Embed Size (px)

Citation preview

Feb,2010

Shin, Je-YoonDeputy Minister

I. Origins of the crisis

II. Fixing the Problems

III What is missing? Root ca se of ImbalancesIII. What is missing? : Root cause of Imbalances

IV What is needed in a world of capital volatility?IV. What is needed in a world of capital volatility?

V. Ahead for strong, sustainable and balanced g,growth

Ⅰ. Origins of the crisis

Ⅰ. Origins of the Crisis : Overview

External Factor Internal Factor

Global ImbalanceLoose

Monetary PolicyFlawed

Financial Regulation

Origin

Capital Inflow to U SExcess Liquidity Rapid

Capital Inflow to U.S& Low Policy rate Financial Innovation

Trans

Low Interest RateMoral Hazard

In Financial SystemTrans

Mission

Leverage-fueled Asset Bubble

3

Leverage fueled Asset Bubble

Ⅰ. Origins of the Crisis : Global Imbalances

A sustained accumulation of imbalances started in 1996→ U.S current deficit peaked at 2005(6% of GDP)

<Average current account deficit/surplus ( % of GDP)>

Current Account 1996-2000 2001-2005 2006-2008

DeficitUSA -2.7% -4.9% -5.3%

DeficitEurope ₁ -0.5% -2.5% -4.7%

China 2.2% 3.8% 10.1%

Surplus

EmergingAsia ₂

2.8% 4.7% 4.3%

Japan 2.4 % 3.2% 3.9%p

Oil Exporters ₃ 5.4% 12.1% 14.2%

1. Europe : United Kingdom, Italy, Spain, Greece2 Emerging Asia : Hongkong Taiwan Korea Singapore Thailand Indonesia

4

2. Emerging Asia : Hongkong, Taiwan, Korea, Singapore, Thailand, Indonesia3. Oil Exporter : Saudi, Libya, Russia, Kuwait, Iran

Ⅰ. Origins of the Crisis : (1) Global Imbalances

C/A Imbalances Capital Flow into the U.S. Low Interest Rate

- Foreign capital from the C/a Surplus countries flowed into the U.S in the form of FX reserve investment

- Mostly invested in the U.S. government and agency bondsAmple capital inflow kept the interest low

<IRA of Emerging Asia and U.S treasuries>

Ample capital inflow kept the interest low.

(

<U.S. 10-year treasury rate (real,%)>

10,000

12,000

25

30

35

Total treasury securities outstandingIRA of Emerging Asia IRA/treasuries outsatanding

(billion Dolla

8

10 rate(%)

6,000

8,000

15

20

25

ars)

2

4

6

2,000

4,000

5

10

-2

0

2

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

5

0

1995 1997 1999 2001 2003 2005 2007

0

-4

Ⅰ. Origins of the Crisis : (2) Excess Liquidity

Loose monetary policy Credit Easing

- Since 2001, Monetary easing began perceiving weakness i th ft th hi h t h ll d 9/11 tt kin the economy after the high-tech collapse and 9/11 attack.* FRB Target Rate : (May 2000) 6.5% → (June 2003) 1%

- Loose monetary stance, coupled with foreign capital inflow, led to

<Marshallian K><Fed Funds Rate (1998-2008)>

y , p g p ,eased credit condition and rapid asset market appreciation.

0.8

0.9

Marshallian K(M2)

Marshallian(M3)

