Embed Size (px)

Citation preview

Distribution Consolidation and Pricing in the Beer Industry

Anton Popov

August 25, 2019

Abstract

This paper studies consolidation of distributors in the beer industry and its interaction with

the uniform pricing by retailers. I build a theoretical model which illustrates how distributor

consolidation in a set of counties may affect retail prices in all counties, depending on how

strong the incentive of retail chains to price uniformly is. Empirically, using Nielsen scanner

price data, I study two events of distributor consolidation in Ohio in 2009–2011, which followed

upstream MillerCoors joint venture in 2008. In one of the events, distributor consolidation has

no price effects. In another, bigger event, prices of consolidated brands (Miller, Coors, Heineken

and Modelo) in treated counties increase by 0.46% relative to the control ABI brands. I find

no evidence of prices in other counties being affected. The findings are consistent with some

regimes of my theoretical model. The implications of this study are that modeling distribution

tier and uniform pricing by retailers may be important for horizontal merger practitioners, both

in retrospect and for forecasting.

1 Introduction

Horizontal merger analysis, a central tool in anti-trust enforcement, often abstracts away from

the vertical structure of the industry by assuming that each firm sets the final price for its

product (e.g., Nevo (2001), Miller and Weinberg (2017)). The analysis resulting from such

assumptions may be limited in two ways. First, consolidation upstream may be followed by

consolidation downstream. Both predicted and actual price increases due to consolidation up-

stream may be mismeasured if one does not include distributor consolidation in the analysis.

Second, interactions of pricing incentives in different distribution tiers may affect the predicted

upward pricing pressure following the merger. For example, retail supermarket chains often

price uniformly in most of their stores (DellaVigna and Gentzkow (2017)). Abstracting away

from this aspect may bias the merger counterfactuals.

1

This paper studies consolidation of beer distributors, which followed the upstream merger of

Miller and Coors in 2008. I show theoretically that distributor consolidation may have effects

on retail prices either in only counties which were treated by consolidation, or in all counties,

depending on how strong the incentive of retailers to price uniformly is. I test empirically both

hypotheses for two events of distributor consolidation in my data. I find support for higher

prices of consolidated brands in treated counties for one of the events. I find no evidence for

higher prices in all counties. Thus, in this empirical setting uniform pricing by retailers does

not have interactions with distributor consolidation. However, the latter does have an effect on

prices, which was missed by the previous studies.

In many US states beer distribution system is three-tiered, with big manufactures only being

able to sell to retailers through distributors. Moreover, some states require exclusive territories

of distribution, effectively giving a distributor monopoly power in its territories. For any beer

brand, the manufacturer needs to divide the state into non-overlapping territories, such that in

any territory only one distributor has the right to sell the brand. This is the case for Ohio state,

which I study in this paper.

Before 2008 some territories in Ohio had Miller and Coors brands sold by separate distribu-

tors. After the merger MillerCoors tried to consolidate their distribution network by switching

Miller brands to distributors of Coors, or vice versa, with two successful attempts. If distrib-

utors have pricing power in this market, such consolidation may let the distributor internalize

the pricing externality, raising wholesale prices, which may reflect in retail price increases for

consolidated brands in treated territories. However, this effect may not be observed if the chains

adopt uniform pricing across territories. Incentives of chains to price uniformly may over-weigh

the upward pricing pressure in any particular store affected by distributor consolidation. Still,

if a consolidated distributor has some additional pricing power, this upward pricing pressure in

a set of territories may manifest in a higher overall pricing level of a uniformly pricing retail

chain.

I start by outlining a stylized model, in which these ideas are formalized. I introduce a penalty

term in the profit function of the monopolist retailer, which reflects the desire of retailer to price

uniformly. The penalty term includes a parameter, which governs how strong uniform pricing

incentive is. I give numerical examples of solutions to a two-stage game where distributors set

wholesale prices first, and a retailer, operating in multiple counties, sets its prices second. I

show that when two distributors of different brands merge in one of the counties, there exist

two types of equilibria: one where it leads to retail price increases only in counties treated

by consolidation, and another where it leads to price increases in all counties. The type of

equilibrium depends on the uniform pricing parameter: naturally, when this parameter is low,

the first type of equilibrium is realized, and when it is high, the second.

2

I continue with a descriptive analysis of pricing by several retail chains in Ohio. I use Nielsen

scanner data from 2009–2011 to show that many chains are pricing uniformly, with 80% of stores

in a given chain setting exactly the same price for a specific beer product for prolonged periods

of time.

Having established the existence of uniform pricing at the retail level, I continue by studying

two events of distributor consolidation. In one of these events, in December 2009, distribution

of Miller brands by Metropolitan distributing company in 6 counties was discontinued, with the

brands transferred to Bonbright Distributors in 3 counties, and the Fisher Company in another 3

counties. Both Bonbright Distributors and Fisher Company were distributors of Coors, Corona

and Heineken at the end of the sample in 2011. In the second event, in June 2010, Kerr

Distributing and Kerr Wholesale, which were distributing Coors brands in 17 counties, were

acquired by AFP Distributors, carrying Miller, Corona and Heineken, in all but one of these

counties. Thus, both of these events led to consolidation of Miller, Coors, Corona and Heineken

brands in the hands of one distributor, whereas before the event one of the brands (either Miller

or Coors) was not consolidated with the other three. I call the counties where the consolidation

events happened “treatment” counties, and all the other counties “control”. The group of

brands which, following the events, was consolidated in the hands of one distributor (Miller,

Coors, Corona and Heineken) are “consolidated” brands, and ABI brands, which were sold by

separate distributors, are “control” brands.

The main contribution of this paper is to study empirically the pricing effects of these two

distribution consolidation events. Using the retail prices from Nielsen data as the main outcome,

I study two hypotheses. First, in the treatment counties consolidated brands may see higher

price increases than non-consolidated brands.1 I use counties not treated by distribution consoli-

dation as control counties. Thus, this hypothesis requires a triple difference approach, where the

coefficient of interest is given by an interaction on (post distributor consolidation)×(treatment

county)×(consolidated brand). Controlling for non-consolidated brands accounts for the marginal

cost shocks which were common to consolidated and non-consolidated brands at the time

of event. Controlling for counties not treated by distribution consolidation accounts for the

marginal cost shocks which were common across the state of Ohio for a given brand, for exam-

ple, at the manufacturer level. Differential marginal cost shocks on both of these dimensions

(brand and geography), coincidental with the timing of consolidation event, may be a problem

for identification of the effect.

To explain the second hypothesis, it is useful to consider whether rejection of the first hy-

pothesis proves that distributors have no pricing power. In the setting where retail chains price

uniformly, it may be the case that in response to a wholesale price increase by a consolidated

1As a standard horizontal merger analysis would suggest.

3

distributor in the treatment counties, the retail chain finds it optimal to increase prices in all

counties, not only the ones where a distributor consolidated. The presence of such price in-

crease, common to all stores of a chain, constitutes the second hypothesis which I test. The

relevant coefficient comes from the double difference approach, on interaction of (post distribu-

tor consolidation)×(consolidated brand). Again, non-consolidated brands here are the control

group, which accounts for the marginal cost shocks coincidental with the consolidation event,

common to all brewers. There are no control counties here, because under the null hypothesis

all counties raise prices by the same amount for consolidated brands, and by the same (different)

amount for control brands.

The empirical results of this study are as follows. For the first hypothesis I find no price

increases during event 1, contemporaneously or in the following 15 months. There is also no

contemporaneous price increase for event 2. However, there is a price effect 9 months after event

2, with consolidated brands increasing prices by 0.51% more in the treated counties. This effect

is statistically significant, with the 95% confidence interval of [0.13%, 0.88%]. My interpretation

of this first set of findings is that the distributors have some degree of pricing power. When

consolidation affects more counties, as is the case with event 2, the incentive of retail chains to

price optimally in those counties seems to over-weigh the incentive to price uniformly. On the

other hand, event 1 only affects 6 counties, so the cost of keeping non-optimal uniform price

may not be high in that case. The lagged impact of distributor consolidation may be due to

rigidity of contracts. The second hypothesis that the distributor consolidation can affect pricing

in all counties does not find support in either of two consolidation events. Intuitively, for this

effect to exist both the uniform pricing incentive of retail chains and the upward pricing pressure

created by the distributor consolidation need to be high. Then it could be optimal to increase

prices in all counties where a retail chain operates, passing through the upward pricing pressure

from treatment counties to all counties. However, given that the price effect (as estimated by

hypothesis 1 testing) is not too high, it is reasonable that the second hypothesis finds no support.

Related literature

This paper is related to a wide range of research on the beer markets. The first group of papers

estimates the effects from the MillerCoors merger itself. Ashenfelter, Hosken, and Weinberg

(2015) compare upward pricing pressure resulting from the merger to cost efficiencies which it

generated by allowing Miller to brew their beers in Coors plants and vice versa, reducing shipping

costs. Using a reduced form approach, they find that increased concentration would raise prices

by 2% on average, but the cost efficiencies offset this price increase. A later paper by Miller

and Weinberg (2017) estimates the coordination parameter between joint MillerCoors and ABI,

4

using a structural model of demand and supply. They conclude that the merger increased the

amount of coordination between MillerCoors and ABI, which led to higher price increases than

what could be anticipated in the absence of coordination effects. The price increases related to

coordination effects are around 6–8 percentage points. It is the presence of coordination effects

which eroded the benefits coming from the cost efficiencies of the merger.

The second group of papers explore effects of exclusive territories on the beer markets. Sass

and Saurman (1996) study Indiana’s 1979 ban on the grant of exclusive territories. By studying

effects of the ban on quantities and prices of beer sold, they empirically estimate if the monopoly

power that exclusive territories give has an overall positive impact. Theoretically it could be bad

for price competition, but good for promoting the optimal dealer effort. Exclusive territories

ban is estimated to have reduced both consumption and prices of beer, leading the authors to

conclude that exclusive territories do increase demand through better dealer services. Burgdorf

(2019) studies a reverse event, where in 2006 Wisconsin required the brewers to assign exclusive

territories to their distributors. He finds that following the new mandate prices of craft beer

went up and quantity decreased. The conclusion is that the exclusive territories caused an

increase in the distribution cost, especially for the craft beer manufacturers.

Asker (2016) considers a different kind of exclusivity. Some distributors work exclusively with

a single manufacturer. In the US this is almost always the case for ABI distributors, whereas

other manufacturers may or may not share distributors. Asker (2016) studies the presence of

foreclosure effects in the markets where Miller uses an exclusive distributor as opposed to the

markets where Miller distributor also carries other brands. Using data on retail beer prices

and quantities in Dominick’s Finer Foods in Illinois in 1994, he estimates a structural model

of the industry and backs out costs and demand effects related to facing a Miller-exclusive

distributor. He does not find any evidence that the competing distributors have higher costs or

lower demand when Miller signs an exclusive contract with one of the distributors, thus rejecting

the foreclosure hypothesis.

What is common to the structural papers on beer markets mentioned above (Miller and

Weinberg (2017) and Asker (2016)) is that in their main specifications they do not model

distributors as price-setting, effectively assuming that the distributors only cover their fixed

costs, and do not contribute to double marginalization. Asker (2016) mentions the institutional

setting in Illinois which justifies such an approach: “The brewer has varying degrees of input

into the wholesale price charged by the distributor to retailers. When dealing with a large

supermarket chain, a sales representative from the brewer will arrive at a wholesale price for

the chain with the chain’s buyer. Distributors are then expected to supply at that price. While

resale price maintenance is prohibited explicitly by the Beer Industry Fair Trading Act... this

practice does not appear to invite legal sanction.”

5

There is also theoretical research laying out a different argument for lack of double marginal-

ization in markets like this. Bernheim and Whinston (1985) show that when a downstream firm

works with multiple upstream firms, the monopolistic outcome may be achieved. Effectively the

upstream firms “sell out” their business to a single agent downstream. Theoretically, incentives

described by Bernheim and Whinston (1985) could be present in the beer markets where a single

distributor may serve multiple brewers in an overlapping set of exclusive territories.

