-

7/28/2019 Final M & A

1/40

1

The Tata Group

A Legacy of Trust Tata is Indias largest and most diversified

business conglomerate

with more than 100 operating companies spread across 85

countries in six different

continents, employing 350,000 people and generating revenue of

US$ 70.8 billion as of

FY 2009. The group's global business operations are spread over

seven business

sectors: communications and information technology, engineering,

materials, services,

energy, consumer products and chemicals.

Tata companies share five core values integrity,

understanding, excellence, unity and responsibility.

Each Tata company agrees to the Tata Code of

Conduct by signing the TATA Brand Equity and

Business Promotion Agreement with Tata Sons

Ltd. This ensures adherence to the Tata ethos and

value system. Adherence to ethics and excellence

and the commitment towards serving communities

have been at the core of Tatas unblemished

growth and sustenance for over 140 years. This

heritage evokes trust and goodwill among

consumers, employees, shareholders and the

larger community. Today, the Tata name is a unique asset

representing Leadership

with Trust. This legacy has earned the admiration of the groups

stakeholders in a

manner few business houses can even hope to match.

Tata Group is one of India's largest and most respected business

groups. Tata Group's

name is synonymous with India's industrialisation. The Group

gave India her first steel

plant, hydro-electric plant, inorganic chemistry plant and

created a reservoir of scientific

and technological manpower for the country. Its Trusts have

instituted the Tata Institute

of Social Sciences in 1936; India's first cancer hospital, the

Tata Memorial in 1941, and

in 1945, the Tata Institute of Fundamental Research, which

became the cradle of India's

Atomic energy program. Today, Tata Group comprises 96 operating

companies in

-

7/28/2019 Final M & A

2/40

2

seven business sectors: information systems and communications;

engineering;

materials; services; energy; consumer products; and chemicals.

The Group has

operations in more than 54 countries across six continents, and

its companies export

products and services to 120 nations.

Jamsetji Nusserwanji Tata laid the foundations of Tata Group

when he started a private

trading firm in 1868. In 1874, he set up the Central India

Spinning Weaving and

Manufacturing Company Limited and thus marked the Group's entry

into textiles. In

1887, Jamsetji Tata formed a partnership firm, Tata & Sons,

with his elder son Sir

Dorabji Tata and his cousin Ratanji Dadabhoy Tata. His younger

son Sir Ratan Tata

joined the firm in 1896. In 1902, the Indian Hotels Company was

incorporated to set up

the Taj Mahal Palace and Tower, India's first luxury hotel,

which opened in 1903. TheTata Iron and Steel Company (now known as

Tata Steel) was established to set up

India's first iron and steel plant in Jamshedpur.

The plant started production in 1912. In 1910, Tata

Hydro-Electric Power Supply

Company, (now Tata Power) was set up. In 1917, Tata Oil Mills

Company was

established to make soaps, detergents and cooking oils. In 1932,

Tatas entered aviation

sector with the establishment of Tata Airlines. In 1939, Tata

Chemicals, presently, the

largest producer of soda ash in India, was established. In 1945,

Tata Engineering and

Locomotive Company (renamed Tata Motors in 2003) was established

to manufacture

locomotive and engineering products. In 1954, India's major

marketing, engineering and

manufacturing organisation, Voltas, was established. In 1962,

Tata Finlay (now Tata

Tea), one of the largest tea producers, was

established.

In 1968, Tata Consultancy Services (TCS), India's

first software services company, was established

as a division of Tata Sons. In 1970, Tata McGraw-

Hill Publishing Company was created to publish

educational and technical books. In 1984, Titan

Industries, a joint venture between the Tata Group

-

7/28/2019 Final M & A

3/40

3

and the Tamil Nadu Industrial Development Corporation (TIDCO),

was set up to

manufacture watches. In 1996, Tata Teleservices (TTSL) was

established to lead the

Group's foray into the telecom sector. In 1998, Tata Indica,

India's first indigenously

designed and manufactured car, was launched by Tata Motors. In

2000, Tata Tea

acquired the Tetley Group, UK. This was the first major

acquisition of an international

brand by an Indian business group. In 2001, Tata entered into

insurance business in

joint venture with Tata AIG. In 2007, Tata Steel acquired Corus

the fifth largest steel

company in the world.

Tata Group Companies

The two Promoter companies of Tata Group are: Tata Sons and Tata

Industries. TataSons is the promoter of all key companies of the

Tata Group and holds the bulk of

shareholding in these companies. Tata Sons is the owner of the

Tata name and the

Tata trademark, which are registered in India and several other

countries. Tata

Industries was set up by Tata Sons in 1945 as a managing agency

for businesses it

promoted. Tata Industries' mandate was recast, in the early

1980s, to promote the

Group's entry into new and high-tech areas. The rest of the Tata

companies spread

over seven sectors in which Tata Group operates are:

1. Engineering

(a) Automotive:

Tata AutoComp Systems Subsidiaries / associates / joint

ventures: Automotive

Composite Systems International, Automotive Stampings and

Assemblies, Knorr

Bremse Systems for Commercial Vehicles, TACO Engineering, TACO

Faurecia

Design Centre, TACO Hendrickson Suspension Systems, TACO

Interiors and

Plastics Division, TacoKunststofftechnik, TACO MobiApps

Telematics, TACO

Supply Chain Management, TACO Tooling, TACO Visteon Engineering

Center,

Tata Ficosa Automotive Systems, Tata Johnson Controls

Automotive, Tata Toyo

Radiator, Tata Yazaki AutoComp, TC Springs, Technical Stampings

Automotive

-

7/28/2019 Final M & A

4/40

4

Tata Motors Subsidiaries / associates / joint ventures: Concorde

Motors, HV

Axels, HV Transmissions, Nita Company, TAL Manufacturing

Solutions, Tata

Cummins, Tata Daewoo Commercial Vehicles Company, Tata

Engineering

Services, Tata Precision Industries, Tata Technologies, Telco

Construction

Equipment Company

(b) Engineering Services

Tata Projects

TCE Consulting Engineers

Voltas

(c) Engineering Products

TAL Manufacturing Solutions

Telco Construction Equipment Company

TRF

2.Materials:

(a) Composites

Tata Advanced Materials

(b) Metals

Tata_steel

Subsidiaries / associates / joint ventures: Hooghly Met Coke and

Power

Company, Jamshedpur Injection Powder (Jamipol), Lanka Special

Steel,

mjunction services, NatSteel, Sila Eastern Company, Tata

Metaliks, TataPigments, Tata Ryerson, Tata Sponge Iron, Tata

Refractories, Tayo Rolls, The

Indian Steel and Wire Products, The Tinplate Company of India,

TM International

Logistics, Wires Division.

