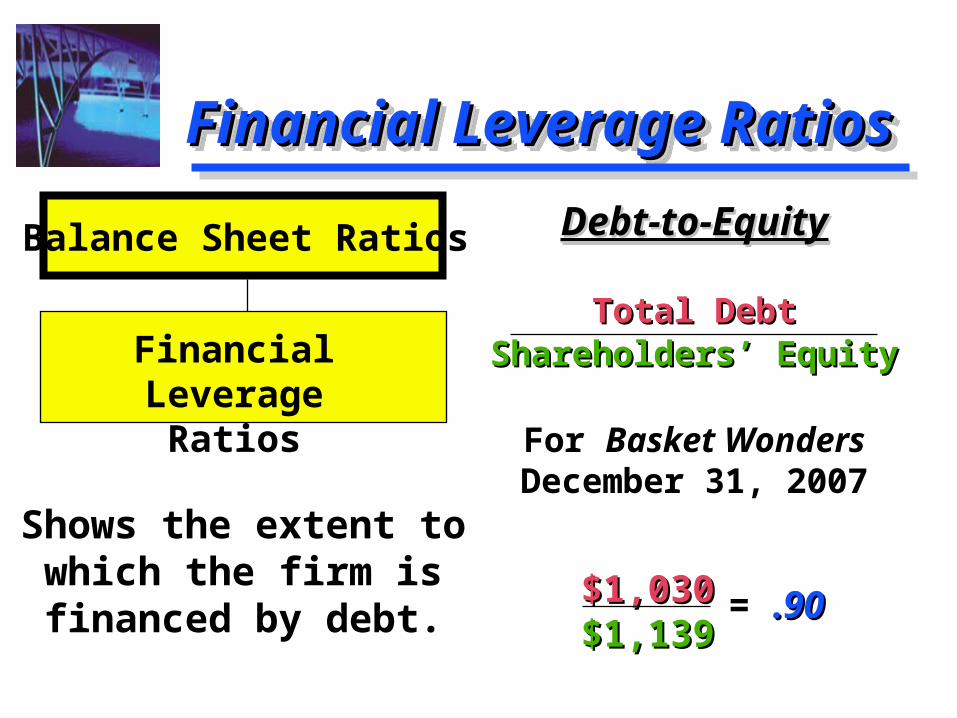

Debt-to-EquityDebt-to-Equity

Total DebtTotal DebtShareholders’ EquityShareholders’ Equity

For Basket Wonders December 31, 2007

Debt-to-EquityDebt-to-Equity

Total DebtTotal DebtShareholders’ EquityShareholders’ Equity

For Basket Wonders December 31, 2007Shows the extent to

which the firm is financed by debt.

Balance Sheet Ratios

Financial LeverageRatios

$1,030$1,030$1,139$1,139

= .90.90

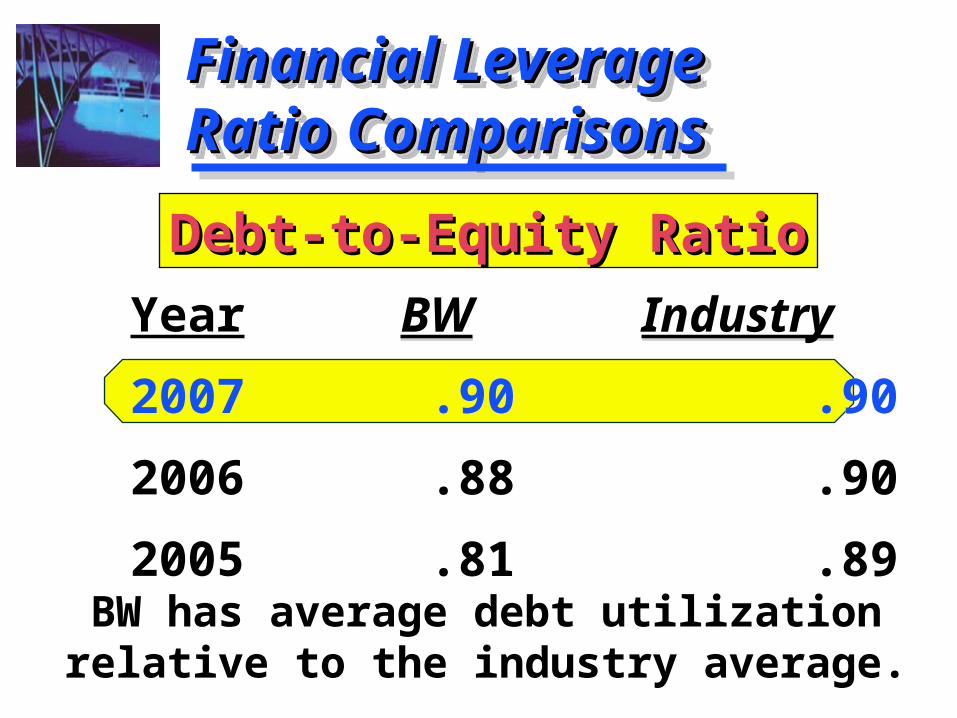

Financial Leverage Financial Leverage Ratio ComparisonsRatio ComparisonsFinancial Leverage Financial Leverage Ratio ComparisonsRatio Comparisons

BW Industry

.90 .90

.88 .90

.81 .89

BW Industry

.90 .90

.88 .90

.81 .89

Year

2007

2006

2005

Debt-to-Equity RatioDebt-to-Equity Ratio

BW has average debt utilizationrelative to the industry average.

Financial Leverage RatiosFinancial Leverage RatiosFinancial Leverage RatiosFinancial Leverage Ratios

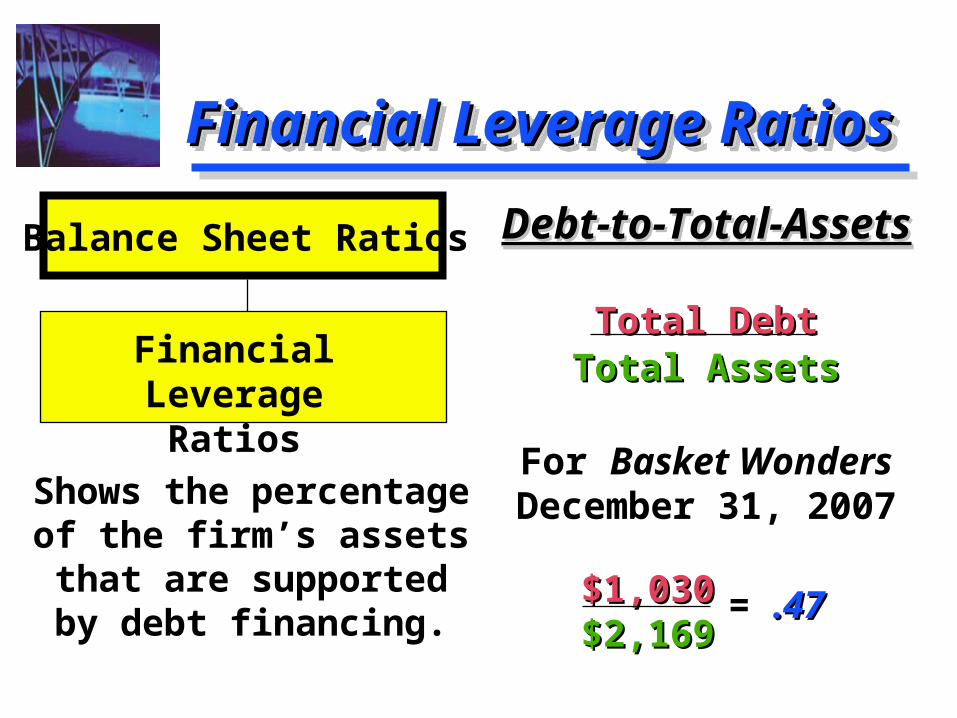

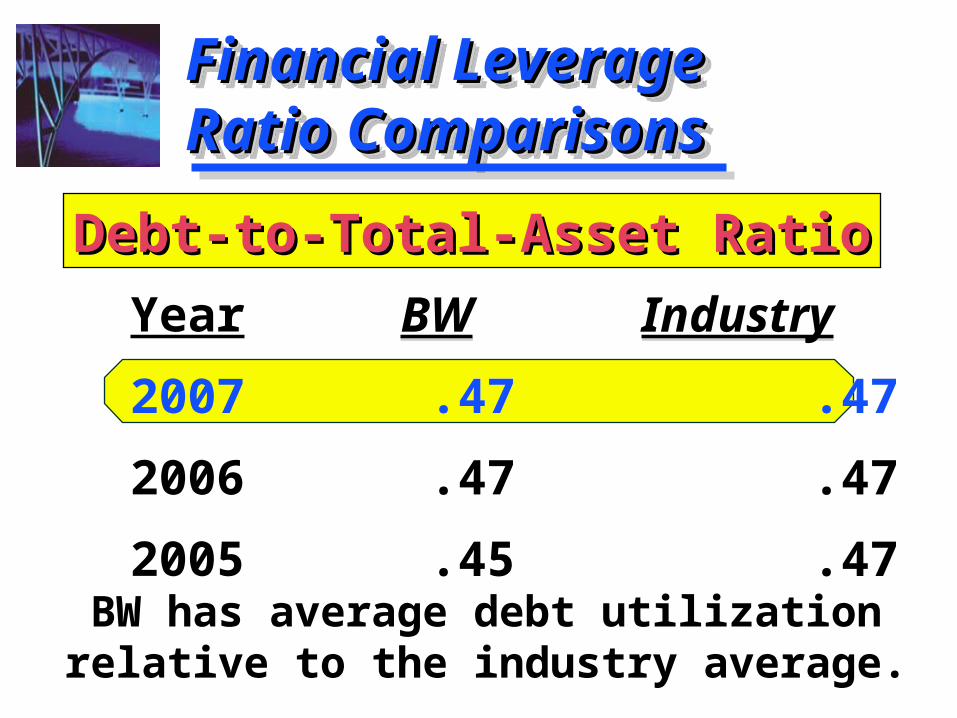

Debt-to-Total-AssetsDebt-to-Total-Assets

Total DebtTotal DebtTotal AssetsTotal Assets

For Basket Wonders December 31, 2007

Debt-to-Total-AssetsDebt-to-Total-Assets

Total DebtTotal DebtTotal AssetsTotal Assets

For Basket Wonders December 31, 2007Shows the percentage

of the firm’s assets that are supported by

debt financing.

Balance Sheet Ratios

Financial LeverageRatios

$1,030$1,030$2,169$2,169

= .47.47

Financial Leverage Financial Leverage Ratio ComparisonsRatio ComparisonsFinancial Leverage Financial Leverage Ratio ComparisonsRatio Comparisons

BW Industry

.47 .47

.47 .47

.45 .47

BW Industry

.47 .47

.47 .47

.45 .47

Year

2007

2006

2005

Debt-to-Total-Asset RatioDebt-to-Total-Asset Ratio

BW has average debt utilizationrelative to the industry average.

Financial Leverage RatiosFinancial Leverage RatiosFinancial Leverage RatiosFinancial Leverage Ratios

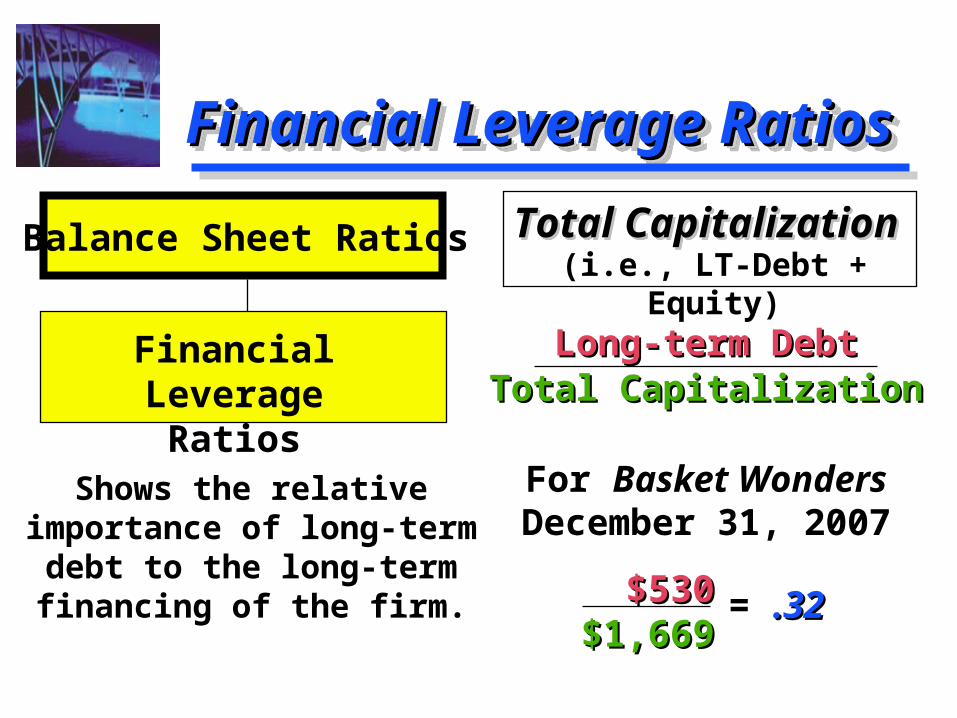

Total CapitalizationTotal Capitalization

Long-term DebtLong-term DebtTotal CapitalizationTotal Capitalization

For Basket Wonders December 31, 2007

Total CapitalizationTotal Capitalization

Long-term DebtLong-term DebtTotal CapitalizationTotal Capitalization

For Basket Wonders December 31, 2007

Shows the relative importance of long-term

debt to the long-term financing of the firm.

Balance Sheet Ratios

Financial LeverageRatios

$530$530$1,669$1,669

= .32.32

(i.e., LT-Debt + Equity)

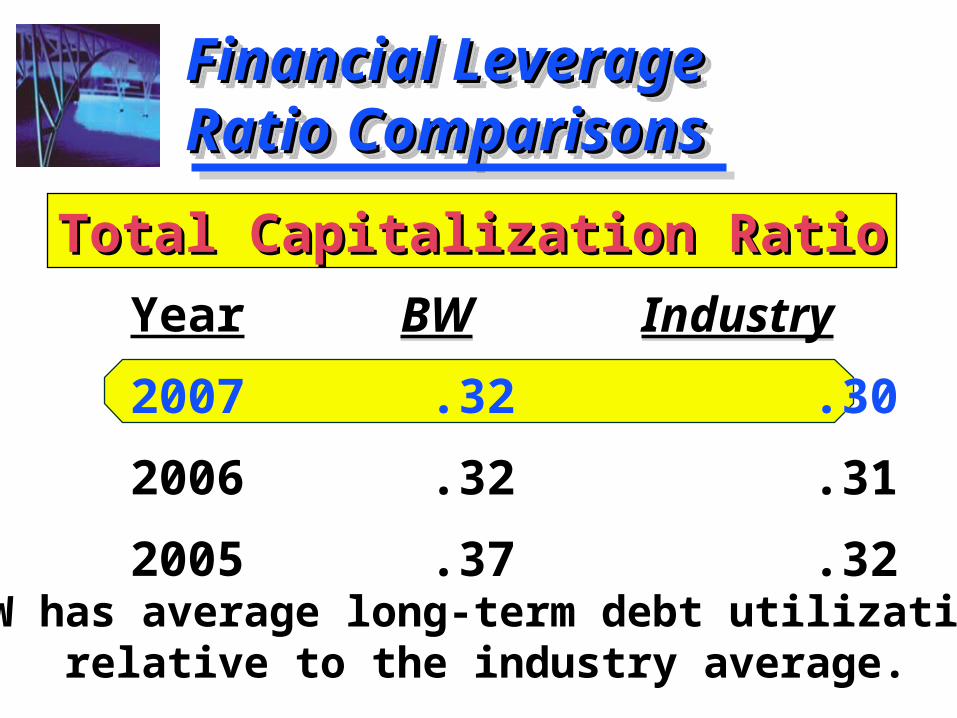

Financial Leverage Financial Leverage Ratio ComparisonsRatio ComparisonsFinancial Leverage Financial Leverage Ratio ComparisonsRatio Comparisons

BW Industry

.32 .30

.32 .31

.37 .32

BW Industry

.32 .30

.32 .31

.37 .32

Year

2007

2006

2005

Total Capitalization RatioTotal Capitalization Ratio

BW has average long-term debt utilizationrelative to the industry average.

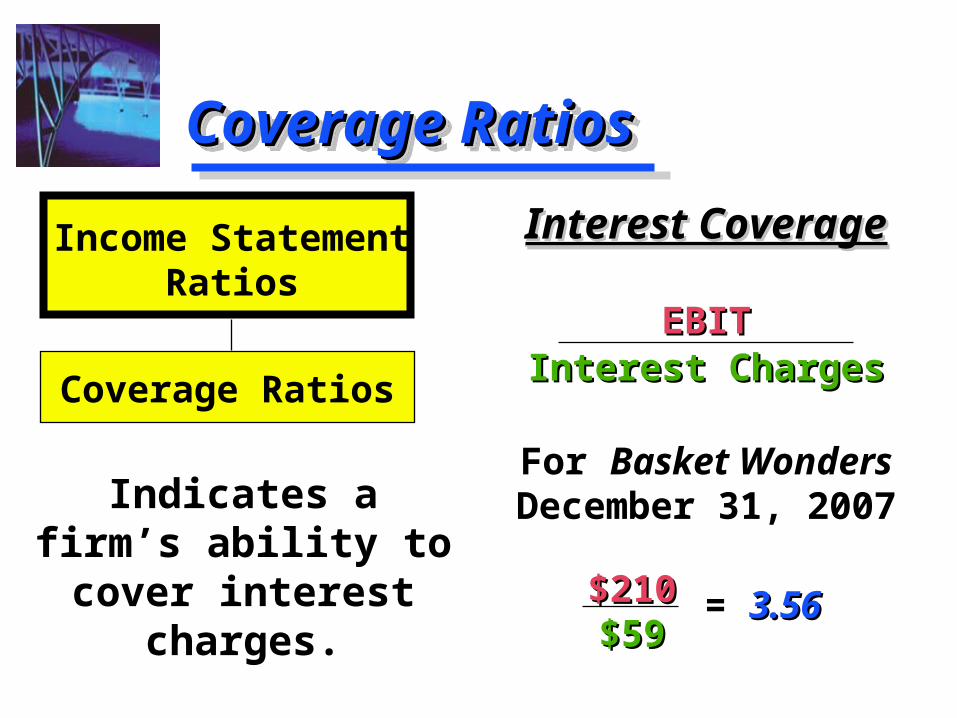

Coverage RatiosCoverage RatiosCoverage RatiosCoverage Ratios

Interest CoverageInterest Coverage

EBITEBITInterest ChargesInterest Charges

For Basket Wonders December 31, 2007

Interest CoverageInterest Coverage

EBITEBITInterest ChargesInterest Charges

For Basket Wonders December 31, 2007Indicates a firm’s

ability to cover interest charges.

Income StatementRatios

Coverage Ratios

$210$210$59$59

= 3.563.56

CoverageCoverageRatio ComparisonsRatio ComparisonsCoverageCoverageRatio ComparisonsRatio Comparisons

BW Industry

3.56 5.19

4.35 5.02

10.30 4.66

BW Industry

3.56 5.19

4.35 5.02

10.30 4.66

Year

2007

2006

2005

Interest Coverage RatioInterest Coverage Ratio

BW has below average interest coveragerelative to the industry average.

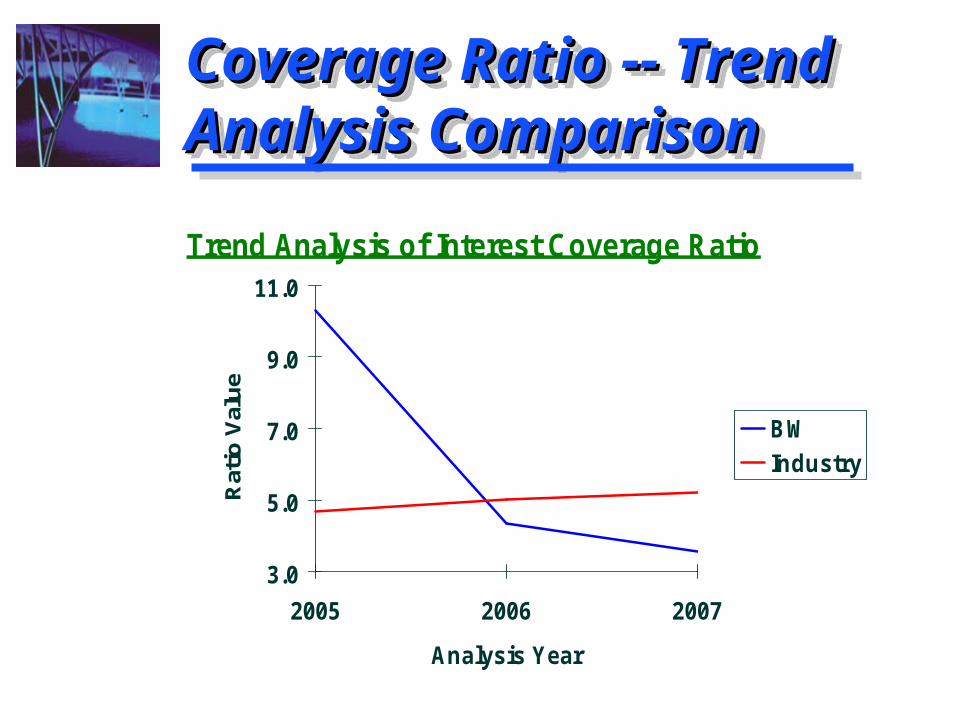

Coverage Ratio -- Trend Coverage Ratio -- Trend Analysis ComparisonAnalysis ComparisonCoverage Ratio -- Trend Coverage Ratio -- Trend Analysis ComparisonAnalysis Comparison

Trend Analysis of Interest Coverage Ratio

3.0

5.0

7.0

9.0

11.0

2005 2006 2007

Analysis Year

Rat

io V

alu

e

BW

Industry

Summary of the Coverage Summary of the Coverage Trend AnalysisTrend AnalysisSummary of the Coverage Summary of the Coverage Trend AnalysisTrend Analysis

This indicates that low earnings low earnings (EBIT) may be a potential problem for BWBW.

Note, we know that debt levels debt levels are in line with the industryindustry averages.

This indicates that low earnings low earnings (EBIT) may be a potential problem for BWBW.

Note, we know that debt levels debt levels are in line with the industryindustry averages.

The interest coverage ratio for BWBW has been falling since 2005. It has been below industryindustry averages for the past two years.

The interest coverage ratio for BWBW has been falling since 2005. It has been below industryindustry averages for the past two years.

