Embed Size (px)

Citation preview

Ref: 5645R/46059003-784/SV

FINAL REPORT (2003) For: ENVIRONMENTAL PROTECTION EXPENDITURE BY INDUSTRY: 2003 UK SURVEY Submitted to: Department for Environment, Food and Rural Affairs June 2005

St George's House, 2nd Floor 5 St George's Road Wimbledon London SW19 4DR Tel: 020 8944 3300 Fax: 020 8944 3301 Email: [email protected]

5645R/46059-003-784/SV Final Report June 2005

The views and recommendations expressed in this report are those of the authors and do

not necessarily represent the views of the Department for Environment, Food and Rural

Affairs, its ministers or officials.

i 5645R/46059-003-784/SV Final Report June 2005

EXECUTIVE SUMMARY

Introduction

This report presents the findings of a study commissioned by the Department for Environment, Food

and Rural Affairs (Defra) and undertaken by URS Corporation Limited (URS), to estimate expenditure

by UK industry on environmental protection in 2003.

The primary objectives of the study are:

• To provide Defra with annual estimates of environmental protection expenditure by UK industry;

and

• To enable Defra to provide these estimates to the European Commission as required under the

EU Structural Business Statistics Regulation 58/97.

In addition to these broad objectives, annual data from the survey may be used to assess how

expenditure is changing and to compare the competitiveness of UK industries relative to other EU

countries. The data also enables companies and trade associations to benchmark their own

environmental performance against that of the industry as a whole, both in the UK and the EU.

This is the seventh survey of this type; previous surveys were carried out in 1994 (a pilot survey),

1997, 1999, 2000, 2001 and 2002. The 2003 survey was conducted in 3 phases between April 2004

and July 2005, steered by a group with representatives from Defra, Department for Trade and

Industry (DTI), Environment Agency, Scottish Environmental Protection Agency (SEPA) and the Office

for National Statistics (ONS).

Methodology

The industry sectors follow the Standard Industrial Classification (SIC) codes and are covered by the

survey as follows:

SIC code Industry 10 – 14 Mining and quarrying15 & 16 Food, beverages and tobacco products 17 – 19 Textiles, clothing and leather products 20 Wood and wood products 21 & 22 Pulp and paper, printing and publishing 23 Coke, petroleum and nuclear fuel 24 Chemicals and chemical products 25 Rubber and plastics 26 Other non-metallic minerals 27 & 28 Basic metals and metal products 29 – 31 Machinery and equipment 32 & 33 Electrical, medical and optical equipment 34 & 35 Transport equipment 36 Furniture manufacture 40 & 41 Energy production and water

ii 5645R/46059-003-784/SV Final Report June 2005

The Government’s Inter Departmental Business Register (IDBR) provided a stratified random sample

of 8,142 companies from the above industry sectors and these were invited on a voluntary basis to

complete and return a postal questionnaire. The total number of validated responses was 1,591,

giving a valid response rate of 19.5 per cent, which is approximately the same as in previous surveys.

The responses were subjected to a range of detailed validation checks.

The survey analysed the following expenditure patterns in UK industry: • Operating expenditure (OPEX), which includes the in-house operating costs of a company’s own

environmental protection activities, and also payments to others for environmental protection

services including waste disposal; and

• Capital expenditure (CAPEX), which consists of ‘end of pipe’ investments (expenditure on

equipment to clean up at the end of the production process) and integrated investment

expenditure (expenditure on equipment which reduces or eliminates emissions and discharges as

part of the production process).

Also identified were the following:

• Income and savings resulting from environmental protection activities carried out in 2003;

• The environmental media (areas) affected by the spending, namely waste water, air, solid waste,

soil/groundwater, noise/vibrations and nature protection; and

• The use of Environmental Reporting Systems.

Main results for 2003

• Gross spending on environmental protection in 2003 by UK industry amounted to an estimated

£3.4 billion;

• The primary spending sectors were food, beverages and tobacco products (12 per cent of total

spend), power industries (14 per cent of total spend) and chemicals and chemical products (18

per cent of total spend);

• Operating expenditure accounted for 85 per cent of the total environmental protection

expenditure, with capital expenditure making up the remainder;

• 40 per cent of the total expenditure was spent on solid waste, with a further 27 per cent spent

on wastewater, and the remaining 33 per cent spent on air, soil/groundwater, noise and nature

protection and other areas;

• This spending was offset by an estimated income of £178 million from the sale of by-products

and estimated cost savings of £265 million from environmental protection measures undertaken

during the year;

iii 5645R/46059-003-784/SV Final Report June 2005

• 22 per cent of companies surveyed separately identify environmental protection expenditure in

their management accounting system. The use of environmental reporting systems is more

widespread amongst companies with over 250 employees; and

• 22 per cent of companies surveyed publicly report on their environmental expenditure in their

annual accounts (12%) or an environmental / sustainability report (10%).

Comparisons between years

Direct comparisons between survey years are not possible because the estimates are subject to wide

confidence intervals and because of improvements made over time to the questionnaire design and

estimation procedures. In the light of this, the following charts show differences in the percentage

shares of total spending reported in each year, rather than the absolute figures. It should be noted

that efforts are made each year to reduce confidence intervals as well as to keep the questionnaire

and methodology consistent.

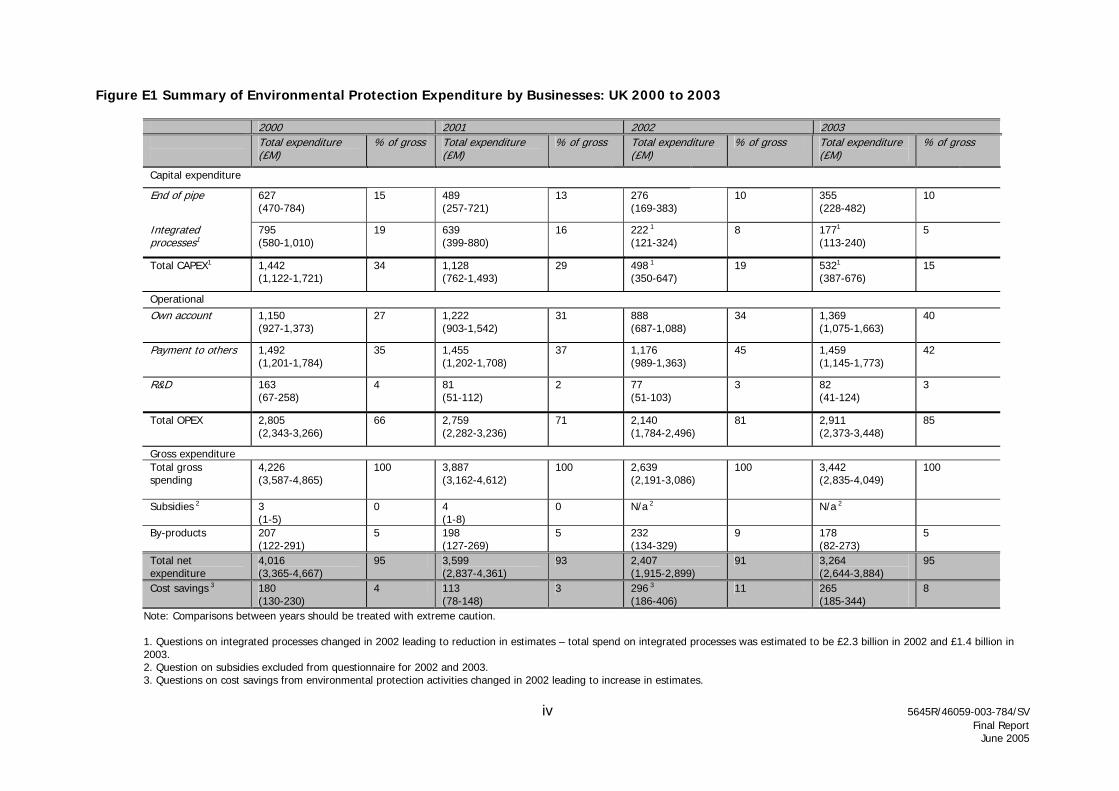

A summary of total environmental protection expenditure by businesses for 2000, 2001, 2002 and

2003 is presented in Figure E1. Ranges indicating the 95 percent confidence intervals associated

with each value are provided in parenthesis where available. Gross spending on environmental

protection in 2003 by UK industry amounted to an estimated £3.4 billion, plus or minus £0.6 billion at

95 per cent confidence. The estimates of previous years were £4.2 billion in 2000, £3.9 billion in

2001, and £2.6 billion in 2002. Although a reduction in spending might have been expected as a

result of the general downturn in the manufacturing sector over the period, it now appears as if the

2002 figure is a bit of an anomaly. A summary of the proportion of total expenditure for 2000, 2001,

2002 and 2003 by the main industry groups is presented in Figure E2.

Figure E1 Summary of Environmental Protection Expenditure by Businesses: UK 2000 to 2003

2000 2001 2002 2003

Total expenditure (£M)

% of gross Total expenditure (£M)

% of gross Total expenditure (£M)

% of gross Total expenditure (£M)

% of gross

Capital expenditure

End of pipe

627 (470-784)

15 489(257-721)

13 276(169-383)

10 355(228-482)

10

Integrated processes1

795 (580-1,010)

19 639(399-880)

16 222 1

(121-324) 8 1771

(113-240) 5

Total CAPEX1

1,442 (1,122-1,721)

34 1,128(762-1,493)

29 498 1

(350-647) 19 5321

(387-676) 15

Operational Own account 1,150

(927-1,373) 27 1,222

(903-1,542) 31 888

(687-1,088) 34 1,369

(1,075-1,663) 40

Payment to others 1,492 (1,201-1,784)

35 1,455(1,202-1,708)

37 1,176(989-1,363)

45 1,459(1,145-1,773)

42

R&D 163 (67-258)

4 81(51-112)

2 77(51-103)

3 82(41-124)

3

Total OPEX

2,805 (2,343-3,266)

66 2,759(2,282-3,236)

71 2,140(1,784-2,496)

81 2,911(2,373-3,448)

85

Gross expenditure Total gross spending

4,226 (3,587-4,865)

100 3,887(3,162-4,612)

100 2,639(2,191-3,086)

100 3,442(2,835-4,049)

100

Subsidies 2 3 (1-5)

0 4(1-8)

0 N/a 2 N/a 2

By-products 207(122-291)

5 198(127-269)

5 232(134-329)

9 178(82-273)

5

Total net expenditure

4,016 (3,365-4,667)

95 3,599 (2,837-4,361)

93 2,407 (1,915-2,899)

91 3,264 (2,644-3,884)

95

Cost savings 3 180 (130-230)

4 113 (78-148)

3 296 3

(186-406) 11 265

(185-344) 8

Note: Comparisons between years should be treated with extreme caution. 1. Questions on integrated processes changed in 2002 leading to reduction in estimates – total spend on integrated processes was estimated to be £2.3 billion in 2002 and £1.4 billion in 2003. 2. Question on subsidies excluded from questionnaire for 2002 and 2003. 3. Questions on cost savings from environmental protection activities changed in 2002 leading to increase in estimates.

iv 5645R/46059-003-784/SV Final Report June 2005

Figure E2 - Proportion of Total Environmental Expenditure by Standard Industrial

Classification (SIC) sectors: UK 2000, 2001, 2002 and 2003.

02468

101214161820

Sector

Pro

port

ion

of T

ota

l Sp

end

(%)

2000

2001

2002

2003

In all four years the primary spending sectors were food, beverages and tobacco products (ranging

from 12 to 19 per cent of total spend), power industries (ranging between 11 and 17 per cent of total

spend) and chemicals and chemical products (ranging between 15 and 19 per cent of total spend).

The detailed analysis of these results is presented in Section 5 of the report.

