Embed Size (px)

Citation preview

Extended Essay Business & Management HL Topic: Growth Strategies What are the factors influencing the effectiveness of the “merger and acquisition” strategy pursued by the Tata group in the last 10 years? Supervisor: Mrs. Helen Andrew School Name: St. Georges British International School Rome School Code: 000817 Candidate Number: 000817-‐058 Candidate Name: Imran Uddin Exam Session: May 2012 Word Count: 3981

Imran Uddin Extended essay (Business & Management) 000817-058

2 St Georges British International School (May 2012)

Acknowledgments Special thanks to my supervisor Mrs Andrew who was always available for support and

advice regarding the essay. Moreover, the meetings were very effective and helped me think

more critically about business strategies and mainly the integration chain. Ultimately helping

me achieve the knowledge beyond the IB syllabus.

Thanks to the rich information on the Tata group website which contributed a lot for my

essay, without which understanding about such a big company would have been overly

difficult.

Lastly, the ‘The Economist’ magazines and the books in the ‘St. Georges British international

school of Rome’ library also helped me get a better picture about business (growth strategies)

from various perspectives.

Word count: 111

Imran Uddin Extended essay (Business & Management) 000817-058

3 St Georges British International School (May 2012)

Abstract The purpose of this report is to analyse the factors that have influenced the effectiveness of

the merger and acquisition (M&A) strategy pursued by the Tata group in the last 10 years.

The success of the M&A programme was measured by examining the increase in turnover of

the group and the performance in the industry sectors where acquisitions have taken place.

An examination of Ansoff’s matrix in relation to alternative growth strategies illustrated that

the choice of acquisition followed a degree of related diversification, which although

acknowledged to be risky allowed high returns if successful.

An analysis of the integration chain showed that in many cases the choice of acquisition

allowed synergies, planning and cost control, and dominance in one particular market or

industry to occur over time. Backward, forward, lateral and horizontal integrations appeared

to be the overwhelming reasons behind acquisition choices. This strategy also enabled the

group to benefit from economies of scale in certain sectors, like the hotel business.

Further benefits were associated with the geographic presence which allowed a spreading of

risk of dependency on certain economic climates, currencies and customer spending. This

approach can reduce the vulnerability of decline from different perspectives.

Lastly, visionary expertise of management enabled acquisitions to take place in advance of

‘holding industry sector’ becoming published. The ‘hot industry’ identified sectors for 2011

which had already been acquired by Tata group in the previous year. This may have

facilitated lower prices to be paid for acquired companies.

Future recommendations focussed on acquisitions involving further backwards integration,

possibly companies dealing with extraction of raw materials, for example mining and forward

integration for example dealing with retail stores for Tata’s products. In addition, there

remains further scope to consolidate the group as a global conglomerate in an increasingly

global market place.

Word count: 299

Imran Uddin Extended essay (Business & Management) 000817-058

4 St Georges British International School (May 2012)

Table of Contents Acknowledgments ........................................................................................................................... 2

Abstract ........................................................................................................................................... 3

Section 1. Introduction ............................................................................................................... 5

Section 1.1 Brief History ..................................................................................................... 5

Section 1.2 Organisational structure of a holding company ............................................... 5

Section 1.3 Industry sectors ................................................................................................ 6

Section 1.4 Evidence of success & rationale for study ....................................................... 7

Section 2. Reasons for growth ................................................................................................... 8

Section 3. Analysis of growth .................................................................................................. 10

Section 3.1 Ansoff matrix ................................................................................................. 11

Section 3.2 Integration chain ............................................................................................. 15

Section 4. Additional Benefits gained from M&As. ................................................................ 19

Section 4.1 Quick and Easy ............................................................................................... 19

Section 4.2 Gaining entry to foreign markets ................................................................... 20

Section 4.3 Gain economies of scale with monopoly position ......................................... 21

Section 5. Innovation ............................................................................................................... 21

Section 6. Globalisation of markets ......................................................................................... 21

Section 7. Visionary expertise of management ........................................................................ 22

Section 8. Defensive position .................................................................................................. 22

Section 9. Conclusion .............................................................................................................. 23

Section 10. Recommendations ................................................................................................... 24

Bibliography ................................................................................................................................. 25

Appendices .................................................................................................................................... 26

Appendix A .......................................................................................................................... 26

Appendix B .......................................................................................................................... 27

Appendix C .......................................................................................................................... 27

Appendix D .......................................................................................................................... 28

Appendix E ........................................................................................................................... 31

Imran Uddin Extended essay (Business & Management) 000817-058

5 St Georges British International School (May 2012)

Section 1. Introduction Tata group is a multinational conglomerate company which is headquartered in Bombay

House, Mumbai in India. It is currently one of the biggest companies in India and has also

diversified into many western markets, now operating in over 80 countries (Tata Group from

Wikipedia, the free encyclopedia). In addition it has interest in many diverse sectors

including communications and information technology, engineering, materials, services,

energy, consumer products and chemicals. Furthermore Tata group has expanded its business

by merging, acquiring and taking over other business. The purpose of this investigation is to

examine the factors influencing the effectiveness of the merger and acquisition strategy

pursued by the Tata group in the last 10 years.

Section 1.1 Brief History Tata Group was founded in 1868 by Jamsetji Nusserwanji Tata, when he established a trading

company dealing with cotton in Mumbai. Nusserwanji eventually started Empress Mills in

Nagpur in 1877 and consecutively founded Taj Mehal Hotel in 1903 (Tata:Our Heritage).

After the death of Nusserwanji, his eldest son Sir Dorab Tata became the chairmen of Tata

group. In charge Dorab help lead the company into steel production (1905) and hydroelectric

power generation (1910). The group expanded significantly under Jehangir Ratanji Dadabhoy

Tata and Tata Group established subsidiaries such as Tata Chemicals (1939), Tata Motors,

Tata Industries (both 1945) Voltas (1954), Tata Tea (1962), Tata Consultancy Services

(1968) and Titan Industries (1984). Ratan Tata replaced JRD Tata and is currently in charge

of Tata Group (1991- now) (Contributor). The list of Tata group’s companies introduced with

time is quoted in (Appendix A).

Section 1.2 Organisational structure of a holding company Taking a closer look at the company structure and knowing that Tata group is a multinational

conglomerate company, it is safe to say that Tata Group can be considered functioning as a

holding company. It will be common for the separate elements owned by Tata group to

remain as separate companies, where often existing management team remain in place, for

example Jaguar & Land rover do not have Indian engineers, in fact Tata group employs more

British workers than any other manufacturer (Economist, Out of India Briefing (The Tata

group)). Legally the companies are independent but are wholly or partially owned by a parent

or holding company (Tata group in this case). In these instances Tata group may simply have

funded companies where R&D or product development (innovation) might be important and

this has allowed competitive advantage to follow (Jewell).

Imran Uddin Extended essay (Business & Management) 000817-058

6 St Georges British International School (May 2012)

3% 4% 4%

5%

16%

32%

36%

TATA Sectors Chemicals

Consumer products

Services

Energy

CommunicaKon & informaKon systems Materials

Engineering

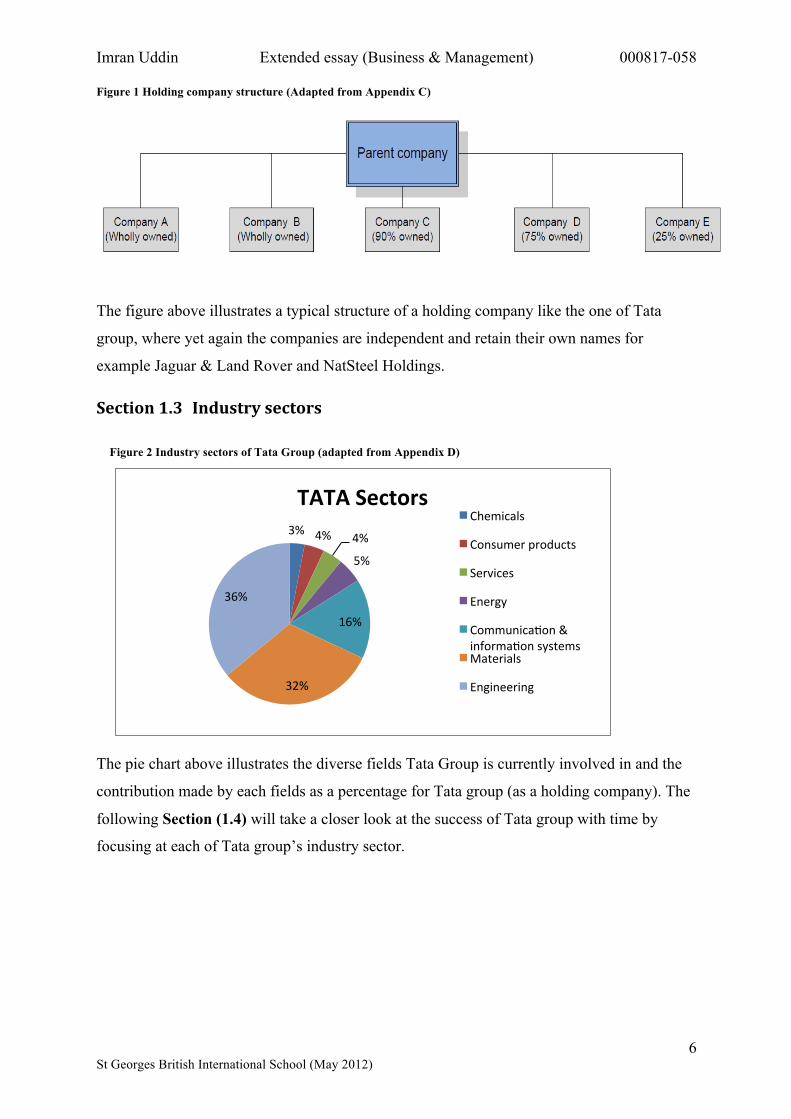

Figure 1 Holding company structure (Adapted from Appendix C)

The figure above illustrates a typical structure of a holding company like the one of Tata

group, where yet again the companies are independent and retain their own names for

example Jaguar & Land Rover and NatSteel Holdings.

