Embed Size (px)

Citation preview

Eindhoven University of Technology

MASTER

Risk in healthcare real estate investment

Kosse, T.H.V.

Award date:2016

Link to publication

DisclaimerThis document contains a student thesis (bachelor's or master's), as authored by a student at Eindhoven University of Technology. Studenttheses are made available in the TU/e repository upon obtaining the required degree. The grade received is not published on the documentas presented in the repository. The required complexity or quality of research of student theses may vary by program, and the requiredminimum study period may vary in duration.

General rightsCopyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright ownersand it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights.

• Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain

Utrecht, February 2016

Risk in Healthcare Real Estate Investment

by

T.H.V. (Tjeerd) Kosse

Student identity number: 0614493

In partial fulfillment of the requirements for the degree of

Master of Science

in Architecture, Building and Planning

Subject headings:

Real Estate Investment, Healthcare Real Estate, Medical Real Estate, Senior Housing, Skilled

Nursing Homes, Memory Homes, Investment Risk, Risk Factors, Determinants of the Cap

Rate, Hedonic Risk Model, Downside Risk.

Supervisors:

Ir. S.J.E. (Stephan) Maussen MRE, TU/e

Dr. Ir. P.E.W. (Pauline) van den Berg, TU/e

Drs. P. (Pim) Diepstraten, company supervisor

Department of the Built Environment

Master Architecture, Building and Planning

Risk in Healthcare Real Estate Investment ii

Colophon

Risk in Healthcare Real Estate Investment

In partial fulfillment of the requirements for the degree of Master of Science at

Eindhoven University of Technology

Department of the Built Environment

Master: Architecture, Building and Planning

Specialization: Real Estate Management and Development

Author

Ing. T.H.V. (Tjeerd) Kosse

Student ID: 0614993

Chairman Graduation Committee

Prof. Dr. T.A. (Theo) Arentze

Department of the Built Environment

Eindhoven University of Technology

Academic Supervisors

Ir. S.J.E. (Stephan) Maussen MRE

Department of the Built Environment

Eindhoven University of Technology

Dr. Ir. P.E.W. (Pauline) van den Berg

Department of the Built Environment

Eindhoven University of Technology

Company Supervisor

Drs. P. (Pim) Diepstraten

Partner & Senior Advisor

Finance Ideas

Date

16 February, 2016

Copyright © T.H.V. Kosse

Risk in Healthcare Real Estate Investment iii

Abstract

This master thesis investigates the risk of investing in healthcare real estate and in particular

skilled nursing and memory homes by finding and analyzing risk factors and their perceived

importance. Risk factors and their importance were found by reviewing the relevant literature

and analyzing data obtained during 22 interviews with experts on healthcare real estate

investment. A total of 75 risk factors and their importance were found offering investors an

instrument to analyze risk. Uncertainty over the risk of investing in healthcare real estate is

mitigated by using long-term rental contracts instead of requiring higher returns. Investors

manage the risk of long-term contracts by assessing the stability of the tenant. Two distinct

points of view were found on risk management in healthcare real estate investment; one

viewpoint is focused on tenant risks and the other viewpoint focuses on property risks. The

most common length of rental contracts is 15 years. In shorter rental contracts of 10 years

property risks are more important while tenant risks are more important when using rental

contracts of 20 years or longer. Markets with short contracts are more suitable for investors

who focus on property risks while markets with long contracts are more suitable for investors

who focus on tenant risks. Unwillingness of Dutch healthcare organizations to sign long-term

rental contracts could shift the focus of investors from tenant risks towards property risks.