My paper serves as an empirical test to whether distributors have no pricing power, as in

Asker (2016) and (most of) Miller and Weinberg (2017). I reject this conjecture for one of

distributor consolidation effects which I study, showing that it did increase retail prices. Notice

that this finding does not, however, reject the model laid out in Bernheim and Whinston (1985).

Indeed, if consolidation leads from three brands being consolidated to four, and Bernheim and

Whinston (1985) predict a monopolistic price in both cases, under standard assumptions the

distributor will set a higher wholesale price when it has four brands consolidated than when it

has three.

The finding that distribution structure matters for retail pricing is an important one both

for studying mergers in the past and modeling mergers under review. For example, one of the

assumptions in Miller and Weinberg (2017) is that MillerCoors, both pre- and post-merger, had

a zero coordination parameter with Heineken and Modelo (brewer of Corona). However, as I

show here, there are price effects related to MillerCoors, Heineken and Modelo being sold by

the same distributor. What the model in Miller and Weinberg (2017) would attribute to pure

unilateral effects of Nash competition between MillerCoors and Heineken/Modelo, may instead

be picking up some of the joint distribution effects, overestimating the magnitude of unilateral

effects. If the true unilateral effects are smaller than what Miller and Weinberg (2017) estimate,

the coordination effects may in reality be even higher.

Finally, this paper is related to the study of uniform pricing by US supermarket chains

in DellaVigna and Gentzkow (2017). They document that despite big variations in consumer

demographics and competition across multiple locations of supermarket chains, they charge

nearly uniform prices for a range of products, including beer. My paper presents similar evidence

of uniform pricing for beer by chains in the state of Ohio.

The rest of the paper is structured as follows. Section 2 lays out a theoretical model, section

3 describes the data, section 4 shows evidence of uniform pricing by chains, section 5 presents

my empirical estimates, section 6 discusses the results, and section 7 concludes.

6

2 Model

In this section I develop a stylized model which demonstrates how consolidation of distributors

in one county may lead to a price increase in only the county treated, or a price increase in all

counties, depending on the importance of uniform pricing for a downstream retailer.

To simplify the exposition, consider a setting with two tiers, retail and wholesale. There is

a single retailer which owns a chain of stores, with one store in each county c ∈ 1, C. Retailer

is acting as a monopolist. It sells two brands of beer, j = 1, 2. Demand for brand j in county c

is given by

qjc = qjc(pjc, p−jc)

with − ∂qj∂pj

>∂qj∂p−j

> 0.

In each county c there is a separate distributor selling beer j and −j, so the total number of

distributors is 2C. Distributors set wholesale prices wjc at which retailers buy. For simplicity,

assume no costs for the distributors or retailers.

The timing is standard, with distributors moving first and retailer second. Hence, the game

will be solved using the standard backward induction.

Retailer has a profit function which includes a non-usual term:

π(p, w, pbase) =

C∑c=1

∑j=1,2

[(pjc − wjc)qjc(pjc, p−jc)− λ|pjc − pbasej |

]The second term λ|pjc−pbasej | reflects the desire of retailer to price uniformly. Retailer picks

prices pjc at which the products are actually sold, and the baseline prices pbasej . Intuitively,

with low λ the uniform pricing incentive is small, and retailer picks different pjc, when there are

differences in demand functions qjc. With high λ uniform pricing incentive is high, and it may

be the case that it is optimal to set pjc = pbasej ∀ c ∈ 1, C. Formally, retailer solves

maxp,pbase

π(p, w, pbase)

The FOC with respect to pbasej is

λ

C∑c=1

∑j=1,2

sign(pjc − pbasej ) = 0

It is clear from this FOC that the baseline price pbasej will be given by the median of pjc, c ∈ 1, C.

As to prices pjc, in general there may be some equal to pbasej , and some lower and higher. The

specifics of setting pjc will depend on demand functions qjc(pjc, p−jc) and the trade-off between

setting non-optimal price for maximizing (pjc−wjc)qjc(pjc, p−jc) and incurring the penalty term

λ|pjc − pbasej |.

FOC with respect to pjc is

qjc(pjc, p−jc)+(pjc−wjc)q′jc,1(pjc, p−jc)+(p−jc−w−jc)q′−jc,2(p−jc, pjc)−λ sign(pjc−pbasej ) = 0

7

Call p∗jc the solution to this distorted problem, and p∗∗jc the solution to non-distorted problem

without λ|pjc − pbasej | term. It is clear from this representation that, if, absent the penalty

term, optimal price p∗∗jc is lower than median of other p**jc ’s, the final term in the distorted FOC

evaluated at p∗∗ is positive, and the first three terms need to be adjusted below to make the FOC

equal 0. For some demand functions this will unambiguously imply that p∗jc is higher than p∗∗jc

(for example, when demand is symmetric and linear in prices, qjc(pjc, p−jc) = a+ bpjc−dp−jc).

Similarly, if the p∗∗jc is higher than median of other p**jc ’s, p∗jc will be lower than p∗∗jc . Thus, even

in the case when λ is small enough to not make any of the prices the same, it does bring prices

closer together.

The prices which come out of the retailer’s optimization problem are functions of the w

vector, and so are the quantities demanded. The distributors, knowing qjc(p∗jc(w), p∗−jc(w)),

play a Nash equilibrium and solve simultaneously

maxwjc

wjc · qjc(p∗jc(w), p∗−jc(w)), j = 1, 2; c ∈ 1, C

Characterizing in more detail possible equilibria of this game is beyond the scope of this paper.

Rather, in the next subsection I use a numerical example to illustrate two types of equilibria:

where prices in all counties are different for small λ, and where prices in all counties are the

same for big λ. I also show what happens when distributors of beers j and −j decide to merge

in one of the counties, for these two types of equilibria.

2.1 Numerical Example

Consider a setting with three counties, c = 1, 2, 3. Let demand for products 1 and 2 be sym-

metric, but different across counties:

qj1 = 100− 2pj1 + p−j1

qj2 = 102− 2pj2 + p−j2

qj3 = 104− 2pj3 + p−j3

When λ = 1, the solution to the game is2

pj{1,2,3} = (67, 68, 69),

pbasej = 68,

wj{1,2,3} = (33, 34, 35).

If two distributors in county 3 merge, they can internalize the effect of product j’s price on

demand for product −j, and vice versa. This, of course, leads to an increase in retail prices in

2Intermediate steps of the solution may be found in Appendix A.

8

county 3. Prices in counties 1 and 2 are not affected by distributor consolidation in county 3.

The solution after distributor consolidation is

ppostj{1,2,3} =

(67, 68, 77

2

3

),

ppost, basej = 68,

wpostj{1,2,3} =

(33, 34, 52

1

3

).

When λ = 21, the solution to pre-consolidation game is

pj{1,2,3} = (81.6, 81.6, 81.6),

pbasej = 81.6,

wj{1,2,3} = (55.2, 61.2, 67.2).

The uniform pricing parameter λ is so high here that it induces the retailer to set all prices the

same.

After distributors in county 3 merge, the equilibrium becomes

ppostj{1,2,3} =

(85

1

3, 85

1

3, 85

1

3

),

ppost, basej = 851

3,

wpostj{1,2,3} = (44, 50, 112).

Note that due to uniform pricing in this regime, distributor consolidation in county 3 leads to

increase in retail prices in all counties. It is also interesting that the retailer is actually losing

money in county 3 (wpostj3 > ppostj3 ).

This numerical example serves as a justification for my empirical approach. As mentioned in

the introduction, I observe two events of distributor consolidation in Ohio. My stylized model

predicts two possible outcomes of distributor consolidation, in the case where distributors are

actively participating in price setting: either prices increase only in counties treated by the

distributor consolidation, or prices increase in all counties. It may also be the case that, unlike

in my model, and similar to the assumptions made, e.g. by Asker (2016) and Miller and Weinberg

(2017), the distributors do not affect pricing. Then the prices would not react to distributor

consolidation at all. Hence, in my empirical specifications I test two hypotheses. First is the

hypothesis of price increase of consolidated brands in only treated counties with the alternative

of no effect. Second is the hypothesis of price increase of consolidated brands in all counties

with the alternative of no effect. I elaborate on my empirical approach in section 5, but it is

useful first to describe the data and evidence on uniform pricing.

9

3 Data

The data come from two sources. The first is Nielsen scanner data. These are weekly data on

quantity sold and average price at the UPC level from multiple store chains that Nielsen tracks.

There are two well-known caveats of the scanner data. First, it records only products that had

a unit sold in any given week. If there are no sales of a UPC in a given week, it could be because

the store was out of this product, or because the product was on the shelf, but nobody bought

it. This first issue may lead to high prices missing in the data for some stores with low demand

(it may be that a store is more likely to not have a product sold when its price is high). Since

the big chains in my data will have a sale of all major products in all weeks, I do not consider

this to be a big issue.3 The second caveat is that the prices may change mid-week. This is not

an issue for my reduced form empirical specifications, which are run on these weekly average

prices taken directly from the data.

The second data set is the information on beer distributors, brands they are carrying, and

their territories from the Ohio Division of Liquor Control. These data for years 2009 to 2011

come in paper form as the scans from the Division of Liquor Control archives. Ideally I would

like to know the changes in the distribution structure in the year of the MillerCoors merger

(2008), as well. Unfortunately, the forms in that period are not very reliable, so I resort to

studying the period following the merger.

In the next subsections I describe each part of the data in more detail.

3.1 Brands

To have some consistency with the previous literature, I restrict attention to the same brands

as Miller and Weinberg (2017). These are 13 flagship brands of ABI, Miller, Coors, Heineken

and Modelo, which account for 40% of revenue of all beers in the Nielsen data.

The data have information at the UPC level, but for the purposes of exposition and empirical

analysis it may be useful to aggregate the data. In my regressions I fix the product level at

brand–(packaging size)–(unit size) combination. An example of a product would be Miller 12-

pack of 12 oz. units. If it is sold both in bottles and cans, such UPCs are aggregated into one

product.

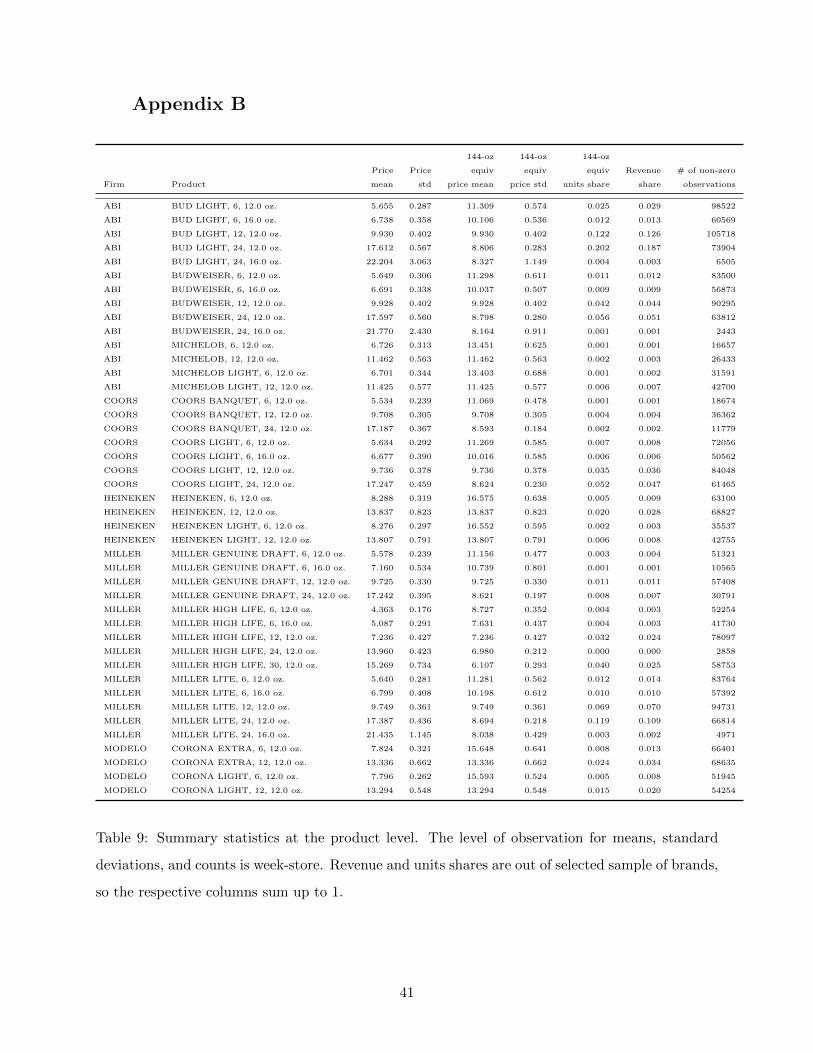

Summary statistics on brands at even more aggregated brand level are shown in Table 1.4

Units and prices here are normalized to a 144-oz equivalent unit to be able to aggregate different

products of a given brand into a meaningful statistic.5 The time period that I use in this study

3Although I admit that the inclusion of smaller chains for which this is more likely to happen could bias the

relevant coefficients down, if the issue is more pronounced for treatment group than for control.4Table 9 in the Appendix shows summary statistics at the product level.5Also following Miller and Weinberg (2017).

