Embed Size (px)

Citation preview

1

Economic outlook: Indonesia in 2017

Jakarta

10 November 2016

Adrian Panggabean

Chief Economist

Treasury and Capital Market

PT Bank CIMB Niaga Tbk

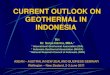

The global context CIMB Group’s global view for 2017: what does it mean for Indonesia?

No Country Growth (%) Inflation (%) Policy rate (%) Exchange Rate

1 US 2.2 1.5 1.25

USD1.05/EUR1.0 Strengthen

2 Eurozone 1.6 1.1 0

3 Japan 0.8 1.1 -0.2 to 0.1 JPY115/USD1.0 Weaken

4 China 6.4 1.6 3.5 RMB6.9/USD1.0 Weaken

• A strong USD benefits Eurozone and Japanese products, who in turn will compete with emerging markets

• A strong USD will hurt emerging market currencies • China weakness (along with its interest to remain competitive) may lead to relative weakness of

RMB that will add pressure to emerging market currencies • China weakness will limit global demand, putting lid on commodity price appreciation

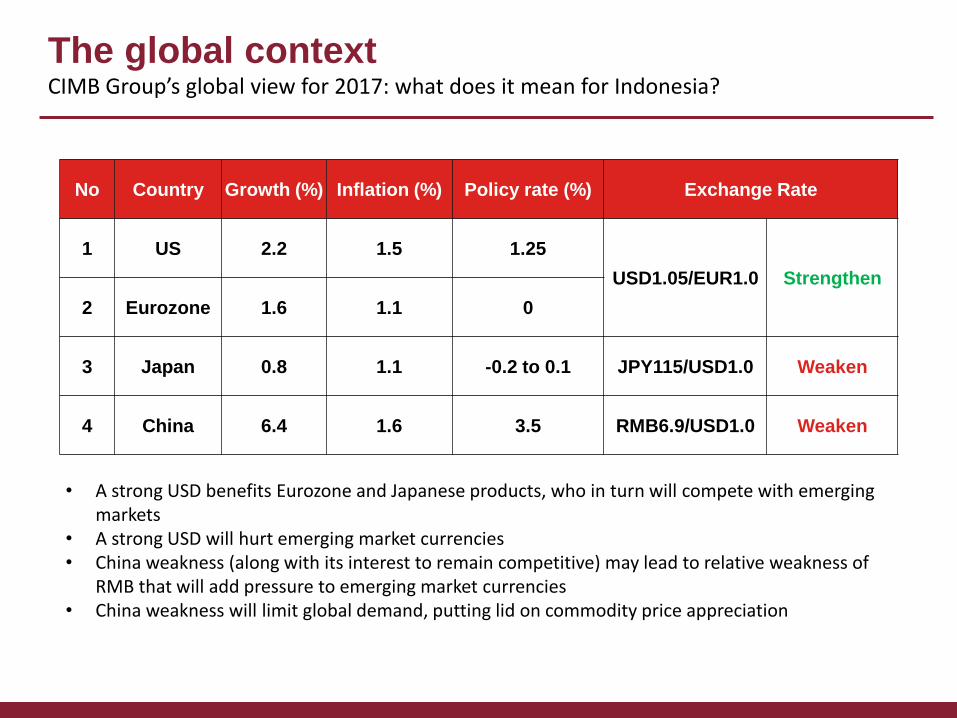

Baltic exchange dry index Global growth will remain either flat or softer, giving impetus to no trade revival

Average index and relative trade strength

Period Average index % relative to

1985 = 100

1985-1990 1,154 0

1991-2000 1,391 21

2001-2005 2,571 123

2006-2010 4,407 282

2011-2014 1,194 3

Full 2015 718 -38

1H2016 486 -58

2H2016 773 -33

Full 2016 607 -47

-100

-50

0

50

100

150

200

250

300

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

198

5

198

8

199

1

199

4

199

7

200

0

200

3

200

6

200

9

201

2

201

5

Baltic ExchangeDry Index (LHS)

% Relative to 1985= 100 (RHS)

