Embed Size (px)

Citation preview

EPAC OIL & GAS INVESTOR

CONFERENCE

June 12, 2013

1

• In the interest of providing information regarding Paramount Resources Ltd.

("Paramount" or the "Company"), including management's assessment of

the Company's future plans and operations, this presentation contains

certain forward-looking information and forward-looking statements.

• The projections, estimates and beliefs contained in such forward-looking

information and statements necessarily involve a number of assumptions

and are subject to known and unknown risks and uncertainties which may

cause the Company's actual performance and financial results in future

periods to differ materially from any estimates or projections of future

performance or results expressed or implied by such forward-looking

statements. The material assumptions, risks and uncertainties are referred

to in the advisories contained in Appendix A.

• Accordingly, shareholders and potential investors are cautioned that events

or circumstances could cause actual results to differ materially from those

predicted.

• Any use of information contained within this presentation is expressly

forbidden.

Future Oriented Information (See additional advisories at the end of this document)

2

• Q1 2013 production: 22,591 Boe/d (~85% gas)

• 95.4 MM shares outstanding

• Market capitalization @ $37.50/share: $3.6 billion

• > 50% insider ownership

• 1.2 million net acres undeveloped land (December 31, 2012)

• Net Debt: $713 MM (March 31, 2013 pro forma equity offering)

• 2013 Capital Expenditure Guidance: $650 MM

• 2013 Production Guidance: Avg 21,000 Boe/d-25,000 Boe/d(1)

– 2014 projected production to attain > 50,000 Boe/d

Corporate Profile

(1) Production reliant on availability of downstream NGLs transportation and processing capacity

3

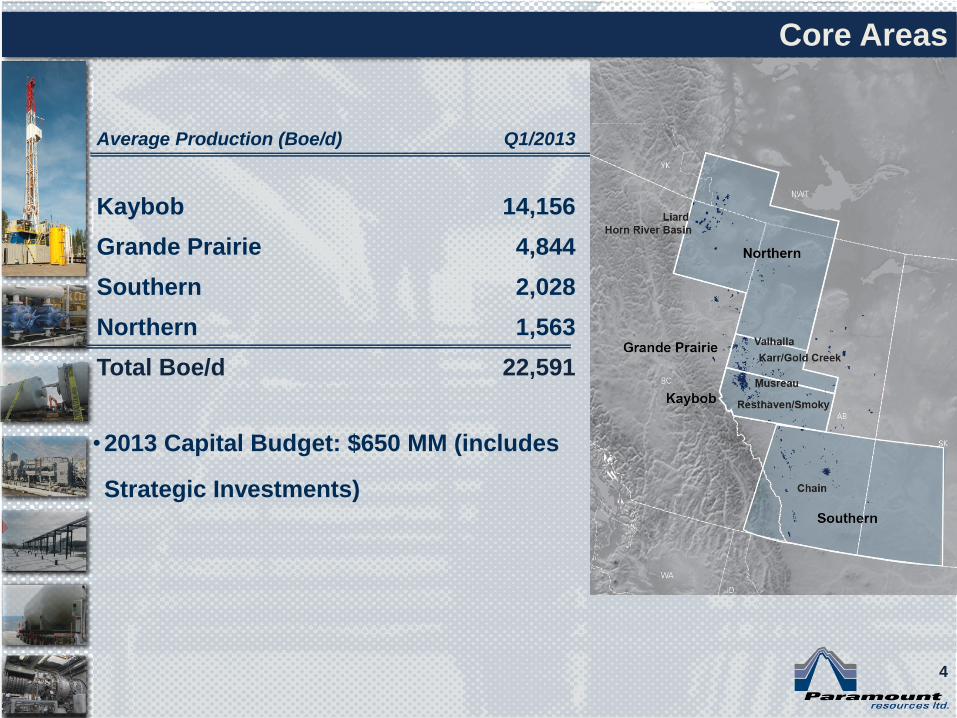

Average Production (Boe/d) Q1/2013

Kaybob 14,156

Grande Prairie 4,844

Southern 2,028

Northern 1,563

Total Boe/d 22,591

Core Areas

•2013 Capital Budget: $650 MM (includes

Strategic Investments)

4

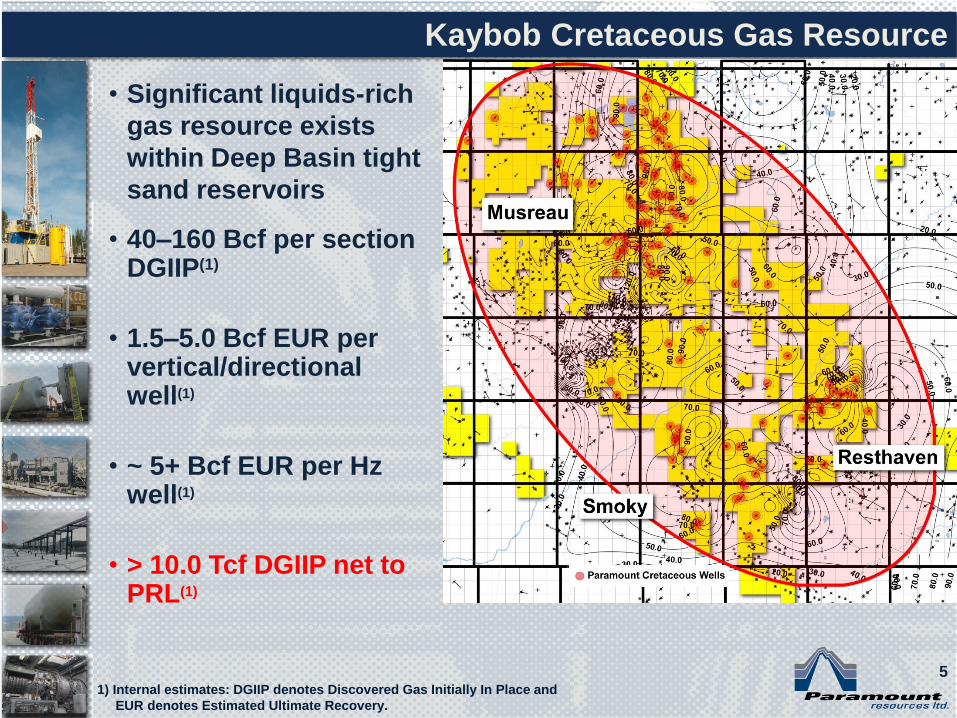

• Significant liquids-rich

gas resource exists

within Deep Basin tight

sand reservoirs

• 40–160 Bcf per section DGIIP(1)

• 1.5–5.0 Bcf EUR per vertical/directional well(1)

• ~ 5+ Bcf EUR per Hz well(1)

• > 10.0 Tcf DGIIP net to PRL(1)

Kaybob Cretaceous Gas Resource

1) Internal estimates: DGIIP denotes Discovered Gas Initially In Place and

EUR denotes Estimated Ultimate Recovery.

70 Bcf/Section Average DGIIP(1)

CRETACEOUS GAS SANDS DGIIP PER SECTION

5

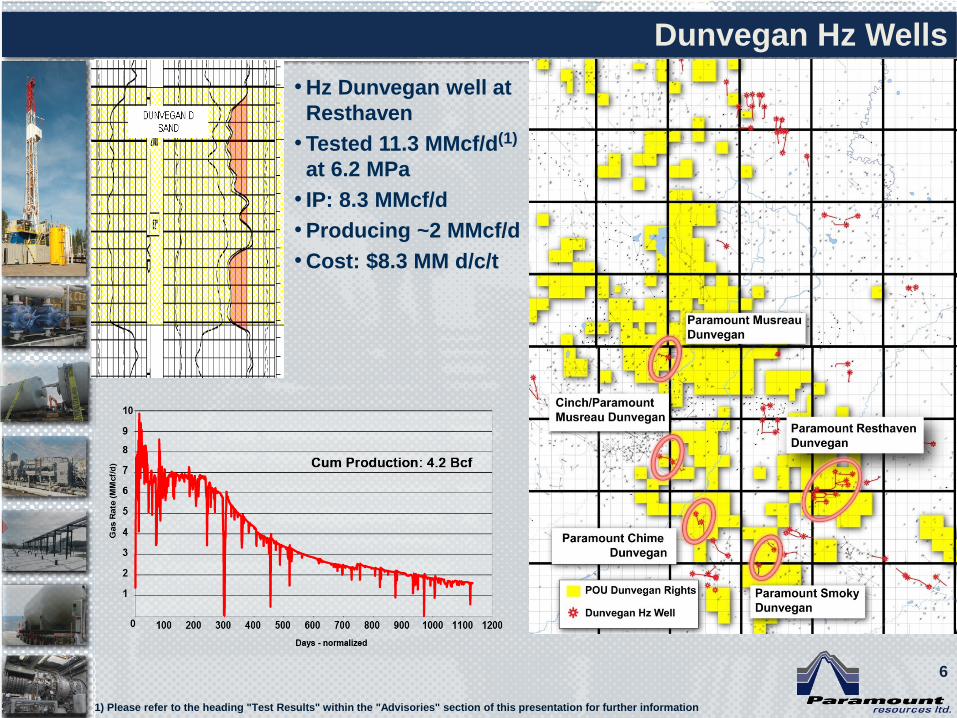

Dunvegan Hz Wells

•Hz Dunvegan well at

Resthaven

•Tested 11.3 MMcf/d(1)

at 6.2 MPa

• IP: 8.3 MMcf/d

•Producing ~2 MMcf/d

•Cost: $8.3 MM d/c/t

1) Please refer to the heading "Test Results" within the "Advisories" section of this presentation for further information

6

• Hz Falher well at

Musreau

• Tested 16.4 MMcf/d(1)

at 20.8 MPa

• IP: 12 MMcf/d

• Producing ~2 MMcf/d

• Cost: $8.6 MM d/c/t

Falher Hz Wells

1) Please refer to the heading "Test Results" within the "Advisories" section of this presentation for further information

