Embed Size (px)

Citation preview

ELECTRONICSNovember 2010

2

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

3

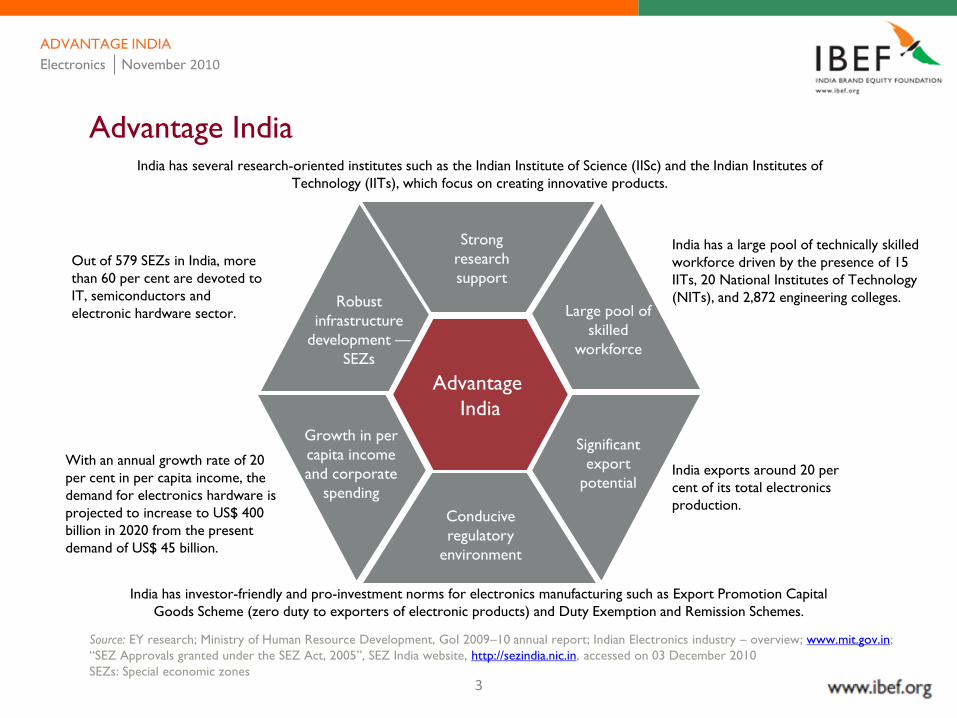

Advantage India

Advantage

India

Strong

research

support

India has several research-oriented institutes such as the Indian Institute of Science (IISc) and the Indian Institutes of

Technology (IITs), which focus on creating innovative products.

Large pool of

skilled

workforce

India has a large pool of technically skilled

workforce driven by the presence of 15

IITs, 20 National Institutes of Technology

(NITs), and 2,872 engineering colleges.

Significant

export

potentialIndia exports around 20 per

cent of its total electronics

production. Conducive

regulatory

environment

India has investor-friendly and pro-investment norms for electronics manufacturing such as Export Promotion Capital

Goods Scheme (zero duty to exporters of electronic products) and Duty Exemption and Remission Schemes.

Growth in per

capita income

and corporate

spending

With an annual growth rate of 20

per cent in per capita income, the

demand for electronics hardware is

projected to increase to US$ 400

billion in 2020 from the present

demand of US$ 45 billion.

Robust

infrastructure

development —

SEZs

Out of 579 SEZs in India, more

than 60 per cent are devoted to

IT, semiconductors and

electronic hardware sector.

Source: EY research; Ministry of Human Resource Development, GoI 2009–10 annual report; Indian Electronics industry – overview; www.mit.gov.in;

―SEZ Approvals granted under the SEZ Act, 2005‖, SEZ India website, http://sezindia.nic.in, accessed on 03 December 2010

SEZs: Special economic zones

Electronics November 2010

ADVANTAGE INDIA

4

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

5

Market overview … (1/4)• The electronics industry is categorised into the following segments:

• Consumer electronics

• Industrial electronics

• Computers

• Communication and broadcasting equipment

• Strategic electronics

• Electronic components

• Electronic hardware production in 2009–10 was US$ 22.90 billion as compared to US$ 20.26 billion in the previous year.

• Demand in consumer electronics and mobile segment has increased by 5 per cent in 2009–10 . With the increase in local production in this segment, the import have declined by 26 per cent.