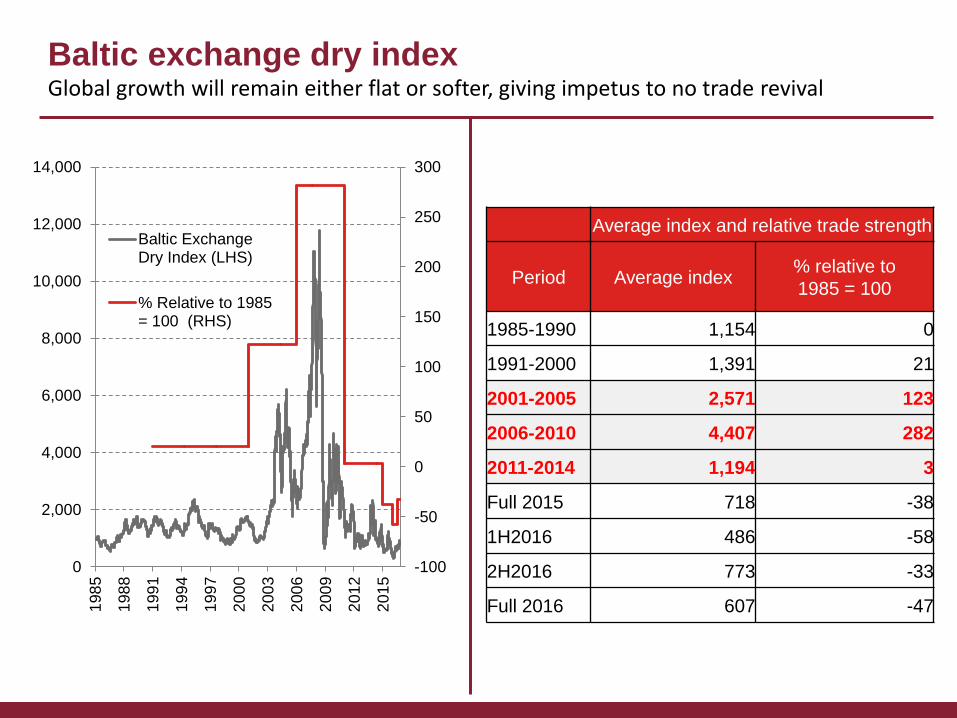

The US economy

Gradually gets stronger but rate increase is likely to be gradual

Source: CEIC

Unemployment, inflation, growth

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

% Yield US 10-year

0

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015 Oct2016

%

Unemployment Rate Inflation Rate

Real GDP Growth

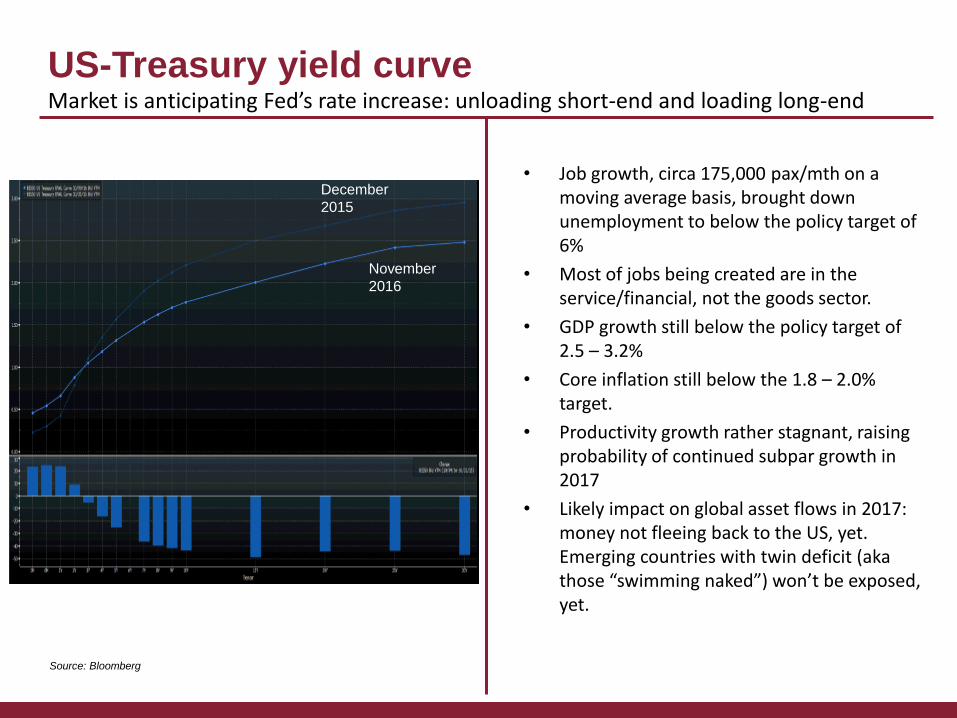

US-Treasury yield curve Market is anticipating Fed’s rate increase: unloading short-end and loading long-end

t

Source: Bloomberg

December

2015

November

2016

• Job growth, circa 175,000 pax/mth on a moving average basis, brought down unemployment to below the policy target of 6%

• Most of jobs being created are in the service/financial, not the goods sector.

• GDP growth still below the policy target of 2.5 – 3.2%

• Core inflation still below the 1.8 – 2.0% target.

• Productivity growth rather stagnant, raising probability of continued subpar growth in 2017

• Likely impact on global asset flows in 2017: money not fleeing back to the US, yet. Emerging countries with twin deficit (aka those “swimming naked”) won’t be exposed, yet.

