Embed Size (px)

Citation preview

NAL Resources Management Limited

EPAC Oil & Gas Investor Showcase

June 12, 2013

Disclaimers

2

• Forward Looking Statements

• This document contains statements that constitute “forward-looking information” within the meaning of applicable securities legislation as to NAL

Resources Management Limited (“NAL’s”) internal projections, expectations and beliefs relating to future events or future performance. This forward-

looking information includes, among others, statements regarding: NAL’s strategic focus, business strategy and plans and budgets; business plans for

drilling, exploration and development, including drilling locations; estimates of production and operations performance; forecasted commodity price

estimates of future sales; estimated amounts, allocation and timing of capital expenditures; estimates of operating costs and unit operating costs; the

estimated timing and results of new development programs; estimates of anticipated funds from operations, cash flow, netbacks, dividends, working

capital and debt levels; estimated rates of return; the anticipated results of NAL’s divestiture program; various tax matters related to NAL; NAL’s

hedging program; NAL’s prospect inventory; and other expectations, beliefs, plans, goals, objectives, assumptions, information and statements about

possible future events, conditions, results of operations or performance.

• Various assumptions were used in drawing the conclusions or making the forecasts and projections contained in the forward-looking information

contained in this presentation including, without limitation, with respect to commodity prices, interest rates, exchange rates, royalty rates, general

and administrative expenses, the success of NAL's drilling programs and the production profile of NAL's oil and natural gas reserves. Forward-looking

information is based on current expectations, estimates and projections that involve a number of risks, which could cause actual results to vary and in

some instances to differ materially from those anticipated by NAL and described in the forward-looking information contained in this document. Undue

reliance should not be placed on forward-looking information. The material risk factors include, but are not limited to: the risks of the oil and gas

industry, such as operational risks in exploring for, developing and producing oil and natural gas, market demand and unpredictable facilities outages;

risks and uncertainties involving the geology of oil and gas deposits; the uncertainty of estimates and projections relating to production, costs and

expenses; potential delays or changes in plans with respect to exploration or development projects or capital expenditures; risk that adequate pipeline

capacity to transport oil and natural gas to market may not be available; fluctuations in oil and gas prices, foreign currency exchange rates and interest

rates; the outcome and effects of any future acquisitions and dispositions; safety and environmental risks; uncertainties as to the availability and cost

of financing and changes in capital markets; competitive actions of other industry participants; changes in general economic and business conditions;

the possibility that government policies or laws may change or governmental approvals may be delayed or withheld; changes in tax laws; changes in

royalty rates; the results of NAL’s risk mitigation strategies, including insurance; and NAL’s ability to implement its business strategy. Readers are

cautioned that the foregoing list of risk factors is not exhaustive.

• Forward-looking information is based on the estimates and opinions of NAL’s management at the time the information is released.

• Boe Conversion

• All dollar amounts in Canadian dollars, unless otherwise stated.

3

Our Strategic Focus

Maximizing Value

From Existing Assets

and New Acquisitions

Establish Additional

Partnerships

Attract Investors for

Direct Investment

Continue to Grow

Manulife’s Business

Invest an additional

$2-3B in WCSB over

next five years

Entry into the US

Entry into mid-

stream sector

Operational JV

partnerships

Exploration JV

partnerships

Farm-ins / Farm-

outs

Allows direct

ownership in assets

Provides on-the-

ground management

Manulife prepared to

co-invest

4

Who We Are

Who

We Are

What

We Do

Areas of

Focus

Western Canadian convention upstream oil &

gas company

20+ years experience managing private assets

Subsidiary of Private Asset Management arm

of Manulife

Find, buy, exploit and produce oil & gas

assets in a cost effective and efficient

manner

Provide an investment vehicle for investors

who do not have on-the-ground management

capacity

Key areas include Central Alberta,

Plenty/Dodsland and SE Saskatchewan

Mandate to acquire and manage U.S. assets

Our Relationship with Manulife

Private Asset Management (PAM)