Risk in Healthcare Real Estate Investment iv

Risk in Healthcare Real Estate Investment v

Table of Contents

Colophon ii

Abstract iii

Table of Contents v

Summary Article: Dutch vii

Summary Article: English xvii

Preface xxvii

RISK IN HEALTHCARE REAL ESTATE INVESTMENT 1

1. Research Context 1

1.1. Introduction 1

1.2. Research Objective and Questions 3

1.3. Scope 3

1.4. Research Design 5

1.5. Research Outline 6

2. Theoretical Background 9

2.1. The Real Estate System, the Asset Market and Market Value 9

2.2. Stages of Maturity of an Asset Market 10

2.3. The Current HCRE Investment Practice in The Netherlands 13

3. Literature Review: Risk in HCRE Investment 17

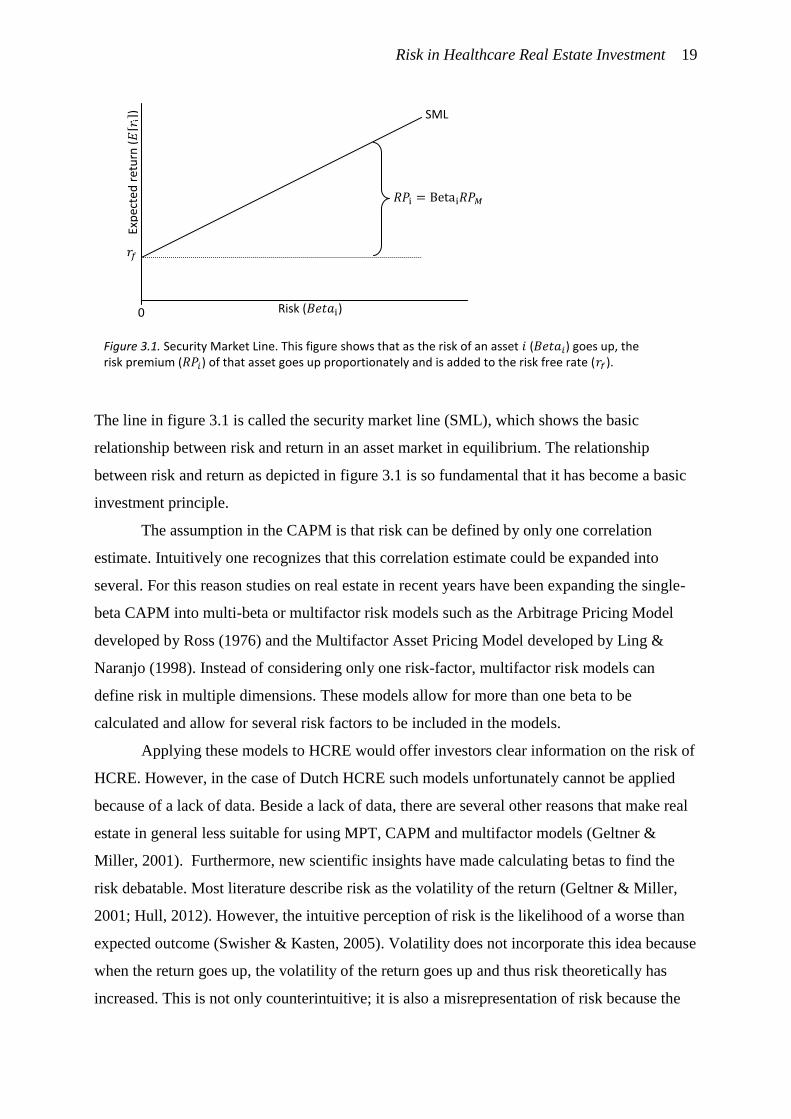

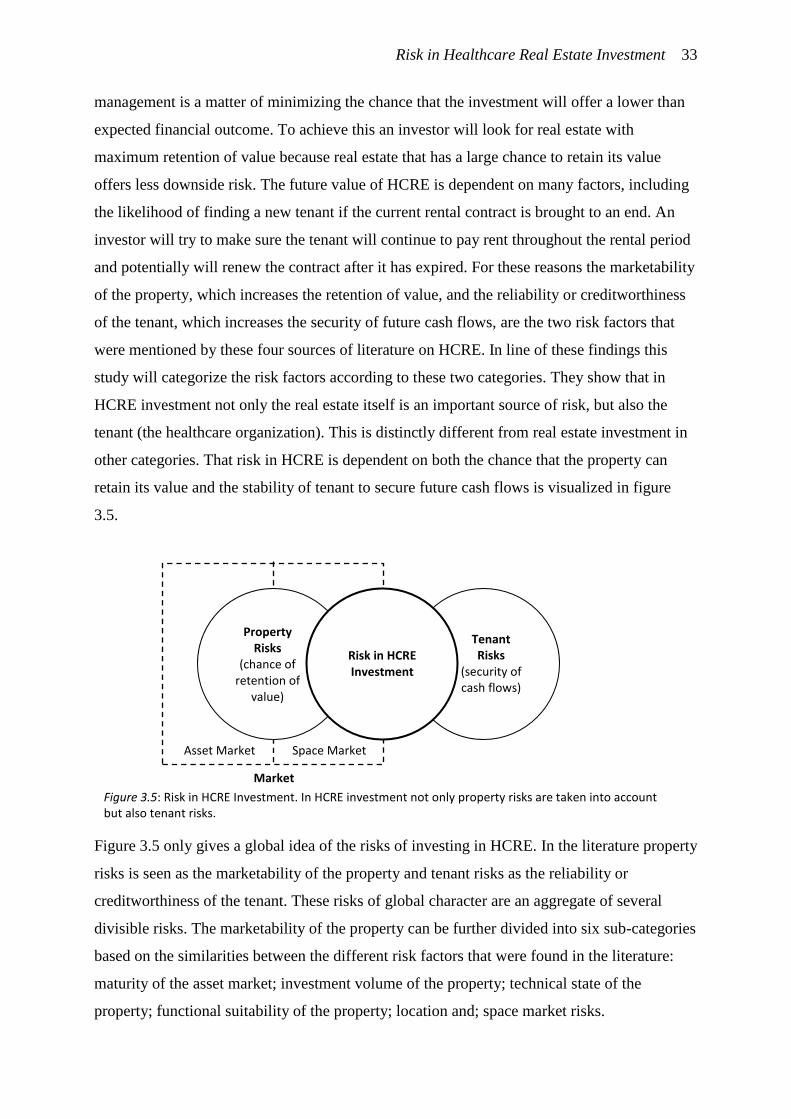

3.1. Risk in the Context of Real Estate Investment 17

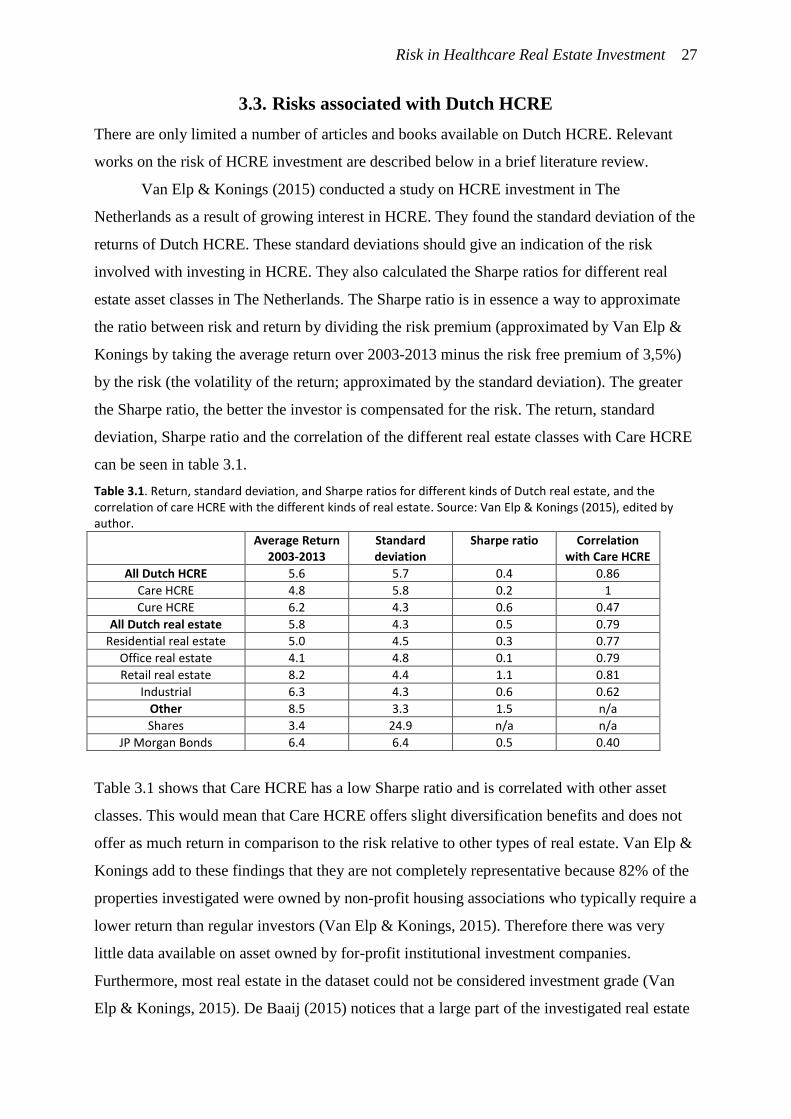

3.2. Risks associated with Real Estate 22

3.3. Risks associated with Dutch HCRE 27

3.4. Synthesis of the Risk Factors Mentioned in the Literature Review 31

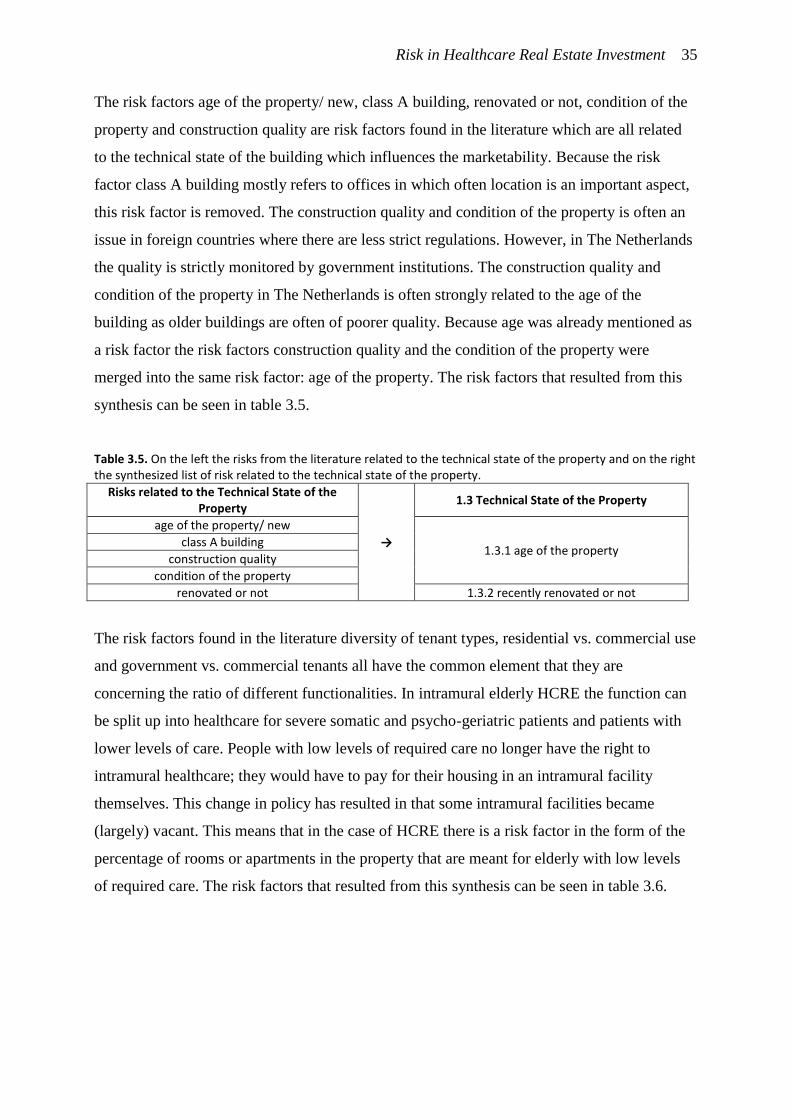

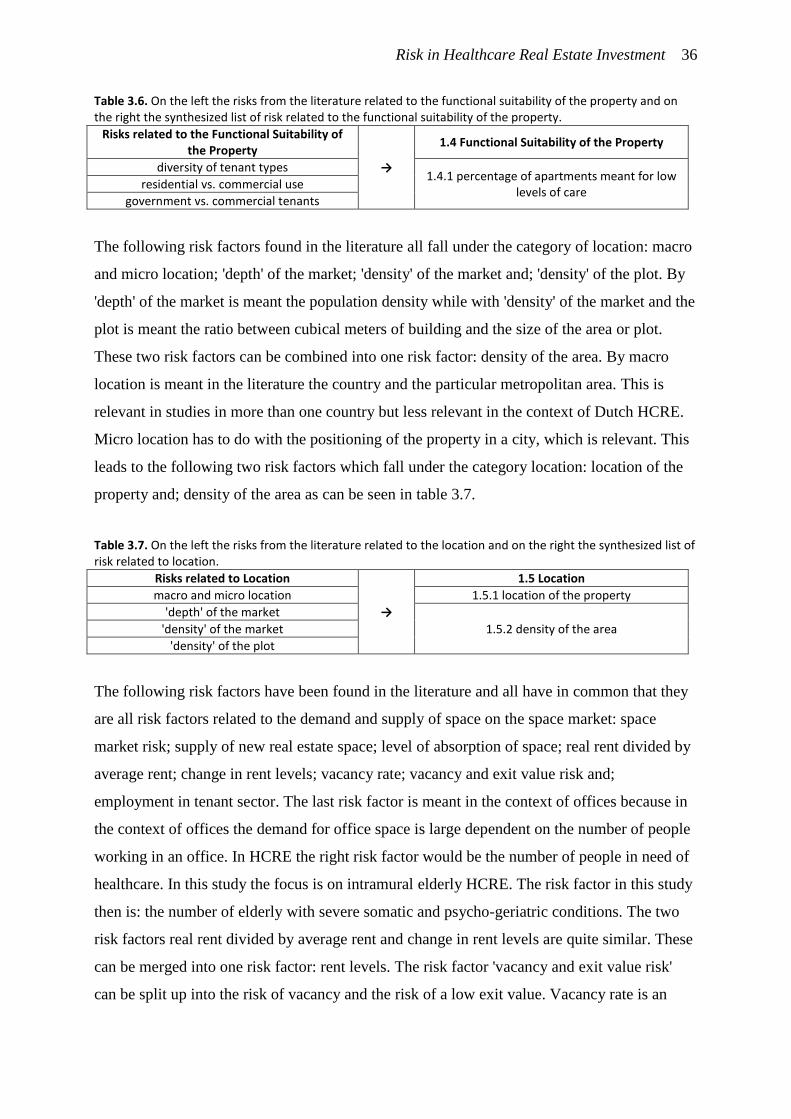

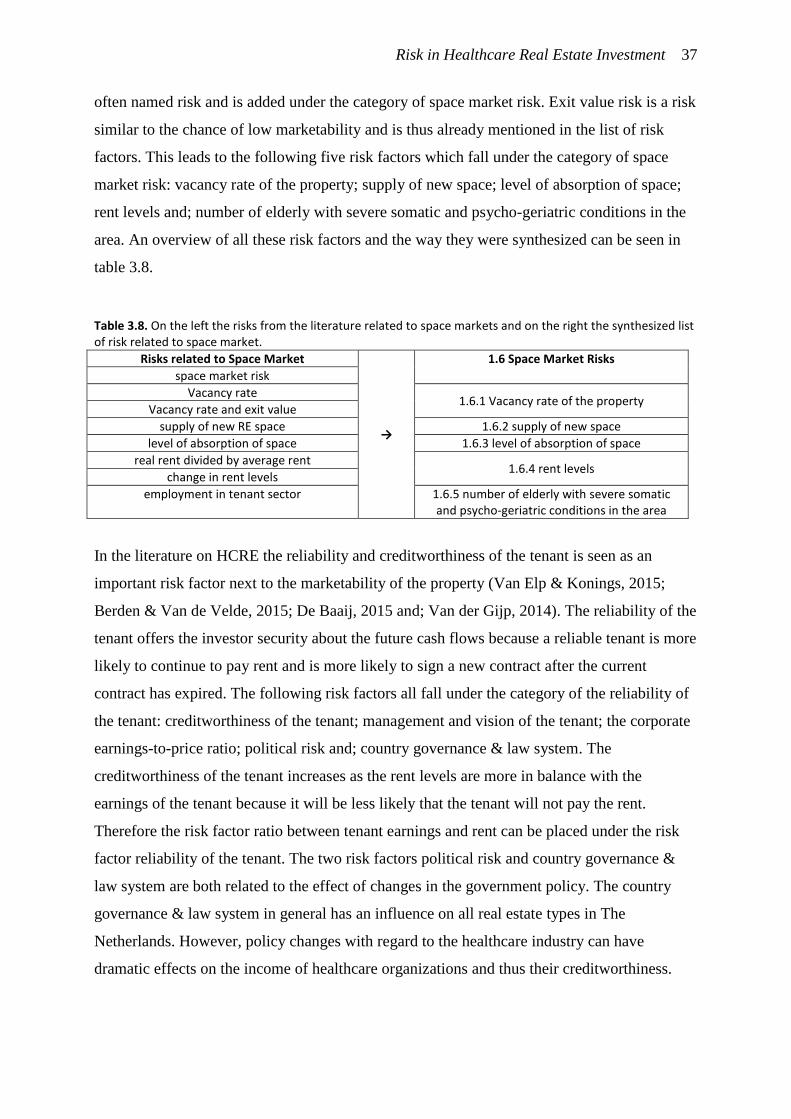

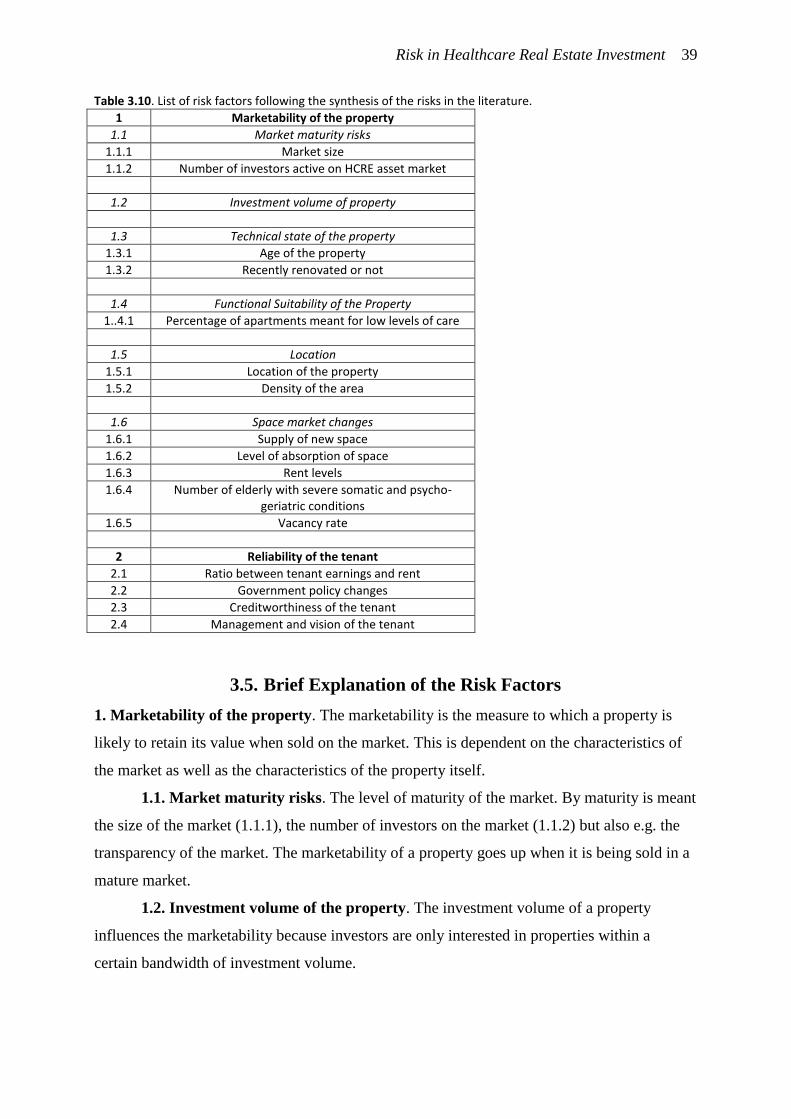

3.5. Brief Explanation of the Risk Factors 39

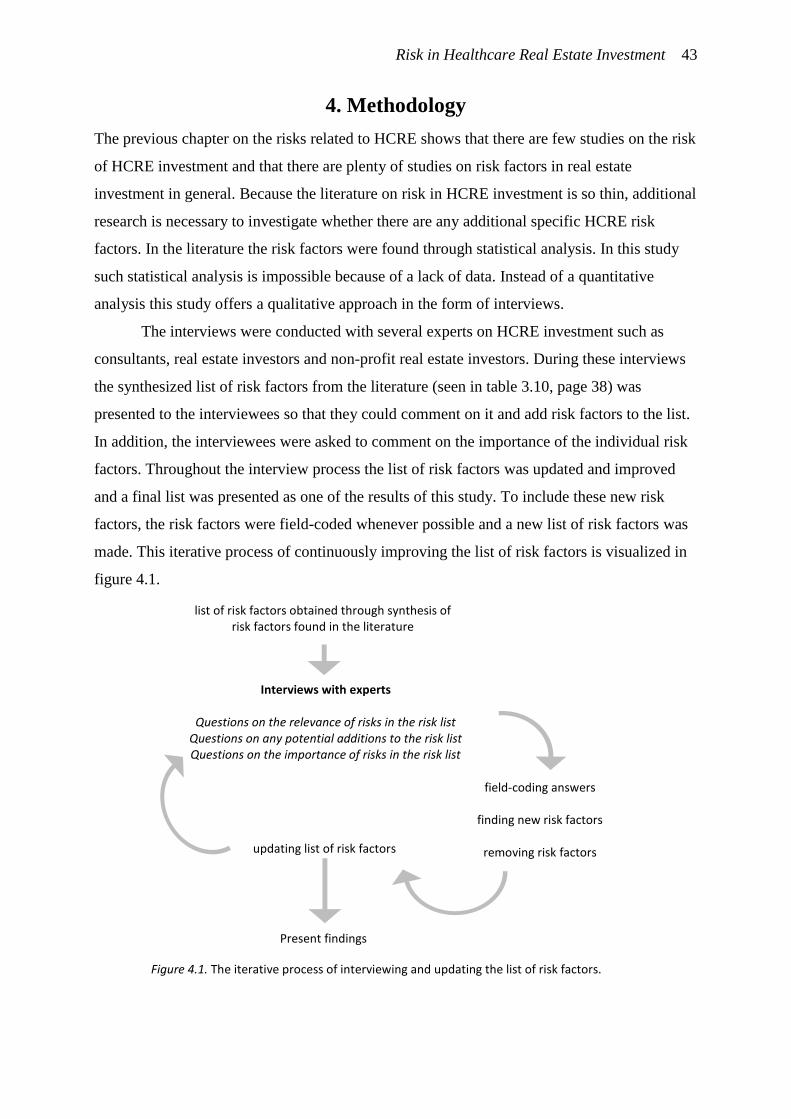

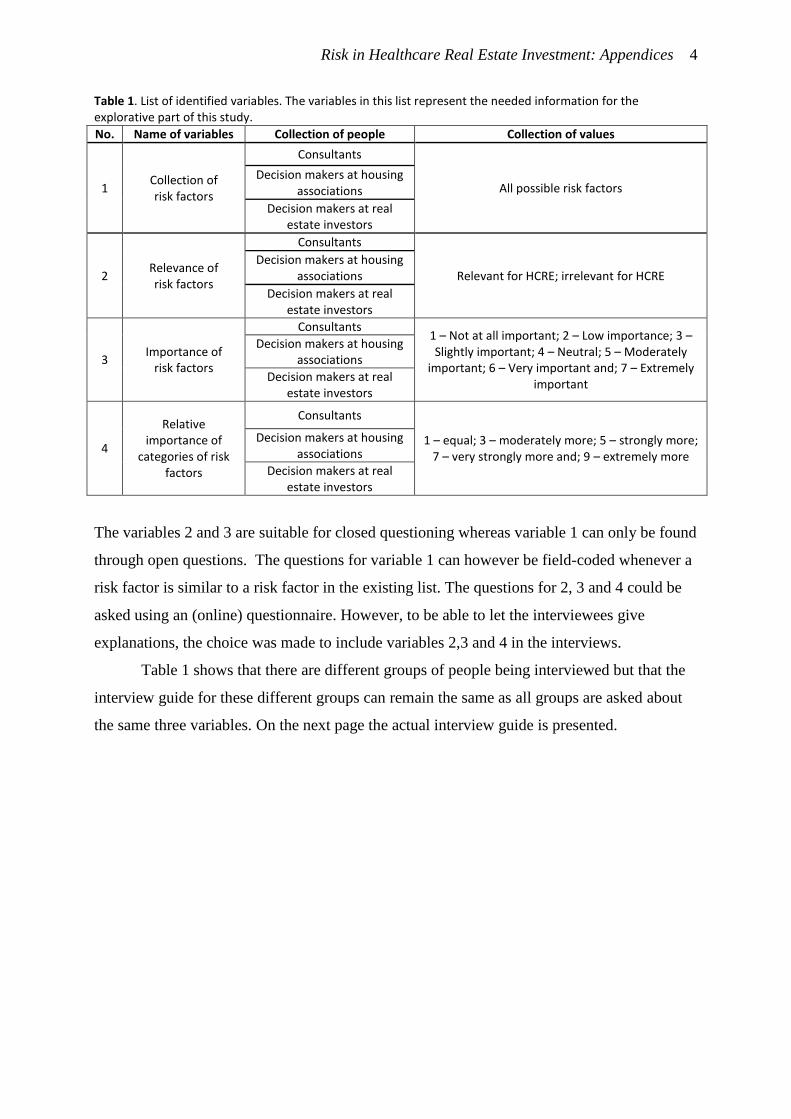

4. Methodology 43

4.1. Interview Guide 44

4.2. Interviewee Selection 44

4.3. Method of Analysis 46

4.4. Description of the Field Work 46

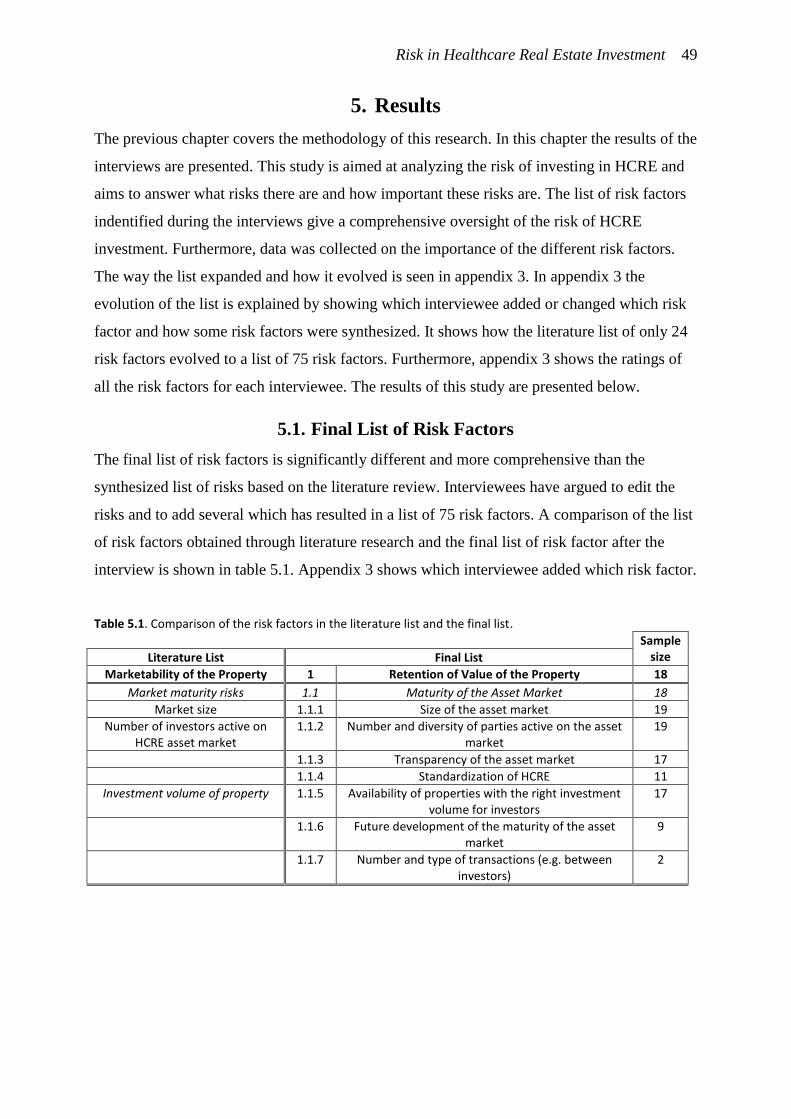

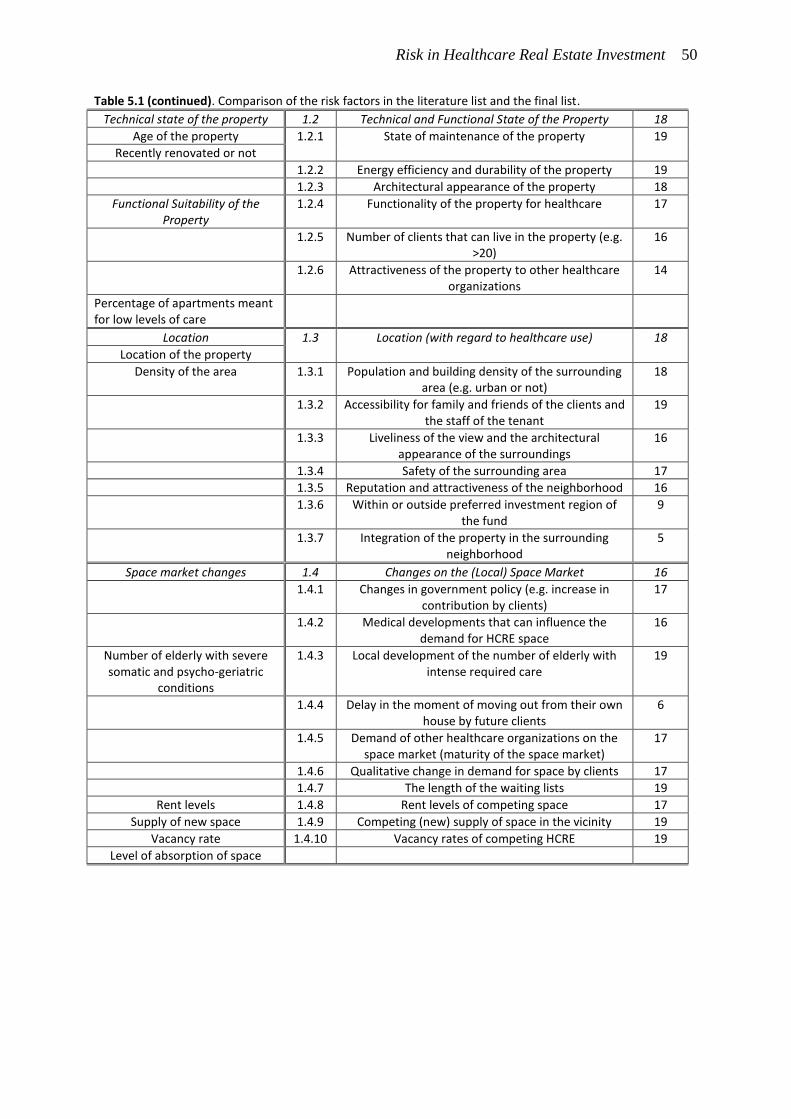

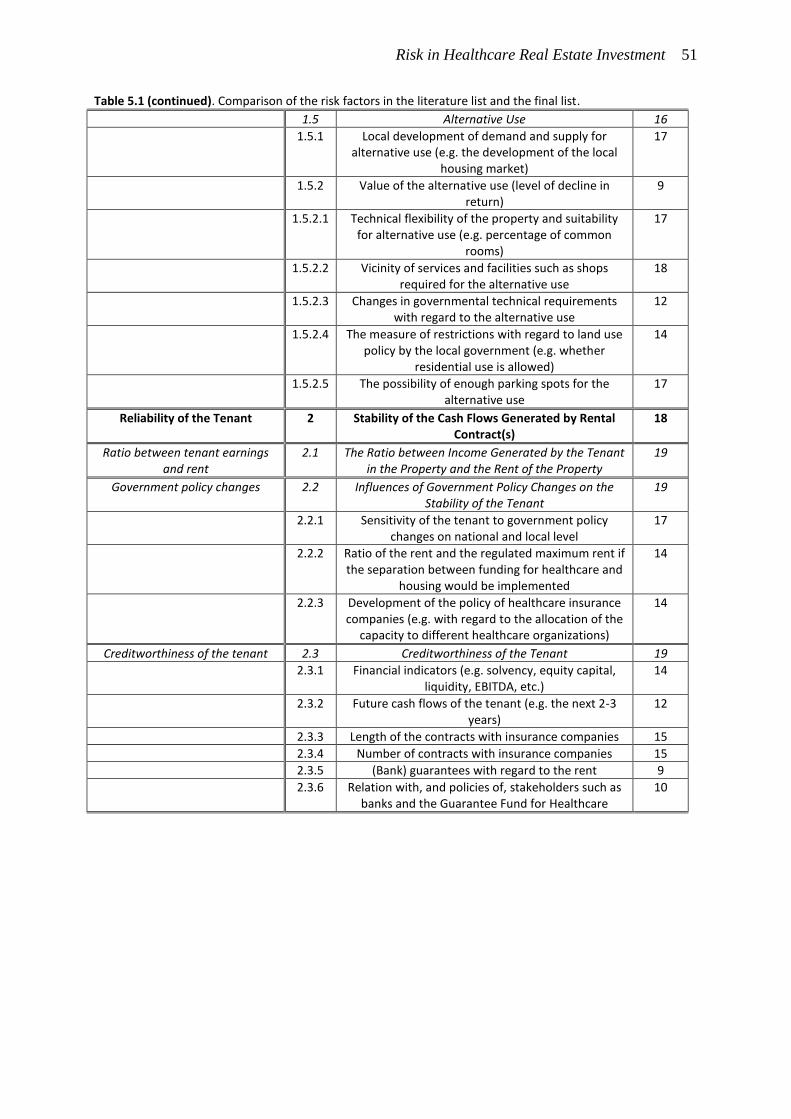

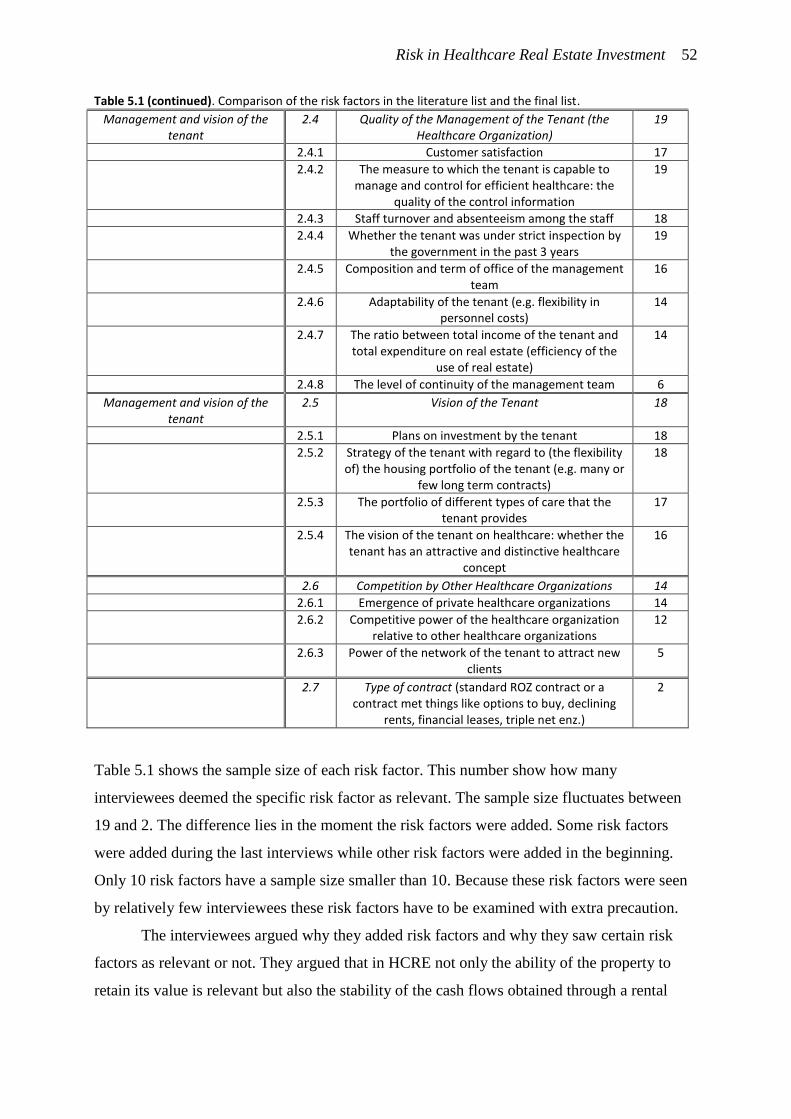

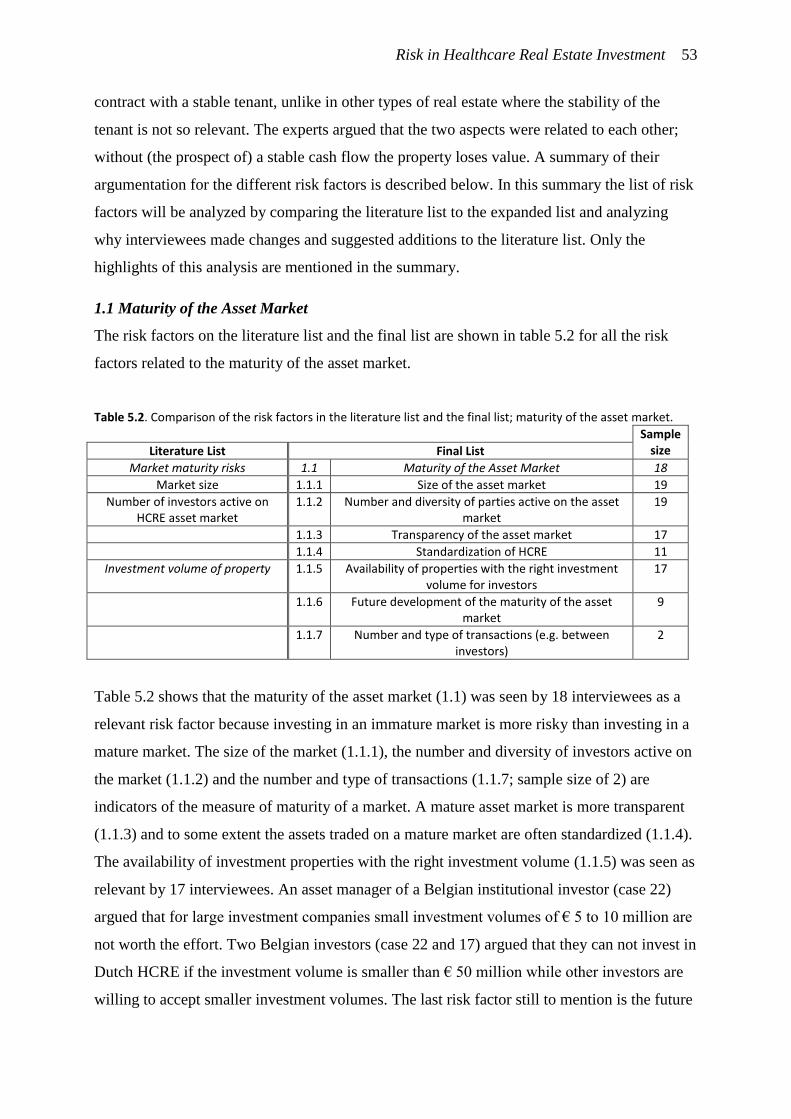

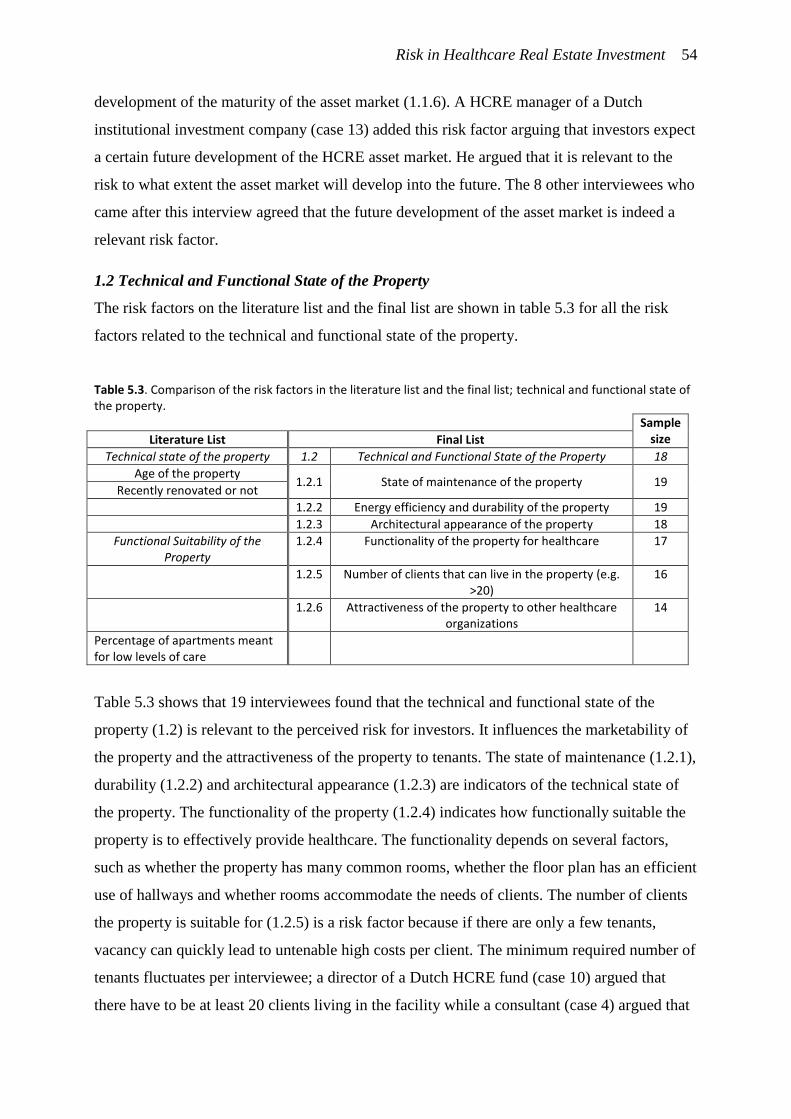

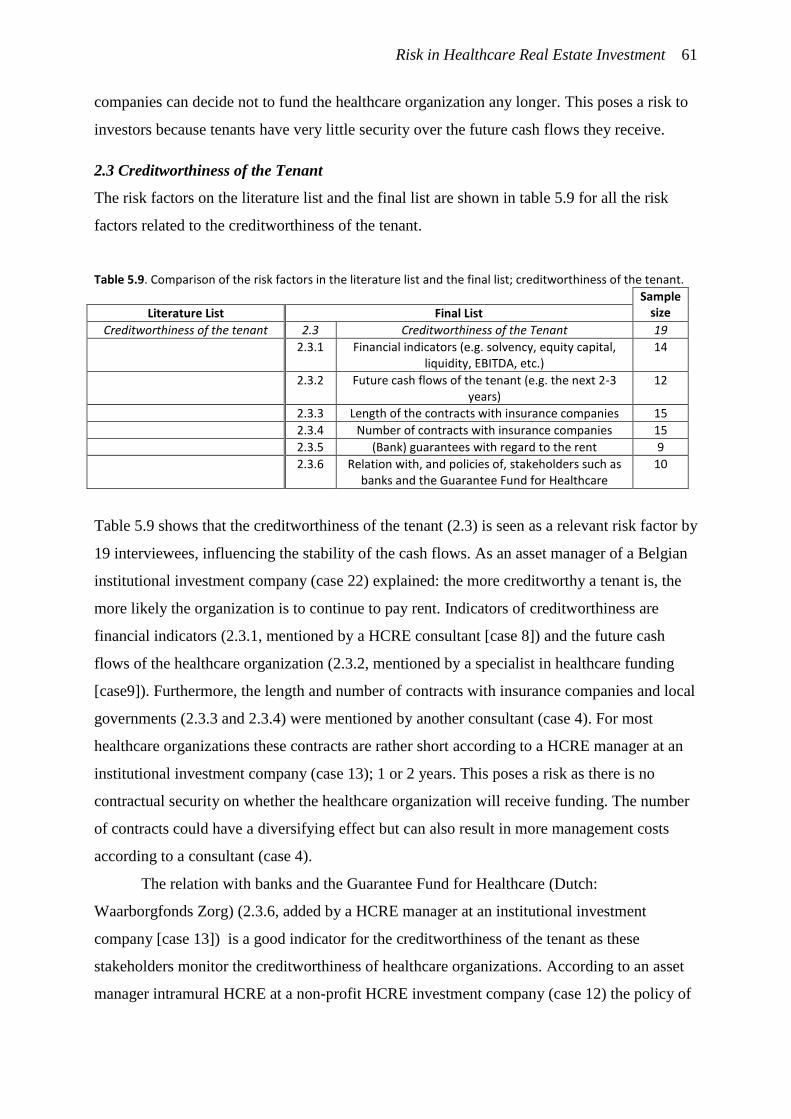

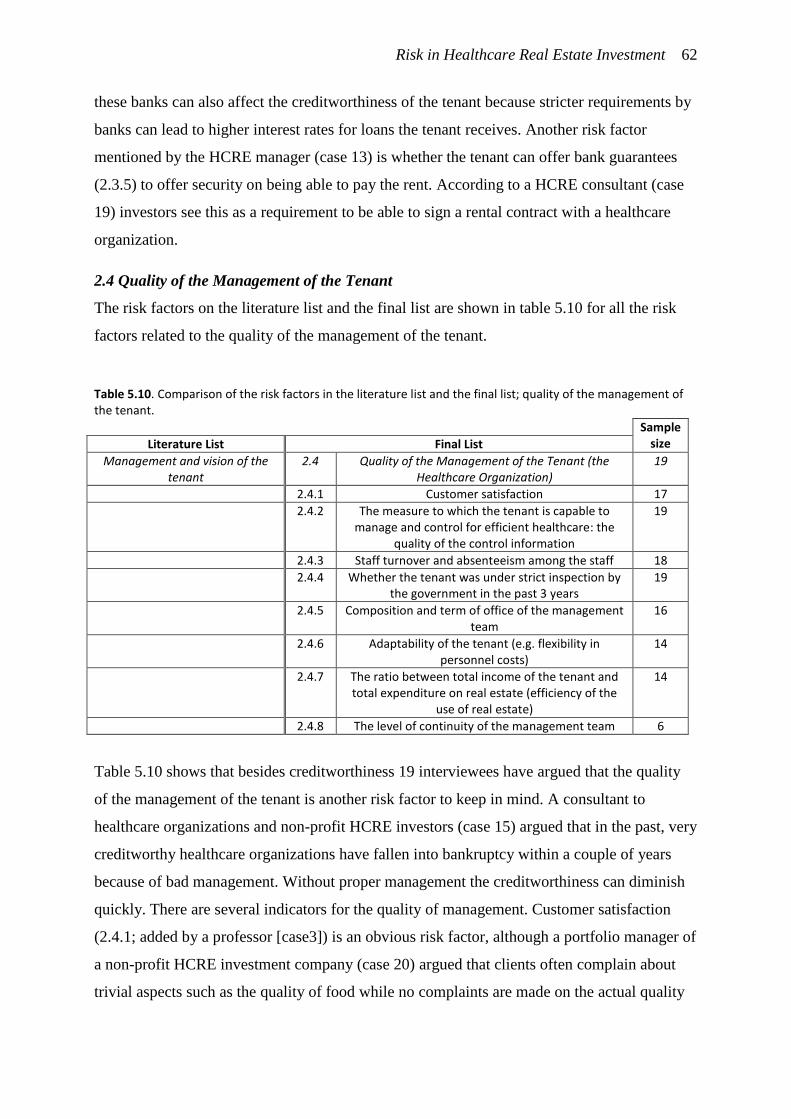

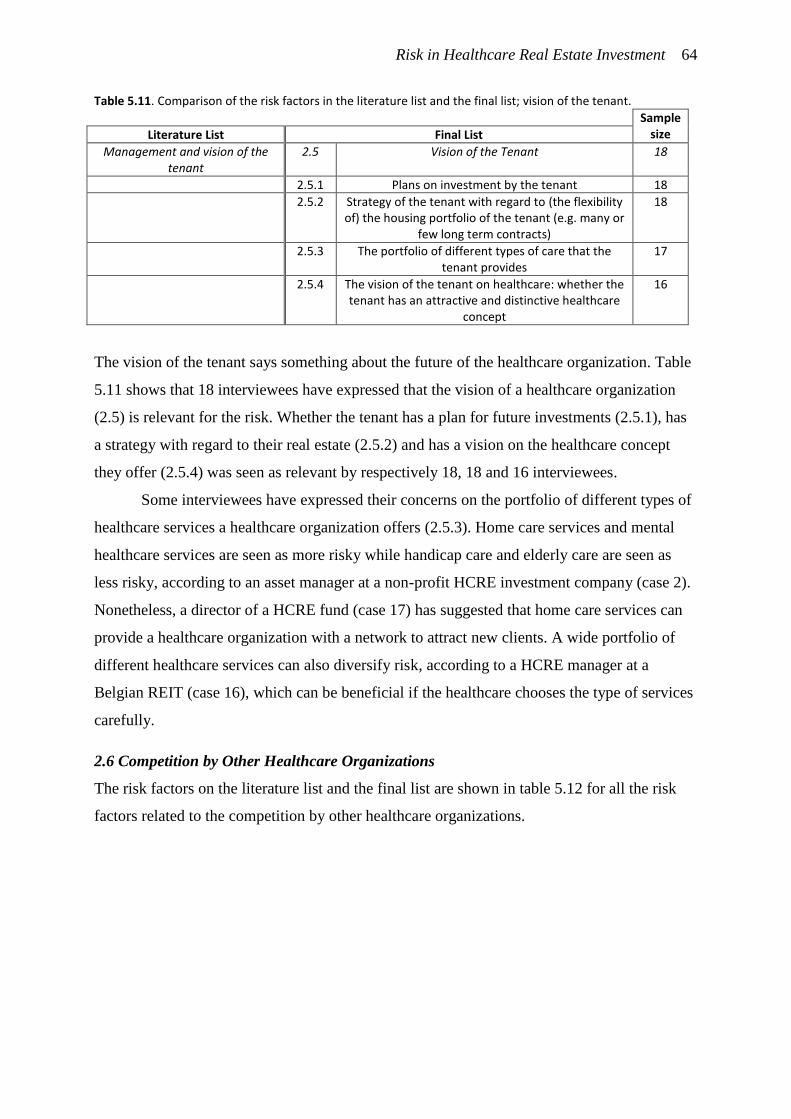

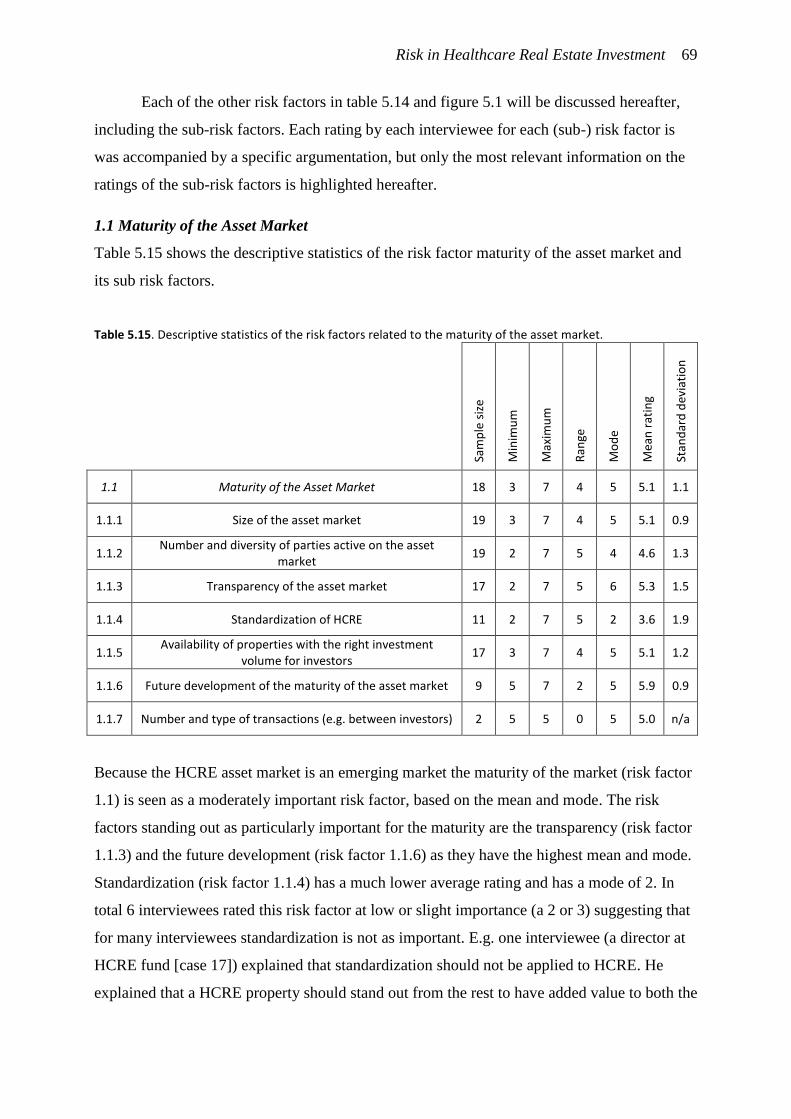

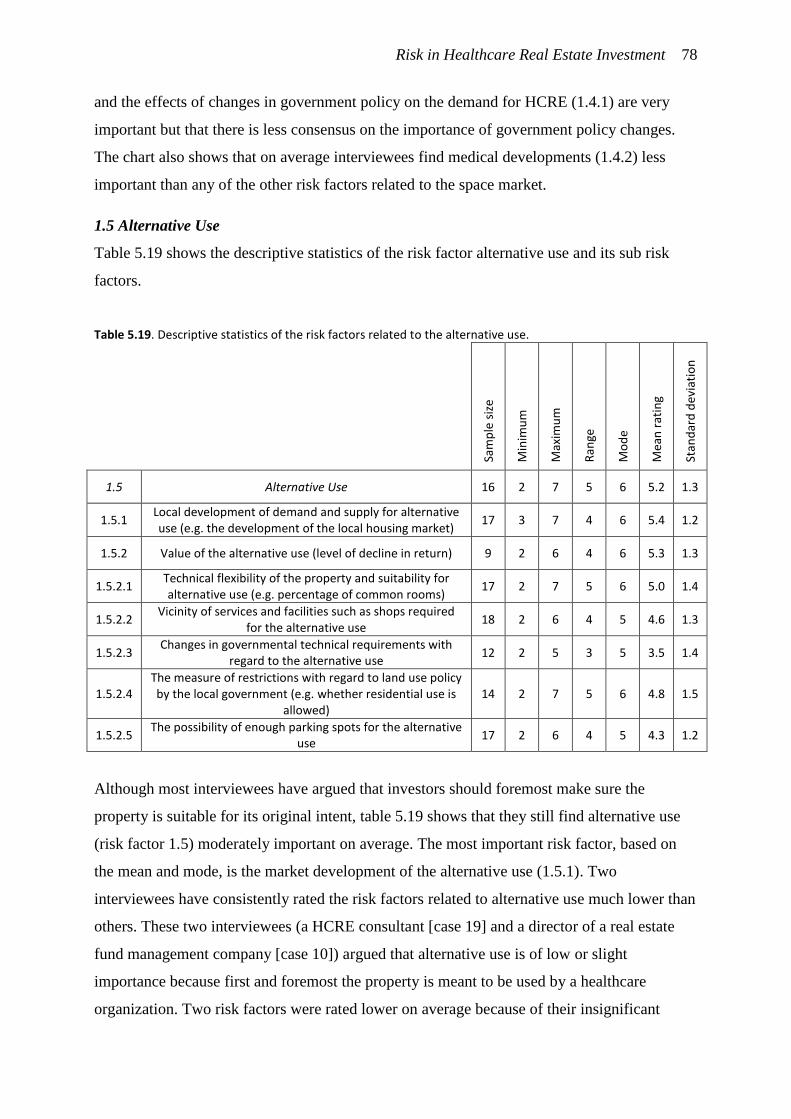

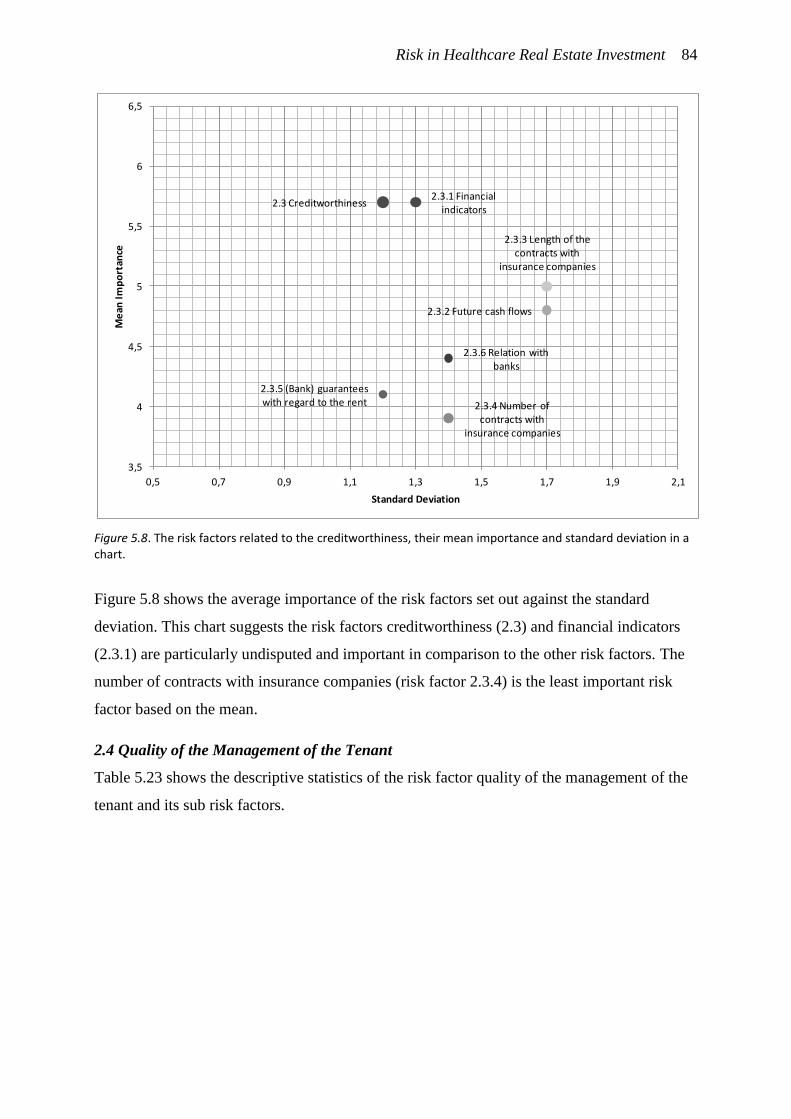

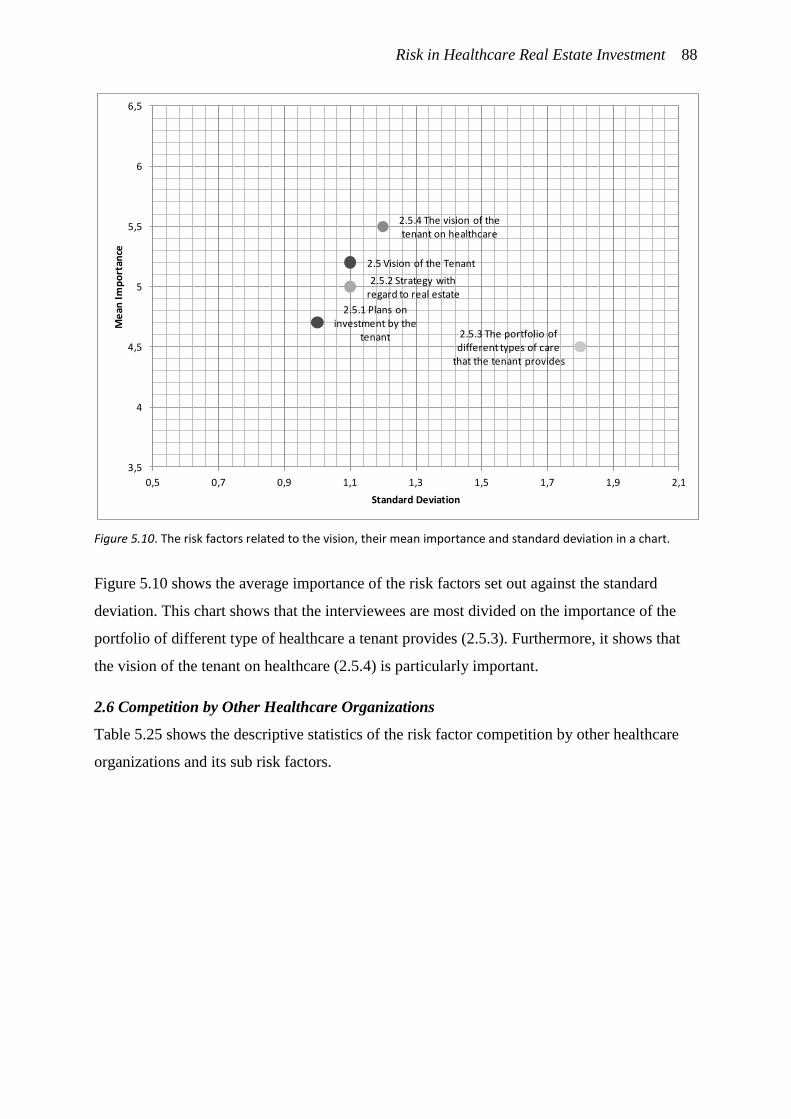

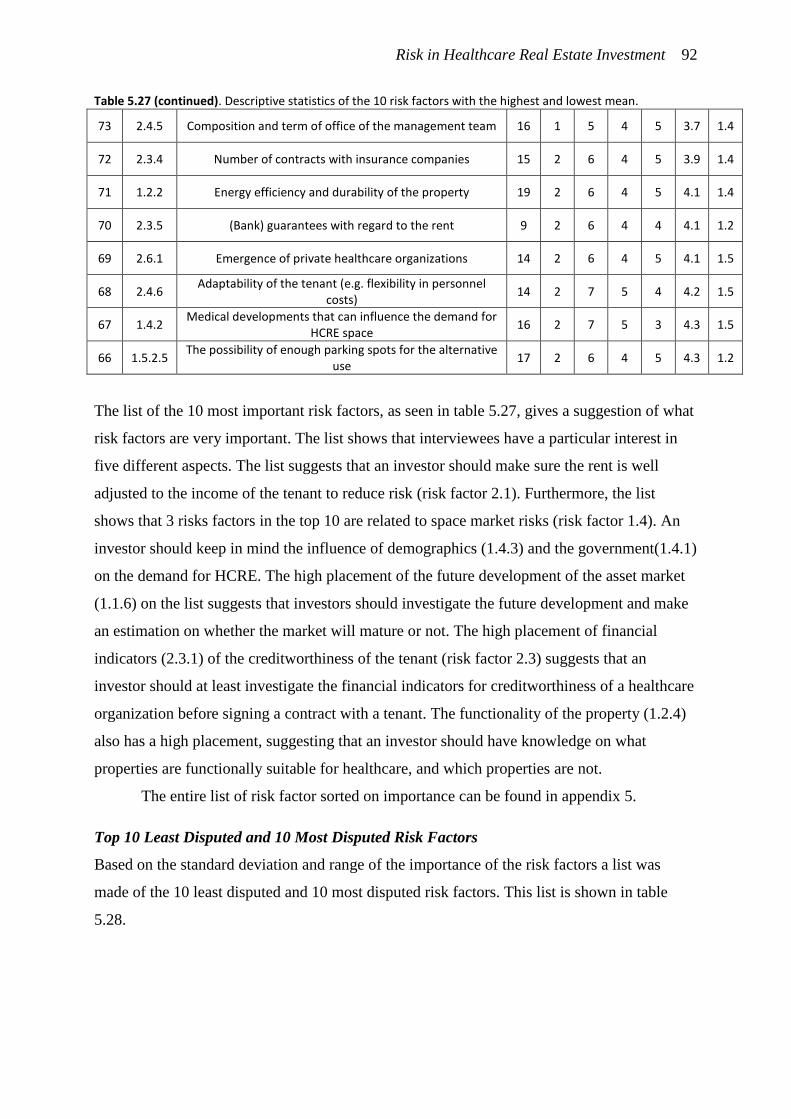

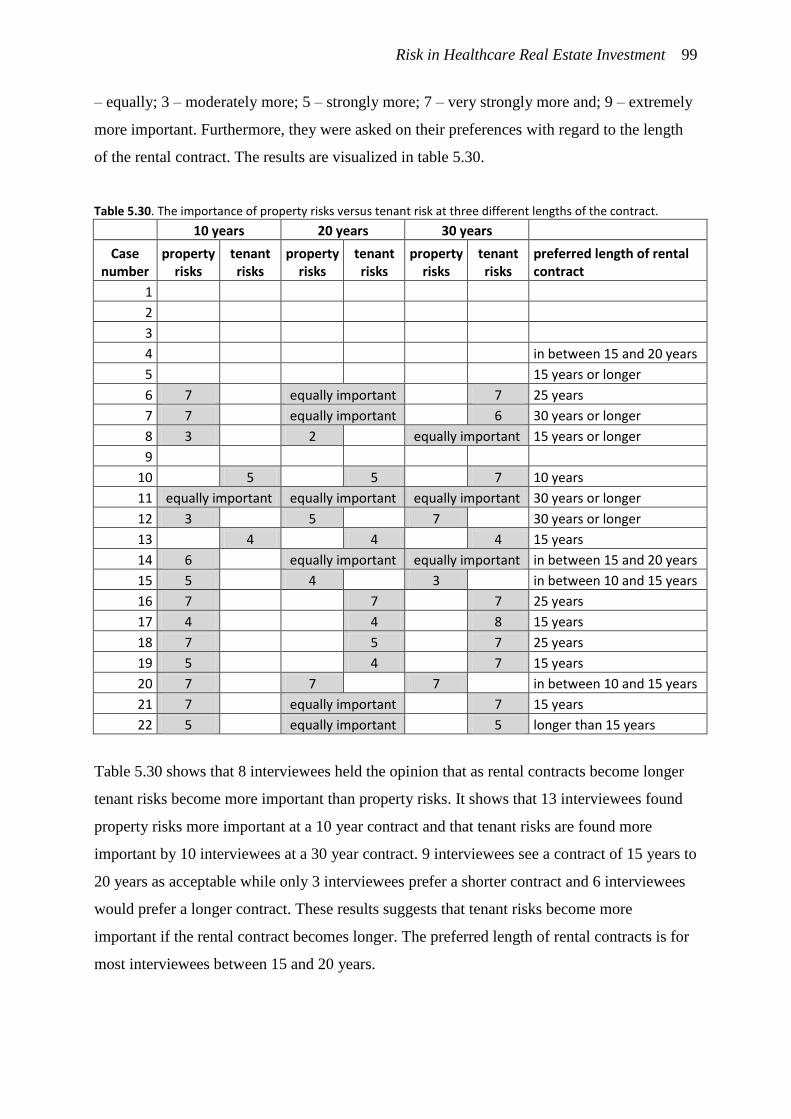

5. Results 49

5.1. Final List of Risk Factors 49

5.2. Importance of Risk Factors 66

5.3. Differences in Points of View between Interviewees 97

5.4. The Influence of the Length of Rental Contracts on the Risk 98

Risk in Healthcare Real Estate Investment vi

5.5. Chapter Conclusion 100

6. Conclusions and Discussion 101

6.1. Theoretical and Practical Implications 101

6.2. Recommendations on Managing the Risk Factors 103

6.3. Recommendations for Further Studies 104

6.4. Discussion 105

Reference List 107

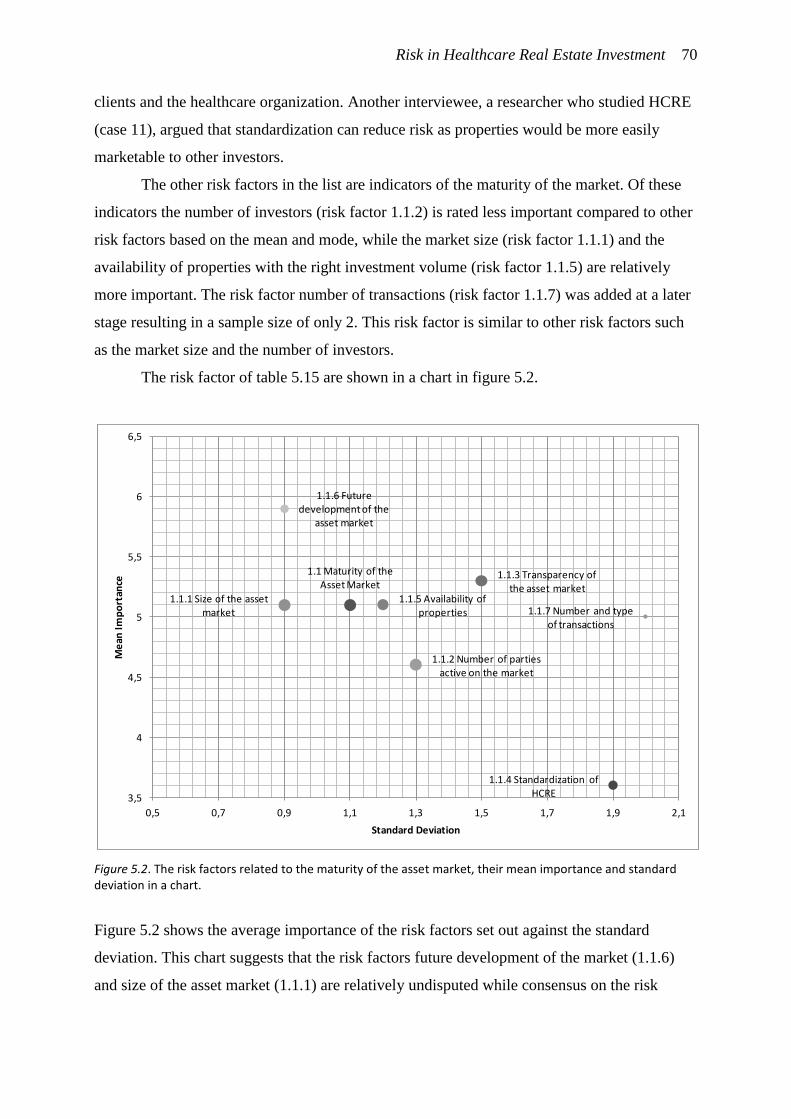

List of Abbreviations 113

List of Figures 114

List of Tables 116

List of Equations 119

Appendix 1: Oversight of Risk Factors from the Literature Review 1

Appendix 2: Interview guide for Interviews with Experts 2

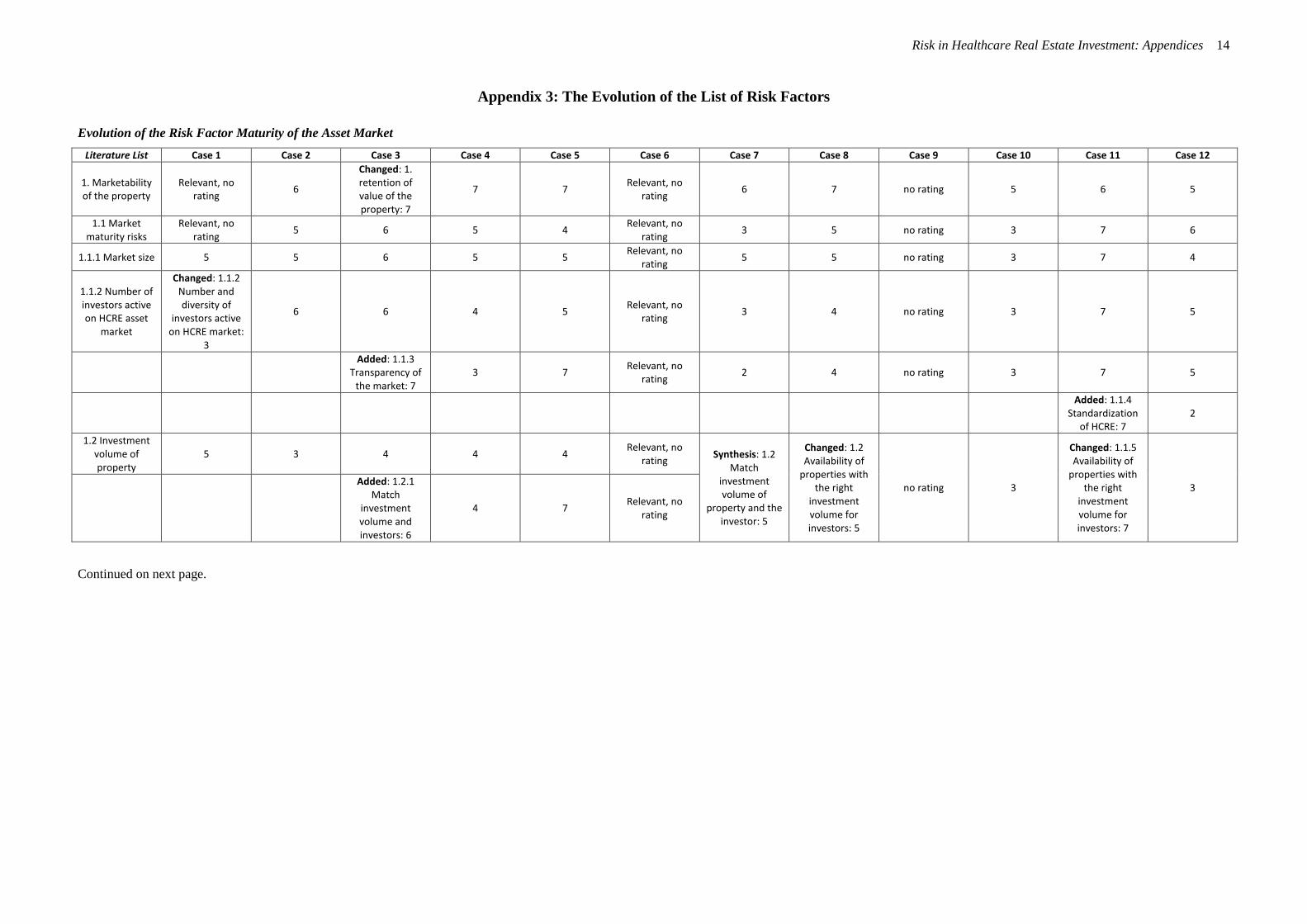

Appendix 3: The Evolution of the List of Risk Factors 14

Appendix 4: Descriptive Statistics of the Variables 29

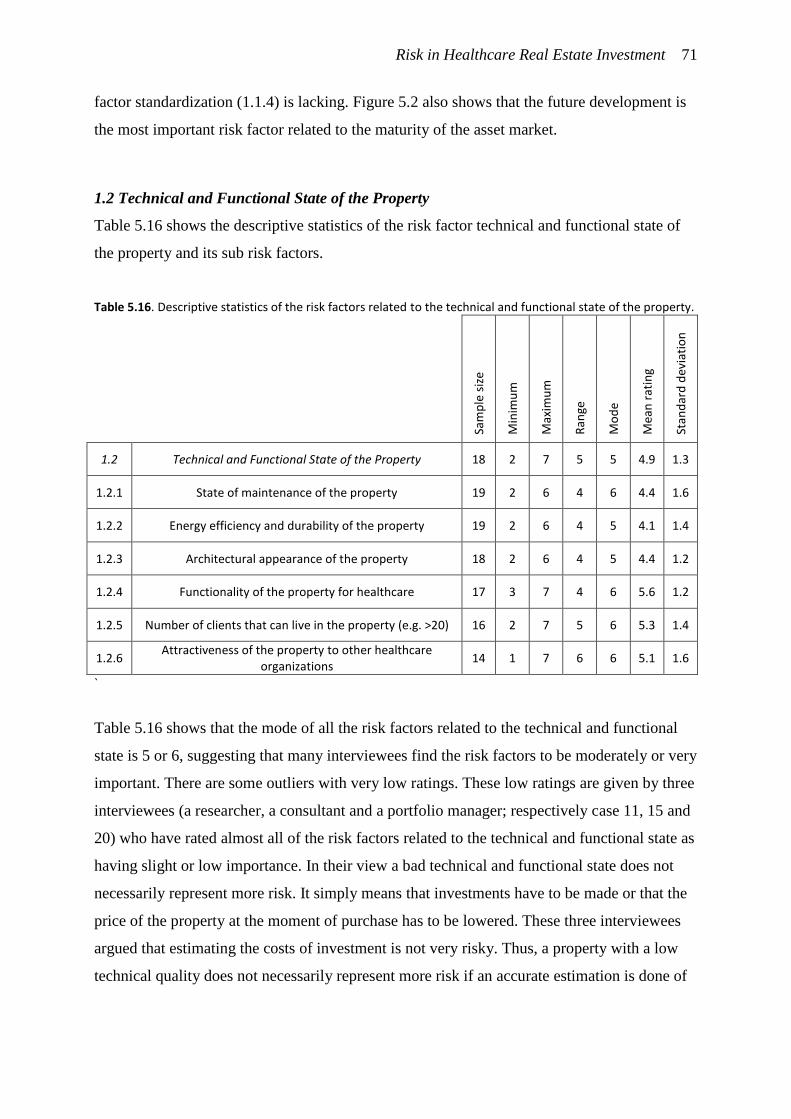