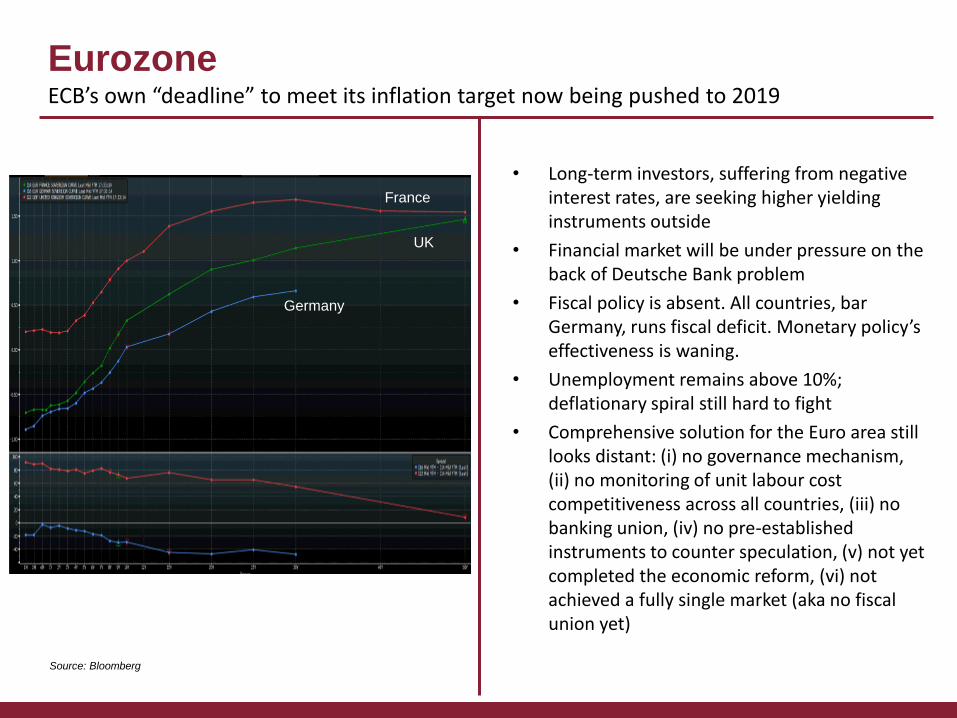

Eurozone ECB’s own “deadline” to meet its inflation target now being pushed to 2019

Source: Bloomberg

UK

France

Germany

• Long-term investors, suffering from negative interest rates, are seeking higher yielding instruments outside

• Financial market will be under pressure on the back of Deutsche Bank problem

• Fiscal policy is absent. All countries, bar Germany, runs fiscal deficit. Monetary policy’s effectiveness is waning.

• Unemployment remains above 10%; deflationary spiral still hard to fight

• Comprehensive solution for the Euro area still looks distant: (i) no governance mechanism, (ii) no monitoring of unit labour cost competitiveness across all countries, (iii) no banking union, (iv) no pre-established instruments to counter speculation, (v) not yet completed the economic reform, (vi) not achieved a fully single market (aka no fiscal union yet)

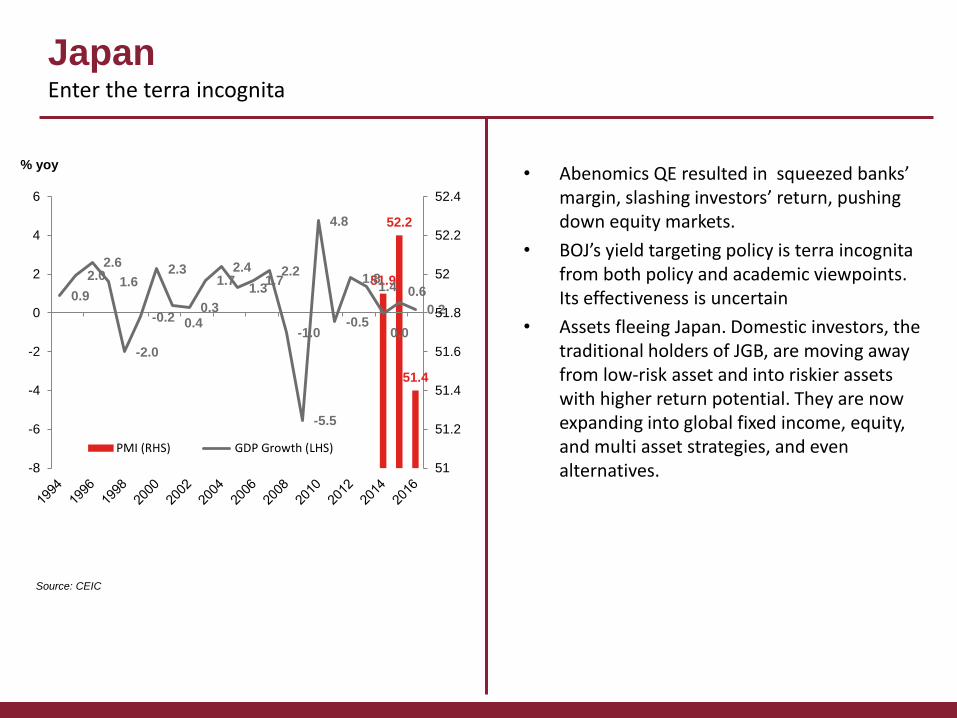

Japan Enter the terra incognita

Source: CEIC

• Abenomics QE resulted in squeezed banks’ margin, slashing investors’ return, pushing down equity markets.