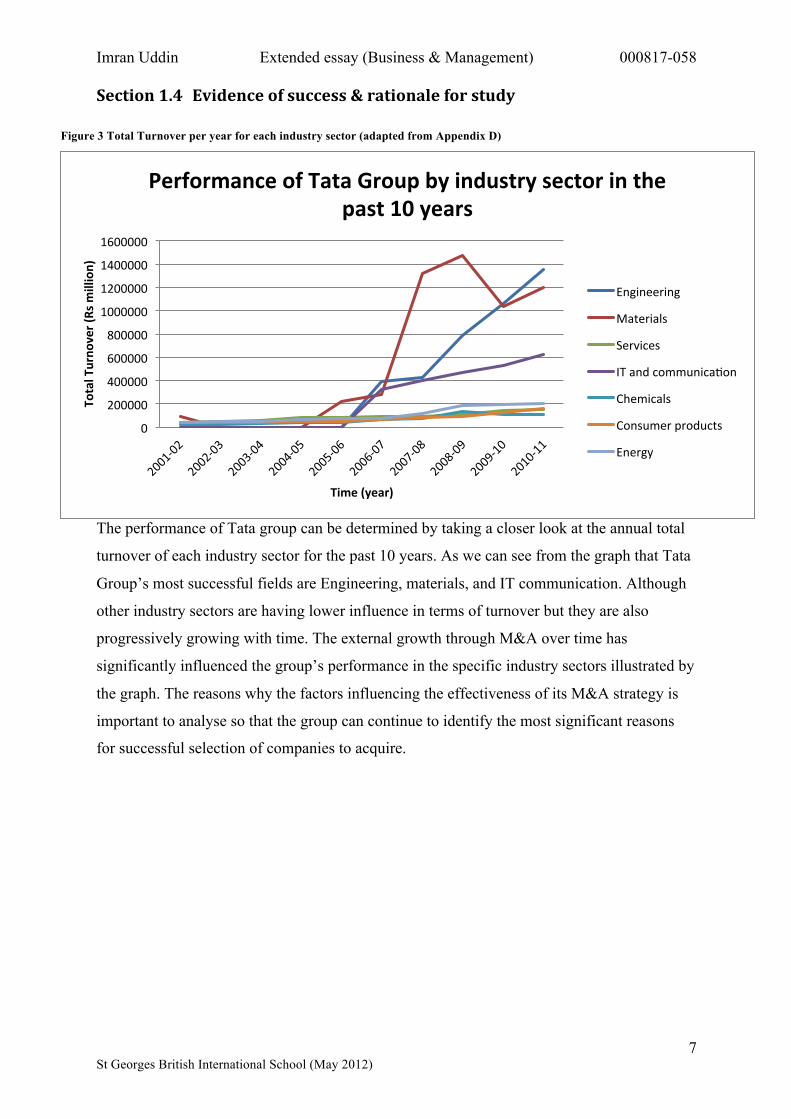

Section 1.3 Industry sectors

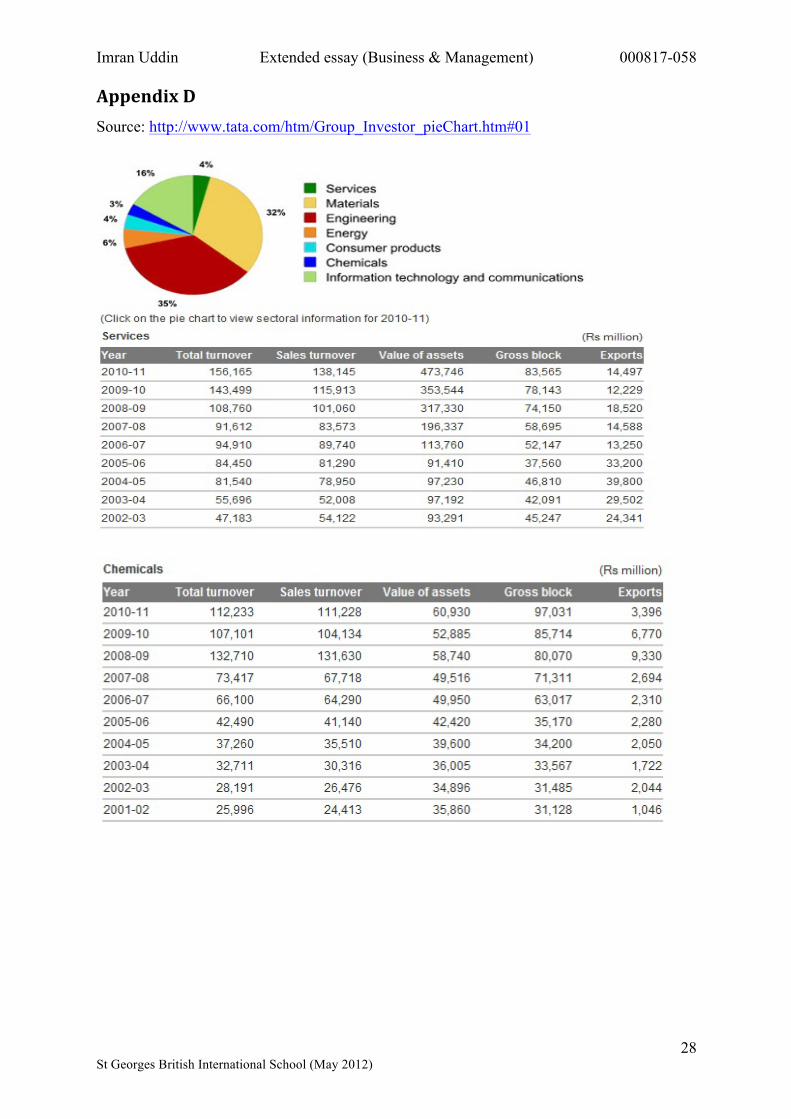

The pie chart above illustrates the diverse fields Tata Group is currently involved in and the

contribution made by each fields as a percentage for Tata group (as a holding company). The

following Section (1.4) will take a closer look at the success of Tata group with time by

focusing at each of Tata group’s industry sector.

Figure 2 Industry sectors of Tata Group (adapted from Appendix D)