-

7/28/2019 Final M & A

5/40

5

3.Energy

(a) Power

Tata BP Solar India

Tata PowerSubsidiaries / associates / joint ventures: Tata

Ceramics, Tata Power

Trading, North Delhi Power Limited

(b) Oil & Gas

Tata Petrodyne

4. Chemicals

Rallis India

Tata Chemicals

Tata Pigments

5.Services

(a) Hotels and Realty

Indian Hotels (Taj group) Subsidiaries / associates / joint

ventures: Taj Air , Roots

Corporation (Ginger Hotels)

THDC

(b) Financial Services

Tata AIG General Insurance

Tata AIG Life Insurance

Tata Asset Management

Tata Financial Services

Tata Investment Corporation

-

7/28/2019 Final M & A

6/40

6

(c) Other Services

Tata Quality Management Services

Tata Services

Tata Strategic Management Group

6. Consumer Products

Infiniti Retail

Tata Tea Subsidiaries / associates / joint ventures: Tetley

Group, Tata Coffee,

Tata Tetley, Tata Tea Inc

Tata Ceramics

Tata McGraw Hill Publishing Company

Titan Industries

Trent

7.Information systems and communication

(a) Information Systems

Nelito Systems Tata Consultancy Services: Subsidiaries /

associates / joint ventures:

APONLINE, Airline Financial Support Services, Aviation Software

Development

Consultancy, CMC, CMC Americas Inc, Conscripti, HOTV, Tata

America

International Corporation, WTI Advanced Technology

Tata Elxsi

SerWizSol

Tata Interactive Systems

Tata Technologies

(b) Communications

Tata Sky

Tata Teleservices

-

7/28/2019 Final M & A

7/40

7

Subsidiaries / associates / joint ventures: Tata Teleservices

(Maharashtra), Tata

Internet Services

VSNL

Tatanet

(c) Industrial Automation

Nelco

Subsidiaries / associates / joint ventures: Tatanet

-

7/28/2019 Final M & A

8/40

8

Case 1: TATA Corus Deal

Summary

Background to the Acquisition

Tata Steel- A Background:

Tata Steel Limited the flagship company of Tata Group is the

largest manufacturer of

steel in India with 25.6 million tonnes of steel capacity. The

company produces HR and

CR coils and sheets, galvanized sheets, tubes, wire rods,

construction reban, rings and

bearings.

Corus Plc Ltd- A Background:

Corus (as of 2007) was Europe's second largest steel producer

with annual revenues of

Rs. 82,674 crores (59.7 billion) and crude steel production of

18.3 million tonnes in 2006.

Corps had a presence in nearly 50 countries, including its

global network of offices and

service centers. Corus was formed on October 6, 1999. Corus'

main steelmaking

operations were located in the UK and the Netherlands with other

plants located in

Germany, Norway and Belgium.

Deal origination:

Tata Steel (part of the Tata Group) acquired the Anglo-Dutch

steel firm Corus after a four

month bidding war with Brazil's CSN (Companhia Sidcrurgica

Nacional) for US $13.75

billion (Rs. 52.(0) crores) - this was the biggest acquisition

by an Indian firm. Tata's

acquisition of Corus made it the fifth largest global steel

producer with an annual capacity

to produce 25 million tons of steel. The acquisition was

intended to give Tata Steel access

to European markets and to achieve potential synergies in the

areas of manufacturing,

procurement. R&D, logistics and back-office operations.

Analysts claimed that the

acquisition price at 608 pence per share was substantially

higher than an earlier offer of

455 pence per share. Additionally, analysts felt that it would

take several years for

potential production and operational synergies to materialize

that would yield significant

cost savings. Following the acquisition Tata Steels stock

suffered a significant decline in

-

7/28/2019 Final M & A

9/40

9

price causing Standard & Poor's to place it on a credit

watch list with negative

implications.

Tata acquired Corus on the 2nd of April 2007 for a price of

$12.1 billion making the

Indian company the world's fifth largest steel producer. This

acquisition process has

started long back in the year 2005. This process started in the

year 2000 and with Tata it

came to an end. In 2005, when the deal was started the price per

share was 455 pence.

But during the time of acquisition held in 2007, the price per

share was 608 pence, which

is 33.6% higher than the first offer.

Tata maintained a low profile compared to CSN aggressive stance

which was part of the

overall tactical plan. It was started that when bidding began.

Arun Gandhi, the M&A whiz

of the group was stationed at the office of the groups lawyer on

Primrose Street, London

EC2A2HS, all night-with a motorcycle stationed kerbside, revved

up and ready to go in

case networks failed and email bids could not be sent. Each

bidder had to email his bid

during each round from his own solicitors office. The bidding

was to go on for nine

rounds, during which a minimum of 5 pence enhancement per share

was allowed over

the offer made by each party. In the ninth round, the parties

had to put in their final bids,

besides indicating the maximum amount they were willing to pay

in case theirs was the

lower bid. When Tata Steel bid 608 pence per share, their bid

was higher than the last

bid put in by CSN by 5 pence.

Valuation Perspective:

As per statistics of the IISI, in 2005, Corus annual production

was 18 million tons (mt),

while that of Tata Steel was at 5 mt. Corus turnover worked out

to $18 billion as

compared to Tata Steels $4.64 billion in FY 2006. The enterprise

value was placed at

$10 billion, including its outstanding debt. Brokerage house,

First Global, estimates that a

$50 fall in global steel prices could lead to a $414 million

loss from the acquisition in theFY 2008.

People often argued that Tata had paid a higher price than what

was paid for Arcelor.

The price earnings ratio (the number of times the price is paid

over the current years

earnings), at 14.8 times was also high. In case of Arcelor

Mittal deal, the acquisition price

-

7/28/2019 Final M & A

10/40

10

per ton worked out to $840 as against $750 paid by Tata for

Corus assets, even though

EV/EBITDA in the case of Tata Corus is higher at 7.6 as against

5.4 in Mittals case.

According to Chokseys estimates, the realization per ton in case

ofCorus is higher that

Tata Steel, at $866 per ton, which was four, times that of

Corus.

At 608 pence per share (which worked out to a price of 5.2

billion pound) the enterprise

value is seven times Corus EBITDA, as against a 5.4 times

payment of Mittal St eel for

acquiring Arcelor, Tata Steel paid nearly 7.6 times. The premium

was for consolidated

capacities.

Logic for Valuation:

According to Muthuraman, Tata Steel MD, the strategic objective

of the deal is that it

brings to Tata Steel 19 million tone capacities at once, at a

cost which is roughly a little

more than half the cost of Greenfield sites. It also gives the

company access to mature

and developed markets of Europe. Moreover, Corus also has highly

developed R&D

capabilities. Corus, which has multi-location plants, is not a

fully integrated steel

company. Unlike the Tata, who have their own coal mines and

captive source of iron ore.

Corus has to source its raw materials from the global markets.

The higher the value

added, wider the speciality product range that Corus can add to

the Tatas product range.

The Tata Group, which had embarked upon a major expansion spree

by setting up

Greenfield projects, is looking at exporting a part of the

semi-finished products from these

capacities to Corus, which would bring down costs

considerably.

Riding the steel cycle boom, beginning in 2003, its cash flow

from operations crossed Rs.

6000 crore in both FY 2005 and FY 2006. With profits of over

$840 million, Tata Steel

was the groups most profitable, company, even ahead of its high

profile TCS, in FY 2005.

-

7/28/2019 Final M & A

11/40

11

Q: 1 what are the strategic reasons for the TATA Corus deal?

A key objective for Tata Steel in this acquisition was gaining

finishing expertise in

European markets, where it could export semi-finished steel from

its plants in India. It

could also shift part of the steel-making capacities to India,

where it was alreadyplanning a massive expansion.

Tata Steel had a number of things to consider in negotiating a

deal for Corus. First of

all, Tata Steel could not make an all cash offer and assume the

assets and liabilities of

Corus on its balance sheet because of the sheer size. Second,

both companies had to

convince their shareholders about the strategic and financial

benefits to the companies.

Shareholders would be concerned about the size of the premium

and the potential

dilution in earnings per share.

Tata Steel goes for Acquisition for the following strategic

reasons:

The cash cost of Tata Steel is around $160 per tonne. I believe

that the cost at Port

Talbot (where Corus has a plant) is perhaps roughly twice of

that. Between the two

teams, we see potential for significant synergies in the area of

manufacturing, in shared

services, in logistics, in the marketplace, sharing best

practices. We do see significant

synergies and a possibility of cost reduction.

In this world of consolidation and growing in size, both in

geography and in size, Tata

Steel has been planning its long-term strategy.