• BOJ’s yield targeting policy is terra incognita from both policy and academic viewpoints. Its effectiveness is uncertain

• Assets fleeing Japan. Domestic investors, the traditional holders of JGB, are moving away from low-risk asset and into riskier assets with higher return potential. They are now expanding into global fixed income, equity, and multi asset strategies, and even alternatives.

% yoy

51.9

52.2

51.4

0.9

2.0 2.6

1.6

-2.0

-0.2

2.3

0.4 0.3

1.7 2.4

1.3 1.7

2.2

-1.0

-5.5

4.8

-0.5

1.8 1.4

0.0

0.6

0.2

51

51.2

51.4

51.6

51.8

52

52.2

52.4

-8

-6

-4

-2

0

2

4

6

PMI (RHS) GDP Growth (LHS)

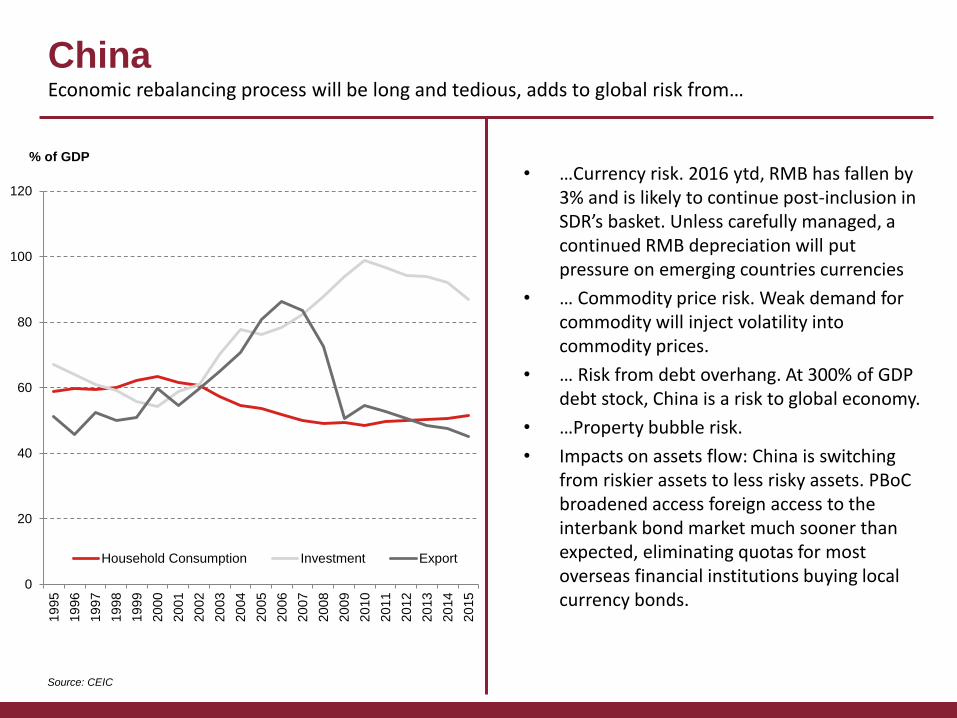

China Economic rebalancing process will be long and tedious, adds to global risk from…

Source: CEIC

• …Currency risk. 2016 ytd, RMB has fallen by 3% and is likely to continue post-inclusion in SDR’s basket. Unless carefully managed, a continued RMB depreciation will put pressure on emerging countries currencies

• … Commodity price risk. Weak demand for commodity will inject volatility into commodity prices.

• … Risk from debt overhang. At 300% of GDP debt stock, China is a risk to global economy.

• …Property bubble risk.

• Impacts on assets flow: China is switching from riskier assets to less risky assets. PBoC broadened access foreign access to the interbank bond market much sooner than expected, eliminating quotas for most overseas financial institutions buying local currency bonds.