Imran Uddin Extended essay (Business & Management) 000817-058

7 St Georges British International School (May 2012)

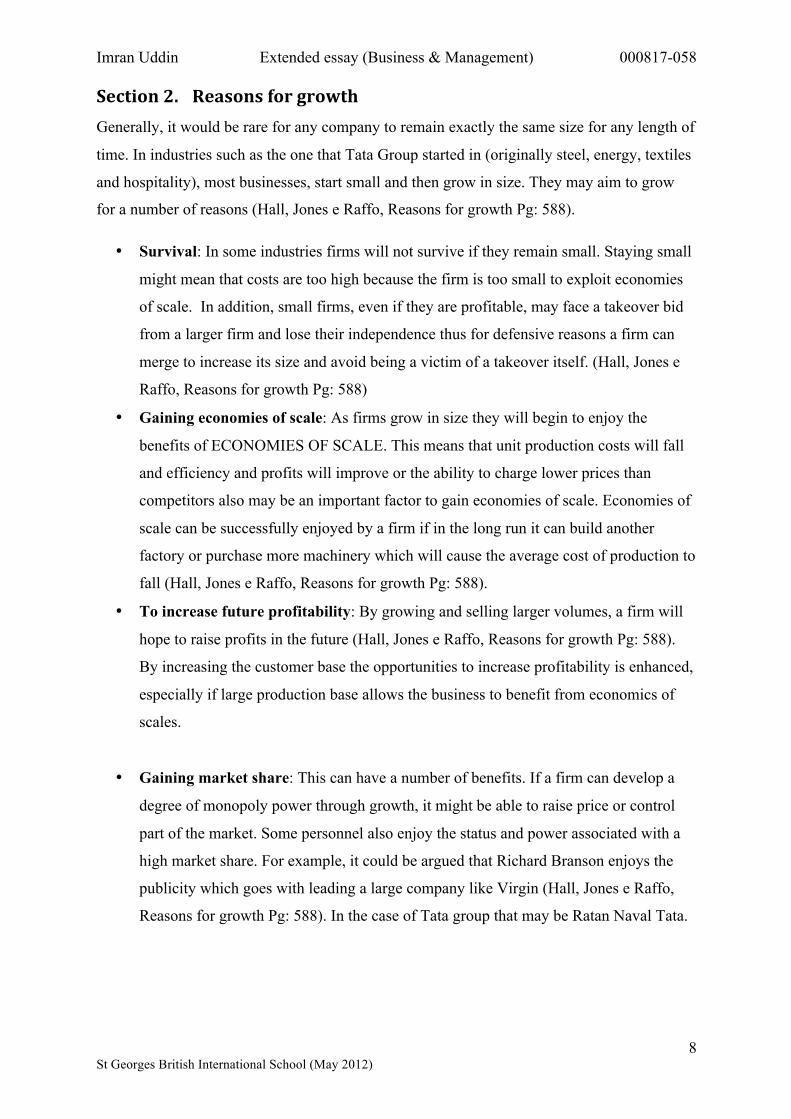

Section 1.4 Evidence of success & rationale for study

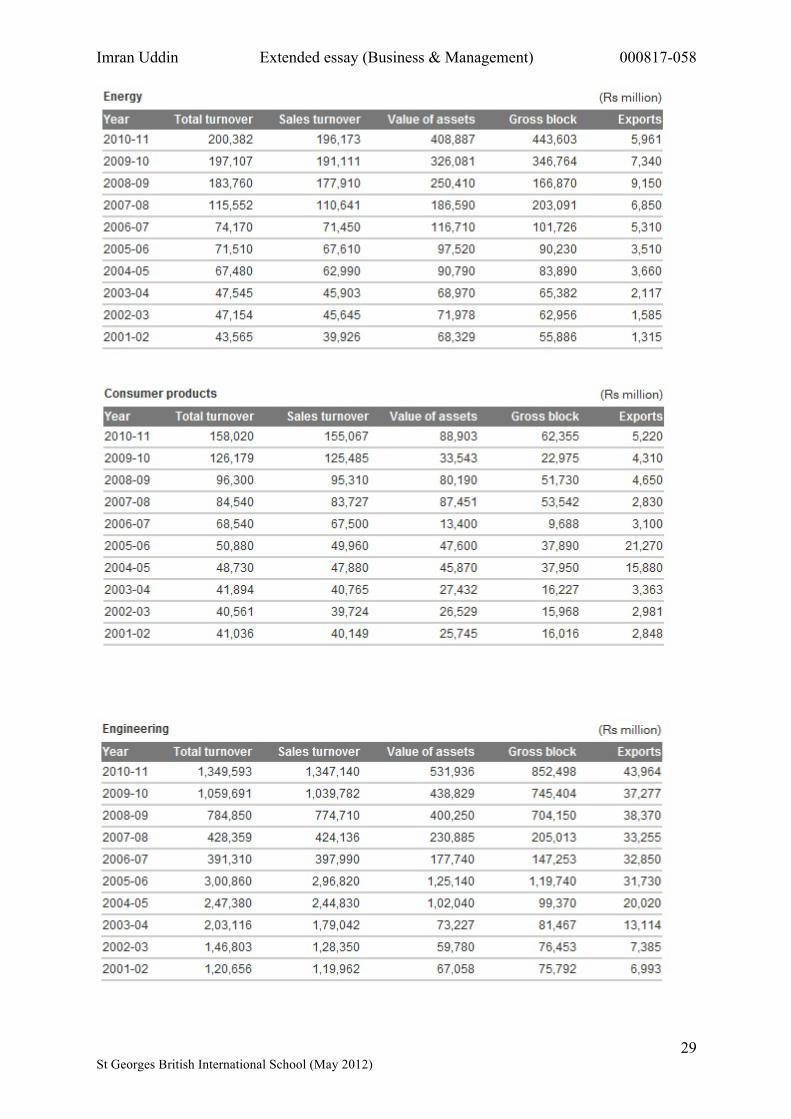

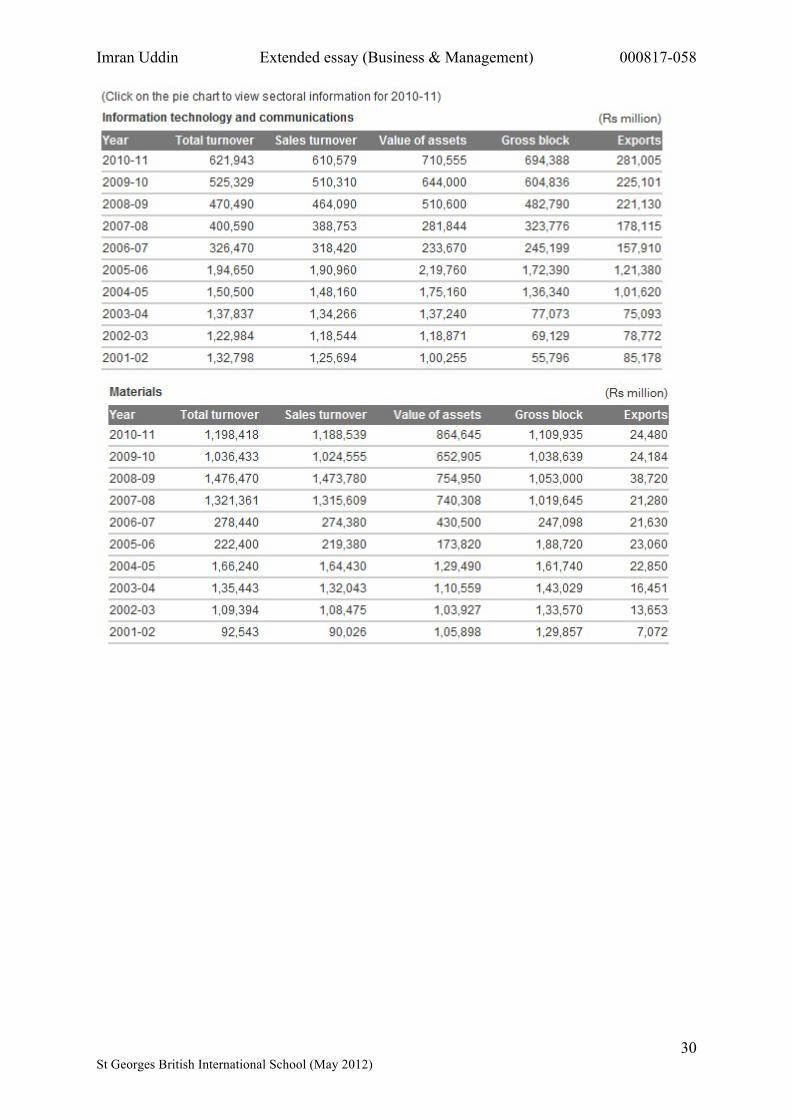

The performance of Tata group can be determined by taking a closer look at the annual total

turnover of each industry sector for the past 10 years. As we can see from the graph that Tata

Group’s most successful fields are Engineering, materials, and IT communication. Although

other industry sectors are having lower influence in terms of turnover but they are also

progressively growing with time. The external growth through M&A over time has

significantly influenced the group’s performance in the specific industry sectors illustrated by

the graph. The reasons why the factors influencing the effectiveness of its M&A strategy is

important to analyse so that the group can continue to identify the most significant reasons

for successful selection of companies to acquire.

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Total Turno

ver (Rs m

illion)

Time (year)

Performance of Tata Group by industry sector in the past 10 years

Engineering

Materials

Services

IT and communicaKon

Chemicals

Consumer products

Energy

Figure 3 Total Turnover per year for each industry sector (adapted from Appendix D)

Imran Uddin Extended essay (Business & Management) 000817-058

8 St Georges British International School (May 2012)

Section 2. Reasons for growth Generally, it would be rare for any company to remain exactly the same size for any length of

time. In industries such as the one that Tata Group started in (originally steel, energy, textiles

and hospitality), most businesses, start small and then grow in size. They may aim to grow

for a number of reasons (Hall, Jones e Raffo, Reasons for growth Pg: 588).

• Survival: In some industries firms will not survive if they remain small. Staying small

might mean that costs are too high because the firm is too small to exploit economies

of scale. In addition, small firms, even if they are profitable, may face a takeover bid

from a larger firm and lose their independence thus for defensive reasons a firm can

merge to increase its size and avoid being a victim of a takeover itself. (Hall, Jones e

Raffo, Reasons for growth Pg: 588)

• Gaining economies of scale: As firms grow in size they will begin to enjoy the

benefits of ECONOMIES OF SCALE. This means that unit production costs will fall

and efficiency and profits will improve or the ability to charge lower prices than

competitors also may be an important factor to gain economies of scale. Economies of

scale can be successfully enjoyed by a firm if in the long run it can build another

factory or purchase more machinery which will cause the average cost of production to

fall (Hall, Jones e Raffo, Reasons for growth Pg: 588).

• To increase future profitability: By growing and selling larger volumes, a firm will

hope to raise profits in the future (Hall, Jones e Raffo, Reasons for growth Pg: 588).

By increasing the customer base the opportunities to increase profitability is enhanced,

especially if large production base allows the business to benefit from economics of

scales.

• Gaining market share: This can have a number of benefits. If a firm can develop a

degree of monopoly power through growth, it might be able to raise price or control

part of the market. Some personnel also enjoy the status and power associated with a

high market share. For example, it could be argued that Richard Branson enjoys the

publicity which goes with leading a large company like Virgin (Hall, Jones e Raffo,

Reasons for growth Pg: 588). In the case of Tata group that may be Ratan Naval Tata.

Imran Uddin Extended essay (Business & Management) 000817-058

9 St Georges British International School (May 2012)

• To reduce risk: Risk can be reduced through diversification. Branching into new

markets and new products means that if one product fails success in others can keep

the company going. For example, tobacco companies have diversified into breweries

to guard against a fall in demand for cigarettes (Hall, Jones e Raffo, Reasons for

growth Pg: 588).

• To create synergy: This occurs when the whole is greater than the sum of the parts,

i.e. when 2+2=5. This is often anticipated in take-overs or mergers, when directors

assert that the purchase of a rival (or willing competitor) will provide such economies

of scale as to make the combined firm a world-beater.

The points quoted above will be considered further for analyses in order to determine the

significance of each of them in shaping the growth of Tata group. These points will also be

reviewed in Section (4) in contrast to the outcomes of the analyses.

Imran Uddin Extended essay (Business & Management) 000817-058

10 St Georges British International School (May 2012)

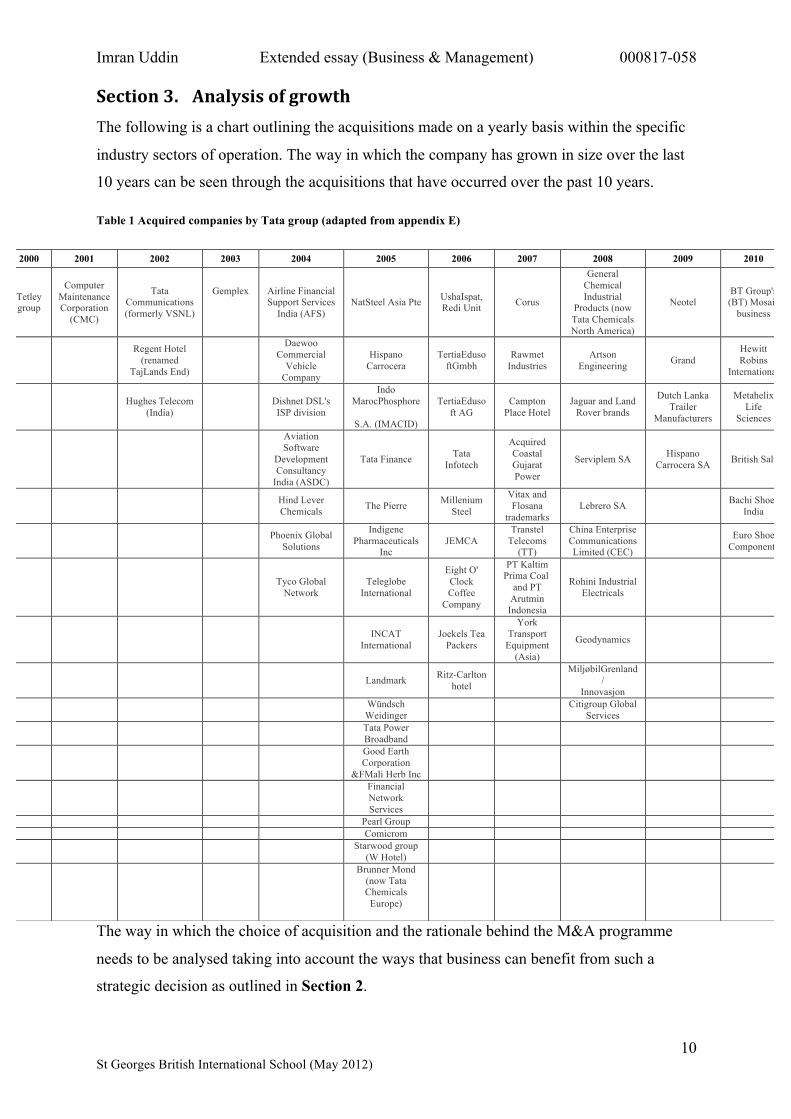

Section 3. Analysis of growth The following is a chart outlining the acquisitions made on a yearly basis within the specific

industry sectors of operation. The way in which the company has grown in size over the last

10 years can be seen through the acquisitions that have occurred over the past 10 years.

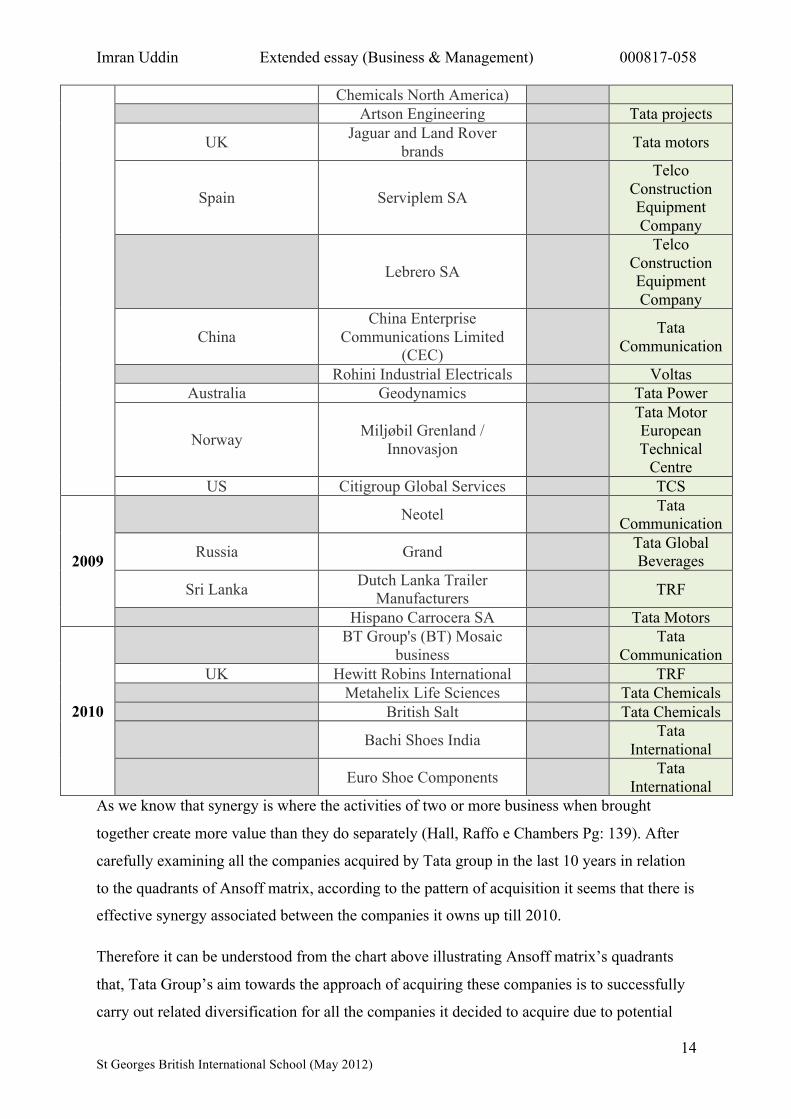

Table 1 Acquired companies by Tata group (adapted from appendix E)

The way in which the choice of acquisition and the rationale behind the M&A programme

needs to be analysed taking into account the ways that business can benefit from such a

strategic decision as outlined in Section 2.