Appendix 5: All Risk Factors Sorted on Average Rating 33

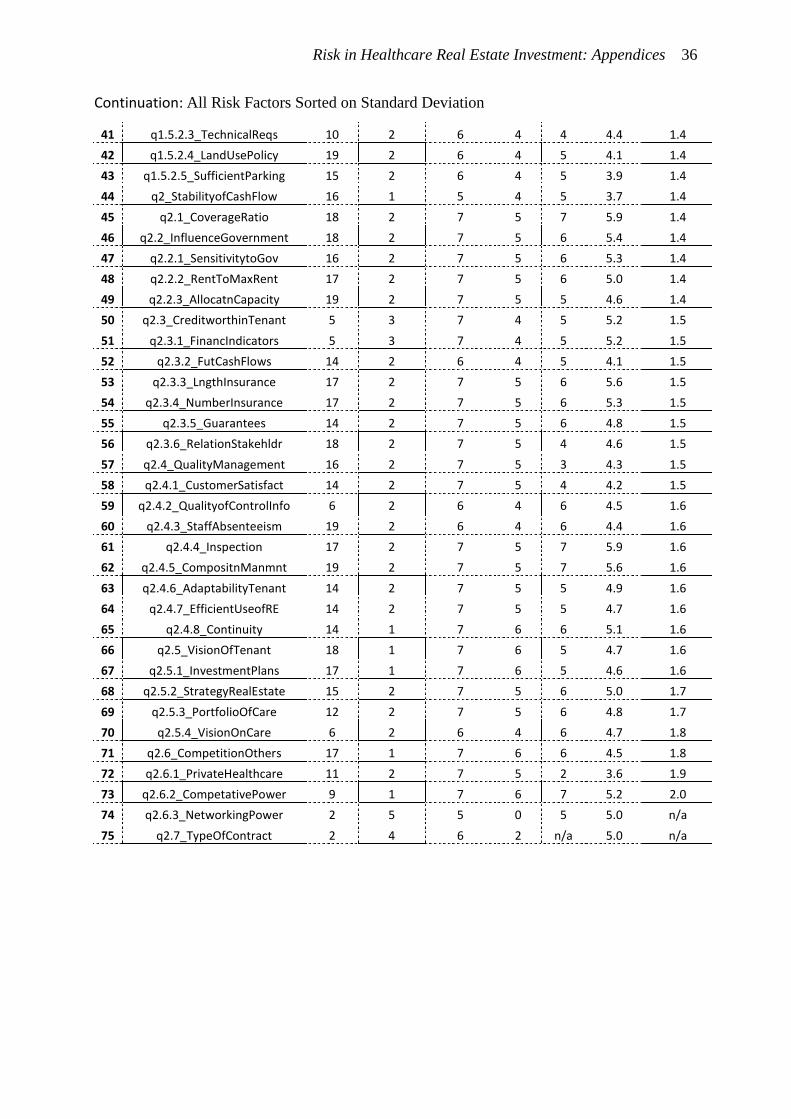

Appendix 6: All Risk Factors Sorted on Standard Deviation 35

Risk in Healthcare Real Estate Investment vii

Risico's bij beleggen in zorgvastgoed

Meer inzicht in het risico vanuit het perspectief van beleggers

Zorgvastgoed als beleggingscategorie is in opkomst in Nederland. Het wordt gezien als een

vastgoedcategorie die wordt gewaardeerd vanwege de stabiele kasstromen, hoge

rendementen en sterke demografische drivers. Ondanks de groeiende interesse is

zorgvastgoed nog een relatief onvolwassen markt. Vanwege de onduidelijkheid over de

risico's bij beleggen in zorgvastgoed zijn veel beleggers nog terughoudend bij het toetreden

tot deze markt. Er is een groeiende behoefte om de risico's bij beleggen in zorgvastgoed

goed in kaart te brengen.

Door ing. Tjeerd Kosse

isico's bij beleggen in vastgoed

zijn vaak onderzocht op basis van

kwantitatieve analyse. Recente

voorbeelden hiervan zijn onderzoeken die

gebruik maken van multifactor modellen

zoals die van Dale, Wolf & Yang (2015)

en Ho & Addae-Dapaah (2015). Daarnaast

zijn er vele onderzoeken geweest naar de

determinanten van de rendementseis,

waardonder door Sivitanidou & Sivitanides

(1999) en Wheaton et al. (2001). Ook op

micro-niveau zijn onderzoeken geweest

naar de determinanten van de

rendementseis. Hieronder valt onder

andere het onderzoek van McDonald &

Dermisi (2009). Wheaton et al.

concluderen dat de rendementseis sterk

samenhangt met onduidelijkheid over de

mate van risico. Omdat er nog geen

onderzoek is gedaan naar de risico's bij

beleggen in zorgvastgoed is er nog sprake

van grote onduidelijkheid. Dit onderzoek

biedt een kwalitatieve kijk op het risico bij

beleggen in zorgvastgoed.

De huidige praktijk

In de huidige praktijk gaat beleggen in

zorgvastgoed vaak gepaard met weinig

vertrouwen in de ontwikkeling van de

eindwaarde van het vastgoed. Omdat

beleggers lage verwachtingen hebben van

de eindwaarde proberen ze de

vastgoedgerelateerde risico's te mitigeren

door lange huurcontracten te tekenen. Op

deze wijze verplaatsen ze het risico van

een lage eindwaarde naar risico's

gerelateerd aan de stabiliteit van de

huurder. Huurders zijn echter niet altijd

bereid lange huurcontracten te tekenen

waardoor beleggers in het verleden

teleurgesteld zijn geraakt in de snelheid en

het gemak waarmee valt te beleggen in

zorgvastgoed. Zorgvastgoed is een

kennisintensief vastgoedtype waarbij

beleggers zowel rekening moeten houden

met vastgoedgerelateerde risico's als

huurdergerelateerde risico's. Uit de

resultaten van dit onderzoek blijkt welke

risico's dit zijn.

R

Risk in Healthcare Real Estate Investment viii

Methode

Dit onderzoek is gedaan aan de hand van

een literatuuronderzoek en 22 interviews

met experts op het gebied van beleggen in

zorgvastgoed. Onder de experts bevonden

zich 11 vertegenwoordigers van

vastgoedbeleggingsmaatschappijen en

woningcorporaties, 7 adviseurs en 4

overige experts. Op basis van de literatuur

