Embed Size (px)

DESCRIPTION

koli

Citation preview

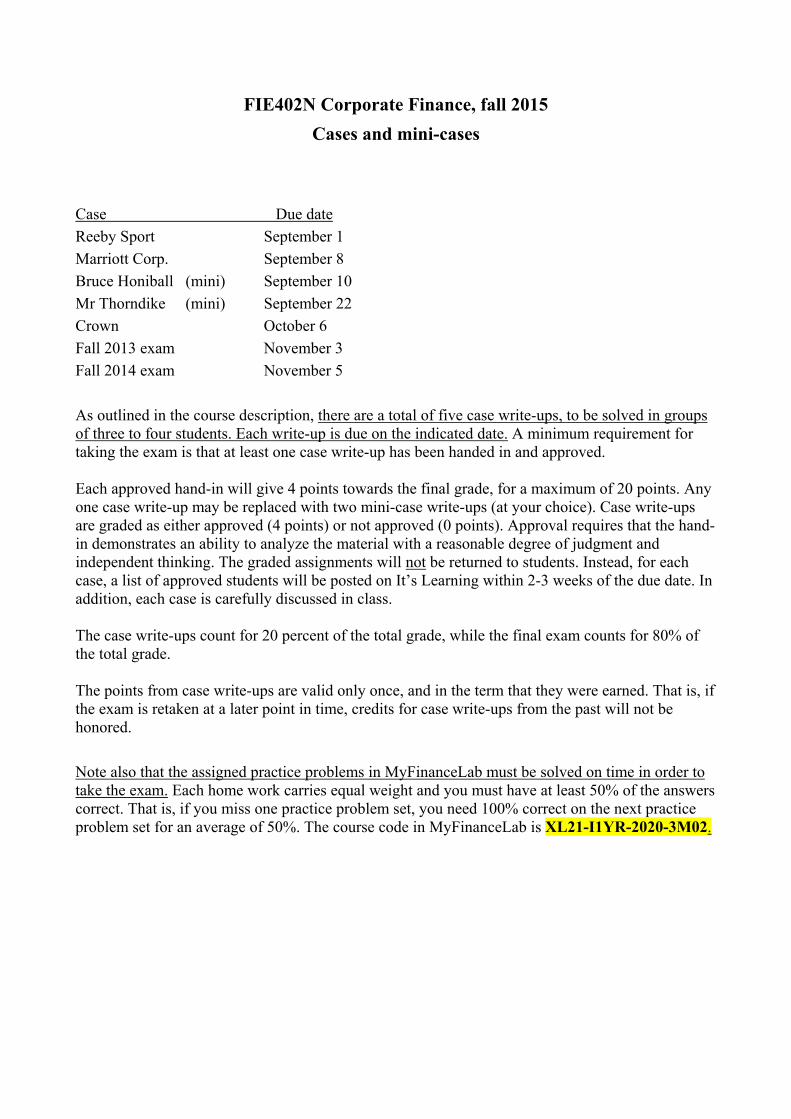

FIE402N Corporate Finance, fall 2015

Cases and mini-cases

Case Due date

Reeby Sport September 1

Marriott Corp. September 8

Bruce Honiball (mini) September 10

Mr Thorndike (mini) September 22

Crown October 6

Fall 2013 exam November 3

Fall 2014 exam November 5

As outlined in the course description, there are a total of five case write-ups, to be solved in groups of three to four students. Each write-up is due on the indicated date. A minimum requirement for taking the exam is that at least one case write-up has been handed in and approved. Each approved hand-in will give 4 points towards the final grade, for a maximum of 20 points. Any one case write-up may be replaced with two mini-case write-ups (at your choice). Case write-ups are graded as either approved (4 points) or not approved (0 points). Approval requires that the hand-in demonstrates an ability to analyze the material with a reasonable degree of judgment and independent thinking. The graded assignments will not be returned to students. Instead, for each case, a list of approved students will be posted on It’s Learning within 2-3 weeks of the due date. In addition, each case is carefully discussed in class. The case write-ups count for 20 percent of the total grade, while the final exam counts for 80% of the total grade. The points from case write-ups are valid only once, and in the term that they were earned. That is, if the exam is retaken at a later point in time, credits for case write-ups from the past will not be honored.

Note also that the assigned practice problems in MyFinanceLab must be solved on time in order to take the exam. Each home work carries equal weight and you must have at least 50% of the answers correct. That is, if you miss one practice problem set, you need 100% correct on the next practice problem set for an average of 50%. The course code in MyFinanceLab is XL21-I1YR-2020-3M02.

1

August 26, 2014

Instruction for handing in the FIE402N case write-ups

There has been some uncertainty regarding the format and the way to hand in the case write-ups. Here are instructions that should help clarify things:

1. I prefer you to hand in the case write-up printed out on paper, and give it to Thore in class. 2. If you have to send it electronically, send it to [email protected]. In the NHH address

list I am also listed with another e-mail address, [email protected] which has expired.

3. Include the full name of all group members on the hand-in. If you include only your student number, I am not able to map it to the list of course participants (I would have to look it up manually). If you send it by e-mail, include the name of all group members in both the e-mail and the written report.

4. Excel sheets are NOT necessary. However, you should include relevant tables and calculations from Excel in your report (copy tables from Excel into your report). Some students did not hand in “self contained” assignments, and satisfactory reports for some of the cases last year and therefore did not pass. Make sure you answer the questions asked, and that it is possible for me to briefly examine how you did your calculations and whether your assumptions are reasonable.

5. We will post a list of students who got a “Pass” grade on their hand-in on It’s learning. The list will be updated within 1-2 weeks after the deadline for each case.

6. If you handed in the case and did not get a “Pass” grade, please contact me at [email protected] as soon as possible. I might have made a mistake, since there are a lot of hand-ins both via It’s learning, e-mail and on paper.

Best regards

Jens Sørlie Kværner

Teaching Assistant FIE402N

1

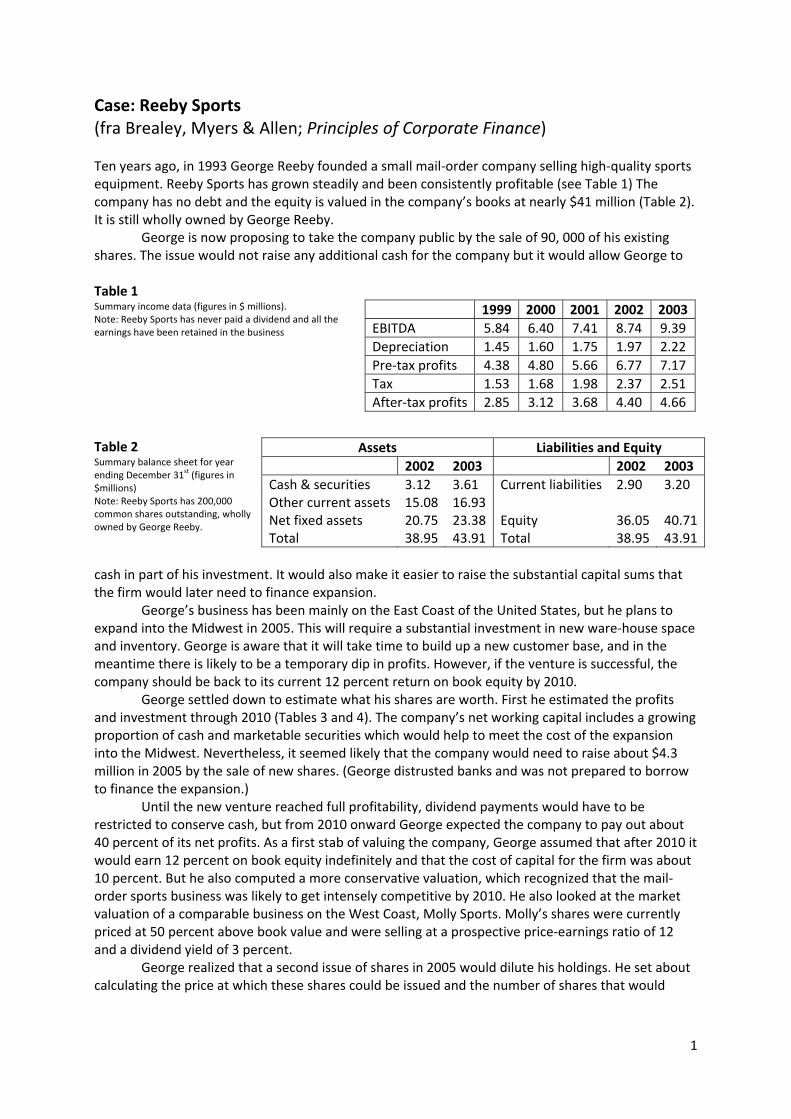

Case: Reeby Sports (fra Brealey, Myers & Allen; Principles of Corporate Finance) Ten years ago, in 1993 George Reeby founded a small mail‐order company selling high‐quality sports equipment. Reeby Sports has grown steadily and been consistently profitable (see Table 1) The company has no debt and the equity is valued in the company’s books at nearly $41 million (Table 2). It is still wholly owned by George Reeby.

George is now proposing to take the company public by the sale of 90, 000 of his existing shares. The issue would not raise any additional cash for the company but it would allow George to Table 1 Summary income data (figures in $ millions). Note: Reeby Sports has never paid a dividend and all the earnings have been retained in the business

Table 2 Summary balance sheet for year ending December 31

st (figures in

$millions) Note: Reeby Sports has 200,000 common shares outstanding, wholly owned by George Reeby.

cash in part of his investment. It would also make it easier to raise the substantial capital sums that the firm would later need to finance expansion.

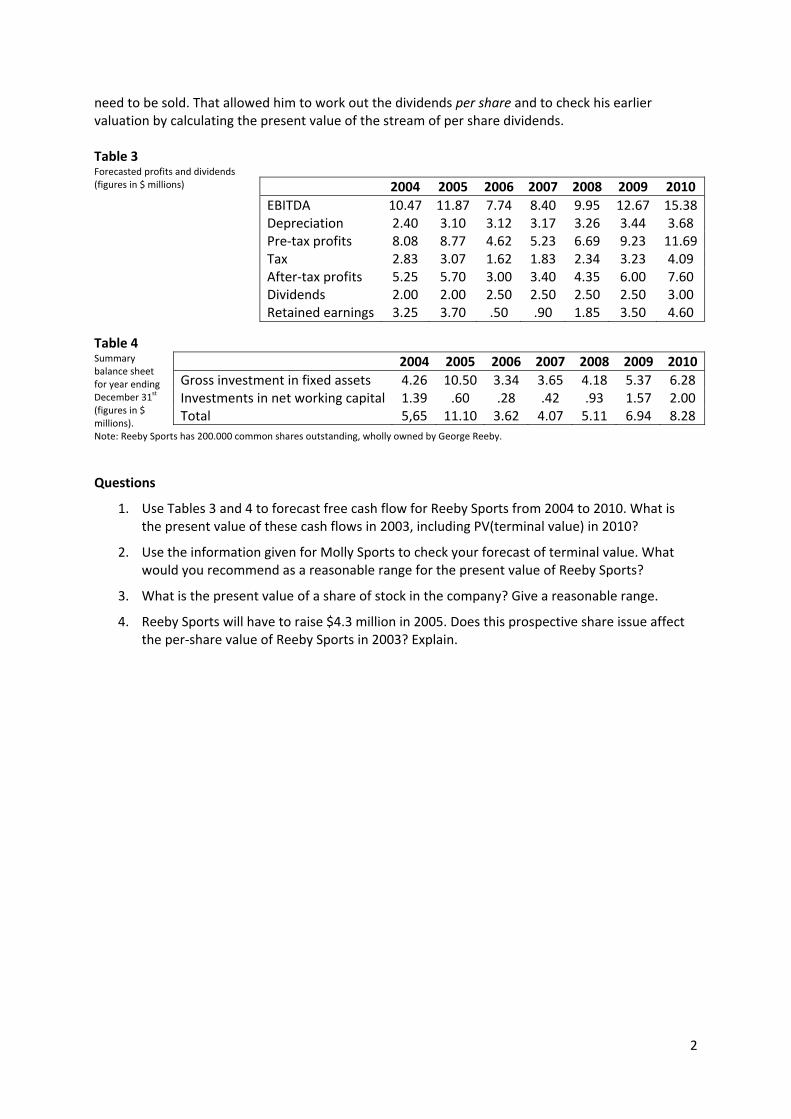

George’s business has been mainly on the East Coast of the United States, but he plans to expand into the Midwest in 2005. This will require a substantial investment in new ware‐house space and inventory. George is aware that it will take time to build up a new customer base, and in the meantime there is likely to be a temporary dip in profits. However, if the venture is successful, the company should be back to its current 12 percent return on book equity by 2010. George settled down to estimate what his shares are worth. First he estimated the profits and investment through 2010 (Tables 3 and 4). The company’s net working capital includes a growing proportion of cash and marketable securities which would help to meet the cost of the expansion into the Midwest. Nevertheless, it seemed likely that the company would need to raise about $4.3 million in 2005 by the sale of new shares. (George distrusted banks and was not prepared to borrow to finance the expansion.) Until the new venture reached full profitability, dividend payments would have to be restricted to conserve cash, but from 2010 onward George expected the company to pay out about 40 percent of its net profits. As a first stab of valuing the company, George assumed that after 2010 it would earn 12 percent on book equity indefinitely and that the cost of capital for the firm was about 10 percent. But he also computed a more conservative valuation, which recognized that the mail‐order sports business was likely to get intensely competitive by 2010. He also looked at the market valuation of a comparable business on the West Coast, Molly Sports. Molly’s shares were currently priced at 50 percent above book value and were selling at a prospective price‐earnings ratio of 12 and a dividend yield of 3 percent. George realized that a second issue of shares in 2005 would dilute his holdings. He set about calculating the price at which these shares could be issued and the number of shares that would

1999 2000 2001 2002 2003

EBITDA 5.84 6.40 7.41 8.74 9.39

Depreciation 1.45 1.60 1.75 1.97 2.22

Pre‐tax profits 4.38 4.80 5.66 6.77 7.17

Tax 1.53 1.68 1.98 2.37 2.51

After‐tax profits 2.85 3.12 3.68 4.40 4.66

Assets Liabilities and Equity

2002 2003 2002 2003

Cash & securities 3.12 3.61 Current liabilities 2.90 3.20 Other current assets 15.08 16.93 Net fixed assets 20.75 23.38 Equity 36.05 40.71Total 38.95 43.91 Total 38.95 43.91

2

need to be sold. That allowed him to work out the dividends per share and to check his earlier valuation by calculating the present value of the stream of per share dividends. Table 3 Forecasted profits and dividends (figures in $ millions)

Table 4 Summary balance sheet for year ending December 31

st

(figures in $ millions). Note: Reeby Sports has 200.000 common shares outstanding, wholly owned by George Reeby.