0

20

40

60

80

100

120

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Household Consumption Investment Export

% of GDP

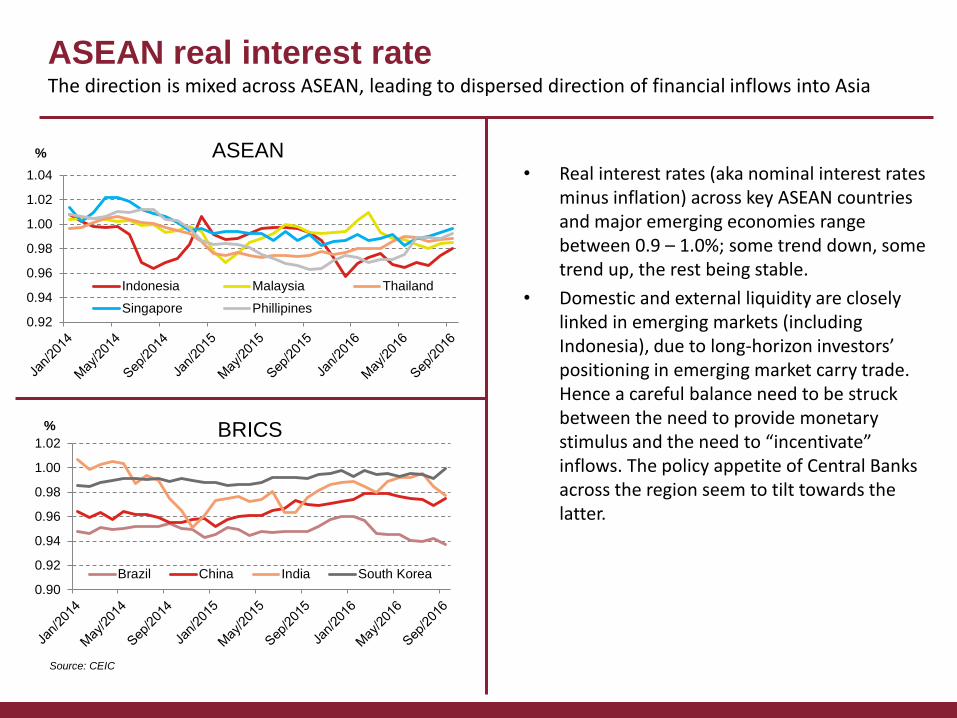

ASEAN real interest rate The direction is mixed across ASEAN, leading to dispersed direction of financial inflows into Asia

Source: CEIC

• Real interest rates (aka nominal interest rates minus inflation) across key ASEAN countries and major emerging economies range between 0.9 – 1.0%; some trend down, some trend up, the rest being stable.

• Domestic and external liquidity are closely linked in emerging markets (including Indonesia), due to long-horizon investors’ positioning in emerging market carry trade. Hence a careful balance need to be struck between the need to provide monetary stimulus and the need to “incentivate” inflows. The policy appetite of Central Banks across the region seem to tilt towards the latter.

0.92

0.94

0.96

0.98

1.00

1.02

1.04

% ASEAN

Indonesia Malaysia Thailand

Singapore Phillipines

0.90

0.92

0.94

0.96

0.98

1.00

1.02

% BRICS

Brazil China India South Korea

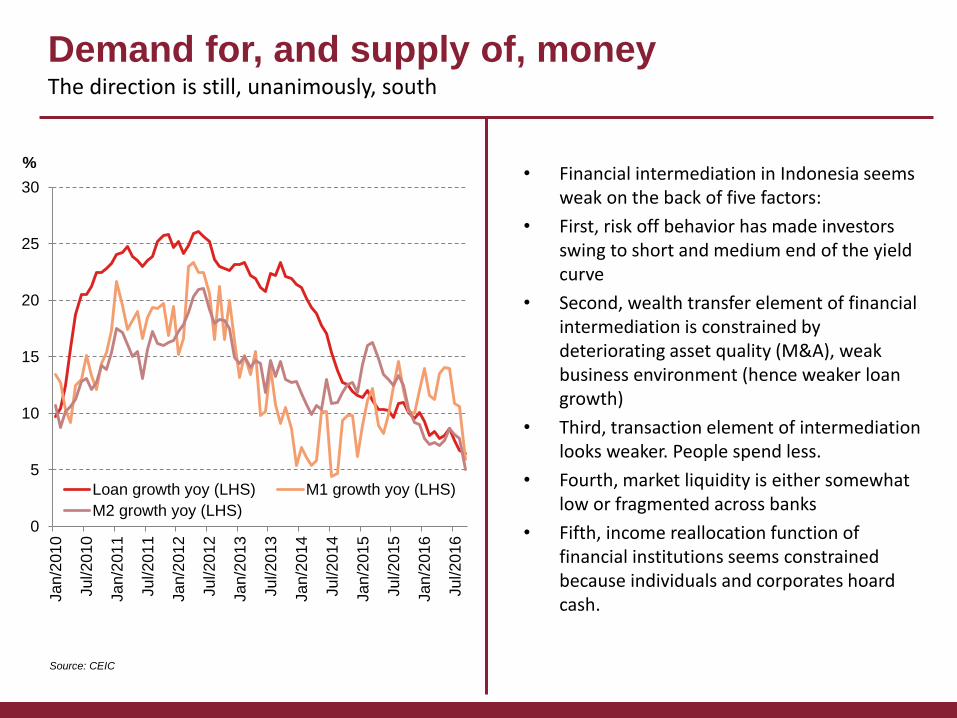

Demand for, and supply of, money The direction is still, unanimously, south

Source: CEIC

• Financial intermediation in Indonesia seems weak on the back of five factors:

• First, risk off behavior has made investors swing to short and medium end of the yield curve

• Second, wealth transfer element of financial intermediation is constrained by deteriorating asset quality (M&A), weak business environment (hence weaker loan growth)

• Third, transaction element of intermediation looks weaker. People spend less.

