Embed Size (px)

Citation preview

Economic Analysis of Protectionist US Trade Policy on Chinese Solar Exports

Prepared by: Prepared for:

Matt Fondacaro

James Harter

Dan Matam

Sabahudin Redzepovic

Amay Sheth

Elaine Tang

Dr. George Tolley

Dr. Stephen Berry

Jing Wu

Jaeyoon Lee

Autumn 2014 – Group 15

2

Acknowledgements

We would like to thank the following people:

Dr. George Tolley, University of Chicago

Dr. R. Stephen Berry, University of Chicago

Jing Wu, University of Chicago

Jaeyoon Lee, University of Chicago

3

Table of Contents

Acknowledgments…………………………………………………………………..…… 2 Abstract…………………………………………………………………………………... 4 Timeline…….……………………………………………………………………………. 6 Part I – Pertinent Information and Analysis of Global Solar Industry and Trade Tensions

Chinese Solar Industry – Rise of Chinese Producers…………………………….. 7 Energy policy that convinced Suntech to begin manufacturing in the United States……………………………………………………………... 9

US Solar Industry……………………………………………………………….. 13 US Manufacturers………………………………………………………. 16

European Solar Industry………………………………………………………... 20 History of Solar in Europe………………………………………………20 Market Development…………………………………………………… 21 Current Market and Forecast…………………………………………… 24 Tariffs in Europe………………………………………………………... 27

US Trade Tariffs…….…………………………………………………………. 30 Chinese Counter-Trade Tariffs…………………………………………………. 38

Part II – Cost-Benefit Analysis

Data Analysis……………………………………………………………….. 40 Cost-Benefit Analysis – an Overview………………………………. 40 Tariffs……………………………………………………………….. 50 Final Notes………………………………………………………….. 53 Quantifying the Social Cost of Carbon Emission…………………... 55

Countervailing Subsidies (CVD) & Anti-Dumping Duties (AD) Impact on Domestic Employment……………………………………………………… 58

Domestic Manufacturing…………………………………………… 58 Overall Domestic Solar Employment Is Not Dependent on Manufacturing………………………………………………………. 61 Demand for Solar Products is Correlated with Employment……….. 65 Analysis of Effects on Employment……………………………...… 71

Aggregate Cost-Benefit Analysis…………………………………………... 72 Part III – Conclusion: Policy Recommendation

Repeal CVD and AD Duties on Chinese Solar Imports………………………... 74 Appendix………………………………………………………………………………... 75 Works Cited…………………………………………………………………………….. 86

4

Abstract Over the past few years, solar trade between the United States, Europe and China has

exploded into a highly contentious international trade and geopolitical issue. In 2012, the

United States Department of Commerce (DOC) imposed anti-dumping and

countervailing duties on solar cells and modules exported from China, and, in 2013, the

European Union followed suit with its own investigation into Chinese solar exports. In

retaliation, China imposed tariffs on polysilicon exports from the United States. In June

2014, the DOC and ITC released a preliminary finding that Chinese producers were

partially circumventing the 2012 tariffs by sourcing solar cells from Taiwan.

The issue of US-China solar trade policy is extremely timely and important as the United

States and China work together to confront the global climate change crisis. In his 2011

State of the Union Address, President Obama called for 80% of US energy to be derived

from clean energy sources by 2035. In November of 2014, President Obama and

President Xi reached a climate accord to reduce greenhouse gas emissions from both

nations. Solar energy could play a central role in reaching these goals if its price can

reach “grid parity,” meaning the energy source becomes cost competitive with traditional

fossil fuels without government incentives. The solar trade conflict between the United

States and China has slowed solar drive to grid parity

Proponents of countervailing and anti-dumping duties against Chinese solar exports

argued that illegal government subsidies enabled Chinese solar firms to expand rapidly

and gain market share through predatory tactics to drive competitors out of business.

5

They argued the tariffs were necessary to prevent further losses in domestic US solar

manufacturing jobs. The purpose of this paper is to determine whether the US policy has

had a net positive or net negative economic impact since the tariffs were implemented in

2012. The paper explains relevant background information on the topic, summarizes the

results of a cost-benefit analysis of the policy since 2012, and provides a forward looking

policy recommendation.

6

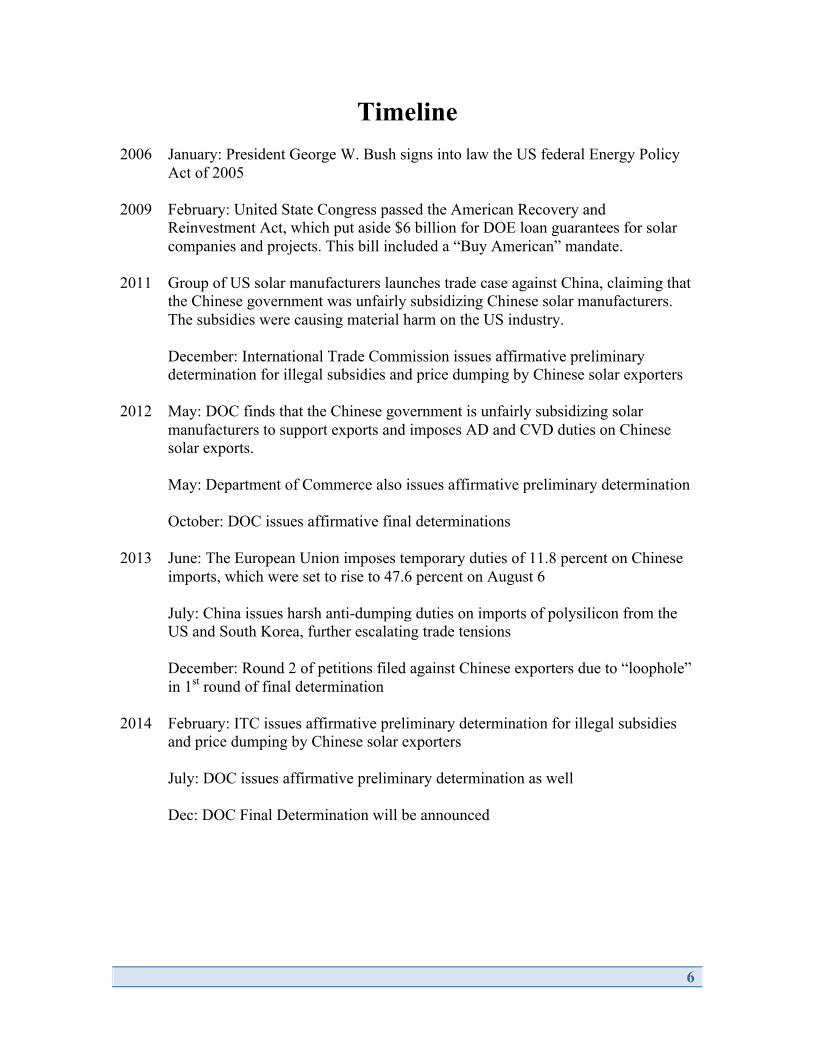

Timeline 2006 January: President George W. Bush signs into law the US federal Energy Policy

Act of 2005 2009 February: United State Congress passed the American Recovery and

Reinvestment Act, which put aside $6 billion for DOE loan guarantees for solar companies and projects. This bill included a “Buy American” mandate.

2011 Group of US solar manufacturers launches trade case against China, claiming that

the Chinese government was unfairly subsidizing Chinese solar manufacturers. The subsidies were causing material harm on the US industry.

December: International Trade Commission issues affirmative preliminary determination for illegal subsidies and price dumping by Chinese solar exporters

2012 May: DOC finds that the Chinese government is unfairly subsidizing solar

manufacturers to support exports and imposes AD and CVD duties on Chinese solar exports.

May: Department of Commerce also issues affirmative preliminary determination

October: DOC issues affirmative final determinations 2013 June: The European Union imposes temporary duties of 11.8 percent on Chinese

imports, which were set to rise to 47.6 percent on August 6

July: China issues harsh anti-dumping duties on imports of polysilicon from the US and South Korea, further escalating trade tensions December: Round 2 of petitions filed against Chinese exporters due to “loophole” in 1st round of final determination

2014 February: ITC issues affirmative preliminary determination for illegal subsidies

and price dumping by Chinese solar exporters July: DOC issues affirmative preliminary determination as well Dec: DOC Final Determination will be announced

7

Chinese Solar Industry – Rise of Chinese Producers

Suntech, a solar energy company founded in 2001, opened the door for China’s solar

revolution. The firm opened its first factory in 2002. Suntech made many breakthroughs

in terms of creating efficient crystalline-silicon solar panels, while simultaneously

discovering ways to cut costs. The success of these breakthroughs is predominantly due

to their aggressive cost-cutting, which has set an example for other Chinese producers

and has made China the largest source of solar panels across the globe.

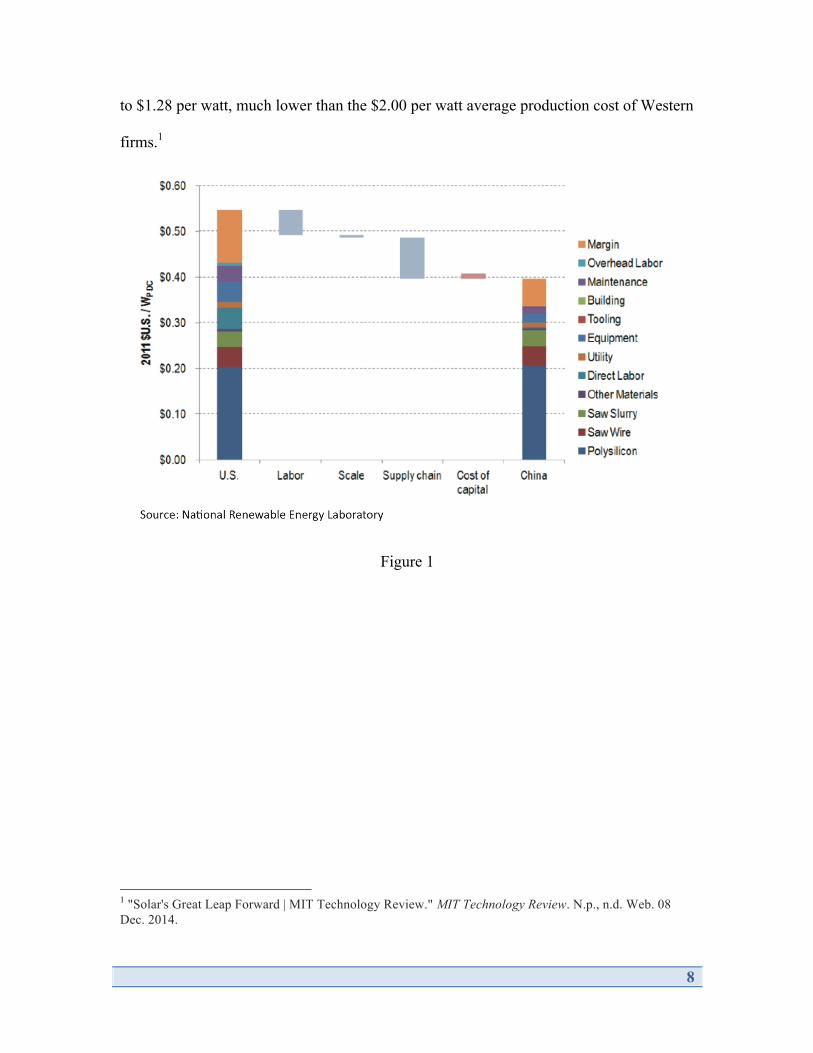

Chinese manufacturers cut costs by relying heavily on various energy policies put into

place. For example, Suntech’s decision to expand production in the United States,

Arizona particularly, was almost entirely due to recently introduced solar energy policy.

One of Suntech’s major reservations about expanding production to the U.S. was that

there was not enough of a supply network. Lack of a dense supply network would cause

Suntech to lose its price advantage. Suntech established its pricing advantage because

China had developed a very close network of suppliers, which were in close proximity to

the production facilities. As you can see in Figure 1, this agglomeration allowed Suntech

to minimize its production costs.

In 2004, silicon solar panels production cost about $3.20 per watt, on average to produce

silicon solar panels. By 2010, a Chinese manufacturer’s cost of production had declined

8

to $1.28 per watt, much lower than the $2.00 per watt average production cost of Western

firms.1

Figure 1

1 "Solar's Great Leap Forward | MIT Technology Review." MIT Technology Review. N.p., n.d. Web. 08 Dec. 2014.

9

Energy policy that convinced Suntech to begin manufacturing in the

United States

Arizona established policies to promote the use of renewable energy. In 1996, the

Arizona Corporate Commission (ACC) aimed to have a mere .2% of the state’s regulated

utility power be generated by solar energy. In 2001, the ACC created an Environmental

Portfolio Standard (EPS), which required that by 2007 1.1% of the state-regulated

utilities energy must be produced via renewable energy. In addition to this, of this 1.1%,

60% of it must come from solar power. The ACC claimed this policy would bring

economic improvements to Arizona and would also create positive environmental

impacts.

In 2006, the ACC decided to approve a new Renewable Energy Standard and Tariff

(REST). This policy mandated that 15% of the energy that regulated utilities generated

had to come from renewable resources by the year 2025. Solar energy firms like Suntech

and FirstSolar were attracted to this type of policy which is why firms were attracted to

Arizona—the solar manufacturing industry had great potential for growth there. In

addition to this, firms embraced the idea that a growing solar industry would draw in a

supply chain, thus lowering production costs. With this great potential, Suntech decided

to expand in the U.S.

