Embed Size (px)

Citation preview

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 1 of 17

and Capital Trade Incorporated

�������������������������������

����������� ���

��������������������� ������������������ ���� �� ��!"�# $% &����� �$ ���'� �('��)��* +������

��# ��!�� ��,�� ���������������� ��� �� ��!"�# $% &����� �$

���'� �('��)��* +��������������-�.�������� ���

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 2 of 17

and Capital Trade Incorporated

����������� ����������������������� ������������������ ���� �� ��!"�# $% &����� �$ ���'� �('��)��* +������

��# ��!�� ��,�� ���������������� ��� �� ��!"�# $% &����� �$ ���'�

� �('��)��* +��������������-�.�������� ����

� ����������� �������������������������������������� �����!� ���"�#$�%�&��'������������&��������()�������� �!���) �������� ��' ��*� � ��������� ����"'��������+%���������()�,� ������-)��������������&����.�� �����������.������������%������/�%���&����*� ����"'���������������.����.������.���� 012� &����*� ����"'������������� � �������)������������� � 3� ����".�����)���4&��'��� � � ���5� 6� 7889� ����������������&��'��' ������������ ���.���������/�������:;<=�&�����������&��'��� 5�&>���)�������������&��&��'�������������� ���.���������/������� ?<?� &��������&��&��'��� � �������)���� ��������� ���"�#$�%���)5�4���)���5����� �����012� &����������� 5� 6� 7889����.���������/� :@<A��������������4����$���()�����/��/�012�&����������-)����.���������/�:<:��������������4����$������012�&��'�����.���������/� 789� ������������4����$� � ������������� ��������� ���� ����#���.�5�����/��)�.�5��%������������� �����*��%�����)'�������'��� ���/5�����&��&������ ���/����/�������*�� ����������� �������������������������������������� ������ 3�' '����)�����%�B%�� ���"�#$�%�'�����&��������� ����%���'��5+��//��������$��&���.�� 0CD2� �-)�� 3���)�����/��)�' 5�����%�����E��������������� ����"5���� ����%�!�����/���!� ����+�E�������������� �������������������������������������� � � �//������ 0CD2� � 3��//��������������)�' � FGHIHJKL�HMNOLOPJONQ� QRSHLT� ��)��$��&���.��-)��/��� 3������& �"�#$�%�������������!�% � �����'��U ���//������ 0CD2� ����*�����&U������������ ����&U�&���//��������������)�' ����//������()�,5����#>���������� (�� �����V��' �.�����%�����E��� ����%�!� ����+�E���!�����/��)�����%�&-*������� ������������5�����W#X��-)����������/&���.���%�� � �����/

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 3 of 17

and Capital Trade Incorporated

�������&���//��������������)�' � (�� ���� ����/&�������!�% 5��//��������������)�' '�������V�����"-�#��%�����E�Y���������5�/����&��%����-)������������4 ��'��'���������/���������� �������-)��(��$��&���.�5��//������0CD2�������+������ Z���/�������)�' �@[9� 6:��� &�����/������)�' 5������������ ������������� (�� �������� ��������������5���������%)���������%�������&�� ����"��&-*�� �����Y���������%)���������� ����������������5�����������5��%�����)�����'��� ���/5�����&��&������ ���/����/��%)�&-*�� ��������&����%)�&-*������%)������(�������/!.�/�%��� � ����%�����������()���������&��&����)�.�&-*�� � ������������������������������� ���%�B%���� � �����'��U �������������� �������������U��!�����/��)��' �������!� ����+�E/������� ���%� �%���/�� ���������.4����"������5��������!�% ��������%����������� ����������� �������������������������������������� ����%� ����+�E �� ����"'�������'�\�����"-�#�'�������������//����������/�7��V�����>E������//�������)�:�F]̂_:T�� 3��V�����>E5����������-)������!�����/&����� ������������5�+������������ :[;� 6������//�������)� 7� F]̂_7T� � 3��V�����>E5���������-)������!�����/&����� ������������5�+������������A[:8� 6��!���)'������//�������*�����V�����>E���������/�W#X��� �'��'��� 3�' ����)�����>E'��������������������� ������������������������ ������������������ ��!"�

:���()�����&���.�&���//������0CD2���)5+���.�5� Z���/��� 3�$��&���.� 6�788:���������*����()��� V� ����E5����"-�#��%�����E��� ����#�&��'��5��//������-�V.� ��/� ��)��5��������V-�&���.� 6� 7889� � ��������*� ����������!�% 5���&������>̀ E� ���������� %���)����.�5�$��&���.��0CD2�'��V.���������� 3������&������ (����&������>̀ E�������&����������� %������������/���&���.����������������������!�% &����&��%����������������/ ����"'����%���������������������������������������� �

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 4 of 17

and Capital Trade Incorporated

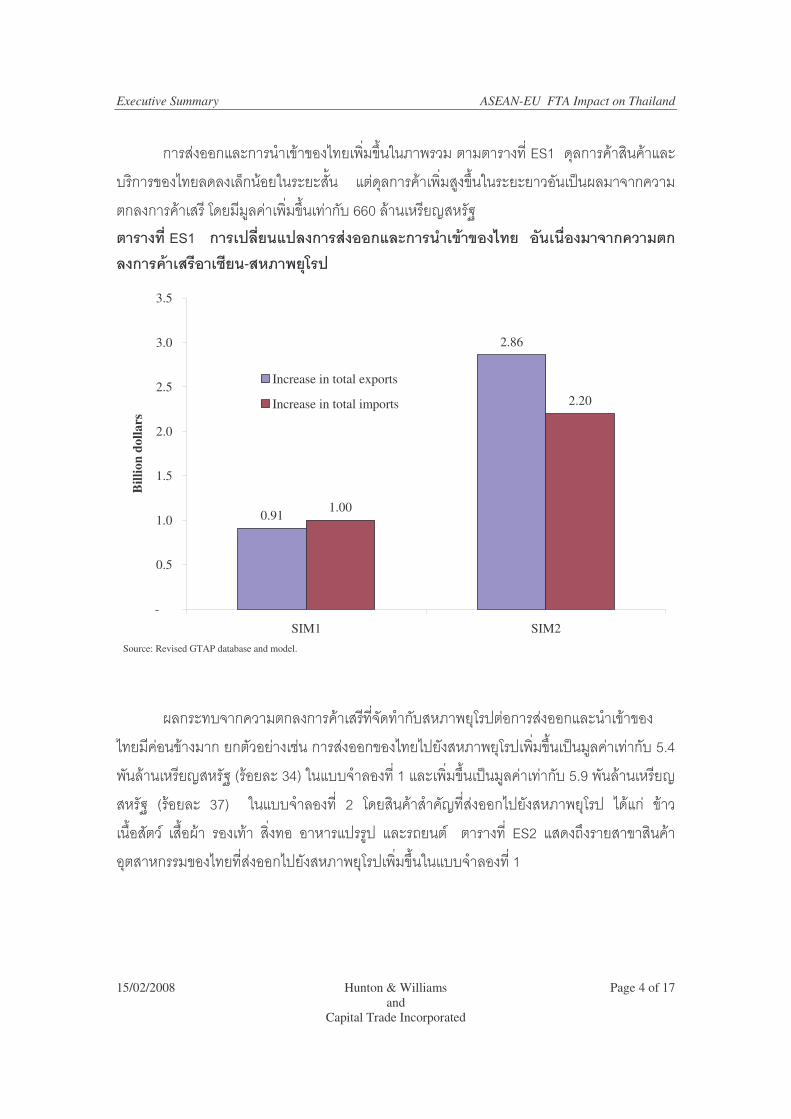

� ������������������&��&��'����%)�&-*�5�������� �� ������)�a]:�����������%������/�%���&��'��������U�����5�������*�� � �����������%)��.�&-*�5������������ 3�!��������� �������������������.�����%)�&-*�������/�998����������4����$�� � ��'/�012�� � ����'/������� ����������� ��# �. .�� ��� �!���3/��& � �$% &����� �$ ���'� �('��)��* +������

0.91

2.86

1.00

2.20

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

SIM1 SIM2

Bill

ion

dolla

rs

Increase in total exports

Increase in total imports

Source: Revised GTAP database and model. ��

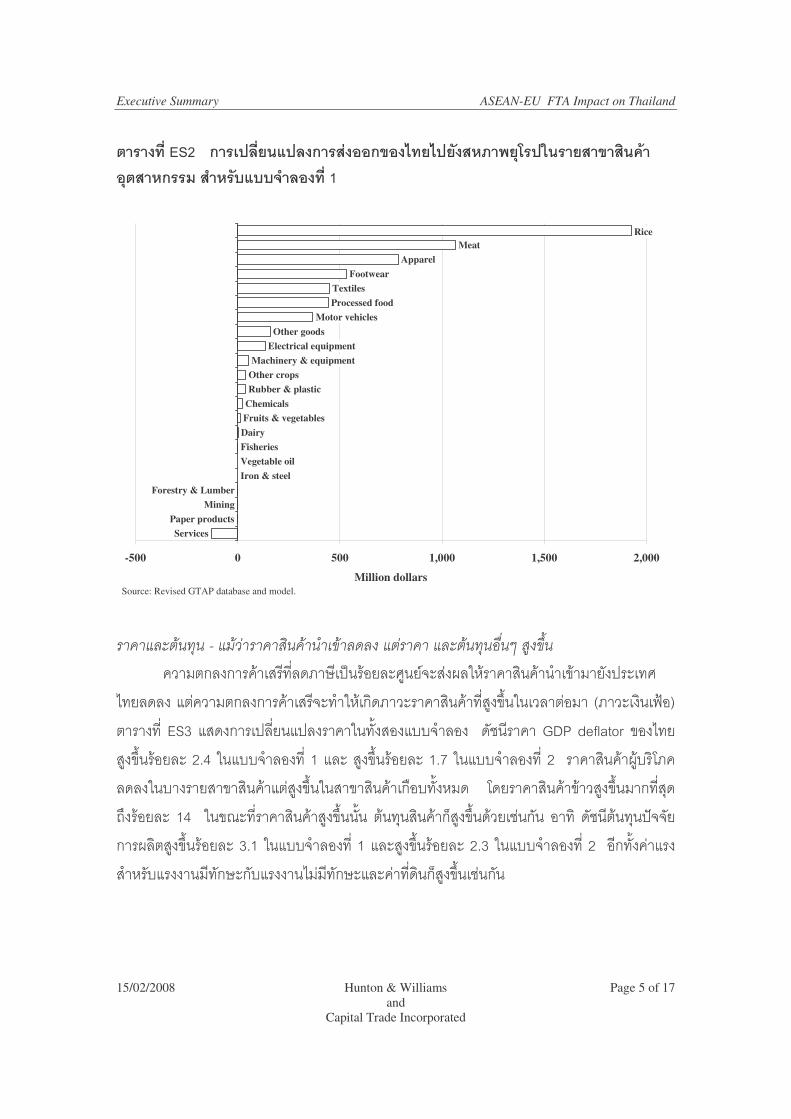

� !�����/������ ��������������)�������/��������� �����������������&��&��'�������&��������� ��������+������������&��'��' ������������ ��%)�&-*�� 3��.���������/�A<@�������������4����$�F�������;@T�5��//�������)�:������%)�&-*�� 3��.���������/�A<=�������������4����$� F������� ;bT� � 5��//�������)� 7� ����%������4��)������' ������������ � '������ &������(*��� �E���(*�!������������%)���������� ��. �����V�� E� � ������)�a]7�����V-������&��%����� �������&��'����)������' ������������ ��%)�&-*�5��//�������)�:���

�

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 5 of 17

and Capital Trade Incorporated

� � ��'/�014�� � ����'/������� �������.�� �� ��!���* +�����5�� �� . ���$ ���� ����&��# ��!�����# ����'/�2���

ServicesPaper products

MiningForestry & Lumber

Iron & steelVegetable oilFisheriesDairyFruits & vegetablesChemicalsRubber & plasticOther cropsMachinery & equipment

Electrical equipmentOther goods

Motor vehiclesProcessed foodTextiles

FootwearApparel

MeatRice

-500 0 500 1,000 1,500 2,000

Million dollarsSource: Revised GTAP database and model. ������� ����� �������"������������������ � ��������� ����� ��#��$��%������ ��� ��������������)����#�� 3�������".��E�����!�5������%������&������� ����"'�������� ���� ����������������5����%���������%�����)�.�&-*�5����� ����� F������%��cd�T�� ������)�a];��������� ��)��� �����5���*�����//������ ���+������012�SHeLKfRJ� &��'���.�&-*��������7<@� 5��//�������)�:������.�&-*��������:<b�5��//�������)�7� �����%���!.�/�%������5�/�������&��%���� ��.�&-*�5���&��%�����(�/��*����� �������%���&����.�&-*������)���V-�������� :@� � 5�&>���)����%����.�&-*���*�� ������%����U�.�&-*������+���������%���+�� ����� Z�������!�% �.�&-*��������;<:�5��//�������)�:�����.�&-*��������7<;�5��//�������)�7� ������*�����������/�����������#���/������'�������#��������)�%��U�.�&-*��+��������

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 6 of 17

and Capital Trade Incorporated

����� � ��'/�016�� ����������� $ ��������.�� ���

�

SIM1 SIM2

GDP deflator 2.4 1.7Import price range by sector -7.9 to 0.1 -7.9 to 0.3Consumption price range by sector -2.1 to 14.0 -2.1 to 14.4Factor cost index 3.1 2.3

Item/SectorPercent Change

Source: Revised GTAP database and model. ���"!�������!������ ������"!�������!�������&!��������'�� ��� 5���� ����%�!�����/������ �������������%��"-�#����� ��)��� ����������%������������ � ��������*� �����-�V-��������������������)��&-*�� ���� ��)��� ������������� ���/����/������%)�&-*�&������������� ��)��� �������()�,� ������)����5� ������)�a]@�!�'����������%�������&��'����)'�������� ��������������()�����/��/!�'����������%�������&��������������������)�.������()�����/��/ ����"��������()�,� � 5��//�������)� :� !�'����������%�������&��'����!�����������%)�&-*�5��� �������� �5��//�������)�7������%)�&-*�&���������������������������)��&-*� ����U��������4�

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 7 of 17

and Capital Trade Incorporated

�� � ��'/�017�� �������� ��%!�"�� ��!�$&��������� ���� �('��������* +������

1.3

3.3

0.1

2.8

7.8

1.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Thailand ASEAN EU

Bill

ions

of d

olla

rs

SIM1 SIM2

Source: Revised GTAP database and model. �

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 8 of 17

and Capital Trade Incorporated

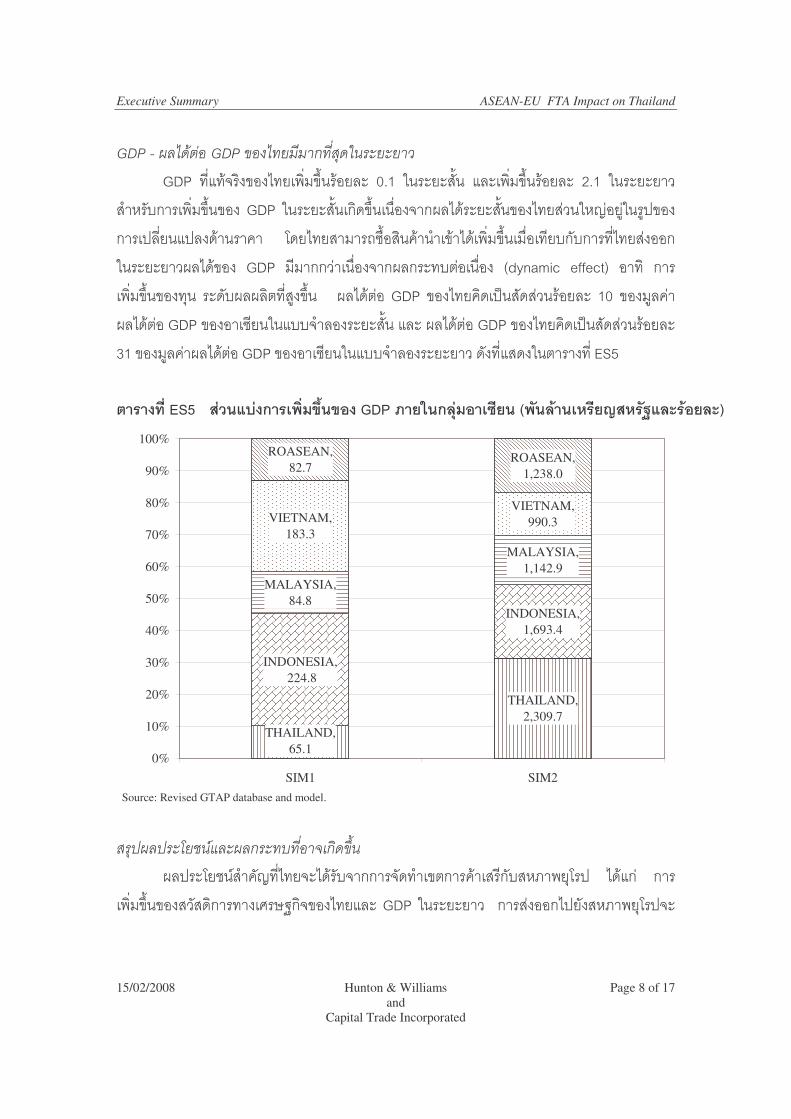

()*���� ������()*�������'����'�� �+�������"�� 012� ��)�����%�&��'����%)�&-*�������� 8<:� 5�������*�� �����%)�&-*�������� 7<:� 5���������������/�����%)�&-*�&���012� 5�������*���%�&-*���()�����!�'��������*�&��'������5�4���.�5��. &������ ��)��� ���������� ���'�������V�(*��%������&��'����%)�&-*���()�����/��/�����)'����������5��������!�'��&��� 012� �����������()�����!�����/ ����()��� FSgIKQOh� HeeHhfT� ���%� �����%)�&-*�&����������/!�!�% ��)�.�&-*�� � �!�'�� ���012� &��'��%�� 3��������������� :8� &���.���!�'�� ���012�&���������5��//�����������*������!�'�� ���012�&��'��%�� 3���������������;:�&���.���!�'�� ���012�&���������5��//������������������)����5� ������)�a]A��� � ��'/�018�� ��%������ ��+�/&.,9�.���:;<�* �5�����&� �('���=+!�� ����'�>���!���������?�

THAILAND, 2,309.7

INDONESIA, 1,693.4

MALAYSIA, 1,142.9

ROASEAN, 1,238.0

THAILAND,65.1