7

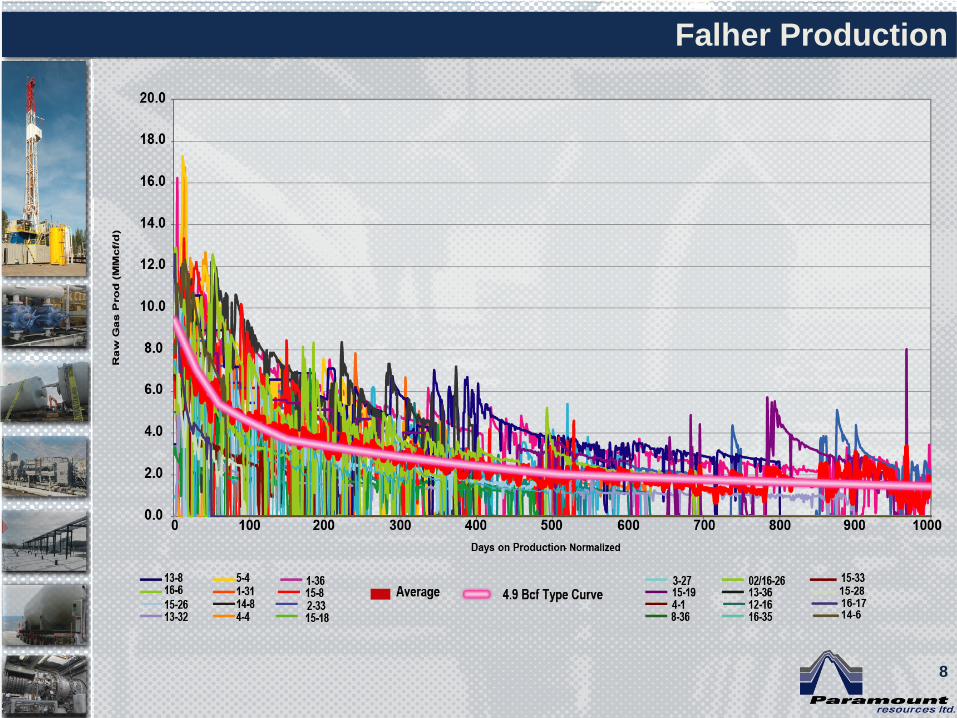

Falher Production

8

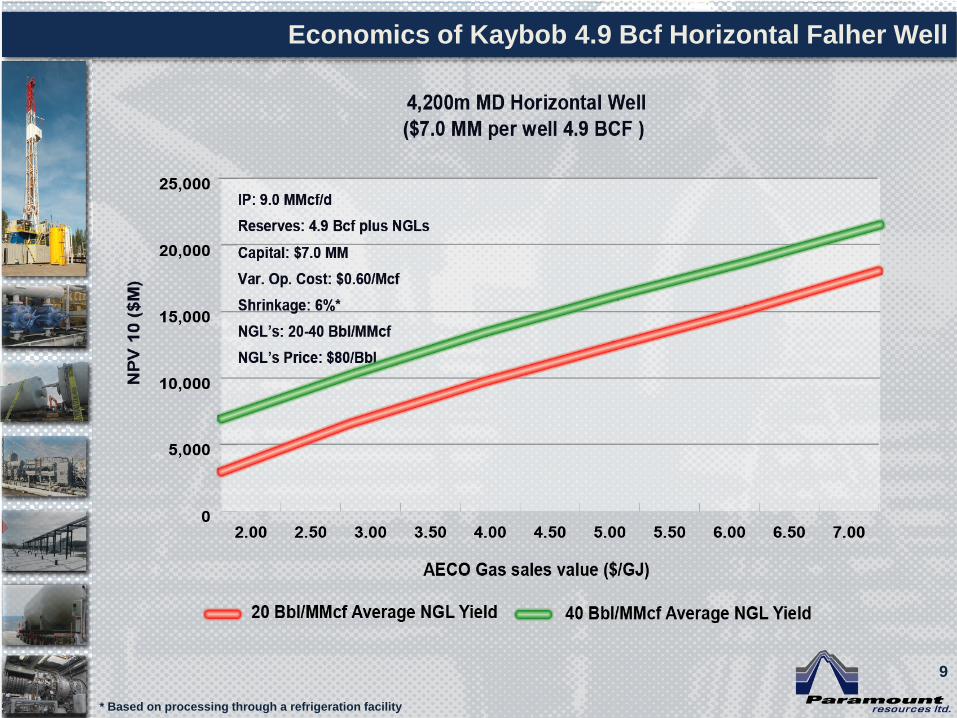

Economics of Kaybob 4.9 Bcf Horizontal Falher Well

* Based on processing through a refrigeration facility

9

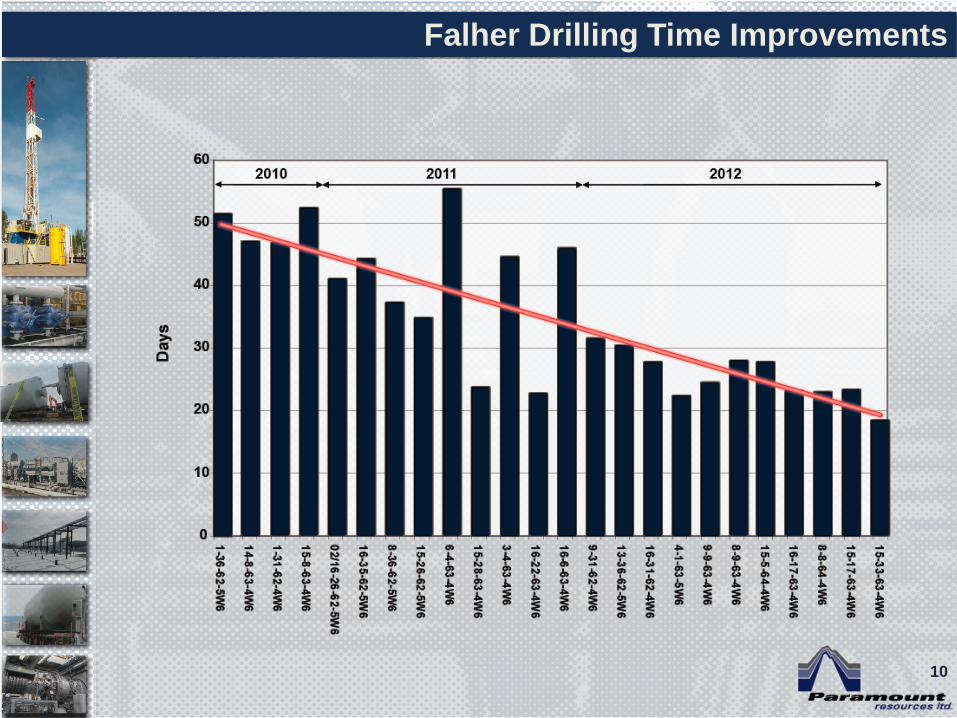

Falher Drilling Time Improvements

10

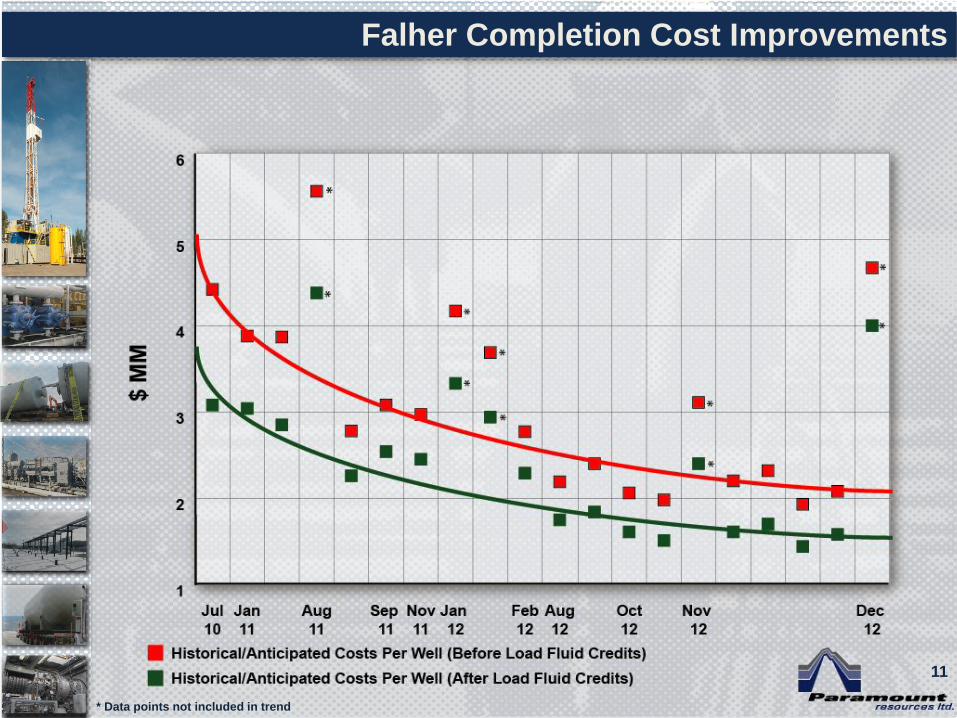

Falher Completion Cost Improvements

* Data points not included in trend

11

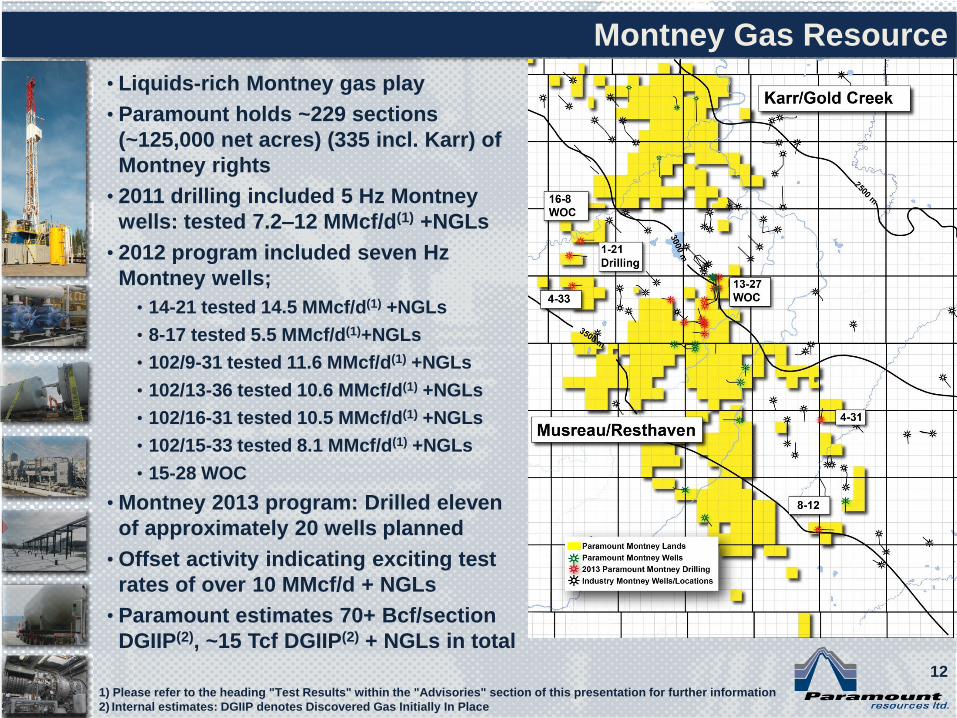

• Liquids-rich Montney gas play

• Paramount holds ~229 sections

(~125,000 net acres) (335 incl. Karr) of

Montney rights

• 2011 drilling included 5 Hz Montney

wells: tested 7.2–12 MMcf/d(1) +NGLs

• 2012 program included seven Hz

Montney wells;

• 14-21 tested 14.5 MMcf/d(1) +NGLs

• 8-17 tested 5.5 MMcf/d(1)+NGLs

• 102/9-31 tested 11.6 MMcf/d(1) +NGLs

• 102/13-36 tested 10.6 MMcf/d(1) +NGLs

• 102/16-31 tested 10.5 MMcf/d(1) +NGLs

