Embed Size (px)

Citation preview

1 | November 10, 2015

DFT’s Strategic Plan

November 10, 2015

2 | November 10, 2015

INTRODUCTION

Speakers today are:

Christopher Eldredge: President & Chief Executive Officer

Jeffrey Foster: Chief Financial Officer

Scott Davis: Executive Vice President of Data Center Operations

Agenda:

Company Presentation: 1:00 p.m. – 3:00 p.m.

Questions & Answers: 3:00 p.m. – 4:00 p.m.

3 | November 10, 2015

FORWARD LOOKING STATEMENTThis presentation contains forward-looking statements. We caution investors that any forward-looking statements included in this presentation are based on management’s beliefs and assumptions made by, and information currently available to, management.

Such forward-looking statements include statements relating to:

projected financial information, including our expected future financial and operational results, and the assumptions underlying such results;

the data center industry, including expected data center utilization, expected data, cloud and Internet utilization and spending rates; our ability to meet our liquidity and capital needs, including access to the capital markets and terms of capital and debt financings; our expected development plans, including entry into new markets and the benefits of new product designs; and our assumptions related to the leasing of available space to third-party customers, including expected rental rates, returns on invested

capital and mark-to-market assumptions following lease expirations.

When used, the words “anticipate,” “believe,” “expect,” “intend,” “may,” “might,” “plan,” “estimate,” “project,” “should,” “will,” “result” and similar expressions, which do not relate solely to historical matters, are intended to identify forward-looking statements.

Such statements are subject to risks, uncertainties and assumptions and are not guarantees of future performance, which may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected.

Some of the risks and uncertainties that may cause our actual results, performance or achievements to differ materially from those expressed or implied by forward-looking statements include, among others, the following: adverse general or local economic or real estate developments in our markets or the technology industry, including a continued and prolonged economic downturn; failure to successfully lease vacant space in or operate properties, defaults on or non-renewal of leases by customers; failure to collect customer obligations and note receivables; failure to obtain necessary financing, extend the maturity of or refinance our existing debt, or comply with the financial and other covenants of the agreements that govern our existing debt; decreased rental rates, increased vacancy rates or customer bankruptcies; increased interest rates; the failure of DuPont Fabros Technology, Inc. (“DFT”) to qualify and maintain qualification as a real estate investment trust, or REIT; adverse changes in tax laws; environmental uncertainties; risks related to natural disasters; financial market fluctuations, including disruptions in the financial and credit markets and the availability of capital and other financing; and changes in real estate and zoning laws.

The risks described above are not exhaustive, and additional factors could adversely affect our business and financial performance, including those discussed DFT’s annual report on Form 10-K for the year ended December 31, 2014 and Form 10-Q for the quarter ended September 30, 2015 filed with the Securities and Exchange Commission. We expressly disclaim any responsibility to update any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. Unless otherwise noted, all information in this presentation is as of September 30, 2015.

4 | November 10, 2015

DFT’s Strategic Plan

November 10, 2015

5 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

6 | November 10, 2015

DFT MISSION

We design and operate innovative data centers.

We create solutions with our customers that free them to focus on

their core business.

7 | November 10, 2015

DFT VISION

To remain the wholesale data center provider of choice, while

diversifying our customer base and expanding our geographic

presence to attain a 10% profitability growth rate.

8 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

9 | November 10, 2015

INVESTIGATION

What do current and prospective customers really want for the future?

What types of products and services might we offer?

What geographies and markets are most promising?

What’s the potential size of the opportunity in terms of MW’s and revenue?

Explored both broad and deep questions using common frameworks

10 | November 10, 2015

LEARNING

Affirmed our current approach and product

Multi-tenant data center remains viable

Current design/product suits existing customers

Surfaced new opportunities

Customer requirements vary

New flexible design attractive to expanded customer verticals

New opportunities and accelerated growth require new approach

11 | November 10, 2015

STRATEGIC FOCUS

We remain committed to the wholesale data center business –

thus capitalizing on our exceptional skill in design and operations,

and where the potential to lead is becoming even greater.

12 | November 10, 2015

CONCLUSION: Stay Focused on Wholesale

Market growth is exploding in large space and power needs which is more effectively served by wholesale Cloud (MSFT, GOOG, AMZN, CRM)

Social Networking (FB, TWTR, LNKD)

Enterprise (Fortune 1000)

Pricing is increasing and returns remain attractive

DFT has highest EBITDA margin Wholesale investment lower than retail

Wholesale G&A lower than retail

DFT only pure play wholesale option for investors

13 | November 10, 2015

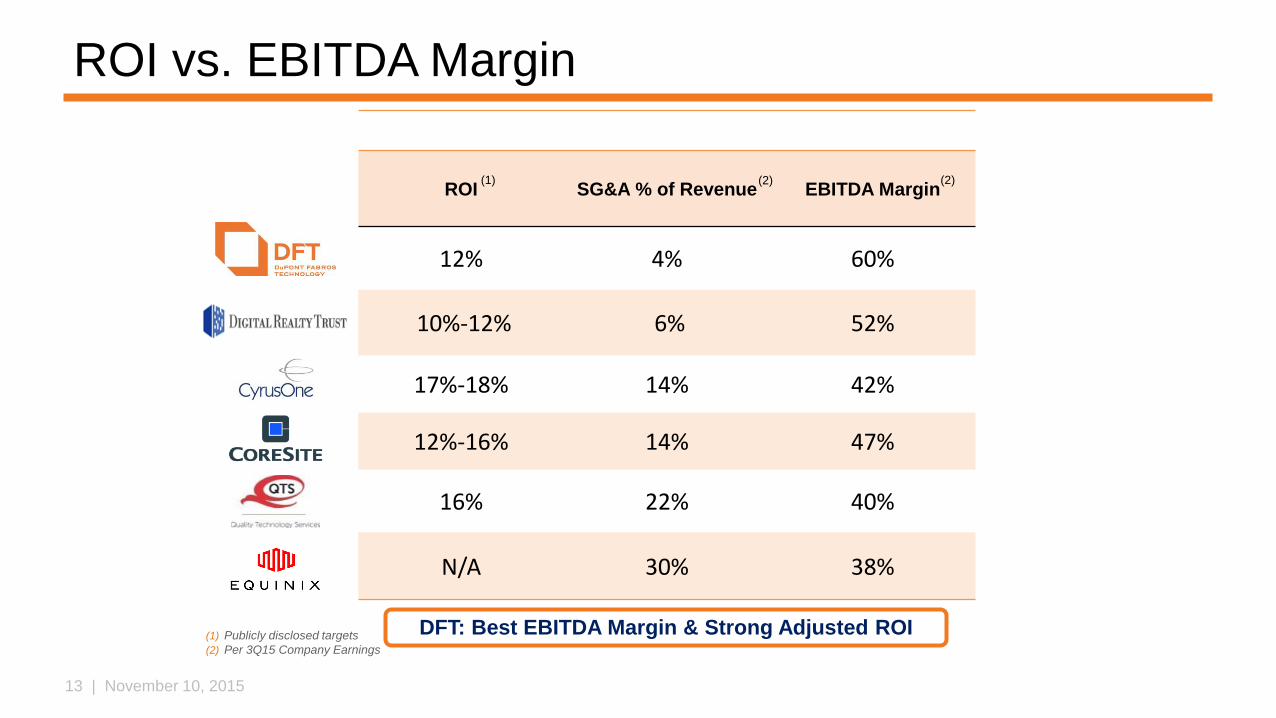

ROI vs. EBITDA Margin

ROI SG&A % of Revenue EBITDA Margin

12% 4% 60%

10%-12% 6% 52%

17%-18% 14% 42%

12%-16% 14% 47%

16% 22% 40%

N/A 30% 38%

(1) Publicly disclosed targets

(2) Per 3Q15 Company Earnings

DFT: Best EBITDA Margin & Strong Adjusted ROI

(1) (2) (2)

14 | November 10, 2015

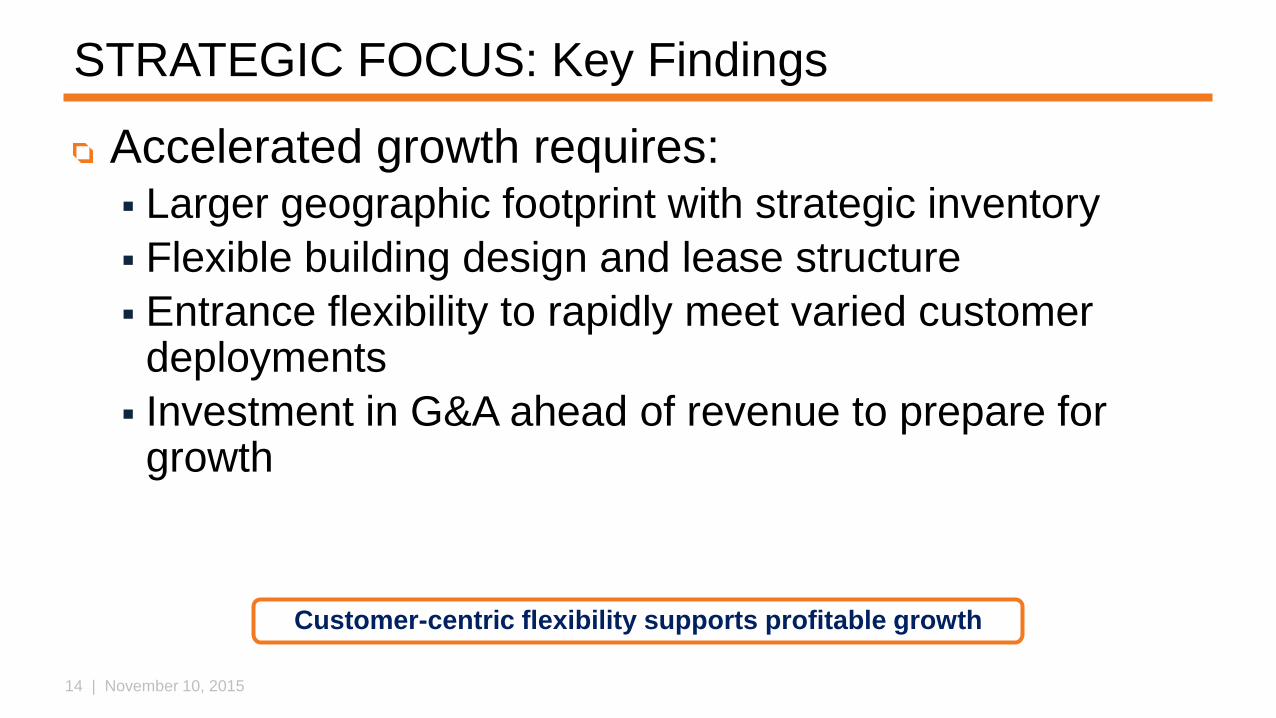

STRATEGIC FOCUS: Key Findings

Accelerated growth requires: Larger geographic footprint with strategic inventory

Flexible building design and lease structure

Entrance flexibility to rapidly meet varied customer deployments

Investment in G&A ahead of revenue to prepare for growth

Customer-centric flexibility supports profitable growth

15 | November 10, 2015

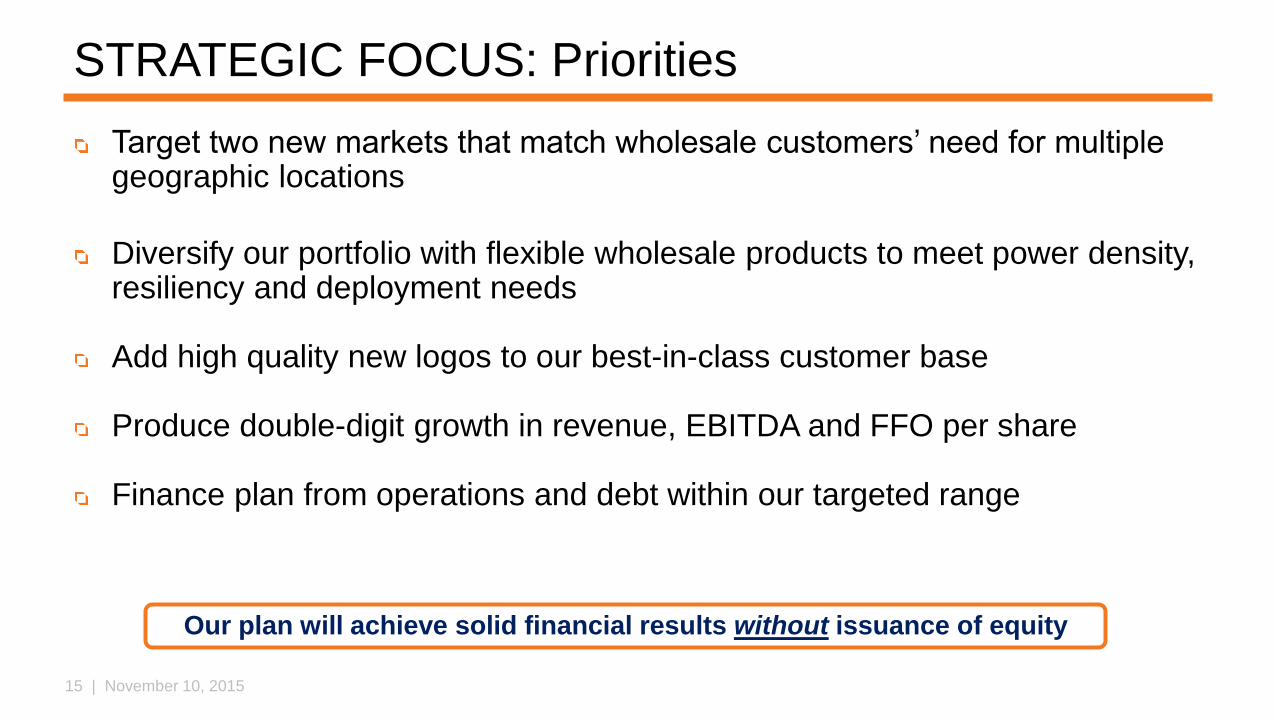

STRATEGIC FOCUS: Priorities

Target two new markets that match wholesale customers’ need for multiple geographic locations