4 Million tone to 30+ Million tone:

Tata Steels strategy, in terms of what it wanted to do over a

period of time of 10 years,

between 2002-03 and 2015, was to grow from four million tonnes

per annum, which

were at that time, to about 30 million tonnes plus, beyond the

shores of India,

multinational, and continuing to be in a low-cost position and

continuing to be EVA

positive. That strategy had six elements. One of them was that

TATA would build a

strong base in India, that is why they are expanding Jamshedpur

from five to 10 million,

and were building three greenfield projects.

-

7/28/2019 Final M & A

12/40

12

De-integration:

The second part of the strategy was that they adopt a

de-integrated strategy where they

believed that the world steel industry, over the last 150 years

or so, had adopted a

certain model of making from iron to finished steel in one

location, irrespective of wherethe raw materials were. TATA always

believed that this model will change, because

steel has to compete with other materials and, for the

sustainable competitiveness of

steel, it is necessary that this business model will undergo a

change. TATA wanted to

be at the forefront of that change in business model, so they

would look for private

steelmaking in countries which are rich in iron ore and coal or

gas. So TATA thought of

plants in India, Bangladesh, and Iran.

Material security:

The third part of the strategy was raw material security. Its

important that TATA have

raw material security to be competitive and sustainable in this

world. We have raw

material security on a 100per cent basis for their existing

operations in Jamshedpur.

TATA have a large extent of self-sufficiency for coal. Each of

their three greenfield

projects in India will carry with it raw material iron ore

security. TATA have some

strategic types and some strategic positions in terms of coal

and limestone beyond the

shores of India. They said: we should continue to look for raw

material security, both in

India and overseas.

Going downstream:

The next part of strategy was getting more out of steel, which

is by branding, by going

downstream, by positioning the products, getting into

construction solutions and so on.

It is with that aim they people formed the joint venture with

BlueScope. It is with that

strategy that they started having a joint venture with Ryerson

of the US, for goingdownstream into processed materials.

Logistics control:

The next part of the strategy was control over logistics. No

large company no large

steel company can be sustainable competitive over a period of

time without some

-

7/28/2019 Final M & A

13/40

13

control on the efficiency and costs of logistics, so we decided

to build a port in Orissa to

connect Indian operations with our overseas operations. TATA

decided to start a

shipping company with NYK of Japan, and these are all in

progress. Acquisition of

Corus and our partner in Corus to form a joint entity is part of

this strategy.

Indeed there was very little shared territory in the markets the

companies served. Tata

Steel had a strong position in India, Singapore, Thailand and

other parts of Asia

whereas Corus had a strong presence in Europe.

Q: 2 discuss the Valuation aspects involved in the deal.

Financing India's largest leveraged buyout comprised of a $3.88

billion equity

contribution from Tata Steel, a fully underwritten non-recourse

debt package of $5.63

billion, and a revolving credit facility of $669 million.

Date TATA Bid CNS Bid

October 20, 2006 455 pence (4.3 billion pound) -

November 17, 2006 - 475 pence

December 11, 2006 4.7 billion pound -

January 31, 2007 - 515 pence

Higher than 608 pence (5.2 billion

pound)

-

Tata Steel UK would offer a price of 455 pence per Corus share

valuing Corus at 4.3b

($8.04b). This price represented a multiple of 7.9 times the

EBITDA of Corus from

continuing operations for the twelve months to July 1, 2006. The

acquisition was to be

structured as a 100 percent leveraged buyout funded through cash

resources and loans

raised by Tata Steel and the SPV. Under the plan Tata Steel UK

would arrange a loan

of 1.6 b ($3056m), a revolving credit facility and a bridge loan

and the rest would come

from Tata Steel (to the SPV).

-

7/28/2019 Final M & A

14/40

14

Valuation Perspective:

Particular Corus TATA Interpretation

Annual production 18 million tons (mt) 5 mt More than 3.5

times

Turnover $18 billion $4.64 billion More than 3.5 times

P/E Ratio 14.8 times - Higher than Industry

Realization

Paid/tone

- $866 per tone 4 times that of Corus.

Overall Valuation 7 Times of EBIDTA - Tata paid nearly

7.6times

Sources of Fund:

Tata Steel appointed Credit Suisse, ABN Amro and Deutsche Bank

to arrange

financing. Of the 3.3 billion of financing being raised at the

SPV level, Credit Suisse

would provide 45per cent and ABN AMRO and Deutsche 27.5per cent

each. The $1.8

billion bridge debt being raised at the Tata Steel level in

India would be shared between

Standard Chartered and ABN AMRO.

-

7/28/2019 Final M & A

15/40

15

Sources of Funds:

-

7/28/2019 Final M & A

16/40

16

Stock Price history of TATA steel

-

7/28/2019 Final M & A

17/40

17

Case 2: The Growth Starategy of TATA group through Mergers

and

Acqusitions

The growth strategy of TATA Group through Mergers and

Acquisitions

Tata group is one of Indias largest and most respected business

conglomerates. The

group comprises 93 operating companies in seven business

sectors. Tata group was

focusing on the strategy of extending its presence in the

international markets. Its

overall acquisitions during the seven years, 2000-2006, have

crossed the $2.5 billion

mark. Tatas strategy was to rationalise the groups business

portfolio and deliver

returns on investment that exceeded the cost of the capital. It

aimed to have a

symbolically unified brand and grab new opportunities.

Period Acquire Target Value(Rs. Incrore)

Motive

February 2000 Tata Tea Tetley UK 1870 To be global beverage

giant

November2001 Tata Sons ComputerMaintenanceCorporationLtd

157 To consolidate itsleadership in ITservices

February 2002 Tata group VSNL 1439 Acquire fromGovernment of

theirdisinvestmentprogramme.

June 2002 Tatateleservices

HughesTelecom India

- Was plan to have acomprehensivepresence across the

countryMay 2003 TCS AirlineFinancialSupportServices

- Global marketpositioning and jointstrategic

businessdevelopment, qualityexcellence and superiorproduct

delivery

-

-

7/28/2019 Final M & A

18/40

18

July 2003 VSNL Gemplex To use existing networkcapability and

readyplatform in high trafficregion

March 2004 Tata Motors Daewoo

Commercialvehicles

459 Chinese market & small

truck segment entry

March 2004 VSNL Dish net DSLsISP Division

270 To strengthen itsinternet based services

March 2004 TCS AviationSoftwareDevelopmentConsultancy

4.02 To be competence anddeveloping thetransaction

processingsystem in businesseslike credit cardprocessing and

railwayreservation system.

Cross selling inaviation industry as wellas in banking,

financialservices and insuranceindustry

May 2004 TCS Phoenix Globalsolution

- To strengthen itsoffering for theinsurance sector

August 2004 Tata steel NatSteel 1313 To have equalpresence in

long andflat products of steel

November 2004 VSNL Tyco GlobalNetwork 13 To become advancedand

extensivesubmarine cableprovider in the world

February 2005 Tata Motors HispanoCarrocera

70 Was able to supplyworld class buses inEurope.

July 2005 VSNL Teleglobe 1076 Was plan to expand inthe new

market and tobecome a leadingglobal player in whole

sell voice andbandwidth andenterprise dataservices

October 2005 Tata tea Good earth 144 To consolidate itsposition

in the specialitytea segment as globalconsumption of

-

7/28/2019 Final M & A

19/40

19

speciality (value added)tea is growing at fasterclip compare to

thetraditional black tea.

December 2005 Tata steel Millennium

Steel

1818 To enhance its market

position in south eastAsia with globalisationinitiative

December 2005 Tatachemicals

Brunner Mond 789 To become largestproducer of soda ash

inEurope.