Questions

1. Use Tables 3 and 4 to forecast free cash flow for Reeby Sports from 2004 to 2010. What is the present value of these cash flows in 2003, including PV(terminal value) in 2010?

2. Use the information given for Molly Sports to check your forecast of terminal value. What would you recommend as a reasonable range for the present value of Reeby Sports?

3. What is the present value of a share of stock in the company? Give a reasonable range.

4. Reeby Sports will have to raise $4.3 million in 2005. Does this prospective share issue affect the per‐share value of Reeby Sports in 2003? Explain.

2004 2005 2006 2007 2008 2009 2010

EBITDA 10.47 11.87 7.74 8.40 9.95 12.67 15.38Depreciation 2.40 3.10 3.12 3.17 3.26 3.44 3.68 Pre‐tax profits 8.08 8.77 4.62 5.23 6.69 9.23 11.69Tax 2.83 3.07 1.62 1.83 2.34 3.23 4.09 After‐tax profits 5.25 5.70 3.00 3.40 4.35 6.00 7.60 Dividends 2.00 2.00 2.50 2.50 2.50 2.50 3.00 Retained earnings 3.25 3.70 .50 .90 1.85 3.50 4.60

2004 2005 2006 2007 2008 2009 2010

Gross investment in fixed assets 4.26 10.50 3.34 3.65 4.18 5.37 6.28 Investments in net working capital 1.39 .60 .28 .42 .93 1.57 2.00 Total 5,65 11.10 3.62 4.07 5.11 6.94 8.28