President Obama signed into law the American Recovery and Reinvestment Act

(ARRA). As a part of this bill, the Advanced Energy Manufacturing Tax Credit supplied

$2.3 billion in tax credits. In addition to this, the law provided the DOE with $6 billion to

10

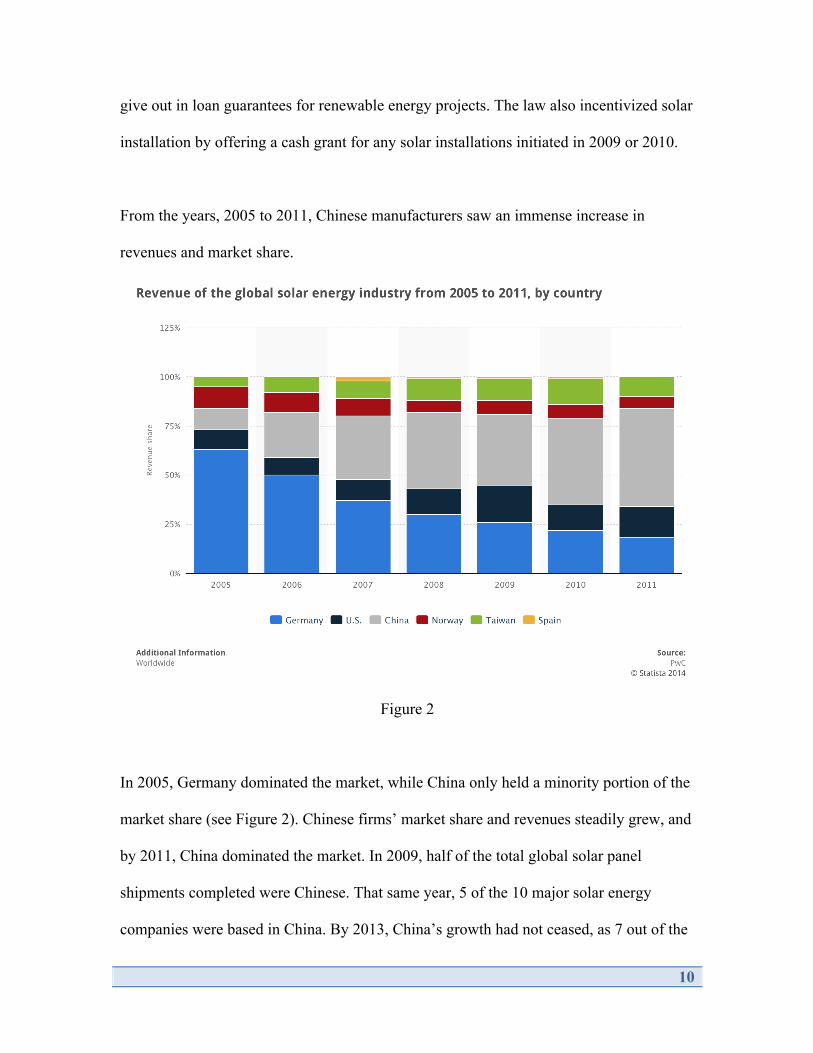

give out in loan guarantees for renewable energy projects. The law also incentivized solar

installation by offering a cash grant for any solar installations initiated in 2009 or 2010.

From the years, 2005 to 2011, Chinese manufacturers saw an immense increase in

revenues and market share.

Figure 2

In 2005, Germany dominated the market, while China only held a minority portion of the

market share (see Figure 2). Chinese firms’ market share and revenues steadily grew, and

by 2011, China dominated the market. In 2009, half of the total global solar panel

shipments completed were Chinese. That same year, 5 of the 10 major solar energy

companies were based in China. By 2013, China’s growth had not ceased, as 7 out of the

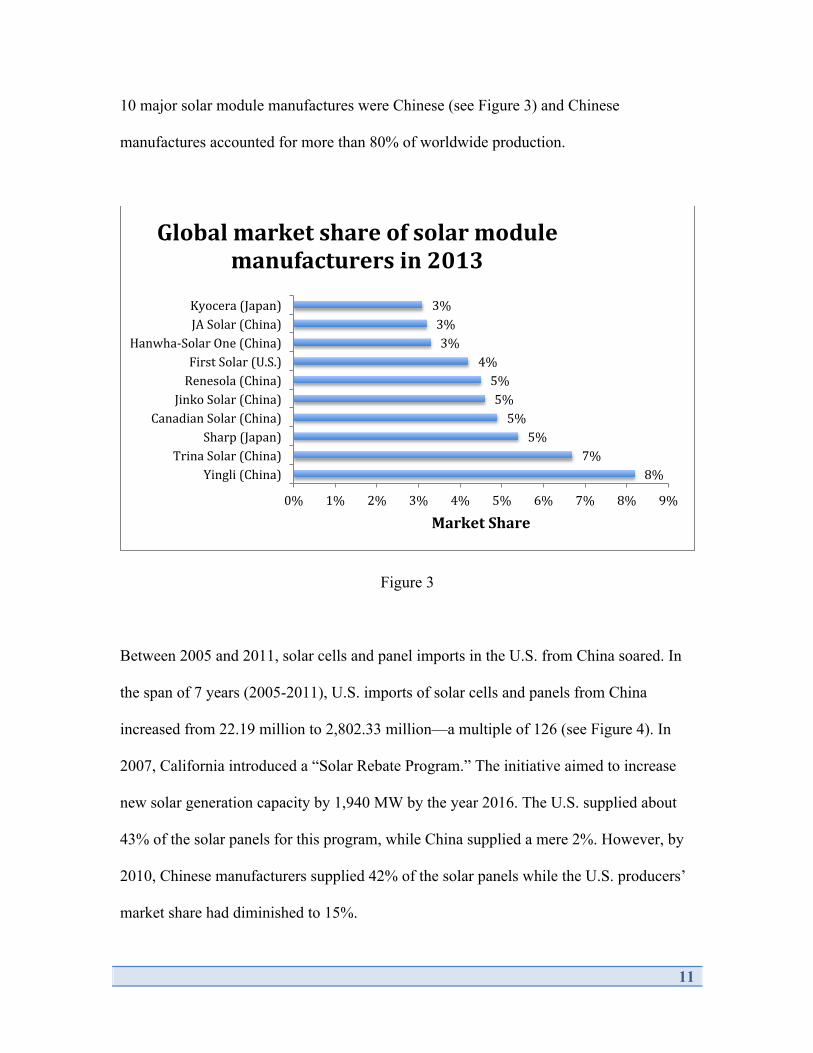

11

10 major solar module manufactures were Chinese (see Figure 3) and Chinese

manufactures accounted for more than 80% of worldwide production.

Figure 3

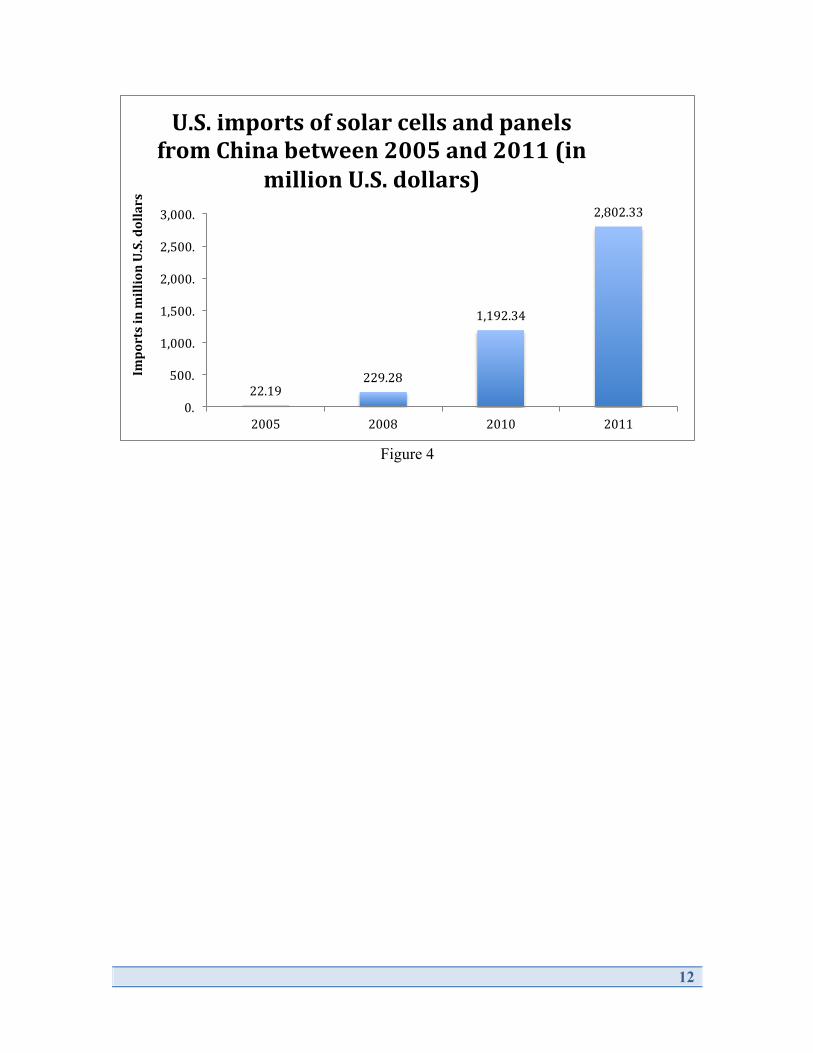

Between 2005 and 2011, solar cells and panel imports in the U.S. from China soared. In

the span of 7 years (2005-2011), U.S. imports of solar cells and panels from China

increased from 22.19 million to 2,802.33 million—a multiple of 126 (see Figure 4). In

2007, California introduced a “Solar Rebate Program.” The initiative aimed to increase

new solar generation capacity by 1,940 MW by the year 2016. The U.S. supplied about

43% of the solar panels for this program, while China supplied a mere 2%. However, by

2010, Chinese manufacturers supplied 42% of the solar panels while the U.S. producers’

market share had diminished to 15%.

8% 7%

5% 5%

5% 5%

4% 3% 3% 3%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Yingli (China) Trina Solar (China)

Sharp (Japan) Canadian Solar (China)

Jinko Solar (China) Renesola (China) First Solar (U.S.)

Hanwha-‐Solar One (China) JA Solar (China) Kyocera (Japan)

Market Share

Global market share of solar module manufacturers in 2013

12

Figure 4

22.19 229.28

1,192.34

2,802.33

0.

500.

1,000.

1,500.

2,000.

2,500.

3,000.

2005 2008 2010 2011

Imports in million U.S. dollars

U.S. imports of solar cells and panels from China between 2005 and 2011 (in

million U.S. dollars)

13

US Solar Industry

In the U.S., solar industry employment grew 53% from 2010-2013, creating 50,000 new

solar jobs. The installation subsector has seen the largest boom in this time frame, as

employment grew by 60% since 2010—that is an increase of 25,000 jobs. Installation

companies in the U.S. employ 69,658 workers, making installation the largest subsector

in the U.S. solar industry. In 2012, photovoltaic (PV) installations increased 41%, to

reach 4,751 MW. Solar was the second-largest source of new electricity generating

capacity, surpassed only by natural gas.

In November of 2013, employment in the U.S. solar industry totaled 142,698 workers,

representing a 20% increase from the previous year. For comparison, this is 10 times

overall growth in U.S. employment.

The solar industry is becoming a substantial source of new jobs for the U.S. economy.

77% of the 24,000 new solar workers (18, 211) workers since 2012, took new jobs and

did not fill existing job (see Figure 5).

14

Figure 5

The primary driver of industry growth has been the decreasing costs of solar products and

installations. Prices have steeply fallen by 44% from Q2 of 2011 to Q2 of 2012. Over the

course of 2012, installation prices decreased by 15%. Following this, prices have

stabilized yet are expected to keep declining regardless of the increase in worldwide

demand. The declining prices are a direct result of Chinese exports; because Chinese

firms were able to effectively cut costs, they set very competitive prices on their solar

products.

Now that the price of solar power has become more affordable, one of the main drivers

for consumer demand is not environmental, but financial. Competitive pricing has been a

key player responsible for these remarkable growth rates. In 2013, the cost of solar

modules dropped to $.70 per watt, which is less than a third of the cost in early 2010.

Solar industry jobs in 2013

Newly created positions

Existing employees given added solar responsibilities

15

Simultaneously, installed costs in the U.S. have fallen from $6.37 per watt in 2010 to

$3.00 per watt in 2012.

Figure 6

Referring to Figure 6, we see that the vast majority of American consumers are motivated

to purchase solar power to save money, while a mere 8% are motivated for environmental

reasons.

60.0% 17.2%

8.3% 3.1% 2.2% 2.2% 4.6% 2.5%

0% 10% 20% 30% 40% 50% 60% 70%

To save money Solar energy costs are now competitive with

To beneUit the environment and mitigate They know a neighbor, friend, or family To have power when the grid goes down

To make America more energy independent Other

Don't Know/Not Available

Consumer Demand Drivers

16

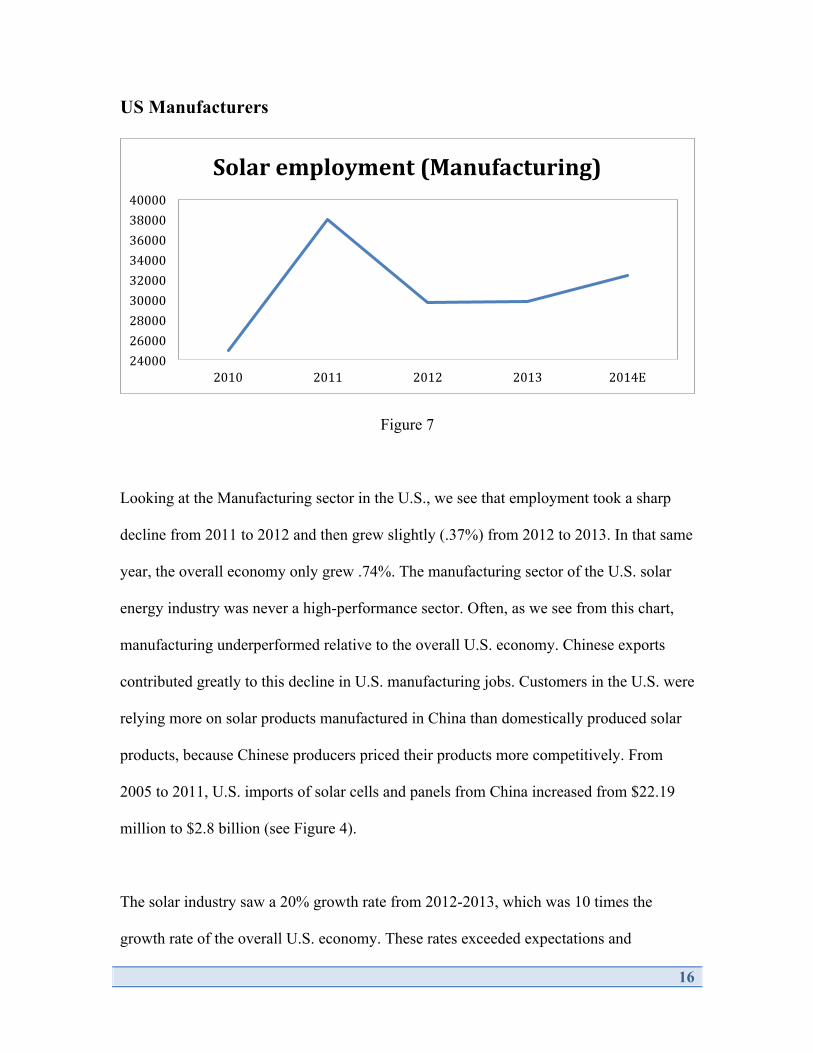

US Manufacturers

Figure 7

Looking at the Manufacturing sector in the U.S., we see that employment took a sharp

decline from 2011 to 2012 and then grew slightly (.37%) from 2012 to 2013. In that same

year, the overall economy only grew .74%. The manufacturing sector of the U.S. solar

energy industry was never a high-performance sector. Often, as we see from this chart,

manufacturing underperformed relative to the overall U.S. economy. Chinese exports

contributed greatly to this decline in U.S. manufacturing jobs. Customers in the U.S. were

relying more on solar products manufactured in China than domestically produced solar

products, because Chinese producers priced their products more competitively. From

2005 to 2011, U.S. imports of solar cells and panels from China increased from $22.19

million to $2.8 billion (see Figure 4).