Diversify our portfolio with flexible wholesale products to meet power density, resiliency and deployment needs

Add high quality new logos to our best-in-class customer base

Produce double-digit growth in revenue, EBITDA and FFO per share

Finance plan from operations and debt within our targeted range

Our plan will achieve solid financial results without issuance of equity

16 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

17 | November 10, 2015

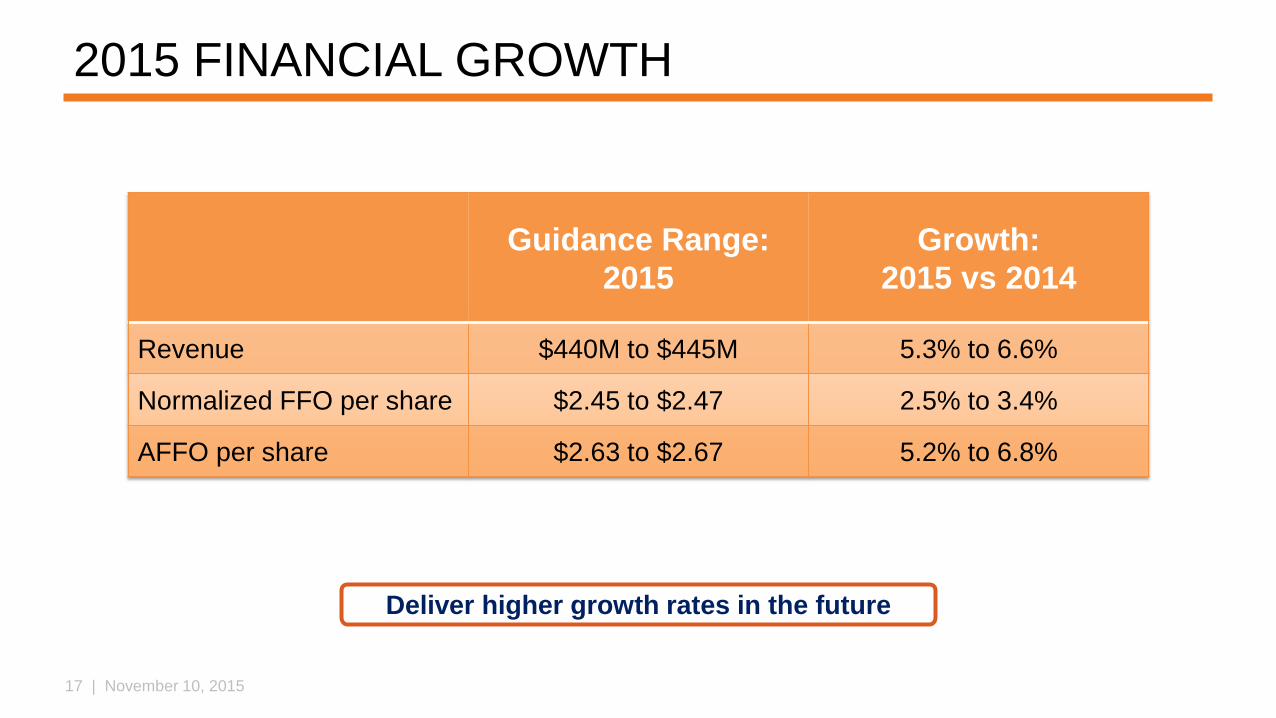

2015 FINANCIAL GROWTH

Deliver higher growth rates in the future

Guidance Range:

2015

Growth:

2015 vs 2014

Revenue $440M to $445M 5.3% to 6.6%

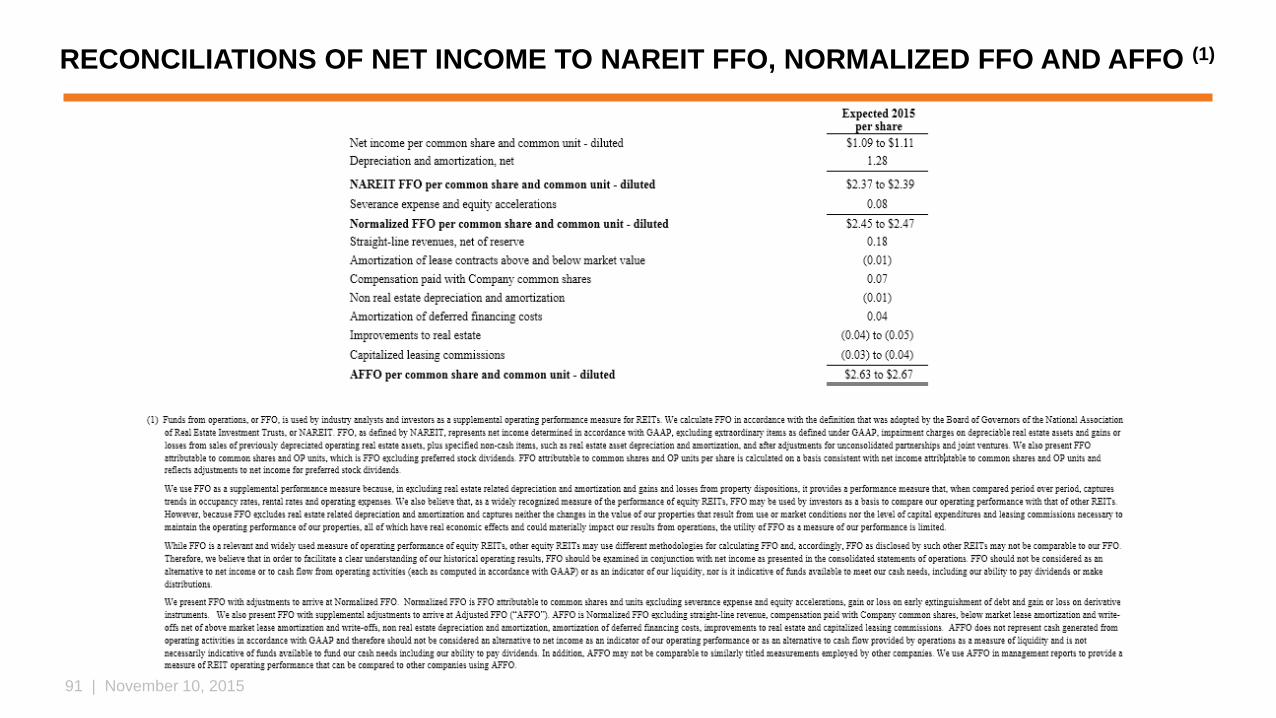

Normalized FFO per share $2.45 to $2.47 2.5% to 3.4%

AFFO per share $2.63 to $2.67 5.2% to 6.8%

18 | November 10, 2015

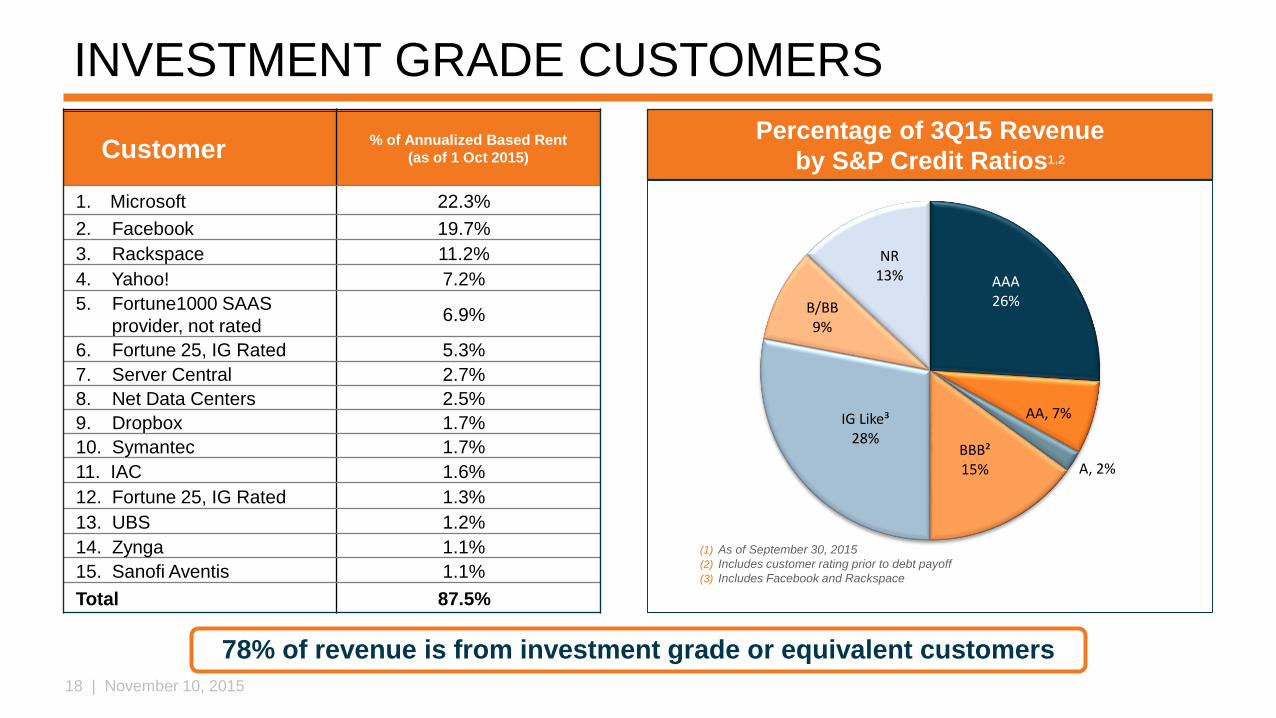

INVESTMENT GRADE CUSTOMERS

AAA26%

AA, 7%

2%

BBB²15%

IG Like³28%

B/BB9%

NR13%

Percentage of 3Q15 Revenue

by S&P Credit Ratios¹,²

(1) As of September 30, 2015

(2) Includes customer rating prior to debt payoff

(3) Includes Facebook and Rackspace

78% of revenue is from investment grade or equivalent customers

Customer% of Annualized Based Rent

(as of 1 Oct 2015)

1. Microsoft 22.3%

2. Facebook 19.7%

3. Rackspace 11.2%

4. Yahoo! 7.2%

5. Fortune1000 SAAS

provider, not rated6.9%

6. Fortune 25, IG Rated 5.3%

7. Server Central 2.7%

8. Net Data Centers 2.5%

9. Dropbox 1.7%

10. Symantec 1.7%

11. IAC 1.6%

12. Fortune 25, IG Rated 1.3%

13. UBS 1.2%

14. Zynga 1.1%

15. Sanofi Aventis 1.1%

Total 87.5%

A, 2%

19 | November 10, 2015

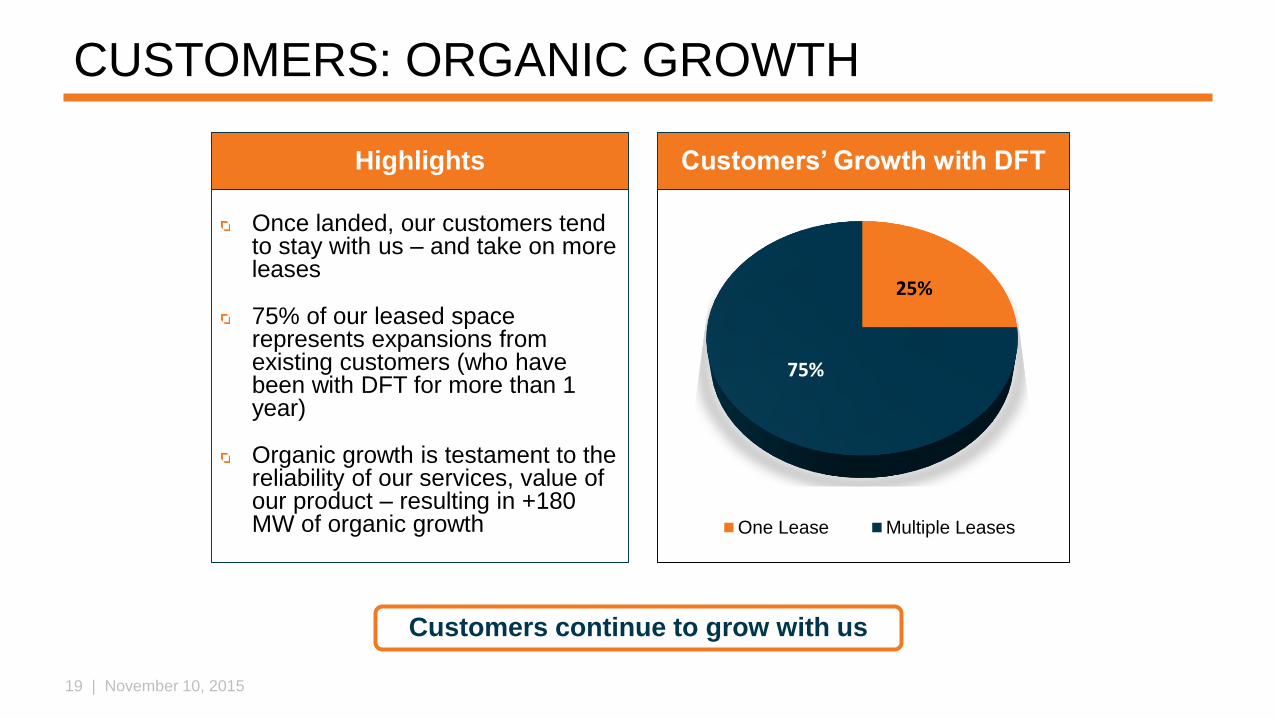

25%

75%

One Lease Multiple Leases

CUSTOMERS: ORGANIC GROWTH

Once landed, our customers tend to stay with us – and take on more leases

75% of our leased space represents expansions from existing customers (who have been with DFT for more than 1 year)

Organic growth is testament to the reliability of our services, value of our product – resulting in +180 MW of organic growth