• 102/15-33 tested 8.1 MMcf/d(1) +NGLs

• 15-28 WOC

• Montney 2013 program: Drilled eleven

of approximately 20 wells planned

• Offset activity indicating exciting test

rates of over 10 MMcf/d + NGLs

• Paramount estimates 70+ Bcf/section

DGIIP(2), ~15 Tcf DGIIP(2) + NGLs in total

Montney Gas Resource

1) Please refer to the heading "Test Results" within the "Advisories" section of this presentation for further information

2) Internal estimates: DGIIP denotes Discovered Gas Initially In Place

12

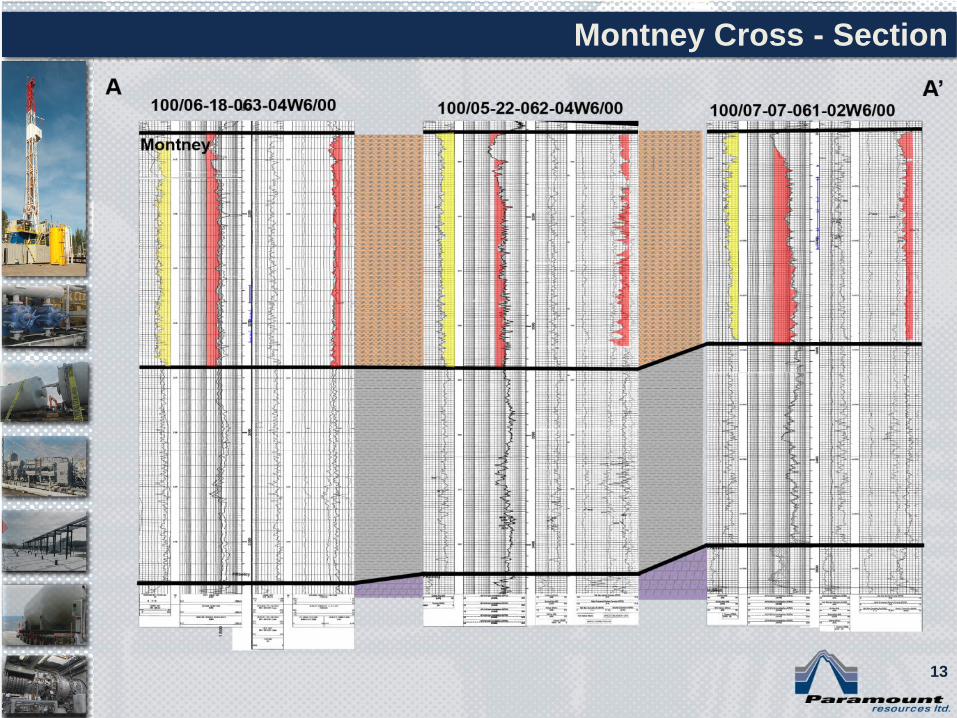

Montney Cross - Section

13

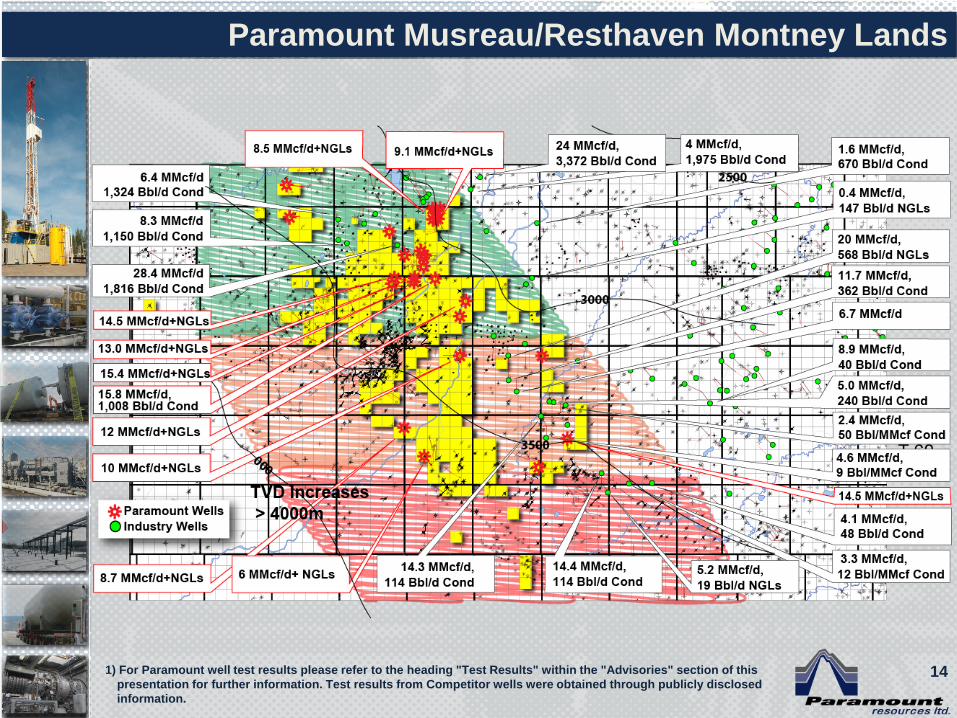

Paramount Musreau/Resthaven Montney Lands

1) For Paramount well test results please refer to the heading "Test Results" within the "Advisories" section of this

presentation for further information. Test results from Competitor wells were obtained through publicly disclosed

information.