• Increasing demands because of relatively higher growth rate in the Indian economy and increasing disposable income with middle class has given India a lucrative chance to increase its electronic hardware production.

Source: Department of Information Technology (DIT) 2009–10 annual report.

MARKET OVERVIEW

Electronics November 2010

6

Market overview … (2/4)

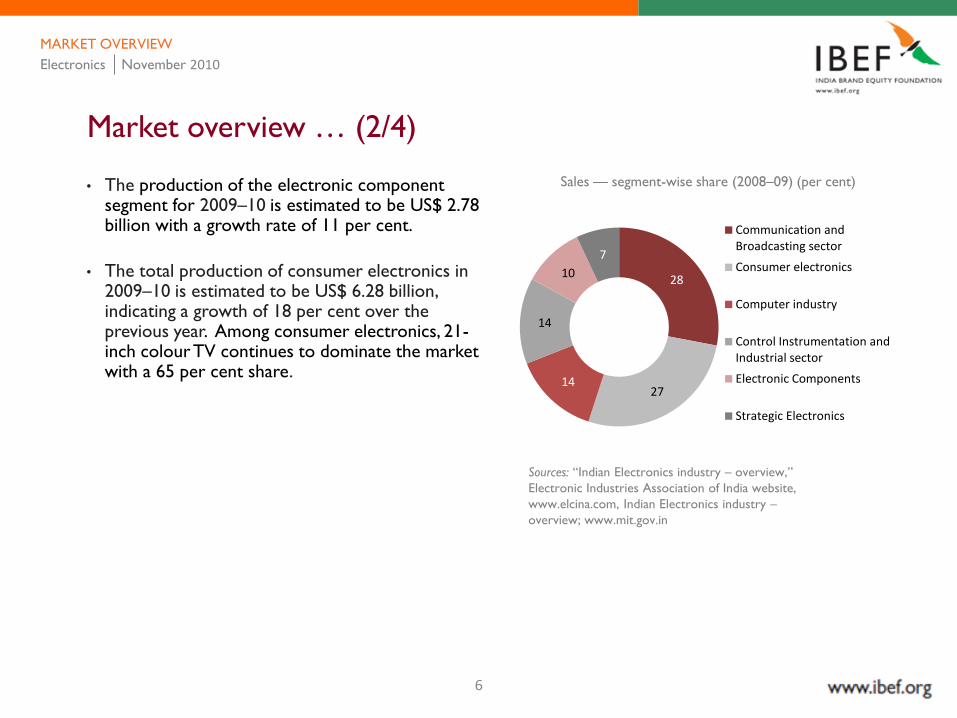

• The production of the electronic component segment for 2009–10 is estimated to be US$ 2.78 billion with a growth rate of 11 per cent.

• The total production of consumer electronics in 2009–10 is estimated to be US$ 6.28 billion, indicating a growth of 18 per cent over the previous year. Among consumer electronics, 21-inch colour TV continues to dominate the market with a 65 per cent share.

Sales — segment-wise share (2008–09) (per cent)

Sources: ―Indian Electronics industry – overview,‖

Electronic Industries Association of India website,

www.elcina.com, Indian Electronics industry –

overview; www.mit.gov.in

MARKET OVERVIEW

28

2714

14

10

7

Communication and Broadcasting sector

Consumer electronics

Computer industry

Control Instrumentation and Industrial sector

Electronic Components

Strategic Electronics

Electronics November 2010

7

Sources: ―Indian Electronics industry – overview,‖ Electronic Industries Association of India website, www.elcina.com, Indian Electronics

industry – overview; www.mit.gov.in

Market overview … (3/4)