is een lijst van risicofactoren opgesteld. De

risicofactoren op deze lijst zijn door de

geïnterviewden aangevuld en beoordeeld

op belangrijkheid op een 7-puntsschaal van

1 (helemaal niet belangrijk) tot 7 (extreem

belangrijk).

Resultaten

De resultaten laten zien dat bij beleggen in

zorgvastgoed zowel vastgoedgerelateerde

als huurdergerelateerde risicofactoren een

rol spelen. Bijlage 1 laat een vergelijking

zien van de risicofactoren verkregen uit

een synthese van de risicofactoren die

gevonden zijn in de literatuur en de

uiteindelijk lijst met risicofactoren uit dit

onderzoek. De vergelijking laat zien dat

vele risicofactoren niet genoemd zijn in de

literatuur. Vooral risicofactoren gerelateerd

aan de stabiliteit van de huurder komen

vrijwel niet voor in de bestaande literatuur.

Onder vastgoedgerelateerde risicofactoren

worden op hoofdniveau verstaan:

1.1 Volwassenheid van de assetmarkt;

1.2 Technische en functionele staat van

het object;

1.3 Fysieke locatie;

1.4 Veranderingen op de (lokale)

ruimtemarkt en;

1.5 Alternatieve aanwendbaarheid.

De huurdergerelateerde risicofactoren zijn

op hoofdniveau:

2.1 De verhouding tussen inkomsten

van de huurder gegenereerd in het

object en de huur van het object

(coverage ratio);

2.2 Invloed van veranderingen in

overheidsbeleid op huurder;

2.3 Kredietwaardigheid van de huurder;

2.4 Kwaliteit van het management van

de huurder;

2.5 Toekomstvisie van de huurder;

2.6 Concurrentie van andere

zorgverleners en;

2.7 Type contract.

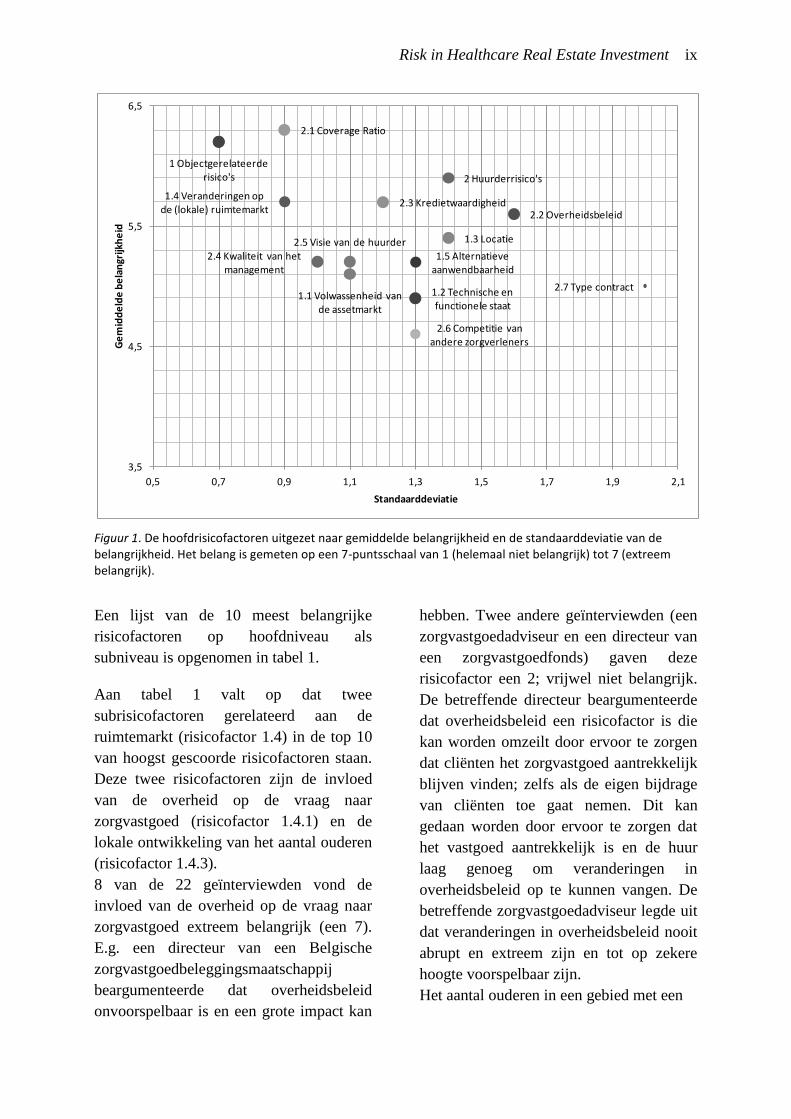

De mate van belangrijkheid van deze

risicofactoren is weergegeven in figuur 1.

In dit figuur is de gemiddelde score van de

risicofactoren uitgezet tegenover de

standaarddeviatie. Aan figuur 1 is te zien

dat de geïnterviewden het met elkaar eens

waren over dat objectgerelateerde risico's

(risicofactor 1) zeer belangrijk zijn terwijl

er meer onenigheid is over het belang van

huurdergerelateerde risico's (risicofactor

2). Verder valt op dat de coverage ratio

(risicofactor 2.1) gemiddeld het

belangrijkst wordt gevonden. Een directeur

van een Belgische zorgvastgoed-

beleggingsmaatschappij legde uit waarom

hij een hoge score gaf aan deze

risicofactor. Door het aanpassen van het

huurniveau aan het inkomen van de

huurder kan een groot deel van het

huurderrisico worden verminderd. Hij

voegde eraan toe dat het inkomen van

zorginstellingen sterk afhankelijk is van

overheidregulering, waardoor de meeste

zorginstellingen vrijwel hetzelfde

maximale inkomen kunnen genereren. Om

deze reden vrijwel alle geïnterviewden de

coverage ratio erg belangrijk.

Risk in Healthcare Real Estate Investment ix

Figuur 1. De hoofdrisicofactoren uitgezet naar gemiddelde belangrijkheid en de standaarddeviatie van de belangrijkheid. Het belang is gemeten op een 7-puntsschaal van 1 (helemaal niet belangrijk) tot 7 (extreem belangrijk).

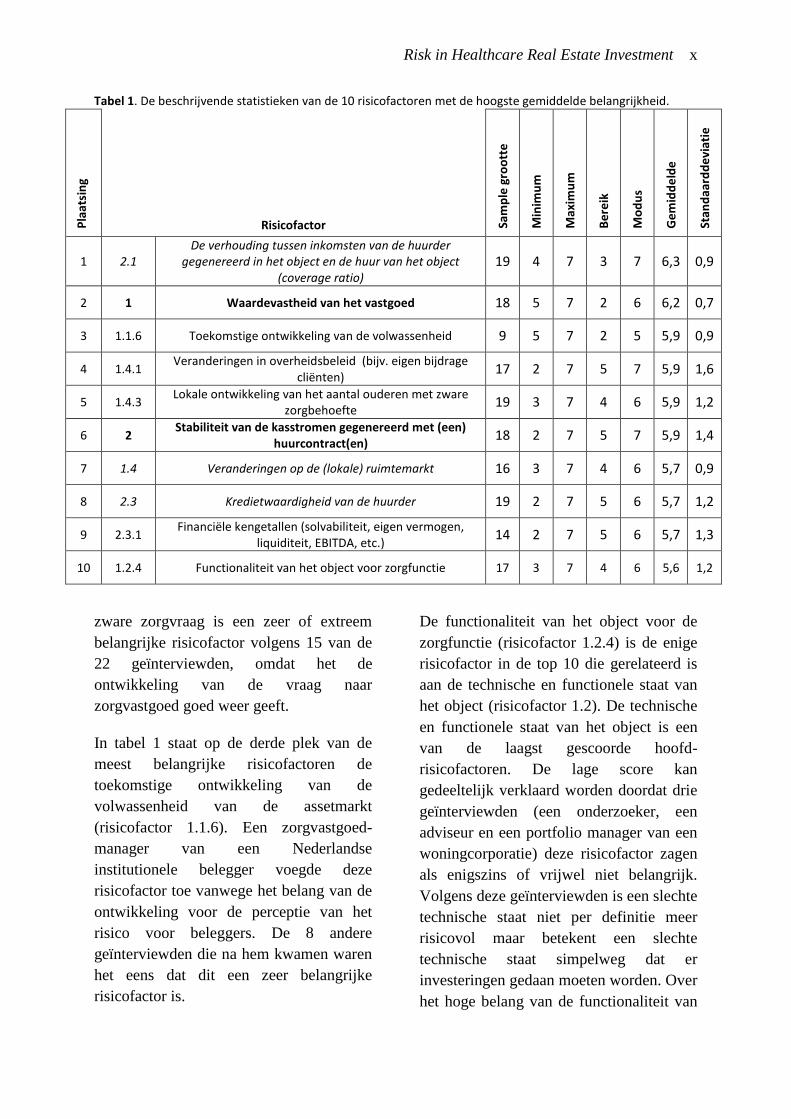

Een lijst van de 10 meest belangrijke

risicofactoren op hoofdniveau als

subniveau is opgenomen in tabel 1.

