Embed Size (px)

Citation preview

Enterprise Risk Management in the Insurance Industry

July 30, 2003 Value

Gro

wth

Retu

rn

Con

sis

ten

cy

Capital

What is Enterprise Risk Management and why is it important to the insurance industry?

Agenda

Key findings of the ERM benchmarking survey

Results of related interviews and other intelligence

Strategic implications

ERM benchmarking study

Why We Did it

Many believe ERM holds great promise Approach to help companies

achieve financial and strategic objectives

But it is unclear whether: Senior managers see the value

of ERM Companies are realizing the

value

What We Hoped to Accomplish

Determine current state of ERM in insurance industry

Judge relevance of ERM to broader business issues

Identify current management practices

Assess satisfaction with current processes, tools and techniques

We surveyed and interviewed leading insurance executives around the world

Surveyed 66 insurance industry chief financial officers, chief actuaries and chief risk officers in major markets worldwide Geography: 60% North America, 40% rest of world Company structure: stock, mutual, other Type of operations: life insurance, property/casualty insurance,

mutual funds, banking Company size: $25 million to $10 billion in direct written premiums

Supplemented with in-depth interviews/company visits

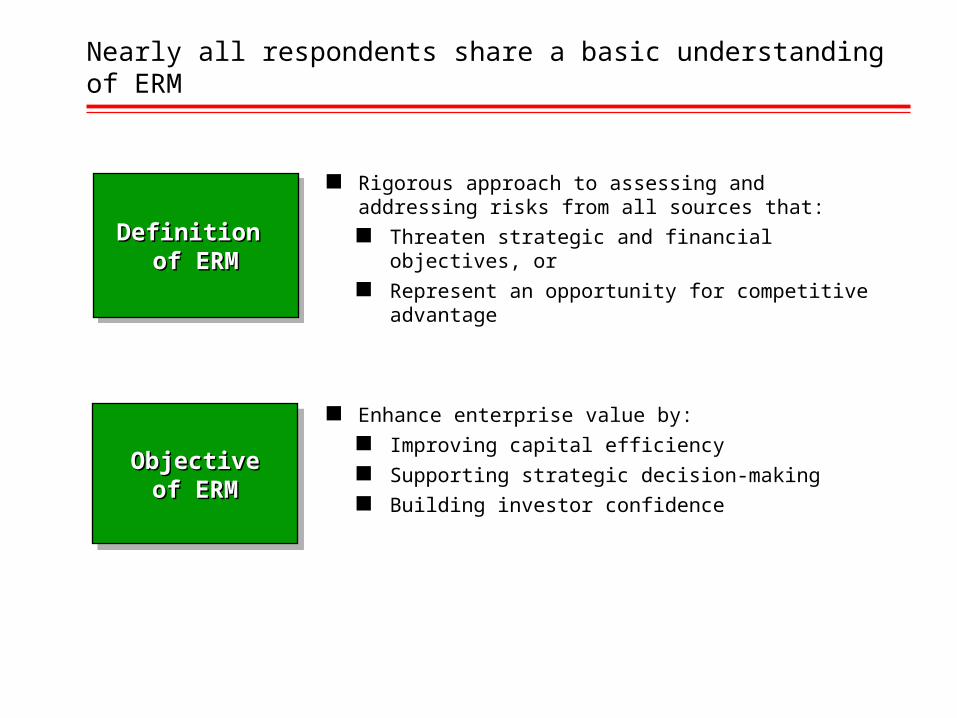

Nearly all respondents share a basic understanding of ERM

Rigorous approach to assessing and addressing risks from all sources that: Threaten strategic and financial objectives, or Represent an opportunity for competitive

advantage

Definition Definition of ERMof ERM

Definition Definition of ERMof ERM

Enhance enterprise value by: Improving capital efficiency Supporting strategic decision-making Building investor confidence

ObjectiveObjectiveof ERMof ERM

ObjectiveObjectiveof ERMof ERM

Here are our key findings in a nutshell

Executives believe ERM is critical to helping them deal with their key business issues

They are not satisfied with current tools, techniques and processes to implement ERM — especially for dealing with operational risks

