Embed Size (px)

Citation preview

Financial management: lecture 10

Capital Structure Decision

MM propositions

Financial management: lecture 10

Today’s plan

Review what we have learned in the last lecture

The capital structure decision

• The capital structure without taxes• MM’s proposition 1

• MM’s proposition 2

• The capital structure with taxes• MM’s proposition 1

• MM’s proposition 2

Financial management: lecture 10

What have we learned in the last lecture

In the last lecture, we have discussed the case in the end of chapter 12, what have you learned from this case?

In the last lecture, we have also discussed three forms of market efficiency, what are they and what is your understanding of these three forms of market efficiency?

Financial management: lecture 10

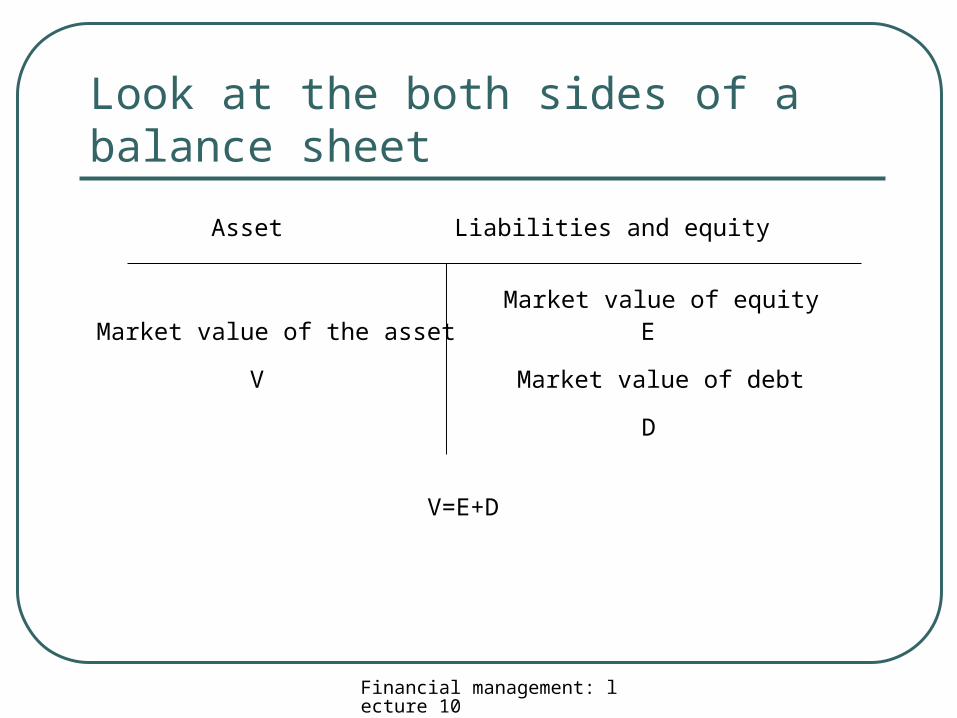

Look at the both sides of a balance sheet

Asset Liabilities and equity

Market value of the asset

V

Market value of equityE

Market value of debt

D

V=E+D

Financial management: lecture 10

Capital structure

Capital structure refers to the mix of debt and equity in a firm.

We often use D/E or D/V (V=D+E) to indicate the capital structure of a firm.• Usually, the higher the ratio, the more debt a firm has

The capital structure problem for a firm is to determine what is the maximum amount of debt a firm should have to maximize the firm’s value.

Financial management: lecture 10

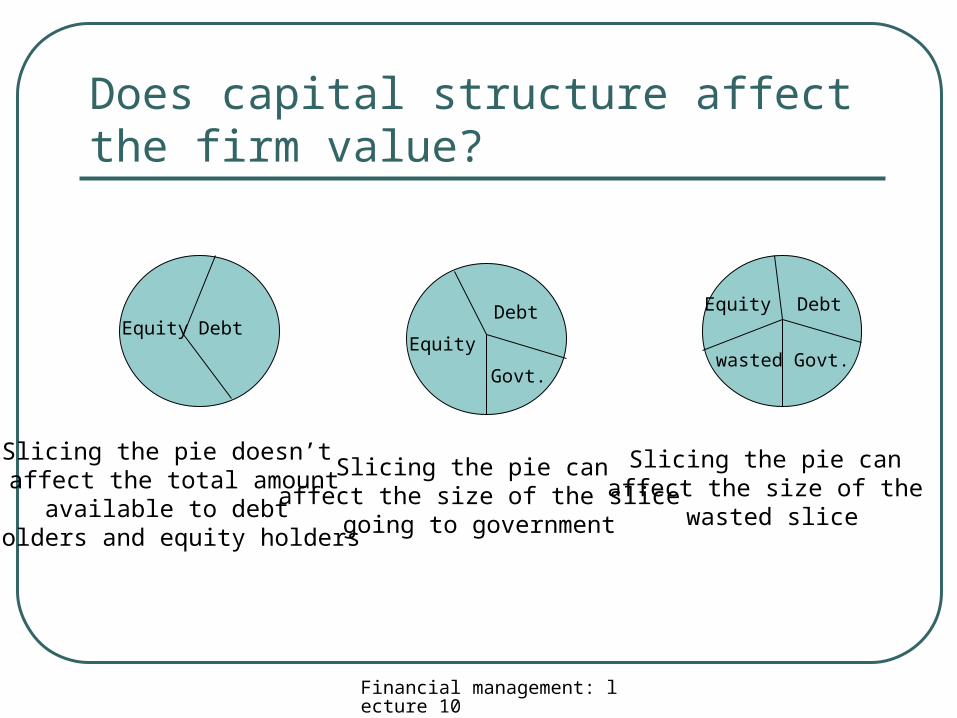

Does capital structure affect the firm value?