The solar industry saw a 20% growth rate from 2012-2013, which was 10 times the

growth rate of the overall U.S. economy. These rates exceeded expectations and

24000 26000 28000 30000 32000 34000 36000 38000 40000

2010 2011 2012 2013 2014E

Solar employment (Manufacturing)

17

projections by a large margin and the growth rates in the U.S. are not expected to lose

momentum. The solar industry will remain to be one of the faster growing industries in

the nation and the industry will continue to play a major role in the U.S.’s economic

recovery. Referring to Figure 8, we see that going forward (through the year 2017),

revenue of the solar industry in the U.S. is expected to grow every year.

Figure 8

U.S. solar energy policy has played the key role in the development and growth of the

solar industry in the United States, both on the national and state level. In the case of

California, Governor Schwarzenegger announced a solar initiative called the “Million

Roofs Program” in 2004. Following this, in 2007 California announces the “Go Solar”

initiative.2 The initiative provided incentives for new energy efficient home construction.3

2 "About the California Solar Initiative (CSI) - Go Solar California." About the California Solar Initiative (CSI) - Go Solar California. N.p., n.d. Web. 08 Dec. 2014.

0.

50.

100.

150.

200.

250.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Revenue in million U.S. dollars

Revenue of the solar power industry in the United States from 2007 to 2017 (in

million U.S. dollars)

18

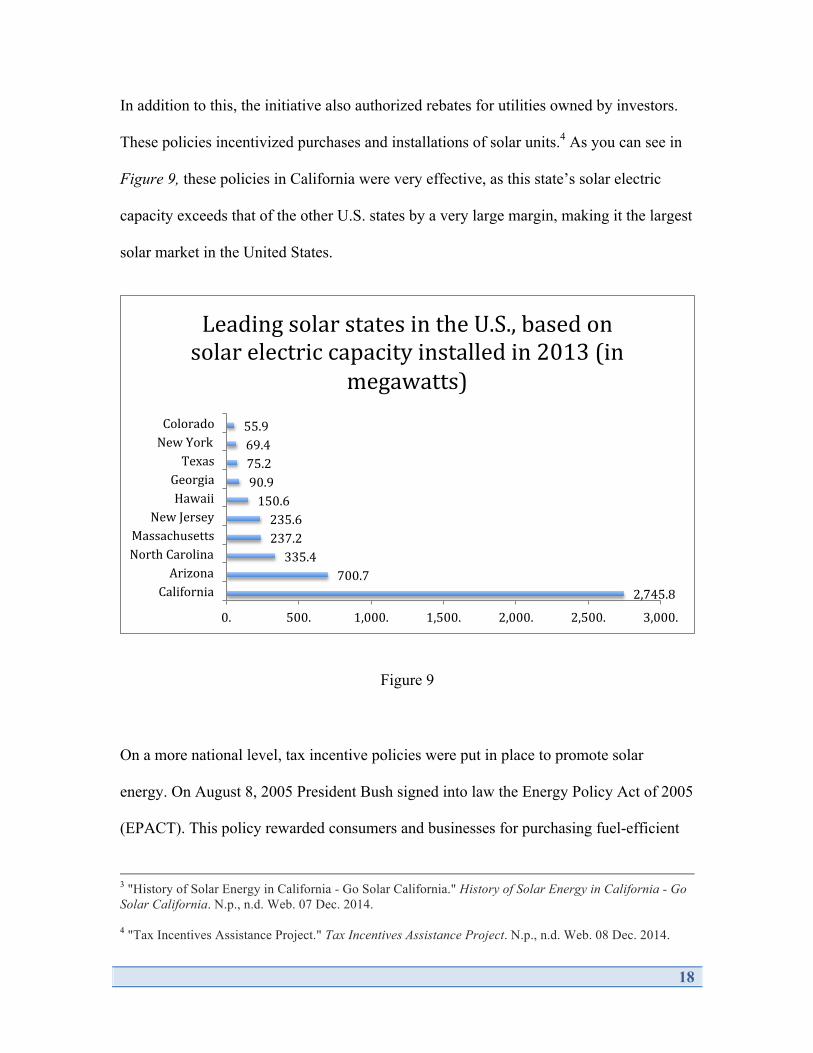

In addition to this, the initiative also authorized rebates for utilities owned by investors.

These policies incentivized purchases and installations of solar units.4 As you can see in

Figure 9, these policies in California were very effective, as this state’s solar electric

capacity exceeds that of the other U.S. states by a very large margin, making it the largest

solar market in the United States.

Figure 9

On a more national level, tax incentive policies were put in place to promote solar

energy. On August 8, 2005 President Bush signed into law the Energy Policy Act of 2005

(EPACT). This policy rewarded consumers and businesses for purchasing fuel-efficient

3 "History of Solar Energy in California - Go Solar California." History of Solar Energy in California - Go Solar California. N.p., n.d. Web. 07 Dec. 2014. 4 "Tax Incentives Assistance Project." Tax Incentives Assistance Project. N.p., n.d. Web. 08 Dec. 2014.

2,745.8 700.7

335.4 237.2 235.6

150.6 90.9 75.2 69.4 55.9

0. 500. 1,000. 1,500. 2,000. 2,500. 3,000.

California Arizona

North Carolina Massachusetts

New Jersey Hawaii Georgia Texas

New York Colorado

Leading solar states in the U.S., based on solar electric capacity installed in 2013 (in

megawatts)

19

products, by offering them federal tax credits.5 The policy restored a Federal Solar Tax

Credit, which permitted the purchaser of a solar panel to recoup up to 30 percent of the

cost of the project. The latest update on this federal tax break was announced on April 21,

2014. The federal tax incentives had expired at the end of 2013 and Congress was

debating the extension of the tax benefits. The future of the U.S. solar industry is

contingent on these policies. As we have seen, the industry will be greatly impacted

depending on how Congress ultimately votes on these policies.

5 "Energy.gov." Qualifying Advanced Energy Manufacturing Investment Tax Credit. N.p., n.d. Web. 08 Dec. 2014.

20

European Solar Industry

History of Solar in Europe

The worldwide growth of photovoltaics has increased exponentially in the last 20 years.

In 1996, the United States was the worldwide leader with installed PV capacity of about

88 megawatts. Japan eventually passed the U.S. and remained the worldwide leader until

2004, which is when Germany overtook it as the worldwide leader in installed capacity.

The passing of the German Renewable Energy Act in 2000 and the subsequent adoption

of feed-in tariffs enabled Germany to overtake Japan as the market leader. The act had

three main principles: 1. investment protection through guaranteed feed-in tariffs, 2. the

renumeration rates were not considered subsidies because they were not paid for by taxes,

but rather as a surcharge included in every consumer’s electricity bill, and 3. feed-in

tariffs in Germany would decrease in regular intervals to exert pressure on manufacturers

to innovate and create more efficient and less expensive technologies6. The German

Renewable Energy Act and the fixed feed-in tariffs associated with it provided a sense of

financial security for investors, generated more competition and was instrumental in

making Germany, and eventually Europe, the worldwide leader in the PV market. The

implementation of price incentives by Germany and other countries fueled a rapid

increase in solar installations, which led to Europe accounting for approximately 80

percent of the global demand for solar panels for much of the 2000s.

6 http://en.wikipedia.org/wiki/German_Renewable_Energy_Act

21

Market Development

Since 2009, total worldwide installed photovoltaic capacity has increased by over 115

GW to nearly 140 GW in 2013. Photovoltaic installations had a record year in 2013,

increasing by over 38 GW. Europe, accounting for close to 60% of worldwide PV

capacity in 2013, is the worldwide leader in terms of installed capacity. While Europe

remains the market leader, it is important to note that installed capacity in the Asia-

Pacific is growing rapidly, and Europe’s market share is down from previous years7.

7 “Global Market Outlook For Photovoltaics 2014-2018, Pg. 17”

22

8

The European market has grown rapidly in the last ten years and had a record year in

2011; it was unable to sustain that pace though due to the volatility of the economy in the

European Union and hostile policies towards PV in certain countries. This resulted in

installations of only about 11 GW in 2013, which was the lowest level since 2009.

Germany, which has been the worldwide market leader in terms of yearly PV

installations for much of the last 15 years dropped to fourth in 2013, but remained the

market leader in Europe. On a regional basis, Europe was second in the PV market

accounting for close to 30% of the installations after the Asia-Pacific Region.

The momentum of the European PV market until 2012 was the result of a few countries

spearheading installations. Due to the financial crisis, the European market stagnated

8 “Global Market Outlook For Photovoltaics 2014-2018, Pg. 17”

23

from 2008 to 2010 but began to grow rapidly again in 2010. Italy, France and Germany

accounted for much of the region’s growth in 2011, and strong installations from these

countries, as well as installations from the UK, Greece and Belgium led to continued

market development in 2012. In 2013, France and Belgium didn’t perform as well, but

development in other markets compensated for this. That same year though, a decline in

installations in Germany and Italy accounted for the contraction of the European market

to 11 GW. While Europe remains the market leader with over 80 GW of installed solar

capacity, it is clear from recent trends that the pace of installations is slowing down.

9

9 “Global Market Outlook For Photovoltaics 2014-2018, Pg. 21”

24

Current Market and Forecast

There are many market forces influencing the rate and feasibility of photovoltaic

installations. Some of these factors include government policies, and others include the

costs of PV installations compared to traditional sources of electricity. The decline in

many important European markets can be attributed to a mix of these factors, but the cuts

in government subsidies and cuts in feed-in tariffs for solar power have been a root cause

of the decline of solar in Europe.

When markets were booming, European governments were very liberal in their spending

on renewable energy and were determined to make them competitive with fossil fuels in

order to meet carbon-dioxide reduction targets. When solar panels were more expensive,

governments had to heavily subsidize the industry to incentive solar installations. But as

the cost of solar panels fell, and with the onset of the financial crisis, European

governments had no choice but to cut back on these subsides because the costs of these

subsidies were being passed on to consumers.

In 2010, Germany and Italy began pulling back on solar incentives, and then France

halted its solar feed-in tariffs that same year. While this decrease in solar subsidies

eventually led to a decrease in yearly installations and forced unprofitable firms to exit

the market, Germany cut back on these subsidies gradually to avoid a similar fate as

Spain which experienced a complete collapse of its market after it cut its subsidies. In

2008, Spain accounted for half of the world’s new solar installations in terms of wattage,

which was made possible via government subsidies. Due to the financial crisis though,

25

Spain cut back on subsidies which led to decreased demand for solar panels and resulted

in massive over supply and a decrease in prices.

Spain’s push into solar power began as an offshoot of its push to become a major player

in wind power. Because wind energy was cheaper than solar, the Spanish government

subsidized solar to make it more attractive. Spain’s spending on solar jumped from $214

million in 2007 to $1.6 billion in 2008. This resulted in a massive increase in its solar

capacity from 695 megawatts in 2007 to 3,342 megawatts in 2008. Due to the financial

crisis though, the Spanish government capped the amount of annual subsidized solar

power at 500 megawatts later that year. This resulted in a shrinking of Spain’s solar

power capacity and had ripple effects on companies that relied on Spain as an end

market. Chinese firms such as Yingli Green Energy, and LDK posted huge quarterly

losses as a result of reduced demand from Spain10.

In addition to a decrease in subsidies and cuts in feed-in tariffs, the rise of China poses a

threat to the European market. China emerged as a dominant industry player and

produced at least half of the world’s solar panels in 2010. Chinese manufacturers have

flooded the market with cheap panels which have put some European manufacturers out

of business. Because of this, European and American firms have filed complaints alleging

that the Chinese government is unfairly subsidizing Chinese manufactures with low-

interest loans and cheap power to run their plants. This has led to tensions between

European, American and Chinese authorities which have each imposed tariffs, and

counter-tariffs, respectively. 10 “http://online.wsj.com/articles/SB125193815050081615”

26

To summarize, the market for PV installations in Europe peaked in 2011 with

approximately 22 GW in installations. This was followed by 17.7 GW of installations in

2012 and 11 GW of installations in 2013, which was the lowest since 2009. Some of this

decrease can be attributed to the financial crisis and a decrease in subsidies, but what is

also clear is that Europe is a very volatile market, and outside of Germany, no European

country has managed to consistently increase annual PV installations as shown in the

above graph. Given the expectation of continued decreases in feed-in tariff programs by

some European countries, as well as the emergence of markets in the Asia-Pacific, it is

reasonable to assume that the European market will hold a smaller percentage of the

overall worldwide PV market11.

12

11 “Global Market Outlook For Photovoltaics 2014-2018, Pg. 31” 12 “Solarbuzz Regional Downstream PV Market”

27

Tariffs in Europe

In 2012, the European Union began to investigate Chinese solar manufacturers due to

allegations of dumping, which is the practice of selling a product below its fair value.

These allegations were brought forth by European solar panel producers who were

struggling to compete with Chinese producers whose panels were approximately 45%

cheaper than those made in Europe. European producers have alleged that unfair support

from the Chinese government enabled Chinese solar panel producers to capture close to

70 percent of the market in Europe. The EU’s investigation found that government aid

enabled these Chinese manufacturers to sell their products close to 90 percent below fair

market value, which enabled them to capture such a large share of the market. This led to

the imposition of duties in June of 2013 of 11.8 percent on Chinese imports, which would

have risen to 47.6 percent in August had the Chinese Chamber of Commerce and the EU

failed to negotiate a settlement. While European solar manufacturers lobbied very

aggressively for tariffs against Chinese imports and argued that tariffs would enable them

to compete more effectively in the market, others believed that tariffs on Chinese imports

would end up causing more harm to the European industry and suggested that the two

sides come to a compromise. This led to a settlement.