10

is 2009–2011.

144-oz 144-oz 144-oz Share of week-store

equiv equiv equiv Revenue observations

Firm Product price mean price std units share share with a unit sold

ABI BUD LIGHT 10.084 1.039 0.365 0.358 0.957

ABI BUDWEISER 10.077 1.017 0.118 0.118 0.858

ABI MICHELOB 12.231 1.133 0.003 0.004 0.275

ABI MICHELOB LIGHT 12.266 1.161 0.007 0.009 0.404

COORS COORS BANQUET 9.892 0.907 0.007 0.007 0.359

COORS COORS LIGHT 9.946 1.048 0.100 0.097 0.792

HEINEKEN HEINEKEN 15.147 1.555 0.025 0.037 0.653

HEINEKEN HEINEKEN LIGHT 15.053 1.540 0.007 0.011 0.421

MILLER MILLER GENUINE DRAFT 10.059 1.041 0.023 0.023 0.539

MILLER MILLER HIGH LIFE 7.353 0.989 0.080 0.056 0.699

MILLER MILLER LITE 9.993 1.056 0.213 0.206 0.884

MODELO CORONA EXTRA 14.473 1.327 0.032 0.046 0.653

MODELO CORONA LIGHT 14.419 1.268 0.020 0.028 0.507

Table 1: Summary statistics at the product level, flagship brands of ABI, MillerCoors, Heineken

and Modelo in 2009–2011. The level of observation for means and standard deviations is week-

store-product. Revenue and units shares are out of selected sample of brands, so the respective

columns sum up to 1.

Out of these 13 brands ABI has the biggest share at 49.3% of volume, with Bud Light being

by far its biggest brand. The Michelob and Michelob Light brands of ABI are quite small, and

slightly more expensive than Budweiser / Bud Light. Miller brands are in the second place by

market share, with 31.6% of revenue, and Coors is in the third place with 10.7%. For Miller and

Coors the most popular are again their light brands, similarly to ABI. Modelo has 5.2% share,

and Heineken 3.2%. Modelo and Heineken are clearly pricing above ABI, Miller and Coors,

which reflects in their higher revenue shares compared to the shares by volume.

Bud Light is also the brand which is sold in the vast majority of week-store observations in the

data, at 95.7%. Closely behind it are Miller Lite (88.4%), Budweiser (85.8%), and Coors Light

(78.2%). The least represented brands by the number of observations are Michelob (27.5%),

Coors Banquet (35.9%), and Michelob Light (40.4%).

3.2 Retail Chains

Nielsen data does not identify the names of retail chains which are in the scanner data. Still,

it may be useful to get a sense of what kind of chains sell beer in Ohio. I also compare the

chains which are in Nielsen data to each other. Unfortunately, I cannot say how the market

11

concentration is distributed in chains outside Nielsen data. Hence, the shares reported below in

Table 2 are out of chains which I observe, for the sample of brands defined above.

Chain Channel Number of storesRevenue share

of selected beer brands

130 Food 219 59.6

89 Food 129 33.2

9104 Food 6 0.5

295 Food 2 0.2

4901 Drug store 194 1.9

4904 Drug store 199 1.4

6901 Mass merch 50 0.8

6904 Mass merch 70 1.6

6914 Mass merch 4 0.0

8199 Convenience store 20 0.8

Table 2: Description of the retail chains selling beer in Ohio in Nielsen scanner data in 2009–2011.

Nielsen classifies chains into four channels: food, drug stores, mass merchandise, and con-

venience stores. Two food chains, 89 and 130, sell the vast majority of beer brands I consider,

corresponding to 92.8% share of all sales. These food chains also have a lot of stores, 219 and

129 respectively, the ratio roughly corresponding to their revenue share ratio. Two other food

chains are very small, with 6 and 2 stores and a combined share of beer sales smaller than 1%.

There are two drug store chains, each close to 200 stores. It seems that people do not buy

much beer at the drug stores, although it is the second biggest beer sale channel in the scanner

data. Their joint revenue share is 3.3%.

There are two big and one small mass merchandise chain with combined 2.4%. The bigger

of the mass merchandise chains is comparable to the drug store chains.

Finally, there is one convenience store chain with a share slightly below 1%.

3.3 Distributors

As mentioned above, the distributors have exclusive territories in Ohio. In theory, distributors

may carve the state into territories in whatever way they like. However, in practice this is usually

done by county border lines. Sometimes a county may be divided into several territories, with

a separate distributor serving each. Distributors of different brands also do not have identical

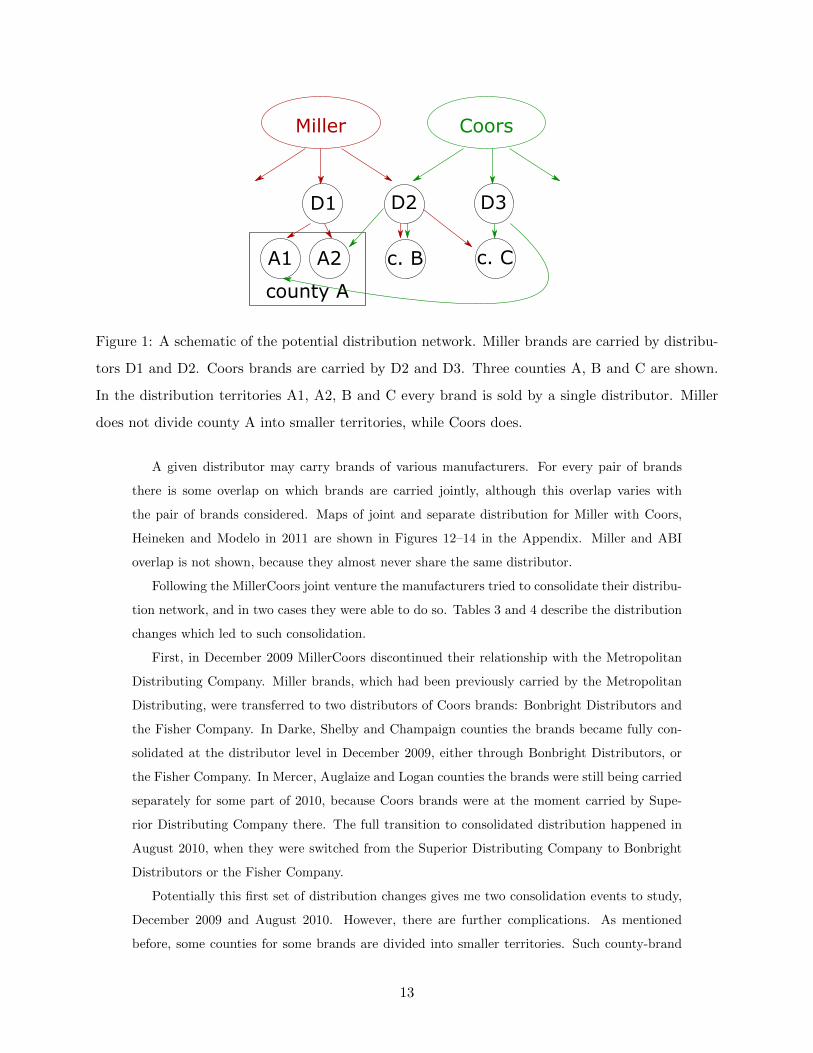

partitions of the state into territories. Schematically the distribution network is shown in Figure

1.

12

Miller Coors

D1 D2 D3

A2A1 c. B c. C

county A

Figure 1: A schematic of the potential distribution network. Miller brands are carried by distribu-

tors D1 and D2. Coors brands are carried by D2 and D3. Three counties A, B and C are shown.

In the distribution territories A1, A2, B and C every brand is sold by a single distributor. Miller

does not divide county A into smaller territories, while Coors does.

A given distributor may carry brands of various manufacturers. For every pair of brands

there is some overlap on which brands are carried jointly, although this overlap varies with