FIE402N Corporate Finance / fall 2013

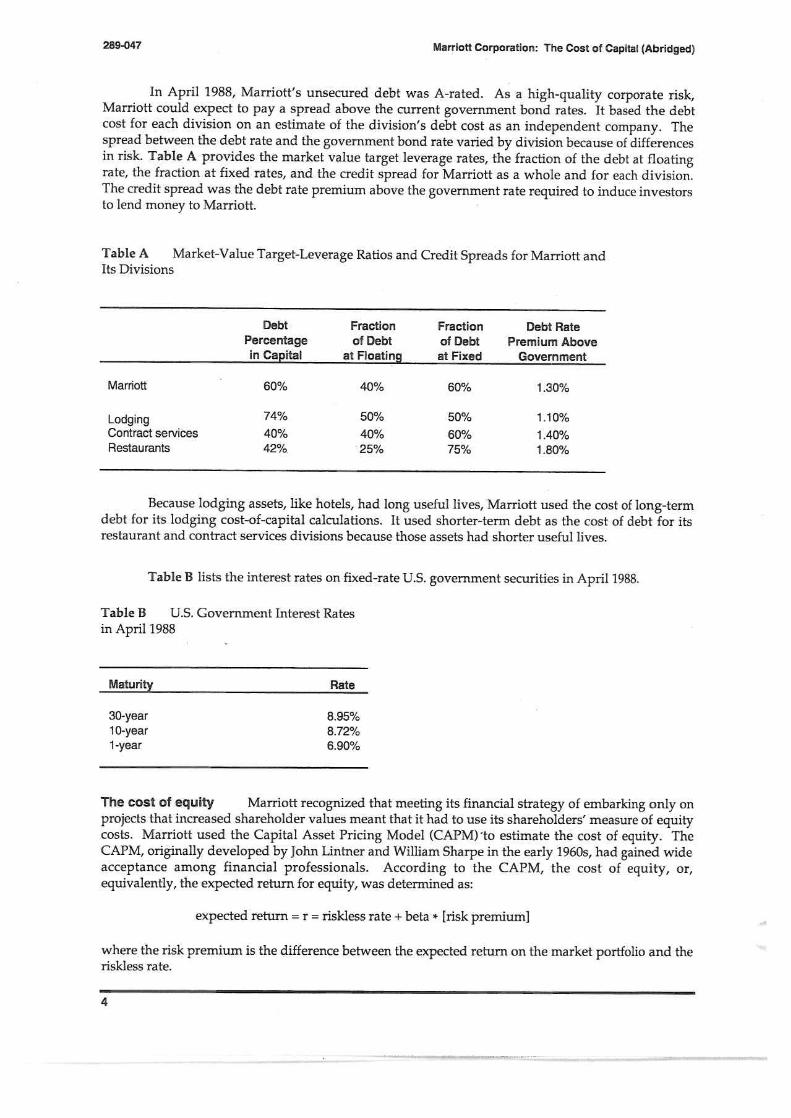

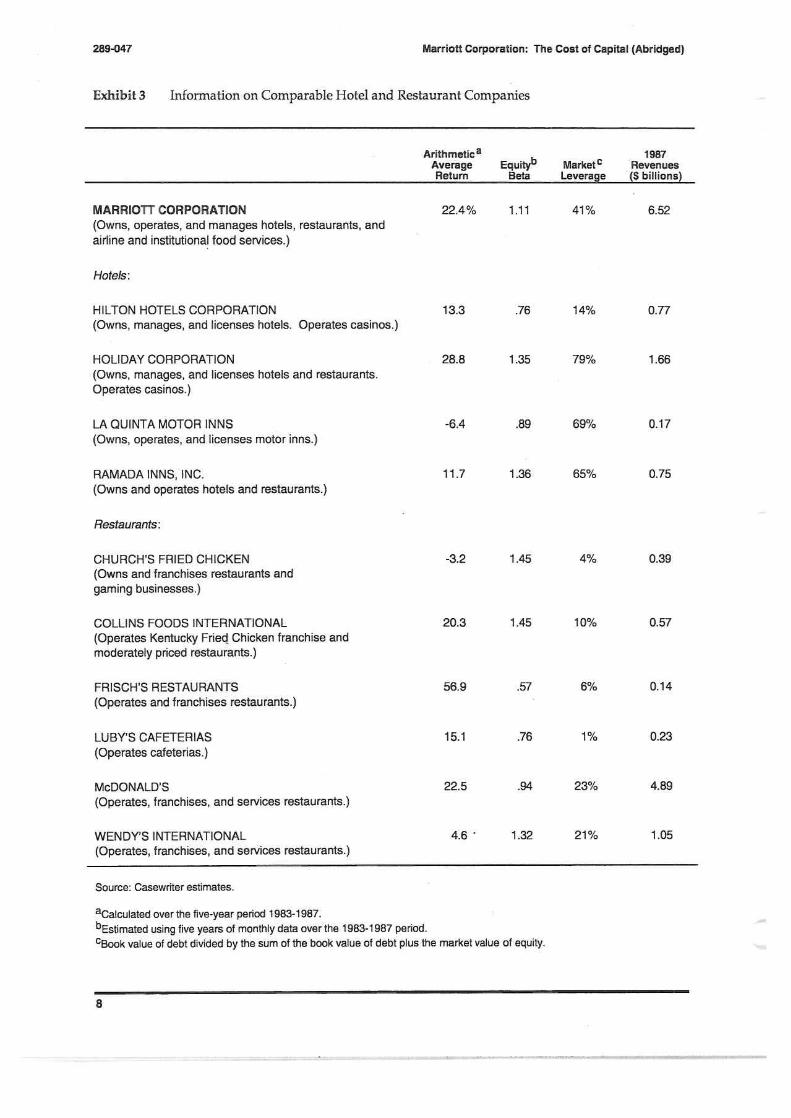

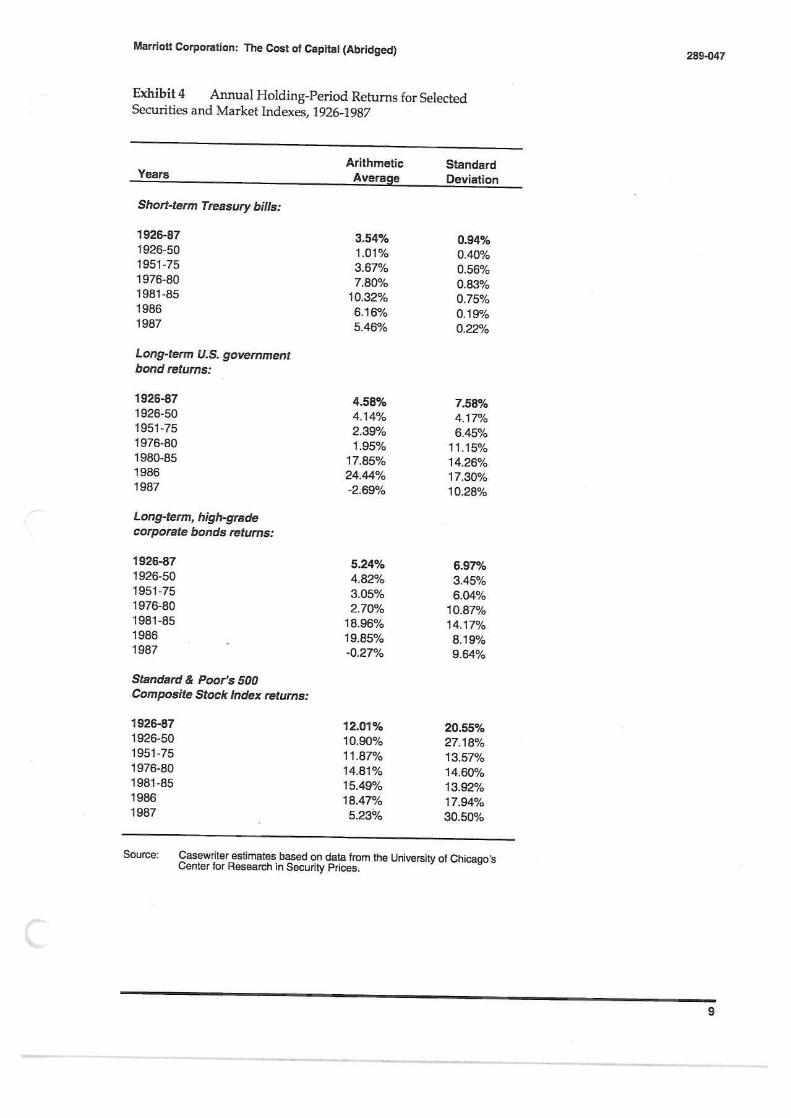

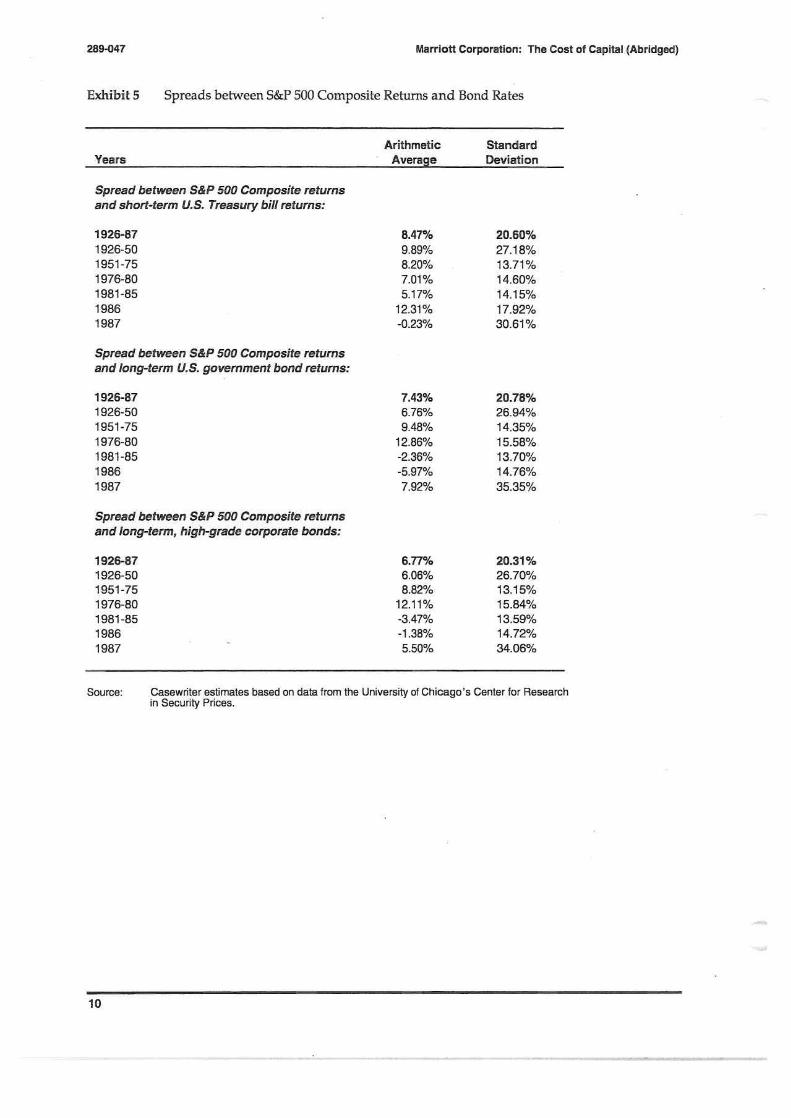

Marriott Corporation: Cost of Capital

Should be handed in at the beginning of (and will be discussed in) class on

Tuesday September 17

This is a group assignment that should be solved and written up in teams of 3-4 students. The write-up should be no more than 10 pages long plus tables.

QUESTIONS

1. What is the WACC (Weighted Average Cost of Capital) for Marriott Corporation?

a. What risk-free rate and market risk premium did you use to compute the company’s cost of equity?

b. How did you estimate Marriott’s cost of debt?

c. What type of investments would you value using Marriott’s WACC?

2. If Marriott used a single corporate cost of capital for evaluating investment opportunities

across its different divisions, how would this affect the company’s expected profitability over time?

3. What is the cost of capital for Marriott’s lodging and restaurant divisions?

a. How did you determine the cost of debt for each individual division? Should the divisions have a different cost of debt? Why or why not?

b. How did you measure the beta for each division?

4. What is the cost of capital for Marriott’s contract services division? How could you estimate the cost of equity for this division without knowing the cost of

equity for comparable publicly traded firms?

5. Calibrate your WACC estimates with the market’s valuation of Marriott. What implications do the observed return on capital employed (ROCE) and the accompanying market pricing have for your WACC estimate? For the company as a whole? For the individual divisions? Use a tax rate of 35% percent.

1

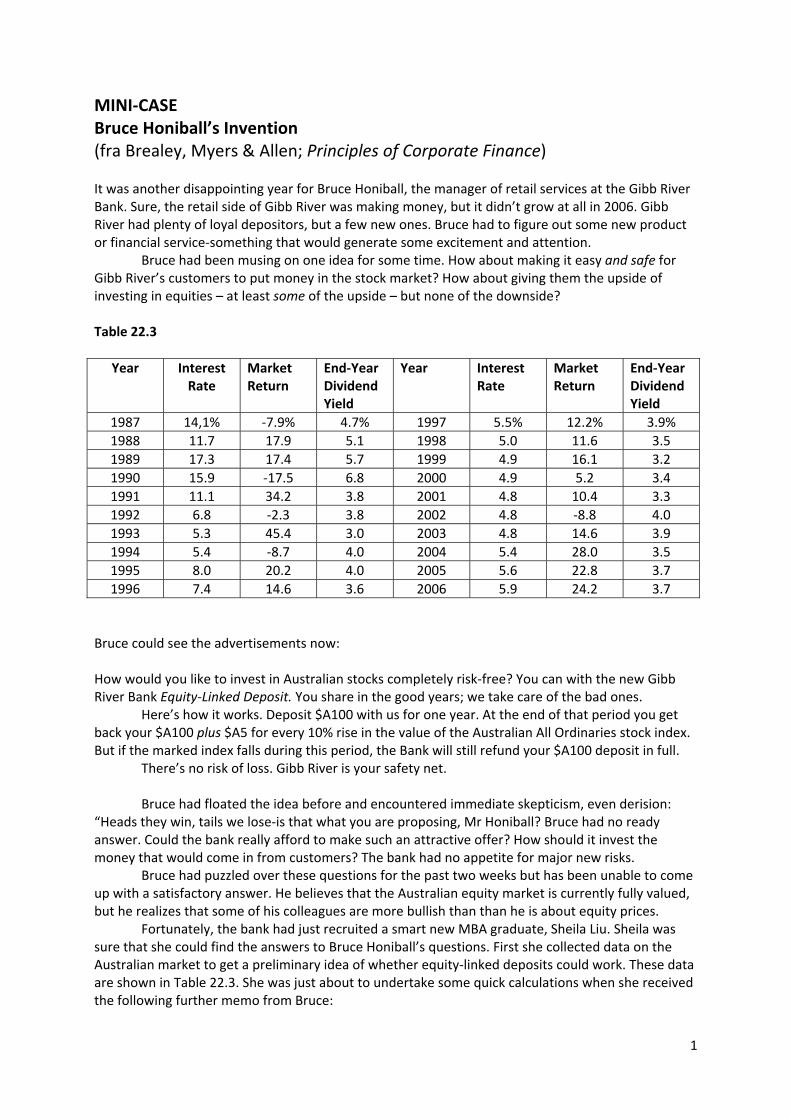

MINI‐CASE Bruce Honiball’s Invention (fra Brealey, Myers & Allen; Principles of Corporate Finance) It was another disappointing year for Bruce Honiball, the manager of retail services at the Gibb River Bank. Sure, the retail side of Gibb River was making money, but it didn’t grow at all in 2006. Gibb River had plenty of loyal depositors, but a few new ones. Bruce had to figure out some new product or financial service‐something that would generate some excitement and attention. Bruce had been musing on one idea for some time. How about making it easy and safe for Gibb River’s customers to put money in the stock market? How about giving them the upside of investing in equities – at least some of the upside – but none of the downside? Table 22.3

Year Interest Rate

Market Return

End‐Year Dividend Yield

Year Interest Rate

Market Return

End‐Year Dividend Yield

1987 14,1% ‐7.9% 4.7% 1997 5.5% 12.2% 3.9%

1988 11.7 17.9 5.1 1998 5.0 11.6 3.5

1989 17.3 17.4 5.7 1999 4.9 16.1 3.2

1990 15.9 ‐17.5 6.8 2000 4.9 5.2 3.4

1991 11.1 34.2 3.8 2001 4.8 10.4 3.3

1992 6.8 ‐2.3 3.8 2002 4.8 ‐8.8 4.0

1993 5.3 45.4 3.0 2003 4.8 14.6 3.9

1994 5.4 ‐8.7 4.0 2004 5.4 28.0 3.5

1995 8.0 20.2 4.0 2005 5.6 22.8 3.7

1996 7.4 14.6 3.6 2006 5.9 24.2 3.7

Bruce could see the advertisements now: How would you like to invest in Australian stocks completely risk‐free? You can with the new Gibb River Bank Equity‐Linked Deposit. You share in the good years; we take care of the bad ones. Here’s how it works. Deposit $A100 with us for one year. At the end of that period you get back your $A100 plus $A5 for every 10% rise in the value of the Australian All Ordinaries stock index. But if the marked index falls during this period, the Bank will still refund your $A100 deposit in full. There’s no risk of loss. Gibb River is your safety net. Bruce had floated the idea before and encountered immediate skepticism, even derision: “Heads they win, tails we lose‐is that what you are proposing, Mr Honiball? Bruce had no ready answer. Could the bank really afford to make such an attractive offer? How should it invest the money that would come in from customers? The bank had no appetite for major new risks. Bruce had puzzled over these questions for the past two weeks but has been unable to come up with a satisfactory answer. He believes that the Australian equity market is currently fully valued, but he realizes that some of his colleagues are more bullish than than he is about equity prices. Fortunately, the bank had just recruited a smart new MBA graduate, Sheila Liu. Sheila was sure that she could find the answers to Bruce Honiball’s questions. First she collected data on the Australian market to get a preliminary idea of whether equity‐linked deposits could work. These data are shown in Table 22.3. She was just about to undertake some quick calculations when she received the following further memo from Bruce:

2

Sheila, I’ve got another idea. A lot of our customers probably share my view that the market is overvalued. Why don’t we also give them a chance to make some money by offering a “bear market deposit”? If the market goes up, they would just get back their $A100 deposit. If it goes down, they get their $A100 back plus $5 for each 10% that the market falls. Can you figure out whether we could do something like this? Bruce. QUESTION

1. What kind of options is Bruce proposing? How much would the options be worth? Would the equity‐linked and bear‐market deposits generate positive NPV for Gibb River Bank?

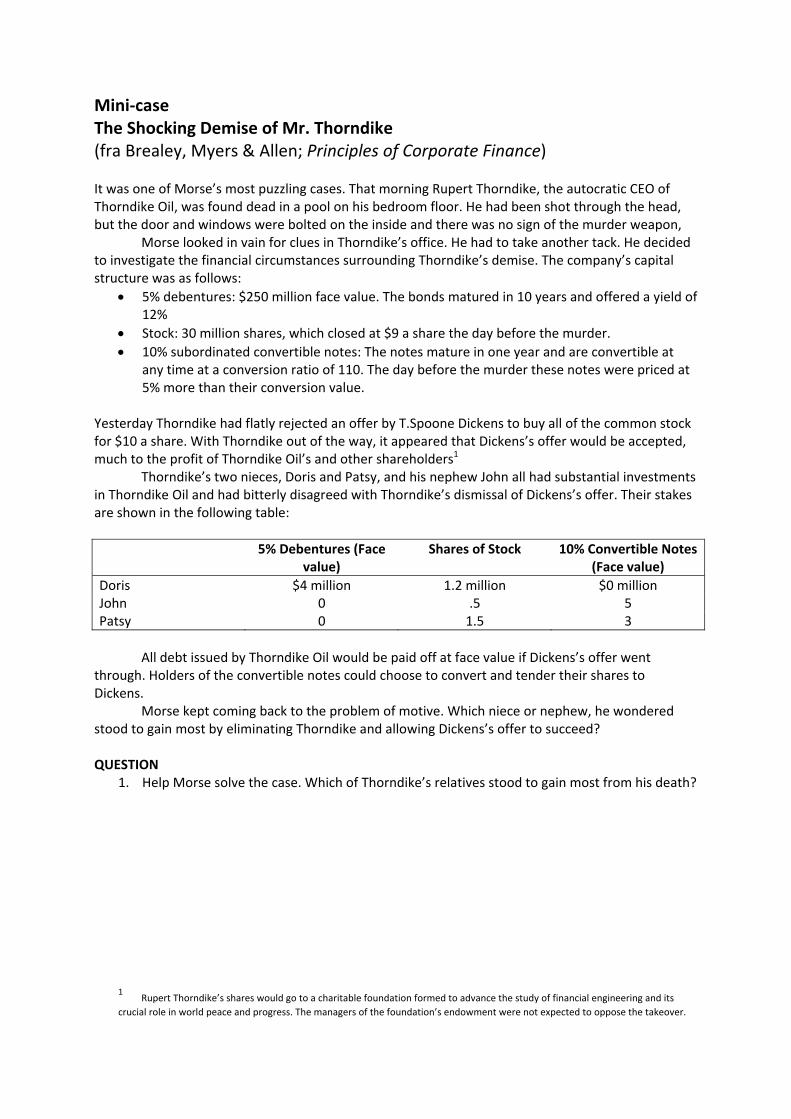

Mini‐case The Shocking Demise of Mr. Thorndike (fra Brealey, Myers & Allen; Principles of Corporate Finance) It was one of Morse’s most puzzling cases. That morning Rupert Thorndike, the autocratic CEO of Thorndike Oil, was found dead in a pool on his bedroom floor. He had been shot through the head, but the door and windows were bolted on the inside and there was no sign of the murder weapon, Morse looked in vain for clues in Thorndike’s office. He had to take another tack. He decided to investigate the financial circumstances surrounding Thorndike’s demise. The company’s capital structure was as follows:

5% debentures: $250 million face value. The bonds matured in 10 years and offered a yield of 12%

Stock: 30 million shares, which closed at $9 a share the day before the murder.

10% subordinated convertible notes: The notes mature in one year and are convertible at any time at a conversion ratio of 110. The day before the murder these notes were priced at 5% more than their conversion value.