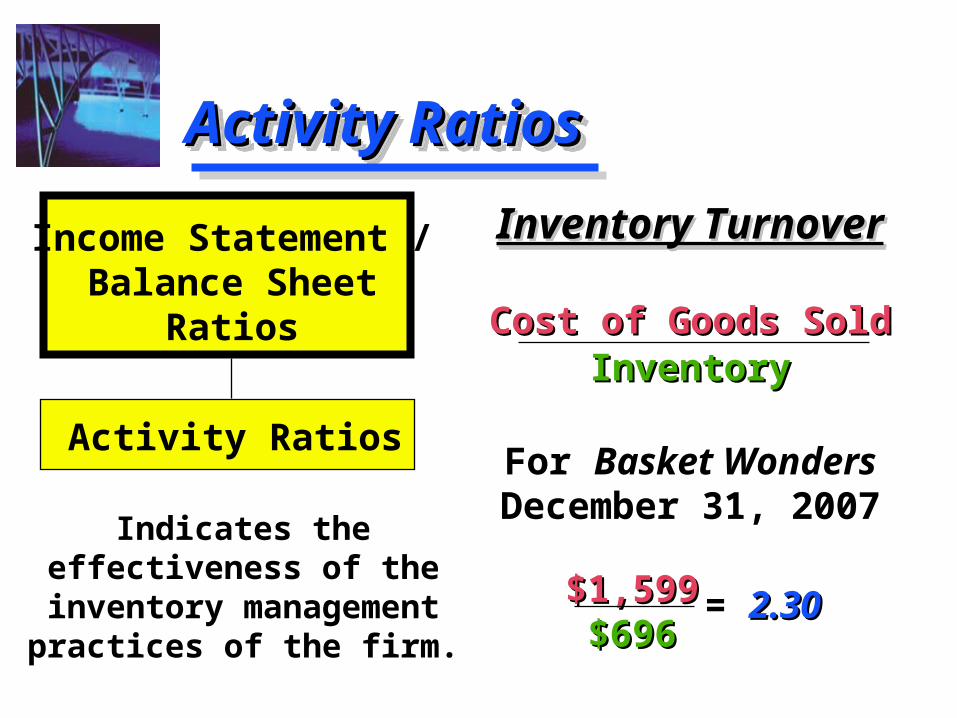

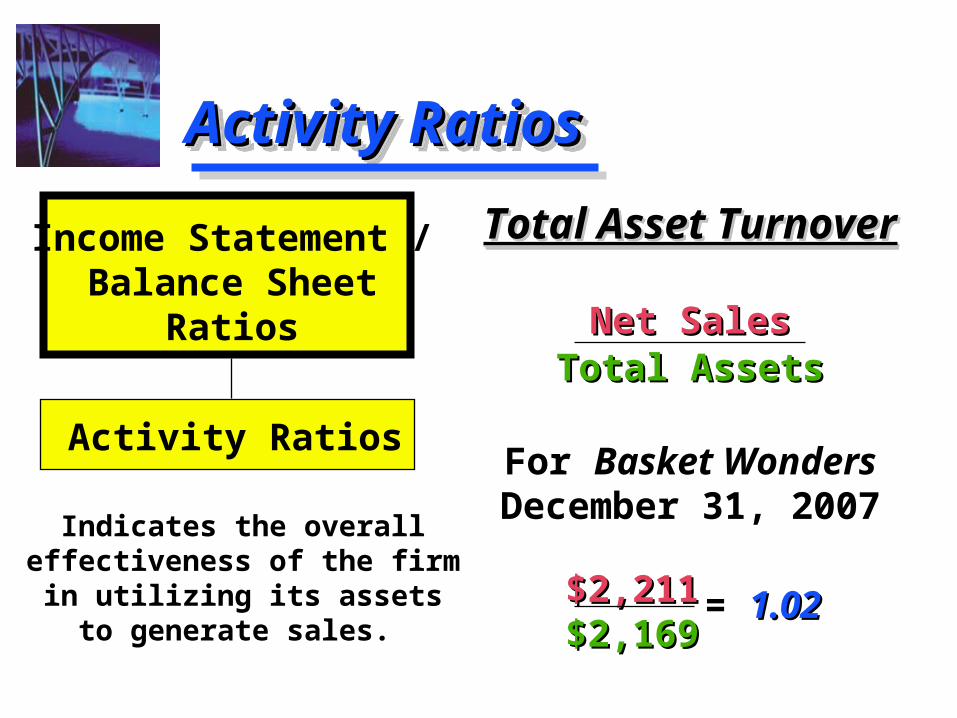

Activity RatiosActivity RatiosActivity RatiosActivity Ratios

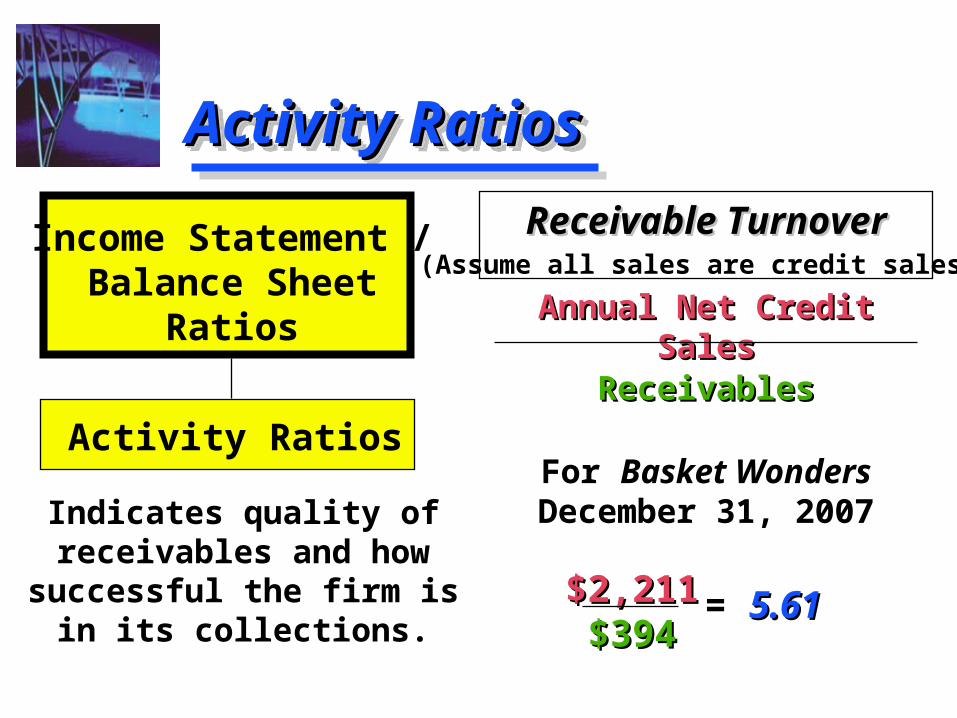

Receivable TurnoverReceivable Turnover

Annual Net Credit SalesAnnual Net Credit SalesReceivablesReceivables

For Basket Wonders December 31, 2007

Receivable TurnoverReceivable Turnover

Annual Net Credit SalesAnnual Net Credit SalesReceivablesReceivables

For Basket Wonders December 31, 2007Indicates quality of

receivables and how successful the firm is in

its collections.

Income Statement /Balance Sheet

Ratios

Activity Ratios

$2,211$2,211$394$394

= 5.615.61

(Assume all sales are credit sales.)

Activity RatiosActivity RatiosActivity RatiosActivity Ratios

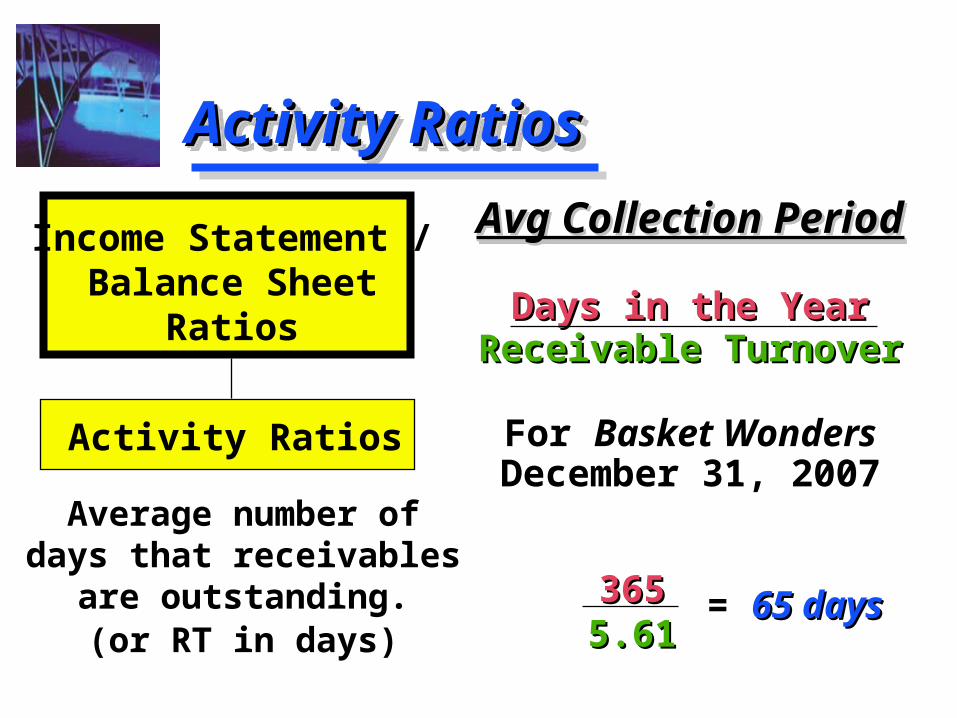

Avg Collection PeriodAvg Collection Period

Days in the YearDays in the YearReceivable TurnoverReceivable Turnover

For Basket Wonders December 31, 2007

Avg Collection PeriodAvg Collection Period

Days in the YearDays in the YearReceivable TurnoverReceivable Turnover

For Basket Wonders December 31, 2007

Average number of days that receivables are

outstanding.(or RT in days)

Income Statement /Balance Sheet

Ratios

Activity Ratios

3653655.615.61

= 65 days65 days

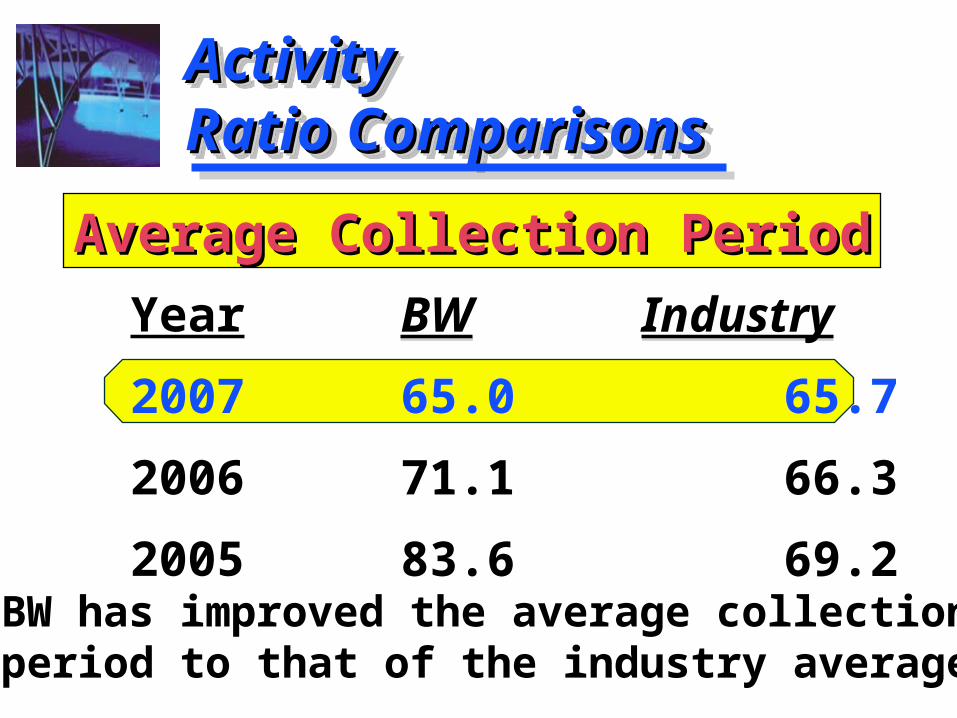

ActivityActivityRatio ComparisonsRatio ComparisonsActivityActivityRatio ComparisonsRatio Comparisons

BW Industry

65.0 65.7

71.1 66.3

83.6 69.2

BW Industry

65.0 65.7

71.1 66.3

83.6 69.2

Year

2007

2006

2005

Average Collection PeriodAverage Collection Period

BW has improved the average collection period to that of the industry average.

Activity RatiosActivity RatiosActivity RatiosActivity Ratios

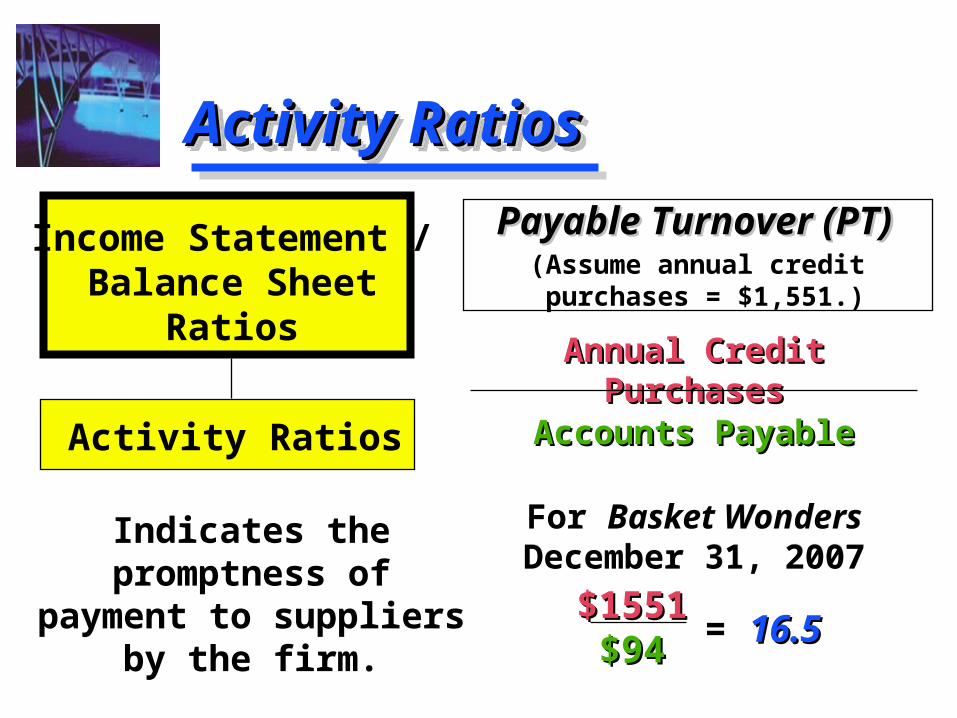

Payable Turnover (PT)Payable Turnover (PT)

Annual Credit PurchasesAnnual Credit PurchasesAccounts PayableAccounts Payable

For Basket Wonders December 31, 2007

Payable Turnover (PT)Payable Turnover (PT)

Annual Credit PurchasesAnnual Credit PurchasesAccounts PayableAccounts Payable

For Basket Wonders December 31, 2007

Indicates the promptness of payment to suppliers by the firm.

Income Statement /Balance Sheet

Ratios

Activity Ratios

$1551$1551$94$94 = 16.516.5

(Assume annual credit purchases = $1,551.)

Activity RatiosActivity RatiosActivity RatiosActivity Ratios

PT in DaysPT in Days

Days in the YearDays in the YearPayable TurnoverPayable Turnover

For Basket Wonders December 31, 2007

PT in DaysPT in Days

Days in the YearDays in the YearPayable TurnoverPayable Turnover

For Basket Wonders December 31, 2007

Average number of days that payables are

outstanding.

Income Statement /Balance Sheet

Ratios

Activity Ratios

36536516.516.5

= 22.1 days22.1 days

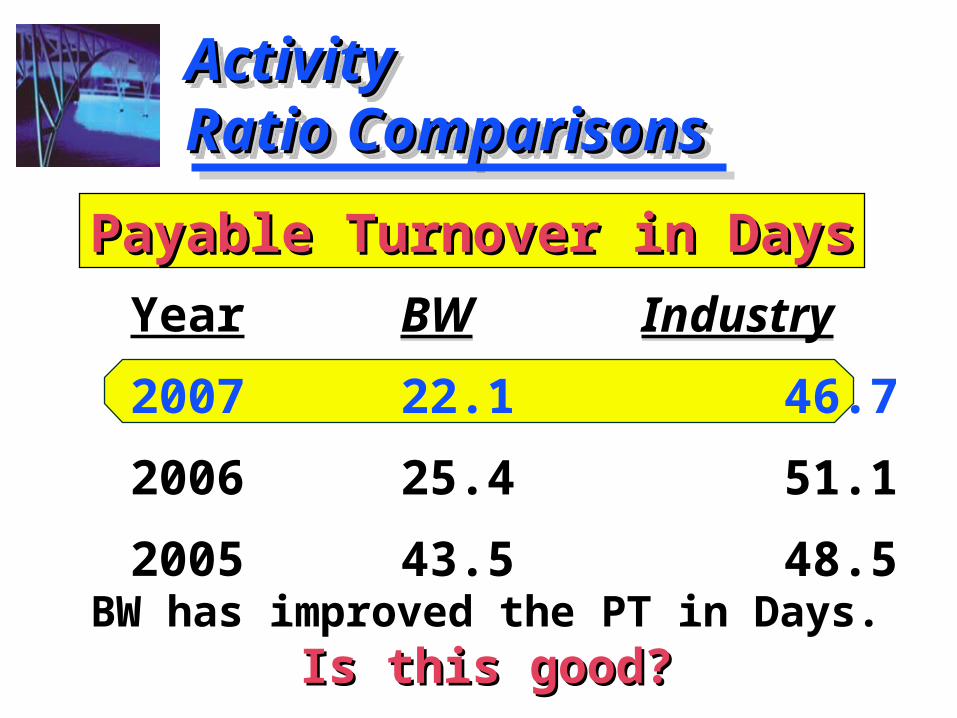

ActivityActivityRatio ComparisonsRatio ComparisonsActivityActivityRatio ComparisonsRatio Comparisons

BW Industry

22.1 46.7

25.4 51.1

43.5 48.5

BW Industry

22.1 46.7

25.4 51.1

43.5 48.5

Year

2007

2006

2005

Payable Turnover in DaysPayable Turnover in Days

BW has improved the PT in Days.Is this good?Is this good?

Activity RatiosActivity RatiosActivity RatiosActivity Ratios

Inventory TurnoverInventory Turnover

Cost of Goods SoldCost of Goods SoldInventoryInventory

For Basket Wonders December 31, 2007

Inventory TurnoverInventory Turnover

Cost of Goods SoldCost of Goods SoldInventoryInventory

For Basket Wonders December 31, 2007

Indicates the effectiveness of the

inventory management practices of the firm.

Income Statement /Balance Sheet

Ratios

Activity Ratios

$1,599$1,599$696$696

= 2.302.30

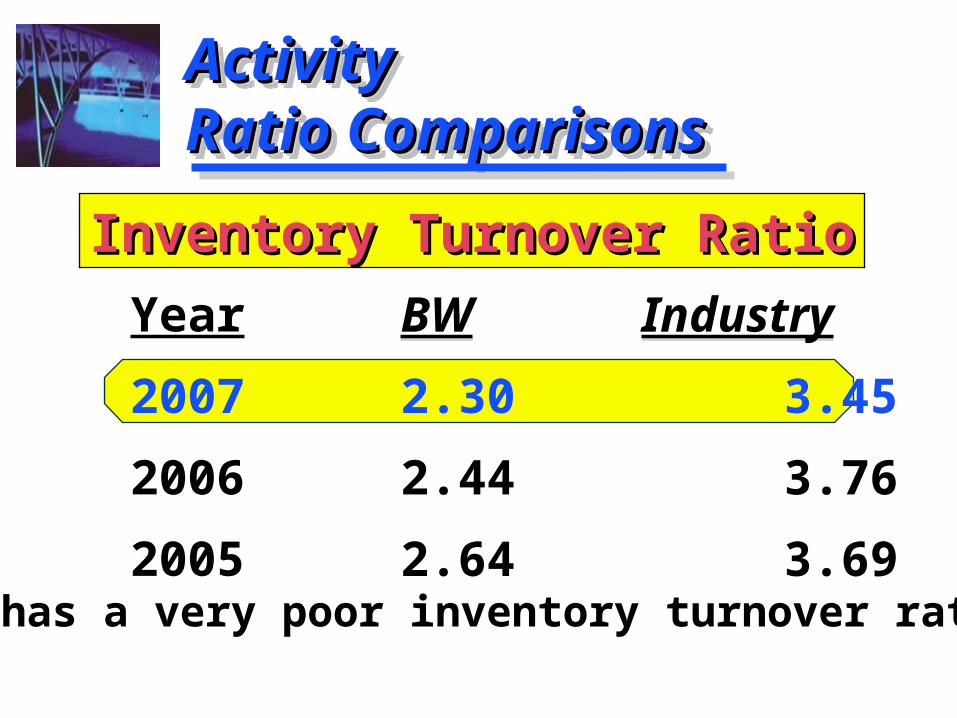

ActivityActivityRatio ComparisonsRatio ComparisonsActivityActivityRatio ComparisonsRatio Comparisons

BW Industry

2.30 3.45

2.44 3.76

2.64 3.69

BW Industry

2.30 3.45

2.44 3.76

2.64 3.69

Year

2007

2006

2005

Inventory Turnover RatioInventory Turnover Ratio

BW has a very poor inventory turnover ratio.

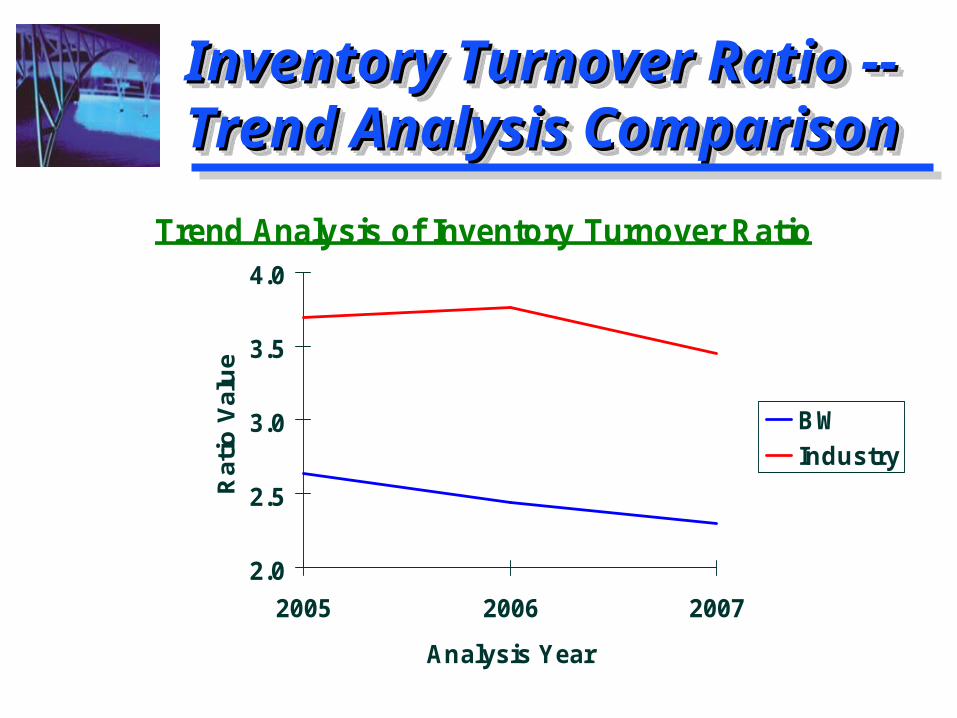

Inventory Turnover Ratio --Inventory Turnover Ratio --Trend Analysis ComparisonTrend Analysis ComparisonInventory Turnover Ratio --Inventory Turnover Ratio --Trend Analysis ComparisonTrend Analysis Comparison

Trend Analysis of Inventory Turnover Ratio

2.0

2.5

3.0

3.5

4.0

2005 2006 2007

Analysis Year

Rat

io V

alu

e

BW

Industry

Activity RatiosActivity RatiosActivity RatiosActivity Ratios

Total Asset TurnoverTotal Asset Turnover

Net SalesNet SalesTotal AssetsTotal Assets

For Basket Wonders December 31, 2007

Total Asset TurnoverTotal Asset Turnover

Net SalesNet SalesTotal AssetsTotal Assets

For Basket Wonders December 31, 2007

Indicates the overall effectiveness of the firm in utilizing its assets to

generate sales.

Income Statement /Balance Sheet

Ratios

Activity Ratios

$2,211$2,211$2,169$2,169

= 1.021.02

ActivityActivityRatio ComparisonsRatio ComparisonsActivityActivityRatio ComparisonsRatio Comparisons

BW Industry

1.02 1.17

1.03 1.14

1.01 1.13

BW Industry

1.02 1.17

1.03 1.14

1.01 1.13

Year

2007

2006

2005

Total Asset Turnover RatioTotal Asset Turnover Ratio

BW has a weak total asset turnover ratio.Why is this ratio considered weak?Why is this ratio considered weak?

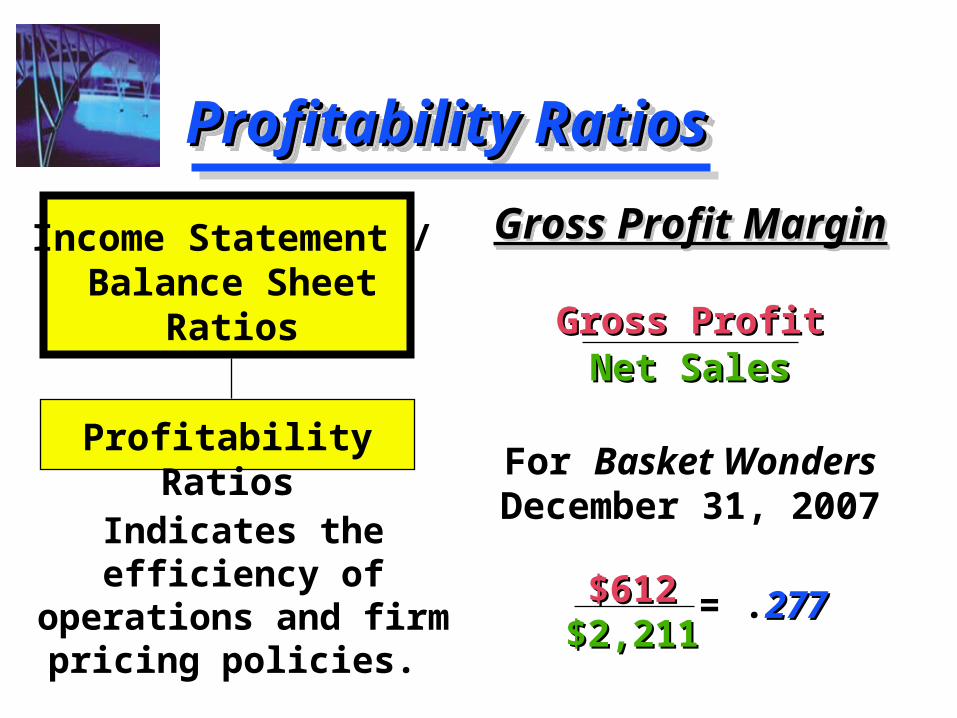

Profitability RatiosProfitability RatiosProfitability RatiosProfitability Ratios

Gross Profit MarginGross Profit Margin

Gross ProfitGross ProfitNet SalesNet Sales

For Basket Wonders December 31, 2007

Gross Profit MarginGross Profit Margin

Gross ProfitGross ProfitNet SalesNet Sales

For Basket Wonders December 31, 2007

Indicates the efficiency of operations and firm

pricing policies.