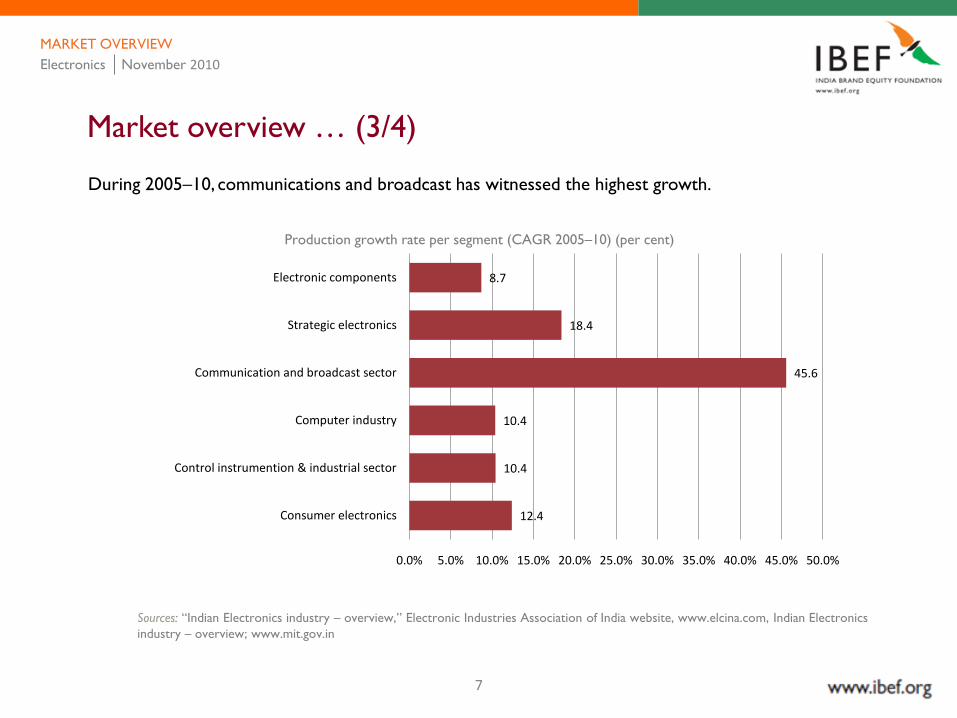

Production growth rate per segment (CAGR 2005–10) (per cent)

MARKET OVERVIEW

12.4

10.4

10.4

45.6

18.4

8.7

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0%

Consumer electronics

Control instrumention & industrial sector

Computer industry

Communication and broadcast sector

Strategic electronics

Electronic components

During 2005–10, communications and broadcast has witnessed the highest growth.

Electronics November 2010

8

10.52 11.79

13.75

17.59

20.26

22.90

-

5.00

10.00

15.00

20.00

25.00

2004-05 2005-06 2006-07 2007-08 2008-09 2009-2010

Source: Department of Information Technology (DIT) 2009–10 annual report.

The market has witnessed consistent growth over the past years.

Market overview … (4/4)

Electronics industry production

CAGR:

17%

(in U

S$ b

illio

n)

MARKET OVERVIEW

Electronics November 2010

9

39

34

14

85 Communication and

broadcast sector

Electronic components

Control instrumention & industrial sector

Consumer electronics

Computer industry

1.67

6.51

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2004-05 2009-10

Exports

• Exports from the electronics industry witnessed a CAGR of 31 per cent between 2004–05 and 2009–10.

• Communication and broadcast sector constitute 39 per cent electronics exports, followed by electronic

components.

• Exports in the electronics industry are estimated to grow from US$ 4.4 billion in 2009 to US$ 15 billion

in 2014 and US$ 80 billion in 2020, at a CAGR of 33 per cent.

Source: Department of Information Technology (DIT) 2009–10 annual report.

CAGR

31%

(in U

S$ b

illio

n)

Electronics industry exports Segment-wise exports (2008–09) (per cent)

MARKET OVERVIEW

Electronics November 2010

10

Bharat Electronics Ltd

The Government of India (GoI) established Bharat Electronics Ltd (BEL) in Bengaluru, India,

under the Ministry of Defence in 1954 to meet the specialised electronic needs of the

Indian defence services. BEL focusses on contract manufacturing, design and manufacturing

services, semiconductor device packaging and software development and quality assurance

facilities. The company’s turnover has increased from US$ 0.68 billion (INR 32.71 billion) in

2004–05 to US$ 1.06 billion (INR 50.93 billion) in 2009–2010.

Videocon

International Ltd

In 1985, through a technical collaboration with Japan’s Toshiba Corporation, Videocon

International Ltd launched India's first world class colour TV. Today, Videocon International

Ltd, Videocon Group’s flagship company, is India's leading manufacturer of consumer

electronic products. Videocon is now a global player and the first Indian company to win the

prestigious Conformite Europeene (CE) approval for exporting colour TVs to Europe.