June 2006 Tata coffee Eight O Clock 1015 Entry into

worldslargest coffee marketUS

April 2007 Tata steel Corus 1210 Scale, range, access toglobal

automakers

MERGERS-

Tata finance ltd was merged into TATA MOTORS. The merger was

under the

scheme of amalgamation, all equity shareholders of TATA FINANCE

LTD were

entitled to receive eight ordinary scheme of TML of Rs. 10 each

for every 100

equity share of Tata Finance of Rs. 10 each. This merger was

expected toenable the vehicle financing business of TFL to grow

stronger by leveraging its

synergies of direct business model with the dealer driven

business of Bureau of

Hire purchase and credits (BHPC). The merger allowed TFL share

holders to

participate in the growth of Tata motors.

Merger was between Tata chemicals and Hindustan Lever chemicals

Ltd. propose

scheme was, HLCL share holders were issued TCL shares in the

ratio of 2.5:1.

The business of HLCL and TCL had natural synergies that

contributed to

superior excellence model. TCLs inorganic chemical business was

a natural fit

with HLCLs bulk chemical business. TCL was the largest

manufacturer of soda

ash, the key raw material for production of detergent where as

HLCL was Indias

-

7/28/2019 Final M & A

20/40

20

largest manufacture of STTP, used as builders in detergents.

TCLs fertilizers

were highly complementary to HLCLs operations. Post merger, the

company

was able to offer wide range of complementary products and

support services to

current base of customers.

Conclusion-

Tata group has used merger and acquisition as a tool for growth

by acquiring and

merging entities to grow and become top companies In that

particular sector. Following

are the benefits Tata group got through merger and

acquisition.

1. Tata steels acquisition to Corus steel, made Tata steel the

fifth largest steel

maker in the world. In fact 30 % of its revenue (Rs. 96,723/-

cr.) revenue from

overseas business had focused on finding on a strategic fit for

its acquisitions.

2. Tata tea acquisition of Tetley Tea, made Tata tea to the no.

2 spot among worlds

tea makers and gave it an international beverage brand.

3. Deal with Daewoo Motors heralded Tata motors big ticket entry

into the medium

and heavy commercial markets of china and South East Asia and

also

rejuvenated its own truck making division through production of

bigger vehicles.

4. Post HLCL and TCL merger, company was able to offer wide

range of

complementary products and services to the current base of

customers.

5. Tata chemicals acquisition of Brunner Mond Group, made Tata

chemicals the

worlds largest producer of Soda ash. Tata power acquired 30%

stake in

Indonesian thermal coal producers, PT Kaltim Prima Coal and PT

Arutmin

Indonesia.

6. The National Iron and Steel Mills Ltd (NISM) enjoyed good

brand recognition in

Singapore and in the other South East Asian region. After

acquisition of NatSteel

gave Tata steel not only footprint in the seven new countries in

Asia-Singapore,

China, Malaysia, Thailand. Australia, Vietnam and Philippines,

also gave

geographic access to Asian region. Tata steels acquisition was a

strategic

initiative to enter the high growth geographies of China and

South East Region.

Main advantage of this acquisition was lowering of input steel

costs. There were

-

7/28/2019 Final M & A

21/40

21

able to offer a more comprehensive basket of products to their

customers and

provide more complete steel solutions.

7. Acquisition of Eight O Clock bought strategic and operational

gains for Tata

coffee as its grand entry into the worlds largest coffee

market.

8. Hispano carrocera is one of the largest bus and coach

bodybuilders in Europe

and North America. It exports 50% of its production to countries

worldwide. Tata

motors acquired 21% stake, after tying up with Tata motors,

Company was able

to supply world class buses in Europe and outside, and gained

access to new

markets in North America and Middle East.

9. Acquisition of Tyco Global Network, was the deal of worlds

largest most

advanced and extensive submarine cable systems, gave control

over a network

that spans 60,000 km and three continents.

10. TFL was merged into Tata Motors, enable the vehicle

financing business of TFL

to grow stronger by leveraging its synergies of the direct

business model with

dealer driven business of BHPC.

11.Tatas VSNL acquired Chennai based Dishnet DSLs internet

service provider,

consolidated VSNLs position in dial up space, giving it control

over 600 owned

and franchised Dishnet cyber caf as well as broadband assets

servicing more

than 50,0000 customers in key cities.

12. To strengthen its offering for the insurance sector, Tata

Consultancy Services

(TCS) acquired Phoenix Global Solution (PGS).

13. TATA acquired UK based Land Rover and Jaguar units from Ford

company of

US. Land rovers benefits are upmarket SUV brand, Access to

latest technology

in four wheel and readymade R & D. Jaguars benefits are

Upmarket brand,

Access to new technologies, premium customer profile competing

with

Mercedes, BMW and Audi and considered the best British

brand.

-

7/28/2019 Final M & A

22/40

22

Case 3: Joint Venture of Maruti Suzuki

Joint Venture:

A joint venture (JV) is a business agreement in which parties

agrees to develop, for a

finite time, a new entity and new assets by contributing equity.

They exercise control

over the enterprise and consequently share revenues, expenses

and assets. There are

other types of companies such as JV limited by guarantee, joint

ventures limited by

guarantee with partners holding shares.

Joint venture in India:

A JV may be defined as any arrangement whereby two or more

parties co-operate in

order to run a business or to achieve a commercial

objective:

This co-operation may take various forms, such as equity-based

or contractual JVs. It

may be on a long-term basis involving the running of a business

in perpetuity or on a

limited basis involving the realization of a particular project.

It may involve an entirely

new business, or an existing business that is expected to

significantly benefit from the

introduction of the new participant. A JV is, therefore, a

highly flexible concept. The

nature of any particular JV will depend to a great extent on its

own underlying facts and

characteristics and on the resources and wishes of the involved

parties. It is an effective

business strategy for enhancing marketing, positioning and

client acquisition which has

stood the test of time. The alliance can be a formal contractual

agreement or an

informal understanding between the parties. Global proliferation

of business and

commerce has given an international dimension to JVs. Corporate

entities across the

globe seek cross-border alliances to share the resources,

opportunities and potential to

deliver cutting edge performance. Such alliances are designed to

suit the commercial

requirements of parties and vary from a mere transitory

arrangement for one partner toestablish its presence in a new

market to a calculated step towards a full merger of the

technologies and capabilities of the partners. JVs are envisaged

as alliances that yield

benefits for the JV partners by offering a platform to attain

their business goals which

would be difficult or uneconomical to attain independently.

Establishing a JV with an

ideal partner provides a fast way to leverage complementary

resources available with

-

7/28/2019 Final M & A

23/40

23

the other partner, share each others capabilities, access new

markets, strengthen

position in the current markets, or diversify into new

businesses. India Inc. has come of

age and is not just an investment destination but also an

aggressive investor. Indian

companies have exhibited, in the recent past, their ambition to

venture into the quest for

overseas expansion. The main stumbling blocks for Indian

companies in achieving

expected levels of global presence are deficiencies in terms of

product quality,

technology, infrastructure and even management processes. These

deficiencies can be

negated by way of an alliance with a foreign counterpart who is

a strategic fit.

Benefits of Joint Venture:

A) Leveraging Resources:

With the globalization, access to labor, capital and

technological resources have

become driving forces for modern businesses to aim to achieve

economies of scale.

Today, business commitments are far too large to be executed by

a single company.

From a wider perspective, the conduct of business mandates a

huge pool of resources

extending from massive financial backup to plenty of skilled

manpower. Cross-border

business projects are all the more demanding and the best

solution is to either outright

acquire or share them by entering into a JV. Co-operation is a

great way of reducing

research and manufacturing costs while limiting exposure.

B) Exploiting Capabilities and Expertise:

Parties to a JV may have complementary skills or capabilities to

contribute to the JV; or

parties may have experience in different industries which it is

hoped will produce

synergistic benefits. The basic tenet of a JV is the sharing of

capabilities and expertise

of both the partners on mutually agreed terms. Such sharing

grants a competitive

advantage to the JV partners over other players in the

market.