Income Statement /Balance Sheet

Ratios

Profitability Ratios

$612$612$2,211$2,211

= .277277

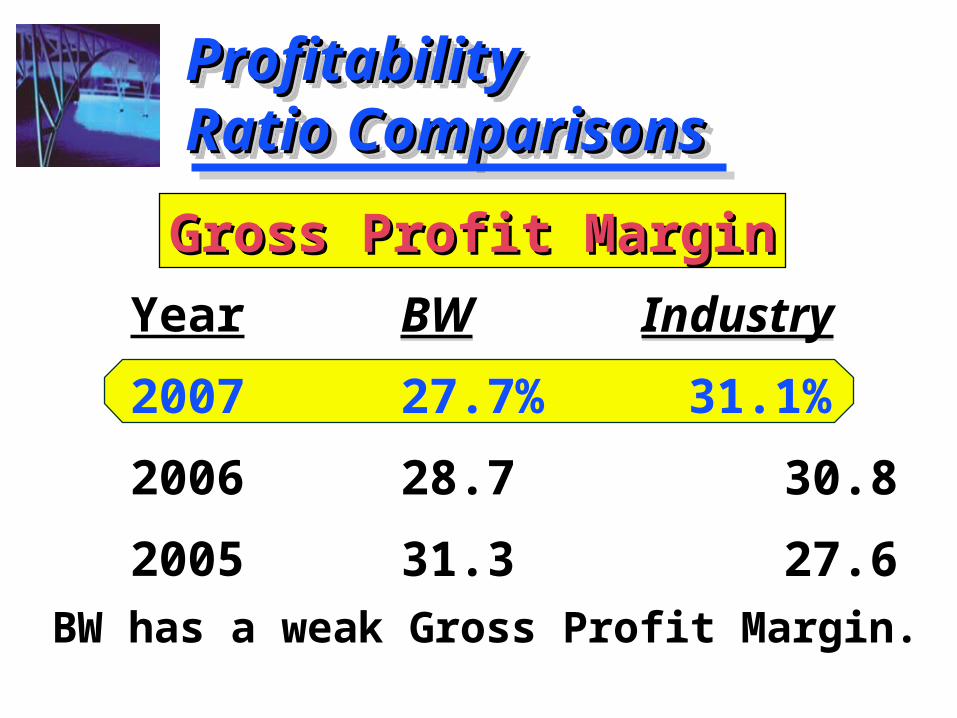

ProfitabilityProfitabilityRatio ComparisonsRatio ComparisonsProfitabilityProfitabilityRatio ComparisonsRatio Comparisons

BW Industry

27.7% 31.1%

28.7 30.8

31.3 27.6

BW Industry

27.7% 31.1%

28.7 30.8

31.3 27.6

Year

2007

2006

2005

Gross Profit MarginGross Profit Margin

BW has a weak Gross Profit Margin.

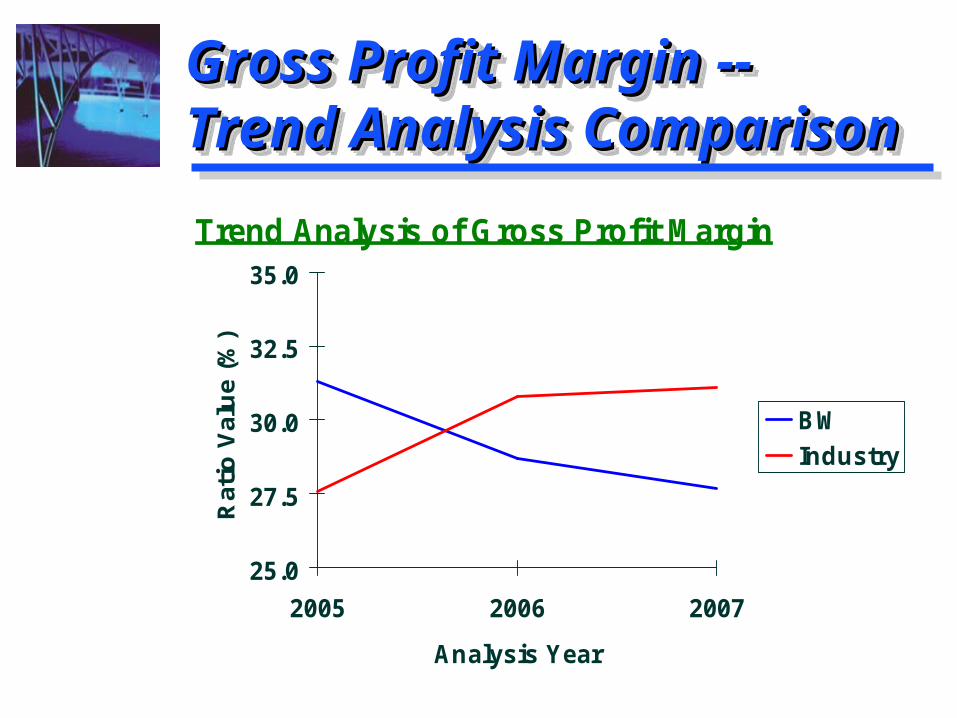

Gross Profit Margin --Gross Profit Margin --Trend Analysis ComparisonTrend Analysis ComparisonGross Profit Margin --Gross Profit Margin --Trend Analysis ComparisonTrend Analysis Comparison

Trend Analysis of Gross Profit Margin

25.0

27.5

30.0

32.5

35.0

2005 2006 2007

Analysis Year

Rat

io V

alu

e (%

)

BW

Industry

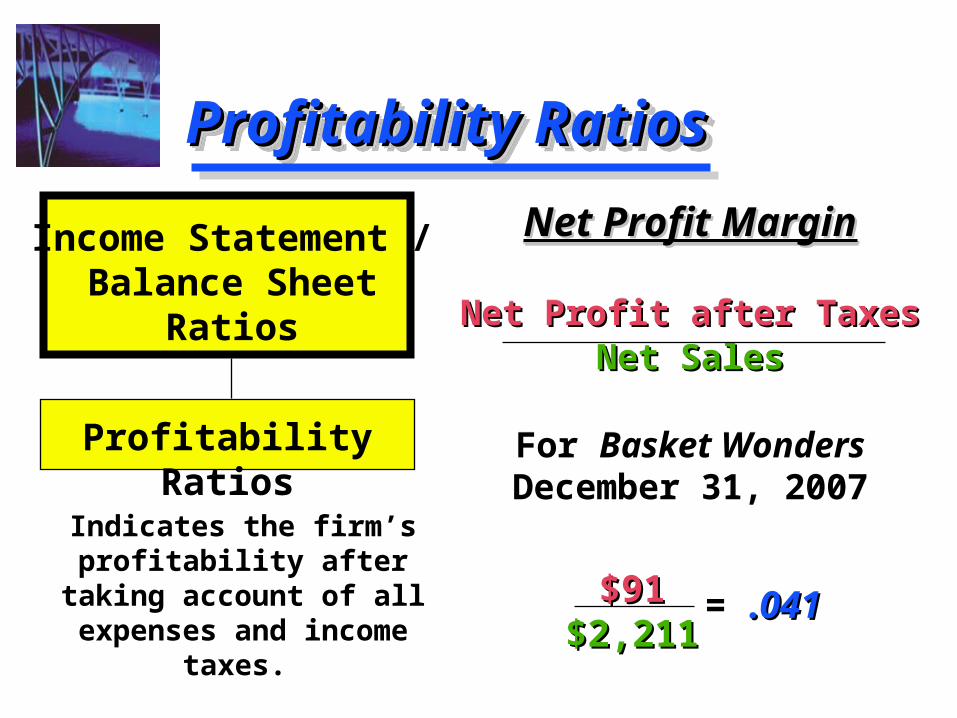

Profitability RatiosProfitability RatiosProfitability RatiosProfitability Ratios

Net Profit MarginNet Profit Margin

Net Profit after TaxesNet Profit after TaxesNet SalesNet Sales

For Basket Wonders December 31, 2007

Net Profit MarginNet Profit Margin

Net Profit after TaxesNet Profit after TaxesNet SalesNet Sales

For Basket Wonders December 31, 2007

Indicates the firm’s profitability after taking account of all expenses

and income taxes.

Income Statement /Balance Sheet

Ratios

Profitability Ratios

$91$91$2,211$2,211

= .041.041

ProfitabilityProfitability Ratio ComparisonsRatio ComparisonsProfitabilityProfitability Ratio ComparisonsRatio Comparisons

BW Industry

4.1% 8.2%

4.9 8.1

9.0 7.6

BW Industry

4.1% 8.2%

4.9 8.1

9.0 7.6

Year

2007

2006

2005

Net Profit MarginNet Profit Margin

BW has a poor Net Profit Margin.

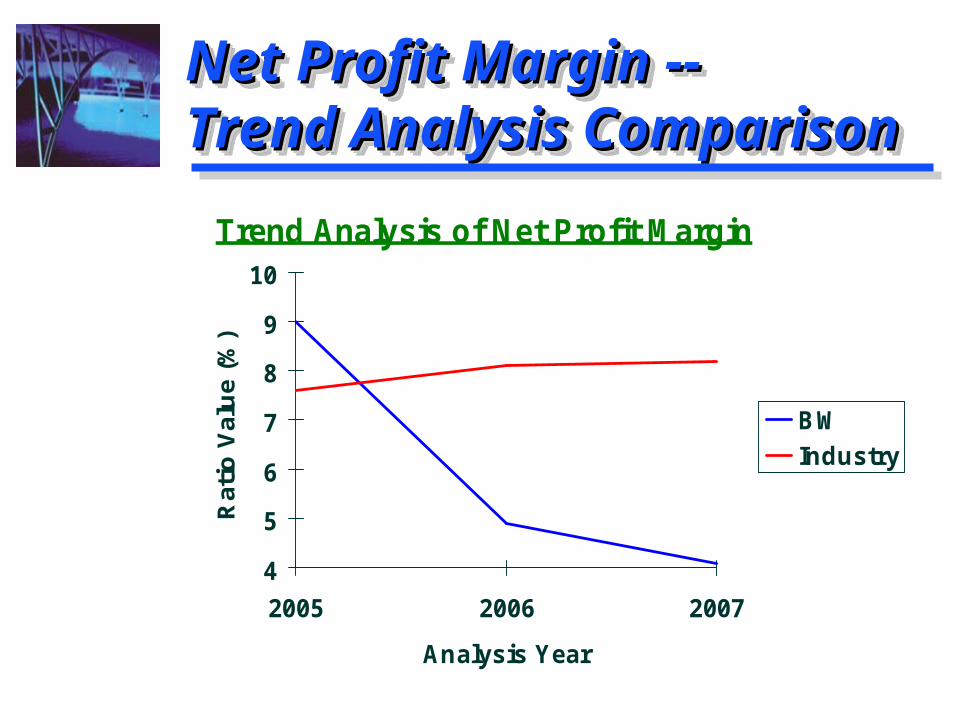

Net Profit Margin --Net Profit Margin --Trend Analysis ComparisonTrend Analysis ComparisonNet Profit Margin --Net Profit Margin --Trend Analysis ComparisonTrend Analysis Comparison

Trend Analysis of Net Profit Margin

4

5

6

7

8

9

10

2005 2006 2007

Analysis Year

Rat

io V

alu

e (%

)

BW

Industry

Profitability RatiosProfitability RatiosProfitability RatiosProfitability Ratios

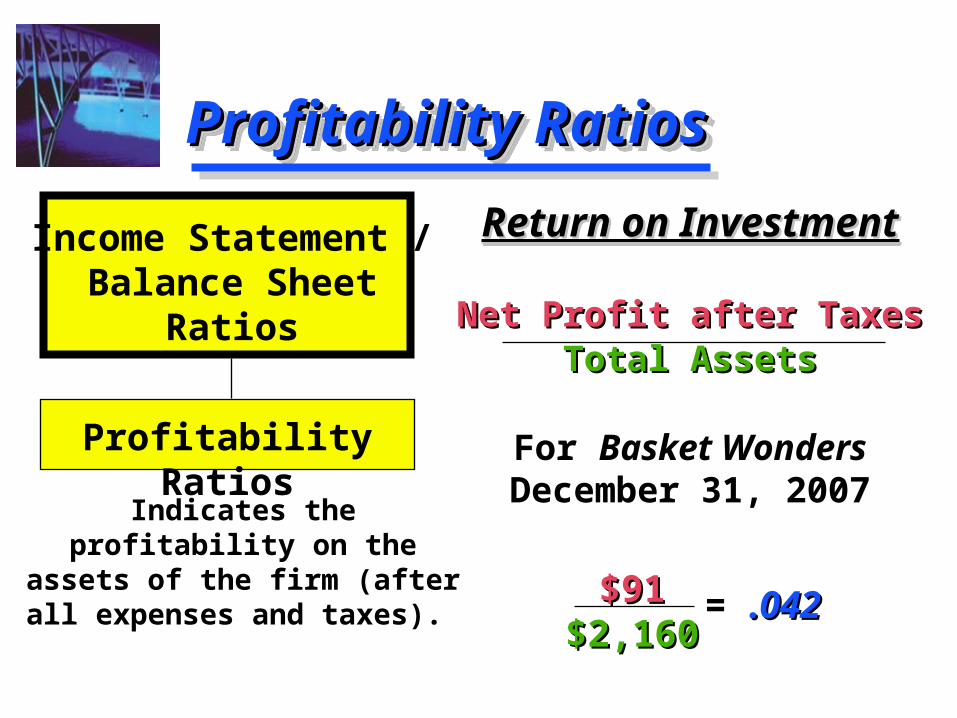

Return on InvestmentReturn on Investment

Net Profit after TaxesNet Profit after TaxesTotal AssetsTotal Assets

For Basket Wonders December 31, 2007

Return on InvestmentReturn on Investment

Net Profit after TaxesNet Profit after TaxesTotal AssetsTotal Assets

For Basket Wonders December 31, 2007Indicates the

profitability on the assets of the firm (after all expenses and taxes).

Income Statement /Balance Sheet

Ratios

Profitability Ratios

$91$91$2,160$2,160

= .042.042

ProfitabilityProfitability Ratio ComparisonsRatio ComparisonsProfitabilityProfitability Ratio ComparisonsRatio Comparisons

BW Industry

4.2% 9.8%

5.0 9.1

9.1 10.8

BW Industry

4.2% 9.8%

5.0 9.1

9.1 10.8

Year

2007

2006

2005

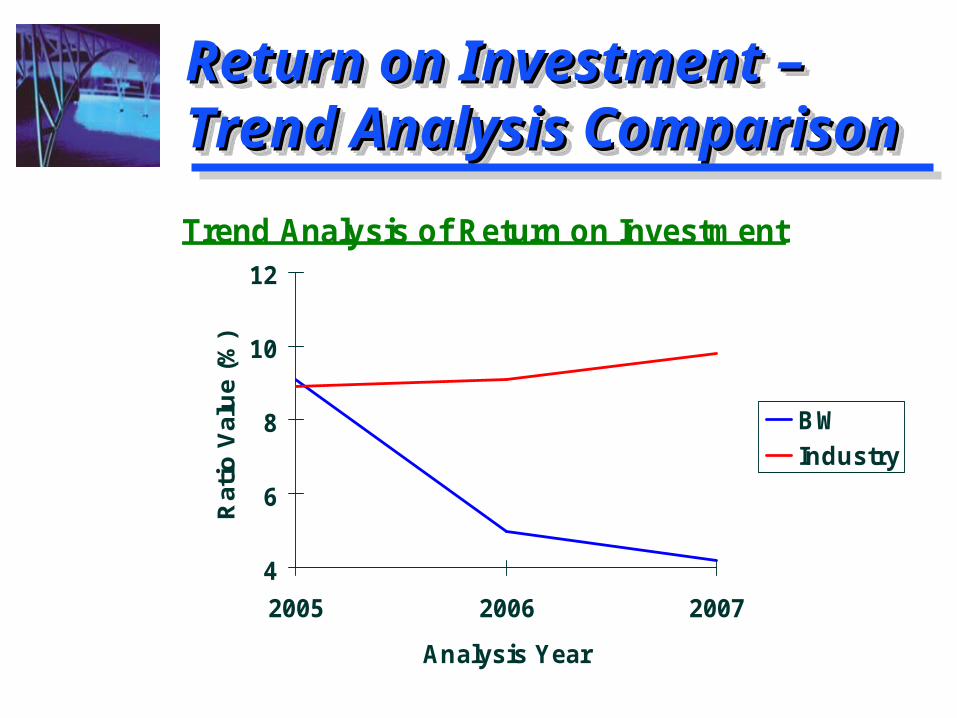

Return on InvestmentReturn on Investment

BW has a poor Return on Investment.

Return on Investment –Return on Investment –Trend Analysis ComparisonTrend Analysis ComparisonReturn on Investment –Return on Investment –Trend Analysis ComparisonTrend Analysis Comparison

Trend Analysis of Return on Investment

4

6

8

10

12

2005 2006 2007

Analysis Year

Rat

io V

alu

e (%

)

BW

Industry

Profitability RatiosProfitability RatiosProfitability RatiosProfitability Ratios

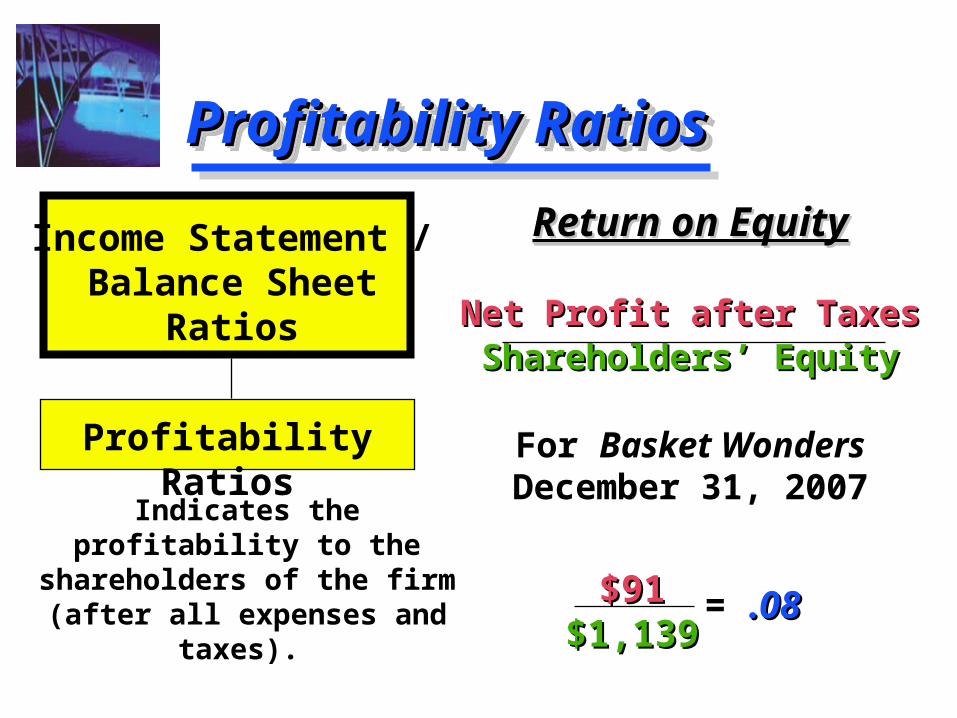

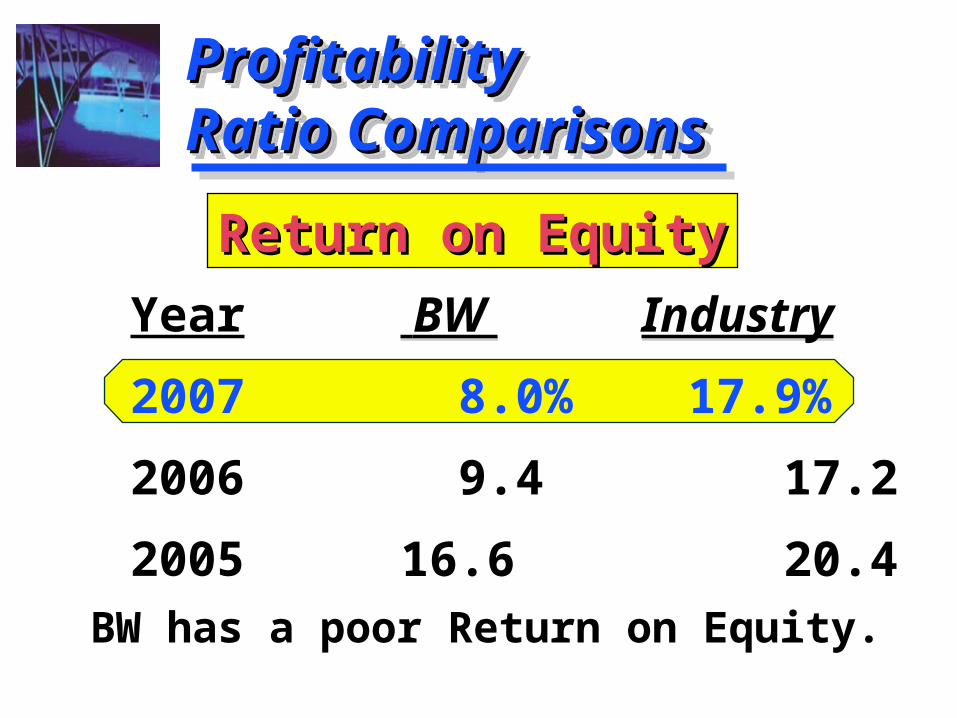

Return on EquityReturn on Equity

Net Profit after TaxesNet Profit after TaxesShareholders’ EquityShareholders’ Equity

For Basket Wonders December 31, 2007

Return on EquityReturn on Equity

Net Profit after TaxesNet Profit after TaxesShareholders’ EquityShareholders’ Equity

For Basket Wonders December 31, 2007Indicates the profitability

to the shareholders of the firm (after all

expenses and taxes).

Income Statement /Balance Sheet

Ratios

Profitability Ratios

$91$91$1,139$1,139

= .08.08

ProfitabilityProfitability Ratio ComparisonsRatio ComparisonsProfitabilityProfitability Ratio ComparisonsRatio Comparisons

BW Industry

8.0% 17.9%

9.4 17.2

16.6 20.4

BW Industry

8.0% 17.9%

9.4 17.2

16.6 20.4

Year

2007

2006

2005

Return on EquityReturn on Equity

BW has a poor Return on Equity.

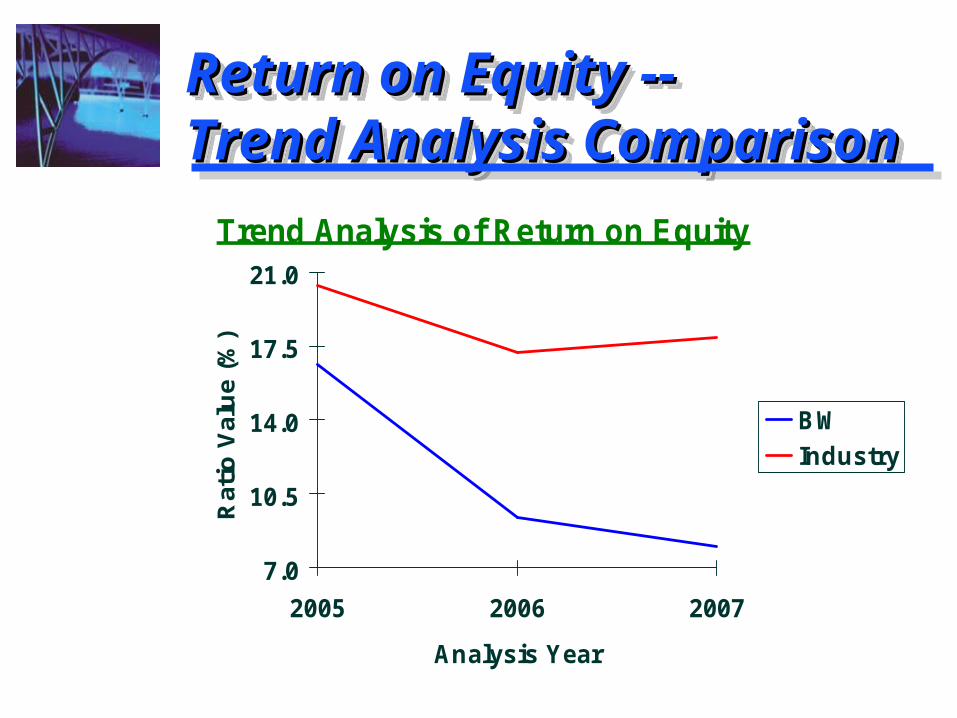

Return on Equity --Return on Equity --Trend Analysis ComparisonTrend Analysis ComparisonReturn on Equity --Return on Equity --Trend Analysis ComparisonTrend Analysis Comparison

Trend Analysis of Return on Equity

7.0

10.5

14.0

17.5

21.0

2005 2006 2007

Analysis Year

Rat

io V

alu

e (%

)

BW

Industry

Summary of the Profitability Summary of the Profitability Trend AnalysesTrend AnalysesSummary of the Profitability Summary of the Profitability Trend AnalysesTrend Analyses

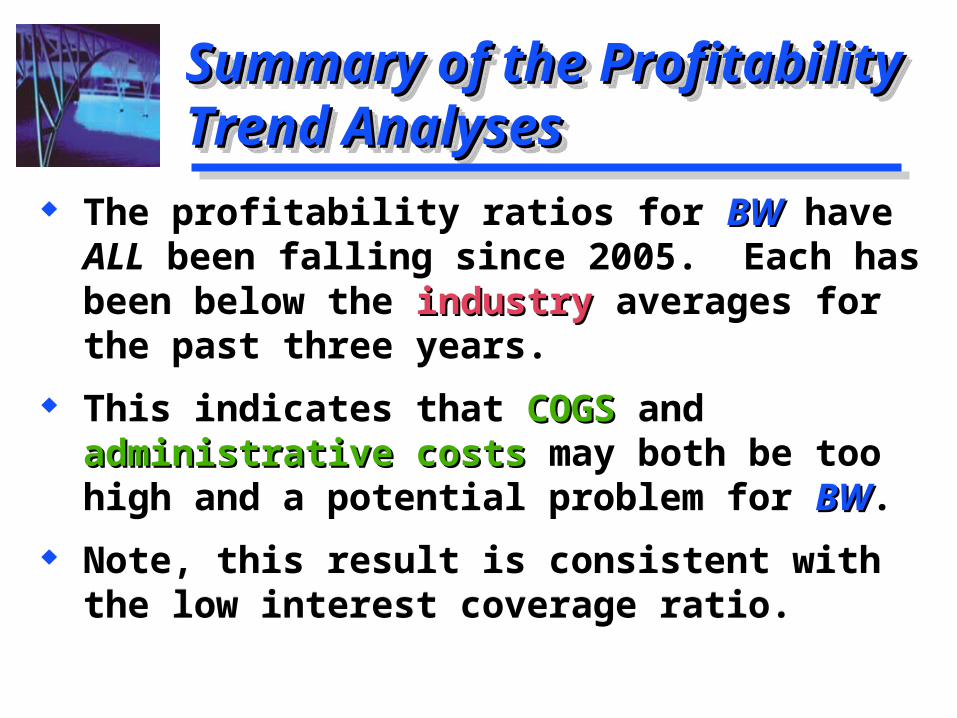

The profitability ratios for BWBW have ALL been falling since 2005. Each has been below the industryindustry averages for the past three years.