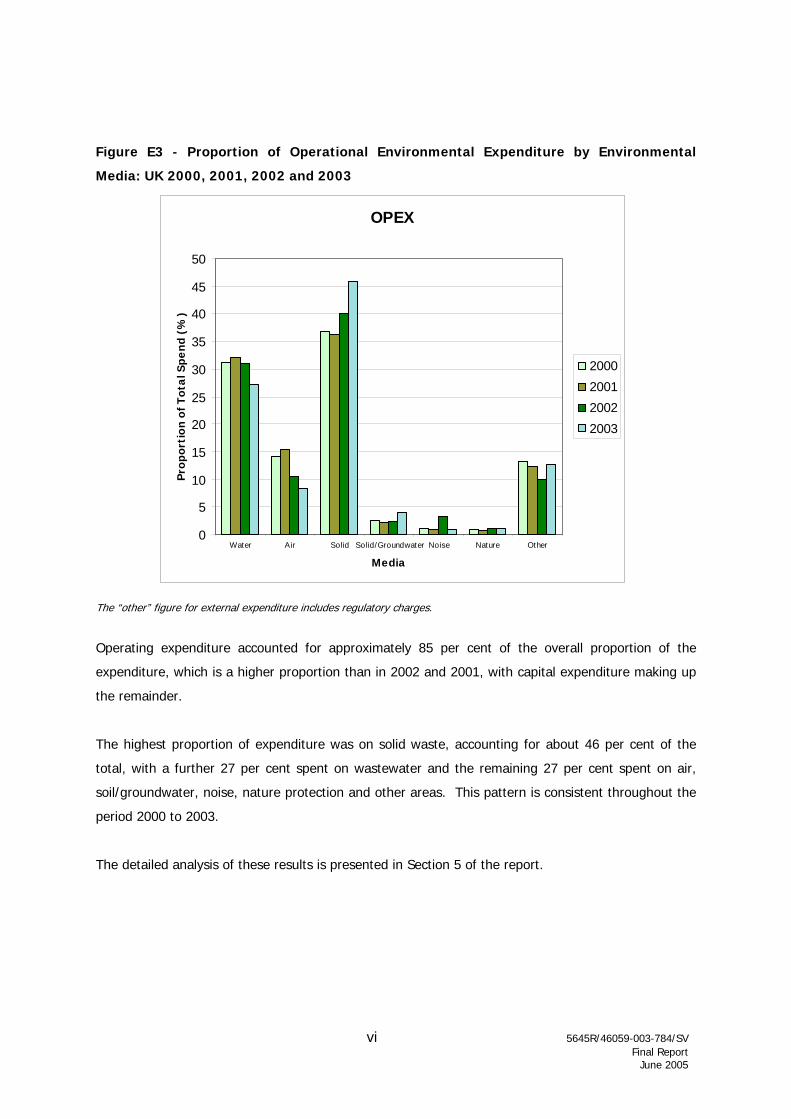

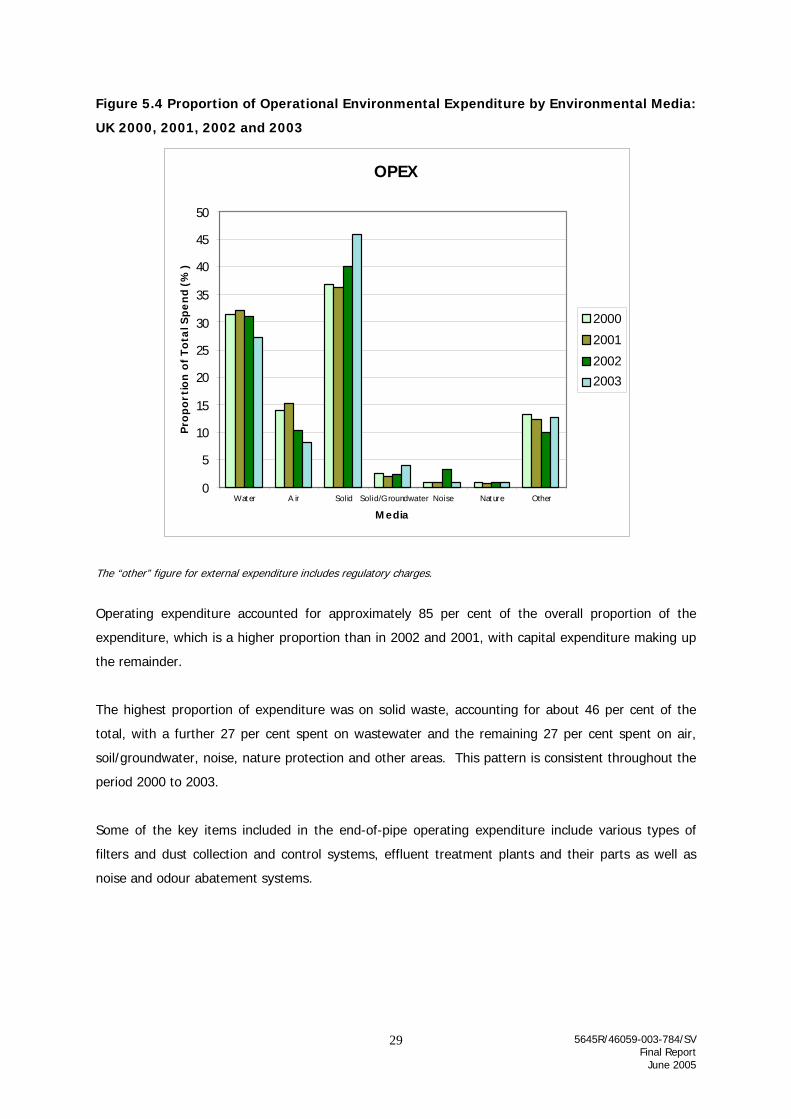

Figures E3 and E4 show the proportion of expenditure across environmental media for operating

and capital expenditures respectively in 2003.

v 5645R/46059-003-784/SV Final Report June 2005

Figure E3 - Proportion of Operational Environmental Expenditure by Environmental

Media: UK 2000, 2001, 2002 and 2003

vi 5645R/46059-003-784/SV Final Report June 2005

OPEX

0

5

10

15

20

25

30

35

40

45

50

Water Air Solid Solid/Groundwater Noise Nature Other

Media

Prop

orti

on

of T

ota

l Sp

end

(%

)

2000

2001

2002

2003

The “other” figure for external expenditure includes regulatory charges.

Operating expenditure accounted for approximately 85 per cent of the overall proportion of the

expenditure, which is a higher proportion than in 2002 and 2001, with capital expenditure making up

the remainder.

The highest proportion of expenditure was on solid waste, accounting for about 46 per cent of the

total, with a further 27 per cent spent on wastewater and the remaining 27 per cent spent on air,

soil/groundwater, noise, nature protection and other areas. This pattern is consistent throughout the

period 2000 to 2003.

The detailed analysis of these results is presented in Section 5 of the report.

Figure E4 - Proportion of Capital Environmental Expenditure by Environmental Media: UK

2000, 2001, 2002 and 2003

vii 5645R/46059-003-784/SV Final Report June 2005

CAPEX

0

5

10

15

20

25

30

35

40

45

50

Water Air Solid Solid/Groundwater Noise Nature Other

Media

Pro

port

ion

of T

ota

l Spe

nd (

%)

2000

2001

2002

2003

The “other” figure for external expenditure includes regulatory charges.

Capital expenditure accounted for about 15% of the overall total environmental protection

expenditure in 2003. The highest proportion of expenditure was on air, accounting for approximately

40 per cent of the total, with a further 27 per cent spent on wastewater, 10 per cent on solid waste

and the remaining 23 per cent spent on soil/groundwater, noise, nature protection and other areas.

The highest areas of capital expenditure were broadly the same in 2000, 2001, and 2002. As

previously noted, the large differences between years in the amounts of capital expenditure recorded

in the survey is in part attributable to changes in the ways the survey questions have been asked in

different years.

The highest proportion of operating expenditure was on solid waste, whereas the highest proportion

of capital expenditure was on air. This could result from the Integrated Pollution Prevention Control

(IPPC) permit increasing the capital expenditure on air protection measures.

The detailed analysis of these results is presented in Section 5 of the report.

TABLE OF CONTENTS

5645R/46059-003-784/SV

viii Final Report June 2005

Page No

EXECUTIVE SUMMARY I

1 INTRODUCTION 1 1.1 OBJECTIVES 1 1.2 SCOPE AND BACKGROUND 2 1.3 DEFINITION OF ENVIRONMENTAL PROTECTION EXPENDITURE 3 1.4 REPORT STRUCTURE 4

2 SURVEY METHODOLOGY AND PREPARATION 5 2.1 MODIFICATIONS INTRODUCED IN THE 2003 SURVEY 6 2.2 SAMPLING METHODOLOGY 7 2.3 DATABASE DESIGN 7 2.4 SURVEY PROMOTION 8

3 CONDUCTING THE SURVEY 9 3.1 METHODOLOGY 9 3.2 TOP COMPANY FOCUS 11

3.2.1 Impact of the Top Company Focus 12 3.2.2 Lessons learnt from the Dedicated Top Company Follow-up 13

3.3 SME SIMPLIFIED APPROACH 14 3.4 HELPDESK SUPPORT 15

4 ANALYSIS OF RESPONSES 17 4.1 RESPONSES 17

4.1.1 Response Rates 17 4.1.2 Weighted Response Rates 20 4.1.3 Repeated Responses 20 4.1.4 Response Bias 22 4.1.5 2002 vs. 2003 Methodology 23

4.2 STANDARD ERRORS AND CONFIDENCE INTERVALS 23

5 SURVEY RESULTS AND ANALYSIS 25 5.1 TOTAL EXPENDITURE 25 5.2 EXPENDITURE BY ENVIRONMENTAL MEDIA 27 5.3 EXPENDITURE BY INDUSTRY SECTOR 31 5.4 COST SAVINGS AND INCOME 32 5.5 ENVIRONMENTAL PROTECTION EXPENDITURE BY INDIVIDUAL (SIC) SECTOR 35

5.5.1 SIC 10 to 14: Mining and Quarrying 36 5.5.2 SIC 15 & 16: Food Products and Beverages, and Tobacco Products 39 5.5.3 SIC 17, 18, and 19: Textiles, Clothing and Leather Products 41 5.5.4 SIC 20: Wood and Wood Products 43 5.5.5 SIC 21: Pulp and Paper 45 5.5.6 SIC 22: Publishing and Printing 47 5.5.7 SIC 23: Coke, Petroleum and Nuclear Fuel 49 5.5.8 SIC 24: Chemicals (Basic, Pharmaceuticals and Other) 51 5.5.9 SIC 251 and 252: Rubber and Plastics 54 5.5.10 SIC 26: Other Non-Metallic Minerals 56 5.5.11 SIC 27: Basic Metals 58

TABLE OF CONTENTS (Continued) Page No

5645R/46059-003-784/SV ix Final Report June 2005

5.5.12 SIC 28: Fabricated Metal Products 60 5.5.13 SIC 29, 30 and 31: Machinery and Equipment, Office Machinery and Apparatus and Electrical Machinery and Apparatus 63 5.5.14 SIC 32 & 33: Radio, TV and Comms, and Medical, Precision and Optical 66 5.5.15 SIC 34 & 35: Motor Vehicles and Other Transport Equipment 68 5.5.16 SIC 36: Furniture Manufacture 71 5.5.17 SIC 40: Electricity, Gas, Steam and Hot Water 73 5.5.18 SIC 41: Collection, Purification and Water Distribution 75

