Embed Size (px)

Citation preview

49355201 Final Report May 2011

FINAL REPORT

ENVIRONMENTAL PROTECTION EXPENDITURE BY INDUSTRY: 2009 UK SURVEY

Department for Environment, Food and Rural Affairs

May 2011

Ref. 49355201

49355201 Final Report May 2011

The views and recommendations expressed in this report are those of the authors and do

not necessarily represent the views of the Department for Environment, Food and Rural

Affairs, its ministers or officials.

49355201 Final Report May 2011

Project Title: Environmental Protection Expenditure Survey by Industry 2009

Report Title: Environmental Protection Expenditure Survey by Industry 2009

Project Ref: 49355201

Status: Draft Report

Client Contact Name: Rocky Harris / Mohammad Ali

Client Company Name: Department for Environment, Food and Rural Affairs (Defra)

Issued By: URS Corporation Ltd

Document Production / Approval Record

Issue No: 1

Name Signature Date Position

Prepared by

Daniel Tuck

Laura Quinton

Consultant

Principal Consultant

Checked by

Kristelle Haslam

Project Manager

Approved by

Sally Vivian

Project Director

Document Revision Record

Issue No Date Details of Revisions

1 April 2011 First draft

2 May 2011 First revised

Final May 2011 Final draft

49355201 Final Report May 2011 i

TABLE OF CONTENTS

Page No

EXECUTIVE SUMMARY 1

1 INTRODUCTION 8 1.1 OBJECTIVES 8 1.2 DEFINITION OF ENVIRONMENTAL PROTECTION EXPENDITURE 9 1.3 SURVEY SCOPE AND BACKGROUND 9 1.4 REPORT STRUCTURE 10

2 SURVEY METHODOLOGY 12 2.1 MODIFICATIONS INTRODUCED IN THE 2009 SURVEY 13 2.2 SAMPLING METHODOLOGY 14 2.3 DATABASE DESIGN 14

3 CONDUCTING THE SURVEY 16 3.1 Methodology 16 3.2 TOP COMPANY FOCUS 17

3.2.1 Additional findings from the Top Company follow-up 17 3.3 HELPDESK SUPPORT 18

4 ANALYSIS OF RESPONSES 19 4.1 Response Rates 19

4.1.1 Weighted Response Rates 19 4.1.2 Response Bias 20

4.2 Methodology 20 4.3 Survey Completion Time 21

5 SURVEY RESULTS AND ANALYSIS 22 5.1 Total expenditure 22 5.2 EXPENDITURE BY ENVIRONMENTAL MEDIA 23 5.3 EXPENDITURE BY INDUSTRY SECTOR 26 5.4 COST SAVINGS AND INCOME 26 5.5 ENVIRONMENTAL PROTECTION EXPENDITURE BY INDIVIDUAL SECTOR 29

5.5.1 SIC 05 to 09: Mining and Quarrying 29 5.5.2 SIC 10 - 12: Food Products and Beverages, and Tobacco Products 31 5.5.3 SIC 17 : Paper and Pulp 33 5.5.4 SIC 19: Coke & Refined Petroleum 36 5.5.5 SIC 24 -25 Basic & Fabricated Metals 38 5.5.6 SIC 20 & 21: Chemicals and Pharmaceuticals 40 5.5.7 SIC 35 & 36: Electricity, Gas and Water 43

5.6 DRIVERS FOR CAPITAL EXPENDITURE 46 5.7 ENVIRONMENTAL MANAGEMENT SYSTEMS 46

6 RECOMMENDATIONS FOR FUTURE SURVEY 48 6.1 GENERAL 48 6.2 SAMPLE FRAME 48 6.3 VALIDATION 48

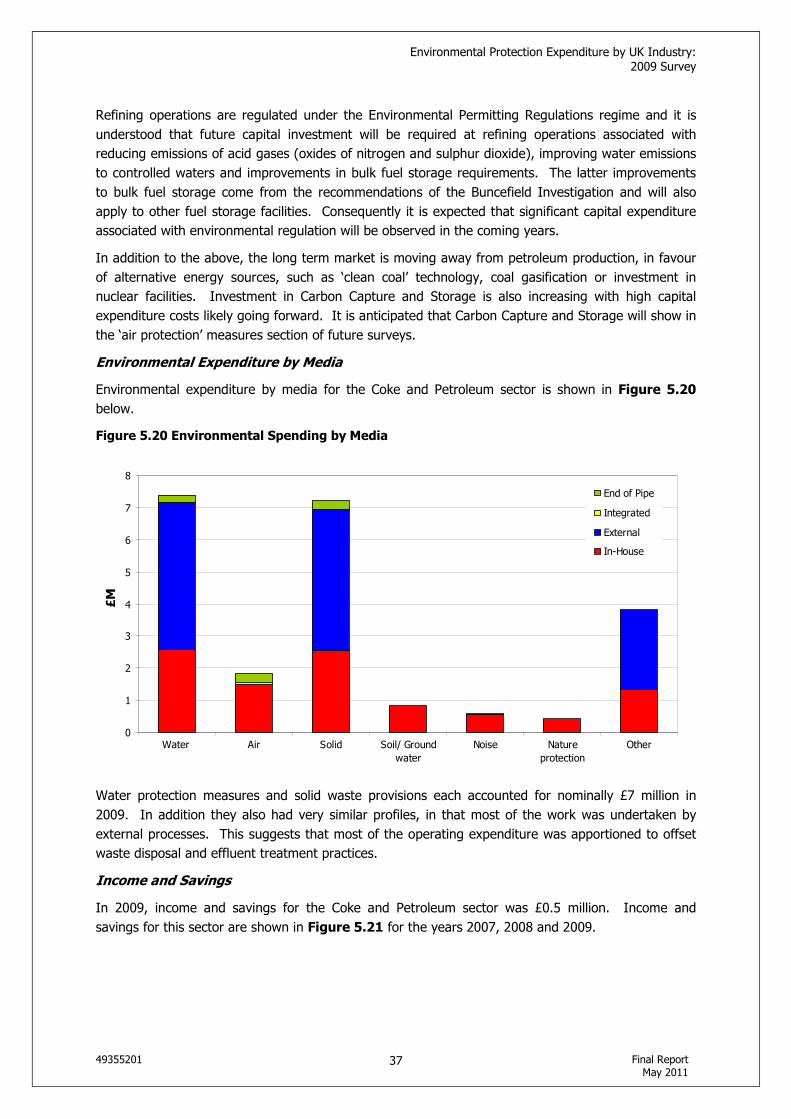

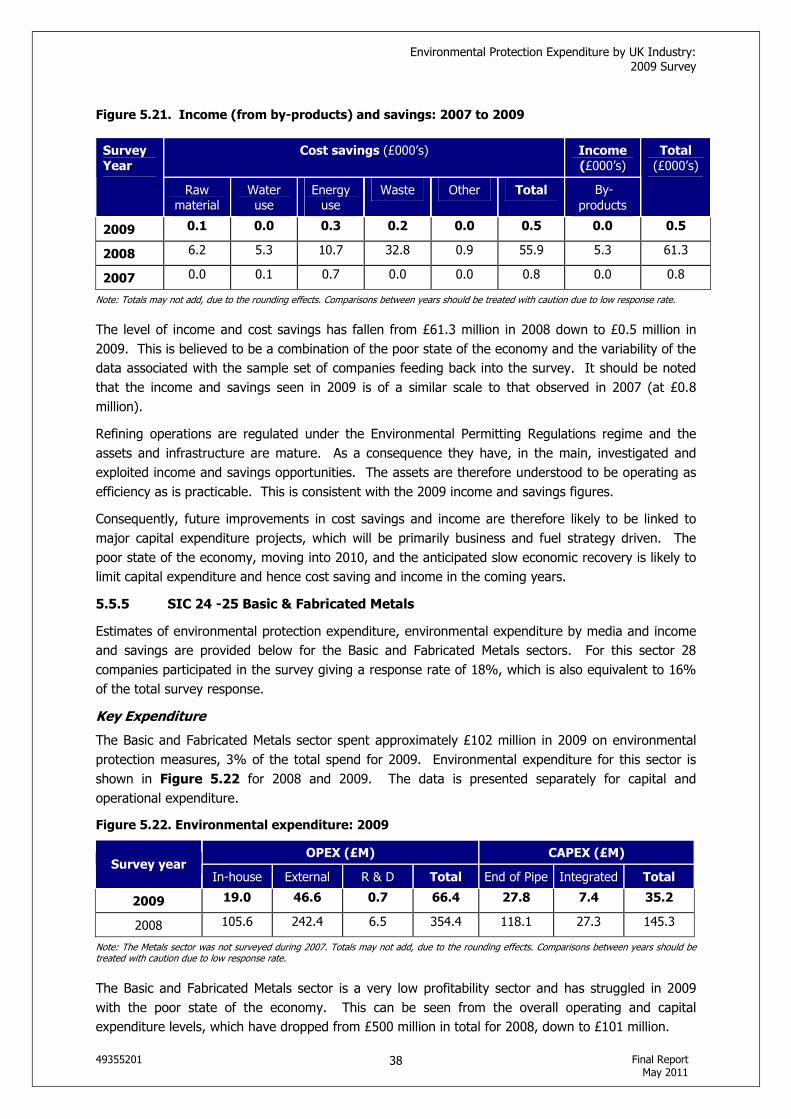

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 ii

6.3 ANALYSIS 49

ABBREVIATIONS & ACCRONYMS 50

49355201 Final Report 1 May 2011

EXECUTIVE SUMMARY

This report presents the findings of a research commissioned by the Department for Environment,

Food and Rural Affairs (Defra) and undertaken by URS Corporation Limited (URS), to estimate the

expenditure by UK industry on environmental protection in 2009.