Equity DebtEquity

Equity

DebtDebt

Govt.Govt.

Slicing the pie doesn’t affect the total amount

available to debt holders and equity holders

Slicing the pie can affect the size of the slice

going to government

Slicing the pie can affect the size of the

wasted slice

wasted

Financial management: lecture 10

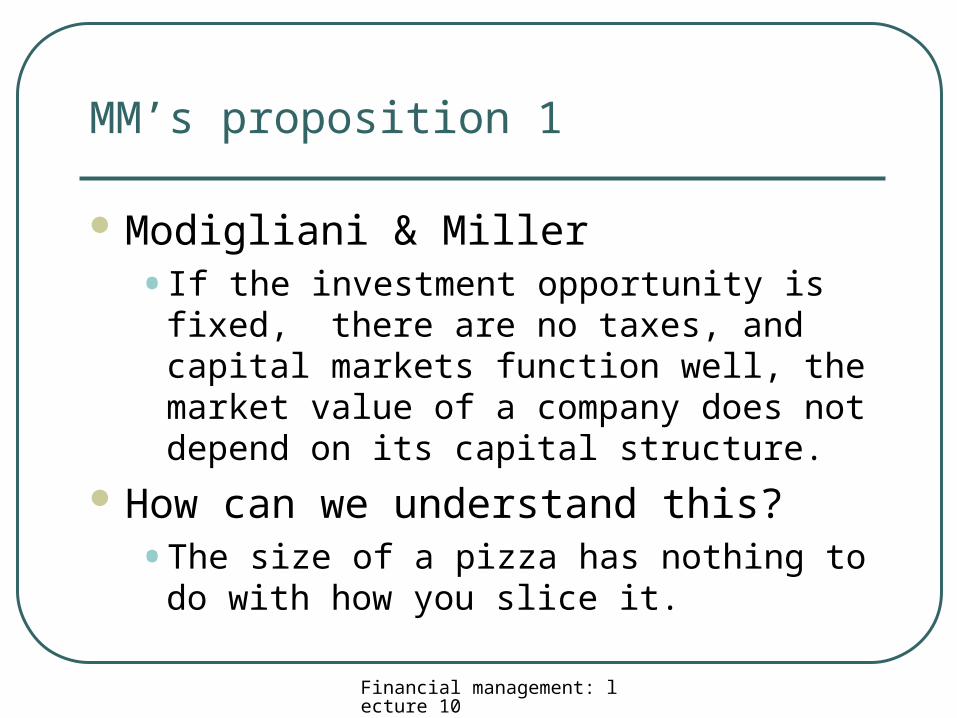

MM’s proposition 1

Modigliani & Miller• If the investment opportunity is fixed, there

are no taxes, and capital markets function well, the market value of a company does not depend on its capital structure.

How can we understand this?• The size of a pizza has nothing to do with

how you slice it.

Financial management: lecture 10

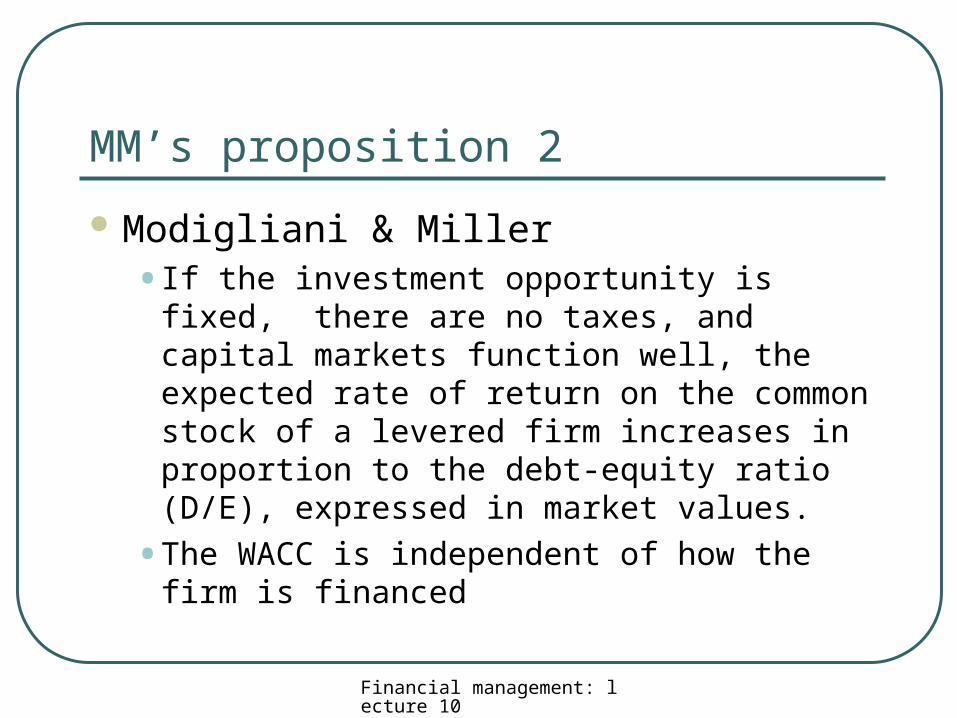

MM’s proposition 2

Modigliani & Miller• If the investment opportunity is fixed, there

are no taxes, and capital markets function well, the expected rate of return on the common stock of a levered firm increases in proportion to the debt-equity ratio (D/E), expressed in market values.