This indicates that COGSCOGS and administrative costsadministrative costs may both be too high and a potential problem for BWBW.

Note, this result is consistent with the low interest coverage ratio.

The profitability ratios for BWBW have ALL been falling since 2005. Each has been below the industryindustry averages for the past three years.

This indicates that COGSCOGS and administrative costsadministrative costs may both be too high and a potential problem for BWBW.

Note, this result is consistent with the low interest coverage ratio.

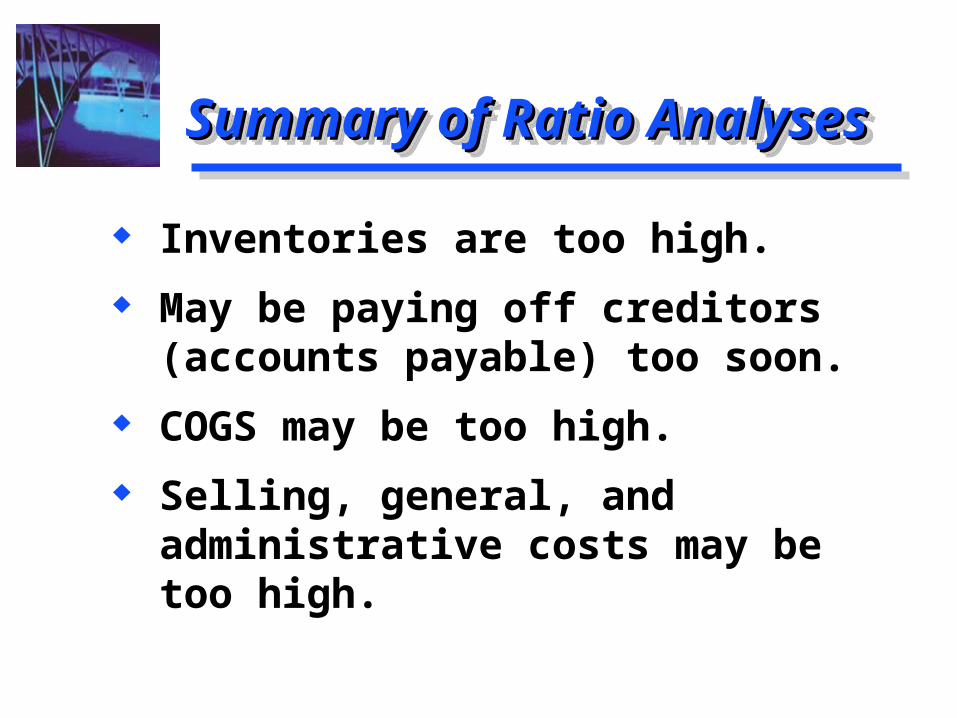

Summary of Ratio AnalysesSummary of Ratio AnalysesSummary of Ratio AnalysesSummary of Ratio Analyses

Inventories are too high.

May be paying off creditors (accounts payable) too soon.

COGS may be too high.

Selling, general, and administrative costs may be too high.

Inventories are too high.

May be paying off creditors (accounts payable) too soon.

COGS may be too high.

Selling, general, and administrative costs may be too high.

Common-size AnalysisCommon-size AnalysisCommon-size AnalysisCommon-size Analysis

An analysis of percentage financial statements where all

balance sheet items are divided by total assets and all income statement items are divided by

net sales or revenues.

An analysis of percentage financial statements where all

balance sheet items are divided by total assets and all income statement items are divided by

net sales or revenues.

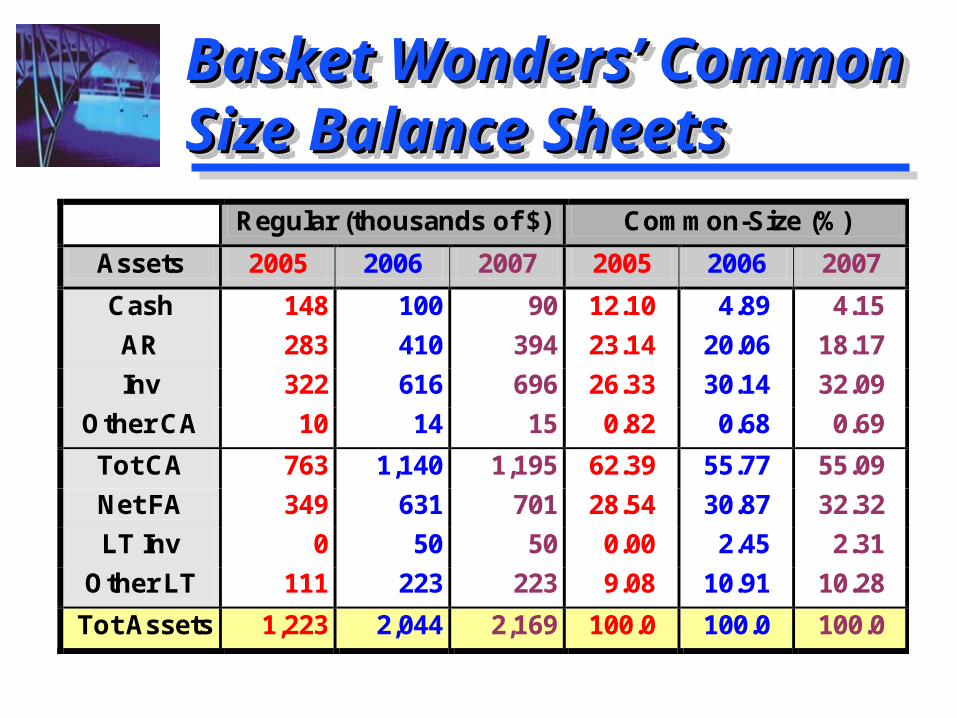

Basket Wonders’ Common Basket Wonders’ Common Size Balance SheetsSize Balance SheetsBasket Wonders’ Common Basket Wonders’ Common Size Balance SheetsSize Balance Sheets

Regular (thousands of $) Common-Size (%)

Assets 2005 2006 2007 2005 2006 2007

Cash 148 100 90 12.10 4.89 4.15

AR 283 410 394 23.14 20.06 18.17

Inv 322 616 696 26.33 30.14 32.09

Other CA 10 14 15 0.82 0.68 0.69

Tot CA 763 1,140 1,195 62.39 55.77 55.09

Net FA 349 631 701 28.54 30.87 32.32

LT Inv 0 50 50 0.00 2.45 2.31

Other LT 111 223 223 9.08 10.91 10.28

Tot Assets 1,223 2,044 2,169 100.0 100.0 100.0

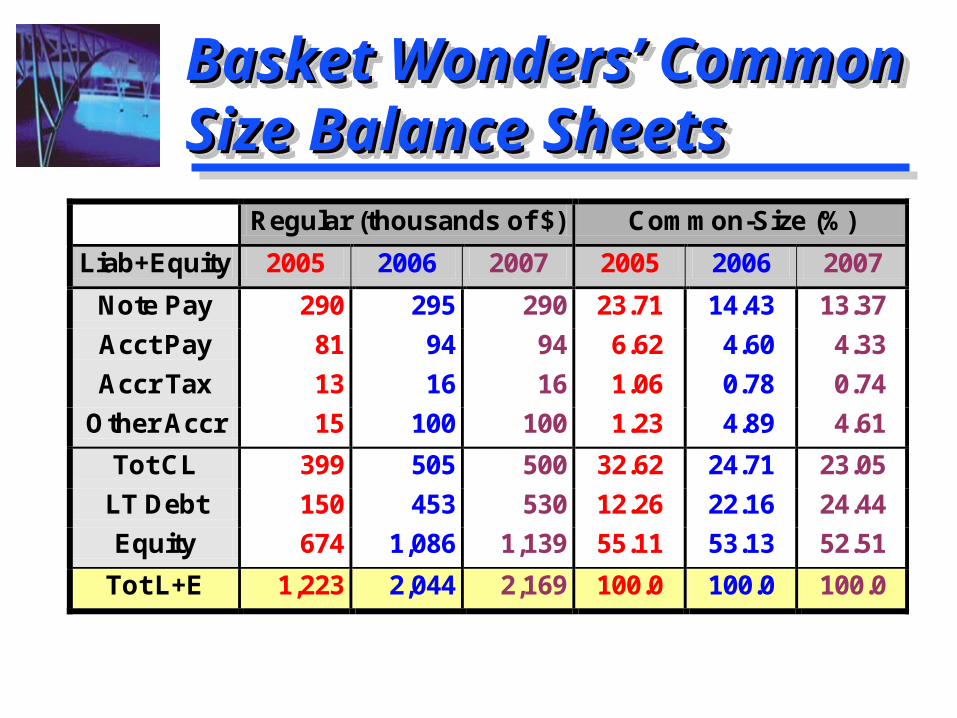

Basket Wonders’ Common Basket Wonders’ Common Size Balance SheetsSize Balance SheetsBasket Wonders’ Common Basket Wonders’ Common Size Balance SheetsSize Balance Sheets

Regular (thousands of $) Common-Size (%)

Liab+Equity 2005 2006 2007 2005 2006 2007

Note Pay 290 295 290 23.71 14.43 13.37

Acct Pay 81 94 94 6.62 4.60 4.33

Accr Tax 13 16 16 1.06 0.78 0.74

Other Accr 15 100 100 1.23 4.89 4.61

Tot CL 399 505 500 32.62 24.71 23.05

LT Debt 150 453 530 12.26 22.16 24.44

Equity 674 1,086 1,139 55.11 53.13 52.51

Tot L+E 1,223 2,044 2,169 100.0 100.0 100.0

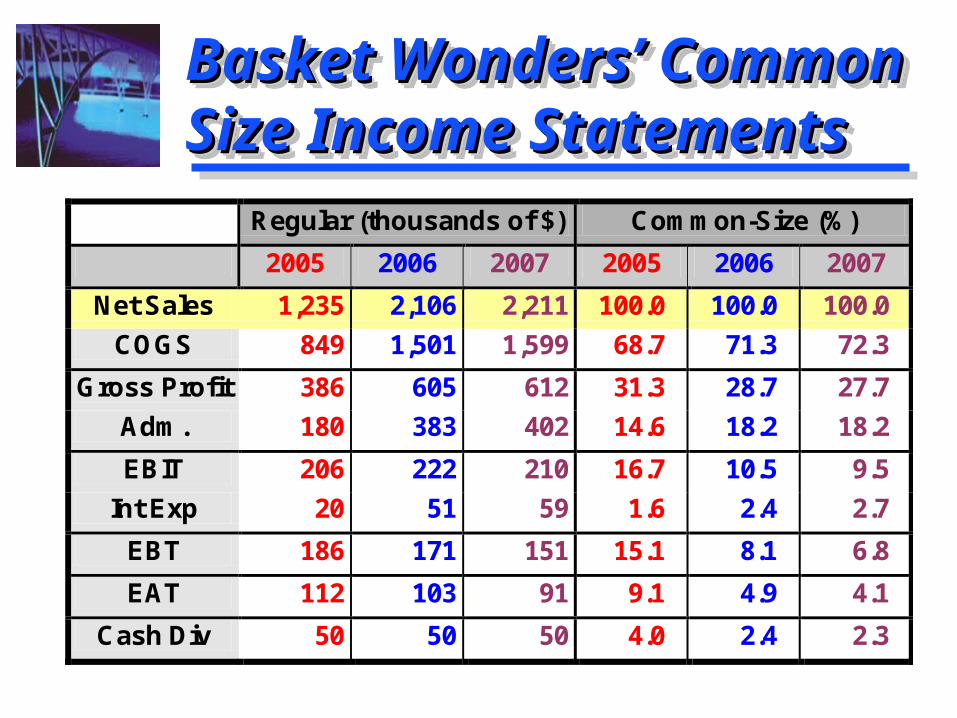

Basket Wonders’ Common Basket Wonders’ Common Size Income StatementsSize Income StatementsBasket Wonders’ Common Basket Wonders’ Common Size Income StatementsSize Income Statements

Regular (thousands of $) Common-Size (%)

2005 2006 2007 2005 2006 2007

Net Sales 1,235 2,106 2,211 100.0 100.0 100.0

COGS 849 1,501 1,599 68.7 71.3 72.3

Gross Profit 386 605 612 31.3 28.7 27.7

Adm. 180 383 402 14.6 18.2 18.2

EBIT 206 222 210 16.7 10.5 9.5

Int Exp 20 51 59 1.6 2.4 2.7

EBT 186 171 151 15.1 8.1 6.8

EAT 112 103 91 9.1 4.9 4.1

Cash Div 50 50 50 4.0 2.4 2.3

Index AnalysesIndex AnalysesIndex AnalysesIndex Analyses

An analysis of percentage financial statements where all balance sheet or income statement figures for a

base year equal 100.0 (percent) and subsequent financial statement

items are expressed as percentages of their values in the base year.

An analysis of percentage financial statements where all balance sheet or income statement figures for a

base year equal 100.0 (percent) and subsequent financial statement

items are expressed as percentages of their values in the base year.

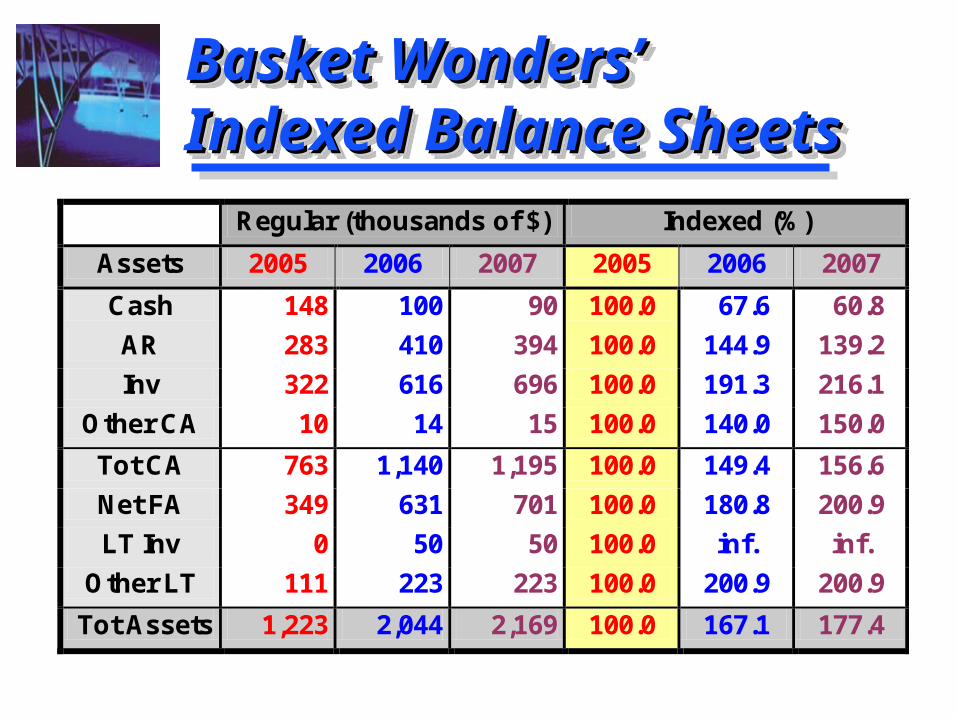

Basket Wonders’ Basket Wonders’ Indexed Balance SheetsIndexed Balance SheetsBasket Wonders’ Basket Wonders’ Indexed Balance SheetsIndexed Balance Sheets

Regular (thousands of $) Indexed (%)

Assets 2005 2006 2007 2005 2006 2007

Cash 148 100 90 100.0 67.6 60.8

AR 283 410 394 100.0 144.9 139.2

Inv 322 616 696 100.0 191.3 216.1

Other CA 10 14 15 100.0 140.0 150.0

Tot CA 763 1,140 1,195 100.0 149.4 156.6

Net FA 349 631 701 100.0 180.8 200.9

LT Inv 0 50 50 100.0 inf. inf.

Other LT 111 223 223 100.0 200.9 200.9

Tot Assets 1,223 2,044 2,169 100.0 167.1 177.4

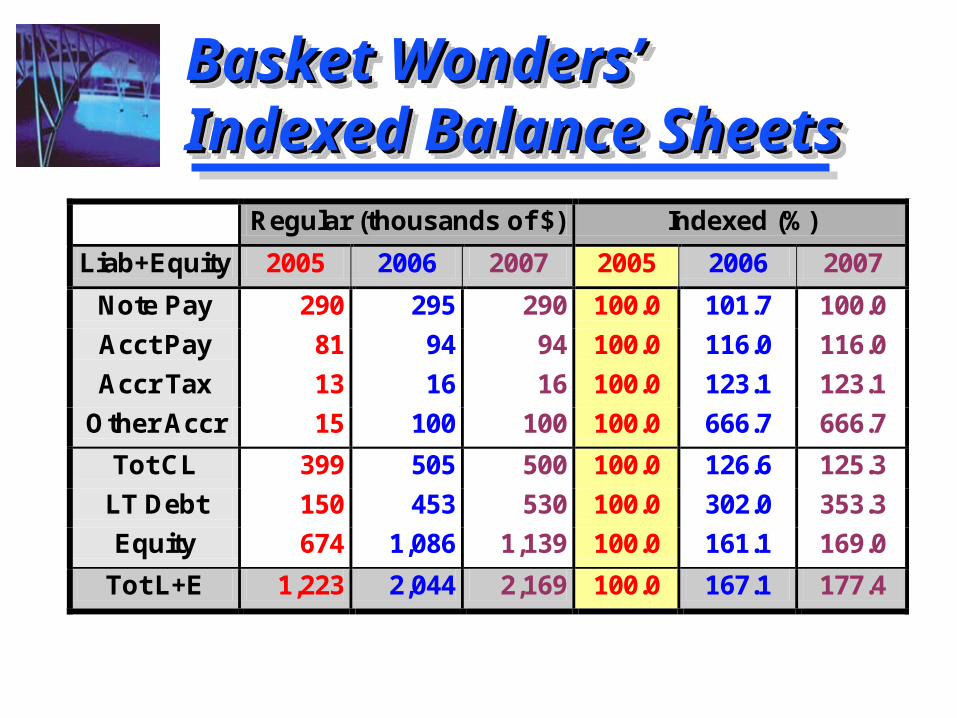

Basket Wonders’ Basket Wonders’ Indexed Balance SheetsIndexed Balance SheetsBasket Wonders’ Basket Wonders’ Indexed Balance SheetsIndexed Balance Sheets

Regular (thousands of $) Indexed (%)

Liab+Equity 2005 2006 2007 2005 2006 2007

Note Pay 290 295 290 100.0 101.7 100.0

Acct Pay 81 94 94 100.0 116.0 116.0

Accr Tax 13 16 16 100.0 123.1 123.1

Other Accr 15 100 100 100.0 666.7 666.7

Tot CL 399 505 500 100.0 126.6 125.3

LT Debt 150 453 530 100.0 302.0 353.3

Equity 674 1,086 1,139 100.0 161.1 169.0

Tot L+E 1,223 2,044 2,169 100.0 167.1 177.4

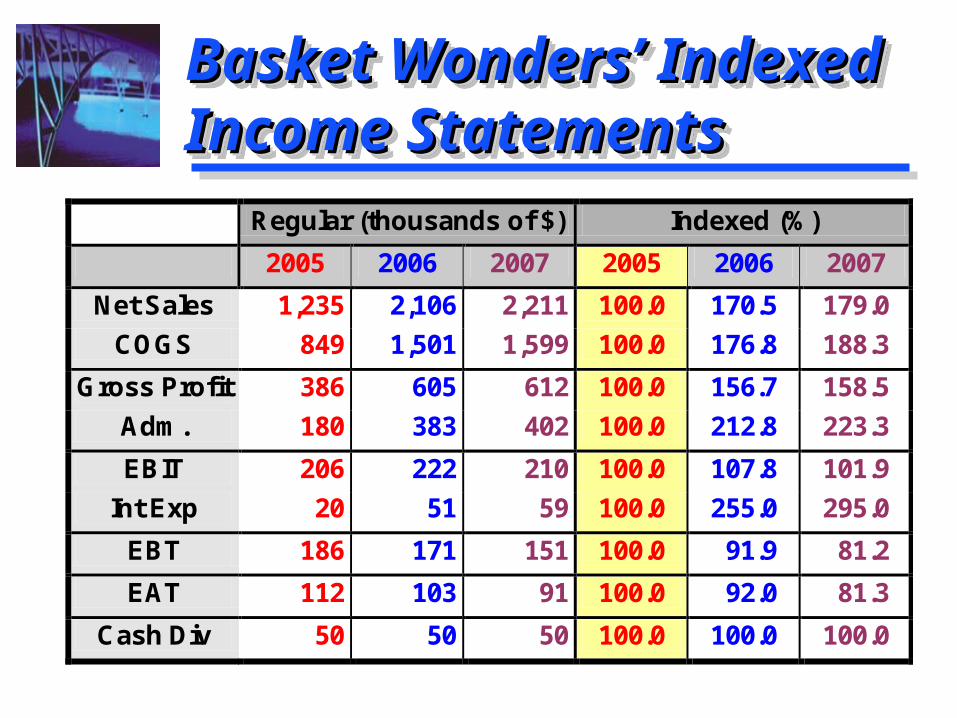

Basket Wonders’ Indexed Basket Wonders’ Indexed Income StatementsIncome StatementsBasket Wonders’ Indexed Basket Wonders’ Indexed Income StatementsIncome Statements

Regular (thousands of $) Indexed (%)

2005 2006 2007 2005 2006 2007

Net Sales 1,235 2,106 2,211 100.0 170.5 179.0

COGS 849 1,501 1,599 100.0 176.8 188.3

Gross Profit 386 605 612 100.0 156.7 158.5

Adm. 180 383 402 100.0 212.8 223.3

EBIT 206 222 210 100.0 107.8 101.9

Int Exp 20 51 59 100.0 255.0 295.0

EBT 186 171 151 100.0 91.9 81.2

EAT 112 103 91 100.0 92.0 81.3

Cash Div 50 50 50 100.0 100.0 100.0

Funds Analysis, Cash-Flow Funds Analysis, Cash-Flow Analysis, and Financial PlanningAnalysis, and Financial PlanningFunds Analysis, Cash-Flow Funds Analysis, Cash-Flow Analysis, and Financial PlanningAnalysis, and Financial Planning

Flow of Funds (Sources and Uses) Statement

Accounting Statement of Cash Flows

Cash-Flow Forecasting

Range of Cash-Flow Estimates

Forecasting Financial Statements

Flow of Funds (Sources and Uses) Statement

Accounting Statement of Cash Flows

Cash-Flow Forecasting

Range of Cash-Flow Estimates

Forecasting Financial Statements

Flow of Funds StatementFlow of Funds StatementFlow of Funds StatementFlow of Funds Statement

Has been replaced by the cash flow cash flow statementstatement (1989) in U.S. audited annual

reports.

Has been replaced by the cash flow cash flow statementstatement (1989) in U.S. audited annual

reports.

A summary of a firm’s changes in financial position from one period to

another; it is also called a sources and uses of funds statement or a statement

of changes in financial position.

A summary of a firm’s changes in financial position from one period to

another; it is also called a sources and uses of funds statement or a statement

of changes in financial position.

Why Examine the Flow Why Examine the Flow of Funds Statementof Funds StatementWhy Examine the Flow Why Examine the Flow of Funds Statementof Funds Statement

QUESTION?QUESTION?

Why should we bother to understand a Flow of Funds Statement that is no longer required to appear in U.S. audited annual reports?

QUESTION?QUESTION?

Why should we bother to understand a Flow of Funds Statement that is no longer required to appear in U.S. audited annual reports?

Why Examine the Flow Why Examine the Flow of Funds Statementof Funds StatementWhy Examine the Flow Why Examine the Flow of Funds Statementof Funds Statement

Includes important noncash transactions while the cash flow statement does not.

Is easy to prepare and often preferred by managers for analysis purposes over the more complex cash flow statement.

Helps you to better understand the cash flow statement, especially if it is prepared under the “indirect method.”

Includes important noncash transactions while the cash flow statement does not.

Is easy to prepare and often preferred by managers for analysis purposes over the more complex cash flow statement.

Helps you to better understand the cash flow statement, especially if it is prepared under the “indirect method.”