Yesterday Thorndike had flatly rejected an offer by T.Spoone Dickens to buy all of the common stock for $10 a share. With Thorndike out of the way, it appeared that Dickens’s offer would be accepted, much to the profit of Thorndike Oil’s and other shareholders1 Thorndike’s two nieces, Doris and Patsy, and his nephew John all had substantial investments in Thorndike Oil and had bitterly disagreed with Thorndike’s dismissal of Dickens’s offer. Their stakes are shown in the following table:

5% Debentures (Face value)

Shares of Stock 10% Convertible Notes (Face value)

Doris $4 million 1.2 million $0 million John 0 .5 5 Patsy 0 1.5 3

All debt issued by Thorndike Oil would be paid off at face value if Dickens’s offer went through. Holders of the convertible notes could choose to convert and tender their shares to Dickens. Morse kept coming back to the problem of motive. Which niece or nephew, he wondered stood to gain most by eliminating Thorndike and allowing Dickens’s offer to succeed? QUESTION

1. Help Morse solve the case. Which of Thorndike’s relatives stood to gain most from his death?

1 Rupert Thorndike’s shares would go to a charitable foundation formed to advance the study of financial engineering and its

crucial role in world peace and progress. The managers of the foundation’s endowment were not expected to oppose the takeover.

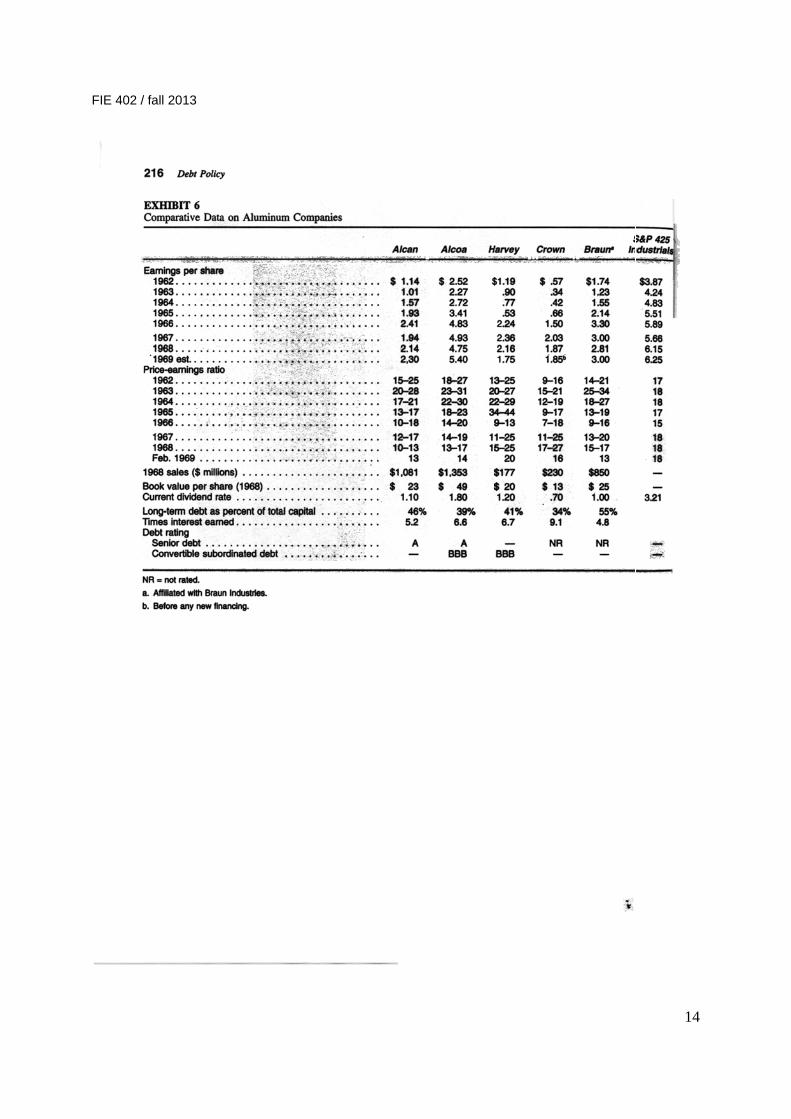

FIE 402 / fall 2013

1

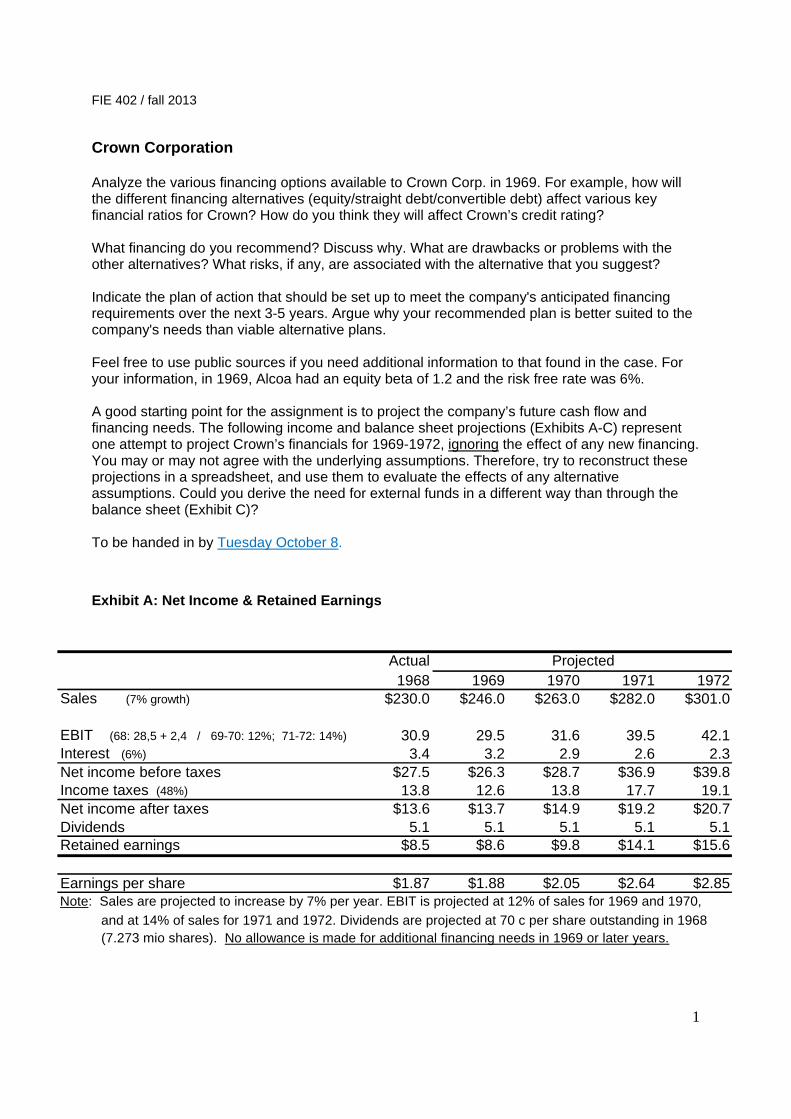

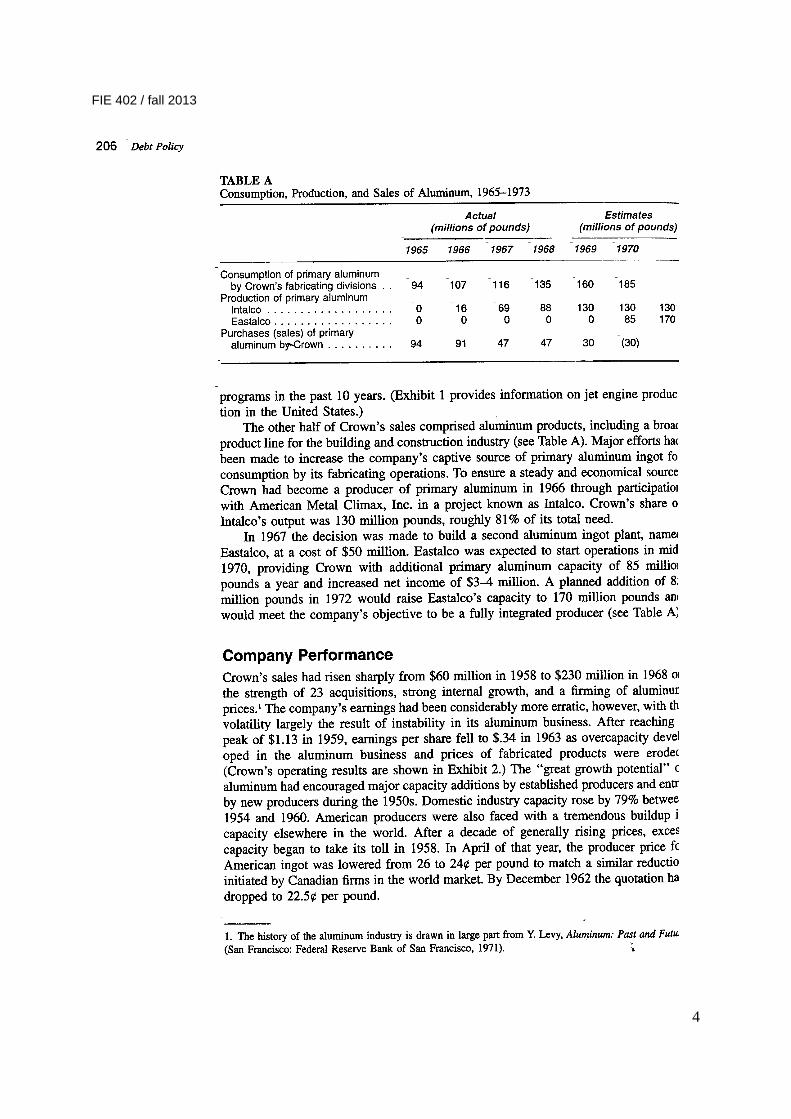

Crown Corporation

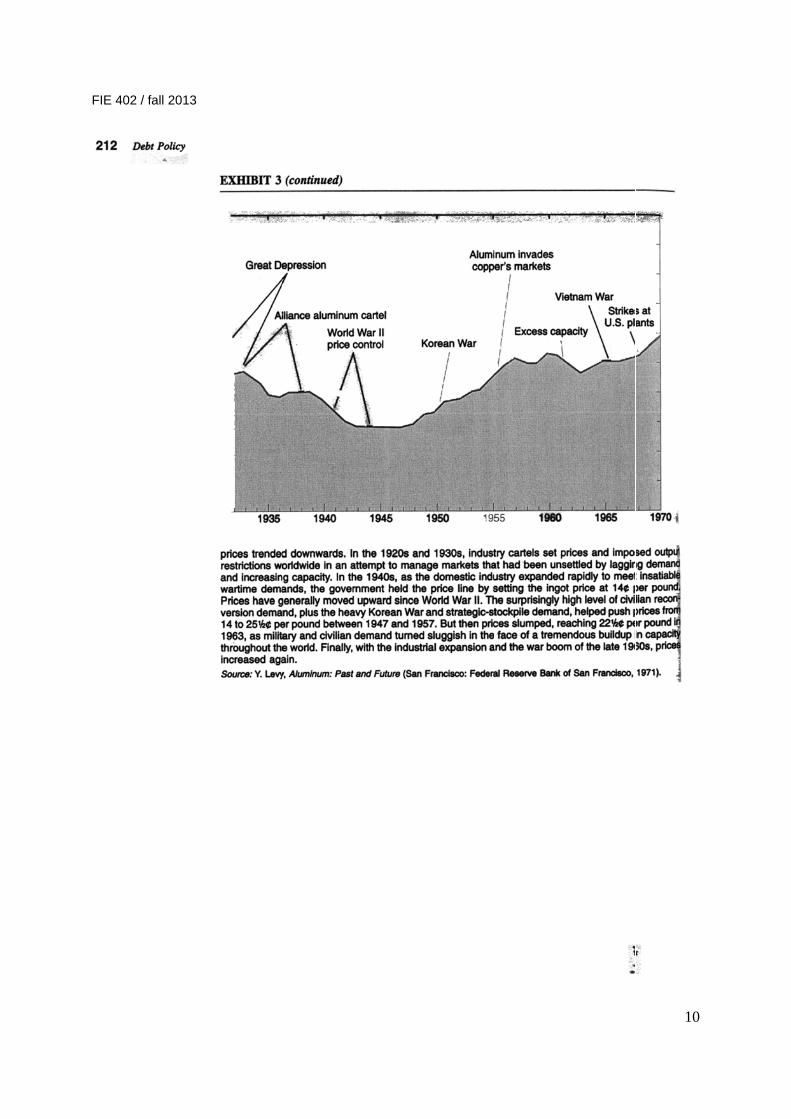

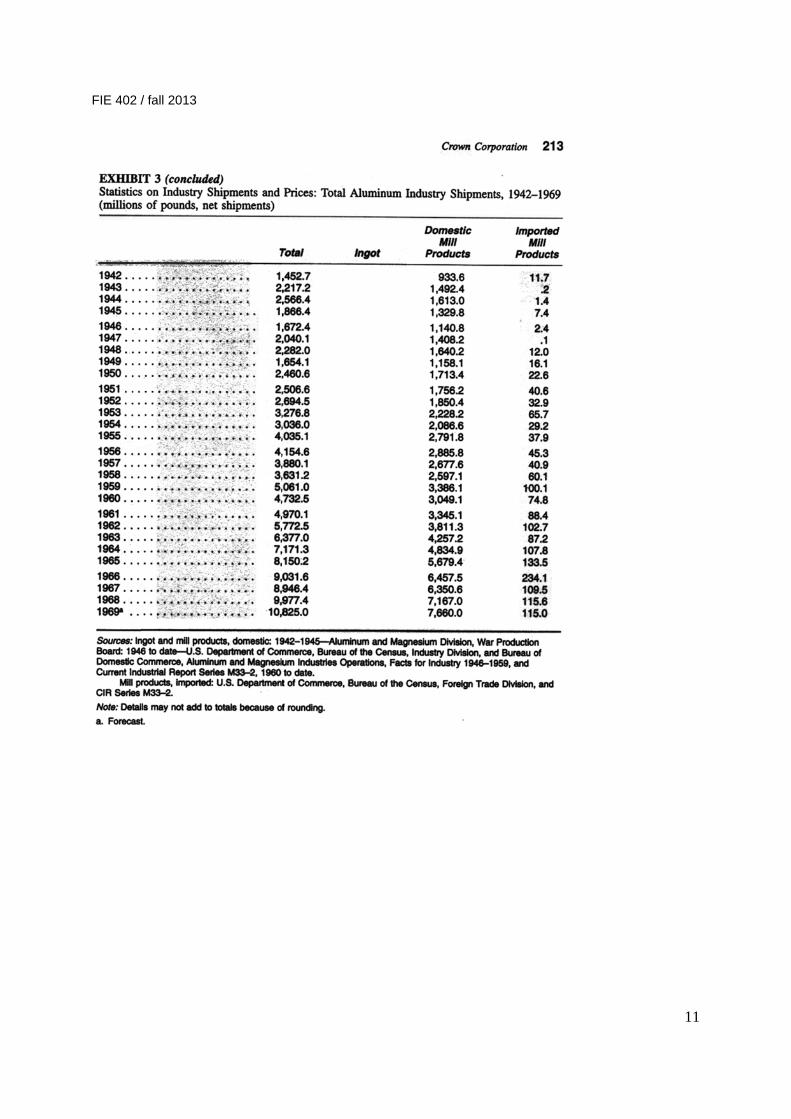

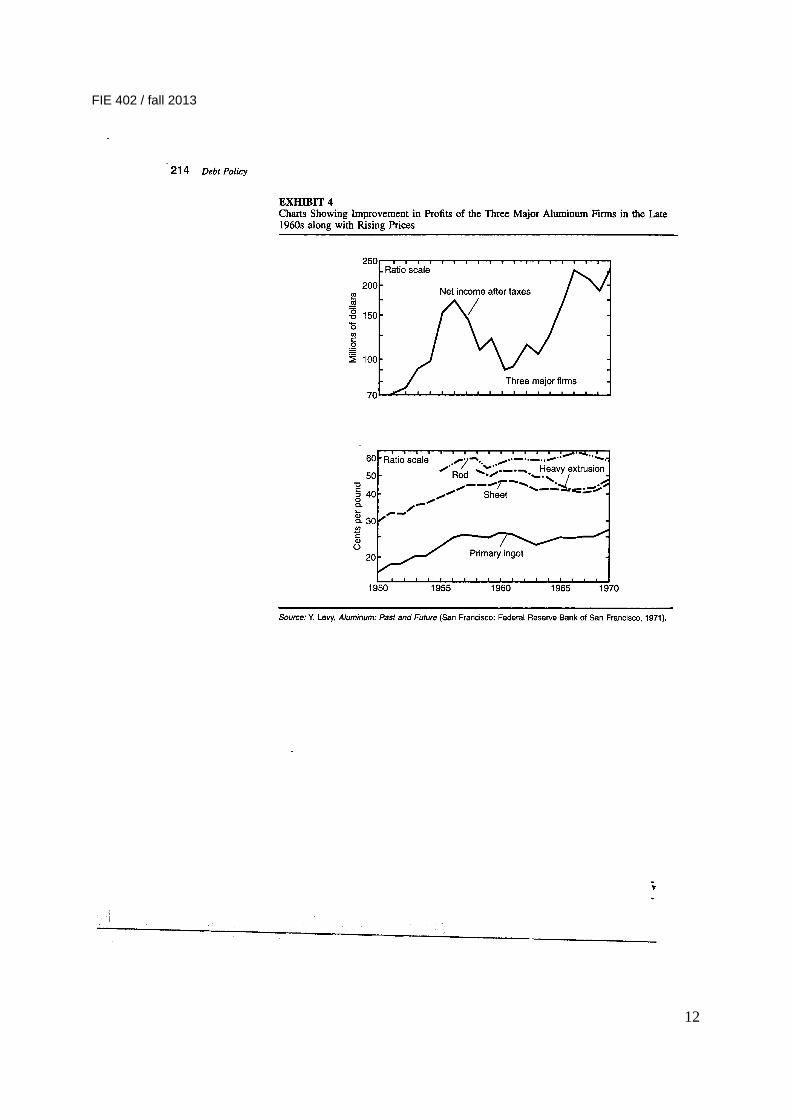

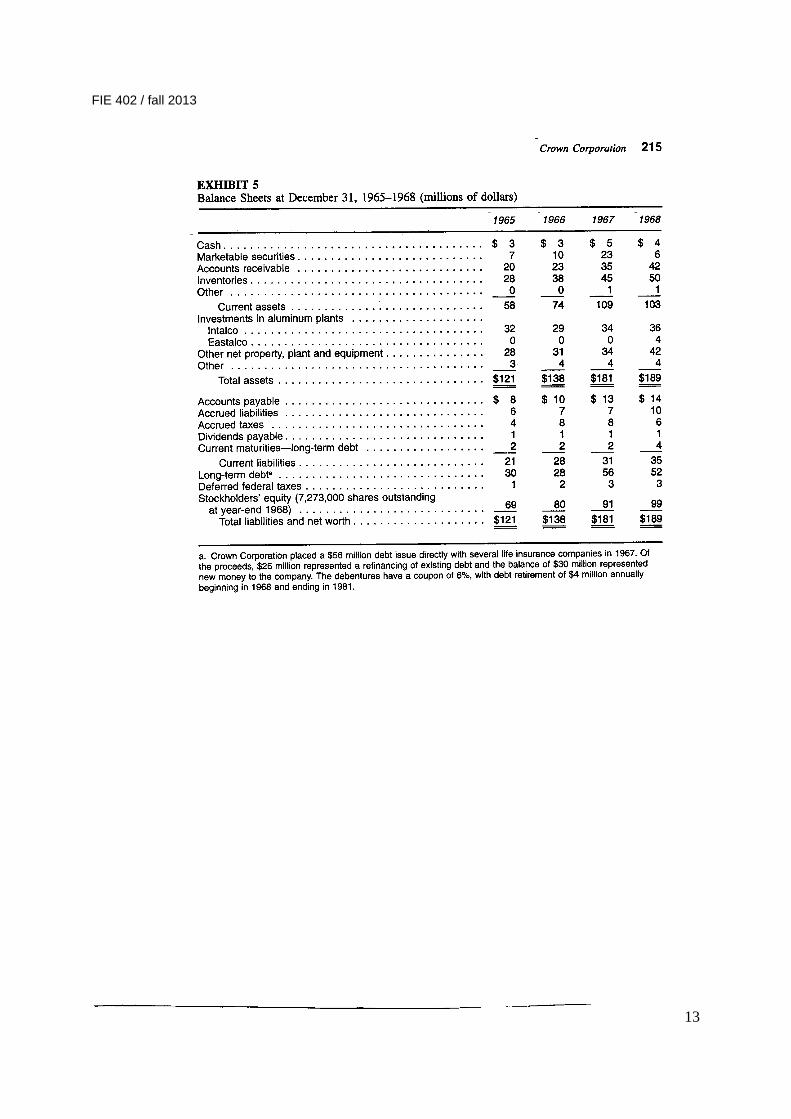

Analyze the various financing options available to Crown Corp. in 1969. For example, how will the different financing alternatives (equity/straight debt/convertible debt) affect various key financial ratios for Crown? How do you think they will affect Crown’s credit rating? What financing do you recommend? Discuss why. What are drawbacks or problems with the other alternatives? What risks, if any, are associated with the alternative that you suggest? Indicate the plan of action that should be set up to meet the company's anticipated financing requirements over