Embed Size (px)

Citation preview

Farm Management

Chapter 13Cash Flow Budgeting

farm management chapter 13

2

Figure 13-1Illustration of cash flows

farm management chapter 13

3

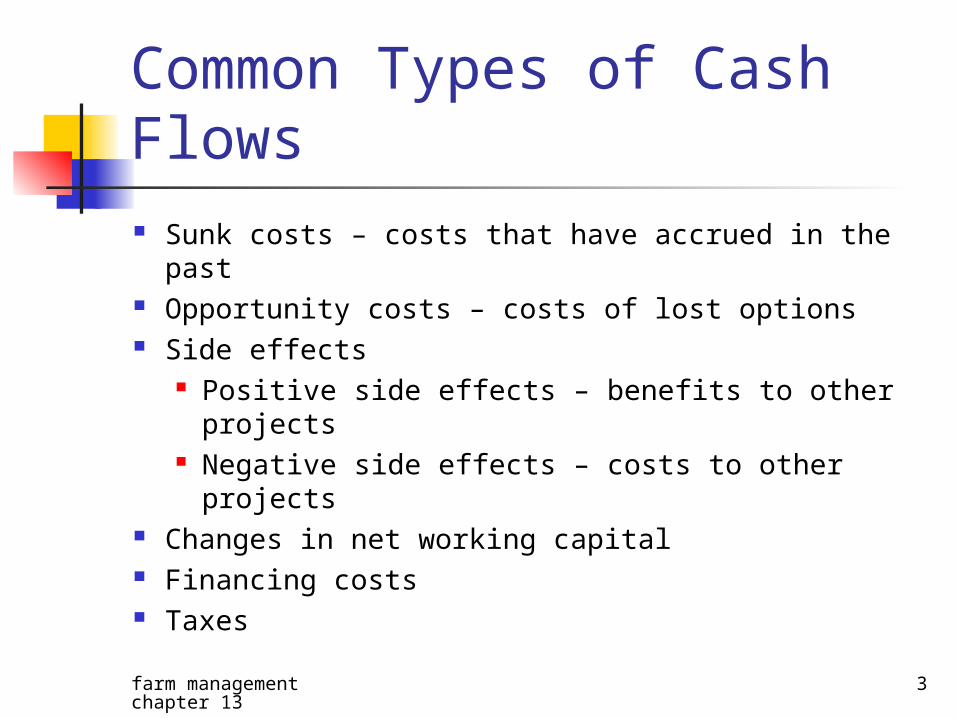

Common Types of Cash Flows Sunk costs – costs that have accrued in the past Opportunity costs – costs of lost options Side effects

Positive side effects – benefits to other projects Negative side effects – costs to other projects