• The WACC is independent of how the firm is financed

Financial management: lecture 10

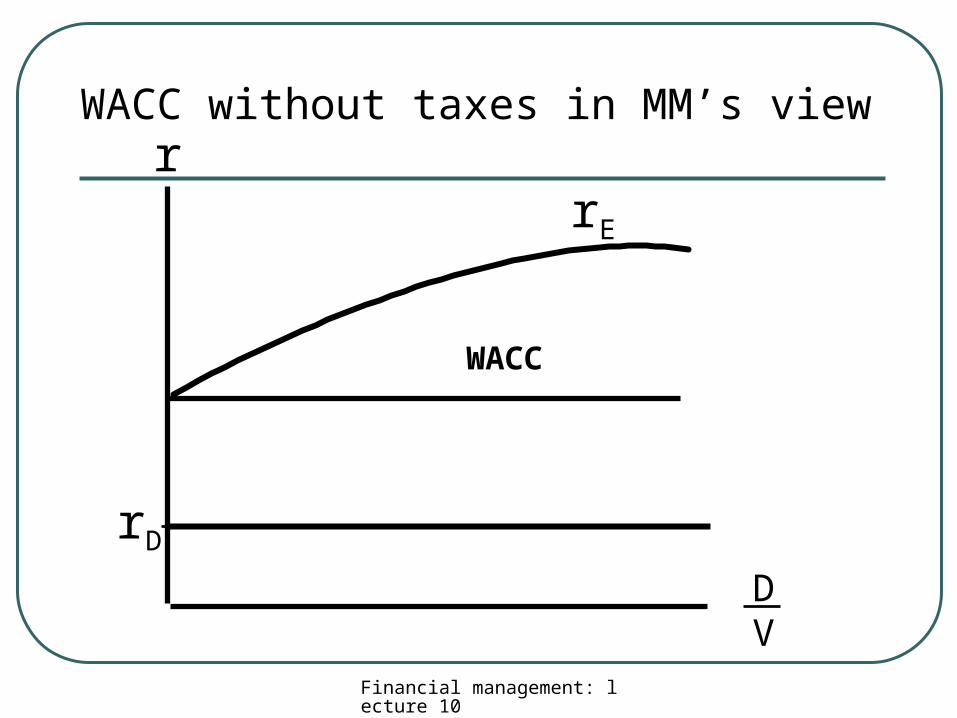

r

DV

rD

rE

WACC

WACC without taxes in MM’s view

Financial management: lecture 10

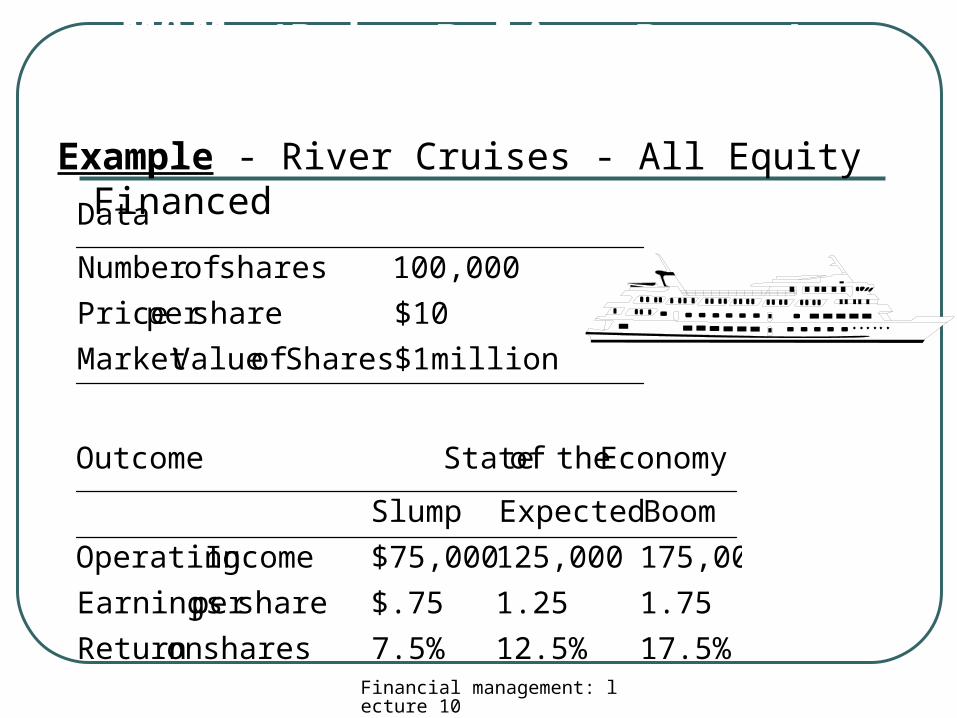

Example - River Cruises - All Equity Financed

17.5%12.5%7.5% shares on Return

1.751.25$.75shareper Earnings

175,000125,000$75,000Income Operating

BoomExpectedSlump

Economy theof State Outcome

million 1 $Shares of ValueMarket

$10shareper Price

100,000shares ofNumber

Data

M&M (Debt Policy Doesn’t Matter)