5

•Dedicated investment group with over 30 years of experience

•On-site management of virtually all of our properties

Real Estate

•World’s largest manager of institutional timber assets

•Manage timberland assets on three continents

Timberland

•Manages farmland in the U.S., Canada, and Australia

Farmland

•20+ years of experience

•Owner/operator of oil & gas properties for private investors

Oil & Gas

•Over 20 years of experience

•Manage mezzanine strategies

Private Equity & Mezzanine

•Active in commercial mortgages since 1887

•Private placement bonds

Alternative Fixed Income

PAM’s Assets Under Management (AUM) exceeds C$85 billion

NALRM is PAM’s best performing asset over the past 10 years

6

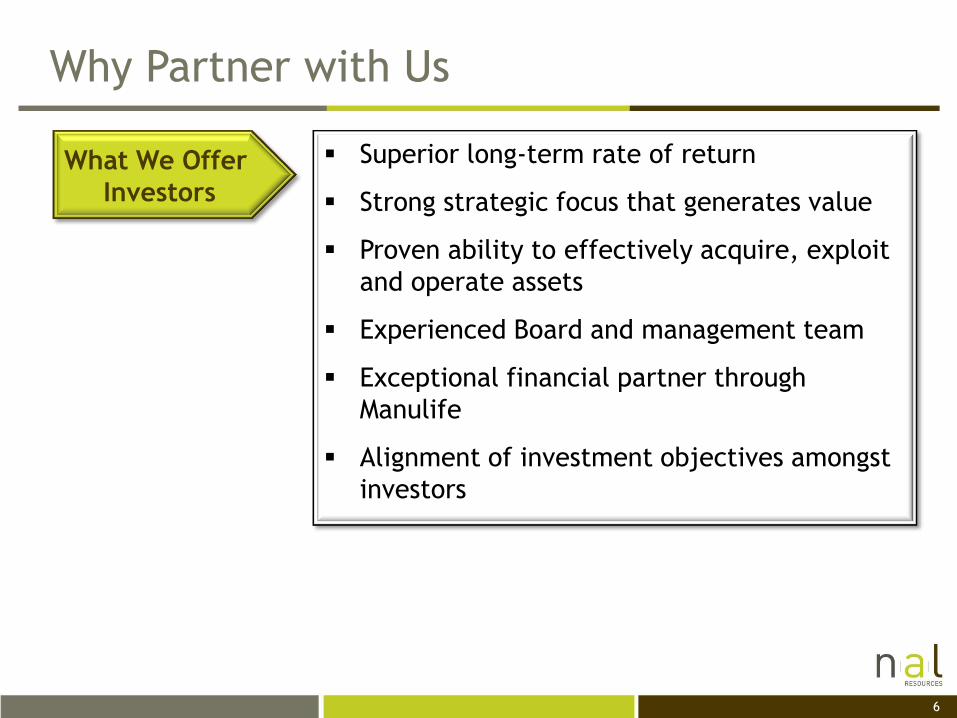

What We Offer

Investors

Superior long-term rate of return

Strong strategic focus that generates value

Proven ability to effectively acquire, exploit

and operate assets

Experienced Board and management team

Exceptional financial partner through

Manulife

Alignment of investment objectives amongst

investors

Why Partner with Us

7

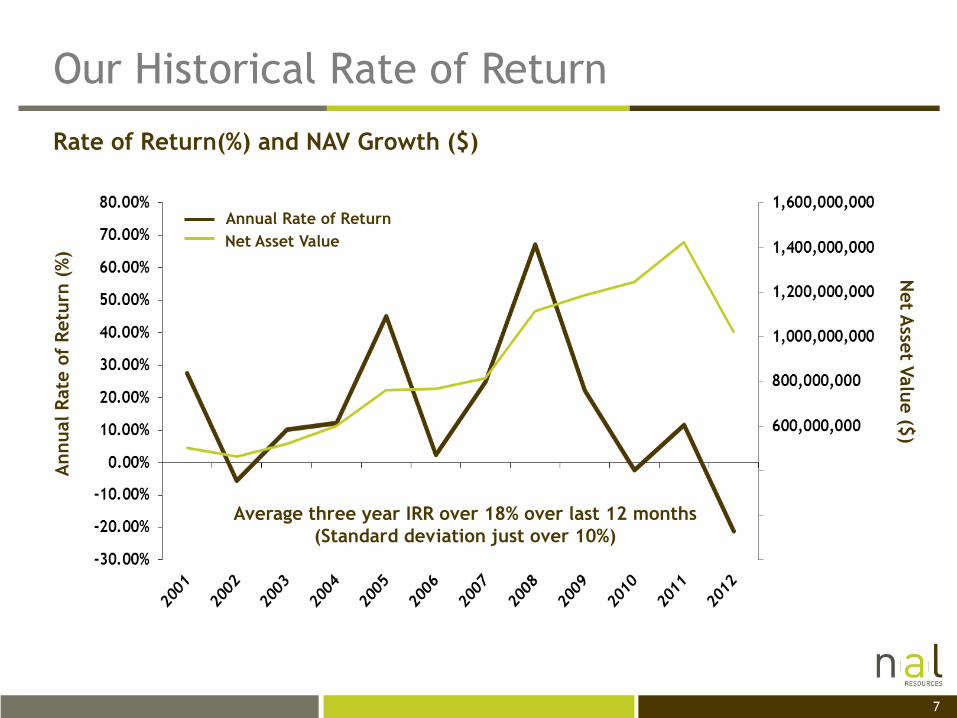

Our Historical Rate of Return

Rate of Return(%) and NAV Growth ($)

Average three year IRR over 18% over last 12 months

(Standard deviation just over 10%)

Annual Rate of Return

Net Asset Value

Annual R

ate

of

Retu

rn (

%)

Net A

sset V

alu

e ($

)