Changes in net working capital Financing costs Taxes

farm management chapter 13

4

Actual versus Estimated Cash Flows

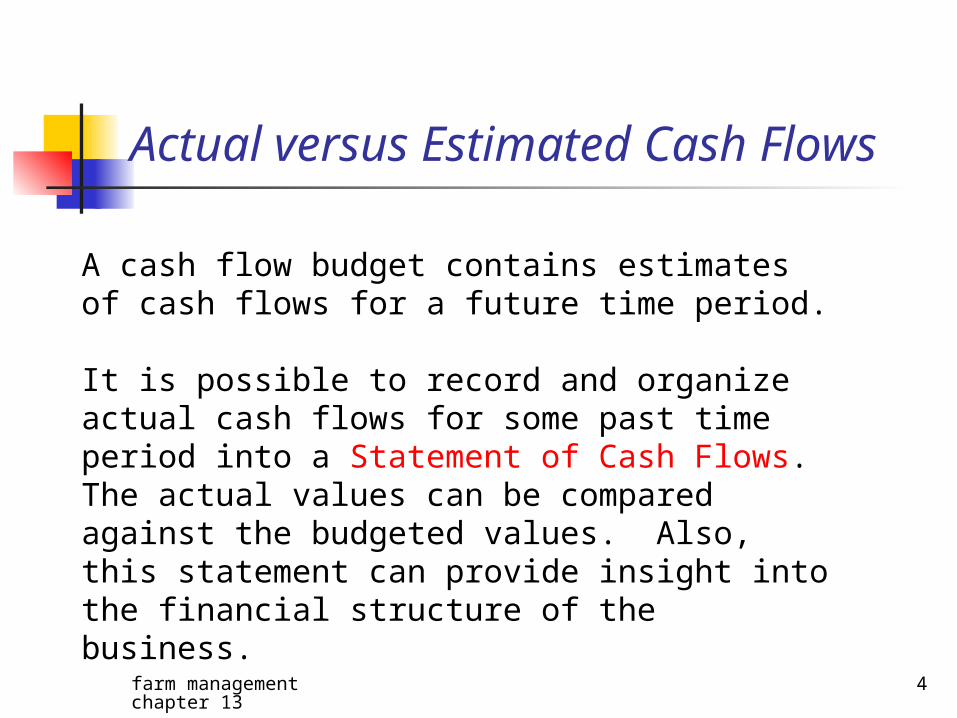

A cash flow budget contains estimatesof cash flows for a future time period. It is possible to record and organizeactual cash flows for some past time period into a Statement of Cash Flows.The actual values can be compared against the budgeted values. Also, this statement can provide insight into the financial structure of the business.

farm management chapter 13

5

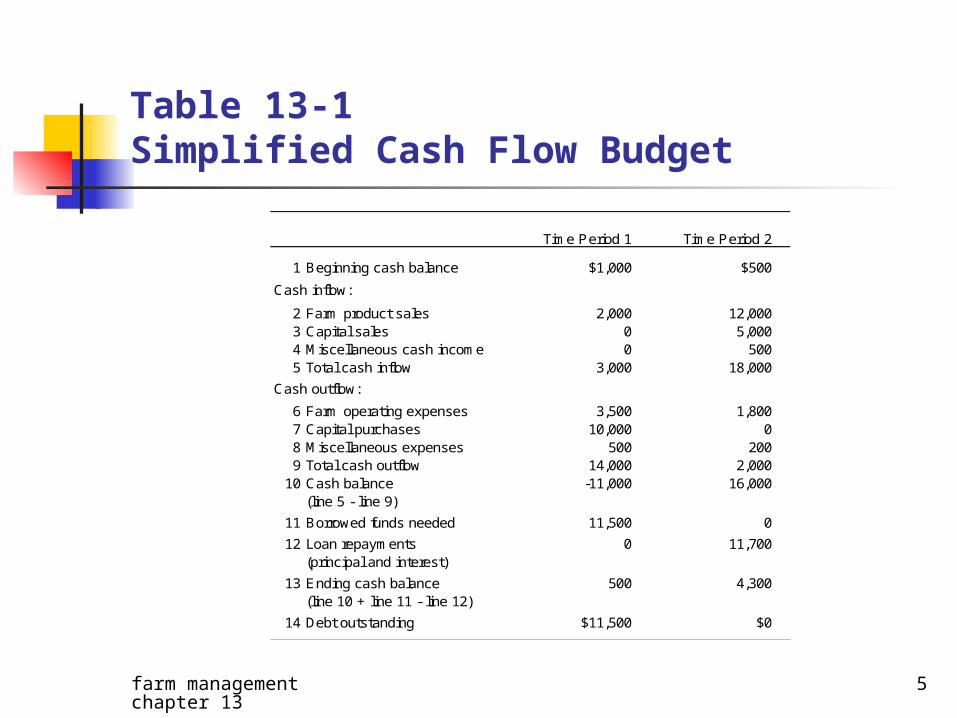

Table 13-1Simplified Cash Flow Budget

Time Period 1 Time Period 2

1 Beginning cash balance $1,000 $500

2 Farm product sales 2,000 12,0003 Capital sales 0 5,0004 Miscellaneous cash income 0 5005 Total cash inflow 3,000 18,000

6 Farm operating expenses 3,500 1,8007 Capital purchases 10,000 08 Miscellaneous expenses 500 2009 Total cash outflow 14,000 2,000

10 Cash balance -11,000 16,000(line 5 - line 9)

11 Borrowed funds needed 11,500 0

12 Loan repayments 0 11,700(principal and interest)

13 Ending cash balance 500 4,300(line 10 + line 11 - line 12)

14 Debt outstanding $11,500 $0

Cash inflow:

Cash outflow:

farm management chapter 13

6

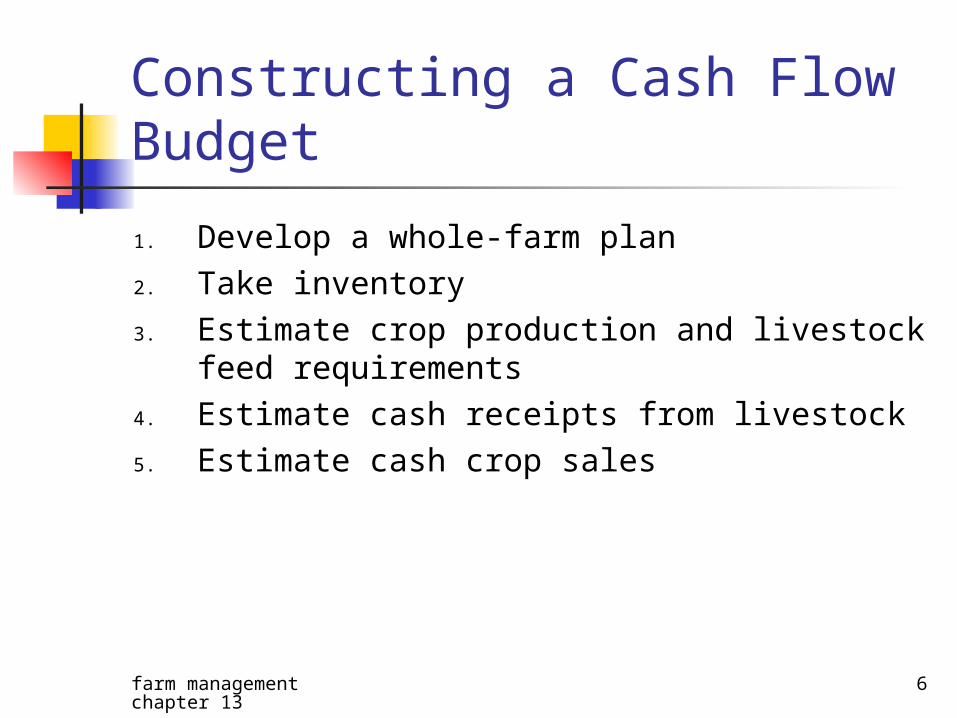

Constructing a Cash Flow Budget

1. Develop a whole-farm plan2. Take inventory3. Estimate crop production and livestock feed

requirements4. Estimate cash receipts from livestock5. Estimate cash crop sales

farm management chapter 13

7

Constructing a Cash Flow Budget (continued)

6. Estimate other cash income7. Estimate cash farm operating expenses8. Estimate personal and nonfarm cash

expenses9. Estimate purchases and sales of capital

assets10. Find and record the scheduled principal and

interest payments on existing debts

farm management chapter 13

8

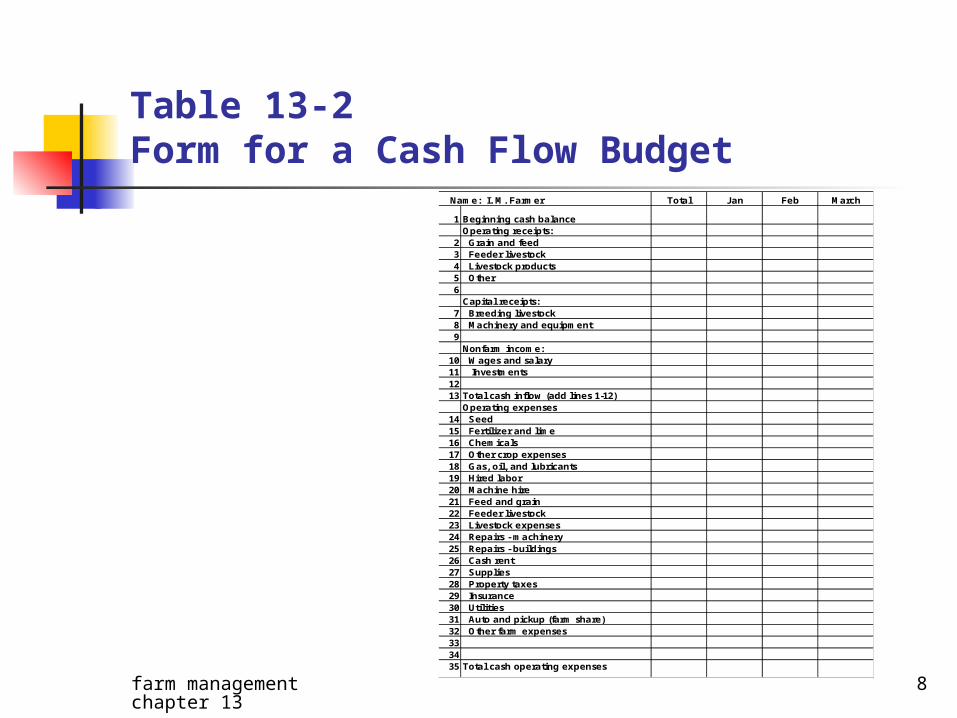

Table 13-2Form for a Cash Flow Budget

Total Jan Feb March

1 Beginning cash balanceOperating receipts:

2 Grain and feed3 Feeder livestock4 Livestock products5 Other6

Capital receipts:7 Breeding livestock8 Machinery and equipment9 Nonfarm income:

10 Wages and salary11 Investments12 13 Total cash inflow (add lines 1-12)

Operating expenses14 Seed15 Fertilizer and lime16 Chemicals17 Other crop expenses18 Gas, oil, and lubricants19 Hired labor20 Machine hire21 Feed and grain22 Feeder livestock23 Livestock expenses24 Repairs - machinery25 Repairs - buildings26 Cash rent27 Supplies28 Property taxes29 Insurance30 Utilities31 Auto and pickup (farm share)32 Other farm expenses333435 Total cash operating expenses

Name: I. M. Farmer

farm management chapter 13

9

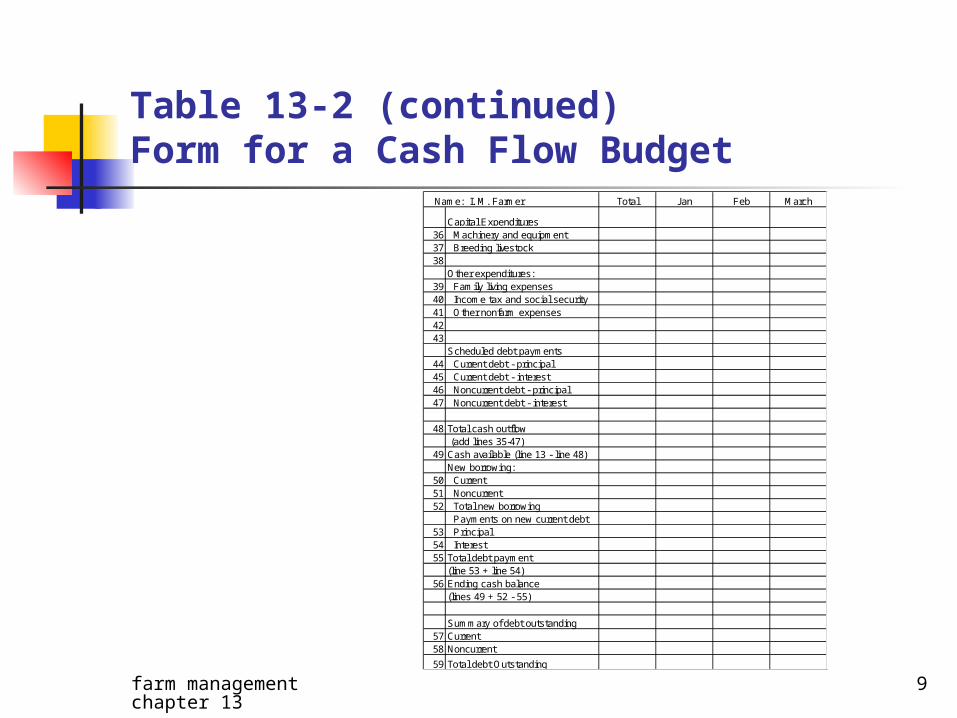

Table 13-2 (continued)Form for a Cash Flow Budget

Total Jan Feb March

36 Machinery and equipment37 Breeding livestock38

Other expenditures:39 Family living expenses40 Income tax and social security41 Other nonfarm expenses42 43

Scheduled debt payments44 Current debt - principal45 Current debt - interest46 Noncurrent debt - principal47 Noncurrent debt - interest

48 Total cash outflow (add lines 35-47)

49 Cash available (line 13 - line 48)New borrowing:

50 Current51 Noncurrent52 Total new borrowing

Payments on new current debt53 Principal54 Interest55 Total debt payment

(line 53 + line 54)56 Ending cash balance

(lines 49 + 52 - 55)