Videocon also has a presence globally, with operations in the Middle East, Europe, Indonesia

and South Africa.

LG Electronics India

Limited

Established in 1997, LG Electronics India Limited is a wholly owned subsidiary of LG

Electronics, South Korea. In India, LG is the market leader in consumer durables and is

recognised as a leading technology innovator in the IT and mobile communications business.

LG Electronics has two manufacturing units in India with the latest technologies at par with

international standards. These facilities are among the most eco-friendly units within all LG

manufacturing plants in the world.

MARKET OVERVIEW

Key players … (1/3)

Electronics November 2010

11

HCL Infosystems Ltd

HCL Infosystems Ltd manufactures and markets PCs, PC servers, storage solutions and display

products, among other electronic products. HCL’s computer hardware manufacturing plants

include four facilities spread across the country. In addition, the company offers IT consulting,

technology integration services and software solutions. HCL’s revenue has grown from

US$ 0.41 billion (INR 19.7 billion) in 2004–05 to US$ 2.52 billion (INR 121.14 billion) in 2009–

2010.

Samsung India

Electronics Ltd

Samsung India Electronics Ltd, a subsidiary of US$ 56 billion Samsung Electronics Co Ltd, has

been operating in India since 1995. It is a leading provider of high-tech consumer electronics,

home appliances, IT and telecom products in the country. Samsung India has set up

manufacturing facilities for color TVs, microwave ovens, washing machines, air conditioners,

color monitors and, more recently, refrigerators. The company has a plant in Noida, Uttar

Pradesh.

Moser Baer India Ltd

Moser Baer India Ltd (MBIL) is the world's second-largest company in the optical storage

media segment. MBIL supplies to a number of branded players such as Sony, Verbatim, TDK,

Maxell, Imation and Samsung and has collaborative R&D programs as well as reciprocal training

programmes with these companies. Further, Moser Baer also has a presence in the

photovoltaic and home entertainment segments. Moser Baer's products are manufactured at

its three state-of-the-art manufacturing facilities. Its revenue has grown from US$ 0.29 billion

(INR 14.21 billion) in 2004–05 to US$ 0.43 billion (INR 20.52 billion) in 2009–2010.

MARKET OVERVIEW

Key players … (2/3)

Electronics November 2010

12

Jabil

• Jabil has a 176,000 sq ft facility in Ranjangaon near Pune, Maharashtra.

• The company offers printed circuit boards, enclosure integration, distribution and repair services with in-region design services support.

• Jabil services the instrumentation, networking, peripherals and telecommunications industries.

• The company acquired Celetronix — one of the largest electronic equipment manufacturers in India in 2006. The acquisition gave Jabil an additional 270,000 sq ft of manufacturing space.

Flextronics

• Flextronics ventured into India in 2001.

• The company offers high-value, high-margin design services for mobile phones and telecom/networking software.

• Flextronics has a 692,457 sq ft manufacturing facility in Chennai.

Elcoteq

• Inaugurated in 2005, Elcoteq Bengaluru’s main businesses in India include wireless

communication terminal products, wireless communications, network equipment and after-

sales services.

• The Bengaluru plant is one of Elcoteq’s four volume manufacturing plants in the Asia-Pacific

region and the first in India.

• The company’s plant (100,000 sq ft) in Bengaluru is equipped with the latest manufacturing

technologies, including surface mount technology (SMT), testing and electrostatic discharge

(ESD) control to support its modernised manufacturing process.

MARKET OVERVIEW

Key players … (3/3)

Electronics November 2010

13

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

14

Industry infrastructure — SEZs … (1/4)

Developer Type Size in hectares

Andhra Pradesh Industrial Infrastructure Corporation Ltd (APIIC) Electronic hardware 111.00

Stargaze Properties Private Ltd (Andhra Pradesh) Electronic hardware, IT/ITeS 68.96

