Embed Size (px)

Citation preview

B-1049 Brussels - Belgium - Office: MO59 4/11. Telephone: direct line (+32-2)299.06.59, switchboard 299.11.11. Fax: (+32-2)295.05.51. Telex: COMEU B 21877. Telegraphic address: COMEUR Brussels. X.400: G=Tove; S=Mogensen; I=TM; P=CEC; A=RTT; C=BE Internet: Internet: [email protected]

EUROPEAN COMMISSION DIRECTORATE GENERAL TAXATION AND CUSTOMS UNION TAX POLICY Excise duties and transport, environment and energy taxes

REF 1.019 May 2004

! ! ! ! ! ! ! ! ! ! ! !

EXCISE DUTY TABLES Part II � Energy products and Electricity

! ! ! ! ! ! ! ! ! ! ! !

New in accordance with the Energy Directive (Council Directive 2003/96/EC)

Now INCLUDING Natural Gas, Coal and Electricity

Intermediate report…to be completed in Autumn 2004

Can be consulted at: http://europa.eu.int/comm/taxation_customs/publications/info_doc/info_doc.htm

(Shows the situation as at 1 May 2004)

2

Intermediate report May 2004

INTRODUCTORY NOTE

In collaboration with the Member States, the European Commission has established the “EXCISE DUTY TABLES” showing rates in force in the Member States of the European Union . As from 1 May 2004 this publication: * covers the 25 Member States of the EU and the two Candidate Countries (Bulgaria and Romania); * has been devided into three different sections:

I Alcoholic Beverages II Energy products and Electricity III Manufactured Tobacco.

This publication aims to provide up-to-date information on Member States main excise duty rates as they apply to typical products. It is intended that Member States will regularly communicate to the Commission all modifications of the rates covered by this publication and that revised editions of the tables will be published at regular intervals. To this end, it is vital that all changes to duty structures or rates are advised by Member States to the Commission as soon as possible so that they may be incorporated in the tables with the least possible delay. All details should be sent to Mrs Tove Mogensen: e-mail [email protected] fax...................Int-32-2-295.05.51; telephone.........Int-32-2-299.06.59. This document together with general information about the Taxation and Customs Union can be found at: http://europa.eu.int/comm/taxation_customs/publications/info_doc/info_doc.htm

3

Intermediate report May 2004

IMPORTANT REMARK

Concerning transitional arrangements for the "new member States"

of the European Union

Council Directive 2003/96/EC – Energy taxation Directive The energy taxation Directive (2003/96/EC – "energy Directive) was adopted in 2003 and defines the fiscal structures and the levels of taxation to be imposed on energy products and electricity. It replaces, with effect from 1 January 2004, Council Directive 92/81/EEC (on the harmonisation of the structures of excise duties on mineral oils) and Council Directive 92/82/EEC (on the approximation of the rates of excise duties on mineral oils). The energy Directive is in compliance with Community commitments to integrate environmental concerns into the energy taxation area and will improve the functioning of the Internal Market. The 2003 Treaty of Accession1 provided for transitional arrangements and specific measures for two new Member States2. In addition, two additional Council Directives for specific arrangements were adopted on 29 April 2004 (Directive 2004/74/EC3 and Directive 2004/75/EC4). Directive 2004/74/EC amends the energy Directive as regards the possibility for the Czech Republic, Estonia, Latvia, Lithuania, Hungary, Malta, Poland, Slovenia and Slovakia to apply temporary exemptions or reductions in the levels of taxation. Directive 2004/75/EC amends the energy Directive as regards the possibility for Cyprus to apply temporary exemptions or reductions in the levels of taxation.

1 OJ L 236, 23.9.2003, p. 17. 2 Cyprus and Poland. 3 OJ L 157, 30.4.2004, p. 87. 4 OJ L 157, 30.4.2004, p. 100.

4

Intermediate report Page printed16/7/2004

UPDATE SITUATION - EXCISE DUTY TABLES

++++++++++++++++++++++++++++++++++++++++++++++++

1 May 2004 New start +++++++++++++++++++++++++++++++++++++++++++++++++++ Year 2003 revenue figures received from: DE, NL, FI, ...♠….and … Some information is still to be received …♠...

5

Intermediate report May 2004 INDEX

INTRODUCTORY NOTE 2 IMPORTANT REMARQUE 3 UPDATE SITUATION 4 EUR exchange rate as of 1 OCTOBER 2003 6

ENERGY PRODUCTS AND ELECTRICITY 7

Petrol 8

Graph - Petrol 11

Gas Oil 12

Graphs �Gas Oil 16

Kerosene 21

Graph �Kerosene 24

Heavy fuel oil 25

Graphs � Heavy fuel oil 28

LPG 30

Graph � LPG 33

Natural Gas 34

Graphs � Natural Gas 37

Coal and Coke 40

Graphs � Coal and Coke 43

Electricity 45

Graphs � Electricity 48

National taxes 50

6

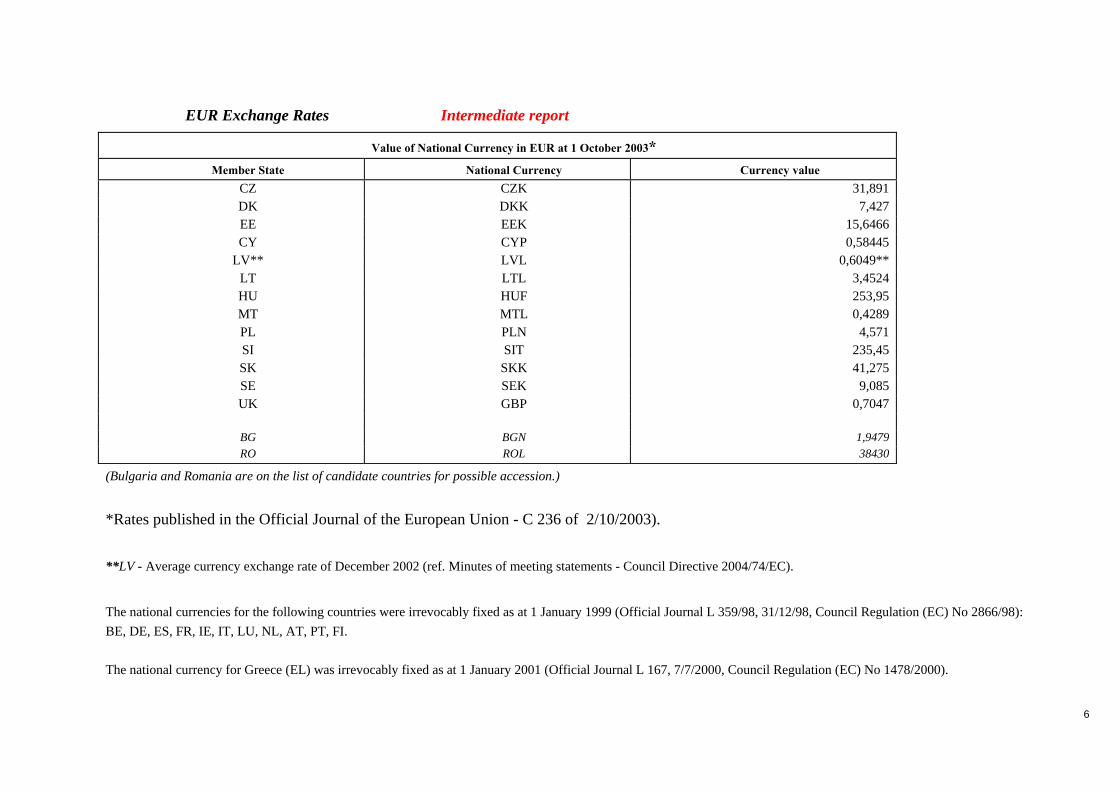

EUR Exchange Rates Intermediate report

Value of National Currency in EUR at 1 October 2003*

Member State National Currency Currency value CZ CZK 31,891 DK DKK 7,427 EE EEK 15,6466 CY CYP 0,58445

LV** LVL 0,6049** LT LTL 3,4524 HU HUF 253,95 MT MTL 0,4289 PL PLN 4,571 SI SIT 235,45 SK SKK 41,275 SE SEK 9,085 UK GBP 0,7047

BG BGN 1,9479 RO ROL 38430

(Bulgaria and Romania are on the list of candidate countries for possible accession.) *Rates published in the Official Journal of the European Union - C 236 of 2/10/2003).

**LV - Average currency exchange rate of December 2002 (ref. Minutes of meeting statements - Council Directive 2004/74/EC).

The national currencies for the following countries were irrevocably fixed as at 1 January 1999 (Official Journal L 359/98, 31/12/98, Council Regulation (EC) No 2866/98): BE, DE, ES, FR, IE, IT, LU, NL, AT, PT, FI. The national currency for Greece (EL) was irrevocably fixed as at 1 January 2001 (Official Journal L 167, 7/7/2000, Council Regulation (EC) No 1478/2000).

7

May 2004

ENERGY PRODUCTS AND ELECTRICITY

▼IMPORTANT AND GENERAL REMARK▼ " For further and complete details concerning the transitional periods and derogations from excise duty for each country and energy product, go through these links to consult the Council Directives 2003/96/EC, 2004/74/EC and 2004/75/EC (links " go to page 3).

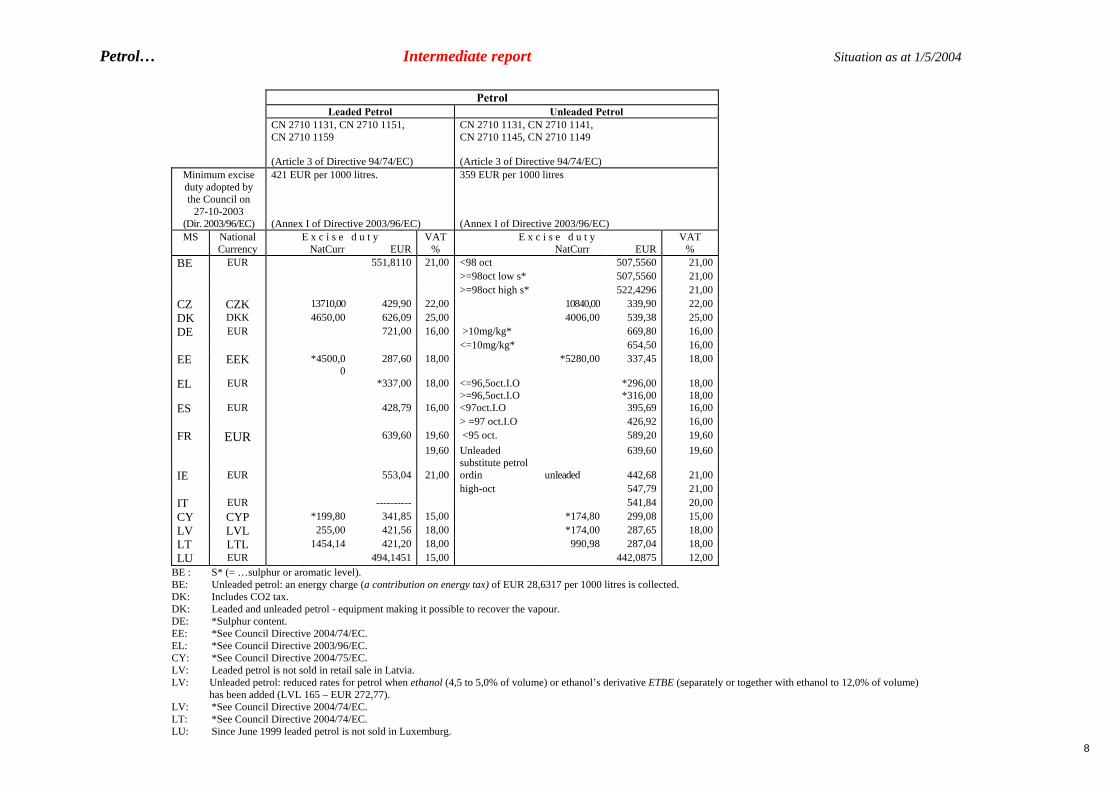

8

Petrol… Intermediate report Situation as at 1/5/2004 Petrol

Leaded Petrol Unleaded Petrol CN 2710 1131, CN 2710 1151,

CN 2710 1159 (Article 3 of Directive 94/74/EC)

CN 2710 1131, CN 2710 1141, CN 2710 1145, CN 2710 1149 (Article 3 of Directive 94/74/EC)

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EC)

421 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

359 EUR per 1000 litres (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

BE EUR 551,8110 21,00 <98 oct 507,5560 21,00 >=98oct low s* 507,5560 21,00 >=98oct high s* 522,4296 21,00CZ CZK 13710,00 429,90 22,00 10840,00 339,90 22,00DK DKK 4650,00 626,09 25,00 4006,00 539,38 25,00DE EUR 721,00 16,00 >10mg/kg* 669,80 16,00 <=10mg/kg* 654,50 16,00EE EEK *4500,0

0 287,60 18,00 *5280,00 337,45 18,00

EL EUR *337,00 18,00 <=96,5oct.I.O >=96,5oct.I.O

*296,00 *316,00

18,00 18,00

ES EUR 428,79 16,00 <97oct.I.O 395,69 16,00 > =97 oct.I.O 426,92 16,00FR EUR 639,60 19,60 <95 oct. 589,20 19,60 19,60 Unleaded

substitute petrol 639,60 19,60

IE EUR 553,04 21,00 ordin unleaded 442,68 21,00 high-oct 547,79 21,00IT EUR ---------- 541,84 20,00CY CYP *199,80 341,85 15,00 *174,80 299,08 15,00LV LVL 255,00 421,56 18,00 *174,00 287,65 18,00LT LTL 1454,14 421,20 18,00 990,98 287,04 18,00LU EUR 494,1451 15,00 442,0875 12,00

BE : S* (= …sulphur or aromatic level). BE: Unleaded petrol: an energy charge (a contribution on energy tax) of EUR 28,6317 per 1000 litres is collected. DK: Includes CO2 tax. DK: Leaded and unleaded petrol - equipment making it possible to recover the vapour. DE: *Sulphur content. EE: *See Council Directive 2004/74/EC. EL: *See Council Directive 2003/96/EC. CY: *See Council Directive 2004/75/EC. LV: Leaded petrol is not sold in retail sale in Latvia. LV: Unleaded petrol: reduced rates for petrol when ethanol (4,5 to 5,0% of volume) or ethanol’s derivative ETBE (separately or together with ethanol to 12,0% of volume)

has been added (LVL 165 – EUR 272,77). LV: *See Council Directive 2004/74/EC. LT: *See Council Directive 2004/74/EC. LU: Since June 1999 leaded petrol is not sold in Luxemburg.

9

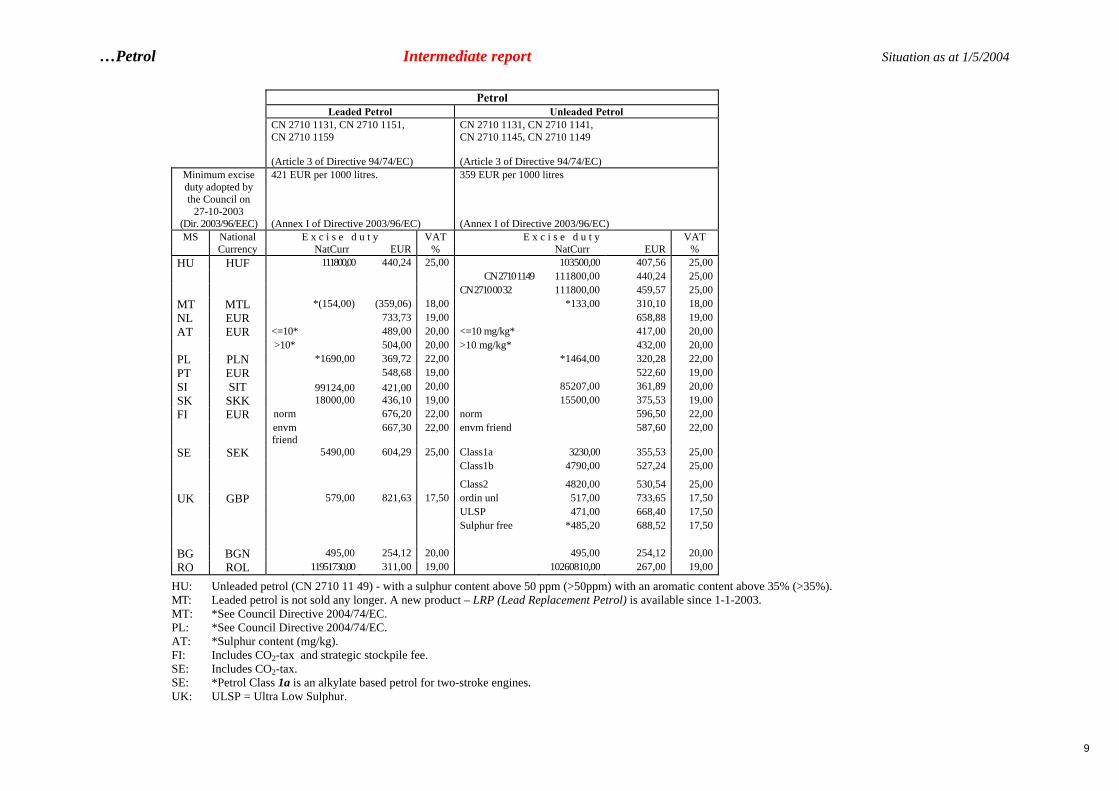

…Petrol Intermediate report Situation as at 1/5/2004 Petrol

Leaded Petrol Unleaded Petrol CN 2710 1131, CN 2710 1151,

CN 2710 1159 (Article 3 of Directive 94/74/EC)

CN 2710 1131, CN 2710 1141, CN 2710 1145, CN 2710 1149 (Article 3 of Directive 94/74/EC)

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

421 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

359 EUR per 1000 litres (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

HU HUF 111800,00 440,24 25,00 103500,00 407,56 25,00 CN 2710 1149 111800,00 440,24 25,00 CN 2710 00 32 111800,00 459,57 25,00MT MTL *(154,00) (359,06) 18,00 *133,00 310,10 18,00NL EUR 733,73 19,00 658,88 19,00AT EUR <=10* 489,00 20,00 <=10 mg/kg* 417,00 20,00 >10* 504,00 20,00 >10 mg/kg* 432,00 20,00PL PLN *1690,00 369,72 22,00 *1464,00 320,28 22,00PT EUR 548,68 19,00 522,60 19,00SI SIT 99124,00 421,00 20,00 85207,00 361,89 20,00SK SKK 18000,00 436,10 19,00 15500,00 375,53 19,00FI EUR norm 676,20 22,00 norm 596,50 22,00 envm

friend 667,30 22,00 envm friend 587,60 22,00

SE SEK 5490,00 604,29 25,00 Class1a 3230,00 355,53 25,00

Class1b 4790,00 527,24 25,00

Class2 4820,00 530,54 25,00UK GBP 579,00 821,63 17,50 ordin unl 517,00 733,65 17,50 ULSP 471,00 668,40 17,50 Sulphur free *485,20 688,52 17,50 BG BGN 495,00 254,12 20,00 495,00 254,12 20,00RO ROL 11951730,00 311,00 19,00 10260810,00 267,00 19,00

HU: Unleaded petrol (CN 2710 11 49) - with a sulphur content above 50 ppm (>50ppm) with an aromatic content above 35% (>35%). MT: Leaded petrol is not sold any longer. A new product – LRP (Lead Replacement Petrol) is available since 1-1-2003. MT: *See Council Directive 2004/74/EC. PL: *See Council Directive 2004/74/EC. AT: *Sulphur content (mg/kg). FI: Includes CO2-tax and strategic stockpile fee. SE: Includes CO2-tax. SE: *Petrol Class 1a is an alkylate based petrol for two-stroke engines. UK: ULSP = Ultra Low Sulphur.