8

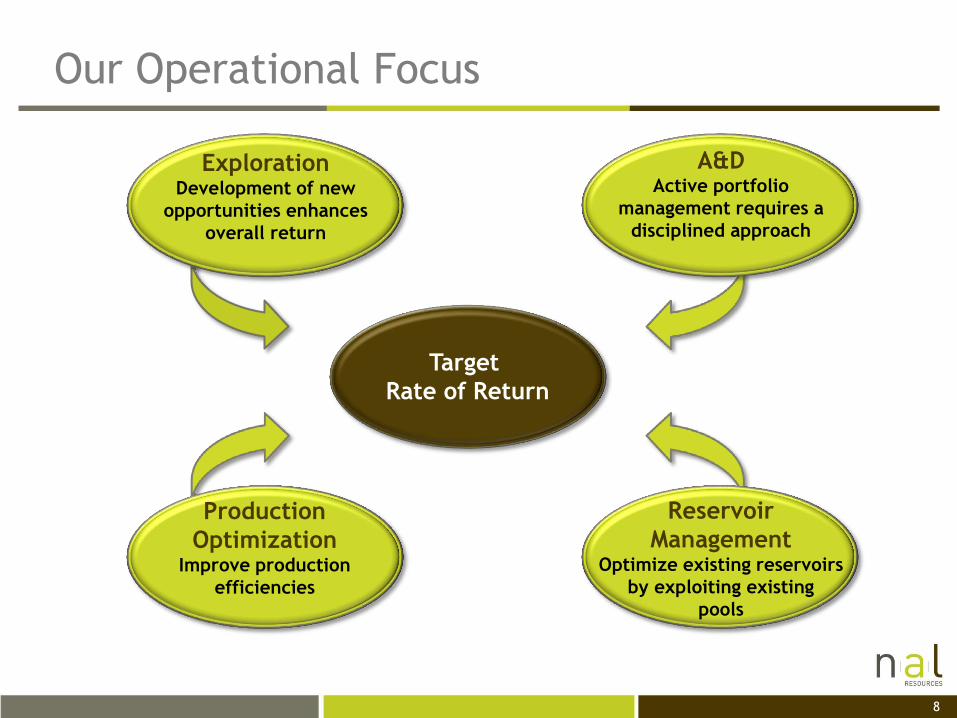

Our Operational Focus

Exploration Development of new

opportunities enhances

overall return

A&D Active portfolio

management requires a

disciplined approach

Production

Optimization Improve production

efficiencies

Reservoir

Management Optimize existing reservoirs

by exploiting existing

pools

Target

Rate of Return

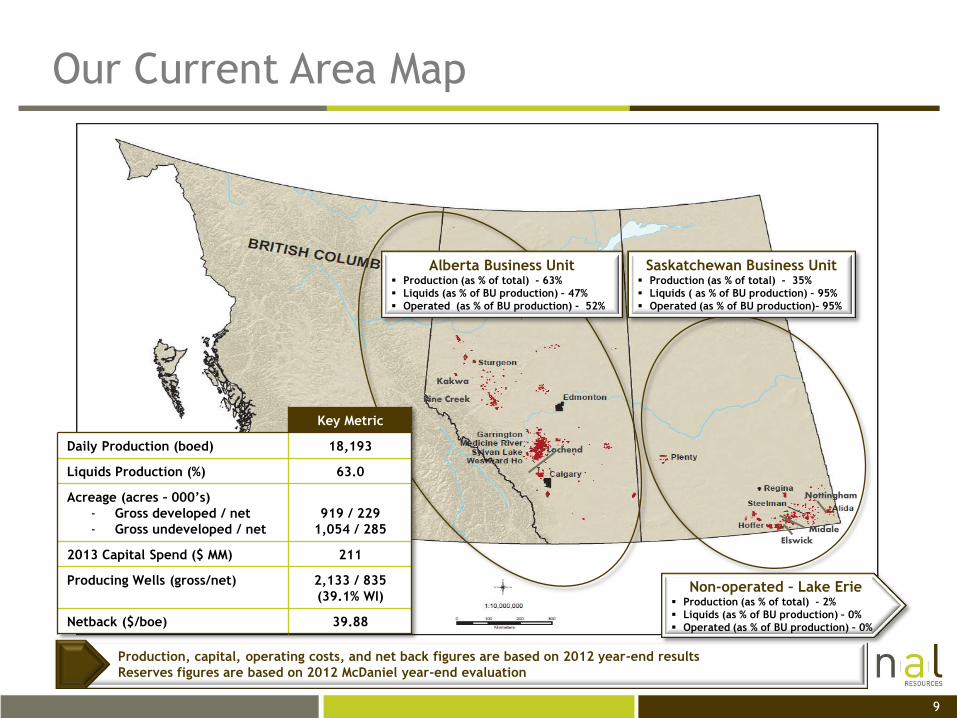

Our Current Area Map

Alberta Business Unit Production (as % of total) - 63%

Liquids (as % of BU production) – 47%

Operated (as % of BU production) - 52%

Saskatchewan Business Unit Production (as % of total) - 35%

Liquids ( as % of BU production) – 95%

Operated (as % of BU production)– 95%

Production, capital, operating costs, and net back figures are based on 2012 year-end results

Reserves figures are based on 2012 McDaniel year-end evaluation

Non-operated – Lake Erie Production (as % of total) - 2%

Liquids (as % of BU production) – 0%

Operated (as % of BU production) – 0%

Pine Creek

Lochend

Elswick Midale

Nottingham

9

Kakwa

Key Metric

Daily Production (boed) 18,193

Liquids Production (%) 63.0

Acreage (acres – 000’s)