Customers continue to grow with us

Customers’ Growth with DFTHighlights

20 | November 10, 2015

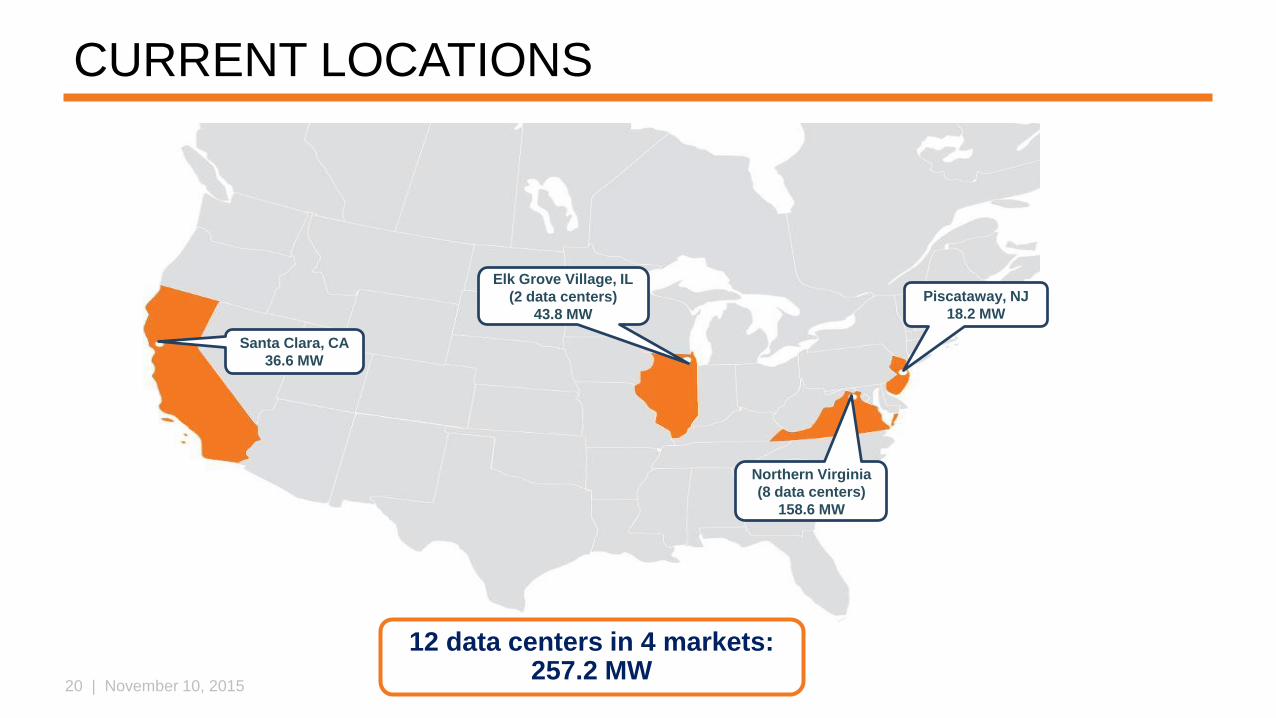

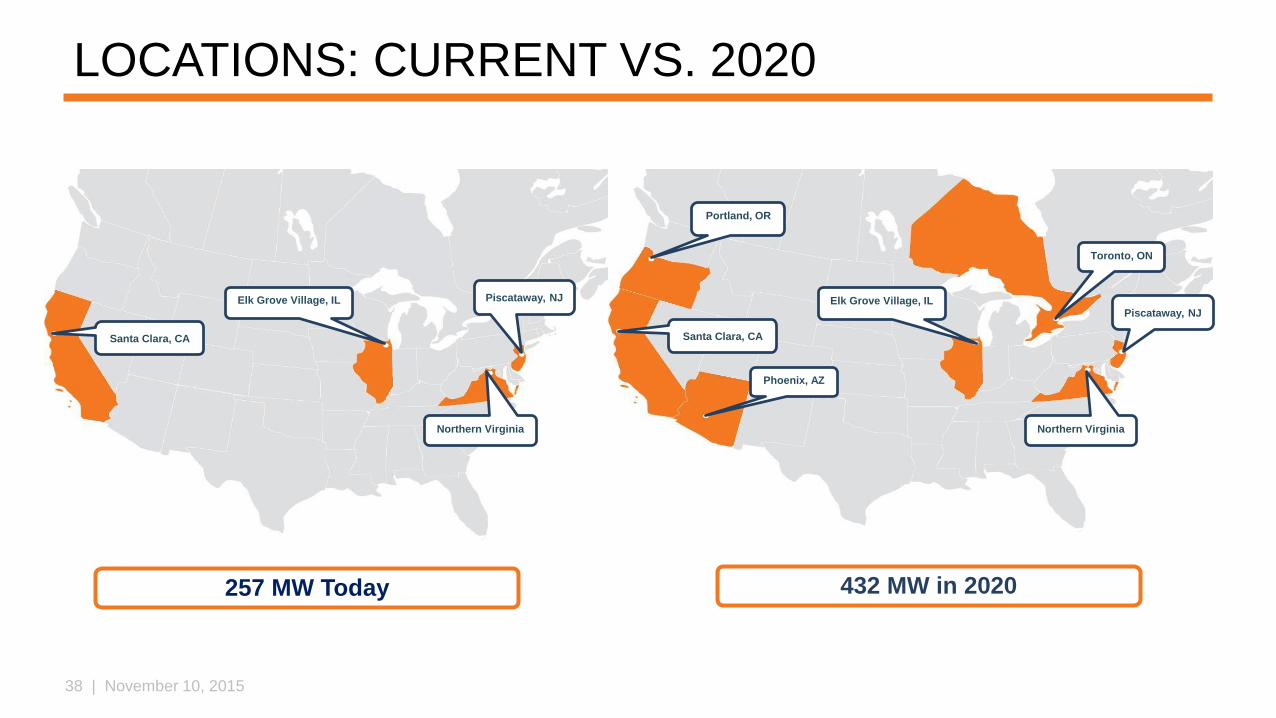

Santa Clara, CA

36.6 MW

Elk Grove Village, IL

(2 data centers)

43.8 MW

Piscataway, NJ

18.2 MW

Northern Virginia

(8 data centers)

158.6 MW

CURRENT LOCATIONS

12 data centers in 4 markets:257.2 MW

21 | November 10, 2015

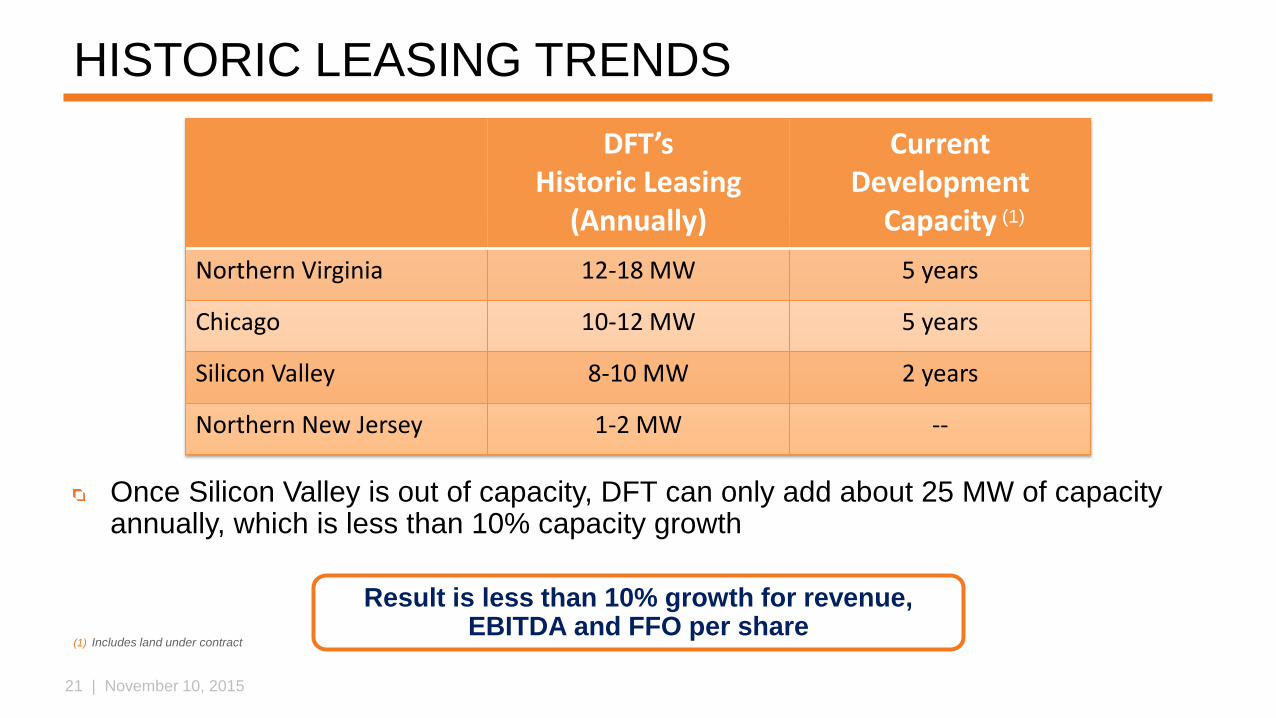

HISTORIC LEASING TRENDS

Once Silicon Valley is out of capacity, DFT can only add about 25 MW of capacity annually, which is less than 10% capacity growth

DFT’s Historic Leasing

(Annually)

Current Development

Capacity

Northern Virginia 12-18 MW 5 years

Chicago 10-12 MW 5 years

Silicon Valley 8-10 MW 2 years

Northern New Jersey 1-2 MW --

(1)

(1) Includes land under contract

Result is less than 10% growth for revenue, EBITDA and FFO per share

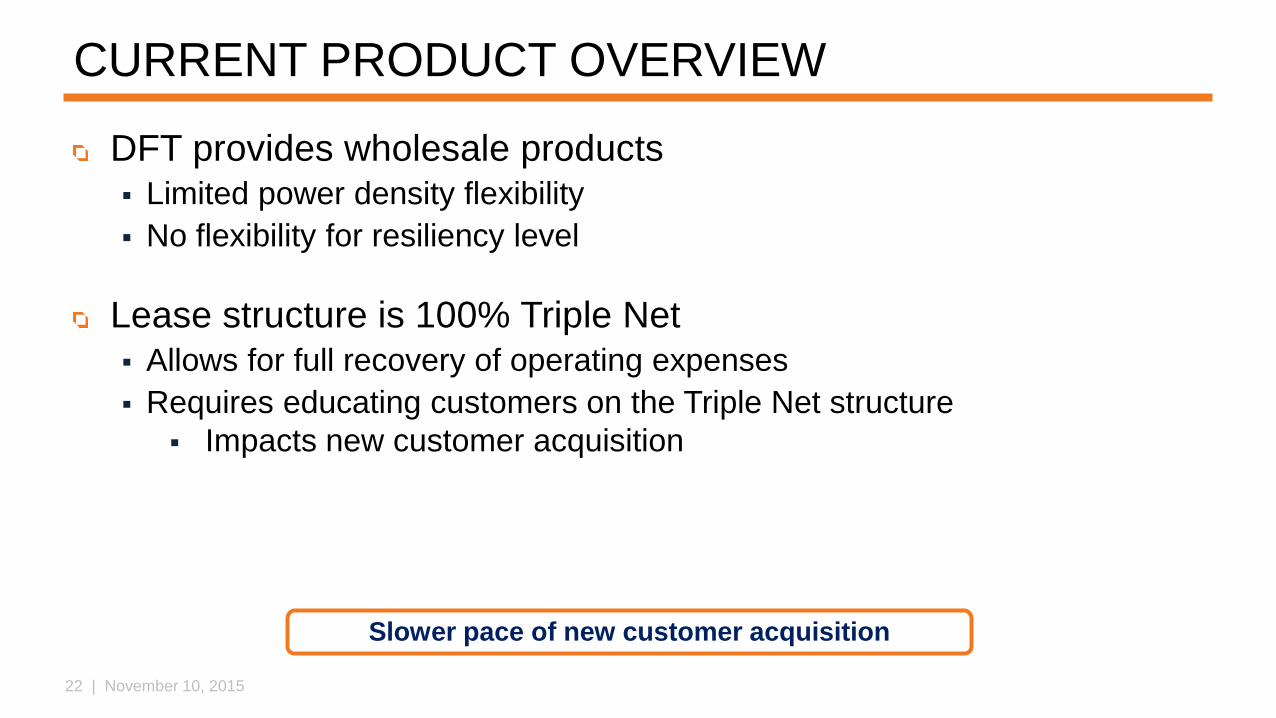

22 | November 10, 2015

Slower pace of new customer acquisition

CURRENT PRODUCT OVERVIEW

DFT provides wholesale products Limited power density flexibility

No flexibility for resiliency level

Lease structure is 100% Triple Net Allows for full recovery of operating expenses