S2tech.com India Private Ltd (Andhra Pradesh) Electronic hardware, IT/ITeS 10.12

Chandigarh administration Electronic hardware, IT/ITeS 31.49

Gujarat Industrial Development Corporation (GIDC) Electronic products 28.00

Mexus Corporation private Ltd (Gujarat) Electronic hardware, IT/ITeS 11.11

Ireo Investment Holding III Ltd (Haryana) Electronic hardware, IT/ITeS 40.00

GP Realtors Pvt Ltd Phase II (Haryana) Electronic hardware, IT/ITeS 11.03

GP Realtors Pvt Ltd Phase III (Haryana) Electronic hardware, IT/ITeS 17.18

Sohna Buildcon Private Ltd (Haryana) Electronic hardware, IT/ITeS 10.00

Wellgrow Buildcon Private Ltd (Haryana) Electronic hardware, IT/ITeS 24.29

Progressive Buildestate Private Ltd (Haryana) Electronic hardware, IT/ITeS 34.41

INDUSTRY INFRASTRUCTURE

Note: This is an indicative list.

Electronics November 2010

15

Industry infrastructure — SEZs … (2/4)

Developer Type Size in hectares

Mikado Realtors Private Ltd (Haryana) Electronic hardware, IT/ITeS 11.02

Ittina Properties Private Ltd (Karnataka) Electronic hardware, IT/ITeS 15.73

Opto Circuits India Ltd (Karnataka) Electronic hardware park 12.23

Opto Infrastructure Ltd (Karnataka) Electronic hardware, IT/ITeS 100.00

Karnataka State Electronics Development Corporation Ltd(KEONICS) Electronic hardware, IT/ITeS 14.5

Gopalan E-Park Electronic hardware, IT/ITeS 11.35

Kerala Industrial Infrastructure Development Corporation (Kerala) Electronic industries 12.14

Magarpatta Township Development and Construction Co Ltd (Maharashtra) Electronic hardware, IT/ITeS 11.98

Kumar Builders Township Ventures Private Ltd (Maharashtra) Electronic hardware, IT/ITeS 49.10

City Parks Private Ltd (Maharashtra) Electronic hardware, IT/ITeS 30.00

Siddhivinayak Knowledge City Developers Private Ltd (Maharashtra) Electronic hardware, IT/ITeS 12.14

Pride Infrastructure & SEZ private Ltd (Maharashtra) Electronic hardware, IT/ITeS 12.34

INDUSTRY INFRASTRUCTURE

Note: This is an indicative list.

Electronics November 2010

16

Industry infrastructure — SEZs … (3/4)

Developer Type Size in hectares

Modern India Property Developers Ltd (Maharashtra) Electronic hardware, IT/ITeS 14.77

Benchmark Realty Private Ltd (Maharashtra) Electronic hardware, IT/ITeS 10.0

Lark Projects Private Ltd (Punjab) Electronic hardware, IT/ITeS 10.9

Somani Worsted Ltd (Rajasthan) Electronic hardware, IT/ITeS 20.0

Flextronics Technology India Private Ltd (Tamil Nadu) Electronic hardware and related services 101.0

Arun Excello IT SEZ Private Ltd (Tamil Nadu) Electronic hardware, IT/ITeS 10.9

State Industries Promotion Corporation of Tamil Nadu Ltd Electronics hardware 140.7

Foxconn India Developers Ltd (Tamil Nadu) Electronic hardware 11.0

Coimbatore Hi-tech Infrastructure Private Ltd (Tamil Nadu) Electronic hardware, IT/ITeS 60.7

KPR Developers (Tamil Nadu) Electronic hardware, IT/ITeS 20.5

True Developers Private Ltd (Tamil Nadu) Electronic hardware, IT/ITeS 11.6

Best and Crompton Engineering Ltd (Tamil Nadu) Electronic hardware, IT/ITeS 10.8

Note: This is an indicative list.