- Gross developed / net

- Gross undeveloped / net

919 / 229

1,054 / 285

2013 Capital Spend ($ MM) 211

Producing Wells (gross/net) 2,133 / 835

(39.1% WI)

Netback ($/boe) 39.88

10

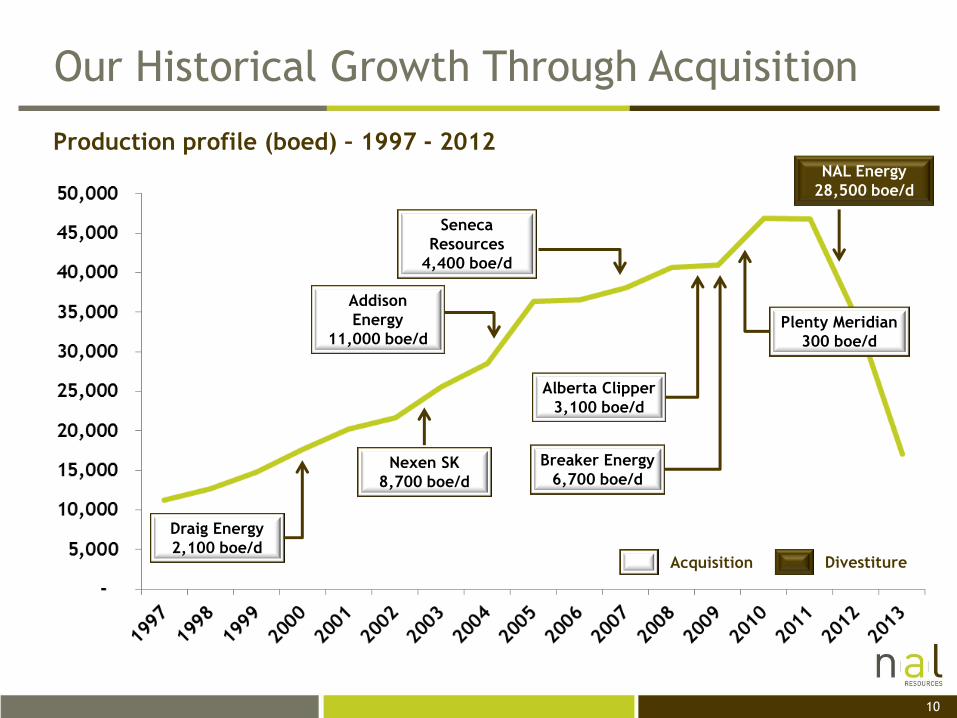

Our Historical Growth Through Acquisition

Production profile (boed) – 1997 - 2012

Plenty Meridian

300 boe/d

Breaker Energy

6,700 boe/d

Alberta Clipper

3,100 boe/d

Seneca

Resources

4,400 boe/d

Addison

Energy

11,000 boe/d

Nexen SK

8,700 boe/d

Draig Energy

2,100 boe/d

NAL Energy

28,500 boe/d

Acquisition Divestiture