the next 3-5 years. Argue why your recommended plan is better suited to the company's needs than viable alternative plans. Feel free to use public sources if you need additional information to that found in the case. For your information, in 1969, Alcoa had an equity beta of 1.2 and the risk free rate was 6%. A good starting point for the assignment is to project the company’s future cash flow and financing needs. The following income and balance sheet projections (Exhibits A-C) represent one attempt to project Crown’s financials for 1969-1972, ignoring the effect of any new financing. You may or may not agree with the underlying assumptions. Therefore, try to reconstruct these projections in a spreadsheet, and use them to evaluate the effects of any alternative assumptions. Could you derive the need for external funds in a different way than through the balance sheet (Exhibit C)? To be handed in by Tuesday October 8.

Exhibit A: Net Income & Retained Earnings

Actual Projected1968 1969 1970 1971 1972

Sales (7% growth) $230.0 $246.0 $263.0 $282.0 $301.0

EBIT (68: 28,5 + 2,4 / 69-70: 12%; 71-72: 14%) 30.9 29.5 31.6 39.5 42.1Interest (6%) 3.4 3.2 2.9 2.6 2.3Net income before taxes $27.5 $26.3 $28.7 $36.9 $39.8Income taxes (48%) 13.8 12.6 13.8 17.7 19.1Net income after taxes $13.6 $13.7 $14.9 $19.2 $20.7Dividends 5.1 5.1 5.1 5.1 5.1Retained earnings $8.5 $8.6 $9.8 $14.1 $15.6

Earnings per share $1.87 $1.88 $2.05 $2.64 $2.85Note: Sales are projected to increase by 7% per year. EBIT is projected at 12% of sales for 1969 and 1970,

and at 14% of sales for 1971 and 1972. Dividends are projected at 70 c per share outstanding in 1968 (7.273 mio shares). No allowance is made for additional financing needs in 1969 or later years.

FIE 402 / fall 2013

2

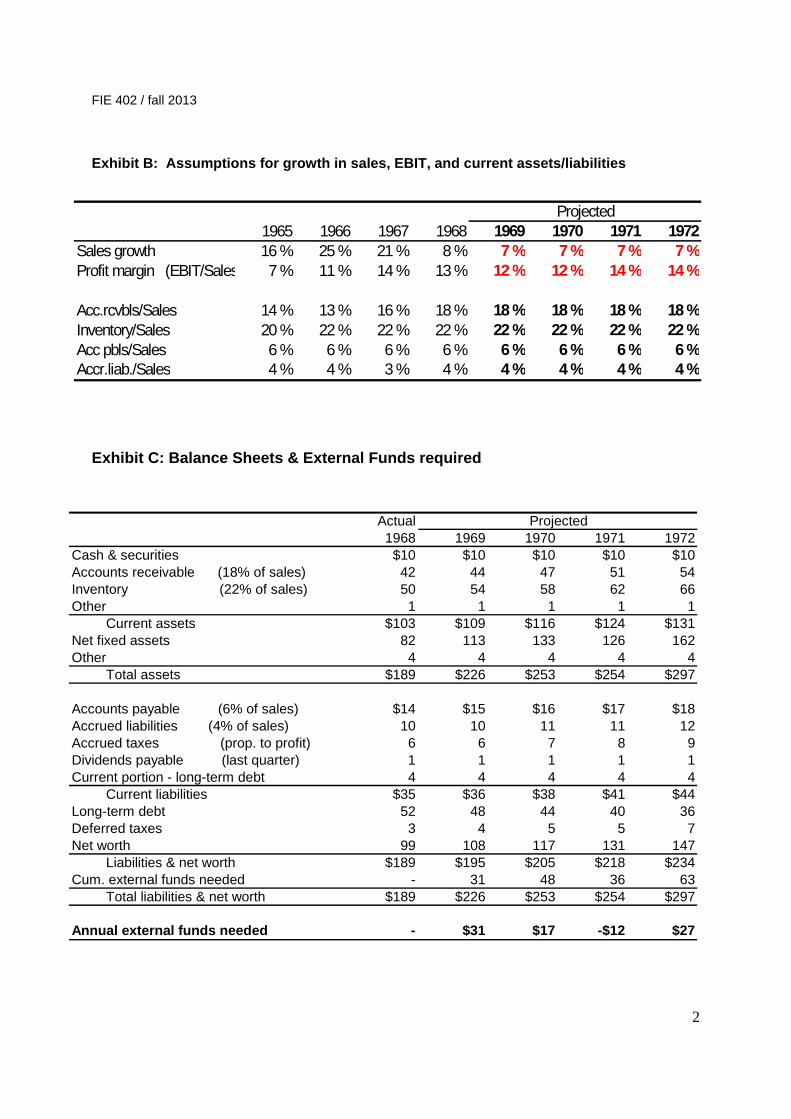

Exhibit B: Assumptions for growth in sales, EBIT, and current assets/liabilities

Exhibit C: Balance Sheets & External Funds required

Actual Projected1968 1969 1970 1971 1972

Cash & securities $10 $10 $10 $10 $10Accounts receivable (18% of sales) 42 44 47 51 54Inventory (22% of sales) 50 54 58 62 66Other 1 1 1 1 1 Current assets $103 $109 $116 $124 $131Net fixed assets 82 113 133 126 162Other 4 4 4 4 4 Total assets $189 $226 $253 $254 $297