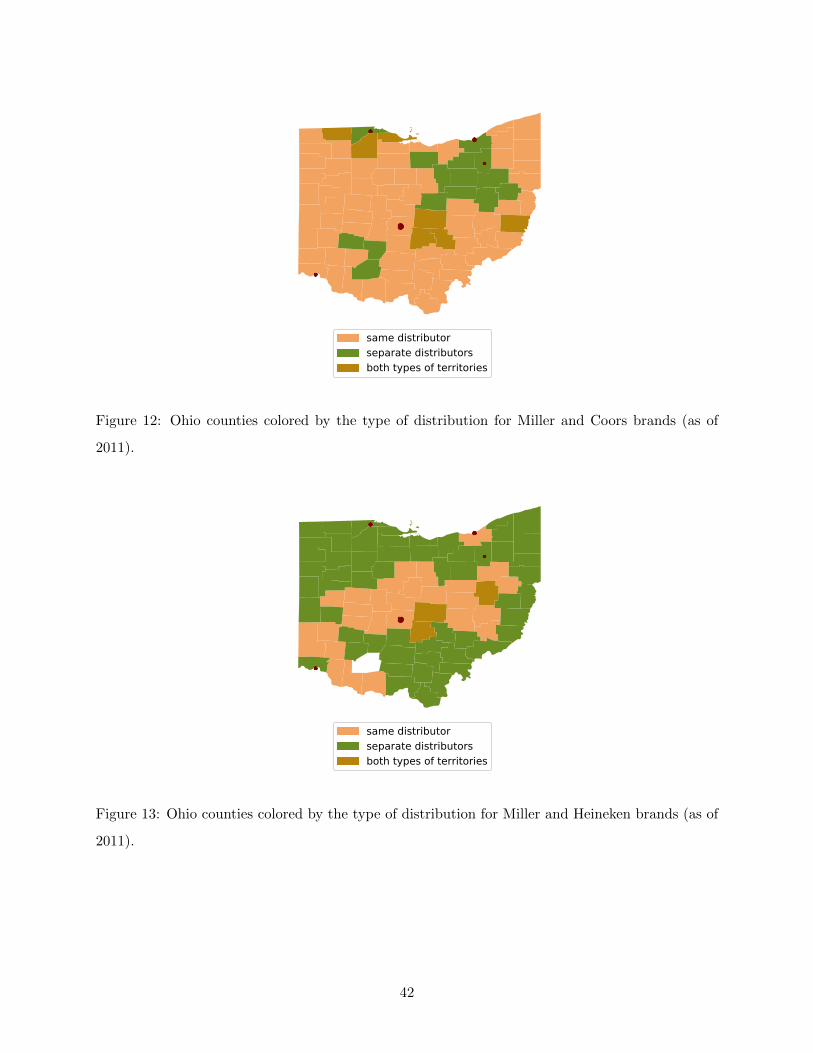

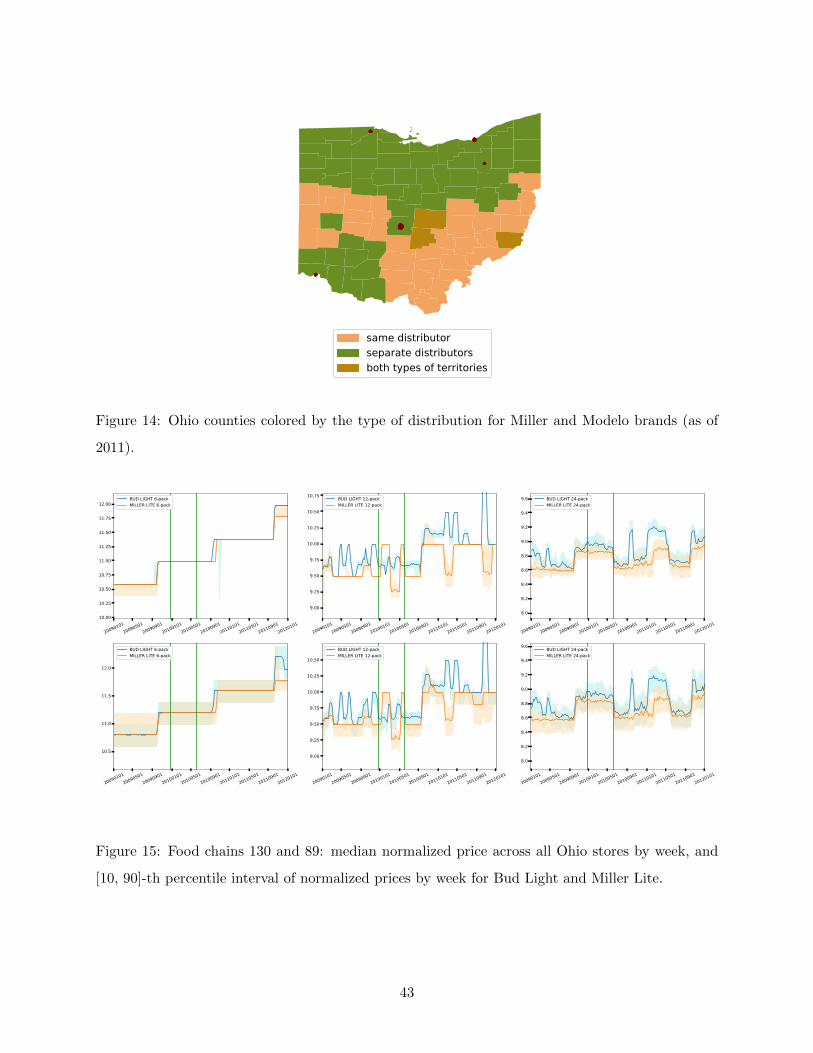

the pair of brands considered. Maps of joint and separate distribution for Miller with Coors,

Heineken and Modelo in 2011 are shown in Figures 12–14 in the Appendix. Miller and ABI

overlap is not shown, because they almost never share the same distributor.

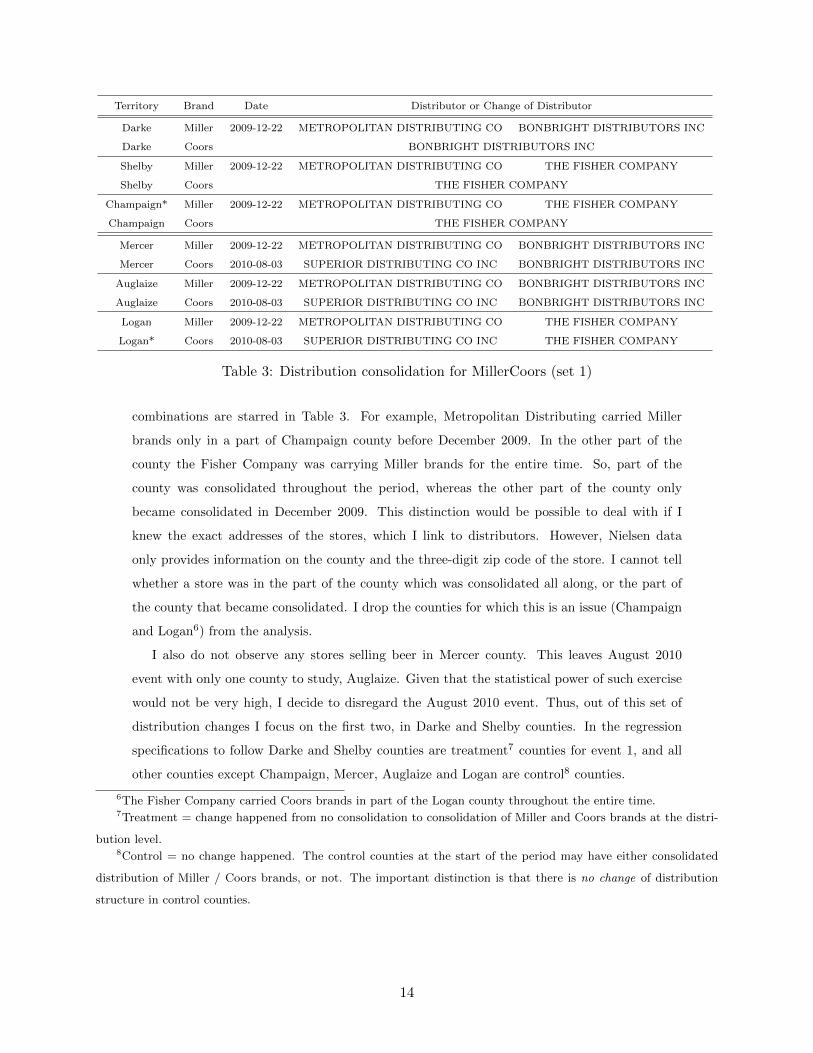

Following the MillerCoors joint venture the manufacturers tried to consolidate their distribu-

tion network, and in two cases they were able to do so. Tables 3 and 4 describe the distribution

changes which led to such consolidation.

First, in December 2009 MillerCoors discontinued their relationship with the Metropolitan

Distributing Company. Miller brands, which had been previously carried by the Metropolitan

Distributing, were transferred to two distributors of Coors brands: Bonbright Distributors and

the Fisher Company. In Darke, Shelby and Champaign counties the brands became fully con-

solidated at the distributor level in December 2009, either through Bonbright Distributors, or

the Fisher Company. In Mercer, Auglaize and Logan counties the brands were still being carried

separately for some part of 2010, because Coors brands were at the moment carried by Supe-

rior Distributing Company there. The full transition to consolidated distribution happened in

August 2010, when they were switched from the Superior Distributing Company to Bonbright

Distributors or the Fisher Company.

Potentially this first set of distribution changes gives me two consolidation events to study,

December 2009 and August 2010. However, there are further complications. As mentioned

before, some counties for some brands are divided into smaller territories. Such county-brand

13

Territory Brand Date Distributor or Change of Distributor

Darke Miller 2009-12-22 METROPOLITAN DISTRIBUTING CO BONBRIGHT DISTRIBUTORS INC

Darke Coors BONBRIGHT DISTRIBUTORS INC

Shelby Miller 2009-12-22 METROPOLITAN DISTRIBUTING CO THE FISHER COMPANY

Shelby Coors THE FISHER COMPANY

Champaign* Miller 2009-12-22 METROPOLITAN DISTRIBUTING CO THE FISHER COMPANY

Champaign Coors THE FISHER COMPANY

Mercer Miller 2009-12-22 METROPOLITAN DISTRIBUTING CO BONBRIGHT DISTRIBUTORS INC

Mercer Coors 2010-08-03 SUPERIOR DISTRIBUTING CO INC BONBRIGHT DISTRIBUTORS INC

Auglaize Miller 2009-12-22 METROPOLITAN DISTRIBUTING CO BONBRIGHT DISTRIBUTORS INC

Auglaize Coors 2010-08-03 SUPERIOR DISTRIBUTING CO INC BONBRIGHT DISTRIBUTORS INC

Logan Miller 2009-12-22 METROPOLITAN DISTRIBUTING CO THE FISHER COMPANY

Logan* Coors 2010-08-03 SUPERIOR DISTRIBUTING CO INC THE FISHER COMPANY

Table 3: Distribution consolidation for MillerCoors (set 1)

combinations are starred in Table 3. For example, Metropolitan Distributing carried Miller

brands only in a part of Champaign county before December 2009. In the other part of the

county the Fisher Company was carrying Miller brands for the entire time. So, part of the

county was consolidated throughout the period, whereas the other part of the county only

became consolidated in December 2009. This distinction would be possible to deal with if I

knew the exact addresses of the stores, which I link to distributors. However, Nielsen data

only provides information on the county and the three-digit zip code of the store. I cannot tell

whether a store was in the part of the county which was consolidated all along, or the part of

the county that became consolidated. I drop the counties for which this is an issue (Champaign

and Logan6) from the analysis.

I also do not observe any stores selling beer in Mercer county. This leaves August 2010

event with only one county to study, Auglaize. Given that the statistical power of such exercise

would not be very high, I decide to disregard the August 2010 event. Thus, out of this set of

distribution changes I focus on the first two, in Darke and Shelby counties. In the regression

specifications to follow Darke and Shelby counties are treatment7 counties for event 1, and all

other counties except Champaign, Mercer, Auglaize and Logan are control8 counties.

6The Fisher Company carried Coors brands in part of the Logan county throughout the entire time.7Treatment = change happened from no consolidation to consolidation of Miller and Coors brands at the distri-

bution level.8Control = no change happened. The control counties at the start of the period may have either consolidated

distribution of Miller / Coors brands, or not. The important distinction is that there is no change of distribution

structure in control counties.

14

Territory Brand Date Distributor or Change of Distributor

Athens Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Athens Miller AFP DISTRIBUTORS INC

Gallia Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Gallia Miller AFP DISTRIBUTORS INC

Hocking Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Hocking Miller AFP DISTRIBUTORS INC

Meigs Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Meigs Miller AFP DISTRIBUTORS INC

Morgan Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Morgan Miller AFP DISTRIBUTORS INC

Washington Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Washington Miller AFP DISTRIBUTORS INC

Fairfield* Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Fairfield Miller AFP DISTRIBUTORS INC

Perry* Coors 2010-06-04 KERR DISTRIBUTING CO INC AFP DISTRIBUTORS INC

Perry Miller AFP DISTRIBUTORS INC

Jackson Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Jackson Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Lawrence Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Lawrence Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Pickaway Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Pickaway Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Pike Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Pike Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Ross Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Ross Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Scioto Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Scioto Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Vinton Coors 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Vinton Miller 2010-06-04 KERR WHOLESALE CO AFP DISTRIBUTORS INC

