Embed Size (px)

Citation preview

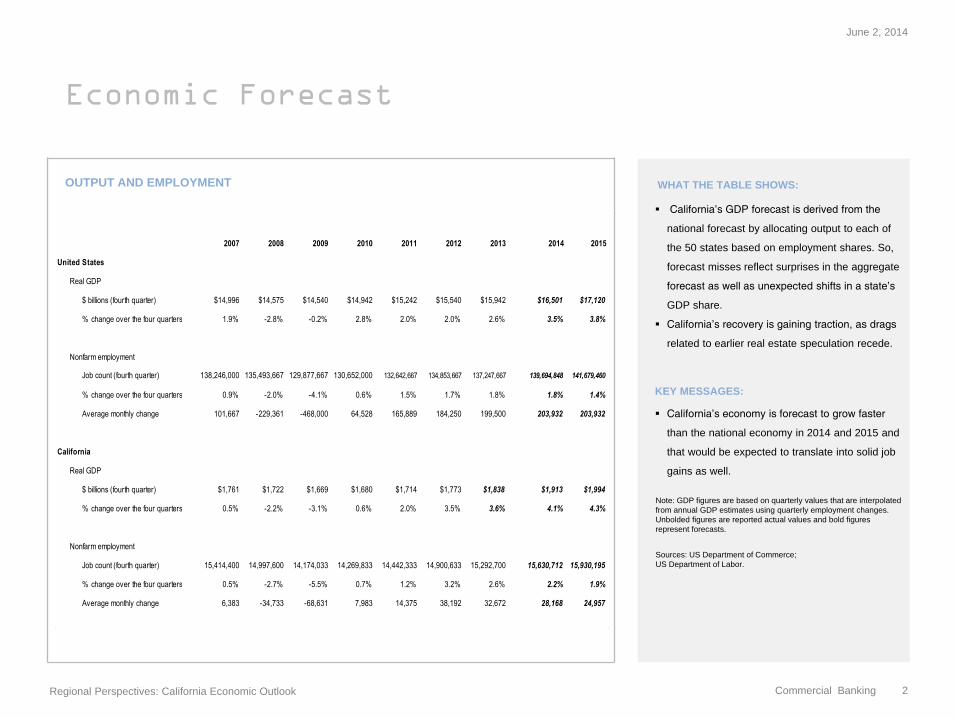

Economic Forecast

OUTPUT AND EMPLOYMENT WHAT THE TABLE SHOWS:

California’s GDP forecast is derived from the

national forecast by allocating output to each of

the 50 states based on employment shares. So,

forecast misses reflect surprises in the aggregate

forecast as well as unexpected shifts in a state’s

GDP share.

California’s recovery is gaining traction, as drags

related to earlier real estate speculation recede.

KEY MESSAGES:

California’s economy is forecast to grow faster

than the national economy in 2014 and 2015 and

that would be expected to translate into solid job

gains as well.

Note: GDP figures are based on quarterly values that are interpolated

from annual GDP estimates using quarterly employment changes.

Unbolded figures are reported actual values and bold figures

represent forecasts.

Sources: US Department of Commerce;

US Department of Labor.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 2

2007 2008 2009 2010 2011 2012 2013 2014 2015

United States

Real GDP

$ billions (fourth quarter) $14,996 $14,575 $14,540 $14,942 $15,242 $15,540 $15,942 $16,501 $17,120

% change over the four quarters 1.9% -2.8% -0.2% 2.8% 2.0% 2.0% 2.6% 3.5% 3.8%

Nonfarm employment

Job count (fourth quarter) 138,246,000 135,493,667 129,877,667 130,652,000 132,642,667 134,853,667 137,247,667 139,694,848 141,679,460

% change over the four quarters 0.9% -2.0% -4.1% 0.6% 1.5% 1.7% 1.8% 1.8% 1.4%

Average monthly change 101,667 -229,361 -468,000 64,528 165,889 184,250 199,500 203,932 203,932

California

Real GDP

$ billions (fourth quarter) $1,761 $1,722 $1,669 $1,680 $1,714 $1,773 $1,838 $1,913 $1,994

% change over the four quarters 0.5% -2.2% -3.1% 0.6% 2.0% 3.5% 3.6% 4.1% 4.3%

Nonfarm employment

Job count (fourth quarter) 15,414,400 14,997,600 14,174,033 14,269,833 14,442,333 14,900,633 15,292,700 15,630,712 15,930,195

% change over the four quarters 0.5% -2.7% -5.5% 0.7% 1.2% 3.2% 2.6% 2.2% 1.9%

Average monthly change 6,383 -34,733 -68,631 7,983 14,375 38,192 32,672 28,168 24,957

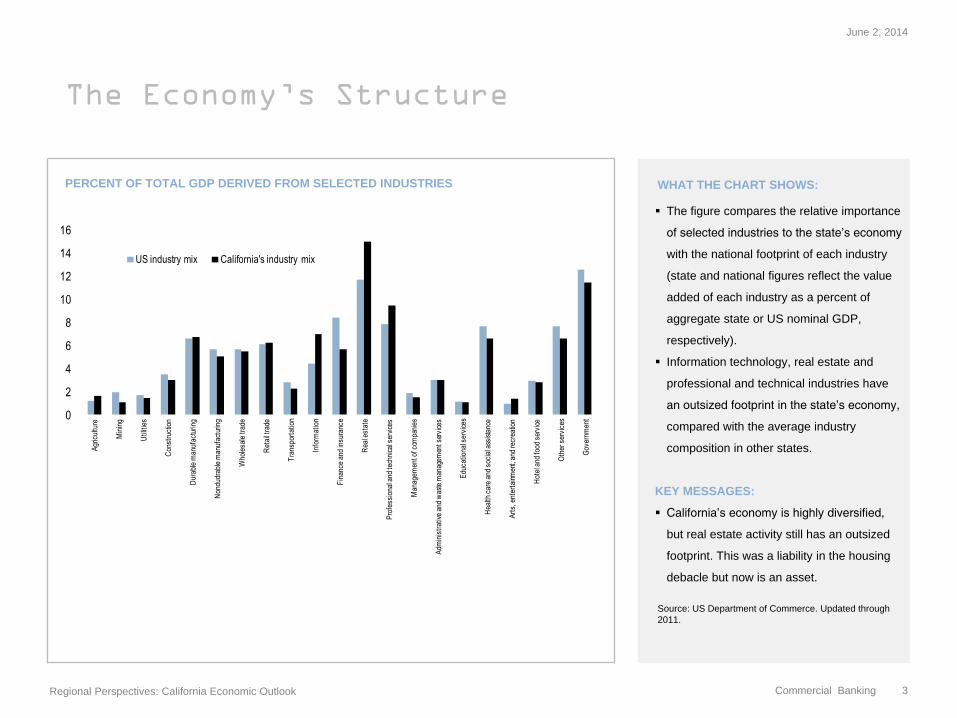

The Economy’s Structure

PERCENT OF TOTAL GDP DERIVED FROM SELECTED INDUSTRIES WHAT THE CHART SHOWS:

The figure compares the relative importance

of selected industries to the state’s economy

with the national footprint of each industry

(state and national figures reflect the value

added of each industry as a percent of

aggregate state or US nominal GDP,

respectively).

Information technology, real estate and

professional and technical industries have

an outsized footprint in the state’s economy,

compared with the average industry

composition in other states.

KEY MESSAGES:

California’s economy is highly diversified,

but real estate activity still has an outsized

footprint. This was a liability in the housing

debacle but now is an asset.

Source: US Department of Commerce. Updated through

2011.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 3

0

2

4

6

8

10

12

14

16

Agr

icul

ture

Min

ing

Util

ities

Con

stru

ctio

n

Dur

able

man

ufac

turin

g

Non

dudr

able

man

ufac

turin

g

Who

lesa

le tr

ade

Ret

ail t

rade

Tra

nspo

rtat

ion

Info

rmat

ion

Fin

ance

and

insu

ranc

e

Rea

l est

ate

Pro

fess

iona

l and

tech

nica

l ser

vice

s

Man

agem

ent o

f com

pani

es

Adm

inis

trat

ive

and

was

te m

anag

emen

t ser

vice

s

Edu

catio

nal s

ervi

ces

Hea

lth c

are

and

soci

al a

ssis

tanc

e

Art

s, e

nter

tain

men

t, an

d re

crea

tion

Hot

el a

nd fo

od s

ervi

ce

Oth

er s

ervi

ces

Gov

ernm

ent

US industry mix California's industry mix

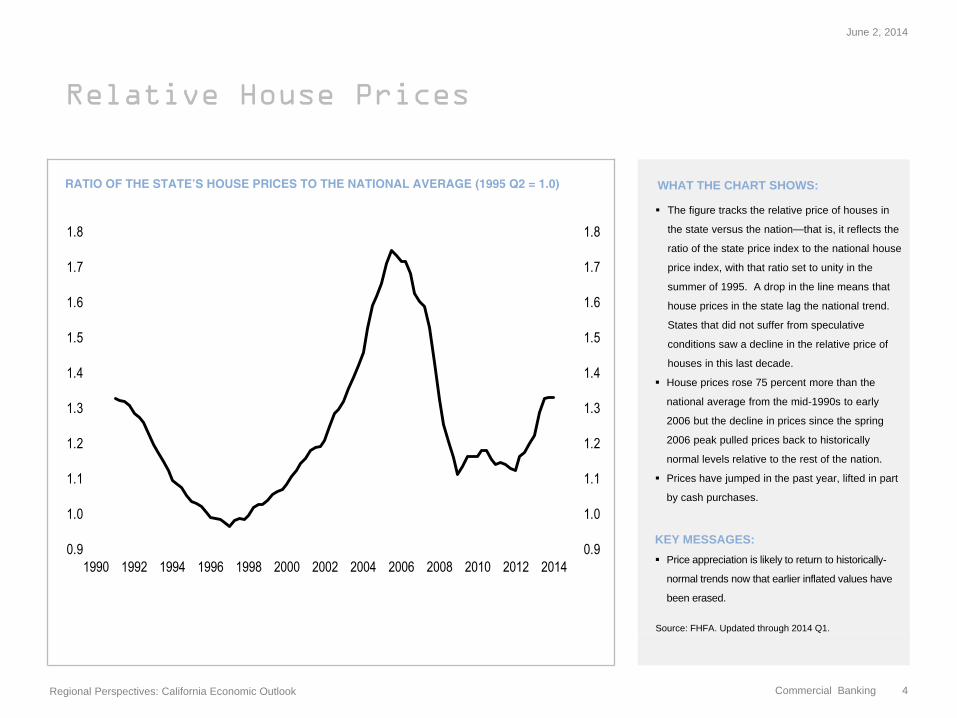

Relative House Prices

RATIO OF THE STATE’S HOUSE PRICES TO THE NATIONAL AVERAGE (1995 Q2 = 1.0) WHAT THE CHART SHOWS:

The figure tracks the relative price of houses in

the state versus the nation—that is, it reflects the

ratio of the state price index to the national house

price index, with that ratio set to unity in the

summer of 1995. A drop in the line means that

house prices in the state lag the national trend.

States that did not suffer from speculative

conditions saw a decline in the relative price of

houses in this last decade.

House prices rose 75 percent more than the

national average from the mid-1990s to early

2006 but the decline in prices since the spring

2006 peak pulled prices back to historically

normal levels relative to the rest of the nation.

Prices have jumped in the past year, lifted in part

by cash purchases.

KEY MESSAGES:

Price appreciation is likely to return to historically-

normal trends now that earlier inflated values have

been erased.