Requires educating customers on the Triple Net structure

Impacts new customer acquisition

23 | November 10, 2015

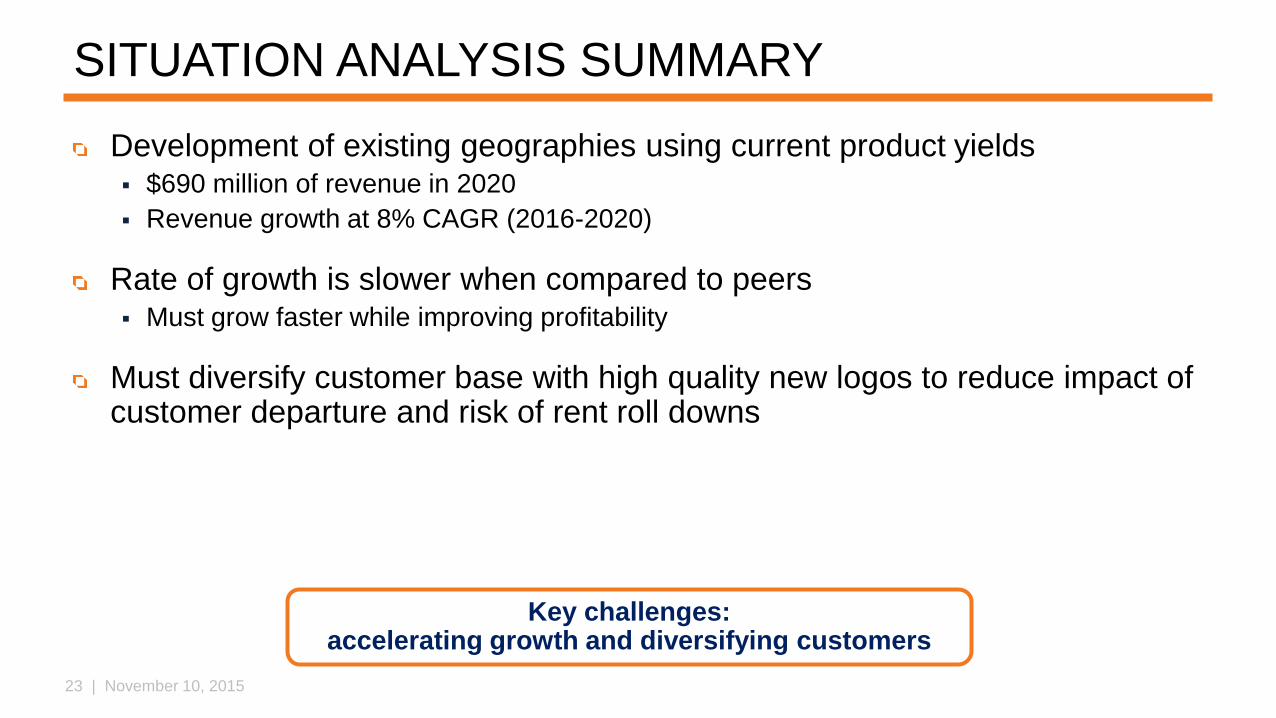

SITUATION ANALYSIS SUMMARY

Development of existing geographies using current product yields $690 million of revenue in 2020

Revenue growth at 8% CAGR (2016-2020)

Rate of growth is slower when compared to peers Must grow faster while improving profitability

Must diversify customer base with high quality new logos to reduce impact of customer departure and risk of rent roll downs

Key challenges: accelerating growth and diversifying customers

24 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

25 | November 10, 2015

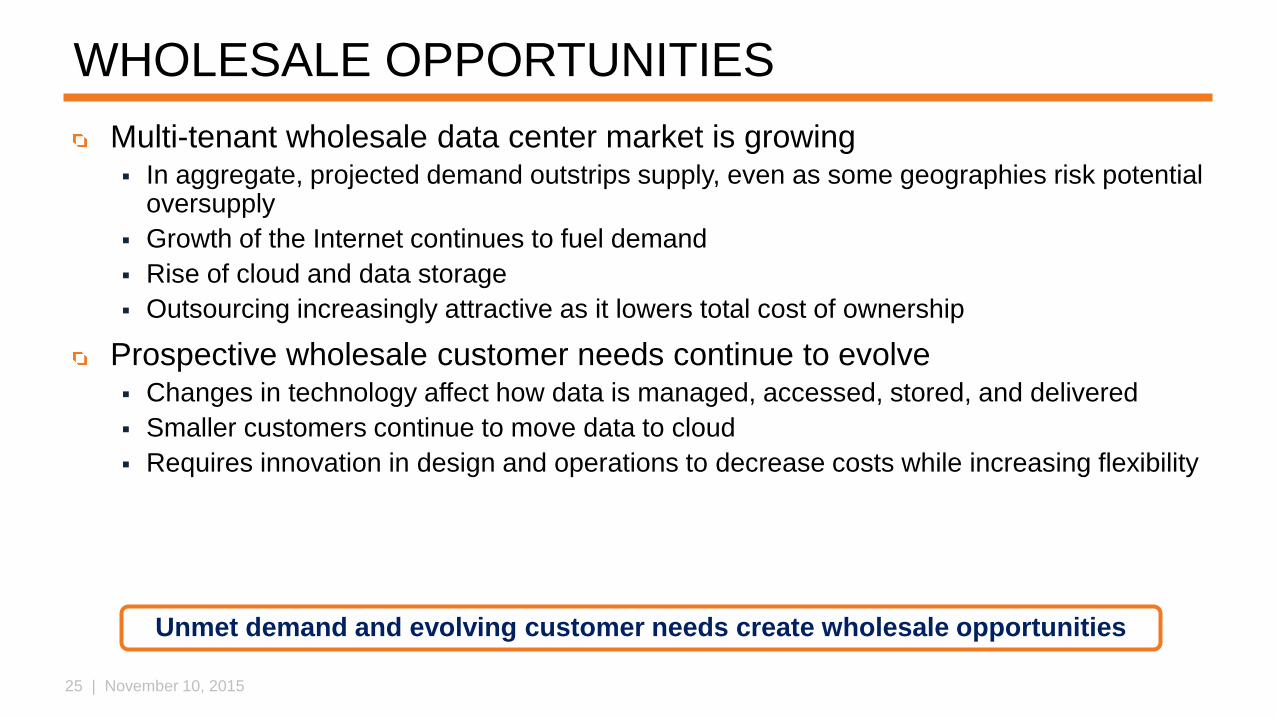

WHOLESALE OPPORTUNITIES

Multi-tenant wholesale data center market is growing In aggregate, projected demand outstrips supply, even as some geographies risk potential

oversupply

Growth of the Internet continues to fuel demand

Rise of cloud and data storage

Outsourcing increasingly attractive as it lowers total cost of ownership

Prospective wholesale customer needs continue to evolve Changes in technology affect how data is managed, accessed, stored, and delivered

Smaller customers continue to move data to cloud

Requires innovation in design and operations to decrease costs while increasing flexibility

Unmet demand and evolving customer needs create wholesale opportunities

26 | November 10, 2015

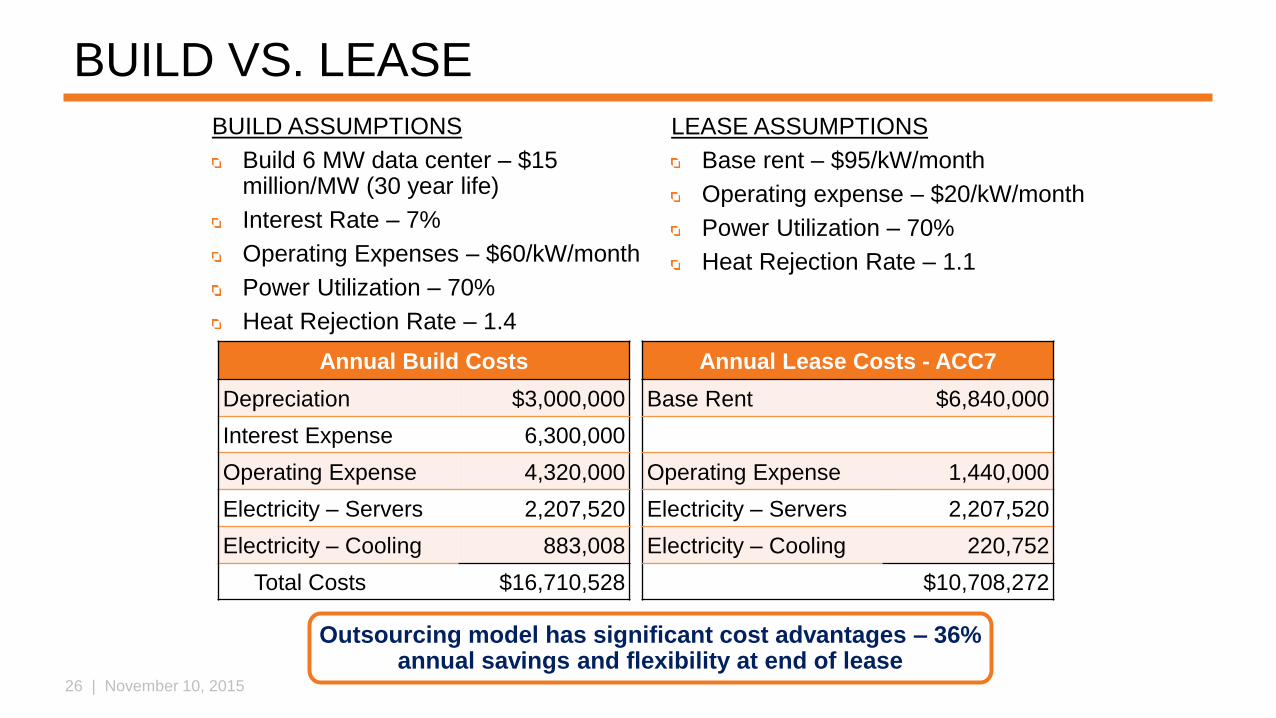

BUILD VS. LEASE

Annual Build Costs Annual Lease Costs - ACC7

Depreciation $3,000,000 Base Rent $6,840,000

Interest Expense 6,300,000

Operating Expense 4,320,000 Operating Expense 1,440,000

Electricity – Servers 2,207,520 Electricity – Servers 2,207,520

Electricity – Cooling 883,008 Electricity – Cooling 220,752

Total Costs $16,710,528 $10,708,272

BUILD ASSUMPTIONS

Build 6 MW data center – $15 million/MW (30 year life)

Interest Rate – 7%

Operating Expenses – $60/kW/month

Power Utilization – 70%

Heat Rejection Rate – 1.4

Outsourcing model has significant cost advantages – 36% annual savings and flexibility at end of lease

LEASE ASSUMPTIONS

Base rent – $95/kW/month

Operating expense – $20/kW/month

Power Utilization – 70%

Heat Rejection Rate – 1.1

27 | November 10, 2015

OPPORTUNITIES

Strong macro trends drive annual data center growth of +13% for North

America

Worldwide IaaS spending forecasted to support +28% CAGR

Public cloud usage and average spend remain strong – across all customer

groups

Near triple digit percentage growth in cloud revenues

Recent performance suggests continued growth and potential

28 | November 10, 2015

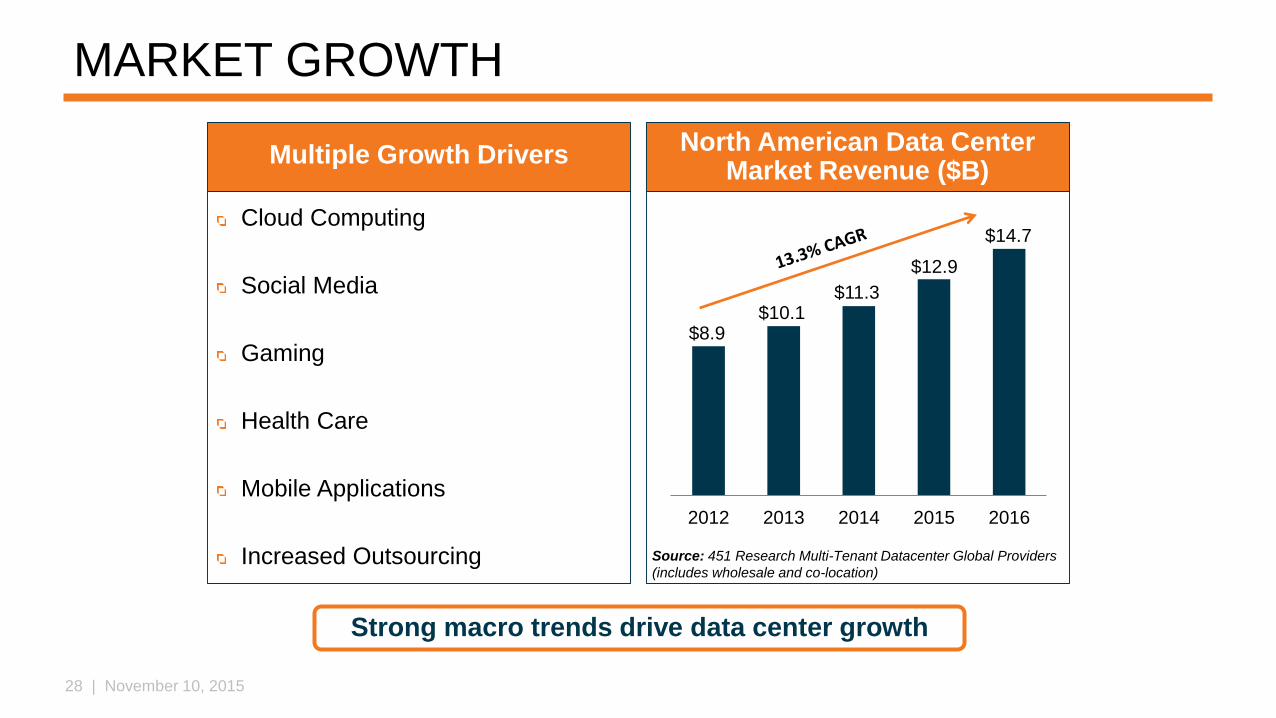

MARKET GROWTH

Cloud Computing

Social Media

Gaming

Health Care

Mobile Applications

Increased Outsourcing

2012 2013 2014 2015 2016

Strong macro trends drive data center growth

Multiple Growth DriversNorth American Data Center

Market Revenue ($B)

Source: 451 Research Multi-Tenant Datacenter Global Providers

(includes wholesale and co-location)