INDUSTRY INFRASTRUCTURE

Electronics November 2010

17

634

34

4

22

IT/ITES/Electronics Hardware/Semiconductors

Pharma

Textile

Multi Product

Biotech

Others

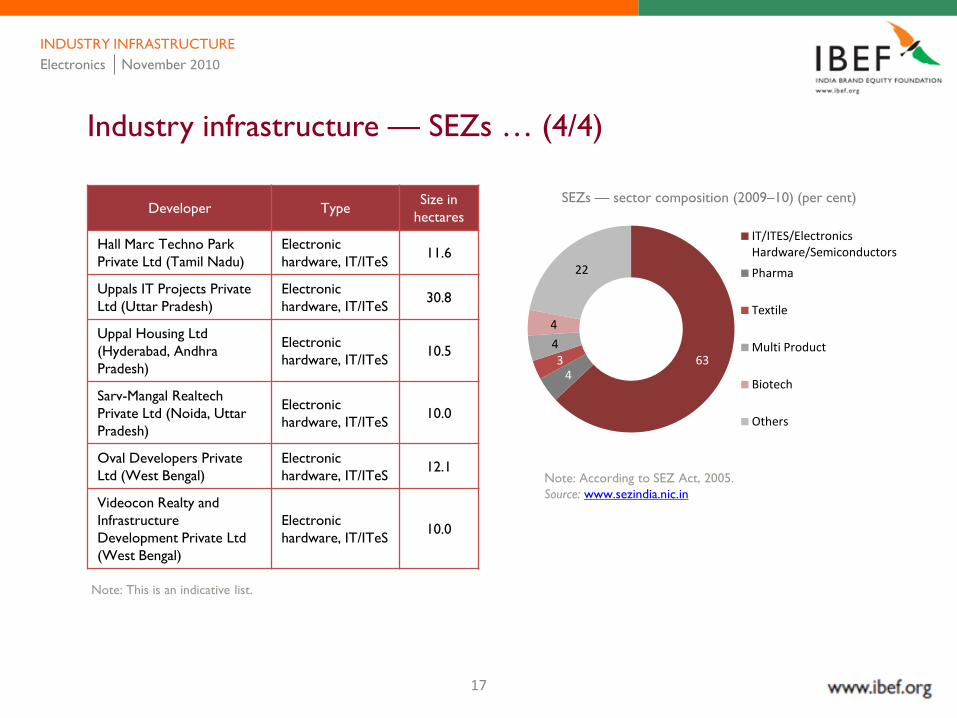

Industry infrastructure — SEZs … (4/4)

Developer Type Size in

hectares

Hall Marc Techno Park

Private Ltd (Tamil Nadu)

Electronic

hardware, IT/ITeS11.6

Uppals IT Projects Private

Ltd (Uttar Pradesh)

Electronic

hardware, IT/ITeS30.8

Uppal Housing Ltd

(Hyderabad, Andhra

Pradesh)

Electronic

hardware, IT/ITeS10.5

Sarv-Mangal Realtech

Private Ltd (Noida, Uttar

Pradesh)

Electronic

hardware, IT/ITeS10.0

Oval Developers Private

Ltd (West Bengal)

Electronic

hardware, IT/ITeS12.1

Videocon Realty and

Infrastructure

Development Private Ltd

(West Bengal)

Electronic

hardware, IT/ITeS10.0

Note: According to SEZ Act, 2005.

Source: www.sezindia.nic.in

SEZs — sector composition (2009–10) (per cent)

INDUSTRY INFRASTRUCTURE

Note: This is an indicative list.

Electronics November 2010

18

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

19

Investment … (1/2)

Cumulative FDI inflows

April 2000 to August 2010

SectorAmount of FDI

(US$ million)

Electronics 826.1

Computer software

and hardware10,330.5

Source: ―Fact Sheet – August 2010 on Foreign Direct Investment (FDI),‖ Department of Industrial Policy and Promotion website, www.dipp.nic.in,

accessed on 28 November 2010

Foreign technology transfers (FTTs)

August 1991 to December 2009

SectorNumber

Total number of FTTs 8,106

Electrical equipment, including

computer software and electronics1,263

INVESTMENTS

Electronics November 2010

20

Key deals (2010)

Deal date Target name AcquirerDeal value (US$

million)

September 28, 2010 Tyco Electronics Ltd-Energy Business Raychem RPG Ltd NA

September 21, 2010 Citigroup Inc-Datacenter Buederich Wipro Technologies NA

August 26, 2010 Venture Infotek Global Pvt Ltd Atos Origin SA NA

September 20, 2010 Micromax Informatics Ltd Investor Group 43.8

October 14, 2010 A Little World Pvt Ltd SBI 18.1

July 9, 2010 In2Soft GmbH KPIT Cummins Infosystems Ltd 3.8

October 18, 2010 El Corp Ltd Yam Keong Chee 1.0

June 30, 2010 MMG India Pvt Ltd Delta Magnets Ltd NA

April 12, 2010 Dynamic Test Solutions Inc Tessolve Services Pvt Ltd NA

March 5, 2010 Undisclosed Electronic Security Co Schneider Electric India Pvt Ltd NA