Source: FHFA. Updated through 2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 4

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

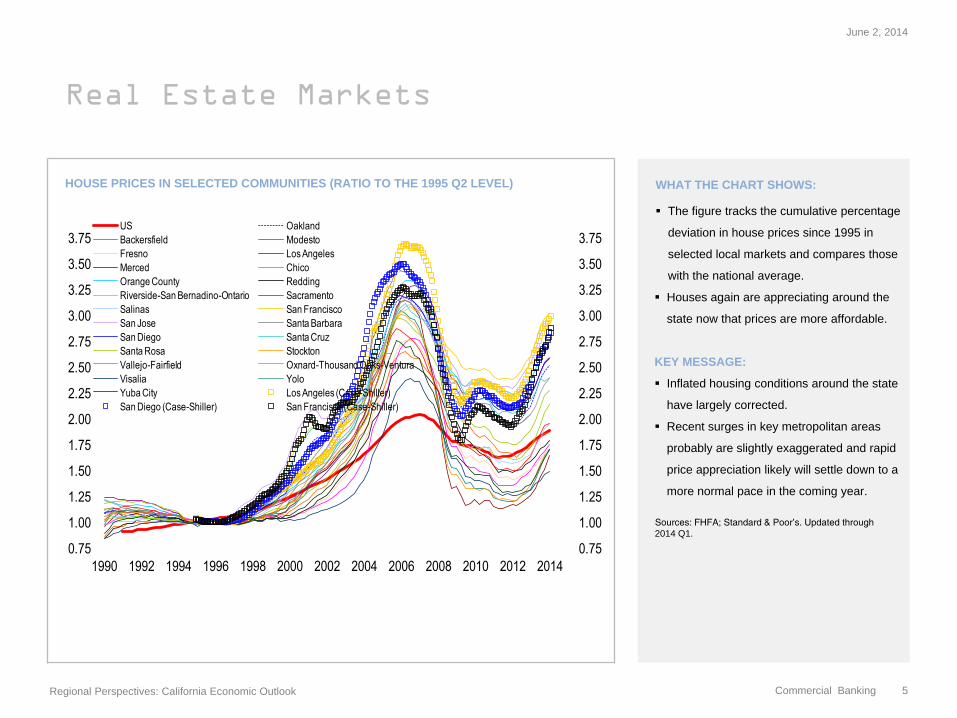

Real Estate Markets

HOUSE PRICES IN SELECTED COMMUNITIES (RATIO TO THE 1995 Q2 LEVEL) WHAT THE CHART SHOWS:

The figure tracks the cumulative percentage

deviation in house prices since 1995 in

selected local markets and compares those

with the national average.

Houses again are appreciating around the

state now that prices are more affordable.

KEY MESSAGE:

Inflated housing conditions around the state

have largely corrected.

Recent surges in key metropolitan areas

probably are slightly exaggerated and rapid

price appreciation likely will settle down to a

more normal pace in the coming year.

Sources: FHFA; Standard & Poor’s. Updated through

2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 5

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

US Oakland

Backersfield Modesto

Fresno Los Angeles

Merced Chico

Orange County Redding

Riverside-San Bernadino-Ontario Sacramento

Salinas San Francisco

San Jose Santa Barbara

San Diego Santa Cruz

Santa Rosa Stockton

Vallejo-Fairfield Oxnard-Thousand Oaks-Ventura

Visalia Yolo

Yuba City Los Angeles (Case-Shiller)

San Diego (Case-Shiller) San Francisco (Case-Shiller)

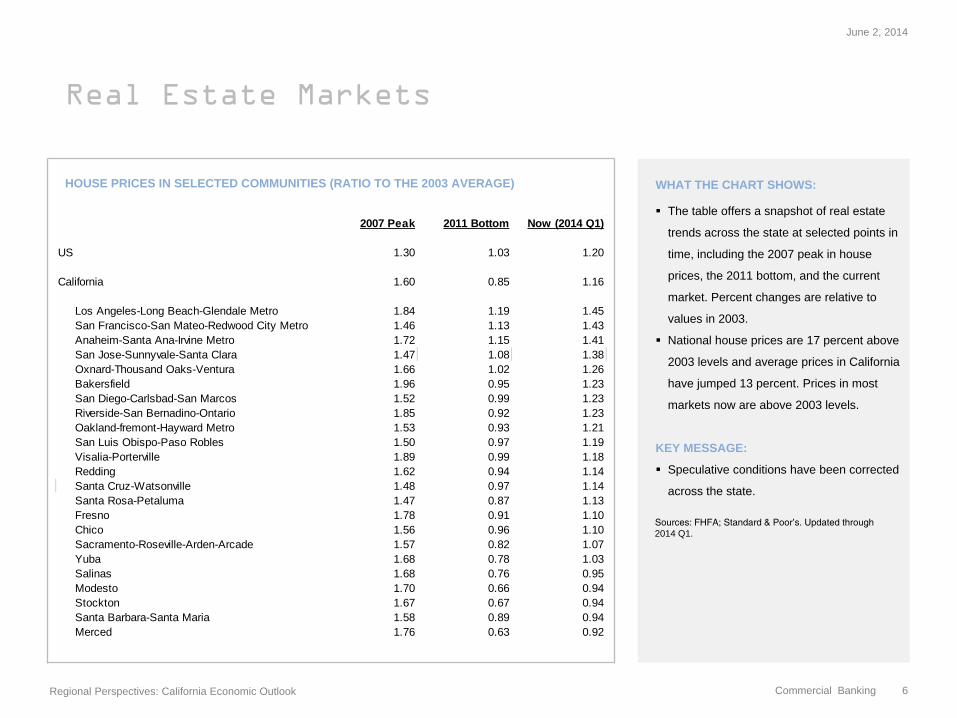

Real Estate Markets

HOUSE PRICES IN SELECTED COMMUNITIES (RATIO TO THE 2003 AVERAGE) WHAT THE CHART SHOWS:

The table offers a snapshot of real estate

trends across the state at selected points in

time, including the 2007 peak in house

prices, the 2011 bottom, and the current

market. Percent changes are relative to

values in 2003.

National house prices are 17 percent above

2003 levels and average prices in California

have jumped 13 percent. Prices in most

markets now are above 2003 levels.

KEY MESSAGE:

Speculative conditions have been corrected

across the state.

Sources: FHFA; Standard & Poor’s. Updated through

2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 6

2007 Peak 2011 Bottom Now (2014 Q1)

US 1.30 1.03 1.20

California 1.60 0.85 1.16

Los Angeles-Long Beach-Glendale Metro 1.84 1.19 1.45

San Francisco-San Mateo-Redwood City Metro 1.46 1.13 1.43

Anaheim-Santa Ana-Irvine Metro 1.72 1.15 1.41

San Jose-Sunnyvale-Santa Clara 1.47 1.08 1.38

Oxnard-Thousand Oaks-Ventura 1.66 1.02 1.26

Bakersfield 1.96 0.95 1.23

San Diego-Carlsbad-San Marcos 1.52 0.99 1.23

Riverside-San Bernadino-Ontario 1.85 0.92 1.23

Oakland-fremont-Hayward Metro 1.53 0.93 1.21

San Luis Obispo-Paso Robles 1.50 0.97 1.19

Visalia-Porterville 1.89 0.99 1.18

Redding 1.62 0.94 1.14

Santa Cruz-Watsonville 1.48 0.97 1.14

Santa Rosa-Petaluma 1.47 0.87 1.13

Fresno 1.78 0.91 1.10

Chico 1.56 0.96 1.10

Sacramento-Roseville-Arden-Arcade 1.57 0.82 1.07

Yuba 1.68 0.78 1.03

Salinas 1.68 0.76 0.95

Modesto 1.70 0.66 0.94

Stockton 1.67 0.67 0.94

Santa Barbara-Santa Maria 1.58 0.89 0.94

Merced 1.76 0.63 0.92

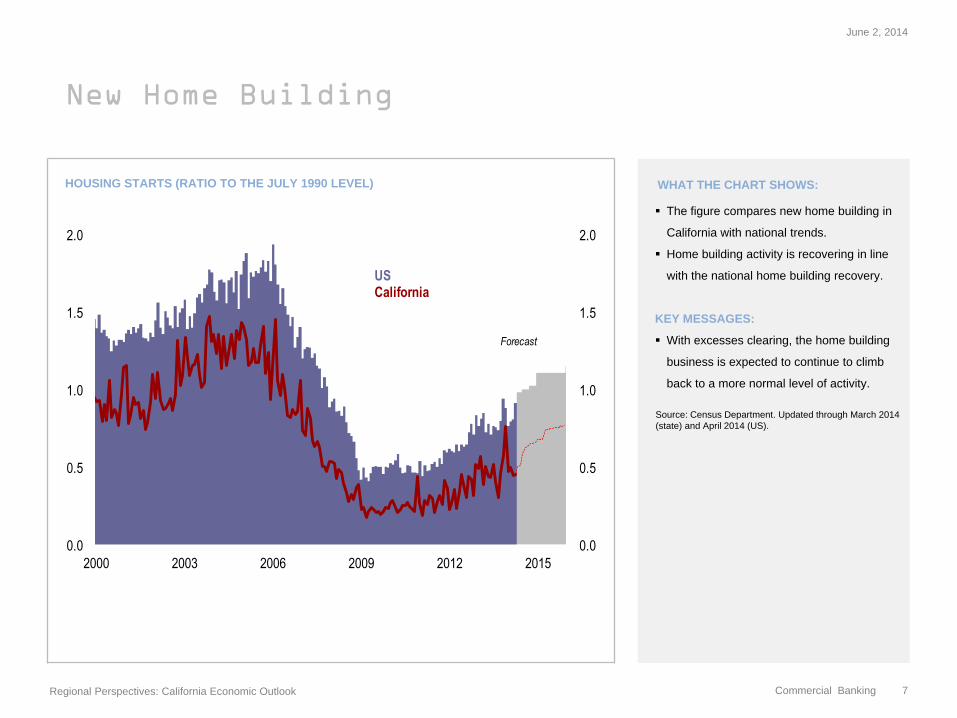

New Home Building

HOUSING STARTS (RATIO TO THE JULY 1990 LEVEL) WHAT THE CHART SHOWS:

The figure compares new home building in

California with national trends.

Home building activity is recovering in line

with the national home building recovery.

KEY MESSAGES:

With excesses clearing, the home building

business is expected to continue to climb

back to a more normal level of activity.

Source: Census Department. Updated through March 2014

(state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 7

0.0

0.5

1.0

1.5

2.0

0.0

0.5

1.0

1.5

2.0

2000 2003 2006 2009 2012 2015

USCalifornia

Forecast

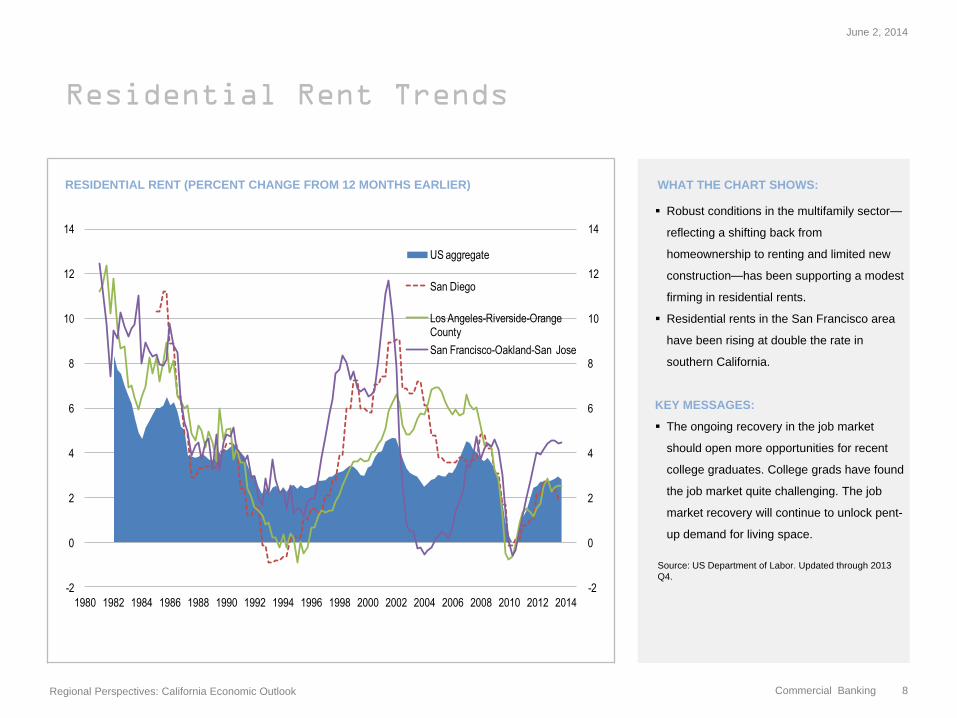

Residential Rent Trends

RESIDENTIAL RENT (PERCENT CHANGE FROM 12 MONTHS EARLIER) WHAT THE CHART SHOWS:

Robust conditions in the multifamily sector—

reflecting a shifting back from

homeownership to renting and limited new

construction—has been supporting a modest

firming in residential rents.