Summary of debt outstanding57 Current58 Noncurrent

59 Total debt Outstanding

Name: I. M. Farmer

Capital Expenditures

farm management chapter 13

10

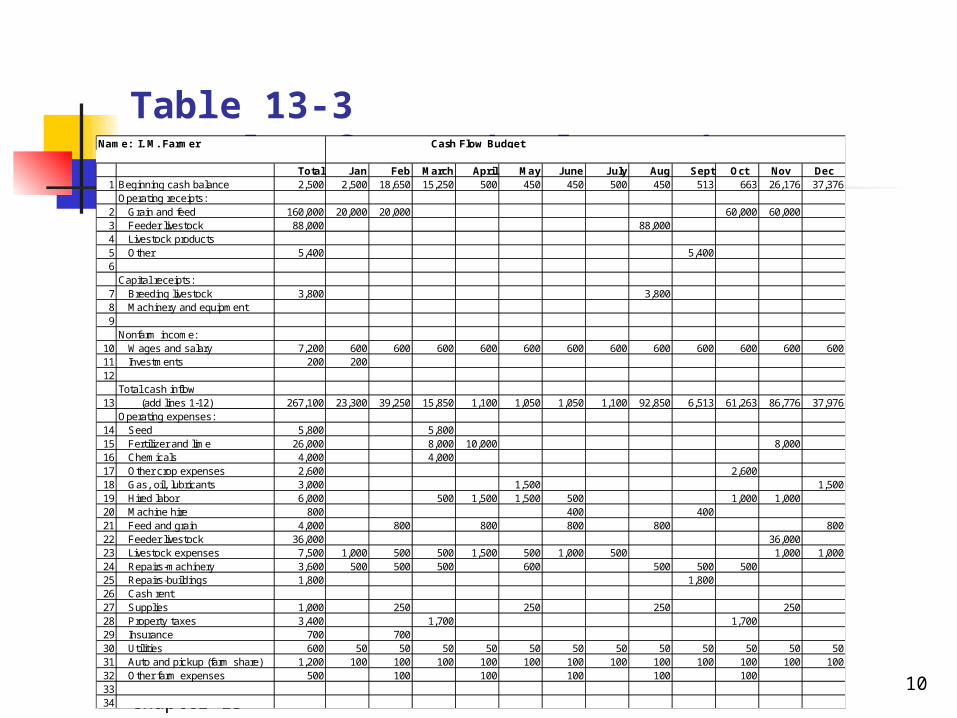

Table 13-3Example of a Cash Flow Budget

Total Jan Feb March April May June July Aug Sept Oct Nov Dec 1 Beginning cash balance 2,500 2,500 18,650 15,250 500 450 450 500 450 513 663 26,176 37,376

Operating receipts:2 Grain and feed 160,000 20,000 20,000 60,000 60,0003 Feeder livestock 88,000 88,0004 Livestock products5 Other 5,400 5,4006

Capital receipts:7 Breeding livestock 3,800 3,8008 Machinery and equipment9

Nonfarm income:10 Wages and salary 7,200 600 600 600 600 600 600 600 600 600 600 600 60011 Investments 200 20012

Total cash inflow 13 (add lines 1-12) 267,100 23,300 39,250 15,850 1,100 1,050 1,050 1,100 92,850 6,513 61,263 86,776 37,976

Operating expenses:14 Seed 5,800 5,80015 Fertilizer and lime 26,000 8,000 10,000 8,00016 Chemicals 4,000 4,00017 Other crop expenses 2,600 2,60018 Gas, oil, lubricants 3,000 1,500 1,50019 Hired labor 6,000 500 1,500 1,500 500 1,000 1,00020 Machine hire 800 400 40021 Feed and grain 4,000 800 800 800 800 80022 Feeder livestock 36,000 36,00023 Livestock expenses 7,500 1,000 500 500 1,500 500 1,000 500 1,000 1,00024 Repairs-machinery 3,600 500 500 500 600 500 500 50025 Repairs-buildings 1,800 1,80026 Cash rent27 Supplies 1,000 250 250 250 25028 Property taxes 3,400 1,700 1,70029 Insurance 700 70030 Utilities 600 50 50 50 50 50 50 50 50 50 50 50 5031 Auto and pickup (farm share) 1,200 100 100 100 100 100 100 100 100 100 100 100 10032 Other farm expenses 500 100 100 100 100 1003334

Cash Flow BudgetName: I. M. Farmer

farm management chapter 13

11

Table 13-3 (continued)Example of a Cash Flow BudgetTotal Jan Feb March April May June July Aug Sept Oct Nov Dec

35 Total cash operating expenses 108,500 1,650 3,000 21,150 14,050 4,500 2,950 650 1,800 2,850 6,050 46,400 3,450Capital expenditures:

36 Machinery and equipment 60,000 60,00037 Breeding livestock 1,000 1,00038

Other expenditures:39 Family living expenses 36,000 3,000 3,000 3,000 3,000 3,000 3,000 3,000 3,000 3,000 3,000 3,000 3,00040 Income tax and social security 8,000 8,00041 Other nonfarm expenses4243