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Tetley group

Computer Maintenance Corporation

(CMC)

Tata Communications (formerly VSNL)

Gemplex

Airline Financial Support Services

India (AFS) NatSteel Asia Pte UshaIspat,

Redi Unit Corus

General Chemical Industrial

Products (now Tata Chemicals North America)

Neotel BT Group's (BT) Mosaic

business

Regent Hotel

(renamed TajLands End)

Daewoo Commercial

Vehicle Company

Hispano Carrocera

TertiaEdusoftGmbh

Rawmet Industries

Artson Engineering Grand

Hewitt Robins

International

Hughes Telecom (India) Dishnet DSL's

ISP division

Indo MarocPhosphore

S.A. (IMACID)

TertiaEdusoft AG

Campton Place Hotel

Jaguar and Land Rover brands

Dutch Lanka Trailer

Manufacturers

Metahelix Life

Sciences

Aviation Software

Development Consultancy

India (ASDC)

Tata Finance Tata Infotech

Acquired Coastal Gujarat Power

Serviplem SA Hispano Carrocera SA British Salt

Hind Lever Chemicals The Pierre Millenium

Steel

Vitax and Flosana

trademarks Lebrero SA Bachi Shoes

India

Phoenix Global Solutions

Indigene Pharmaceuticals

Inc JEMCA

Transtel Telecoms

(TT)

China Enterprise Communications Limited (CEC)

Euro Shoe Components

Tyco Global Network

Teleglobe International

Eight O' Clock Coffee

Company

PT Kaltim Prima Coal

and PT Arutmin

Indonesia

Rohini Industrial Electricals

INCAT International

Joekels Tea Packers

York Transport

Equipment (Asia)

Geodynamics

Landmark Ritz-Carlton hotel

MiljøbilGrenland /

Innovasjon

Wündsch Weidinger Citigroup Global

Services

Tata Power Broadband

Good Earth Corporation

&FMali Herb Inc

Financial Network Services

Pearl Group Comicrom

Starwood group (W Hotel)

Brunner Mond (now Tata Chemicals

Europe)

Imran Uddin Extended essay (Business & Management) 000817-058

11 St Georges British International School (May 2012)

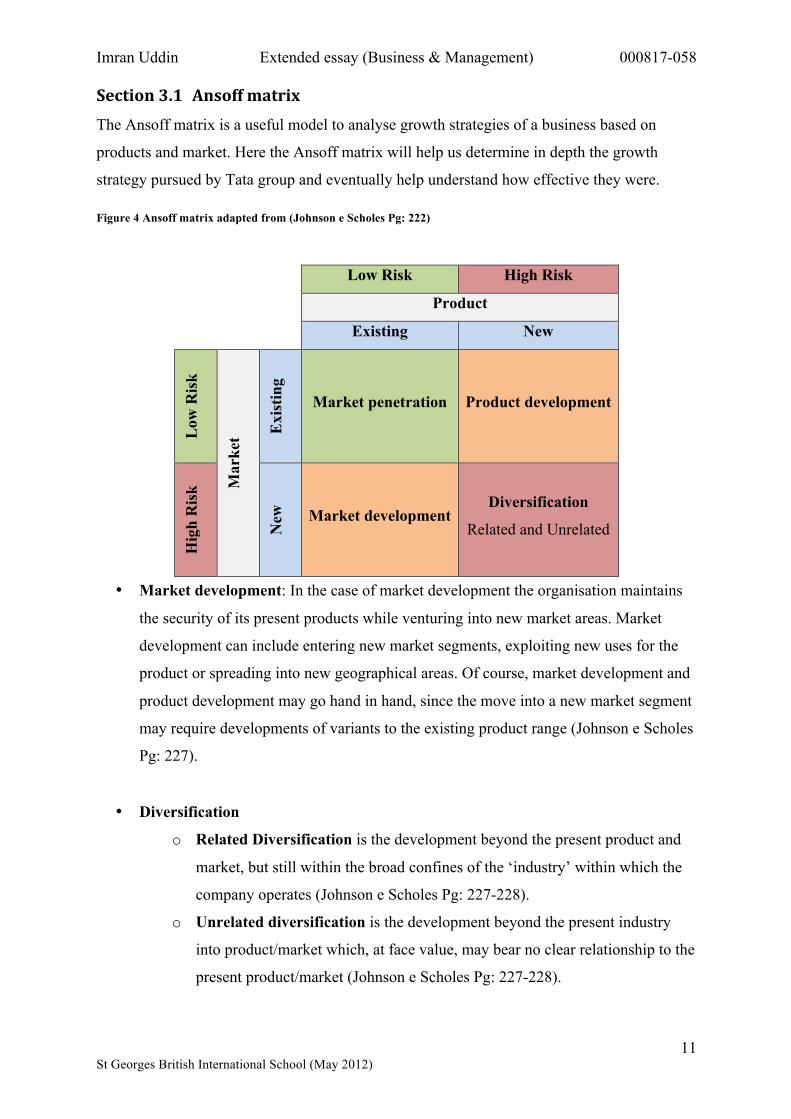

Section 3.1 Ansoff matrix The Ansoff matrix is a useful model to analyse growth strategies of a business based on

products and market. Here the Ansoff matrix will help us determine in depth the growth

strategy pursued by Tata group and eventually help understand how effective they were.

Figure 4 Ansoff matrix adapted from (Johnson e Scholes Pg: 222)

• Market development: In the case of market development the organisation maintains

the security of its present products while venturing into new market areas. Market

development can include entering new market segments, exploiting new uses for the

product or spreading into new geographical areas. Of course, market development and

product development may go hand in hand, since the move into a new market segment

may require developments of variants to the existing product range (Johnson e Scholes

Pg: 227).

• Diversification

o Related Diversification is the development beyond the present product and

market, but still within the broad confines of the ‘industry’ within which the

company operates (Johnson e Scholes Pg: 227-228).

o Unrelated diversification is the development beyond the present industry

into product/market which, at face value, may bear no clear relationship to the

present product/market (Johnson e Scholes Pg: 227-228).

Low Risk High Risk

Product

Existing New

Low

Ris

k

Mar

ket E

xist

ing

Market penetration Product development

Hig

h R

isk

New

Market development Diversification

Related and Unrelated

Imran Uddin Extended essay (Business & Management) 000817-058

12 St Georges British International School (May 2012)

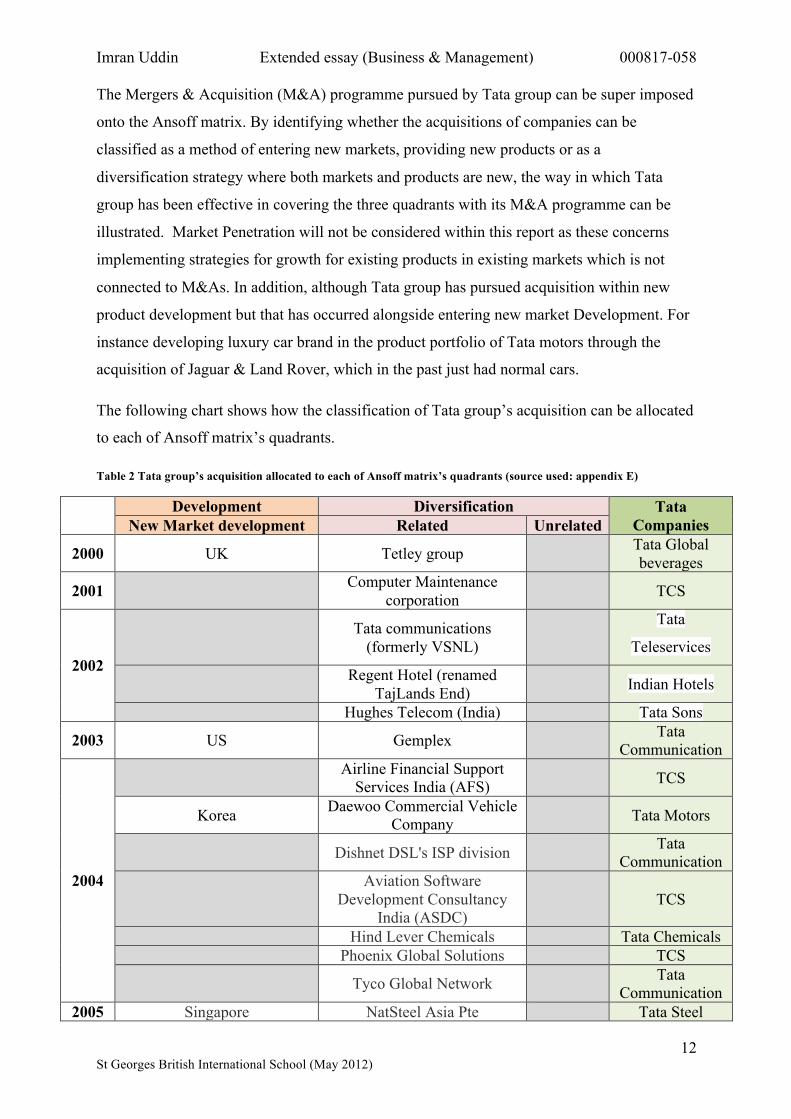

The Mergers & Acquisition (M&A) programme pursued by Tata group can be super imposed

onto the Ansoff matrix. By identifying whether the acquisitions of companies can be

classified as a method of entering new markets, providing new products or as a

diversification strategy where both markets and products are new, the way in which Tata

group has been effective in covering the three quadrants with its M&A programme can be

illustrated. Market Penetration will not be considered within this report as these concerns

implementing strategies for growth for existing products in existing markets which is not

connected to M&As. In addition, although Tata group has pursued acquisition within new

product development but that has occurred alongside entering new market Development. For

instance developing luxury car brand in the product portfolio of Tata motors through the

acquisition of Jaguar & Land Rover, which in the past just had normal cars.