10

Petrol...-Additional comments Intermediate report Situation as at 1/5/2004

▼IMPORTANT AND GENERAL REMARK▼ " For further and complete details concerning the transitional periods and derogations from excise duty for each country and energy product, go through these links to consult the Council Directives 2003/96/EC, 2004/74/EC and 2004/75/EC (links " go to page 3). UK: VAT rate of 17,5% - non domestic use. Domestic use for deliveries of less than 2300 litres - VAT rate of 5%. UK: Higher octane unleaded petrol (super unleaded or lead replacement petrol) – separate rate abolished in 2001. Duty is now charged on this fuel at the rate appropriate to

unleaded petrol or ULSP (ultra low sulphur petrol) dependent upon the sulphur and aromatics content of the fuel. Reduced rate of duty for sulphur-free petrol will be introduced on 1/9/2004.

UK: Fuel substitutes: Biodiesel used as road fuel. effective rate from 1/19/2003 – GBP 271 (EUR 384,56 per 1000 litres). Other fuel substitutes are taxed as ULSP when used as petrol and taxed as ULSD when used as diesel. until 1/9/2004 when other fuel substitutes will be taxed as sulphur-free petrol when used as petrol and taxed as sulphur-free diesel when used as diesel. New duty rate on bioethanol (GBP 271/1000 l (EUR 384,56)) will come into effect on 1/1/2005.

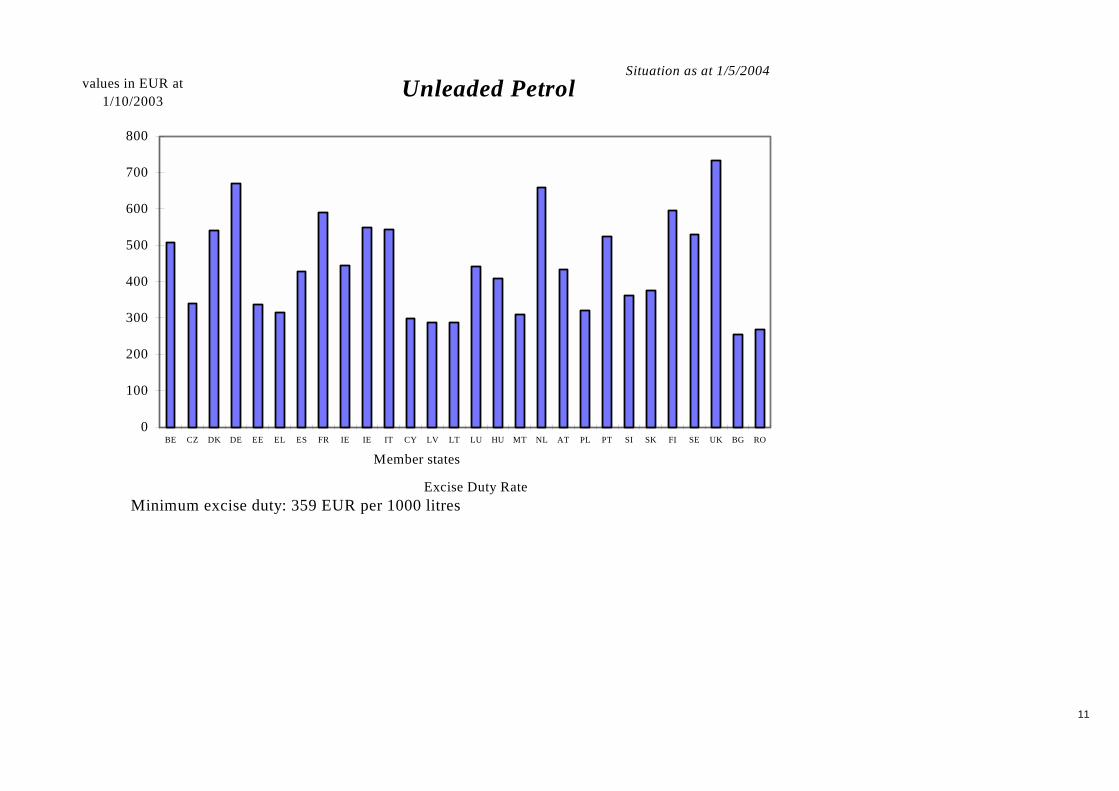

11

Situation as at 1/5/2004

0

100

200

300

400

500

600

700

800

BE CZ DK DE EE EL ES FR IE IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Unleaded Petrol

Minimum excise duty: 359 EUR per 1000 litresExcise Duty Rate

12

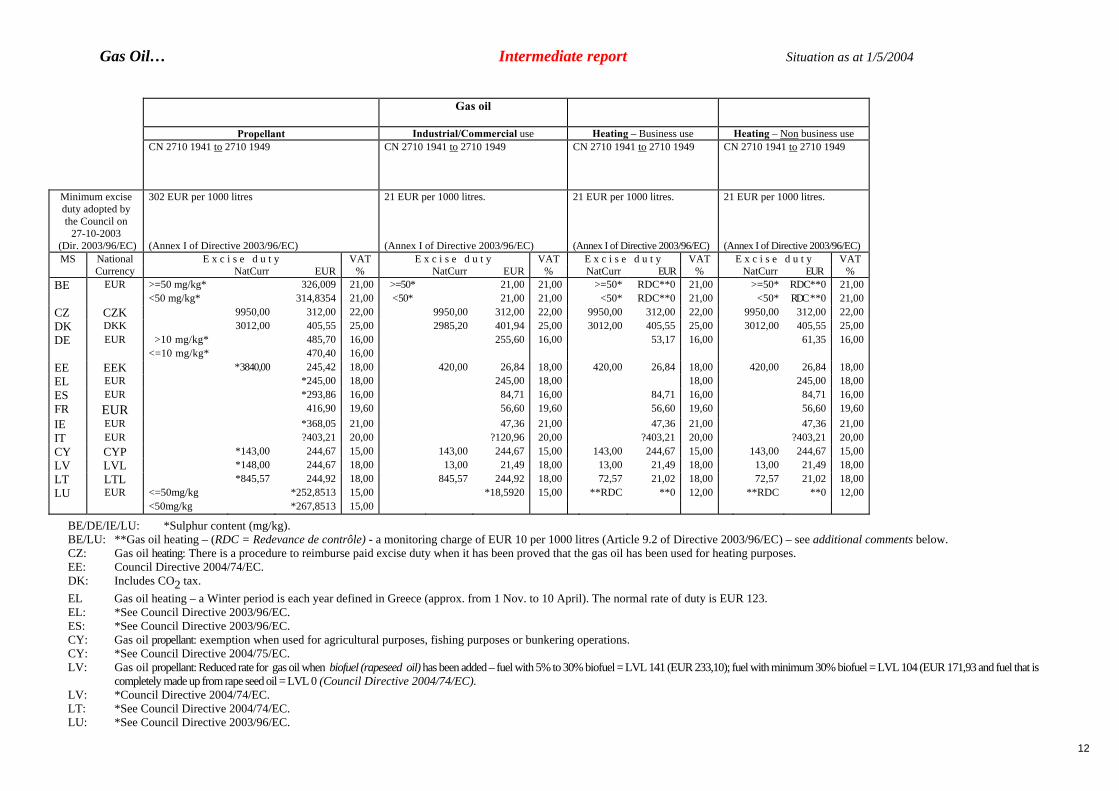

Gas Oil… Intermediate report Situation as at 1/5/2004

Gas oil

Propellant Industrial/Commercial use Heating � Business use Heating – Non business use CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EC)

302 EUR per 1000 litres (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR %

BE EUR >=50 mg/kg* 326,009 21,00 >=50* 21,00 21,00 >=50* RDC**0 21,00 >=50* RDC**0 21,00 <50 mg/kg* 314,8354 21,00 <50* 21,00 21,00 <50* RDC**0 21,00 <50* RDC **0 21,00CZ CZK 9950,00 312,00 22,00 9950,00 312,00 22,00 9950,00 312,00 22,00 9950,00 312,00 22,00DK DKK 3012,00 405,55 25,00 2985,20 401,94 25,00 3012,00 405,55 25,00 3012,00 405,55 25,00DE EUR >10 mg/kg* 485,70 16,00 255,60 16,00 53,17 16,00 61,35 16,00 <=10 mg/kg* 470,40 16,00 EE EEK *3840,00 245,42 18,00 420,00 26,84 18,00 420,00 26,84 18,00 420,00 26,84 18,00EL EUR *245,00 18,00 245,00 18,00 18,00 245,00 18,00ES EUR *293,86 16,00 84,71 16,00 84,71 16,00 84,71 16,00FR EUR 416,90 19,60 56,60 19,60 56,60 19,60 56,60 19,60IE EUR *368,05 21,00 47,36 21,00 47,36 21,00 47,36 21,00IT EUR ?403,21 20,00 ?120,96 20,00 ?403,21 20,00 ?403,21 20,00CY CYP *143,00 244,67 15,00 143,00 244,67 15,00 143,00 244,67 15,00 143,00 244,67 15,00LV LVL *148,00 244,67 18,00 13,00 21,49 18,00 13,00 21,49 18,00 13,00 21,49 18,00LT LTL *845,57 244,92 18,00 845,57 244,92 18,00 72,57 21,02 18,00 72,57 21,02 18,00LU EUR <=50mg/kg *252,8513 15,00 *18,5920 15,00 **RDC **0 12,00 **RDC **0 12,00 <50mg/kg *267,8513 15,00

BE/DE/IE/LU: *Sulphur content (mg/kg). BE/LU: **Gas oil heating – (RDC = Redevance de contrôle) - a monitoring charge of EUR 10 per 1000 litres (Article 9.2 of Directive 2003/96/EC) – see additional comments below. CZ: Gas oil heating: There is a procedure to reimburse paid excise duty when it has been proved that the gas oil has been used for heating purposes. EE: Council Directive 2004/74/EC. DK: Includes CO2 tax. EL Gas oil heating – a Winter period is each year defined in Greece (approx. from 1 Nov. to 10 April). The normal rate of duty is EUR 123. EL: *See Council Directive 2003/96/EC. ES: *See Council Directive 2003/96/EC. CY: Gas oil propellant: exemption when used for agricultural purposes, fishing purposes or bunkering operations. CY: *See Council Directive 2004/75/EC. LV: Gas oil propellant: Reduced rate for gas oil when biofuel (rapeseed oil) has been added – fuel with 5% to 30% biofuel = LVL 141 (EUR 233,10); fuel with minimum 30% biofuel = LVL 104 (EUR 171,93 and fuel that is

completely made up from rape seed oil = LVL 0 (Council Directive 2004/74/EC). LV: *Council Directive 2004/74/EC. LT: *See Council Directive 2004/74/EC. LU: *See Council Directive 2003/96/EC.

13

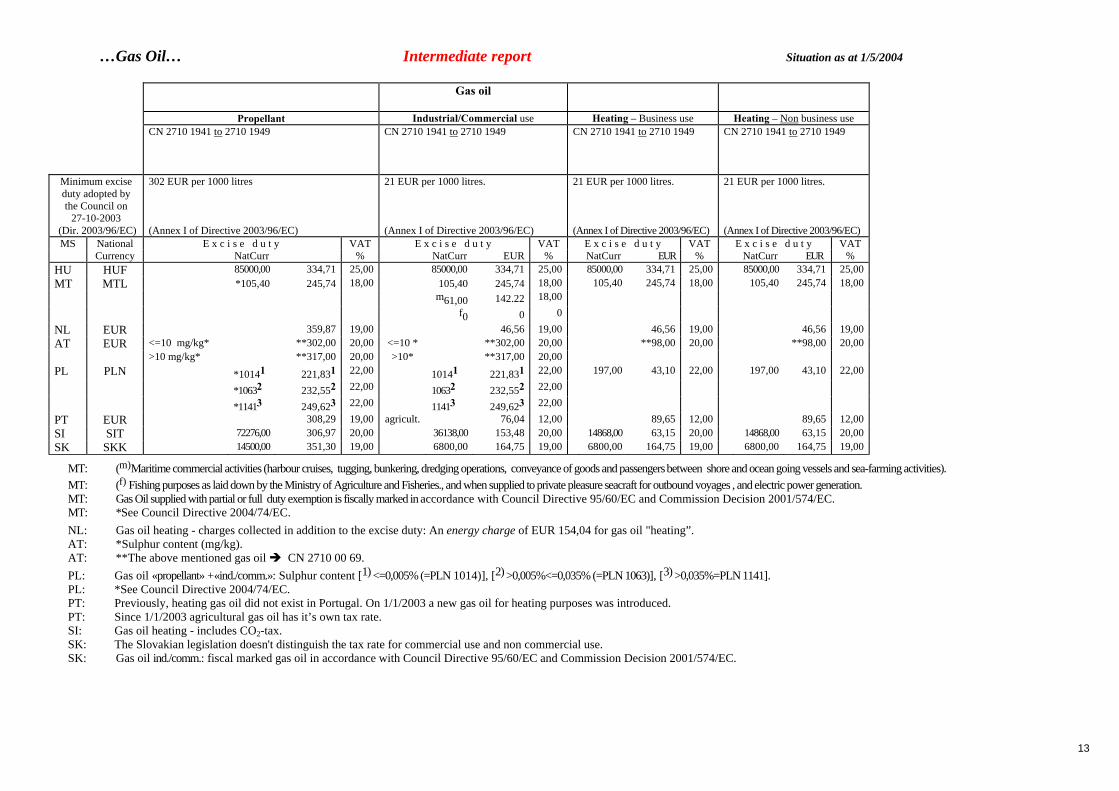

…Gas Oil… Intermediate report Situation as at 1/5/2004

Gas oil

Propellant Industrial/Commercial use Heating � Business use Heating – Non business use CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EC)

302 EUR per 1000 litres (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr % NatCurr EUR % NatCurr EUR % NatCurr EUR %

HU HUF 85000,00 334,71 25,00 85000,00 334,71 25,00 85000,00 334,71 25,00 85000,00 334,71 25,00MT MTL *105,40 245,74 18,00 105,40 245,74 18,00 105,40 245,74 18,00 105,40 245,74 18,00 m61,00 142.22 18,00 f0 0 0

NL EUR 359,87 19,00 46,56 19,00 46,56 19,00 46,56 19,00AT EUR <=10 mg/kg* **302,00 20,00 <=10 * **302,00 20,00 **98,00 20,00 **98,00 20,00 >10 mg/kg* **317,00 20,00 >10* **317,00 20,00 PL PLN *10141 221,831 22,00 10141 221,831 22,00 197,00 43,10 22,00 197,00 43,10 22,00 *10632 232,552 22,00 10632 232,552 22,00

*11413 249,623 22,00 11413 249,623 22,00 PT EUR 308,29 19,00 agricult. 76,04 12,00 89,65 12,00 89,65 12,00SI SIT 72276,00 306,97 20,00 36138,00 153,48 20,00 14868,00 63,15 20,00 14868,00 63,15 20,00SK SKK 14500,00 351,30 19,00 6800,00 164,75 19,00 6800,00 164,75 19,00 6800,00 164,75 19,00

MT: (m)Maritime commercial activities (harbour cruises, tugging, bunkering, dredging operations, conveyance of goods and passengers between shore and ocean going vessels and sea-farming activities). MT: (f) Fishing purposes as laid down by the Ministry of Agriculture and Fisheries., and when supplied to private pleasure seacraft for outbound voyages , and electric power generation. MT: Gas Oil supplied with partial or full duty exemption is fiscally marked in accordance with Council Directive 95/60/EC and Commission Decision 2001/574/EC. MT: *See Council Directive 2004/74/EC. NL: Gas oil heating - charges collected in addition to the excise duty: An energy charge of EUR 154,04 for gas oil "heating”. AT: *Sulphur content (mg/kg). AT: **The above mentioned gas oil " CN 2710 00 69. PL: Gas oil «propellant» +«ind./comm.»: Sulphur content [1) <=0,005% (=PLN 1014)], [2) >0,005%<=0,035% (=PLN 1063)], [3) >0,035%=PLN 1141]. PL: *See Council Directive 2004/74/EC. PT: Previously, heating gas oil did not exist in Portugal. On 1/1/2003 a new gas oil for heating purposes was introduced. PT: Since 1/1/2003 agricultural gas oil has it’s own tax rate. SI: Gas oil heating - includes CO2-tax. SK: The Slovakian legislation doesn't distinguish the tax rate for commercial use and non commercial use. SK: Gas oil ind./comm.: fiscal marked gas oil in accordance with Council Directive 95/60/EC and Commission Decision 2001/574/EC.

14

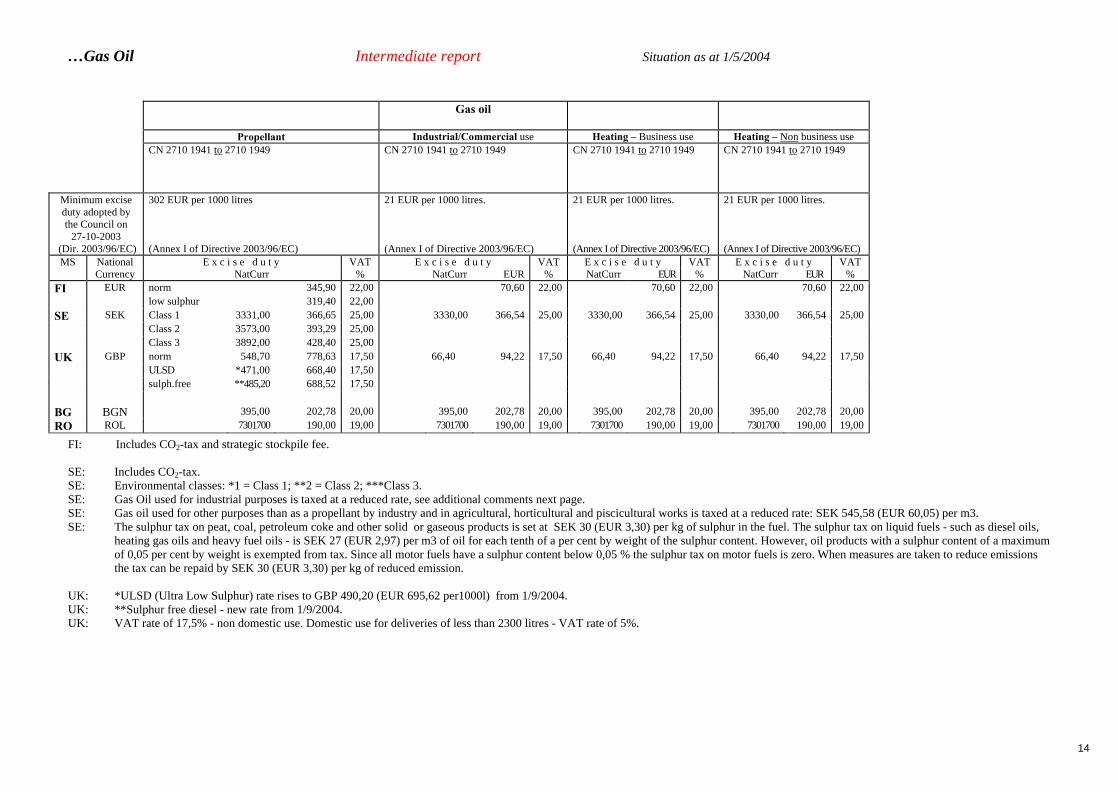

…Gas Oil Intermediate report Situation as at 1/5/2004

Gas oil

Propellant Industrial/Commercial use Heating � Business use Heating – Non business use CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

CN 2710 1941 to 2710 1949

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EC)

302 EUR per 1000 litres (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr % NatCurr EUR % NatCurr EUR % NatCurr EUR %

FI EUR norm 345,90 22,00 70,60 22,00 70,60 22,00 70,60 22,00 low sulphur 319,40 22,00 SE SEK Class 1 3331,00 366,65 25,00 3330,00 366,54 25,00 3330,00 366,54 25,00 3330,00 366,54 25,00 Class 2 3573,00 393,29 25,00 Class 3 3892,00 428,40 25,00 UK GBP norm 548,70 778,63 17,50 66,40 94,22 17,50 66,40 94,22 17,50 66,40 94,22 17,50 ULSD *471,00 668,40 17,50 sulph.free **485,20 688,52 17,50 BG BGN 395,00 202,78 20,00 395,00 202,78 20,00 395,00 202,78 20,00 395,00 202,78 20,00RO ROL 7301700 190,00 19,00 7301700 190,00 19,00 7301700 190,00 19,00 7301700 190,00 19,00

FI: Includes CO2-tax and strategic stockpile fee. SE: Includes CO2-tax. SE: Environmental classes: *1 = Class 1; **2 = Class 2; ***Class 3. SE: Gas Oil used for industrial purposes is taxed at a reduced rate, see additional comments next page. SE: Gas oil used for other purposes than as a propellant by industry and in agricultural, horticultural and piscicultural works is taxed at a reduced rate: SEK 545,58 (EUR 60,05) per m3. SE: The sulphur tax on peat, coal, petroleum coke and other solid or gaseous products is set at SEK 30 (EUR 3,30) per kg of sulphur in the fuel. The sulphur tax on liquid fuels - such as diesel oils,

heating gas oils and heavy fuel oils - is SEK 27 (EUR 2,97) per m3 of oil for each tenth of a per cent by weight of the sulphur content. However, oil products with a sulphur content of a maximum of 0,05 per cent by weight is exempted from tax. Since all motor fuels have a sulphur content below 0,05 % the sulphur tax on motor fuels is zero. When measures are taken to reduce emissions the tax can be repaid by SEK 30 (EUR 3,30) per kg of reduced emission.