5.6 COMPARISON OF CURRENT EXPENDITURE WITH SUPPLY SIDE ESTIMATES77 5.7 ENVIRONMENTAL REPORTING SYSTEMS 80

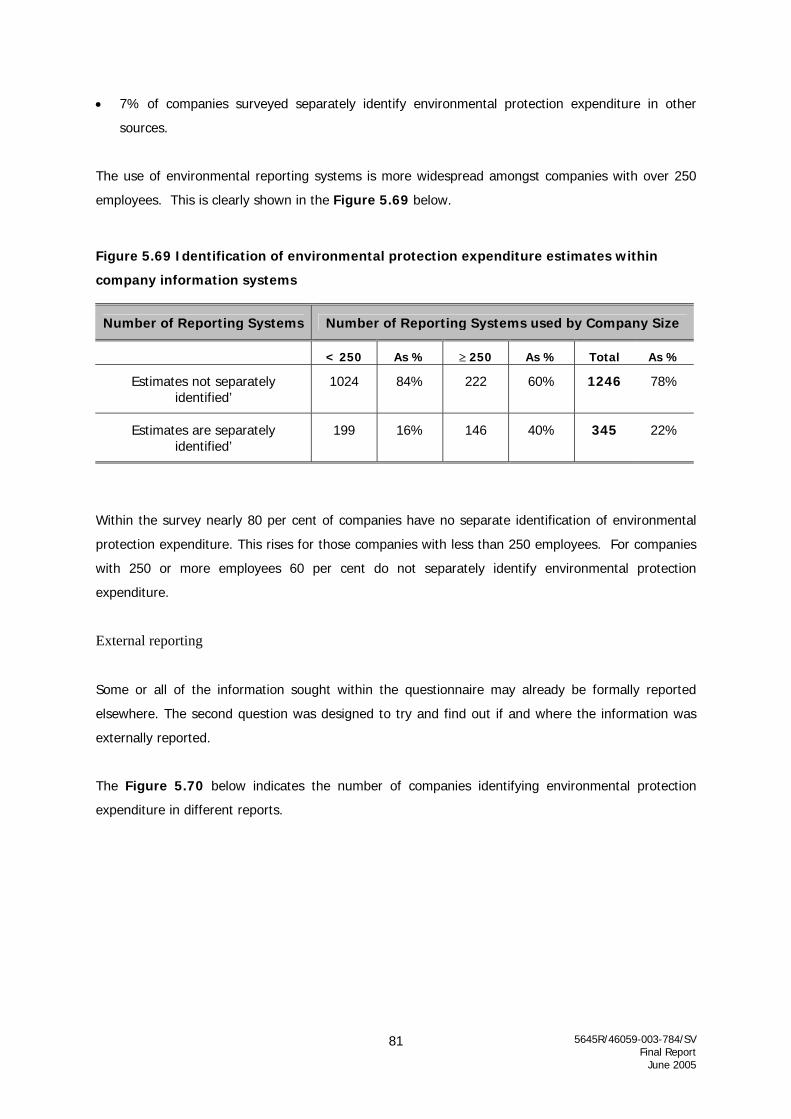

5.7.1 Separate Identification of Environmental Expenditure in information systems 80 5.7.2 Findings 82

6 RECOMMENDATIONS FOR FUTURE SURVEYS 83 6.1 GENERAL 83 6.2 QUESTIONNAIRE DESIGN 85 6.3 VALIDATION PROCESS 86

LIST OF ABBREVIATIONS 87

LIST OF STANDARD INDUSTRIAL CLASSIFICATION (SIC) CODES 88

5645R/46059-003-784/SV Final Report June 2005

1

1 INTRODUCTION

This report presents the results for the seventh annual study commissioned by the Department for

Environment, Food and Rural Affairs (Defra) and undertaken by URS Corporation Limited (URS), to

estimate expenditure by UK industry on environmental protection in 2003. Previous surveys were

carried out in 1994 (a pilot survey), 1997, 1999, 2000, 2001, and 2002. The following sections of the

report summarise the findings from the analysis of the 2003 questionnaires completed by

participating UK companies.

The 2003 data is shown in contrast to the results from the 2000, 2001 and 2002 surveys. Direct

comparisons between survey years are not, however, possible because;

• The estimates are subject to wide confidence intervals; and

• Improvements have been made to the questionnaire design and estimation procedures.

In light of these discontinuities, comparisons are shown as percentage shares of the total spending

reported in each year, rather than the absolute figures. However, comparisons between years should

still be treated with caution.

1.1 OBJECTIVES

The primary objectives of the study were to:

• Provide Defra with annual estimates of environmental protection expenditure by UK industry; and

• Enable the UK Government to meet the requirements of the European Union (EU) Structural

Business Statistics Regulation 58/97, which provided a tool for regular data collection on the

variables and economic activities and is designed to give information on the service sector.

In addition to these broad objectives, annual data from the survey may be used to assess how

expenditure is changing and to compare the competitiveness of UK industries relative to other EU

countries. The data enables companies and trade associations to benchmark their own environmental

spending against that of the industry as a whole, both in the UK and the EU.

5645R/46059-003-784/SV Final Report June 2005

2

1.2 SCOPE AND BACKGROUND

The current survey covers all expenditure incurred in 2003 (financial year 2003/2004). In accordance

with the EU Regulations, industries that have been surveyed are those in NACE1 sections C, D and E.

These are businesses involved in extraction, manufacturing, energy and water supply. Expenditure

estimates are provided for the following:

• In-house and external operating costs (including research & development, regulatory charges

etc);

• End-of-pipe capital investments;

• Integrated or ‘clean’ technology capital investments; and

• Income and savings (the sale of environmental protection by-products).

This expenditure is also reported by the environmental media to which they relate to, as shown

below:

Waste water – collection and transport of waste water, the prevention or reduction in quantity of

waste water and of substances in waste water, the prevention of incidental water pollution, the

treatment of cooling water before draining to the surface or groundwater and monitoring of surface

water.

Air – prevention or reduction of gaseous, liquid or particulate emissions to the atmosphere and the

monitoring of air emissions.

(Solid) Waste – the prevention or reduction of waste, the collection, transport, treatment and

disposal and monitoring of waste.

Soil/groundwater – decontamination of polluted soils and cleansing of polluted ground water.

Includes the protection of soil and groundwater against pollution infiltration, monitoring of soil and

groundwater and the transport and disposal of contaminated soil.

Noise/vibration – measures to decrease noise and vibration levels at source, to isolate receivers

from noise/vibration and the monitoring of levels. Protection of the workplace is excluded.

Nature protection – protection of species, landscapes and habitats; rehabilitation of damaged

landscapes due to past or current actions. Reforestation is included.

1 NACE: ‘Nomenclature Generale des Activites Economiques dans les Communautes Europeennes’

5645R/46059-003-784/SV Final Report June 2005

3

This survey succeeds the Defra (formerly known as Department of Environment, Transport and the

Regions - DETR) surveys carried out in 2002, 2001, 2000, 1999, 1997 and research on environmental

protection expenditure in 1994 (pilot study). The reports from these surveys can be downloaded at:

http://www.defra.gov.uk/environment/statistics/envsurvey/index.htm

1.3 DEFINITION OF ENVIRONMENTAL PROTECTION EXPENDITURE

The definition of environmental protection expenditure used for this survey was established by the

Statistical Office of the European Community (SOEC) as follows:

‘Environmental protection expenditure is the sum of capital and current expenditure on environmental protection activities. Environmental protection is an action or activity (involving the use of equipment, labour, manufacturing techniques and practices, information networks or products) where the main purpose is to collect, treat, reduce, prevent, or eliminate pollutants and pollution or any other degradation of the environment resulting from the activity of the company. Environmental protection expenditure may relate to activities that generate marketable by-products, or results in savings, or are financed by subsidies or capital allowances. In such cases, environmental protection expenditure should be reported gross of any such cost offsets.’

Environmental protection expenditure includes: expenditure to reduce or prevent emission to air and

water; expenditure to protect or clean up soil and groundwater; expenditure to prevent noise and

vibration; and expenditure to reduce, treat and dispose of waste materials. Expenditure may be

operating expenditure (OPEX) or capital expenditure (CAPEX).

OPEX includes the operating costs of a company’s own environmental protection equipment and

services and also payments to others for environmental protection services (including waste disposal).

CAPEX consists of end-of-pipe expenditure and expenditure on integrated processes. End-of-

pipe CAPEX is defined as expenditure on equipment used to treat, handle, measure or dispose of

emissions and wastes from production. Examples include effluent treatment plant, exhaust air

scrubbing systems, and solid waste compactors.

Capital expenditure on integrated processes relates to new or modified production facilities

designed to integrate environmental protection into the production process. This might include

adaptation of an existing installation/process whereby the integrated expenditure is then the total

purchase cost of the adaptation. It also includes installing a new process in which the design takes

environmental protection into account and in this case the expenditure counted is only the extra cost

compared with installing a ‘dirtier’ alternative.

5645R/46059-003-784/SV Final Report June 2005

4

Energy costs are not included in the definition of environmental protection expenditure, except where

energy is specifically used to run environmental protection equipment or services. Also excluded is

any expenditure on health and safety equipment or services.

1.4 REPORT STRUCTURE

This report consists of the following sections:

Section 1 Introduction;

Section 2 Survey Methodology and Preparation;

Section 3 Conducting the Survey;

Section 4 Analysis of Responses;

Section 5 Survey Results and Analysis; and

Section 6 Recommendations for Future Surveys.

This main report is supplemented by detailed annexes, as described below, which are presented as a

separate document:

Annex 1 Cover Letters and Technical Guidance Notes;

Annex 2 Detailed Sampling Methodology;

Annex 3 Validation of Responses;

Annex 4 Copies of promotional material;

Annex 5 Response codes for sorting correspondence;

Annex 6 Drivers behind participation;

Annex 7 Output of Data Analysis;

Annex 8 Grossing-up Procedure;

Annex 9 Methods for derivation of standard error and confidence intervals;

Annex 10 Detailed Results Tables; and

Annex 11 Valid Data.

The report and the Annexes can be downloaded from Defra’s web site at

http://www.defra.gov.uk/environment/statistics/envsurvey/index.htm

5645R/46059-003-784/SV Final Report June 2005

5

2 SURVEY METHODOLOGY AND PREPARATION

The main survey consisted of three phases, conducted between April 2004 and July 2005, which were

sub-divided into individual tasks/activities:

• Pre-survey is the first survey phase, which includes the following activities (April

2004 – May 2004):

o Review the previous year’s survey and introduction of modifications o Promote survey results o Produce a Project Initiation Document (PID) o Steering Group meeting participation

• Survey phase, which includes the following activities (June 2004 – February

2005):

o Select sample from the IDBR and carry out subsequent database work (request for the IDBR sample was sent out in March 2004)

o Review and submit mailout materials to Defra o Amend and approve mailout materials as required o Coordinate printing of the mailout materials o Provide helpdesk support o Dispatch survey pack to companies o Data entry of survey returns o Dispatch the reminder postcard o Survey resends as required o Reminder letter dispatch o Produce interim report

• Analysis and Final Reporting, this phase of the project includes the following

activities (March 2005 – July 2005):

o Creation / updating of validation process o Continuous validation (statistically and by calling companies to clarify issues) o Grossing of Results o Estimation of Non-response Bias o Supply of retrieval database to Defra o Assessment of previous Year’s Survey o Final Reporting and Feedback

Progress of the survey is guided by a Steering Group comprising of representatives from Defra,

Department for Trade and Industry (DTI), Environment Agency, Scottish Environmental Protection

Agency (SEPA) and the Office for National Statistics (ONS). URS are grateful for the guidance and

assistance provided by the Steering Group.

A few of the activities described above are discussed in detail below. These include introducing

modifications for 2003 survey, preparation of sampling methodology, changes in the database design,

and survey promotion.

5645R/46059-003-784/SV Final Report June 2005

6

2.1 MODIFICATIONS INTRODUCED IN THE 2003 SURVEY

Several modifications that were introduced during previous surveys were carried through to the 2003

survey, which in particular sought to improve awareness, help with definition issues and widen

ownership of the survey. These include for example the following activities:

• In order to continue to reduce respondent burden, micro sized companies, companies with 1 to 9

employees, were again excluded from the survey in 2003. In addition, small to medium sized

enterprises (SMEs), companies with between 10 and 50 employees, received a simplified cover

letter that asked them to complete only specific questions. Larger SMEs, large companies

(companies 250 plus employees) and top companies (specifically selected based on their

employee number and turnover as well as if they had responded to a number of previous

surveys) all received slightly different cover letters emphasising different issues. The definitions

of these company groups are explained in full in section 3.1 and the cover letters can be seen in

Annex 1.

• Helpdesk staff were trained to encourage companies to fill in specific / minimum questions in

cases where they felt that the survey was not relevant to them. This approach was carried over

from the previous surveys, as it proved useful in persuading companies to respond when they

contacted the Helpdesk.

• At the data entry stage, validation of internal inconsistencies and calculation errors were carried

out continuously during data entry, using a process specifically built into the Access database. In

addition to these inconsistency checks all of the other validation checks were built into the

database for the 2002 survey. The list of validation checks was updated to correspond to the

new 2003 survey form. This approach was continued because it made the further validation

process easier and quicker. It also enabled companies to be contacted with any queries fairly

soon after they had returned the questionnaire, while the information was still fresh in their

minds.

A number of new modifications were introduced for the survey in 2003, which aimed to reduce the

burden on respondents as well as to increase the response rate. These included the following

activities:

• The survey period was increased from ten to twelve weeks to allow enough time for completion

during a busy period of the year, and also to allow enough time for the questionnaire to reach the

right person within the company. In addition, to increasing the survey period, survey returns

were accepted several weeks after the final deadline.

5645R/46059-003-784/SV Final Report June 2005

7

• Chasing of Top Companies was increased by sending an additional e-mail to the companies’

general helpdesks, using the information that was available on their websites. The email

requested a contact name and email address of the person who was specifically responsible for

this type of information. Subsequently, the survey was sent to this contact, with a request to

complete the necessary information.