The primary objectives of the study are:

• To provide Defra with annual estimates of environmental protection expenditure by UK

industry.

• To enable Defra to provide these estimates to the European Commission as required under

the EU Structural Business Statistics Regulation 58/97.

In addition to these broad objectives, annual data from the survey can be used to assess how

expenditure is changing and to compare the levels of expenditure of UK industries relative to those in

other EU countries. The data also enable companies and trade associations to benchmark their own

environmental spending against that of their sector and industry as a whole, both in the UK and the

EU. Furthermore, information on companies’ environmental expenditure and trends can be used to

support evidence based policy-making.

This is the thirteenth survey of this type; previous surveys were carried out in 1994 (a pilot survey),

1997, and annually between 1999 and 2008. The 2009 survey was conducted in three phases

between May 2010 and June 2011 and overseen by a steering group with representatives from Defra

and the Office for National Statistics (ONS).

Methodology

In 2009, the survey was provided to companies within the following Standard Industrial Classification

(SIC 2007) categories:

• Mining and Quarrying

• Food Products and Beverages and Tobacco Products

• Pulp and Paper

• Coke and Refined Petroleum

• Basic and Fabricated Metals

• Chemicals and Pharmaceuticals

• Electricity, Gas and Water

The UK Government’s Inter Departmental Business Register (IDBR) provided a stratified random

sample of 974 companies across these industries, who were invited to complete a postal or web

based questionnaire on a voluntary basis. The sampling procedure was designed to target sectors

where the expenditure was expected to be greatest, based on feedback and findings from previous

surveys. The total number of validated responses was 171, giving a valid response rate of 17.8 %.

The responses were subjected to a range of detailed validation checks.

The survey analysed the following expenditure patterns in UK industry:

• Operating expenditure (OPEX), which consists of in-house operating costs of a company’s own

environmental protection activities, and also payments to others for environmental protection

services including waste disposal.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 2

• Capital expenditure (CAPEX), which consists of ‘end of pipe’ investments (expenditure on

equipment to clean up at the end of the production process) and integrated investment

expenditure (expenditure on equipment which reduces or eliminates emissions and discharges as

part of the production process).

The following were also identified:

• Income and savings resulting from environmental protection activities carried out in 2009

• The environmental media (areas) affected by the spending, namely waste water, air, solid waste,

soil/groundwater, noise/vibrations and nature protection.

• The use of Environmental Management Systems

Key findings for 2009

The main findings from the 2009 survey are as follows:

• Gross spending on environmental protection in 2009 by UK industry for the selected sectors was

an estimated £3.3 billion.

• Operating expenditure (OPEX) accounted for 58% of the total environmental protection

expenditure, with capital expenditure (CAPEX) making up the remaining 42%.

• The greatest operating spend comprised water protection measures accounting for 46% of total

environmental OPEX, followed by solid waste at 20% of total operating cost.

• Spend on wastewater accounted for 69% of total CAPEX, followed by air protection measures

with a 22% share of total CAPEX spend.

• This spending was offset by an estimated income from the sale of by-products of £17.5 million

and an estimated overall cost saving of £146 million.

• Of the industry sectors covered in the 2009 survey, the primary spending sector was, by far, the

Electricity, Gas, and Water sector (81% of total expenditure). Followed by Food Products and

Beverages and Tobacco Products with 10% share of total expenditure in 2009.

• In 2009, 81% of surveyed companies had implemented an environmental management system

(EMS). Of the EMS in place, 63% were ISO14001 certified, 37% were certified to another

recognised standard (e.g. BRC Global, BS8555), and the remaining 19% were not certified.

Year-on-year comparisons

Direct comparisons between survey years should not be made, due to the following reasons:

• The most important difference between the 2008 and 2009 surveys and previous surveys is the

SIC used; SIC 2007 was used to group 2008 and 2009 datasets, whilst previous survey data were

grouped using SIC 2003. While 2008 and 2009 survey methodology is broadly consistent with

that of the 2007 survey, there are a small number of companies which are reclassified into a

different main SIC grouping under the new classification.

• In addition, the coverage of the 2007, 2008 and 2009 surveys was restricted to a limited number

of industry sectors, which had previously been more comprehensive.

• Following a review of the survey methodology, outcomes and drivers in 2006, a number of

changes were made to the survey design and layout for subsequent surveys. The key change was

a reduction in the sample size and specific targeting of key sectors for the annual survey with a

more comprehensive survey on a four yearly basis.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 3

• It is possible for one company’s expenditure to affect the final figure to a considerable degree; an

individual company may make a large “one-off” investment during the active survey period and

then return a small or even a zero response in the following survey. This variability along with the

smaller sample frame has led to larger confidence intervals during the reduced surveys in 2007,

2008 and 2009.

The 2007 survey did not include basic & fabricated metal sector, which was included in 2008 and

2009 surveys. Furthermore, the change to SIC 2007 may have affected the results. In light of this,

the following charts include confidence ranges as well as absolute figures for total spending reported

in 2007, 2008 and 2009.

A summary of total expenditure between 2007 and 2009 is presented in Figure E1.

Figure E1. Summary of environmental protection expenditure by UK businesses: 2007 to 2009

2009 2008 2007

Total expenditure (£M)

% of gross

Total expenditure (£M)

% of gross

Total expenditure (£M)

% of gross

Capital expenditure

End of pipe 947

(92 – 1,802)

29 652

(11 – 1,294)

20 185

(33 – 337)

6

Integrated processes 443

(0 – 918)

13 790

(29 – 1,551)

24 522

(0 – 1,139)

16

Sub-Total 1,389

(259 – 2,519)

42 1,442

(420 – 2,465)

45 707

(59 – 1,356)

21

Operational expenditure

In-house 1,222

(318 – 2,126)

37 606

(237 – 974)

19 811

(105 – 1,518)

24

External 628

(212 – 1,044)

19 1,065

(217 – 1,913)

33 1,709

(804 – 2,614)

51

R&D 72

(0 – 177)

2 118

(0 – 275)

4 116

(0 – 301)

3

Sub-Total 1,922

(935 – 2,909)

58 1,788

(779 – 2,797)

55 2,636

(1416 – 3,857)

79

Gross expenditure

Total gross spend 3,311

(1,600 – 5,022)

100 3,231

(1,368 – 5,093)

100 3,344

(1,814 – 4,873)

100

By-products income 18

(0 – 42)

1 11

(0 - 22)

0 104

(0 – 275)

3

Total net expenditure

3,293

(1,559 – 5,027)

- 3,220

(1,357 – 5,082)

- 3,239

(1,700 – 4,778))

-

Total cost savings 146 - 106 - 94 -

Note: Comparisons between years should be treated with caution.

End-of-pipe Capex shows an increase, but a larger decrease for integrated processes has resulted in

an overall decrease for total Capex. An increase in end of pipe expenditure may have resulted due to

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 4

process operators focussing their budget and spend on emissions abatement as apposed to investing

in new process / production plant and equipment due to economic uncertainty.

Total Opex has increased compared to 2008, with a shift in expenditure to in-house services and

away from external parties, but with a decrease in R&D spend. This shift may be attributed to less

outsourcing / buying in of services and more internal maintenance of equipment and an increase in

internal training, so having the in-house expertise as appose to needing to use a third party; together

with an increased focus on resource efficiency, including waste and water minimisation resulting in a

reduction in the disposal costs associated with solid and liquid waste and wastewater. The decrease

in research and development (R&D) spend may also be linked to economic uncertainty.

Cost savings show an increase which can be associated with campaigns and efforts associated with

resource efficiency, including waste and water minimisation, product reworking / reuse. The increase

in by-product revenue may be associated with Environment Agency/WRAP quality protocols end of

waste criteria being developed and Environment Agency Regulatory Position Statements providing

regulatory clarification on, if and when, a waste ceases to be a waste.