Accounts payable (6% of sales) $14 $15 $16 $17 $18Accrued liabilities (4% of sales) 10 10 11 11 12Accrued taxes (prop. to profit) 6 6 7 8 9Dividends payable (last quarter) 1 1 1 1 1Current portion - long-term debt 4 4 4 4 4 Current liabilities $35 $36 $38 $41 $44Long-term debt 52 48 44 40 36Deferred taxes 3 4 5 5 7Net worth 99 108 117 131 147 Liabilities & net worth $189 $195 $205 $218 $234Cum. external funds needed - 31 48 36 63 Total liabilities & net worth $189 $226 $253 $254 $297

Annual external funds needed - $31 $17 -$12 $27

Projected1965 1966 1967 1968 1969 1970 1971 1972

Sales growth 16 % 25 % 21 % 8 % 7 % 7 % 7 % 7 %Profit margin (EBIT/Sales 7 % 11 % 14 % 13 % 12 % 12 % 14 % 14 %

Acc.rcvbls/Sales 14 % 13 % 16 % 18 % 18 % 18 % 18 % 18 %Inventory/Sales 20 % 22 % 22 % 22 % 22 % 22 % 22 % 22 %Acc pbls/Sales 6 % 6 % 6 % 6 % 6 % 6 % 6 % 6 %Accr.liab./Sales 4 % 4 % 3 % 4 % 4 % 4 % 4 % 4 %

FIE 402 / fall 2013

3

FIE 402 / fall 2013

4

FIE 402 / fall 2013

5

FIE 402 / fall 2013

6

FIE 402 / fall 2013

7

FIE 402 / fall 2013

8

FIE 402 /

/ fall 2013

9

FIE 402 /

/ fall 2013

10

FIE 402 /

/ fall 2013

11

FIE 402 / fall 2013

12

FIE 402 / fall 2013

13

FIE 402 /

/ fall 2013

14

1 of 8

NORWEGIAN SCHOOL OF ECONOMICS

Examination fall semester 2012 Code: FIE402N Title: Corporate Finance / Foretakets Finansiering Date: 19 November Time: 09:00-13:00 The course instructor will not visit the examination room, but may be contacted by an examination attendant at 59 291 or mob. 970 19 567

The students may respond in Norwegian or English. Materials permitted for use during the examination: Materials permitted: YES, cf list below: X Electronic calculator: YES: X In accordance with the rules specified in ”Utfyllende bestemmelser til Forskrift om eksamen ved Norges Handelshøyskole (fulltidsstudiene)” List of materials permitted: One dictionary

2 of 8

FIE 402 CORPORATE FINANCE FALL 2012 All five problems on the next six pages should be answered. The last sheet contains a collection of formulas, some of which may be useful during the exam. The stated time limits may be helpful in allocating your time among the questions — they are also the weights for the total grade. Short and precise answers are favored. PROBLEM 1. Multiple Choice (Q1 through Q10) (max 85 min) Q1 Which of the following statements is false? A. The intrinsic value of an option is the value it would have if it expired immediately. B. European option cannot be worth less than its American counterpart. C. A put option cannot be worth more than its strike price. D. Put options increase in value as the stock price falls.

Q2 Which of the following statements about M&A is false?

A. Cost-reduction synergies are hard to predict and achieve. B. Because the CEOs of small firms receive information so quickly, small firms are

often able to react in timely way to changes in the economic environment. C. Synergies usually fall into two categories: cost reductions and revenue

enhancements. D. There may also be costs associated with size.

Q3 Luther Industries currently has 100 million shares of stock outstanding at a price of $25 per share. The company would like to raise money and has announced a rights issue. Every existing shareholder will be sent one right per share of stock that he or she owns. The company plans to require twenty rights to purchase one share at a price of $20 per share. The amount of money that Luther will raise through its rights offering is closest to: A. $125 million B. $500 million C. $100 million D. $400 million

3 of 8

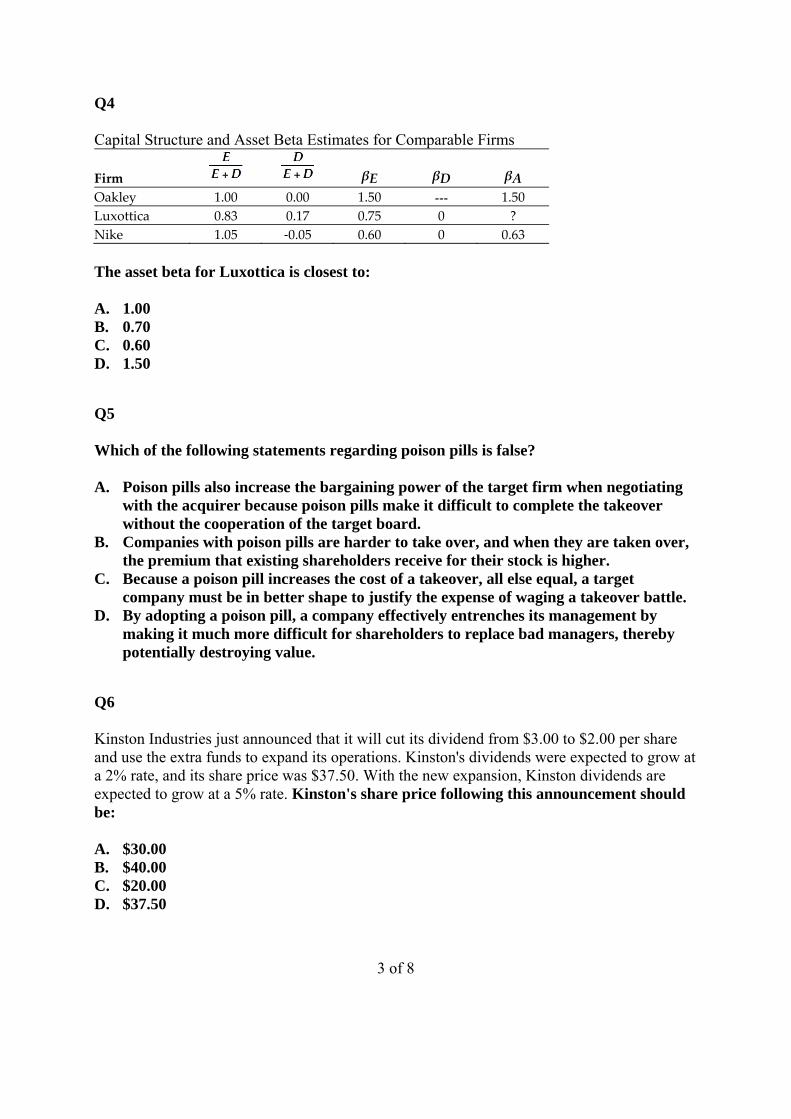

Q4 Capital Structure and Asset Beta Estimates for Comparable Firms

Firm βE βD βA

Oakley 1.00 0.00 1.50 --- 1.50

Luxottica 0.83 0.17 0.75 0 ?

Nike 1.05 -0.05 0.60 0 0.63

The asset beta for Luxottica is closest to: A. 1.00 B. 0.70 C. 0.60 D. 1.50

Q5 Which of the following statements regarding poison pills is false? A. Poison pills also increase the bargaining power of the target firm when negotiating

with the acquirer because poison pills make it difficult to complete the takeover without the cooperation of the target board.

B. Companies with poison pills are harder to take over, and when they are taken over, the premium that existing shareholders receive for their stock is higher.

C. Because a poison pill increases the cost of a takeover, all else equal, a target company must be in better shape to justify the expense of waging a takeover battle.

D. By adopting a poison pill, a company effectively entrenches its management by making it much more difficult for shareholders to replace bad managers, thereby potentially destroying value.

Q6 Kinston Industries just announced that it will cut its dividend from $3.00 to $2.00 per share and use the extra funds to expand its operations. Kinston's dividends were expected to grow at a 2% rate, and its share price was $37.50. With the new expansion, Kinston dividends are expected to grow at a 5% rate. Kinston's share price following this announcement should be: A. $30.00 B. $40.00 C. $20.00 D. $37.50

4 of 8

Q7 You founded your own firm three years ago. You initially contributed $200,000 of your own money and in return you received 2 million shares of stock. Since then, you have sold an additional 1 million shares of stock to angel investors. You are now considering raising capital from a venture capital firm. This venture capital firm would invest $5 million and would receive 2 million newly issued shares in return. The post-money valuation of your firm is closest to: A. $10.0 million B. $5.0 million C. $12.5 million D. $5.2 million

Q8 Luther Industries is currently trading for $27 per share. The stock pays no dividends. A one-year European put option on Luther with a strike price of $30 is currently trading for $2.60. The risk-free interest rate is 6% per year. The price of a one-year European call option on Luther with a strike price of $30 will be closest to: A. $1.30 B. $7.10 C. $1.95 D. $2.60

Q9 Which of the following is not one of the four characteristics of IPOs that puzzle financial economists? A. On average, IPOs appear to be underpriced. B. The long-run performance of a newly public company (three to five years from the

date of issue) is superior to the overall market return. C. The number of issues is highly cyclical. D. The costs of the IPO are very high, and it is unclear why firms willingly incur such

high costs.

5 of 8

Q10 Which of the following statements about a firm’s pay-out policy is false? A. Managers are much less committed to dividend payments than to share

repurchases. B. Share repurchases are a credible signal that the shares are under-priced, because if

they are over-priced a share repurchase is costly for current shareholders. C. While an increase of a firm’s dividend may signal management’s optimism

regarding its future cash flows, it might also signal a lack of investment opportunities.

D. Managers will clearly be more likely to repurchase shares if they believe the stock to be under-valued.

PROBLEM 2. Valuation and cost of capital (45 min) A company has total assets of $ 1 000 million at book value, and is funded with $ 400 million of interest bearing liabilities (debt), 200 million of other liabilities and $ 400 million in equity. The average interest cost of the debt is 6%, which also corresponds to the cost of new debt. The tax rate is 35%. The 10 million shares outstanding are trading at twice book value per share. The firm is expected to pay a constant fraction of yearly earnings as dividends, and not to issue/repurchase shares. The stock is expected to earn a dividend return of 4%. The risk free rate is 4%, the market risk premium is 5% and the stock’s beta is 1.2. a) Determine the firm’s cost of equity and the expected yearly growth in dividends

(implicit in the current price). b) Determine the firm’s expected return on equity (ROE), and separate the stock price

into static and PVGO value. Explain. The firm is expected to maintain a constant debt to equity ratio, in market value terms. c) Determine the firm’s WACC, ROCE (after tax return on capital employed), and

next year’s total EVA. d) Show that the added Enterprise Value relative to Capital Employed may be

determined directly by the sum discounted values of future expected EVAs. Explain.

e) Alternatively, determine the added Market value of Equity relative to the book value by the sum discounted values of Residual Income (“super profit”). Explain any difference to your analysis of EVA and Enterprise Value added in questions c-d).

6 of 8

PROBLEM 3. Equity Rights Issue (40 min) A company is planning a rights issue at $10 a share of one new share per four shares held. Before the issue there were 10 million shares outstanding, and the share price was $12. a) Determine the number of shares issued and the prospective stock price after the

issue. b) Current shareholders receive one Right per share held. Determine the value of each

right. Explain c) For a stockholder holding four shares before the issue, compare her financial

situation before and after the issue, and dependent upon whether she uses or sells her rights. Explain.

Suppose they issue the new shares at $8 per share instead of $10. d) Redo questions a-b) above and explain differences in your answers. e) Are the current shareholders any better off with this lower issue price? Why/why

not? PROBLEM 4. Mergers and Acquisitions (40 min) Rearden Metal has earnings per share of $2. It has 10 million shares outstanding and is trading at $20 per share. Rearden Metal is thinking of buying Associated Steel, which has earnings per share of $1.25, 4 million shares outstanding, and a price per share of $15. Rearden Metal will pay for Associated Steel by issuing new shares. There are no expected synergies from the transaction. Assume that Rearden offers an exchange ratio such that, at current pre-announcement share prices for both firms, the offer represents a 20% price premium to buy Associated Steel.

a) Determine the total number of shares offered to the owners of Associated Steel and earnings per share for Rearden Metal after the merger.

b) What will be the price per share for Associated Steel immediately after the

announcement of Rearden’s offer? Explain.

c) What will be the price per share for Rearden Metal immediately after the announcement of Rearden’s offer? Explain.

d) What is the premium Rearden will actually end up paying for Associated Steel?