14

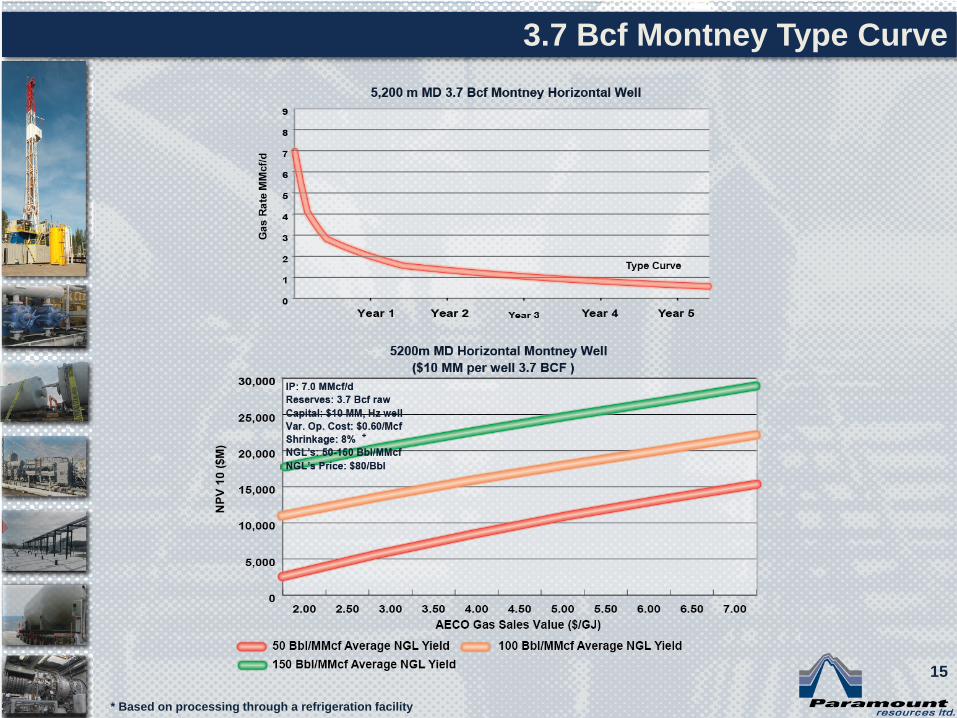

3.7 Bcf Montney Type Curve

* Based on processing through a refrigeration facility

15

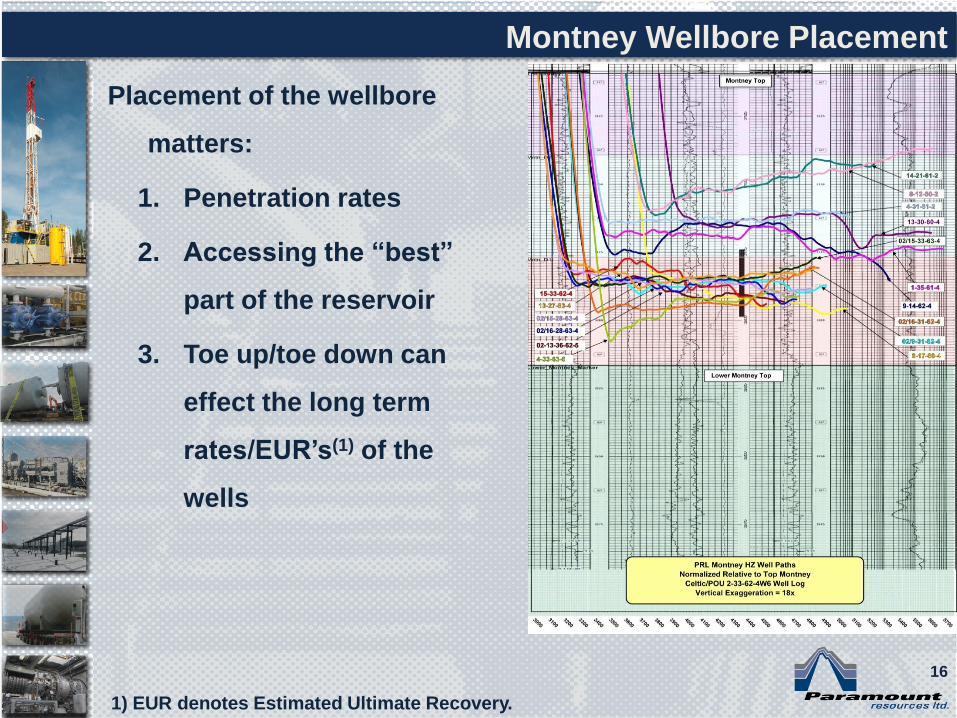

Placement of the wellbore

matters:

1. Penetration rates

2. Accessing the “best”

part of the reservoir

3. Toe up/toe down can

effect the long term

rates/EUR’s(1) of the

wells

Montney Wellbore Placement

1) EUR denotes Estimated Ultimate Recovery.

16

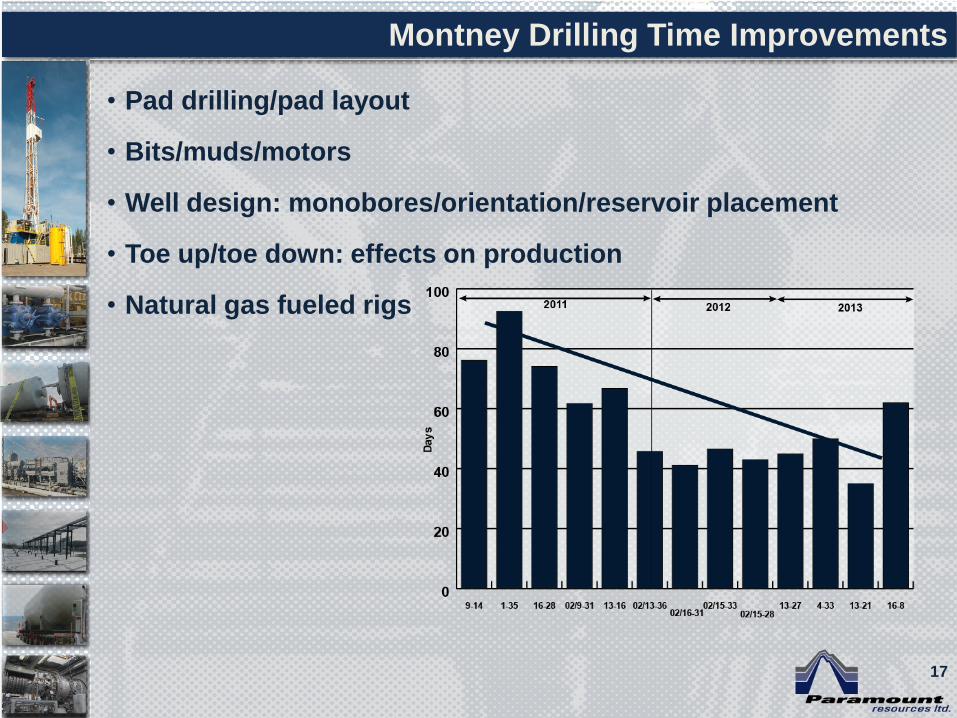

• Pad drilling/pad layout

• Bits/muds/motors

• Well design: monobores/orientation/reservoir placement

• Toe up/toe down: effects on production

• Natural gas fueled rigs

Montney Drilling Time Improvements

17

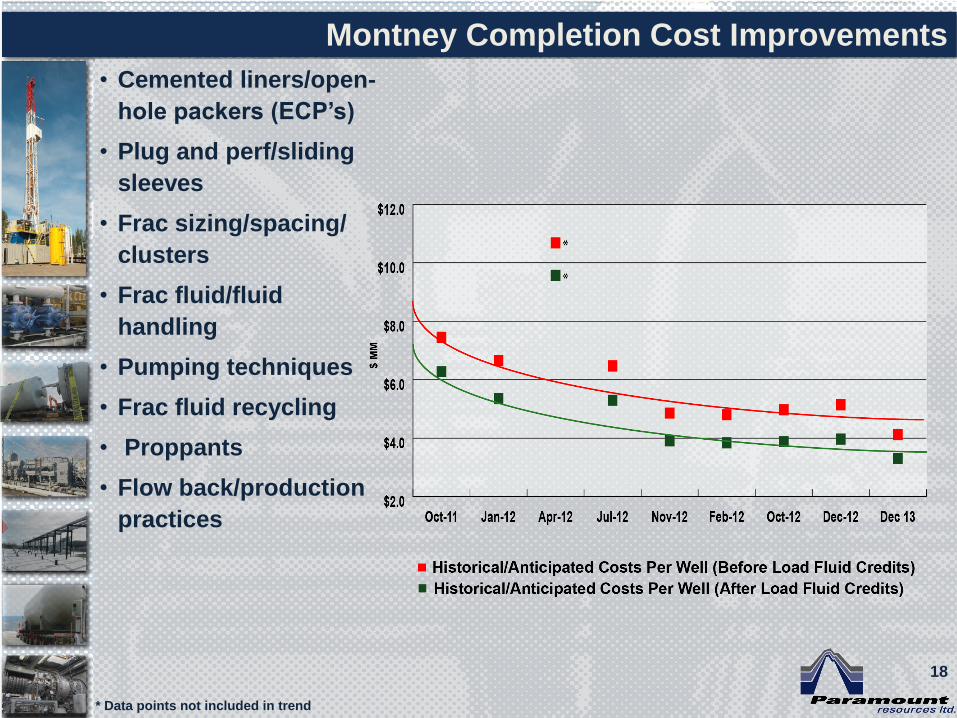

• Cemented liners/open-

hole packers (ECP’s)

• Plug and perf/sliding

sleeves

• Frac sizing/spacing/

clusters

• Frac fluid/fluid

handling

• Pumping techniques

• Frac fluid recycling

• Proppants

• Flow back/production

practices

Montney Completion Cost Improvements

* Data points not included in trend

18

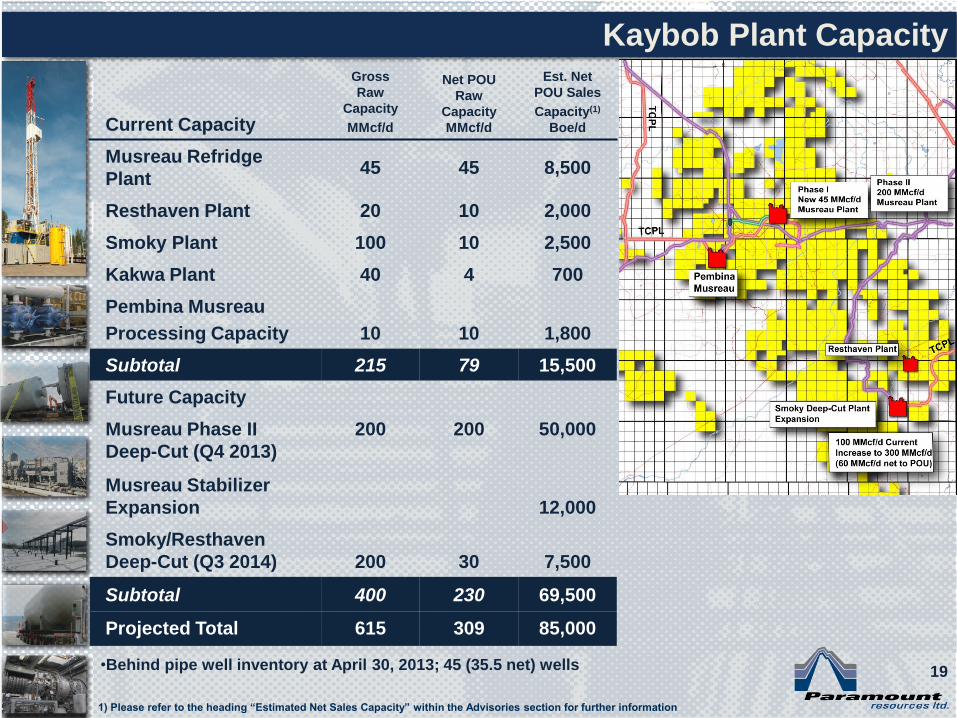

Current Capacity

Gross

Raw

Capacity

MMcf/d

Net POU

Raw

Capacity

MMcf/d

Est. Net

POU Sales

Capacity(1)

Boe/d

Musreau Refridge

Plant 45 45 8,500

Resthaven Plant 20 10 2,000

Smoky Plant 100 10 2,500

Kakwa Plant 40 4 700

Pembina Musreau

Processing Capacity 10 10 1,800

Subtotal 215 79 15,500

Future Capacity

Musreau Phase II

Deep-Cut (Q4 2013)