Scheduled debt payments:44 Current debt - principal 045 Current debt - interest 046 Noncurrent debt - principal 32,000 6,000 20,000 6,00047 Noncurrent debt - interest 27,200 12,000 3,200 12,000

Total cash outflow48 (add lines 35-47) 272,700 4,650 24,000 92,150 17,050 7,500 30,150 3,650 22,800 5,850 9,050 49,400 6,45049 Cash available (line 13-line48) (5600) 18,650 15,250 (76,300) (15,950) (6,450) (29,100) (2,550) 70,050 663 52,213 37,376 31,526

New borrowing:50 Current 92,700 36,800 16,400 6,900 29,600 3,00051 Noncurrent 40,000 40,00052 Total new borrowing 132,700 76,800 16,400 6,900 29,600 3,000

Payments on new current debt53 Principal 92,700 67,400 25,30054 Interest 2,874 2,137 737

Total debt payments55 (line 53 + line 54) 95,574 69,537 26,037

Ending cash balance (lines 49 + 52 - 55) 31,526 18,650 15,250 500 450 450 500 450 513 663 26,176 37,376 31,526

Summary of debt outstanding Current (beginning of $0) 0 0 0 36,800 53,200 60,100 89,700 92,700 25,300 25,300 0 0 0 Noncurrent (beg. of $340,000) 340,000 340,000 334,000 374,000 374,000 374,000 354,000 354,000 348,000 348,000 348,000 348,000 348,000 Total debt outstanding 340,000 340,000 334,000 410,800 427,200 434,100 443,700 446,700 373,300 373,300 348,000 348,000 348,000

farm management chapter 13

12

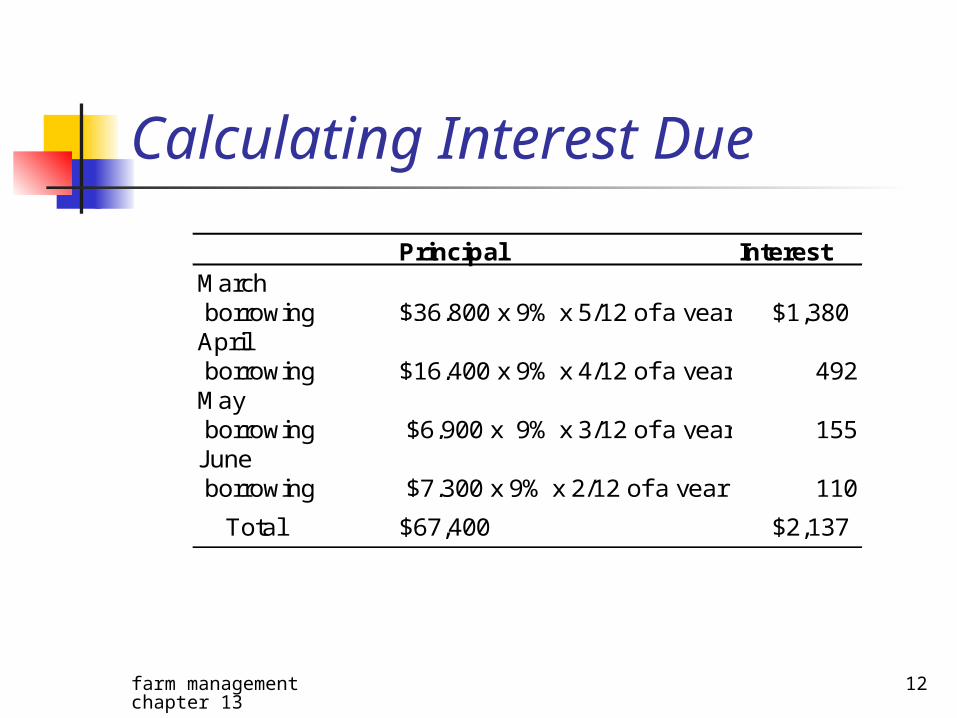

Calculating Interest Due

Principal InterestMarch borrowing $36,800 x 9% x 5/12 of a year = $1,380April borrowing $16,400 x 9% x 4/12 of a year = 492May borrowing $6,900 x 9% x 3/12 of a year = 155June borrowing $7,300 x 9% x 2/12 of a year = 110

Total $67,400 $2,137

farm management chapter 13

13

Uses for a Cash Flow Budget

1. Plan borrowing and debt repayment2. Suggest ways to minimize borrowing3. Combine business and personal financial

affairs into one complete plan4. Help establish realistic line of credit5. Plan purchases to obtain discounts6. Aid tax planning7. Find imbalances between current and

noncurrent debt

farm management chapter 13

14

Monitoring Actual Cash Flows

A cash flow budget can be used formonitoring and control. The budgetedamounts can be compared to whatactually transpires.