2.2 SAMPLING METHODOLOGY

The final stage of preparation involved selecting the sample of companies, which would be sent the

final questionnaire. In 2003, 8,142 companies were sampled across the extraction, manufacturing,

energy and water supply industries (see Figure 2.1 below a breakdown of the industry sectors

covered by the survey). A census was taken of the larger companies (companies with 250 plus

employees) with a stratified sampling approach, weighted towards the industry sectors with high

expenditure rates in the past, used to sample the smaller companies. The sampling procedure was

also designed to optimise the sample in terms of the sectors where the expenditure would be

greatest. The sampling methodology is described in full in Annex 2.

Figure 2.1 Industry sectors covered by the survey

SIC code Industry 10 – 14 Mining & Quarrying 15 – 37 Manufacturing 15-16 17-19 20 21-22 23 24-25 26 27 28-36

Food, beverages and tobacco products Textiles Wood and wood products Pulp, paper and printing Coke, petroleum and nuclear fuel Chemicals, plastics and rubber Non-metallic mineral products Basic metals Other manufacturing

40-41 Electricity, gas & water. 2.3 DATABASE DESIGN

The 2002 survey database was re-developed for the 2003 survey. The database was designed and

built using Microsoft Access 2000 to store information from the surveys. The database was intended

for use by:

• URS personnel gathering information from postal questionnaires and other correspondence;

5645R/46059-003-784/SV Final Report June 2005

8

• URS personnel to carry out continuous validation checks of the data entry process and to record

all of the phone calls made to the responding companies when confirming the data; and

• URS personnel conducting statistical analysis of each year’s data.

The database was re-developed for the 2003 survey to incorporate some additional validation tests.

Some of the data from the previous survey was retained within the database to allow for comparisons

to be made. Validation checks incorporated into the database are shown in Annex 3.

There are a number of advantages of building the validation checks into the data entry system:

1. Checks could be run more frequently;

2. The results of any follow up calls or validation changes were recorded;

3. The validation tests took account of the data types and conversions;

4. There was no delay between the data entry and the return of the validation checks; and

5. Companies could be contacted promptly after returning their completed questionnaires with any

queries.

After the validation tests were run, the results were stored for manual validation. The records within

the list would not change until the validation tests were run again.

2.4 SURVEY PROMOTION

Survey promotion was carried out as previously. A separate article was published independently by

ENDS, which is presented in Annex 4.

5645R/46059-003-784/SV Final Report June 2005

9

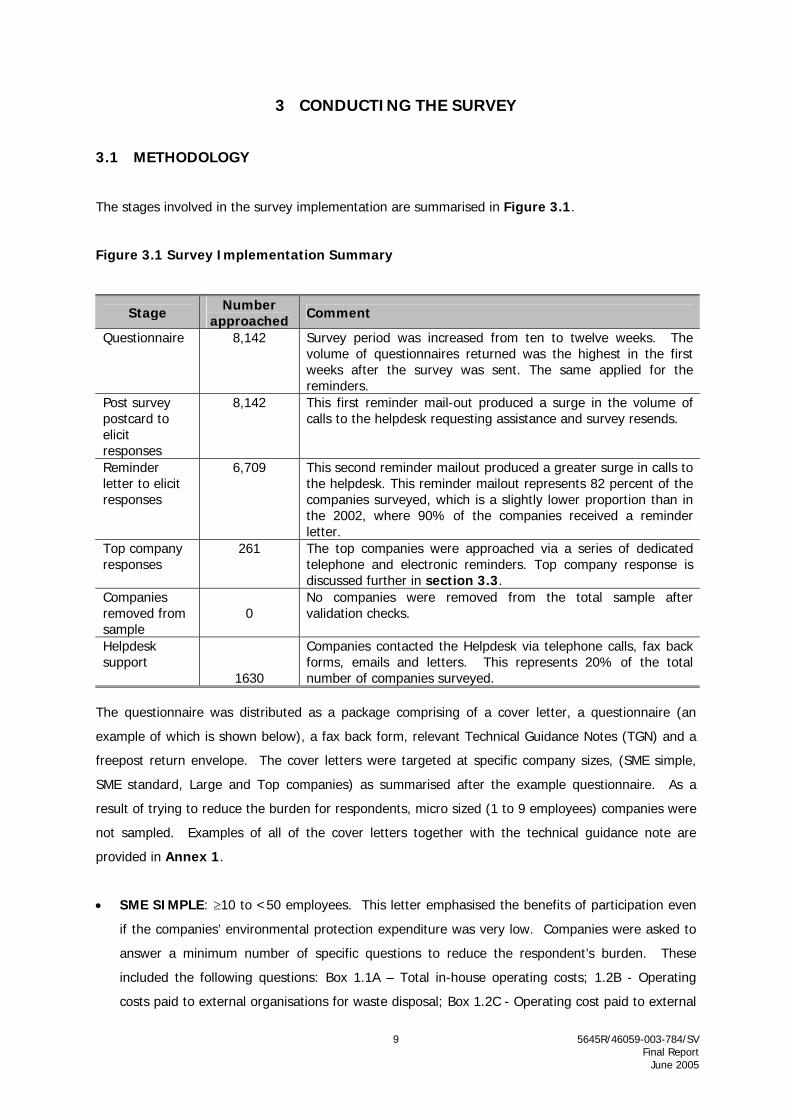

3 CONDUCTING THE SURVEY

3.1 METHODOLOGY

The stages involved in the survey implementation are summarised in Figure 3.1.

Figure 3.1 Survey Implementation Summary

Stage Number approached Comment

Questionnaire 8,142 Survey period was increased from ten to twelve weeks. The volume of questionnaires returned was the highest in the first weeks after the survey was sent. The same applied for the reminders.

Post survey postcard to elicit responses

8,142 This first reminder mail-out produced a surge in the volume of calls to the helpdesk requesting assistance and survey resends.

Reminder letter to elicit responses

6,709 This second reminder mailout produced a greater surge in calls to the helpdesk. This reminder mailout represents 82 percent of the companies surveyed, which is a slightly lower proportion than in the 2002, where 90% of the companies received a reminder letter.

Top company responses

261 The top companies were approached via a series of dedicated telephone and electronic reminders. Top company response is discussed further in section 3.3.

Companies removed from sample

0

No companies were removed from the total sample after validation checks.

Helpdesk support

1630

Companies contacted the Helpdesk via telephone calls, fax back forms, emails and letters. This represents 20% of the total number of companies surveyed.

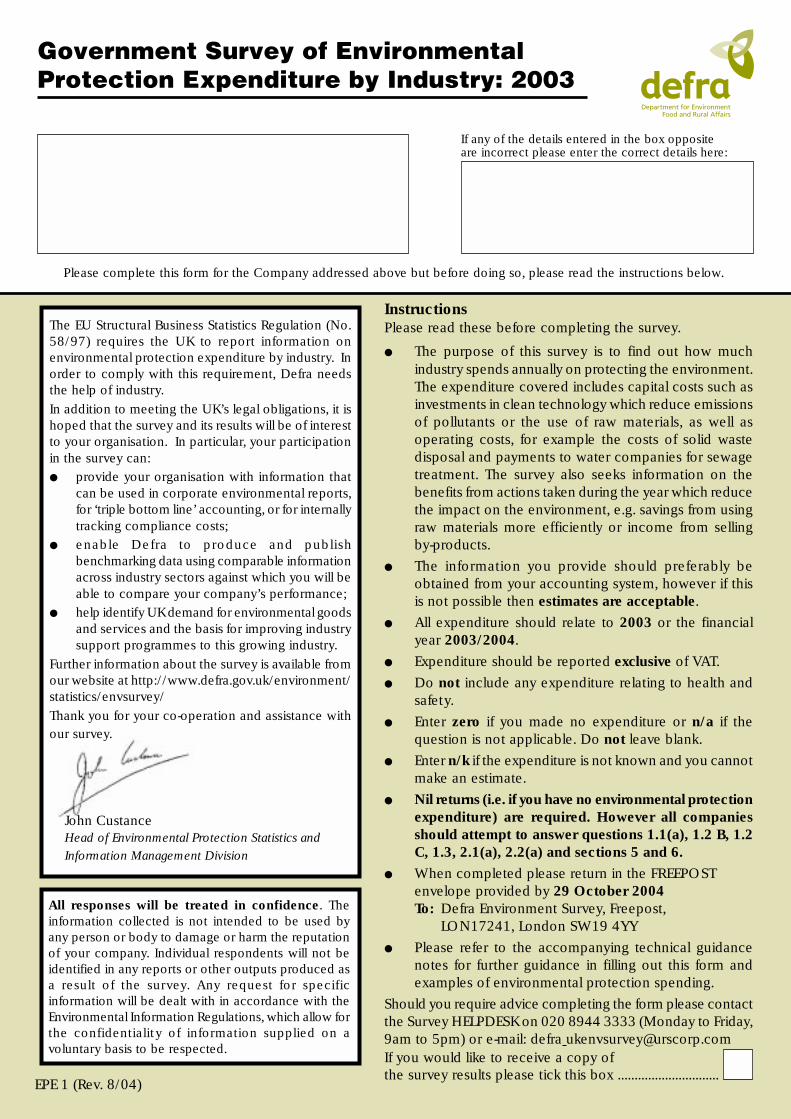

The questionnaire was distributed as a package comprising of a cover letter, a questionnaire (an

example of which is shown below), a fax back form, relevant Technical Guidance Notes (TGN) and a

freepost return envelope. The cover letters were targeted at specific company sizes, (SME simple,

SME standard, Large and Top companies) as summarised after the example questionnaire. As a

result of trying to reduce the burden for respondents, micro sized (1 to 9 employees) companies were

not sampled. Examples of all of the cover letters together with the technical guidance note are

provided in Annex 1.

• SME SIMPLE: ≥10 to <50 employees. This letter emphasised the benefits of participation even

if the companies’ environmental protection expenditure was very low. Companies were asked to

answer a minimum number of specific questions to reduce the respondent’s burden. These

included the following questions: Box 1.1A – Total in-house operating costs; 1.2B - Operating

costs paid to external organisations for waste disposal; Box 1.2C - Operating cost paid to external

Government Survey of EnvironmentalProtection Expenditure by Industry: 2003

If any of the details entered in the box oppositeare incorrect please enter the correct details here:

Please complete this form for the Company addressed above but before doing so, please read the instructions below.

InstructionsPlease read these before completing the survey.

● The purpose of this survey is to find out how muchindustry spends annually on protecting the environment.The expenditure covered includes capital costs such asinvestments in clean technology which reduce emissionsof pollutants or the use of raw materials, as well asoperating costs, for example the costs of solid wastedisposal and payments to water companies for sewagetreatment. The survey also seeks information on thebenefits from actions taken during the year which reducethe impact on the environment, e.g. savings from usingraw materials more efficiently or income from sellingby-products.

● The information you provide should preferably beobtained from your accounting system, however if thisis not possible then estimates are acceptable.

● All expenditure should relate to 2003 or the financialyear 2003/2004.

● Expenditure should be reported exclusive of VAT.

● Do not include any expenditure relating to health andsafety.

● Enter zero if you made no expenditure or n/a if thequestion is not applicable. Do not leave blank.

● Enter n/k if the expenditure is not known and you cannotmake an estimate.

● Nil returns (i.e. if you have no environmental protectionexpenditure) are required. However all companiesshould attempt to answer questions 1.1(a), 1.2 B, 1.2C, 1.3, 2.1(a), 2.2(a) and sections 5 and 6.

● When completed please return in the FREEPOSTenvelope provided by 29 October 2004To: Defra Environment Survey, Freepost,

LON17241, London SW19 4YY

● Please refer to the accompanying technical guidancenotes for further guidance in filling out this form andexamples of environmental protection spending.

Should you require advice completing the form please contactthe Survey HELPDESK on 020 8944 3333 (Monday to Friday,9am to 5pm) or e-mail: defra [email protected] you would like to receive a copy ofthe survey results please tick this box ..............................

EPE 1 (Rev. 8/04)

The EU Structural Business Statistics Regulation (No.58/97) requires the UK to report information onenvironmental protection expenditure by industry. Inorder to comply with this requirement, Defra needsthe help of industry.In addition to meeting the UK’s legal obligations, it ishoped that the survey and its results will be of interestto your organisation. In particular, your participationin the survey can:● provide your organisation with information that

can be used in corporate environmental reports,for ‘triple bottom line’ accounting, or for internallytracking compliance costs;

● enable Defra to produce and publishbenchmarking data using comparable informationacross industry sectors against which you will beable to compare your company’s performance;

● help identify UK demand for environmental goodsand services and the basis for improving industrysupport programmes to this growing industry.

