Embed Size (px)

Citation preview

According to the latest Economic Activity Monthly Estimate (EMAE) released by INDEC (the National Statistics Institute), economic activity posted a growth of 1.1% in June compared with May (seasonally adjusted). In con-trast, compared with June 2011, economic activity showed no change. Overall, the accumu-lated growth in the last 12 months has reached 2.5%. (EMAE shows the progress of eco-nomic activity on a monthly basis while GDP figures are released

quarterly).

Economic activity in June 2012

INDEC’s provisional estimate of GDP (Gross Domestic Product) for the first quarter of 2012 shows a growth of 5.2% compared with the same quarter of 2011 and of 0.9 % (seasonally adjusted) com-pared with the previous quarter. In particular, production of goods increased by 3.2% while services grew by 6.5% year-on-year.

September 2012

Official figures 1-3

Trade 4

Events 6-7

Bilateral Trade 5

Contents Monthly

% change Annual

% change

July 11 -0.4 % 9.0 %

Aug 11 0.6 % 10.1 %

Sep 11 0.1 % 8.9 %

Oct 11 0.5 % 9.1 %

Nov 11 0.0 % 7.3 %

Dec 11 0.2 % 5.6 %

Jan 12 -0.2% 6.1 %

Feb 12 0.0% 5.6%

Mar 12 0.5% 4.1%

Apr 12 -1.3% 0.6%

May 12 0.2% -0.5%

June 12 1.1% 0.0%

Official figures

EMAE: A year at a glance

Newsletter Economic and Commercial

GDP growth of 5.2% in first quarter 2012

9.29.9

9.1 9.3

7.3

5.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12

GDP Annual Change by Quarter%

Source: INDEC

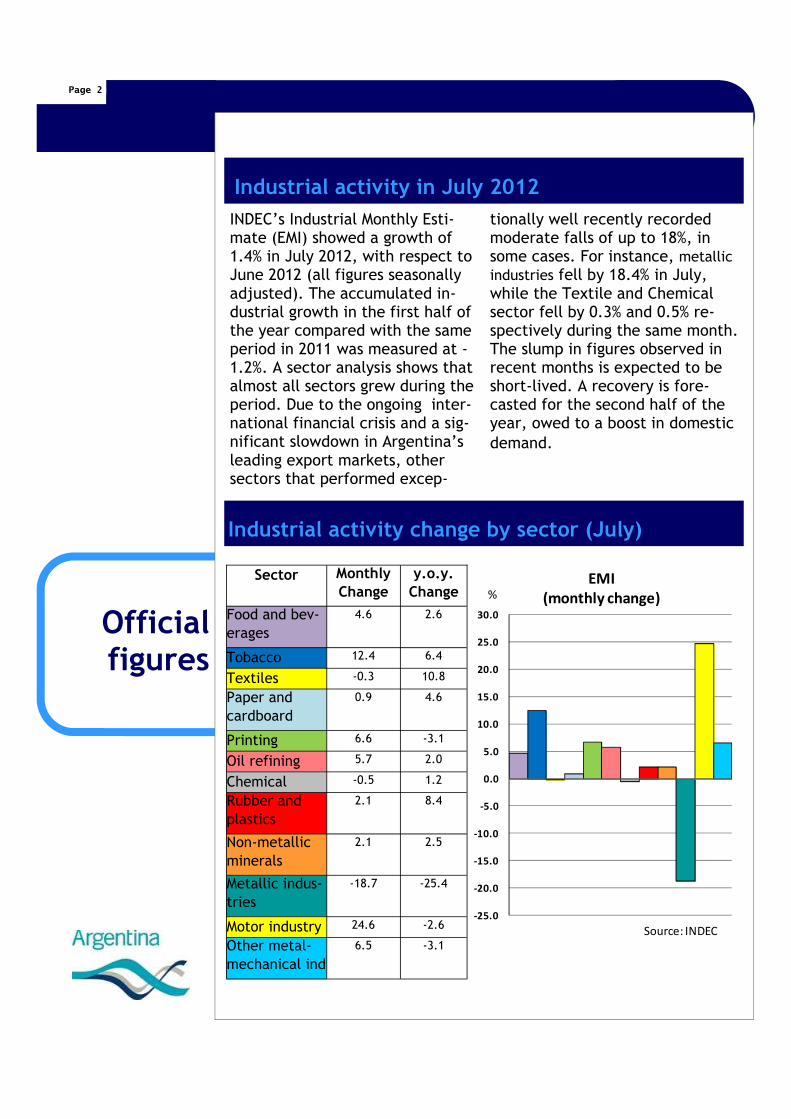

Industrial activity change by sector (July)