The Chinese Chamber of Commerce and the EU reached a two-part settlement. The first

part of the settlement initially set a minimum price floor of €0.74 per watt before a 47.6

percent anti-dumping tariff would take effect. The price was then reduced to €0.56 per

watt. The second part of the settlement set a volume limit on Chinese imports at 7 GW.

This means that the 90 Chinese companies who signed the agreement were allowed to

28

export up to 7 GW into Europe in 2013 at a minimum price of €0.56 per watt before the

tariff would take effect. The Chinese companies who did not sign the agreement have to

pay the 47.6 percent tariff but they are not subject to the minimum price. An important

thing to note from the below graph is that demand was predicted to shrink from 17 GW in

2012 to 11.6 GW in 2013. Another important thing to be aware of is that the volume cap

on Chinese imports was reduced from 7 GW to 5.8 GW after the European Photovoltaic

Industry lowered its installation forecast for 2014 from 11.5 GW to approximately 9.6

GW, and that the price floor was lowered from €0.56 per watt to €0.53 per watt due to

lower average module prices.

13

The settlement reached by the EU and the Chinese Chamber of Commerce dissatisfied

EU solar-panel producers, who wanted higher minimum import prices and a lower

volume limit. EU ProSun even resorted to filing a lawsuit to try and void the settlement.

13 “GTM Research”

29

Mike Nitzschke, President of EU ProSun said, “these EU solar tariffs are the first ray of

hope for European companies to reenter the market with high-value products”14.

Following these trade disputes, the Chinese magazine Ecns.cn reported that China’s

exports of crystalline photovoltaic products fell sharply and revenue from exported solar

cells and solar modules to Europe declined by 62 percent to $3.7 billion15. According to

GTM Research, Chinese manufacturers such as Trina and Yingli expected first quarter

2014 shipments to slump by at least 30 percent compared to the prior quarter. So far it

appears that the minimum price level and volume limits on Chinese manufacturers has

been successful in raising the price of solar panels in Europe, and it appears to be

decreasing the market power of Chinese manufacturers, but it is also having other effects.

According to Jinko Solar’s Director for Europe, Frank Niendorf, the minimum price level

is delaying grid parity in important European markets. He says that prices have actually

gone down due to the minimum price level and that grid parity in Europe would be

achievable if Jinko was able to offer modules at the same price as other markets.

14 “http://www.bloomberg.com/news/2013-12-02/u-nations-approve-pact-with-china-on-solar-panel-trade.html” 15 ” http://www.pv-magazine.com/news/details/beitrag/eu-lowers-chinese-pv-import-volume_100014771/#axzz2yUQqu22O”

30

US Trade Tariffs

Understanding Tariffs presented by Department of Commerce

The US-China Solar Trade War dates to October 2011, when the US subsidiary of

German-based SolarWorld, representing several other US solar manufacturers, filed a

petition with the Department of Commerce and (DOC) and the International Trade

Commission (ITC). SolarWorld claimed that Chinese solar manufacturers were receiving

massive illegal subsidies from the Chinese government in the form of funds for land,

electricity, material inputs, financing at below market rates, and even direct financial

support and other preferential policies. Furthermore, SolarWorld claims that Chinese

solar manufacturers were illegally “dumping” solar cells into the US market and prices

below production costs. The petitioners claimed the combination of the illegal subsidies

and dumping severely damaged employment, pricing, production, and shipment with

respect to the domestic solar industry in the United States.16 This has been followed by a

long and complicated process of administering tariffs against Chinese manufacturers who

specifically export either solar cells or solar modules17 to the US.

Essentially, the petition asked for relief for domestic manufacturers by preventing unfair

practices by Chinese producers of solar cells and modules. The Department of Commerce

(DOC) is the department of the US government tasked with promoting economic growth.

The DOC responded to the petitions by imposing tariffs against the Chinese firms

16 “U.S. Manufacturers of Solar Cells File Dumping and Subsidy Petitions Against China,” Coalition for American Solar Manufacturing, 10/19/2011 17 A solar module is an assembly of solar cells that have been electrically interconnected and encapsulated.

31

involved in the illegal subsidies and dumping provided by local Chinese governments.18

The tariffs involved include “Countervailing Duties” (CVD)19 and “Anti-dumping

Duties” (AD)20. CVDs (also known as anti-subsidy duties) are tariffs imposed under the

World Trade Organization (WTO) rules to neutralize the negative effects of subsidies

once a foreign country is found guilty of subsidizing its exports, which hurts domestic

producers in the importing country. ADs are protectionist tariffs imposed on foreign

imports that are believed to be priced below market value; in the US, they typically

exceed 100%.

The DOC can justify imposing tariffs on Chinese imports for several reasons. First and

foremost, it is undoubtedly going to aid hurting US manufactures of solar panels. If the

rapid reversal of market share gains of Chinese producers in the US market was due to

illegally subsided and dumped Chinese exports, the DOC has the prerogative to step in

and protect domestic industry. This can be seen in 2007; US manufacturers were

responsible for 43% of solar panels for the California Solar Rebate Program vs. Chinese

companies’ 2% share. However, just three years later in 2010, Chinese companies

captured a 42% market share while US firms fell down to 15%21.

18 SolarWorld provides a list of Chinese firms involved in the unfair practices to the DOC. 19 “Countervailing Duties,” Wikipedia 20“Anti-Dumping Duty,” Investopedia 21 Bullis, Kevin, “Solar’s Great Leap Forward,” MIT Technology Review, June 22, 2010

32

The first is US-based Solyndra – it received more than $500 million in a federal loan

guarantee from the Department of Energy along with a $25 million tax break from

California’s Alternative Energy and Advanced Transportation Financing Authority.

Nevertheless, it filed for Chapter 11 bankruptcy in 2011 and laid off all 1,000 of its

employees. Next is Japan-based Shar Solar – it withdrew almost entirely from solar

manufacturing after being bailed out by the Japanese government. Although it led the

world in revenue in solar production in 2009, its productions costs were still 30-40%

higher than its cheapest Chinese and Taiwanese competitors by 2011; its business was

not sustainable at this rate. It eventually closed its marketing operations in the US and

Europe22. Lastly, we have German-based Q-Cells – for years, it had been the largest

global maker of solar cells and an investor favorite, constantly meeting or exceeding Wall

Street expectations. By 2012, it filed for bankruptcy23. These scenarios are to serve as

examples that even the most well established firms could fall. In this tumultuous business

climate for the solar sector, the DOC reviewed the SolarWorld petition.

Brief History on US-imposed Tariffs on Chinese Exporters

In late 2011, the DOC and ITC began investigating claims made by SolarWorld against

Chinese solar manufacturers. By December 2011, ITC was first to issue an affirmative

preliminary determination, meaning that both the subsidies and dumping from China

indeed hurt the US solar industry. By May 2012, the DOC shortly followed suit; it issued

a preliminary finding and began imposing duties on Chinese products. By October 2012,

22 Shah, Sneha, “Sharp to Bail Out of Solar As It Gets Bailed Out by Japanese Banks,” Green World Investor, October 11, 2012 23 Schultz, Stefan, “Twilight of an Industry: Bankruptcies Have German Solar on The Ropes,” Der Speigel, April 3, 2012

33

DOC had issued its affirmative final determination and decided to continue the CVD and

AD tariffs against the Chinese exporters; DOC discovered they had “sold cells in the

United States at dumping margins ranging from 18.32 to 249.96 percent [and] Chinese

producers/exporters have received countervailable subsidies of 14.78 to 15.97 percent.”24

Nevertheless, the difficult times for US solar manufacturers reawakened shortly later; the

Chinese exporters managed to find a loophole. The final determination could be evaded

by many of the producers by “commissioning manufacturers in other countries to

partially or fully produce solar photovoltaic cells for assembly into solar panels back in

China”.25 Imports headed to the US from China contained about 70% Taiwanese cells,

according to state-controlled Chinese media. It seems that this battle would continue

indefinitely – except that SolarWorld again submitted a petition.

Just recently, measures to fix this loophole have been taken by the DOC – this past

summer, the DOC announced its affirmative preliminary determination for both CVDs

for solar products from China26 and ADs for solar products from China and Taiwan27.

The DOC calculated a preliminary subsidy rate ranging from 18.56-35.21%, depending

on the specific Chinese exporter with all those not described in the tariff having a rate of

26.89%.

24 Dept. of Commerce & Int’l Trade Admin., Fact Sheet: Commerce Finds Dumping & Subsidization of Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled into Modules from the People’s Republic of China (2012) 25 Wesoff, Eric, “Big Tariffs in US-China Solar Panel Trade Case; No Settlement in Sight,” Green Tech Media, June 4, 2014 26 Dept. of Commerce & Int’l Trade Admin., Fact Sheet: Commerce Preliminarily Finds Countervailable Subsidization of Imports of Certain Crystalline Silicon Photovoltaic Products from the People’s Republic of China (June 3, 2014) 27 Dept. of Commerce & Int’l Trade Admin., Fact Sheet: Commerce Preliminarily Finds Dumping of Imports of Certain Crystalline Silicon Photovoltaic Products from China and Taiwan (July 25, 2014)

34

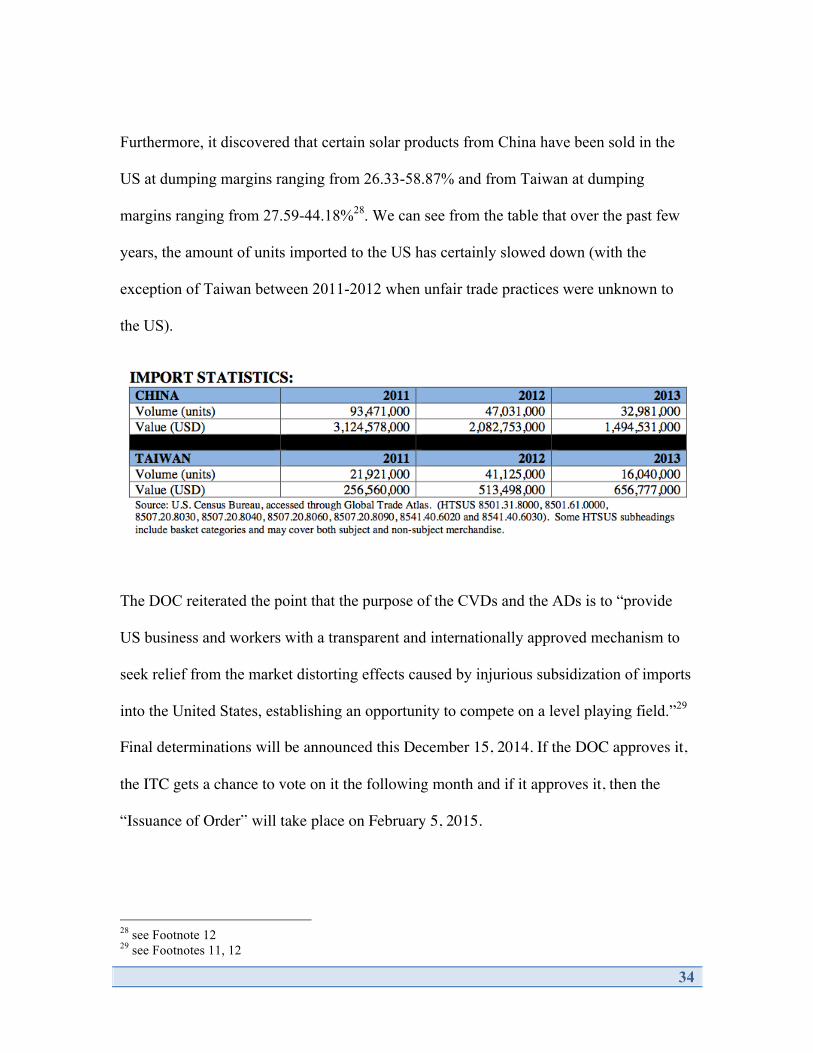

Furthermore, it discovered that certain solar products from China have been sold in the

US at dumping margins ranging from 26.33-58.87% and from Taiwan at dumping

margins ranging from 27.59-44.18%28. We can see from the table that over the past few

years, the amount of units imported to the US has certainly slowed down (with the

exception of Taiwan between 2011-2012 when unfair trade practices were unknown to

the US).

The DOC reiterated the point that the purpose of the CVDs and the ADs is to “provide

US business and workers with a transparent and internationally approved mechanism to

seek relief from the market distorting effects caused by injurious subsidization of imports

into the United States, establishing an opportunity to compete on a level playing field.”29

Final determinations will be announced this December 15, 2014. If the DOC approves it,

the ITC gets a chance to vote on it the following month and if it approves it, then the

“Issuance of Order” will take place on February 5, 2015.

28 see Footnote 12 29 see Footnotes 11, 12

35

Regarding our data, you will see shortly that we use tariff figures from 2012 and not the

more recently published 2014 for several reasons. First, the final determination hasn’t

been announced yet, so we cannot use a true, reflective figure due to this lack of

information; we are better of working with historical information. Second, we want to

anticipate changes before and after the introduction of the tariff on Chinese

manufacturers. Because these new preliminary determinations were announced so

recently, accurate and representative data revolving changes due to the new tariff rates

has been difficult to find. Lastly, the changes between the two sets of tariffs are not

expected to change much; a Vice President from GTM Research said the following in

regard to the most recent summer update about the tariffs: “Unless the DOC revises the

scope prior to its final determination, there is no question that tariffs imposed in this case

will have a larger impact than those already in place from the 2012 ruling.”30 Therefore,

we are in confident in using known, correct 2012 figures to gain us a deeper

understanding of the affect of tariffs on the pricing and demand of solar products in the

United States.