0 5

0.6

0.7

0 3

0.4

0.5

6

0.3

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

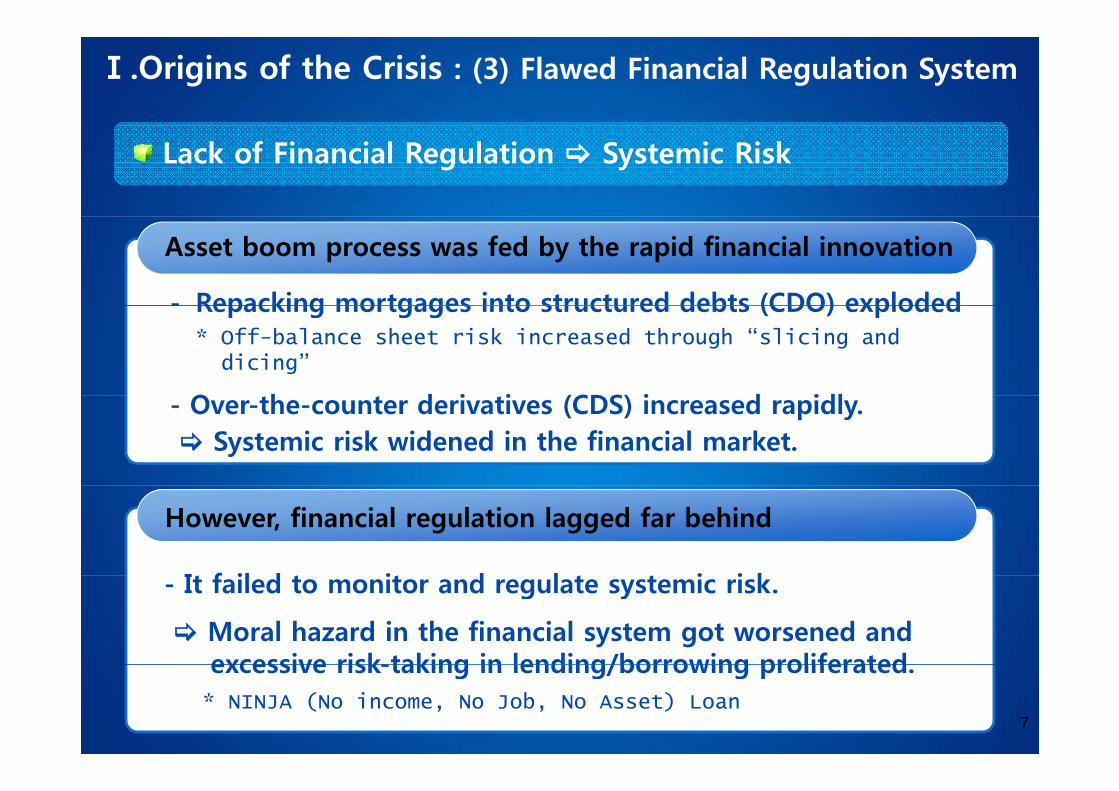

Ⅰ.Origins of the Crisis : (3) Flawed Financial Regulation System

Lack of Financial Regulation Systemic Risk

- Repacking mortgages into structured debts (CDO) exploded

Asset boom process was fed by the rapid financial innovation

Repacking mortgages into structured debts (CDO) exploded * Off-balance sheet risk increased through “slicing anddicing”

O h d i i (CDS) i d idl- Over-the-counter derivatives (CDS) increased rapidly.Systemic risk widened in the financial market.

However, financial regulation lagged far behind

I f il d i d l i i k- It failed to monitor and regulate systemic risk.

Moral hazard in the financial system got worsened andexcessive risk-taking in lending/borrowing proliferated

7

excessive risk-taking in lending/borrowing proliferated.* NINJA (No income, No Job, No Asset) Loan

Ⅰ. Origins of the Crisis : Boom-Bust Cycle

Interaction among external and internal factors Asset Market Bubble and Bust

Ample foreign capital inflow and excess liquidity led to low- Ample foreign capital inflow and excess liquidity led to low interest rates and credit easing. Housing market boom began.

- With lack of relevant financial regulation, housing market boom g gdeveloped into full-fledged leverage-fueled bubble.

<U.S. Housing and Stock Market Price>

Nasdaq

S&P/ Case-Shiller index

S&P 500

8

Ⅱ. Fixing The Problems

Ⅱ. Fixing The Problems – Conventional Approach

Various measures are discussed on the table to fix the origins of the global financial crisis.

Gl b l Adjusting F/X MarketGlobalImbalances

Adjusting F/X Market

Rebalancing aggregatedemands across countries

Flawed Financial

RegulationOverhauling FinancialRegulatory system

10

Ⅲ. Fixing The Problems – Global Imbalances

1. Adjustment of exchange rate

The past : End of Bretton-woods(1971), Plaza Accord(1985) used as a prescription to fix then global imbalancesused as a prescription to fix then global imbalances

How about now? : Further discussion on the scope and pace neededToo heavy a shock to some economies anticipatedToo heavy a shock to some economies anticipatedif abruptly implemented

R b l i<Germany & Japan’s Exchange rates since 1970s>

Rebalancing aggregatedemands across countries

0.6

0.7

0.8

0.007

0.008

0.009

Bretton-Woods Plaza Accord

0 3

0.4

0.5

0 003

0.004

0.005

0.006

0

0.1

0.2

0.3

0

0.001

0.002

0.003

U.S.$/DM(left axis)U.S.$/Yen(right axis)