Industrial symbiosis may also have contributed to the by-product revenue increase, bringing together

separate industries and organisations from all business sectors with the aim of improving cross

industry resource efficiency and sustainability; for example involving the physical exchange of

materials and/or by-products.

A breakdown of total expenditure by key industry sectors between 2007 and 2009 is presented in

Figure E21.

Figure E2. Total environmental expenditure by industry sector: 2007 to 2009.

0

10

20

30

40

50

60

70

80

90

Min

ing a

nd

Quarr

yin

g

Food,

Bevera

ges

& T

obacco

Paper

Pro

ducts

Coke &

Refined

Petr

ole

um

Basic

&

Fabricate

d

Meta

ls

Chem

ical and

Pharm

aceuticals

Ele

ctr

city,

Gas

and W

ate

r

Pro

po

rtio

n o

f T

ota

l S

pen

d (

%)

2007

2008

2009

1 It is important to note that basic and fabricated metals was not included in 2007, resulting in a zero value in

figure E2.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 5

Of the industry sectors covered in the 2009 survey, the primary spending sector was, by far, the

Electricity, Gas, and Water sector (81% of total expenditure). Followed by Food Products and

Beverages and Tobacco Products with 10% share of total expenditure in 2009.

Figures E3 and E4 show the expenditure across environmental media for operating and capital

expenditures between 2007 and 2009.

Figure E3. OPEX by environmental media: 2007 to 2009.

0

10

20

30

40

50

60

Water Air So lid Waste Soil/

Groundwater

No ise Nature Other

Media

Pro

po

rtio

n o

f T

ota

l S

pe

nd

(%

)

2007

2008

2009

Note: ‘Other’ includes, for instance, environmental regulatory charges.

Opex was the highest by media for water followed by solid waste. Water shows a large increase

compared to 2008 and ‘Other’ a large decrease, which may be associated with definition

interpretation, for example associated with site infrastructure/maintenance.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 6

Figure E4. CAPEX by environmental media: 2007 to 2009.

0

10

20

30

40

50

60

70

80

Water A ir Solid Waste Soil/

Groundwater

Noise Nature Other

Media

Pro

po

rtio

n o

f T

ota

l S

pen

d (

%)

2007

2008

2009

Note: ‘Other’ includes, for instance, environmental regulatory charges.

Capex was the highest by media for water followed by air, which were also the highest for end of

pipe and integrated expenditure, end of pipe being the larger amounts for both media; suggesting

larger investments in wastewater/aqueous wastes treatment, possibly associated with meeting

compliance limits and water reuse and recycling in on site processes; and air emissions abatement to

meet compliance limits and possibly associated with continuous automated monitoring equipment.

The continuing increase of capital expenditure on water is likely to be driven by legislation - primarily

permitting regulations (e.g. the Water Framework Directive, and the Environmental Permitting

Regulations) - which imposed increasingly stringent environmental standards for emissions to air, and

water and wastewater treatment, and have also extended to the industry sectors that are subject to

process-related regulation.

Environmental Management Systems

In 2009, 81% of surveyed companies had implemented an environmental management system

(EMS). Of the EMS in place, 63% were ISO14001 certified, 37% were certified to another recognised

standard (e.g. BRC Global, BS8555), and the remaining 19% were not certified.

Figure E5 presents the types of environmental management systems used by different industries,

i.e. and where ISO14001-certified EMS, an EMS certified to another recognised standard, or an

uncertified (‘in-house’) EMS.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011 7

Figure E5. Types of EMS by SIC Sector

20% 30% 40% 50% 60% 70% 80% 90% 100%

Mining & Quarrying

Food, Beverages & Tobacco

Paper & Pulp

Coke & Refined Petrol

Chemical & Pharmaceuticals

Basic & Fabricated Metals

Electricity, Gas & Water

EMS Percentage Uptake

ISO14001

non-ISO

Other

Companies in the Basic & Fabricated Metal and Electricity, Gas & Water sectors were most likely to

have an EMS in place (100%). Of the sectors surveyed, the former were most likely to have their own

in-house system, whilst the latter were most likely to have a certified EMS (100%).

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

8

1 INTRODUCTION

This report presents the results of the thirteenth annual survey commissioned by the Department for

Environment, Food and Rural Affairs (Defra) and undertaken by URS Corporation Limited (URS), to

estimate expenditure by UK industry on environmental protection in 2009. Previous surveys were

carried out in 1994 (a pilot survey), 1997, and from 1999 to 2008.

In 2009, the survey was distributed to total of 974 companies across the Mining and Quarrying; Food

Products and Beverages and Tobacco Products; Pulp and Paper; Coke and Refined Petroleum; Basic

and Fabricated Metals; Chemicals and Pharmaceuticals and the Electricity, Gas and Water sectors, as

defined by the UK Standard Industry Classifications for Business (SIC) in 2007.

The following sections of the report summarise analysis findings from the 2009 questionnaires

returned by participating UK companies. The 2009 data is presented alongside 2007 and 2008

Direct comparisons between survey years should not be made, due to the following reasons:

• The most important difference between the 2008 and 2009 surveys and previous surveys was the

change to the SIC used. The main classification system used to analyse the 2008 and 2009

datasets was SIC 2007, which is the latest system available reflecting the changes in the UK

industry. In previous years, the SIC 2003 system had been used; while the survey methodology

is kept consistent with the 2007 survey, there are a small number of companies which are

reclassified into a different main SIC grouping under the new classification. This is not thought to

affect the main results and comparisons with previous years should generally be possible.

• In addition, the coverage of the 2007, 2008 and 2009 surveys was restricted to a limited number

of industry sectors, which had previously been more comprehensive.

• Following a review of the survey methodology, outcomes and drivers in 2006, a number of

changes were made to the survey design and layout for subsequent surveys. The key change was

a reduction in the sample size and specific targeting of key sectors.

• The process of generating estimates of sectoral expenditure means that it is possible for one

company’s expenditure to affect the final figure to a considerable degree; it is possible that an

individual company may make a large “one-off” investment during the active survey period and

then return a small or even a zero response in the following survey. This variability along with the

smaller sample frame has led to larger confidence intervals during the reduced surveys in 2007,

2008 and 2009.

The 2007 survey did not include the Basic & Fabricated Metal sector, which was included in 2008 and

2009 surveys. Furthermore, the change to SIC 2007 may have affected the results. In light of these

issues, comparisons include confidence ranges for the total spending reported in each year, as well as

absolute figures. However, comparisons between years should still be treated with caution.

Further information regarding modifications and changes is provided in Section 2.1.

1.1 OBJECTIVES

The primary objectives of the study are:

• To provide Defra with the data from which annual estimates of environmental protection

expenditure by UK industry could be calculated; and

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

9

• To enable the UK Government to meet the requirements of the European Union (EU) Structural

Business Statistics Regulation 58/97, which provides a tool for regular data collection on the

variables and economic activities and is designed to give information on the service sector.

In addition to these broad objectives, annual data from the survey can be used to assess how

expenditure is changing and to compare the levels of expenditure of UK industries relative to other

EU countries. The data enable companies and trade associations to benchmark their own

environmental spending against that of the industry as a whole, both in the UK and the EU.

1.2 DEFINITION OF ENVIRONMENTAL PROTECTION EXPENDITURE

The Statistical Office of the European Community defines environmental protection expenditure as:

‘…the sum of capital and current expenditure on environmental protection activities.

Environmental protection is an action or activity (involving the use of equipment, labour,

manufacturing techniques and practices, information networks or products) where the main

purpose is to collect, treat, reduce, prevent, or eliminate pollutants and pollution or any other

degradation of the environment resulting from the activity of the company. Environmental

protection expenditure may relate to activities that generate marketable by-products, or results

in savings, or are financed by subsidies or capital allowances. In such cases, environmental

protection expenditure should be reported gross of any such cost offsets.’

Environmental protection expenditure includes: expenditure to reduce or prevent emission to air and

water; expenditure to protect or clean up soil and groundwater; expenditure to prevent noise and

vibration; and expenditure to reduce, treat and dispose of waste materials. Expenditure may be

operating expenditure (OPEX) or capital expenditure (CAPEX).

OPEX includes the operating costs of a company’s own environmental protection equipment and

services and also payments to others for environmental protection services (including waste

disposal and sewage treatment).

CAPEX consists of end-of-pipe expenditure and expenditure on integrated processes. End-of-

pipe capital expenditure is defined as expenditure on equipment used to treat, handle, measure or

dispose of emissions and wastes from production. Examples include effluent treatment plants,

exhaust air scrubbing systems and solid waste compactors.