The following chart shows how the classification of Tata group’s acquisition can be allocated

to each of Ansoff matrix’s quadrants.

Table 2 Tata group’s acquisition allocated to each of Ansoff matrix’s quadrants (source used: appendix E)

Development Diversification Tata Companies New Market development Related Unrelated

2000 UK Tetley group Tata Global beverages

2001 Computer Maintenance corporation TCS

2002

Tata communications (formerly VSNL)

Tata

Teleservices

Regent Hotel (renamed TajLands End) Indian Hotels

Hughes Telecom (India) Tata Sons

2003 US Gemplex Tata Communication

2004

Airline Financial Support Services India (AFS) TCS

Korea Daewoo Commercial Vehicle Company Tata Motors

Dishnet DSL's ISP division Tata Communication

Aviation Software

Development Consultancy India (ASDC)

TCS

Hind Lever Chemicals Tata Chemicals Phoenix Global Solutions TCS

Tyco Global Network Tata Communication

2005 Singapore NatSteel Asia Pte Tata Steel

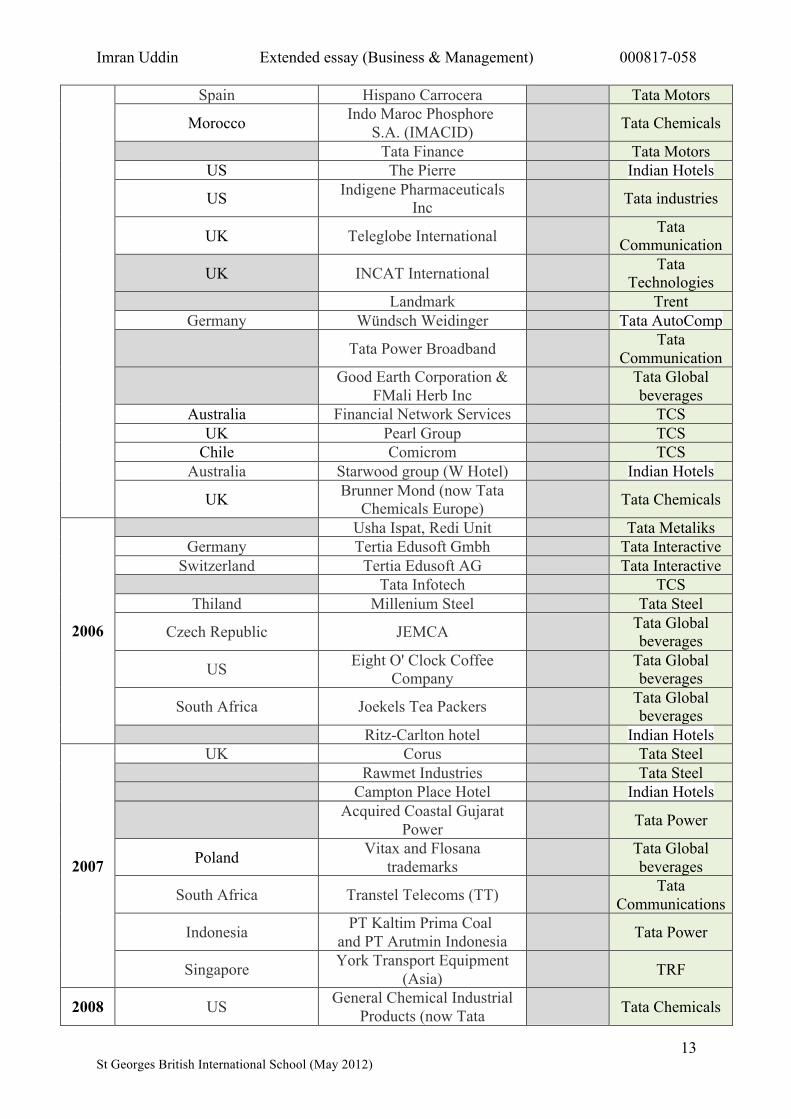

Imran Uddin Extended essay (Business & Management) 000817-058

13 St Georges British International School (May 2012)

Spain Hispano Carrocera Tata Motors

Morocco Indo Maroc Phosphore S.A. (IMACID) Tata Chemicals

Tata Finance Tata Motors US The Pierre Indian Hotels

US Indigene Pharmaceuticals Inc Tata industries

UK Teleglobe International Tata Communication

UK INCAT International Tata Technologies

Landmark Trent Germany Wündsch Weidinger Tata AutoComp

Tata Power Broadband Tata Communication

Good Earth Corporation & FMali Herb Inc Tata Global

beverages Australia Financial Network Services TCS

UK Pearl Group TCS Chile Comicrom TCS

Australia Starwood group (W Hotel) Indian Hotels

UK Brunner Mond (now Tata Chemicals Europe) Tata Chemicals

2006

Usha Ispat, Redi Unit Tata Metaliks Germany Tertia Edusoft Gmbh Tata Interactive

Switzerland Tertia Edusoft AG Tata Interactive Tata Infotech TCS

Thiland Millenium Steel Tata Steel

Czech Republic JEMCA Tata Global beverages

US Eight O' Clock Coffee Company Tata Global

beverages

South Africa Joekels Tea Packers Tata Global beverages

Ritz-Carlton hotel Indian Hotels

2007

UK Corus Tata Steel Rawmet Industries Tata Steel Campton Place Hotel Indian Hotels

Acquired Coastal Gujarat Power Tata Power

Poland Vitax and Flosana trademarks Tata Global

beverages

South Africa Transtel Telecoms (TT) Tata Communications

Indonesia PT Kaltim Prima Coal and PT Arutmin Indonesia Tata Power

Singapore York Transport Equipment (Asia) TRF

2008 US General Chemical Industrial Products (now Tata Tata Chemicals

Imran Uddin Extended essay (Business & Management) 000817-058

14 St Georges British International School (May 2012)

Chemicals North America) Artson Engineering Tata projects

UK Jaguar and Land Rover brands Tata motors

Spain Serviplem SA

Telco Construction Equipment Company

Lebrero SA

Telco Construction Equipment Company

China China Enterprise

Communications Limited (CEC)

Tata Communication

Rohini Industrial Electricals Voltas Australia Geodynamics Tata Power

Norway Miljøbil Grenland / Innovasjon

Tata Motor European Technical

Centre US Citigroup Global Services TCS

2009

Neotel Tata Communication

Russia Grand Tata Global Beverages

Sri Lanka Dutch Lanka Trailer Manufacturers TRF

Hispano Carrocera SA Tata Motors

2010

BT Group's (BT) Mosaic business Tata

Communication UK Hewitt Robins International TRF

Metahelix Life Sciences Tata Chemicals British Salt Tata Chemicals

Bachi Shoes India Tata International

Euro Shoe Components Tata International

As we know that synergy is where the activities of two or more business when brought

together create more value than they do separately (Hall, Raffo e Chambers Pg: 139). After

carefully examining all the companies acquired by Tata group in the last 10 years in relation

to the quadrants of Ansoff matrix, according to the pattern of acquisition it seems that there is

effective synergy associated between the companies it owns up till 2010.

Therefore it can be understood from the chart above illustrating Ansoff matrix’s quadrants

that, Tata Group’s aim towards the approach of acquiring these companies is to successfully

carry out related diversification for all the companies it decided to acquire due to potential

Imran Uddin Extended essay (Business & Management) 000817-058

15 St Georges British International School (May 2012)

synergies in order to ultimately achieve growth in its industries. Although as usual there are

risks associated with diversification but choosing related diversification controls the risk to

some extend and ensures a higher level of certainty of success as Tata group would have a

better potential for handling those companies due to them being related to the current

operations of Tata group. This is further discussed in detail with reference to the integration

chain in Section 3.2.

In addition, along with diversification it has successfully developed into new markets through

some of its acquisitions thus geographically expanding their sectors which spreads the risk so

that the companies are not just depended upon a certain particular geographic region and its

economic climate of any one time. In addition this can give access to different currencies and

reduce the consequences of exchange rate fluctuations associated with one particular

currency.

Moreover, no unrelated diversification was carried out because there are more related

opportunities due to Tata group’s diverse industry sectors (Appendix B) thus there is more

flexibility to go for related diversification and manage the risk effectively. This nature of

M&A was adapted by Tata group so that it can operate in the sectors which it recognises thus

avoiding unnecessary risk.

Section 3.2 Integration chain Integration refers to the bringing together of two or more companies, either by take-over or

merger (Lines, Marcousé e Martin, Integration Pg: 136). The integration chain is one of the

ways to class the mergers, but not all mergers fit in neatly. As identified before that Tata

group is very much involved and keen at performing related diversification and doing so

causes the movement within the integration chain.

Figure 5 Integration chain adapted from (Hall, Jones e Raffo, Types of merger or integration Pg: 651)

Imran Uddin Extended essay (Business & Management) 000817-058

16 St Georges British International School (May 2012)

• Vertical integration

o Backwards integration: refers to development into activities which are

concerned with the inputs into the company’s current business (i.e. are further

back in the value system). For example raw materials, machinery and labour

are all important inputs into a manufacturing company (Johnson e Scholes Pg:

228).

o Forward integration: refers to development into activities which are

concerned with a company’s outputs (i.e. are further forward in the value

system), such as transport, distribution, repairs and servicing (Johnson e

Scholes Pg: 228).

• Horizontal integration: refers to development into activities which are competitive

with, or directly complementary to, a company’s present activities (Johnson e Scholes

Pg: 228).

Imran Uddin Extended essay (Business & Management) 000817-058

17 St Georges British International School (May 2012)

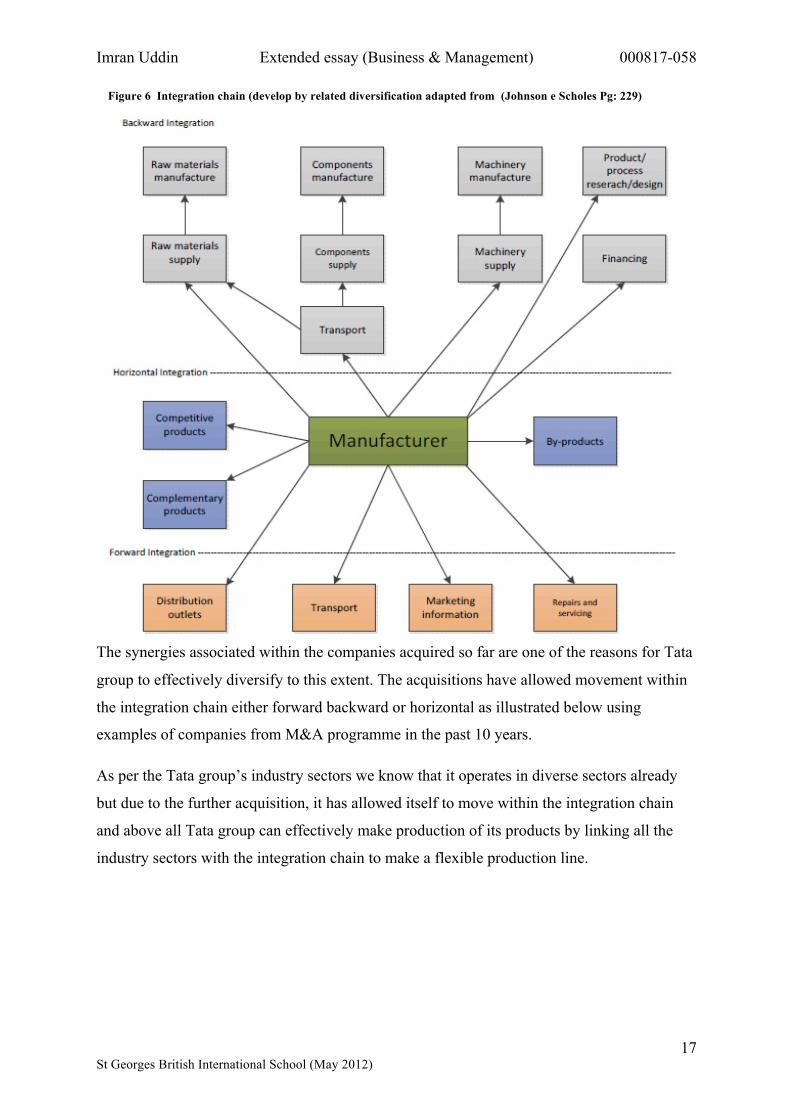

The synergies associated within the companies acquired so far are one of the reasons for Tata

group to effectively diversify to this extent. The acquisitions have allowed movement within

the integration chain either forward backward or horizontal as illustrated below using

examples of companies from M&A programme in the past 10 years.