Official figures

Page 2

Industrial activity in July 2012

INDEC’s Industrial Monthly Esti-mate (EMI) showed a growth of 1.4% in July 2012, with respect to June 2012 (all figures seasonally adjusted). The accumulated in-dustrial growth in the first half of the year compared with the same period in 2011 was measured at -1.2%. A sector analysis shows that almost all sectors grew during the period. Due to the ongoing inter-national financial crisis and a sig-nificant slowdown in Argentina’s leading export markets, other sectors that performed excep-

tionally well recently recorded moderate falls of up to 18%, in some cases. For instance, metallic industries fell by 18.4% in July, while the Textile and Chemical sector fell by 0.3% and 0.5% re-spectively during the same month. The slump in figures observed in recent months is expected to be short-lived. A recovery is fore-casted for the second half of the year, owed to a boost in domestic demand.

Sector Monthly

Change

y.o.y.

Change

Food and bev-erages

4.6 2.6

Tobacco 12.4 6.4

Textiles -0.3 10.8

Paper and cardboard

0.9 4.6

Printing 6.6 -3.1

Oil refining 5.7 2.0

Chemical -0.5 1.2

Rubber and plastics

2.1 8.4

Non-metallic minerals

2.1 2.5

Metallic indus-tries

-18.7 -25.4

Motor industry 24.6 -2.6

Other metal-mechanical ind

6.5 -3.1

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

EMI

(monthly change)

Source: INDEC

%

Page 3

sale Prices Index increased by 1.0% and the Construction Costs Index by 1.3% during the same month, according to INDEC.

The Consumer Prices Index (CPI) for the city of Buenos Aires and its metropolitan area showed an increase of 0.8% in July 2012, ac-cumulating a 9.9% rate to the year from July 2011. The Whole-