-

7/28/2019 Final M & A

24/40

24

C) Sharing Liabilities:

A JV also offers parties an opportunity to jointly manage the

risks associated with new

ventures. Through a JV they can limit their individual exposure

by sharing the liabilities.

When the liabilities and risks are shared the pressure on each

individual partner iscorrespondingly reduced. It reduces the risks

in a number of ways as the business

activities of the JV can be expanded with smaller investment

outlays than if financed

independently.

D) Market Access:

JVs are the most efficient mode of gaining better market access.

Companies utilize JV

agreements to expand their business into other geographies,

consumer segments and

product markets. In the case of a cross-border JV, the

involvement of a locally-based

party may be necessary or desirable in countries where it is

difficult for a foreign

company to penetrate the market or where the local law limits

the ownership structure

by foreigners. For instance, in India, certain market sectors

remain restricted for foreign

investment and a local partner with a certain shareholding in

the company is a

regulatory necessity for commencing business and making

investments. These

restrictions are discussed in further detail in a later

section.

E) Flexible Business Diversification:

JVs offer many flexible business diversification opportunities

to the partners. A JV may

be set up, as a prelude to a full merger or only for part of the

business. It offers a

creative way for companies to enter into non-core businesses

while maintaining an easy

exit option. Companies can also resort to JVs as a method to

gradually separate a

business from the rest of the organization and eventually, sell

it off. In certain

circumstances, JVs may be set up with strategic investors in the

process of entering intoa new market so as to initially provide the

foreign participant local infrastructure and

guidance but with a view to integrate the operations of the JV

into the main company in

the future. In this situation, the foreign participant may

choose to acquire the local

participants interest once the venture is up and running. This

can be highly beneficial to

-

7/28/2019 Final M & A

25/40

25

both parties as the foreign party is able to establish itself in

the local market while the

local party gets a liquid exit.

COMPANY HISTORY AND BACKGROUND

A) Maruti Udyog Limited (MUL):

Maruti Udyog Limited (MUL) was established in Feb 1981 through

an Act of Parliament,

to meet the growing demand of a personal mode of transport

caused by the lack of an

efficient public transport system. It was established with the

objectives of - modernizing

the Indian automobile industry, producing fuel efficient

vehicles to conserve scarce

resources and producing indigenous utility cars for the growing

needs of the Indian

population. A license and a Joint Venture agreement were signed

with the Suzuki Motor

Company of Japan in Oct 1983, by which Suzuki acquired 26% of

the equity and agreed

to provide the latest technology as well as Japanese management

practices. Suzuki

was preferred for the joint venture because of its track record

in manufacturing and

selling small cars all over the world. There was an option in

the agreement to raise

Suzukis equity to 40%, which it exercised in 1987. Five years

later, in 1992, Suzuki

further increased its equity to 50% turning Maruti into a

non-government organization

managed on the lines of Japanese management practices.

Maruti created history by going into production in a record 13

months. Maruti is the

highest volume car manufacturer in Asia, outside Japan and

Korea, having produced

over 5 million vehicles by May 2005. Maruti is one of the most

successful automobile

joint ventures, and has made profits every year since inception

till 2000-01. In 2000-01,

although Maruti generated operating profits on an income of Rs

92.5 billion, high

depreciation on new model launches resulted in a book loss.

The Evolution

Marutis history of evolution can be examined in four phases: two

phases during pre-

liberalization period (1983-86, 1986-1992) and two phases during

post-liberalization

period (1992-97, 1997-2002), followed by the full privatization

of Maruti in June 2003

-

7/28/2019 Final M & A

26/40

26

with the launch of an initial public offering (IPO).The first

phase started when Maruti

rolled out its first car in December 1983. During the initial

years Maruti had 883

employees, a capital of Rs. 607 mn and profit of Rs. 17 mn

without any tax obligation.

From such a modest start the company in just about a decade

(beginning of second

phase in 1992) had turned itself into an automobile giant

capturing about 80% of the

market share in India. Employees grew to 2000 (end of first

phase 1986), 3900 (end of

second phase 1992) and 5700 in 1999. The profit after tax

increased from Rs 18.67 mn

in 1984 to Rs. 6854.54 mn in 1998 but started declining during

1997-2001.

During the pre-liberalization period (1983-1992) a major source

of Marutis strength was

the wholehearted willingness of the Government of India to

subscribe to Suzukis

technology and the principles and practices of Japanese

management. Large number of

Indian managers, supervisors and workers were regularly sent to

the Suzuki plants in

Japan for training. Batches of Japanese personnel came over to

Maruti to train,

supervise and manage. Marutis style of management was

essentially to follow

Japanese management practices.

The Path to Success for Maruti was as follows:

(a) Teamwork and recognition that each employees future growth

and prosperity is

totally dependent on the companys growth and prosperity

(b) Strict work discipline for individuals and the

organization

(c) Constant efforts to increase the productivity of labor and

capital

(d) Steady improvements in quality and reduction in costs

(e) Customer orientation

(f) Long-term objectives and policies with the confidence to

realize the goals

(g) Respect of law, ethics and human beings. The path to success

translated into

practices that Marutis culture approximated from the Japanese

management practices.

-

7/28/2019 Final M & A

27/40

27

Maruti adopted the norm of wearing a uniform of the same color

and quality of the fabric

for all its employees thus giving an identity. All the employees

ate in the same canteen.

They commuted in the same buses without any discrimination in

seating arrangements.

Employees reported early in shifts so that there were no time

loss in-between shifts.

Attendance approximated around 94-95%. The plant had an open

office system and

practiced on-the-job training, quality circles, kaizen

activities, teamwork and job-

rotation. Near-total transparency was introduced in the decision

making process. There

were laid-down norms, principles and procedures for group

decision making. These

practices were unheard of in other Indian organizations but they

worked well in Maruti.

During the pre- liberalization period the focus was solely on

production. Employees

were handsomely rewarded with increasing bonus as Maruti

produced more and sold

more in a sellers market commanding an almost monopoly

situation.

B) Suzuki:

Suzuki is Japan's 4th largest automobile manufacturer after

Toyota, Nissan and Honda,

the 9th largest automobile manufacturer in the world by

production volume, employs

over 45,000, has 35 main production facilities in 23 countries

and 133 distributors in 192

countries. According to statistics from the Japan Automobile

Manufacturers Association

(JAMA), Suzuki is Japan's second-largest manufacturer of small

cars and trucks.

In 1909, Michio Suzuki (18871982) founded the Suzuki Loom Works

in the small

seacoast village of Hamamatsu, Japan. Business boomed as Suzuki

built weaving

looms for Japan's giant silk industry. In 1929, Michio Suzuki

invented a new type of

weaving machine, which was exported overseas. Suzuki filed as

many as 120 patents

and utility model rights. The company's first 30 years focused

on the development and

production of these exceptionally complex machines.

Despite the success of his looms, it occurred to Suzuki that his

company would benefit

from diversification and he began to look at other products.

Based on consumer

demand, he decided that building a small car would be the most

practical new venture.

The project began in 1937, and within two years Suzuki had

completed several compact

prototype cars. These first Suzuki motor vehicles were powered

by a then-innovative,

-

7/28/2019 Final M & A

28/40

28

liquid-cooled, four-stroke, four-cylinder engine. It featured a

cast aluminum crankcase

and gearbox and generated 13 horsepower (9.7 kW) from a

displacement of less than

800cc.

With the onset of World War II, production plans for Suzuki's

new vehicles were haltedwhen the government declared civilian

passenger cars a "non-essential commodity." At

the conclusion of the war, Suzuki went back to producing looms.