11

0

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990

0

Ⅱ. Fixing The Problems – Global Imbalances

Surplus Countries Deficit Co ntries

2. Rebalancing aggregate demands across countries

Surplus Countries

▪ Strengthening incentives to

Deficit Countries

▪ Increasing private consumption

private saving

▪ Fiscal consolidation over

ex) financial market development

strengthening service industry

▪ Reducing precautionary savingthe mid and long term

▪ Curbing excessively leveraged

Reducing precautionary saving

ex) fortifying social safety net

▪ Increase depressed investment g y g

consumption and investmentIncrease depressed investment

ex) tax incentives on facility investment

Needs to be implemented over the mid- and long-term

12

p gthrough concerted efforts of international community

Ⅱ. Fixing The Problems – Overhauling Regulatory System

1. Ending Myth of “Too big to Fail”

(ex) New Proposal by U.S. President Obama (Jan 21, 2010)

· Scope: preventing banks from investing in hedge funds and PEFs· Size : limiting consolidations of financial sector Size : limiting consolidations of financial sector

2 St th d t i ti “ i i k t ki ”2. Strengthened restriction on “excessive risk-taking”

(ex) Aligning compensation practices with long-termf

3 P i i i “fi i l fi d k ”

performances

3. Promoting supervision on “financial firms and market”

(ex) Enhancing regulation on securitization markets, credit

13

rating agencies and over-the-counter derivatives

Ⅲ Wh t i i i ?Ⅲ. What is missing?

: Root cause of Global Imbalances: Root cause of Global Imbalances

Ⅲ. What is missing? : Root cause of Global Imbalances

1. Past episodes of the global imbalances

Three big events of global imbalances – 1960s, 1980s, present

<Historical Pattern of Global imbalances (U.S. C/A of GDP, %)>

0%

1%

2%Bretton-Woods System Plaza Accord Present

Rebalancing aggregatedemands across countries

-2%

-1%

0%

1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005

-4%

-3%

-2%

-6%

-5%

4%

current deficit/GDP

15

-7%

Ⅲ. What is missing? : Root cause of Global Imbalances

(1) Break-down of the Bretton-Woods System(1960~1971)

Root Cause : Confidence in gold convertibility of $ was lostRoot Cause : Confidence in gold convertibility of $ was lost

Gold-Dollar Fixed FX system with “$” as a reserve currency- Worsening U.S. C/A balance and capital outflows without proper F/X rate adjustment

External U.S. liabilities exceeded the U.S. gold reserve<U.S. C/A & F/A in 1960s >

Adjustment(1971)

Suspension of ld tibilit b th U S

/ /

4000

6000

8000

(million D

gold convertibility by the U.S.

Adoption of float managingFX

0

2000

4000

1960 1962 1964 1966 1968 1970 1972D

ollars)

FX system

-6000

-4000

-20001960 1962 1964 1966 1968 1970 1972

16-10000

-8000 CURRENT ACCOUNT

FINANCIAL ACCOUNT

Ⅲ. What is missing? : Root cause of Global Imbalances

(2) Early 1980s’ Imbalances and Plaza Accord

Root Cause : Misaligned FX rates due to policy factors

In the early 1980s, U.S. fiscal and C/A deficits grew rapidly due to expansionary fiscal policy.

Follo ing monetar contraction to pre ent inflation keptFollowing monetary contraction to prevent inflation kept the U.S. dollar excessively over-valued.

Imbalances between the U.S. and surplus countries persisted.

Adjustment(1985)

Coordinated intervention

<U.S., Germany, Japan C/A in 1970s>

100

(billion

of G-5 countries in the market 0

50

1979 1981 1983 1985 1987 1989

n Dollars)

-100

-50

17-200

-150Germany Japan U.S.

Ⅲ. What is missing? : Root cause of Global Imbalances

2. Current Imbalances? : Self-insurance against capital volatility

Past global imbalances could be adjusted through fixingPast global imbalances could be adjusted through fixing the underlying cause : adjustment of FX rates

However, current imbalance has a different origin

Growing capital volatility emerged as a main potential threatto the emerging market countries since 1990’s

<World capital flows over the past 20 years><World capital flows over the past 20 years>

14 000

16,000

18,000

35%

40%

45%

World Capital Flows

World Trade(Export)

(billion

8,000

10,000

12,000

14,000

20%

25%

30%

35%World Trade(Export)

Capital Flows/Export

Dollars)

2,000

4,000

6,000

,

5%

10%

15%

18

0

World 1982 1985 1988 1991 1994 1997 2000 2003 2006

0%

Ⅲ. What is missing? : Root cause of Global Imbalances

Lessons from the Past and Present Crises

1998 Asian Crisis : Sudden stop forced Asian emerging economies to face the financial crisis

1to face the financial crisis

Recent Global Crisis : Rapid capital reversal due to massive deleveragingshocked the emerging financial markets.

2

Lesson : Instable capital movement with the nature of “greed & fear”can be a potential risk of crisis to the EM countries.