July inflation rate at 0.8%

Official figures

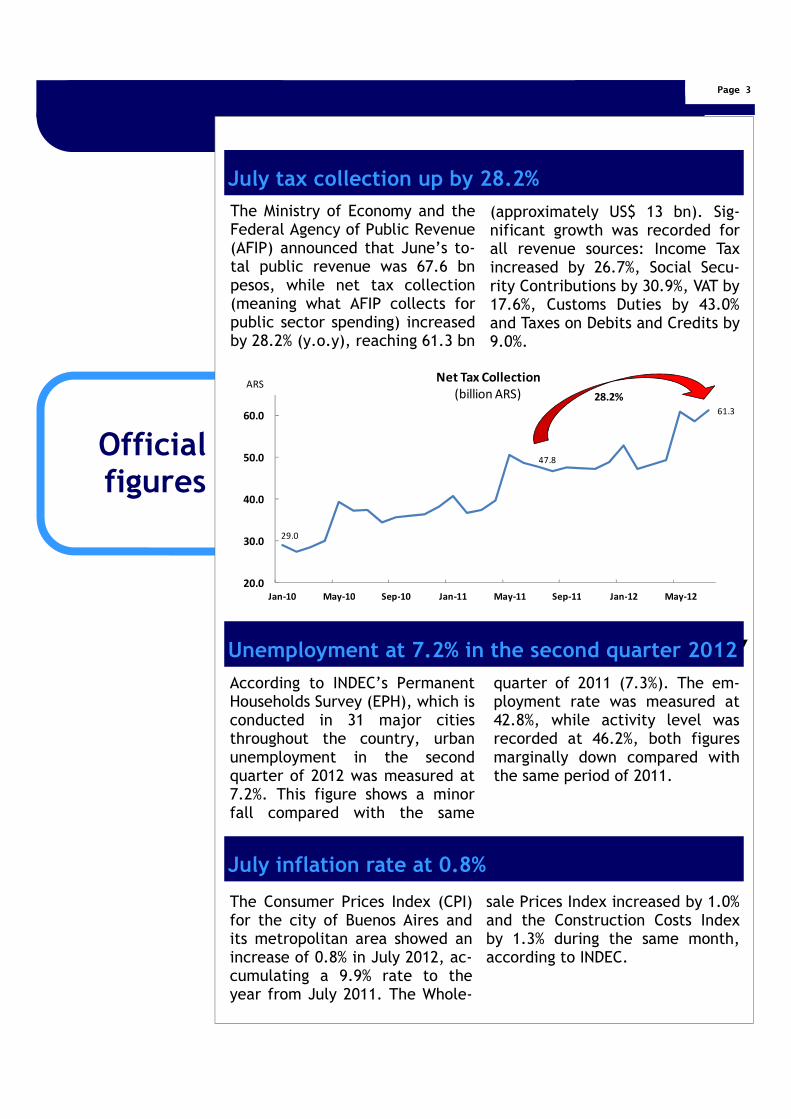

The Ministry of Economy and the Federal Agency of Public Revenue (AFIP) announced that June’s to-tal public revenue was 67.6 bn pesos, while net tax collection (meaning what AFIP collects for public sector spending) increased by 28.2% (y.o.y), reaching 61.3 bn

(approximately US$ 13 bn). Sig-nificant growth was recorded for all revenue sources: Income Tax increased by 26.7%, Social Secu-rity Contributions by 30.9%, VAT by 17.6%, Customs Duties by 43.0% and Taxes on Debits and Credits by 9.0%.

July tax collection up by 28.2%

Unemployment at 7.2% in the second quarter 2012

According to INDEC’s Permanent Households Survey (EPH), which is conducted in 31 major cities throughout the country, urban unemployment in the second quarter of 2012 was measured at 7.2%. This figure shows a minor fall compared with the same

quarter of 2011 (7.3%). The em-ployment rate was measured at 42.8%, while activity level was recorded at 46.2%, both figures marginally down compared with the same period of 2011.