Further information about the survey is available fromour website at http://www.defra.gov.uk/environment/statistics/envsurvey/Thank you for your co-operation and assistance withour survey.

John CustanceHead of Environmental Protection Statistics andInformation Management Division

All responses will be treated in confidence. Theinformation collected is not intended to be used byany person or body to damage or harm the reputationof your company. Individual respondents will not beidentified in any reports or other outputs produced asa result of the survey. Any request for specificinformation will be dealt with in accordance with theEnvironmental Information Regulations, which allow forthe confidentiality of information supplied on avoluntary basis to be respected.

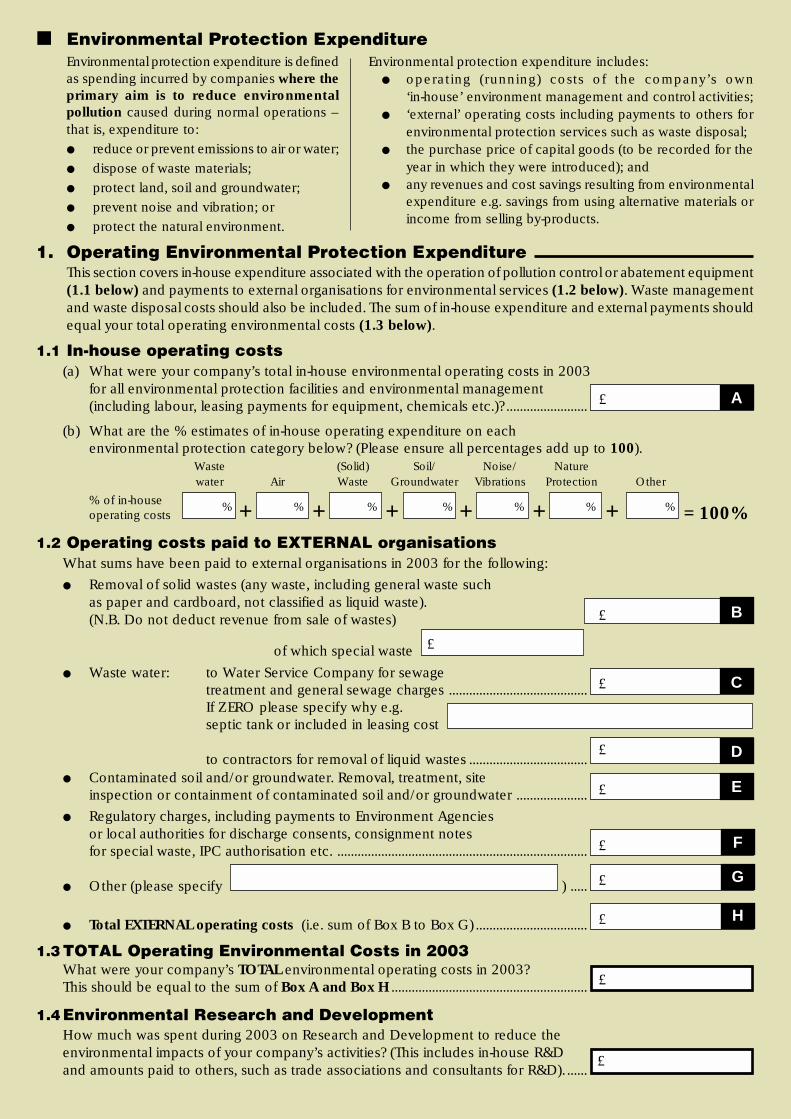

■ Environmental Protection ExpenditureEnvironmental protection expenditure is definedas spending incurred by companies where theprimary aim is to reduce environmentalpollution caused during normal operations –that is, expenditure to:● reduce or prevent emissions to air or water;● dispose of waste materials;● protect land, soil and groundwater;● prevent noise and vibration; or● protect the natural environment.

Environmental protection expenditure includes:● operating (running) costs of the company’s own

‘in-house’ environment management and control activities;● ‘external’ operating costs including payments to others for

environmental protection services such as waste disposal;● the purchase price of capital goods (to be recorded for the

year in which they were introduced); and● any revenues and cost savings resulting from environmental

expenditure e.g. savings from using alternative materials orincome from selling by-products.

1. Operating Environmental Protection ExpenditureThis section covers in-house expenditure associated with the operation of pollution control or abatement equipment(1.1 below) and payments to external organisations for environmental services (1.2 below). Waste managementand waste disposal costs should also be included. The sum of in-house expenditure and external payments shouldequal your total operating environmental costs (1.3 below).

1.1 In-house operating costs(a) What were your company’s total in-house environmental operating costs in 2003

for all environmental protection facilities and environmental management(including labour, leasing payments for equipment, chemicals etc.)? ........................

(b) What are the % estimates of in-house operating expenditure on eachenvironmental protection category below? (Please ensure all percentages add up to 100).

Waste (Solid) Soil/ Noise/ Naturewater Air Waste Groundwater Vibrations Protection Other

% of in-houseoperating costs + + + + + + = 100%

1.2 Operating costs paid to EXTERNAL organisationsWhat sums have been paid to external organisations in 2003 for the following:

● Removal of solid wastes (any waste, including general waste suchas paper and cardboard, not classified as liquid waste).(N.B. Do not deduct revenue from sale of wastes)

of which special waste

● Waste water: to Water Service Company for sewagetreatment and general sewage charges .........................................If ZERO please specify why e.g.septic tank or included in leasing cost

to contractors for removal of liquid wastes ...................................● Contaminated soil and/or groundwater. Removal, treatment, site

inspection or containment of contaminated soil and/or groundwater .....................

● Regulatory charges, including payments to Environment Agenciesor local authorities for discharge consents, consignment notesfor special waste, IPC authorisation etc. ..........................................................................

● Other (please specify ) .....

● Total EXTERNAL operating costs (i.e. sum of Box B to Box G) .................................

1.3 TOTAL Operating Environmental Costs in 2003What were your company’s TOTAL environmental operating costs in 2003?This should be equal to the sum of Box A and Box H ..........................................................

1.4Environmental Research and DevelopmentHow much was spent during 2003 on Research and Development to reduce theenvironmental impacts of your company’s activities? (This includes in-house R&Dand amounts paid to others, such as trade associations and consultants for R&D). ......

£

£

£

£

% % % % % % %

£

A

B

C

£

£

£

£

£

£

D

E

F

G

H

2. Capital Environmental Protection Expenditures

2.1 ‘End-of-Pipe’ Capital Expenditure‘End-of-pipe’ equipment is used to treat, handle, measure or dispose of emissions and wastes from production,but not equipment which is used in, or as part of, production processes or installations (covered in 2.2 below).Examples of ‘end-of-pipe’ equipment include effluent treatment plant and exhaust air scrubbing systems.

For further examples refer to the technical guidance notes.

(a) What was your company’s total capital expenditure (exclusive of VAT)on ‘end-of-pipe’ pollution control equipment, which became operationalin 2003, including equipment and installation costs? ...................................................

(b) What are the % estimates of 2003 ‘end-of-pipe’ capital expenditure on eachenvironmental protection category below? (Please ensure all percentages add up to 100).

Waste (Solid) Soil/ Noise/ Naturewater Air Waste Groundwater Vibrations Protection Other% of ‘end of

pipe’ capitalexpenditure + + + + + + = 100%

(c) Please provide a brief description of the main ‘end-of-pipe‘ capital expenditure.

2.2 ‘Integrated’ Capital Expenditure‘Integrated’ capital expenditure relates to new or modified production facilities, which have been designed sothat environmental protection is an integral part of the process.

(a) Most new integrated processes are more efficient and contribute to reducingpollution and/or the use of raw materials in some way. What was the totalexpenditure on such integrated processes that became operational in 2003? .......

(b) The primary aim of some of the expenditure recorded in 2.2(a) may not beto reduce environmental pollution. What is the element that specifically relatesto the additional cost of environmentally friendly processes? .....................................For example, if a new production process was installed in which the design takes account of environmental protection requirements,the environmental protection expenditure comprises the extra cost compared with a cheaper and less environmentally friendlyalternative. It can also include the adaptation of an existing installation/process. The environmental protection expenditure is then thetotal purchase cost of the adaptation.

(c) Of the expenditure recorded in 2.2(b), what are the percentages on each of the environmental protectioncategories shown below? (Please ensure all percentages add up to 100).

Waste (Solid) Soil/ Noise/ Nature% ofwater Air Waste Groundwater Vibrations Protection Other‘integrated’

capitalexpenditure + + + + + + = 100%

(d) Please provide a brief description of the main ‘integrated’ capital expenditure.

3. Cost Savings and IncomeThis section covers cost savings or income arising from expenditures or processchanges taken in 2003 that have resulted in environmental improvements.

3.1 Annualised cost savings resulting from:

(i) improved use of or substitution of raw materials ...........................................................

(ii) reductions in water use or production of effluent .........................................................

(iii) reductions in energy use......................................................................................................

(iv) savings in waste disposal costs ...........................................................................................

(v) other .........................................................................................................................................

% % % % % % %

% % % % % % %

£

£

£

£

£

£

£

£

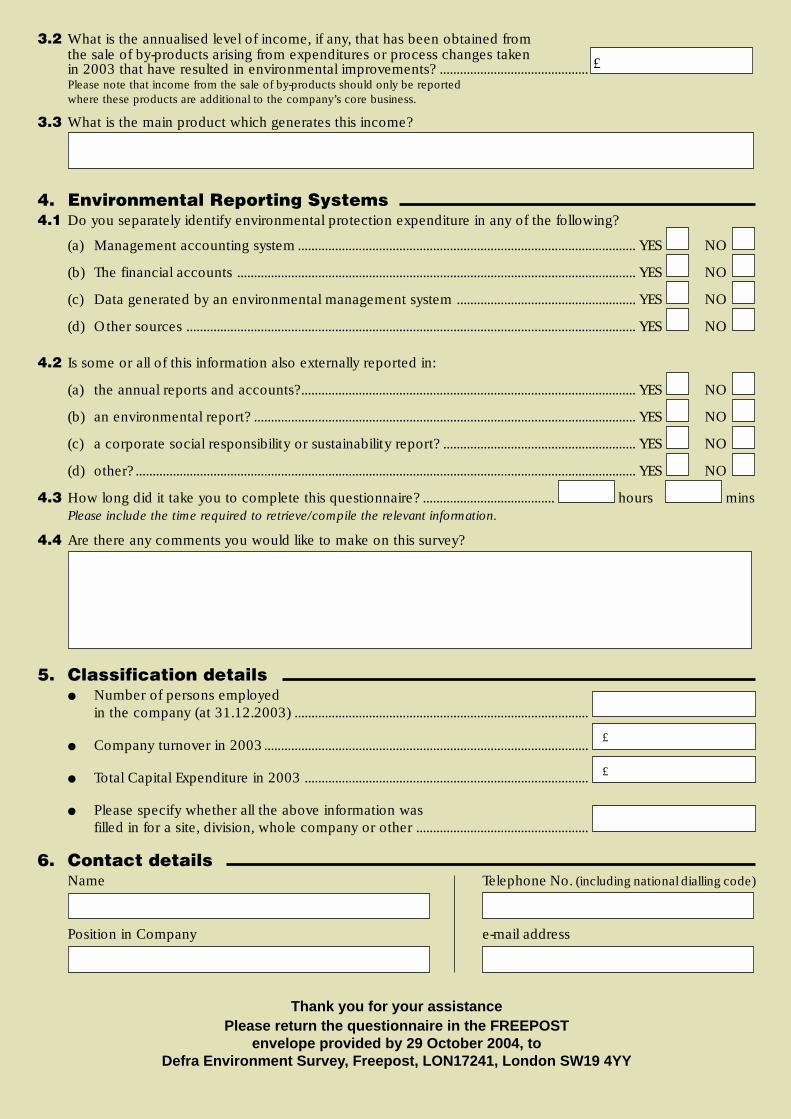

5. Classification details● Number of persons employed

in the company (at 31.12.2003) .......................................................................................

● Company turnover in 2003................................................................................................

● Total Capital Expenditure in 2003 ....................................................................................