UK: *ULSD (Ultra Low Sulphur) rate rises to GBP 490,20 (EUR 695,62 per1000l) from 1/9/2004. UK: **Sulphur free diesel - new rate from 1/9/2004. UK: VAT rate of 17,5% - non domestic use. Domestic use for deliveries of less than 2300 litres - VAT rate of 5%.

15

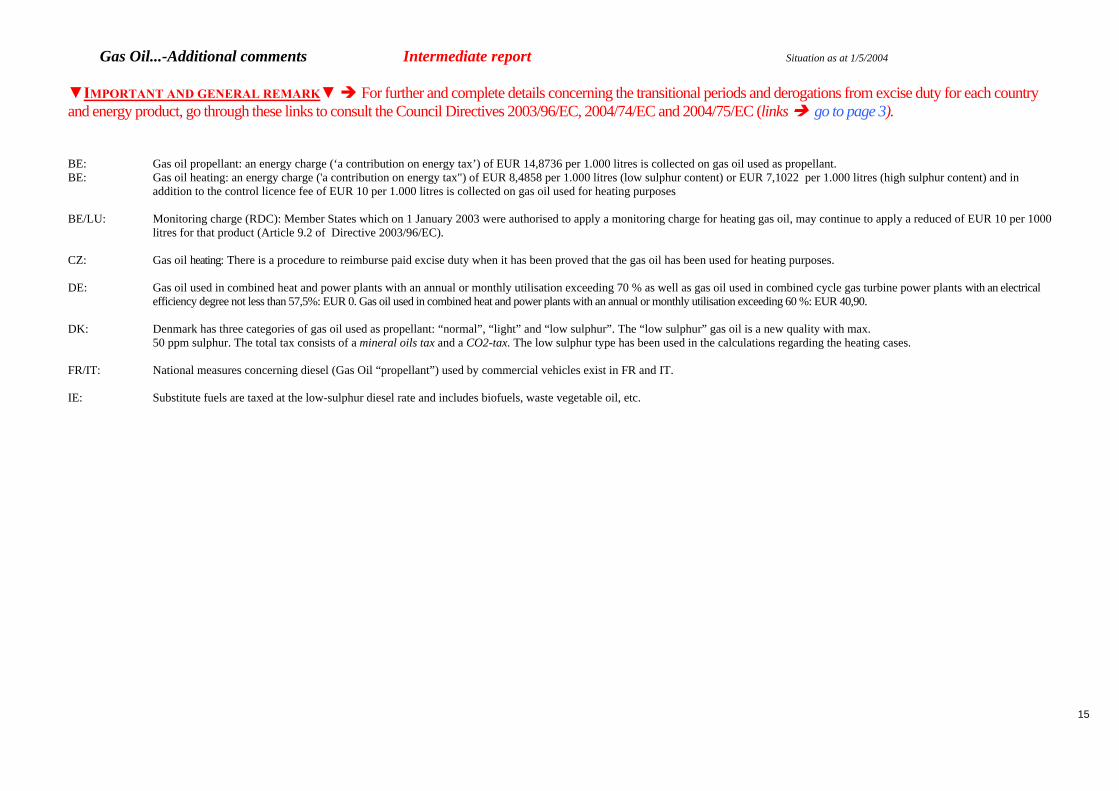

Gas Oil...-Additional comments Intermediate report Situation as at 1/5/2004 ▼IMPORTANT AND GENERAL REMARK▼ " For further and complete details concerning the transitional periods and derogations from excise duty for each country and energy product, go through these links to consult the Council Directives 2003/96/EC, 2004/74/EC and 2004/75/EC (links " go to page 3). BE: Gas oil propellant: an energy charge (‘a contribution on energy tax’) of EUR 14,8736 per 1.000 litres is collected on gas oil used as propellant. BE: Gas oil heating: an energy charge ('a contribution on energy tax") of EUR 8,4858 per 1.000 litres (low sulphur content) or EUR 7,1022 per 1.000 litres (high sulphur content) and in

addition to the control licence fee of EUR 10 per 1.000 litres is collected on gas oil used for heating purposes BE/LU: Monitoring charge (RDC): Member States which on 1 January 2003 were authorised to apply a monitoring charge for heating gas oil, may continue to apply a reduced of EUR 10 per 1000

litres for that product (Article 9.2 of Directive 2003/96/EC). CZ: Gas oil heating: There is a procedure to reimburse paid excise duty when it has been proved that the gas oil has been used for heating purposes. DE: Gas oil used in combined heat and power plants with an annual or monthly utilisation exceeding 70 % as well as gas oil used in combined cycle gas turbine power plants with an electrical

efficiency degree not less than 57,5%: EUR 0. Gas oil used in combined heat and power plants with an annual or monthly utilisation exceeding 60 %: EUR 40,90. DK: Denmark has three categories of gas oil used as propellant: “normal”, “light” and “low sulphur”. The “low sulphur” gas oil is a new quality with max.

50 ppm sulphur. The total tax consists of a mineral oils tax and a CO2-tax. The low sulphur type has been used in the calculations regarding the heating cases. FR/IT: National measures concerning diesel (Gas Oil “propellant”) used by commercial vehicles exist in FR and IT. IE: Substitute fuels are taxed at the low-sulphur diesel rate and includes biofuels, waste vegetable oil, etc.

16

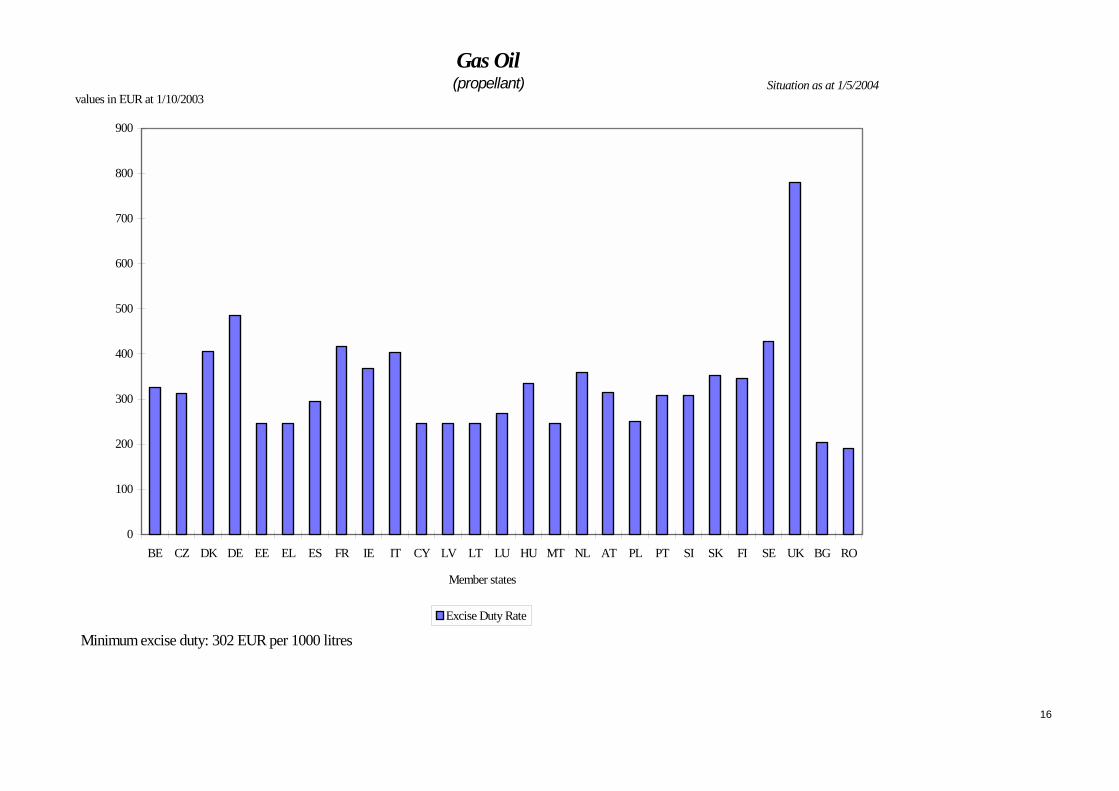

Situation as at 1/5/2004

0

100

200

300

400

500

600

700

800

900

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Gas Oil(propellant)

Minimum excise duty: 302 EUR per 1000 litres

17

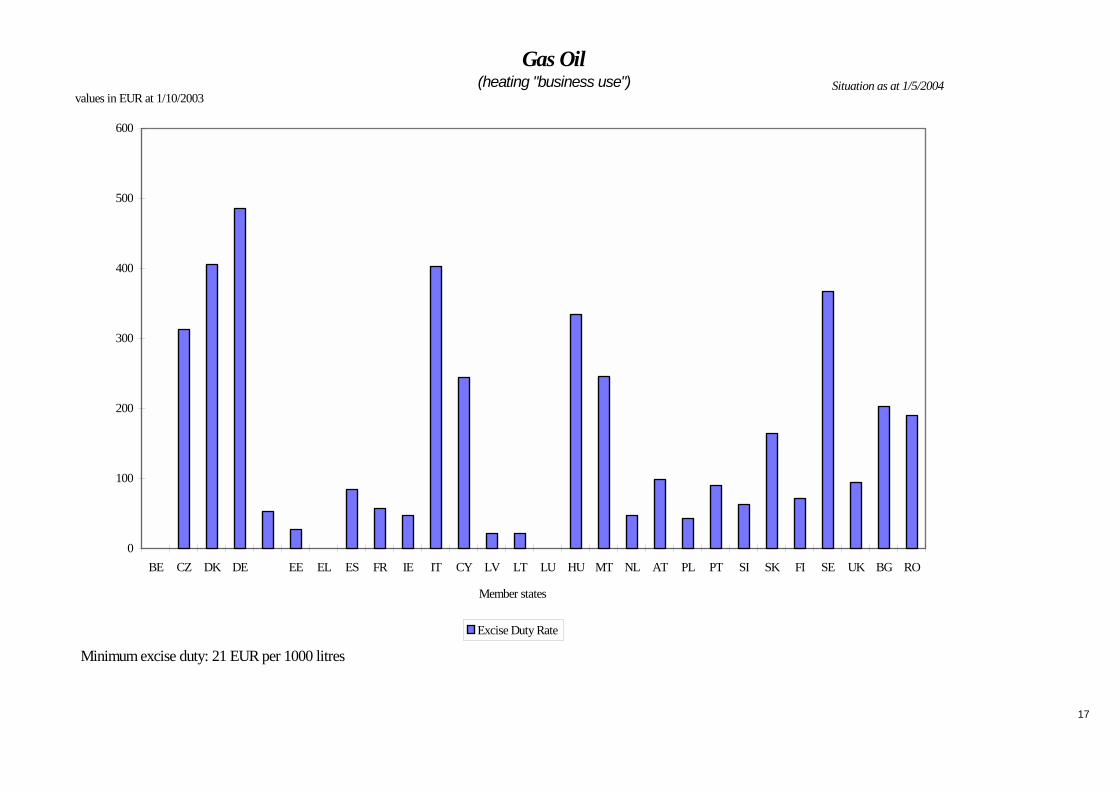

Situation as at 1/5/2004

0

100

200

300

400

500

600

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Gas Oil(heating "business use")

Minimum excise duty: 21 EUR per 1000 litres

18

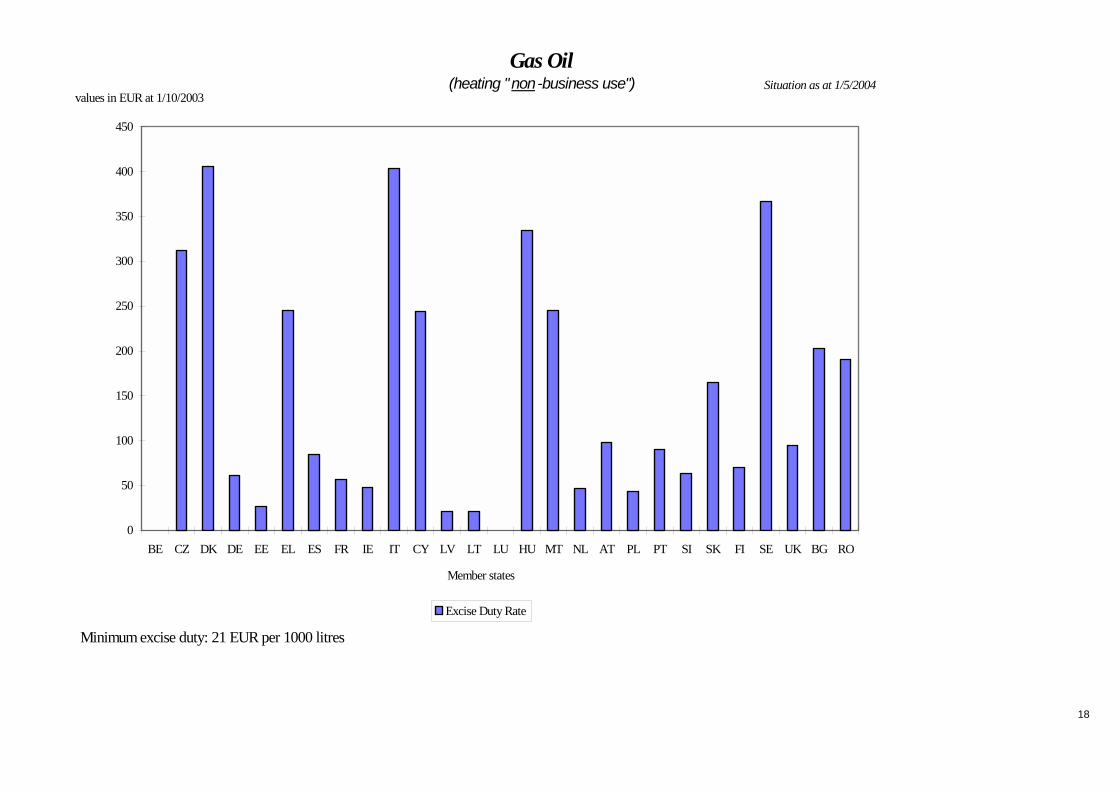

Situation as at 1/5/2004

0

50

100

150

200

250

300

350

400

450

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Gas Oil(heating "non-business use")

Minimum excise duty: 21 EUR per 1000 litres

19

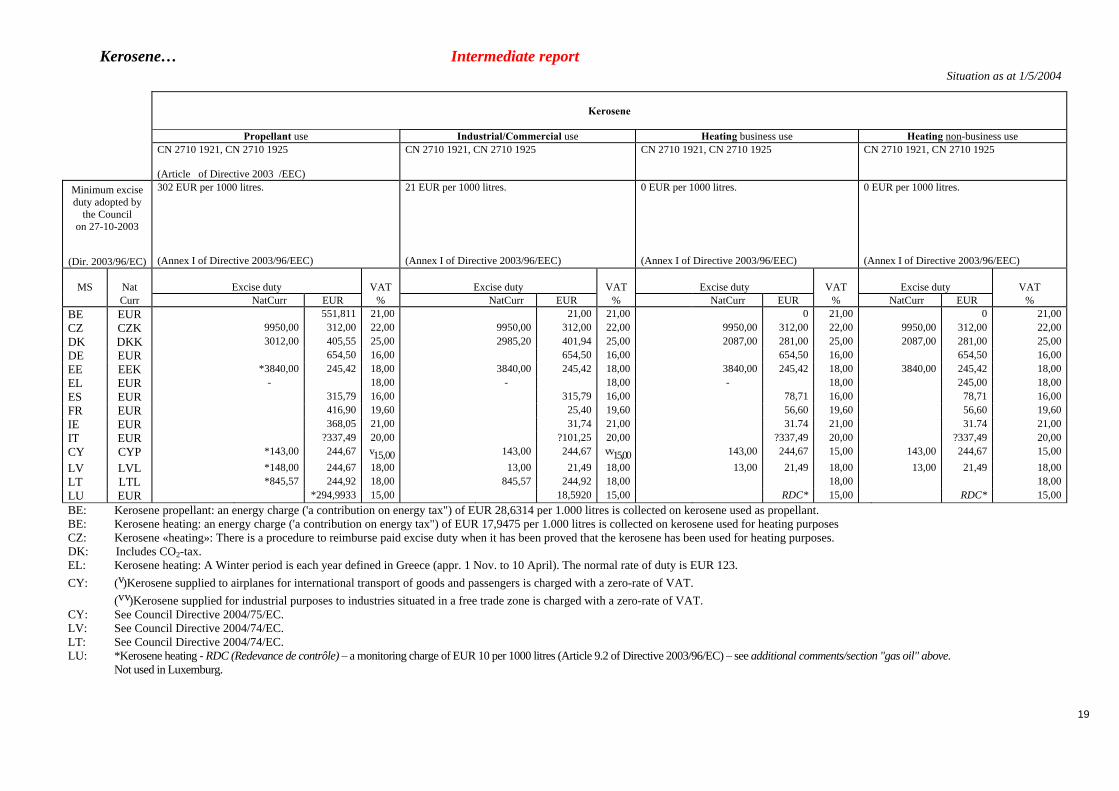

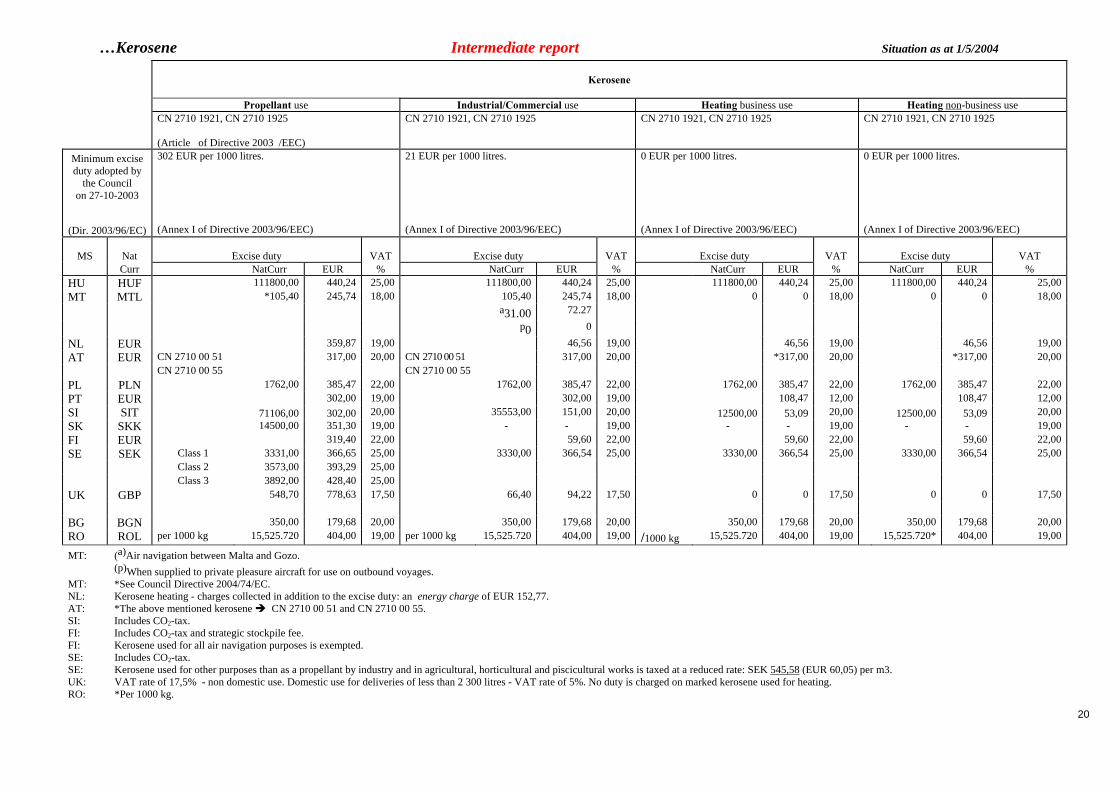

Kerosene… Intermediate report Situation as at 1/5/2004

Kerosene

Propellant use Industrial/Commercial use Heating business use Heating non-business use