29.0

47.8

61.3

20.0

30.0

40.0

50.0

60.0

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12

Net Tax Collection

(billion ARS)ARS

28.2%

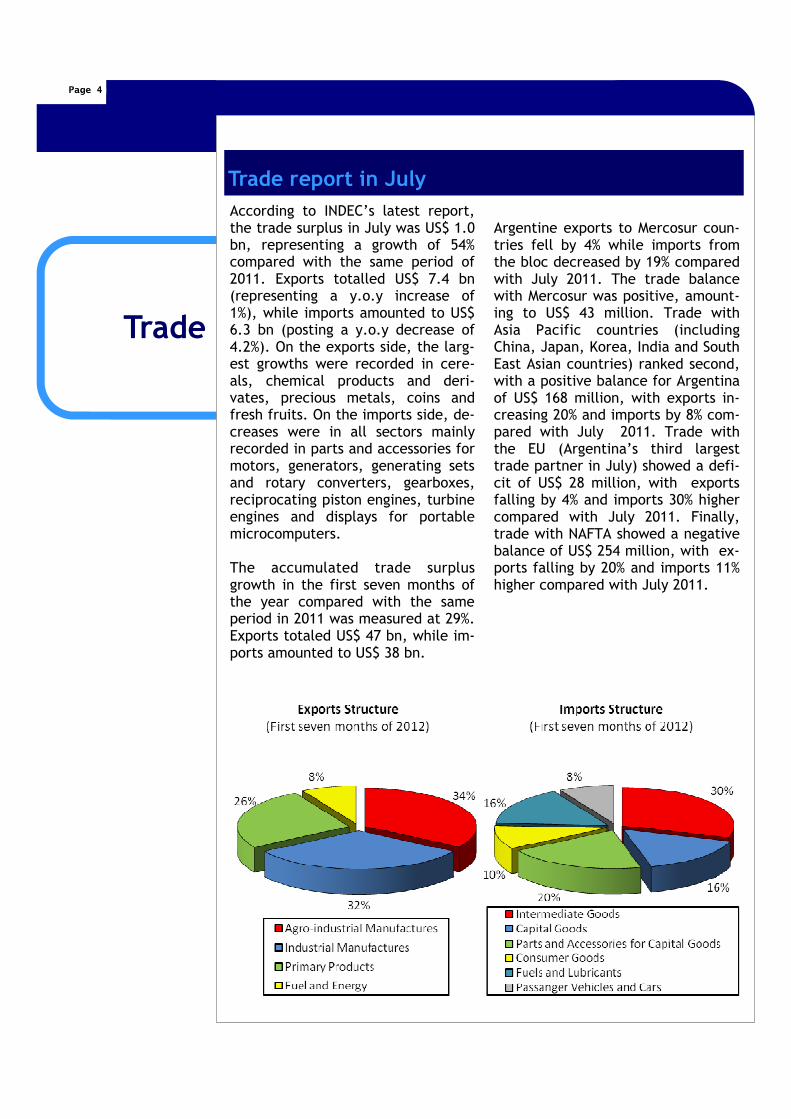

According to INDEC’s latest report, the trade surplus in July was US$ 1.0 bn, representing a growth of 54% compared with the same period of 2011. Exports totalled US$ 7.4 bn (representing a y.o.y increase of 1%), while imports amounted to US$ 6.3 bn (posting a y.o.y decrease of 4.2%). On the exports side, the larg-est growths were recorded in cere-als, chemical products and deri-vates, precious metals, coins and fresh fruits. On the imports side, de-creases were in all sectors mainly recorded in parts and accessories for motors, generators, generating sets and rotary converters, gearboxes, reciprocating piston engines, turbine engines and displays for portable microcomputers. The accumulated trade surplus growth in the first seven months of the year compared with the same period in 2011 was measured at 29%. Exports totaled US$ 47 bn, while im-ports amounted to US$ 38 bn.

Trade report in July

Trade

Page 4

Argentine exports to Mercosur coun-tries fell by 4% while imports from the bloc decreased by 19% compared with July 2011. The trade balance with Mercosur was positive, amount-ing to US$ 43 million. Trade with Asia Pacific countries (including China, Japan, Korea, India and South East Asian countries) ranked second, with a positive balance for Argentina of US$ 168 million, with exports in-creasing 20% and imports by 8% com-pared with July 2011. Trade with the EU (Argentina’s third largest trade partner in July) showed a defi-cit of US$ 28 million, with exports falling by 4% and imports 30% higher compared with July 2011. Finally, trade with NAFTA showed a negative balance of US$ 254 million, with ex-ports falling by 20% and imports 11% higher compared with July 2011.

Page 5

Bilateral Trade

Bilateral Trade

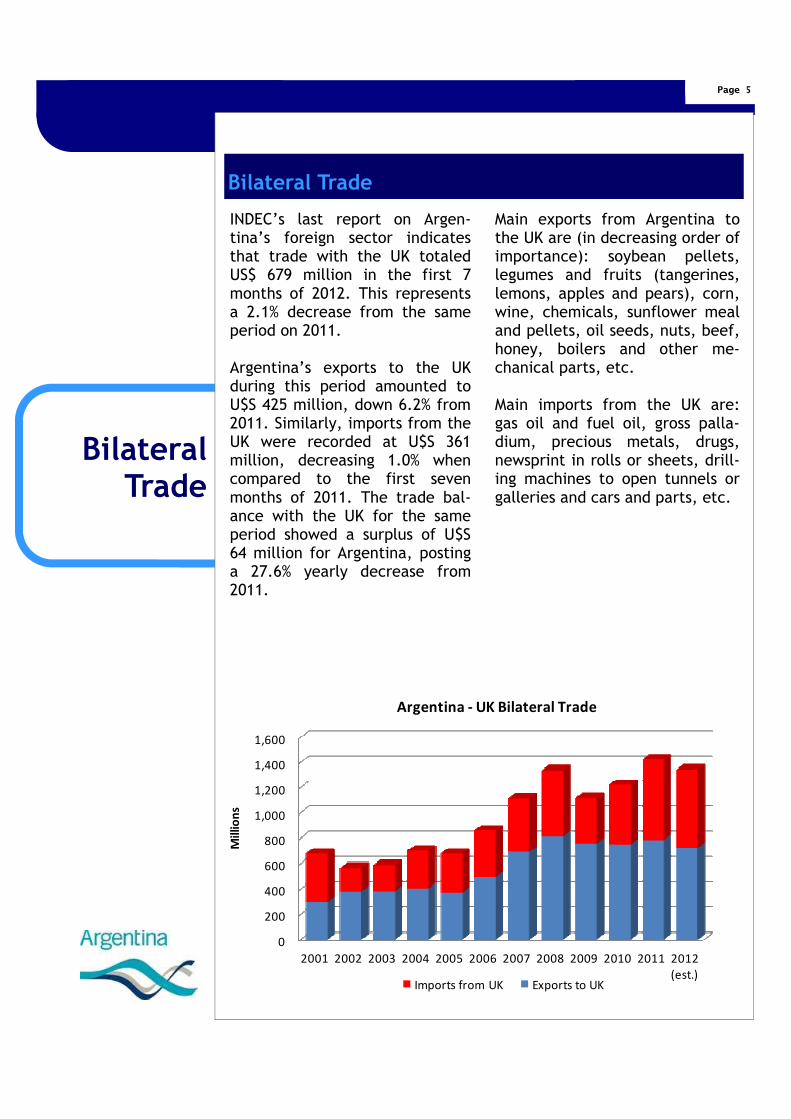

INDEC’s last report on Argen-tina’s foreign sector indicates that trade with the UK totaled US$ 679 million in the first 7 months of 2012. This represents a 2.1% decrease from the same period on 2011. Argentina’s exports to the UK during this period amounted to U$S 425 million, down 6.2% from 2011. Similarly, imports from the UK were recorded at U$S 361 million, decreasing 1.0% when compared to the first seven months of 2011. The trade bal-ance with the UK for the same period showed a surplus of U$S 64 million for Argentina, posting a 27.6% yearly decrease from 2011.