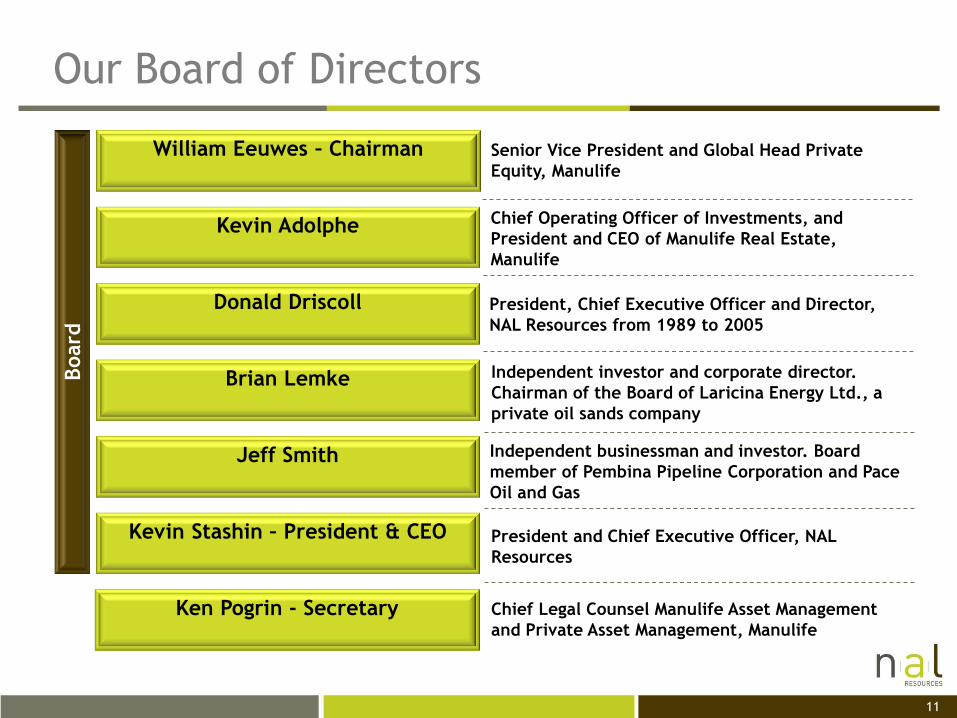

Chief Operating Officer of Investments, and

President and CEO of Manulife Real Estate,

Manulife

11

Our Board of Directors Board

William Eeuwes – Chairman

Donald Driscoll

Brian Lemke

Kevin Adolphe

Senior Vice President and Global Head Private

Equity, Manulife

Jeff Smith

Ken Pogrin - Secretary

President, Chief Executive Officer and Director,

NAL Resources from 1989 to 2005

Independent businessman and investor. Board

member of Pembina Pipeline Corporation and Pace

Oil and Gas

Independent investor and corporate director.