Loom production was

given a boost when the U.S. government approved the shipping of

cotton to Japan.

Suzuki's fortunes brightened as orders began to increase from

domestic textile

manufacturers. But the joy was short-lived as the cotton market

collapsed in 1951.

Faced with this colossal challenge, Suzuki's thoughts went back

to motor vehicles. After

the war, the Japanese had a great need for affordable, reliable

personal transportation.

A number of firms began offering "clip-on" gas-powered engines

that could be attached

to the typical bicycle. Suzuki's first two-wheel ingenuity came

in the form a bicycle fitted

with a motor called, the "Power Free." Designed to be

inexpensive and simple to build

and maintain, the 1952 Power Free featured a 36 cc, one

horsepower, two-stroke

engine. An unprecedented feature was the double-sprocket gear

system, enabling the

rider to either pedal with the engine assisting, pedal without

engine assist, or simply

disconnect the pedals and run on engine power alone. The system

was so ingenious

that the patent office of the new democratic government granted

Suzuki a financial

subsidy to continue research in motorcycle engineering, and so

was born Suzuki Motor

Corporation.

In 1953, Suzuki scored the first of many racing victories when

the tiny 60 cc "Diamond

Free" won its class in the Mount Fuji Hill Climb.

By 1954, Suzuki was producing 6,000 motorcycles per month and

had officially changed

its name to Suzuki Motor Co., Ltd. Following the success of its

first motorcycles, Suzuki

created an even more successful automobile: the 1955 Suzuki

Suzulight. Suzuki

showcased its penchant for innovation from the beginning. The

Suzulight included front-

wheel drive, four-wheel independent suspension and

rack-and-pinion steeringfeatures

not common on cars until three decades later.

-

7/28/2019 Final M & A

29/40

29

Volkswagen AG completed the purchase of 19.9% of Suzuki Motor

Corporation's issued

shares on 15 January 2010; Volkswagen AG is the biggest

shareholder in Suzuki.

History of Maruti Suzuki after joint venture:

Founded in the month of February in the year 1981, Maruti Udyog

Limited started its

manufacturing operations in 1983. After a through market

research, the first car rolled

out on 14th December 1983. This car was launched under the

flagship of Maruti Udyog

Limited which was later renamed Maruti Suzuki IndiaLimited.

The headquarters of the company is located in New Delhi. The

Indian Government

initially owned 18.28 per cent of the Maruti Suzuki Company and

54.2 per cent was

owned by Suzuki of Japan. In the month of June in year 2003, the

BJP led government

offered a public issue of 25 per cent of the Maruti Udyog

Limited. On 10 May 2007, the

government of India sold the complete share of Maruti Udyog

Limited to Financial

Corporations. By doing this, the Government of India no longer

has a stake in Maruti

Udyog Limited.

Maruti Suzuki Company in India is a subsidiary of Suzuki Motor

Corporation. Being the

leader in manufacturing passenger cars and multipurpose vehicles

in India, the

company is accounted for acquiring nearly 50 per cent of the

total industry sales. During

the year 2009-2010, the Maruti Suzuki Company in India sold over

1,018,365 vehicles.

This comprises of 870,790 vehicles in the domestic market and

147,575 vehicles in the

foreign markets. In total, the Maruti Suzuki Company in India

produced and sold over

eight million cars. In the year 2009-2010, the company had an

income of Rs.301, 198

million. The Maruti Suzuki company information states that the

company has a

financially enriched balance sheet with surplus and reserves of

Rs. 116.9 billion and thedebt equity ratio of 0.07 as on 31st

March, 2010. Maruti Suzuki Company is a limited

firm, which is listed on the National Stock Exchange of India

Limited and Bombay Stock

Exchange Limited.

-

7/28/2019 Final M & A

30/40

30

Maruti Suzuki company in India has two producing unit based at

Gurgaon and Manesar,

south of New Delhi, India. The combined production capacity of

both the units is

somewhere around one million cars per annum. In the year

2009-2010, the company

acquired 700 acres of land in Rohtak, Haryana, India for setting

up an excellent test

course for research and development. The Maruti Suzuki Company

Profile ensures

complete customer satisfaction with 'one-stop-shop' facility

providing different services

such as Automobile Finance, Automobile Insurance, Maruti Genuine

Parts and

Accessories, Extended Warranty and Maruti Certified pre-owned

cars. Maruti Suzuki

Company in India has established 358 pre-owned car outlets in

210 cities.

Present Scenario of Maruti Suzuki:

Maruti Suzuki Company in India sold a total of 75,300 vehicles

in the month of July in

2011. This total includes a sum of 8796 units of exports.

However in July 2010, the

Maruti Suzuki company had sold a sum of 1, 00,857 vehicles,

which proved to be quite

a feat for the company. Due to the following activities of the

Maruti Suzuki Company,

the total sales of the company suffered.

Manufacturing process for Swift Dzire was shifted from Manesar

to Gurgaon. Due to

these planned changes, the production of the model was

temporarily affected.

Therefore, the sales units were 5,471, lower than the production

in the month of July in

2010.

The production of old Swift was discontinued in the month of

July in the year 2011. New

model of swift was launched on the 17th of August, 2011. While

the Maruti Suzuki

Company dispatched 11,828 units in July 2010, the delivery in

the month of July 2011

was only 348 units.

With these two planned activities of the Maruti Suzuki company,

the sales in the monthof July in the year 2011 dropped by around

17000 units as compared to July 2010.

Maruti Suzuki Way Ahead:

The Maruti Suzuki Company information reports that it is

planning to expand its

manufacturing capacity to 1.75 million from 1.2 million by the

year 2013. The chairman

-

7/28/2019 Final M & A

31/40

31

of the Maruti Suzuki Company, RC Bhargava stated that the

production in the Gurgaon

plant is to be reduced since the plant is very old and

congested. Estimated output will

be reduced to 6 lac units from 6.5 lac units per annum. Two new

upcoming units will be

developed in Manesar plant and will have a total manufacturing

capacity of 2.5 lac units

per annum. The second unit in the Manesar plant will be opened

by September-

October, of this year. However, the third unit will start

functioning from 2012-2013.

The Maruti Suzuki Company in India will be offering two new

models in the Indian Car

Market between 2011 and 2013. A new model of Maruti Suzuki Swift

was launched in

August 2011. On the other hand, Maruti Suzuki Swift Dzire will

be launched in the

earlier part of 2012. The Maruti Suzuki Swift was initially

launched in the European

market and the production of this variant has begun in their

Hungarian plant. New

variant of Swift is somewhat wider and longer than the previous

model. Besides, Maruti

Suzuki Swift Dzire has the same engine configuration but the

length and width of the car

has increased.

Stake of Suzuki in Maruti Suzuki:

1) 1981:

The Indian Central government at the behest of Indira Gandhi

salvages Maruti limited

and starts looking for an active collaborator for this

company.Maruti Udyog Ltd was

incorporated under the provisions of the Indian Companies Act,

1956.

2) 1982:

License and Joint Venture Agreement (JVA) signed between Maruti

Udyog Ltd.(Indian

Government) and Suzuki Motors Corporation of Japan.

3) 1991:

65 percent of the components, for all vehicles produced, are

indigenized (produced

locally). Liberalization of the Indian economy opens new

opportunities but also brings

more competition to segment.

-

7/28/2019 Final M & A

32/40

32

4) 1992:

Suzuki increases its stake in Maruti to 50 percent, making the

company a 50-50 JV with

the Government of India the other stake holder.

5)1997:

Government nominated Mr. S.S.L.N. Bhaskarudu as the Managing

Director on August

27, as the then current Managing director, R.C.Bhargava, was

completing his tenure.