$8.9$10.1

$11.3

$12.9

$14.7

29 | November 10, 2015

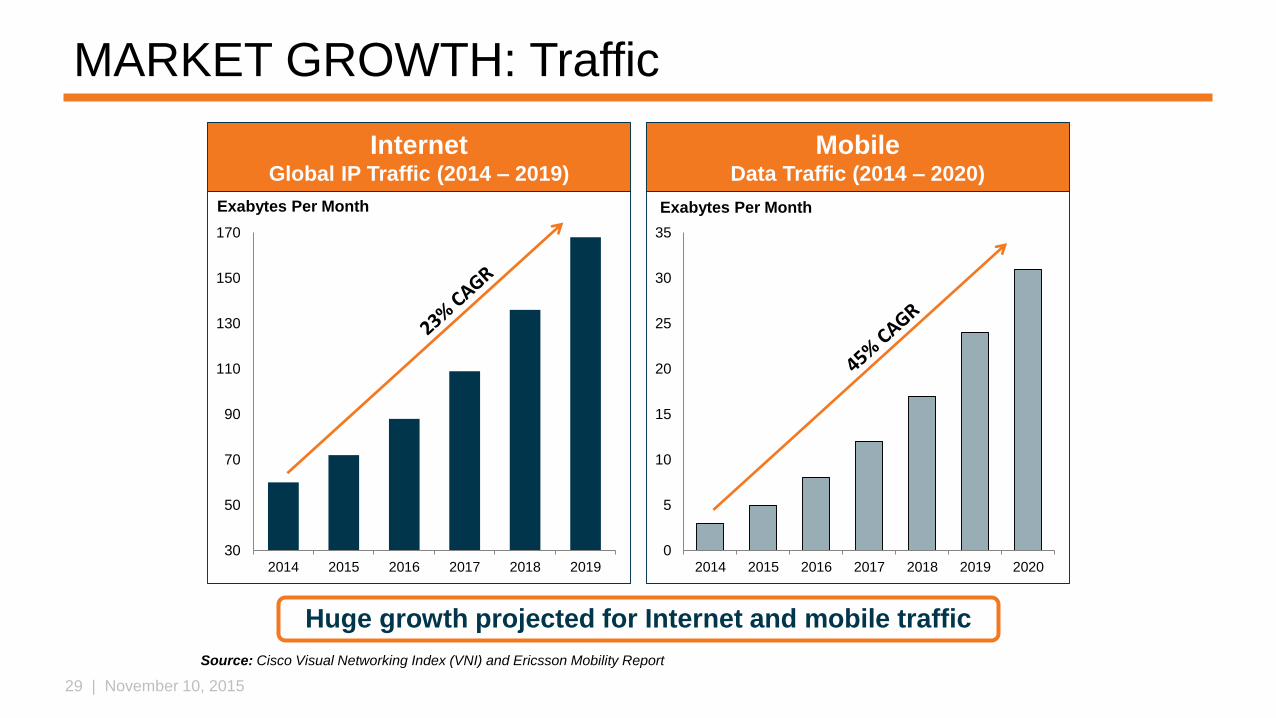

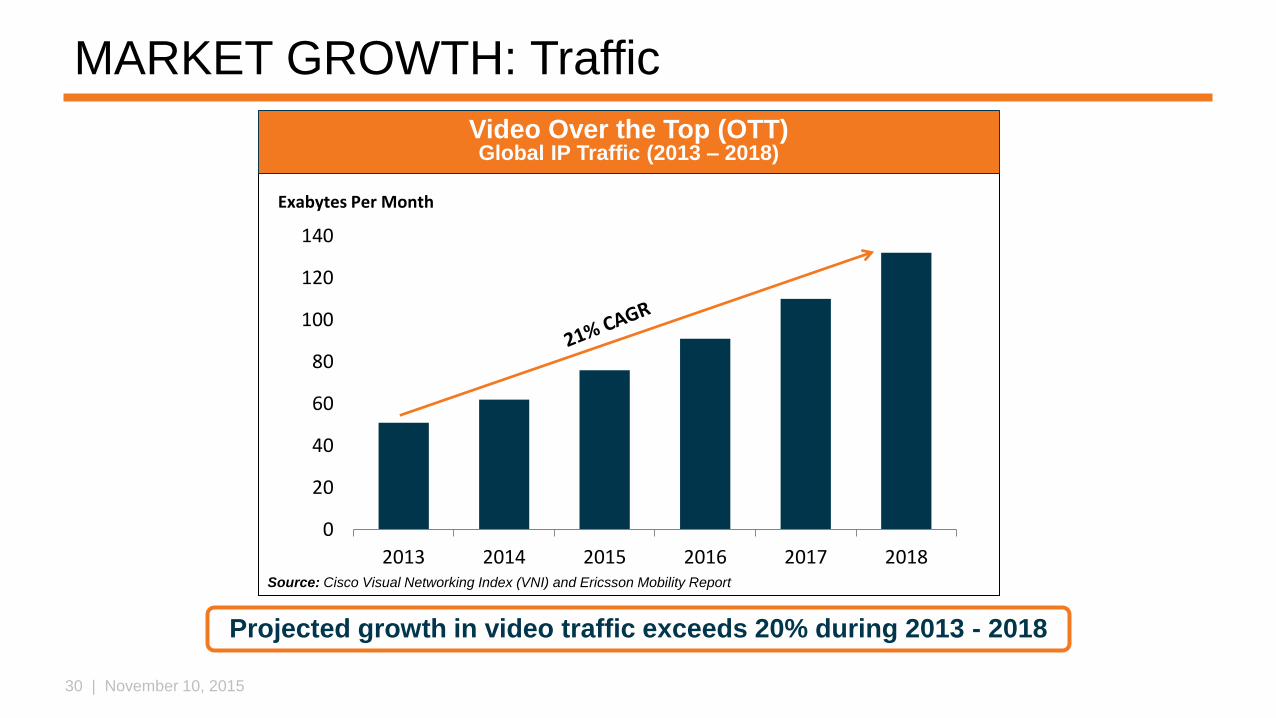

MARKET GROWTH: Traffic

30

50

70

90

110

130

150

170

2014 2015 2016 2017 2018 2019

Exabytes Per Month

Huge growth projected for Internet and mobile traffic

InternetGlobal IP Traffic (2014 – 2019)

MobileData Traffic (2014 – 2020)

Source: Cisco Visual Networking Index (VNI) and Ericsson Mobility Report

0

5

10

15

20

25

30

35

2014 2015 2016 2017 2018 2019 2020

Exabytes Per Month

30 | November 10, 2015

0

20

40

60

80

100

120

140

2013 2014 2015 2016 2017 2018Source: Cisco Visual Networking Index (VNI) and Ericsson Mobility Report

Exabytes Per Month

MARKET GROWTH: Traffic

Projected growth in video traffic exceeds 20% during 2013 - 2018

Video Over the Top (OTT)Global IP Traffic (2013 – 2018)

31 | November 10, 2015

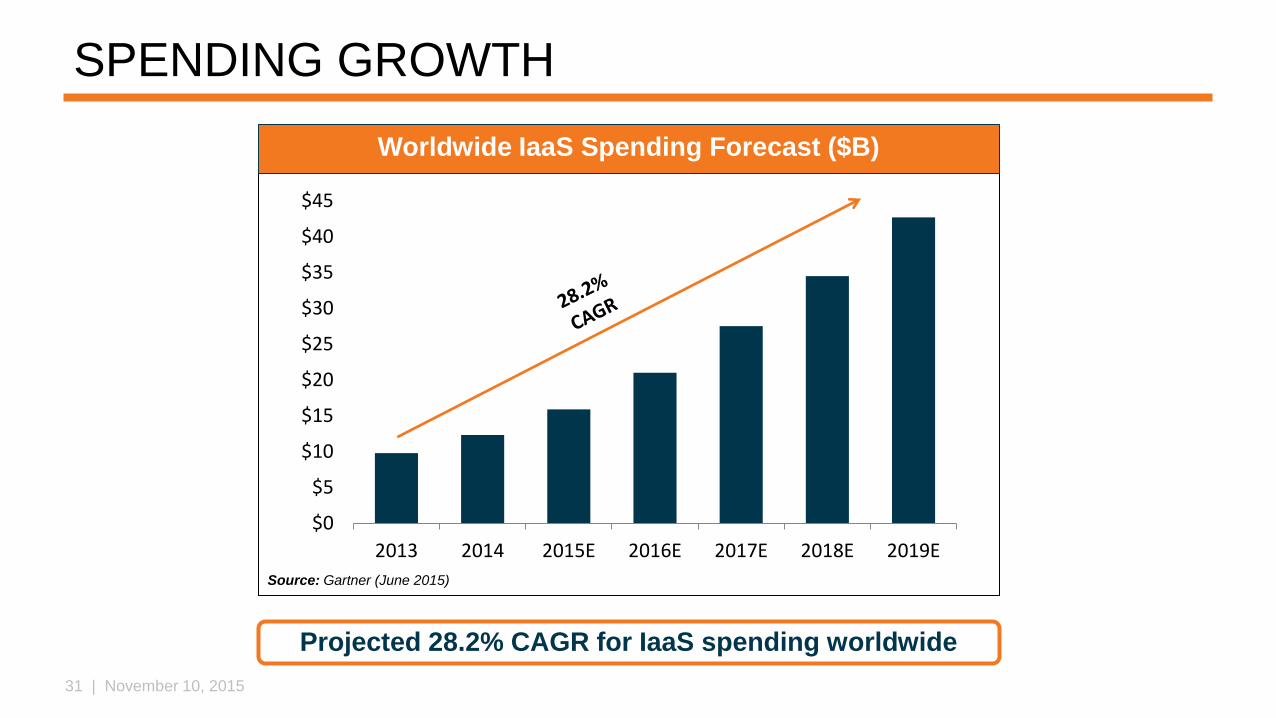

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2013 2014 2015E 2016E 2017E 2018E 2019E

Source: Gartner (June 2015)

SPENDING GROWTH

Projected 28.2% CAGR for IaaS spending worldwide

Worldwide IaaS Spending Forecast ($B)

32 | November 10, 2015

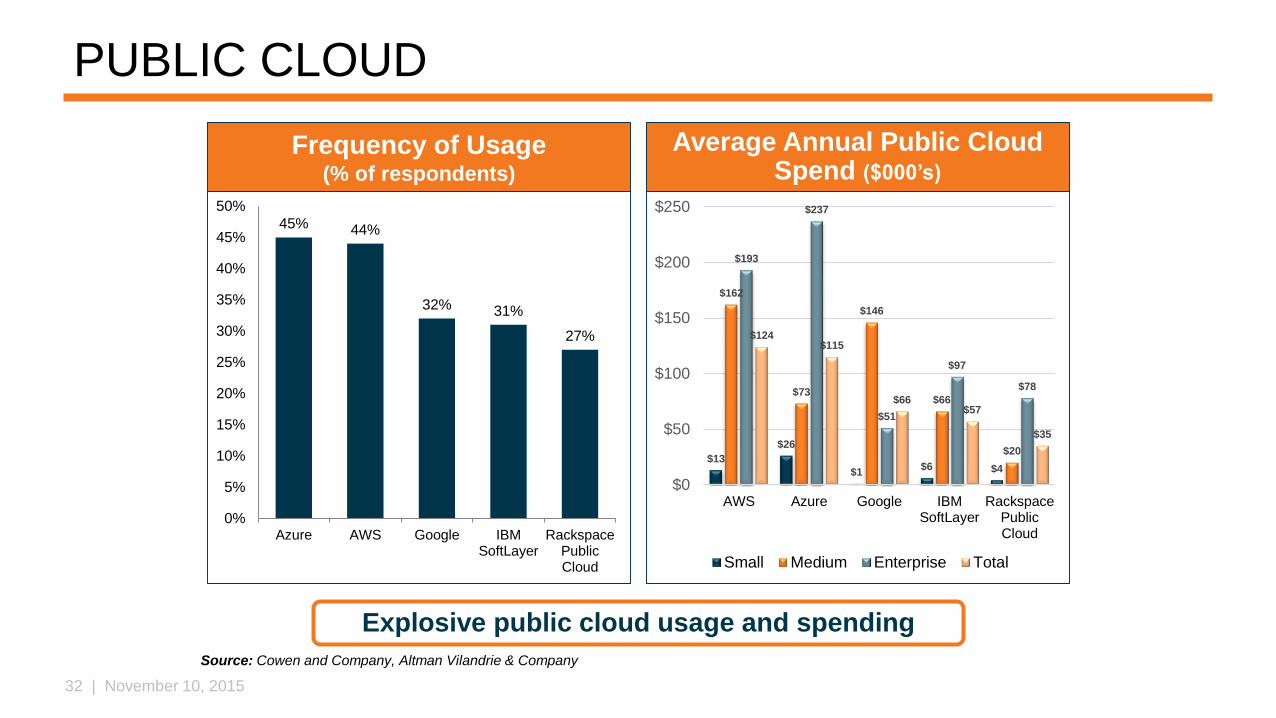

$13

$26

$1$6 $4

$162

$73

$146

$66

$20

$193

$237

$51

$97

$78

$124$115

$66$57

$35

$0

$50

$100

$150

$200

$250

AWS Azure Google IBMSoftLayer

RackspacePublicCloud

Small Medium Enterprise Total

PUBLIC CLOUD

45% 44%

32% 31%

27%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Azure AWS Google IBMSoftLayer

RackspacePublicCloud

Explosive public cloud usage and spending

Frequency of Usage(% of respondents)

Average Annual Public Cloud Spend ($000’s)