Chairman of the Board of Laricina Energy Ltd., a

private oil sands company

Chief Legal Counsel Manulife Asset Management

and Private Asset Management, Manulife

Kevin Stashin – President & CEO

President and Chief Executive Officer, NAL

Resources

30 years

32 years

12

Our Senior Management Team Senio

r M

anagem

ent

Team

Kevin Stashin

President and CEO

Darcy Redding

Vice President, Operations

Keith Steeves

CFO

Paul Kunkel

Vice President, Finance

Cory Bergh

Vice President, Operations Accounting & IT

John Kanik

Director, Marketing

Angele Mullins

Director, Human Resources

20 years

19 years

Kevin Christie

Vice President, Exploration

20 years

25 years

36 years

19 years

Experience

13

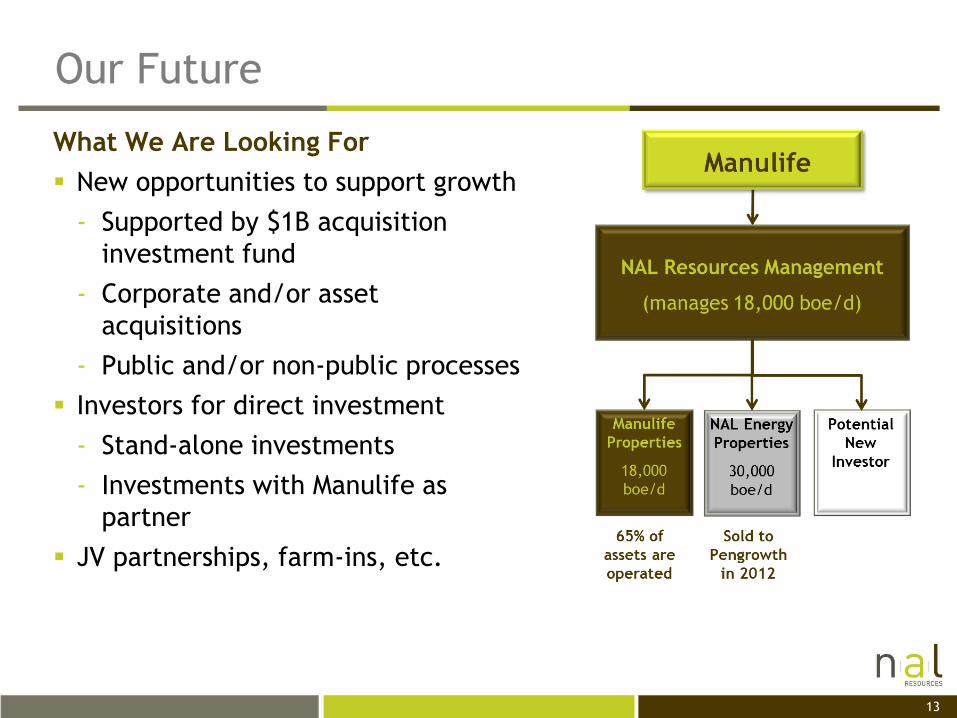

Our Future

What We Are Looking For

New opportunities to support growth

- Supported by $1B acquisition

investment fund

- Corporate and/or asset

acquisitions

- Public and/or non-public processes

Investors for direct investment

- Stand-alone investments

- Investments with Manulife as

partner

JV partnerships, farm-ins, etc.

Appendix

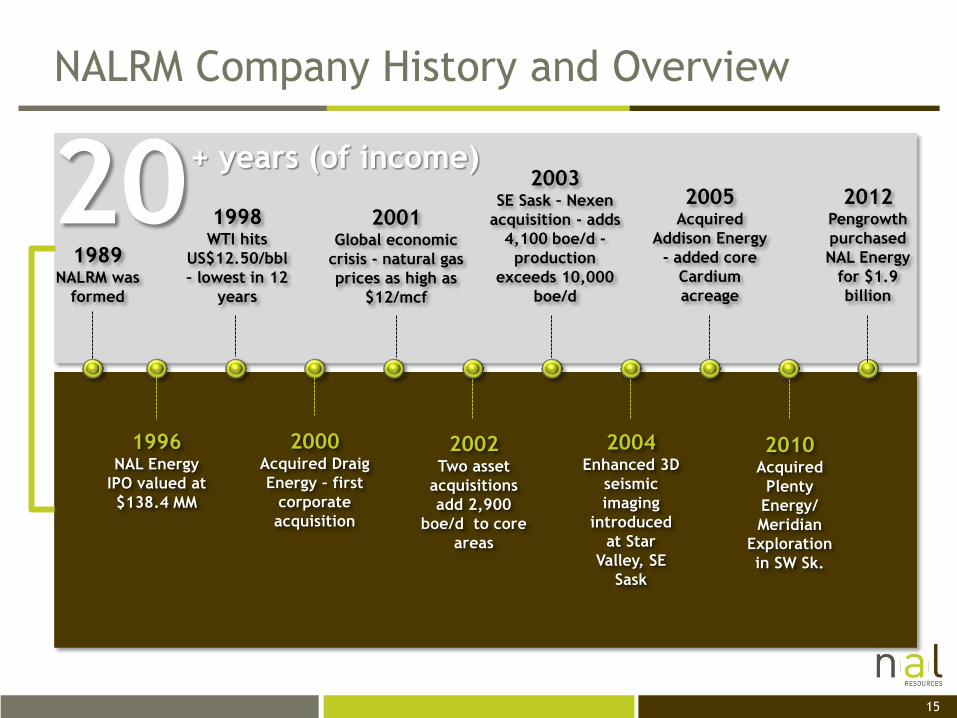

NALRM Company History and Overview

15

20 + years (of income)