CN 2710 1921, CN 2710 1925 (Article of Directive 2003 /EEC)

CN 2710 1921, CN 2710 1925 CN 2710 1921, CN 2710 1925 CN 2710 1921, CN 2710 1925

Minimum excise duty adopted by

the Council on 27-10-2003

(Dir. 2003/96/EC)

302 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

0 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

0 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

MS

Nat

Excise duty

VAT

Excise duty

VAT

Excise duty

VAT

Excise duty

VAT

Curr NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR % BE EUR 551,811 21,00 21,00 21,00 0 21,00 0 21,00 CZ CZK 9950,00 312,00 22,00 9950,00 312,00 22,00 9950,00 312,00 22,00 9950,00 312,00 22,00 DK DKK 3012,00 405,55 25,00 2985,20 401,94 25,00 2087,00 281,00 25,00 2087,00 281,00 25,00 DE EUR 654,50 16,00 654,50 16,00 654,50 16,00 654,50 16,00 EE EEK *3840,00 245,42 18,00 3840,00 245,42 18,00 3840,00 245,42 18,00 3840,00 245,42 18,00 EL EUR - 18,00 - 18,00 - 18,00 245,00 18,00 ES EUR 315,79 16,00 315,79 16,00 78,71 16,00 78,71 16,00 FR EUR 416,90 19,60 25,40 19,60 56,60 19,60 56,60 19,60 IE EUR 368,05 21,00 31,74 21,00 31.74 21,00 31.74 21,00 IT EUR ?337,49 20,00 ?101,25 20,00 ?337,49 20,00 ?337,49 20,00 CY CYP *143,00 244,67 v15,00 143,00 244,67 vv15,00 143,00 244,67 15,00 143,00 244,67 15,00

LV LVL *148,00 244,67 18,00 13,00 21,49 18,00 13,00 21,49 18,00 13,00 21,49 18,00 LT LTL *845,57 244,92 18,00 845,57 244,92 18,00 18,00 18,00 LU EUR *294,9933 15,00 18,5920 15,00 RDC* 15,00 RDC* 15,00 BE: Kerosene propellant: an energy charge ('a contribution on energy tax") of EUR 28,6314 per 1.000 litres is collected on kerosene used as propellant. BE: Kerosene heating: an energy charge ('a contribution on energy tax") of EUR 17,9475 per 1.000 litres is collected on kerosene used for heating purposes CZ: Kerosene «heating»: There is a procedure to reimburse paid excise duty when it has been proved that the kerosene has been used for heating purposes. DK: Includes CO2-tax. EL: Kerosene heating: A Winter period is each year defined in Greece (appr. 1 Nov. to 10 April). The normal rate of duty is EUR 123. CY: (v)Kerosene supplied to airplanes for international transport of goods and passengers is charged with a zero-rate of VAT.

(v v)Kerosene supplied for industrial purposes to industries situated in a free trade zone is charged with a zero-rate of VAT. CY: See Council Directive 2004/75/EC. LV: See Council Directive 2004/74/EC. LT: See Council Directive 2004/74/EC. LU: *Kerosene heating - RDC (Redevance de contrôle) – a monitoring charge of EUR 10 per 1000 litres (Article 9.2 of Directive 2003/96/EC) – see additional comments/section "gas oil" above.

Not used in Luxemburg.

20

…Kerosene Intermediate report Situation as at 1/5/2004

Kerosene

Propellant use Industrial/Commercial use Heating business use Heating non-business use CN 2710 1921, CN 2710 1925

(Article of Directive 2003 /EEC)

CN 2710 1921, CN 2710 1925 CN 2710 1921, CN 2710 1925 CN 2710 1921, CN 2710 1925

Minimum excise duty adopted by

the Council on 27-10-2003

(Dir. 2003/96/EC)

302 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

21 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

0 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

0 EUR per 1000 litres. (Annex I of Directive 2003/96/EEC)

MS

Nat

Excise duty

VAT

Excise duty

VAT

Excise duty

VAT

Excise duty

VAT

Curr NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR % HU HUF 111800,00 440,24 25,00 111800,00 440,24 25,00 111800,00 440,24 25,00 111800,00 440,24 25,00 MT MTL *105,40 245,74 18,00 105,40 245,74 18,00 0 0 18,00 0 0 18,00 a31.00 72.27

p0 0

NL EUR 359,87 19,00 46,56 19,00 46,56 19,00 46,56 19,00 AT EUR CN 2710 00 51 317,00 20,00 CN 2710 00 51 317,00 20,00 *317,00 20,00 *317,00 20,00 CN 2710 00 55 CN 2710 00 55 PL PLN 1762,00 385,47 22,00 1762,00 385,47 22,00 1762,00 385,47 22,00 1762,00 385,47 22,00 PT EUR 302,00 19,00 302,00 19,00 108,47 12,00 108,47 12,00 SI SIT 71106,00 302,00 20,00 35553,00 151,00 20,00 12500,00 53,09 20,00 12500,00 53,09 20,00 SK SKK 14500,00 351,30 19,00 - - 19,00 - - 19,00 - - 19,00 FI EUR 319,40 22,00 59,60 22,00 59,60 22,00 59,60 22,00 SE SEK Class 1 3331,00 366,65 25,00 3330,00 366,54 25,00 3330,00 366,54 25,00 3330,00 366,54 25,00 Class 2 3573,00 393,29 25,00 Class 3 3892,00 428,40 25,00 UK GBP 548,70 778,63 17,50 66,40 94,22 17,50 0 0 17,50 0 0 17,50 BG BGN 350,00 179,68 20,00 350,00 179,68 20,00 350,00 179,68 20,00 350,00 179,68 20,00 RO ROL per 1000 kg 15,525.720 404,00 19,00 per 1000 kg 15,525.720 404,00 19,00 /1000 kg 15,525.720 404,00 19,00 15,525.720* 404,00 19,00

MT: (a)Air navigation between Malta and Gozo. (p)When supplied to private pleasure aircraft for use on outbound voyages.

MT: *See Council Directive 2004/74/EC. NL: Kerosene heating - charges collected in addition to the excise duty: an energy charge of EUR 152,77. AT: *The above mentioned kerosene " CN 2710 00 51 and CN 2710 00 55. SI: Includes CO2-tax. FI: Includes CO2-tax and strategic stockpile fee. FI: Kerosene used for all air navigation purposes is exempted. SE: Includes CO2-tax. SE: Kerosene used for other purposes than as a propellant by industry and in agricultural, horticultural and piscicultural works is taxed at a reduced rate: SEK 545,58 (EUR 60,05) per m3. UK: VAT rate of 17,5% - non domestic use. Domestic use for deliveries of less than 2 300 litres - VAT rate of 5%. No duty is charged on marked kerosene used for heating. RO: *Per 1000 kg.

21

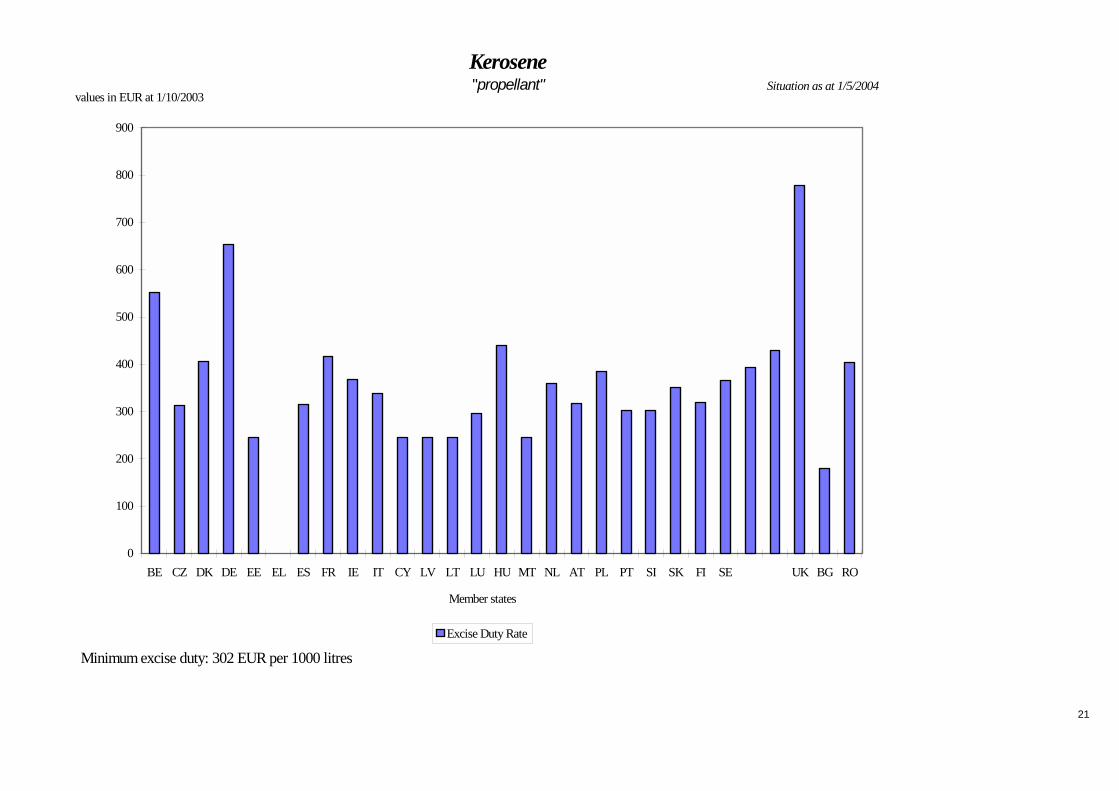

Situation as at 1/5/2004

0

100

200

300

400

500

600

700

800

900

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Kerosene "propellant"

Minimum excise duty: 302 EUR per 1000 litres

22

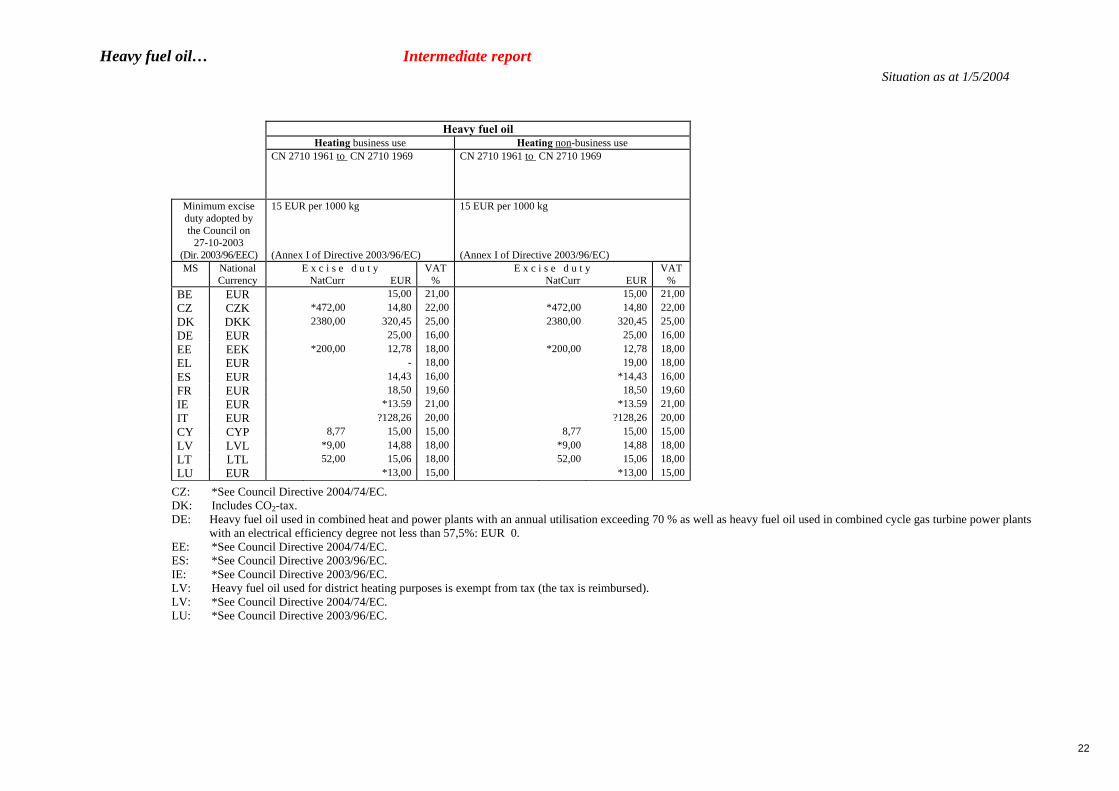

Heavy fuel oil… Intermediate report Situation as at 1/5/2004

Heavy fuel oil

Heating business use Heating non-business use CN 2710 1961 to CN 2710 1969

CN 2710 1961 to CN 2710 1969

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

15 EUR per 1000 kg (Annex I of Directive 2003/96/EC)

15 EUR per 1000 kg (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

BE EUR 15,00 21,00 15,00 21,00CZ CZK *472,00 14,80 22,00 *472,00 14,80 22,00DK DKK 2380,00 320,45 25,00 2380,00 320,45 25,00DE EUR 25,00 16,00 25,00 16,00EE EEK *200,00 12,78 18,00 *200,00 12,78 18,00EL EUR - 18,00 19,00 18,00ES EUR 14,43 16,00 *14,43 16,00FR EUR 18,50 19,60 18,50 19,60IE EUR *13.59 21,00 *13.59 21,00IT EUR ?128,26 20,00 ?128,26 20,00CY CYP 8,77 15,00 15,00 8,77 15,00 15,00LV LVL *9,00 14,88 18,00 *9,00 14,88 18,00LT LTL 52,00 15,06 18,00 52,00 15,06 18,00LU EUR *13,00 15,00 *13,00 15,00

CZ: *See Council Directive 2004/74/EC. DK: Includes CO2-tax. DE: Heavy fuel oil used in combined heat and power plants with an annual utilisation exceeding 70 % as well as heavy fuel oil used in combined cycle gas turbine power plants

with an electrical efficiency degree not less than 57,5%: EUR 0. EE: *See Council Directive 2004/74/EC. ES: *See Council Directive 2003/96/EC. IE: *See Council Directive 2003/96/EC. LV: Heavy fuel oil used for district heating purposes is exempt from tax (the tax is reimbursed). LV: *See Council Directive 2004/74/EC. LU: *See Council Directive 2003/96/EC.

23

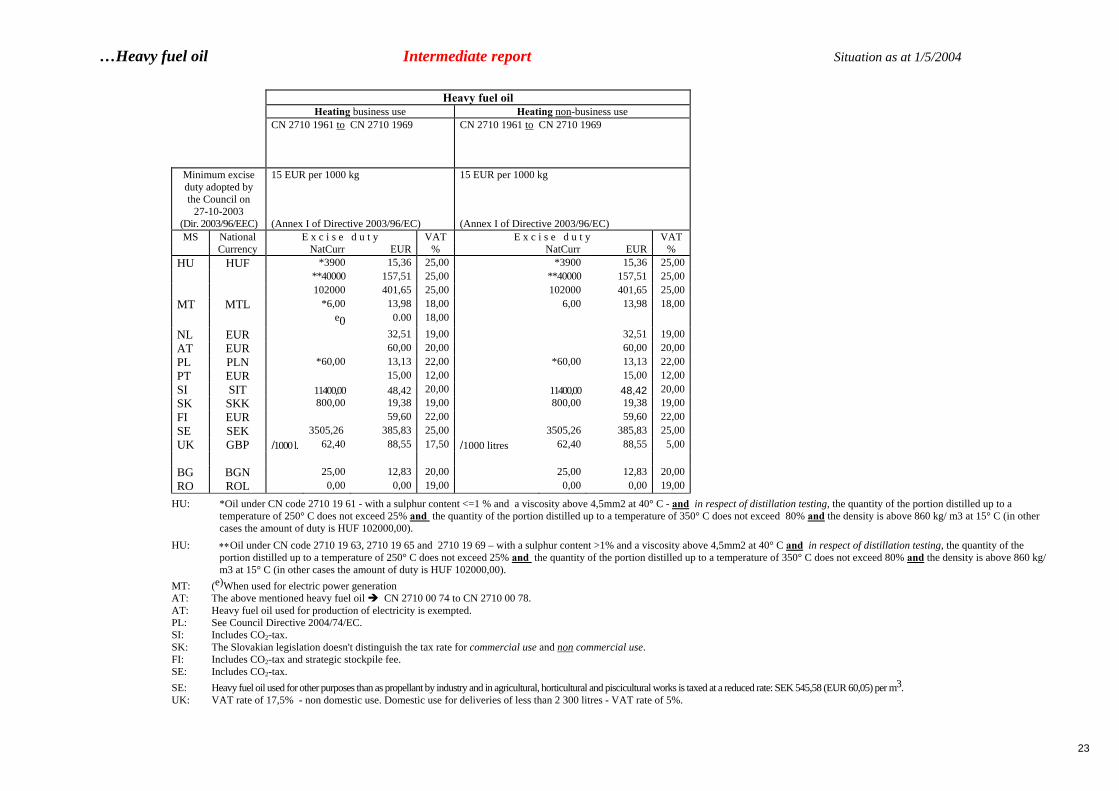

…Heavy fuel oil Intermediate report Situation as at 1/5/2004 Heavy fuel oil

Heating business use Heating non-business use CN 2710 1961 to CN 2710 1969

CN 2710 1961 to CN 2710 1969

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

15 EUR per 1000 kg (Annex I of Directive 2003/96/EC)

15 EUR per 1000 kg (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

HU HUF *3900 15,36 25,00 *3900 15,36 25,00 **40000 157,51 25,00 **40000 157,51 25,00 102000 401,65 25,00 102000 401,65 25,00MT MTL *6,00 13,98 18,00 6,00 13,98 18,00 e0 0.00 18,00

NL EUR 32,51 19,00 32,51 19,00AT EUR 60,00 20,00 60,00 20,00PL PLN *60,00 13,13 22,00 *60,00 13,13 22,00PT EUR 15,00 12,00 15,00 12,00SI SIT 11400,00 48,42 20,00 11400,00 48,42 20,00SK SKK 800,00 19,38 19,00 800,00 19,38 19,00FI EUR 59,60 22,00 59,60 22,00SE SEK 3505,26 385,83 25,00 3505,26 385,83 25,00UK GBP /1000 l. 62,40 88,55 17,50 /1000 litres 62,40 88,55 5,00 BG BGN 25,00 12,83 20,00 25,00 12,83 20,00RO ROL 0,00 0,00 19,00 0,00 0,00 19,00

HU: *Oil under CN code 2710 19 61 - with a sulphur content <=1 % and a viscosity above 4,5mm2 at 40° C - and in respect of distillation testing, the quantity of the portion distilled up to a temperature of 250° C does not exceed 25% and the quantity of the portion distilled up to a temperature of 350° C does not exceed 80% and the density is above 860 kg/ m3 at 15° C (in other cases the amount of duty is HUF 102000,00).