Financial management: lecture 10

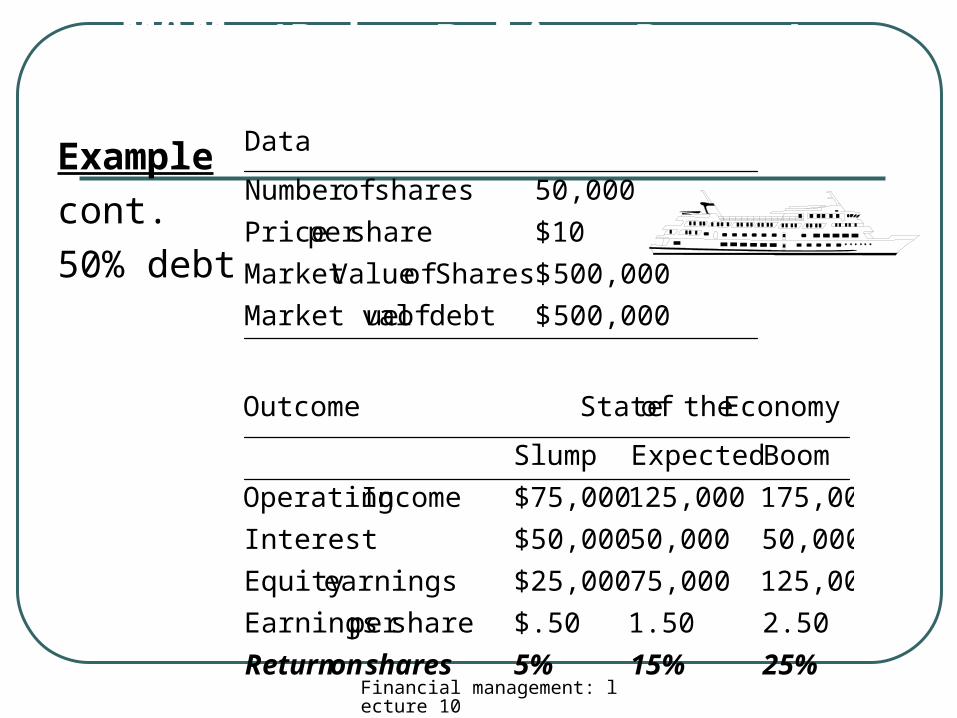

Example

cont.

50% debt

25%15%5% shares on Return

2.501.50$.50shareper Earnings

125,00075,000$25,000earningsEquity

50,00050,000$50,000Interest

175,000125,000$75,000Income Operating

BoomExpectedSlump

Economy theof State Outcome

500,000 $debt of ueMarket val

500,000 $Shares of ValueMarket

$10shareper Price

50,000shares ofNumber

Data

M&M (Debt Policy Doesn’t Matter)

Financial management: lecture 10

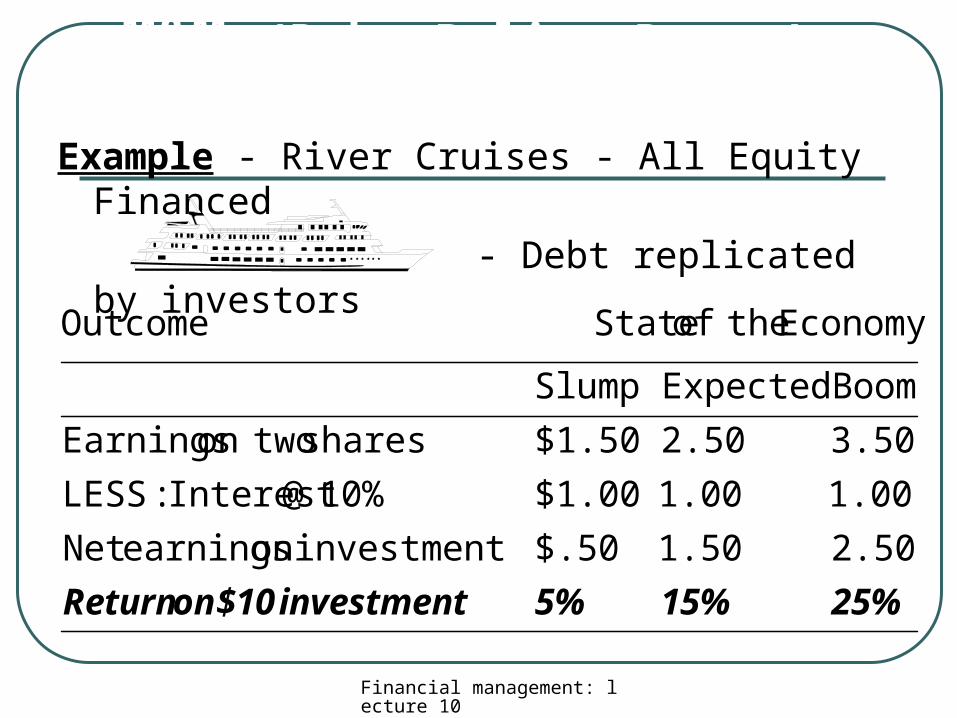

Example - River Cruises - All Equity Financed

- Debt replicated by investors

25%15%5% investment$10 on Return

2.501.50$.50investment on earningsNet

1.001.00$1.0010% @Interest :LESS

3.502.50$1.50shares twoon Earnings

BoomExpectedSlump

Economy theof State Outcome

M&M (Debt Policy Doesn’t Matter)

Financial management: lecture 10

The use of debt has a lot of implications:• Financial risk- The use of debt will increase the risk to

share holders and thus Increase the variability of shareholder returns.

• Interest tax shield- The savings resulting from deductibility of interest payments.