● Please specify whether all the above information wasfilled in for a site, division, whole company or other ...................................................

6. Contact detailsName Telephone No. (including national dialling code)

Position in Company e-mail address

Thank you for your assistancePlease return the questionnaire in the FREEPOST

envelope provided by 29 October 2004, toDefra Environment Survey, Freepost, LON17241, London SW19 4YY

£

£

3.2 What is the annualised level of income, if any, that has been obtained fromthe sale of by-products arising from expenditures or process changes takenin 2003 that have resulted in environmental improvements? ............................................Please note that income from the sale of by-products should only be reportedwhere these products are additional to the company’s core business.

3.3 What is the main product which generates this income?

4. Environmental Reporting Systems4.1 Do you separately identify environmental protection expenditure in any of the following?

(a) Management accounting system .................................................................................................... YES NO

(b) The financial accounts ...................................................................................................................... YES NO

(c) Data generated by an environmental management system ..................................................... YES NO

(d) Other sources ..................................................................................................................................... YES NO

4.2 Is some or all of this information also externally reported in:

(a) the annual reports and accounts?................................................................................................... YES NO

(b) an environmental report? ................................................................................................................. YES NO

(c) a corporate social responsibility or sustainability report? ......................................................... YES NO

(d) other? .................................................................................................................................................... YES NO

4.3 How long did it take you to complete this questionnaire? ....................................... hours minsPlease include the time required to retrieve/compile the relevant information.

4.4 Are there any comments you would like to make on this survey?

£

5645R/46059-003-784/SV Final Report June 2005

10

organisations for wastewater disposal; Box 1.3 - Total environmental operating costs in 2002; Box

2.1a - Total 'end of pipe' capital expenditure; Box 2.2a - Total 'integrated' expenditure; and

Sections 4, 5 and 6 – Completing information on environmental reporting systems, the

classification and company contact details;

• SME STANDARD:≥50 to <250 employees. The letter concentrated on emphasising the benefits

of participation to this size of company as the performance benchmarking and environmental

compliance;

• LARGE: ≥ 250 employees, excluding the top 261 companies. The letter emphasised the benefits

of participation by including Turnbull Guidance. The information collated in the survey may be

used to satisfy the corporate governance requirements; and

• TOP COMPANIES: ≥ 250 employees, selected companies from a ranked pool of the top 261

companies ranked by turnover and employee numbers. In addition to companies selected by

turnover and employee number, the 28 companies that did not respond in 2002 but did respond

in 1999, 2000, and 2001, and the 40 companies that did not respond in 2002 survey but did in

2000 and 2001, were also selected as Top Companies.

A change in methodology for the 2001 survey meant those companies with fewer than 10 employees

were excluded from the sample frame. This approach was continued for the 2002 and 2003 surveys

and the adjustment allowed more sampling to occur for companies with 10 to 249 employees. It was

felt that this change could be continued in 2003 because there seemed to be no real difference

between the expenditure per employee for the different size bands.

This change also aimed to improve the confidence intervals in the estimation of expenditure, and had

the added benefit of reducing the burden placed on the smallest companies. However the removal of

a complete section of the population meant that additional qualifications needed to be made

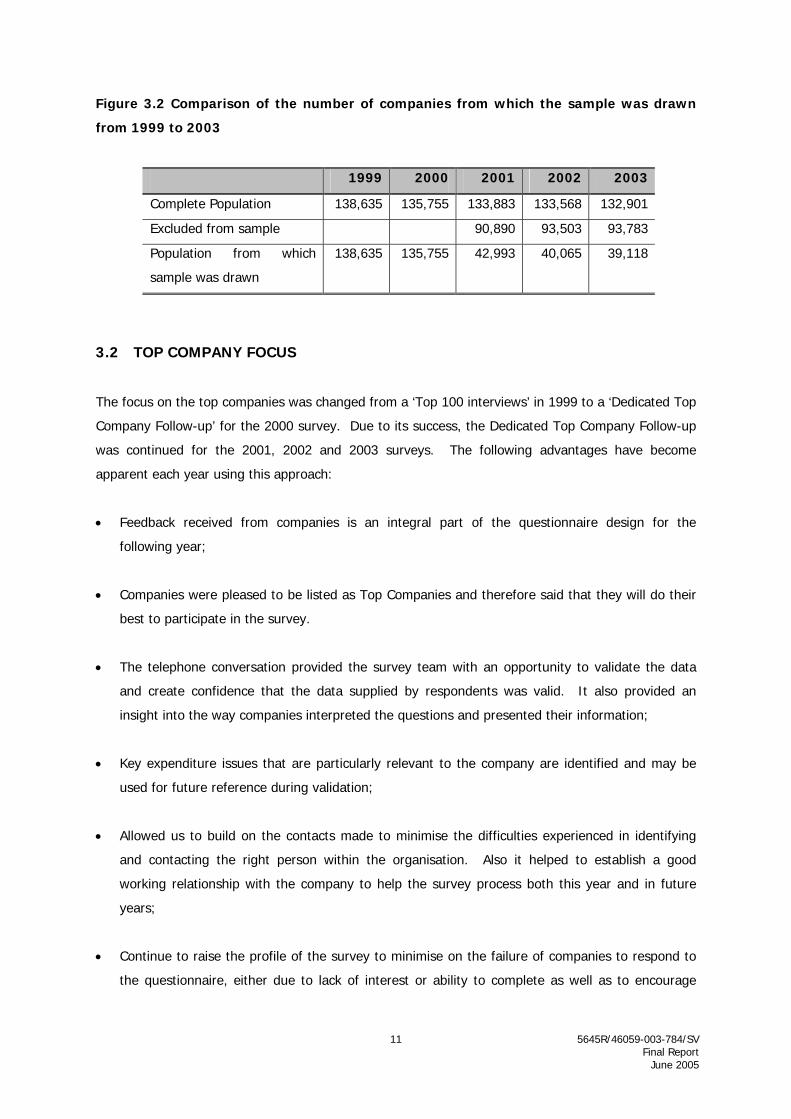

regarding the results of the survey. A comparison of the number of companies from which the

sample was drawn shows the clear effect of excluding the companies with under 10 employees as

seen in Figure 3.2.

5645R/46059-003-784/SV Final Report June 2005

11

Figure 3.2 Comparison of the number of companies from which the sample was drawn

from 1999 to 2003

1999 2000 2001 2002 2003

Complete Population 138,635 135,755 133,883 133,568 132,901

Excluded from sample 90,890 93,503 93,783

Population from which

sample was drawn

138,635 135,755 42,993 40,065 39,118

3.2 TOP COMPANY FOCUS

The focus on the top companies was changed from a ‘Top 100 interviews’ in 1999 to a ‘Dedicated Top

Company Follow-up’ for the 2000 survey. Due to its success, the Dedicated Top Company Follow-up

was continued for the 2001, 2002 and 2003 surveys. The following advantages have become

apparent each year using this approach:

• Feedback received from companies is an integral part of the questionnaire design for the

following year;

• Companies were pleased to be listed as Top Companies and therefore said that they will do their

best to participate in the survey.

• The telephone conversation provided the survey team with an opportunity to validate the data

and create confidence that the data supplied by respondents was valid. It also provided an

insight into the way companies interpreted the questions and presented their information;

• Key expenditure issues that are particularly relevant to the company are identified and may be

used for future reference during validation;

• Allowed us to build on the contacts made to minimise the difficulties experienced in identifying

and contacting the right person within the organisation. Also it helped to establish a good

working relationship with the company to help the survey process both this year and in future

years;

• Continue to raise the profile of the survey to minimise on the failure of companies to respond to

the questionnaire, either due to lack of interest or ability to complete as well as to encourage

5645R/46059-003-784/SV Final Report June 2005

12

companies to allocate time/resources to complete the survey and set up their accounting systems

to account for the required environmental protection expenditure information; and

• Continue to raise the profile to encourage response from the larger multi-nationals with a policy

of not partaking in voluntary surveys.

In addition to the standard Top Company Follow-up carried over from the previous years surveys, an

extra dimension was added into the process for the 2003 survey. For those Top Companies where

the contact person was not reachable by phone, an additional e-mail was sent to the companies’

general helpdesk, utilising the information they provided on their websites, enquiring whom the

appropriate person would be to contact with regards to the survey. The questionnaire and

corresponding material was then sent to the contact. The number of queries sent to a general

helpdesk was 51 and as a result contact was made with 7 companies. It is not possible to say which

survey returns are a direct result of the additional e-mail sent to the companies’ general helpdesk due

to the variety of methods used to contact the Top Companies and the difficulty in identifying exactly

why a company responded.

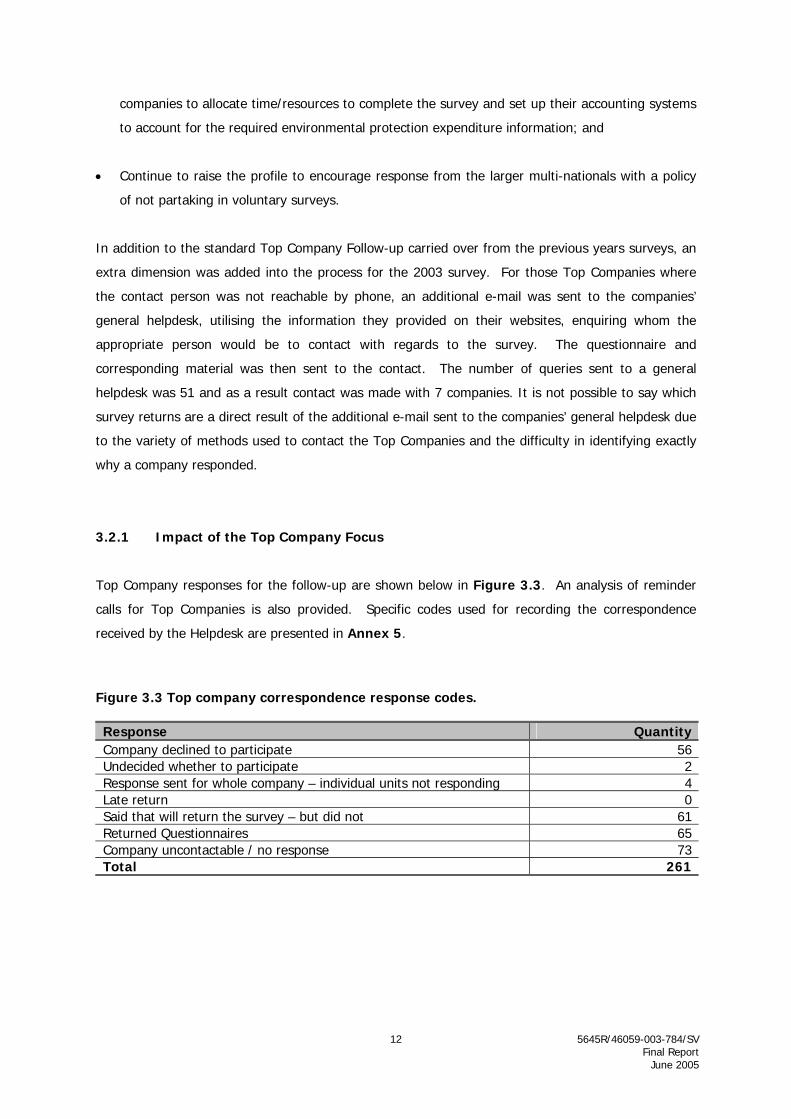

3.2.1 Impact of the Top Company Focus

Top Company responses for the follow-up are shown below in Figure 3.3. An analysis of reminder

calls for Top Companies is also provided. Specific codes used for recording the correspondence

received by the Helpdesk are presented in Annex 5.

Figure 3.3 Top company correspondence response codes. Response QuantityCompany declined to participate 56Undecided whether to participate 2Response sent for whole company – individual units not responding 4Late return 0Said that will return the survey – but did not 61Returned Questionnaires 65Company uncontactable / no response 73Total 261

5645R/46059-003-784/SV Final Report June 2005

13

3.2.2 Lessons learnt from the Dedicated Top Company Follow-up

During the reminder call phase for the Top Companies, more detail was noted during the telephone

conversations than at any previous stage. As a result, more specific analysis could be conducted

from this Top Company Follow-up. Key findings include:

• For the Top Companies that declined to participate in this year’s survey (2003) the most common

reasons were the same as in previous surveys. These included that next year would be more

convenient and that they did not have the resources or time available at present to complete the

survey. A commonly occurring reason was that the information that would support a response

was not readily available. Related to this, another reason was that due to the size and nature of

the companies, gathering the required information would necessitate too much time to be

devoted to it as the company’s accounting procedures do not separately identify environmental

protection expenditure; and

• Requests for resends were particularly prevalent where questionnaires had been sent to

unnamed persons and hence had gone missing or passed on from department to department, or

from person to person. As a result there was difficulty in finding the person made responsible for

its completion to remind them about the deadline.