Criticism / Concerns with US Trade Tariffs

SolarWorld’s requests for the DOC to administer tariffs to Chinese exporters who

perform in unfair trade practices in the US solar market are opposed mainly by the

Coalition for Affordable Solar Energy (CASE), the Solar Energy Industries Association

(SEIA), and others who believe that the tariffs do more damage than provide well-being

for players in the US solar market. The two aforementioned organizations root their

30 Wesoff, Eric, “SolarWorld Wins Again: Big Anti-Dumping Tariffs in US-China Solar Panel Trade Case,” Green Tech Media, July 25, 2014

36

opposition to the tariffs because they believe it will immediately increase the price of

solar power and cost American jobs in one of the fastest-growing sectors of the US

economy31. After the second round of preliminary determinations for ADs occurred on

June 4, 2014, SEIA came out with the following statement:

“These damaging tariffs will increase costs for US solar consumers and, in turn, slow the adoption of solar within the United States. Ironically, the tariffs may provide little to no direct benefit to the sole petition SolarWorld, as we saw in the 2012 investigations. It’s time to end this needless litigation with a negotiated solution that addresses SolarWorld’s trade allegations while ensuring the continued growth of the US solar market”32

These organizations are more concerned with resolving the global issue of moving

towards renewable energy sources; they want everyone to work together to find a

solution that benefits all segments of the industry. Tariffs feature a dead-weight loss that

is both costly and divisive; essentially, all they do is hurt relationships among people.

Although the tariffs from 2012 and especially those from more recent times have not

fully been able to give us a clear understanding of their effects, one thing is collectively

agreed upon by everybody: “pricing for Chinese modules shipped to the US is highly

likely to increase starting in July 2014.”33 Besides the immediate effects on pricing, much

of the consequences regarding the tariffs have not yet been realized. Only time will tell us

what is to come next.

31 Wesoff, Eric, “Big Tariffs in US-China Solar Panel Trade Case; No Settlement in Sight,” Green Tech Media, June 4, 2014 32 Wesoff, Eric, “Big Tariffs in US-China Solar Panel Trade Case; No Settlement in Sight,” Green Tech Media, June 4, 2014 33 Wesoff, Eric, “SolarWorld Wins Again: Big Anti-Dumping Tariffs in US-China Solar Panel Trade Case,” Green Tech Media, July 25, 2014

37

Besides the obvious benefit of the tariffs – enhanced domestic manufacturing in the solar

space – experts have made claims on possible future negative impacts. One economic

implication the tariffs possess is trade diversion, which is described as the shift from

trade with one exporting country to trade with another exporting country34. Studies

show35 that when the US imposes CVDs and ADs against one country, other countries

begin producing the tariffed product at a higher rate, which creates a niche market for

other foreign countries to exploit the US domestic market at the expense of US

manufacturers. So, rather than motivating the US producers to manufacture the tariffed

good, it is possible that the US could turn to a different country that produces that good

since (we now assume) quantity will be readily available elsewhere. This has been seen

in 2005 with many Chinese wooden furniture manufacturers; those manufactures moved

their facilities elsewhere (Vietnam, Indonesia, etc.) in order to avoid the heavy tariffs.36

At the end of the day, trade diversion continues to harm US industry because US

consumers still receive the good but not from domestic suppliers.

34 Carrier, Paul, An Assessment of Regional Economic Integration Agreements After the Uruguay Round, 9 N.Y. Int’l L. Rev. 1, 15 (1996) 35 Higgins, Andrew, “From China, an End Run Around US Tariffs,” The Washington Post, May 23, 2011 36 see Footnote 20

38

Chinese Counter-Tariffs

Background

In May of 2012, the U.S. Department of Commerce placed a 31 percent anti-dumping

tariff on solar panels produced with solar cells made in China. This tariff was put in place

after the U.S. Trade Commission came to the conclusion that the U.S. solar industry was

being harmed by imports from Chinese manufacturers who were being subsidized by the

Chinese government. In response to this, the Chinese Ministry of Commerce announced

that it would impose counter-tariffs on imports of polysilicon from U.S. manufacturers.

Similarly, the European Union imposed tariffs on Chinese solar imports in June of 2013.

Immediately after the EU announced this, China’s commerce ministry announced that it

would launch an investigation into European wine imports.

Effect of Counter-Tariffs

While imposing tariffs on Chinese importers may make it easier for U.S. solar companies

to compete, the tariffs will also make it more expensive for U.S. consumers by pushing

up the price of solar power, which will reduce demand. This decrease in demand will

limit new solar projects, as well as lead to a reduction in jobs. Chinese counter-tariffs

have also affected U.S. exporters of polysilicon. Hemlock Semiconductor and AE

Polysilicon are just two of the U.S. polysilicon manufacturers expected to be affected by

the Chinese tariffs, which could be as high as 57 percent. In January of 2013, Hemlock

Semiconductor announced that they would lay off approximately 400 employees in

39

Michigan and Tennessee. The threat of Chinese tariffs on polysilicon was one of the

factors that led to this. Andrew Tometich, president of Hemlock Semiconductor said,

“The unresolved trade disputes among the U.S., China and Europe are a major factor in

Hemlock Semiconductor's actions as the threat of tariffs on U.S. polysilicon imported

into China has significantly decreased orders from China, which is home to one of the

largest markets for our products."37

In addition to this, the companies that the U.S. tariffs will help only represent a small

percentage of the American solar industry. Approximately 95 percent of solar industry

jobs in the U.S. are with upstream producers of capital equipment, polysilicon

manufacturers and various other manufacturers of solar components. Free trade with

China is crucial to preserving these jobs. China is the largest consumer of many of

America’s solar products. “According to a Brattle Group analysis commissioned by

Coalition for Affordable Solar Energy, America could lose 11,000 jobs if Beijing were to

impose tariffs on American polysilicon. And trade battles between these two

governments could encourage other countries to raise protectionist barriers”38.

37 “http://www.hscpoly.com/content/hsc_comp/Hemlock_Semiconductor_Announcement.aspx” 38 “http://www.wsj.com/articles/SB10001424052702303816504577304841180770350”

40

Data Analysis

Cost-Benefit Analysis – An Overview

Cost-benefit analysis includes five components:

1) The with and without principle

2) Present value

3) Whose benefits and whose costs

4) Quantifying the unquantifiable

5) Allowing for uncertainty

In our data analysis, we will weigh the benefits and costs of United States tariffs placed

on Chinese solar PV module imports.

1) We will first model the relationship between price of solar and quantity demanded

based on observed data gathered from 2004 to 2013. From the data, we will find an

equation for quantity of solar demanded as a function of price. Because the industry

average selling prices are taken from the reported selling prices of each firm’s Form 10-K

or 20-F, the prices exclude US import taxes. Using the equation we derive for quantity

demanded, we will adjust the price by the tariff for 2012 and 2013, since the tariff was

imposed starting in 2012. We will input these new prices into the equation for quantity

demanded, which allows us to calculate and compare revenues with and without tariffs in

2012 and 2013.

41

2) Because the tariffs were imposed in 2012, we will analyze data from 2012 and 2013.

The with and without principle stands on historical data - we will compare revenues with

and without tariffs, both of which can be calculated using our model, for the years 2012

and 2013. We will quantify the costs and benefits we would have received had the tariff

not been imposed at all and compare it to the costs and benefits of having the tariff.

Therefore, present value analysis is not needed for the exercise and as such, there is no

discounting involved.

3) The benefits and costs apply to United States consumers, the United States

government and Chinese producers. Change in revenue will be broken down into the

increase in US government revenue and resulting revenue foregone by Chinese

producers, which aggregates to the total change in revenue due to the imposition of

import tariffs. Other benefits and costs that need to be quantified are the social cost of

using carbon-heavy energy sources rather than solar and the dollar amount of forgone

solar employment salaries in the US, both of which stem from reduced demand due to

higher price of solar with tariffs. By summing the total costs and benefits of revenue

change, social cost of carbon, and forgone US solar job salaries, we will see the net cost

of the imposition of tariffs, in dollars, over the years 2012 and 2013, which allows us to

make an argument for their repeal.

4) Because our analysis relies on historical data, including the historical average selling

price of solar, historical capacity of solar PV modules installed, historical tariff

information and historical quantity of solar jobs, it consists of discrete numbers rather

than ranges, making it so there are no estimates used as inputs in the data analysis.

42

Regarding the social cost of carbon emission, which is seemingly unquantifiable, we use

a published average price per metric ton. We believe using an average is appropriate

because it incorporates a range of estimates from numerous established research

authorities. This idea of using an average also applies to foregone salaries from US solar

jobs, for which we use the median of a large data set of salaries from US solar.

5) Since we are using historical data, much of the uncertainty of the variables we use,

such as the price of modules, installed solar PV capacity, and US solar employment, is

removed. We choose to use past data rather than make future predictions because solar

energy is highly dependent on government incentives, consumer preferences and

geopolitical factors, making it so that it is difficult to accurately estimate future demand

for solar PV modules. This causes limitations in our model for quantity of solar

demanded as a function of its price because it is both subject to historical price trends and

uses price as its only input. Because of this the model cannot account for factors like

consumer taste and the movement for a greener world, which is illustrated in the

deviation between the output quantity demanded of our model for the year 2013,

inclusive of tariff, versus the observed quantity demanded in the US for the year 2013,

inclusive of tariff.

43

Approximating the Demand Curve

From 2004 to 2013, we will take a look at historical data on industry average selling price

of solar and quantity of solar PV module energy demanded in the US. We will then

remove the time variable, and observe how price and quantity relate to one another. We

will treat this as an approximation to the demand curve, and we will calculate a formula

for quantity demanded Q as a function of a given price P.

Price and Year

In order to quantify how tariffs affected the revenue generated from the sale of PV

modules, we must first examine the relationship between the average selling price of PV

modules and the quantity of PV modules demanded at each price level, measured by total

annual installations in the United States in watts. Due to the boom of solar in the early

2000s, many key players in the space went public, particularly Chinese firms. We can

find the average selling price of PV modules by firm within each public firm’s financial

statements. We then aggregate this data to see the trend in falling solar prices by year.

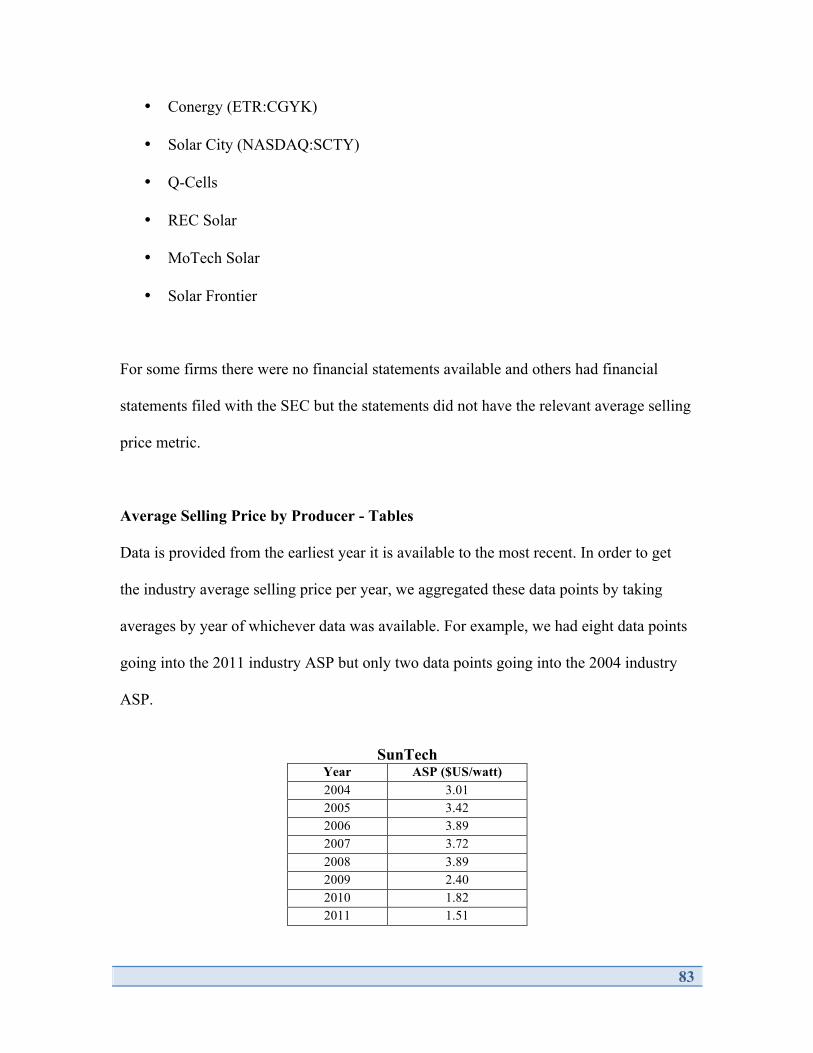

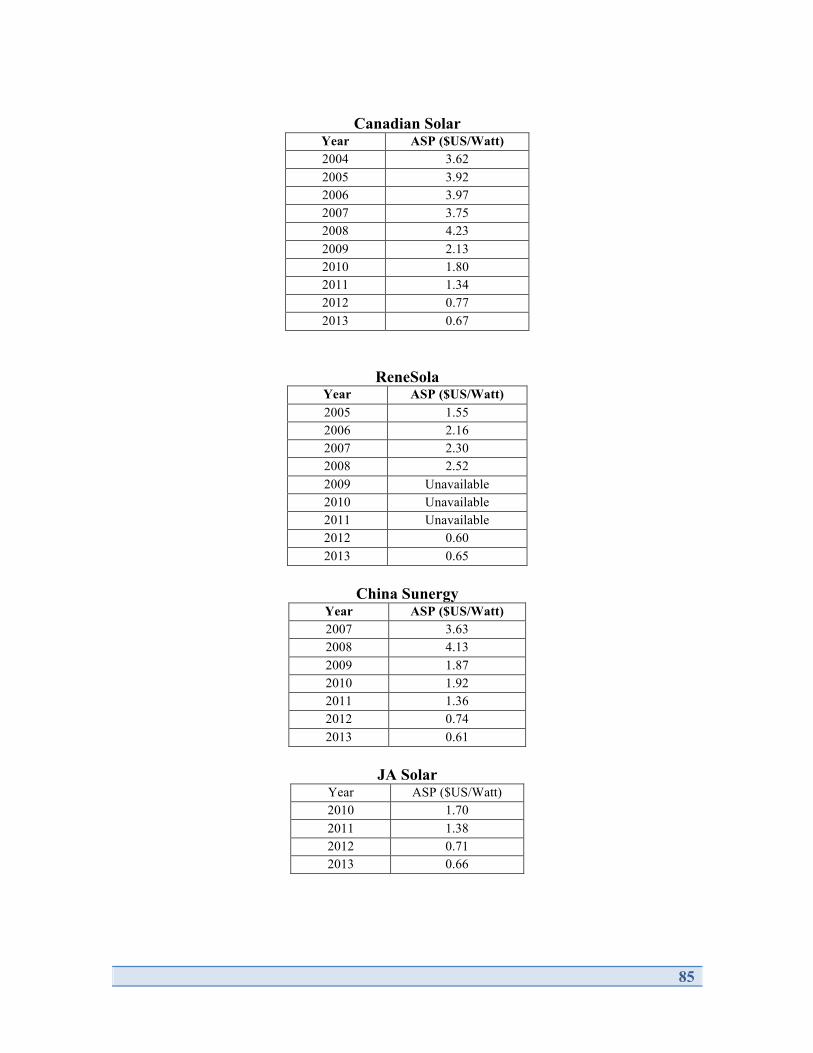

The nine largest key players we used were as follows:

• SunTech Power Holdings Co. (OTCMKTS:STPFQ)

• Trina Solar Limited (NYSE:TSL)

• Hanwha SolarOne Co. Ltd. (NASDAQ:HSOL)

• Yingli Green Energy Hold. Co. Ltd. (NYSE:YGE)

• JinkoSolar Holding Co., Ltd. (NYSE:JKS)

• Canadian Solar Inc. (NASDAQ:CSIQ)

• ReneSola Ltd. (NYSE:SOL)

44

• China Sunergy Co. Ltd. (NASDAQ:CSUN)

• JA Solar Holdings Co., Ltd. (NASDAQ:JASO)

See appendix for business overviews of each firm we analyzed as taken from the 10-

K’s39.