HU: ∗∗Oil under CN code 2710 19 63, 2710 19 65 and 2710 19 69 – with a sulphur content >1% and a viscosity above 4,5mm2 at 40° C and in respect of distillation testing, the quantity of the portion distilled up to a temperature of 250° C does not exceed 25% and the quantity of the portion distilled up to a temperature of 350° C does not exceed 80% and the density is above 860 kg/ m3 at 15° C (in other cases the amount of duty is HUF 102000,00).

MT: (e)When used for electric power generation AT: The above mentioned heavy fuel oil " CN 2710 00 74 to CN 2710 00 78. AT: Heavy fuel oil used for production of electricity is exempted. PL: See Council Directive 2004/74/EC. SI: Includes CO2-tax. SK: The Slovakian legislation doesn't distinguish the tax rate for commercial use and non commercial use. FI: Includes CO2-tax and strategic stockpile fee. SE: Includes CO2-tax. SE: Heavy fuel oil used for other purposes than as propellant by industry and in agricultural, horticultural and piscicultural works is taxed at a reduced rate: SEK 545,58 (EUR 60,05) per m3. UK: VAT rate of 17,5% - non domestic use. Domestic use for deliveries of less than 2 300 litres - VAT rate of 5%.

24

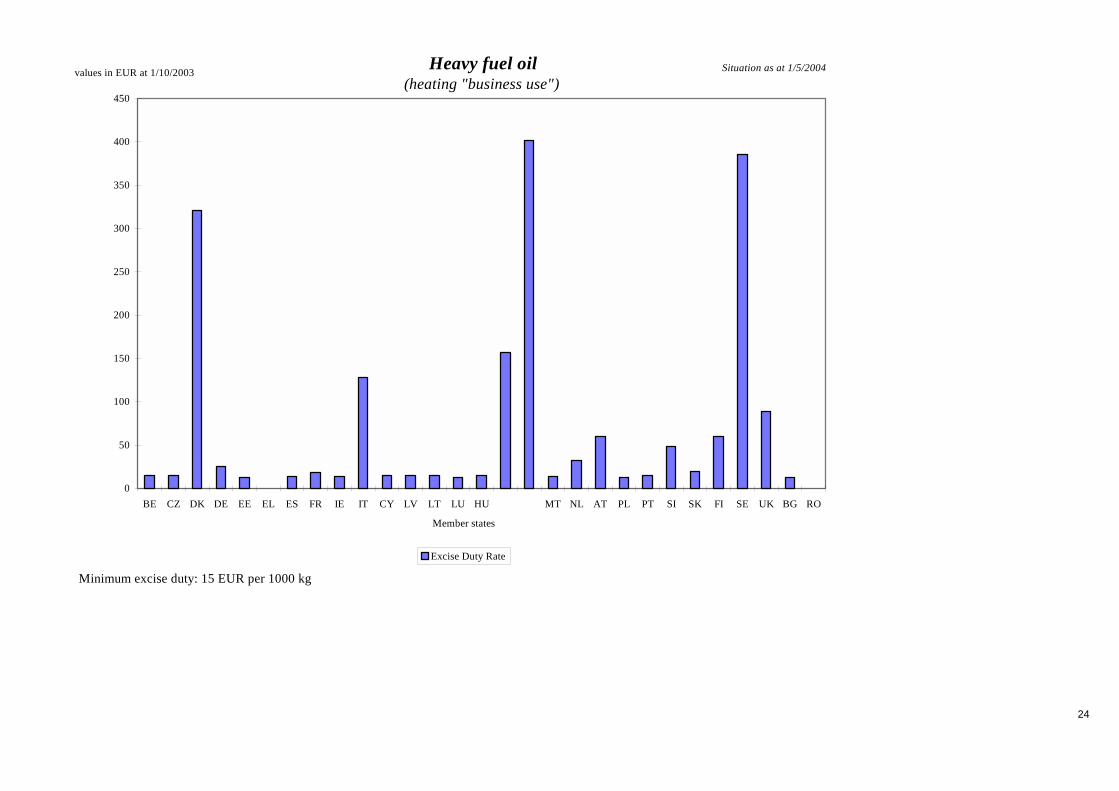

Situation as at 1/5/2004

0

50

100

150

200

250

300

350

400

450

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Heavy fuel oil (heating "business use")

Minimum excise duty: 15 EUR per 1000 kg

25

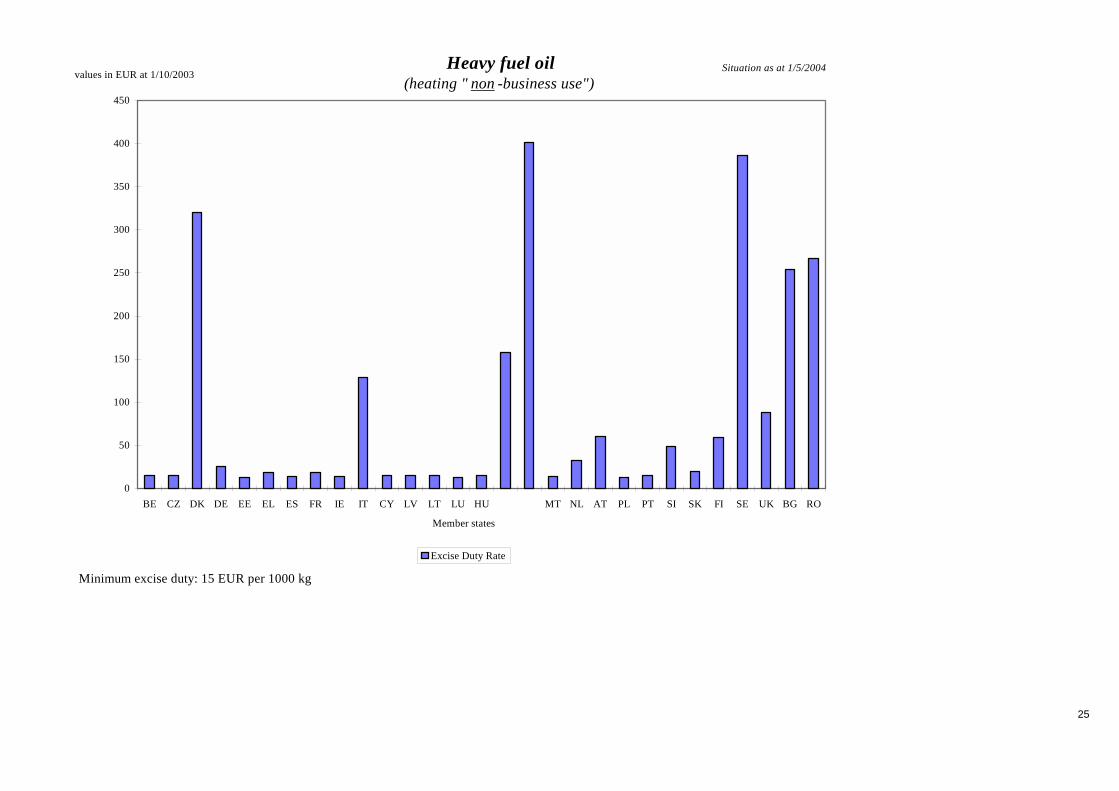

Situation as at 1/5/2004

0

50

100

150

200

250

300

350

400

450

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Heavy fuel oil (heating " non -business use")

Minimum excise duty: 15 EUR per 1000 kg

26

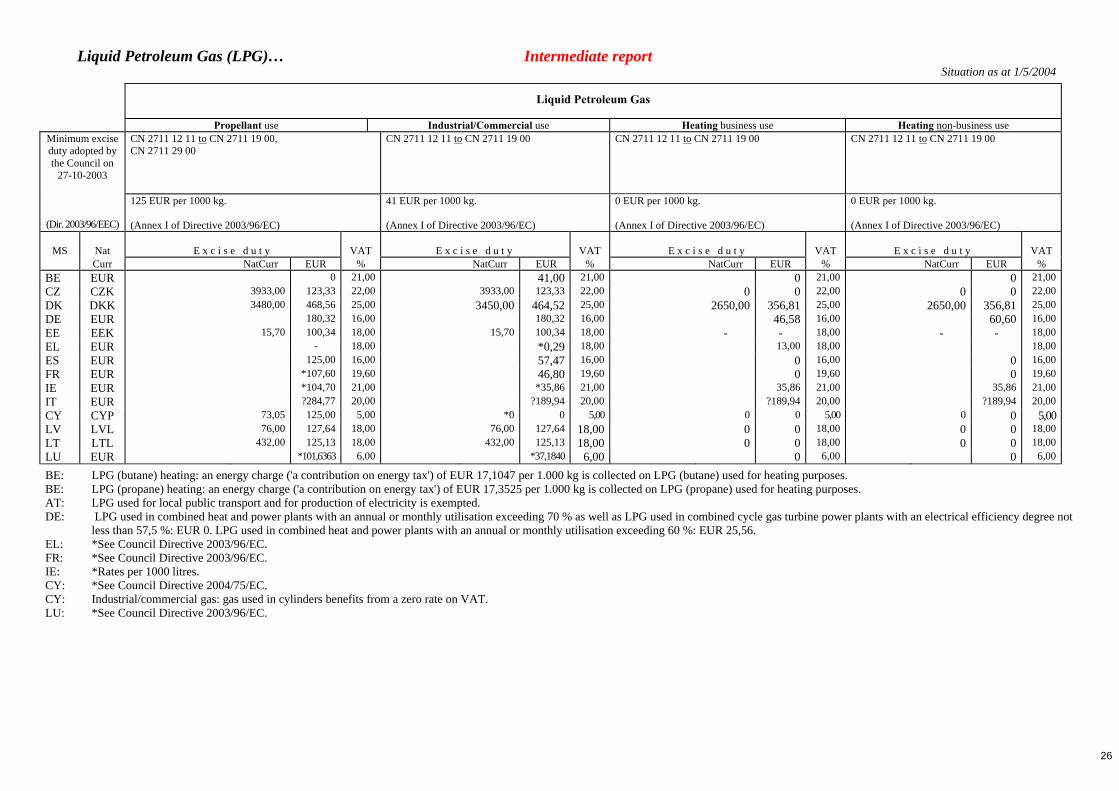

Liquid Petroleum Gas (LPG)… Intermediate report Situation as at 1/5/2004

Liquid Petroleum Gas

Propellant use Industrial/Commercial use Heating business use Heating non-business use CN 2711 12 11 to CN 2711 19 00, CN 2711 29 00

CN 2711 12 11 to CN 2711 19 00

CN 2711 12 11 to CN 2711 19 00

CN 2711 12 11 to CN 2711 19 00

Minimum excise duty adopted by the Council on

27-10-2003

(Dir. 2003/96/EEC)

125 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

41 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

0 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

0 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

MS

Nat

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

Curr NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR % BE EUR 0 21,00 41,00 21,00 0 21,00 0 21,00 CZ CZK 3933,00 123,33 22,00 3933,00 123,33 22,00 0 0 22,00 0 0 22,00 DK DKK 3480,00 468,56 25,00 3450,00 464,52 25,00 2650,00 356,81 25,00 2650,00 356,81 25,00 DE EUR 180,32 16,00 180,32 16,00 46,58 16,00 60,60 16,00 EE EEK 15,70 100,34 18,00 15,70 100,34 18,00 - - 18,00 - - 18,00 EL EUR - 18,00 *0,29 18,00 13,00 18,00 18,00 ES EUR 125,00 16,00 57,47 16,00 0 16,00 0 16,00 FR EUR *107,60 19,60 46,80 19,60 0 19,60 0 19,60 IE EUR *104,70 21,00 *35,86 21,00 35,86 21,00 35,86 21,00 IT EUR ?284,77 20,00 ?189,94 20,00 ?189,94 20,00 ?189,94 20,00 CY CYP 73,05 125,00 5,00 *0 0 5,00 0 0 5,00 0 0 5,00 LV LVL 76,00 127,64 18,00 76,00 127,64 18,00 0 0 18,00 0 0 18,00 LT LTL 432,00 125,13 18,00 432,00 125,13 18,00 0 0 18,00 0 0 18,00 LU EUR *101,6363 6,00 *37,1840 6,00 0 6,00 0 6,00

BE: LPG (butane) heating: an energy charge ('a contribution on energy tax') of EUR 17,1047 per 1.000 kg is collected on LPG (butane) used for heating purposes. BE: LPG (propane) heating: an energy charge ('a contribution on energy tax') of EUR 17,3525 per 1.000 kg is collected on LPG (propane) used for heating purposes. AT: LPG used for local public transport and for production of electricity is exempted. DE: LPG used in combined heat and power plants with an annual or monthly utilisation exceeding 70 % as well as LPG used in combined cycle gas turbine power plants with an electrical efficiency degree not

less than 57,5 %: EUR 0. LPG used in combined heat and power plants with an annual or monthly utilisation exceeding 60 %: EUR 25,56. EL: *See Council Directive 2003/96/EC. FR: *See Council Directive 2003/96/EC. IE: *Rates per 1000 litres. CY: *See Council Directive 2004/75/EC. CY: Industrial/commercial gas: gas used in cylinders benefits from a zero rate on VAT. LU: *See Council Directive 2003/96/EC.

27

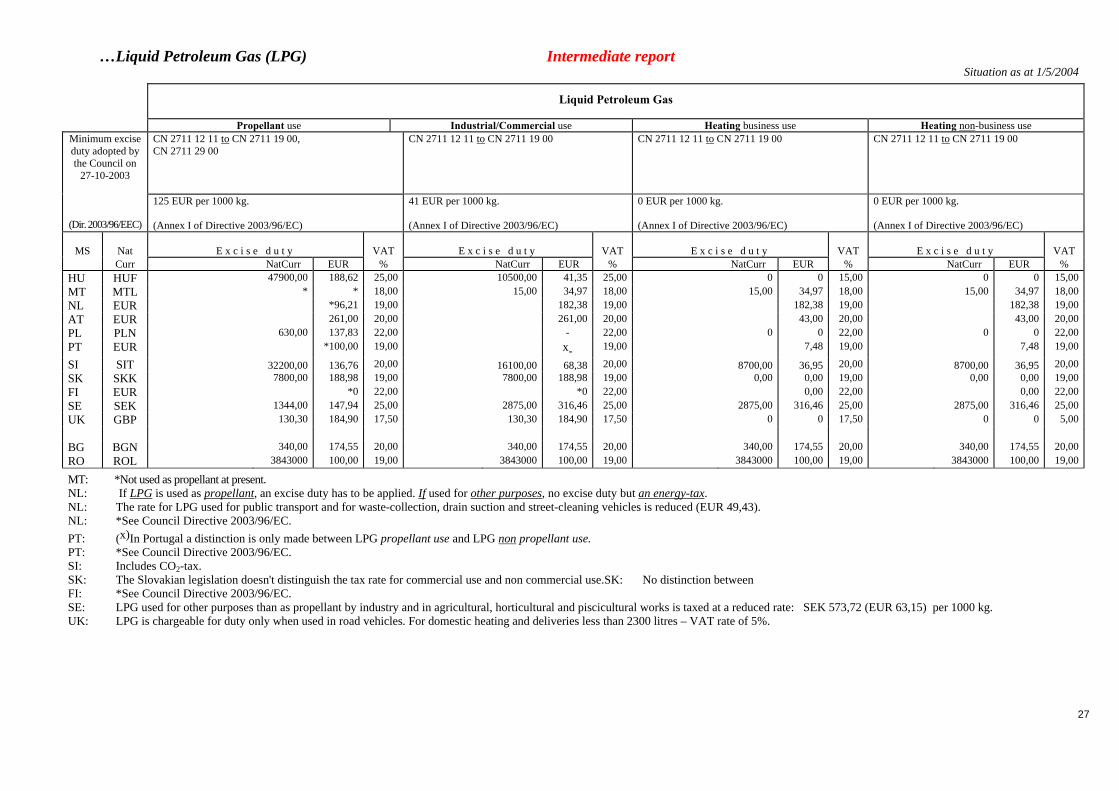

…Liquid Petroleum Gas (LPG) Intermediate report Situation as at 1/5/2004

Liquid Petroleum Gas

Propellant use Industrial/Commercial use Heating business use Heating non-business use CN 2711 12 11 to CN 2711 19 00, CN 2711 29 00

CN 2711 12 11 to CN 2711 19 00

CN 2711 12 11 to CN 2711 19 00

CN 2711 12 11 to CN 2711 19 00

Minimum excise duty adopted by the Council on

27-10-2003

(Dir. 2003/96/EEC)

125 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

41 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

0 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

0 EUR per 1000 kg. (Annex I of Directive 2003/96/EC)

MS

Nat

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

Curr NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR % HU HUF 47900,00 188,62 25,00 10500,00 41,35 25,00 0 0 15,00 0 0 15,00 MT MTL * * 18,00 15,00 34,97 18,00 15,00 34,97 18,00 15,00 34,97 18,00 NL EUR *96,21 19,00 182,38 19,00 182,38 19,00 182,38 19,00 AT EUR 261,00 20,00 261,00 20,00 43,00 20,00 43,00 20,00 PL PLN 630,00 137,83 22,00 - 22,00 0 0 22,00 0 0 22,00 PT EUR *100,00 19,00 x- 19,00 7,48 19,00 7,48 19,00

SI SIT 32200,00 136,76 20,00 16100,00 68,38 20,00 8700,00 36,95 20,00 8700,00 36,95 20,00 SK SKK 7800,00 188,98 19,00 7800,00 188,98 19,00 0,00 0,00 19,00 0,00 0,00 19,00 FI EUR *0 22,00 *0 22,00 0,00 22,00 0,00 22,00 SE SEK 1344,00 147,94 25,00 2875,00 316,46 25,00 2875,00 316,46 25,00 2875,00 316,46 25,00 UK GBP 130,30 184,90 17,50 130,30 184,90 17,50 0 0 17,50 0 0 5,00 BG BGN 340,00 174,55 20,00 340,00 174,55 20,00 340,00 174,55 20,00 340,00 174,55 20,00 RO ROL 3843000 100,00 19,00 3843000 100,00 19,00 3843000 100,00 19,00 3843000 100,00 19,00

MT: *Not used as propellant at present. NL: If LPG is used as propellant, an excise duty has to be applied. If used for other purposes, no excise duty but an energy-tax. NL: The rate for LPG used for public transport and for waste-collection, drain suction and street-cleaning vehicles is reduced (EUR 49,43). NL: *See Council Directive 2003/96/EC. PT: (x)In Portugal a distinction is only made between LPG propellant use and LPG non propellant use. PT: *See Council Directive 2003/96/EC. SI: Includes CO2-tax. SK: The Slovakian legislation doesn't distinguish the tax rate for commercial use and non commercial use.SK: No distinction between FI: *See Council Directive 2003/96/EC. SE: LPG used for other purposes than as propellant by industry and in agricultural, horticultural and piscicultural works is taxed at a reduced rate: SEK 573,72 (EUR 63,15) per 1000 kg. UK: LPG is chargeable for duty only when used in road vehicles. For domestic heating and deliveries less than 2300 litres – VAT rate of 5%.