Residential rents in the San Francisco area

have been rising at double the rate in

southern California.

KEY MESSAGES:

The ongoing recovery in the job market

should open more opportunities for recent

college graduates. College grads have found

the job market quite challenging. The job

market recovery will continue to unlock pent-

up demand for living space.

Source: US Department of Labor. Updated through 2013

Q4.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 8

-2

0

2

4

6

8

10

12

14

-2

0

2

4

6

8

10

12

14

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

US aggregate

San Diego

Los Angeles-Riverside-Orange County

San Francisco-Oakland-San Jose

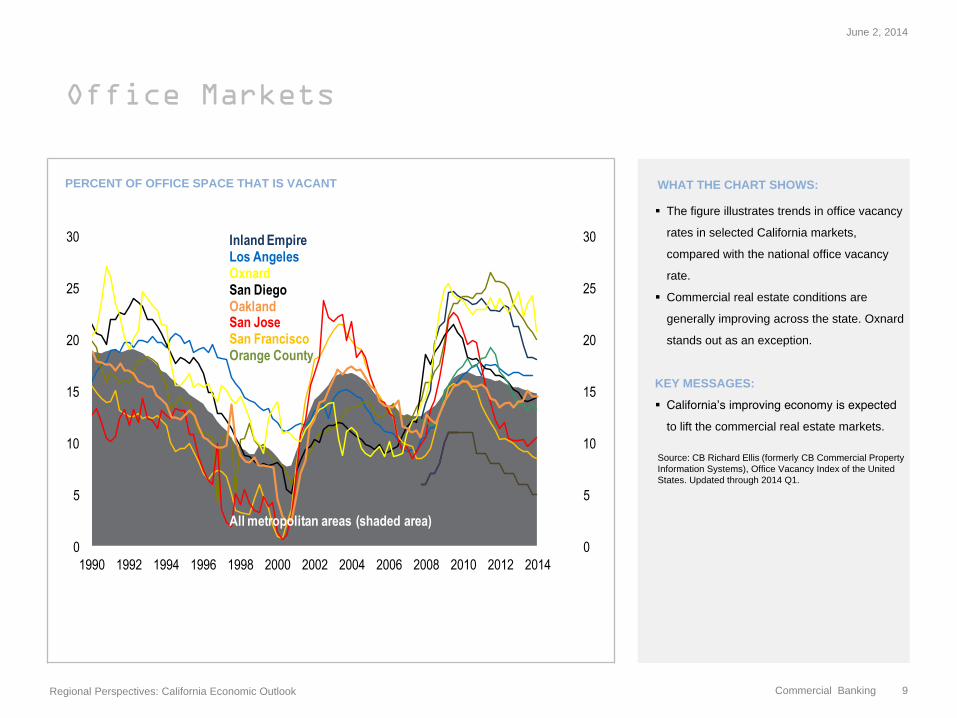

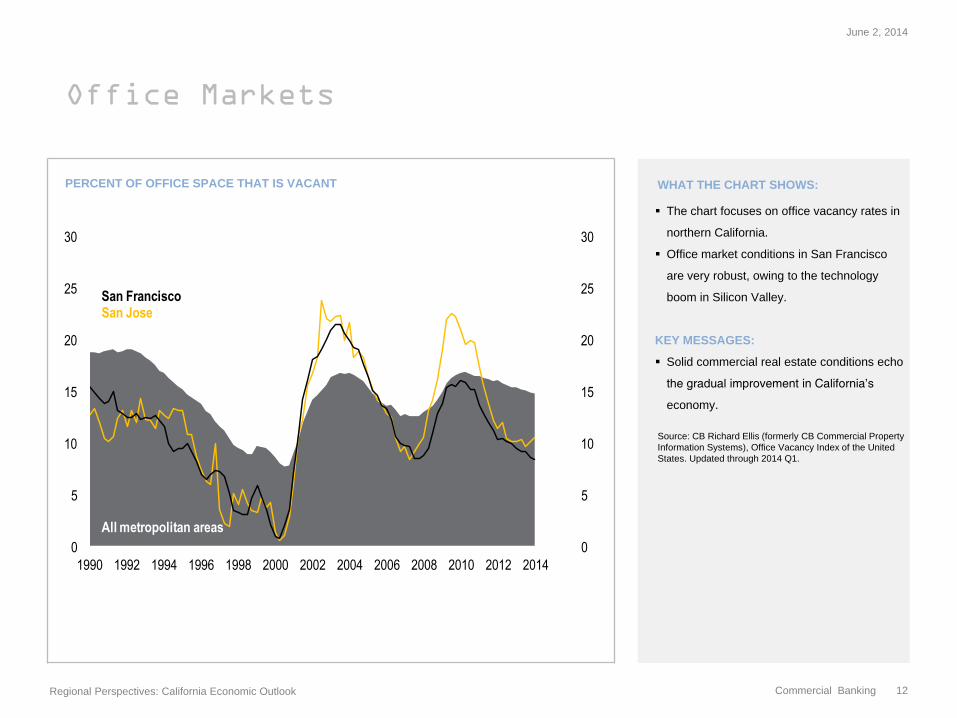

Office Markets

PERCENT OF OFFICE SPACE THAT IS VACANT WHAT THE CHART SHOWS:

The figure illustrates trends in office vacancy

rates in selected California markets,

compared with the national office vacancy

rate.

Commercial real estate conditions are

generally improving across the state. Oxnard

stands out as an exception.

KEY MESSAGES:

California’s improving economy is expected

to lift the commercial real estate markets.

Source: CB Richard Ellis (formerly CB Commercial Property

Information Systems), Office Vacancy Index of the United

States. Updated through 2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 9

0

5

10

15

20

25

30

0

5

10

15

20

25

30

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Inland EmpireLos AngelesOxnardSan DiegoOaklandSan JoseSan FranciscoOrange County

All metropolitan areas (shaded area)

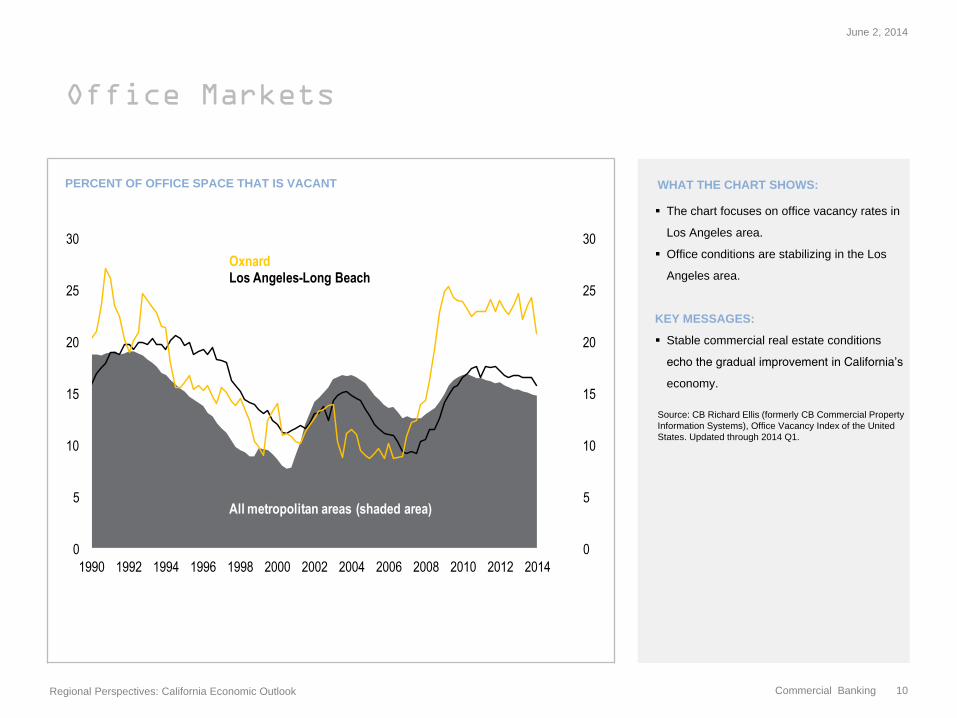

Office Markets

PERCENT OF OFFICE SPACE THAT IS VACANT WHAT THE CHART SHOWS:

The chart focuses on office vacancy rates in

Los Angeles area.

Office conditions are stabilizing in the Los

Angeles area.

KEY MESSAGES:

Stable commercial real estate conditions

echo the gradual improvement in California’s

economy.

Source: CB Richard Ellis (formerly CB Commercial Property

Information Systems), Office Vacancy Index of the United

States. Updated through 2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 10

0

5

10

15

20

25

30

0

5

10

15

20

25

30

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

OxnardLos Angeles-Long Beach

All metropolitan areas (shaded area)

Office Markets

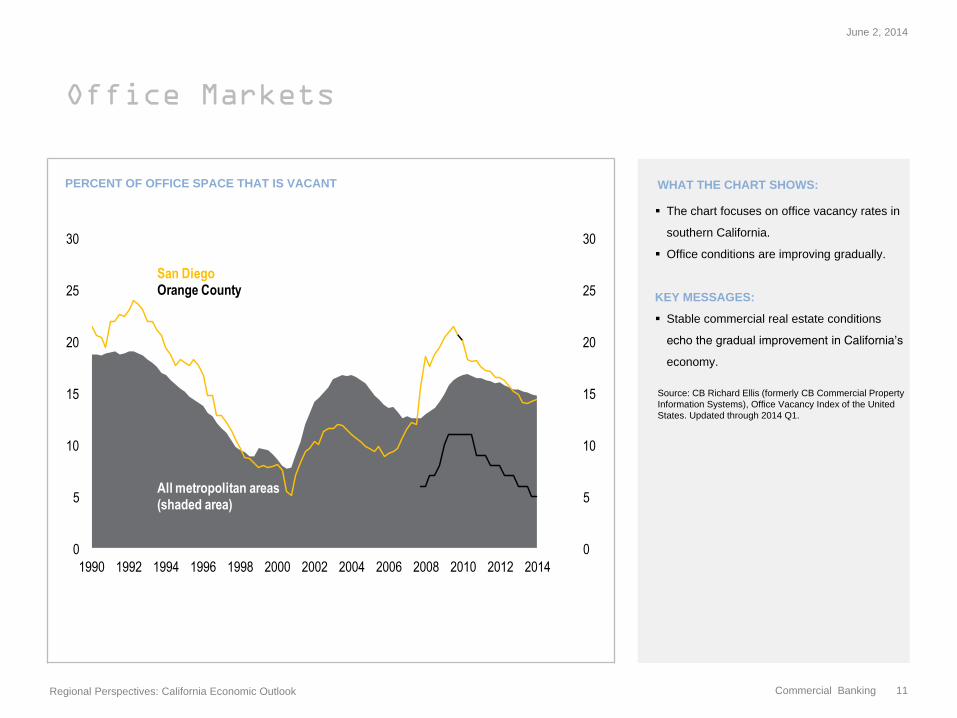

PERCENT OF OFFICE SPACE THAT IS VACANT WHAT THE CHART SHOWS:

The chart focuses on office vacancy rates in

southern California.