1989 NALRM was

formed

1996 NAL Energy

IPO valued at

$138.4 MM

1998 WTI hits

US$12.50/bbl

– lowest in 12

years

2000 Acquired Draig

Energy – first

corporate

acquisition

2001 Global economic

crisis - natural gas

prices as high as

$12/mcf

2002 Two asset

acquisitions

add 2,900

boe/d to core

areas

2003 SE Sask – Nexen

acquisition - adds

4,100 boe/d -

production

exceeds 10,000

boe/d

2004 Enhanced 3D

seismic

imaging

introduced

at Star

Valley, SE

Sask

2005 Acquired

Addison Energy

- added core

Cardium

acreage

2010 Acquired

Plenty

Energy/

Meridian

Exploration

in SW Sk.

2012 Pengrowth

purchased

NAL Energy

for $1.9

billion

16

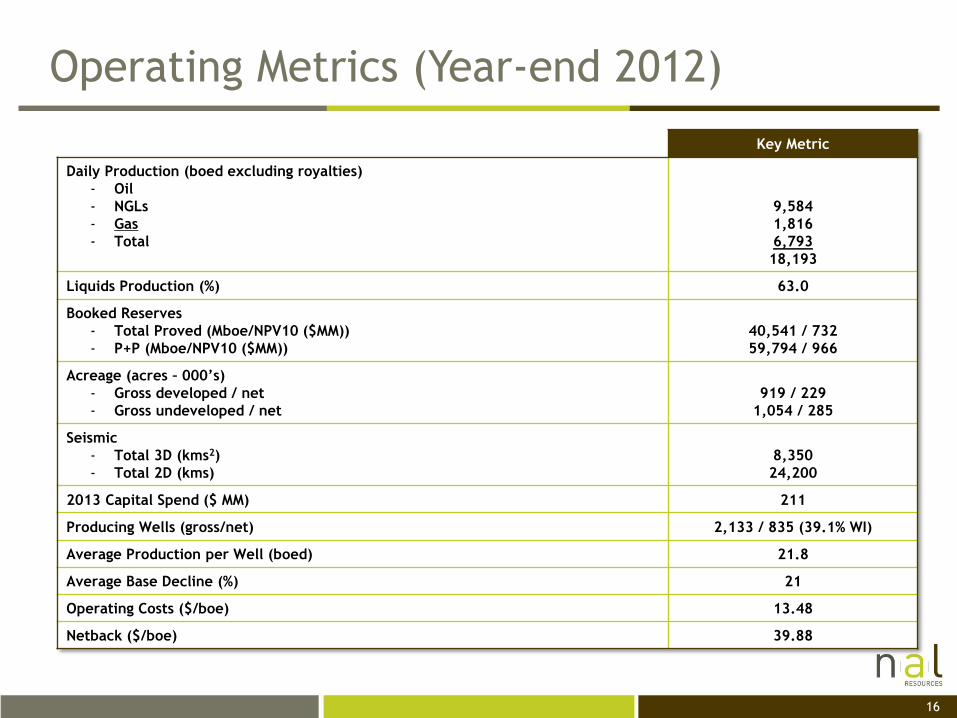

Operating Metrics (Year-end 2012)

Key Metric

Daily Production (boed excluding royalties)

- Oil

- NGLs

- Gas

- Total

9,584

1,816

6,793

18,193

Liquids Production (%) 63.0

Booked Reserves

- Total Proved (Mboe/NPV10 ($MM))

- P+P (Mboe/NPV10 ($MM))

40,541 / 732

59,794 / 966

Acreage (acres – 000’s)

- Gross developed / net

- Gross undeveloped / net

919 / 229

1,054 / 285

Seismic

- Total 3D (kms2)

- Total 2D (kms)

8,350

24,200

2013 Capital Spend ($ MM) 211

Producing Wells (gross/net) 2,133 / 835 (39.1% WI)

Average Production per Well (boed) 21.8

Average Base Decline (%) 21

Operating Costs ($/boe) 13.48

Netback ($/boe) 39.88