Creating a conflict with Suzuki

6) 2002:

Suzuki Motor Corporation (SMC) increases its stake in Maruti to

54.2 percent.

7) 2003:

Maruti Udyog Ltd is listed on BSE and NSE after a public issue,

which is oversubscribed

10 times.

Maruti Suzuki India Ltd (MSIL) was incorporated as a 74:26 joint

venture (JV) between

the Government of India and Suzuki Motor Corporation (SMC) in

1981 as Maruti Udyog

Ltd (MUL). SMC acquired 26 per cent equity in MSIL and increased

it to 54.2 per cent in

2002, making MUL a subsidiary of SMC. In June 2003, the

government offloaded

another 25 per cent of its stake in MSIL through an initial

public offer (IPO). MSILs

manufacturing facilities are located at Gurgaon and Manesar. In

200607, the company

amalgamated with MSAIL, which was incorporated on April 12, 2005

as a JV

manufacturing facility (Manesar), in which MSIL and SMC had a

70:30 partnership.

Japanese parent Suzuki Motor had controlled 70% of the Suzuki

Powertrain JV; the

newly formed JV is 54% owned by Suzuki and 46% owned by Maruti.

The realignment

will strengthen our company by giving us greater flexibility and

longer lead time in

meeting the changing market demand, Nakanishi says.

-

7/28/2019 Final M & A

33/40

33

The takeover amounts to a friendly swap of stock. Suzuki

Powertrain is valued at Rs21

billion ($367.4 million), and it will receive Maruti Suzuki

shares valued at Rs15 billion

($262.4 million).

The merger and fresh investment plans bring Maruti Suzukis

entire annual diesel-

engine capacity of 900,000 units under a single management.

Analysts believe the

merger will increase the auto makers net profits and operating

margins.

The mergerwill result in a lot of synergies between the

companies that will boost our

balance sheet, says Ajay Seth, Maruti Suzukis chief financial

officer.

Reasons for Joint Venture:

The reason why Suzuki entered the Indian market is clear. Suzuki

chose an untapped

market while Japans bigger auto makersToyota, Nissan, and

Hondaengaged in

fierce competition within Japan. Osamu Suzuki, CEO and COO of

the company (and a

grandson-in-law of its founder), is a creative decision-maker, a

maverick who considers

himself an old man in a mom-and-pop company that concentrated

most of its

resources on producing motorcycles and light motor vehicles. Yet

when he decided to

diversify and focus on India, many criticized him as being

reckless, because India was

so unfamiliar to Japanese companies. Indeed, while there are

currently at least 19,000

Japanese companies in the Chinese market, there are only about

260 in India.

Suzukis decision to enter the Indian market turned out to be a

resoundingly wise

choice. Japans population peaked in 2004 and is now falling,

while its younger

generations show diminishing interest in automobiles. In the

past, young Japanese were

proud of their knowledge about cars, and every teenage boy knew

which model would

attract the most girls. Today, however, Japanese driving schools

suffer from a fall-off in

students, which cannot be explained solely by declining

population.

-

7/28/2019 Final M & A

34/40

34

Indias population, on the other hand, is increasing dramatically

in the absence of a one-

child policy, such as exists in China. It makes sense, then,

that Japanese companies

should head to the expanding Indian market.

Doing so, moreover, makes geo-strategic sense as well, with

successive Japanesegovernments increasingly regarding India as a

vital diplomatic and political partner. For

example, in August 2007, then Prime Minister Shinzo Abe headed a

big delegation to

India, followed by an official visit in December by current

Prime Minister Yukio

Hatoyama.

The Strategic and Global Partnership between Japan and India,

established in 2006,

rests on the recognition that Japan and India share common

values and interests, as

they are the two major entrenched democratic countries in Asia.

These shared values

distinguish the Japan-India relationship from Japans

relationship with China. The

growing congruence of strategic interests led to the 2008

Japan-India security

agreement, a significant milestone in building a stable

geopolitical order in Asia.

A constellation of Asian democracies linked by strategic

cooperation and common

interests is becoming critical to ensuring equilibrium at a time

when Asias security

challenges are mounting due to the shift in global economic and

political power from

west to east. The emerging Japan-India partnership looks like a

necessary foundation

for pan-Asian security in the 21st century.

The key point today is that the governments in both India and

Japan are keen on

developing their strategic consensus about Asias future, a fact

underscored by the

many bilateral discussions between defence and military

officials of both countries that

are taking place. These discussions include joint initiatives on

maritime security,

counterterrorism, weapons proliferation, disaster prevention and

management, and

energy security.

More is needed. India and Japan should, for example, jointly

develop new defence

capacities. Today, India and Japan cooperate on missile defence

in partnership with

Israel and the US. Bilateral efforts should also be launched to

develop other defence

-

7/28/2019 Final M & A

35/40

35

technologies. Suzukis joint venture in India suggests that

cooperation in high-tech

manufacturing is eminently possible.

Suzukis success is a powerful precedent not only for other

Japanese companies that

are looking at the Indian market, but also for further deepening

cooperation between thetwo countries. Osamu Suzuki may not be

willing to share all of the secrets of his

success with his competitors, but they and Japanese diplomats

should be studying the

Suzuki method. Japans economy and Asian security depend on its

replication.

Financial information of Maruti Suzuki:

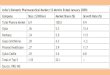

Year Sales (in Cr.) Operating profit

2008 35,587.09 2,512.892009 36,299.74 4,202.15

2010 29,623.01 3,954.29

2011 20,852.52 1,832.06

2012 17,860.28 2,167.37

Above is the sales and operating profit of Maruti Suzuki of last

5 years. Its really huge

in number. As a joint venture firm, the Maruti Suzuki is

performing really well.

Disputes between Suzuki Motor and the Government of India

(GoI):

The case gives detailed insight into the disputes between Suzuki

Motor and the

Government of India (GoI), joint venture partners in Maruti

Udyog Limited (MUL), an

automobile giant in India.

Covering the expansion plan, appointment of Bhaskarudu as the

managing director and

the disinvestment of MUL, it describes in-depth the disputes

between the partners.

Disinvestment of Maruti, problems in the Joint Venture between

Maruti & Suzuki, role

of Government of India in J V, passenger car market in

India.

-

7/28/2019 Final M & A

36/40

36

"Maruti is a national company which has grown because of the

support of the

government. We can't hand it over to Suzuki on a platter."

- Murasoli Maran, Industry Minister, India, 1997.

"Suzuki feels they can no longer afford the disadvantage of

government control over

Maruti's decision making. They feel they can do better on their

own."

- A Government of India Source, 1997.

A Bitter Fight:

In August 1997, the Government of India (GoI) appointed

R.S.S.L.N. Bhaskarudu

(Bhaskarudu) as the managing director (MD) of India's passenger

car market leader

Maruti Udyog Ltd. (MUL). The appointment was strongly opposed by

Suzuki Motors

Corporation (SMC) of Japan, the GoI's 50% partner in MUL joint

venture. In a press

release following the appointment, Osamu Suzuki (Osamu),

President of SMC, claimed

that the appointment was illegal on the grounds five of the

directors who comprised the

majority of MUL's board strength of nine, had objected to the

appointment. Suzuki even

alleged that Bhaskarudu was incompetent and unsuitable for the

MD post.

The GoI argued that as per the 1992 amendment in the GoI-SMC

joint venture

agreement, both the partners were entitled to nominate the MD

for five years in turns,

and there was no need for any consultation on it. Industry

minister Murasoli Maran

(Maran) alleged that SMC was opposing the appointment of

Bhaskarudu as it wanted

Jagdish Khattar (Khattar), Executive Director (ED), MUL

(reportedly a SMC loyalist) to

become the MD. Following the disagreement over Bhaskurudu's

appointment, a furious

exchange of letters took place between SMC and the Industry

ministry. SMC asked for

Bhaskurudu's resignation claiming that the minutes of the

meeting when Bhaskurudu

was appointed, did not fully record its objections to the same.