200 200 50,000

Musreau Stabilizer

Expansion 12,000

Smoky/Resthaven

Deep-Cut (Q3 2014) 200 30 7,500

Subtotal 400 230 69,500

Projected Total 615 309 85,000

Kaybob Plant Capacity

•Behind pipe well inventory at April 30, 2013; 45 (35.5 net) wells

1) Please refer to the heading “Estimated Net Sales Capacity” within the Advisories section for further information

19

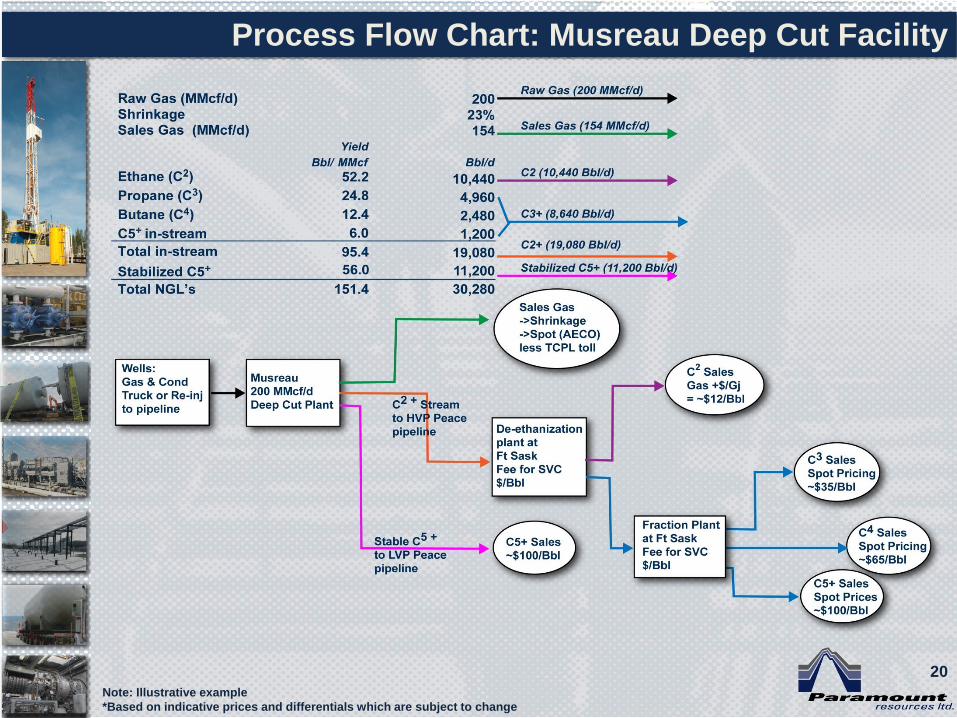

Process Flow Chart: Musreau Deep Cut Facility

Note: Illustrative example

*Based on indicative prices and differentials which are subject to change

20

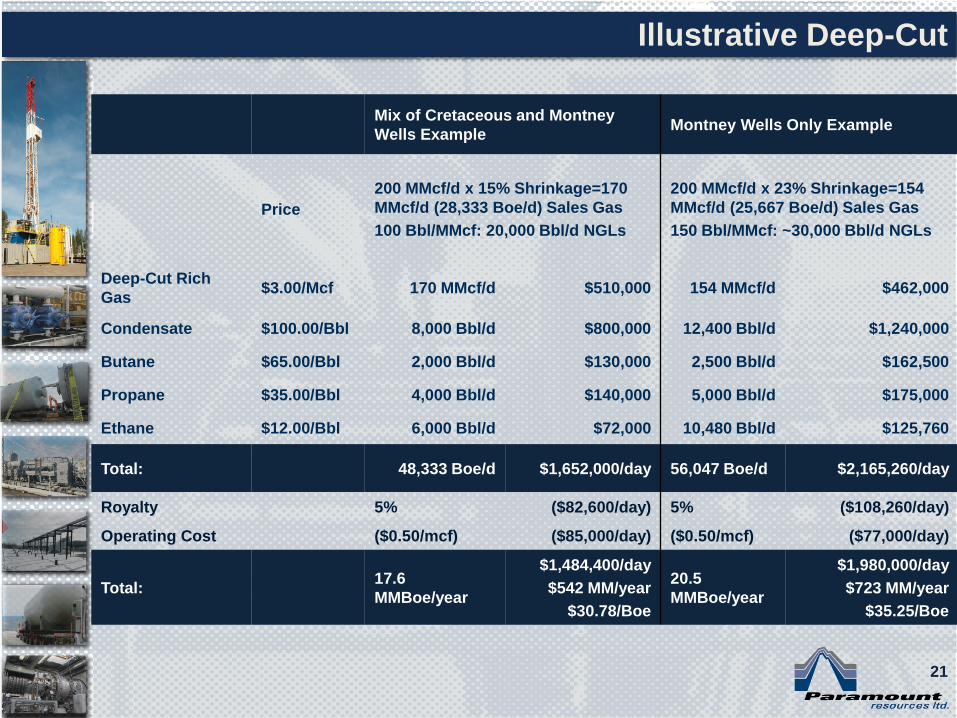

Mix of Cretaceous and Montney

Wells Example Montney Wells Only Example

Price

200 MMcf/d x 15% Shrinkage=170

MMcf/d (28,333 Boe/d) Sales Gas

100 Bbl/MMcf: 20,000 Bbl/d NGLs

200 MMcf/d x 23% Shrinkage=154

MMcf/d (25,667 Boe/d) Sales Gas

150 Bbl/MMcf: ~30,000 Bbl/d NGLs

Deep-Cut Rich

Gas $3.00/Mcf 170 MMcf/d $510,000 154 MMcf/d $462,000

Condensate $100.00/Bbl 8,000 Bbl/d $800,000 12,400 Bbl/d $1,240,000

Butane $65.00/Bbl 2,000 Bbl/d $130,000 2,500 Bbl/d $162,500

Propane $35.00/Bbl 4,000 Bbl/d $140,000 5,000 Bbl/d $175,000

Ethane $12.00/Bbl 6,000 Bbl/d $72,000 10,480 Bbl/d $125,760

Total: 48,333 Boe/d $1,652,000/day 56,047 Boe/d $2,165,260/day

Royalty 5% ($82,600/day) 5% ($108,260/day)

Operating Cost ($0.50/mcf) ($85,000/day) ($0.50/mcf) ($77,000/day)

Total: 17.6

MMBoe/year

$1,484,400/day

$542 MM/year

$30.78/Boe

20.5

MMBoe/year

$1,980,000/day

$723 MM/year

$35.25/Boe

Illustrative Deep-Cut

21

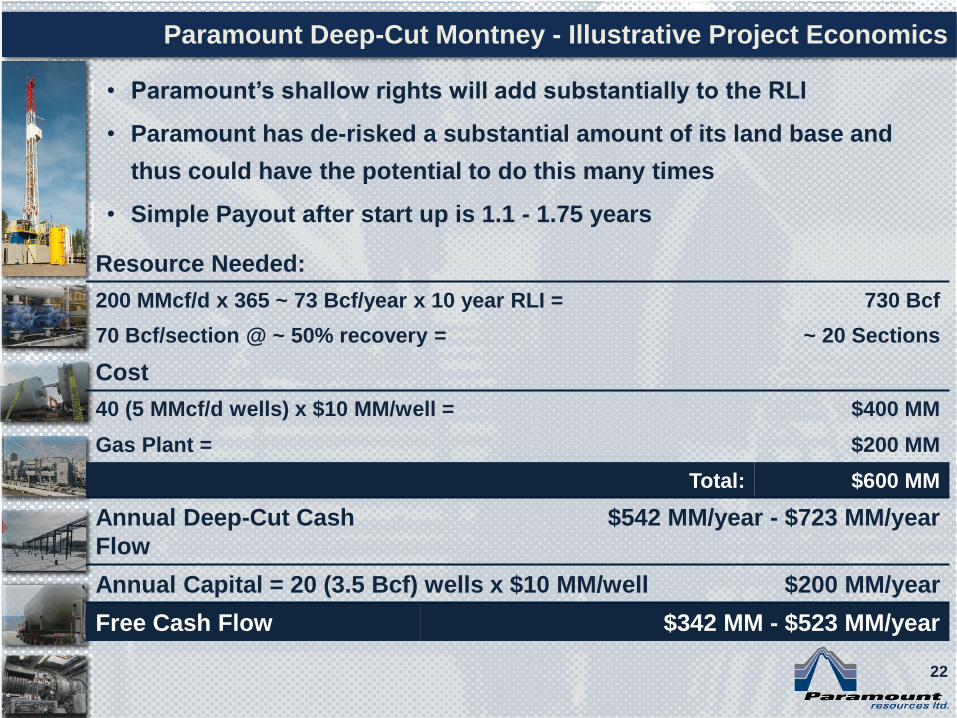

• Paramount’s shallow rights will add substantially to the RLI

• Paramount has de-risked a substantial amount of its land base and

thus could have the potential to do this many times

• Simple Payout after start up is 1.1 - 1.75 years

Paramount Deep-Cut Montney - Illustrative Project Economics

Resource Needed:

200 MMcf/d x 365 ~ 73 Bcf/year x 10 year RLI = 730 Bcf

70 Bcf/section @ ~ 50% recovery = ~ 20 Sections

Cost

40 (5 MMcf/d wells) x $10 MM/well = $400 MM

Gas Plant = $200 MM

Total: $600 MM

Annual Deep-Cut Cash

Flow

$542 MM/year - $723 MM/year

Annual Capital = 20 (3.5 Bcf) wells x $10 MM/well $200 MM/year

Free Cash Flow $342 MM - $523 MM/year

22

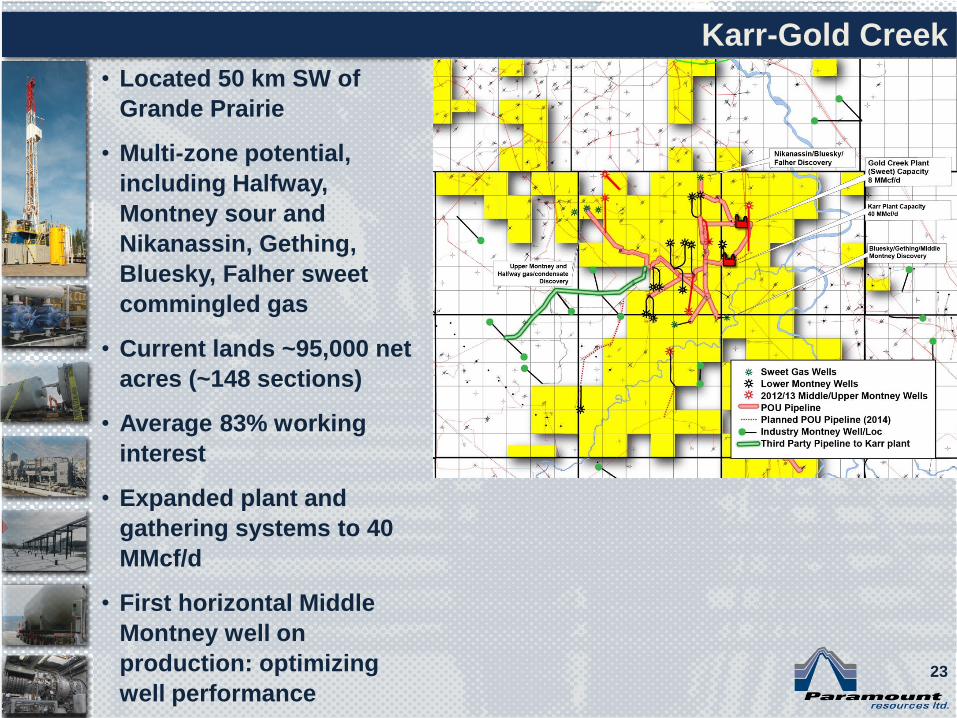

• Located 50 km SW of

Grande Prairie

• Multi-zone potential,

including Halfway,

Montney sour and

Nikanassin, Gething,

Bluesky, Falher sweet

commingled gas

• Current lands ~95,000 net

acres (~148 sections)

• Average 83% working

interest

• Expanded plant and

gathering systems to 40

MMcf/d

• First horizontal Middle

Montney well on

production: optimizing

well performance

Karr-Gold Creek

23

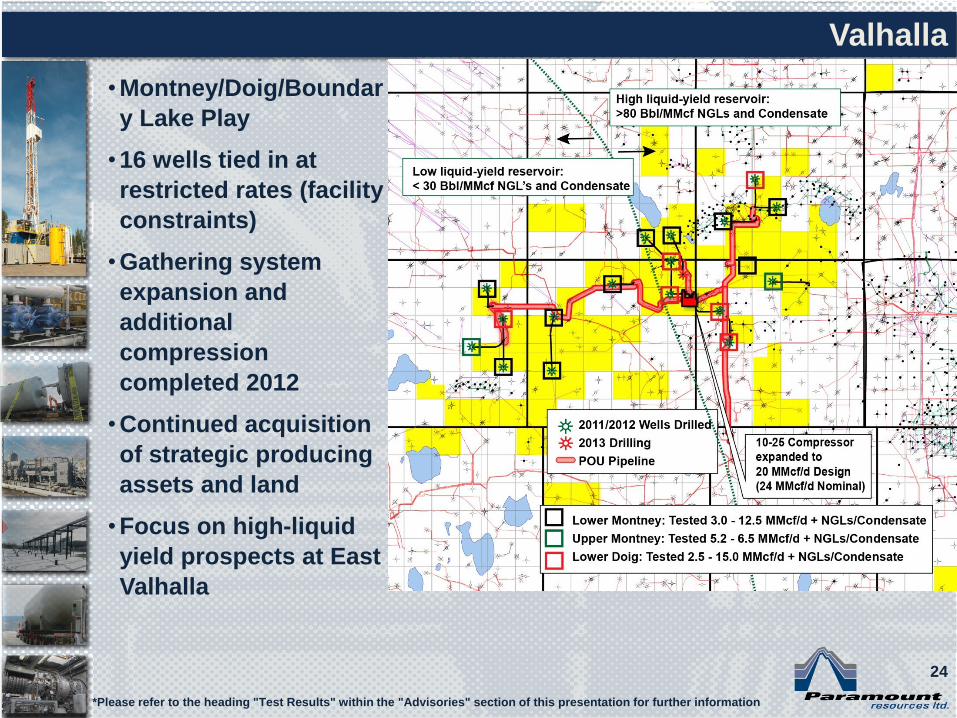

•Montney/Doig/Boundar

y Lake Play

•16 wells tied in at

restricted rates (facility

constraints)

•Gathering system

expansion and

additional

compression

completed 2012

•Continued acquisition

of strategic producing

assets and land

•Focus on high-liquid

yield prospects at East

Valhalla

Valhalla

*Please refer to the heading "Test Results" within the "Advisories" section of this presentation for further information

24

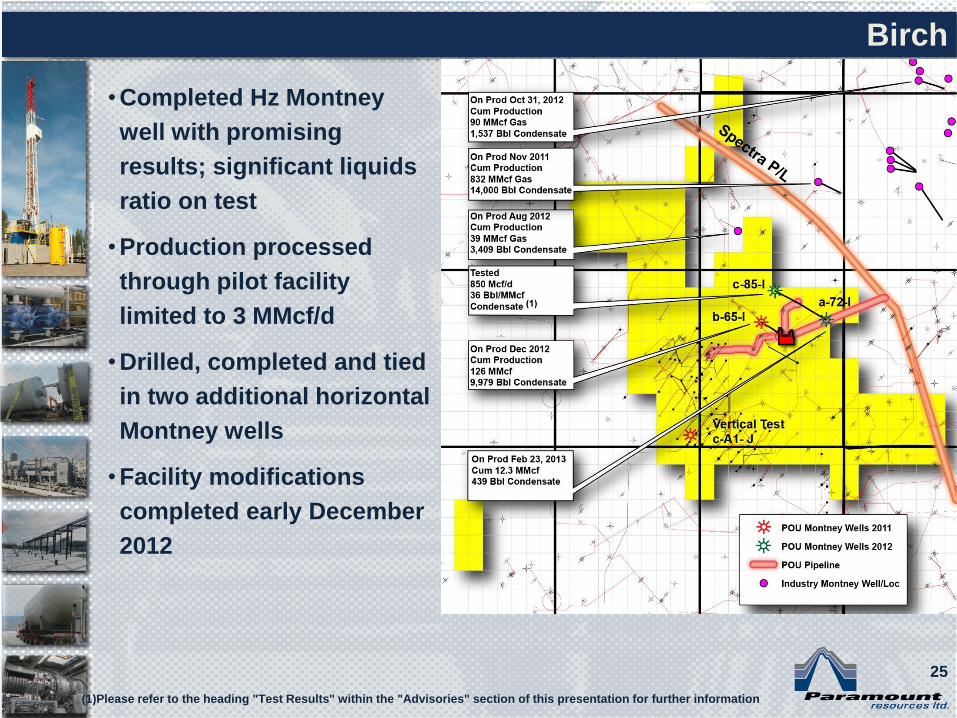

•Completed Hz Montney

well with promising

results; significant liquids

ratio on test

•Production processed

through pilot facility

limited to 3 MMcf/d

•Drilled, completed and tied

in two additional horizontal

Montney wells

•Facility modifications

completed early December

2012

Birch

(1)Please refer to the heading "Test Results" within the "Advisories" section of this presentation for further information

25

PARAMOUNT INVESTMENTS

26

CAVALIER ENERGY INC.

28

• Created in December 2011

• Experienced team led by CEO Dr. Will Roach (ex UTS)

• Paramount has contributed its oilsands assets and seed

capital to Cavalier Energy

• Funding at the Cavalier level will be via a combination of

equity and debt

• Assets retained as 100% WI within Cavalier Energy

• Regulatory application for the development of the first 10,000

Bbl/d SAGD project at Hoole filed November 2012

Cavalier Energy Inc.

29

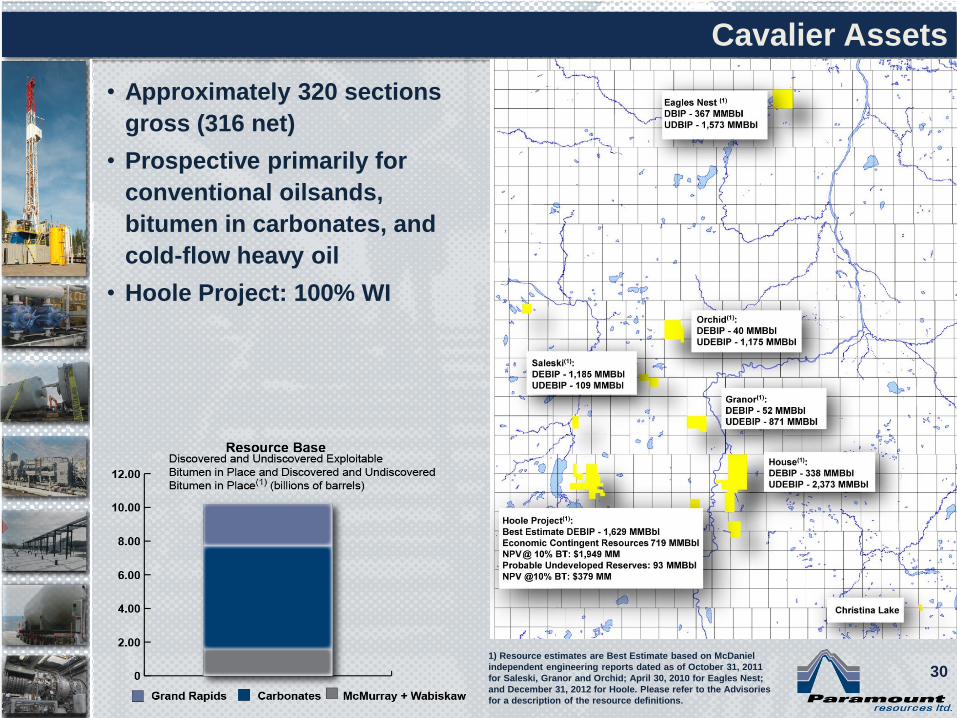

• Approximately 320 sections

gross (316 net)

• Prospective primarily for

conventional oilsands,

bitumen in carbonates, and

cold-flow heavy oil

• Hoole Project: 100% WI

Cavalier Assets

1) Resource estimates are Best Estimate based on McDaniel

independent engineering reports dated as of October 31, 2011

for Saleski, Granor and Orchid; April 30, 2010 for Eagles Nest;

and December 31, 2012 for Hoole. Please refer to the Advisories

for a description of the resource definitions.