Source: Cowen and Company, Altman Vilandrie & Company

33 | November 10, 2015

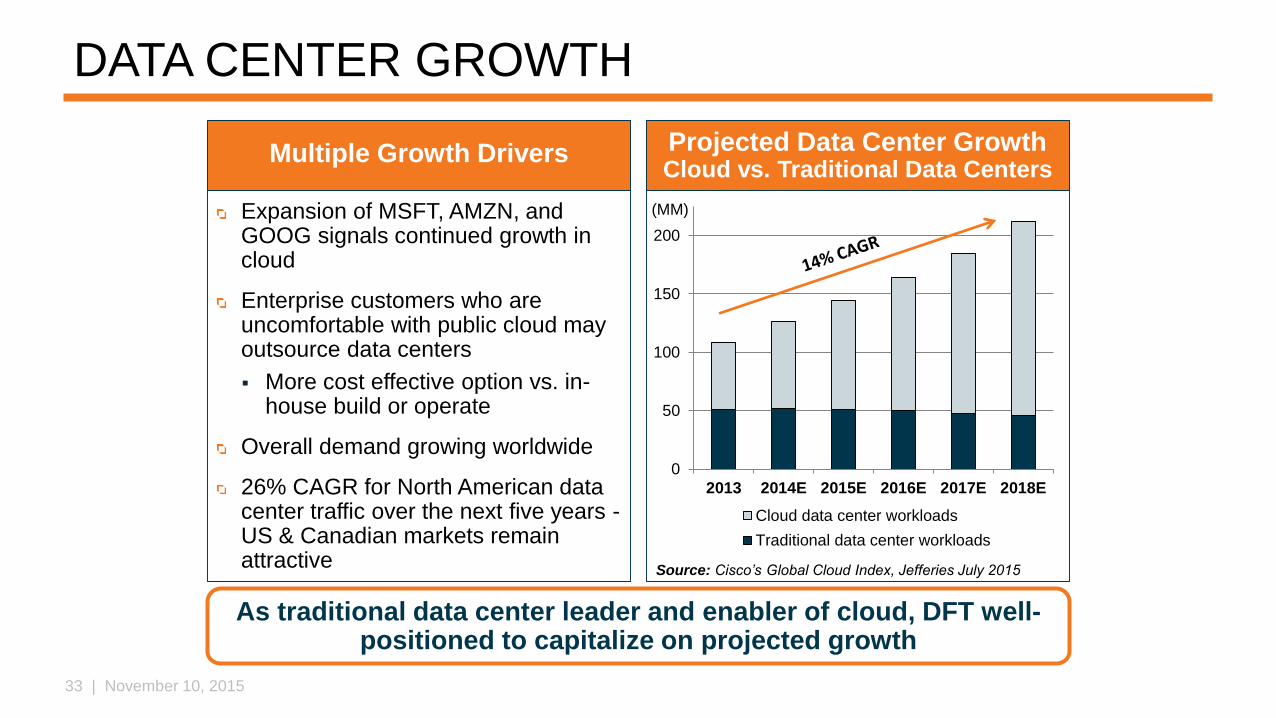

DATA CENTER GROWTH

Expansion of MSFT, AMZN, and GOOG signals continued growth in cloud

Enterprise customers who are uncomfortable with public cloud may outsource data centers

More cost effective option vs. in-house build or operate

Overall demand growing worldwide

26% CAGR for North American data center traffic over the next five years -US & Canadian markets remain attractive

As traditional data center leader and enabler of cloud, DFT well-positioned to capitalize on projected growth

Multiple Growth Drivers Projected Data Center GrowthCloud vs. Traditional Data Centers

0

50

100

150

200

2013 2014E 2015E 2016E 2017E 2018E

Cloud data center workloads

Traditional data center workloads

Source: Cisco’s Global Cloud Index, Jefferies July 2015

(MM)

34 | November 10, 2015

CONCLUSION: Stay Focused on Wholesale

Market growth is exploding in large space and power needs which is more effectively served by wholesale Cloud (MSFT, GOOG, AMZN, CRM)

Social Networking (FB, TWTR, LNKD)

Enterprise (Fortune 1000)

Pricing is increasing and returns remain attractive

DFT has highest EBITDA margin Wholesale investment lower than retail

Wholesale G&A lower than retail

DFT only pure play wholesale option for investors

35 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

36 | November 10, 2015

STRATEGIC PRIORITIES: NEW MARKETS

37 | November 10, 2015

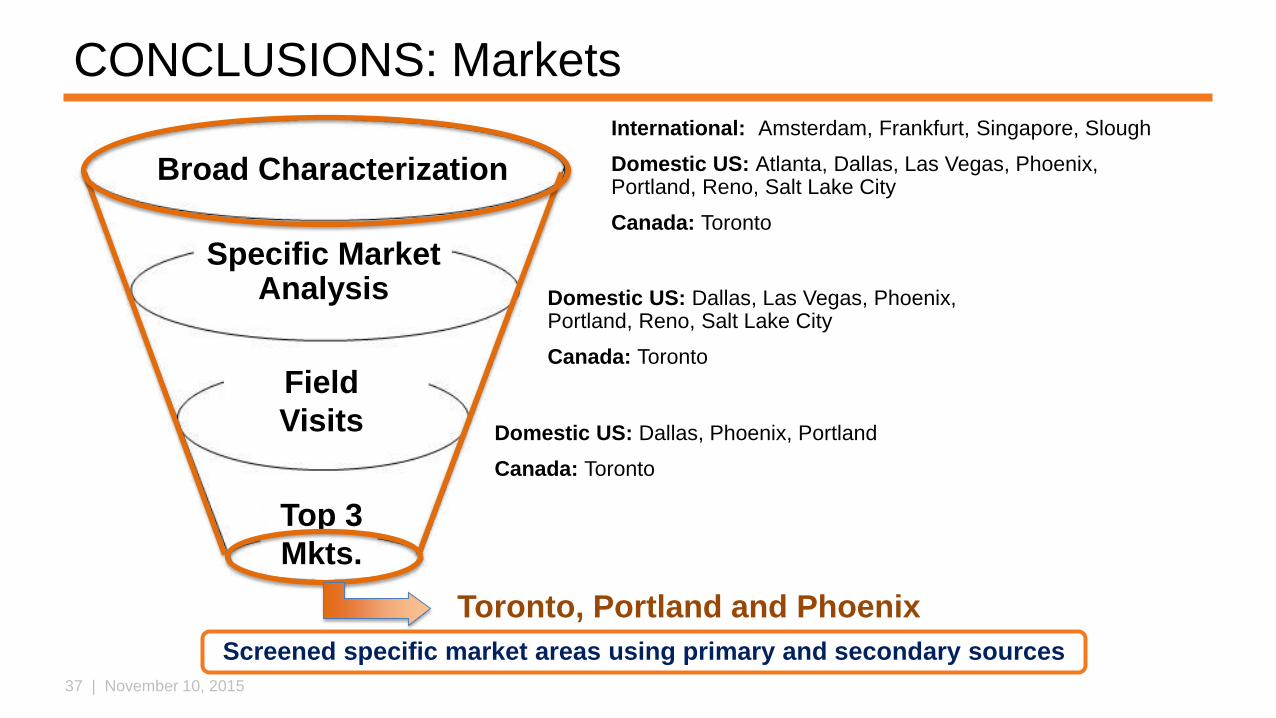

CONCLUSIONS: Markets

Broad Characterization

Specific Market Analysis

Field

Visits

Top 3

Mkts.