INDONESIA, 224.8

MALAYSIA,84.8

VIETNAM,990.3VIETNAM,

183.3

ROASEAN,82.7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SIM1 SIM2Source: Revised GTAP database and model. ���� ,� ,��-�&�.� �� ����/�'�������������� !� ����+�E���4��)'����'����/������������& �����������/��������� � '������ �����%)�&-*�&�������%�������"�#$�%�&��'������012� 5��������� ����������' ������������ ��

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 9 of 17

and Capital Trade Incorporated

��%)�&-*��������������*����������5��������������� � ������&����)����5�� ����+�E���!.�/�%�������B���%�'����)�(*��� V��%/���&����������������)�.�&-*����!�����/��*������������#����'�������#���� �����'��U ��� �����%)�&-*�&������������ 3������%)�&-*���������� ��5��%���&���� ��(*��� �E���(*�!������������%)���������� ��. �����V�� E����()�������������������()������' ��������&��%�����)�������������%)�&-*�� �-���5��!�!�% ������'��5������&��%����()������-)��%�����)���4&��'��5� Z���/������%��%����%��U�����%��E������������ %�����������*���� ��������������5������%����.�&-*�� F������%��cd�T� ��������� Z�������!�% ��)�.�&-*�'�������/��/����%���&�*����������)�.�&-*�' ����������U ������ Z�������������������*� 3�!�����/��)���4������������& ����������������������&��-�/���� ��()�����!�����//������ 0CD2� ��(�����%�����E����"�#$�%�����//�����5����#>��()����5��������45�����%���>�V-�������(����%�&������������� �//�����'������#�� 3�������".��E�����/�������*����������� ����"���+%�������������������� � � 5���� i%/� %�������������5������������#�� 3�/�����������������������#������/�%�������'��� ����%�������'������������.�5�������%�����(*��� �E��� "��� �E� ���������%)��������(*�!����-)���������������&��'��5�������%��������������.�&-*�����()������&�������&������ j�����5�������%����������������������5������������#���)���&-*�� �������5��!�'��������������&��'��5��%���������������� ���� 3���������������%��cd��������.4�������!�!�% ��)���������%�&-*�5��%����()�,&��'��� � �����*�� >������kl��'�����������()��������)����������5���������������#�������������5������������%������4� � ����5 ��V�����>E Z���/��� ��������5��������#���)�������)�������������)��%)�&-*������Y�/�����U'��'��� 3���()����)'�����������)�&��5���� �����/����/�)���/���������� FfJKSH� SOmHJnORIT� ���5������ ����"���+%�������������������!�����/ ���� �������&��'��5�/����&��� �������������*�� ����.4������)��%�

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 10 of 17

and Capital Trade Incorporated

�������/�)���/���������&�� ����"���+%��������V.���/' �����()�+�)��*�������/!�'����)�������'����/�������.4������)��%��������/�)���/���������&�� ����"�()�,��)'��'��� 3�������-)�&������������� �������������������[��������� � � �����*�� �������� ��������5��������������������&��'���-���������4���������������� �������/��������� �

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 11 of 17

and Capital Trade Incorporated

EXECUTIVE SUMMARY Economic Costs and Benefits to Thailand of an ASEAN-EU FTA

for

the Study on ASEAN-EU FTA Impact on Thailand and Thailand’s Strategy

The envisioned FTA between ASEAN and the European Union will have far

reaching consequences for Thailand’s economy for four fundamental reasons. First,

Thailand and other ASEAN countries are highly dependent on trade. Total trade of

goods and services exceeds GDP for both Thailand and ASEAN. Second, the EU is also

a major trading partner of Thailand. In 2006, the EU absorbed 13.9 percent of Thailand’s

exports and supplied 8.8 percent of Thailand’s imports. Third, the EU collectively is the

world’s largest economy. Its GDP in 2006 was $14.5 trillion dollars compared to $1.1

trillion for ASEAN economy and $206 billion for Thailand. Finally, the EU has high

tariffs in many product categories, including many in which Thailand has a comparative

advantage. As a result of these circumstances, an FTA between ASEAN and the EU

appears likely to have a relatively large impact on the Thai economy.

In order to assess the costs and benefits of the envisioned FTA between ASEAN

and the EU, we used the GTAP model and database, which is commonly accepted in

international trade analysis. The GTAP model is a multiregion and multisector applied

general equilibrium model. There are advantages and disadvantages to such a model.

The advantage of the GTAP model and others like it is that they allow us to assess and

quantify the benefits and costs likely to arise from a given agreement in a theoretically

consistent way with real data. On the minus side, the sector composition in the model

may not allow in some cases for specific analysis of some narrowly defined industry

sectors that may be important to Thailand. Another drawback is that the data in such

models are generally 4-to-6 years out of date. 2

2 Unfortunately, the data requirements for the GTAP model are so large that the current database for the model is based on 2001 data. For purposes of our analysis, we have modified the tariff rates in the model for Thailand so that they reflect 2006 levels. We have also decomposed the existing chemical, rubber, and plastic sector in the GTAP database into a chemical sector and a rubber and plastic sector by incorporating the trade and production share data of these sectors for Thailand, Indonesia, Malaysia, Vietnam, and the EU.

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 12 of 17

and Capital Trade Incorporated

The standard argument in favor of trade agreements is that they increase trade and

national welfare. In particular, trade agreements are expected to increase exports in

sectors that have a comparative advantage, increase imports and therefore consumer

choice, reduce price levels due to increased competition, and produce a more efficient

allocation of resources. However, even the most ardent proponents of free trade note that

there are costs that partially offset the benefits. Such costs include sector-specific losses

in output and employment.

How does the envisioned FTA between ASEAN and the EU benefit Thailand?

We performed two simulations. SIM1 is a medium run scenario that simulates the impact

of the FTA in one-to-three years. SIM2 is a long-run scenario that can be viewed as

reflecting the impact of the FTA in 5-to-10 years. The results are consistent with theory,

but nevertheless surprising.

Trade—Exports and imports increase, but Thailand’s gains are concentrated.

Thailand’s exports and imports increase overall, as shown in ES1 below.

Thailand’s balance of trade in goods and services declines slightly in the short run but

increases in the long run as a result of the agreement by $660 million.