As per the Tata group’s industry sectors we know that it operates in diverse sectors already

but due to the further acquisition, it has allowed itself to move within the integration chain

and above all Tata group can effectively make production of its products by linking all the

industry sectors with the integration chain to make a flexible production line.

Figure 6 Integration chain (develop by related diversification adapted from (Johnson e Scholes Pg: 229)

Imran Uddin Extended essay (Business & Management) 000817-058

18 St Georges British International School (May 2012)

• Examples with reference to Tata group

o UK’s ‘Tetley group’ was acquired by Tata group in the year 2000 and after in

2005 USA’s ‘Eight O’clock coffee’ was also acquired this shows us Tata

group’s lateral movement within the integration chain thus ultimately

increasing the product portfolio of Tata global beverages and gaining entry

into USA and UK. This has allowed the company to benefit by using similar

production processes and expertise with two companies involved in hot

beverages. In the same year Tata group acquired Joekels Tea Packers of South

Africa which shows us Tata group’s forward integration within the integration

chain.

These operations can benefit the production of the two previously mentioned

companies products as the companies are linked in different parts of the

integration chain of the production of the products for Tata Global Beverages

thus this can reduce the dependence upon other business. In addition Tata

global beverages can also effectively control the quality of its products and

promote the products crucially as now it has a packaging company.

o The acquisition of the first automobile company took place in 2004 of the

‘Daewoo Commercial Vehicle Company’ thus integrating horizontally and

becoming part of Tata motors. The following year Spain’s ‘Hispano

Carrocera’ was also acquired (an automobile company mainly dealing with

coaches) and followed by the acquisition of Germany’s ’Wündsch Weidinger’

which became a part of Tata AutoComp which is responsible for making

automobile dashboards and various other automobile parts. In 2008 ‘Jaguar

and land Rover brands’ was acquired thus integrating horizontally and yet

again becoming a part of Tata motors and subsequently increasing the

portfolio of Tata motors and getting them involved with luxury automobiles.

Also Norway’s ‘Miljøbil Grenland /Innovasjon’ became part of Tata Motor

European Technical Centre in the same year.

Furthermore Singapore’s ‘NatSteel Asia pte’ was the first acquisition of a

steel company by Tata group thus integrating horizontally the same way.

Moreover, in 2006 Thailand’s ‘Millenium Steel’ was also acquired and

Imran Uddin Extended essay (Business & Management) 000817-058

19 St Georges British International School (May 2012)

following year the acquisition of Corus occurred making Tata steel one of the

largest provider of steel in the market.

Focusing on all these steel, automobile and other maintenance fields acquired

by Tata group we can see an important growth in each industry sector through

horizontal integration. Having all these companies in hand, Tata group can

effectively link all these sectors thus moving within the integration and

ultimately making production of its products effectively without being

interdependent with other companies and save cost of production. Moreover

having companies like Tata AutoComp can help control the quality of its

products and the acquisition of ’Wündsch Weidinger’ has also given access to

German technologies which Tata motors can use to efficiently produce

automobiles in its other automobile industries. To sum up we can see that

Tata group has performed successful integration planning which is often one

of the hard factors to achieve through mergers and acquisition.

Section 4. Additional Benefits gained from M&As. This section will look into benefits to be gained through mergers & acquisitions programme

(other than those related to integration chain) and analyse whether Tata group has derived

these benefits. In this way the effectiveness of its programme can be measured and used to

identify which factors have influenced this occurring.

Section 4.1 Quick and Easy Mergers and acquisition is a quick and easy way to expand the business. For example if a

restaurant wanted to open another fifty restaurants, its way could be to buy a company that

already owns some restaurants and convert them into their own chain (HORIZONTAL

INTEGRATION). This was the strategy first used by Tata group after the Tetley group

acquisition. The Indian companies within India are acquired or merged by Tata Group due to

this particular reason. In general it is easier to merge or acquire a business from your own

country because the companies deal with the same currency and culture.

Speed is particularly relevant to Tata Group due to the nature of the type of industries it is

operating in. For example, in 2000 when it bought Tetley Group, there was an established

company making teas, with factory production facilities and an experienced workforce. This

Imran Uddin Extended essay (Business & Management) 000817-058

20 St Georges British International School (May 2012)

enabled them to quickly enter an industry which had a huge customer base in their home

country with potentially high profits.

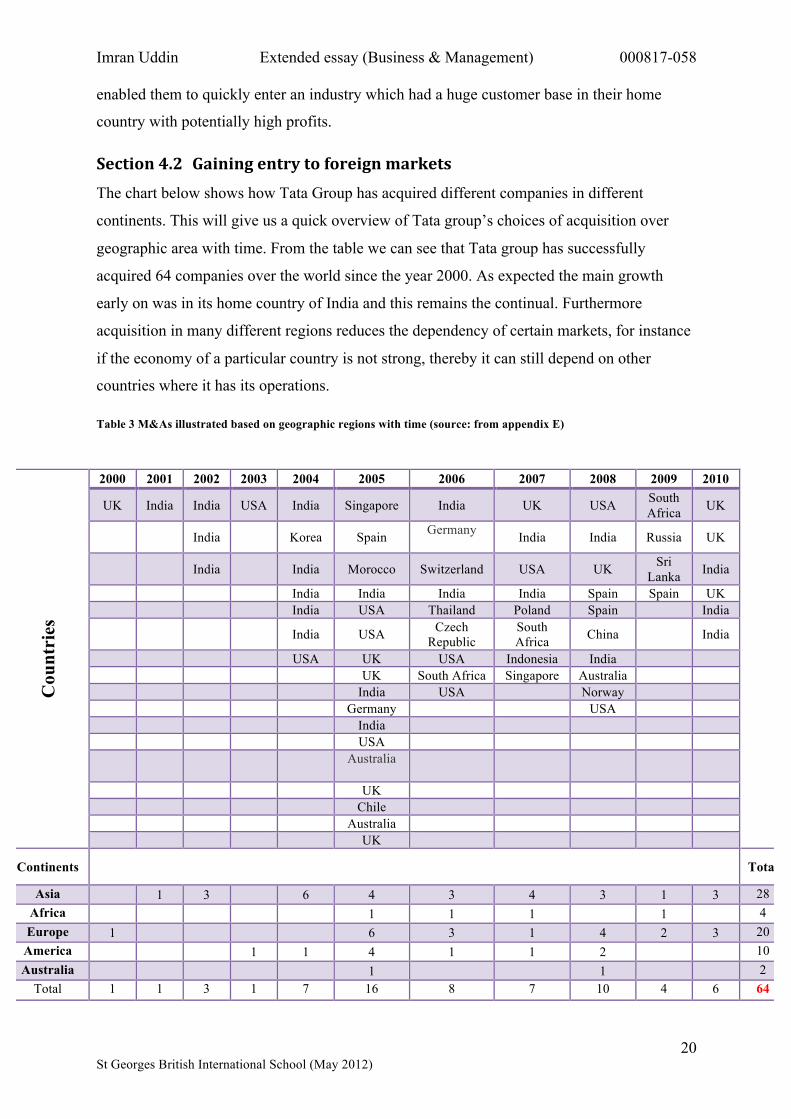

Section 4.2 Gaining entry to foreign markets The chart below shows how Tata Group has acquired different companies in different

continents. This will give us a quick overview of Tata group’s choices of acquisition over

geographic area with time. From the table we can see that Tata group has successfully

acquired 64 companies over the world since the year 2000. As expected the main growth

early on was in its home country of India and this remains the continual. Furthermore

acquisition in many different regions reduces the dependency of certain markets, for instance

if the economy of a particular country is not strong, thereby it can still depend on other

countries where it has its operations.

Table 3 M&As illustrated based on geographic regions with time (source: from appendix E)

Cou

ntri

es

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

UK India India USA India Singapore India UK USA South Africa UK

India Korea Spain Germany India India Russia UK

India India Morocco Switzerland USA UK Sri Lanka India

India India India India Spain Spain UK India USA Thailand Poland Spain India

India USA Czech Republic

South Africa China India

USA UK USA Indonesia India UK South Africa Singapore Australia India USA Norway Germany USA India USA

Australia

UK Chile Australia UK

Continents Total

Asia 1 3 6 4 3 4 3 1 3 28 Africa 1 1 1 1 4 Europe 1 6 3 1 4 2 3 20

America 1 1 4 1 1 2 10 Australia 1 1 2

Total 1 1 3 1 7 16 8 7 10 4 6 64

Imran Uddin Extended essay (Business & Management) 000817-058

21 St Georges British International School (May 2012)

Section 4.3 Gain economies of scale with monopoly position Throughout Tata group’s history of merging and acquisitions, it has managed to combine

different companies in the same industry for example it has merged and acquired many steel

companies starting from NatSteel Asia Pte of Singapore and other steel companies in Asia

then eventually acquiring Corus of UK which has increased the economies of scale of Tata

steel and made it the Top 7 steel company of the world according to world steel association

(World Steel Association). This has also allowed it to become the sole producer of steel in the

UK giving it a dominant position and control over supply chains.

Section 5. Innovation Innovation means bringing a new idea into being within the market-place (product

innovation) or workplace (process innovation) (Lines, Marcousé e Martin, Integration Pg:

135). Above all Tata group’s M&A programme has influenced, innovating the company by

giving it access to western technologies and culture from new market development, which

Tata group uses effectively. Tata group is also responsible for forming many of Indian’s

greatest institutions such as the Indian Institute of Science and the Tata Institute of

Fundamental Research. These institutes play an in important role in contributing R&D for

India. Moreover Tata group’s Tata Research Development and Design Centre (TRDDC) has

projects in many Universities such as Columbia University, Georgia Institute of Technology,

Indian Institute of Technology and Stanford University which can penetrate its market

segments more effectively and be used to drive the innovation in existing companies held by

the group and to help identify possible future acquisition where market growth may be high

(TCS Innovation Labs Tata Research Development & Design Center).