Capital structure and Corporate Taxes

Financial management: lecture 10

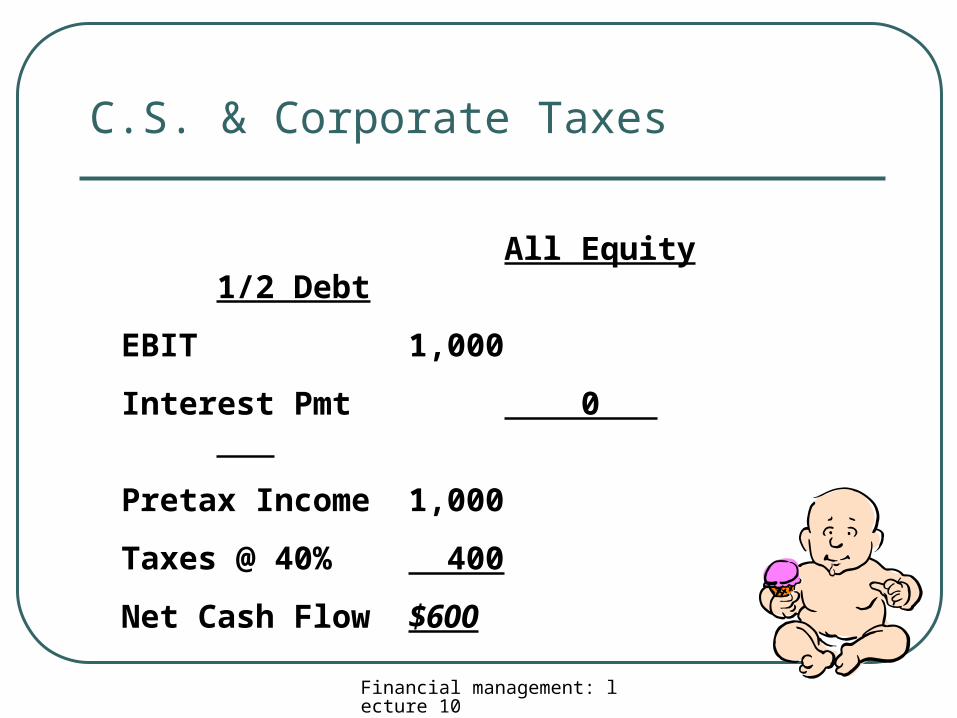

You own all the equity of Space Babies Diaper Co.. The company has no debt. The company’s annual cash flow is $1,000, before interest and taxes. The corporate tax rate is 40%. You have the option to exchange 1/2 of your equity position for 10% bonds with a face value of $1,000.

Should you do this and why?