Fayette Coors 2010-06-04 KERR WHOLESALE CO THE FISHER COMPANY

Fayette Miller 2010-06-04 KERR WHOLESALE CO THE FISHER COMPANY

Highland Coors 2010-06-04 BONBRIGHT DISTRIBUTORS INC

Highland* Miller 2010-06-04 KERR WHOLESALE CO STAGNARO DISTRIBUTING

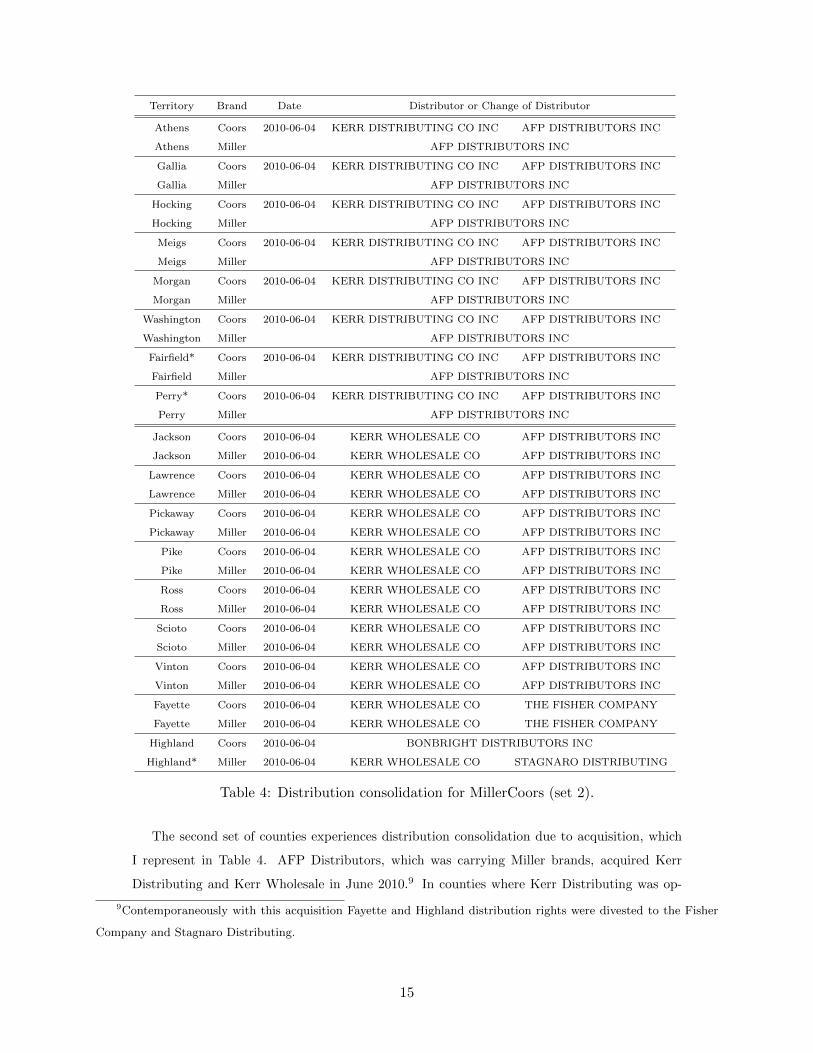

Table 4: Distribution consolidation for MillerCoors (set 2).

The second set of counties experiences distribution consolidation due to acquisition, which

I represent in Table 4. AFP Distributors, which was carrying Miller brands, acquired Kerr

Distributing and Kerr Wholesale in June 2010.9 In counties where Kerr Distributing was op-

9Contemporaneously with this acquisition Fayette and Highland distribution rights were divested to the Fisher

Company and Stagnaro Distributing.

15

erating, this acquisition led to consolidation of Miller and Coors brands in the hands of AFP

Distributors. In counties where Kerr Wholesale was operating, Miller and Coors were already

consolidated, so the change of ownership from Kerr Wholesale to AFP Distributors did not

affect the distribution consolidation status. Thus, counties of Kerr Distributing will serve as

treatment counties for this event, which I will call event 2 in the rest of the paper. Counties

of Kerr Wholesale will serve as control counties, along with many other counties where the

distribution consolidation status did not change.

Again, there are county-brand combinations divided into smaller territories (starred). With-

out documenting here which distributors carry the brands in parts of these counties, I sim-

ply state that the existence of county sub-division does not allow for clean data construction.

Similarly to analogous situation with event 1, I cannot tell whether distribution consolidation

happened or not in the upstream of the specific stores I observe. Thus, such counties (Fairfield,

Perry, Highland) are dropped from the analysis.

Finally, it turns out that all of the final distributors in the treatment counties also carried

Heineken and Modelo brands at the time when consolidation of MillerCoors distribution was

taking place. This means that not only Miller and Coors brands were consolidated in the hands

of one distributor, but also a brand that was transferred (Miller or Coors) was newly co-carried

with Heineken and Modelo. So, these brands should also be considered as “consolidated” brands,

along with Miller and Coors.

I explain my empirical strategy in more detail in section 5, but before that it is useful to

describe the uniform pricing which the chains employ across the state of Ohio.

4 Evidence on Uniform Pricing

As will be clear from the graphs below, the degree to which chains participate in uniform pricing

is quite high. However, it is not perfect in the sense that there are stores which deviate from

the median price in almost any week for a wide range of products. To illustrate these two points

I construct the following statistics. For each chain c, week t and product j, build a median

normalized10 price pmedjct across the stores s of chain c, and build the 10% and 90% empirical

percentiles of normalized prices.

10Where normalization is, as before, in terms of price for an equivalent of 144-oz. product volume.

16

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

10.00

10.25

10.50

10.75

11.00

11.25

11.50

11.75

12.00COORS LIGHT 6-packMILLER LITE 6-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

8.75

9.00

9.25

9.50

9.75

10.00

10.25

10.50COORS LIGHT 12-packMILLER LITE 12-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4COOR LIGHT 24-packMILLER LITE 24-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

10.5

11.0

11.5

12.0

COORS LIGHT 6-packMILLER LITE 6-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

9.00

9.25

9.50

9.75

10.00

10.25

10.50

COORS LIGHT 12-packMILLER LITE 12-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6 COORS LIGHT 24-packMILLER LITE 24-pack

Figure 2: Food chains 130 and 89: median normalized price across all Ohio stores by week, and

[10, 90]-th percentile interval of normalized prices by week for Coors Light and Miller Lite.

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

10.25

10.50

10.75

11.00

11.25

11.50

11.75

12.00

12.25 COORS LIGHT 6-packMILLER LITE 6-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

8.75

9.00

9.25

9.50

9.75

10.00

10.25

10.50COORS LIGHT 12-packMILLER LITE 12-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

7.8

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4 COOR LIGHT 24-packMILLER LITE 24-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

11.0

11.5

12.0

12.5

13.0COORS LIGHT 6-packMILLER LITE 6-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

9.25

9.50

9.75

10.00

10.25

10.50

10.75

11.00COORS LIGHT 12-packMILLER LITE 12-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4

9.6COORS LIGHT 24-packMILLER LITE 24-pack

Figure 3: Drug store chains 4901 and 4904: median normalized price across all Ohio stores by week,

and [10, 90]-th percentile interval of normalized prices by week for Coors Light and Miller Lite.

17

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

10.5

11.0

11.5

12.0

COORS LIGHT 6-packMILLER LITE 6-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

9.00

9.25

9.50

9.75

10.00

10.25

10.50COORS LIGHT 12-packMILLER LITE 12-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

7.8

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4 COOR LIGHT 24-packMILLER LITE 24-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

10.00

10.25

10.50

10.75

11.00

11.25

11.50

11.75

12.00 COORS LIGHT 6-packMILLER LITE 6-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

8.75

9.00

9.25

9.50

9.75

10.00

10.25

10.50COORS LIGHT 12-packMILLER LITE 12-pack

2009010120090501

2009090120100101

2010050120100901

2011010120110501

2011090120120101

7.8

8.0

8.2

8.4

8.6

8.8

9.0

9.2

9.4 COORS LIGHT 24-packMILLER LITE 24-pack

Figure 4: Mass merchandise chains 6901 and 6904: median normalized price across all Ohio stores

by week, and [10, 90]-th percentile interval of normalized prices by week for Coors Light and Miller

Lite.

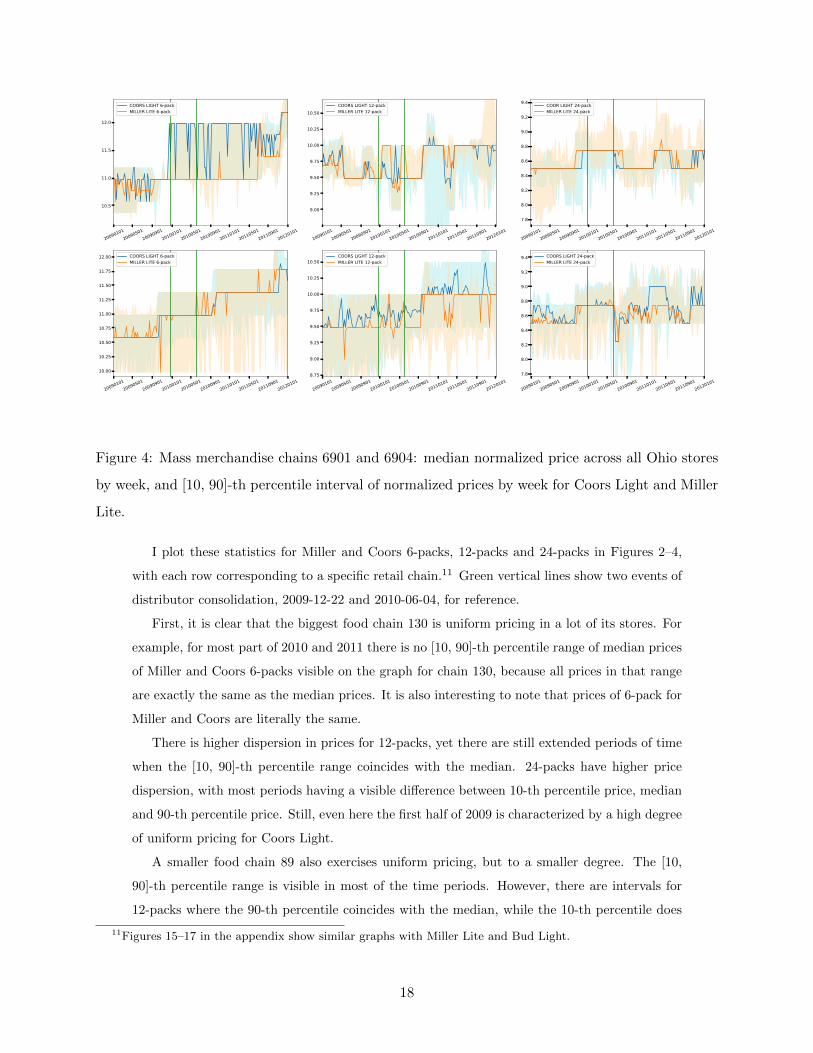

I plot these statistics for Miller and Coors 6-packs, 12-packs and 24-packs in Figures 2–4,

with each row corresponding to a specific retail chain.11 Green vertical lines show two events of

distributor consolidation, 2009-12-22 and 2010-06-04, for reference.

First, it is clear that the biggest food chain 130 is uniform pricing in a lot of its stores. For

example, for most part of 2010 and 2011 there is no [10, 90]-th percentile range of median prices

of Miller and Coors 6-packs visible on the graph for chain 130, because all prices in that range

are exactly the same as the median prices. It is also interesting to note that prices of 6-pack for

Miller and Coors are literally the same.

There is higher dispersion in prices for 12-packs, yet there are still extended periods of time

when the [10, 90]-th percentile range coincides with the median. 24-packs have higher price

dispersion, with most periods having a visible difference between 10-th percentile price, median

and 90-th percentile price. Still, even here the first half of 2009 is characterized by a high degree

of uniform pricing for Coors Light.

A smaller food chain 89 also exercises uniform pricing, but to a smaller degree. The [10,

90]-th percentile range is visible in most of the time periods. However, there are intervals for

12-packs where the 90-th percentile coincides with the median, while the 10-th percentile does

11Figures 15–17 in the appendix show similar graphs with Miller Lite and Bud Light.

18

not. This may be an indicator that it is more costly for a chain to allow a specific store to

deviate to a higher price, than to allow a discount.

Looking at the drug store chains in figure 3, the same patterns are visible here, with signifi-

cant amount of uniform pricing: note almost entire year for Miller 24-packs in chain 6901, and

September 2010 to September 2011 period for 6-packs and 12-packs in chain 6904. When the

deviations from the uniform price happen, they seem to be more pronounced than those for the

big food chains.