The Flow of Funds Statement:The Flow of Funds Statement:

Flow of Funds StatementFlow of Funds StatementFlow of Funds StatementFlow of Funds Statement

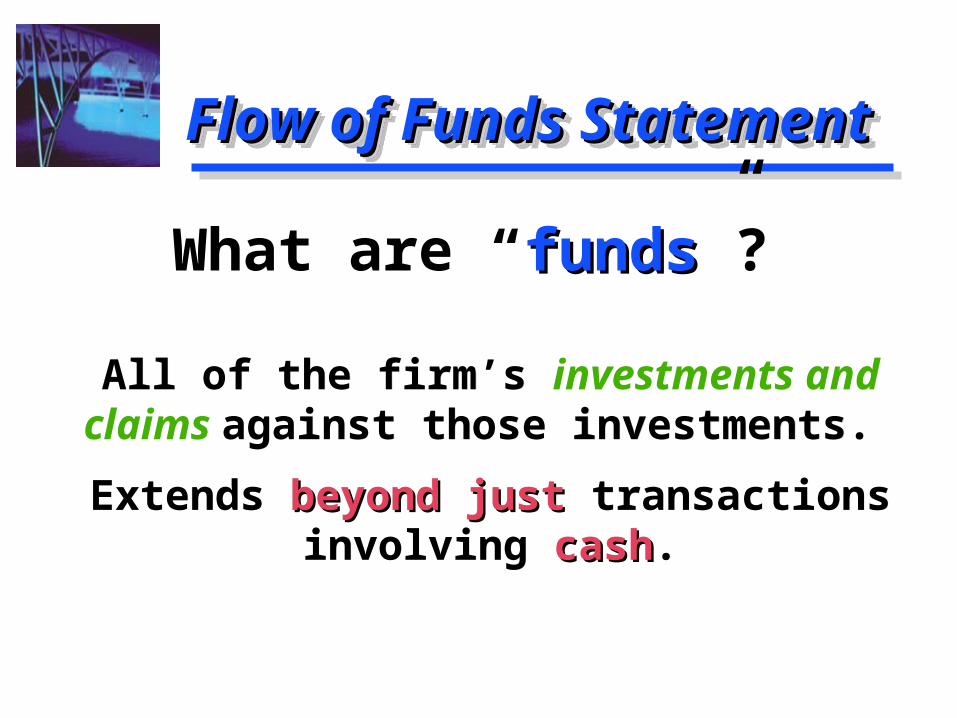

All of the firm’s investments and claims against those investments.

Extends beyond just beyond just transactions involving cashcash.

All of the firm’s investments and claims against those investments.

Extends beyond just beyond just transactions involving cashcash.

What are “fundsfunds”?

Sources and Sources and Uses StatementUses StatementSources and Sources and Uses StatementUses Statement

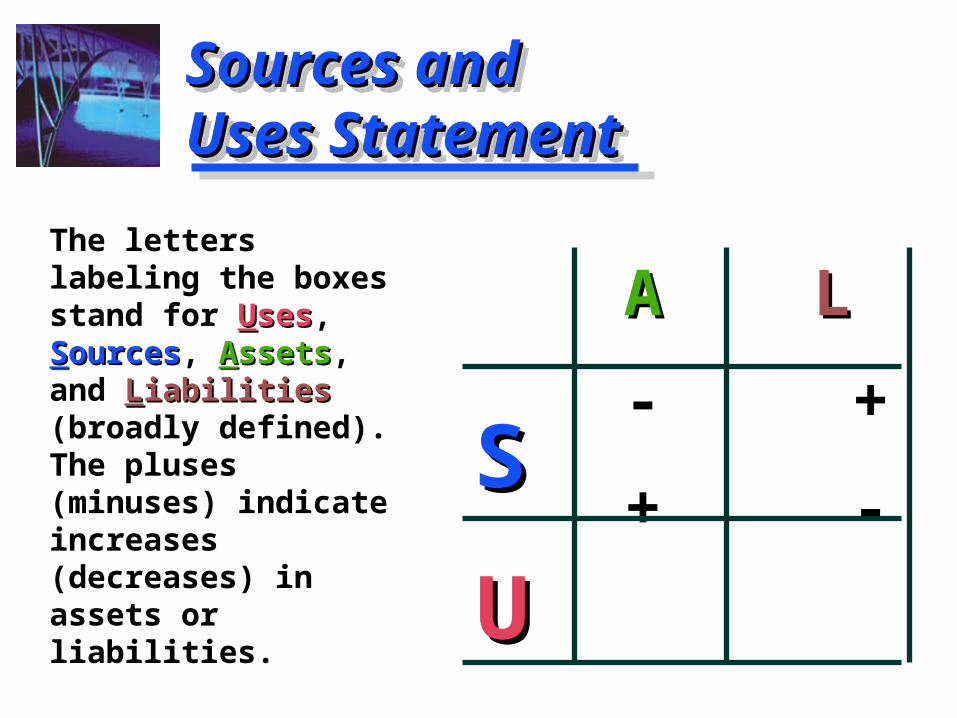

The letters labeling the boxes stand for UUsesses, SSourcesources, AAssetsssets, and LLiabilitiesiabilities (broadly defined). The pluses (minuses) indicate increases (decreases) in assets or liabilities.

The letters labeling the boxes stand for UUsesses, SSourcesources, AAssetsssets, and LLiabilitiesiabilities (broadly defined). The pluses (minuses) indicate increases (decreases) in assets or liabilities.

AA LL

- +

+ -

SS

UU

BW’s Determination BW’s Determination of Sources and Usesof Sources and UsesBW’s Determination BW’s Determination of Sources and Usesof Sources and Uses

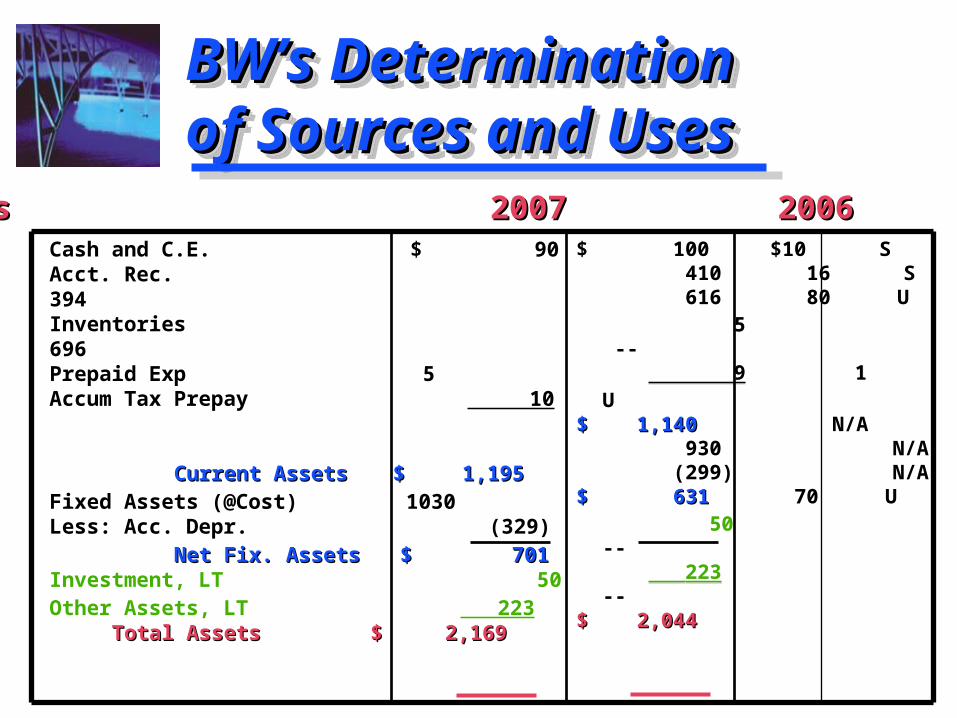

$ 100 - S 410 - S 616 + U 5 -- 9 + U$ 1,140$ 1,140 N/A 930 N/A (299) N/A$ 631$ 631 + U 50 -- 223 --$ 2,044$ 2,044

$ 100 - S 410 - S 616 + U 5 -- 9 + U$ 1,140$ 1,140 N/A 930 N/A (299) N/A$ 631$ 631 + U 50 -- 223 --$ 2,044$ 2,044

Cash and C.E. $ 90 Acct. Rec. 394 Inventories 696 Prepaid Exp 5 Accum Tax Prepay 10 Current AssetsCurrent Assets $ $ 1,195 1,195 Fixed Assets (@Cost) 1030 Less: Acc. Depr. (329) Net Fix. AssetsNet Fix. Assets $ 701 $ 701 Investment, LT 50 Other Assets, LT 223

Total AssetsTotal Assets $ 2,169$ 2,169

Assets 2007 2006 +/- S/UAssets 2007 2006 +/- S/U

BW’s Determination BW’s Determination of Sources and Usesof Sources and UsesBW’s Determination BW’s Determination of Sources and Usesof Sources and Uses

$ 100 $10 S 410 16 S 616 80 U 5 -- 9 1 U

$ 1,140$ 1,140 N/A 930 N/A (299) N/A$ 631$ 631 70 U 50 -- 223 --$ 2,044$ 2,044

$ 100 $10 S 410 16 S 616 80 U 5 -- 9 1 U

$ 1,140$ 1,140 N/A 930 N/A (299) N/A$ 631$ 631 70 U 50 -- 223 --$ 2,044$ 2,044

Cash and C.E. $ 90 Acct. Rec. 394 Inventories 696 Prepaid Exp 5 Accum Tax Prepay 10 Current AssetsCurrent Assets $ $ 1,195 1,195 Fixed Assets (@Cost) 1030 Less: Acc. Depr. (329) Net Fix. AssetsNet Fix. Assets $ 701 $ 701 Investment, LT 50 Other Assets, LT 223

Total AssetsTotal Assets $ 2,169$ 2,169

Assets 2007 2006 +/- S/UAssets 2007 2006 +/- S/U

BW’s Determination BW’s Determination of Sources and Usesof Sources and UsesBW’s Determination BW’s Determination of Sources and Usesof Sources and Uses

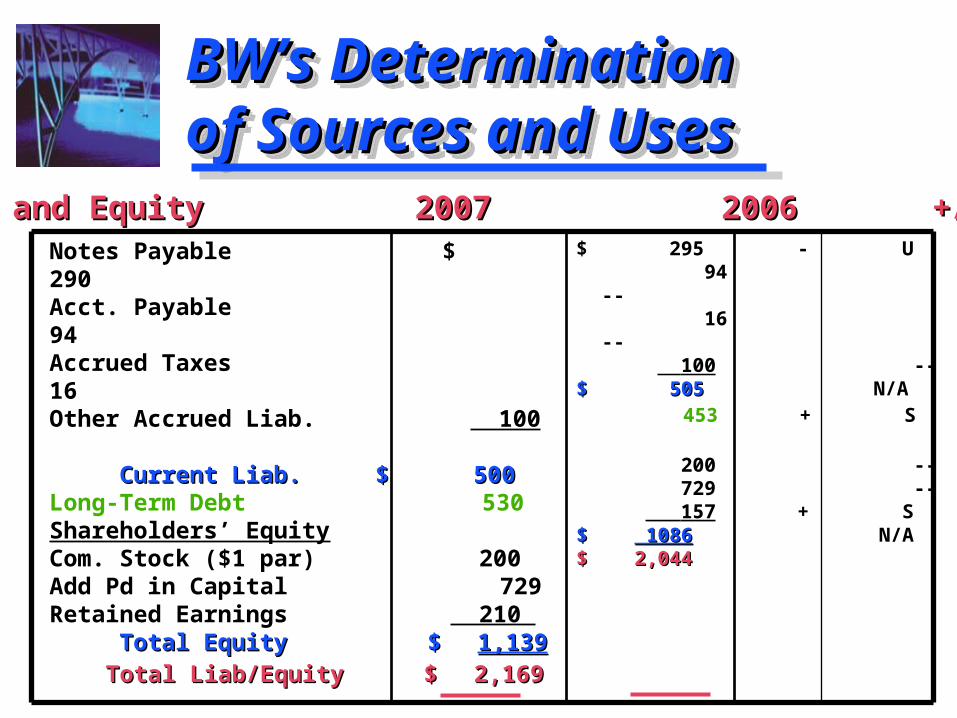

$ 295 - U 94 -- 16 -- 100 --$$ 505505 N/A

453 + S 200 -- 729 -- 157 + S$ $ 1086 1086 N/A$ 2,044$ 2,044

$ 295 - U 94 -- 16 -- 100 --$$ 505505 N/A

453 + S 200 -- 729 -- 157 + S$ $ 1086 1086 N/A$ 2,044$ 2,044

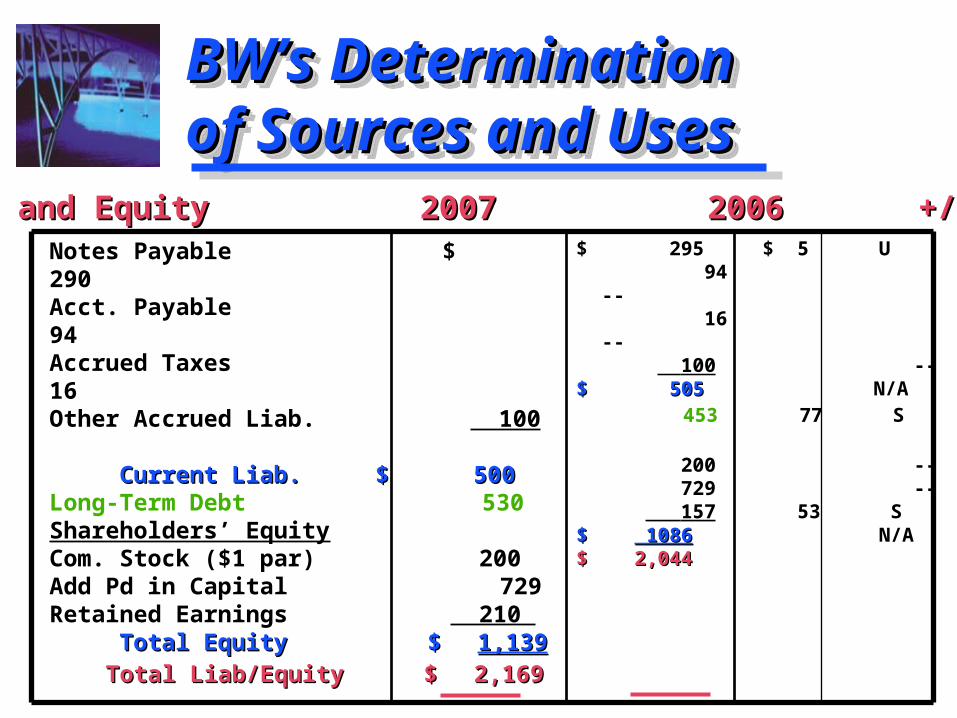

Notes Payable $ 290 Acct. Payable 94 Accrued Taxes 16 Other Accrued Liab. 100

Current Liab.Current Liab. $ 500 $ 500 Long-Term Debt 530 Shareholders’ Equity Com. Stock ($1 par) 200 Add Pd in Capital 729 Retained Earnings 210

Total EquityTotal Equity $ $ 1,1391,139 Total Liab/EquityTotal Liab/Equity $ $ 2,1692,169

Liabilities and Equity 2007 2006 +/- S/ULiabilities and Equity 2007 2006 +/- S/U

BW’s Determination BW’s Determination of Sources and Usesof Sources and UsesBW’s Determination BW’s Determination of Sources and Usesof Sources and Uses

$ 295 $ 5 U 94 -- 16 -- 100 --$$ 505505 N/A

453 77 S 200 -- 729 -- 157 53 S$ $ 1086 1086 N/A$ 2,044$ 2,044

$ 295 $ 5 U 94 -- 16 -- 100 --$$ 505505 N/A

453 77 S 200 -- 729 -- 157 53 S$ $ 1086 1086 N/A$ 2,044$ 2,044

Notes Payable $ 290 Acct. Payable 94 Accrued Taxes 16 Other Accrued Liab. 100

Current Liab.Current Liab. $ 500 $ 500 Long-Term Debt 530 Shareholders’ Equity Com. Stock ($1 par) 200 Add Pd in Capital 729 Retained Earnings 210

Total EquityTotal Equity $ $ 1,1391,139 Total Liab/EquityTotal Liab/Equity $ $ 2,1692,169

Liabilities and Equity 2007 2006 +/- S/ULiabilities and Equity 2007 2006 +/- S/U

Risk and Risk and ReturnReturn

Risk and Risk and ReturnReturn

© Pearson Education Limited 2004Fundamentals of Financial Management, 12/e

Created by: Gregory A. Kuhlemeyer, Ph.D.Carroll College, Waukesha, WI

Defining RiskDefining RiskDefining RiskDefining Risk

What rate of return do you expect on your What rate of return do you expect on your investment (savings) this year?investment (savings) this year?

What rate will you actually earn?What rate will you actually earn?

Does it matter if it is a bank CD or a share Does it matter if it is a bank CD or a share of stock?of stock?

What rate of return do you expect on your What rate of return do you expect on your investment (savings) this year?investment (savings) this year?

What rate will you actually earn?What rate will you actually earn?

Does it matter if it is a bank CD or a share Does it matter if it is a bank CD or a share of stock?of stock?

The variability of returns from The variability of returns from those that are expected.those that are expected.

The variability of returns from The variability of returns from those that are expected.those that are expected.

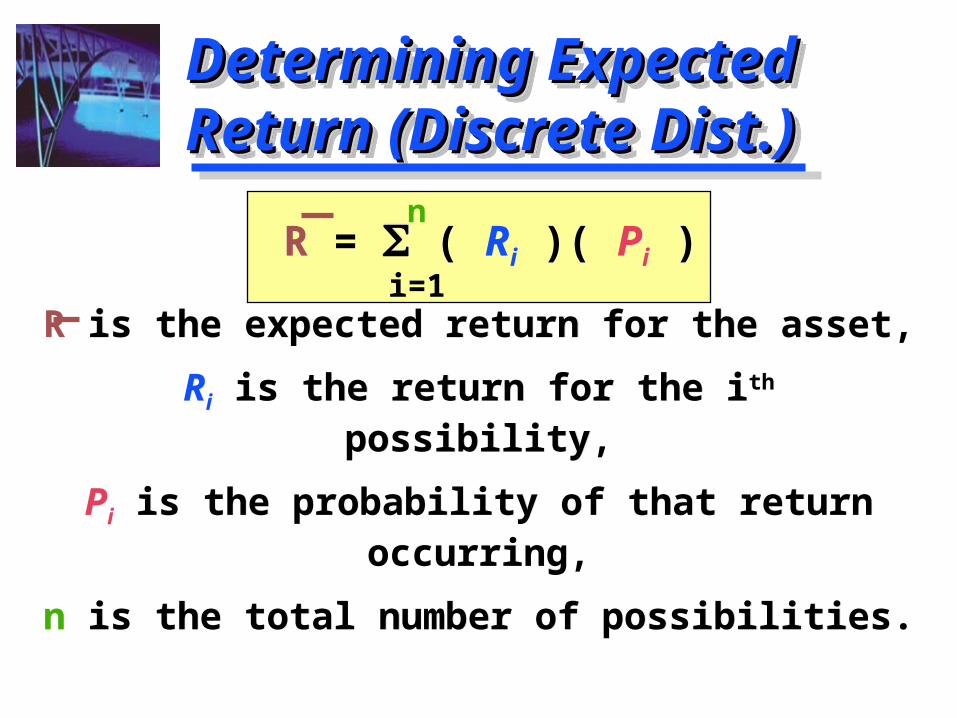

Determining Expected Determining Expected Return (Discrete Dist.)Return (Discrete Dist.)Determining Expected Determining Expected Return (Discrete Dist.)Return (Discrete Dist.)

R = ( Ri )( Pi )

R is the expected return for the asset,

Ri is the return for the ith possibility,

Pi is the probability of that return occurring,

n is the total number of possibilities.

R = ( Ri )( Pi )

R is the expected return for the asset,

Ri is the return for the ith possibility,

Pi is the probability of that return occurring,

n is the total number of possibilities.

n

i=1

How to Determine the Expected How to Determine the Expected Return and Standard DeviationReturn and Standard DeviationHow to Determine the Expected How to Determine the Expected Return and Standard DeviationReturn and Standard Deviation

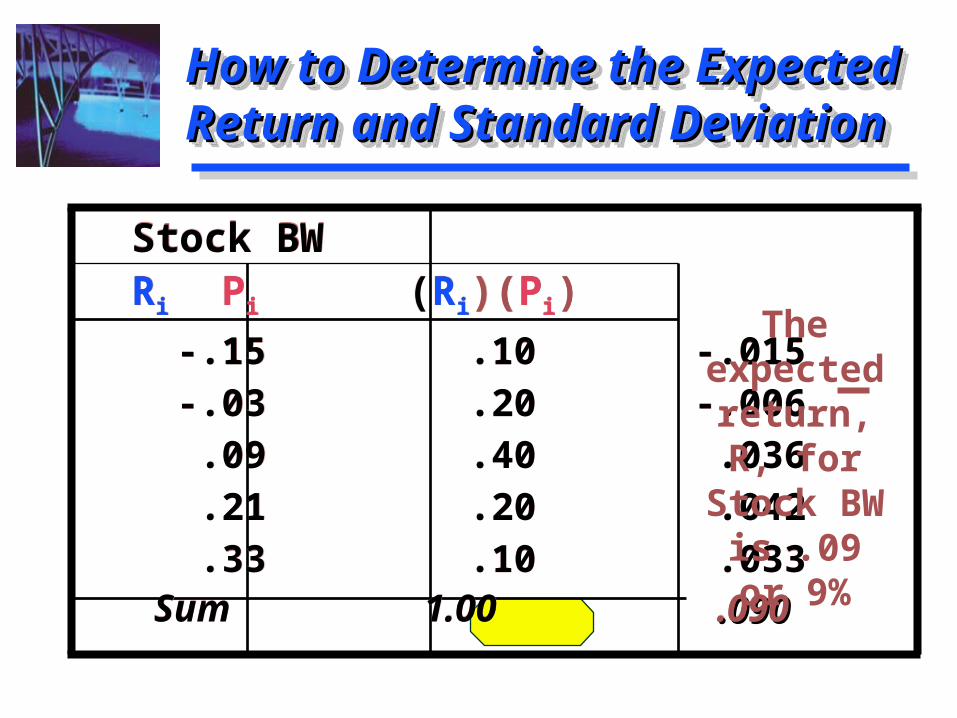

Stock BW Ri Pi (Ri)(Pi)

-.15 .10 -.015 -.03 .20 -.006 .09 .40 .036 .21 .20 .042 .33 .10 .033 Sum 1.00 .090.090

Stock BW Ri Pi (Ri)(Pi)

-.15 .10 -.015 -.03 .20 -.006 .09 .40 .036 .21 .20 .042 .33 .10 .033 Sum 1.00 .090.090

The expected return, R, for Stock BW is .09

or 9%

Determining Standard Determining Standard Deviation (Risk Measure)Deviation (Risk Measure)Determining Standard Determining Standard Deviation (Risk Measure)Deviation (Risk Measure)

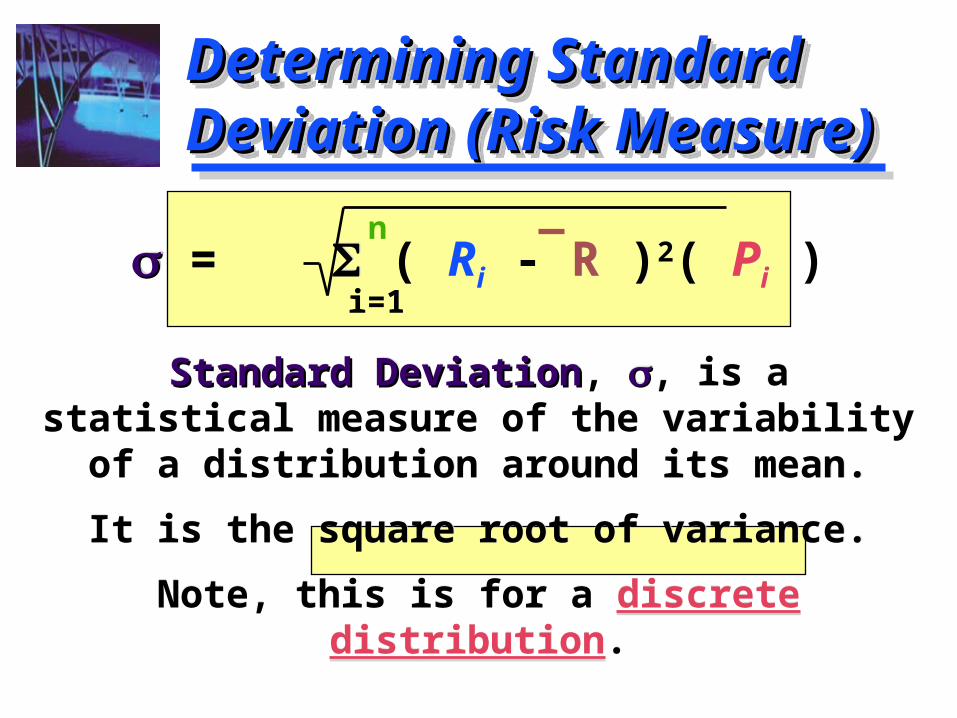

= ( Ri - R )2( Pi )

Standard DeviationStandard Deviation, , is a statistical measure of the variability of a distribution

around its mean.

It is the square root of variance.

Note, this is for a discrete distribution.

= ( Ri - R )2( Pi )

Standard DeviationStandard Deviation, , is a statistical measure of the variability of a distribution

around its mean.

It is the square root of variance.