They want a more robust conceptual and methodological framework that: Encompasses all relevant risks — both financial and operational Integrates both financial and operational strategies to manage those

risks

Detailed Findings

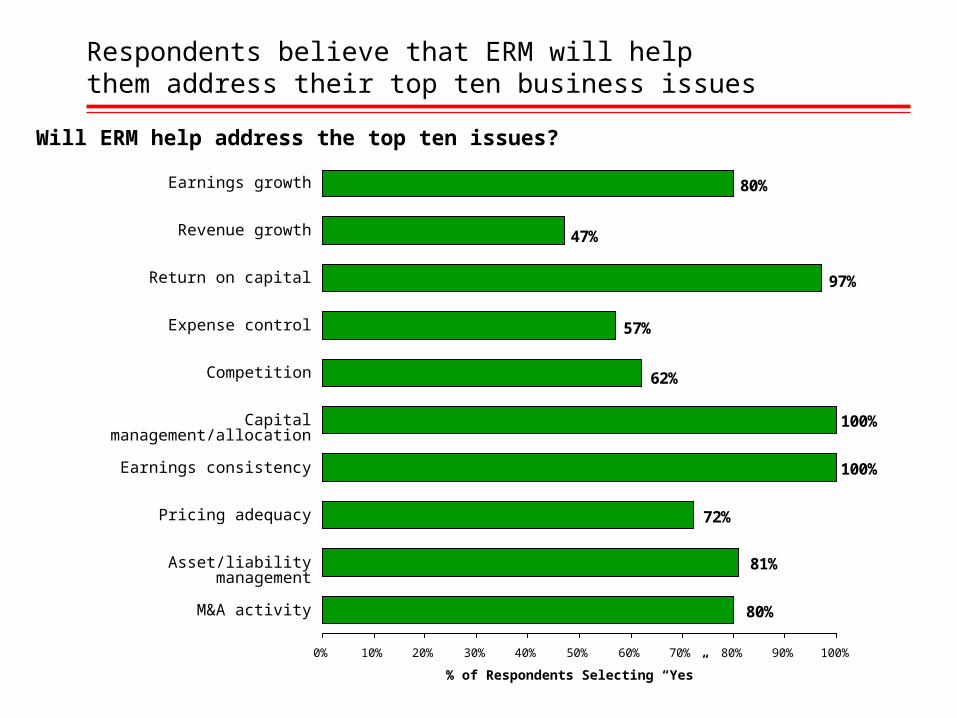

“Top Ten Issues Facing Insurers Today”

1.Earnings growth

2.Revenue growth

3.Return on capital

4.Expense control

5.Competition

6.Capital management and allocation

7.Earnings consistency

8.Pricing adequacy

9.Asset/liability management

10. M&A activity

Respondents believe that ERM will help them address their top ten business issues

% of Respondents Selecting “Yes”

80%

81%

72%

100%

100%

62%

57%

97%

47%

80%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Earnings growth

Revenue growth

Return on capital

Expense control

Competition

Pricing adequacy

Earnings consistency

Capital management/allocation

Asset/liability management

M&A activity

Will ERM help address the top ten issues?

Companies are trying to manage their most important financial and operational risks

% of Respondents Actively Managing

44%

37%

71%

76%

66%

67%

77%

88%

75%

60%

89%

92%

82%

81%

85%

89%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Technology

Are you actively managing important risks?

Interest rate

Distribution channel

Reputation/rating

Expenses

Products

People/intellectual capital

Asset market value

Liquidity

Credit

Reinvestment

Political/regulatory

Liability

Catastrophe

Capital markets

Currency

Respondents are generally satisfied with the tools they are using to manage financial risks...

87%

84%

82%

80%

77%

76%

69%

69%

75%

78%

63%

71%

71%

77%

74%

58%

69%

73%

67%

64%

71%

66%

74%

53%

Interest rate

How satisfied are you with your current tools to manage risk?

Credit

Reinvestment

Asset market value

Liability

Liquidity

Currency

Capital markets

Mitigation Retention/transferAssessment/measurement

…But they are less satisfied with the tools they are using to manage operational risks

69%

66%

66%

64%

63%

62%

61%

34%

60%

58%

61%

49%

50%

55%

53%

33%

57%

62%

56%

43%

48%

54%

49%

28%

Reputation/rating

Products

Political/regulatory

Expenses

Technology

Catastrophe

Distribution channel

People/intellectual capital

Mitigation Retention/transferAssessment/measurement

How satisfied are you with your current tools to manage risk?

Other key findings

Very few companies have a chief risk officer (CRO), although the position is much more prevalent outside of North America

Companies recognize the importance of integrating risk into their company’s strategic, operational and financial planning, but not all do so because of: Tools Organizational turf Processes Time

Most companies include operational risk in the internal audit plan, but far fewer include financial risk

Continued . . .