Finally, moving to the mass merchandise chains 6901 and 6904, we see that the extent of

uniform pricing is probably lower than for the food chains and drug stores, and the deviations

from the uniform price are higher in magnitudes.

I should note that more jagged graphs in Figures 3 and 4 relative to Figure 2 may be due

to the nature of Nielsen data. Drug stores and mass merchandise stores do not sell a lot of

beer, as we saw in the summary statistics. Since any given store may be missing a sale of a

product in a significant share of weeks, store which occupies a specific percentile may vary a

lot, causing high variation in percentiles from week to week. However, the higher magnitude of

[10, 90]-th percentile range is still a valid finding in these circumstances. If the stores fall out

of distribution due to a lack of a unit sold at random, this should not change the magnitude of

[10, 90]-th percentile range.12

The uniform pricing by chains documented in this section may be important in interpreting

the results of event studies of distributor consolidation, as is illustrated by a theoretical model

in Section 2. I turn to describing my empirical strategy and results next.

5 Distribution Consolidation Event Study

It is helpful to first fix some ideas about the possible effects of distributor consolidation, without

laying out the math for it. The extant literature modeling beer markets (Miller and Weinberg

(2017), Asker (2016)) assumed that the distributors are not actively exercising market power,

simply covering their costs with a markup.13

Consider for a moment what would happen if the distributors in fact were exercising market

12A reader may conjecture that stores in the right tail of price distribution should have a higher probability of

not having a unit sold. However, it may not be the case: stores which are pricing higher may be doing that based

on demand, so these higher prices in some neighborhoods may have the same demand (and probability of no sale) as

lower prices in other neighborhoods.13This view is sometimes supported by anecdotal evidence. As Asker (2016) writes in his study of Chicago beer

market in 1994, “When dealing with a large supermarket chain, a sales representative from the brewer will arrive at

a wholesale price for the chain with the chain’s buyer. Distributors are then expected to supply at that price. While

RPM is prohibited explicitly... this practice does not appear to invite legal sanction.”

19

power. Consolidation of distribution, such as moving Miller brand to the same distributor who is

carrying Coors, Heineken and Modelo, would create the same incentives for the distributor as in

a usual horizontal merger. The distributor would be able to internalize the effect of raising Miller

prices on the demand for Coors, Heinieken and Modelo, and the other way around. This would

create upward pricing pressure for these brands. A distributor of a different, non-consolidated

brand, like ABI, will raise its prices in turn, following the usual logic of prices being strategic

complements in Nash-Bertrand price competition. However, this price increase would not be as

big as the price increase of consolidated brands, because ABI does not have the additional effect

of internalizing the pricing externality.

This description calls for a difference-in-difference approach to testing if distributors actively

exercise market power. If they do, following distributor consolidation, price increase of the

consolidated brands (Miller, Coors, Heineken, Modelo), should be higher than price change of

the brands not consolidated (ABI).

There is also a concern that contemporaneously with distributor consolidation there may be

some differential changes to the marginal costs of brands involved, which may contaminate the

results. For example, a decrease in marginal costs for only ABI would decrease its prices relative

to the brands involved in distribution consolidation, and give a false impression of the significant

effect of distributor marker power.14 In order to control for this, it is better to compare the

price changes in the counties that experienced the distributor consolidation to price changes in

counties which did not.15

The considerations above leads me to the following triple difference-in-difference empirical

specification:

log pjs(c)t(m) = γ1Itreatc + γ2Ipostt + γ3Itreatc · Ipostt +

+ γ4Itreatc · Iconsj + γ5Ipostt · Iconsj + γ6Itreatc · Ipostt · Iconsj +

+ αjc + βm + εjst

(1)

where indices are j for product, s for store, c for county, t for week, and m for month; the

observation level is product-week-store.

Price is regressed on the indicator of treatment Itreatc — the counties which experienced

distributor consolidation, indicator of post consolidation event Ipostt , their interaction, and in-

teractions of each of these three variables with the indicator of brands directly participating

in distributor consolidation Iconsj . The regression also includes chain-product fixed effects αjc

to control for the average price that a chain sets for a product, and month fixed effects βm to

14A contemporaneous state-wide change in the pricing policy of one of the manufacturers, like a price slash for a

state-wide sale of inventories by ABI, would be problematic in the same way.15Regardless of whether they were or were not consolidated in the first place. What is essential is that they do

not have a change of distribution event in the studied period.

20

control for seasonality in beer pricing. I use the entire period of 2009–2011 in the regressions

to be able to capture these seasonality effects from at least three years of data.16 I use robust

standard errors, clustered at the product level: graphical representation of prices in the previous

section indicates that prices of a given product may have common shocks across different chains.

To clarify ideas about which coefficients in this regression I care about, in Table 5 I show

which of the indicators will be one for which observations. As explained in the discussion

above, first I want to test whether the distributor consolidation has a differential effect on

the consolidated brands (Miller, Coors, Heineken, Modelo) vs. those non-consolidated (ABI).

For ABI the difference in price change between treatment and control counties is given by the

coefficient on Itreatc · Ipostt , γ3. For consolidated brands the difference in price change between

treatment and control counties is given by the coefficients on Itreatc · Ipostt and Itreatc · Ipostt · Iconsj ,

γ3 + γ6. Hence, to test my first hypothesis I need to look at the coefficient γ6.

Pre Post

ABI in control counties - Ipostt

ABI in treatment counties Itreatc Itreat

c , Ipostt , Itreat

c · Ipostt

Consolidated brands in control counties - Ipostt , Ipost

t · Iconsj

Consolidated brands Itreatc , Itreat

c · Iconsj Itreat

c , Itreatc · Icons

j , Ipostt , Ipost

t · Iconsj ,

in treatment counties Itreatc · Ipost

t , Itreatc · Ipost

t · Iconsj

Table 5: Indicator variables which are equal to one for different groups of observations.

The second hypothesis is that distributor consolidation in some counties creates upward

pricing pressure, which cannot manifest locally, due to uniform chain pricing. However, this

upward pricing pressure may reflect in the higher price level for consolidated brands across

all counties. As follows from Table 5, the relevant coefficient to test this hypothesis is on

Ipostt · Iconsj , γ5. When we think about pre / post comparison for all counties, Ipostt is the effect

which is present in both ABI and consolidated brand cells, and Ipostt ·Iconsj is the additional effect

present only for consolidated brands. I only include in the regression chains which have stores

in the treatment counties, in order to be able to test this hypothesis. If I included the chains

which never sell in the treatment counties, the effect estimate could be attenuated (since such

chains do not experience the distributor consolidation for any of their stores, but they would

participate in estimation of Ipostt · Iconsj coefficient).

Another thing to mention here is the control counties need to be picked carefully. The

16In Table 10 in appendix I report the same regressions as in the main part of the paper, but only on 2009–2010,

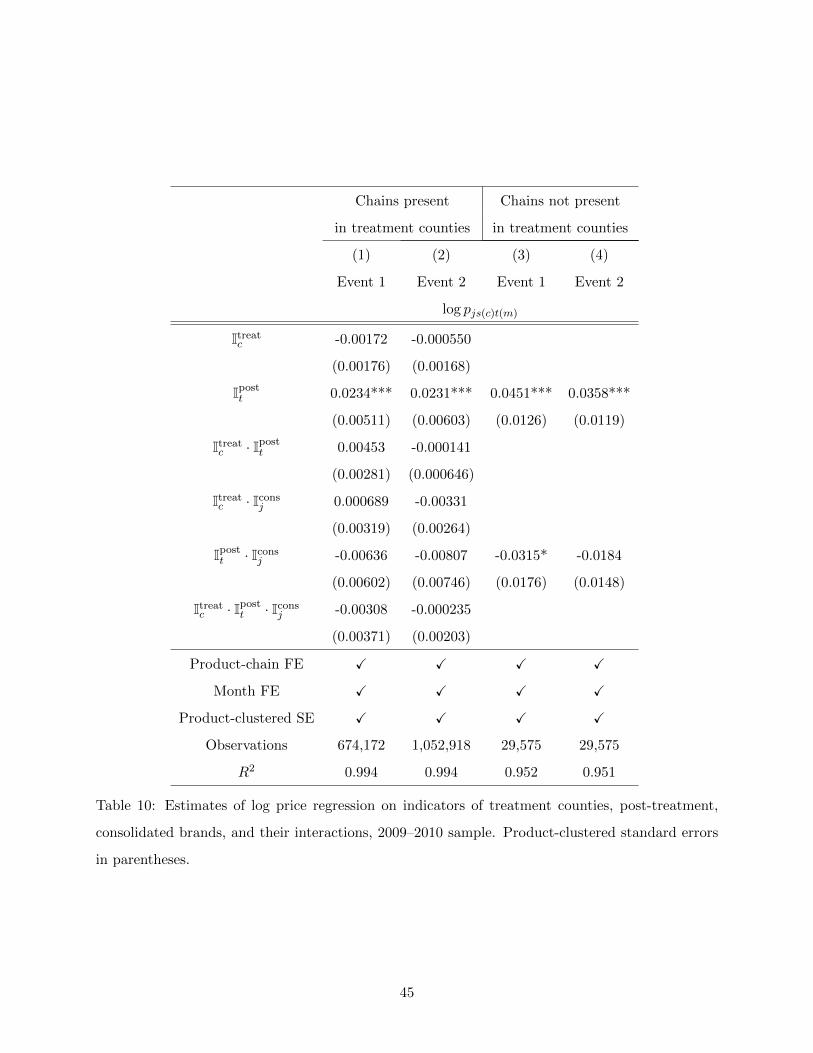

as a robustness check. The results are qualitatively the same.

21

counties which are participating or ambiguous in distributor consolidation for event 2 cannot be

used as control counties for event 1.17 For example, if there is a distribution consolidation effect,

such counties of event 2, if included in the regression for event 1 as control, will experience it in

the post period in control group, and this will bias the estimate of γ6 down. Consistently with

this logic and the description of the data in Tables 3 and 4 counties Athens, Gallia, Hocking,

Meigs, Morgan, Washington (treatment of event 2) are excluded from the regression for event 1.

Counties Darke and Shelby (treatment of event 1) are excluded from the regression for event 2.

Counties Champaign, Mercer, Auglaize, Logan, Fairfield, Perry and Highland (those for which

I cannot tell apart the stores where distribution consolidation happened vs. not) are excluded

from both regressions.