Note, this is for a discrete distribution.

n

i=1

How to Determine the Expected How to Determine the Expected Return and Standard DeviationReturn and Standard DeviationHow to Determine the Expected How to Determine the Expected Return and Standard DeviationReturn and Standard Deviation

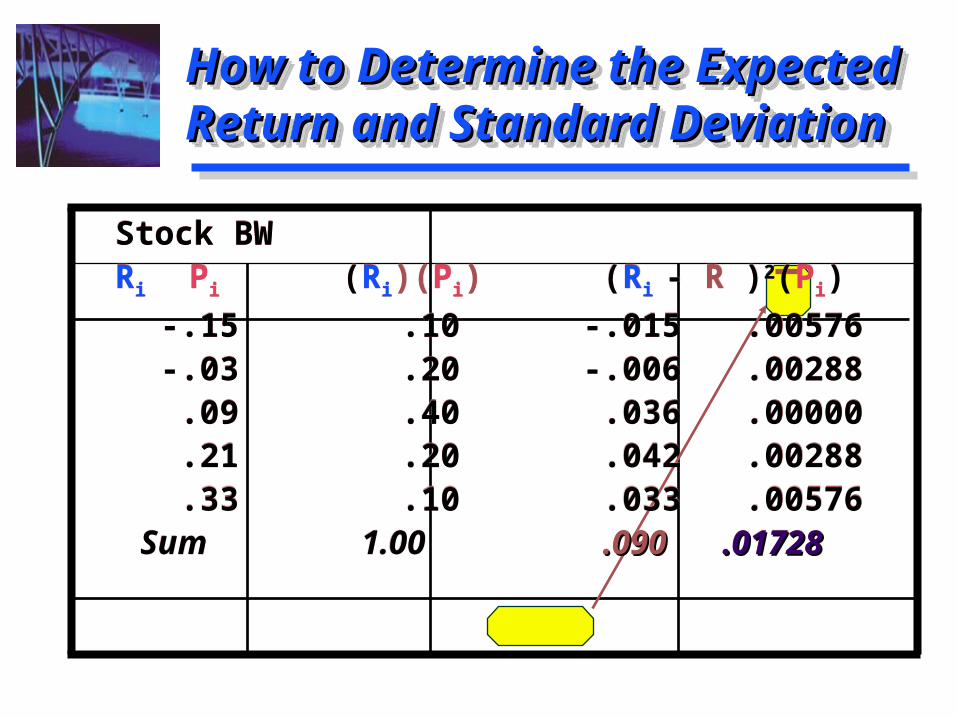

Stock BW Ri Pi (Ri)(Pi) (Ri - R )2(Pi)

-.15 .10 -.015 .00576 -.03 .20 -.006 .00288 .09 .40 .036 .00000 .21 .20 .042 .00288 .33 .10 .033 .00576 Sum 1.00 .090.090 .01728.01728

Stock BW Ri Pi (Ri)(Pi) (Ri - R )2(Pi)

-.15 .10 -.015 .00576 -.03 .20 -.006 .00288 .09 .40 .036 .00000 .21 .20 .042 .00288 .33 .10 .033 .00576 Sum 1.00 .090.090 .01728.01728

Determining Standard Determining Standard Deviation (Risk Measure)Deviation (Risk Measure)Determining Standard Determining Standard Deviation (Risk Measure)Deviation (Risk Measure)

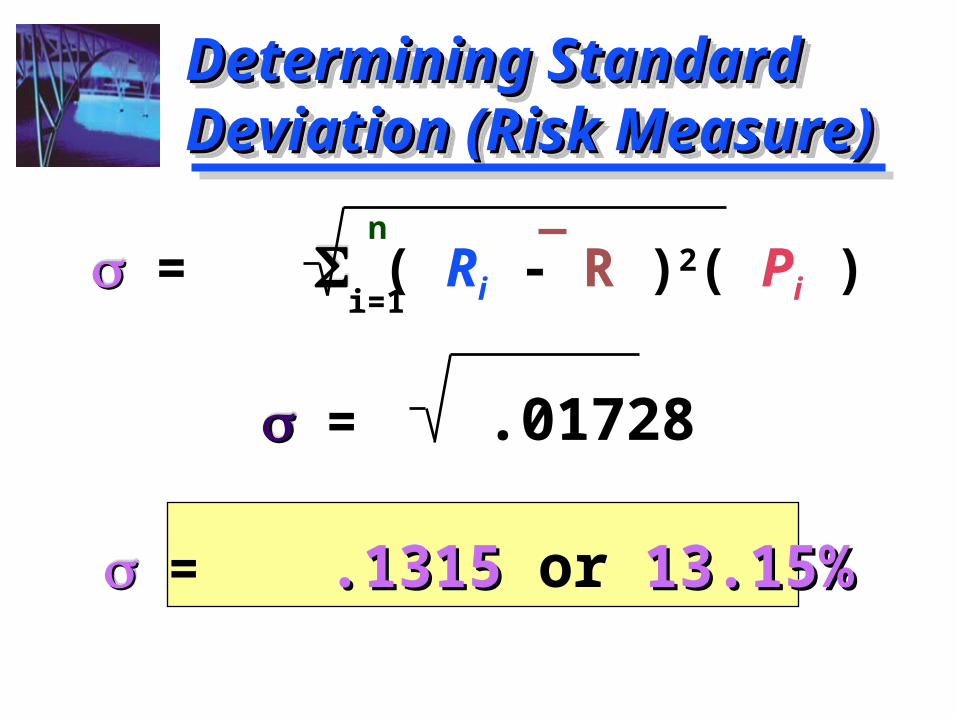

= ( Ri - R )2( Pi )

= .01728

= .1315.1315 or 13.15%13.15%

= ( Ri - R )2( Pi )

= .01728

= .1315.1315 or 13.15%13.15%

n

i=1

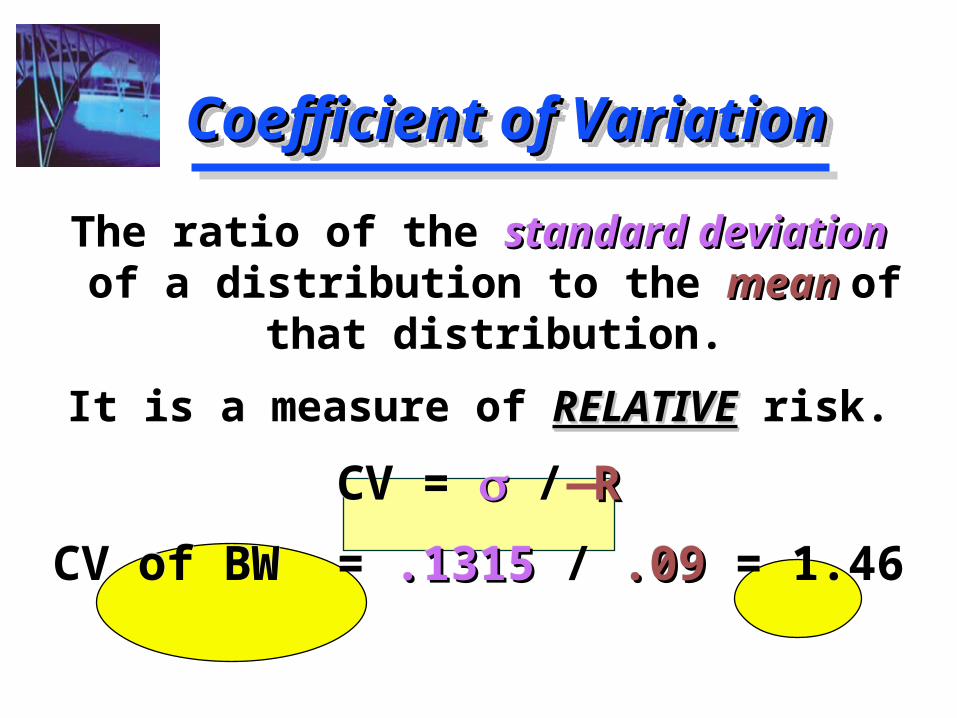

Coefficient of VariationCoefficient of VariationCoefficient of VariationCoefficient of Variation

The ratio of the standard deviation standard deviation of a distribution to the mean mean of that

distribution.

It is a measure of RELATIVERELATIVE risk.

CV = / RR

CV of BW = .1315.1315 / .09.09 = 1.46

The ratio of the standard deviation standard deviation of a distribution to the mean mean of that

distribution.

It is a measure of RELATIVERELATIVE risk.

CV = / RR

CV of BW = .1315.1315 / .09.09 = 1.46

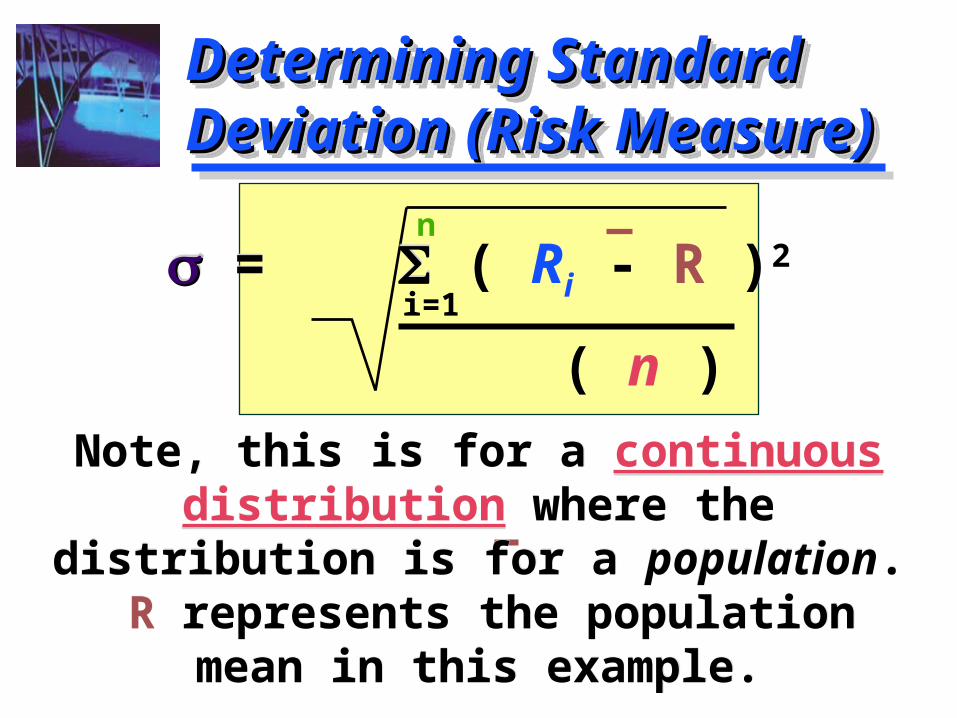

Determining Standard Determining Standard Deviation (Risk Measure)Deviation (Risk Measure)Determining Standard Determining Standard Deviation (Risk Measure)Deviation (Risk Measure)

n

i=1 = ( Ri - R )2

( n )

Note, this is for a continuous distribution where the distribution is for a population. R represents the population mean in this example.

= ( Ri - R )2

( n )

Note, this is for a continuous distribution where the distribution is for a population. R represents the population mean in this example.

RP = ( Wj )( Rj )

RP is the expected return for the portfolio,

Wj is the weight (investment proportion) for the jth asset in the portfolio,

Rj is the expected return of the jth asset,

m is the total number of assets in the portfolio.

RP = ( Wj )( Rj )

RP is the expected return for the portfolio,

Wj is the weight (investment proportion) for the jth asset in the portfolio,

Rj is the expected return of the jth asset,

m is the total number of assets in the portfolio.

Determining PortfolioDetermining PortfolioExpected ReturnExpected ReturnDetermining PortfolioDetermining PortfolioExpected ReturnExpected Return

m

j=1

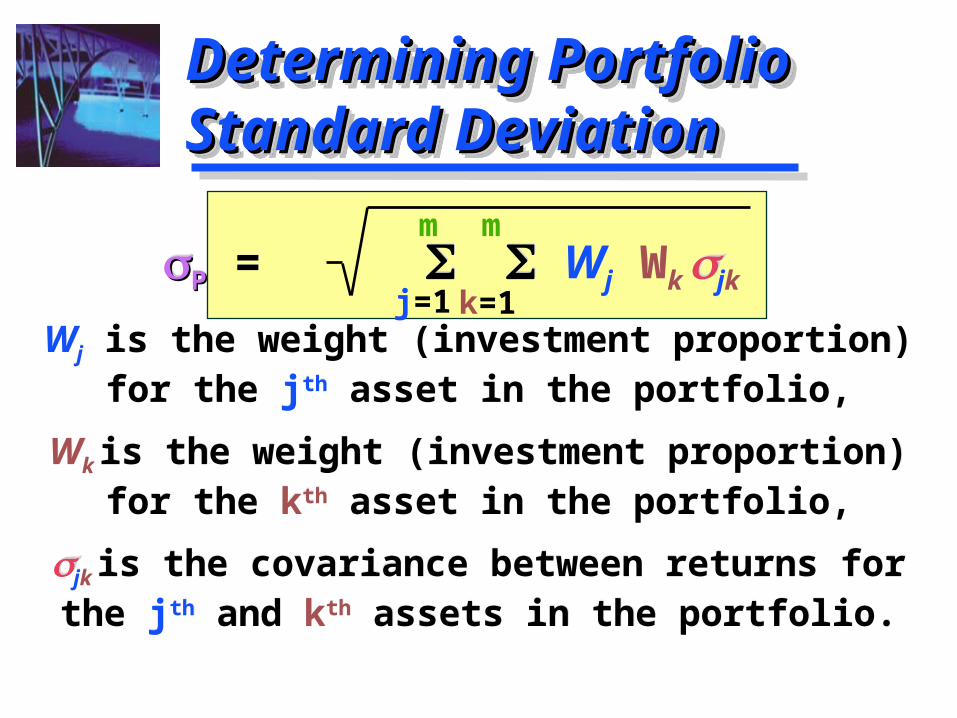

Determining Portfolio Determining Portfolio Standard DeviationStandard DeviationDetermining Portfolio Determining Portfolio Standard DeviationStandard Deviation

m

j=1

m

k=1PP = Wj Wk jk

Wj is the weight (investment proportion) for the jth asset in the portfolio,

Wk is the weight (investment proportion) for the kth asset in the portfolio,

jk is the covariance between returns for the jth and kth assets in the portfolio.

PP = Wj Wk jk

Wj is the weight (investment proportion) for the jth asset in the portfolio,

Wk is the weight (investment proportion) for the kth asset in the portfolio,

jk is the covariance between returns for the jth and kth assets in the portfolio.

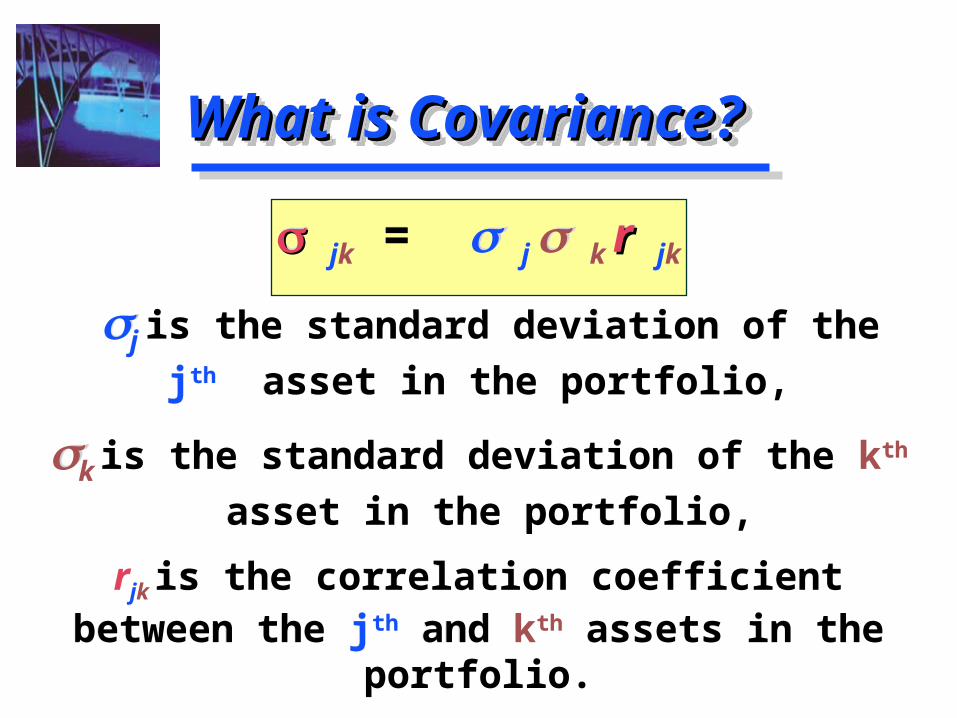

What is Covariance?What is Covariance?What is Covariance?What is Covariance?

jk = j k rrjk

j is the standard deviation of the jth

asset in the portfolio,

k is the standard deviation of the kth

asset in the portfolio,

rjk is the correlation coefficient between the jth and kth assets in the portfolio.

jk = j k rrjk

j is the standard deviation of the jth

asset in the portfolio,

k is the standard deviation of the kth

asset in the portfolio,

rjk is the correlation coefficient between the jth and kth assets in the portfolio.

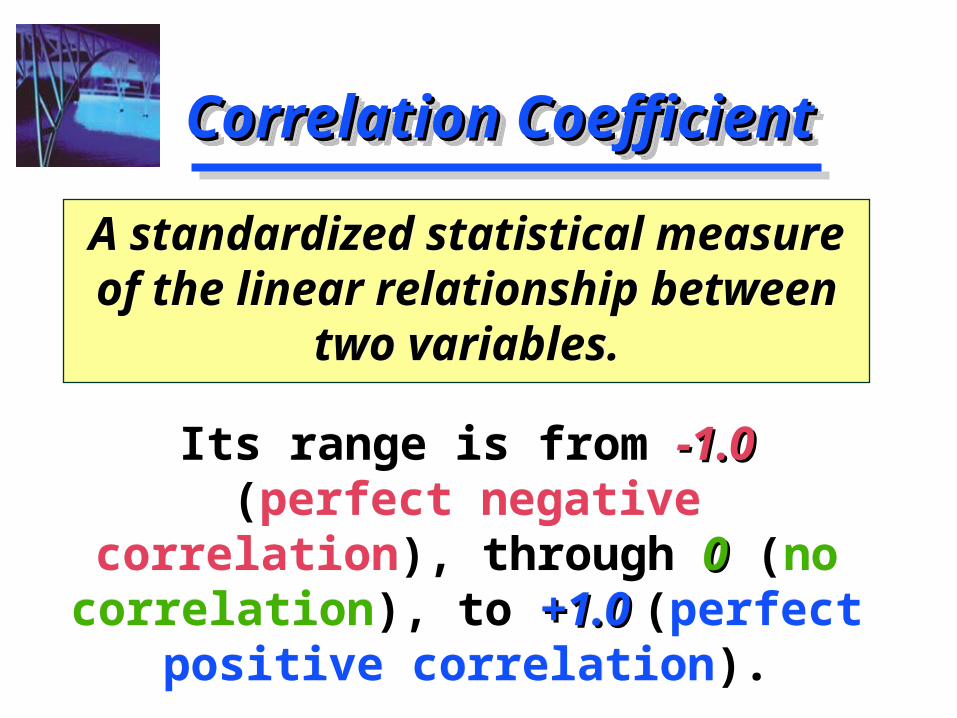

Correlation CoefficientCorrelation CoefficientCorrelation CoefficientCorrelation Coefficient

A standardized statistical measure of the linear relationship between

two variables.

Its range is from -1.0 -1.0 (perfect negative correlation), through 00 (no correlation), to +1.0 +1.0 (perfect

positive correlation).

A standardized statistical measure of the linear relationship between

two variables.

Its range is from -1.0 -1.0 (perfect negative correlation), through 00 (no correlation), to +1.0 +1.0 (perfect

positive correlation).

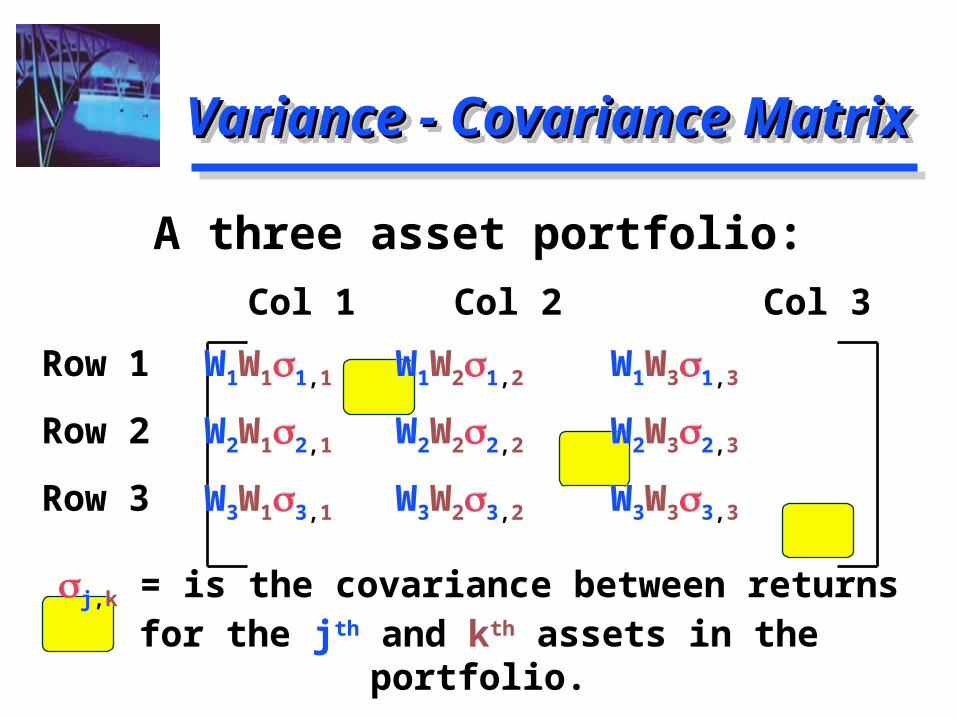

Variance - Covariance MatrixVariance - Covariance MatrixVariance - Covariance MatrixVariance - Covariance Matrix

A three asset portfolio:

Col 1 Col 2 Col 3

Row 1 W1W11,1 W1W21,2 W1W31,3

Row 2 W2W12,1 W2W22,2 W2W32,3

Row 3 W3W13,1 W3W23,2 W3W33,3

j,k = is the covariance between returns for the jth and kth assets in the portfolio.

A three asset portfolio:

Col 1 Col 2 Col 3

Row 1 W1W11,1 W1W21,2 W1W31,3

Row 2 W2W12,1 W2W22,2 W2W32,3

Row 3 W3W13,1 W3W23,2 W3W33,3

j,k = is the covariance between returns for the jth and kth assets in the portfolio.

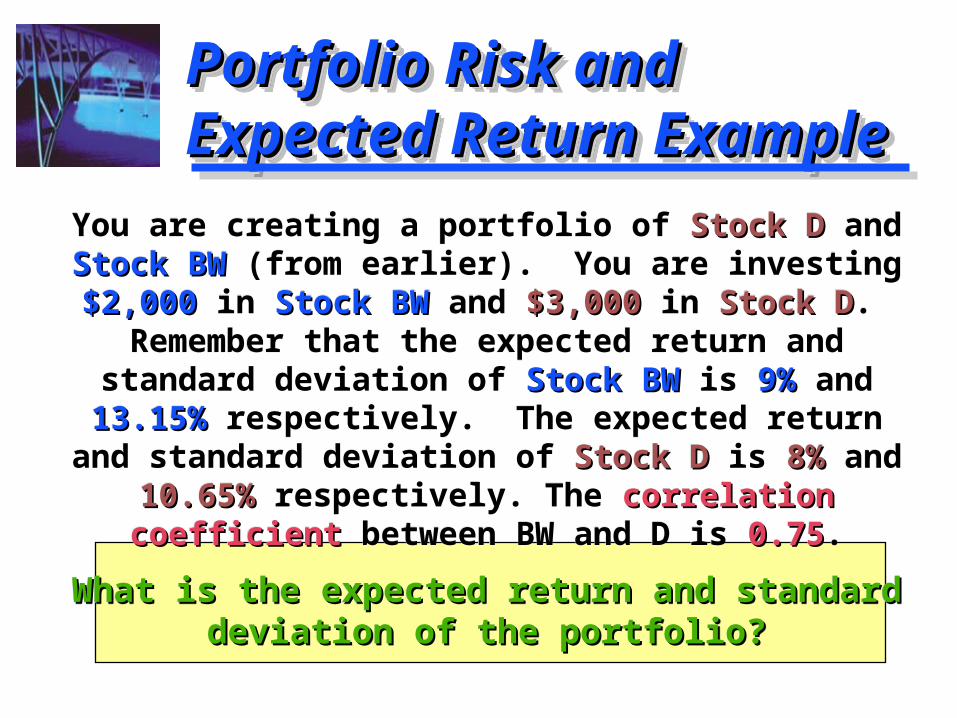

You are creating a portfolio of Stock D Stock D and Stock Stock BW BW (from earlier). You are investing $2,000$2,000 in

Stock BW Stock BW and $3,000$3,000 in Stock DStock D. Remember that the expected return and standard deviation of Stock BWStock BW is 9%9% and 13.15%13.15% respectively. The

expected return and standard deviation of Stock D Stock D is 8%8% and 10.65%10.65% respectively. The correlation correlation

coefficient coefficient between BW and D is 0.750.75.

What is the expected return and standard What is the expected return and standard deviation of the portfolio?deviation of the portfolio?

You are creating a portfolio of Stock D Stock D and Stock Stock BW BW (from earlier). You are investing $2,000$2,000 in

Stock BW Stock BW and $3,000$3,000 in Stock DStock D. Remember that the expected return and standard deviation of Stock BWStock BW is 9%9% and 13.15%13.15% respectively. The

expected return and standard deviation of Stock D Stock D is 8%8% and 10.65%10.65% respectively. The correlation correlation

coefficient coefficient between BW and D is 0.750.75.