Aan tabel 1 valt op dat twee

subrisicofactoren gerelateerd aan de

ruimtemarkt (risicofactor 1.4) in de top 10

van hoogst gescoorde risicofactoren staan.

Deze twee risicofactoren zijn de invloed

van de overheid op de vraag naar

zorgvastgoed (risicofactor 1.4.1) en de

lokale ontwikkeling van het aantal ouderen

(risicofactor 1.4.3).

8 van de 22 geïnterviewden vond de

invloed van de overheid op de vraag naar

zorgvastgoed extreem belangrijk (een 7).

E.g. een directeur van een Belgische

zorgvastgoedbeleggingsmaatschappij

beargumenteerde dat overheidsbeleid

onvoorspelbaar is en een grote impact kan

hebben. Twee andere geïnterviewden (een

zorgvastgoedadviseur en een directeur van

een zorgvastgoedfonds) gaven deze

risicofactor een 2; vrijwel niet belangrijk.

De betreffende directeur beargumenteerde

dat overheidsbeleid een risicofactor is die

kan worden omzeilt door ervoor te zorgen

dat cliënten het zorgvastgoed aantrekkelijk

blijven vinden; zelfs als de eigen bijdrage

van cliënten toe gaat nemen. Dit kan

gedaan worden door ervoor te zorgen dat

het vastgoed aantrekkelijk is en de huur

laag genoeg om veranderingen in

overheidsbeleid op te kunnen vangen. De

betreffende zorgvastgoedadviseur legde uit

dat veranderingen in overheidsbeleid nooit

abrupt en extreem zijn en tot op zekere

hoogte voorspelbaar zijn.

Het aantal ouderen in een gebied met een

1 Objectgerelateerde risico's

1.1 Volwassenheid van de assetmarkt

1.2 Technische en functionele staat

1.3 Locatie

1.4 Veranderingen op de (lokale) ruimtemarkt

1.5 Alternatieve aanwendbaarheid

2 Huurderrisico's

2.1 Coverage Ratio

2.2 Overheidsbeleid2.3 Kredietwaardigheid

2.4 Kwaliteit van het management

2.5 Visie van de huurder

2.6 Competitie van andere zorgverleners

2.7 Type contract

3,5

4,5

5,5

6,5

0,5 0,7 0,9 1,1 1,3 1,5 1,7 1,9 2,1

Ge

mid

de

lde

be

lan

grijk

he

id

Standaarddeviatie

Risk in Healthcare Real Estate Investment x

Tabel 1. De beschrijvende statistieken van de 10 risicofactoren met de hoogste gemiddelde belangrijkheid.

Pla

atsi

ng

Risicofactor

Sam

ple

gro

ott

e

Min

imu

m

Max

imu

m

Be

reik

Mo

du

s

Ge

mid

de

lde

Stan

daa

rdd

evi

atie

1 2.1 De verhouding tussen inkomsten van de huurder

gegenereerd in het object en de huur van het object (coverage ratio)

19 4 7 3 7 6,3 0,9

2 1 Waardevastheid van het vastgoed 18 5 7 2 6 6,2 0,7

3 1.1.6 Toekomstige ontwikkeling van de volwassenheid 9 5 7 2 5 5,9 0,9

4 1.4.1 Veranderingen in overheidsbeleid (bijv. eigen bijdrage

cliënten) 17 2 7 5 7 5,9 1,6

5 1.4.3 Lokale ontwikkeling van het aantal ouderen met zware

zorgbehoefte 19 3 7 4 6 5,9 1,2

6 2 Stabiliteit van de kasstromen gegenereerd met (een)

huurcontract(en) 18 2 7 5 7 5,9 1,4

7 1.4 Veranderingen op de (lokale) ruimtemarkt 16 3 7 4 6 5,7 0,9

8 2.3 Kredietwaardigheid van de huurder 19 2 7 5 6 5,7 1,2

9 2.3.1 Financiële kengetallen (solvabiliteit, eigen vermogen,

liquiditeit, EBITDA, etc.) 14 2 7 5 6 5,7 1,3

10 1.2.4 Functionaliteit van het object voor zorgfunctie 17 3 7 4 6 5,6 1,2

zware zorgvraag is een zeer of extreem

belangrijke risicofactor volgens 15 van de

22 geïnterviewden, omdat het de

ontwikkeling van de vraag naar

zorgvastgoed goed weer geeft.

In tabel 1 staat op de derde plek van de

meest belangrijke risicofactoren de

toekomstige ontwikkeling van de

volwassenheid van de assetmarkt

(risicofactor 1.1.6). Een zorgvastgoed-

manager van een Nederlandse

institutionele belegger voegde deze

risicofactor toe vanwege het belang van de

ontwikkeling voor de perceptie van het

risico voor beleggers. De 8 andere

geïnterviewden die na hem kwamen waren

het eens dat dit een zeer belangrijke

risicofactor is.

De functionaliteit van het object voor de

zorgfunctie (risicofactor 1.2.4) is de enige

risicofactor in de top 10 die gerelateerd is

aan de technische en functionele staat van

het object (risicofactor 1.2). De technische

en functionele staat van het object is een

van de laagst gescoorde hoofd-

risicofactoren. De lage score kan

gedeeltelijk verklaard worden doordat drie

geïnterviewden (een onderzoeker, een

adviseur en een portfolio manager van een

woningcorporatie) deze risicofactor zagen

als enigszins of vrijwel niet belangrijk.

Volgens deze geïnterviewden is een slechte

technische staat niet per definitie meer

risicovol maar betekent een slechte

technische staat simpelweg dat er

investeringen gedaan moeten worden. Over

het hoge belang van de functionaliteit van

Risk in Healthcare Real Estate Investment xi

het object was meer consensus onder de

geïnterviewden.

De enige subrisicofactor die in de top 10

staat, en gerelateerd is aan de

huurderrisico, is de financiële kengetallen

van een huurder (risicofactor 2.3.1).

Financiële kengetallen tonen de

kredietwaardigheid van een huurder

(risicofactor 2.3) die door veel

geïnterviewden belangrijk wordt

gevonden. Een kredietwaardige huurder

betekent minder risico dat de huurder

vroegtijdig het contract moet opzeggen

vanwege een faillissement. Een

zorgvastgoedadviseur waarschuwde dat,

ook al is het analyseren van de

kredietwaardigheid een goede manier om

contractrisico te mitigeren, de

kredietwaardigheid van de zorginstelling

snel kan dalen als de zorginstelling slecht

management heeft of een slechte visie

heeft.

Verschillende zienswijzen beleggers

Tijdens de interviews werd het duidelijk

dat er twee verschillende manieren zijn om

naar beleggen in zorgvastgoed te kijken.

Sommige beleggers hebben de neiging om

risico te beheersen door zich te richten op

het risico van een instabiele huurder.

Andere beleggers proberen risico te

verminderen door alleen in objecten te

beleggen met een lage kans op

waardevermindering, zelfs als de huurder

failliet zou gaan. Het eerste perspectief

heeft overeenkomsten met

bedrijfsfinanciering, terwijl de het tweede

perspectief typerend is voor

vastgoedbeleggers.

Invloed van lengte huurcontract

De meest gebruikelijke lengte van

huurcontracten bij zorgvastgoed is 15 jaar.

Wanneer men korte huurcontracten

gebruikt van 10 jaar zijn objectgerelateerde

risico's belangrijker terwijl huurderrisico's

belangrijker zijn als men huurcontracten

gebruikt van langer dan 20 jaar. Markten

met kortere huurcontracten zijn meer

geschikt voor beleggers die zich richten op

objectgerelateerde risico's terwijl markten

met lange huurcontracten meer geschikt

zijn voor beleggers die zich richten op

huurderrisico's. Omdat zorginstellingen

niet altijd bereid zijn om lange

huurcontracten te tekenen kunnen zij een

verschuiving laten plaatsen waarbij

beleggers steeds meer aandacht besteden

aan objectgerelateerde risicofactoren in

plaats van huurdergerelateerde

risicofactoren.

Onzekerheid over het risico

De onderzoeksresultaten laten zien dat er

nog onzekerheid is over de mate van risico

bij beleggen in zorgvastgoed. De

risicofactoren hebben een

standaarddeviatie tussen de 0,7 en 2,0. Dit

suggereert dat meningen van experts over

de belangrijkheid van de risicofactoren

uiteen lopen. De gemiddelde score van 4,9

laat zien dat risicofactoren asymmetrisch

zijn gescoord. Een mogelijke verklaring

hiervoor zou kunnen zijn dat

geïnterviewden bij twijfel risicofactoren

belangrijker inschatten.

Conclusies

De bevindingen van dit onderzoek zijn van

toegevoegde waarde voor de bestaande

literatuur op een aantal manieren. Dit

onderzoek laat zien dat, naast macro-

economische risicofactoren, er ook

risicofactoren zijn op microniveau die de

risicoperceptie van beleggers beïnvloeden.

Het laat zien dat er verschillen zijn in

risicoperceptie tussen beleggers en dat er

Risk in Healthcare Real Estate Investment xii

verschillende manieren zijn om beleggen

in zorgvastgoed te benaderen. Bovendien

legt het de onzekerheden bloot die er zijn

bij beleggen in zorgvastgoed en toont dat

onzekerheid een rol speelt bij de

risicoperceptie bij beleggen in

zorgvastgoed.

De resultaten geven beleggers, taxateurs en

onderzoekers input voor een betere

benadering van risico. De risicofactoren en

hun belang kunnen gebruikt worden bij

beleggingsbeslissingen en bij het maken

van betere waardebepalingen. Door de

risicofactoren en hun belang in kaart te

brengen draagt dit onderzoek ook bij aan

de transparantie en volwassenheid van

zorgvastgoedmarkt.

Discussie

Dit onderzoek heeft enkele beperkingen.

Zo kunnen vraagtekens worden gezet bij

de onderzoeksmethode die heeft geleid tot

een te groot aantal risicofactoren. Een

selectie van de meest belangrijke

risicofactoren kunnen in

vervolgonderzoeken worden gebruikt om

het risico bij beleggen in zorgvastgoed

nader te bepalen. Ondanks deze

beperkingen heeft het onderzoek de kennis

over de risico's bij beleggen in

zorgvastgoed uitgebreid. Dit onderzoek is

het eerste kwalitatieve onderzoek naar

Nederlands zorgvastgoed dat zich volledig

richt op de risico's. Het biedt beleggers

nieuwe kennis die ze kunnen

implementeren in hun beslissingsproces en

geeft inzicht in de verschillende

zienswijzen van beleggers.

Bronnen

Dale, D., Wolf, R., & Yang, H.F. (2015).

An assessment of the risk and return of

residential real estate. Managerial

Finance, 41(6), 591 - 599.

Ho, D.K.H., & Addae-Dapaah, K. (2015).

International Direct Real Estate Risk

Premiums in a Multi-Factor Estimation

Model. Journal of Real Estate Financial

Economics, 52–85.

McDonald, J.F., & & Dermisi, S. (2009).

Office building capitalization rates: the

case of downtown Chicago. The Journal

of Real Estate Finance and Economics,

39(4), 472-485.

Sivitanidou, R.C., & Sivitanides, P.S.

(1999). Office Capitalization Rates: Real

Estate and Capital Market Influences.

Journal of Real Estate Finance and

Economics, (18)3, 297-322.

Wheaton, W.C., Torto, R.G., Sivitanides,

P.S., Southard, J.A., Hopkins, R.E., &

Costello, J.M. (2001). Real estate risk: a

forward-looking approach. Real Estate

Finance, 18(3), 20-28.

Risk in Healthcare Real Estate Investment xiii

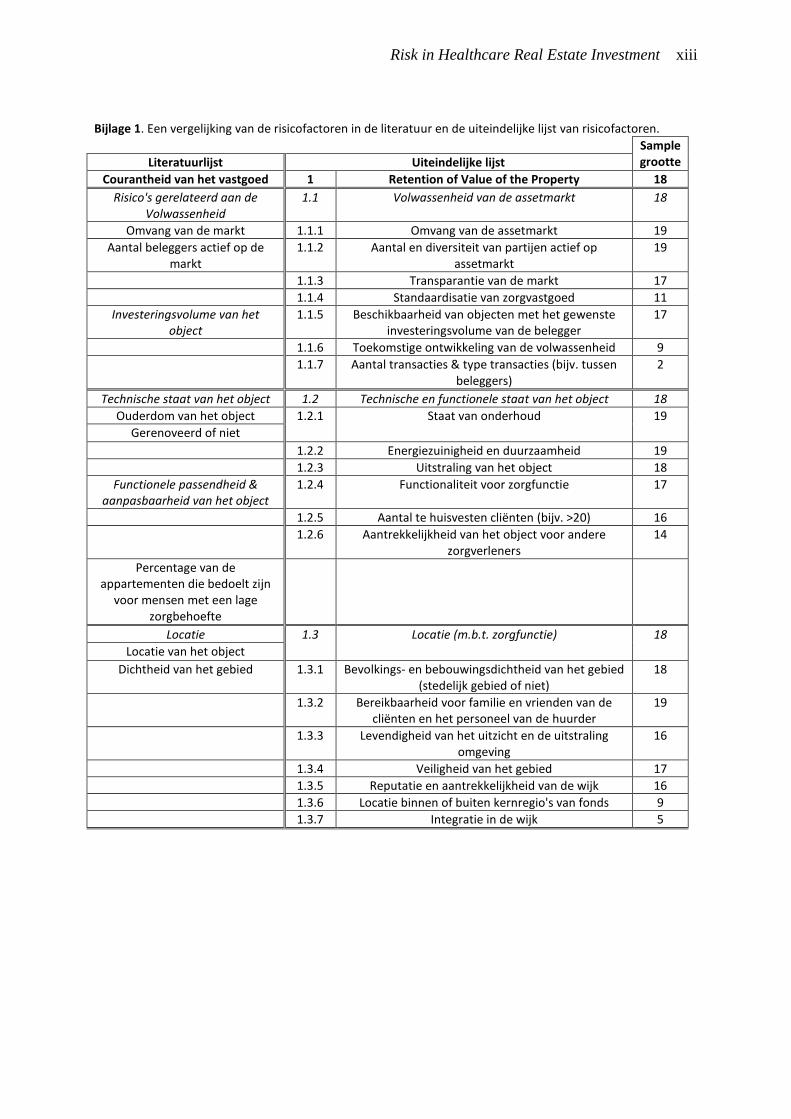

Bijlage 1. Een vergelijking van de risicofactoren in de literatuur en de uiteindelijke lijst van risicofactoren.

Sample grootte Literatuurlijst Uiteindelijke lijst

Courantheid van het vastgoed 1 Retention of Value of the Property 18

Risico's gerelateerd aan de Volwassenheid

1.1 Volwassenheid van de assetmarkt 18

Omvang van de markt 1.1.1 Omvang van de assetmarkt 19

Aantal beleggers actief op de markt

1.1.2 Aantal en diversiteit van partijen actief op assetmarkt

19

1.1.3 Transparantie van de markt 17

1.1.4 Standaardisatie van zorgvastgoed 11

Investeringsvolume van het object

1.1.5 Beschikbaarheid van objecten met het gewenste investeringsvolume van de belegger

17

1.1.6 Toekomstige ontwikkeling van de volwassenheid 9

1.1.7 Aantal transacties & type transacties (bijv. tussen beleggers)

2

Technische staat van het object 1.2 Technische en functionele staat van het object 18

Ouderdom van het object 1.2.1 Staat van onderhoud

19

Gerenoveerd of niet

1.2.2 Energiezuinigheid en duurzaamheid 19

1.2.3 Uitstraling van het object 18

Functionele passendheid & aanpasbaarheid van het object

1.2.4 Functionaliteit voor zorgfunctie 17

1.2.5 Aantal te huisvesten cliënten (bijv. >20) 16

1.2.6 Aantrekkelijkheid van het object voor andere zorgverleners

14

Percentage van de appartementen die bedoelt zijn

voor mensen met een lage zorgbehoefte

Locatie 1.3 Locatie (m.b.t. zorgfunctie)

18

Locatie van het object

Dichtheid van het gebied 1.3.1 Bevolkings- en bebouwingsdichtheid van het gebied (stedelijk gebied of niet)

18

1.3.2 Bereikbaarheid voor familie en vrienden van de cliënten en het personeel van de huurder

19

1.3.3 Levendigheid van het uitzicht en de uitstraling omgeving

16

1.3.4 Veiligheid van het gebied 17

1.3.5 Reputatie en aantrekkelijkheid van de wijk 16

1.3.6 Locatie binnen of buiten kernregio's van fonds 9

1.3.7 Integratie in de wijk 5

Risk in Healthcare Real Estate Investment xiv

Bijlage 1 (vervolg). Een vergelijking van de risicofactoren in de literatuur en de uiteindelijke lijst van risicofactoren.

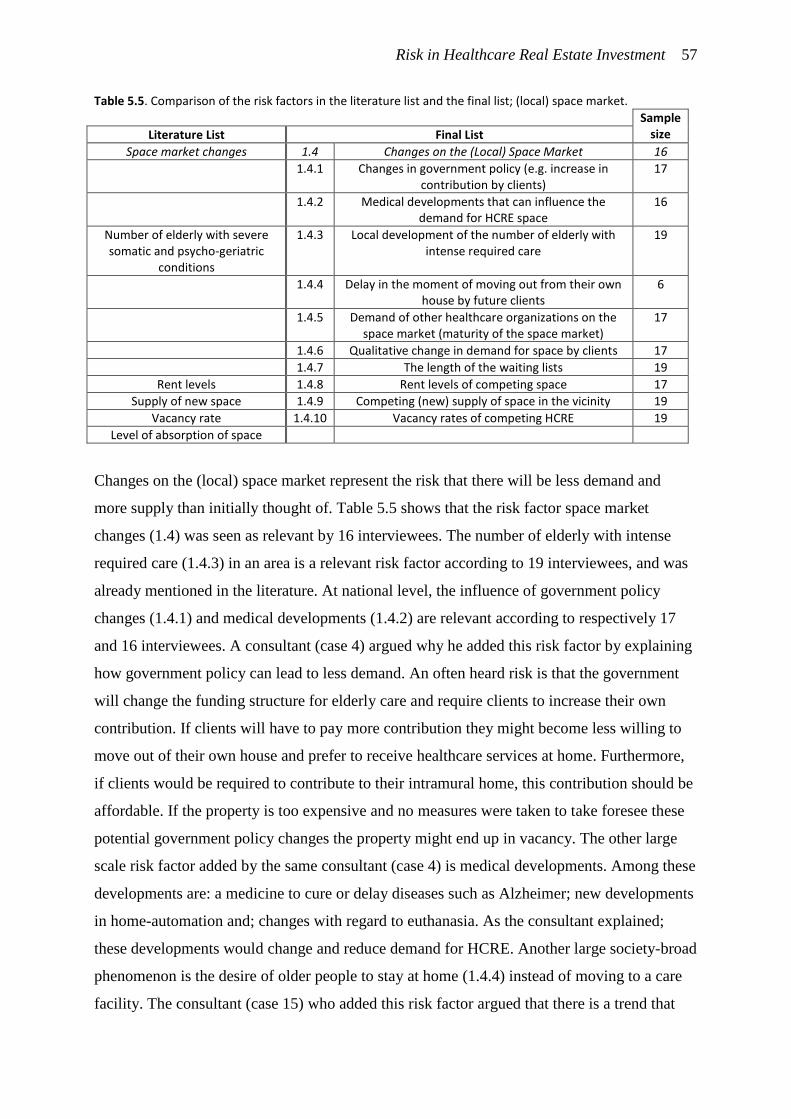

Veranderingen op de ruimtemarkt

1.4 Veranderingen op de (lokale) ruimtemarkt 16

1.4.1 Veranderingen in overheidsbeleid (bijv. eigen bijdrage cliënten)

17

1.4.2 Medische ontwikkeling die invloed hebben op vraag 16

Aantal ouderen met zware zorgbehoefte

1.4.3 Lokale ontwikkeling van het aantal ouderen met zware zorgbehoefte

19

1.4.4 Uitstellen van moment van uit eigen huis gaan van cliënten

6

1.4.5 Vraag van andere zorgverleners op de huurmarkt 17

1.4.6 Kwalitatieve verandering in vraagbehoefte 17

1.4.7 De lengte van de wachtlijsten 19

Huurniveaus 1.4.8 Huurniveaus van concurrerend aanbod 17

Aanbod aan nieuwe ruimte 1.4.9 Concurrerend (nieuw) ruimteaanbod in omgeving 19

Leegstandspercentage 1.4.10 Leegstandspercentages van concurrerend zorgvastgoed

19

Mate van absorptie van ruimte

1.5 Alternatieve aanwendbaarheid (andere functie) 16

1.5.1 Lokale ontwikkeling van vraag en aanbod alternatieve functies (bijv. ontwikkeling lokale

woningmarkt)

17

1.5.2 Waarde van alternatieve aanwending (rendementsterugval)

9

1.5.2.1 Bouwtechnische flexibiliteit en passendheid voor alternatieve functie (o.a. percentage algemene

ruimtes)

17

1.5.2.2 Nabijheid van voorzieningen voor alternatieve functie

18

1.5.2.3 Veranderende bouwbesluit-eisen bij alternatieve functie

12

1.5.2.4 Bestemmingsbeleid gemeente (bijv. woonbestemming)

14

1.5.2.5 Voldoende parkeerplaatsen 17

Betrouwbaarheid van de huurder

2 Stabiliteit van de kasstromen gegenereerd met (een) huurcontract(en)

18

De verhouding tussen de inkomsten van de huurder en de

huur

2.1 De verhouding tussen inkomsten van de huurder gegenereerd in het object en de huur van het object

(coverage ratio)

19

Veranderingen in overheidsbeleid 2.2 Invloed van veranderingen in overheidsbeleid op huurder

19

2.2.1 Gevoeligheid van huurder voor beleidsveranderingen op nationaal- en

gemeenteniveau

17

2.2.2 Verhouding huur en de maximale huur op basis van het woningwaarderingsstelsel bij Scheiden Wonen

Zorg

14

2.2.3 Ontwikkeling van het beleid van zorgkantoren/zorgverzekeraars (bijv. toekenning

capaciteit)

14

Risk in Healthcare Real Estate Investment xv

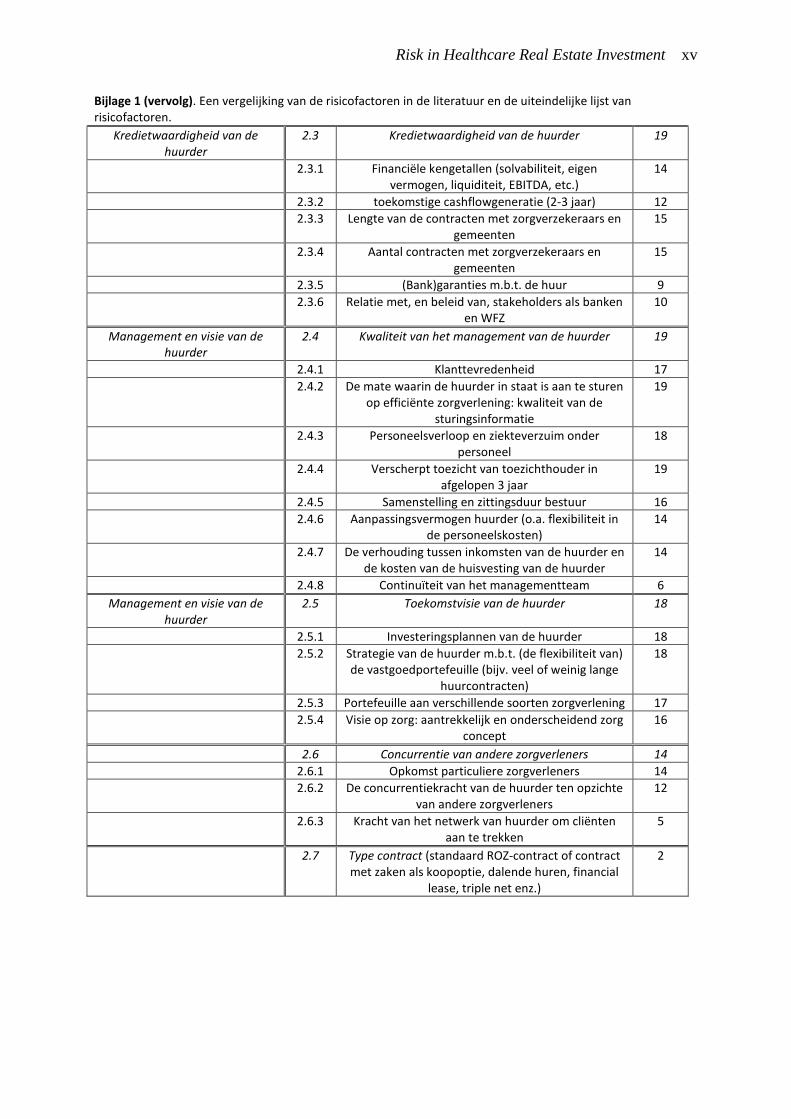

Bijlage 1 (vervolg). Een vergelijking van de risicofactoren in de literatuur en de uiteindelijke lijst van risicofactoren.