Office conditions are improving gradually.

KEY MESSAGES:

Stable commercial real estate conditions

echo the gradual improvement in California’s

economy.

Source: CB Richard Ellis (formerly CB Commercial Property

Information Systems), Office Vacancy Index of the United

States. Updated through 2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 11

0

5

10

15

20

25

30

0

5

10

15

20

25

30

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

San DiegoOrange County

All metropolitan areas (shaded area)

Office Markets

PERCENT OF OFFICE SPACE THAT IS VACANT WHAT THE CHART SHOWS:

The chart focuses on office vacancy rates in

northern California.

Office market conditions in San Francisco

are very robust, owing to the technology

boom in Silicon Valley.

KEY MESSAGES:

Solid commercial real estate conditions echo

the gradual improvement in California’s

economy.

Source: CB Richard Ellis (formerly CB Commercial Property

Information Systems), Office Vacancy Index of the United

States. Updated through 2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 12

0

5

10

15

20

25

30

0

5

10

15

20

25

30

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

San FranciscoSan Jose

All metropolitan areas

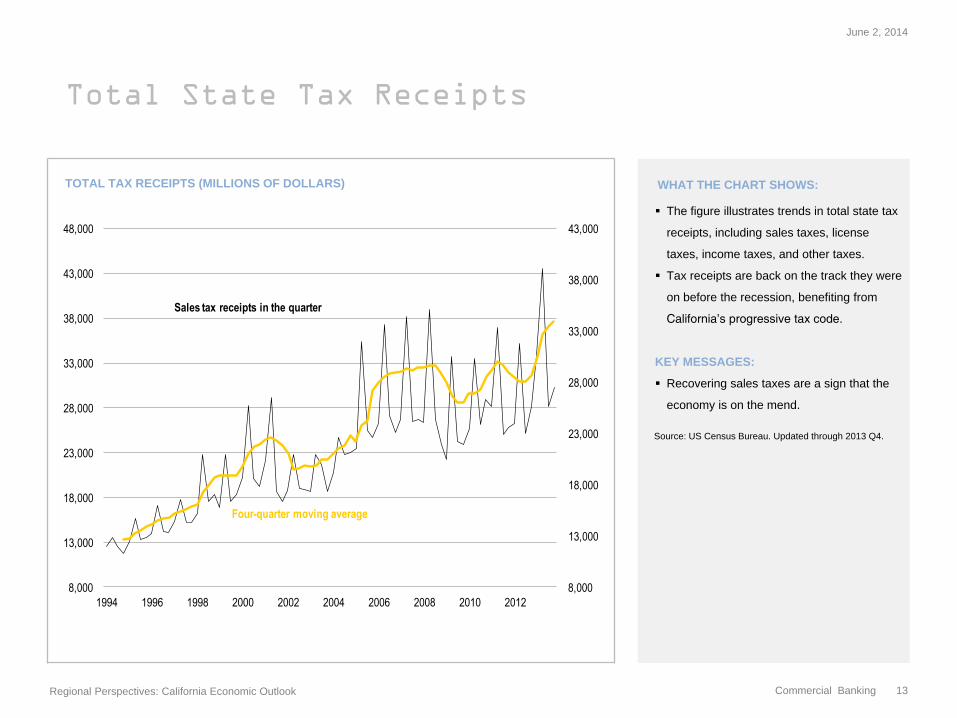

Total State Tax Receipts

TOTAL TAX RECEIPTS (MILLIONS OF DOLLARS) WHAT THE CHART SHOWS:

The figure illustrates trends in total state tax

receipts, including sales taxes, license

taxes, income taxes, and other taxes.

Tax receipts are back on the track they were

on before the recession, benefiting from

California’s progressive tax code.

KEY MESSAGES:

Recovering sales taxes are a sign that the

economy is on the mend.

Source: US Census Bureau. Updated through 2013 Q4.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 13

8,000

13,000

18,000

23,000

28,000

33,000

38,000

43,000

8,000

13,000

18,000

23,000

28,000

33,000

38,000

43,000

48,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Sales tax receipts in the quarter

Four-quarter moving average

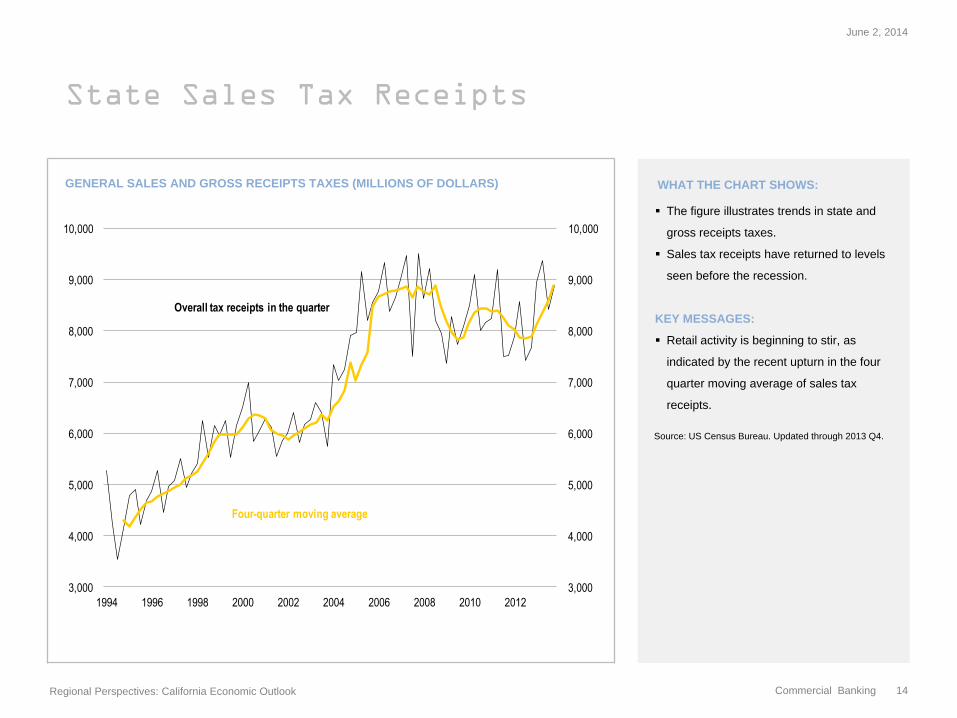

State Sales Tax Receipts

GENERAL SALES AND GROSS RECEIPTS TAXES (MILLIONS OF DOLLARS) WHAT THE CHART SHOWS:

The figure illustrates trends in state and

gross receipts taxes.

Sales tax receipts have returned to levels

seen before the recession.

KEY MESSAGES:

Retail activity is beginning to stir, as

indicated by the recent upturn in the four

quarter moving average of sales tax

receipts.

Source: US Census Bureau. Updated through 2013 Q4.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 14

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Overall tax receipts in the quarter

Four-quarter moving average

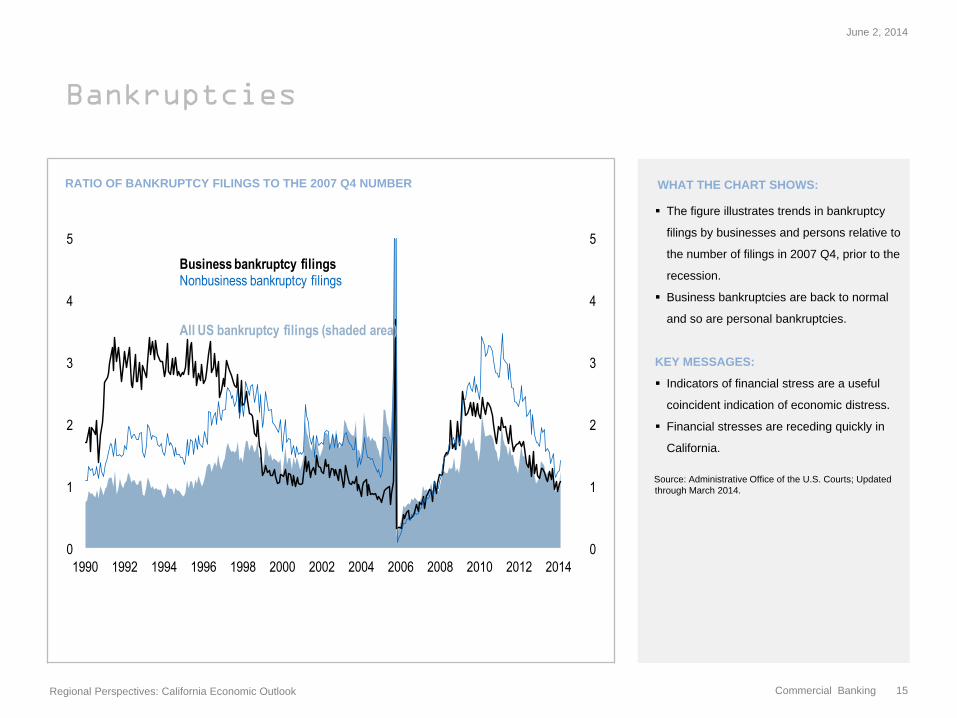

Bankruptcies

RATIO OF BANKRUPTCY FILINGS TO THE 2007 Q4 NUMBER WHAT THE CHART SHOWS:

The figure illustrates trends in bankruptcy

filings by businesses and persons relative to

the number of filings in 2007 Q4, prior to the

recession.

Business bankruptcies are back to normal

and so are personal bankruptcies.

KEY MESSAGES:

Indicators of financial stress are a useful

coincident indication of economic distress.

Financial stresses are receding quickly in

California.

Source: Administrative Office of the U.S. Courts; Updated

through March 2014.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 15

0

1

2

3

4

5

0

1

2

3

4

5

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Business bankruptcy filingsNonbusiness bankruptcy filings

All US bankruptcy filings (shaded area)

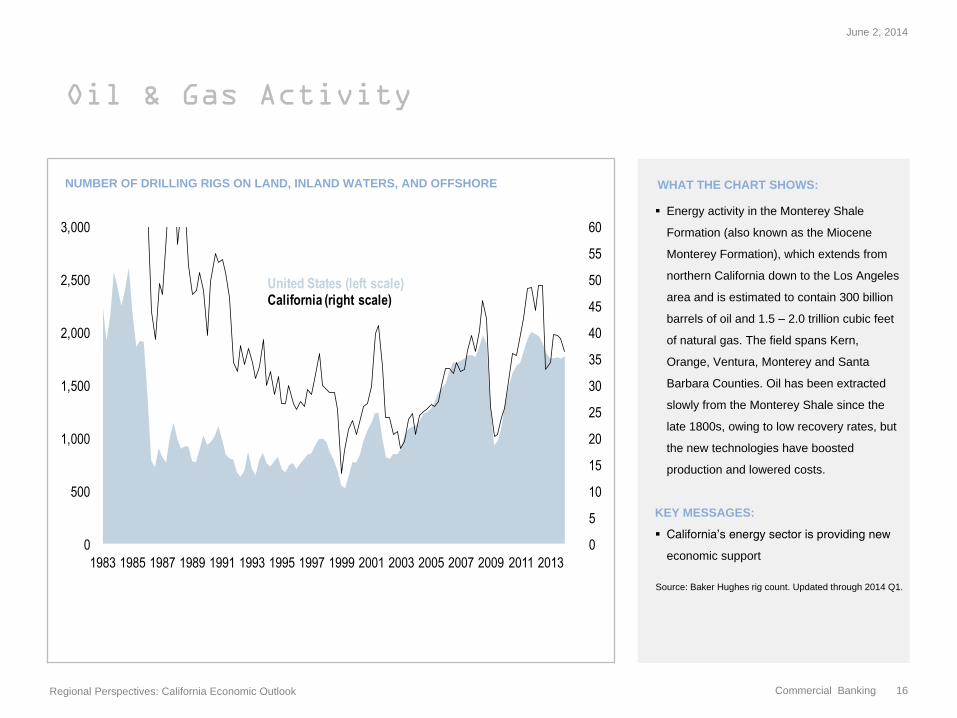

Oil & Gas Activity

NUMBER OF DRILLING RIGS ON LAND, INLAND WATERS, AND OFFSHORE WHAT THE CHART SHOWS:

Energy activity in the Monterey Shale

Formation (also known as the Miocene

Monterey Formation), which extends from

northern California down to the Los Angeles

area and is estimated to contain 300 billion

barrels of oil and 1.5 – 2.0 trillion cubic feet

of natural gas. The field spans Kern,

Orange, Ventura, Monterey and Santa

Barbara Counties. Oil has been extracted

slowly from the Monterey Shale since the

late 1800s, owing to low recovery rates, but

the new technologies have boosted

production and lowered costs.