Section 6. Globalisation of markets Globalisation is the term used to describe the growing integration of the world’s economy

and it has played an important role in shaping Tata group so far. Tata group as a business

thinks globally about its strategies. It can be argued that its success is basically based on its

activities in global markets. As an example Tata produces steel in a specific region and

manufactures cars in some other region by having this Tata can cost effectively and

efficiently distribute its products to its customers. In addition being globally present enables

them to have larger scale operations and therefore most likely enables Tata to enjoy

economies of scale.

Imran Uddin Extended essay (Business & Management) 000817-058

22 St Georges British International School (May 2012)

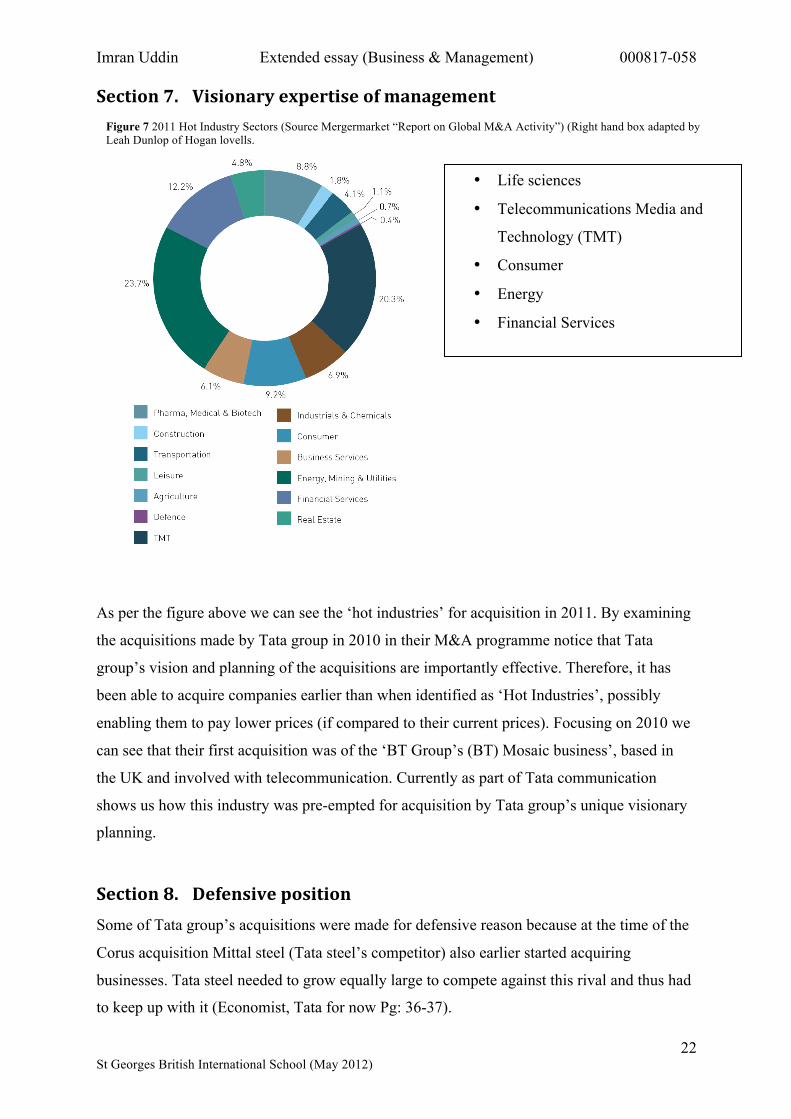

Section 7. Visionary expertise of management

As per the figure above we can see the ‘hot industries’ for acquisition in 2011. By examining

the acquisitions made by Tata group in 2010 in their M&A programme notice that Tata

group’s vision and planning of the acquisitions are importantly effective. Therefore, it has

been able to acquire companies earlier than when identified as ‘Hot Industries’, possibly

enabling them to pay lower prices (if compared to their current prices). Focusing on 2010 we

can see that their first acquisition was of the ‘BT Group’s (BT) Mosaic business’, based in

the UK and involved with telecommunication. Currently as part of Tata communication

shows us how this industry was pre-empted for acquisition by Tata group’s unique visionary

planning.

Section 8. Defensive position Some of Tata group’s acquisitions were made for defensive reason because at the time of the

Corus acquisition Mittal steel (Tata steel’s competitor) also earlier started acquiring

businesses. Tata steel needed to grow equally large to compete against this rival and thus had

to keep up with it (Economist, Tata for now Pg: 36-37).

• Life sciences

• Telecommunications Media and

Technology (TMT)

• Consumer

• Energy

• Financial Services

Figure 7 2011 Hot Industry Sectors (Source Mergermarket “Report on Global M&A Activity”) (Right hand box adapted by Leah Dunlop of Hogan lovells.

Imran Uddin Extended essay (Business & Management) 000817-058

23 St Georges British International School (May 2012)

Section 9. Conclusion The effectiveness of the M&A strategy in choosing appropriate companies to purchase by

Tata group in the last 10 years has had an important role in bringing the holding company to

this current position. Also M&A strategy helped Tata group achieve an increase in turnover

for each of its market sectors in the past 10 years.

Tata group’s effective allocation for alternative growth using the Ansoff matrix had a positive

result on the company. Tata group undertook diversification which is the riskiest of all the

other options but making that choice has enabled them to grow rapidly. Nevertheless Tata

group managed to minimize the level of risk within diversification and undertook related

diversification which increased the certainty of their decision, and after left existing

management structures in place.

Consecutively, strategic diversification strategy reveals links within the integration chain.

Tata group’s ingenious strategy of the evaluation of synergy, integration planning of

choosing the companies and taking the risk to acquire them was successful due to them fitting

neatly into the integration chain thus benefiting the holding company to overall have better

control of supplies markets and quality. Innovation useful in many areas can flourish by links

with universities and R&D companies.

Increased geographic presence of the company has reduced its dependency on any one

market and balanced the risk. Moreover, it also helped gain economics of scale at a point

making it a sole provider, therefore enjoying monopoly power in same cases and as a

defensive position against rival’s acquisition in others.

Tata group being involved in different industry sectors has enabled them to experience the

flavour of different industries and spread risk. The intensions of growing through M&A was

one of the wise choice for a holding company as originating from such emerging markets but

Tata group’s strategy is not based on presumption, in fact it’s the ingenious visionary

expertise which penetrates every aspect of doing business. The visionary expertise is so

advanced that intuitively it seems anomalous as Tata’s executive of purchase of Tetley

quoted that “What looked too high in 2000 looked brilliant by 2007 and a sweet deal by

2010” (Economist, Tata for now Pg: 36-37). In general to summarize the factors influencing

the effectiveness of the M&A are the crucial decision making strategy and management

which are like the brain of Tata group.

Imran Uddin Extended essay (Business & Management) 000817-058

24 St Georges British International School (May 2012)

Section 10. Recommendations Tata group’s strategy can further help contribute the holding company in future. In general

from evidence of achieved success, it is safe to arguably say that Tata group should maintain

its strategies for future acquisitions. Perhaps, for a possible recommendation for future

acquisitions Tata group can perform backward integration, for instance becoming involved

with extracting raw material possibly starting mining operations. Furthermore, they can also

perform forward integration, for example by opening retail store for Tata goods.

Imran Uddin Extended essay (Business & Management) 000817-058

25 St Georges British International School (May 2012)

Bibliography Contributor, Wikipedia. Tata Group. n.d. 16 October 2011

<http://en.wikipedia.org/wiki/Tata_Group>.

Economist. “Out of India Briefing (The Tata group).” The economist 5 March 2011: 68-70.

—. “Tata for now.” The Economist 10 September 2011: 36-37.

Hall, Dave, et al. “Key terms.” Hall, Dave, et al. Business studies Third Edition. Causeway Press, 2007.

Hall, Dave, Rob Jones and Carlo Raffo. “Reasons for growth.” Hall, Dave, Rob Jones and Carlo Raffo. Business Studies Third Edition. Causeway Press Ltd, 2006.

Hall, Dave, Rob Jones and Carlo Raffo. “Types of merger or integration.” Hall, Dave, Rob Jones and Carlo Raffo. Business Studies Third Edition. Causeway Press Ltd, 2006.

Jewell, Bruce. An integrated approach to business studies. Harlow: Longman, 1996.

Johnson, Gerry and Kevan Scholes. “Alternative directions for strategy development.” Exploring Corporate Strategy (Text and Cases) Third Edition. Prentice Hall International (UK) Ltd, 1993.

Lines, David, Ian Marcousé and Barry Martin. “Integration.” Lines, David, Ian Marcousé and Barry Martin. COMPLETE A-Z Business Studied HANDBOOK 5th edition. The Bath Press Ltd, 2006. 135.

Lines, David, Ian Marcousé and Barry Martin. “Integration.” Lines, David, Ian Marcousé and Barry Martin. Complete A-Z business studies handbook. London: Hodder Arnold, 2006. 136.

Tata Group from Wikipedia, the free encyclopedia. n.d. 3 August 2011 <http://en.wikipedia.org/wiki/Tata_Group>.

Tata:Our Heritage. n.d. 16 October 2011 <http://www.tata.com/htm/heritage/HeritageOption1.html>.

TCS Innovation Labs Tata Research Development & Design Center. n.d. 23 November 2011 <http://www.tcs-trddc.com/>.

World Steel Association. n.d. 9 November 2011 <http://www.worldsteel.org/statistics/top-producers.html>.