CAPEX on integrated processes relates to new or modified production facilities designed to

integrate environmental protection into the production process. This might include adaptation of an

existing installation/process whereby the integrated expenditure is then the total purchase cost of the

adaptation. It also includes installing a new process in which the design takes environmental

protection into account. In this case, the expenditure counted is only the extra cost compared with

installing a less environmental friendly alternative.

Energy costs are not included in the definition of environmental protection expenditure, except where

energy is specifically used to run environmental protection equipment or services. Expenditure on

health and safety equipment or services is also excluded.

1.3 SURVEY SCOPE AND BACKGROUND

The current 2009 survey covers expenditure incurred during the financial year April 2009 to March

2010. In accordance with the EU Regulations, industries that have been surveyed are those in NACE2

2 NACE: General Industrial Classification of Economic Activities within the European Communities (the EC statistical office (Eurostat) classification scheme of economic activities).

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

10

sections C, D and E (extraction, manufacturing, energy and water supply). Therefore, in 2009, 974

companies were invited to participate in the survey, across the following industry sectors:

• Mining & Quarrying

• Food Products & Beverages, and Tobacco Products

• Pulp and Paper

• Coke & Refined Petroleum

• Basic & Fabricated Metals

• Chemicals & Pharmaceuticals

• Electricity, Gas & Water

Expenditure estimates are presented for the following:

• In-house and external operating costs (e.g. research and development, regulatory charges etc)

• End-of-pipe capital investments;

• Integrated or ‘clean’ technology capital investments

• Income and savings (e.g. the sale of environmental protection by-products)

This expenditure is also reported by the environmental media to which they relate, as shown below:

• Wastewater: Collection and transport of wastewater, the prevention or reduction in quantity of

wastewater and of substances in wastewater, the prevention of incidental water pollution, the

treatment of cooling water before draining to the surface or groundwater and monitoring of

surface water.

• Air: Prevention or reduction of gaseous, liquid or particulate emissions to the atmosphere, and

the monitoring of air emissions.

• Solid Waste: Prevention or reduction of waste, including the collection, transport, treatment and

disposal and monitoring of waste.

• Soil/groundwater: Decontamination of polluted soils and cleansing of polluted groundwater.

Includes the protection of soil and groundwater against pollution infiltration, monitoring of soil

and groundwater, and the transport and disposal of contaminated soil.

• Noise/vibration: Measures to decrease noise and vibration levels at source, to isolate receivers

from noise/vibration and the monitoring of levels. Protection of the workplace is excluded.

• Nature protection: Protection of species, landscapes and habitats; rehabilitation of damaged

landscapes due to past or current actions. Reforestation is included.

This survey succeeds the Defra surveys carried out in 1997 and 1999 to 2008, and research on

environmental protection expenditure in 1994 (pilot study). The reports from these surveys can be

downloaded at: http://www.defra.gov.uk/statistics/environment/environmental-survey/survey-results/

1.4 REPORT STRUCTURE

This report consists of the following sections:

Section 1 Introduction

Section 2 Survey Methodology and Preparation

Section 3 Conducting the Survey

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

11

Section 4 Analysis of Responses

Section 5 Survey Results and Analysis

Section 6 Recommendations for Future Surveys

This main report is supplemented by detailed annexes, which are presented as separate documents:

Annex 1 Survey, Technical Guidance Note and Cover Letters

Annex 2 Validation of Responses

Annex 3 Response Codes for Sorting Correspondence

Annex 4 Drivers behind Participation

Annex 5 Output of Data Analysis

Annex 6 Grossing-up Procedure

Annex 7 Method for Derivation of Standard Error and Confidence Intervals

The report and annexes can be downloaded from Defra’s website:

http://www.defra.gov.uk/statistics/environment/environmental-survey/survey-results/

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

12

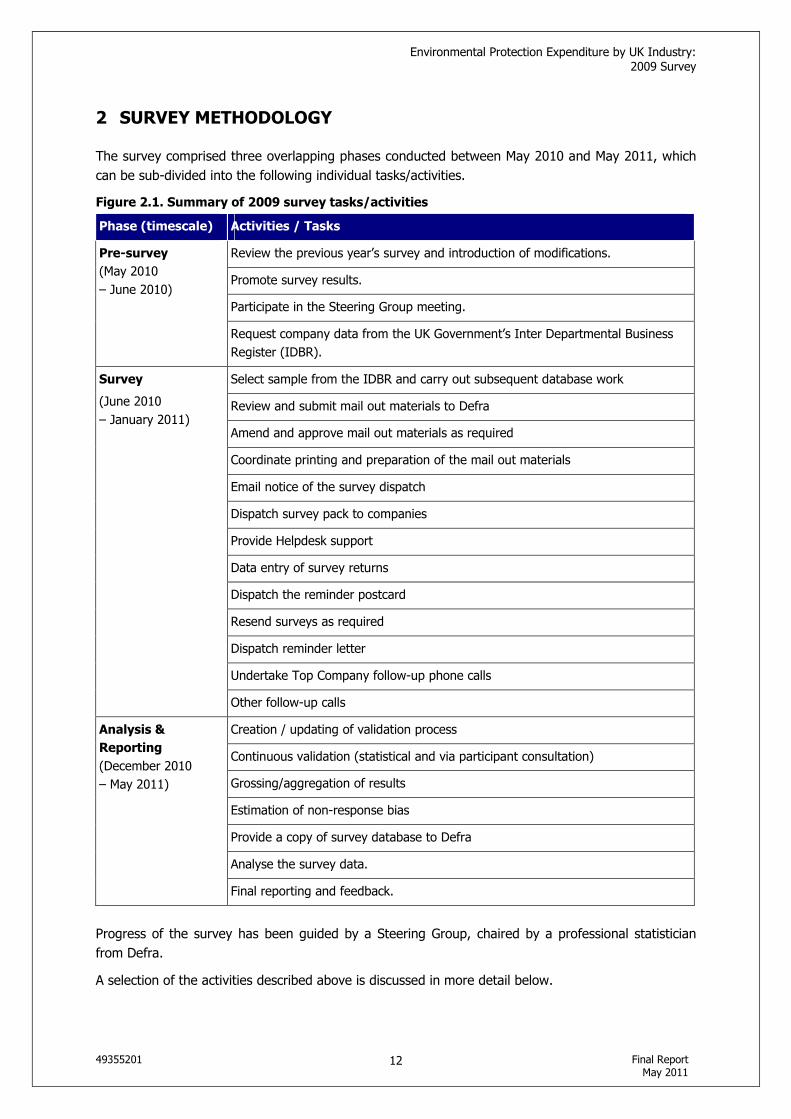

2 SURVEY METHODOLOGY

The survey comprised three overlapping phases conducted between May 2010 and May 2011, which

can be sub-divided into the following individual tasks/activities.

Figure 2.1. Summary of 2009 survey tasks/activities

Phase (timescale) Activities / Tasks

Review the previous year’s survey and introduction of modifications.

Promote survey results.

Participate in the Steering Group meeting.

Pre-survey

(May 2010

– June 2010)

Request company data from the UK Government’s Inter Departmental Business

Register (IDBR).

Select sample from the IDBR and carry out subsequent database work

Review and submit mail out materials to Defra

Amend and approve mail out materials as required

Coordinate printing and preparation of the mail out materials

Email notice of the survey dispatch

Dispatch survey pack to companies

Provide Helpdesk support

Data entry of survey returns

Dispatch the reminder postcard

Resend surveys as required

Dispatch reminder letter

Undertake Top Company follow-up phone calls

Survey

(June 2010

– January 2011)

Other follow-up calls

Creation / updating of validation process

Continuous validation (statistical and via participant consultation)

Grossing/aggregation of results

Estimation of non-response bias

Provide a copy of survey database to Defra

Analyse the survey data.

Analysis &

Reporting

(December 2010

– May 2011)

Final reporting and feedback.

Progress of the survey has been guided by a Steering Group, chaired by a professional statistician

from Defra.

A selection of the activities described above is discussed in more detail below.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

13

2.1 MODIFICATIONS INTRODUCED IN THE 2009 SURVEY

Several modifications that were introduced during previous surveys were carried through to the 2009

survey, which in particular sought to improve awareness, help with definition issues and widen

ownership of the survey. These include, for example, the following activities:

• Top Companies (specifically selected based on their employee number and turnover as well as if

they had responded to a number of previous surveys) received a slightly different cover letter to

the other recipients, which emphasised different issues.

• Prior to the launch of the survey, an e-mail was sent out to all companies that had responded to

the 2008 survey. The e-mail invited each company to participate in the survey and also to

provide information from the previous survey. This enabled the company to prepare for the

survey and provided the Helpdesk with the right contact details.