7 of 8

PROBLEM 5. Convertible Bond (max 30 min) A company is considering making a $ 100 million convertible bond issue. Each bond having a $ 1 000 face value and paying a yearly coupon of 5 %. 5 year length with full repayment at maturity and no bond call. Conversion price of $ 25 per share. The company’s shares are trading at $ 20, and are not expected to pay any dividend within the 5 years’ period. The risk free rate is 4.60%, the stock’s beta is 1.2, and the firm may alternatively raise 5 year’s straight, subordinated debt at 8%. a) Determine the implicit value of the conversion rights of the issue. b) Using the 0.4-rule, determine the implicit volatility (p.a.) used in pricing the

conversion rights (the warrants). What do you think of the pricing of the issue? Assume now, that the company’s shares are assumed to pay a constant dividend of $ 1 per share for each of the five years. c) Redo question b), and explain the difference.

8 of 8

Useful formulas ??

X)PV(F0,5 PV(F)Tσ0,4 C

11 DBE

EBITt)(1ROCE

1BE

EROE

g-k

d = p 1

WACC = Rf + A MP + Debt

DEU βDτ)-(1 E

Dβ

Dτ)-(1 E

E β

1 n

xp

n

x q t

g -k

1] -/k [RInv +

k

E = V

*1

*

1

DEA βD E

Dβ

D E

E β

AA

T

/nV

S V x

1 of 11

NORWEGIAN SCHOOL OF ECONOMICS

Examination fall semester 2013 Code: FIE402N Title: Corporate Finance / Foretakets Finansiering Date: 18 November Time: 09:00-13:00 The course instructor will not visit the examination room, but may be contacted by an examination attendant at 59 291 or mob. 970 19 567

• The students may respond in Norwegian or English. Materials permitted for use during the examination: Materials permitted: YES, cf list below: X Electronic calculator: YES: X In accordance with the rules specified in ”Utfyllende bestemmelser til Forskrift om eksamen ved Norges Handelshøyskole (fulltidsstudiene)” List of materials permitted: One dictionary

2 of 11

FIE 402 CORPORATE FINANCE FALL 2013 All four problem sets on the next six pages should be answered. The last sheet contains a collection of formulas, some of which may be useful during the exam. The stated time limits may be helpful in allocating your time among the questions — they are also the weights for the total grade. Short and precise answers are favored. PROBLEM 1. Multiple Choice (Q1 through Q12) (max 85 min) Q1 Which of the following is NOT one of Modigliani and Miller's set of conditions referred to as perfect capital markets?

A) All investors hold the efficient portfolio of assets. B) There are no taxes, transaction costs, or issuance costs associated with security

trading. C) A firm's financing decisions do not change the cash flows generated by its

investments, nor do they reveal new information about them. D) Investors and firms can trade the same set of securities at competitive market prices

equal to the present value of their future cash flows. Q2 White Rock Energy had a net income of $ 78 million last year, and a free cash flow (FCF) of $ 52 million. The company repurchased 1 million shares at $ 10 per share. Furthermore, the company retained 40 % of last year’s net income (increased its cash holding) and increased the net debt by $ 12 million. After-tax interest expenses were $ 4 million. How much did White Rock pay in dividends?

A) $ 10 million B) $ 10.8 million C) $ 18.8 million D) $ 26 million

3 of 11

Q3 Compare a convertible bond with an otherwise identical bond without a conversion feature. Which of the following statements is TRUE?

A) Yield is determined by the risk free rate and credit spread, and is unaffected by the conversion feature. Both bonds will have the same coupon.

B) The option to convert stock into bond is valuable, hence the price of the convertible will be lower and its coupon is higher.

C) The option to convert bond into stock is valuable, hence the price of the convertible will be lower and its coupon is higher.

D) The option to convert bond into stock is valuable, hence the price of the convertible will be higher and its coupon is lower.

Q4 The shares in Luther Industries are trading at $100. The company has just paid a dividend of $4.50 per share, and the dividend is expected to grow at a constant rate. Luther has a cost of equity capital of 12%. The grow rate of Luther's dividends are closest to:

A) 7.0% B) 7.5% C) 16.5% D) 12%

Q5 Which of the following statements is FALSE?

A) After deciding to go public, managers of the company work with an underwriter, an investment banking firm that manages the offering and designs its structure.

B) The shares that are sold in the IPO may either be new shares that raise new capital, known as a secondary offering, or existing shares that are sold by current shareholders (as part of their exit strategy), known as a primary offering.

C) Many IPOs, especially the larger offerings, are managed by a group of underwriters. D) At an IPO, a firm offers a large block of shares for sale to the public for the first time.

4 of 11

Q6 Which of the following statements is FALSE?

A) The option price is more sensitive to changes in volatility for at-the-money options than it is for in-the-money options.

B) A share of stock can be thought of as a put option on the assets of the firm with a strike price equal to the value of debt outstanding.

C) In the context of corporate finance, equity is at-the-money when a firm is close to bankruptcy.

D) Because the price of equity is increasing with the volatility of the firm's assets, equity holders benefit from a zero-NPV project that increases the volatility of the firm's assets.

Q7 You work for a leveraged buyout firm and are evaluating a potential buyout of Barrick Mining. Barrick Mining’s stock price is $15 and it has 10 million shares outstanding. You believe that if you buy the company and replace its management, its value will increase by 50%. You are planning on doing a leveraged buyout of Barrick Mining, and will offer $20 per share for control of the company. Assume American legislation, such that the buyer is allowed to consolidate the debt. Assume that you get 50% control of Barrick Mining. The price of the non-tendered shares will be closest to:

A) $12.50 B) $15.00 C) $17.50 D) $20.00

Q8 Use the information in the previous question. Regarding your tender offer, shareholders will:

A) not tender their shares since the post LBO price is higher than the offer price. B) not tender their shares since the post LBO price is higher than the current price. C) tender their shares since the post LBO price is higher than the offer price. D) tender their shares since the post LBO price is lower than the current price.

5 of 11

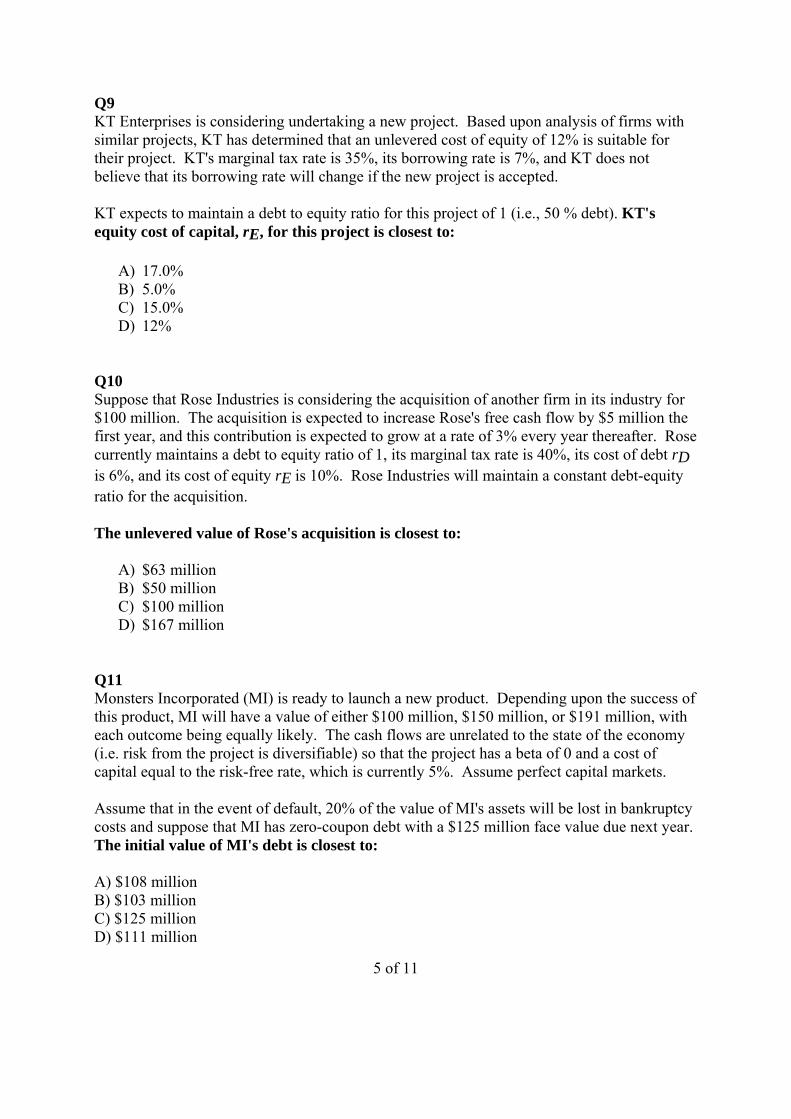

Q9 KT Enterprises is considering undertaking a new project. Based upon analysis of firms with similar projects, KT has determined that an unlevered cost of equity of 12% is suitable for their project. KT's marginal tax rate is 35%, its borrowing rate is 7%, and KT does not believe that its borrowing rate will change if the new project is accepted. KT expects to maintain a debt to equity ratio for this project of 1 (i.e., 50 % debt). KT's equity cost of capital, rE, for this project is closest to:

A) 17.0% B) 5.0% C) 15.0% D) 12%

Q10 Suppose that Rose Industries is considering the acquisition of another firm in its industry for $100 million. The acquisition is expected to increase Rose's free cash flow by $5 million the first year, and this contribution is expected to grow at a rate of 3% every year thereafter. Rose currently maintains a debt to equity ratio of 1, its marginal tax rate is 40%, its cost of debt rD is 6%, and its cost of equity rE is 10%. Rose Industries will maintain a constant debt-equity ratio for the acquisition. The unlevered value of Rose's acquisition is closest to:

A) $63 million B) $50 million C) $100 million D) $167 million

Q11 Monsters Incorporated (MI) is ready to launch a new product. Depending upon the success of this product, MI will have a value of either $100 million, $150 million, or $191 million, with each outcome being equally likely. The cash flows are unrelated to the state of the economy (i.e. risk from the project is diversifiable) so that the project has a beta of 0 and a cost of capital equal to the risk-free rate, which is currently 5%. Assume perfect capital markets. Assume that in the event of default, 20% of the value of MI's assets will be lost in bankruptcy costs and suppose that MI has zero-coupon debt with a $125 million face value due next year. The initial value of MI's debt is closest to: A) $108 million B) $103 million C) $125 million D) $111 million

6 of 11

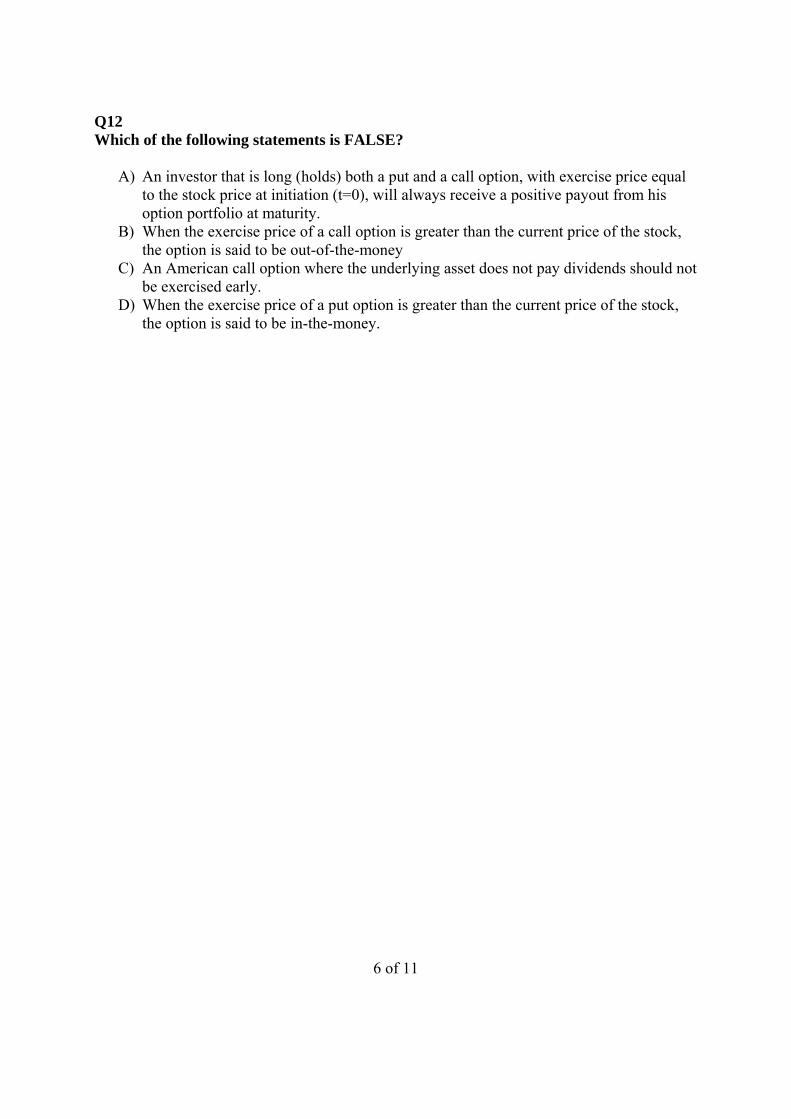

Q12 Which of the following statements is FALSE?