KEY MESSAGES:

California’s energy sector is providing new

economic support

Source: Baker Hughes rig count. Updated through 2014 Q1.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 16

0

5

10

15

20

25

30

35

40

45

50

55

60

0

500

1,000

1,500

2,000

2,500

3,000

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

United States (left scale)California (right scale)

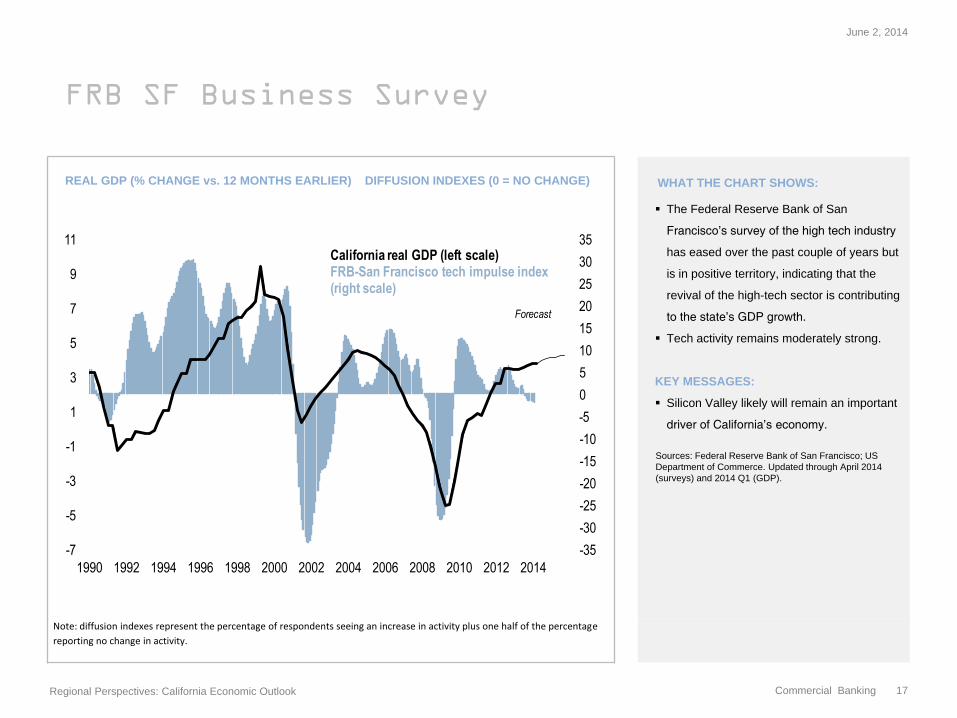

FRB SF Business Survey

REAL GDP (% CHANGE vs. 12 MONTHS EARLIER) DIFFUSION INDEXES (0 = NO CHANGE) WHAT THE CHART SHOWS:

The Federal Reserve Bank of San

Francisco’s survey of the high tech industry

has eased over the past couple of years but

is in positive territory, indicating that the

revival of the high-tech sector is contributing

to the state’s GDP growth.

Tech activity remains moderately strong.

KEY MESSAGES:

Silicon Valley likely will remain an important

driver of California’s economy.

Sources: Federal Reserve Bank of San Francisco; US

Department of Commerce. Updated through April 2014

(surveys) and 2014 Q1 (GDP).

Note: diffusion indexes represent the percentage of respondents seeing an increase in activity plus one half of the percentage

reporting no change in activity.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 17

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

-7

-5

-3

-1

1

3

5

7

9

11

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

California real GDP (left scale)FRB-San Francisco tech impulse index (right scale)

Forecast

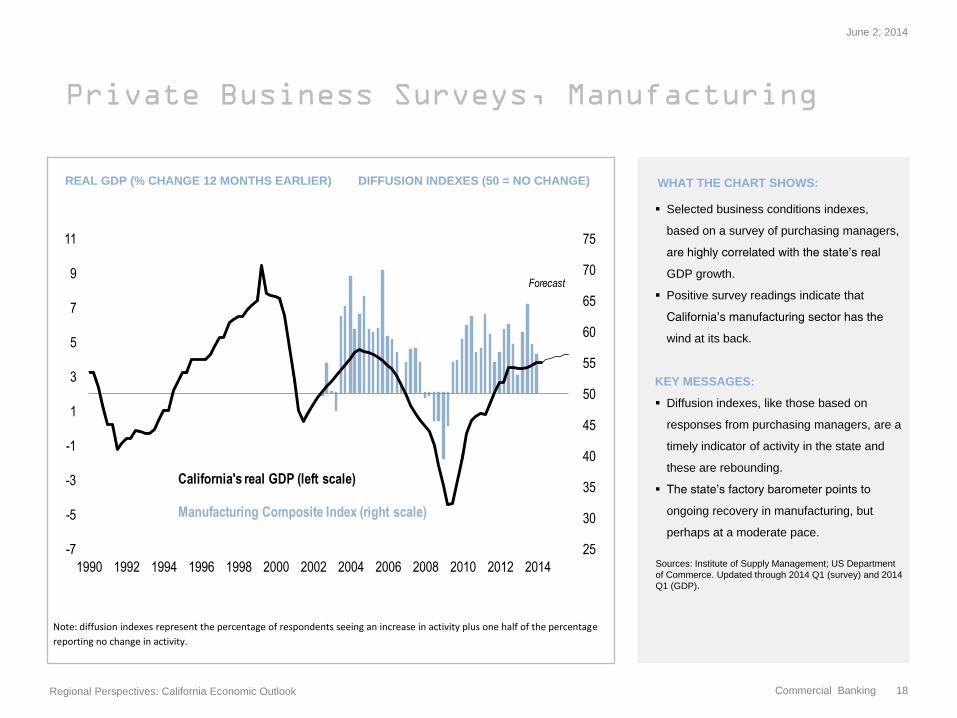

Private Business Surveys, Manufacturing

REAL GDP (% CHANGE 12 MONTHS EARLIER) DIFFUSION INDEXES (50 = NO CHANGE) WHAT THE CHART SHOWS:

Selected business conditions indexes,

based on a survey of purchasing managers,

are highly correlated with the state’s real

GDP growth.

Positive survey readings indicate that

California’s manufacturing sector has the

wind at its back.

KEY MESSAGES:

Diffusion indexes, like those based on

responses from purchasing managers, are a

timely indicator of activity in the state and

these are rebounding.

The state’s factory barometer points to

ongoing recovery in manufacturing, but

perhaps at a moderate pace.

Sources: Institute of Supply Management; US Department

of Commerce. Updated through 2014 Q1 (survey) and 2014

Q1 (GDP).

Note: diffusion indexes represent the percentage of respondents seeing an increase in activity plus one half of the percentage

reporting no change in activity.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 18

25

30

35

40

45

50

55

60

65

70

75

-7

-5

-3

-1

1

3

5

7

9

11

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

California's real GDP (left scale)

Manufacturing Composite Index (right scale)

Forecast

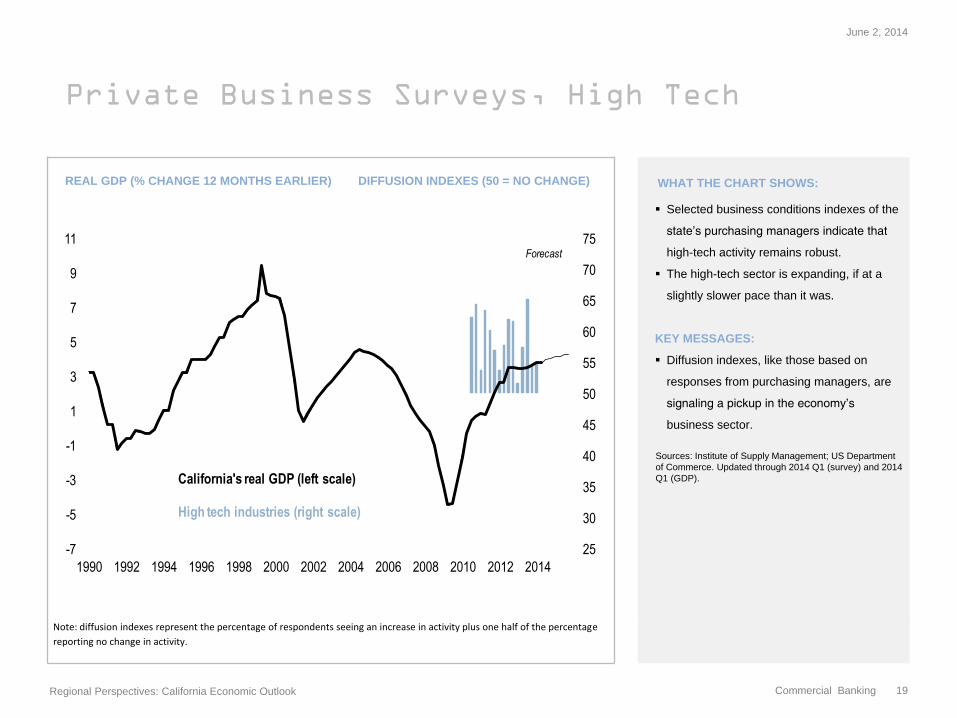

Private Business Surveys, High Tech

REAL GDP (% CHANGE 12 MONTHS EARLIER) DIFFUSION INDEXES (50 = NO CHANGE) WHAT THE CHART SHOWS:

Selected business conditions indexes of the

state’s purchasing managers indicate that

high-tech activity remains robust.

The high-tech sector is expanding, if at a

slightly slower pace than it was.

KEY MESSAGES:

Diffusion indexes, like those based on

responses from purchasing managers, are

signaling a pickup in the economy’s

business sector.

Sources: Institute of Supply Management; US Department

of Commerce. Updated through 2014 Q1 (survey) and 2014

Q1 (GDP).