Kredietwaardigheid van de huurder

2.3 Kredietwaardigheid van de huurder 19

2.3.1 Financiële kengetallen (solvabiliteit, eigen vermogen, liquiditeit, EBITDA, etc.)

14

2.3.2 toekomstige cashflowgeneratie (2-3 jaar) 12

2.3.3 Lengte van de contracten met zorgverzekeraars en gemeenten

15

2.3.4 Aantal contracten met zorgverzekeraars en gemeenten

15

2.3.5 (Bank)garanties m.b.t. de huur 9

2.3.6 Relatie met, en beleid van, stakeholders als banken en WFZ

10

Management en visie van de huurder

2.4 Kwaliteit van het management van de huurder 19

2.4.1 Klanttevredenheid 17

2.4.2 De mate waarin de huurder in staat is aan te sturen op efficiënte zorgverlening: kwaliteit van de

sturingsinformatie

19

2.4.3 Personeelsverloop en ziekteverzuim onder personeel

18

2.4.4 Verscherpt toezicht van toezichthouder in afgelopen 3 jaar

19

2.4.5 Samenstelling en zittingsduur bestuur 16

2.4.6 Aanpassingsvermogen huurder (o.a. flexibiliteit in de personeelskosten)

14

2.4.7 De verhouding tussen inkomsten van de huurder en de kosten van de huisvesting van de huurder

14

2.4.8 Continuïteit van het managementteam 6

Management en visie van de huurder

2.5 Toekomstvisie van de huurder 18

2.5.1 Investeringsplannen van de huurder 18

2.5.2 Strategie van de huurder m.b.t. (de flexibiliteit van) de vastgoedportefeuille (bijv. veel of weinig lange

huurcontracten)

18

2.5.3 Portefeuille aan verschillende soorten zorgverlening 17

2.5.4 Visie op zorg: aantrekkelijk en onderscheidend zorg concept

16

2.6 Concurrentie van andere zorgverleners 14

2.6.1 Opkomst particuliere zorgverleners 14

2.6.2 De concurrentiekracht van de huurder ten opzichte van andere zorgverleners

12

2.6.3 Kracht van het netwerk van huurder om cliënten aan te trekken

5

2.7 Type contract (standaard ROZ-contract of contract met zaken als koopoptie, dalende huren, financial

lease, triple net enz.)

2

Risk in Healthcare Real Estate Investment xvi

Risk in Healthcare Real Estate Investment xvii

Risk in Healthcare Real Estate Investment

More insight into the risk from the perspective of investors

Healthcare real estate is an emerging investment category in The Netherlands. It is

appreciated as a real estate category for its stable cash flows, high returns and strong

demographic drivers. Despite the growing interest in healthcare real estate the healthcare

real estate market is still immature. Because of the uncertainty surrounding the risk of

healthcare real estate investment many investors are still reluctant to step into this market.

There is a growing need to map out the risks involved with investing in healthcare real

estate.

By ing. Tjeerd Kosse

isk in real estate investing has

been subject of many quantitative

studies. Recent examples are

studies in which multifactor models are

being used such as those by Dale, Wolf &

Yang (2015) en Ho & Addae-Dapaah

(2015). Moreover, there were many studies

on the determinants of the cap rate,

amongst others by Sivitanidou &

Sivitanides (1999) and Wheaton et al.

(2001). There have also been studies at

micro-level on the determinants of the cap

rate. One of these studies is a study by

McDonald & Dermisi (2009). Wheaton et

al. conclude that the cap rate is strong

related to uncertainty on the measure of

risk. Because there are yet no studies on

the risk of healthcare real estate investment

there is still uncertainty on the risk. This

study offers a quantitative view into the

risk of investing in healthcare real estate.

The Current Practice

In current practice investing in healthcare

real estate is coupled with little trust in the

development of the exit value of the

property. Because investors have low

expectations on the exit value they try to

mitigate the property related risks by

signing long-term rental contracts. In this

way they shift the risk of a low exit value

to risks related to the stability of the tenant.

Tenants are, however, not always willing

to sign long-term rental contracts which

has caused some disappointment amongst

investors in the speed and ease of investing

in healthcare real estate. Healthcare real

estate is knowledge intensive and investors

need to take into account both property as

tenant related risks. The results of this

study show which risks to take into

account.

R

Risk in Healthcare Real Estate Investment xviii

Method

This study is based on a literature review

and 22 interviews with experts on

investing in healthcare real estate. Among

the experts were 11 representatives of

(non-profit) real estate investment

companies, 7 consultants and 4 other

experts. On the basis of the literature a list

of risk factors was composed. Interviewees

completed this list with additional risk

factors and rated the risk factors on

importance on a 7-point scale from 1 (not

at all important) to 7 (extremely

important).

Results

The results show that in healthcare real

estate investment both property and tenant

related risk factors play a role. Appendix 1

shows a comparison of the risk factors

obtained from a synthesis of the risk

factors found in a literature review with the

final list of risk factors found in this study.

The comparison shows that many risk

factors were not mentioned in the

literature. Especially risk factors related to

the reliability of the tenant are missing in

the existing literature.

The main risk factors related to property

are:

1.1 Maturity of the Asset Market;

1.2 Technical and Functional State of

the Property;

1.3 The Physical Location;

1.4 Local Space Market Changes and;

1.5 Alternative Use.

The tenant related risk factors are at main

level:

2.1 The Ratio between Income

Generated by the Tenant in the Property

and the Rent of the Property (Coverage

Ratio);

2.2 Influence of the Government on the

Stability of the Tenant;

2.3 Creditworthiness of the Tenant;

2.4 Quality of the Management of the

Tenant;

2.5 Vision of the Tenant;

2.6 Competition by Other Healthcare

Organizations and;

2.7 Type of Contract.

The importance of these risk factors are

shown in figure 1. In this figure the

average rating is set out against the

standard deviation. Figure 1 shows that

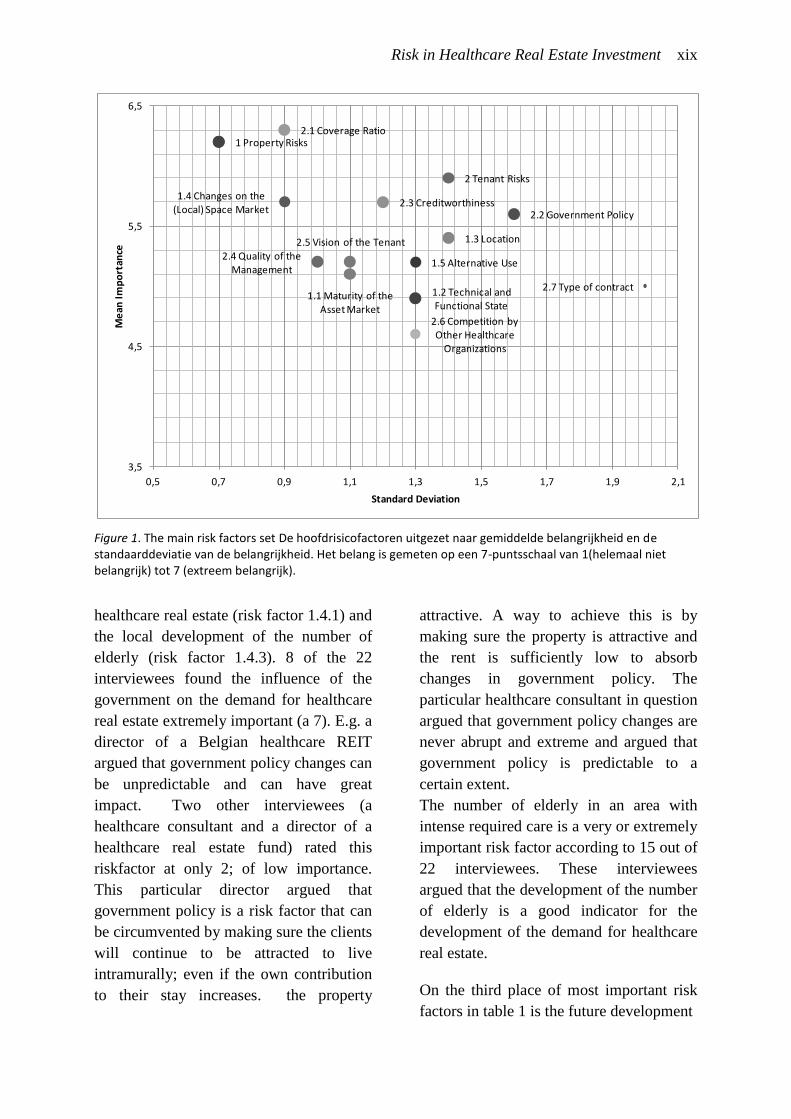

interviewees agreed that property related

risks (risk factor 1) are very important

while there is less consensus over the

importance of tenant related risks (risk

factor 2). It is noticeable that the coverage

ratio (risk factor 2.1) was found most

important on average. A director of a

Belgian healthcare REIT explained why he

gave a high rating to this risk factor. By

adjusting the rent level to the income of the

tenant a large part of the tenant risk can be

reduced. He added that the income of

healthcare organizations is strongly

dependent on government regulation so

that most healthcare organizations generate

roughly the same maximum income. For

this reasons most interviewees found this

risk factor very important.

A list of the 10 most important risk factors

at main level and sub level is shown in

table 1.

Table 1 shows that two sub-risk factors

related to the space market (risk factor 1.4)

are in the top 1 of highest rated risk

factors. These two risks are the influence

of the government on the demand for

Risk in Healthcare Real Estate Investment xix

Figure 1. The main risk factors set De hoofdrisicofactoren uitgezet naar gemiddelde belangrijkheid en de standaarddeviatie van de belangrijkheid. Het belang is gemeten op een 7-puntsschaal van 1(helemaal niet belangrijk) tot 7 (extreem belangrijk).

healthcare real estate (risk factor 1.4.1) and

the local development of the number of

elderly (risk factor 1.4.3). 8 of the 22

interviewees found the influence of the

government on the demand for healthcare

real estate extremely important (a 7). E.g. a

director of a Belgian healthcare REIT

argued that government policy changes can

be unpredictable and can have great

impact. Two other interviewees (a

healthcare consultant and a director of a

healthcare real estate fund) rated this

riskfactor at only 2; of low importance.

This particular director argued that

government policy is a risk factor that can

be circumvented by making sure the clients

will continue to be attracted to live

intramurally; even if the own contribution

to their stay increases. the property

attractive. A way to achieve this is by

making sure the property is attractive and

the rent is sufficiently low to absorb

changes in government policy. The

particular healthcare consultant in question

argued that government policy changes are

never abrupt and extreme and argued that

government policy is predictable to a

certain extent.

The number of elderly in an area with

intense required care is a very or extremely

important risk factor according to 15 out of

22 interviewees. These interviewees

argued that the development of the number

of elderly is a good indicator for the

development of the demand for healthcare

real estate.

On the third place of most important risk

factors in table 1 is the future development

1 Property Risks

1.1 Maturity of the Asset Market

1.2 Technical and Functional State

1.3 Location

1.4 Changes on the (Local) Space Market

1.5 Alternative Use

2 Tenant Risks

2.1 Coverage Ratio

2.2 Government Policy 2.3 Creditworthiness

2.4 Quality of the Management

2.5 Vision of the Tenant

2.6 Competition by Other Healthcare

Organizations

2.7 Type of contract

3,5

4,5

5,5

6,5

0,5 0,7 0,9 1,1 1,3 1,5 1,7 1,9 2,1

Me

an I

mp

ort

ance

Standard Deviation

Risk in Healthcare Real Estate Investment xx

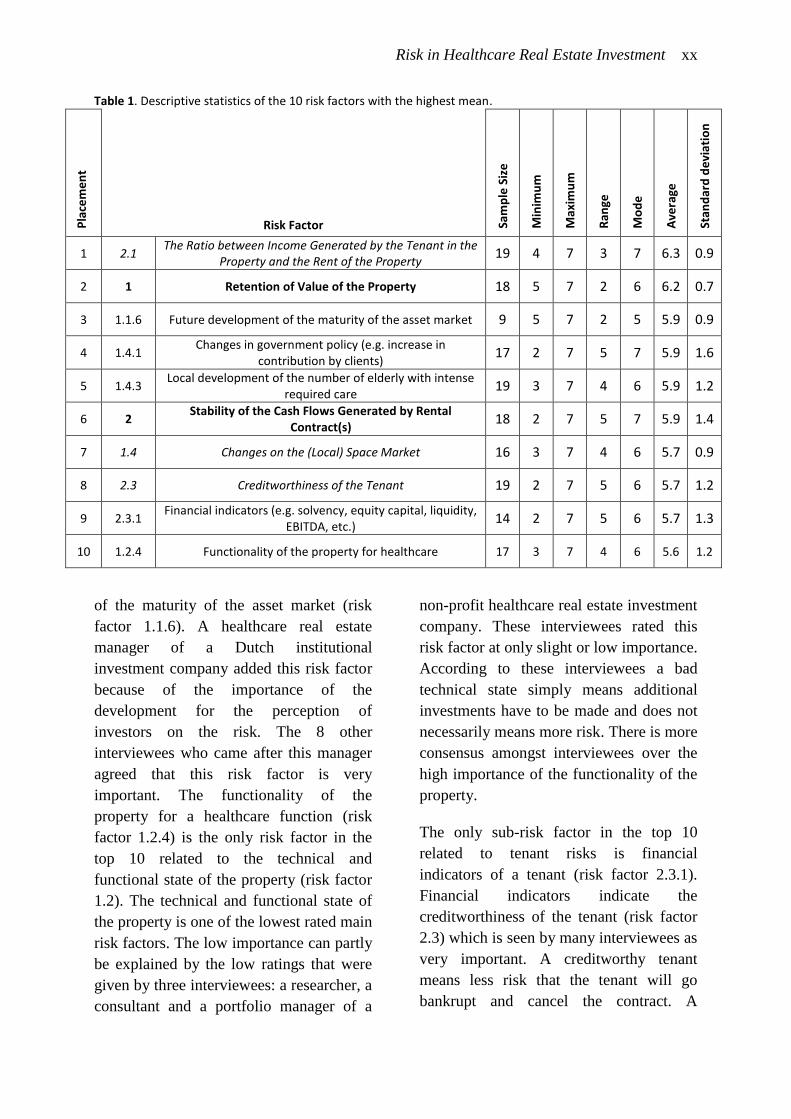

Table 1. Descriptive statistics of the 10 risk factors with the highest mean.

Pla

cem

en

t

Risk Factor

Sam

ple

Siz

e

Min

imu

m

Max

imu

m

Ran

ge

Mo

de

Ave

rage

Stan

dar

d d

evi

atio

n

1 2.1 The Ratio between Income Generated by the Tenant in the

Property and the Rent of the Property 19 4 7 3 7 6.3 0.9

2 1 Retention of Value of the Property 18 5 7 2 6 6.2 0.7

3 1.1.6 Future development of the maturity of the asset market 9 5 7 2 5 5.9 0.9

4 1.4.1 Changes in government policy (e.g. increase in

contribution by clients) 17 2 7 5 7 5.9 1.6

5 1.4.3 Local development of the number of elderly with intense

required care 19 3 7 4 6 5.9 1.2

6 2 Stability of the Cash Flows Generated by Rental

Contract(s) 18 2 7 5 7 5.9 1.4

7 1.4 Changes on the (Local) Space Market 16 3 7 4 6 5.7 0.9

8 2.3 Creditworthiness of the Tenant 19 2 7 5 6 5.7 1.2

9 2.3.1 Financial indicators (e.g. solvency, equity capital, liquidity,

EBITDA, etc.) 14 2 7 5 6 5.7 1.3

10 1.2.4 Functionality of the property for healthcare 17 3 7 4 6 5.6 1.2

of the maturity of the asset market (risk

factor 1.1.6). A healthcare real estate

manager of a Dutch institutional

investment company added this risk factor

because of the importance of the

development for the perception of

investors on the risk. The 8 other

interviewees who came after this manager

agreed that this risk factor is very

important. The functionality of the

property for a healthcare function (risk

factor 1.2.4) is the only risk factor in the

top 10 related to the technical and

functional state of the property (risk factor

1.2). The technical and functional state of

the property is one of the lowest rated main

risk factors. The low importance can partly

be explained by the low ratings that were

given by three interviewees: a researcher, a

consultant and a portfolio manager of a

non-profit healthcare real estate investment

company. These interviewees rated this

risk factor at only slight or low importance.

According to these interviewees a bad

technical state simply means additional

investments have to be made and does not

necessarily means more risk. There is more

consensus amongst interviewees over the

high importance of the functionality of the

property.

The only sub-risk factor in the top 10

related to tenant risks is financial

indicators of a tenant (risk factor 2.3.1).

Financial indicators indicate the

creditworthiness of the tenant (risk factor

2.3) which is seen by many interviewees as

very important. A creditworthy tenant

means less risk that the tenant will go

bankrupt and cancel the contract. A

Risk in Healthcare Real Estate Investment xxi

healthcare real estate consultant warned

that, although taking into account the

creditworthiness of the tenant is an

excellent way to mitigate contract risk, the

creditworthiness of a tenant can decline

rapidly if the healthcare organization has

bad management or a bad vision.

Different Points of View

During the interviewees it became evident

that there are two different points of view

on healthcare real estate investment. Some

investors have a tendency to manage risk

by focusing on the risk of an instable

tenant. Other investors try to reduce risk by

investing solely in properties with a low

chance of depreciation, even if the tenant

would go bankrupt. The first perspective

has similarities with corporate investment

while the second perspective is typical for

real estate investors.

Influence of the Length of Contracts

The most usual length of rental contracts is

15 years. When using short contracts of 10

years property related risk become more

important while tenant risks are more

important when using rental contracts

longer than 20 years. Markets with shorter

rental contracts are more suitable for

investors who focus on property related

risks factors while markets with longer

rental contracts are more suitable for

investors who focus on tenant risks.

Because healthcare organizations are not

always willing to sign long-term contracts

a shift can take place in which investors

are forced to focus more on property risks

instead of tenant risks.

Uncertainty over the Risk

The results show that there is still

uncertainty over the level of risk in

healthcare real estate investment. The risk

factors have a large standard deviation

between 0.7 and 2.0. This suggests that

opinions differ on the importance of the

risk factors. The average rating of 4.9

shows that the risk factors were rated

asymmetrically. A possible explanation is

that interviewees rated risk factors of

higher importance when in doubt.

Conclusions

The findings of this study are of added

value to the existing literature in a number

of ways. This study shows that, besides

macro-economic risk factors, there are

numerous risk factors at micro level that

influence the risk perception of investors.

It shows that there are differences in the

risk perception of investors and that there

are different ways to approach healthcare

real estate investment. Moreover, it

uncovers the uncertainties there are

surrounding healthcare real estate

investment and shows that uncertainty

places a role in risk perception in

healthcare real estate investment.

The results give investors, appraisers and

researchers input for a better

approximation for risk. The risk factors

and their importance can be used in the

investment decision process and to

appraise healthcare properties better. By

mapping out the risk factors and their

importance this study contributes to the

transparency and maturity of the healthcare

real estate market.

Discussion

This study has a couple of limitations. The

research method can be called into

question because it has resulted in too

many risk factors. A selection of the risk

factors can be used in follow up studies to

examine risk in healthcare real estate

Risk in Healthcare Real Estate Investment xxii

investment more closely. Despite these

limitations the study has contributed to the

knowledge on the risk of investing in

healthcare real estate. This study is the first

qualitative study on Dutch healthcare real

estate focusing solely on the risks. It offers

investors new knowledge they can

implement in their investment decision

process and gives insight in the different

points of view amongst investors.

Sources

Dale, D., Wolf, R., & Yang, H.F. (2015).

An assessment of the risk and return of

residential real estate. Managerial

Finance, 41(6), 591 - 599.

Ho, D.K.H., & Addae-Dapaah, K. (2015).

International Direct Real Estate Risk

Premiums in a Multi-Factor Estimation

Model. Journal of Real Estate Financial

Economics, 52–85.

McDonald, J.F., & & Dermisi, S. (2009).

Office building capitalization rates: the

case of downtown Chicago. The Journal

of Real Estate Finance and Economics,

39(4), 472-485.

Sivitanidou, R.C., & Sivitanides, P.S.

(1999). Office Capitalization Rates: Real

Estate and Capital Market Influences.

Journal of Real Estate Finance and

Economics, (18)3, 297-322.

Wheaton, W.C., Torto, R.G., Sivitanides,

P.S., Southard, J.A., Hopkins, R.E., &

Costello, J.M. (2001). Real estate risk: a

forward-looking approach. Real Estate

Finance, 18(3), 20-28.

Risk in Healthcare Real Estate Investment xxiii

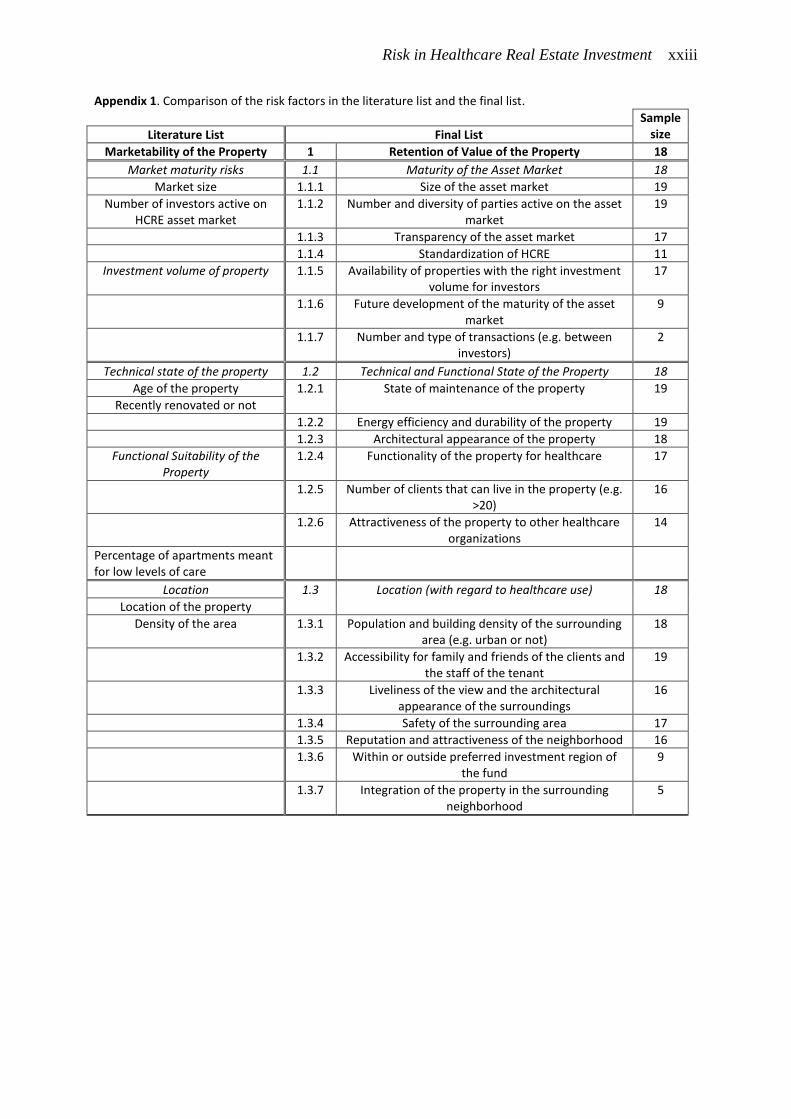

Appendix 1. Comparison of the risk factors in the literature list and the final list.