International: Amsterdam, Frankfurt, Singapore, Slough

Domestic US: Atlanta, Dallas, Las Vegas, Phoenix, Portland, Reno, Salt Lake City

Canada: Toronto

Domestic US: Dallas, Las Vegas, Phoenix, Portland, Reno, Salt Lake City

Canada: Toronto

Domestic US: Dallas, Phoenix, Portland

Canada: Toronto

Toronto, Portland and Phoenix

Screened specific market areas using primary and secondary sources

38 | November 10, 2015

Santa Clara, CA

Piscataway, NJ

LOCATIONS: CURRENT VS. 2020

257 MW Today

Portland, OR

Phoenix, AZ

Toronto, ON

Elk Grove Village, IL

Santa Clara, CA

Northern Virginia

Piscataway, NJ

432 MW in 2020

Elk Grove Village, IL

Northern Virginia

39 | November 10, 2015

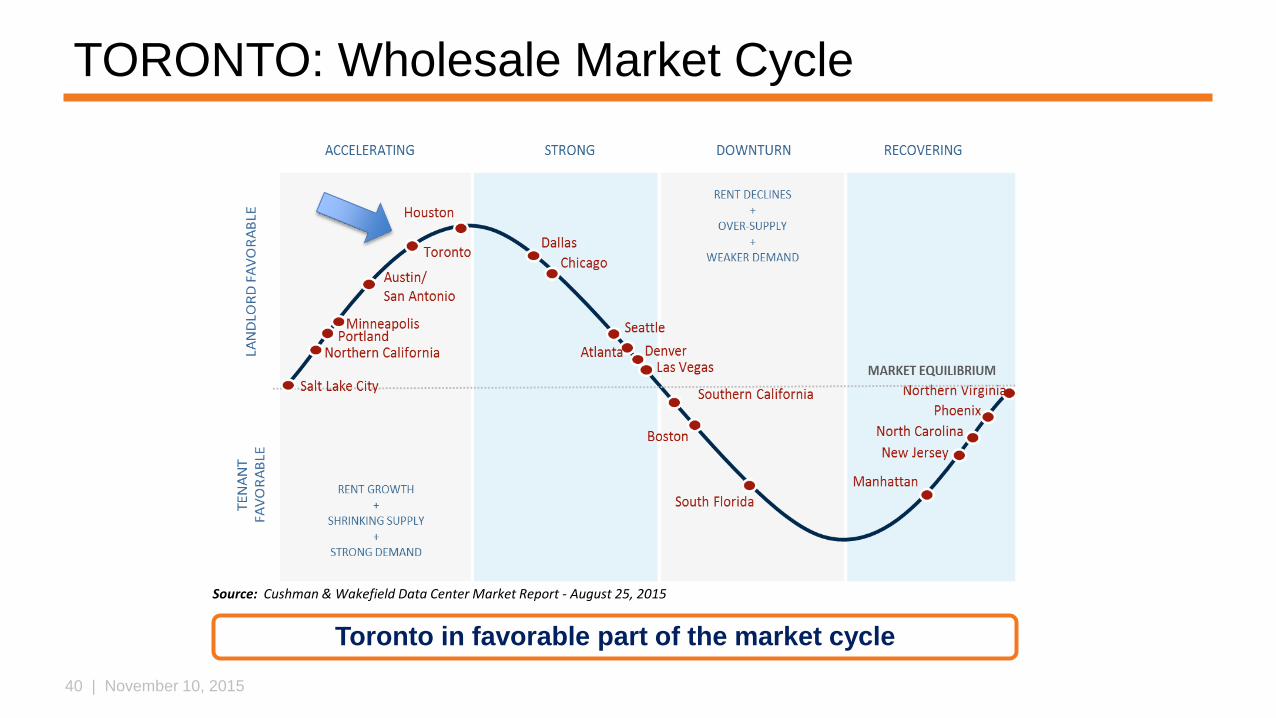

STRATEGIC PRIORITIES: NEW MARKETSTORONTO MARKET OPPORTUNITY

40 | November 10, 2015

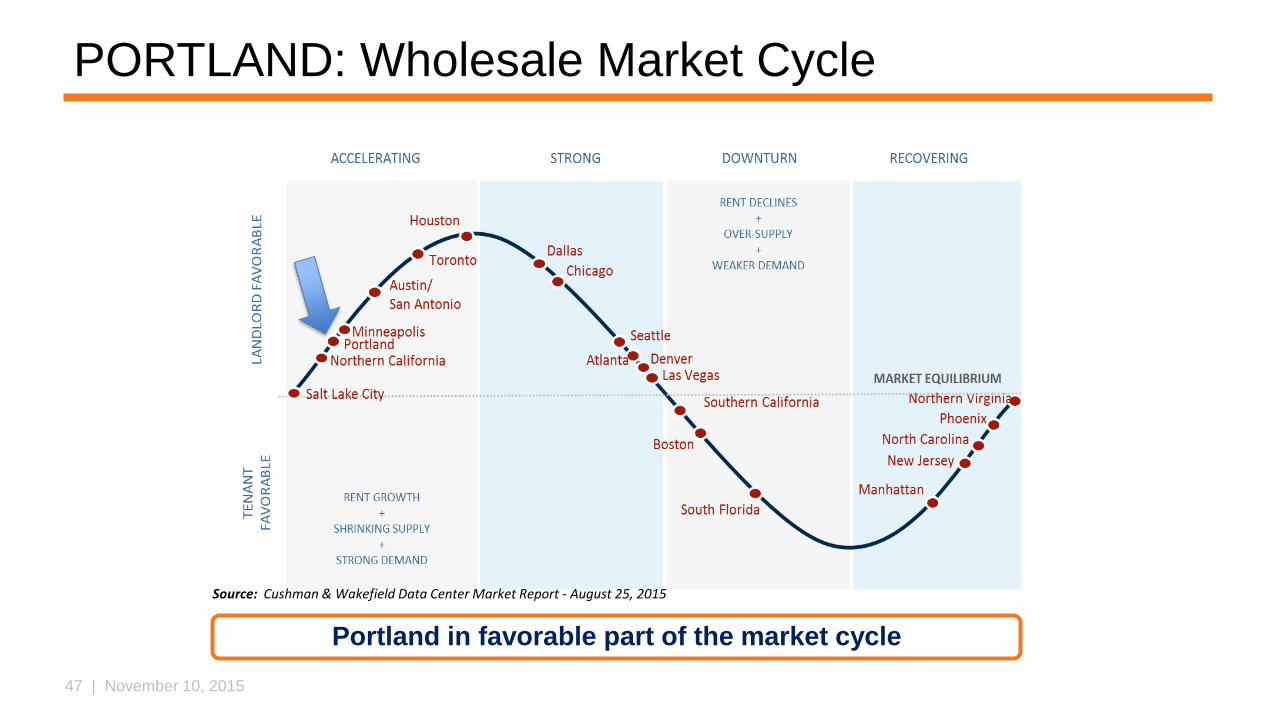

TORONTO: Wholesale Market Cycle

Toronto in favorable part of the market cycle

Source: Cushman & Wakefield Data Center Market Report - August 25, 2015

41 | November 10, 2015

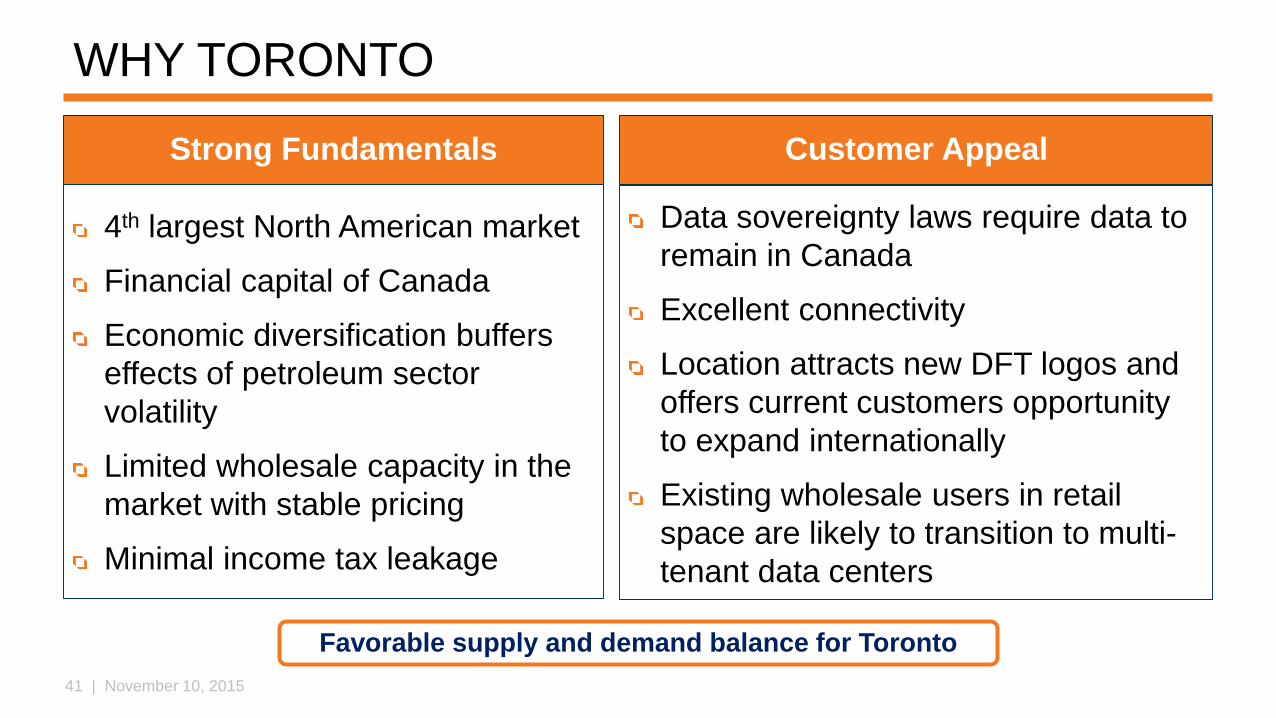

WHY TORONTO

4th largest North American market

Financial capital of Canada

Economic diversification buffers

effects of petroleum sector

volatility

Limited wholesale capacity in the

market with stable pricing

Minimal income tax leakage

Favorable supply and demand balance for Toronto

Customer AppealStrong Fundamentals

Data sovereignty laws require data to

remain in Canada

Excellent connectivity

Location attracts new DFT logos and

offers current customers opportunity

to expand internationally

Existing wholesale users in retail

space are likely to transition to multi-

tenant data centers

42 | November 10, 2015

34%

25%

19%

11%

11%

Q9NETWORKS

ALLIEDPROPERTIESREIT

TELUS

SUNGARDAVAILABILITYSERVICES

EQUINIX

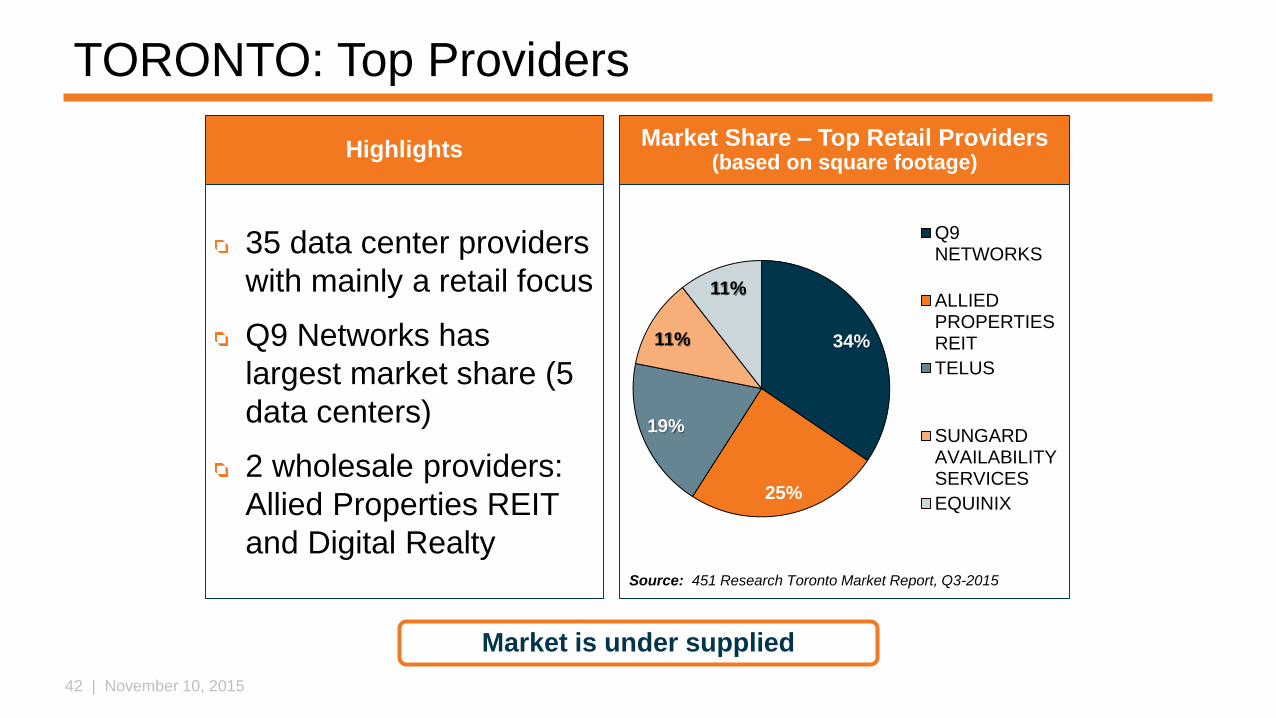

TORONTO: Top Providers

35 data center providers

with mainly a retail focus

Q9 Networks has

largest market share (5

data centers)

2 wholesale providers:

Allied Properties REIT

and Digital Realty

Market is under supplied

Market Share – Top Retail Providers(based on square footage)

Highlights

Source: 451 Research Toronto Market Report, Q3-2015

43 | November 10, 2015

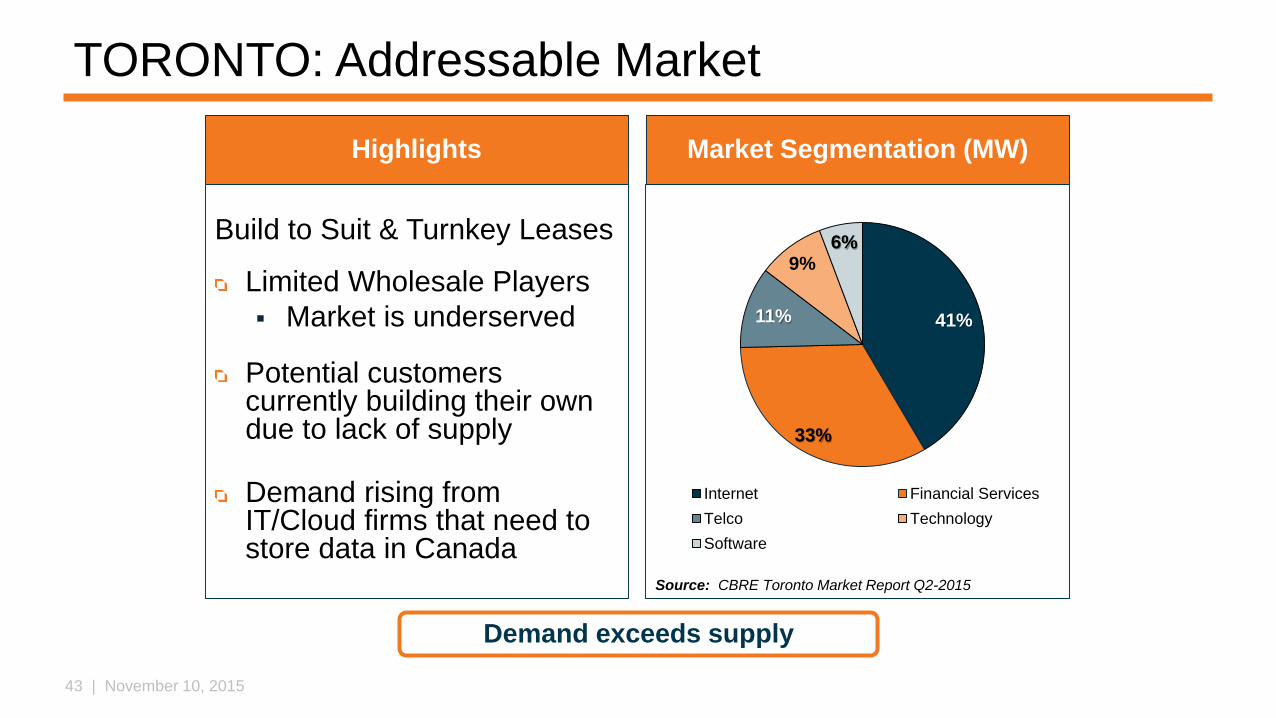

TORONTO: Addressable Market

Build to Suit & Turnkey Leases

Limited Wholesale Players

Market is underserved

Potential customers currently building their own due to lack of supply

Demand rising from IT/Cloud firms that need to store data in Canada

Demand exceeds supply

Market Segmentation (MW)Highlights

Source: CBRE Toronto Market Report Q2-2015

41%

33%

11%

9%6%

Internet Financial Services

Telco Technology

Software

44 | November 10, 2015

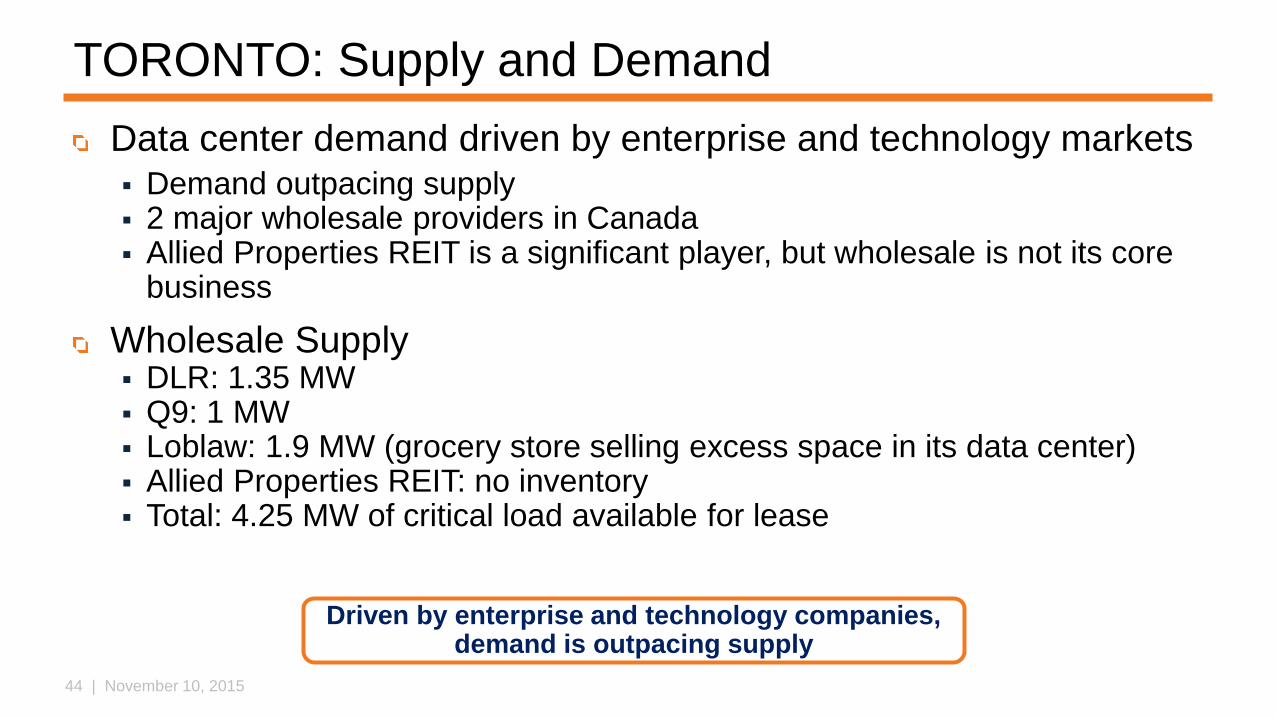

TORONTO: Supply and Demand

Data center demand driven by enterprise and technology markets Demand outpacing supply 2 major wholesale providers in Canada Allied Properties REIT is a significant player, but wholesale is not its core

business

Wholesale Supply DLR: 1.35 MW Q9: 1 MW Loblaw: 1.9 MW (grocery store selling excess space in its data center) Allied Properties REIT: no inventory Total: 4.25 MW of critical load available for lease