An example on Tax shield

Financial management: lecture 10

All Equity 1/2 Debt

EBIT 1,000

Interest Pmt 0

Pretax Income 1,000

Taxes @ 40% 400

Net Cash Flow $600

C.S. & Corporate Taxes

Financial management: lecture 10

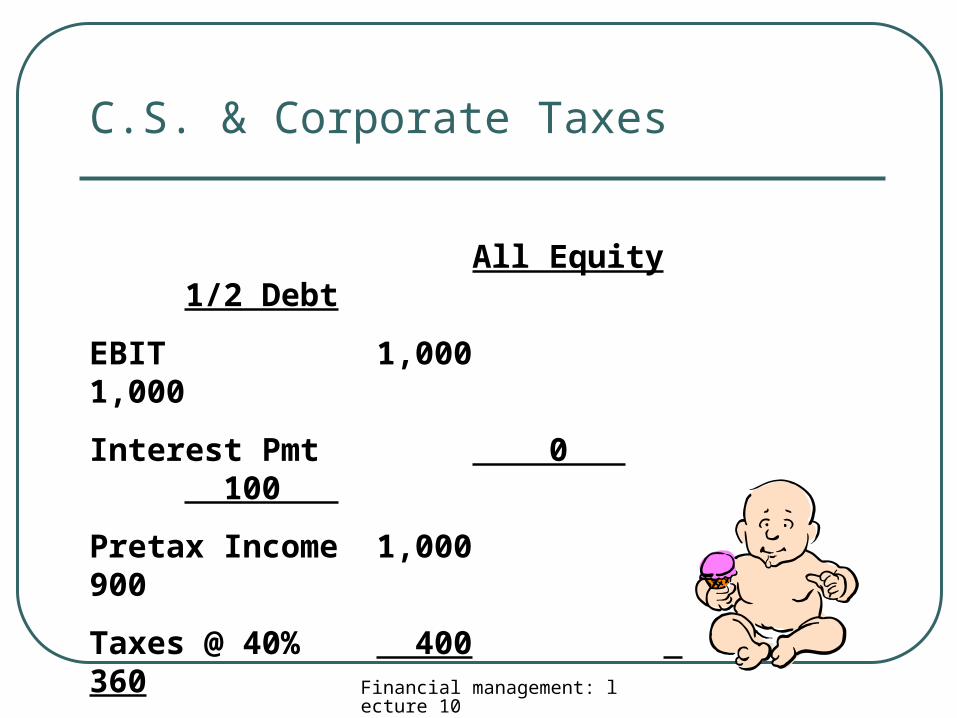

All Equity 1/2 Debt

EBIT 1,000 1,000

Interest Pmt 0 100

Pretax Income 1,000 900

Taxes @ 40% 400 360

Net Cash Flow $600 $540

C.S. & Corporate Taxes

Financial management: lecture 10

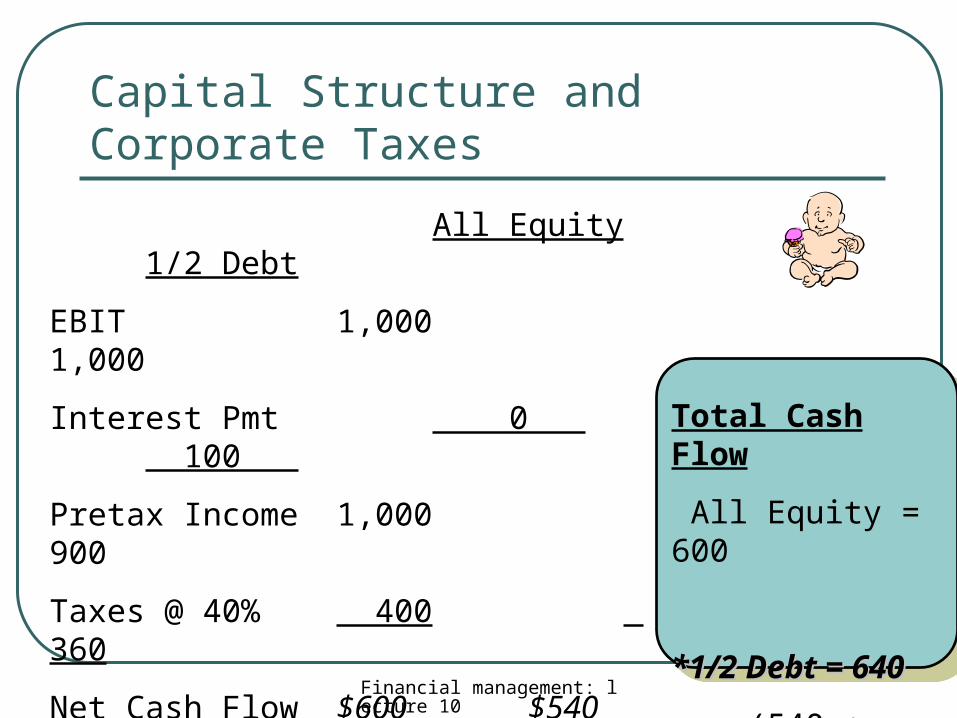

Capital Structure and Corporate Taxes

All Equity 1/2 Debt

EBIT 1,000 1,000

Interest Pmt 0 100

Pretax Income 1,000 900

Taxes @ 40% 400 360

Net Cash Flow $600 $540

Total Cash Flow

All Equity = 600

*1/2 Debt = 640*1/2 Debt = 640

(540 + 100)

Financial management: lecture 10

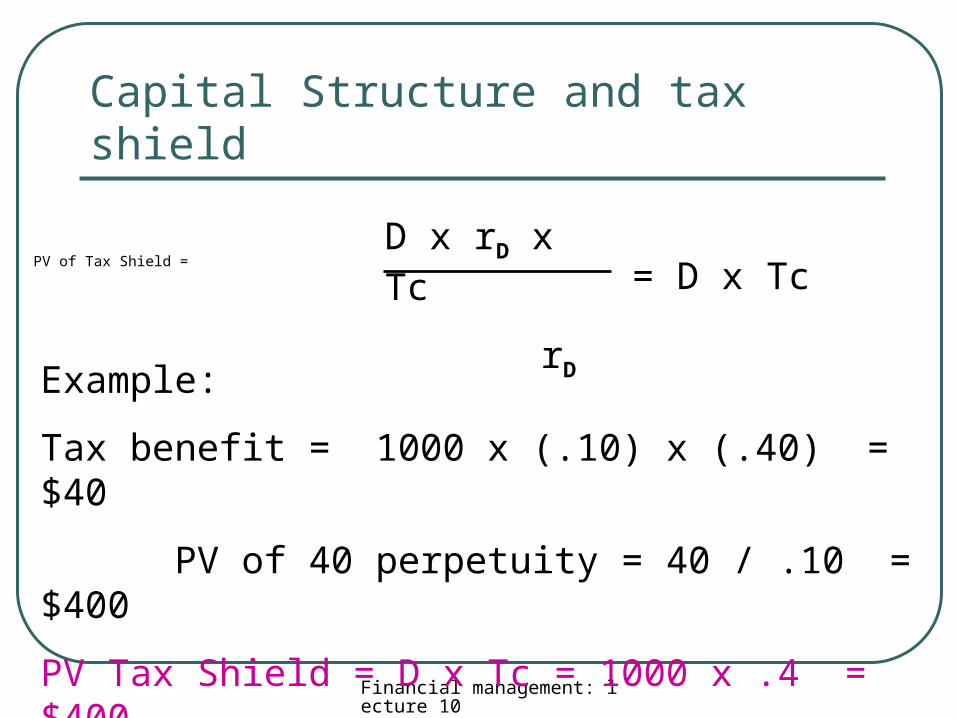

Capital Structure and tax shield

PV of Tax Shield =

D x rD x Tc

rD

= D x Tc

Example:

Tax benefit = 1000 x (.10) x (.40) = $40

PV of 40 perpetuity = 40 / .10 = $400

PV Tax Shield = D x Tc = 1000 x .4 = $400

Financial management: lecture 10

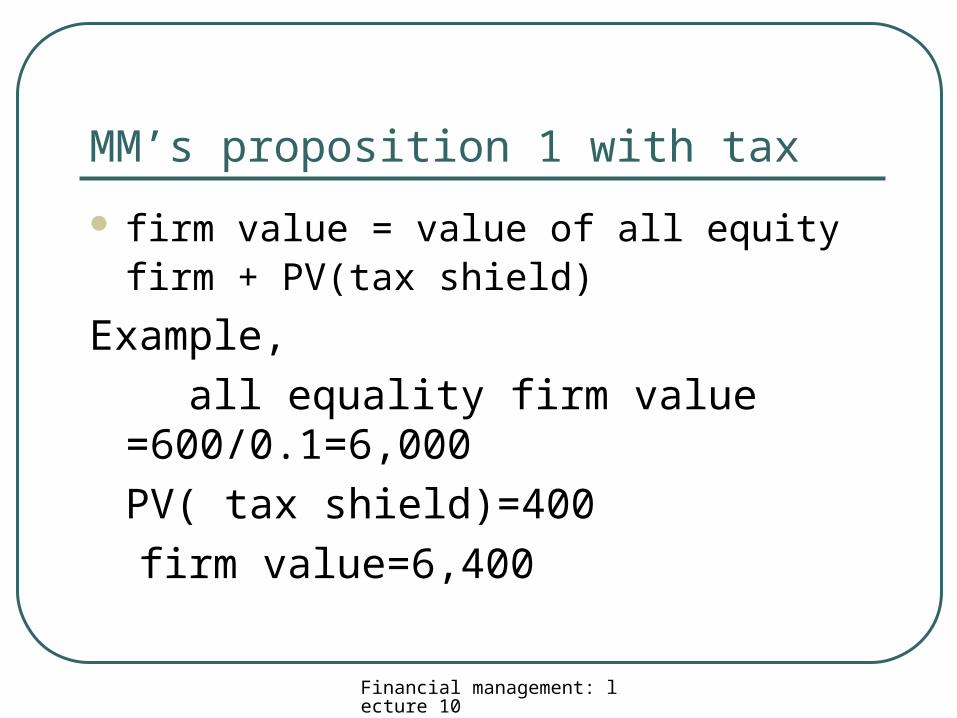

MM’s proposition 1 with tax

firm value = value of all equity firm + PV(tax shield)

Example,

all equality firm value =600/0.1=6,000

PV( tax shield)=400

firm value=6,400

Financial management: lecture 10

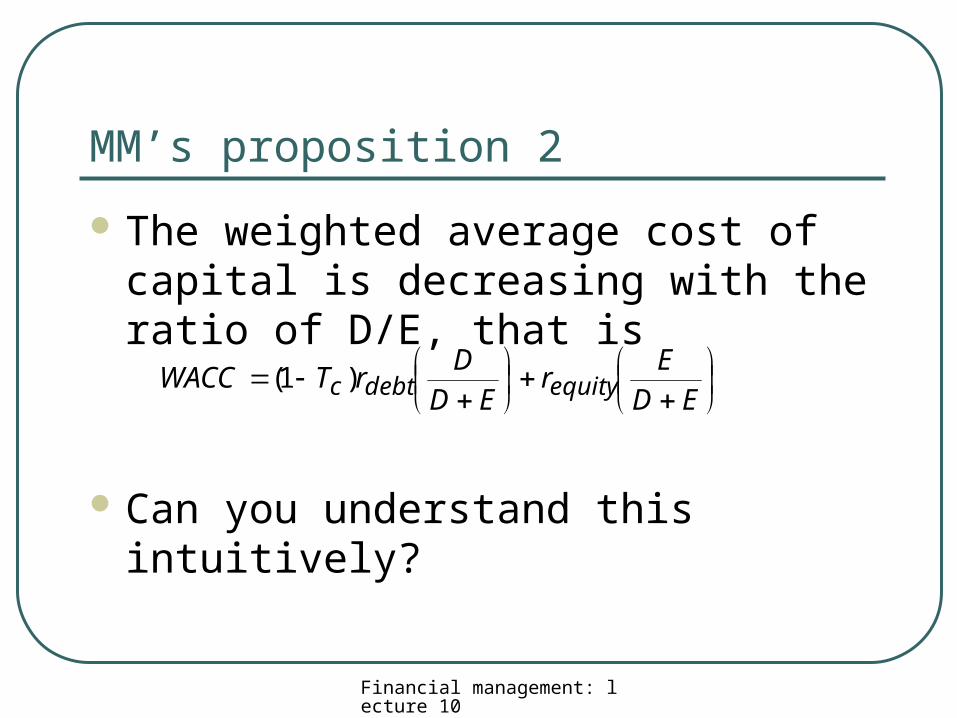

MM’s proposition 2

The weighted average cost of capital is decreasing with the ratio of D/E, that is

Can you understand this intuitively?