All PV module average selling price (ASP) data is taken from each firm’s Form 10-K or

20-F, based on which country the firm is incorporated in. The data’s range is from the

earliest year in which it is publicly filed by the SEC, typically between 2004 and 2006,

through the most recent year for which it is available.

All average selling price data is displayed in its USD equivalent. In some financial

statements, the ASP is displayed in $US/watt whereas in others it is displayed in a foreign

currency per watt. In order to make conversions where appropriate, the average exchange

rate for the relevant year was used – this number can be found in the exchange rate

section of each financial statement. For example, to convert a 2007 data point in

RMB/watt to $US/watt, we used the conversion factor listed as average “RMB per US

Dollar Noon Buying Rate” for the year 2007. We did not consider the high, low or period

end exchange rate. All numbers are in average selling price of PV modules, as these

constitute the greatest portion of revenue for each firm as compared to the sale of

individual PV wafers.

39 http://www.sec.gov/edgar/searchedgar/companysearch.html

45

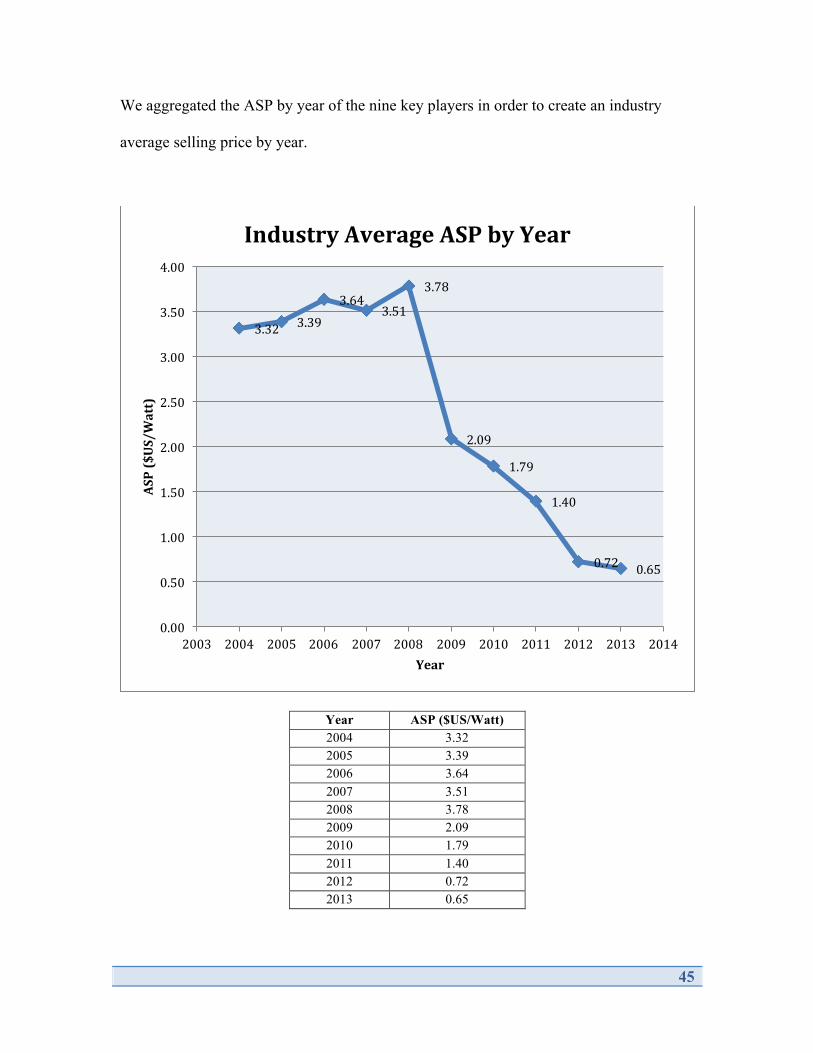

We aggregated the ASP by year of the nine key players in order to create an industry

average selling price by year.

Year ASP ($US/Watt) 2004 3.32 2005 3.39 2006 3.64 2007 3.51 2008 3.78 2009 2.09 2010 1.79 2011 1.40 2012 0.72 2013 0.65

3.32 3.39

3.64 3.51

3.78

2.09

1.79

1.40

0.72 0.65

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

ASP ($US/Watt)

Year

Industry Average ASP by Year

46

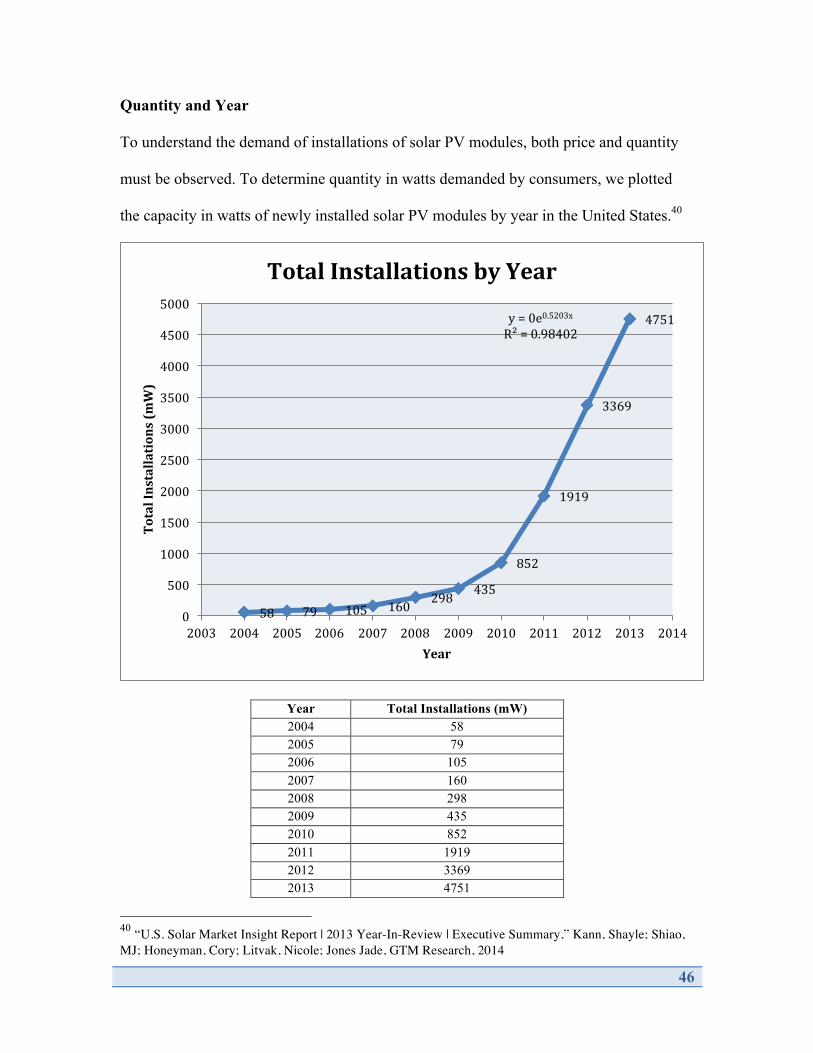

Quantity and Year

To understand the demand of installations of solar PV modules, both price and quantity

must be observed. To determine quantity in watts demanded by consumers, we plotted

the capacity in watts of newly installed solar PV modules by year in the United States.40

Year Total Installations (mW) 2004 58 2005 79 2006 105 2007 160 2008 298 2009 435 2010 852 2011 1919 2012 3369 2013 4751

40 “U.S. Solar Market Insight Report | 2013 Year-In-Review | Executive Summary,” Kann, Shayle; Shiao, MJ; Honeyman, Cory; Litvak, Nicole; Jones Jade, GTM Research, 2014

58 79 105 160 298 435

852

1919

3369

4751 y = 0e0.5203x R² = 0.98402

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total Installations (mW)

Year

Total Installations by Year

47

Price and Quantity à Demand

Based on the historical data regarding the industry average selling price, we observe that

ASP trends downward as time passes. Meanwhile, as time passes, the capacity of newly

installed solar PV modules trends upward. By aligning capacity demanded and average

selling price by year, we can remove the time variable and see a trend between price and

capacity: as price decreases, the capacity in watts of PV modules demanded increases.

Thus, we have created an approximation of the demand curve of capacity of installed

solar PV modules as a function of their average selling price.

y = 3.2836e-‐4E-‐10x R² = 0.90879

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

0 1E+09 2E+09 3E+09 4E+09 5E+09

ASP ($US/Watt)

Solar PV Capacity (Watt)

Demand of Solar PV Capacity

48

Total Installations (W) ASP ($US/Watt) 58000000 3.32 79000000 3.39

105000000 3.64 160000000 3.51 298000000 3.78 435000000 2.09 852000000 1.79

1919000000 1.40 3369000000 0.72 4751000000 0.65

Formula of Quantity Demanded as a Function of Price

We applied an exponential regression to this approximation of the demand curve of solar

PV modules in watts because it had the highest correlation coefficient of R2 = 0.90879.

The resulting regression provided us an equation that represented the relationship

between the quantity of solar demanded, in watts, and the average selling price of solar,

in $US/watt. The equation is as follows:

Where P = Average Selling Price of Solar PV Module;

Q = Capacity of Solar PV Module Demanded

e = Euler’s number

This function models price as a function of quantity demanded. However, quantity

demanded as a function of price is more applicable to the real world, so we solve for the

inverse, which is as follows:

49

Where Q = Capacity of Solar PV Module Demanded

P = Average Selling Price of Solar PV Module

We now have quantity demanded as a function of price, so given any input price, we can

estimate the quantity demanded of solar PV capacity.

50

Tariffs

We will analyze the effect of the tariff on total revenue generated in 2012 and 2013. We

will use the tariff amount of 31% because it is about equal to the average of the

countervailing subsidy range of 14.78% – 15.97% and the antidumping subsidy of 47%;

these are the two components of the tariff.

Revenue in 2012 without Tariff

By multiplying an ASP with the quantity demanded at that ASP, we get the total revenue

generated at each selling price. We can now move forward with our analysis in

determining how total solar revenue is impacted by tariffs.

Tariffs were put into place starting in 2012, so with our model and our ASP data from

2012 and 2013, we can compare the total revenue generated in a scenario with tariffs to a

scenario without tariffs for those two years.

For 2012, we have the industry ASP of $0.72/watt. We plug this P into the Q (P) function

above and obtain the total installation amount of 3,793,611,121 watts, or approximately

3,794 megawatts. This yields the total revenue from solar sales in 2012 as

$2,731,400,007 or about $2.73 billion.

51

Revenue in 2012 with Tariff of 31%

Now we consider the case with a tariff of 31%. The average selling price published in

each 10-K and 20-F does not reflect the additional cost of the tariff, so we tack on the

tariff to the industry ASP for 2012 by using the function Q (1.31P). This yields the new

quantity of installations demanded of 3,119 megawatts, which is 17.8% lower since the

tariff causes a greater cost to consumers, driving them to demand fewer units of solar and

use other sources of energy. We then multiply the price with the tariff tacked on by the

new, lower installation quantity demanded and get the total revenue of solar sales with

tariff in 2012 as $2,941,410,020, about $2.94 billion.

Analysis of Revenue Increase

Of the $2.94 billion in revenue, 31%, or about $696 million goes to the US government,

leaving the producers with revenue of $2.25 billion. For 2012, the tariff causes the

producers to lose about $480 million relative to the total solar sales revenue without the

tariff. However, we must note that the total revenue generated with the tariff by both the

government and the producers is greater than without the tariff due to the elasticity of the

equation. We can now quantify the cost of the tariff in terms of total producer revenue

lost from the imposition of the tariff in 2012 by taking the difference of the two total

revenue numbers. Therefore we conclude that in 2012, the total foregone revenue to

producers of solar due to imposition of a tariff – i.e., the opportunity cost – is $486

million.

52

Revenue in 2013 without Tariff

We conduct the same analysis for 2013, where the industry ASP is $0.65. Using the Q (P)

function, we get the installation quantity demanded of 4,049,308,244 watts, or 4,049

megawatts. The total revenue generated pre-tariff is $2,632,050,359, or about $2.63

billion. We again note that all of this revenue goes to producers.

Revenue in 2013 with Tariff of 31%

With the imposition of the 31% tariff, 2013 Q (1.31P) is 3,374,240,401 watts, or 3,374

megawatts demanded. The total revenue generated post-tariff is then $2,873,165,701 or

about $2.87 billion.

Analysis of Revenue Increase

Of this, producers receive about $2.19 billion and the US government receives about

$680 million. In 2013, the total foregone revenue to producers of solar due to the

imposition of a tariff – i.e. the opportunity cost – is $439 million. Again, we recognize

that while the total revenue generated with a tariff is greater than that generated without a

tariff for both years, the tariff causes the producers to forego over 16% of revenue both

years. It redistributes revenue generated by siphoning a large portion off to the US

government, making it negative to producers and consumers but positive for the

government.