farm management chapter 13

15

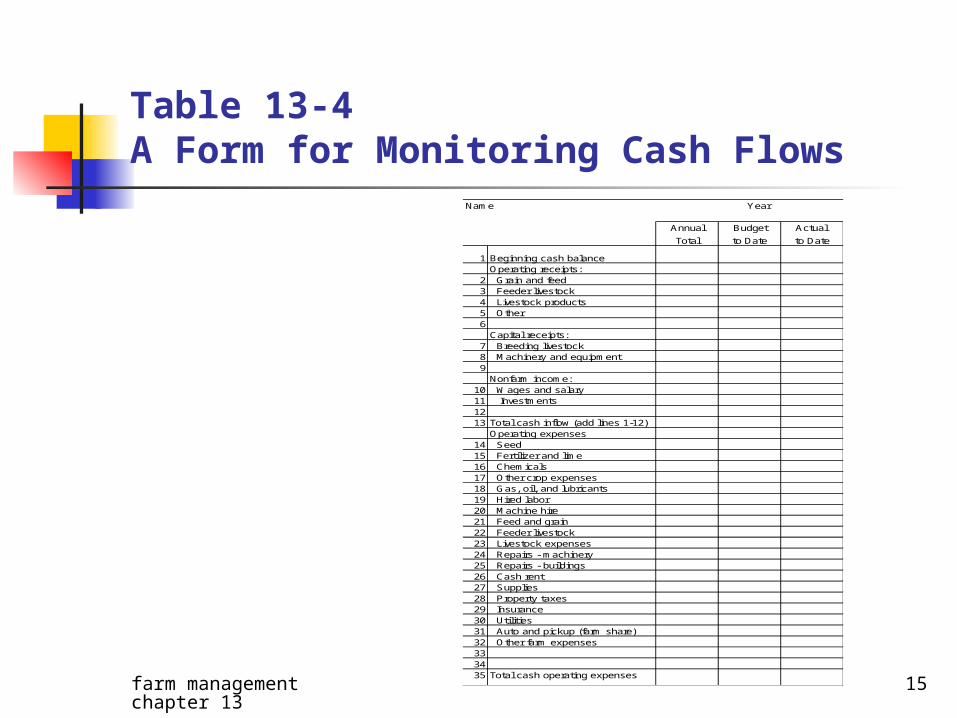

Table 13-4A Form for Monitoring Cash Flows

Annual Budget Actual

Total to Date to Date

1 Beginning cash balanceOperating receipts:

2 Grain and feed3 Feeder livestock4 Livestock products5 Other6

Capital receipts:7 Breeding livestock8 Machinery and equipment9 Nonfarm income:

10 Wages and salary11 Investments12 13 Total cash inflow (add lines 1-12)

Operating expenses14 Seed15 Fertilizer and lime16 Chemicals17 Other crop expenses18 Gas, oil, and lubricants19 Hired labor20 Machine hire21 Feed and grain22 Feeder livestock23 Livestock expenses24 Repairs - machinery25 Repairs - buildings26 Cash rent27 Supplies28 Property taxes29 Insurance30 Utilities31 Auto and pickup (farm share)32 Other farm expenses333435 Total cash operating expenses

Name___________________ Year ____________

farm management chapter 13

16

Investment Analysis Using a Cash Flow Budget

Will a new investment generateenough cash income to meet itsadditional cash requirements? Inother words, is the investmentfinancially feasible?