Sample size Literature List Final List

Marketability of the Property 1 Retention of Value of the Property 18

Market maturity risks 1.1 Maturity of the Asset Market 18

Market size 1.1.1 Size of the asset market 19

Number of investors active on HCRE asset market

1.1.2 Number and diversity of parties active on the asset market

19

1.1.3 Transparency of the asset market 17

1.1.4 Standardization of HCRE 11

Investment volume of property 1.1.5 Availability of properties with the right investment volume for investors

17

1.1.6 Future development of the maturity of the asset market

9

1.1.7 Number and type of transactions (e.g. between investors)

2

Technical state of the property 1.2 Technical and Functional State of the Property 18

Age of the property 1.2.1 State of maintenance of the property 19

Recently renovated or not

1.2.2 Energy efficiency and durability of the property 19

1.2.3 Architectural appearance of the property 18

Functional Suitability of the Property

1.2.4 Functionality of the property for healthcare 17

1.2.5 Number of clients that can live in the property (e.g. >20)

16

1.2.6 Attractiveness of the property to other healthcare organizations

14

Percentage of apartments meant for low levels of care

Location 1.3 Location (with regard to healthcare use) 18

Location of the property

Density of the area 1.3.1 Population and building density of the surrounding area (e.g. urban or not)

18

1.3.2 Accessibility for family and friends of the clients and the staff of the tenant

19

1.3.3 Liveliness of the view and the architectural appearance of the surroundings

16

1.3.4 Safety of the surrounding area 17

1.3.5 Reputation and attractiveness of the neighborhood 16

1.3.6 Within or outside preferred investment region of the fund

9

1.3.7 Integration of the property in the surrounding neighborhood

5

Risk in Healthcare Real Estate Investment xxiv

Appendix 1 (continued). Comparison of the risk factors in the literature list and the final list.

Space market changes 1.4 Changes on the (Local) Space Market 16

1.4.1 Changes in government policy (e.g. increase in contribution by clients)

17

1.4.2 Medical developments that can influence the demand for HCRE space

16

Number of elderly with severe somatic and psycho-geriatric

conditions

1.4.3 Local development of the number of elderly with intense required care

19

1.4.4 Delay in the moment of moving out from their own house by future clients

6

1.4.5 Demand of other healthcare organizations on the space market (maturity of the space market)

17

1.4.6 Qualitative change in demand for space by clients 17

1.4.7 The length of the waiting lists 19

Rent levels 1.4.8 Rent levels of competing space 17

Supply of new space 1.4.9 Competing (new) supply of space in the vicinity 19

Vacancy rate 1.4.10 Vacancy rates of competing HCRE 19

Level of absorption of space

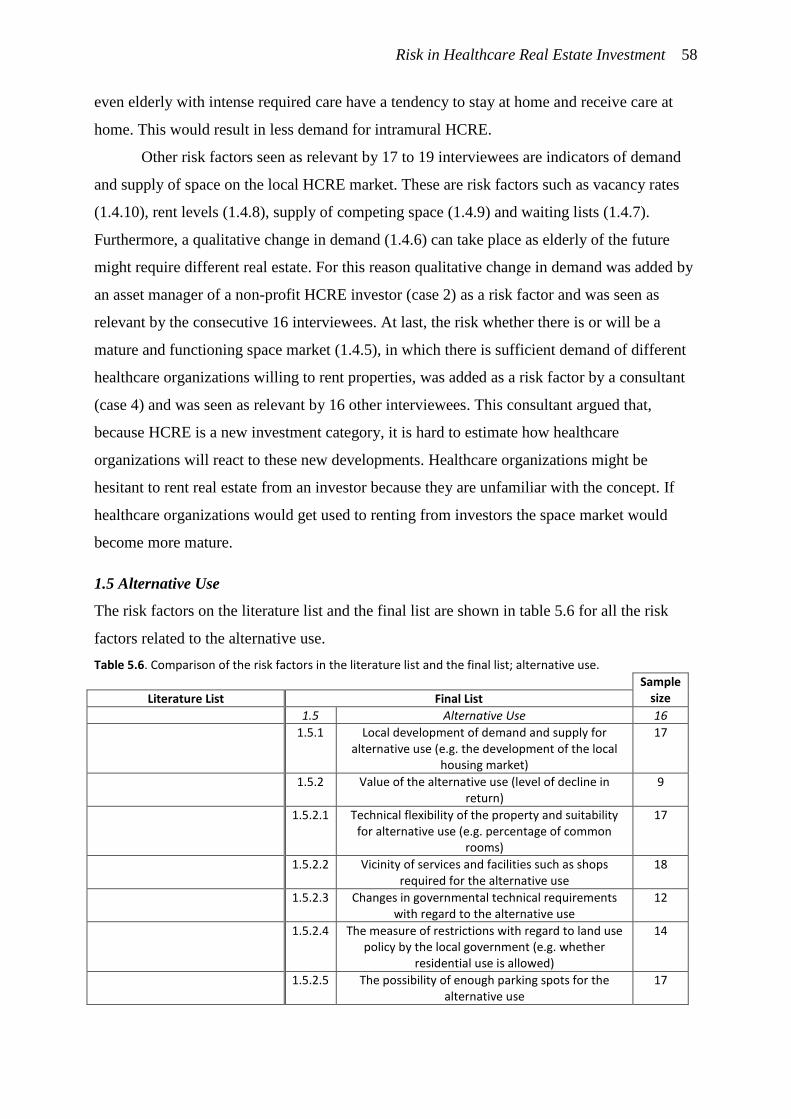

1.5 Alternative Use 16

1.5.1 Local development of demand and supply for alternative use (e.g. the development of the local

housing market)

17

1.5.2 Value of the alternative use (level of decline in return)

9

1.5.2.1 Technical flexibility of the property and suitability for alternative use (e.g. percentage of common

rooms)

17

1.5.2.2 Vicinity of services and facilities such as shops required for the alternative use

18

1.5.2.3 Changes in governmental technical requirements with regard to the alternative use

12

1.5.2.4 The measure of restrictions with regard to land use policy by the local government (e.g. whether

residential use is allowed)

14

1.5.2.5 The possibility of enough parking spots for the alternative use

17

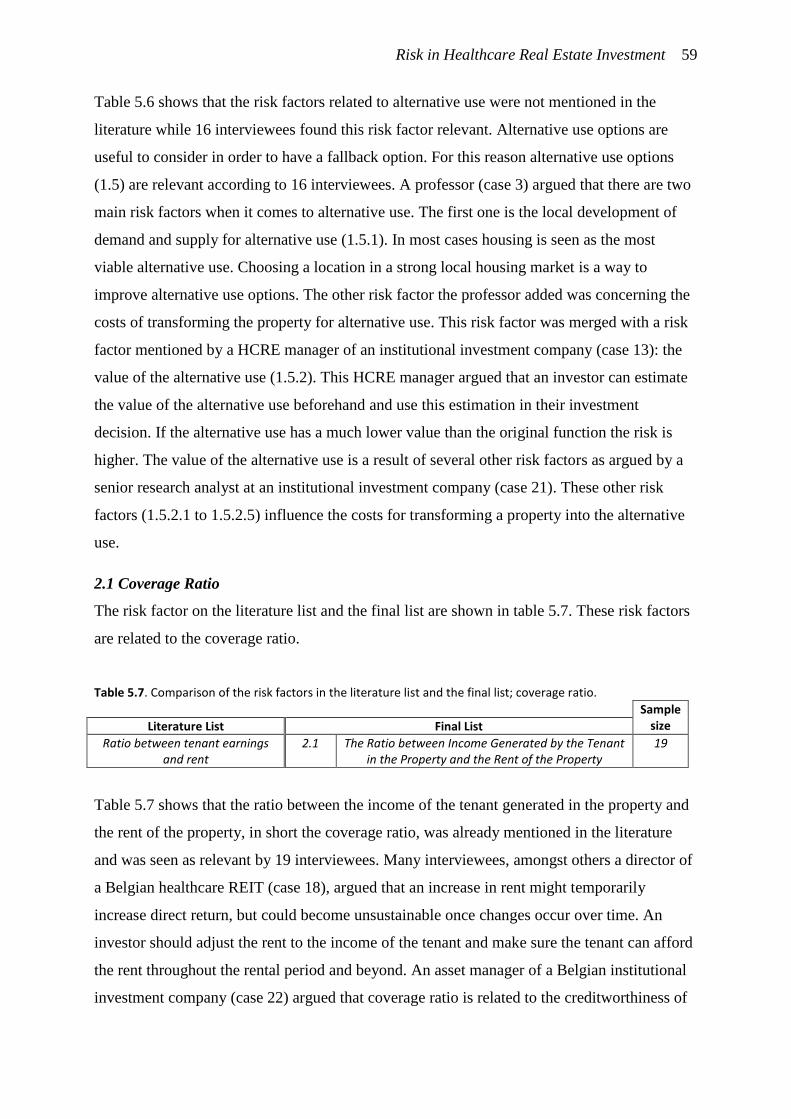

Reliability of the Tenant 2 Stability of the Cash Flows Generated by Rental Contract(s)

18

Ratio between tenant earnings and rent

2.1 The Ratio between Income Generated by the Tenant in the Property and the Rent of the Property

19

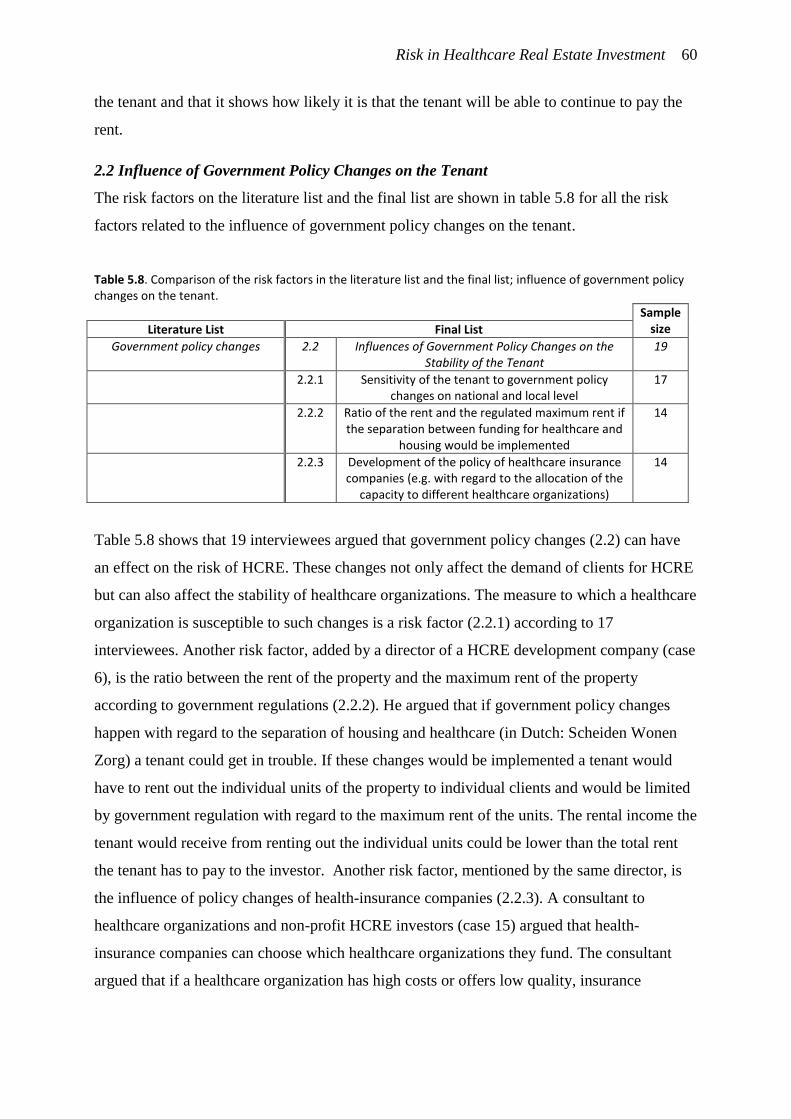

Government policy changes 2.2 Influences of Government Policy Changes on the Stability of the Tenant

19

2.2.1 Sensitivity of the tenant to government policy changes on national and local level

17

2.2.2 Ratio of the rent and the regulated maximum rent if the separation between funding for healthcare and

housing would be implemented

14

2.2.3 Development of the policy of healthcare insurance companies (e.g. with regard to the allocation of the

capacity to different healthcare organizations)

14

Risk in Healthcare Real Estate Investment xxv

Appendix 1 (continued). Comparison of the risk factors in the literature list and the final list.

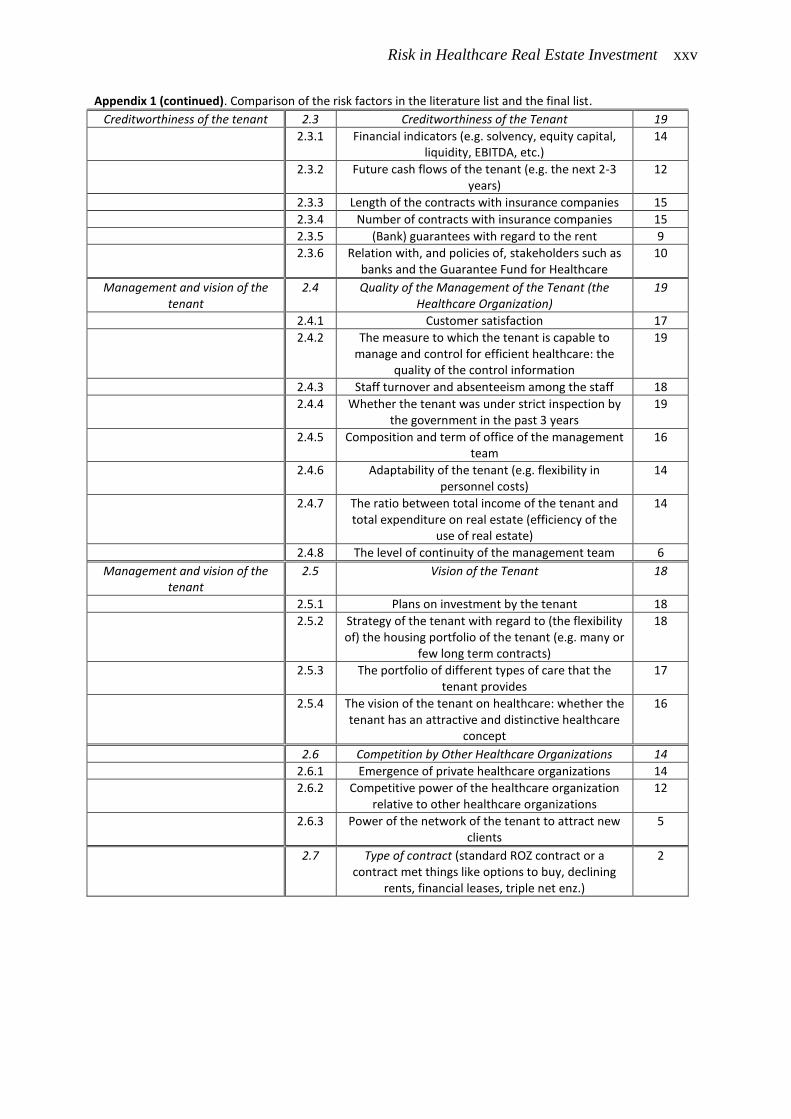

Creditworthiness of the tenant 2.3 Creditworthiness of the Tenant 19

2.3.1 Financial indicators (e.g. solvency, equity capital, liquidity, EBITDA, etc.)

14

2.3.2 Future cash flows of the tenant (e.g. the next 2-3 years)

12

2.3.3 Length of the contracts with insurance companies 15

2.3.4 Number of contracts with insurance companies 15

2.3.5 (Bank) guarantees with regard to the rent 9

2.3.6 Relation with, and policies of, stakeholders such as banks and the Guarantee Fund for Healthcare

10

Management and vision of the tenant

2.4 Quality of the Management of the Tenant (the Healthcare Organization)

19

2.4.1 Customer satisfaction 17

2.4.2 The measure to which the tenant is capable to manage and control for efficient healthcare: the

quality of the control information

19

2.4.3 Staff turnover and absenteeism among the staff 18

2.4.4 Whether the tenant was under strict inspection by the government in the past 3 years

19

2.4.5 Composition and term of office of the management team

16

2.4.6 Adaptability of the tenant (e.g. flexibility in personnel costs)

14

2.4.7 The ratio between total income of the tenant and total expenditure on real estate (efficiency of the

use of real estate)

14

2.4.8 The level of continuity of the management team 6

Management and vision of the tenant

2.5 Vision of the Tenant 18

2.5.1 Plans on investment by the tenant 18

2.5.2 Strategy of the tenant with regard to (the flexibility of) the housing portfolio of the tenant (e.g. many or

few long term contracts)

18

2.5.3 The portfolio of different types of care that the tenant provides

17

2.5.4 The vision of the tenant on healthcare: whether the tenant has an attractive and distinctive healthcare

concept

16

2.6 Competition by Other Healthcare Organizations 14

2.6.1 Emergence of private healthcare organizations 14

2.6.2 Competitive power of the healthcare organization relative to other healthcare organizations

12

2.6.3 Power of the network of the tenant to attract new clients

5

2.7 Type of contract (standard ROZ contract or a contract met things like options to buy, declining

rents, financial leases, triple net enz.)

2

Risk in Healthcare Real Estate Investment xxvi

Risk in Healthcare Real Estate Investment xxvii

Preface

This report is the final product of my graduation thesis which serves to complete my master

Real Estate Management & Development at Eindhoven University of Technology. My

interest in real estate investment led me to the topic of healthcare real estate. Healthcare real

estate offers investors a new and growing real estate asset market, but investing in healthcare

real estate requires that investors gain new knowledge. With this study I hope to have

expanded on the currently underdeveloped knowledge on healthcare real estate investment.

I would like to thank several people for their involvement in this project. I would like

to thank Finance Ideas for offering me the opportunity to graduate on this interesting subject.

Furthermore, I would like to thank all the interviewees for sharing their knowledge so

enthusiastically. Your contribution has resulted in a deeper understanding of the healthcare

real estate market and the risks and uncertainties investors face. Thanks to your contribution

knowledge on healthcare real estate is greatly expanded and will result in a reduction in the

sense of uncertainty surrounding this new asset class.

I am grateful for my academic supervisors Stephan Maussen and Pauline van den

Berg, who gave excellent academic support and asked critical questions at the right moments.

I thank my company supervisor Pim Diepstraten for his practical input and support throughout

the entire process. Furthermore, I would like to thank Piet Eichholz for his support at decisive

moments, which has helped tremendously.

Last but not least, I would like to thank my family, friends and colleagues for their

support. You offered the conditions that made this study possible.

Tjeerd Kosse

Utrecht, February 2016

Risk in Healthcare Real Estate Investment xxviii

Risk in Healthcare Real Estate Investment 1

RISK IN HEALTHCARE REAL ESTATE INVESTMENT

1. Research Context

1.1. Introduction

The healthcare industry in The Netherlands has undergone big changes in recent years (Van

Ewijk, Van der Horst, & Besseling, 2013; Van der Wielen, 2014). These changes were mostly

caused by government policy changes in order to cut back the constant and alarming growth

of healthcare costs (Dantuma & Winkel, 2015; Van Ewijk et al., 2013; Ministerie van VWS,

2014; Van der Wielen, 2014). One of the ways to cut back costs was to change the way of

funding of healthcare real estate (HCRE) and to switch to performance oriented funding (Van

der Schaar, 2002; Nederlandse Zorgautoriteit, 2009; Nederlandse Zorgautoriteit, 2011). The

system of ex-post reimbursement is gradually changed to a performance oriented system

(Nederlandse Zorgautoriteit, 2011). In the performance oriented system funding will take

place entirely based on the number and type of clients the healthcare organizations receive

(Nederlandse Zorgautoriteit, 2011).

Because of this change it is evident that healthcare organizations have to adapt

themselves to the changing policies by making sure their real estate costs are covered based

on their performance. No longer is it financially viable to have high vacancy rates because

performance fees only cover the costs of most HCRE at an occupancy rate of 97%

(Nederlandse Zorgautoriteit, 2009). The policy changes have made healthcare organizations

responsible for the costs of real estate.

Because healthcare organizations are now funded based on their performance, lending

to an healthcare organization has become more risky (Van der Wielen, 2014; De Baaij, 2014,

2015; Postema, 2015). Banks have become more hesitant in providing funding for healthcare

organizations and set more strict terms on their loans to healthcare organizations (Van der

Wielen, 2014; Hermus, 2014; Postema, 2015). Housing associations are also retreating from

the HCRE asset market in order to focus on providing social housing (Van der Gijp, 2014;

Hermus, 2014, 2015; De Baaij, 2015) because government policy now encourages non-profit

housing associations to focus on their core purpose, which is to provide social housing

(Hermus, 2015; Scheijgrond, Anker, & Besier, 2015). This new situation has created the

incentive for healthcare organizations to search for alternative ways of financing their

Risk in Healthcare Real Estate Investment 2

operations and real estate (Van der Wielen, 2014; De Baaij, 2014; Hermus, 2014; Postema,

2015). One of these ways is by partnering up with real estate investors to rent (parts of) their

real estate instead of owning it (Hermus, 2014; 2015).

In foreign countries such as Belgium, the United Kingdom and the United States

investors have been investing in HCRE for several years (Van Elp & Konings, 2015; Berden

& Van de Velde, 2015; Hermus, 2015). Based on the positive experiences abroad, are

considering investing in Dutch HCRE (DTZ Zadelhoff, 2014; Schellens & De Bruijn, 2014).

HCRE is associated with diversification benefits, a hedge against an aging population, long

rental agreements, steady cash flows, growth perspectives, high availability of properties and

low risk with high returns (DTZ Zadelhoff, 2014; Van der Gijp, 2014; Van Elp & Konings,

2015; Hermus, 2014). Based on the prospect of adding a new asset class to their portfolio with

all these benefits, investors show clear signs of willingness to invest in HCRE (Berden & Van

de Velde, 2015; Hermus, 2014; Van Schie, 2014). Berden & Van de Velde (2015) argue that

HCRE is at the beginning of a boom which will lead to a mature and proper functioning asset

market. Van Elp & Konings (2015) estimate that the total volume of HCRE is 52 million

square meter (comparable to the size of the Dutch office market) and that it grows by roughly

0,8 million square meter per year. According to Van Elp & Konings the HCRE asset market

will be larger than the retail asset market by 2030. These findings are confirmed by DTZ

Zadelhoff (2014) who estimate that the amount of investment will have increased to € 825

million by 2017. This would mean a sevenfold increase in four years time (DTZ Zadelhoff,

2014). Because of this growth, DTZ Zadelhoff expects that by 2017 the demand will surpass

the supply of HCRE. However, in reality investors have not yet substantively invested in

HCRE (Schellens & De Bruijn, 2014). Investors are still unsure about the risks of investing in

HCRE. When they do wish to invest they often offer a lower price or require a higher return

than healthcare organizations are willing to accept (Van Schie, 2014; De Baaij, 2015). This is

caused by the phenomenon that as uncertainty over the risk of investing in real estate

increases the required cap rates increase (Wheaton et al., 2001). This leads to the following

problem statement.

Healthcare organizations are looking for alternative ways to finance their real estate.

Dutch real estate investors, on the other hand, show willingness to invest in HCRE but

hesitate because of uncertainty on the risk of investing in HCRE. HCRE is at the beginning

stage of becoming a new and substantial asset class on the Dutch real estate asset market

(Berden & Van de Velde, 2015; Van Elp & Konings, 2015). But the investment volume in

HCRE is still at a low level because investors are unsure of the risks and require a higher

Risk in Healthcare Real Estate Investment 3

return than healthcare organizations are willing to accept (Van Schie, 2014; De Baaij, 2015).

Wheaton et al. (2001) present support that as uncertainty over the risk of investing in real

estate increases the required cap rates increase. This phenomenon can be seen on the Dutch

HCRE market, where high risk premiums are required because of uncertainty on the risk of

investing in HCRE (Van Schie, 2014; De Baaij, 2015). To stimulate more investment more

knowledge is required on the risk of investing in HCRE to take away some of the uncertainty.