It may be concluded that the numerous reminder calls made to these companies (with a majority of

the Top Companies being called at least three times or until a definite response was received) helped

to achieve a good response. In addition it is suggested that the timing of the 2003 survey suited

companies particularly well as it did not overlap with the end of year and Christmas periods as in

2002. 65 survey returns from 261 Top Companies gives a response rate of 25 per cent, which is an

increase on the 2002 response rate of 20 per cent. The highest responding sectors were Wood and

Wood Products (100%), Fabricated Metal Products (50%) and Furniture Manufacture (50%). Sectors

with the lowest response rates were Textiles (0%), Leather Products (0%) and Publishing & Printing

(0%).

5645R/46059-003-784/SV Final Report June 2005

14

3.3 SME SIMPLIFIED APPROACH

The expanded SME approach used for the 2001 and 2002 survey was continued in 2003. Hence, for

the 2001, 2002 and 2003 surveys, all companies with between 10 and 49 employees received a

simplified request. In contrast, the 2000 survey, half of the SME Simple and all of the micro-sized

companies received this simplified cover letter, and the other half received a standard cover letter.

The simplified cover letter instructed companies to answer specific questions. The specific questions

included the following:

• Box A in section 1.1 – Total in-house operating costs;

• Box B in section 1.2 - Operating costs paid to external organisations covering waste disposal;

• Box C in section 1.2 - Operating costs paid to external organisations covering wastewater

disposal;

• Box 1.3 - Total environmental operating costs in 2002;

• Box 2.1a - Total 'end of pipe' capital expenditure;

• Box 2.2a - Total 'integrated' expenditure; and

• Sections 5 and 6 - Complete the classification and contact details sections (see questionnaire for

further detail).

Companies in other categories (SME Standard, Large and Top) received the standard cover letters,

which instructed companies to answer all of the questions. The standard letter emphasised the

benefits of participation to this size of company, particularly focusing on the benefits and relevance of

the survey for performance benchmarking and environmental compliance purposes.

The highest responding sectors with the SME Simple approach included sector Collection, Purification

& Water Distribution (43%), Medical, Precision & Optical (38%), Radio, Television & Communications

(26%) and Chemical & Chemical Products – Other and Basic (26% and 25% respectively). This is

very similar to the 2002 survey with the exception of Radio, Television & Communications and Basic

Chemicals being amongst the highest 2003 respondents. In 2001 and 2002 the highest responding

sectors were Fabricated Metal Products, Chemical & Chemical Products and Machinery & Equipment.

The overall response rate of 20% within the SME Simple companies is in line with the overall

response rate for the survey. The SME Simple approach ensures that smaller companies also take

part in the survey and therefore, that the survey provides a broad representation of UK industry.

The percentage of response rates is not merely a reflection of the effect of the letter type but is also

the influence of the company’s size. As such, they should not be compared with the results of

simplified letters within the 2002 survey.

5645R/46059-003-784/SV Final Report June 2005

15

It should be noted that the majority (around 90 per cent) of the companies that received the

simplified request actually completed additional sections within the questionnaire. This extra data has

been included within the data set and subsequent analysis.

3.4 HELPDESK SUPPORT

The Helpdesk provided a key area of focus for the survey with companies using the facility to discuss

all aspects of the survey and opening a constructive dialogue between the sample population and the

URS survey team. This provided insight into the information from which the data have been derived,

allowed the data to be validated, and feedback to be obtained from companies as to their individual

experiences with the survey.

A Helpdesk telephone line, fax and email facilities were available to participating companies

throughout the entire survey period. Companies could use any or all of these methods to contact a

member of the URS survey team.

Throughout the main survey period about 1,560 calls and faxes and approximately 70 emails were

received. These facilities, in conjunction with the website, have proved to be a valuable part of the

survey process. The feedback provided has enabled the survey team to track the reasons for

participation and constraints identified by potential survey participants. Annex 6 identifies the main

drivers behind participation and also the reasons why companies declined to participate. This

feedback will be utilised when designing future surveys.

Companies that have used the Helpdesk services commented that it provided useful information,

clarification and assistance in completing the survey form. In addition, the Helpdesk phone calls were

utilised to persuade companies to respond to the questionnaire even if they thought that the survey

was not relevant to them. The URS survey team asked companies to complete the minimum

questions required including external operating cost paid for waste disposal, and for wastewater

charges, as well as the environmental reporting, company classification and contact details.

The website has been maintained and continually updated throughout the year. The website address

is: http://www.defra.gov.uk/environment/statistics/envsurvey/index.htm.

The website has been used in conjunction with the Helpdesk to provide companies with additional

copies of the questionnaire, technical guidance notes and other information relating to the survey.

Approximately 40 companies were directed to the website in order to obtain another copy of the 2003

survey or to fill it in online. When survey resends were requested the website was used as a primary

means of providing another copy of the questionnaire, a copy sent by e-mail and fax was used as a

5645R/46059-003-784/SV Final Report June 2005

16

secondary means and a postal copy was only offered as a final resort. Despite this, companies

mostly preferred to receive an additional copy of the survey by post.

In addition a web-based questionnaire was used for the 2003 in order for companies to be able to fill

in the survey online. This method of responding was encouraged through the calls received at

helpdesk. However, only handful of questionnaires filled in online were received by e-mail by the end

of the survey period. This approach was introduced to reduce the burden on respondents as well as

on the helpdesk staff and will be encouraged in the following survey. Introduction of the web-based

questionnaire was well received and provided added flexibility to the survey. It is therefore

recommended that this approach be mentioned in the survey correspondence sent to the companies.

5645R/46059-003-784/SV Final Report June 2005

17

4 ANALYSIS OF RESPONSES

4.1 RESPONSES

4.1.1 Response Rates

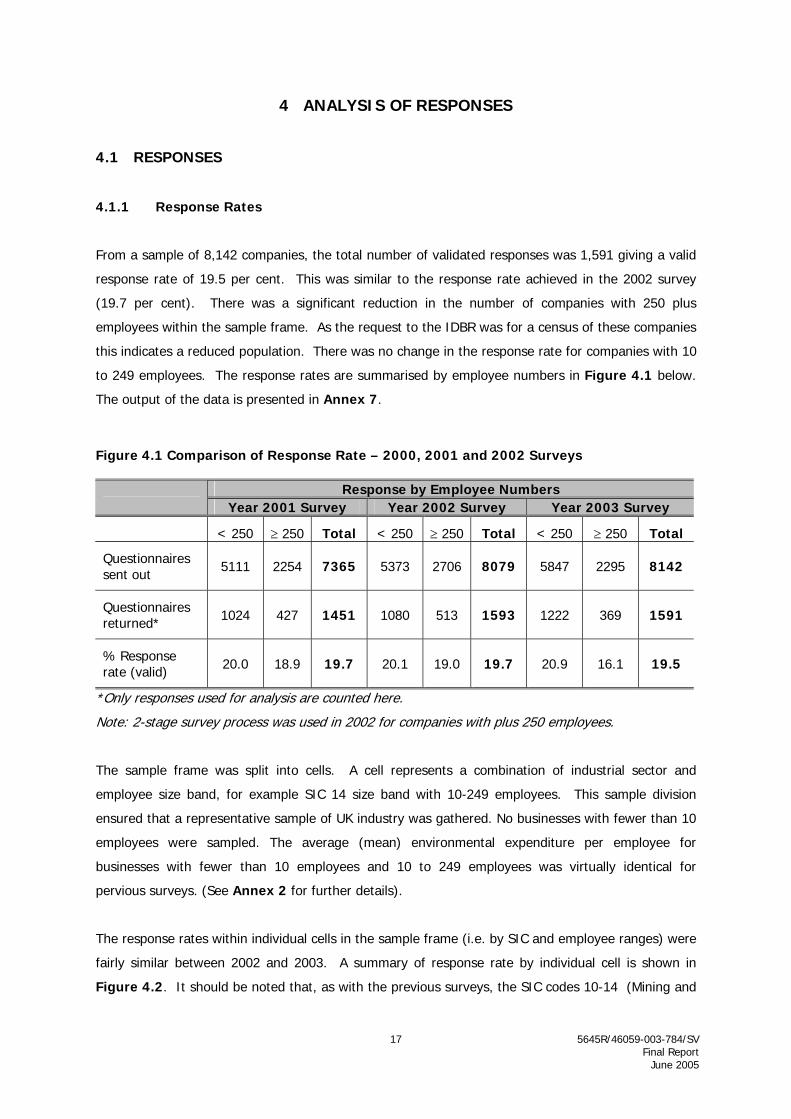

From a sample of 8,142 companies, the total number of validated responses was 1,591 giving a valid

response rate of 19.5 per cent. This was similar to the response rate achieved in the 2002 survey

(19.7 per cent). There was a significant reduction in the number of companies with 250 plus

employees within the sample frame. As the request to the IDBR was for a census of these companies

this indicates a reduced population. There was no change in the response rate for companies with 10

to 249 employees. The response rates are summarised by employee numbers in Figure 4.1 below.

The output of the data is presented in Annex 7.

Figure 4.1 Comparison of Response Rate – 2000, 2001 and 2002 Surveys

Response by Employee Numbers Year 2001 Survey Year 2002 Survey Year 2003 Survey

< 250 ≥ 250 Total < 250 ≥ 250 Total < 250 ≥ 250 Total

Questionnaires sent out 5111 2254 7365 5373 2706 8079 5847 2295 8142

Questionnaires returned* 1024 427 1451 1080 513 1593 1222 369 1591

% Response rate (valid) 20.0 18.9 19.7 20.1 19.0 19.7 20.9 16.1 19.5

*Only responses used for analysis are counted here.

Note: 2-stage survey process was used in 2002 for companies with plus 250 employees.

The sample frame was split into cells. A cell represents a combination of industrial sector and

employee size band, for example SIC 14 size band with 10-249 employees. This sample division

ensured that a representative sample of UK industry was gathered. No businesses with fewer than 10

employees were sampled. The average (mean) environmental expenditure per employee for

businesses with fewer than 10 employees and 10 to 249 employees was virtually identical for

pervious surveys. (See Annex 2 for further details).

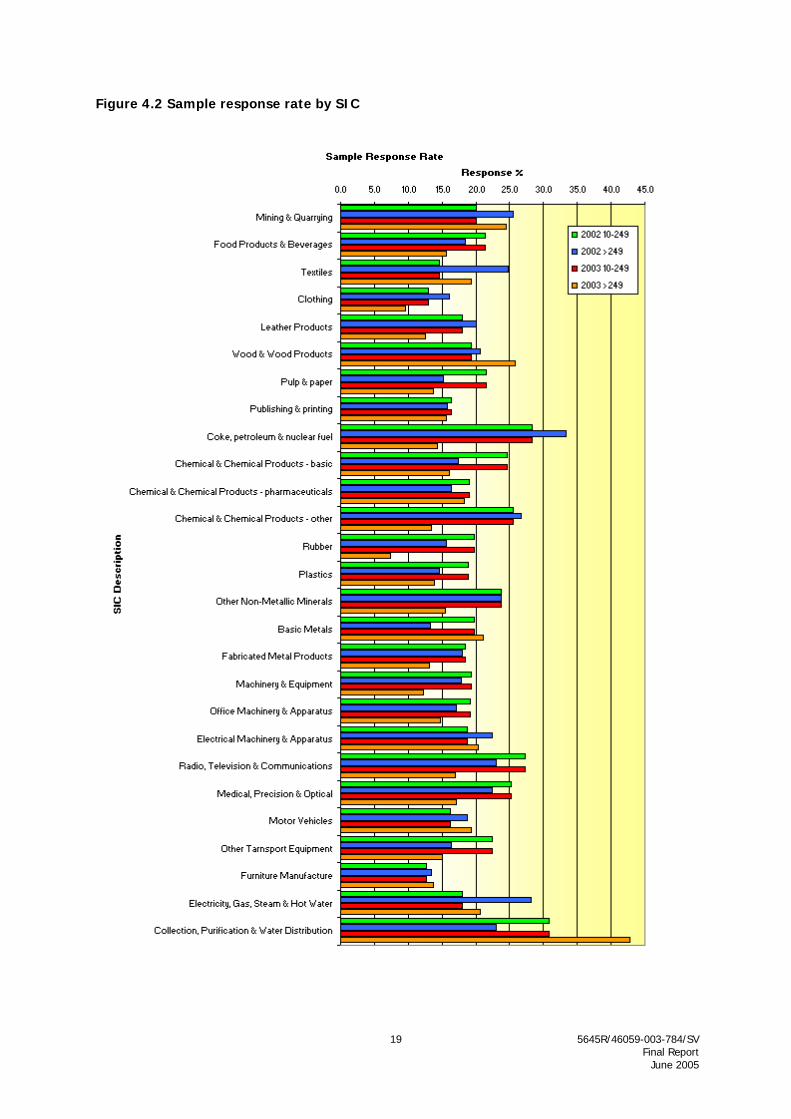

The response rates within individual cells in the sample frame (i.e. by SIC and employee ranges) were

fairly similar between 2002 and 2003. A summary of response rate by individual cell is shown in

Figure 4.2. It should be noted that, as with the previous surveys, the SIC codes 10-14 (Mining and

5645R/46059-003-784/SV Final Report June 2005

18

Quarrying) and 15 and 16 (Food Products and Beverages including Tobacco Products) are combined

for reporting purposes. Details of the valid data are presented in Annex 11.