Note: diffusion indexes represent the percentage of respondents seeing an increase in activity plus one half of the percentage

reporting no change in activity.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 19

25

30

35

40

45

50

55

60

65

70

75

-7

-5

-3

-1

1

3

5

7

9

11

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

California's real GDP (left scale)

High tech industries (right scale)

Forecast

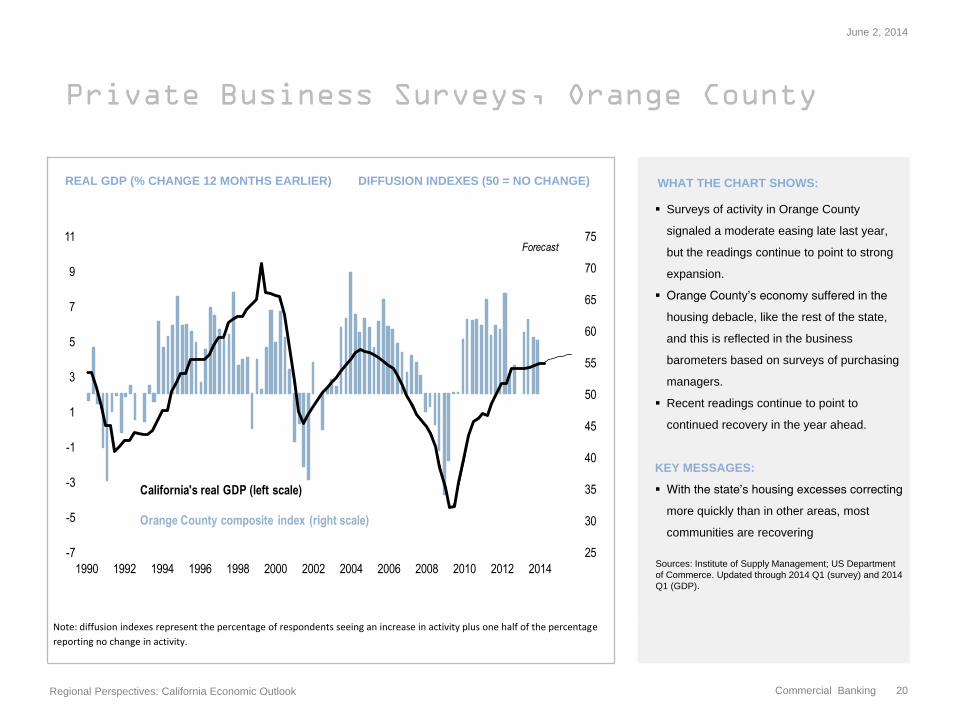

Private Business Surveys, Orange County

REAL GDP (% CHANGE 12 MONTHS EARLIER) DIFFUSION INDEXES (50 = NO CHANGE) WHAT THE CHART SHOWS:

Surveys of activity in Orange County

signaled a moderate easing late last year,

but the readings continue to point to strong

expansion.

Orange County’s economy suffered in the

housing debacle, like the rest of the state,

and this is reflected in the business

barometers based on surveys of purchasing

managers.

Recent readings continue to point to

continued recovery in the year ahead.

KEY MESSAGES:

With the state’s housing excesses correcting

more quickly than in other areas, most

communities are recovering

Sources: Institute of Supply Management; US Department

of Commerce. Updated through 2014 Q1 (survey) and 2014

Q1 (GDP).

Note: diffusion indexes represent the percentage of respondents seeing an increase in activity plus one half of the percentage

reporting no change in activity.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 20

25

30

35

40

45

50

55

60

65

70

75

-7

-5

-3

-1

1

3

5

7

9

11

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

California's real GDP (left scale)

Orange County composite index (right scale)

Forecast

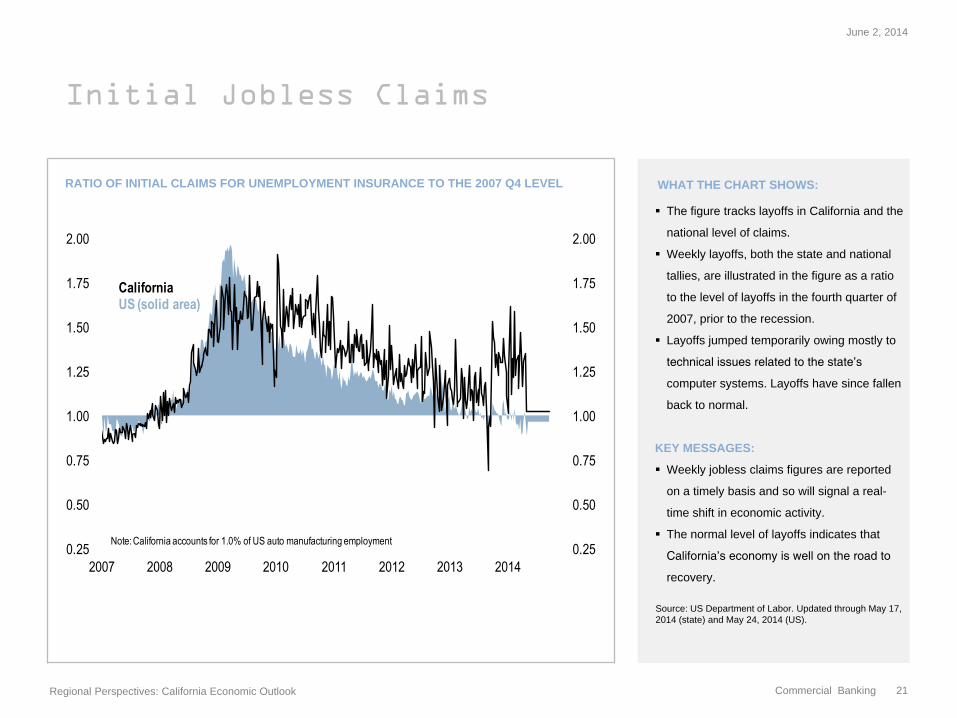

Initial Jobless Claims

RATIO OF INITIAL CLAIMS FOR UNEMPLOYMENT INSURANCE TO THE 2007 Q4 LEVEL WHAT THE CHART SHOWS:

The figure tracks layoffs in California and the

national level of claims.

Weekly layoffs, both the state and national

tallies, are illustrated in the figure as a ratio

to the level of layoffs in the fourth quarter of

2007, prior to the recession.

Layoffs jumped temporarily owing mostly to

technical issues related to the state’s

computer systems. Layoffs have since fallen

back to normal.

KEY MESSAGES:

Weekly jobless claims figures are reported

on a timely basis and so will signal a real-

time shift in economic activity.

The normal level of layoffs indicates that

California’s economy is well on the road to

recovery.

Source: US Department of Labor. Updated through May 17,

2014 (state) and May 24, 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 21

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2007 2008 2009 2010 2011 2012 2013 2014

CaliforniaUS (solid area)

Note: California accounts for 1.0% of US auto manufacturing employment

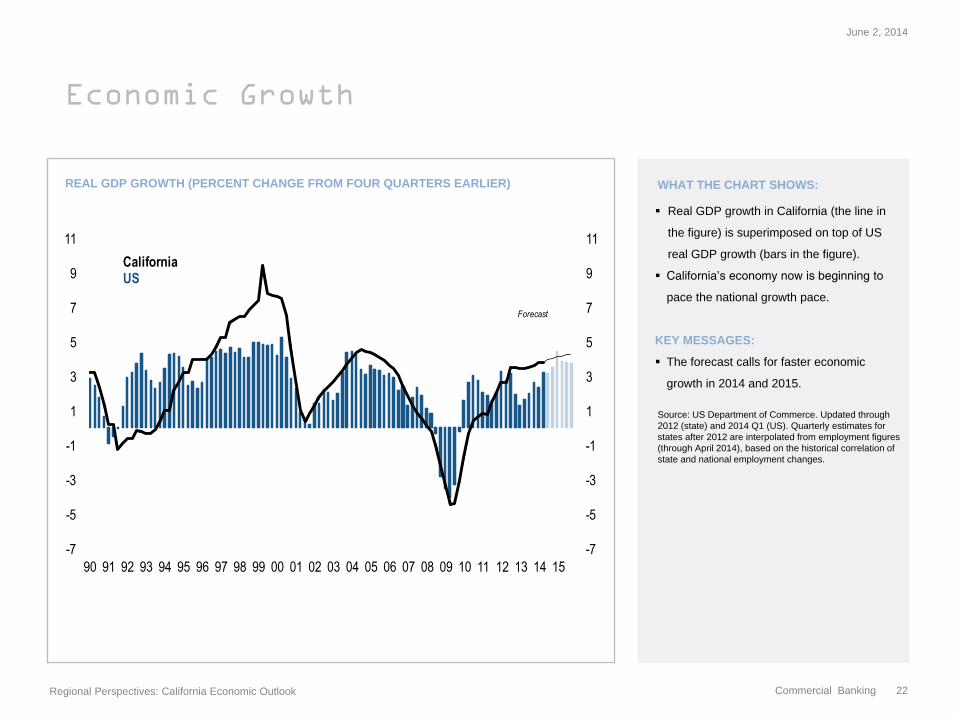

Economic Growth

REAL GDP GROWTH (PERCENT CHANGE FROM FOUR QUARTERS EARLIER) WHAT THE CHART SHOWS:

Real GDP growth in California (the line in

the figure) is superimposed on top of US

real GDP growth (bars in the figure).

California’s economy now is beginning to

pace the national growth pace.

KEY MESSAGES:

The forecast calls for faster economic

growth in 2014 and 2015.

Source: US Department of Commerce. Updated through

2012 (state) and 2014 Q1 (US). Quarterly estimates for

states after 2012 are interpolated from employment figures

(through April 2014), based on the historical correlation of

state and national employment changes.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 22

-7

-5

-3

-1

1

3

5

7

9

11

-7

-5

-3

-1

1

3

5

7

9

11

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

CaliforniaUS

Forecast

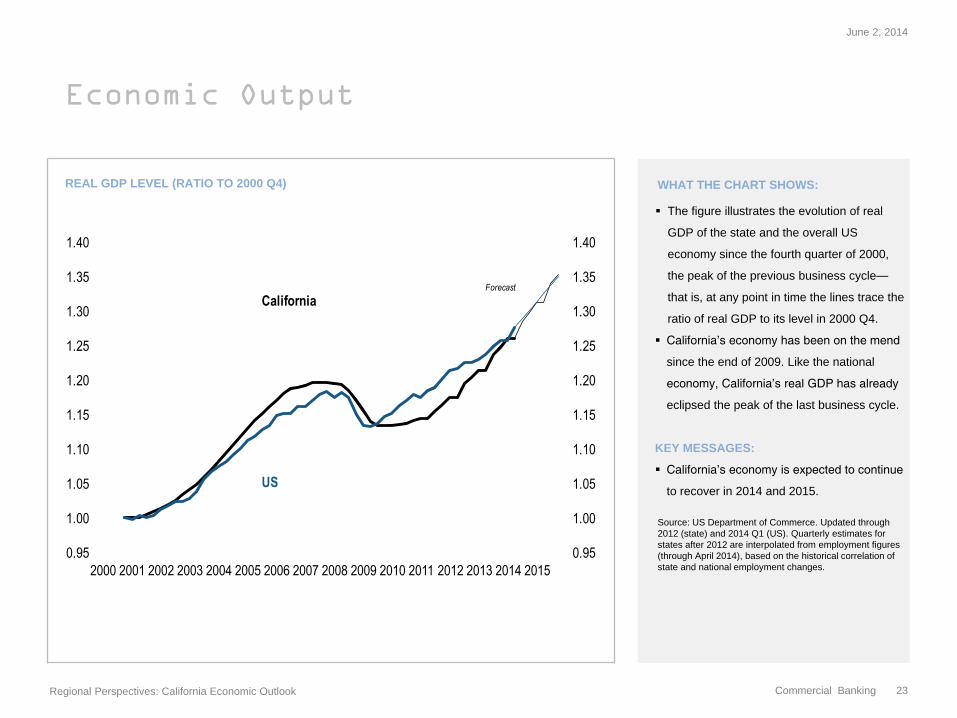

Economic Output

REAL GDP LEVEL (RATIO TO 2000 Q4) WHAT THE CHART SHOWS:

The figure illustrates the evolution of real

GDP of the state and the overall US

economy since the fourth quarter of 2000,

the peak of the previous business cycle—

that is, at any point in time the lines trace the

ratio of real GDP to its level in 2000 Q4.

California’s economy has been on the mend

since the end of 2009. Like the national

economy, California’s real GDP has already

eclipsed the peak of the last business cycle.

KEY MESSAGES:

California’s economy is expected to continue

to recover in 2014 and 2015.

Source: US Department of Commerce. Updated through

2012 (state) and 2014 Q1 (US). Quarterly estimates for

states after 2012 are interpolated from employment figures

(through April 2014), based on the historical correlation of

state and national employment changes.