30

UWID: 1AA/06-13-081-24W4/00 Well Name: PARA HOOLE 6-13-81-24 ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ CURR OPER: Paramount Rsrcs Ltd [0AW4] LIC#: 0302898 ORIG OPER: Paramount Rsrcs Ltd [%463] Date: 2004/01/28 LIC Substance: Crude Bitumen

GOVT KB: 614.1m GL: 609.9m MD: TVD: 483.0m LOGS KB: 613.9m GL: 609.9m PROJ DPTH: 482.0m PROJ FM@TD: Dwabamun FM@TD: Kmcmurray

BH COORDS: N 583.6m SW 13-081-24W4 BH LAT: 56°1'7.104" N : E 608.9m BH LON:113°37'21.648" W

SPUD: 2004/02/25 CMPL DRL: 2004/02/27 DAYS: 3 RR: 2004/02/28 DRL RIG: Artisan Corp #32

STAT: 2004/01/28 Location;2004/02/28 Drld & ABD CASG: 177.8mm SRF @ 126.0m LOGS: (PWT, Rm=3.200@25C) CS (126.2 ~ 461.3m), CNFD (126.2 ~ 473.7m), DISF (126.2 ~ 481.2m) ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ USER FORMATION TOPS geoSCOUT REF ELEV: 614.1m FORMATION TVD ELEV FORMATION TVD ELEV Kbfs 181.2 +432.9 Klloyd_ss 325.5 +288.6 Kviking 213.7 +400.4 Kclearwtr 340.4 +273.7 Kvik_ss 220.7 +393.4 Kmcmurray 439.4 +174.7 Kjoli_fou 239.3 +374.8 Kwabiskaw 439.5 +174.6 Kgrand_rp 252.0 +362.1 ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ CORES #01. 440.0 ~ 449.0m Kmcmurray Rec 0.0m #02. 449.0 ~ 458.0m " " Rec 0.0m

250

275

300

Kgrand_rp

Kjoli_fou

614.1

Paramount Kwabiskaw

Paramount 2004/02/28

483.0

1AA/06-13-081-24W4/00

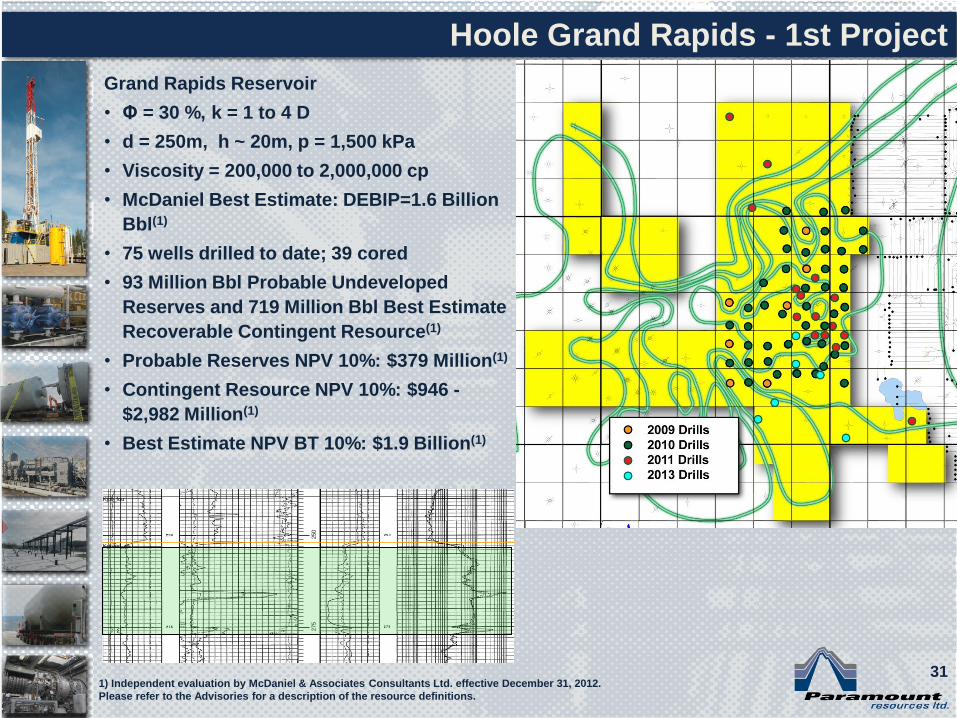

Grand Rapids Reservoir

• Φ = 30 %, k = 1 to 4 D

• d = 250m, h ~ 20m, p = 1,500 kPa

• Viscosity = 200,000 to 2,000,000 cp

• McDaniel Best Estimate: DEBIP=1.6 Billion

Bbl(1)

• 75 wells drilled to date; 39 cored

• 93 Million Bbl Probable Undeveloped

Reserves and 719 Million Bbl Best Estimate

Recoverable Contingent Resource(1)

• Probable Reserves NPV 10%: $379 Million(1)

• Contingent Resource NPV 10%: $946 -

$2,982 Million(1)

• Best Estimate NPV BT 10%: $1.9 Billion(1)

Hoole Grand Rapids - 1st Project

31 1) Independent evaluation by McDaniel & Associates Consultants Ltd. effective December 31, 2012.

Please refer to the Advisories for a description of the resource definitions.

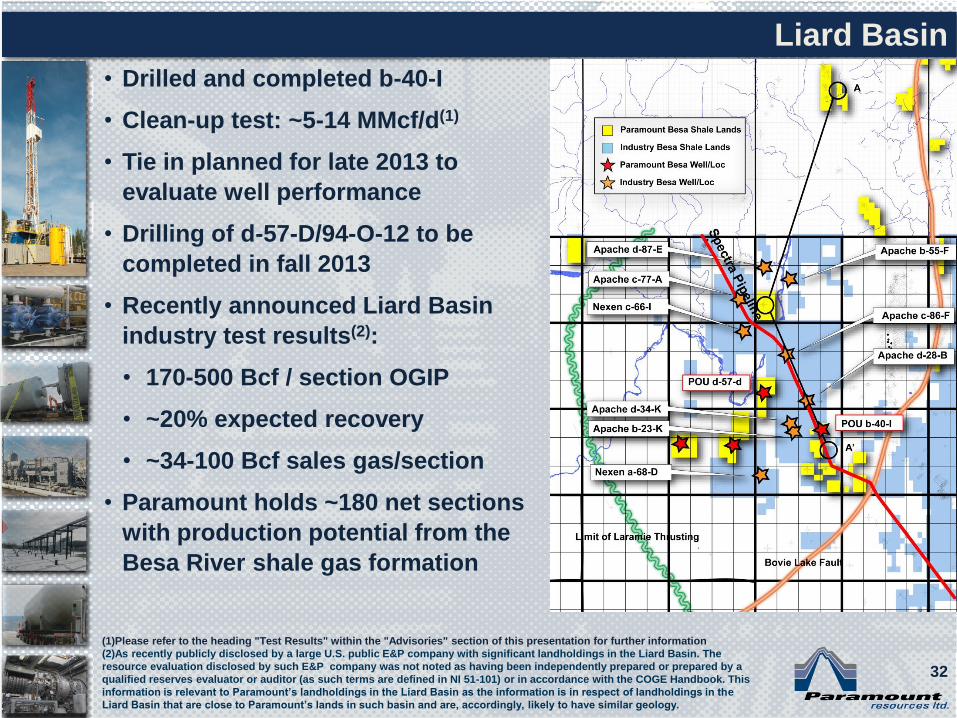

• Drilled and completed b-40-I

• Clean-up test: ~5-14 MMcf/d(1)

• Tie in planned for late 2013 to

evaluate well performance

• Drilling of d-57-D/94-O-12 to be

completed in fall 2013

• Recently announced Liard Basin

industry test results(2):

• 170-500 Bcf / section OGIP

• ~20% expected recovery

• ~34-100 Bcf sales gas/section

• Paramount holds ~180 net sections

with production potential from the

Besa River shale gas formation

Liard Basin

(1)Please refer to the heading "Test Results" within the "Advisories" section of this presentation for further information

(2)As recently publicly disclosed by a large U.S. public E&P company with significant landholdings in the Liard Basin. The

resource evaluation disclosed by such E&P company was not noted as having been independently prepared or prepared by a

qualified reserves evaluator or auditor (as such terms are defined in NI 51-101) or in accordance with the COGE Handbook. This

information is relevant to Paramount’s landholdings in the Liard Basin as the information is in respect of landholdings in the

Liard Basin that are close to Paramount’s lands in such basin and are, accordingly, likely to have similar geology.