March 1, 2010Zicom Electronic Security Systems Ltd-

Electronic Security SystemSchneider Electric SA 48.89

February 24, 2010Home Solutions Retail(India) Ltd-

Consumer Durable,Furniture BusinessPantaloon Retail(India)Ltd NA

February 24, 2010 Wavetel Mobiles Sangeetha Mobiles Pvt Ltd 2.81

February 22, 2010 TexTech International Pvt Ltd Jouve 5.41

February 17, 2010 SEI Cable Accessories(India)P vt Ltd Sumitomo Electric Industries Ltd 0.13

January 21, 2010 MIC Electronics Ltd Investor Group NA

January 21, 2010 Global Access Spice Retail Ltd NA

January 13, 2010 BA Systems India Private Ltd OneAccess Networks SA NA

January 12, 2010 Micromax Informatics Ltd TA Associates Inc 45.00

Source: Thomson ONE Banker

Investment … (2/2)

Electronics November 2010

INVESTMENTS

21

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

22

Policy and regulatory framework

Key policy initiatives

• There is no customs duty on ITA-1 items (217 items).

• Excise duty on computers has been removed. Microprocessors, hard disc drives, floppy disc drives and CD ROM drives are exempt from excise duty.

• Foreign equity participation of upto100 per cent is permissible.

• The GoI has decided to set up Information Technology Investment Regions (ITIRs) to provide superior infrastructure support.

• Units undertaking the export of their complete range of goods and services may be set up under the EHTP scheme.

Source: Indian Electronics industry – overview; www.mit.gov.in

ITA-1: Information Technology Agreement

POLICY AND REGULATORY FRAMEWORK

Electronics November 2010

23

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

24

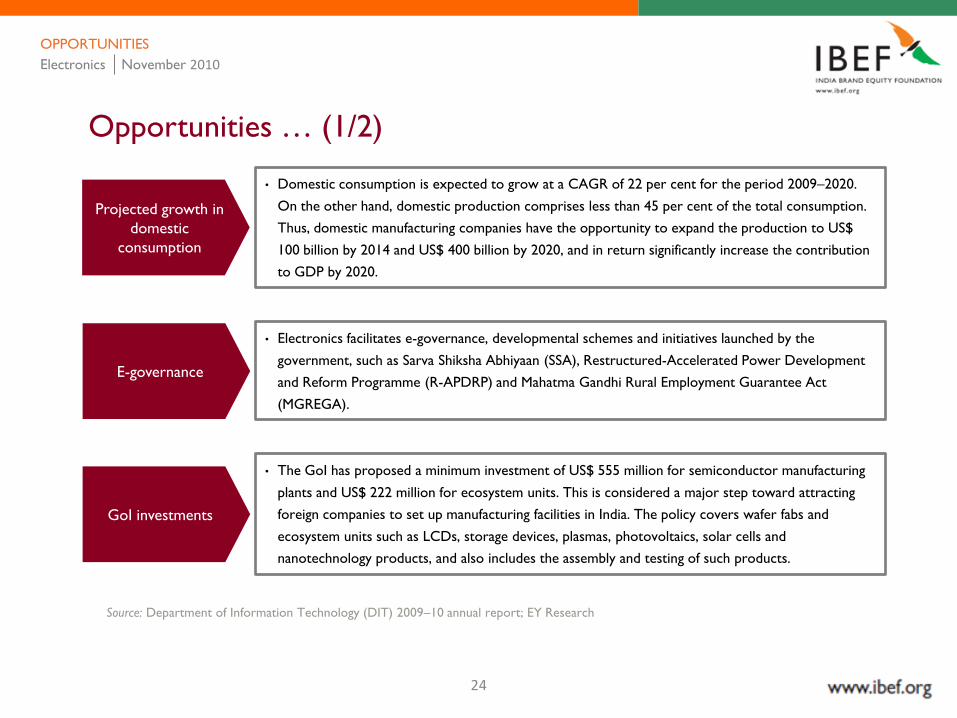

Opportunities … (1/2)

OPPORTUNITIES

Source: Department of Information Technology (DIT) 2009–10 annual report; EY Research

Projected growth in

domestic

consumption

E-governance

GoI investments

Electronics November 2010

• Domestic consumption is expected to grow at a CAGR of 22 per cent for the period 2009–2020.