53

Final Notes

As a final note, in using the data collected, we must note that the industry ASPs are pre-

tariff and that the total PV capacity of installations/quantity demanded are pre-tariff from

2004 – 2011 and post-tariff for 2012 and 2013. Therefore, there are discrepancies

between the output of quantity demanded equation Q (P) and the observed quantity

demanded in 2012 and 2013. For example, while industry ASP only dropped seven cents

from 2012 to 2013, implying only a 6.7% increase in quantity demanded as per the

model, in the observed numbers of the real world, installation demand actually increased

41% from 2012 to 2013 despite a relatively small price decrease. This demonstrates that

the installation quantity demanded of solar is not only correlated to its price but is also

linked to other variables, such as consumer preferences and the movement for a greener

world.

Calculations

All calculations for years 2012 and 2013 are outlined in the tables that follow:

54

2012: 2013:

Without Tariff ASP ($US/watt) 0.72 Q (P): Installation Quantity Demanded (watts) 3,793,611,121

Revenue Generated ($) 2,731,400,007

With 31% Tariff ASP ($US/watt) 0.9432 Q (1.31 P): Installation Quantity Demanded (watts) 3,118,543,278

Revenue Generated ($) 2,941,410,020

No Tariff v. Tariff Analysis % Change in Quantity Demanded -17.79%

Revenue to producers ($) 2,245,351,160 Revenue to US Government ($) 696,058,860 Loss in Producer Revenue ($) 486,048,847 % Change Producer Revenue -17.79%

Without Tariff

ASP ($US/watt) 0.65 Q (P) - Installation Quantity Demanded (watts) 4,049,308,244

Revenue Generated ($) 2,632,050,359

With 31% Tariff ASP w/ 31% tariff ($US/watt) 0.8515 Q (1.31 P) - Installation Quantity Demanded (watts) 3,374,240,401

Revenue Generated ($) 2,873,165,701

No Tariff v. Tariff Analysis % Change in Quantity Demanded -16.67%

Revenue to producers ($) 2,193,256,261

Revenue to US Gov't ($) 679,909,441 Loss in producer Revenue ($) 438,794,098 % Change Producer Revenue -16.67%

55

Quantifying the Social Cost of Carbon Emissions

The next aspect of our data analysis involves quantifying the social cost of CO2

emissions that result from the tariff being put into place.

Assumptions

1. Whether or not there is a tariff on solar, the same amount of total energy from all

sources is expended.

2. The decrease in watts of solar quantity demanded translates directly to an increase in

the burning of fossil fuel of the same amount of watts

For the purposes of our analysis, we will use two assumptions. The first assumption is

that the same amount of total energy is expended regardless of tariff, so the loss in

quantity of solar demanded is fully replaced by other sources of energy. The second

assumption is the replacement sources of energy solely come from the burning of fossil

fuels. For example, in 2012, the quantity of solar demanded with the tariff is 675,067,843

watts, or 675 megawatts, less than that without the tariff. From Assumption 1, we take as

given the fact that 675 megawatts of energy will be expended through another or a

combination of other sources. From Assumption 2, we will assume that the only other

available source of energy is the burning of fossil fuels. Consequently, using both

assumptions, we come to the conclusion that the loss of 675 megawatts in solar

demanded due to the tariff is completely replenished by 675 megawatts sourced from

burning fossil fuel.

56

Social Cost of Carbon in 2012

For 2012, we gauge the social cost of generating 675 megawatts of energy from the

burning of fossil fuel. According to the IPCC Special Report on Renewable Energy

Sources and Climate Change Mitigation, the 50th percentile of the amount of greenhouse

gas emissions from using coal as an energy source is 1,001 g CO2/kWh, which is

equivalent to 1,001,000 g CO2/mWh. We multiply this by 8,784 hours, as that is the

amount of hours in 2012. This yields 8,792,784,000 g CO2/mW, which we multiply by

675 mW, yielding 5,935,129,200,000 g CO2, which is equivalent to 5,935,129,200 kg

CO2. According to an average of peer-reviewed estimates, the social cost of carbon is

$43/metric ton of carbon, which is equivalent to about $10.75/metric ton of CO2. We

convert 5,935,129,200 kg of CO2 to metric tons and get 5,935,129.2 metric tons. Finally,

to quantify the social cost of CO2 emissions, we multiply by $10.75 and get an answer of

$63,802,638.90 for the year 2012.

We must remember to subtract out the social cost of the emission of greenhouse gas that

comes from the 675 megawatts of solar production, which is significantly lower than that

of the burning of fossil fuel. The 50th percentile of the amount of greenhouse gas

emissions from using solar PV as an energy source is 46 g CO2/kWh41. Following the

same logic as above, we multiply 46,000 g CO2/mWh by 8,784 hours, yielding

404,064,000 g CO2/mW, which we multiply by 675 megawatts to get 272,743.2 metric

tons CO2. We multiply this by $10.75/metric ton CO2 and get an answer of

$2,931,989.40. We remove this from $63,802,638.90 and end up with a 2012 net social 41 Moomaw, W., P. Burgherr, G. Heath, M. Lenzen, J. Nyboer, A. Verbruggen, 2011: Annex II: Methodology. In IPCC: Special Report on Renewable Energy Sources and Climate Change Mitigation (ref. page 10)

57

cost of $60,870,649.50 for the carbon emissions from the burning of fossil fuels rather

than using solar.

Social Cost of Carbon in 2013

Due to the nature of the Q (P) function, for 2013 the amount of energy that needs to be

generated from the burning of fossil fuel is again 675 megawatts, giving us the same

social cost of $60,870,649.50. However, since the forgone solar modules in 2012 have

extended lifetimes, the modules could have been used in 2013. Therefore, the total social

cost of carbon in 2013 is the sum of the social cost of carbon from the loss of solar PV

module capacity demanded in 2012 and in 2013, or $60,870,649.50 + $60,870,649.50.

The total social cost of carbon in 2013, then, is $121,741,299.00.

Total Social Cost of Carbon from Tariffs Installed in 2012

The total social cost of carbon from the loss in solar demanded is the sum of social cost

of carbon in 2012 and total social cost of carbon in 2013, or $60,870,649.50 +

$121,741,299.00. Therefore, the net social cost of the burning of fossil fuels in 2012 and

2013 due to the imposition of a tariff on solar amounts to $182,611,948.50.

58

Countervailing Subsidies (CVD) & Anti-Dumping Duties (AD) Impact on Domestic Employment

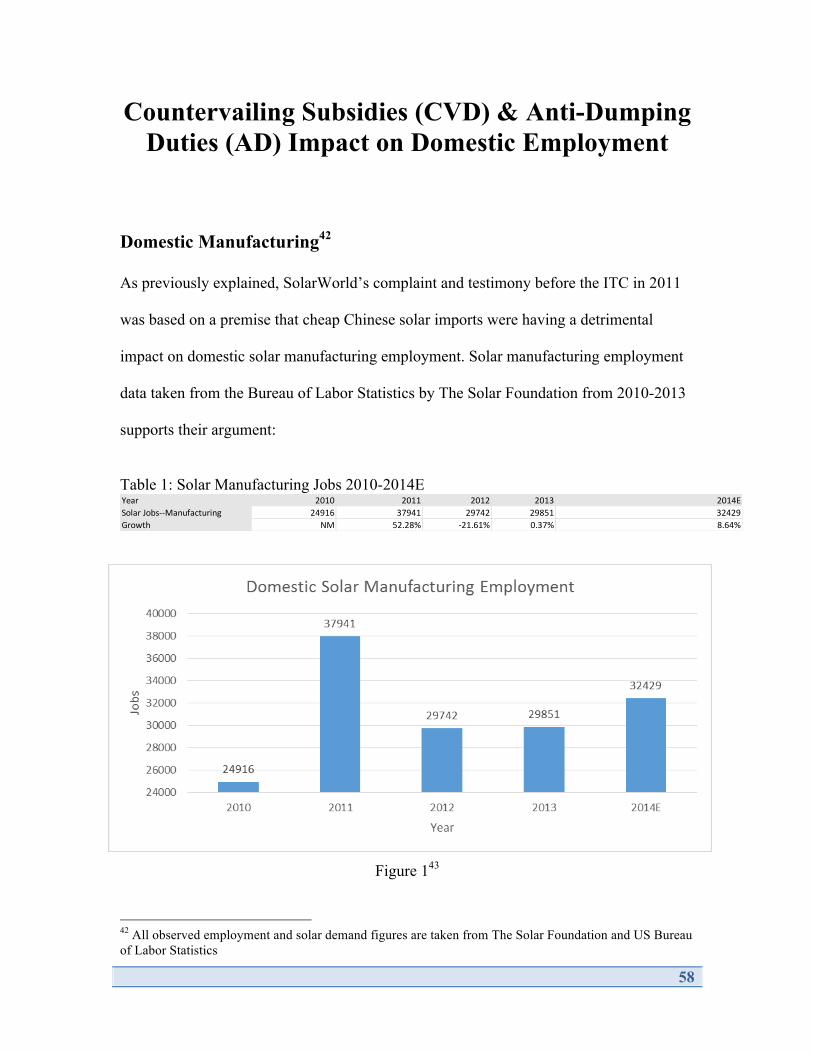

Domestic Manufacturing42

As previously explained, SolarWorld’s complaint and testimony before the ITC in 2011

was based on a premise that cheap Chinese solar imports were having a detrimental

impact on domestic solar manufacturing employment. Solar manufacturing employment

data taken from the Bureau of Labor Statistics by The Solar Foundation from 2010-2013

supports their argument:

Table 1: Solar Manufacturing Jobs 2010-2014E

Figure 143

42 All observed employment and solar demand figures are taken from The Solar Foundation and US Bureau of Labor Statistics

Year 2010 2011 2012 2013 2014ESolar Jobs-‐-‐Manufacturing 24916 37941 29742 29851 32429Growth NM 52.28% -‐21.61% 0.37% 8.64%

59

Table 2: Value of Chinese Solar Exports to the United States 2010-2013

Figure 244

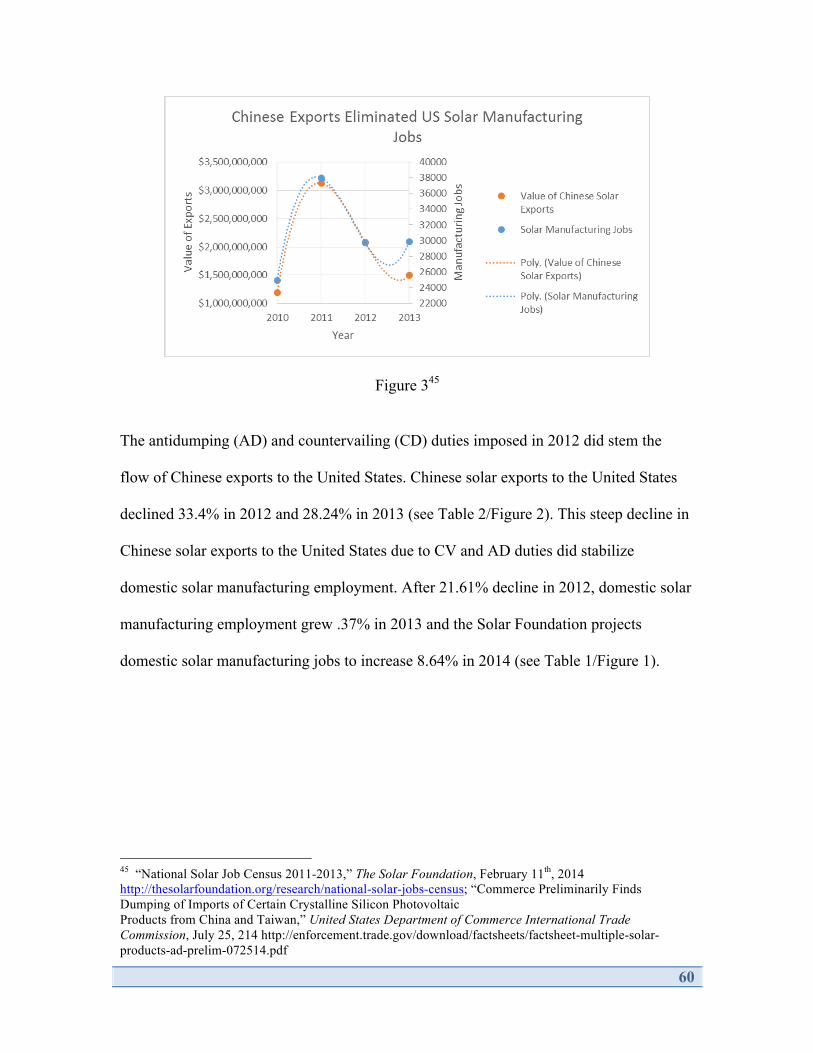

Data shows the number of solar manufacturing jobs declined sharply (21.61%) between

2011 and 2012 (see Table 1/Figure 1). This reduction in employment corresponds to the

surge in Chinese exports to the United States from 2010-2011 (162.05%) (see Table

2/Figure 2/Figure 3). Domestic solar manufacturing firms shed jobs in 2011-2012 after

the sharp rise in Chinese exports the previous year and subsequent downward pricing

pressure.

43 “National Solar Job Census 2011-2013,” The Solar Foundation, February 11th, 2014 http://thesolarfoundation.org/research/national-solar-jobs-census 44 “Commerce Preliminarily Finds Dumping of Imports of Certain Crystalline Silicon Photovoltaic Products from China and Taiwan,” United States Department of Commerce International Trade Commission, July 25, 214 http://enforcement.trade.gov/download/factsheets/factsheet-multiple-solar-products-ad-prelim-072514.pdf

Year 2010 2011 2012 2013Value of Chinese Solar Exports $1,192,340,000 $3,124,578,000 $2,082,753,000 $1,494,531,000Growth NM 162.05% -‐33.34% -‐28.24%

60

Figure 345

The antidumping (AD) and countervailing (CD) duties imposed in 2012 did stem the

flow of Chinese exports to the United States. Chinese solar exports to the United States

declined 33.4% in 2012 and 28.24% in 2013 (see Table 2/Figure 2). This steep decline in

Chinese solar exports to the United States due to CV and AD duties did stabilize

domestic solar manufacturing employment. After 21.61% decline in 2012, domestic solar

manufacturing employment grew .37% in 2013 and the Solar Foundation projects

domestic solar manufacturing jobs to increase 8.64% in 2014 (see Table 1/Figure 1).

