-

Dr Dong-Wook SongThe University of Hong KongAsian Container

Ports:Development, Competition & Implications for Busan

Busan Development Institute

-

Discussion PointsReview of port development in the

regionCompetition status between the portsOverview of transport

logisticsStrategic Implications

Busan Development Institute

-

Port in International Logistics and Trade International

TradeTransport Logistics (international)Maritime

TransportPortShipping

Busan Development Institute

-

Implications from the DiagramTransport demand is derived not a

direct, primary or final demand !Demand for maritime transport is

derived particularly from international trade

At the same time, maritime transport is constrained by

international logistics

Busan Development Institute

-

World Top 10 Container Ports(Unit:: 000 TEUs)Source:

Containerisiation International (March, 2004)

Busan Development Institute

-

World Top 20 Container Ports

Busan Development Institute

-

Regional Container Ports in AsiaSource: Loo and Hook (2002)

Busan Development Institute

-

Major PortsFeeder PortsTanjung PelepasShenzhenBusanKaoshuingHong

KongSingaporeto North Americato EuropeCompetition from adjacent

PortsAsian Container Port NetworkShanghai

Busan Development Institute

-

Committed & Planned Port Development - Northeast China

-Source: Ocean Shipping Consultants (2003)

PortProjectQuay Length (metres) Annual Capacity(million TEUs per

year)Completion by endTianjinContainer Terminal 3

North Basin: 5 New

Berths3503503503503503503503500.3750.3750.3750.340.340.340.340.3420042005200620072008200920102011QingdaoP&O

Ports Terminal- 5th Berth- Two Berths- Further

Berthage4878002,8000.501.003.40200420052006-10DalianDCT- Four

Berths6403200.750.37520042005

Busan Development Institute

-

Committed & Planned Port Development - East and Southeast

China -Source: Ocean Shipping Consultants (2003)

PortProjectQuay Length (metres) Annual Capacity(million TEUs per

year)Completion by endHong KongTerminal 9

Terminal 103501,5601,5000.482.122.50200320042008ShanghaiPhase

IIIPhase IVJinshanzui: new terminal

Yangshan

Port6656656006002,0000.600.600.600.402.2012.5020022003200420082007-092010

-NingboFour Berths309.51,2000.251.3020042006-10ShenzenYantian Phase

III

Shekou Phase IIChiwan 4th

Berth3507003507007000.501.000.500.800.7020042005200620062004

Busan Development Institute

-

Committed & Planned Port Development - Southeast Asia

-Source: Ocean Shipping Consultants (2003)

PortProjectQuay Length (metres) Annual Capacity(million TEUs per

year)Completion by endPSAEfficiency ImprovementsPasir Panjang:

Phase

II-2,6002,6004,8000.503.003.005.5020022005-072008-102010-PTP

KlangPhase IIFurther Phases

Westport

ExpansionNorthport1,0801,0802,1606003561.901.903.800.800.402004-052009-10202020022003T.

PriokJICT: new berth & other804330.200.5020032005

Busan Development Institute

-

Committed & Planned Port Development - Korea -Source: Ocean

Shipping Consultants (2003)

PortProjectQuay Length (metres) Annual Capacity(million TEUs per

year)Completion by endBusanShin-Gamman TerminalPECT Terminal

Expansion8263000.650.2520022006Newport(Busan)Phase I 1 Stage APhase

I 1 Stage B- Full CapacityPhase I - 21,0001,000

1,20001.001.001.3752.602006200720092012-14GwangyangPhase II

Stage IPhase II Stage 2Phase

III1,3501,1501,4000.721.251.5620022004-052007-08IncheonSouth

Harbour

CT3003003000.3750.3750.375200320052008UlsanCT1,0001,0000.850.8520062011

Busan Development Institute

-

Source: Ocean Shipping Consultants (2001)

Busan Development Institute

Chart1

18.618.1

18.619.05

19.0820.42

20.0321.77

21.223.2

21.224.74

23.730.68

Supply

Demand

Year

Million TEUs

Supply and Demand (HK)

Sheet1

2000200120022003200420052010

Supply18.618.619.0820.0321.221.223.7

Demand18.119.0520.4221.7723.224.7430.68

Sheet2

Sheet3

Sheet4

Sheet5

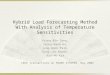

-

Source: Ocean Shipping Consultants (2001)

Busan Development Institute

Chart1

21.0517.04

21.717.38

22.218.54

22.219.82

22.221.18

25.222.64

33.731.17

Supply

Demand

Year

Million TEUs

Supply and Demand (Singapore)

Sheet1

2000200120022003200420052010

Supply21.0521.722.222.222.225.233.7

Demand17.0417.3818.5419.8221.1822.6431.17

Sheet2

Sheet3

Sheet4

Sheet5

-

Source: Ocean Shipping Consultants (2001)