In addition, 2009 survey questions relating to environmental management systems (EMS) were

slightly amended to enable more comparable responses. Other minor modifications made to the

survey are described in the Figure 2.2 below.

Figure 2.2 Changes to the 2009 Questionnaire Design

Section / Question Modification

Instructions Helpdesk email address Email address simplified to [email protected]

Contact details

Company name Space added for respondents to specify the company name.

Contact details

Company reference number

Company reference number added to ‘Contact Details’ section.

1.1 (a) In-house operating costs

Narrative added to remind respondents not to include wages and bills etc.

1.1 (a) In-house operating costs

Title amended to ‘In-House Environmental Operating Costs’.

1.2 Operating costs paid to external organisations

Boxes B and C indicated as ‘minimum responses”, and the information for them can be found on waste and water bills.

1.2 Operating costs paid to external organisations

Box added so companies can explain whether the cost includes water supply and removal of effluent.

1.2 Operating costs paid to external organisations

Reference amended from ‘IPC Authorisation’ to ‘Environmental Permit’.

2.1 - 2.2 Capital expenditure ‘Energy efficiency’ and ‘climate change’ tick-boxes added as a reason for Capex spends.

2.3 Reason for capital expenditure

‘Financial savings’ have been added as a potential reason for Capex spends.

2.3 Reason for capital expenditure

Title amended to ‘Main Reason for Environmental Capital Expenditure’.

3.1 Cost savings and income

Text clarified (‘annualised’ changed to ‘annual’)

3.1 Cost savings and income

Units of measurements amended to include financial cost.

4.3 a-c EMS costs Clarification of questions and amendments made to layout.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

14

2.2 SAMPLING METHODOLOGY

The sampling procedure was designed to target the sectors where the expenditure would be greatest,

based on feedback and findings from previous surveys. In 2009, 974 companies across the relevant

SIC 2007 sectors were selected from the IBDR sample data (see Figure 2.2). The respective SIC

2003 codes are provided for reference only.

Figure 2.2. Industry sectors covered by the 2009 survey

SIC

2007

Industry SIC

2003

Industry

05 - 09 Mining & Quarrying 10 - 14 Mining & Quarrying

10 - 12 Food Products & Beverages, Tobacco

Products

15 - 16 Food Products & Beverages, Tobacco

Products

17 Paper and Pulp 21 - 22 Pulp & Paper, Publishing & Printing

19 Coke & Refined Petroleum 23 Coke, Petroleum & Nuclear Fuel

24 - 25 Basic & Fabricated Metals 27 - 28 Basic Metals & Metal Products

20 - 21 Chemicals & Pharmaceuticals 24 Chemicals & Chemical Products

35 - 36 Electricity, Gas & Water 40 - 41 Electricity, Gas & Water

To maintain a degree of comparability between surveys before and after the SIC revision in 2008, it

was decided that SICs 19 and 35-36 (Coke & Refined Petroleum and Electricity, Gas & Water) would

be sampled for all companies with 10 or more employees. SIC 05-09 (Mining & Quarrying) would be

sampled for companies with 50 or more employees and all the remaining sectors would be restricted

to just companies with 200 or more employees.

2.3 DATABASE DESIGN

Survey data has been collated and stored in an Access database. The database was intended for use

by URS personnel:

To gather information from postal questionnaires and other correspondence, to carry out continuous

validation checks of the data entry process and to record all the phone calls made to the responding

companies when confirming the data.

• To conduct statistical analysis of each year’s data

There are a number of advantages of building the validation checks into the data entry system:

• Checks could be run more frequently

• The results of any follow up calls or validation changes were recorded. The validation tests took

account of the data types and conversions

• There was no delay between the data entry and the return of the validation checks

• Companies could be contacted promptly after returning their completed questionnaires with any

queries.

After the validation tests were run, the results were stored for manual validation. The records within

the list would not change until the validation tests were run again.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

15

Details of the validation process are presented in Annex 2.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

16

3 CONDUCTING THE SURVEY

3.1 Methodology

The stages involved in the survey implementation are summarised in Figure 3.1.

Figure 3.1. Survey Implementation Summary

Activity Number of

companies involved

Description

Pre-survey email 69

Prior to the survey questionnaire being launched, an email was sent out to all companies that responded to the 2008 survey, were included in the 2009 survey and for whom email addresses were held. The email invited the company to participate in the current survey and also provided summary information from the previous survey.

Survey questionnaire 974 The questionnaire was distributed as a package comprising a cover letter, a questionnaire, a fax back form, relevant Technical Guidance Notes and a freepost envelope.

Post-survey postcard 893

This first reminder mail-out increased the volume of calls to the Helpdesk requesting assistance and survey resends.

The reminder postcard was not sent to companies that had already returned the survey or declined to participate.

Reminder letters 861 This reminder mail out represents 90% of the companies initially surveyed, and produced an increase in calls to the Helpdesk.

Top company questionnaire received

30 The Top Companies were approached via a series of dedicated telephone calls.

Number of questionnaires received

171

This equates to an overall response rate of 17.8%.

The volume of questionnaires returned was highest between the 8th and 9th weeks of the survey, corresponding with the written and phone call reminders.

Companies removed from sample

7 Seven companies were removed from the sample after validation checks.

* A number of companies were contacted more than once.

One of two types of cover letter was included in the survey package depending on the category of the

company:

• ‘Top Companies’: The 50 ‘top companies’ by turnover and the ‘top 50 companies’ by number of

employees were selected from the IBDR data (with some organisations featuring in both). In

addition, companies with over 250 employees in SICs 05-09, 10-12, 17, 19 and 35-36 were

included. In total, 164 ‘top companies’ were provided with a tailored cover letter.

• General companies: The letter emphasised potential benefits of participation, and also

highlighted that the information collated in the survey might be used to satisfy the corporate

governance requirements.

Examples of the questionnaire, all cover letters and the Technical Guidance Notes are provided in

Annex 1.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

17

3.2 TOP COMPANY FOCUS

The focus on the Top Companies was changed from a ‘Top 100 interviews’ in 1999 to a ‘Dedicated

Top Company Follow-up’ for the 2000 survey. Owing to its success in increasing participation levels,

the dedicated Top Company follow-up (i.e. repeat calls etc) was continued for all subsequent surveys.

In order to increase the response rate, the Top Companies that had stated that they would fill in the

survey but had not sent it back, were contacted at the end of the survey period in order to let them

know the surveys would still be accepted.

Since the adoption of this Top Company follow up approach the following advantages have been

consistently identified which has led to this being an integral part of the survey design each year:

• Feedback received from companies is an integral part of the questionnaire design for the

following year.

• Organisations were pleased to be considered as Top Companies and owing to the classification

said that they would do their best to participate in the survey.

• The follow-up telephone conversations were helpful in data validation and quality control process.

• The calls also provided an insight into the way companies had interpreted the questions and

answered them.

• Key expenditure issues that were particularly relevant to the company were identified and might

be used for future reference during validation.

• The telephone calls enabled the survey team to build on their existing contact lists, and helped

minimise future issues normally experienced in identifying and contacting the right person within

the different organisations.

• The calls also helped to establish a good working relationship with the company to help the

survey process both for the current year and those years to come.

In previous years, the reasons for non-responses included a lack of interest or inability to complete

the survey. Therefore, in order to improve participation, efforts were made to increase the profile of

the survey during the Top Company telephone calls; for example, by explaining the purpose and

objectives of the survey and offering as much assistance as possible.

3.2.1 Additional findings from the Top Company follow-up

The following were the key findings from the reminder call phase for the Top Companies:

• The most common reason for declining to participate was a lack of available resources or time to

complete the survey. The second most common reason for declining was that the company did

not have the required accounting procedures in place.

• Requests for resends were particularly prevalent where questionnaires had been sent to unnamed

persons; calls made to the Top Company helped to establish named contacts.

Through making the following up calls 110 companies were successfully contacted and were ‘closed

out’ compared with 121 companies in 2008. Closed out means that the appropriate person was

contacted and it was confirmed that they had either:

• Returned their survey to the address given on the form

• Received the survey and would be returning it shortly and definitely by the extended

deadline.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

18

• Not received a copy of the survey, or had mislaid the copy they were sent and would like to

be issued with a replacement (in the majority of these cases copies were issued by e-mail, a

few were issued by post or fax).

• Would not be returning their survey due to various factors including lack of time and

personnel, inability to obtain the information required and company policy not to complete

non-compulsory surveys.

3.3 HELPDESK SUPPORT

A Helpdesk, with direct phone line, fax and email, was available to participating companies

throughout the survey period. Companies were encouraged to use any or all of these methods to

contact a member of the URS survey team.

Contact made through the Helpdesk provided an insight into the information from which the data had

been derived, allowing the data to be validated more efficiently and feedback to be obtained from

companies regarding their individual experiences with the survey.