• Fourth, market liquidity is either somewhat low or fragmented across banks

• Fifth, income reallocation function of financial institutions seems constrained because individuals and corporates hoard cash.

0

5

10

15

20

25

30

Ja

n/2

01

0

Ju

l/20

10

Ja

n/2

01

1

Ju

l/20

11

Ja

n/2

01

2

Ju

l/20

12

Ja

n/2

01

3

Ju

l/20

13

Ja

n/2

01

4

Ju

l/20

14

Ja

n/2

01

5

Ju

l/20

15

Ja

n/2

01

6

Ju

l/20

16

%

Loan growth yoy (LHS) M1 growth yoy (LHS)

M2 growth yoy (LHS)

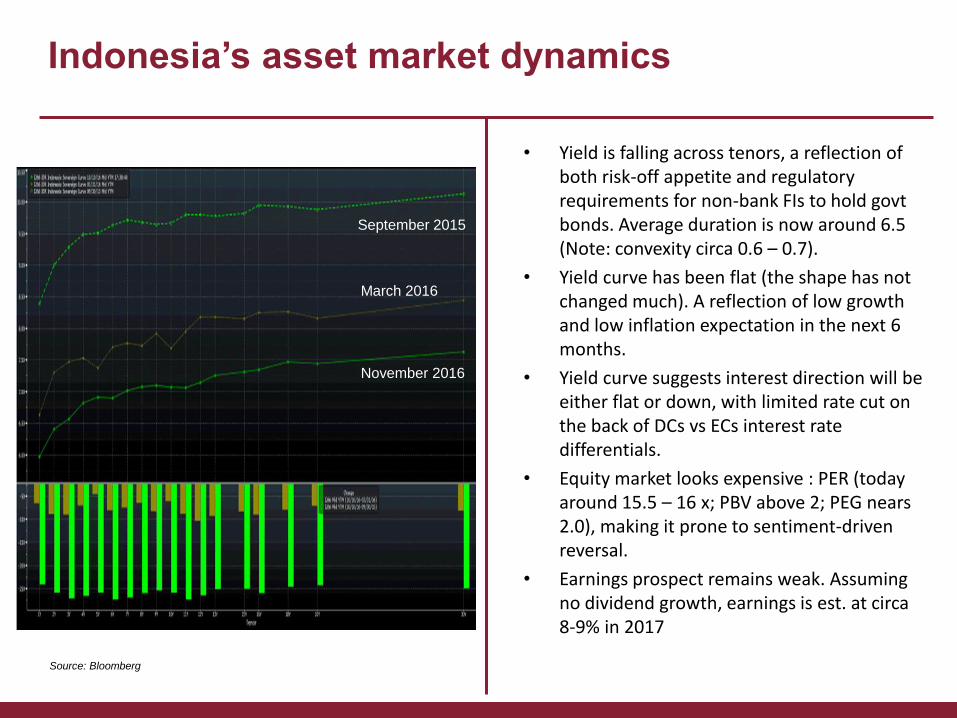

Indonesia’s asset market dynamics

Source: Bloomberg

• Yield is falling across tenors, a reflection of both risk-off appetite and regulatory requirements for non-bank FIs to hold govt bonds. Average duration is now around 6.5 (Note: convexity circa 0.6 – 0.7).

• Yield curve has been flat (the shape has not changed much). A reflection of low growth and low inflation expectation in the next 6 months.

• Yield curve suggests interest direction will be either flat or down, with limited rate cut on the back of DCs vs ECs interest rate differentials.

• Equity market looks expensive : PER (today around 15.5 – 16 x; PBV above 2; PEG nears 2.0), making it prone to sentiment-driven reversal.

• Earnings prospect remains weak. Assuming no dividend growth, earnings is est. at circa 8-9% in 2017

September 2015

March 2016

November 2016

GDP growth by province 2015 Eastern Indonesia is apparently able to withstand economic slowdown in 2015…

1.4

5.3

5.7

4.5

5.2

3.2

3.9

4.9

4.9

4.3

5.3 6.5

5.2

5.5

6.1 5.9

6.0

12.0

5.1

4.4

-0.6

6.6

4.1

8.7

7.2 7.5

15.1

7.7

5.6

6.1

6.5

5.2

14.0

GDP growth by province 9M2016 …and in 2016

9.4

9.7

8.1

4.4

8.8

9.5

6.6

10.1

8.1

6.0

10.1 9.4

8.4

8.5

8.3 9.8

10.5

13.8

11.2

4.2

-4.51

5.7

4.0

8.5

11.3 10.