Main exports from Argentina to the UK are (in decreasing order of importance): soybean pellets, legumes and fruits (tangerines, lemons, apples and pears), corn, wine, chemicals, sunflower meal and pellets, oil seeds, nuts, beef, honey, boilers and other me-chanical parts, etc. Main imports from the UK are: gas oil and fuel oil, gross palla-dium, precious metals, drugs, newsprint in rolls or sheets, drill-ing machines to open tunnels or galleries and cars and parts, etc.

0

200

400

600

800

1,000

1,200

1,400

1,600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

(est.)

Mil

lio

ns

Imports from UK Exports to UK

Argentina - UK Bilateral Trade

Events

Page 6

For the second year run-ning, The Argentine Em-bassy was present at Taste of London, the most important gastro-nomic fair in London. From 21 to 24 June, a vast number of peo-ple were attracted by around 9 Argentine restaurants and were able to taste Argen-tine steak, empanadas, locro and other deli-catessen at the Argentine Pavilion and the Argentine Tourism Board hosted Argentine mate tasting sessions. Also, there were a number of wine merchants tasting Argentine wines and Quilmes, the Argentine beer pro-ducer, tasted beer to visitors. This year, the Argentine stand had a prime location, which gave the best context for a tango show each of the 4 days of the event.

Taste of London 2012

From 26 to 28 June, the Ar-gentine Embassy was pre-sent with a stand at the “5th Annual Agriculture In-vestment Summit”, show-cased at the Victoria Parl Plaza Hotel, London. On the 26th, the Argentine Em-bassy sponsored a reception with a Tango show, as well as Argentine wines and beef tasting.

Agriculture Investment Summit

Page 7

Events

Argentine Village 2012

The Embassy has been pre-sent once again during the British polo season with the Argentine Village. This year, the Village was deployed at Polo in the Park (8-10 June) and Veuve Clicquot Gold Cup Finals (15 July), in both occa-sions joined by Aerolíneas Ar-gentinas. Polo in the Park was played at Hurlingham Park, Fulham (London), between 6 teams (Camino Real ‘Team Buenos Ai-res’, City AM ‘Team Delhi’, Mandarin Oriental Hyde Park ‘Team Abu Dhabi’, Mint ‘Team Londres’, IG Index ‘Team Sydney’ y Otkritie ‘Team Moscú’), within which there were 5 Argentine polo payers (Oscar Mancini, Matías Machado, Tomás Ruíz Guiñazú, Rodrigo Rueda y An-drea Vianini),the attendance was of around 25.000 people (according to our own estimations). Among the 45 retailers there were Argentine companies such as Estribos, Kevingston and La Martina, and as it is the custom, the Argentine Embassy provided advice on tourism in Argen-tina and gave away leaflets including maps and useful information for people aiming at travelling to and within Argentina. On the other hand, Veuve Clicquot Gold Cup Finals took place at Cowdray Park Polo Club, Midhurst (West Sussex), between El Remanso and Cor-tium (counting 3 Argentine polo payers within them: Gui-llermo Terrera, Francisco Eli-zalde y Polito Pieres), and was attended by around 18.000 people (according to our own estimations); among the 45 retailers there were Argentine companies such as Estribos, Kevingston La Mar-tina and La Tarde; the Argentine Embassy provided advice on tourism in Argentina and gave away tourism leaflets, including those of Hotel Llao Llao, located in San Carlos de Bariloche. Additionally, the Em-bassy exhibited in this opportunity handcrafts made by Argentine craftsmen grouped in a project developed by the Argentine Ministry of Social Development called ‘Emprendedores de Nuestra Tierra’ (‘Entrepreneurs of Our Land’), regarded by the public as high-quality crafts .

![Mancini Song Book[1]](https://img.pdfslide.us/doc/110x75/577d27931a28ab4e1ea43f3a/mancini-song-book1.jpg)