What is the expected return and standard What is the expected return and standard deviation of the portfolio?deviation of the portfolio?

Portfolio Risk and Portfolio Risk and Expected Return ExampleExpected Return ExamplePortfolio Risk and Portfolio Risk and Expected Return ExampleExpected Return Example

Determining Portfolio Determining Portfolio Expected ReturnExpected ReturnDetermining Portfolio Determining Portfolio Expected ReturnExpected Return

WBW = $2,000 / $5,000 = .4

WWDD = $3,000 / $5,000 = .6 .6

RP = (WBW)(RBW) + (WWDD)(RRDD)

RP = (.4)(9%) + (.6.6)(8%8%)

RP = (3.6%) + (4.8%4.8%) = 8.4%8.4%

WBW = $2,000 / $5,000 = .4

WWDD = $3,000 / $5,000 = .6 .6

RP = (WBW)(RBW) + (WWDD)(RRDD)

RP = (.4)(9%) + (.6.6)(8%8%)

RP = (3.6%) + (4.8%4.8%) = 8.4%8.4%

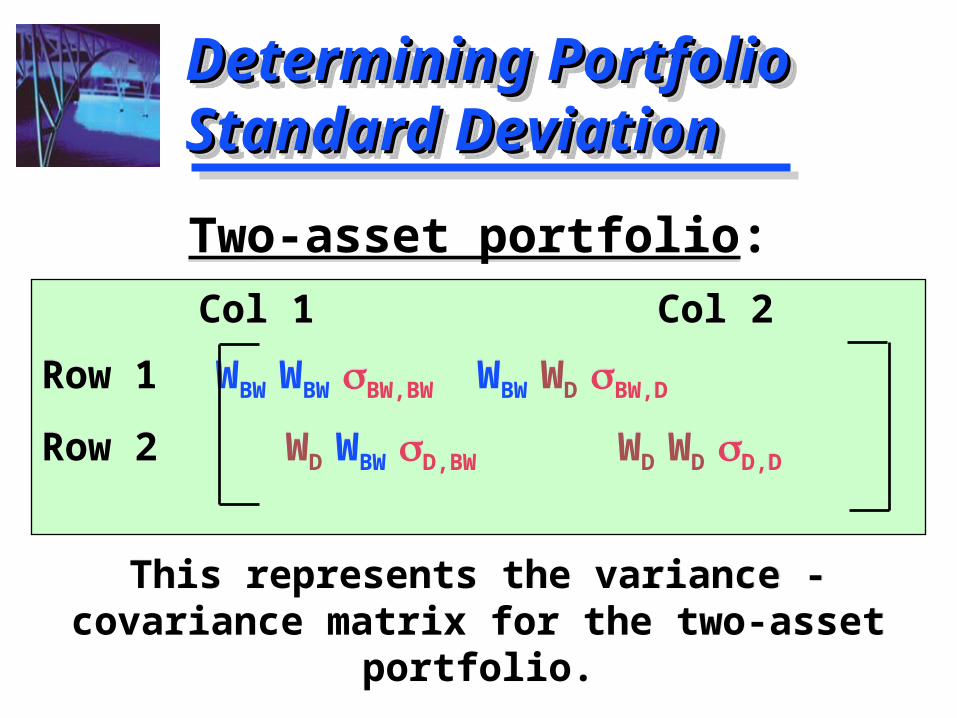

Two-asset portfolio:

Col 1 Col 2

Row 1 WBW WBW BW,BW WBW WD BW,D

Row 2 WD WBW D,BW WD WD D,D

This represents the variance - covariance matrix for the two-asset portfolio.

Two-asset portfolio:

Col 1 Col 2

Row 1 WBW WBW BW,BW WBW WD BW,D

Row 2 WD WBW D,BW WD WD D,D

This represents the variance - covariance matrix for the two-asset portfolio.

Determining Portfolio Determining Portfolio Standard DeviationStandard DeviationDetermining Portfolio Determining Portfolio Standard DeviationStandard Deviation

Two-asset portfolio:

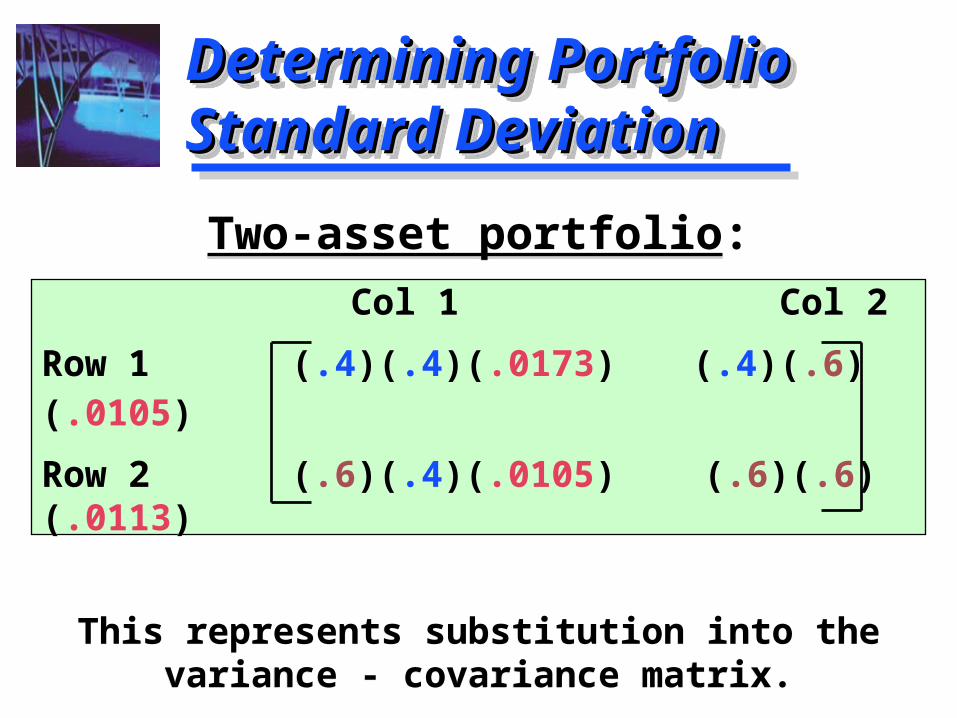

Col 1 Col 2

Row 1 (.4)(.4)(.0173) (.4)(.6)(.0105)

Row 2 (.6)(.4)(.0105) (.6)(.6)(.0113)

This represents substitution into the variance - covariance matrix.

Two-asset portfolio:

Col 1 Col 2

Row 1 (.4)(.4)(.0173) (.4)(.6)(.0105)

Row 2 (.6)(.4)(.0105) (.6)(.6)(.0113)

This represents substitution into the variance - covariance matrix.

Determining Portfolio Determining Portfolio Standard DeviationStandard DeviationDetermining Portfolio Determining Portfolio Standard DeviationStandard Deviation

Two-asset portfolio:

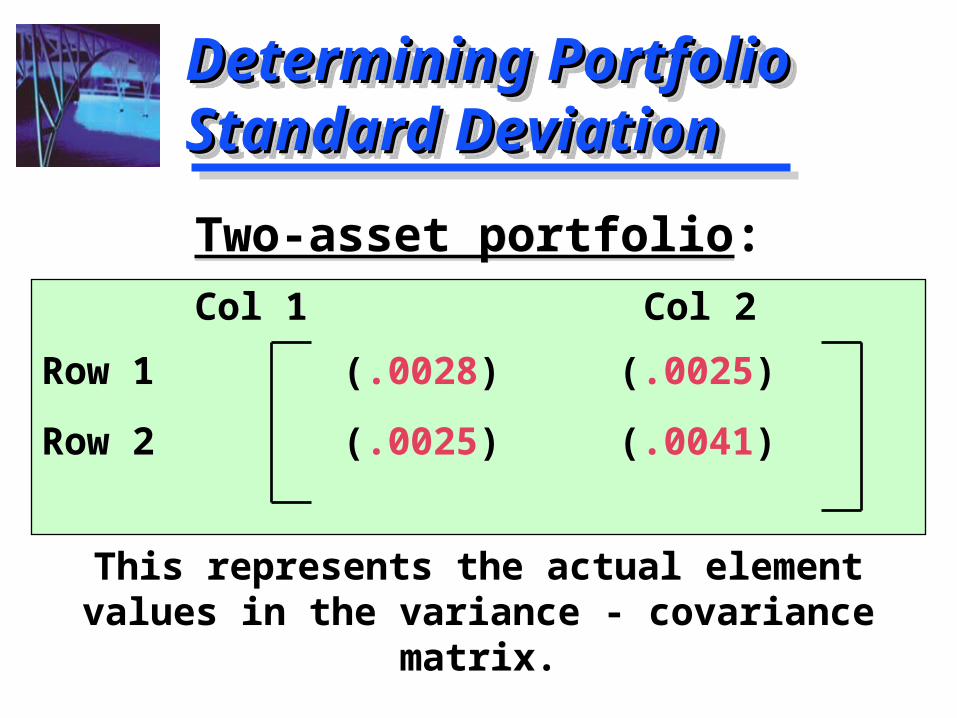

Col 1 Col 2

Row 1 (.0028) (.0025)

Row 2 (.0025) (.0041)

This represents the actual element values in the variance - covariance matrix.

Two-asset portfolio:

Col 1 Col 2

Row 1 (.0028) (.0025)

Row 2 (.0025) (.0041)

This represents the actual element values in the variance - covariance matrix.

Determining Portfolio Determining Portfolio Standard DeviationStandard DeviationDetermining Portfolio Determining Portfolio Standard DeviationStandard Deviation

Determining Portfolio Determining Portfolio Standard DeviationStandard DeviationDetermining Portfolio Determining Portfolio Standard DeviationStandard Deviation

P = .0028 + (2)(.0025) + .0041

P = SQRT(.0119)

P = .1091 or 10.91%

A weighted average of the individual standard deviations is INCORRECT.

P = .0028 + (2)(.0025) + .0041

P = SQRT(.0119)

P = .1091 or 10.91%

A weighted average of the individual standard deviations is INCORRECT.

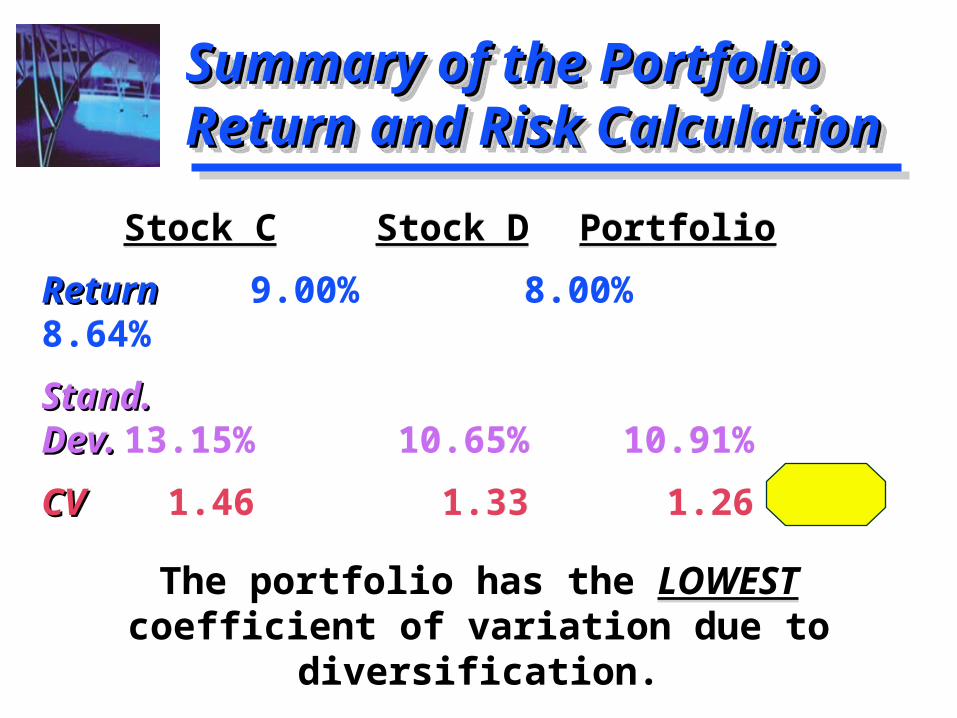

Stock C Stock D Portfolio

ReturnReturn 9.00% 8.00% 8.64%

Stand.Stand.Dev.Dev. 13.15% 10.65% 10.91%

CVCV 1.46 1.33 1.26

The portfolio has the LOWEST coefficient of variation due to diversification.

Stock C Stock D Portfolio

ReturnReturn 9.00% 8.00% 8.64%

Stand.Stand.Dev.Dev. 13.15% 10.65% 10.91%

CVCV 1.46 1.33 1.26

The portfolio has the LOWEST coefficient of variation due to diversification.

Summary of the Portfolio Summary of the Portfolio Return and Risk CalculationReturn and Risk CalculationSummary of the Portfolio Summary of the Portfolio Return and Risk CalculationReturn and Risk Calculation

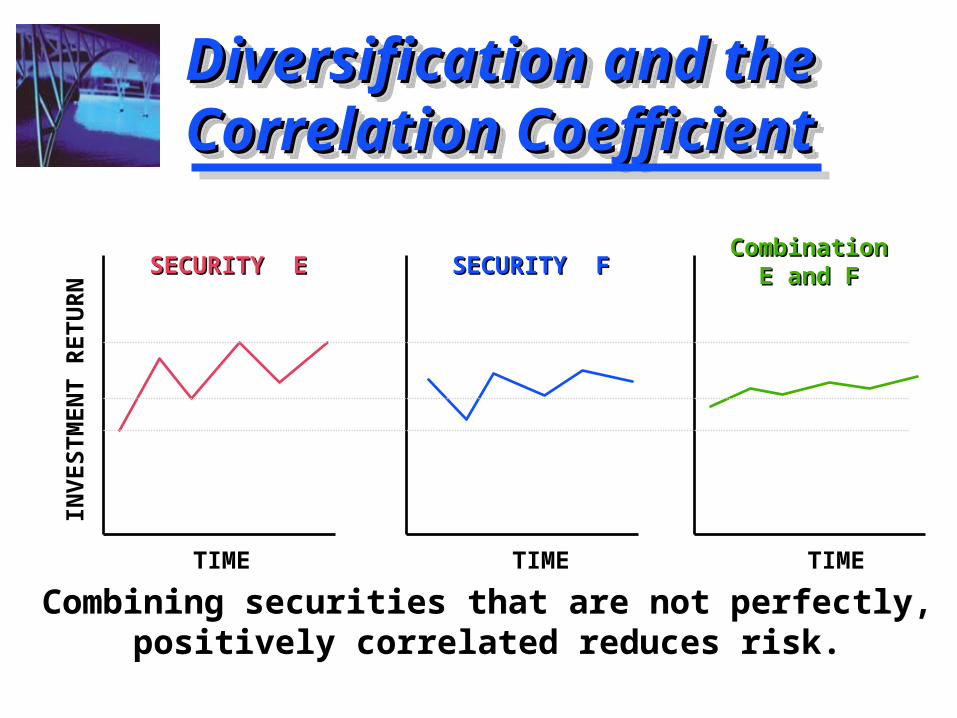

Combining securities that are not perfectly, positively correlated reduces risk.

Combining securities that are not perfectly, positively correlated reduces risk.

Diversification and the Diversification and the Correlation CoefficientCorrelation CoefficientDiversification and the Diversification and the Correlation CoefficientCorrelation CoefficientIN

VE

ST

ME

NT

RE

TU

RN

TIME TIMETIME

SECURITY ESECURITY E SECURITY FSECURITY FCombinationCombination

E and FE and F

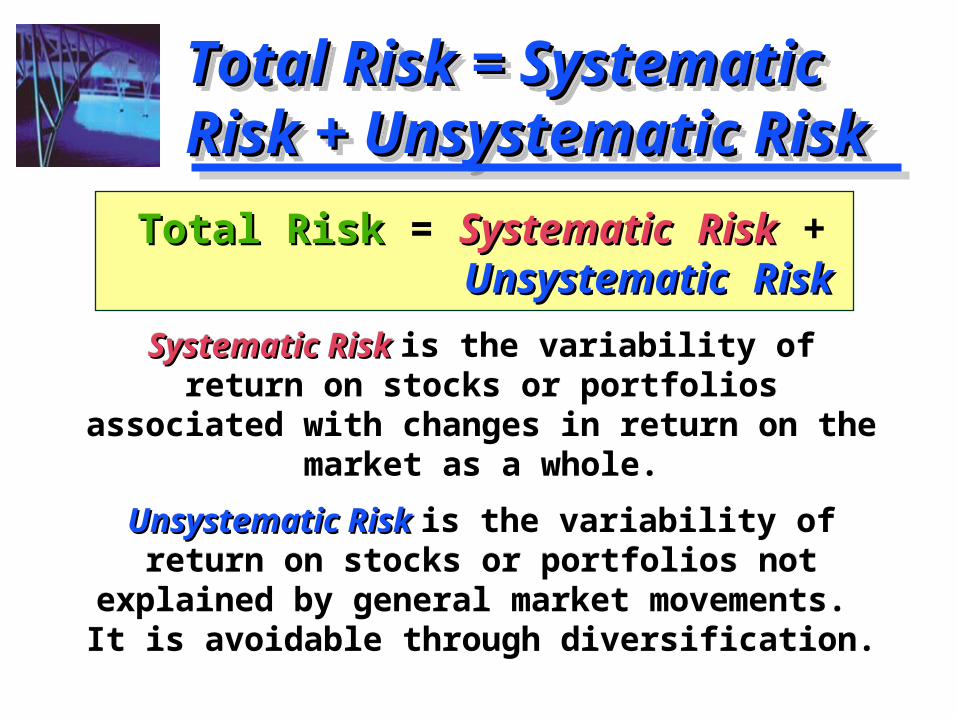

Systematic Risk Systematic Risk is the variability of return on stocks or portfolios associated with

changes in return on the market as a whole.

Unsystematic Risk Unsystematic Risk is the variability of return on stocks or portfolios not explained by

general market movements. It is avoidable through diversification.

Systematic Risk Systematic Risk is the variability of return on stocks or portfolios associated with

changes in return on the market as a whole.

Unsystematic Risk Unsystematic Risk is the variability of return on stocks or portfolios not explained by

general market movements. It is avoidable through diversification.

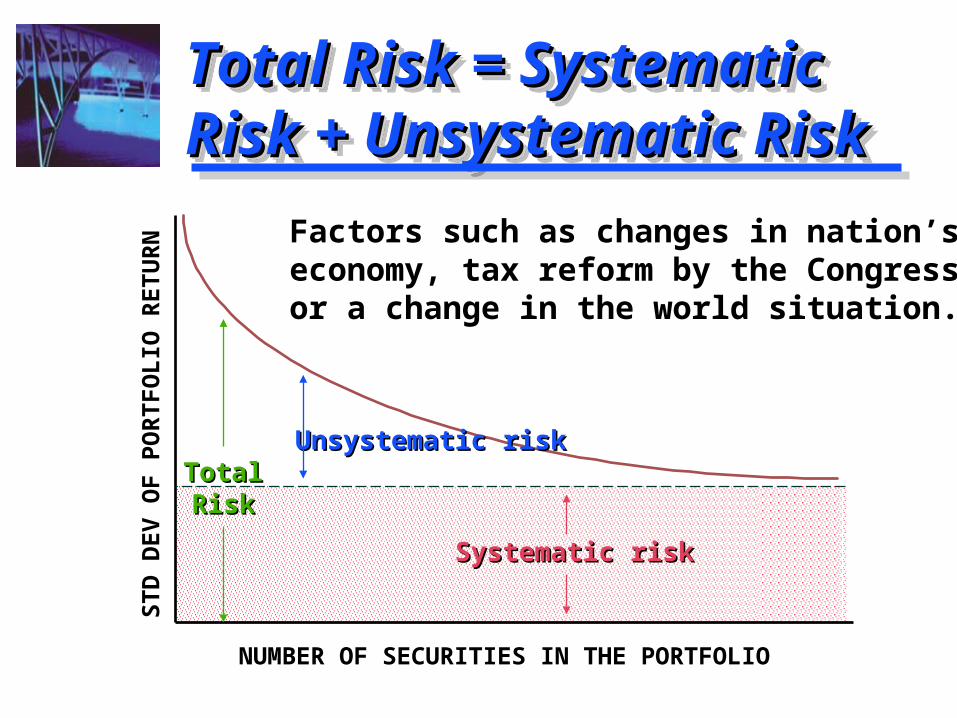

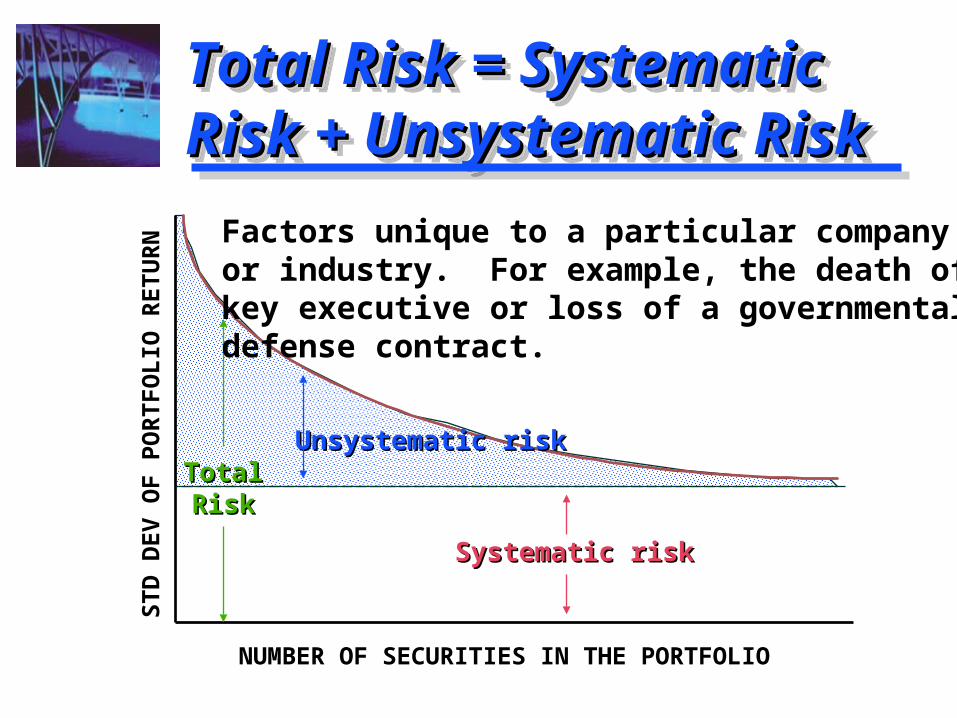

Total Risk = Systematic Total Risk = Systematic Risk + Unsystematic RiskRisk + Unsystematic RiskTotal Risk = Systematic Total Risk = Systematic Risk + Unsystematic RiskRisk + Unsystematic Risk

Total Risk Total Risk = SystematicSystematic RiskRisk + UnsystematicUnsystematic RiskRisk

Total Risk = Systematic Total Risk = Systematic Risk + Unsystematic RiskRisk + Unsystematic RiskTotal Risk = Systematic Total Risk = Systematic Risk + Unsystematic RiskRisk + Unsystematic Risk

TotalTotalRiskRisk

Unsystematic riskUnsystematic risk

Systematic riskSystematic risk

ST

D D

EV

OF

PO

RT

FO

LIO

RE

TU

RN

NUMBER OF SECURITIES IN THE PORTFOLIO

Factors such as changes in nation’s economy, tax reform by the Congress,or a change in the world situation.

Total Risk = Systematic Total Risk = Systematic Risk + Unsystematic RiskRisk + Unsystematic RiskTotal Risk = Systematic Total Risk = Systematic Risk + Unsystematic RiskRisk + Unsystematic Risk

TotalTotalRiskRisk

Unsystematic riskUnsystematic risk

Systematic riskSystematic risk

ST

D D

EV

OF

PO

RT

FO

LIO

RE

TU

RN

NUMBER OF SECURITIES IN THE PORTFOLIO

Factors unique to a particular companyor industry. For example, the death of akey executive or loss of a governmentaldefense contract.

CAPM is a model that describes the relationship between risk and

expected (required) return; in this model, a security’s expected

(required) return is the risk-free rate risk-free rate plus a premium a premium based on the

systematic risk systematic risk of the security.

CAPM is a model that describes the relationship between risk and

expected (required) return; in this model, a security’s expected

(required) return is the risk-free rate risk-free rate plus a premium a premium based on the

systematic risk systematic risk of the security.