A) An investor that is long (holds) both a put and a call option, with exercise price equal to the stock price at initiation (t=0), will always receive a positive payout from his option portfolio at maturity.

B) When the exercise price of a call option is greater than the current price of the stock, the option is said to be out-of-the-money

C) An American call option where the underlying asset does not pay dividends should not be exercised early.

D) When the exercise price of a put option is greater than the current price of the stock, the option is said to be in-the-money.

7 of 11

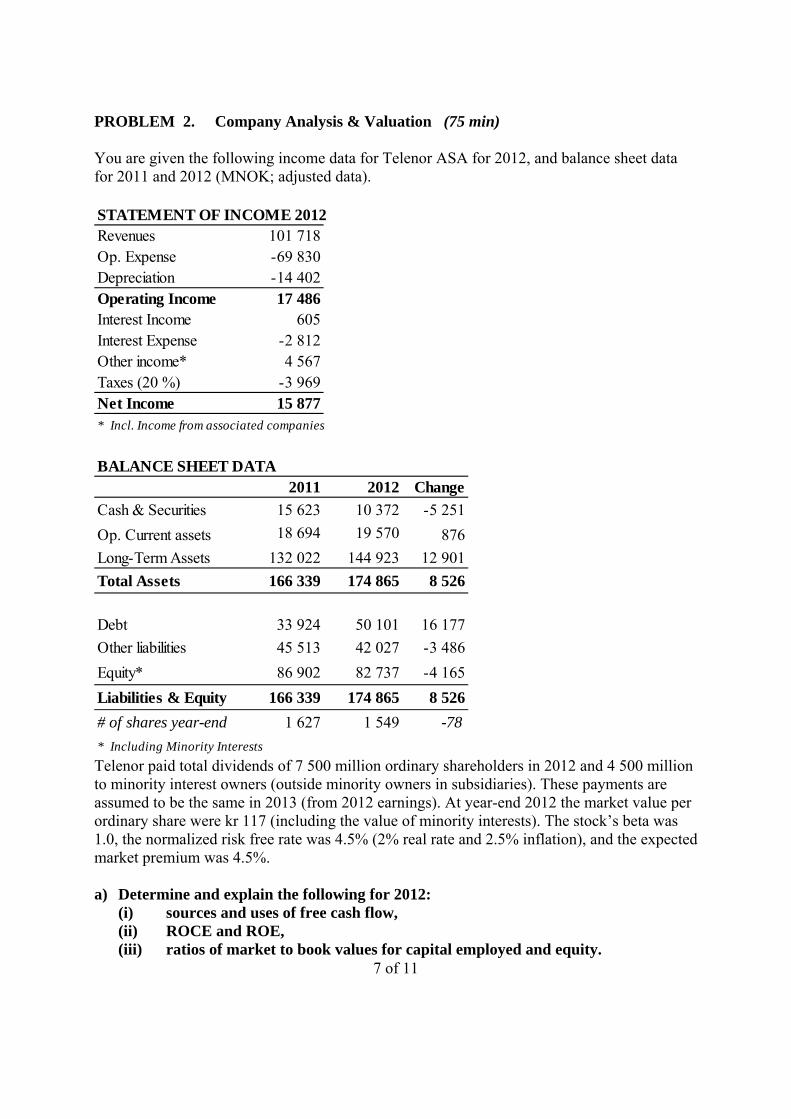

PROBLEM 2. Company Analysis & Valuation (75 min) You are given the following income data for Telenor ASA for 2012, and balance sheet data for 2011 and 2012 (MNOK; adjusted data).

Telenor paid total dividends of 7 500 million ordinary shareholders in 2012 and 4 500 million to minority interest owners (outside minority owners in subsidiaries). These payments are assumed to be the same in 2013 (from 2012 earnings). At year-end 2012 the market value per ordinary share were kr 117 (including the value of minority interests). The stock’s beta was 1.0, the normalized risk free rate was 4.5% (2% real rate and 2.5% inflation), and the expected market premium was 4.5%. a) Determine and explain the following for 2012:

(i) sources and uses of free cash flow, (ii) ROCE and ROE, (iii) ratios of market to book values for capital employed and equity.

STATEMENT OF INCOME 2012Revenues 101 718Op. Expense -69 830Depreciation -14 402Operating Income 17 486Interest Income 605Interest Expense -2 812Other income* 4 567Taxes (20 %) -3 969Net Income 15 877* Incl. Income from associated companies

BALANCE SHEET DATA2011 2012 Change

Cash & Securities 15 623 10 372 -5 251

Op. Current assets 18 694 19 570 876

Long-Term Assets 132 022 144 923 12 901

Total Assets 166 339 174 865 8 526

Debt 33 924 50 101 16 177

Other liabilities 45 513 42 027 -3 486

Equity* 86 902 82 737 -4 165

Liabilities & Equity 166 339 174 865 8 526

# of shares year-end 1 627 1 549 -78* Including Minority Interests

8 of 11

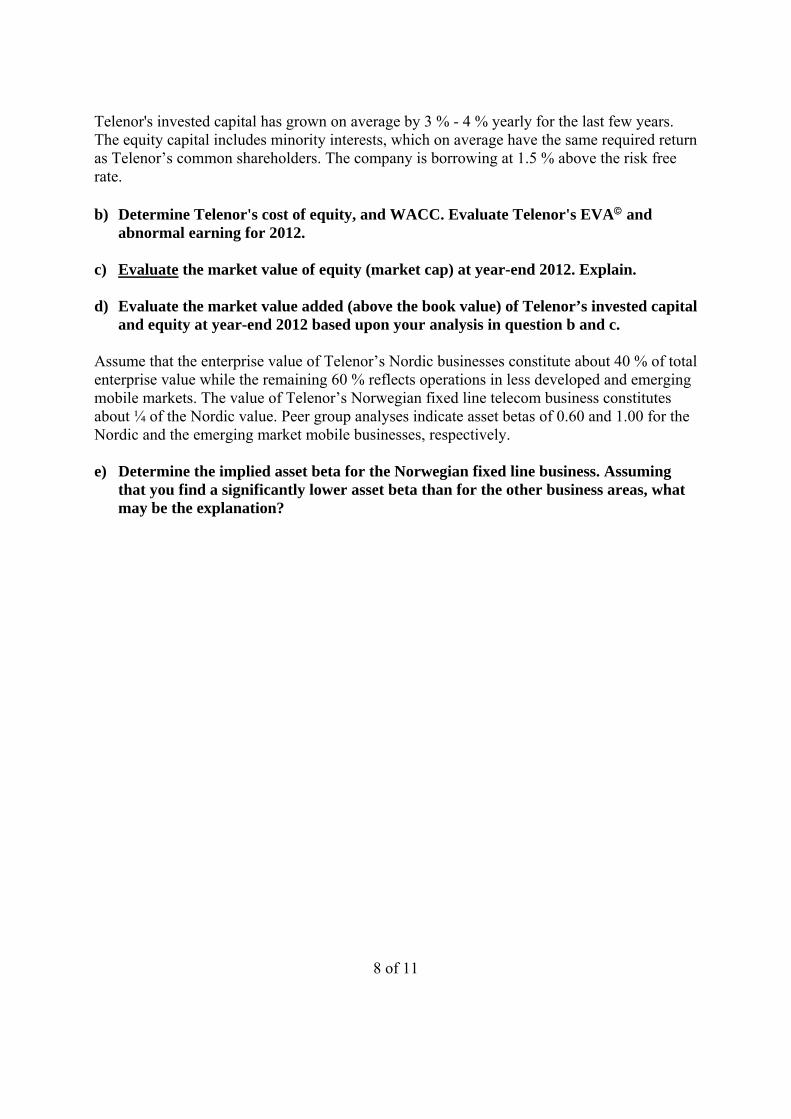

Telenor's invested capital has grown on average by 3 % - 4 % yearly for the last few years. The equity capital includes minority interests, which on average have the same required return as Telenor’s common shareholders. The company is borrowing at 1.5 % above the risk free rate.

b) Determine Telenor's cost of equity, and WACC. Evaluate Telenor's EVA and

abnormal earning for 2012. c) Evaluate the market value of equity (market cap) at year-end 2012. Explain.

d) Evaluate the market value added (above the book value) of Telenor’s invested capital

and equity at year-end 2012 based upon your analysis in question b and c. Assume that the enterprise value of Telenor’s Nordic businesses constitute about 40 % of total enterprise value while the remaining 60 % reflects operations in less developed and emerging mobile markets. The value of Telenor’s Norwegian fixed line telecom business constitutes about ¼ of the Nordic value. Peer group analyses indicate asset betas of 0.60 and 1.00 for the Nordic and the emerging market mobile businesses, respectively. e) Determine the implied asset beta for the Norwegian fixed line business. Assuming

that you find a significantly lower asset beta than for the other business areas, what may be the explanation?

9 of 11

PROBLEM 3. Debt funding (max 50 min) Concise answers to the following two questions will be appreciated. a) Present an intuitive explanation of Miller & Modligiani’s claim that a company’s

Enterprise Value will not be affected by changes in the company’s capital structure. b) In practice, the firm’s choice of a capital structure may well affect its Enterprise

Value. Identify the main reasons for this deviation from MM, and discuss why and how they work. Relate your discussion to relevant company or industry characteristics.

It is claimed that both Equity and Debt in a (significantly) leveraged corporation may be viewed fully or partly as options. c) Evaluate this claim with the use of a diagram. Why may this analogy to options give

a useful perspective for understanding a potential conflict between owners and lenders? What can be done to reduce this conflict?

A corporation has an Enterprise Value’ (EV) of NOK 10 billion. The interest bearing debt matures in one year with an amount of NOK 9 billion (face value plus interest). EV has a volatility of 30 % p.a. and the risk free rate is 4 %. The stock is not paying dividends. You observe the following premium values (B&S) for 1-year call and put options on a stock index with volatility 30 % p.a. This is a total return index. % av today's index value

Strike: 9.0 10.0 Call premium 1.91 1.37 Put premium 0.56 0.99 d) Calculate the market value of the company’s equity and debt. Explain. What is the

yield on the debt? e) Evaluate the B&S premium values in the table with a simplified .4/.5-calculation The company has an asset beta of 0.8 and the market premium is 5 %. f) Give an estimate of the probability of default at the end of the year, assuming a

normal distribution for next year’s enterprise value (hint: probability weight 68 % of +/- 1 stdev. around the mean value). What if the enterprise value instead is log-normally distributed?

10 of 11

PROBLEM 4 Structured Products (max 30 min) You are evaluating the premium levels of (European) options on a stock index with current index value 100. 3 years’ Call and Put options (warrant) with strike 100 have premium values of 23.7 and 10.1, respectively. The 3 years’ treasury rate is 5 %. The index is a return index, which is adjusted for dividends. The shares in the index are expected to pay a combined continuous dividend of 2.5 % p.a. (a) Estimate the implicit volatility for one of these options, using the 0.4/0.5-rule. In a bank, you are responsible for the pricing of two alternative retail products which is based on the above index. The Bull or Bear Deposit: The customer will receive his invested amount in 3 years, plus a rate of return on this amount equal to a multiplier m times any percentage increase (Bull Deposit) or decrease (Bear Deposit) in the index over these three years. (b) Determine the largest multiplier value m for each product which will give the bank

a total fee 4 % of the invested amount (in present value). Explain your calculations and discuss why the Bear Deposit should have a significantly larger multiplier.

(c) Discuss the likely effect on the maximum multiplier of each product of using a price

version of the same index, which is not adjusted for dividends.

11 of 11

Useful formulas ??

X)PV(F0,5 PV(F)Tσ0,4 C −⋅+⋅⋅=

11 DBE

EBITt)(1ROCE

−− +⋅−=

1BE

EROE

−

=

g-k

d = p 1

WACC = Rf + βA ⋅ MP + Debt

DEU βDτ)-(1 E

Dβ

Dτ)-(1 E

E β ⋅

⋅+

+⋅

⋅+

=

1 n

xp

n

x q t

+−=−=

g -k

1] -/k [RInv +

k

E = V

*1

*

1 ⋅

DEA βD E

Dβ

D E

E β ⋅

++⋅

+=

AA

T

/nV

S V x

+≤