However, the GoI refused

to remove Bhaskurudu and reportedly even started looking for a

prospective partner in

the event of SMC's exit.

Soon after, in the AGM held on September22, 1997, SMC and the

GoI representatives

even resorted to verbal violence.1 SMC nominees on the board

attempted to prove

-

7/28/2019 Final M & A

37/40

37

Bhaskarudu's unsuitability of the post by questioning him

regarding MUL's functioning.

When Bhaskarudu's appointment was put to vote, there was a tie.

Prabir Sengupta

(Sengupta), Chairman of the MUL board, used his casting vote to

ratify the

appointment. Following this, SMC nominees passed a no confidence

motion against

Sengupta and proposed the name of Yoshio Saito2(Saito) for the

chairmanship.

The GoI strongly backed Sengupta stating that he should be

allowed to complete his

scheduled term of five years until 2000. SMC then lodged an

arbitration petition against

Bhaskarudu's appointment in the International Court of

Arbitration.3 In June 1998, the

new ruling Bharatiya Janata Party (BJP) government intervened

into the issue and

arranged for an out-of-court settlement between the parties.4 As

per the settlement

deal, Bhaskarudu was to step down in December 1999, two years

ahead of schedule

and Khattar was to replace him in January 2000.5 Further, Saito

was to replace

Sengupta as the chairman. Though the dispute between SMC and GoI

seemed to have

been put to rest for the time being, the issue did not come as a

major surprise to

industry watchers. This was because the company's history was

marked with frequent

conflicts between the two partners over the years.

Background Note:

Till the early 1980s, the Indian passenger car industry offered

limited choice to the

customers, with only two popular models in the form of Hindustan

Motors' (HM)

Ambassador and Premier Automobiles' (PAL) Padmini. The

government not only

controlled the price mechanism in the industry, but the entry of

foreign players was also

strictly regulated.

However, the scenario changed in 1981, when the GoI itself

entered the car business

by establishing MUL by acquiring the assets of Maruti Ltd.6 In

October 1982, the GoI

signed a licensing and joint venture agreement with SMC where in

Suzuki acquired the

26% share of the equity.7 Suzuki's history dates back to 1903,

when Michio Suzuki

founded Suzuki Loom Works in Hamamatsu in Shizuoka, Japan. For

the first 30 years,

company focused on the development and production of complex

machines for Japan's

silk industry. In 1937, the company diversified into building

cars and in 1939 began

-

7/28/2019 Final M & A

38/40

38

manufacturing cars for the Japanese market. But due to the

Second World War it had to

stop the production of cars and concentrated on the manufacture

of the looms.

The company shifted its focus back to automobiles with the

termination of war and

collapse of cotton market in 1951. In 1952 it manufactured its

first motorized bicyclecalled 'Power Free'.

In 1954, the company changed its name to Suzuki Motor Co. Ltd.

and was by then

producing around 6,000 cars per month. With 57 production

centers all over world, its

manufacturing and assembly network expanded to over 26 countries

all over the world.

Company established 22 automotive manufacturing facilities in 17

countries. Suzuki's

vehicles were sold through 134 distributors in 175 countries. By

March 2001, Suzuki's

net sales were 1,600, 253 billion and it was one of the top 5

automobile manufacturers

of the world. MUL manufactured passenger cars at its factory in

Gurgaon, Haryana with

an installed capacity of 350,000 vehicles. The first product,

Maruti 800 was launched in

1984. Consumers hitherto without any choice rushed to buy the

vehicle. Maruti 800

earned the tag of being the 'people's car...'

The Conflict:

SMC had raised its stake in MUL to 40% in 1987 and to 50%

subsequently in 1992. As

MUL ceased to be a government unit, SMC began managing the

company, with MD

R.C. Bhargava (Bhargava) taking directions from Japan.

As R.C. Bhargava reportedly shared a good rapport with the

secretary and other higher

officials at the Industry ministry, the relations between SMC

and GoI remained cordial.

The first signs of dispute surfaced in late 1993, when SMC

proposed a Rs 2,200 crore

expansion and modernization plan. The plan envisaged increasing

the production by

100,000 vehicles to effectively meet the growing competition in

the sector. The HeavyIndustry secretary Ashok Chandra and the

Finance secretary, Montek Singh Ahluwalia

suggested SMC, in an informal discussion, to go in for a public

issue to raise the finance

for the expansion plan. Though initially SMC was reluctant to go

for a public issue,

Bhargava managed to persuade it in 1995 for the same. However,

things changed with

K.Karunakaran (Karunakaran) becoming the Union minister for

Industries in 1995...

-

7/28/2019 Final M & A

39/40

39

The MUL Disinvestment Issue:

In late 1999, following the recommendations of Disinvestment

Commission, the GoI

announced its decision to divest its stake in MUL. The GoI

decision was a part of its

industrial policy to privatize PSUs through gradual

disinvestment or strategic sale. Thefirst phase of MUL's

disinvestment was to start with a Rs 400 crore rights issue

with

renunciation option for the government, in December 2001.

The second and final phase of MUL disinvestment was to be

completed by the end of

2002, wherein GoI would divest its remaining equity holding in

MUL through a public

offering. The GoI was to sell its interest to the best bidder at

a premium. However,

subject to a clause in the MUL joint venture agreement, the GoI

could not sell its stake

without the written consent of SMC. This was expected to

complicate the disvestment

process of MUL. In January 2002, the GoI announced its

willingness to renounce its

portion of the rights in favour of SMC during the rights issue.

The negotiations between

the GoI and SMC to fix the renunciation premium and the control

premium were

scheduled to begin in January 2002. GoI was reportedly hopeful

of getting a substantial

'control premium' for letting SMC get MUL's full control.

BENEFITS OF JOINT VENTURE:

For Maruti:

Suzuki motor Corporation, the parent company, is a global leader

in mini and

compact cars for three decades:

The Suzuki motors is a global leader in mini and compact car for

many years. Its really

usefull for the maruti ti tie up with the Suzuki, so that they

can have the huge advantage

of the brand name of suzuki specially at global level,

Suzuki's technical superior:

The Suzukis technical superior is one of the main reason of

joint venture rom Maruti

point of view. The Maruti Udhyog lacking in technology before

joint venture compare to

-

7/28/2019 Final M & A

40/40

other players specially at global level. The technical superior

of Suzuki helps the Maruti

a lot in technological upgradation.

lightweight engine that is clean and fuel efficient:

The efficient engine of Suzuki helps the Maruti to perform

better in Indian market as well

as in foreign market too. The upgradation in the technology

improve the performance of

company.

Nearly 75,000 people are employed directly by Maruti Suzuki and

its partners:

For better tecnology, efficient and the employees who has the

knowledge of that

technology in important for any firm. As the technology is

provided by Suzuki, with that

they appointed 75000 people who has good knowledge of working

with this kind a

technology. To train the new employee about new technology is

difficult.

For Suzuki:

Large Indian Market:

For Suzuki, a major advantage is the large indian market. As

suzuki is now in indian

market, they has that opportunity to target the huge market of

india which can provide

huge opportunity to the company. That is something golden chance

for the the Suzuki

motors to enter directly in Indian market with ready made market

of Maruti and at the

same time target new market too.

Availability of resources:

The all major resources like raw material, labour, new

technologies etc are available in

India. In fact the labour cost is cheaper in Indian market

compare to foreign countries

which help in cost control. At the same time government of India

is also providing many

incentives to this industry. So, that is good opportunity for

Suzuki to enter in Indian

market.