Capital Asset Capital Asset Pricing Model (CAPM)Pricing Model (CAPM)Capital Asset Capital Asset Pricing Model (CAPM)Pricing Model (CAPM)

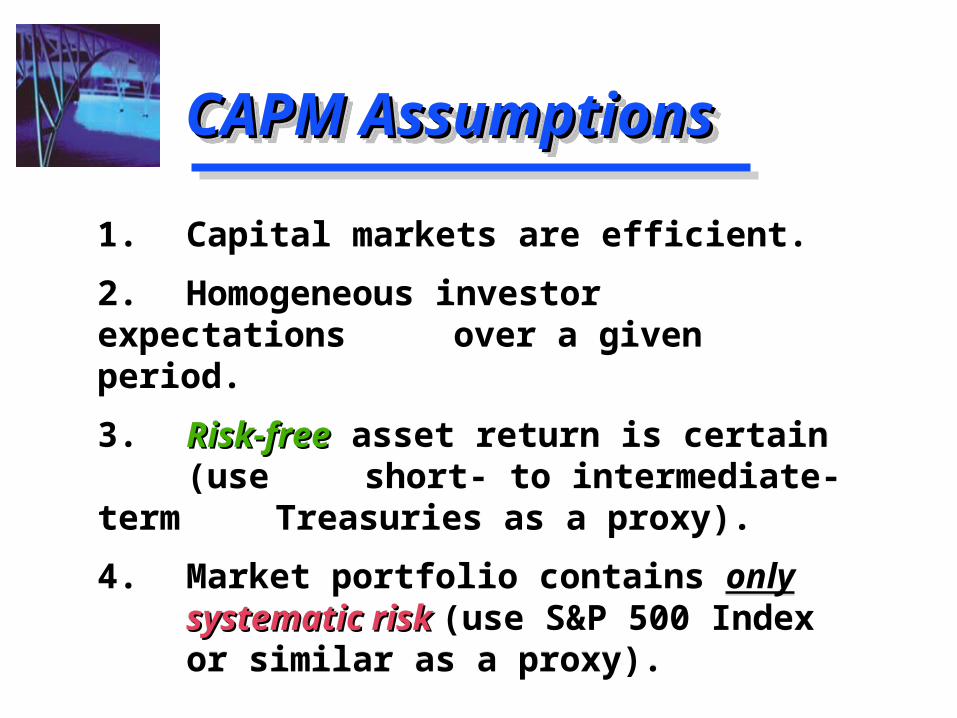

1. Capital markets are efficient.

2. Homogeneous investor expectations over a given period.

3. Risk-freeRisk-free asset return is certain (use short- to intermediate-term Treasuries as a proxy).

4. Market portfolio contains only systematic risk systematic risk (use S&P 500 Indexor similar as a proxy).

1. Capital markets are efficient.

2. Homogeneous investor expectations over a given period.

3. Risk-freeRisk-free asset return is certain (use short- to intermediate-term Treasuries as a proxy).

4. Market portfolio contains only systematic risk systematic risk (use S&P 500 Indexor similar as a proxy).

CAPM AssumptionsCAPM AssumptionsCAPM AssumptionsCAPM Assumptions

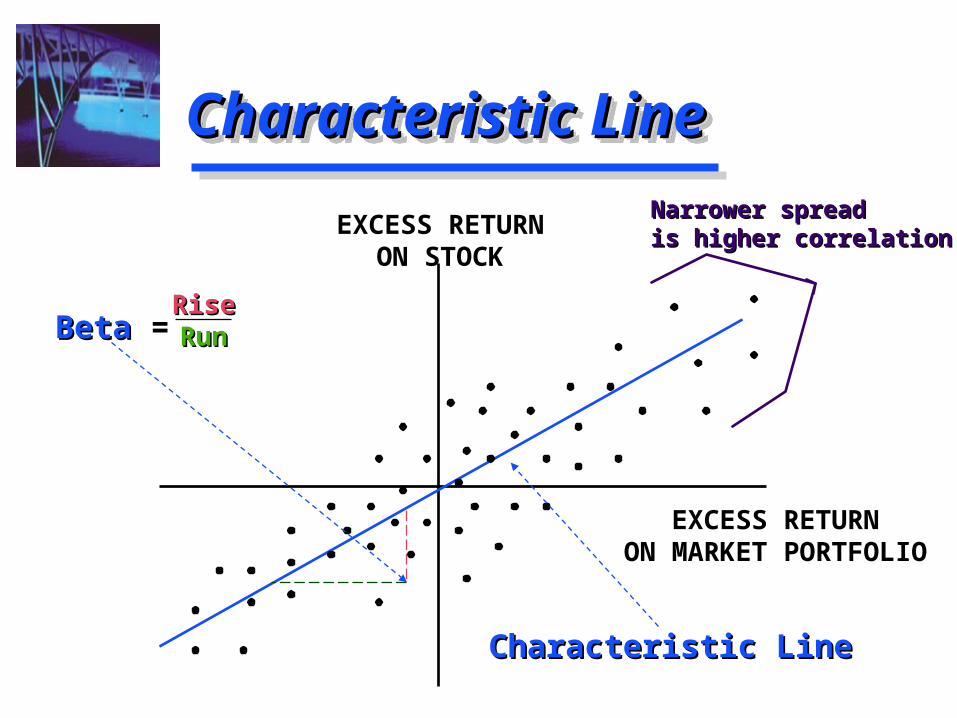

Characteristic LineCharacteristic LineCharacteristic LineCharacteristic Line

EXCESS RETURNON STOCK

EXCESS RETURNON MARKET PORTFOLIO

BetaBeta =RiseRiseRunRun

Narrower spreadNarrower spreadis higher correlationis higher correlation

Characteristic LineCharacteristic Line

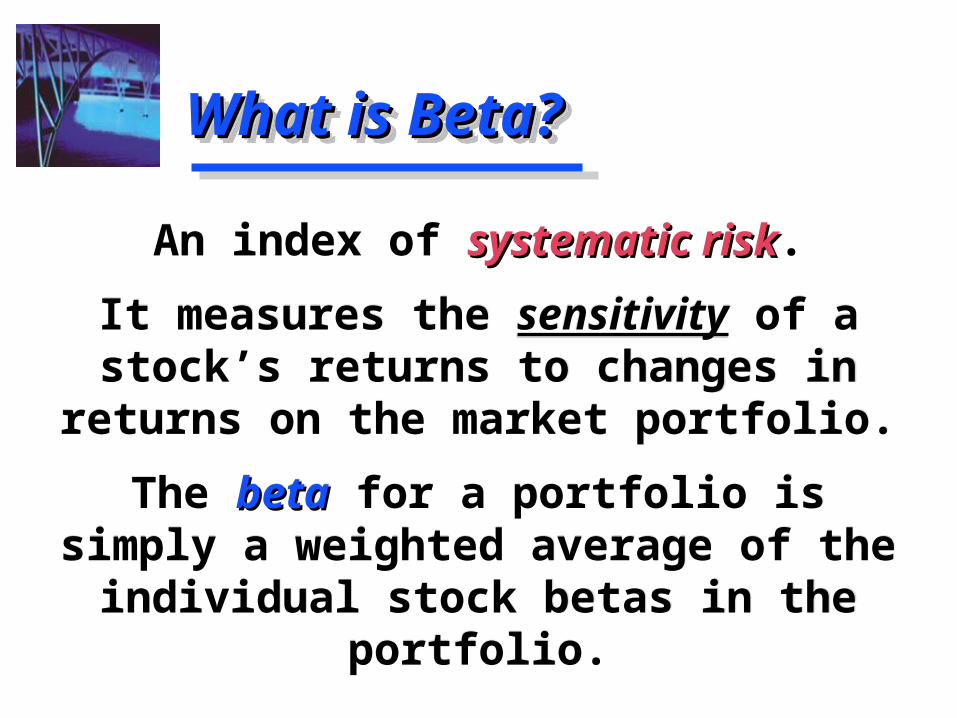

An index of systematic risksystematic risk.

It measures the sensitivity of a stock’s returns to changes in

returns on the market portfolio.

The betabeta for a portfolio is simply a weighted average of the individual

stock betas in the portfolio.

An index of systematic risksystematic risk.

It measures the sensitivity of a stock’s returns to changes in

returns on the market portfolio.

The betabeta for a portfolio is simply a weighted average of the individual

stock betas in the portfolio.

What is Beta?What is Beta?What is Beta?What is Beta?

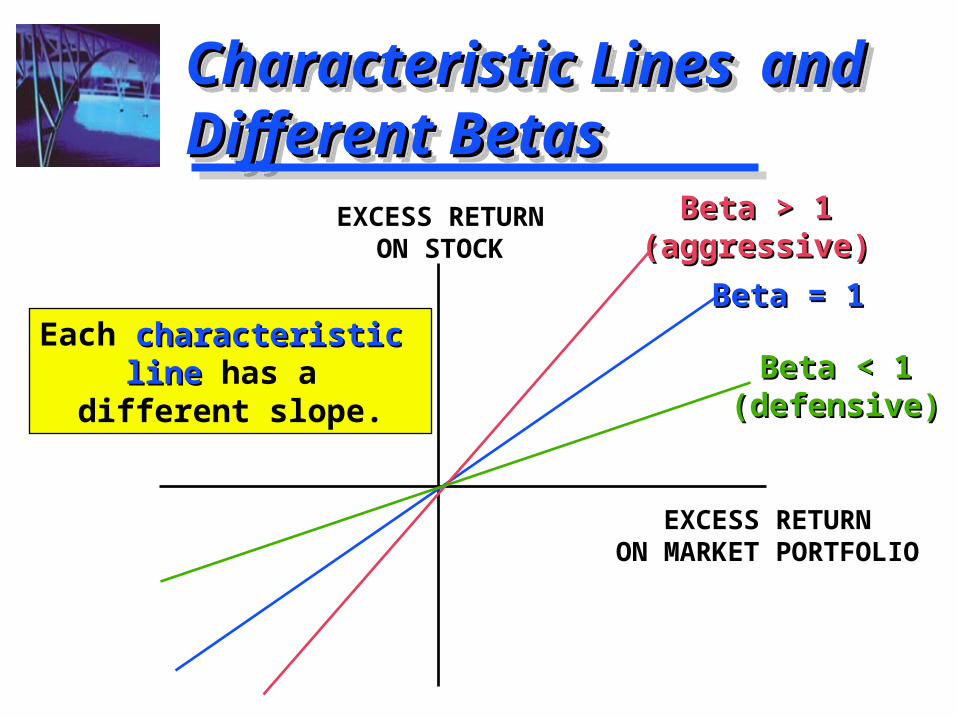

Characteristic Lines Characteristic Lines and Different Betasand Different BetasCharacteristic Lines Characteristic Lines and Different Betasand Different Betas

EXCESS RETURNON STOCK

EXCESS RETURNON MARKET PORTFOLIO

Beta < 1Beta < 1(defensive)(defensive)

Beta = 1Beta = 1

Beta > 1Beta > 1(aggressive)(aggressive)

Each characteristic characteristic line line has a

different slope.

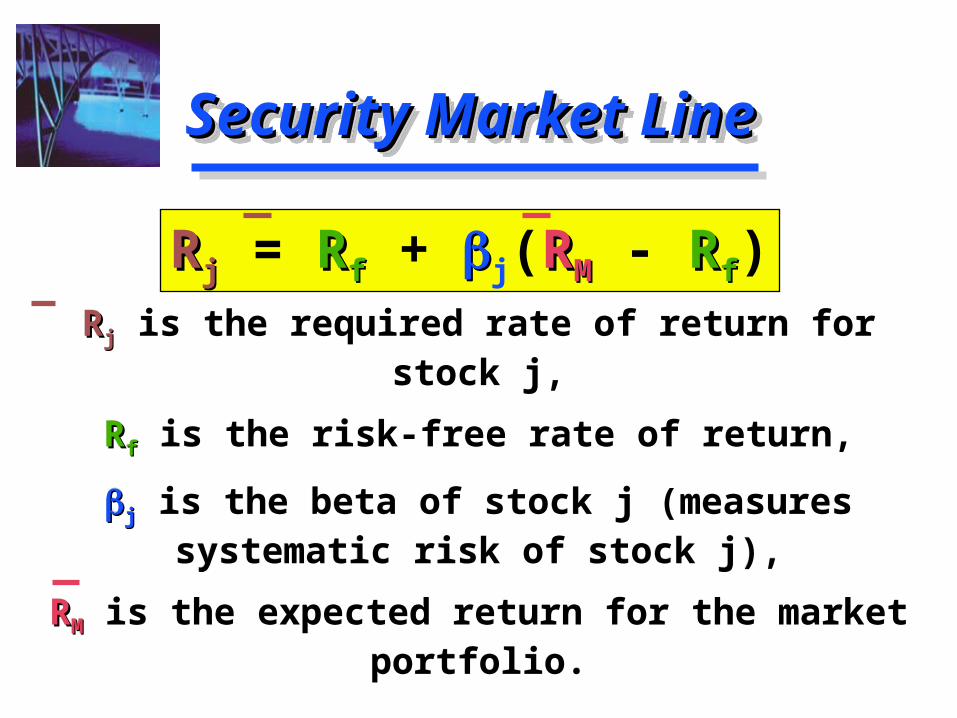

RRjj is the required rate of return for stock j,

RRff is the risk-free rate of return,

jj is the beta of stock j (measures systematic risk of stock j),

RRMM is the expected return for the market portfolio.

RRjj is the required rate of return for stock j,

RRff is the risk-free rate of return,

jj is the beta of stock j (measures systematic risk of stock j),

RRMM is the expected return for the market portfolio.

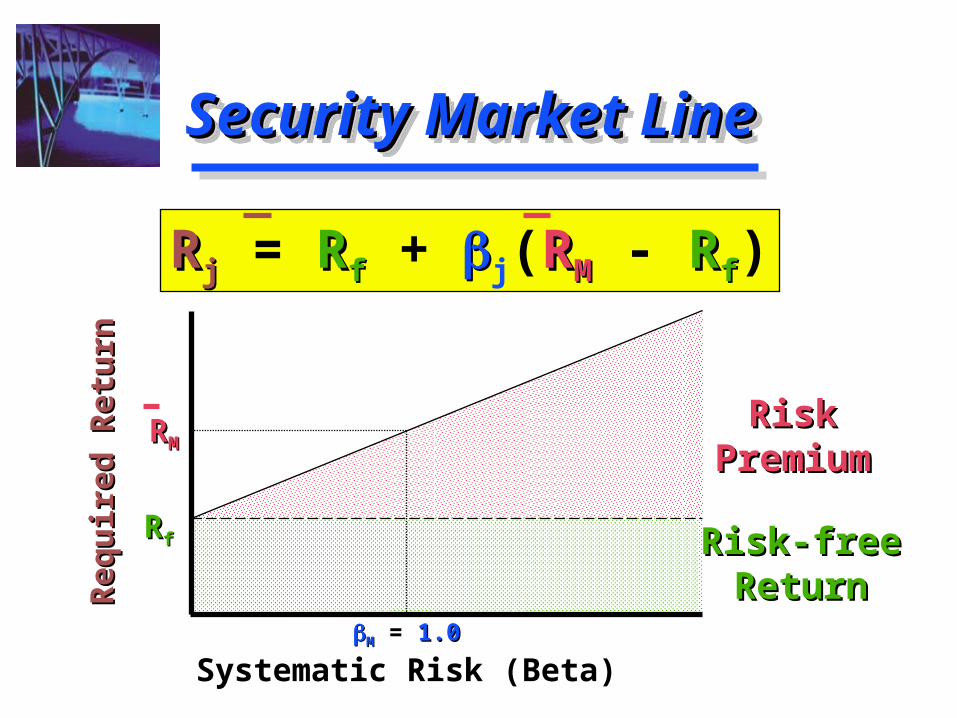

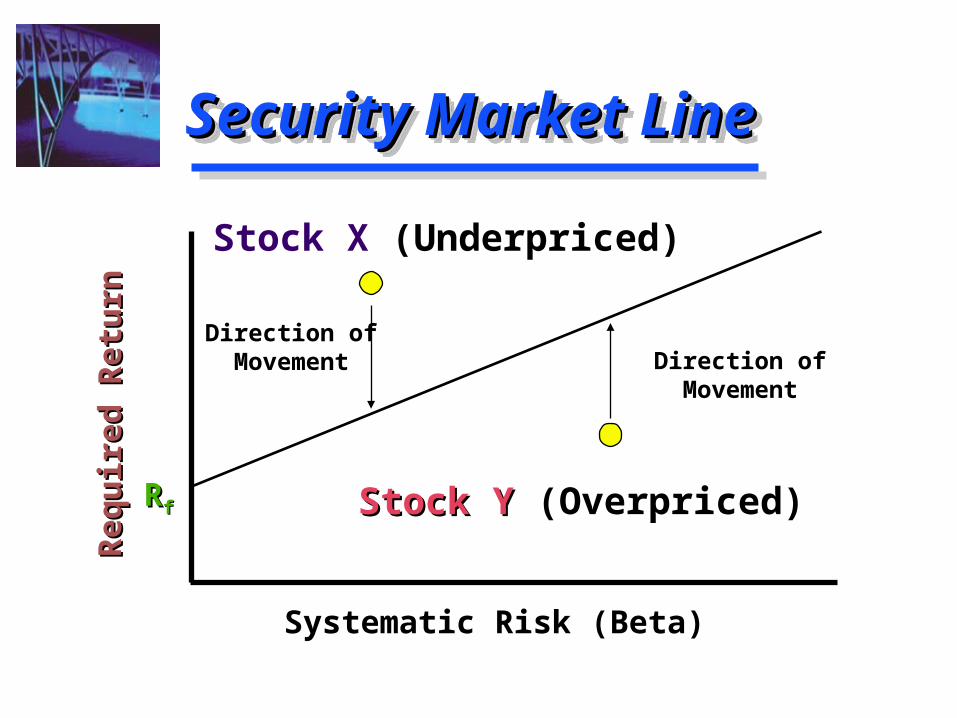

Security Market LineSecurity Market LineSecurity Market LineSecurity Market Line

RRjj = RRff + j(RRMM - RRff)

Security Market LineSecurity Market LineSecurity Market LineSecurity Market Line

RRjj = RRff + j(RRMM - RRff)

MM = 1.01.0

Systematic Risk (Beta)

RRff

RRMM

Req

uir

ed R

etu

rnR

equ

ired

Ret

urn

RiskRiskPremiumPremium

Risk-freeRisk-freeReturnReturn

Security Market LineSecurity Market LineSecurity Market LineSecurity Market Line

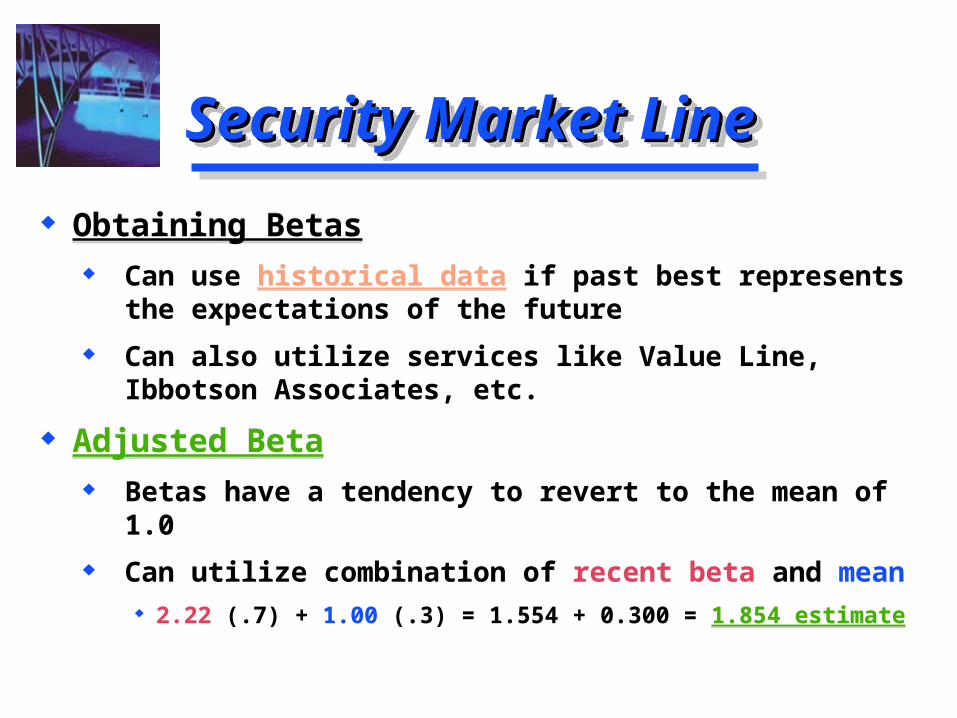

Obtaining Betas Can use historical data if past best represents the

expectations of the future

Can also utilize services like Value Line, Ibbotson Associates, etc.

Adjusted Beta Betas have a tendency to revert to the mean of 1.0

Can utilize combination of recent beta and mean 2.22 (.7) + 1.00 (.3) = 1.554 + 0.300 = 1.854 estimate

Obtaining Betas Can use historical data if past best represents the

expectations of the future

Can also utilize services like Value Line, Ibbotson Associates, etc.

Adjusted Beta Betas have a tendency to revert to the mean of 1.0

Can utilize combination of recent beta and mean 2.22 (.7) + 1.00 (.3) = 1.554 + 0.300 = 1.854 estimate

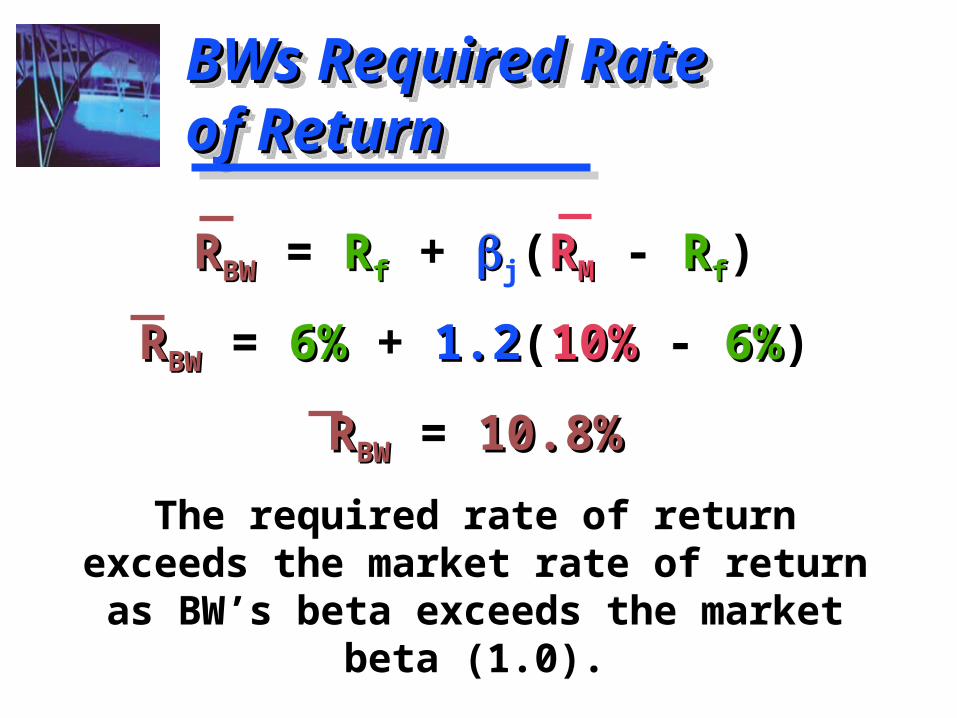

Lisa Miller at Basket Wonders is attempting to determine the rate of return required by their stock investors. Lisa is

using a 6% R6% Rff and a long-term market market

expected rate of return expected rate of return of 10%10%. A stock analyst following the firm has calculated

that the firm betabeta is 1.21.2. What is the required rate of returnrequired rate of return on the stock of

Basket Wonders?

Lisa Miller at Basket Wonders is attempting to determine the rate of return required by their stock investors. Lisa is

using a 6% R6% Rff and a long-term market market

expected rate of return expected rate of return of 10%10%. A stock analyst following the firm has calculated

that the firm betabeta is 1.21.2. What is the required rate of returnrequired rate of return on the stock of

Basket Wonders?

Determination of the Determination of the Required Rate of ReturnRequired Rate of ReturnDetermination of the Determination of the Required Rate of ReturnRequired Rate of Return

RRBWBW = RRff + j(RRMM - RRff)

RRBWBW = 6%6% + 1.21.2(10%10% - 6%6%)

RRBWBW = 10.8%10.8%

The required rate of return exceeds the market rate of return as BW’s

beta exceeds the market beta (1.0).

RRBWBW = RRff + j(RRMM - RRff)

RRBWBW = 6%6% + 1.21.2(10%10% - 6%6%)

RRBWBW = 10.8%10.8%

The required rate of return exceeds the market rate of return as BW’s

beta exceeds the market beta (1.0).

BWs Required BWs Required Rate of ReturnRate of ReturnBWs Required BWs Required Rate of ReturnRate of Return

Lisa Miller at BW is also attempting to determine the intrinsic value intrinsic value of the stock. She is using the constant growth model.

Lisa estimates that the dividend next period dividend next period will be $0.50$0.50 and that BW will growgrow at a

constant rate of 5.8%5.8%. The stock is currently selling for $15.

What is the intrinsic value intrinsic value of the stock? Is the stock overover or underpricedunderpriced?

Lisa Miller at BW is also attempting to determine the intrinsic value intrinsic value of the stock. She is using the constant growth model.

Lisa estimates that the dividend next period dividend next period will be $0.50$0.50 and that BW will growgrow at a

constant rate of 5.8%5.8%. The stock is currently selling for $15.

What is the intrinsic value intrinsic value of the stock? Is the stock overover or underpricedunderpriced?

Determination of the Determination of the Intrinsic Value of BWIntrinsic Value of BWDetermination of the Determination of the Intrinsic Value of BWIntrinsic Value of BW

The stock is OVERVALUED as the market price ($15) exceeds

the intrinsic value intrinsic value ($10$10).

The stock is OVERVALUED as the market price ($15) exceeds

the intrinsic value intrinsic value ($10$10).

Determination of the Determination of the Intrinsic Value of BWIntrinsic Value of BWDetermination of the Determination of the Intrinsic Value of BWIntrinsic Value of BW

$0.50$0.5010.8%10.8% - 5.8%5.8%

IntrinsicIntrinsicValueValue

=

= $10$10

Security Market LineSecurity Market LineSecurity Market LineSecurity Market Line

Systematic Risk (Beta)

RRff

Req

uir

ed R

etu

rnR

equ

ired

Ret

urn

Direction ofMovement

Direction ofMovement

Stock Y Stock Y (Overpriced)

Stock X (Underpriced)