Imran Uddin Extended essay (Business & Management) 000817-058

26 St Georges British International School (May 2012)

Appendices

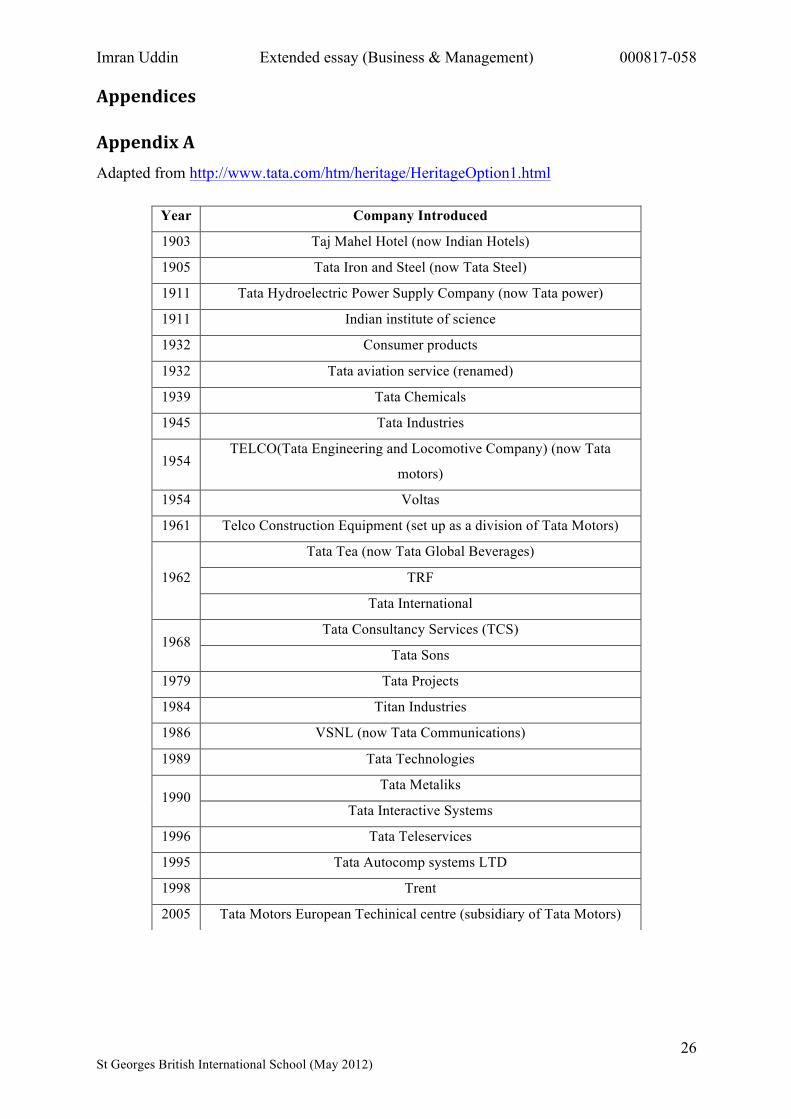

Appendix A Adapted from http://www.tata.com/htm/heritage/HeritageOption1.html

Year Company Introduced

1903 Taj Mahel Hotel (now Indian Hotels)

1905 Tata Iron and Steel (now Tata Steel)

1911 Tata Hydroelectric Power Supply Company (now Tata power)

1911 Indian institute of science

1932 Consumer products

1932 Tata aviation service (renamed)

1939 Tata Chemicals

1945 Tata Industries

1954 TELCO(Tata Engineering and Locomotive Company) (now Tata

motors)

1954 Voltas

1961 Telco Construction Equipment (set up as a division of Tata Motors)

1962

Tata Tea (now Tata Global Beverages)

TRF

Tata International

1968 Tata Consultancy Services (TCS)

Tata Sons

1979 Tata Projects

1984 Titan Industries

1986 VSNL (now Tata Communications)

1989 Tata Technologies

1990 Tata Metaliks

Tata Interactive Systems

1996 Tata Teleservices

1995 Tata Autocomp systems LTD

1998 Trent

2005 Tata Motors European Techinical centre (subsidiary of Tata Motors)

Imran Uddin Extended essay (Business & Management) 000817-058

27 St Georges British International School (May 2012)

Appendix B Adapted from http://en.wikipedia.org/wiki/Tata_Group

Appendix C Source adapted from class hand-out.

TATA Group • Steel • Automobiles • Digital television • Power • IT Services/ITES • Hotels • Consumer goods • Retail • Agriculture • Financial services • Defence • Chemicals • Hospitality • Engineering • Beverages • ConstrucKon • Aerospace • Pharma

Imran Uddin Extended essay (Business & Management) 000817-058

28 St Georges British International School (May 2012)

Appendix D Source: http://www.tata.com/htm/Group_Investor_pieChart.htm#01

Imran Uddin Extended essay (Business & Management) 000817-058

29 St Georges British International School (May 2012)

Imran Uddin Extended essay (Business & Management) 000817-058

30 St Georges British International School (May 2012)

Imran Uddin Extended essay (Business & Management) 000817-058

31 St Georges British International School (May 2012)

Appendix E Source http://www.tata.com/htm/Group_MnA_YearWise.htm

Tata company

Acquired company

Country Stake acquired

Value

2010

January Tata Communications

BT Group's (BT) Mosaic business

UK 100 per cent £0.5 million

April TRF Hewitt Robins International

UK £3 million

December Rallis India (through Tata Chemicals)

Metahelix Life Sciences

India 53.5 per cent Rs99.5 crore

Tata Chemicals British Salt UK 100 per cent (wholly-owned)

£93 million (approximately Rs650 crore)

Tata International

Bachi Shoes India

India 76 per cent

Tata International

Euro Shoe Components

India 76 per cent

2009

January Tata Communications

Neotel South Africa

30 per cent

March Tata Tea (now Tata Global Beverages)

Grand Russia 33.2 per cent

July TRF Dutch Lanka Trailer Manufacturers

Sri Lanka 51 per cent $8.67 million

October Tata Motors Hispano Carrocera SA

Spain Remaining 79 per cent

2008

January Tata Chemicals General US 100 per cent

Imran Uddin Extended essay (Business & Management) 000817-058

32 St Georges British International School (May 2012)

Chemical Industrial Products (now Tata Chemicals North America)

stake

Tata Projects Artson Engineering

India

March Tata Motors Jaguar and Land Rover brands

UK $2.3 billion (approximately)

Telco Construction Equipment Company (Telcon)

Serviplem SA Spain 79 per cent

Telco Construction Equipment Company (Telcon)

Lebrero SA Spain 60 per cent

June Tata Communications

China Enterprise Communications Limited (CEC)

China 50 per cent equity interest

August Voltas Rohini Industrial Electricals

India 51 per cent Rs62 crore

September Tata Power Geodynamics Australia 10 per cent $37.5 million

October Tata Motors European Technical Centre Plc

Miljøbil Grenland / Innovasjon

Norway 50.3 per cent Kroner 12 million (Rs9.40 crore)

December TCS Citigroup Global Services

US 100 per cent $512 million

2007

January Tata Steel Corus UK 100 per cent

March Tata Steel Rawmet Industries

India Rs101 crore

Imran Uddin Extended essay (Business & Management) 000817-058

33 St Georges British International School (May 2012)

April Indian Hotels Campton Place Hotel

US $58 million

Tata Power Acquired Coastal Gujarat Power

India

Tata Tea through Tetley group (now Tata Global Beverages)

Vitax and Flosana trademarks

Poland

Tata Communications

Transtel Telecoms (TT)

South Africa

$33 million (approximately)

June Tata Power PT Kaltim Prima Coal and PT Arutmin Indonesia

Indonesia 30 per cent equity stake

October TRF York Transport Equipment (Asia)

Singapore 51 per cent stake

2006

January Tata Metaliks Usha Ispat, Redi Unit

India 100 per cent (wholly-owned)

Rs115 crore

Tata Interactive Tertia Edusoft Gmbh

Germany 90 per cent

Tertia Edusoft AG

Switzerland 90.38 per cent

February TCS Tata Infotech India

April Tata Steel Millenium Steel Thailand 67.11 per cent $167 million (Baht6.5 billion)

May Tata Tea through Tata Tea (GB) (now Tata Global Beverages)

JEMCA Czech Republic

Assets: intangible and tangible

GBP11.60 million

June Tata Coffee (now Tata Global

Eight O' Clock Coffee

US 100 per cent (wholly-

$220 million (Rs1015 crore)

Imran Uddin Extended essay (Business & Management) 000817-058

34 St Georges British International School (May 2012)

Beverages) Company owned)

September Tata Tea through Tata Tea (GB) (now Tata Global Beverages)

Joekels Tea Packers

South Africa

33.3 per cent GBP0.91 million

November Indian hotels Ritz-Carlton hotel

US $170 million

2005

February Tata Steel NatSteel Asia Pte

Singapore 100 per cent (wholly-owned)

S$468.10 million

Tata Motors Hispano Carrocera

Spain 21 per cent Euro12 million (Rs70 crore)

March Tata Chemicals Indo Maroc Phosphore S.A. (IMACID)

Morocco Equal partner $38 million (Rs166 crore)

April Tata Motors Tata Finance India Merger

July Indian Hotels The Pierre US $9 million Lease of the property

Tata Industries Indigene Pharmaceuticals Inc

US <30 per cent

Tata Communications

Teleglobe International

UK

August Tata Technologies

INCAT International

UK

Trent Landmark India 76 per cent $24.09 million (Rs103.60 crore)

September Tata AutoComp Wündsch Weidinger

Germany Euro7 million

Tata Communications

Tata Power Broadband

India

October Tata Tea through Tata Tea (GB)

Good Earth Corporation &

US 100 per cent (wholly-

$31 million

Imran Uddin Extended essay (Business & Management) 000817-058

35 St Georges British International School (May 2012)

(now Tata Global Beverages)

FMali Herb Inc owned)

TCS Financial Network Services

Australia

TCS Pearl Group UK Structured deal

November TCS Comicrom Chile

December Indian Hotels Starwood group (W Hotel)

Sydney 100 per cent (wholly-owned)

$29 million

Tata Chemicals Brunner Mond (now Tata Chemicals Europe)

UK 63.5 per cent (December 2005)

Rs508 crore (December 2005)

36.5 per cent (March 2006)

Rs290 crore (March 2006)

2004

January TCS Airline Financial Support Services India (AFS)

India 100 per cent (wholly-owned)

GBP271 million

March Tata Motors Daewoo Commercial Vehicle Company

Korea 100 per cent (wholly-owned)

KRW120 billion ($102 million / Rs465 crore)

Tata Communications

Dishnet DSL's ISP division

India

TCS Aviation Software Development Consultancy India (ASDC)

India

June Tata Chemicals Hind Lever Chemicals

India Amalgamation

Imran Uddin Extended essay (Business & Management) 000817-058

36 St Georges British International School (May 2012)

July TCS Phoenix Global Solutions

India

November Tata Communications

Tyco Global Network

US

2003

July Tata Communications

Gemplex US

2002

February Tata Sons Tata Communications (formerly VSNL)

India 100 per cent (wholly-owned)

GBP271 million

September Indian Hotels Regent Hotel (renamed Taj Lands End)

India Effective 100 per cent stake

Rs450 crore

December Tata Teleservices

Hughes Telecom (India)

India 50.83 per cent Rs858.83 crore

2001

November Tata Sons (TCS) Computer Maintenance Corporation (CMC)

India

2000

February Tata Tea and Tata Sons (now Tata Global Beverages)

Tetley group UK 100 per cent (wholly-owned)

GBP271 millionGBP271 million

Imran Uddin Extended essay (Business & Management) 000817-058

37 St Georges British International School (May 2012)

![MEGADYNE M EE GG AA WW EE LL G AA WW EE LL DD M W · PDF file5 CINGHIE TRAPEZOIDALI “V” BELTS MEGADYNE KEILRIEMEN Codice Code Typ Sezione Cross section Abmessung B x H [mm] Forza](https://img.pdfslide.us/doc/110x75/5a7c03b07f8b9a72118c60e7/megadyne-m-ee-gg-aa-ww-ee-ll-g-aa-ww-ee-ll-dd-m-w-cinghie-trapezoidali-v.jpg)

![DRAGON'S LAIR G e n e v i e v e D i d i o n K - 8 M a y 2 ... · upcoming events ee]a ee]a a ee]a a ee]a ee]a a a ee]a ee]a ee]a ee]a ee]a ee]a ee]a ee]a ee]a dragon's lair g e n](https://img.pdfslide.us/doc/110x75/5edb079c09ac2c67fa68b1f0/dragons-lair-g-e-n-e-v-i-e-v-e-d-i-d-i-o-n-k-8-m-a-y-2-upcoming-events-eea.jpg)