5.1 Contemporaneous effect of distributor consolidation

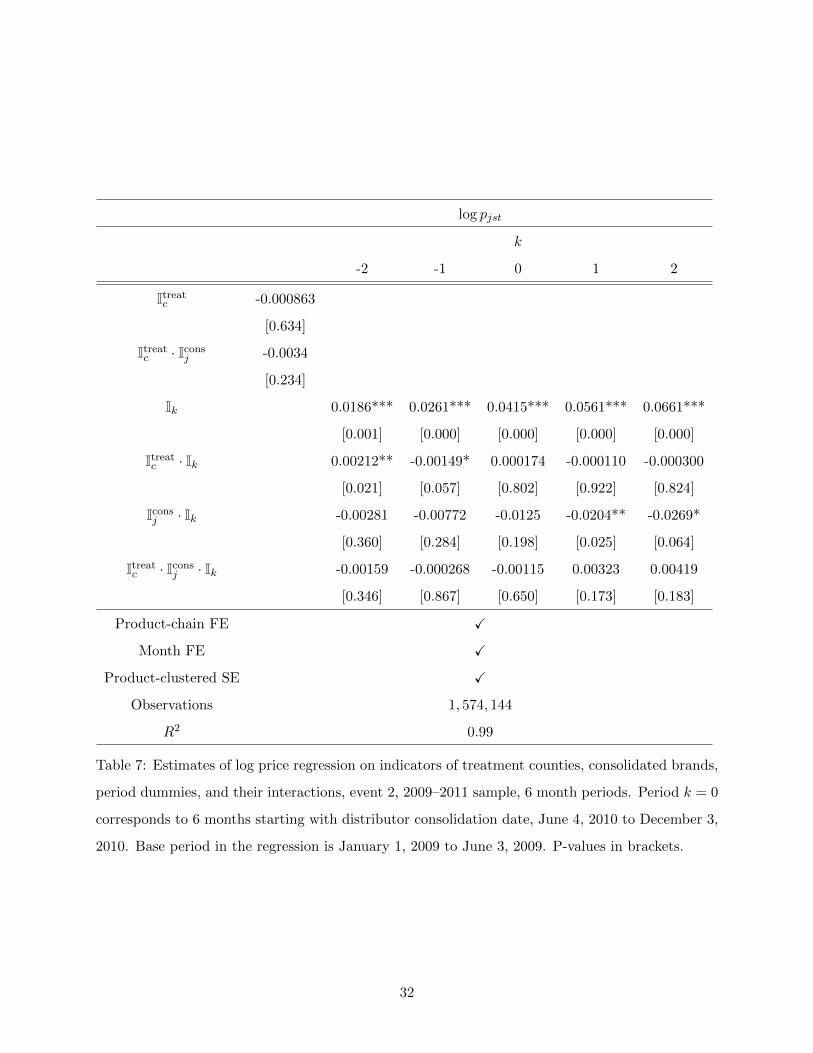

Table 6 reports the results of empirical specification 1, in column 1 for event 1 around December

2009, and in column 2 for event 2 around June 2010. First, it is useful to note that the prices

of both consolidated and non-consolidated brands are statistically the same in treatment and

control counties before distribution consolidation: both coefficients on Itreatc and Itreatc · Iconsj are

close to 0 and insignificant.18

Turning to the coefficient of interest on the interaction Itreatc ·Ipostt ·Iconsj , we see that it is close

to zero and not statistically significant. The point estimates of the effect of distribution con-

solidation effect on prices are −0.36% and 0.28% respectively. I should note, however, that my

standard errors are comparable to the point estimates. For event 1, the 95% confidence interval

of the distribution consolidation effect is [−1.21%, 0.49%], and for event 2 it is [−0.10%, 0.65%].

Thus, the largest positive effect I cannot reject is 0.65%. Overall I find these results indicative of

no economically important contemporaneous effect of distributor consolidation on consolidated

brands in treated counties.

Of course, this finding may not be very surprising, given the evidence of chain uniform

pricing I showed in section 4. If the store managers are constrained by the chain pricing policy,

they may not increase local prices even if the distributor in their area raises the wholesale prices

post-consolidation. This idea justifies the second test which I consider. The higher pricing

pressure by the consolidated distributor may reflect not in higher local prices, but rather in

higher prices across the entire state of Ohio. As discussed above, the coefficient on Ipostt · Iconsj

17and vice versa18I drop Michelob brands in all regressions, and only keep Budweiser and Bud Light for ABI. This is driven by

the fact that Michelob brands were actually priced differently in the treatment and control counties pre-distribution

change, as opposed to the other brands included in the regression. This potentially indicated that Michelob brands,

as more niche, are not very suitable as a control group.

22

Chains present Chains not present

in treatment counties in treatment counties

(1) (2) (3) (4)

Event 1 Event 2 Event 1 Event 2

log pjs(c)t(m)

Itreatc -0.00147 -0.000564

(0.00175) (0.00165)

Ipostt 0.0368*** 0.0384*** 0.0636*** 0.0529***

(0.00584) (0.00630) (0.0136) (0.0110)

Itreatc · Ipost

t 0.00495 -0.000247

(0.00356) (0.000822)

Itreatc · Icons

j 0.000858 -0.00406

(0.00302) (0.00262)

Ipostt · Icons

j -0.0139* -0.0166* -0.0400** -0.0303**

(0.00759) (0.00849) (0.0182) (0.0142)

Itreatc · Ipost

t · Iconsj -0.00357 0.00275

(0.00421) (0.00188)

Product-chain FE X X X X

Month FE X X X X

Product-clustered SE X X X X

Observations 1,001,064 1,574,144 46,948 46,948

R2 0.993 0.993 0.949 0.948

Table 6: Estimates of log price regression on indicators of treatment counties, post-treatment,

consolidated brands, and their interactions, 2009–2011 sample. Product-clustered standard errors

in parentheses.

23

tests this hypothesis.

The respective point estimates are −1.39% and −1.66%, significant at the 10% level. If

anything, prices changes of consolidated brands were lower than price changes of ABI.19

The idea that distributor consolidation may not only affect the stores in the distributor’s

territories, but the entire chain, allows for some additional evidence. There are chains in my

data which never sold in the territories treated by the distributor change. These are the smaller

food chains 295 and 9104, mass merchandise chain 6914 and convenience store chain 8199, selling

a combined 1.5% of the selected beer brands in Nielsen data.

For these chains I run a simpler difference-in-difference specification:

log pjs(c)t(m) = γ2Ipostt + γ5Ipostt · Iconsj +

+ αjc + βm + εjst

(2)

This regression allows me to see price increases of ABI, and price increases of other brands

post-distribution change for the chains which should not have been affected by the distribution

change at all. The results are reported in columns 3 and 4 of Table 6. For some reason ABI

prices increased more at these chains than chains from regressions 1–2 (compare 6.36% increase

to 3.68% for event 1, and 5.29% increase to 3.84% for event 2). However, price increases of

other brands were the same. Summing up γ2 + γ5, for event 1 we have 2.29% price increase of

consolidated brands for the chains present in counties with newly consolidated distributors, and

2.36% increase for the chains not present. For event 2, the estimated price increases are 2.18%

and 2.26%.

Interpretation of these findings is a little complicated by the differential effect of ABI. If

one believes that ABI is the correct control group when comparing column 1 to 3, and column

2 to 4, she would conclude the following. For chains which were not treated by distribution

consolidation, price changes of Miller, Coors, Heineken and Modelo brands have a bigger gap

with ABI price changes. Thus, the distributor consolidation must have had a positive effect on

prices at the chains to which consolidated distributors do sell.

However, my interpretation is that the differential price changes of ABI in these columns

indicate something idiosyncratic to ABI and the small chains which participate in regressions (3),

(4).20 To me close price changes of Miller, Coors, Heineken and Modelo in chains to which newly

consolidated distributors do and do not sell serve as additional evidence that contemporaneously

the distribution structure did not have an effect on the overall pricing of a chain.

19I should note that this finding could also be explained by different changes in marginal costs for ABI and

consolidated brands around the same point in time.20Note that this was not a problem for interpretation of results in columns 1 and 2 in solitary, since the additional

effect on ABI brands in treatment counties (Itreatc · Ipostt ) was not statistically significant.

24

5.2 Lagged effect of distributor consolidation

In this subsection I show, first, evidence of parallel trends before the consolidation event, and,

second, evidence of lagged effect for event 2.

To illustrate the validity of parallel trends assumption, the date of ‘placebo’ event is placed

in different parts of the timeline to show that there is no significant effect before the actual event

date. A reader would like to see that, when placed in the ‘placebo’ spots, the event dummy

interacted with relevant variables is not statistically significant. If these placebo tests turn out

to fail (showing a significant coefficient) before the actual event, this may indicate a potential

problem with identification: it would seem that there are some unobserved events which lead to

effects being different in treatment and control groups.

If a significant coefficient is found after the actual event, this indicates a lagged effect of the

distributor consolidation, which is another reason to do this exercise.

Formally, I run the same regressions as in 1, but with post variable Ipostt varying its timing.

I change the timing of Ipostt in monthly intervals, up to 15 months before and after the actual

event, as long as there are at least 3 months of data left in the pre- or post-period. For every

month I run a separate regression, and report coefficients of interest and their 95% confidence

intervals varying with month in Figures 5–7 for event 1, and Figures 8–11 for event 2. The plots

show a vertical line at the time of the actual event, and a horizontal line at zero.

0.0

1.0

2.0

3In

tera

ctio

n of

trea

tmen

t*po

st c

oef.

22jun2009 22dec2009 22jun2010 22dec2010date

Figure 5: Coefficient on Itreatc · Ipost

t with placebo event dates: Additional price increase of ABI in

the post period in treatment counties relative to control counties. Set of counties and chains for

event 1. The point estimate and 95% confidence interval are shown. Green vertical line represents

the actual event date.

25

I start the analysis with event 1, coefficient on Itreatc ·Ipostt , which is shown in Figure 5. Recall

from Table 5 that this is the additional price increase of ABI in the treatment counties relative

to control counties in the post period. It is useful to look at this coefficient to check if the

control group — ABI brands — is experiencing any differential price changes in treatment vs

control counties. We can see that all the coefficients for both pre-actual event and post-actual

event are not significantly different from zero. So, price increases of ABI are the same in control

and treatment counties, which is what we could expect, given that ABI brands are not directly

affected by distributor consolidation.21

-.04

-.03

-.02

-.01

0In

tera

ctio

n of

pos

t*co

nsol

idat

ed b

rand

s co

ef.

22jun2009 22dec2009 22jun2010 22dec2010date

Figure 6: Coefficient on Ipostt · Icons

j with placebo event dates: Additional price increase of consoli-

dated brands (Miller, Coors, Heineken, Modelo) relative to ABI in the post period in all counties.

Set of counties and chains for event 1. The point estimate and 95% confidence interval are shown.

Green vertical line represents the actual event date.

Figure 6 displays the coefficient on Ipostt · Iconsj , which tests my second hypothesis of dis-

tributor consolidation increasing prices across the entire chain. Recall from contemporaneous

analysis that this coefficient was negative, and significant at 10% confidence level. The placebo

analysis reveals that this coefficient barely changes with the placebo event date, staying bor-

derline significant at 5% level. The interpretation of this is that, wherever you put the placebo

event date, the consolidated brands are increasing their prices less in the post period than ABI.

21I need to mention here that if consolidated brands did increase their prices more in the treatment counties post-

consolidation, the strategic complementarity of prices should in theory lead to ABI also increasing their prices more

in treatment counties. We do not observe this, which serves as indirect evidence of lack of distribution consolidation

effect for event 1.

26

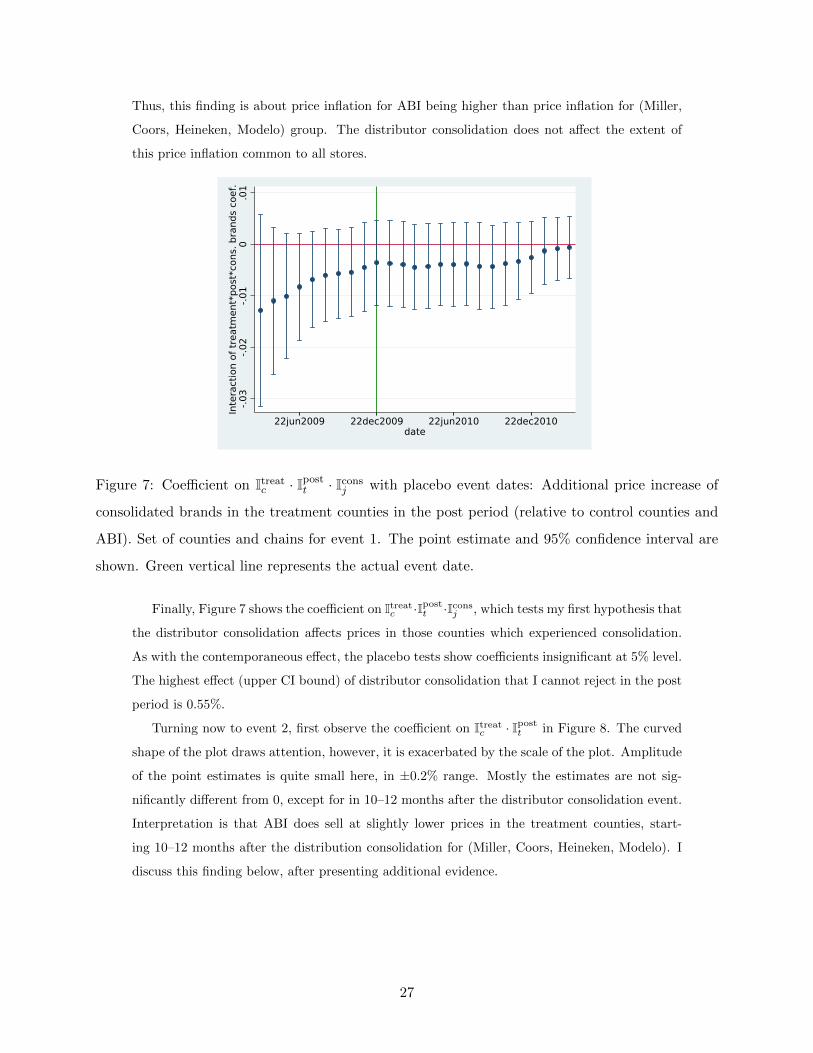

Thus, this finding is about price inflation for ABI being higher than price inflation for (Miller,

Coors, Heineken, Modelo) group. The distributor consolidation does not affect the extent of

this price inflation common to all stores.