These facilities, in conjunction with the website, have proved to be a valuable part of the survey

process. The feedback provided has enabled the survey team to find the reasons for participation

and constraints identified by potential survey participants. Annex 4 identifies the main drivers

behind participation and also the reasons why companies declined to participate. This feedback will

be utilised when designing future surveys.

Companies that used the Helpdesk service commented that it had provided useful information,

clarification and assistance in completing the survey form. In addition, the Helpdesk phone calls were

utilised to persuade companies to respond to the questionnaire even if they had thought that the

survey was not relevant to them.

The website has been maintained and continually updated throughout the year. The website address

is: http://www.defra.gov.uk/statistics/environment/environmental-survey/.

The website has been used in conjunction with the Helpdesk to provide companies with additional

copies of the questionnaire, technical guidance notes and other information relating to the survey.

Where appropriate companies were directed to the website in order to obtain another copy of the

2009 survey or to download online a questionnaire. When survey resends were requested the

website was used as a primary source of providing another copy of the questionnaire, a copy sent by

e-mail and fax was used as a secondary source and a postal copy was only offered as a final resort.

A web-based questionnaire, created in 2007 and 2008 has continued to be used. This approach was

introduced in 2005, but not used due to technical problems for the 2006 survey.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

19

4 ANALYSIS OF RESPONSES

4.1 Response Rates

From a sample of 974 companies, the total number of validated responses was 171, giving a

response rate of 18%. The response rates are summarised in Figure 4.1 below.

Figure 4.1. Survey response rates: 2007 to 2009

2009 2008 2007

Questionnaires sent out 974 1,008 955

Questionnaires returned* 171 204 175

Response rate (%) 18 20 18

*Only responses used for analysis are counted here.

A summary of response rates by individual sector is shown in Figure 4.2.

Figure 4.2. Response rates by industry sector: 2007 to 2009.

0 5 10 15 20 25 30

Mining and Quarrying

Food Products, Beverages

& Tobacco Products

Pulp & Paper

Coke & Refined Petrol

Basic and Fabricated

Metals

Chemicals and

Pharmaceuticals

Electricity, Gas and Water

Response %

2009

2008

2007

*The Basic and Fabricated Metals sectors were not surveyed in the 2007.

4.1.1 Weighted Response Rates

The overall response rate given above assumes each company as an equal contributor to the final

figures. The sample frame for previous survey years was designed to target higher spending sectors

and the largest employers. This meant that the effective response rate measures in some cases were

somewhat higher, in terms of expenditure covered.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

20

The 2009 sample frame was designed to take a census of companies over a given size within a

smaller set of highest spending industry groups. The effective response rate measured by the

number of employees in the sampled companies was 21%, although it should be noted that this

might be influenced by the fluctuations in the numbers employed during the year of the survey. The

effective response rate measured by spending proportion was 65%; the sample frame was geared to

the largest employers in the highest spending sectors with the aim of increasing the coverage of

expenditure.

4.1.2 Response Bias

As in previous years’ surveys, the following potential response bias has been identified in the 2009

survey:

• Companies with zero or low expenditure are more likely to respond because they have less of the

questionnaire to complete.

• Companies with dedicated environmental resource are more likely to respond, and have greater

data availability.

• Companies that have completed the survey in previous years are more likely to participate and

submit a completed questionnaire.

The effect of these possible biases is likely to be reduced by the stratified sampling and grossing

arrangements (refer to Annex 6 for further details). This means that using a relatively large number

of cells (determined by size of company and SIC) to categorise companies with similar characteristics

that any bias is then ‘contained’ within the cell.

The repetition of the survey over a number of years has allowed for measures to be taken to obtain a

better understanding of the potential and likely significance of these response biases. For example, a

number of companies respond and state they will not participate, as they have zero environmental

expenditure.

4.2 Methodology

Caution should be exercised in comparing datasets from different survey years (e.g. 2007, 2008 and

2009) for a number of reasons. For instance:

• The ranges indicated by the confidence intervals for the total expenditure were relatively large,

owing to the small sample size. Hence, the absolute values should be compared with caution.

• The process of generating estimates of expenditure from the sample sets means that it is possible

for one company’s expenditure to affect the final figure to a considerable degree, e.g. through a

large ‘one-off’ investment (e.g. capital equipment upgrade). This principally relates to capital

expenditure rather than operating expenditure, which would be expected to be generally more

consistent from one year to the next.

Details of the derivation of standard error and confidence interval are presented in Annex 7.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

21

Where a single response distorts the calculated total, the company has been excluded from the

grossing procedure and added back at a later stage. The decision to do this is undertaken on a case

by case basis. The 2009 data responses received from seven companies were identified as potential

outliers, which could potentially distort overall expenditure figures; these responses have been

grossed in accordance with Annex 6.

4.3 Survey Completion Time

Responses indicated that companies with less than 50 employees took an average of only 50 minutes

to complete the survey, whereas those with between 50 and 250 employees spent an of average 2

hours 17 minutes completing the questionnaire (comparative to the 2008 average of 2 hours 2

minutes). Companies with 250 or more employees took an average completion time of 2 hours 39

minutes.

The time taken to complete the questionnaire by company size (i.e. number of employees) can be

seen in Figure 4.3 below.

Figure 4.3. Completion time by company size: 2007 to 2009

0:00

0:30

1:00

1:30

2:00

2:30

3:00

3:30

4:00

4:30

5:00

<50 50-249 250-499 >500

Tim

e T

aken

(H

ou

rs a

nd

Min

ute

s)

2007

2008

2009

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

22

5 SURVEY RESULTS AND ANALYSIS

5.1 Total expenditure

An estimated total of £3.3 billion was spent by UK industry on environmental protection in 20093

In 2009, OPEX accounted for approximately 58% of the total, with CAPEX making up the remainder.

Spending on internal processes was 64% (34% in 2008). External operating costs accounted for 33%

of OPEX (60% in 2008). Spending on integrated processes accounted for 32% of CAPEX in 2009,

compared to 55% in 2008 for the comparable sectors.

A summary of total expenditure is presented in Figure 5.1 in conjunction with equivalent data from

the 2007 and 2008 surveys for comparison. Ranges indicating the 95% confidence intervals

associated with each value are provided in parenthesis where available. Detailed tables of the

expenditure can be found in Annex 5.

Direct comparisons between survey years should not be made because the estimates are subject to

wide confidence intervals; the sample size has changed considerably and because of changes made

over time to the questionnaire design and estimation procedures. In light of this, comparisons have

been shown as percentage shares of the total spending reported in each year, as well as absolute

figures.

Figure 5.1. Summary of total expenditure: 2007 to 2009

2009 2008 2007

Total expenditure (£M)

% of gross

Total expenditure (£M)

% of gross

Total expenditure (£M)

% of gross

Capital expenditure

End of pipe 947

(92 – 1,802)

29 652

(11 – 1,294)

20 185

(33 – 337)

6

Integrated processes 443

(0 – 918)

13 790

(29 – 1,551)

24 522

(0 – 1,139)

16

Sub-Total 1,389

(259 – 2,519)

42 1,442

(420 – 2,465)

45 707

(59 – 1,356)

21

Operational expenditure

In-house 1,222

(318 – 2,126)

37 606

(237 – 974)

19 811

(105 – 1,518)

24

External 628

(212 – 1,044)

19 1,065

(217 – 1,913)

33 1,709

(804 – 2,614)

51

R&D 72

(0 – 177)

2 118

(0 – 275)

4 116

(0 – 301)

3

Sub-Total 1,922

(935 – 2,909)

58 1,788

(779 – 2,797)

55 2,636

(1416 – 3,857)

79

Gross expenditure

Total gross spend 3,311

(1,600 – 5,022)

100 3,231

(1,368 – 5,093)

100 3,344

(1,814 – 4,873)

100

3 The estimate for 2008 was £3.2 billion for comparable sectors.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

23

By-products income 18

(0 – 42)

1 11

(0 - 22)

0 104

(0 – 275)

3

Total net

expenditure

3,293

(1,559 – 5,027)

- 3,220

(1,357 – 5,082)

- 3,239

(1,700 – 4,778))

-

Total cost savings 146 - 106 - 94 -

Note: Direct comparisons between survey years should be treated with extreme caution.

End-of-pipe Capex shows an increase, but a larger decrease for integrated processes has resulted in

an overall decrease for total Capex. An increase in end of pipe expenditure may have resulted due to

process operators focussing their budget and spend on emissions abatement as apposed to investing

in new or upgraded process / production plant and equipment due to economic uncertainty.