45 “National Solar Job Census 2011-2013,” The Solar Foundation, February 11th, 2014 http://thesolarfoundation.org/research/national-solar-jobs-census; “Commerce Preliminarily Finds Dumping of Imports of Certain Crystalline Silicon Photovoltaic Products from China and Taiwan,” United States Department of Commerce International Trade Commission, July 25, 214 http://enforcement.trade.gov/download/factsheets/factsheet-multiple-solar-products-ad-prelim-072514.pdf

61

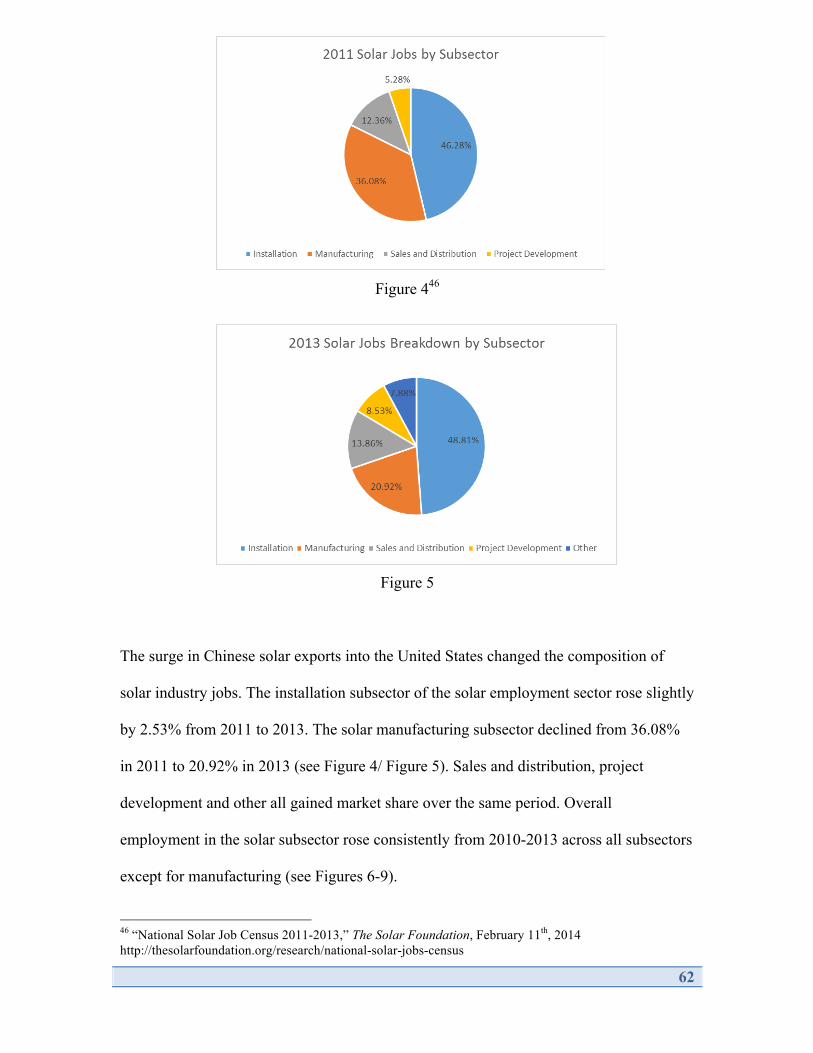

Overall Domestic Solar Employment Is Not Dependent on

Manufacturing

While those advocates of AD and CV duties were correct that Chinese solar exports to

the United States were leading to many foregone domestic manufacturing jobs in the

United States, the employment argument is misleading. Even in 2011, the high-water

mark of domestic solar manufacturing, solar employment related to manufacturing

represented roughly 36% of total jobs in the solar employment sector. That same year, the

largest subsector was installation, which comprised 46.28% of total jobs in the solar

employment sector (see Figure 4).

Table 3: Solar Industry Jobs by Subsector

Subsector Installation Manufacturing Sales and Distribution Project Development Other Total2010 Jobs 43934 24916 11744 N/A 12908 935022011 Jobs 48656 37941 13000 N/A 5548 1051452012 Jobs 57177 29742 16005 7988 8105 1190172013 Jobs 69658 29851 19771 12169 11248 1426982014 Jobs (Projected) 84331 32429 22585 12529 13064 164938

62

Figure 446

Figure 5

The surge in Chinese solar exports into the United States changed the composition of

solar industry jobs. The installation subsector of the solar employment sector rose slightly

by 2.53% from 2011 to 2013. The solar manufacturing subsector declined from 36.08%

in 2011 to 20.92% in 2013 (see Figure 4/ Figure 5). Sales and distribution, project

development and other all gained market share over the same period. Overall

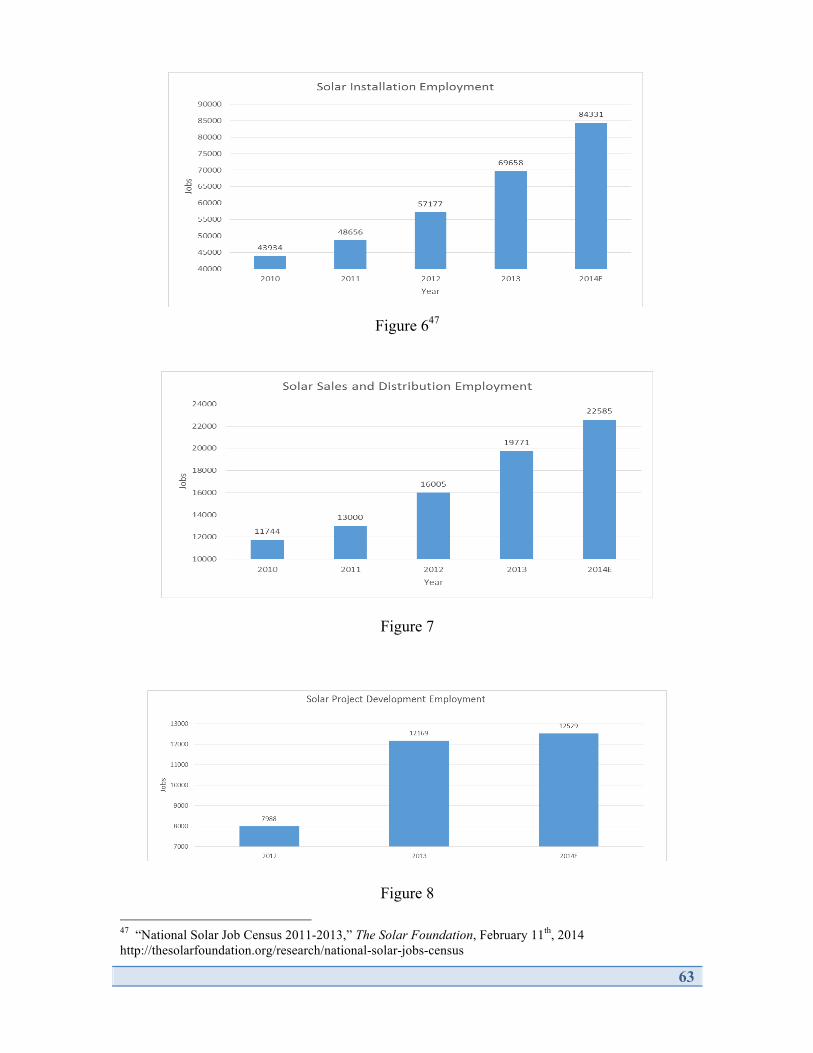

employment in the solar subsector rose consistently from 2010-2013 across all subsectors

except for manufacturing (see Figures 6-9).

46 “National Solar Job Census 2011-2013,” The Solar Foundation, February 11th, 2014 http://thesolarfoundation.org/research/national-solar-jobs-census

63

Figure 647

Figure 7

Figure 8 47 “National Solar Job Census 2011-2013,” The Solar Foundation, February 11th, 2014 http://thesolarfoundation.org/research/national-solar-jobs-census

64

Figure 9

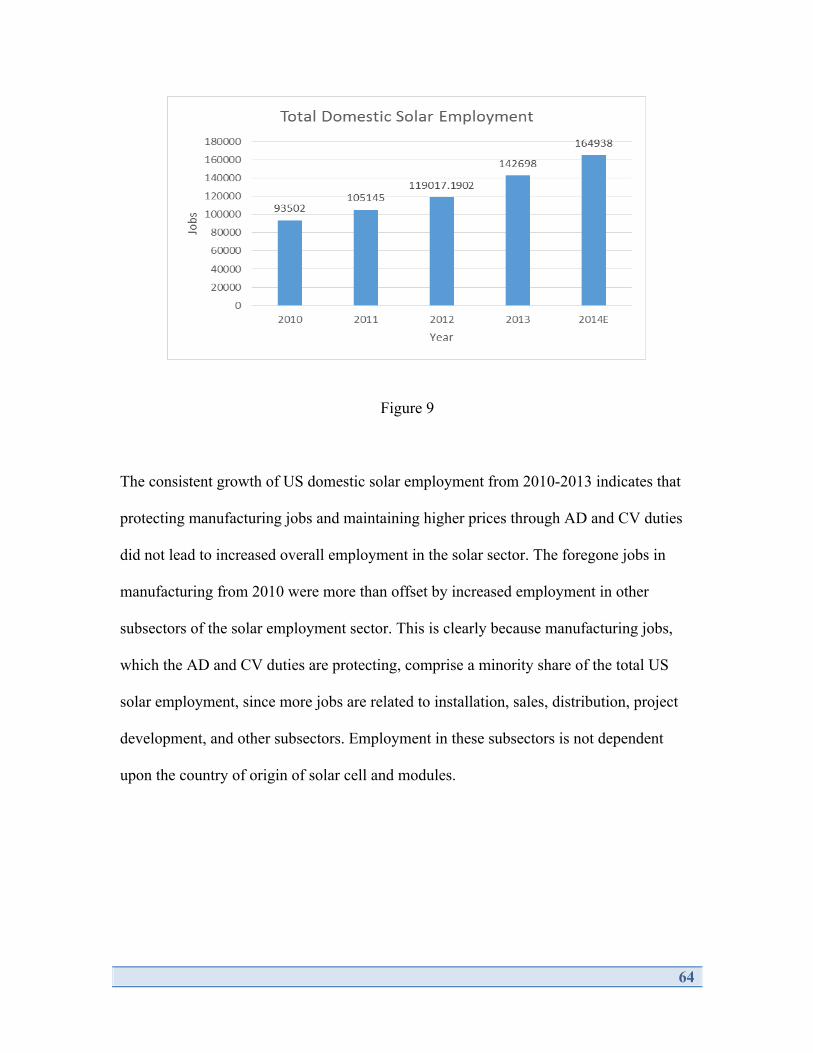

The consistent growth of US domestic solar employment from 2010-2013 indicates that

protecting manufacturing jobs and maintaining higher prices through AD and CV duties

did not lead to increased overall employment in the solar sector. The foregone jobs in

manufacturing from 2010 were more than offset by increased employment in other

subsectors of the solar employment sector. This is clearly because manufacturing jobs,

which the AD and CV duties are protecting, comprise a minority share of the total US

solar employment, since more jobs are related to installation, sales, distribution, project

development, and other subsectors. Employment in these subsectors is not dependent

upon the country of origin of solar cell and modules.

65

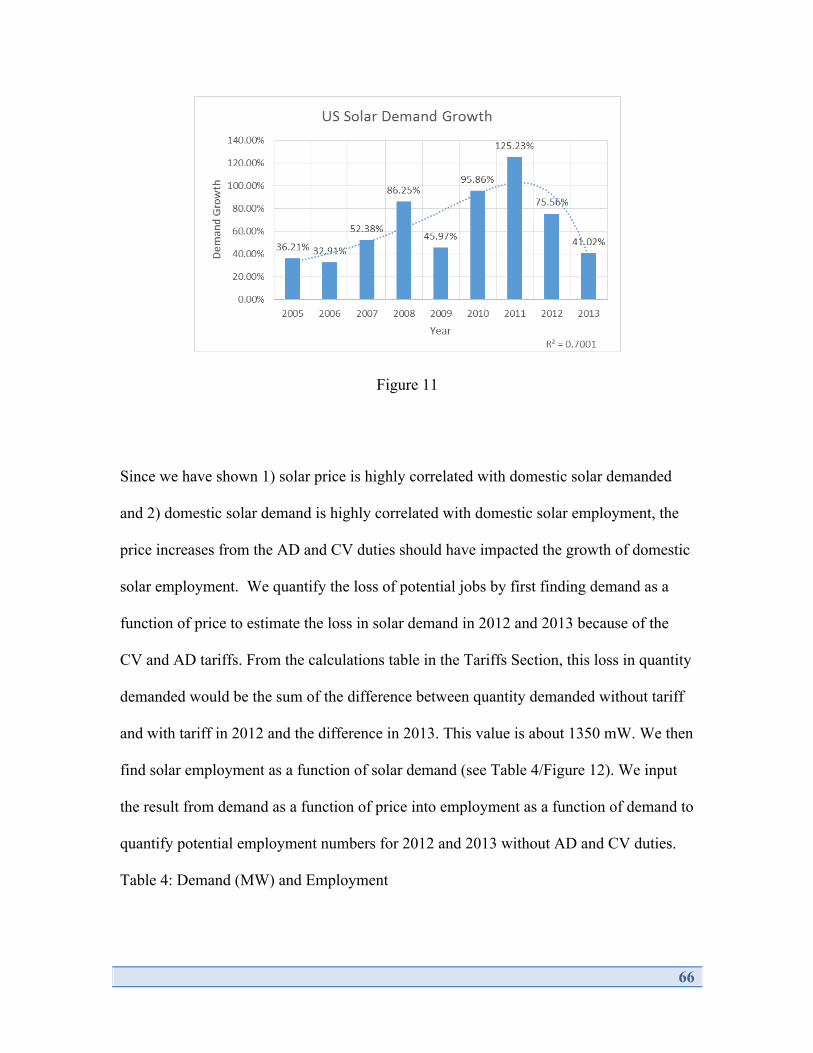

Demand for Solar Products is Correlated with Employment

As has been previously explained, data shows that price and demand of solar products

have an inverse relationship: the lower the cost of the products, the higher the demand (as

expected). Thus, the downward pricing pressure from Chinese products increased

demand for solar products. Section II explained that overall employment in the solar

sector is not dependent upon domestic solar manufacturing jobs.