-.03

-.02

-.01

0.0

1In

tera

ctio

n of

trea

tmen

t*po

st*c

ons.

bra

nds

coef

.

22jun2009 22dec2009 22jun2010 22dec2010date

Figure 7: Coefficient on Itreatc · Ipost

t · Iconsj with placebo event dates: Additional price increase of

consolidated brands in the treatment counties in the post period (relative to control counties and

ABI). Set of counties and chains for event 1. The point estimate and 95% confidence interval are

shown. Green vertical line represents the actual event date.

Finally, Figure 7 shows the coefficient on Itreatc ·Ipostt ·Iconsj , which tests my first hypothesis that

the distributor consolidation affects prices in those counties which experienced consolidation.

As with the contemporaneous effect, the placebo tests show coefficients insignificant at 5% level.

The highest effect (upper CI bound) of distributor consolidation that I cannot reject in the post

period is 0.55%.

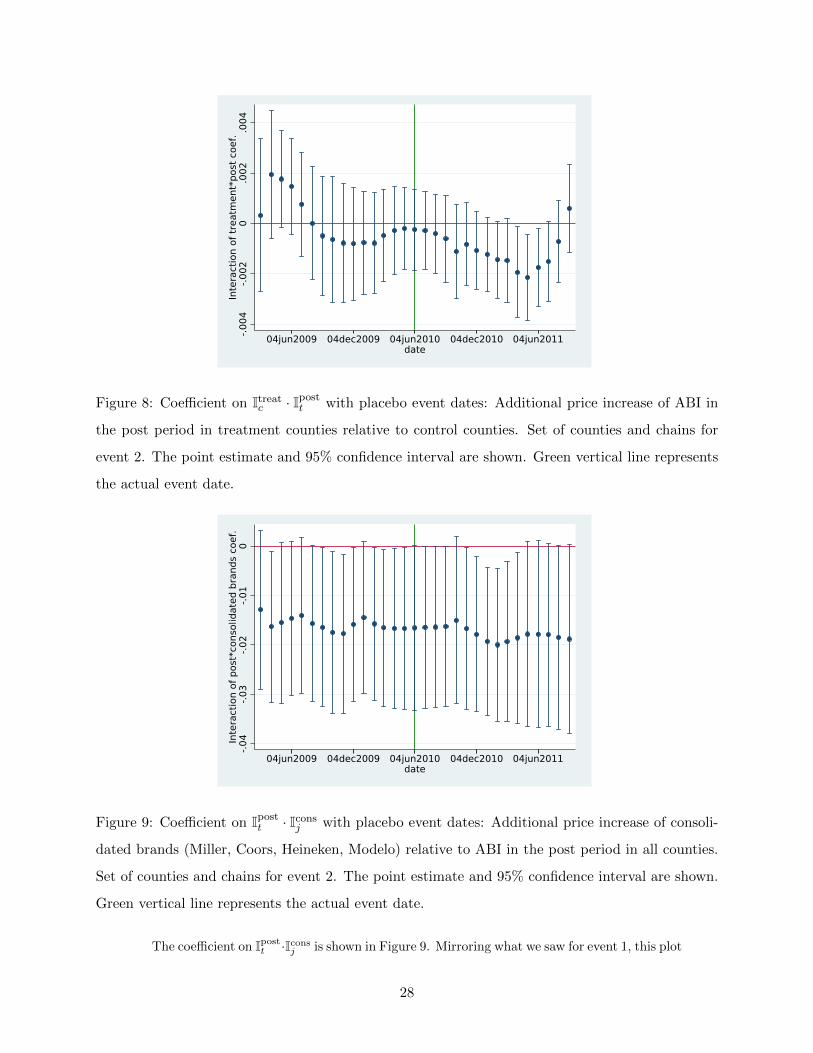

Turning now to event 2, first observe the coefficient on Itreatc · Ipostt in Figure 8. The curved

shape of the plot draws attention, however, it is exacerbated by the scale of the plot. Amplitude

of the point estimates is quite small here, in ±0.2% range. Mostly the estimates are not sig-

nificantly different from 0, except for in 10–12 months after the distributor consolidation event.

Interpretation is that ABI does sell at slightly lower prices in the treatment counties, start-

ing 10–12 months after the distribution consolidation for (Miller, Coors, Heineken, Modelo). I

discuss this finding below, after presenting additional evidence.

27

-.004

-.002

0.0

02.0

04In

tera

ctio

n of

trea

tmen

t*po

st c

oef.

04jun2009 04dec2009 04jun2010 04dec2010 04jun2011date

Figure 8: Coefficient on Itreatc · Ipost

t with placebo event dates: Additional price increase of ABI in

the post period in treatment counties relative to control counties. Set of counties and chains for

event 2. The point estimate and 95% confidence interval are shown. Green vertical line represents

the actual event date.

-.04

-.03

-.02

-.01

0In

tera

ctio

n of

pos

t*co

nsol

idat

ed b

rand

s co

ef.

04jun2009 04dec2009 04jun2010 04dec2010 04jun2011date

Figure 9: Coefficient on Ipostt · Icons

j with placebo event dates: Additional price increase of consoli-

dated brands (Miller, Coors, Heineken, Modelo) relative to ABI in the post period in all counties.

Set of counties and chains for event 2. The point estimate and 95% confidence interval are shown.

Green vertical line represents the actual event date.

The coefficient on Ipostt ·Iconsj is shown in Figure 9. Mirroring what we saw for event 1, this plot

28

suggests that the price inflation across all counties for consolidated brands is smaller than the

price inflation for ABI, and is not affected positively by the distributor consolidation. If anything,

the graph suggests that price inflation for (Miller, Coors, Heineken, Modelo) group goes down

in 6–10 months after the distributor consolidation event, relative to ABI price inflation.

-.01

-.005

0.0

05.0

1In

tera

ctio

n of

trea

tmen

t*po

st*c

ons.

bra

nds

coef

.

04jun2009 04dec2009 04jun2010 04dec2010 04jun2011date

Figure 10: Coefficient on Itreatc · Ipost

t · Iconsj with placebo event dates: Additional price increase of

consolidated brands in the treatment counties in the post period (relative to control counties and

ABI). Set of counties and chains for event 2. The point estimate and 95% confidence interval are

shown. Green vertical line represents the actual event date.

Finally, the most interesting finding is for the coefficient on Itreatc · Ipostt · Iconsj in Figure 10.

This coefficient is non-trivial and statistically significant for placebo dates 5–12 months after the

actual distribution consolidation. This may be perfectly explained by the distributors actually

having pricing power, which manifests a little later after the consolidation, for example, due to

rigidity of contracts in the short term.

Given that the consolidated brands increase prices more in the treatment counties starting

at 5–12 months after the event, we would also expect that ABI would increase prices more in

those counties due to price complementarity in Nash-Bertrand equilibrium. However, we do

not observe this: recall from Figure 8 that ABI actually decreased their prices in the treatment

counties, starting 10–12 months after the event. It is hard to say why this is the case without

having any additional information on ABI and its costs. It could be, for example, that the cost

of distribution for ABI in the treatment counties decreased, which created this negative effect.

Of course, such a possibility would make ABI not a proper control group. One would then be

interested in comparison of consolidated brands post- and pre- the placebo date in treatment

29

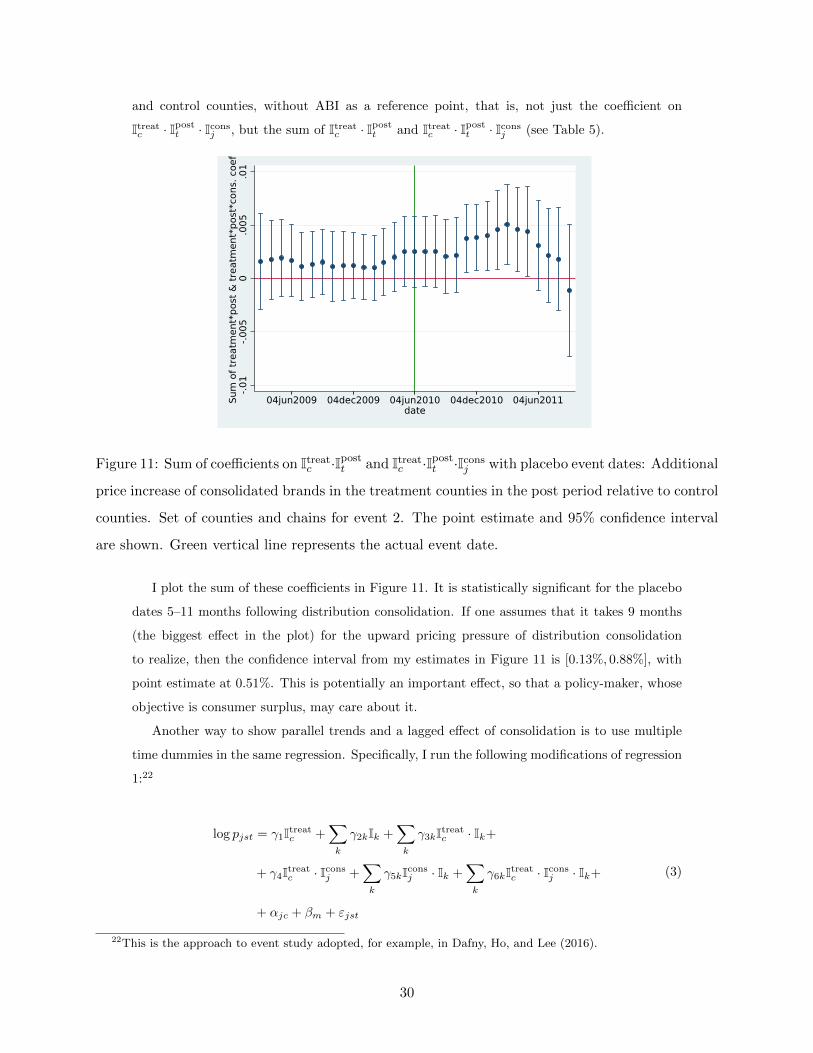

and control counties, without ABI as a reference point, that is, not just the coefficient on

Itreatc · Ipostt · Iconsj , but the sum of Itreatc · Ipostt and Itreatc · Ipostt · Iconsj (see Table 5).

-.01

-.005

0.0

05.0

1Su

m o

f tre

atm

ent*

post

& tr

eatm

ent*

post

*con

s. c

oef.

04jun2009 04dec2009 04jun2010 04dec2010 04jun2011date

Figure 11: Sum of coefficients on Itreatc ·Ipost

t and Itreatc ·Ipost

t ·Iconsj with placebo event dates: Additional

price increase of consolidated brands in the treatment counties in the post period relative to control

counties. Set of counties and chains for event 2. The point estimate and 95% confidence interval

are shown. Green vertical line represents the actual event date.

I plot the sum of these coefficients in Figure 11. It is statistically significant for the placebo