farm management chapter 13

17

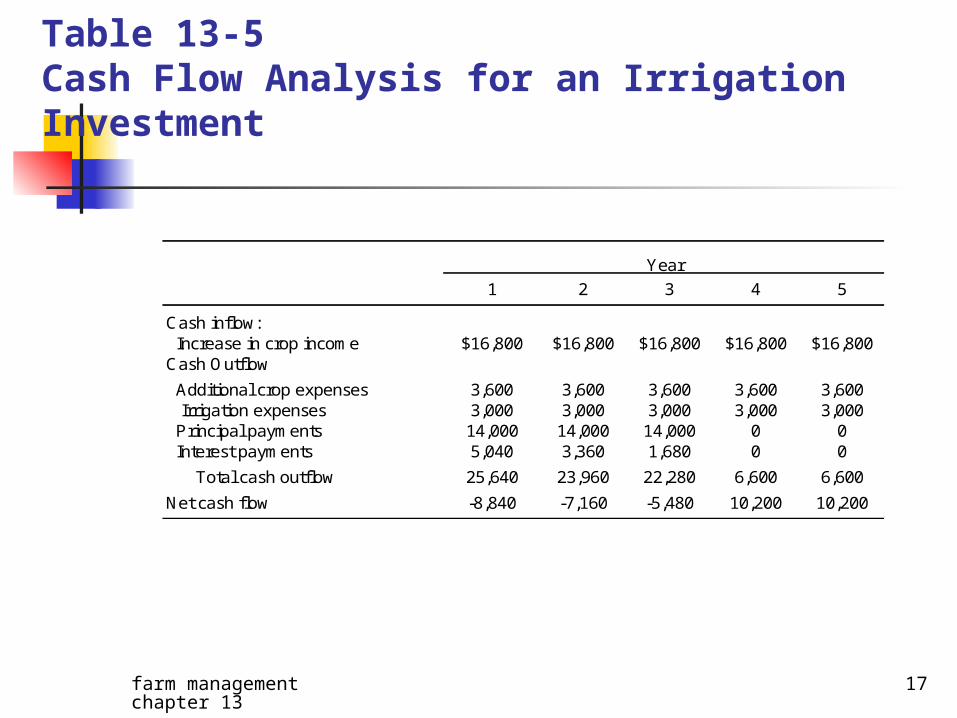

Table 13-5Cash Flow Analysis for an Irrigation Investment

1 2 3 4 5

Cash inflow: Increase in crop income $16,800 $16,800 $16,800 $16,800 $16,800Cash Outflow

Additional crop expenses 3,600 3,600 3,600 3,600 3,600 Irrigation expenses 3,000 3,000 3,000 3,000 3,000 Principal payments 14,000 14,000 14,000 0 0 Interest payments 5,040 3,360 1,680 0 0

Total cash outflow 25,640 23,960 22,280 6,600 6,600

Net cash flow -8,840 -7,160 -5,480 10,200 10,200

Year

farm management chapter 13

18

Summary

A cash flow budget is a summary ofall cash inflows and outflows for a givenfuture time period. No noncash entriesare included. This budget can providean estimate of borrowing needs andrepayment capacity. It can also beused to analyze the feasibility of investment alternatives.

farm management chapter 13

19

1. Why is machinery depreciation not included on a cash flow budget?

Machinery depreciation is a noncash expense and only expenses requiring a cash outflow are included on a cash flow budget. For this reason, a cash flow budget contains no depreciation of any kind.

farm management chapter 13

20

2. Identify four sources of cash inflows which would not be included on an income statement but which would be on a cash flow budget. Why are they on the cash flow budget?

Cash received from: 1) new loans, 2) nonfarm income, 3) full sale price of capital assets, and 4) gifts and inheritances. They are on a cash flow budget because they are cash inflows and represent cash, which is or could be available for farm use even though they are not farm business revenues.

farm management chapter 13

21

3. Identify four types of cash outflows which would not be included on an income statement but which would be on a cash flow budget. Why are they on the cash flow budget?

Cash used for: 1) principal payments on debt, 2) full purchase price of capital assets, 3) family living expenses and other personal withdrawals, and 4) income and self employment taxes. They are on a cash flow budget because each requires the expenditure of cash but are not farm business expenses.

farm management chapter 13

22

4. Identify four noncash entries found on an

income statement but not on a cash flow budget

Noncash entries found on an income statement but not on a cash flow budget include: 1) inventory changes,

2) accounts receivable, 3) accounts payable, and 4) depreciation

farm management chapter 13

23

5. Discuss the truth or falsity of the following statement: A cash flow budget is used primarily to show profit from the business.

This statement is false. A cash flow budget should not be used to project profit. Questions 2, 3, and 4 above illustrate some of the major differences between finding net cash flow and net farm income. While a large number of the same items appear on both of these financial documents, there are too many differences to be able to estimate net farm income from a cash flow budget.

farm management chapter 13

24

Discuss how you would use a cash flow budget when applying for a farm business loan

A cash flow budget is extremely helpful when applying for a loan. It shows why, when, and how much money will be needed. Just as important, it shows if, when, and how much of the loan can be repaid with interest. A lender is interested in both aspects but particularly in the repayment ability shown on the cash flow budget.

farm management chapter 13

25

8. A feasible cash flow budget should project a positive cash balance for each month of the year, as well as for the entire year. When making adjustments to the budget to achieve this, should you begin with the annual cash flow or

the monthly values? Why