5645R/46059-003-784/SV Final Report June 2005

19

Figure 4.2 Sample response rate by SIC

4.1.2 Weighted Response Rates

The overall response rate given above considers each company as an equal contributor to the final

results. The sample frame has, however, been designed to target higher spending sectors and the

largest employers. This means that other response rate measures may be more appropriate. A

number of alternative effective response rates are given in the Figure 4.3 below.

Figure 4.3 Alternative measures of response rate

Measure response rate by:

Sample Frame Grouping Response Rate

Census 17.8%

Non-Census 20.5%

Number of Companies

All 19.5%

Census 21.7%

Non-Census 22.8%

Number of Employees

All 21.8%

Census 26.8%

Non-Census 22.7%

Turnover

All 26.5%

Census 27.8%

Non-Census 22.0%

Spending

All 27.3%

This analysis shows that the sampling strategy is effective in targeting the highest spending sectors,

with 27 per cent of the estimated spending of the sample accounted for by respondents.

4.1.3 Repeated Responses

With five years of survey data it is possible to consider the responses of individual companies across

the five-year period. Figure 4.4 shows the distribution of repeat responses based upon the 2003

respondents. It should be noted that the opportunities to respond to the surveys are not the same

for all companies. Some may have been included in every survey, whilst for others 2003 was their

first chance to respond.

20 5645R/46059-003-784/SV Final Report June 2005

Figure 4.4 Distribution of repeat sampling

Company Size Number of times a response was received <250 >250 Total

1 586 104 690 2 529 87 616 3 71 96 167 4 22 42 64 5 15 40 55

Total 1223 369 1592 No of companies with 2 or

more responses 637 265 902

Figure 4.5 shows which of the previous surveys 2003 respondents had also returned questionnaires

for.

Figure 4.5 Yearly breakdown of repeat responses

Year Number of 2003 respondents that also responded

1999 166

2000 160

2001 247

2002 789

It is apparent that half of the respondents in 2003 had also returned the survey in 2002, whereas

only 15% of the respondents in 2003 had also returned the survey in 2001.

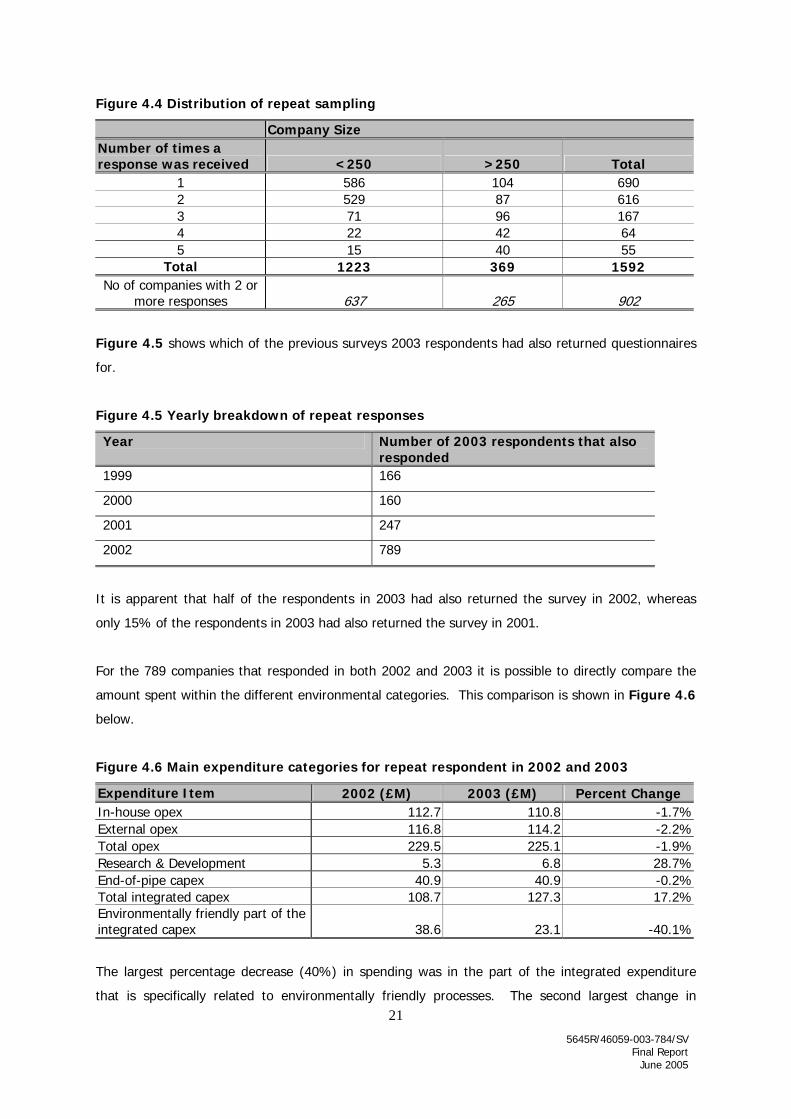

For the 789 companies that responded in both 2002 and 2003 it is possible to directly compare the

amount spent within the different environmental categories. This comparison is shown in Figure 4.6

below.

Figure 4.6 Main expenditure categories for repeat respondent in 2002 and 2003

Expenditure Item 2002 (£M) 2003 (£M) Percent Change In-house opex 112.7 110.8 -1.7%External opex 116.8 114.2 -2.2%Total opex 229.5 225.1 -1.9%Research & Development 5.3 6.8 28.7%End-of-pipe capex 40.9 40.9 -0.2%Total integrated capex 108.7 127.3 17.2%Environmentally friendly part of the integrated capex 38.6 23.1 -40.1%

The largest percentage decrease (40%) in spending was in the part of the integrated expenditure

that is specifically related to environmentally friendly processes. The second largest change in

21 5645R/46059-003-784/SV Final Report June 2005

spending was the increase (28%) in spending on research and development and the third largest is

the increase in the total spending on integrated expenditure (17%). The spending has shifted

towards the total integrated expenditure from the part of the integrated expenditure that specifically

related to environmental protection. It should be noted that the values seen in Figure 4.6 are for the

repeat respondent’s total spending without any grossing up.

4.1.4 Response Bias

There are many forms of response bias associated with this survey and these have been well

documented in previous reports. To recount, the potential sources of response bias previously

identified included:

• Companies with zero or low expenditure being more likely to respond because they have less of

the questionnaire to complete;

• Larger companies with organised environmental departments being more likely to respond

because of availability of the data;

• Possible bias from companies that have completed the survey in previous years being more likely

be able to complete one for 2003; and

• Companies that take environmental protection expenditure more seriously may well be more

likely to respond to the survey, but would be expected to have higher expenditure.

The effect of these possible biases is likely to be reduced, however, by the stratified sampling and

grossing arrangements (details of the grossing-up procedure are presented in Annex 8), that is,

using a relatively large number of cells (determined by size of company and SIC) to categorise

companies with similar characteristics – any bias is then “contained” within the cell.

The repetition of the survey over a number of years has allowed for measures to be taken to obtain a

better understanding of the potential and likely significance of these response biases. For example:

• The question on the reporting systems used indicated that most companies complete the

questionnaire without a reporting system suggesting that even without easily available data

companies do manage to respond; and

• A number of companies actually self-exclude themselves from the survey if they have zero

expenditure suggesting that zero expenditure may not increase the likelihood of a company

responding.

22 5645R/46059-003-784/SV Final Report June 2005

4.1.5 2002 vs. 2003 Methodology

In comparing the two sets of data, there are a number of factors that need to be considered. The

ranges indicated by the confidence intervals for the total expenditure are relatively large, and there

have been improvements made to the questionnaire design and estimation procedure. Hence

comparing the absolute values should be undertaken with caution. The process of generating

estimates of expenditure from the sample sets means that it is possible for one company’s

expenditure, to affect the final figure to a considerable degree. Furthermore the nature of

environmental protection expenditure is such that an individual company may make a large “one-off”

investment (e.g. capital equipment upgrade). Therefore, even though these large figures may make

a considerable difference in the final expenditure they should still be included. This principally relates

to capital expenditure rather than operating expenditure, which is generally more consistent from one

year to the next.

4.2 STANDARD ERRORS AND CONFIDENCE INTERVALS

The methodology adopted for the standard error calculation follows that used in the previous studies.

The results of the 2003 survey, in general, have similar standard errors to the equivalent results in

2002. This could be attributed to the limited number of changes made to both the sample frame and

the questionnaire between the 2002 and 2003 surveys.

The methods for deriving standard errors and 95 percent confidence intervals are presented in

Annex 9, together with the calculated standard errors and confidence limits themselves. Annex 9

explains the method of calculating standard errors (SE), for aggregates, i.e., operating expenditure,

capital expenditure, total gross, and total net expenditures.

The method followed involves aggregating the responses for each business. It is then possible to

calculate overall standard errors by using these aggregate sums. This method takes into account the

correlation between the responses to different questions by individual companies. Some companies

have zero expenditure for all questions whereas others have high expenditures for most questions.

This reflects the different types of businesses operating within particular SIC sectors. Figure 4.7

shows the standard errors for total environmental protection expenditure for different SIC sectors.

23 5645R/46059-003-784/SV Final Report June 2005

Figure 4. 7 Standard error for total environmental expenditure for different SIC sectors

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

SIC

Sta

nd

ard

Err

or /

Tot

al E

xpen

dit

ure

2000

2001

2002

2003

24 5645R/46059-003-784/SV Final Report June 2005

5 SURVEY RESULTS AND ANALYSIS

5.1 TOTAL EXPENDITURE

An estimated total of £3.4 billion was spent by UK industry on environmental protection in 2003.

Operating expenditure accounted for approximately 85 per cent of the total, with capital expenditure

making up the remainder. In-house operating costs account for nearly half of all operating costs, a

rather higher proportion than in previous years, most of the remainder being accounted for by

payments to others. Capital expenditure is dominated by spending on end-of-pipe processes, which

shows signs of decline since 2000. Spending on integrated processes is estimated at a relatively low

level of £180 million in 2003.

A summary of total expenditure is presented in Figure 5.1 in conjunction with equivalent data from

the 2000, 2001 and surveys for comparison. Ranges indicating the 95 percent confidence intervals

associated with each value are provided in parenthesis where available. As might be expected

because of the higher level of estimated expenditure, generally the interval 95 percent confidence

intervals are higher for the 2003 survey than the 2002 survey. Detailed tables of the expenditure can

be found in Annex 10. Gross spending on environmental protection in 2003 by UK industry

amounted to an estimated £3.4 billion, plus or minus £0.6 billion at 95 per cent confidence. The

estimates for previous years were £4.2 billion in 2000, £3.9 billion in 2001, and £2.6 billion in 2002.

Although a reduction in spending might have been expected as a result of the general downturn in

the manufacturing sector over the period, it now appears as if the 2002 figure is a bit of an anomaly.

Direct comparisons between survey years are not possible because the estimates are subject to wide

confidence intervals and because of improvements made over time to the questionnaire design and

estimation procedures. In light of this, comparisons will be shown as percentage shares of the total