Other key findings

Less than half of respondents are factoring interactions among risk sources into their: Assessment/measurement Determination of diversification benefit Mitigation/financing strategies

There is a high level of dissatisfaction with respect to: Stochastically modeling the important risks Including operational risk in determining economic capital Prioritizing disparate risks using a common metric Optimizing financial and operational strategies in light of risk/reward

requirements Coordinating all these activities within a coherent framework

Strategic Implications

We see several strategic implications of the study results

Insurers face great uncertainty that challenges consistent high performance

Investors, regulators and rating agencies are demanding consistent performance, especially earnings

Insurers do not believe they have the tools to manage the risks that create the uncertainty — particularly operational risks

Insurers need an industry-specific ERM

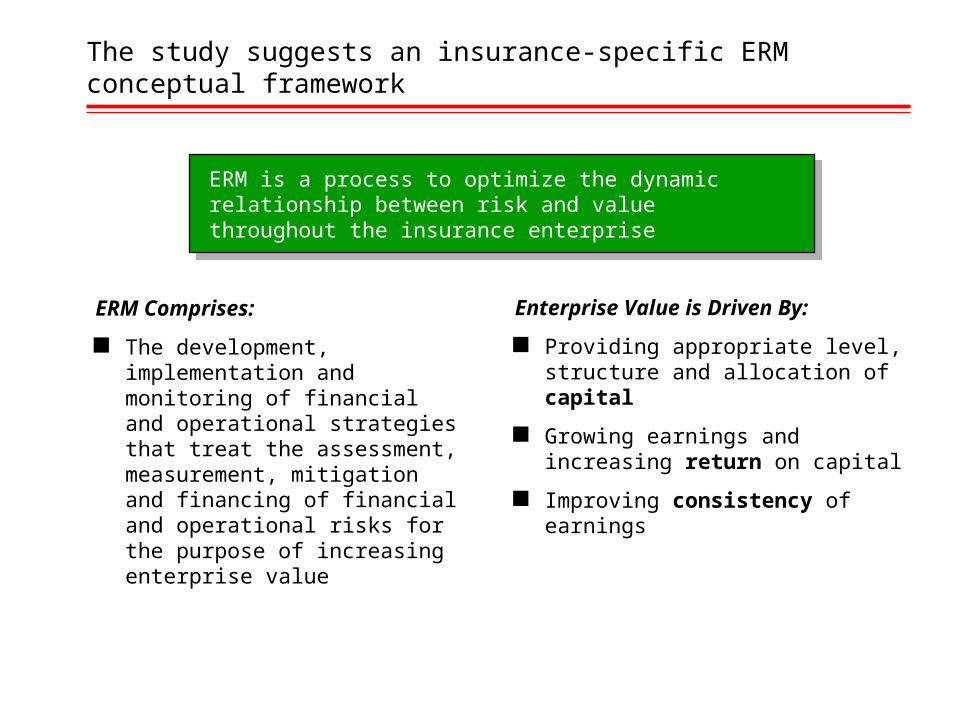

The study suggests an insurance-specific ERM conceptual framework

ERM is a process to optimize the dynamic relationship between risk and value throughout the insurance enterprise

ERM is a process to optimize the dynamic relationship between risk and value throughout the insurance enterprise

ERM Comprises:

The development, implementation and monitoring of financial and operational strategies that treat the assessment, measurement, mitigation and financing of financial and operational risks for the purpose of increasing enterprise value

Enterprise Value is Driven By:

Providing appropriate level, structure and allocation of capital

Growing earnings and increasing return on capital

Improving consistency of earnings

This framework can also be illustrated graphically

Increase Value

Holisticallymanageall risks

Holisticallymanageall risks

Reinsurance

Capital Structur

e

Product Mix

Investment Strategy

Incentive Programs

Technology

Internal Controls

Distribution

M&A

Customer Service

Market Strategy

Hiring/Training

Investigate both financial

and operational strategies

Pricing

Dynamic Hedging

Gro

wth

Retu

rn

Con

sis

ten

cy

Capital

Technology

Expansion/Diversification

People

Culture

Distribution

Processes

Risk Appetite

Understand both internal and external

environments

Investor Expectations

Economicconditions

Customer Behavior

Social/LegalTrends

Political/Regulatory Climate

Competition

Natural Catastrophes

Financial Risk

Operational Risk

Exploit natural hedges

and portfolio effects

Exploit natural hedges

and portfolio effects

The framework must recognize the unique nature of insurance operations

ERM for insurers and ERM for other financial services companies have some similarities — and some fundamental differences Single-period value-at-risk approaches are not sufficient for insurance

enterprises Statistical approaches do not capture causal relationships Structural simulation models are needed to anticipate the complex

interrelationships among risks in dynamic environments

The right framework can yield the results that insurers want but say they aren’t getting

The Right ERM Framework Can Help Insurers:

Determine necessary capital level and structure, efficient deployment of capital and improved return on capital

Properly allocate capital to business segments, supporting performance tracking

Ensure that owners receive proper compensation for risks they assume

Determine the optimal risk financing strategy

And It Can Provide:

Stability in earnings

Improved information

In summary...

Insurance executives believe ERM is critical to helping them deal with their top business issues

They are not satisfied with the current tools, techniques and processes they are using to implement ERM

They want a more robust conceptual framework and methodology that is unique to their industry

Analysis of survey results and interviews suggests what that framework would look like — and that it would deliver on the promise of ERM for insurers