32

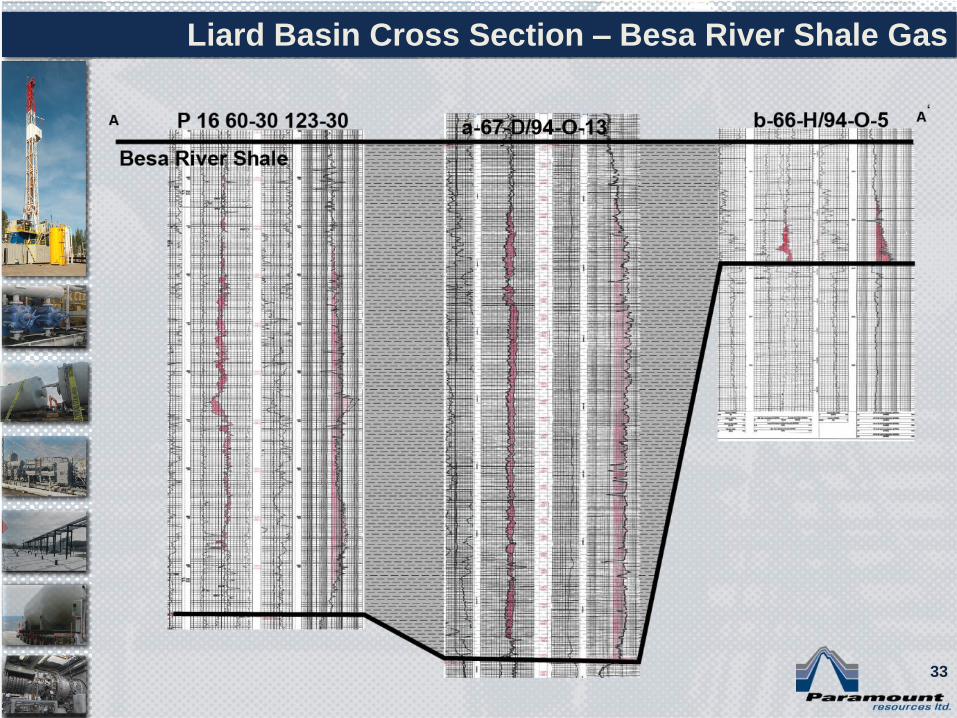

Liard Basin Cross Section – Besa River Shale Gas

33

33

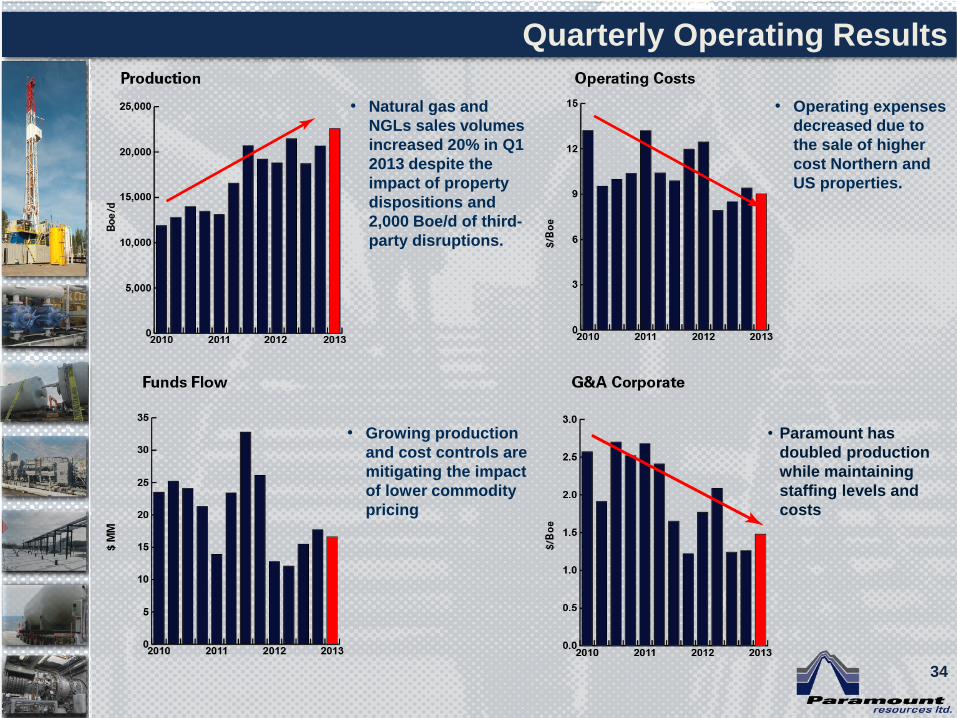

Quarterly Operating Results

• Natural gas and

NGLs sales volumes

increased 20% in Q1

2013 despite the

impact of property

dispositions and

2,000 Boe/d of third-

party disruptions.

• Growing production

and cost controls are

mitigating the impact

of lower commodity

pricing

• Operating expenses

decreased due to

the sale of higher

cost Northern and

US properties.

• Paramount has

doubled production

while maintaining

staffing levels and

costs

34

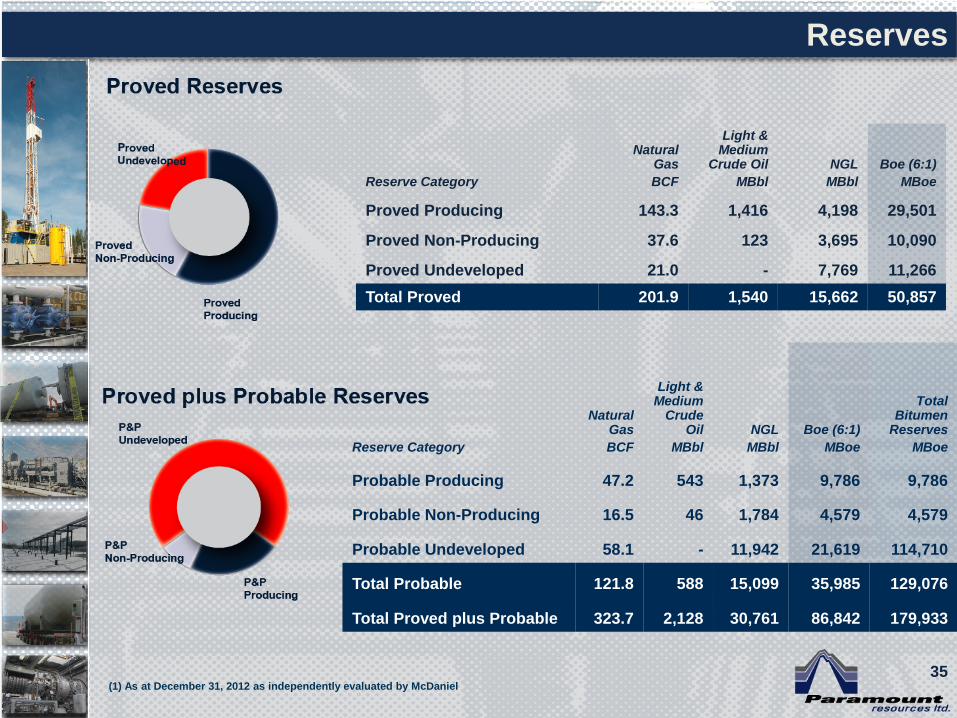

Reserves

Reserve Category

Natural Gas

BCF

Light & Medium

Crude Oil

MBbl

NGL

MBbl

Boe (6:1)

MBoe

Proved Producing 143.3 1,416 4,198 29,501

Proved Non-Producing 37.6 123 3,695 10,090

Proved Undeveloped 21.0 - 7,769 11,266

Total Proved 201.9 1,540 15,662 50,857

Reserve Category

Natural Gas

BCF

Light & Medium

Crude Oil

MBbl

NGL

MBbl

Boe (6:1)

MBoe

Total Bitumen

Reserves

MBoe

Probable Producing 47.2 543 1,373 9,786 9,786

Probable Non-Producing 16.5 46 1,784 4,579 4,579

Probable Undeveloped 58.1 - 11,942 21,619 114,710

Total Probable 121.8 588 15,099 35,985 129,076

Total Proved plus Probable 323.7 2,128 30,761 86,842 179,933

35 (1) As at December 31, 2012 as independently evaluated by McDaniel

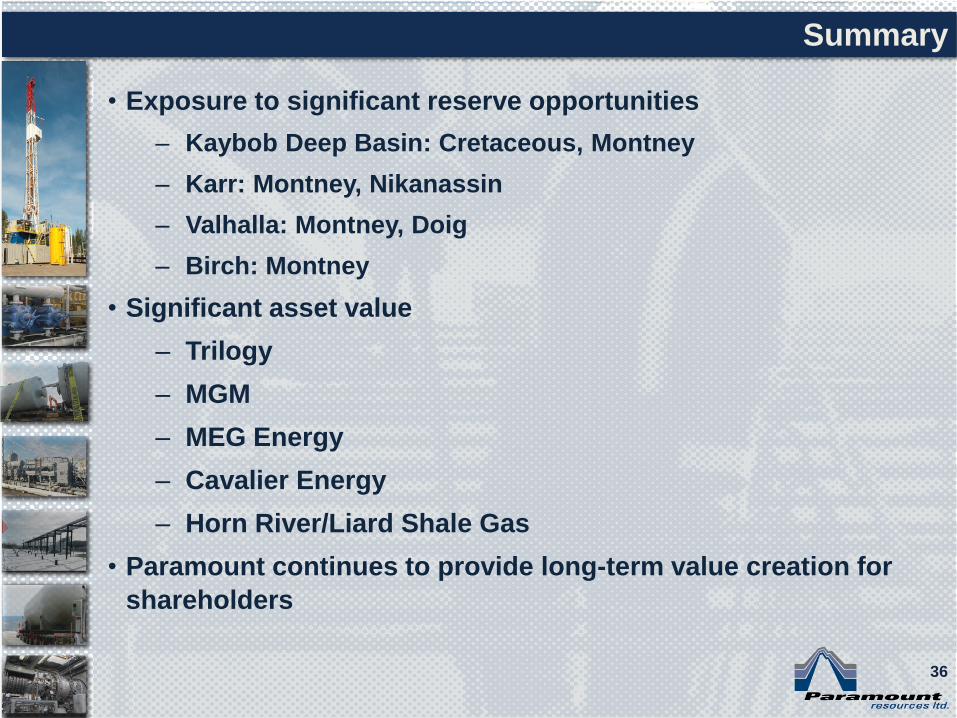

• Exposure to significant reserve opportunities

– Kaybob Deep Basin: Cretaceous, Montney

– Karr: Montney, Nikanassin

– Valhalla: Montney, Doig

– Birch: Montney

• Significant asset value

– Trilogy

– MGM

– MEG Energy

– Cavalier Energy

– Horn River/Liard Shale Gas

• Paramount continues to provide long-term value creation for

shareholders

Summary

36

4700 Bankers Hall West

888 Third Street S.W.

Calgary, Alberta

Canada T2P 5C5

Telephone: (403) 290-3600

Facsimile: (403) 262-7994

www.paramountres.com

42