ED

Er

ED

DrTWACC equitydebtc )1(

Financial management: lecture 10

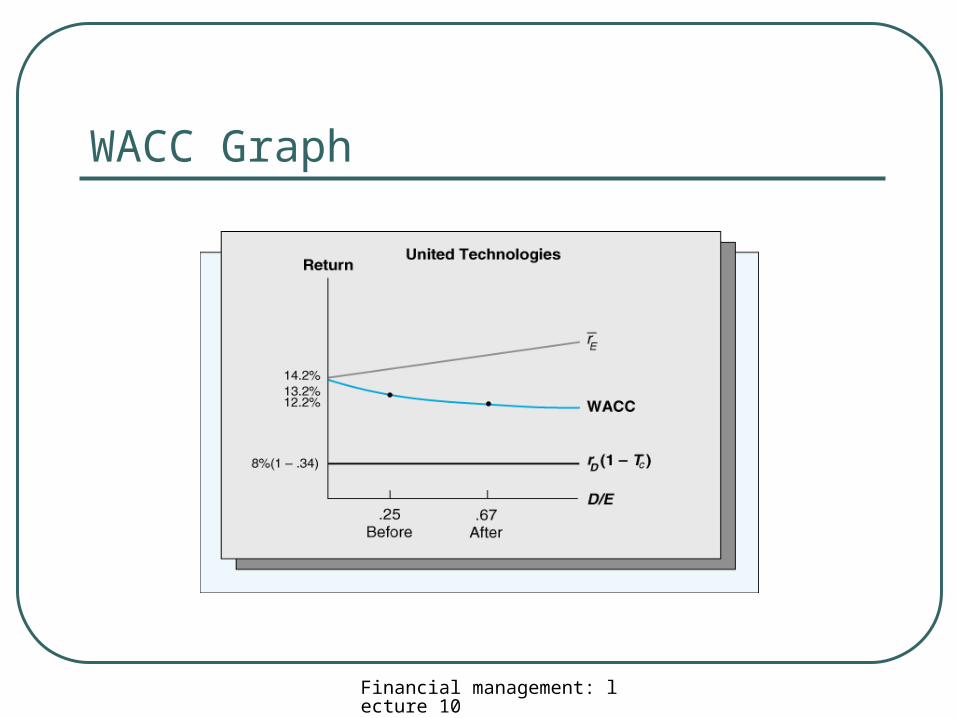

WACC Graph

Financial management: lecture 10

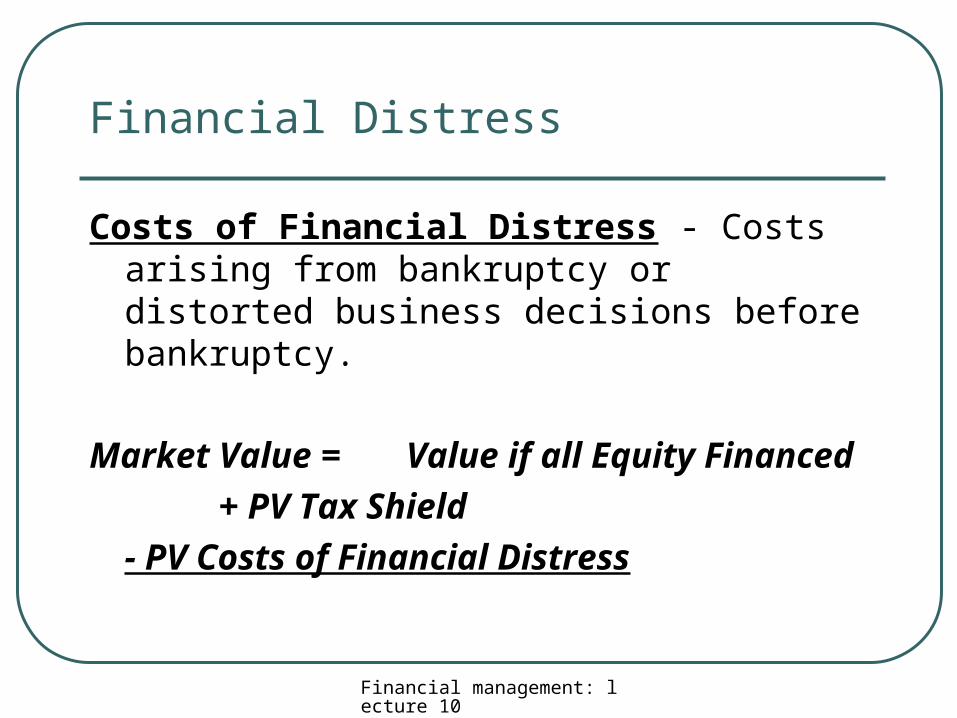

Financial Distress

Costs of Financial Distress - Costs arising from bankruptcy or distorted business decisions before bankruptcy.

Market Value = Value if all Equity Financed

+ PV Tax Shield

- PV Costs of Financial Distress

Financial management: lecture 10

Financial distress

Costs of Financial Distress - Costs arising from bankruptcy or distorted business decisions before bankruptcy.

Market Value = Value if all Equity Financed

+ PV Tax Shield

- PV Costs of Financial Distress

Financial management: lecture 10

Optimal Capital structure

Trade-off Theory - Theory that capital structure is based on a trade-off between tax savings and distress costs of debt.

Pecking Order Theory - Theory stating that firms prefer to issue debt rather than equity if internal finance is insufficient.

Financial management: lecture 10

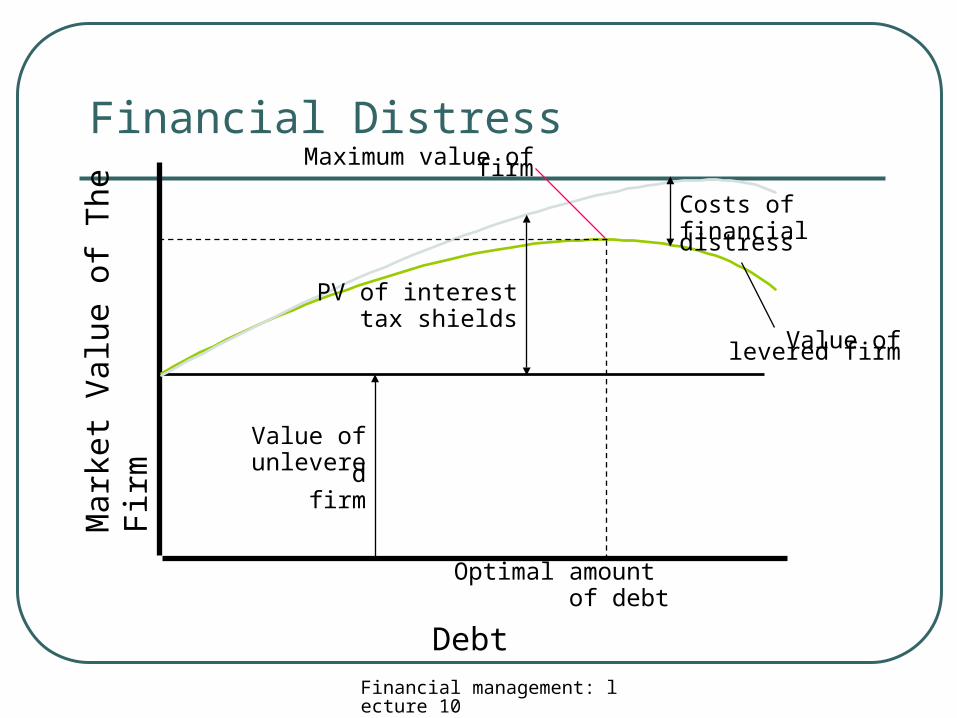

Financial Distress

Debt

Mar

ket V

alue

of

The

Fir

m

Value ofunlevered

firm

PV of interesttax shields

Costs offinancial distress

Value of levered firm

Optimal amount of debt

Maximum value of firm