Total Opex has increased overall compared to 2008, with a shift in expenditure to in-house services

and away from external parties, but with a decrease in R&D spend. This shift may be attributed to

less outsourcing / buying in of services and more internal maintenance of equipment and an increase

in internal training or retraining, so having the in-house expertise as appose to needing to use a third

party; together with an increased focus on resource efficiency, including waste and water

minimisation resulting in a reduction in the disposal costs associated with solid and liquid waste and

wastewater. The decrease in research and development (R&D) spend and the shift to internal

resourcing may be linked to economic uncertainty.

Cost savings show an increase which can be associated with campaigns and efforts associated with

resource efficiency, including waste and water minimisation, product reworking / reuse. The increase

in by-product revenue may be associated with Environment Agency/WRAP quality protocols end of

waste criteria being developed and Environment Agency Regulatory Position Statements providing

regulatory clarification on, if and when, a waste ceases to be a waste.

Industrial symbiosis may also have contributed to the by-product revenue increase, bringing together

separate industries and organisations from all business sectors with the aim of improving cross

industry resource efficiency and sustainability; for example involving the physical exchange of

materials and/or by-products.

5.2 EXPENDITURE BY ENVIRONMENTAL MEDIA

This section summarises the amount of expenditure allocated to various environmental protection

categories. Responses are classified under operating expenditure and capital expenditure (refer to

Figures 5.2 - 5.5).

Figure 5.2. Environmental OPEX by Media in 2009

2009 2008 2007

Environmental

media Internal

(£M)

External

(£M) Total (£M) % of total % of total* % of total*

Water 621.7 222.6 844.3 46% 22% 12%

Air 165.4 1.6 166.9 9% 13% 7%

Solid waste 201.3 161.1 362.3 20% 27% 50%

Soil / groundwater 88.4 103.2 191.6 10% 3% 2%

Noise 6.2 0.7 6.8 0% 0% 0%

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

24

2009 2008 2007

Environmental media

Internal

(£M)

External (£M)

Total (£M) % of total % of total* % of total*

Nature protection 105.8 0.6 106.5 6% 2% 1%

Other* 33.6 137.9 171.5 9% 32% 28%

Total (£M) 1,222.3 627.6 1,849.9 100% 100% 100%

* Includes regulator charges

The greatest operating spend comprised water protection measures accounting for 46% of total

environmental OPEX, followed by solid waste at 20% of total operating cost (excluding research and

development); these were also the top two media in 2008. Water shows a large increase compared to

2008 and ‘Other’ a large decrease, which may be associated with definition interpretation, for

example associated with site infrastructure/maintenance.

Figure 5.3. Environmental OPEX by Media: 2007 to 2009

0

10

20

30

40

50

60

Water A ir Solid Waste So il/

Groundwater

No ise Nature Other

Media

Pro

po

rtio

n o

f T

ota

l S

pe

nd

(%

)

2007

2008

2009

Note: ‘Other’ includes external expenditure, e.g. regulatory charges.

Figure 5.4. Environmental CAPEX by environmental media: 2009.

Capital Expenditure (£M)

Integrated Expenditure

Environmental

media Integrated End-of-Pipe Total

% of total % of total Integrated

Water 259.3 693.2 952.5 69% 59%

Air 93.2 206.4 299.7 22% 21%

Solid waste 14.7 31.3 46 3% 3%

Soil /groundwater 30.6 2 32.7 2% 7%

Noise 2.8 0.3 3.1 0% 1%

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

25

Nature

protection 36.9 0.7 37.6 3% 8%

Other 5.1 12.6 17.7 1% 1%

Total (£M) 442.6 946.5 1,389.20 100% 100%

*Please note that the zero percentages stated in the figure above, may be less than 0.5% due to rounding effects.

Capital expenditure on water management/disposal accounted for over two-thirds of total CAPEX

(69%, £953 million). Followed by air protection measures, with a 22% share of total spend (£300

million).

Figure 5.5. Environmental CAPEX by environmental media: 2007 to 2009

0

10

20

30

40

50

60

70

80

Water A ir Solid Waste Soil/

Groundwater

Noise Nature Other

Media

Pro

po

rtio

n o

f T

ota

l S

pen

d (

%)

2007

2008

2009

Note: ‘Other’ includes external expenditure, e.g. regulatory charges.

Capex was the highest by media for water followed by air, which were also the highest for end of

pipe and integrated expenditure, end of pipe being the larger amounts for both media; suggesting

larger investments in wastewater/aqueous wastes treatment, possibly associated with meeting

compliance limits and water reuse and recycling in on site processes; and air emissions abatement to

meet compliance limits and possibly associated with continuous automated monitoring equipment.

The continuing increase of capital expenditure on water and air is likely to be driven by legislation -

primarily permitting regulations (e.g. the Water Framework Directive, and the Environmental

Permitting Regulations) - which imposed increasingly stringent environmental standards for emissions

to air, and water and wastewater treatment, and have also extended to the industry sectors that are

subject to process-related regulation.

Predictions for future changes are likely to be associated with further implications and drivers

associated with the Environmental Permitting Regulations; Registration, Evaluation, Authorisation and

Restriction of Chemicals (REACH); the Environmental Damage (Prevention and Remediation)

Regulations 2009; Water Framework Directive, and implementing the requirements of the revised

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

26

Waste Framework Directive. Other than legislative drivers the cost of fuel both directly and indirectly,

for example waste management logistic transport costs may also have an impact.

5.3 EXPENDITURE BY INDUSTRY SECTOR

Of the industry sectors covered in the 2009 survey, the primary spending sector was, by far, the

Electricity, Gas, and Water sector (81% of total expenditure). Followed by Food Products and

Beverages and Tobacco Products with 10% share of total expenditure in 2009.

Figure 5.6. Total environmental expenditure by industry sector: 2007 to 2009

0

10

20

30

40

50

60

70

80

90

Min

ing a

nd

Quarr

yin

g

Food,

Bevera

ges

& T

obacco

Paper

Pro

ducts

Coke &

Refined

Petr

ole

um

Basic

&

Fabricate

d

Meta

ls

Chem

ical and

Pharm

aceuticals

Ele

ctr

city,

Gas

and W

ate

r

Pro

po

rtio

n o

f T

ota

l S

pen

d (

%)

2007

2008

2009

Note: The Basic and Fabricated Metals sector was not included in the 2007 survey.

5.4 COST SAVINGS AND INCOME

This section summarises the amount of income and savings generated by environmental measures.

Figure 5.7 and 5.8 show the cost savings in 2007, 2008 and 2009. As mentioned earlier,

comparisons between years should be treated with caution.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

27

Figure 5.7. Cost savings: 2007 to 2009

0

10

20

30

40

50

60

70

80

Min

ing a

nd

Quarr

yin

g

Food,

Bevera

ges

& T

obacco

Pro

ducts

Pulp

& P

aper

Coke &

Refined

Petr

ole

um

Basic

&

Fabricate

d

Meta

ls

Chem

icals

&

Pharm

aceuticals

Ele

ctr

icity,

Gas

and W

ate

r

Co

st

Sa

vin

gs

(£

M's

)

2007

2008

2009

Note: The Basic and Fabricated Metals sector was not included in the 2007 survey.

Overall the total cost savings in 2009 were £146 million, significantly more than in 2007 and 2008.

Basic and Fabricated Metals sector recorded the highest level of savings at £69 million (47% of total

cost savings).

Annual cost savings are by environmental media are summarised in Figure 5.8 below.

Figure 5.8. Summary of cost savings: 2007 to 2009

2009 2008 2007

Environmental

Media Total cost

savings (£M) % of Total Total cost

Saving (£M) % of Total Total cost

Saving (£M) % of Total

Raw materials 15.2 10% 18.7 20% 13.1 14%

Water use 10.5 7% 9.4 10% 29.5 31%

Energy use 43.2 30% 26.1 28% 42.4 45%

Waste 72.6 50% 39.5 42% 8.9 10%

Other 4.5 3% 1.2 1% 0.1 0%

Total 145.9 - 95.1 - 94.0 -

The highest cost savings in 2009 were associated with waste management/disposal costs (50% of

total savings); similar to trends in 2008. This was, followed by improved energy usage (30%) and

improvements to the use or substitution of raw materials (10%); again, in line with 2008 trends.

Income received from the sale or redistribution of by-products between 2007 and 2009 is shown in

Figure 5.9 below.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

28

Figure 5.9 Income from by-products (£M): 2007 to 2009.

10

25

40

55

70

85

100

2007

2008

2009

0

2

4

6

8

10

12

Min

ing

an

d

Qu

arr

yin

g

Fo

od

, B

eve

rag

es

& T

ob

acco

Pa

pe

r P

rod

ucts

Co

ke

& R

efin

ed

Pe

tro

leu

m

Ba

sic

&

Fa

bri

ca

ted

Me

tals

Ch

em

ica

l &

Ph

arm

ace

utica

ls

Ele

ctr

icity, G

as

an

d W

ate

r

Income and savings resulting from the sale of by-products in 2009 was £17.5 million, which is much

less than in previous years. The highest saving as a result of by-products was within the Basic and

Fabricated Metals sector (£7 million; 42% of total by-products sale).