28

Situation as at 1/5/2004

0

50

100

150

200

250

300

350

400

450

500

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

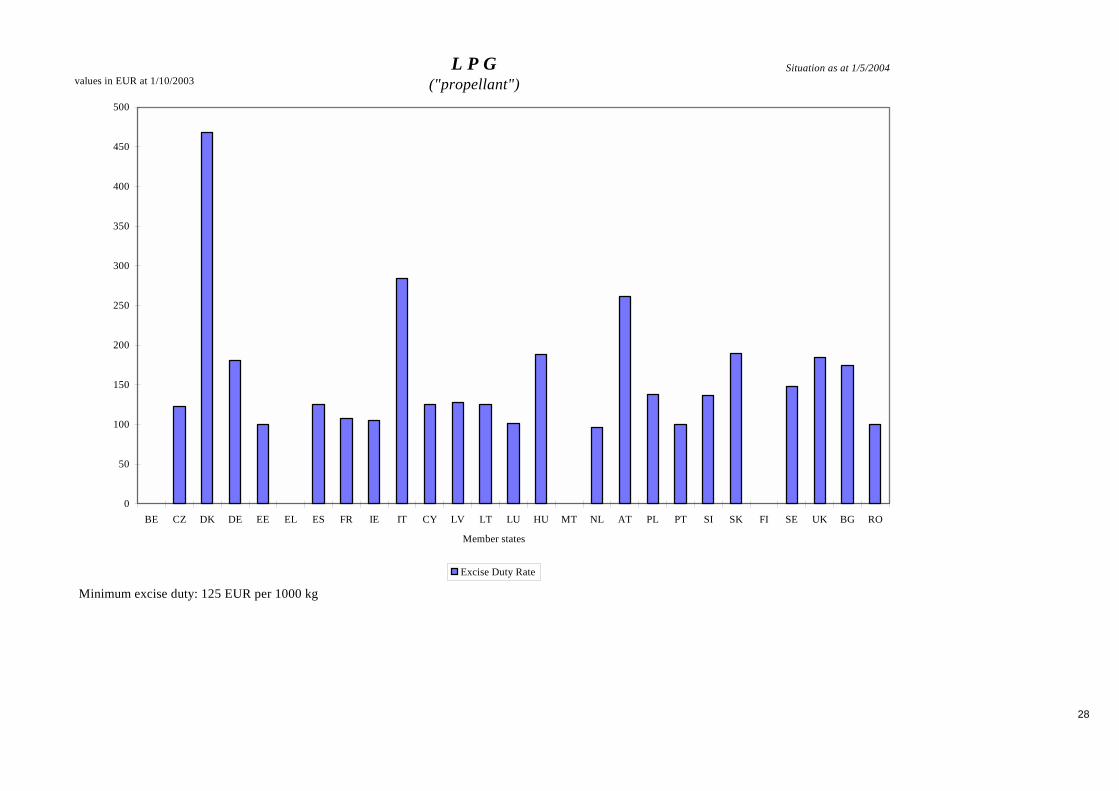

L P G ("propellant")

Minimum excise duty: 125 EUR per 1000 kg

29

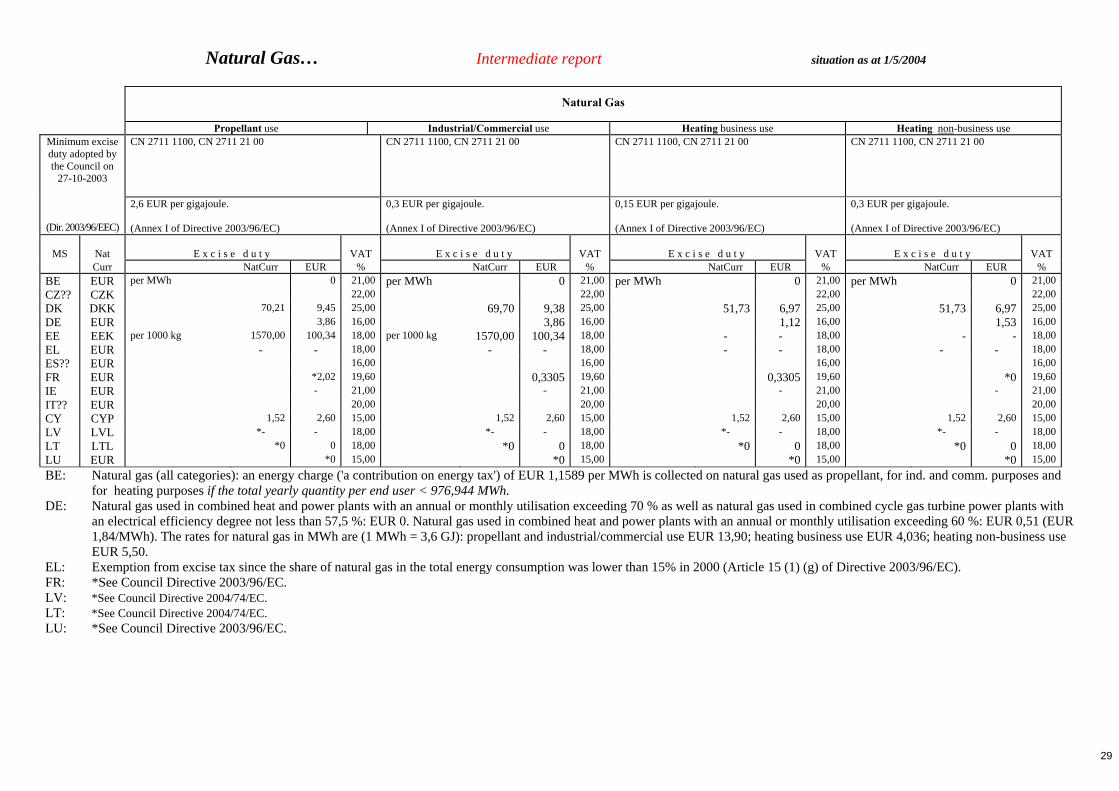

Natural Gas… Intermediate report situation as at 1/5/2004

Natural Gas

Propellant use Industrial/Commercial use Heating business use Heating non-business use CN 2711 1100, CN 2711 21 00

CN 2711 1100, CN 2711 21 00

CN 2711 1100, CN 2711 21 00

CN 2711 1100, CN 2711 21 00

Minimum excise duty adopted by the Council on

27-10-2003

(Dir. 2003/96/EEC)

2,6 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

0,3 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

0,15 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

0,3 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

MS

Nat

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

Curr NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR % BE EUR per MWh 0 21,00 per MWh 0 21,00 per MWh 0 21,00 per MWh 0 21,00 CZ?? CZK 22,00 22,00 22,00 22,00 DK DKK 70,21 9,45 25,00 69,70 9,38 25,00 51,73 6,97 25,00 51,73 6,97 25,00 DE EUR 3,86 16,00 3,86 16,00 1,12 16,00 1,53 16,00 EE EEK per 1000 kg 1570,00 100,34 18,00 per 1000 kg 1570,00 100,34 18,00 - - 18,00 - - 18,00 EL EUR - - 18,00 - - 18,00 - - 18,00 - - 18,00 ES?? EUR 16,00 16,00 16,00 16,00 FR EUR *2,02 19,60 0,3305 19,60 0,3305 19,60 *0 19,60 IE EUR - 21,00 - 21,00 - 21,00 - 21,00 IT?? EUR 20,00 20,00 20,00 20,00 CY CYP 1,52 2,60 15,00 1,52 2,60 15,00 1,52 2,60 15,00 1,52 2,60 15,00 LV LVL *- - 18,00 *- - 18,00 *- - 18,00 *- - 18,00 LT LTL *0 0 18,00 *0 0 18,00 *0 0 18,00 *0 0 18,00 LU EUR *0 15,00 *0 15,00 *0 15,00 *0 15,00 BE: Natural gas (all categories): an energy charge ('a contribution on energy tax') of EUR 1,1589 per MWh is collected on natural gas used as propellant, for ind. and comm. purposes and

for heating purposes if the total yearly quantity per end user < 976,944 MWh. DE: Natural gas used in combined heat and power plants with an annual or monthly utilisation exceeding 70 % as well as natural gas used in combined cycle gas turbine power plants with

an electrical efficiency degree not less than 57,5 %: EUR 0. Natural gas used in combined heat and power plants with an annual or monthly utilisation exceeding 60 %: EUR 0,51 (EUR 1,84/MWh). The rates for natural gas in MWh are (1 MWh = 3,6 GJ): propellant and industrial/commercial use EUR 13,90; heating business use EUR 4,036; heating non-business use EUR 5,50.

EL: Exemption from excise tax since the share of natural gas in the total energy consumption was lower than 15% in 2000 (Article 15 (1) (g) of Directive 2003/96/EC). FR: *See Council Directive 2003/96/EC. LV: *See Council Directive 2004/74/EC. LT: *See Council Directive 2004/74/EC. LU: *See Council Directive 2003/96/EC.

30

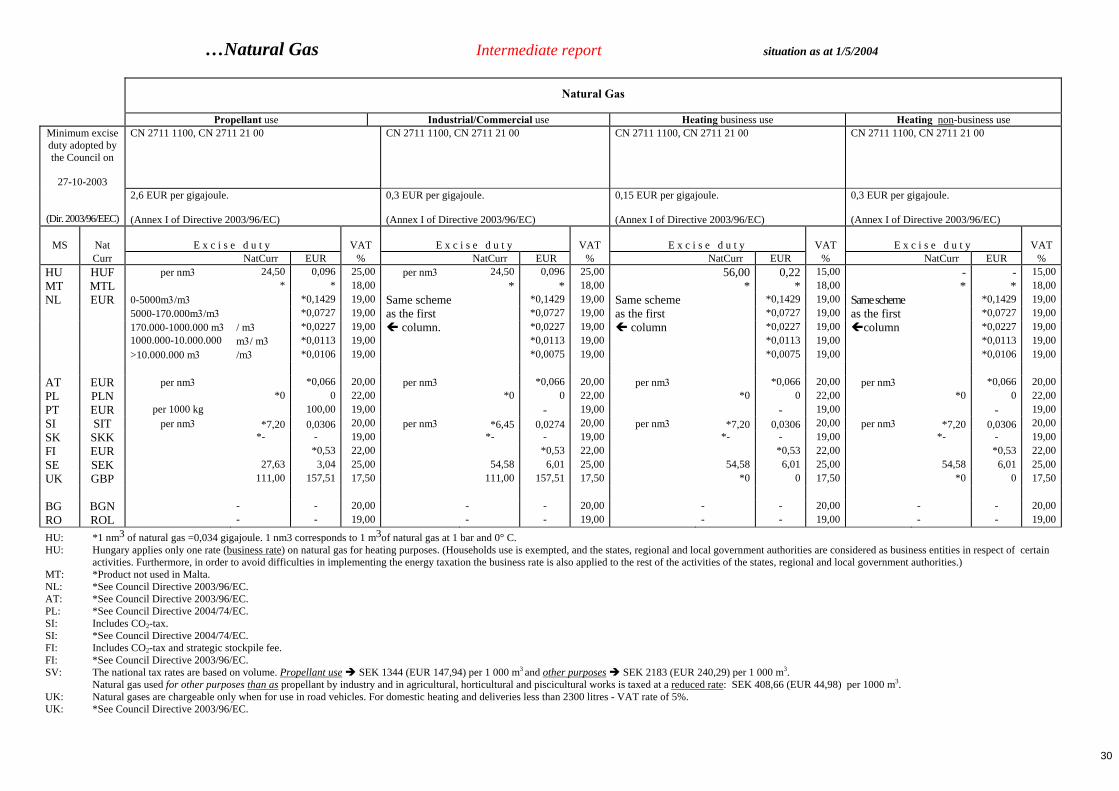

…Natural Gas Intermediate report situation as at 1/5/2004

Natural Gas

Propellant use Industrial/Commercial use Heating business use Heating non-business use CN 2711 1100, CN 2711 21 00

CN 2711 1100, CN 2711 21 00

CN 2711 1100, CN 2711 21 00

CN 2711 1100, CN 2711 21 00

Minimum excise duty adopted by the Council on

27-10-2003

(Dir. 2003/96/EEC)

2,6 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

0,3 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

0,15 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

0,3 EUR per gigajoule. (Annex I of Directive 2003/96/EC)

MS

Nat

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

E x c i s e d u t y

VAT

Curr NatCurr EUR % NatCurr EUR % NatCurr EUR % NatCurr EUR % HU HUF per nm3 24,50 0,096 25,00 per nm3 24,50 0,096 25,00 56,00 0,22 15,00 - - 15,00 MT MTL * * 18,00 * * 18,00 * * 18,00 * * 18,00 NL EUR 0-5000m3/m3 *0,1429 19,00 Same scheme *0,1429 19,00 Same scheme *0,1429 19,00 Same scheme *0,1429 19,00 5000-170.000m3/m3 *0,0727 19,00 as the first *0,0727 19,00 as the first *0,0727 19,00 as the first *0,0727 19,00 170.000-1000.000 m3 / m3 *0,0227 19,00 # column. *0,0227 19,00 # column *0,0227 19,00 #column *0,0227 19,00 1000.000-10.000.000 m3/ m3 *0,0113 19,00 *0,0113 19,00 *0,0113 19,00 *0,0113 19,00 >10.000.000 m3 /m3 *0,0106 19,00 *0,0075 19,00 *0,0075 19,00 *0,0106 19,00 AT EUR per nm3 *0,066 20,00 per nm3 *0,066 20,00 per nm3 *0,066 20,00 per nm3 *0,066 20,00 PL PLN *0 0 22,00 *0 0 22,00 *0 0 22,00 *0 0 22,00 PT EUR per 1000 kg 100,00 19,00 - 19,00 - 19,00 - 19,00 SI SIT per nm3 *7,20 0,0306 20,00 per nm3 *6,45 0,0274 20,00 per nm3 *7,20 0,0306 20,00 per nm3 *7,20 0,0306 20,00 SK SKK *- - 19,00 *- - 19,00 *- - 19,00 *- - 19,00 FI EUR *0,53 22,00 *0,53 22,00 *0,53 22,00 *0,53 22,00 SE SEK 27,63 3,04 25,00 54,58 6,01 25,00 54,58 6,01 25,00 54,58 6,01 25,00 UK GBP 111,00 157,51 17,50 111,00 157,51 17,50 *0 0 17,50 *0 0 17,50 BG BGN - - 20,00 - - 20,00 - - 20,00 - - 20,00 RO ROL - - 19,00 - - 19,00 - - 19,00 - - 19,00

HU: *1 nm3 of natural gas =0,034 gigajoule. 1 nm3 corresponds to 1 m3of natural gas at 1 bar and 0° C. HU: Hungary applies only one rate (business rate) on natural gas for heating purposes. (Households use is exempted, and the states, regional and local government authorities are considered as business entities in respect of certain

activities. Furthermore, in order to avoid difficulties in implementing the energy taxation the business rate is also applied to the rest of the activities of the states, regional and local government authorities.) MT: *Product not used in Malta. NL: *See Council Directive 2003/96/EC. AT: *See Council Directive 2003/96/EC. PL: *See Council Directive 2004/74/EC. SI: Includes CO2-tax. SI: *See Council Directive 2004/74/EC. FI: Includes CO2-tax and strategic stockpile fee. FI: *See Council Directive 2003/96/EC. SV: The national tax rates are based on volume. Propellant use " SEK 1344 (EUR 147,94) per 1 000 m3 and other purposes " SEK 2183 (EUR 240,29) per 1 000 m3.

Natural gas used for other purposes than as propellant by industry and in agricultural, horticultural and piscicultural works is taxed at a reduced rate: SEK 408,66 (EUR 44,98) per 1000 m3. UK: Natural gases are chargeable only when for use in road vehicles. For domestic heating and deliveries less than 2300 litres - VAT rate of 5%. UK: *See Council Directive 2003/96/EC.