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 23

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

California

US

Forecast

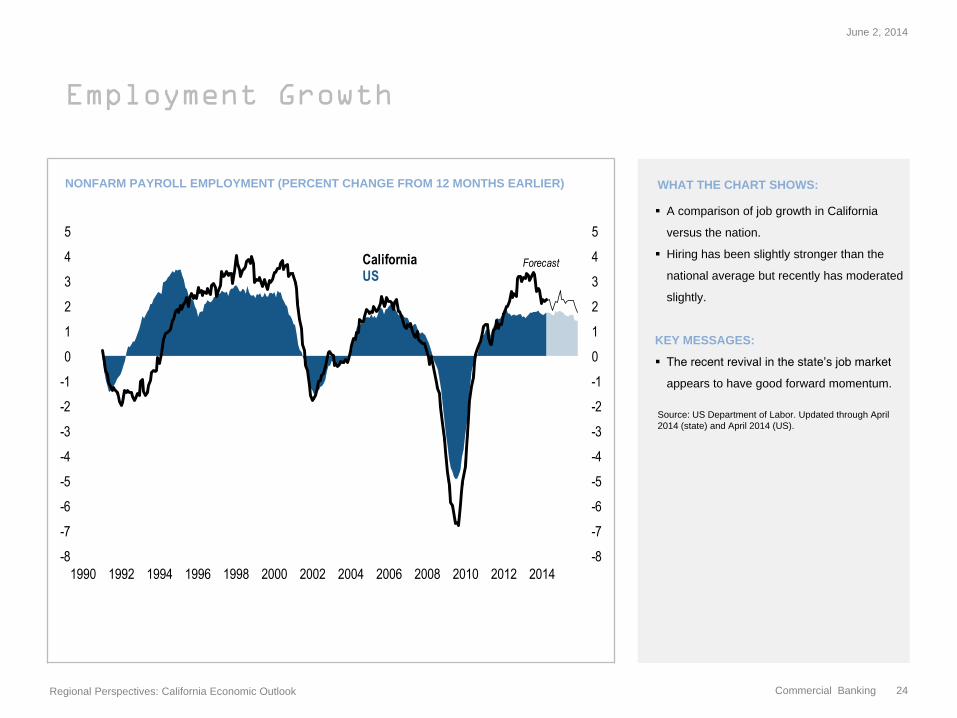

Employment Growth

NONFARM PAYROLL EMPLOYMENT (PERCENT CHANGE FROM 12 MONTHS EARLIER) WHAT THE CHART SHOWS:

A comparison of job growth in California

versus the nation.

Hiring has been slightly stronger than the

national average but recently has moderated

slightly.

KEY MESSAGES:

The recent revival in the state’s job market

appears to have good forward momentum.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 24

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

CaliforniaUS

Forecast

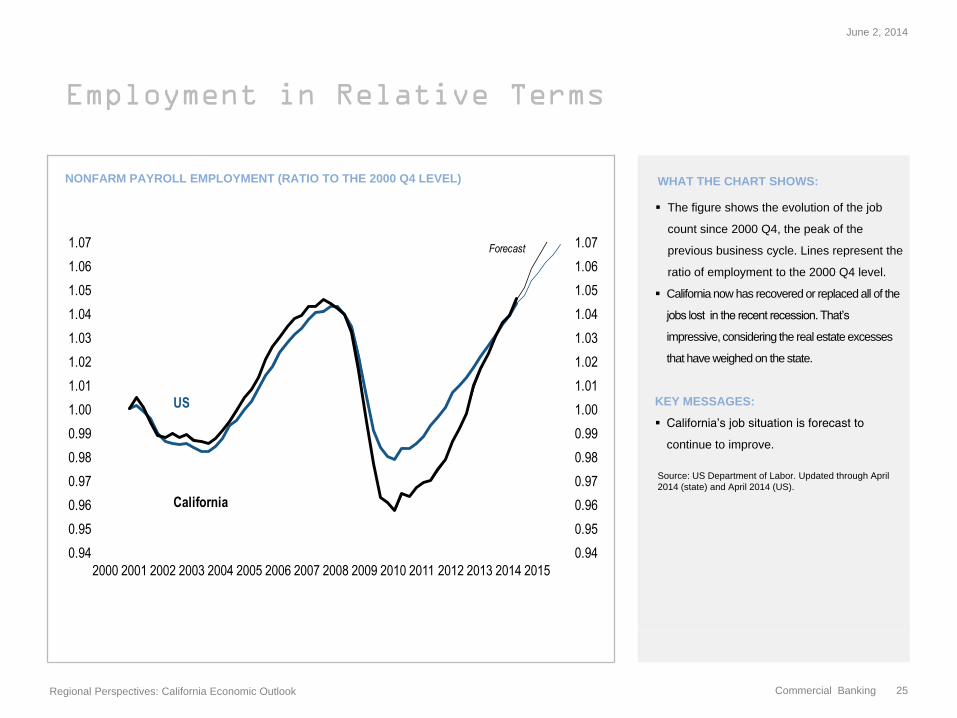

Employment in Relative Terms

NONFARM PAYROLL EMPLOYMENT (RATIO TO THE 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

The figure shows the evolution of the job

count since 2000 Q4, the peak of the

previous business cycle. Lines represent the

ratio of employment to the 2000 Q4 level.

California now has recovered or replaced all of the

jobs lost in the recent recession. That’s

impressive, considering the real estate excesses

that have weighed on the state.

KEY MESSAGES:

California’s job situation is forecast to

continue to improve.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 25

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US

California

Forecast

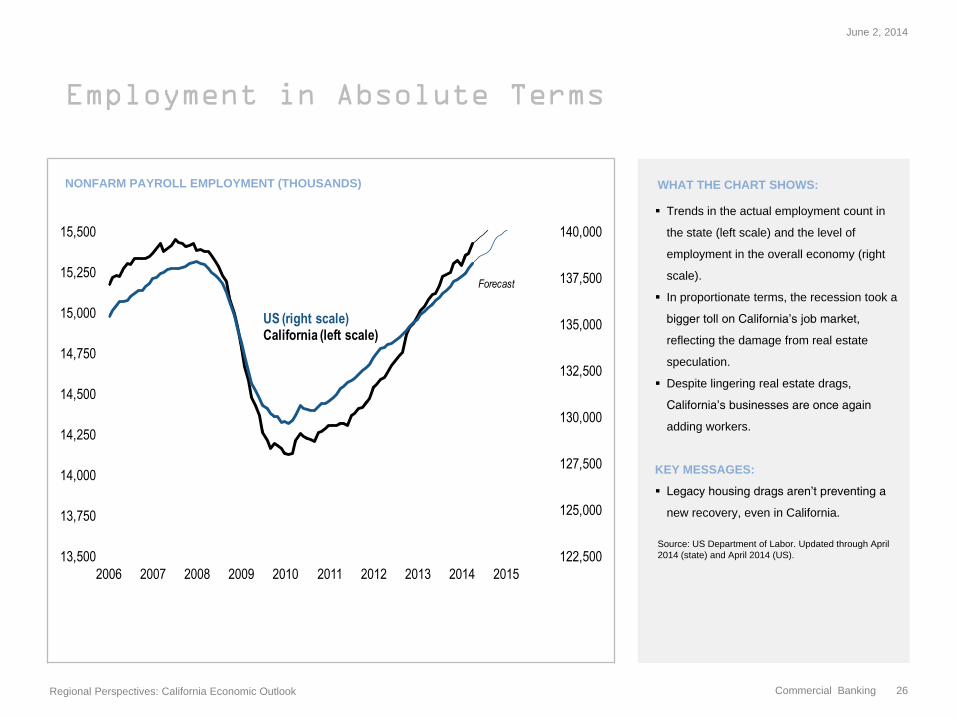

Employment in Absolute Terms

NONFARM PAYROLL EMPLOYMENT (THOUSANDS) WHAT THE CHART SHOWS:

Trends in the actual employment count in

the state (left scale) and the level of

employment in the overall economy (right

scale).

In proportionate terms, the recession took a

bigger toll on California’s job market,

reflecting the damage from real estate

speculation.

Despite lingering real estate drags,

California’s businesses are once again

adding workers.

KEY MESSAGES:

Legacy housing drags aren’t preventing a

new recovery, even in California.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 26

122,500

125,000

127,500

130,000

132,500

135,000

137,500

140,000

13,500

13,750

14,000

14,250

14,500

14,750

15,000

15,250

15,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US (right scale)California (left scale)

Forecast

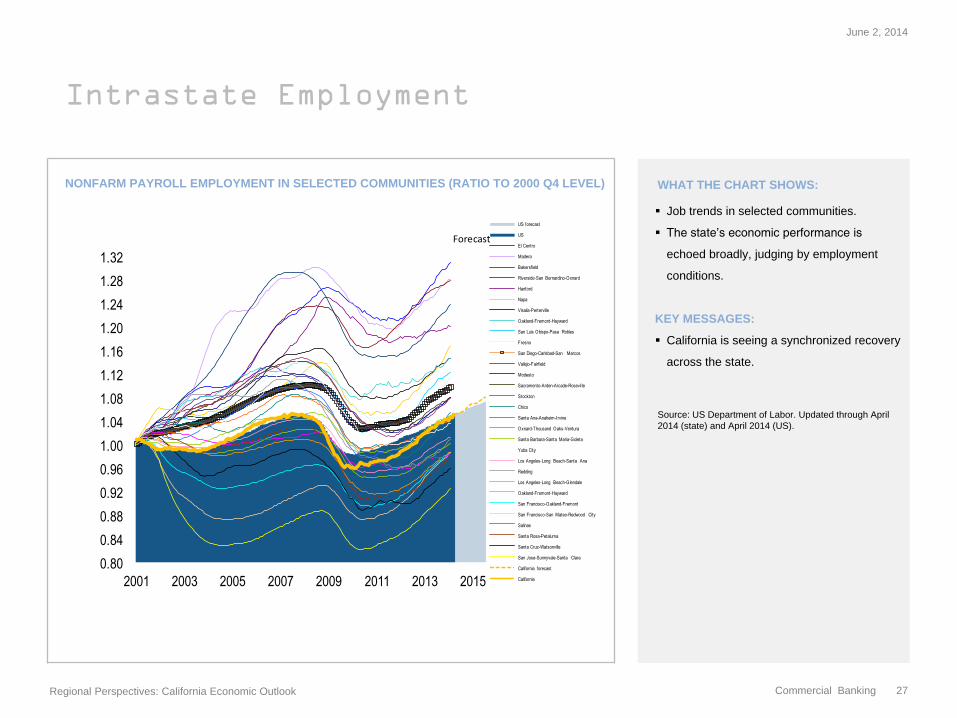

Intrastate Employment

NONFARM PAYROLL EMPLOYMENT IN SELECTED COMMUNITIES (RATIO TO 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

Job trends in selected communities.

The state’s economic performance is

echoed broadly, judging by employment

conditions.