Busan Development Institute

Chart1

18.618.1

18.619.05

19.0820.42

20.0321.77

21.223.2

21.224.74

23.730.68

Supply

Demand

Year

Million TEUs

Supply and Demand (HK Port)

Sheet1

2000200120022003200420052010

Supply18.618.619.0820.0321.221.223.7

Demand18.119.0520.4221.7723.224.7430.68

Chart2

13.3214.9

14.9316.99

15.7819.88

18.0322.72

19.2825.27

20.1827.93

25.7841.5

Supply

Demand

Year

Million TEUs

Supply and Demand (China)

Sheet2

2000200120022003200420052010

Supply13.3214.9315.7818.0319.2820.1825.78

Demand14.916.9919.8822.7225.2727.9341.5

Sheet3

Sheet4

Sheet5

-

Source: Ocean Shipping Consultants (2003)

Busan Development Institute

Chart1

9.759.99

11.1211.27

11.512.23

12.8413.28

13.8414.34

19.7920.55

Supply

Demand

Year

Million TEUs

Supply and Demand (Korea)

Sheet1

200120022003200420052010

Supply9.7511.1211.512.8413.8419.79

Demand9.9911.2712.2313.2814.3420.55

Sheet2

Sheet3

Sheet4

Sheet5

-

Forecast is forecast: forecast tends to be optimistic !!Thus, we

have to seriously answer questions below - Do we have enough

cargoes (or demand) ?Is the ever-expansion of port capacity

justifiable or only a solution ?However, at the same time, the

following facts are to be taken into account Only those ports which

have enough capacity and / or proper facility can enjoy demand

increased like a lottery !!!Lead time, capital intensive

investment, high sunk costs .. make decision-making problems

delicate and complicated.Points to be noted !!!

Busan Development Institute

-

Asian Container Throughput by Region (Unit: %)Source: Ocean

Shipping Consultants (2003)

Busan Development Institute

-

Some Thoughts on Port Demand

Demand for shipping services is derived from international

trade.

Demand for port services is derived from or subject to shipping

lines decision.

Shipping demand is the second; Port demand is the third ?

Ports become a prawn in international trade !!!

* * * * *How should a port react and respond ?

Busan Development Institute

-

Port Market DrivenTo become more price competitiveTo improve

service quality To expand service rangeTo cope with increased

customer's negotiation power (e.g. shipping alliances,

ever-increasing vessel size)

Busan Development Institute

-

Structural Changes in Transport LogisticsFordismPost-Fordism

Economies of scale Standardisation Quantity-oriented Long trade

cycle Uni-modal transport Others Economies of scope Flexibility

Quality-oriented Short trade cycle Multi-modal transport Global

operation Outsourcing VAL services Others

Busan Development Institute

-

Current Development in Transport LogisticsMore logistics

activities outsourcedLogistics services integrated and

improvedInformation technology (IT) widely applied3PLs service

scope expanded

Busan Development Institute

-

ClientSupplierConsumerLLP or 4PL(Logistics

Integrator)ShippingCompanyRailOperatorTerminalOperatorWarehouseRoadHaulerBargeOperatorInformation

flow between LLP and 3PLsInformation flow in the supply chain of

client

Busan Development Institute

-

A Strategic Response from PortsThe Three Generic Strategies for

creating a defensible position and outperforming competitors

(Porter, 1980)

Cost leadership strategyDifferentiation strategyFocus

strategy

Busan Development Institute

-

A Strategic Response from Ports (I)

Busan Development Institute

-

A Strategic Response from Ports (II)

Hub portFeeder port

A comprehensive market analysis is a pre-requisite !!Focus or

Positioning

Busan Development Institute

-

Strategic Options in GeneralCompetition in 1980s Win & Lose

Game

Co-operation in 1990s Win & Win Game

Co-opetition in the MillenniumSelective Win & Lose

GameCo-operate to Compete To identify your collaborator and

competitore.g. Port alliances against shipping alliances

Busan Development Institute

-

Source: Lloyds Freight Transport Buyer Asia (July/August,

2002)

Busan Development Institute

-

For Competitive and Successful Port Management in the Logistics

EraTo constantly cope with changing market environmentTo be global

business players beyond port boundariesTo be global logistics

service providers to customers To achieve economies of scale being

complemented by economies of scope To focus on core competencies

& outsource other logistics functionsTo be technologically

innovativeTo be more commercially oriented

Busan Development Institute

-

Concluding RemarksMaritime transport is subject to international

trade and transport logistics chains.Ever-changing business

environment in maritime transport and logistics is a fact of

challenging as well as opportunity.New strategies are to

continuously developed and implemented to be competitive and

sustainable.Objective market analysis and market positioning seem a

key for Busans further success

Busan Development Institute