31

Situation as at 1/5/2004

0

1

2

3

4

5

6

7

8

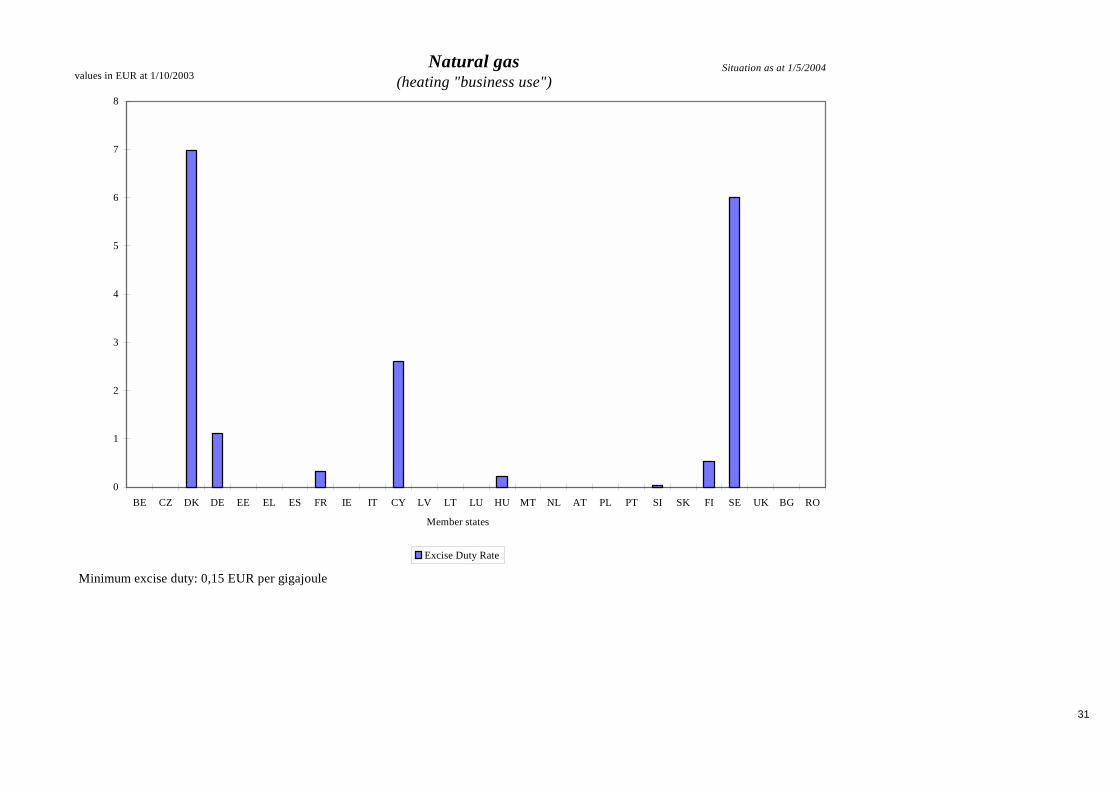

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

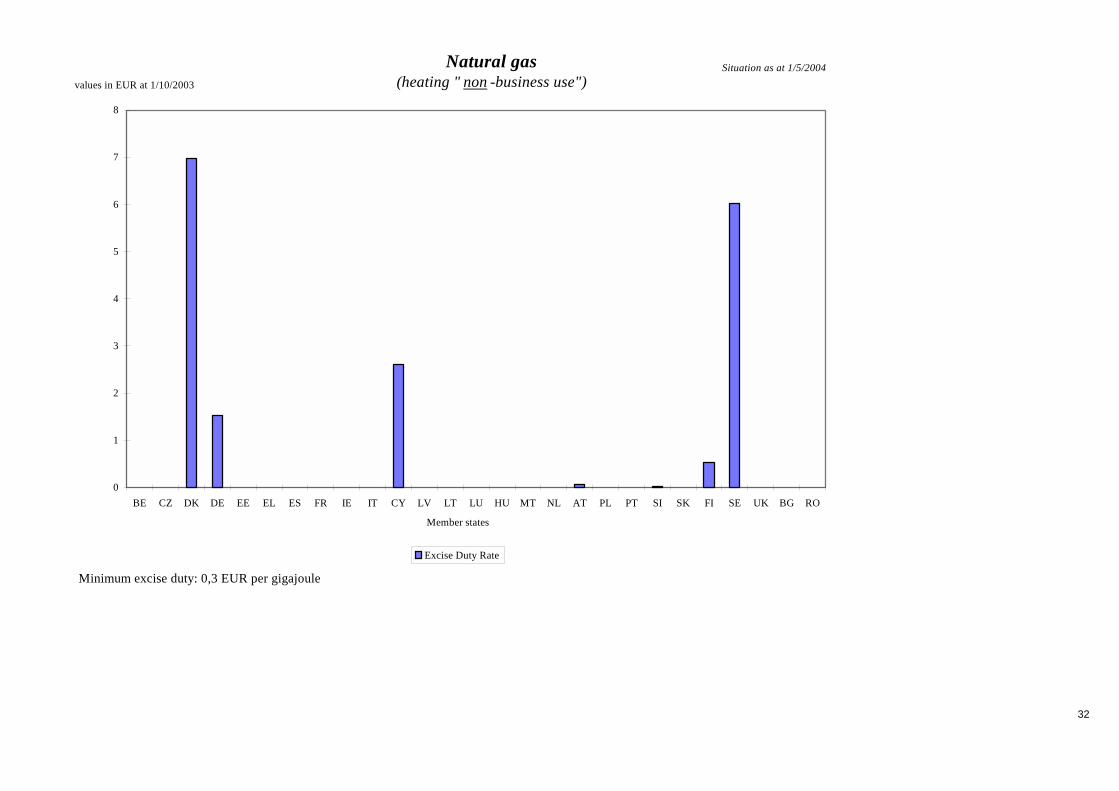

Excise Duty Rate

Natural gas (heating "business use")

Minimum excise duty: 0,15 EUR per gigajoule

32

Situation as at 1/5/2004

0

1

2

3

4

5

6

7

8

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Natural gas (heating " non -business use")

Minimum excise duty: 0,3 EUR per gigajoule

33

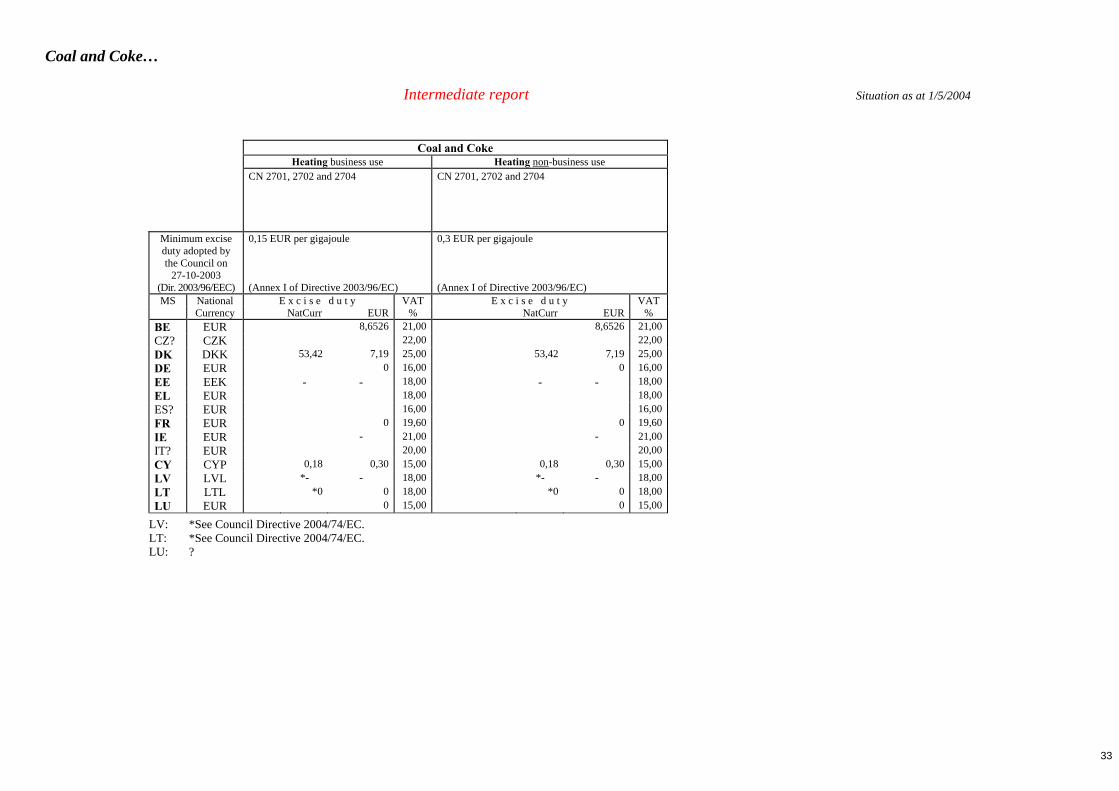

Coal and Coke…

Intermediate report Situation as at 1/5/2004

Coal and Coke

Heating business use Heating non-business use CN 2701, 2702 and 2704

CN 2701, 2702 and 2704

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

0,15 EUR per gigajoule (Annex I of Directive 2003/96/EC)

0,3 EUR per gigajoule (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

BE EUR 8,6526 21,00 8,6526 21,00CZ? CZK 22,00 22,00DK DKK 53,42 7,19 25,00 53,42 7,19 25,00DE EUR 0 16,00 0 16,00EE EEK - - 18,00 - - 18,00EL EUR 18,00 18,00ES? EUR 16,00 16,00FR EUR 0 19,60 0 19,60IE EUR - 21,00 - 21,00IT? EUR 20,00 20,00CY CYP 0,18 0,30 15,00 0,18 0,30 15,00LV LVL *- - 18,00 *- - 18,00LT LTL *0 0 18,00 *0 0 18,00LU EUR 0 15,00 0 15,00

LV: *See Council Directive 2004/74/EC. LT: *See Council Directive 2004/74/EC. LU: ?

34

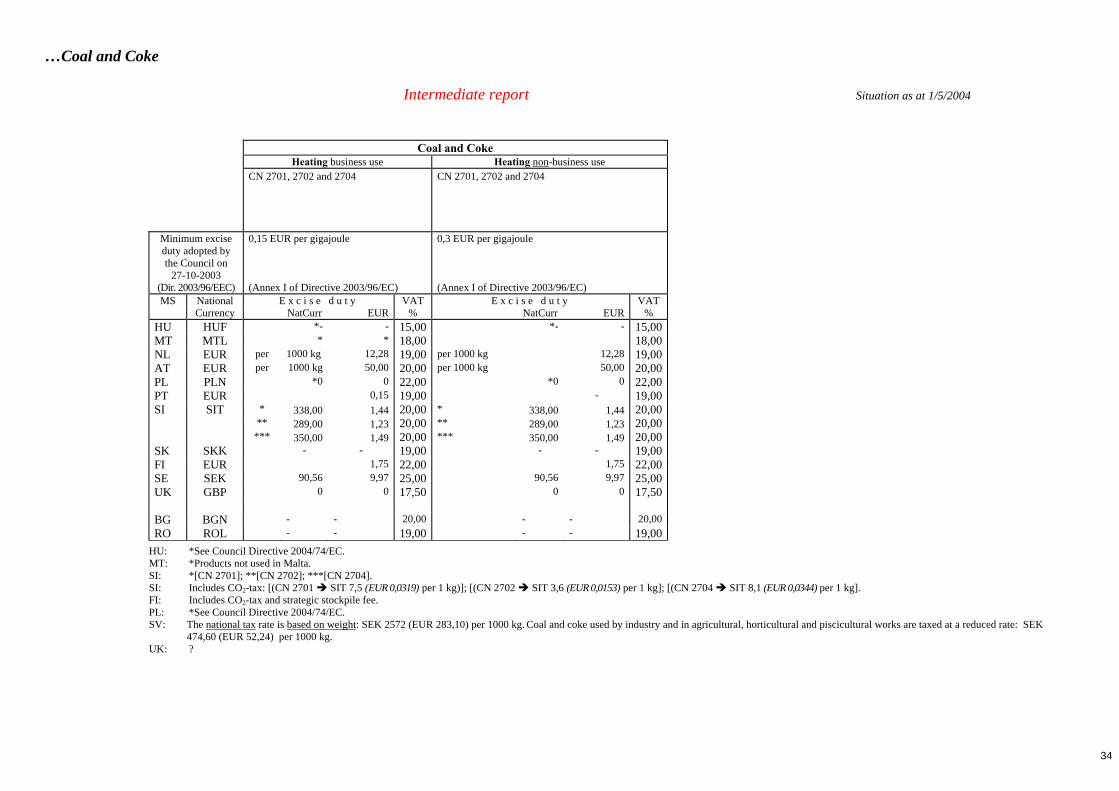

…Coal and Coke

Intermediate report Situation as at 1/5/2004

Coal and Coke

Heating business use Heating non-business use CN 2701, 2702 and 2704

CN 2701, 2702 and 2704

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

0,15 EUR per gigajoule (Annex I of Directive 2003/96/EC)

0,3 EUR per gigajoule (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

HU HUF *- - 15,00 *- - 15,00MT MTL * * 18,00 18,00NL EUR per 1000 kg 12,28 19,00 per 1000 kg 12,28 19,00AT EUR per 1000 kg 50,00 20,00 per 1000 kg 50,00 20,00PL PLN *0 0 22,00 *0 0 22,00PT EUR 0,15 19,00 - 19,00SI SIT * 338,00 1,44 20,00 * 338,00 1,44 20,00 ** 289,00 1,23 20,00 ** 289,00 1,23 20,00 *** 350,00 1,49 20,00 *** 350,00 1,49 20,00SK SKK - - 19,00 - - 19,00FI EUR 1,75 22,00 1,75 22,00SE SEK 90,56 9,97 25,00 90,56 9,97 25,00UK GBP 0 0 17,50 0 0 17,50 BG BGN - - 20,00 - - 20,00RO ROL - - 19,00 - - 19,00

HU: *See Council Directive 2004/74/EC. MT: *Products not used in Malta. SI: *[CN 2701]; **[CN 2702]; ***[CN 2704]. SI: Includes CO2-tax: [(CN 2701 " SIT 7,5 (EUR 0,0319) per 1 kg)]; [(CN 2702 " SIT 3,6 (EUR 0,0153) per 1 kg]; [(CN 2704 " SIT 8,1 (EUR 0,0344) per 1 kg]. FI: Includes CO2-tax and strategic stockpile fee. PL: *See Council Directive 2004/74/EC. SV: The national tax rate is based on weight: SEK 2572 (EUR 283,10) per 1000 kg. Coal and coke used by industry and in agricultural, horticultural and piscicultural works are taxed at a reduced rate: SEK

474,60 (EUR 52,24) per 1000 kg. UK: ?

35

Situation as at 1/5/2004

0

2

4

6

8

10

12

14

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

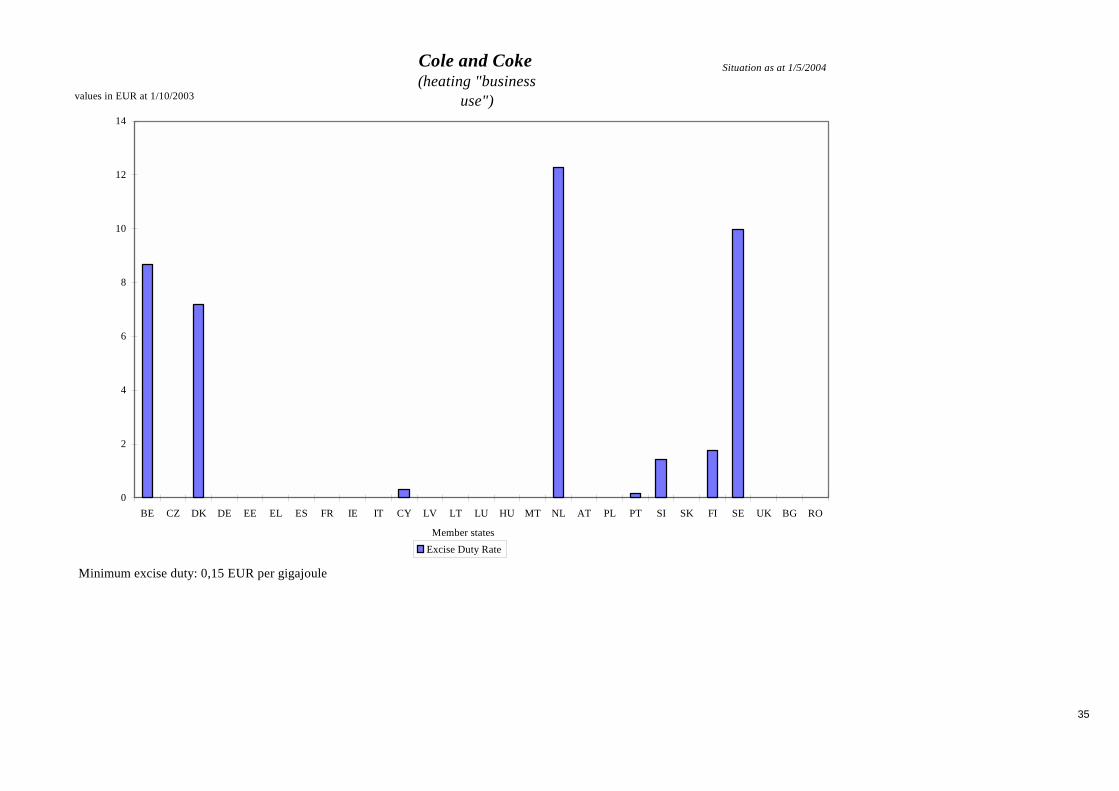

Excise Duty Rate

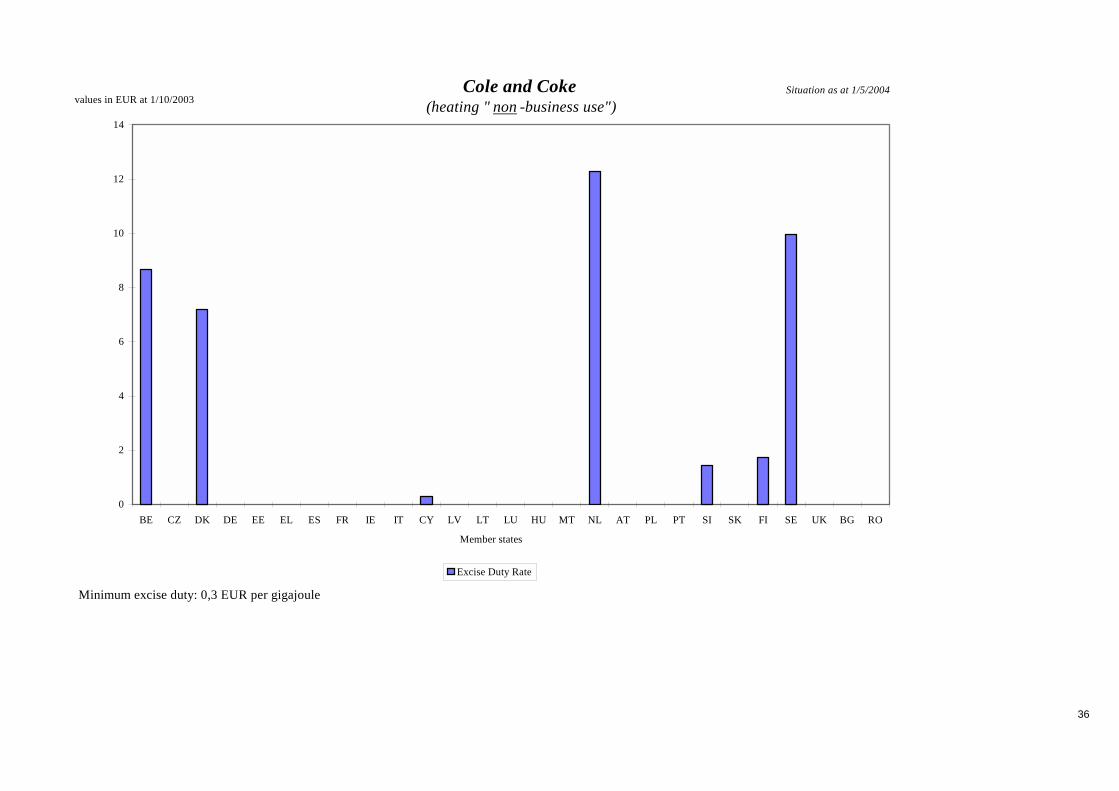

Cole and Coke (heating "business

use")

Minimum excise duty: 0,15 EUR per gigajoule

36

Situation as at 1/5/2004

0

2

4

6

8

10

12

14

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Cole and Coke (heating " non -business use")

Minimum excise duty: 0,3 EUR per gigajoule

37

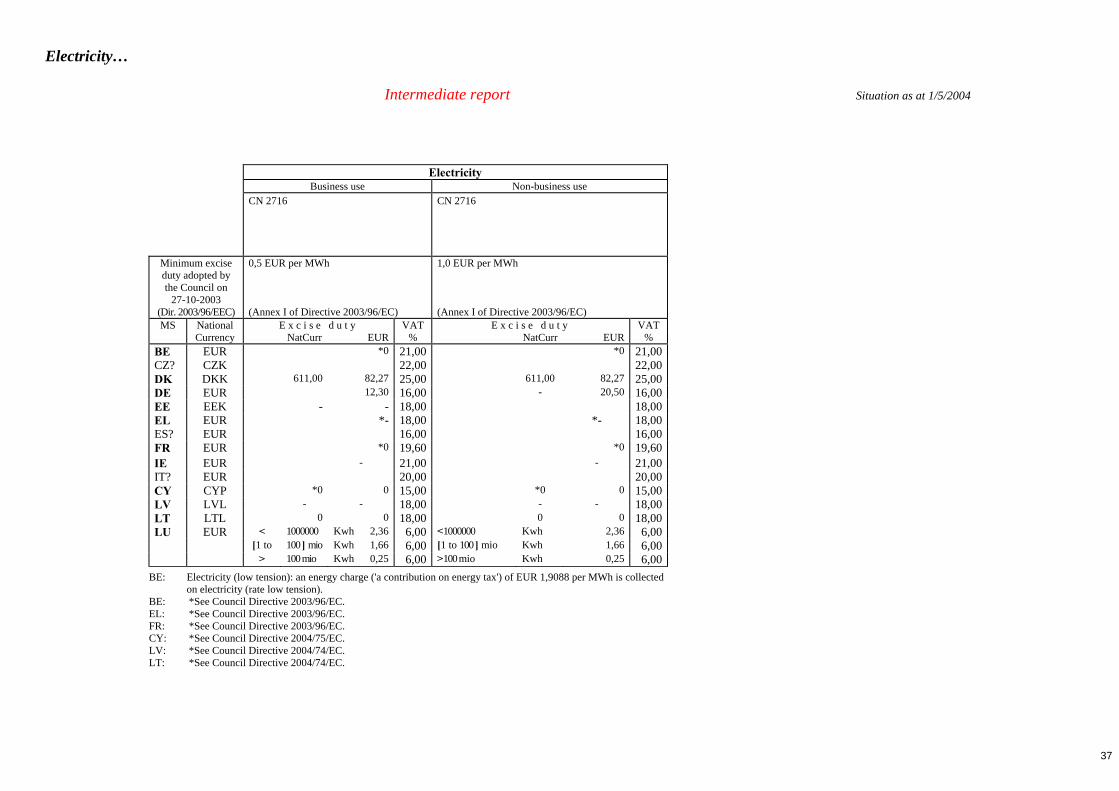

Electricity…

Intermediate report Situation as at 1/5/2004

Electricity

Business use Non-business use CN 2716

CN 2716

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

0,5 EUR per MWh (Annex I of Directive 2003/96/EC)

1,0 EUR per MWh (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

BE EUR *0 21,00 *0 21,00CZ? CZK 22,00 22,00DK DKK 611,00 82,27 25,00 611,00 82,27 25,00DE EUR 12,30 16,00 - 20,50 16,00EE EEK - - 18,00 18,00EL EUR *- 18,00 *- 18,00ES? EUR 16,00 16,00FR EUR *0 19,60 *0 19,60IE EUR - 21,00 - 21,00IT? EUR 20,00 20,00CY CYP *0 0 15,00 *0 0 15,00LV LVL - - 18,00 - - 18,00LT LTL 0 0 18,00 0 0 18,00LU EUR < 1000000 Kwh 2,36 6,00 <1000000 Kwh 2,36 6,00 [1 to 100 ] mio Kwh 1,66 6,00 [1 to 100 ] mio Kwh 1,66 6,00 > 100 mio Kwh 0,25 6,00 >100 mio Kwh 0,25 6,00

BE: Electricity (low tension): an energy charge ('a contribution on energy tax') of EUR 1,9088 per MWh is collected on electricity (rate low tension).