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 13 of 17

and Capital Trade Incorporated

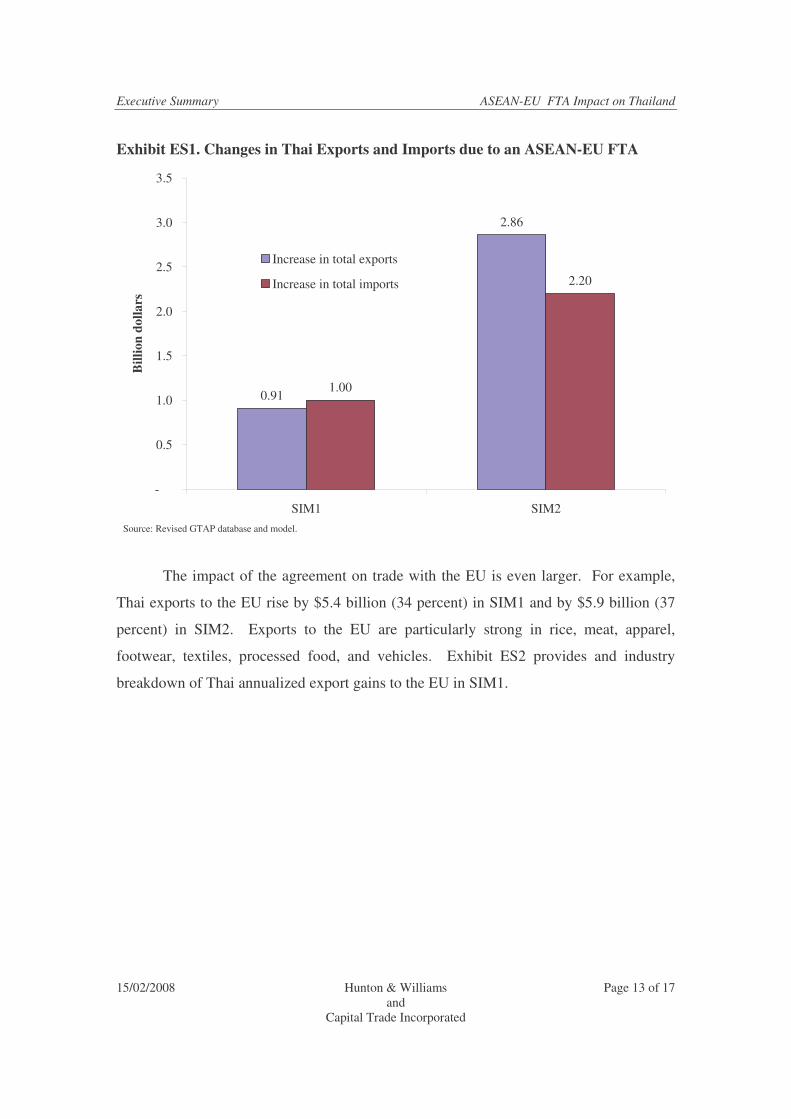

Exhibit ES1. Changes in Thai Exports and Imports due to an ASEAN-EU FTA

0.91

2.86

1.00

2.20

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

SIM1 SIM2

Bill

ion

dolla

rs

Increase in total exports

Increase in total imports

Source: Revised GTAP database and model.

The impact of the agreement on trade with the EU is even larger. For example,

Thai exports to the EU rise by $5.4 billion (34 percent) in SIM1 and by $5.9 billion (37

percent) in SIM2. Exports to the EU are particularly strong in rice, meat, apparel,

footwear, textiles, processed food, and vehicles. Exhibit ES2 provides and industry

breakdown of Thai annualized export gains to the EU in SIM1.

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 14 of 17

and Capital Trade Incorporated

Exhibit ES2. Changes in Thai Exports to EU by Industry in SIM1

ServicesPaper products

MiningForestry & Lumber

Iron & steelVegetable oilFisheriesDairyFruits & vegetablesChemicalsRubber & plasticOther cropsMachinery & equipment

Electrical equipmentOther goods

Motor vehiclesProcessed foodTextiles

FootwearApparel

MeatRice

-500 0 500 1,000 1,500 2,000

Million dollarsSource: Revised GTAP database and model.

Prices and Costs—Though import prices decline, other prices and costs increase.

An FTA that eliminates duties would result in lower import prices in Thailand,

but the FTA is by and large inflationary. Exhibit ES3 summarizes the prices changes

from the two simulations. Thailand’s GDP deflator increases 2.4 percent in SIM1 and

1.7 percent in SIM2. Consumption prices fall in some sectors but are higher in most,

with the price of rice rising by 14 percent. While businesses get higher prices for their

products, business costs rise as well; the index of factor costs increases by 3.1 percent in

SIM1 and 2.3 percent in SIM2. Labor costs for skilled and unskilled workers and the

price of land also increase.