Income from by-products (£M’s)

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

29

5.5 ENVIRONMENTAL PROTECTION EXPENDITURE BY INDIVIDUAL SECTOR

This section looks at each sector individually, identifies any notable features under the following

headings including a brief analysis discussing trends and drivers of environmental protection

expenditure in 2009:

• Key expenditure: Summary of key data by operating expenditure (OPEX) and capital

expenditure (CAPEX) categories along with the expenditure in 2007, 2008 and 2009.

• Environmental expenditure by media: Expenditure has been subdivided according to media

type (e.g. water, solid waste, noise etc). This is shown in graph form for external, in-house,

integrated and end-of-pipe expenditure.

• Income and savings: Summary of key data by cost savings and by-product sales in expenditure

for 2007, 2008 and 2009.

As mentioned earlier in this report, direct comparisons between survey years are not advisable, as

estimates are subject to wide confidence intervals, sample sizes have changed and modification have

been made to the questionnaire design and estimation procedures. In light of these discontinuities,

comparisons will still be shown but percentage shares of the total spending (e.g. as shown in Figure

E2) are preferable, but should also be treated with caution.

5.5.1 SIC 05 to 09: Mining and Quarrying

The Mining and Quarrying sector has a relatively small number of companies in the UK and there are

several large companies that have responded to the survey in one year and not in the others, which

increases the potential for skewed results.

Estimates of environmental protection expenditure, environmental expenditure by media and income

and savings are provided below for the Mining and Quarrying sector. For this sector, 18 companies

participated in the survey giving a response rate for the sector of 15%, which is equivalent to 11% of

the total survey response.

The most significant and recent regulatory drivers of change in the UK Mining and Quarrying industry

are the Mining Waste Directive, EU Landfill Directive, Integrated Pollution Prevention and Control

(IPPC) Directive and Water Framework Directive.

Key Expenditure

The Mining and Quarrying sector spent approximately £31 million in 2009 on environmental

protection measures, 1% of the total spend for 2009. Environmental expenditure for this sector is

shown in Figure 5.10 for the years 2007, 2008 and 2009. The data is presented separately for

capital and operational expenditure.

Figure 5.10. Expenditure: 2007 to 2009

OPEX (£M) CAPEX (£M) Survey year

In-house External R & D Total End of Pipe Integrated Total

2009 15.0 8.9 0.3 24.1 0.8 6.9 7.7

2008 7.6 25.1 0.8 33.5 31.7 108.0 139.7

2007 69.6 41.8 3.9 115.3 108.6 0.2 108.8

Note: Totals may not add due to the rounding effects. Comparisons between years should be treated with caution because of

the low response rate.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

30

OPEX accounted for 76% of total environmental spending by the Mining and Quarrying sector in

2009. External expenditure in 2009 was higher than in-house costs, maintaining the unpredictability

within OPEX seen over recent years. OPEX reduced from the 2008 levels, maybe as companies

undertook the minimum to be in compliance with the law.

There was a significant reduction in the CAPEX spend in 2009, this could be due to the global

financial crisis

The main driver for environmental expenditure has been for companies to protect their balance

sheets, and so as and when the economy improves and confidence returns to the market the

investment in environment is expected to return.

It should also be noted that the change in survey design and the reduced number of companies

within the sample may be responsible for some variation within results from one survey to the next.

Environmental Expenditure by Media

Environmental expenditure by media for the Mining and Quarrying sector is shown below in Figure

5.11. In previous years, wastewater, solid waste and air quality management were areas where the

majority of spend occurred. The massive reduction in CAPEX means that investment in these areas

has reduced relative to the other areas, and it is considered that this is due to companies only

undertaking the minimum in all the media.

The Mining Waste Directive, currently being transposed into UK law, covers the management of

“extractive waste” resulting from the prospecting, extraction, treatment and storage of mineral

resources and the working of quarries. It may lead to the reduction in waste disposal costs observed

in future surveys as certain materials are no longer classified as waste.

Figure 5.11. Environmental expenditure by media

0

1

2

3

4

5

6

7

Water Air Solid Soil/ Ground

water

Noise Nature

protection

Other

£M

End of Pipe

Integrated

External

In-House

Income and Savings

In 2009, income and savings for the Mining and Quarrying sector was approximately £2.7 million.

This result is shown along with the 2008 and 2007 survey data in Figure 5.12. It should be noted

that the change in survey design and the reduced number of companies within the sample may be

responsible for the variation within results from one survey to the next.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

31

Figure 5.12. Income (from by-products) and savings: 2007 to 2009

Cost savings (£000’s) Income

(£000’s) Survey

Year

Raw material

Water use

Energy use

Waste Other Total By- products

Total (£000’s)

2009 0.1 0.1 1.4 0.0 0.1 1.6 1.1 2.7

2008 0.2 0.3 0.0 0.1 0.1 0.7 0.5 1.2

2007 0.0 0.1 0.0 0.0 0.1 0.2 0.2 0.4

Note: Totals may not add due to the rounding effects. Comparisons between years should be treated with caution because of the low response rate.

Cost savings in the sector for 2009 were £1.6 million, of which the sale of by-products accounted for

approximately 41% of this saving. The magnitude increase in cost savings could be due to the

companies endeavouring to achieve a reduction driven by the economic climate

5.5.2 SIC 10 - 12: Food Products and Beverages, and Tobacco Products

The Food Products and Beverages, and Tobacco Products sector is the largest sector in terms of

response in the 2009 survey, and the sector is at least in part driven by its water intensive nature.

Estimates of environmental protection expenditure, environmental expenditure by media and income

and savings are provided below for the Food Products and Beverages, and Tobacco Products sector.

For this sector, 49 companies participated in the survey giving a response rate of 15%, which is also

equivalent to 29% of the total survey response.

Key Expenditure

The Food Products and Beverages and Tobacco Products sector spent approximately £322 million in

2009 on environmental protection measures, 10% of the total spend for 2009. Environmental

expenditure for this sector is shown in Figure 5.13 for the years 2007, 2008 and 2009. The data is

presented separately for capital and operational expenditure.

Figure 5.13. Environmental expenditure: 2009

OPEX (£M) CAPEX (£M) Survey year

In-house External R & D Total End of Pipe Integrated Total

2009 99.2 182.4 1.7 283.4 13.4 25.0 38.4

2008 135.3 186.9 2.8 325.0 127.8 28.5 156.2

2007 131.2 208.0 4.2 343.4 42.4 71.6 114.0

Note: Totals may not add, due to the rounding effects. Comparisons between years should be treated with caution due to low response rate.

Operating expenditure accounted for approximately 88% of total environmental spending by the Food

Products and Beverages, and Tobacco Products sector in 2009.

With regards to operating expenditure, the external expenditure level observed in 2009 is consistent

with the levels observed in the two previous years. This reflects that, despite a down turn in the

economy, the industry has defined externally provided fixed operating costs such as effluent

treatment costs by third party trade effluent treatment service providers.

Environmental Protection Expenditure by UK Industry: 2009 Survey

49355201 Final Report May 2011

32

Of note is that the level of in-house operating expenditure has reduced. This is thought to be due to

optimisation of operations, due to the tight economic constraints in 2009, and also due to increased

regulator pressure under environmental legislation, e.g. the Environmental Permitting Regulations etc.

The level of capital expenditure for integrated activities, on areas such as process improvements or

manufacturing optimisation, has remained steady from 2008 into 2009. This indicates that there is a

constant baseline of internal process improvements that can be undertaken to streamline and

improve inherent manufacturing operations.

Of particular note is that the level of capital expenditure for end of pipe solutions has shrunk by 90%

from 2008 levels. This is in line with the worsening state of the economy and that the industry, with

low profit margins, was capital averse in 2009.

Owing to the poor economic situation, moving forward into 2010, it is highly likely that the low level

of capital expenditure will continue and that the level of in-house operating expenditure will fall

further.

Environmental Expenditure by Media

Environmental expenditure by media for the Food Products and Beverages and Tobacco Products

sector is shown in Figure 5.14 below. This sector spent £151 million on water protection measures

and £99 million dealing with solid waste in 2009, of which most is accounted for by external operating

expenditure (£91 million). The distribution of expenditure by media in this sector is consistent with

previous years; water and solid waste remain the dominant environmental issues for the industry.

Figure 5.14 Environmental Spending by Media

0

20

40

60

80

100

120

140

160