KEY MESSAGES:

California is seeing a synchronized recovery

across the state.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 27

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

0.80

0.84

0.88

0.92

0.96

1.00

1.04

1.08

1.12

1.16

1.20

1.24

1.28

1.32

2001 2003 2005 2007 2009 2011 2013 2015

US forecast

US

El Centro

Madera

Bakersfield

Riverside-San Bernardino-Oxnard

Hanford

Napa

Visalia-Perterville

Oakland-Fremont-Hayward

San Luis Obispo-Pasa Robles

Fresno

San Diego-Carlsbad-San Marcos

Vallejo-Fairfield

Modesto

Sacramento-Arden-Arcade-Rosevil le

Stockton

Chico

Santa Ana-Anaheim-Irvine

Oxnard-Thousand Oaks-Ventura

Santa Barbara-Santa Maria-Goleta

Yuba City

Los Angeles-Long Beach-Santa Ana

Redding

Los Angeles-Long Beach-Glendale

Oakland-Fremont-Hayward

San Francisco-Oakland-Fremont

San Francisco-San Mateo-Redwood City

Salinas

Santa Rosa-Petaluma

Santa Cruz-Watsonville

San Jose-Sunnyvale-Santa Clara

California forecast

California

Forecast

Intrastate Employment

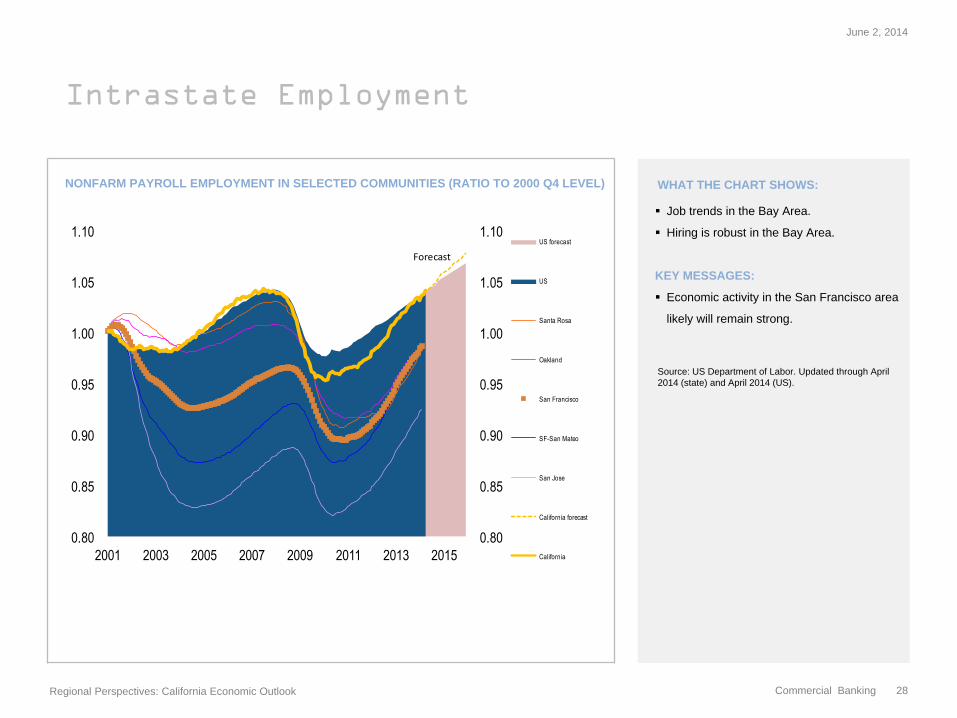

NONFARM PAYROLL EMPLOYMENT IN SELECTED COMMUNITIES (RATIO TO 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

Job trends in the Bay Area.

Hiring is robust in the Bay Area.

KEY MESSAGES:

Economic activity in the San Francisco area

likely will remain strong.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 28

0.80

0.85

0.90

0.95

1.00

1.05

1.10

0.80

0.85

0.90

0.95

1.00

1.05

1.10

2001 2003 2005 2007 2009 2011 2013 2015

US forecast

US

Santa Rosa

Oakland

San Francisco

SF-San Mateo

San Jose

California forecast

California

Forecast

Intrastate Employment

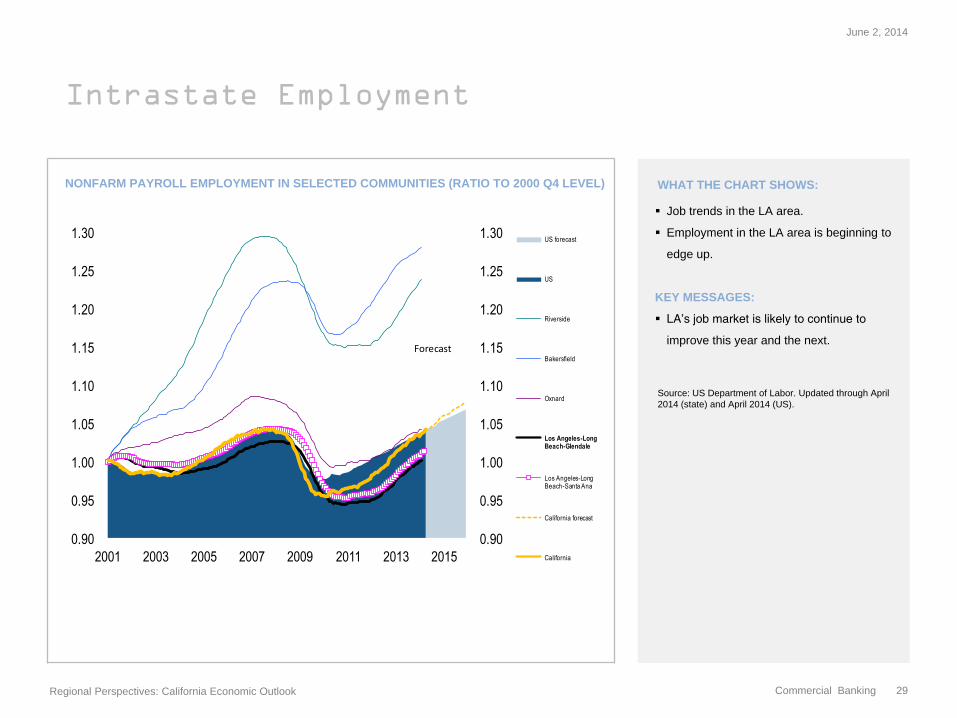

NONFARM PAYROLL EMPLOYMENT IN SELECTED COMMUNITIES (RATIO TO 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

Job trends in the LA area.

Employment in the LA area is beginning to

edge up.

KEY MESSAGES:

LA’s job market is likely to continue to

improve this year and the next.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 29

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

2001 2003 2005 2007 2009 2011 2013 2015

US forecast

US

Riverside

Bakersfield

Oxnard

Los Angeles-Long Beach-Glendale

Los Angeles-Long Beach-Santa Ana

California forecast

California

Forecast

Intrastate Employment

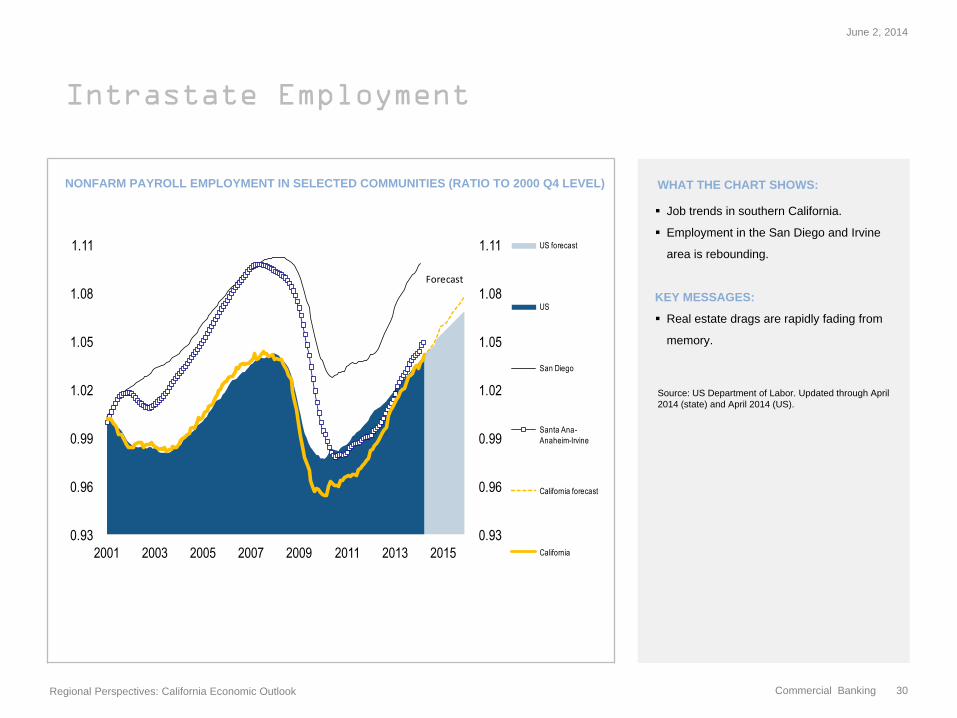

NONFARM PAYROLL EMPLOYMENT IN SELECTED COMMUNITIES (RATIO TO 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

Job trends in southern California.

Employment in the San Diego and Irvine

area is rebounding.

KEY MESSAGES:

Real estate drags are rapidly fading from

memory.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 30

0.93

0.96

0.99

1.02

1.05

1.08

1.11

0.93

0.96

0.99

1.02

1.05

1.08

1.11

2001 2003 2005 2007 2009 2011 2013 2015

US forecast

US

San Diego

Santa Ana-

Anaheim-Irvine

California forecast

California

Forecast

Unemployment

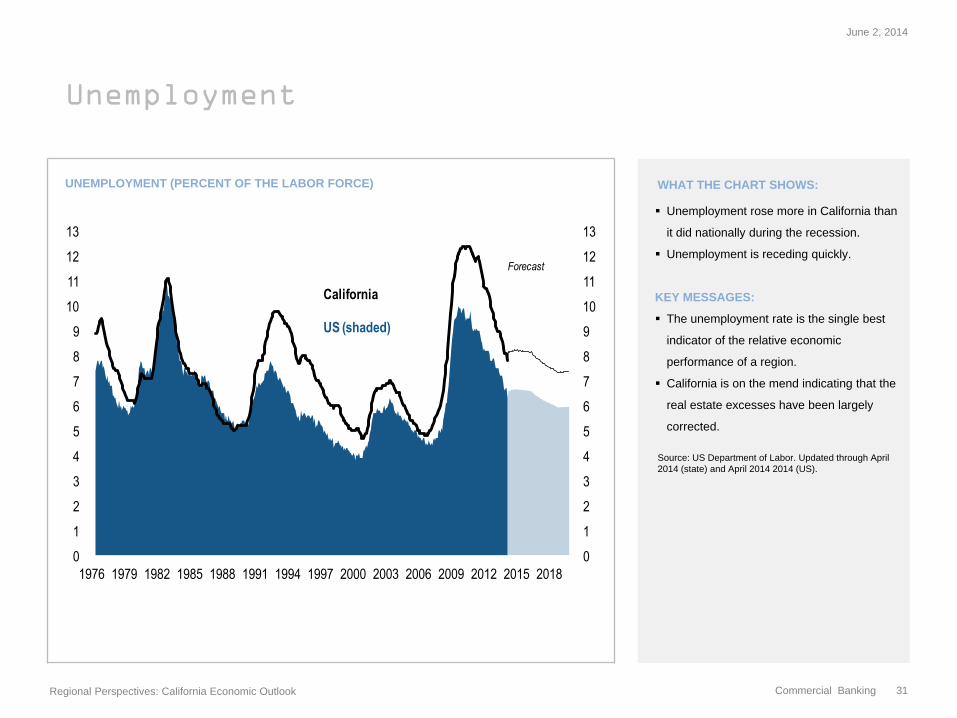

UNEMPLOYMENT (PERCENT OF THE LABOR FORCE) WHAT THE CHART SHOWS:

Unemployment rose more in California than

it did nationally during the recession.

Unemployment is receding quickly.

KEY MESSAGES:

The unemployment rate is the single best

indicator of the relative economic

performance of a region.

California is on the mend indicating that the

real estate excesses have been largely

corrected.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 2014 (US).

June 2, 2014

Regional Perspectives: California Economic Outlook

Commercial Banking 31

0

1

2

3

4

5

6

7

8

9

10

11

12

13

0

1

2

3

4

5

6

7

8

9

10

11

12

13

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

California

US (shaded)

Forecast

CONTACT:

James E. Glassman

Telephone: (212) 270-0778

© 2014 JPMorgan Chase & Co. All rights reserved. Chase, JPMorgan and JPMorgan Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide

(collectively, “JPMC”). The material contained herein is intended as a general market commentary. To the extent indices have been used in this commentary, please note that it is not possible to

invest directly in an index. Opinions expressed herein are those of James Glassman and may differ from those of other J.P. Morgan employees and affiliates. This information in no way constitutes

J.P. Morgan research and should not be treated as such. Further, the views expressed herein may differ from that contained in J.P. Morgan research reports. The above

summary/prices/quotes/statistics have been obtained from sources deemed to be reliable, but we do not guarantee their accuracy or completeness.