Exhibit ES3. Price and Cost Effects on Thailand SIM1 SIM2

GDP deflator 2.4 1.7Import price range by sector -7.9 to 0.1 -7.9 to 0.3Consumption price range by sector -2.1 to 14.0 -2.1 to 14.4Factor cost index 3.1 2.3

Item/SectorPercent Change

Source: Revised GTAP database and model.

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 15 of 17

and Capital Trade Incorporated

Welfare—Thailand’s welfare gains show the strongest performance.

Changes in welfare are a preferred way to assess the impact of trade agreements.

It takes into account not only improvements in resource allocation, but also relative price

changes, additions to capital stock, and other changes. As shown in Exhibit ES4,

Thailand accounts for a disproportionately high share of ASEAN’s welfare gains

resulting from the FTA. In SIM1, Thailand’s gains are largely the result of an

improvement in the terms of trade. In SIM2, the addition of capital stock and improved

resource allocation are also important.

Exhibit ES4. Welfare Effects on Thailand, ASEAN, and the EU

1.3

3.3

0.1

2.8

7.8

1.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Thailand ASEAN EU

Bill

ions

of d

olla

rs

SIM1 SIM2

Source: Revised GTAP database and model.

GDP—Thailand’s GDP gains are greatest in the long-run.

Thailand’s real GDP increases by a 0.1 percent in the short run and 2.1 percent in

the long run. The modest short run increase occurs because most of Thailand’s short-run

gains are in the form of price changes: Thailand is able to purchase more imports with its

exports. The GDP gains are much larger in the long run because dynamic effects, such as

the addition of capital stock, enable higher levels of output. Thailand’s GDP gains

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 16 of 17

and Capital Trade Incorporated

account for 10 percent of ASEAN GDP gains in the short run simulation, but 31 percent

of those gains in the long run simulation, as shown is ES5.

Exhibit ES5. Distribution of GDP Increases within ASEAN ($ Bil. and percent)

THAILAND, 2,309.7

INDONESIA, 1,693.4

MALAYSIA, 1,142.9

ROASEAN, 1,238.0

THAILAND,65.1

INDONESIA, 224.8

MALAYSIA,84.8

VIETNAM,990.3VIETNAM,

183.3

ROASEAN,82.7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SIM1 SIM2Source: Revised GTAP database and model.

Summary of benefits and costs

The major benefits of an FTA with the EU would be an increase in Thailand’s

economic welfare and, in the long run, GDP. Exports rise by a significant amount to the

EU, and rise overall as well. Import prices decline, benefiting consumers and Thai

businesses that purchase imported inputs. Wages rise, benefiting both skilled and

unskilled workers.

However, the increase in exports is heavily concentrated in rice, meat, apparel,

footwear, textiles, processed food, and vehicles. As labor and capital resources shift into

sectors where export demand is booming, output and revenue declines in other sectors,

some of which are currently important to Thailand, including the electronics and rubber

and plastic. The agreement is also inflationary, though higher prices for inputs are offset

by even higher prices for final goods. These are the main costs of an FTA.

Executive Summary ASEAN-EU FTA Impact on Thailand

15/02/2008 Hunton & Williams Page 17 of 17

and Capital Trade Incorporated

Policy implications

When drawing implications from GTAP experiments, or any other model-based

economic analysis, it is important to consider how realistic the experiments are.

The simulations eliminate duties on all trade between ASEAN countries and the

EU. In practice, there will be phase-in periods, partial duty reductions, and even

exclusions for sensitive products. Many of these sensitive products are in the meat and

live animals section, and in the textile and apparel sections, where Thai exports are

predicted to increase. Limitations on liberalization in those sectors, as well longer phase-

in periods, are likely to reduce the Thai export gains in those sectors, and limit inflation

and output losses predicted for other Thai industries. Thai negotiators should fight to

avoid excessive phase-in periods for key products, but under the current circumstances,

phase-in periods that avoid sudden, potentially disruptive, increases in export demand are

not such a bad thing.

As for trade diversion among ASEAN countries, it is expected to affect only a

few Thai industries. Any trade diversion losses to ASEAN countries are far outweighed

by trade diversion gains at the expense of other countries that would not be part of the

ASEAN-EU FTA. Internal negotiations within ASEAN, therefore, are less important to

securing overall gains for Thailand than are negotiations with the EU.