2

13.4

12.5

10.

5

9.3

8.3

4.3

14.6

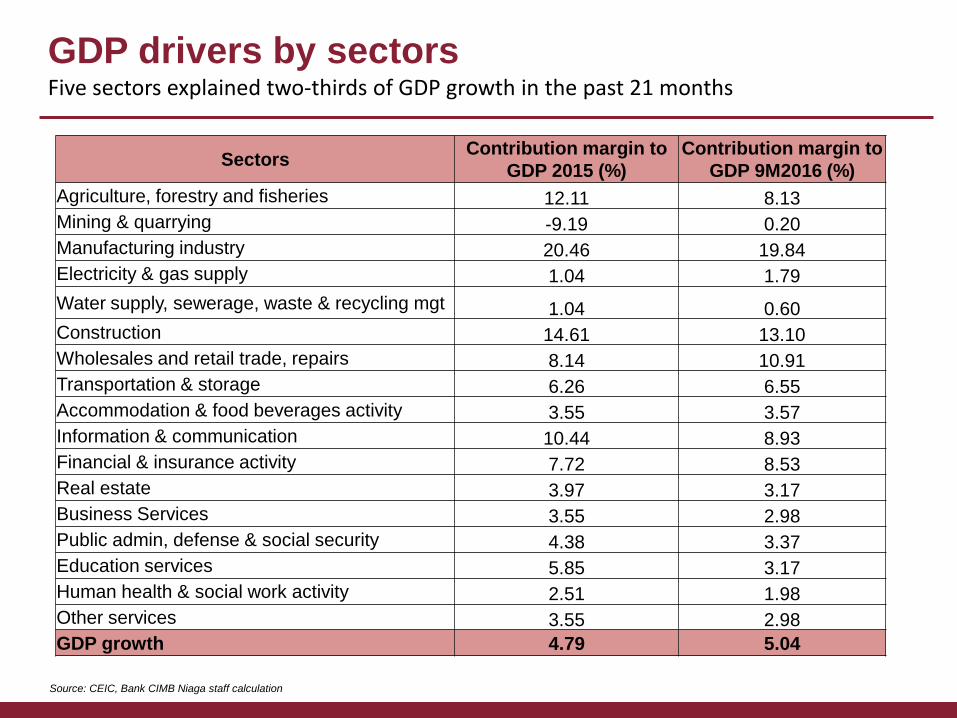

GDP drivers by sectors

Five sectors explained two-thirds of GDP growth in the past 21 months

Source: CEIC, Bank CIMB Niaga staff calculation

Sectors Contribution margin to

GDP 2015 (%)

Contribution margin to

GDP 9M2016 (%)