<Capital Account in Major EMDCs>

350

400

Capital Account

(Global Crisis)

(billion

150

200

250

300Capital Account

(Asian Crisis)

n Dollars)

0

50

100

150

19-100

-50 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

* China, Hong-kong, India, Indonesia, Malaysia, Korea, Brazil, Russia, Philippine, Thailand

Ⅲ. What is missing? : Root cause of Global Imbalances

Inevitable Choice : Building Self-safety Nets

Guarding against potential risk of capital volatility, EM countriesbegan to build up self-financial safety netsbegan to build up self-financial safety nets,

by accumulating international reserves and C/A surpluses.

Benefits of having self-safety nets counteracting potential capital flowBenefits of having self safety nets counteracting potential capital flowshock exceed the cost* of maintaining excess reserve assets.

Without sufficient global financial safety nets, it would not be f EM i C/A leasy for EM countries to narrow C/A surpluses.

<Current Account & Change of Reserve Assets in Major EMDCs>500

(bill

300

400

Current AccountChange of Reseve Asset

lion Dollars)

0

100

200`

)

20-100

0

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

* China, Hong-kong, India, Indonesia, Malaysia, Korea, Brazil, Russia, Philippine, Thailand

Ⅳ What is needed in a world of capitalⅣ. What is needed in a world of capitalvolatility?

Ⅳ. What is needed in a world of capital volatility? : Building Strengthened Global Financial Safety Net

(1) Strengthening surveillance and regulation on capital movement

C i l C l?

(1) Strengthening surveillance and regulation on capital movementcan be another solution…… But not enough…..

Capital Control?

- Capital controls must be temporary since they could hamper p p y y peconomic growth and financial market development.

- Information gap : It’s almost impossible catch up the speed of fi i l i i

Capital Surveillance?

financial innovation

22

Ⅳ. What is needed in a world of capital volatility? : Building Strengthened Global Financial Safety Net

(2) Overview of existing safety-net

- Lack of available resources (ex. Korea IRA U.S.$270 Billion)

IMF Lending Facility : U.S. $450 Billion

- Stigma Effect : Concern over negative market signals (ex. FCL)

- Harsh & One-fits-all conditionality

- It’s too linked to IMF’s lending : Only 20% is de-linked

CMI (Chiang-Mai Initiative) : U.S. $120 Billion

It s too linked to IMF s lending : Only 20% is de linked

- Weak & dependent surveillance

IMF S i l D i Ri ht U S $250 Billi (2009 A t)IMF Special Drawing Rights : U.S. $250 Billion (2009, August)

- Tight condition on issuance of SDRs (85% of members)

- Absence of deep and liquid market (Only used for official sector)

23

- Absence of deep and liquid market (Only used for official sector)

Ⅳ. What is needed in a world of capital volatility? : Building Strengthened Global Financial Safety Net

(3) Suggestion for Strong Global Financial Safety Net

Global safety net should be …… 1 sufficient in scale &

2 highly accessible as a precautionary purpose

- Sufficient enough to substitute self-defense-safety-net of emerging

Sufficiency : Ample & Multiple shield

g y p y p p

1

Sufficient enough to substitute self defense safety net of emergingmarket countries

- Combined with regional safety net such as CMI, bilateral sway, etc

2 Accessibility as a precautionary measure

S iftl il bl i ti f d- Swiftly available in time of need

- Ensuring certainty over usability when in need and availableresource size

24

Ⅴ. Ahead for Strong, Sustainable, and balanced growtha d ba a ced g o t

Ⅵ. Ahead for strong, sustainable and balancedgrowth

Strategies for the picture of post-crisis era are on the table ofthe unprecedented international cooperation led by the G20

ⅰ) Framework for Strong, Sustainable and balanced growth : MAP

p p y

ⅱ) Strengthening the international financial regulatory systemⅱ) Strengthening the international financial regulatory system

- Strengthening prudential oversight, improving risk management- Strengthening transparency

ⅲ) Global financial safety net : Reform of IMF lending facility, etc

- Establishing supervisory colleges

For the strategies to succeed with solid concerted efforts, mutuallybeneficial ways to all members of the global economy must be pursued

Building a strong global financial safety net would be a significant step toward strong balanced and sustainable growth

26

a significant step toward strong, balanced and sustainable growth

![Curriculum Vitae: Jangho Yoon, M.S.P.H., Ph.D....2019/10/10 · 2016 Feb 13. [Epub ahead of print]. DOI 10.1007/s10488-016-0722-9. 16. Jangho Yoon, Hyunwoong Shin, Yun-Hong Noh, and](https://img.pdfslide.us/doc/110x75/5f087ff67e708231d4225104/curriculum-vitae-jangho-yoon-msph-phd-20191010-2016-feb-13-epub.jpg)