The supposition of this study is that by offering more clarity on the risks investors will

become less hesitant about investing in HCRE. In short the problem statement is:

There is a lack of knowledge on the level of risk of investing in HCRE properties.

1.2. Research Objective and Questions

The preceding introduction has shown a knowledge gap in the practice of HCRE investment.

In order to connect demand and supply on the HCRE property market new knowledge is

required on the risk of HCRE. This has resulted in the following research objective and

research questions.

1.2.1. Research Objective

The main objective of this thesis is to investigate the risks of investing in Dutch HCRE and

the importance of these different risks to real estate investors.

1.2.2. Research Question

What are the risks of investing in Dutch HCRE and the importance of these risks to real estate

investors?

I. What is the context of the current situation on the HCRE asset market?

II. What are the risks of investing in HCRE?

III. How important is each of these risks to investors?

1.3. Scope

The scope of this study is limited to only one category of HCRE. There is no unequivocal

definition of HCRE, although a generally accepted definition of HCRE is "real estate related

to healthcare". Because this definition is rather vague, more specific definitions have been

developed. The definition of HCRE used in this thesis is based on the broad definition used by

Van der Gijp (2014) and Van Elp & Konings (2015):

HCRE is real estate in which healthcare services are being provided.

Risk in Healthcare Real Estate Investment 4

HCRE is in more diverse in form and appearance than housing, offices or retail. Large

hospitals, worth of hundreds of millions, and housing at which inhabitants receive healthcare

services both fall into the same category. To simply limit the scope of this study only one

category is selected: intramural elderly HCRE. Intramural elderly HCRE are facilities for

elderly with high levels of required care. The real estate comes in the form of memory care

facilities and skilled nursing care facilities, or a combination of both. Besides elderly

intramural HCRE there are the following other seven categories of HCRE: life-cycle proof

housing; care at home; intramural mental HCRE; intramural handicap HCRE; and primary,

secondary and tertiary HCRE (Van der Gijp, 2014). An overview of all eight categories of

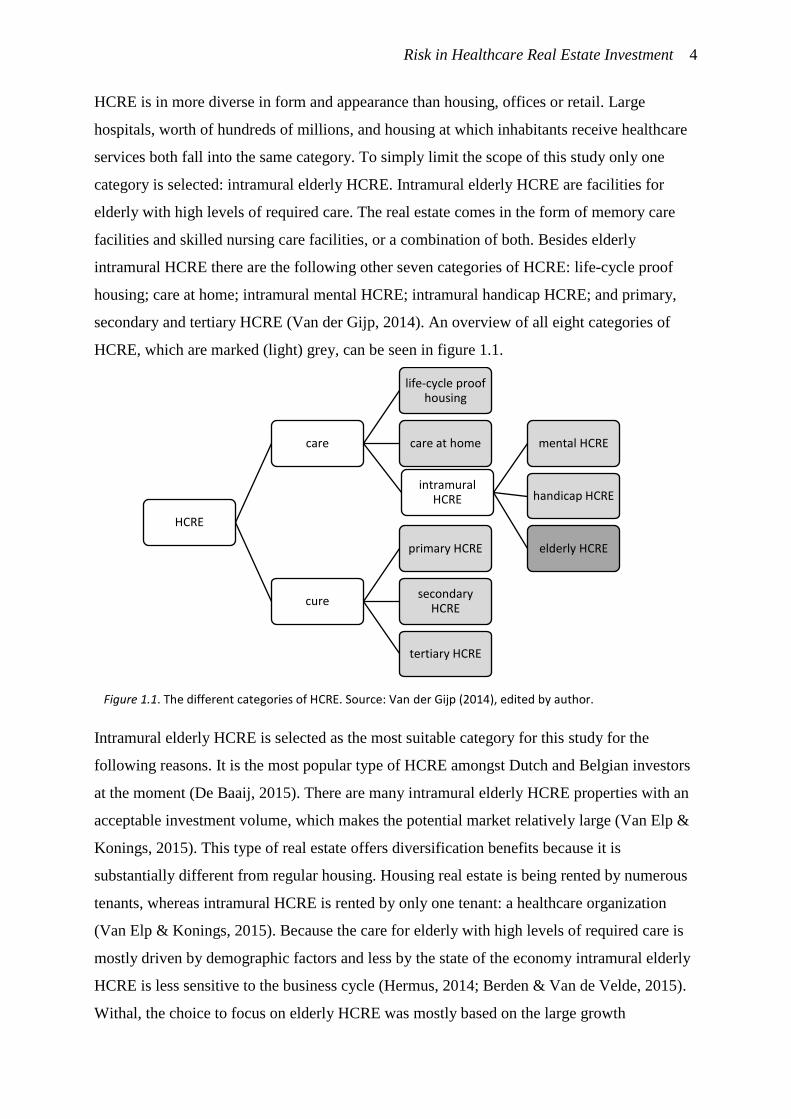

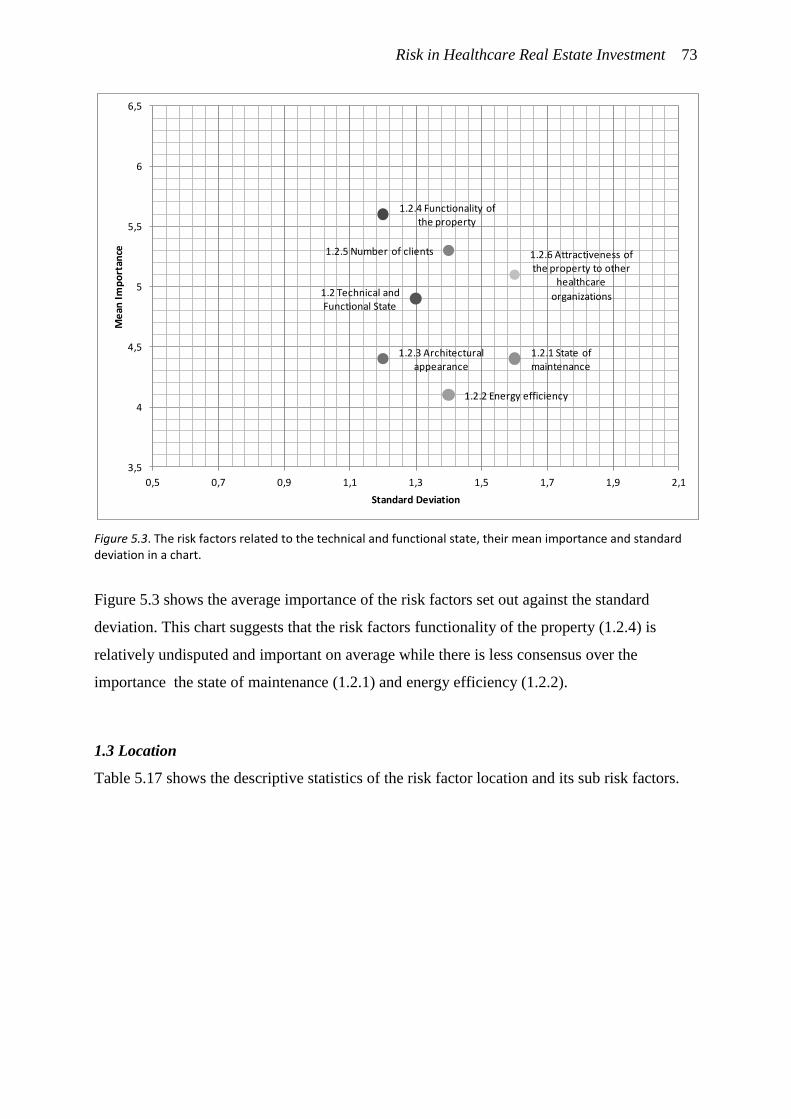

HCRE, which are marked (light) grey, can be seen in figure 1.1.

Intramural elderly HCRE is selected as the most suitable category for this study for the

following reasons. It is the most popular type of HCRE amongst Dutch and Belgian investors

at the moment (De Baaij, 2015). There are many intramural elderly HCRE properties with an

acceptable investment volume, which makes the potential market relatively large (Van Elp &

Konings, 2015). This type of real estate offers diversification benefits because it is

substantially different from regular housing. Housing real estate is being rented by numerous

tenants, whereas intramural HCRE is rented by only one tenant: a healthcare organization

(Van Elp & Konings, 2015). Because the care for elderly with high levels of required care is

mostly driven by demographic factors and less by the state of the economy intramural elderly

HCRE is less sensitive to the business cycle (Hermus, 2014; Berden & Van de Velde, 2015).

Withal, the choice to focus on elderly HCRE was mostly based on the large growth

HCRE

care

life-cycle proof housing

care at home

intramural HCRE

mental HCRE

handicap HCRE

elderly HCRE

cure

primary HCRE

secondary HCRE

tertiary HCRE

Figure 1.1. The different categories of HCRE. Source: Van der Gijp (2014), edited by author.

Risk in Healthcare Real Estate Investment 5

perspective. It is expected that the amount of people in need of elderly healthcare will grow

because the population is ageing (Van Elp & Konings, 2015; Van der Gijp, 2014). This might

seem contradictory to recent events because recent policy changes have temporarily reduced

the total number of elderly residing in intramural HCRE (Van Galen, Willems, & Poulus,

2012). Elderly with low levels of required care are no longer eligible for intramural

healthcare, which has temporarily resulted in a decrease of demand for this target group

(Regeling langdurige zorg, 2015; Van Galen, Willems, & Poulus, 2012). However, elderly

with severe somatic and psycho-geriatric health problems, who require more intense care,

continue to receive intramural healthcare (Regeling langdurige zorg, 2015; Van Galen,

Willems, & Poulus, 2012). The number of people with this high level of required care is

expected to grow substantially (Van Galen, Willems, & Poulus, 2012). This can be seen in

figure 1.2.

Figure 1.2. Development of demand for intramural elderly HCRE. The number of people with high levels of required care, categorized by type of required care. Source: Van Galen, Willems, & Poulus (2012), edited by author.

Figure 1.2 shows that the demand for memory care will continue to rise particularly rapidly.

Because of the aging population dementia will grow explosively the coming years; by over

100% by 2040 (Alzheimer Nederland, 2014). Alzheimer Nederland (2014) expects that the

number of dementia patients will peak in 2055 at 690.000 people. These numbers show that

there are strong demographic drivers for intramural elderly HCRE.

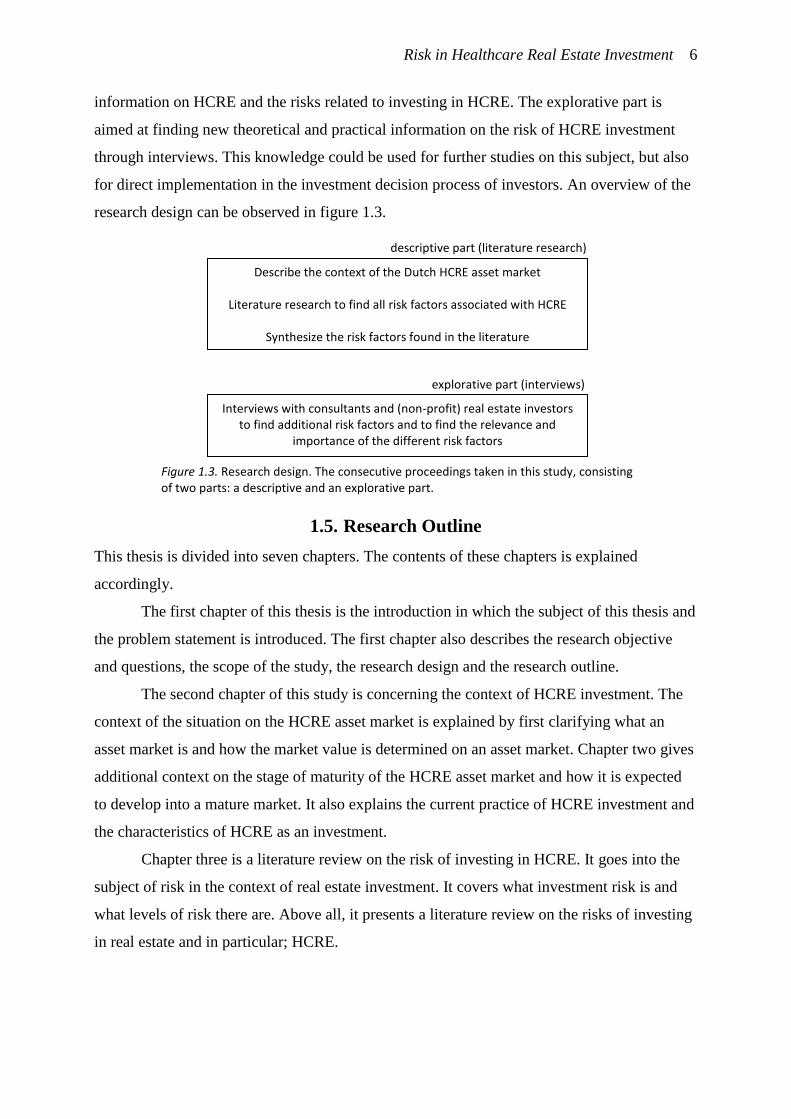

1.4. Research Design

This study is divided into two parts: a descriptive part, which consists mostly of literature

research, and an explorative part. The literature research is aimed at collecting all relevant

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Memory Care Skilled Nursing

Specific Memory Care Specific Skilled Nursing Care

Risk in Healthcare Real Estate Investment 6

information on HCRE and the risks related to investing in HCRE. The explorative part is

aimed at finding new theoretical and practical information on the risk of HCRE investment

through interviews. This knowledge could be used for further studies on this subject, but also

for direct implementation in the investment decision process of investors. An overview of the

research design can be observed in figure 1.3.

1.5. Research Outline

This thesis is divided into seven chapters. The contents of these chapters is explained

accordingly.

The first chapter of this thesis is the introduction in which the subject of this thesis and

the problem statement is introduced. The first chapter also describes the research objective

and questions, the scope of the study, the research design and the research outline.

The second chapter of this study is concerning the context of HCRE investment. The

context of the situation on the HCRE asset market is explained by first clarifying what an

asset market is and how the market value is determined on an asset market. Chapter two gives

additional context on the stage of maturity of the HCRE asset market and how it is expected

to develop into a mature market. It also explains the current practice of HCRE investment and

the characteristics of HCRE as an investment.

Chapter three is a literature review on the risk of investing in HCRE. It goes into the

subject of risk in the context of real estate investment. It covers what investment risk is and

what levels of risk there are. Above all, it presents a literature review on the risks of investing

in real estate and in particular; HCRE.

Interviews with consultants and (non-profit) real estate investors to find additional risk factors and to find the relevance and

importance of the different risk factors

Describe the context of the Dutch HCRE asset market

Literature research to find all risk factors associated with HCRE

Synthesize the risk factors found in the literature

descriptive part (literature research)

explorative part (interviews)

Figure 1.3. Research design. The consecutive proceedings taken in this study, consisting of two parts: a descriptive and an explorative part.

Risk in Healthcare Real Estate Investment 7

Chapter four explains the methodology this study and covers the way the interviews

were carried out. Furthermore, it contains information on the interviewee selection, method of

analysis and contains a description of the fieldwork.

In Chapter five the results of this study are presented.

In Chapter six the practical and theoretical implications of the results are discussed as

well as recommendations and a discussion.

Risk in Healthcare Real Estate Investment 8

Risk in Healthcare Real Estate Investment 9

2. Theoretical Background

The introduction already stated that in the current HCRE asset market there is lack of

knowledge on the risk. This chapter goes more into detail on how this leads to higher return

requirements, longer rental agreements or a lower market value. Furthermore this chapter

gives a frame of reference to the stage of maturity the HCRE property market currently is in.

Lastly, it explains current practice in HCRE investment and clarifies the characteristics of

HCRE as an investment.

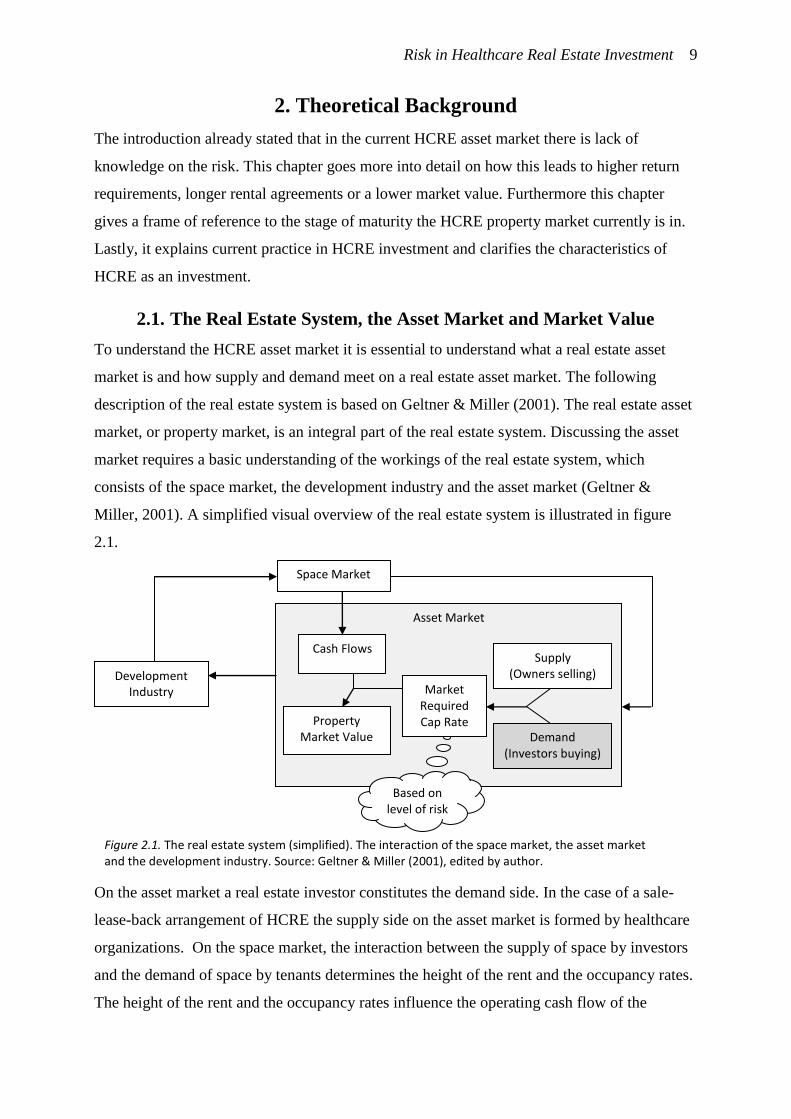

2.1. The Real Estate System, the Asset Market and Market Value

To understand the HCRE asset market it is essential to understand what a real estate asset

market is and how supply and demand meet on a real estate asset market. The following

description of the real estate system is based on Geltner & Miller (2001). The real estate asset

market, or property market, is an integral part of the real estate system. Discussing the asset

market requires a basic understanding of the workings of the real estate system, which

consists of the space market, the development industry and the asset market (Geltner &

Miller, 2001). A simplified visual overview of the real estate system is illustrated in figure

2.1.

On the asset market a real estate investor constitutes the demand side. In the case of a sale-

lease-back arrangement of HCRE the supply side on the asset market is formed by healthcare

organizations. On the space market, the interaction between the supply of space by investors

and the demand of space by tenants determines the height of the rent and the occupancy rates.

The height of the rent and the occupancy rates influence the operating cash flow of the

Asset Market

Based on level of risk

Development Industry

Space Market

Cash Flows

Property Market Value

Market Required Cap Rate

Supply (Owners selling)

Demand (Investors buying)

Figure 2.1. The real estate system (simplified). The interaction of the space market, the asset market and the development industry. Source: Geltner & Miller (2001), edited by author.

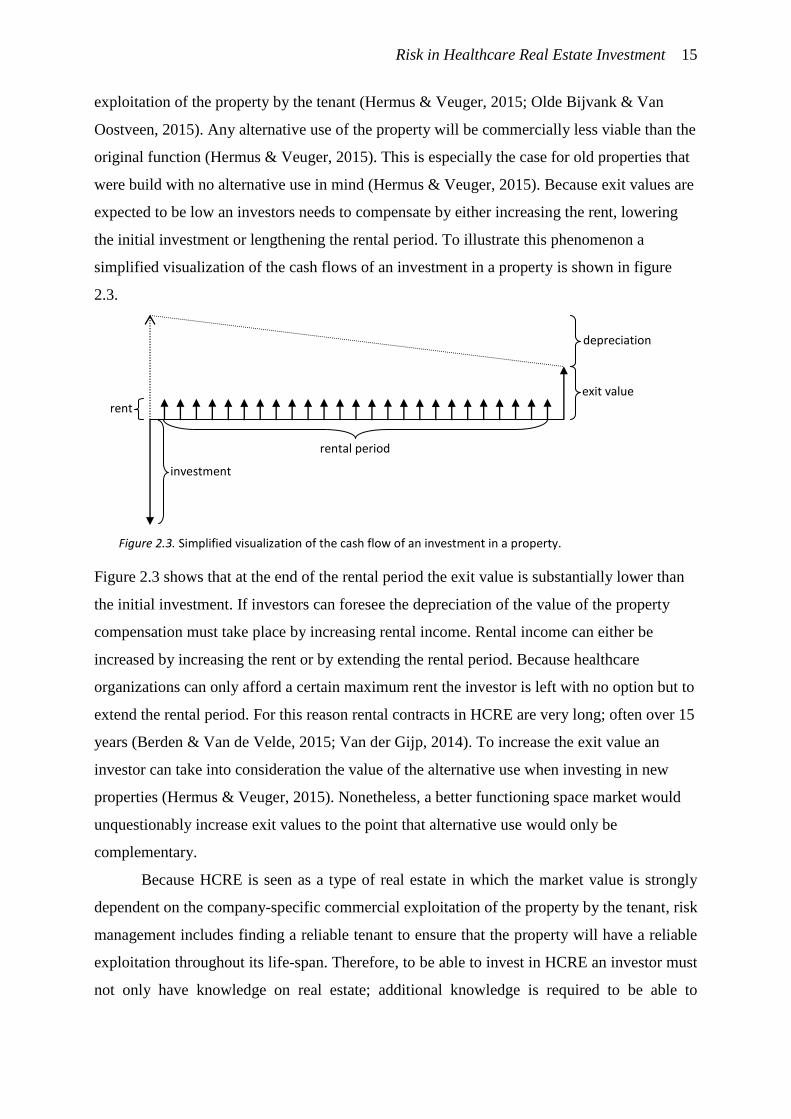

Risk in Healthcare Real Estate Investment 10

property. Since the operating cash flow is one of the elements used to determine the market

value of a property on the asset market the space market is inseparably connected to the asset

market.

In the asset market supply and demand consists of owners selling and investors

buying. The market value of the property is determined by both the cash flows of the property

and the market required cap rate. Investors ideally determine the market required cap rate

based on their perceptions on risk1.

On the HCRE asset market real estate investors are undecided on the risk of investing

in HCRE. When they do wish to invest they often require a high cap rate (Van Schie, 2014;

De Baaij, 2015). Wheaton et al. (2001) present support that as uncertainty over the risk of

investing in real estate increases the required cap rates increase. This phenomenon is

exemplified on the Dutch HCRE market, where high risk premiums are required by investors

because of a lack of consensus on the risk (Van Schie, 2014; De Baaij, 2015). Because market

required cap rates are high on the HCRE asset market the market value of the properties on

this market are low. This is due to the way cap rates influence the market value; when cash

flows remain equal and the market required cap rate rises, the market value of properties

depreciates. Because investors require a high cap rate the appraised market value is below the

acceptance levels of most healthcare organizations (Van Schie, 2014; De Baaij, 2015). Some

investors are willing to accommodate an acceptable return if the healthcare organization

agrees to sign a long-term contract. This epitomizes the predicament on the HCRE asset

market at its current stage; the beginning stage.

2.2. Stages of Maturity of an Asset Market

HCRE is at the onset of becoming a new and substantial asset class on the Dutch real estate

asset market (Van Elp & Konings, 2015; Berden & Van de Velde, 2015; Hermus, 2015). An

asset market goes through certain stages as it matures. Although these stages are gradual and

inadmissible to define, three stages are distinguished in the literature: the emerging market,

the developing market and the mature market (Keogh & D'Arcy, 1994; Chin, Dent, &