Agriculture, forestry and fisheries 12.11 8.13

Mining & quarrying -9.19 0.20

Manufacturing industry 20.46 19.84

Electricity & gas supply 1.04 1.79

Water supply, sewerage, waste & recycling mgt 1.04 0.60

Construction 14.61 13.10

Wholesales and retail trade, repairs 8.14 10.91

Transportation & storage 6.26 6.55

Accommodation & food beverages activity 3.55 3.57

Information & communication 10.44 8.93

Financial & insurance activity 7.72 8.53

Real estate 3.97 3.17

Business Services 3.55 2.98

Public admin, defense & social security 4.38 3.37

Education services 5.85 3.17

Human health & social work activity 2.51 1.98

Other services 3.55 2.98

GDP growth 4.79 5.04

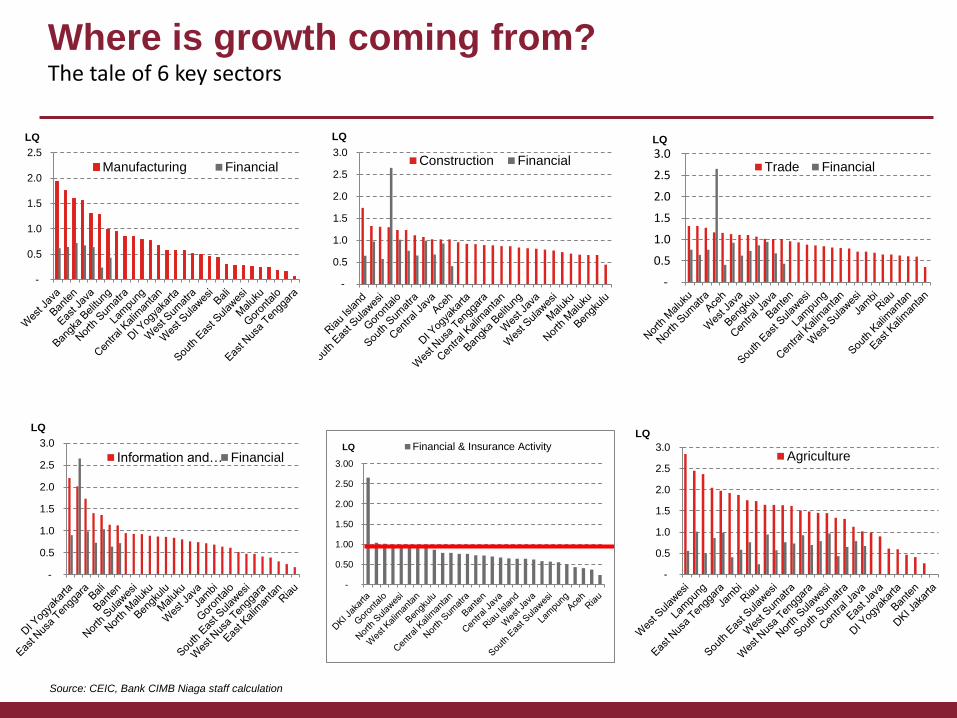

Where is growth coming from? The tale of 6 key sectors

Source: CEIC, Bank CIMB Niaga staff calculation

-

0.50

1.00

1.50

2.00

2.50

3.00

Financial & Insurance ActivityLQ

-

0.5

1.0

1.5

2.0

2.5

LQ

Manufacturing Financial

-

0.5

1.0

1.5

2.0

2.5

3.0

LQ

Construction Financial

-

0.5

1.0

1.5

2.0

2.5

3.0LQ

Trade Financial

-

0.5

1.0

1.5

2.0

2.5

3.0

LQ

Information and… Financial

-

0.5

1.0

1.5

2.0

2.5

3.0

LQ

Agriculture

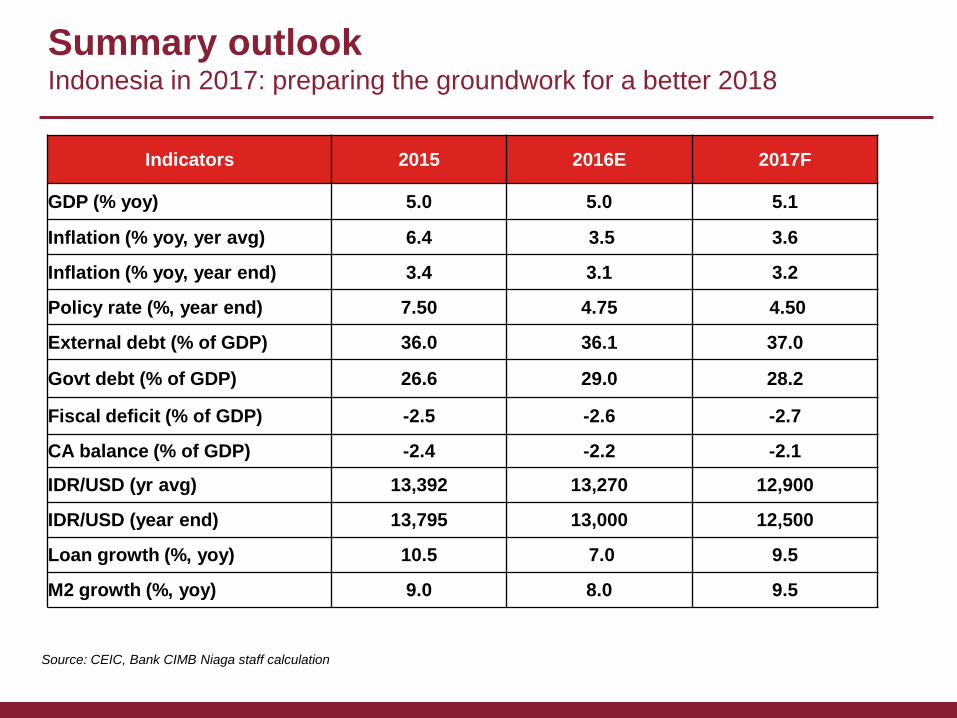

Summary outlook Indonesia in 2017: preparing the groundwork for a better 2018

Indicators 2015 2016E 2017F

GDP (% yoy) 5.0 5.0 5.1

Inflation (% yoy, yer avg) 6.4 3.5 3.6

Inflation (% yoy, year end) 3.4 3.1 3.2

Policy rate (%, year end) 7.50 4.75 4.50

External debt (% of GDP) 36.0 36.1 37.0

Govt debt (% of GDP) 26.6 29.0 28.2

Fiscal deficit (% of GDP) -2.5 -2.6 -2.7

CA balance (% of GDP) -2.4 -2.2 -2.1

IDR/USD (yr avg) 13,392 13,270 12,900

IDR/USD (year end) 13,795 13,000 12,500

Loan growth (%, yoy) 10.5 7.0 9.5

M2 growth (%, yoy) 9.0 8.0 9.5

Source: CEIC, Bank CIMB Niaga staff calculation