BE: *See Council Directive 2003/96/EC. EL: *See Council Directive 2003/96/EC. FR: *See Council Directive 2003/96/EC. CY: *See Council Directive 2004/75/EC. LV: *See Council Directive 2004/74/EC. LT: *See Council Directive 2004/74/EC.

38

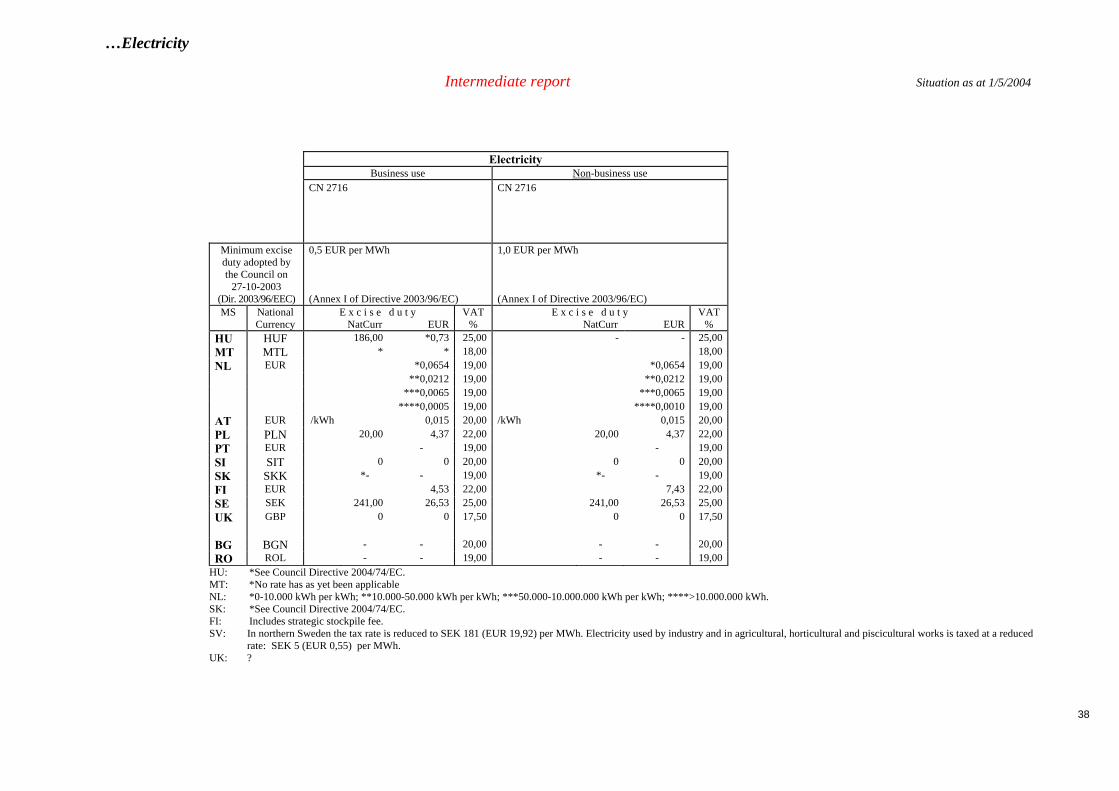

…Electricity

Intermediate report Situation as at 1/5/2004

Electricity

Business use Non-business use CN 2716

CN 2716

Minimum excise duty adopted by the Council on

27-10-2003 (Dir. 2003/96/EEC)

0,5 EUR per MWh (Annex I of Directive 2003/96/EC)

1,0 EUR per MWh (Annex I of Directive 2003/96/EC)

MS National E x c i s e d u t y VAT E x c i s e d u t y VAT Currency NatCurr EUR % NatCurr EUR %

HU HUF 186,00 *0,73 25,00 - - 25,00MT MTL * * 18,00 18,00NL EUR *0,0654 19,00 *0,0654 19,00 **0,0212 19,00 **0,0212 19,00 ***0,0065 19,00 ***0,0065 19,00 ****0,0005 19,00 ****0,0010 19,00AT EUR /kWh 0,015 20,00 /kWh 0,015 20,00PL PLN 20,00 4,37 22,00 20,00 4,37 22,00PT EUR - 19,00 - 19,00SI SIT 0 0 20,00 0 0 20,00SK SKK *- - 19,00 *- - 19,00FI EUR 4,53 22,00 7,43 22,00SE SEK 241,00 26,53 25,00 241,00 26,53 25,00UK GBP 0 0 17,50 0 0 17,50 BG BGN - - 20,00 - - 20,00RO ROL - - 19,00 - - 19,00

HU: *See Council Directive 2004/74/EC. MT: *No rate has as yet been applicable NL: *0-10.000 kWh per kWh; **10.000-50.000 kWh per kWh; ***50.000-10.000.000 kWh per kWh; ****>10.000.000 kWh. SK: *See Council Directive 2004/74/EC. FI: Includes strategic stockpile fee. SV: In northern Sweden the tax rate is reduced to SEK 181 (EUR 19,92) per MWh. Electricity used by industry and in agricultural, horticultural and piscicultural works is taxed at a reduced

rate: SEK 5 (EUR 0,55) per MWh. UK: ?

39

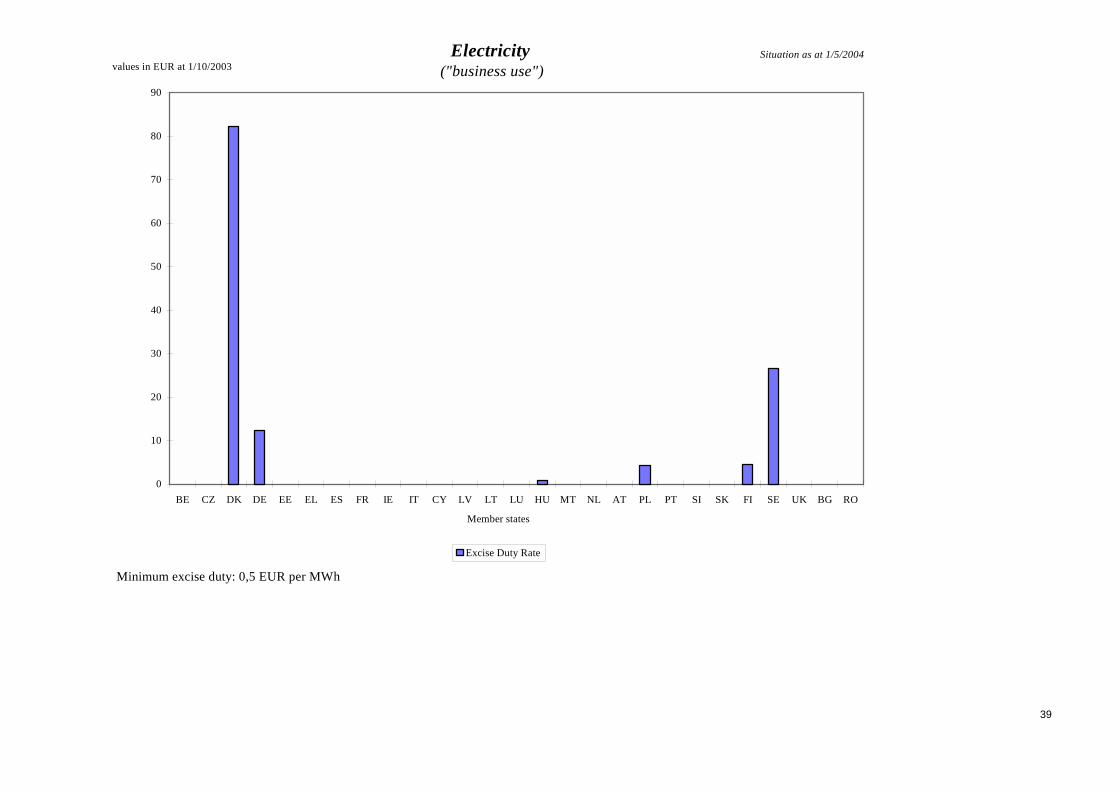

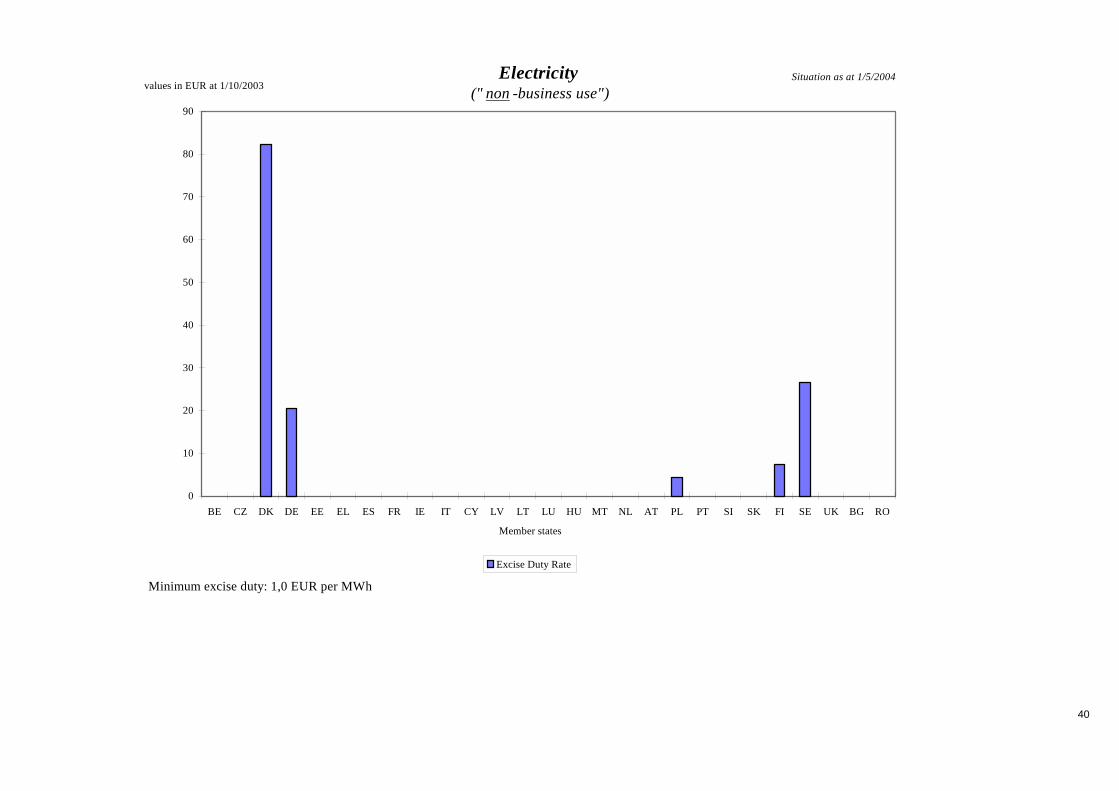

Situation as at 1/5/2004

0

10

20

30

40

50

60

70

80

90

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Electricity ("business use")

Minimum excise duty: 0,5 EUR per MWh

40

Situation as at 1/5/2004

0

10

20

30

40

50

60

70

80

90

BE CZ DK DE EE EL ES FR IE IT CY LV LT LU HU MT NL AT PL PT SI SK FI SE UK BG RO

Member states

values in EUR at 1/10/2003

Excise Duty Rate

Electricity (" non -business use")

Minimum excise duty: 1,0 EUR per MWh

41

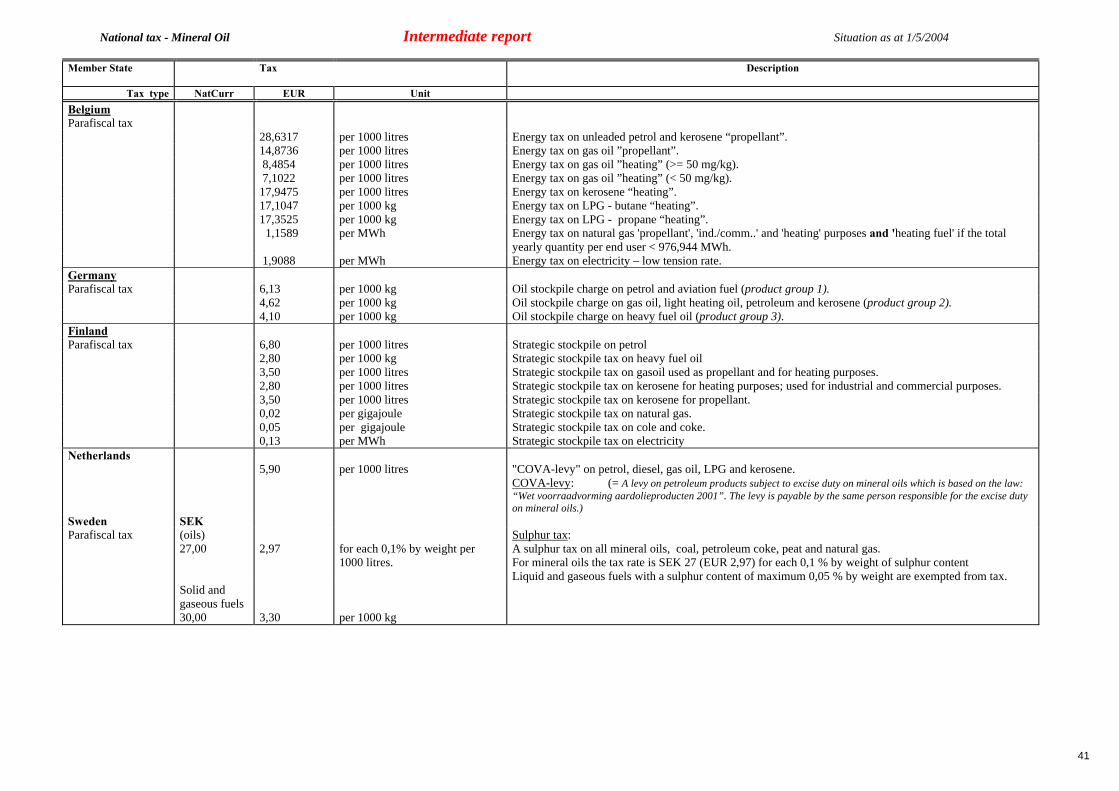

National tax - Mineral Oil Intermediate report Situation as at 1/5/2004

Member State

Tax Description

Tax type NatCurr EUR Unit Belgium Parafiscal tax 28,6317 per 1000 litres Energy tax on unleaded petrol and kerosene “propellant”. 14,8736 per 1000 litres Energy tax on gas oil ”propellant”. 8,4854 per 1000 litres Energy tax on gas oil ”heating” (>= 50 mg/kg). 7,1022 per 1000 litres Energy tax on gas oil ”heating” (< 50 mg/kg). 17,9475 per 1000 litres Energy tax on kerosene “heating”. 17,1047 per 1000 kg Energy tax on LPG - butane “heating”. 17,3525 per 1000 kg Energy tax on LPG - propane “heating”. 1,1589 per MWh Energy tax on natural gas 'propellant', 'ind./comm..' and 'heating' purposes and 'heating fuel' if the total

yearly quantity per end user < 976,944 MWh. 1,9088 per MWh Energy tax on electricity – low tension rate. Germany Parafiscal tax 6,13 per 1000 kg Oil stockpile charge on petrol and aviation fuel (product group 1). 4,62 per 1000 kg Oil stockpile charge on gas oil, light heating oil, petroleum and kerosene (product group 2). 4,10 per 1000 kg Oil stockpile charge on heavy fuel oil (product group 3). Finland Parafiscal tax 6,80 per 1000 litres Strategic stockpile on petrol 2,80 per 1000 kg Strategic stockpile tax on heavy fuel oil 3,50 per 1000 litres Strategic stockpile tax on gasoil used as propellant and for heating purposes. 2,80 per 1000 litres Strategic stockpile tax on kerosene for heating purposes; used for industrial and commercial purposes. 3,50 per 1000 litres Strategic stockpile tax on kerosene for propellant. 0,02 per gigajoule Strategic stockpile tax on natural gas. 0,05 per gigajoule Strategic stockpile tax on cole and coke. 0,13 per MWh Strategic stockpile tax on electricity Netherlands 5,90 per 1000 litres "COVA-levy" on petrol, diesel, gas oil, LPG and kerosene.

COVA-levy: (= A levy on petroleum products subject to excise duty on mineral oils which is based on the law: “Wet voorraadvorming aardolieproducten 2001”. The levy is payable by the same person responsible for the excise duty on mineral oils.)

Sweden SEK Parafiscal tax (oils)

27,00 2,97

for each 0,1% by weight per 1000 litres.

Sulphur tax: A sulphur tax on all mineral oils, coal, petroleum coke, peat and natural gas. For mineral oils the tax rate is SEK 27 (EUR 2,97) for each 0,1 % by weight of sulphur content Liquid and gaseous fuels with a sulphur content of maximum 0,05 % by weight are exempted from tax.

Solid and gaseous fuels 30,00

3,30

per 1000 kg

42