On the other hand, domestic production comprises less than 45 per cent of the total consumption.

Thus, domestic manufacturing companies have the opportunity to expand the production to US$

100 billion by 2014 and US$ 400 billion by 2020, and in return significantly increase the contribution

to GDP by 2020.

• Electronics facilitates e-governance, developmental schemes and initiatives launched by the

government, such as Sarva Shiksha Abhiyaan (SSA), Restructured-Accelerated Power Development

and Reform Programme (R-APDRP) and Mahatma Gandhi Rural Employment Guarantee Act

(MGREGA).

• The GoI has proposed a minimum investment of US$ 555 million for semiconductor manufacturing

plants and US$ 222 million for ecosystem units. This is considered a major step toward attracting

foreign companies to set up manufacturing facilities in India. The policy covers wafer fabs and

ecosystem units such as LCDs, storage devices, plasmas, photovoltaics, solar cells and

nanotechnology products, and also includes the assembly and testing of such products.

25

Opportunities … (2/2)

OPPORTUNITIES

Source: Department of Information Technology (DIT) 2009–10 annual report; EY Research

Electronic

components

Low penetration in

consumer durables

Electronics November 2010

• With growth engines such as strong demand, availability of skilled labor and increase in GoI spending

in related verticals, electronic component segment production is expected to reach US$ 2.6 billion

in 2014 and US$ 3.4 billion in 2020.

• Low penetration levels in most consumer durables provides an opportunity to manufacturers to

increase demand by reaching for untapped market . According to the National Council for Applied

Economic Research (NCAER), in 2008 penetration levels for white goods stood at 31.9%,

refrigerators at 16.1%, PCs at 0.08% and colour TVs at 21.3%.

26

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

ELECTRONICS November 2010

27

Industry associationsElectronics Industries Association of India (ELCINA)

ELCINA House, 422 Okhla Industrial Estate, New Delhi – 110 020, India

Phone: 91 11 26924597,26928053

Fax: 91 11 26923440

E-mail: [email protected]

Website: www.elcina.com/

Telecom Equipment Manufacturers Association (TEMA)

4th Floor, PHD House, Opp. Asian Village, New Delhi – 110 016, India

Tel: 91 11 26859621

Fax: 91 11 26859620

E-mail: [email protected]

Website: http://www.tfci.com/cni/tema.htm

Manufacturers Association for Information Technology (MAIT)

4th Floor, PHD House, Opp. Asian Games Village, New Delhi 110 016, India

Tel: 91 11 26855487

Fax: 91 11 26851321

E-mail: [email protected]

Website: www.mait.com/

INDUSTRY ASSOCIATIONS

Electronics November 2010

28

Note

Wherever applicable, numbers in the report have been rounded off to the nearest whole number.

Conversion rate used: US$ 1= INR 48.

NOTE

Electronics November 2010

29

India Brand Equity Foundation (IBEF) engaged Ernst &

Young Pvt Ltd to prepare this presentation and the same

has been prepared by Ernst & Young in consultation with

IBEF.

All rights reserved. All copyright in this presentation and

related works is solely and exclusively owned by IBEF. The

same may not be reproduced, wholly or in part in any

material form (including photocopying or storing it in any

medium by electronic means and whether or not

transiently or incidentally to some other use of this

presentation), modified or in any manner communicated

to any third party except with the written approval of

IBEF.

This presentation is for information purposes only. While

due care has been taken during the compilation of this

presentation to ensure that the information is accurate to

the best of Ernst & Young and IBEF’s knowledge and belief,

the content is not to be construed in any manner

whatsoever as a substitute for professional advice.

Ernst & Young and IBEF neither recommend nor endorse

any specific products or services that may have been

mentioned in this presentation and nor do they assume

any liability or responsibility for the outcome of decisions

taken as a result of any reliance placed on this

presentation.

Neither Ernst & Young nor IBEF shall be liable for any

direct or indirect damages that may arise due to any act

or omission on the part of the user due to any reliance

placed or guidance taken from any portion of this

presentation.

DISCLAIMER

ELECTRONICS November 2010