Driven by enterprise and technology companies, demand is outpacing supply

45 | November 10, 2015

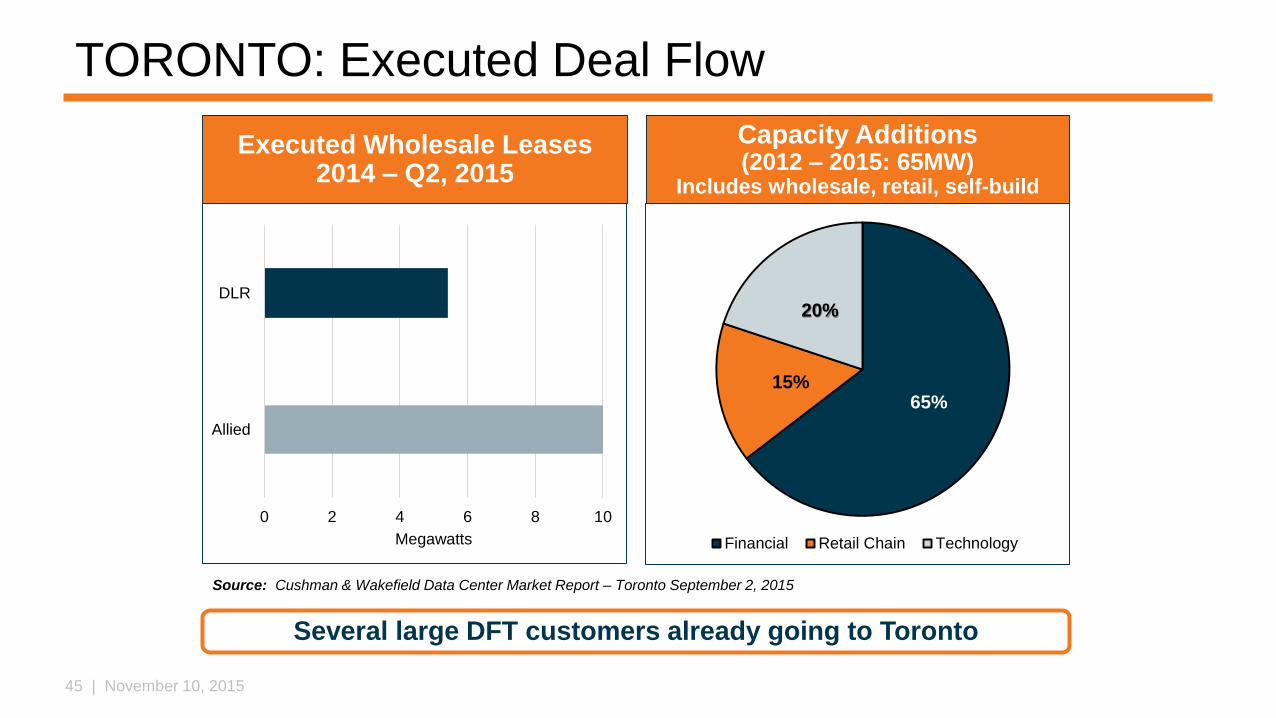

TORONTO: Executed Deal Flow

0 2 4 6 8 10

Allied

DLR

Megawatts

Several large DFT customers already going to Toronto

Capacity Additions(2012 – 2015: 65MW)

Includes wholesale, retail, self-build

Executed Wholesale Leases2014 – Q2, 2015

65%15%

20%

Financial Retail Chain Technology

Source: Cushman & Wakefield Data Center Market Report – Toronto September 2, 2015

46 | November 10, 2015

STRATEGIC PRIORITIES: NEW MARKETSPORTLAND MARKET OPPORTUNITY

47 | November 10, 2015

PORTLAND: Wholesale Market Cycle

Portland in favorable part of the market cycle

Source: Cushman & Wakefield Data Center Market Report - August 25, 2015

48 | November 10, 2015

WHY PORTLAND

3rd largest city in the Pacific

Northwest

Limited wholesale capacity

Tax advantages and enterprise

zones

Favorable market conditions for Portland

Customer AppealStrong Fundamentals

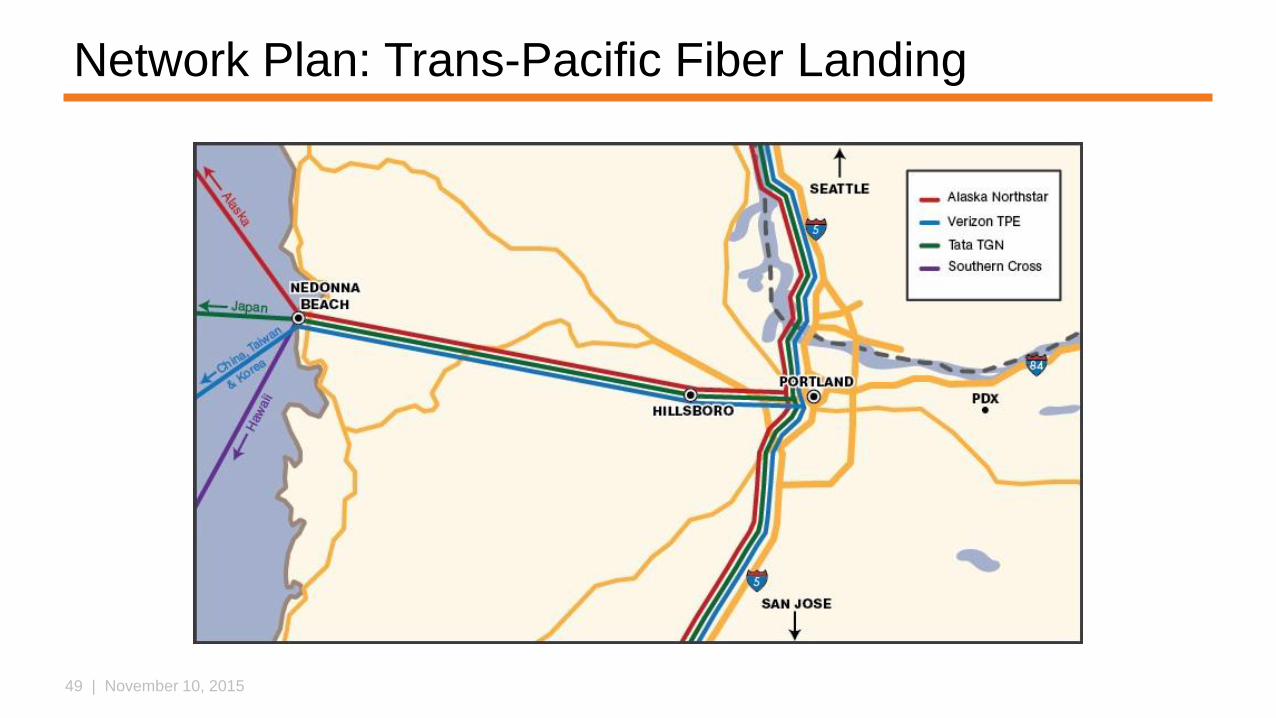

Excellent network connectivity

New Trans-Pacific Fiber Landing

Three major cable systems pulled through

Hillsboro

Google Fiber going into Portland

Cost-effective, abundant and reliable

electricity

Mild climate reduces cooling costs

49 | November 10, 2015

Network Plan: Trans-Pacific Fiber Landing

50 | November 10, 2015

45%

28%

14%

13%

Top Wholesale Providers

Portland NAP Infomart Data Centers

T5 Data Centers Other

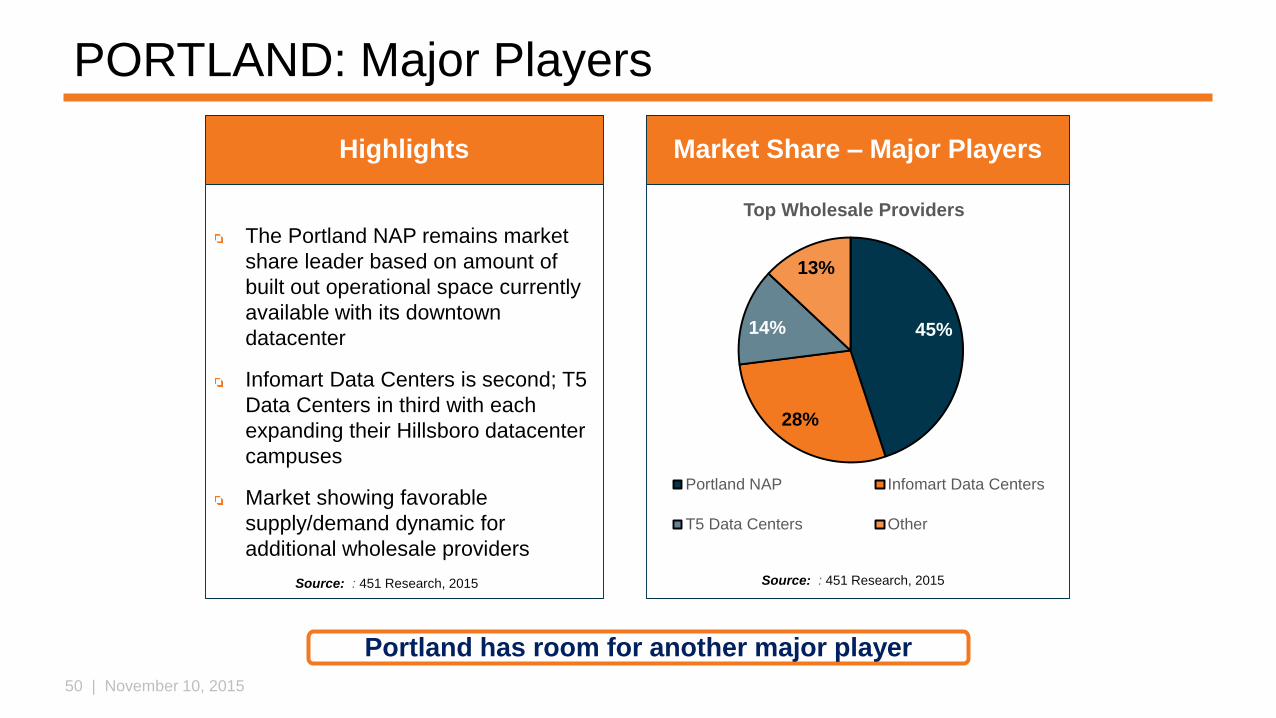

PORTLAND: Major Players

Market Share – Major Players

Source: : 451 Research, 2015

The Portland NAP remains market

share leader based on amount of

built out operational space currently

available with its downtown

datacenter

Infomart Data Centers is second; T5

Data Centers in third with each

expanding their Hillsboro datacenter

campuses

Market showing favorable

supply/demand dynamic for

additional wholesale providers

Highlights

Portland has room for another major player

Source: : 451 Research, 2015

51 | November 10, 2015

38%

42%

14%

6%

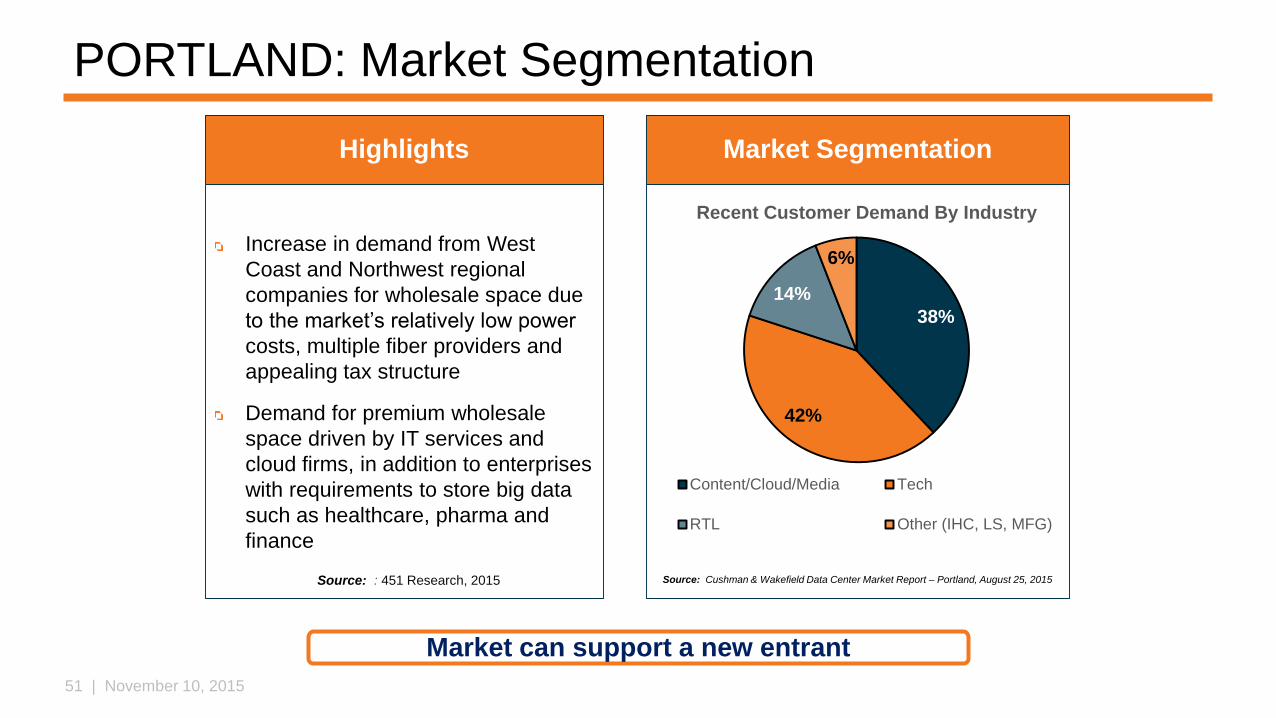

Recent Customer Demand By Industry

Content/Cloud/Media Tech

RTL Other (IHC, LS, MFG)

PORTLAND: Market Segmentation

Market Segmentation

Increase in demand from West

Coast and Northwest regional

companies for wholesale space due

to the market’s relatively low power

costs, multiple fiber providers and

appealing tax structure

Demand for premium wholesale

space driven by IT services and

cloud firms, in addition to enterprises

with requirements to store big data

such as healthcare, pharma and

finance

Highlights

Market can support a new entrant

Source: : 451 Research, 2015 Source: Cushman & Wakefield Data Center Market Report – Portland, August 25, 2015

52 | November 10, 2015

PORTLAND: Supply and Demand

Data center demand driven by enterprise and technology markets Recent transactions

• CMCSA – 8.5 MW

• LNKD - 8 MW

Additional demand is estimated to be roughly 20 MW

Potential addressable market increasing with build outs from cloud providers

Major Wholesale Supply DLR: no inventory T5: no inventory Infomart: no inventory

Demand is outpacing supply

53 | November 10, 2015

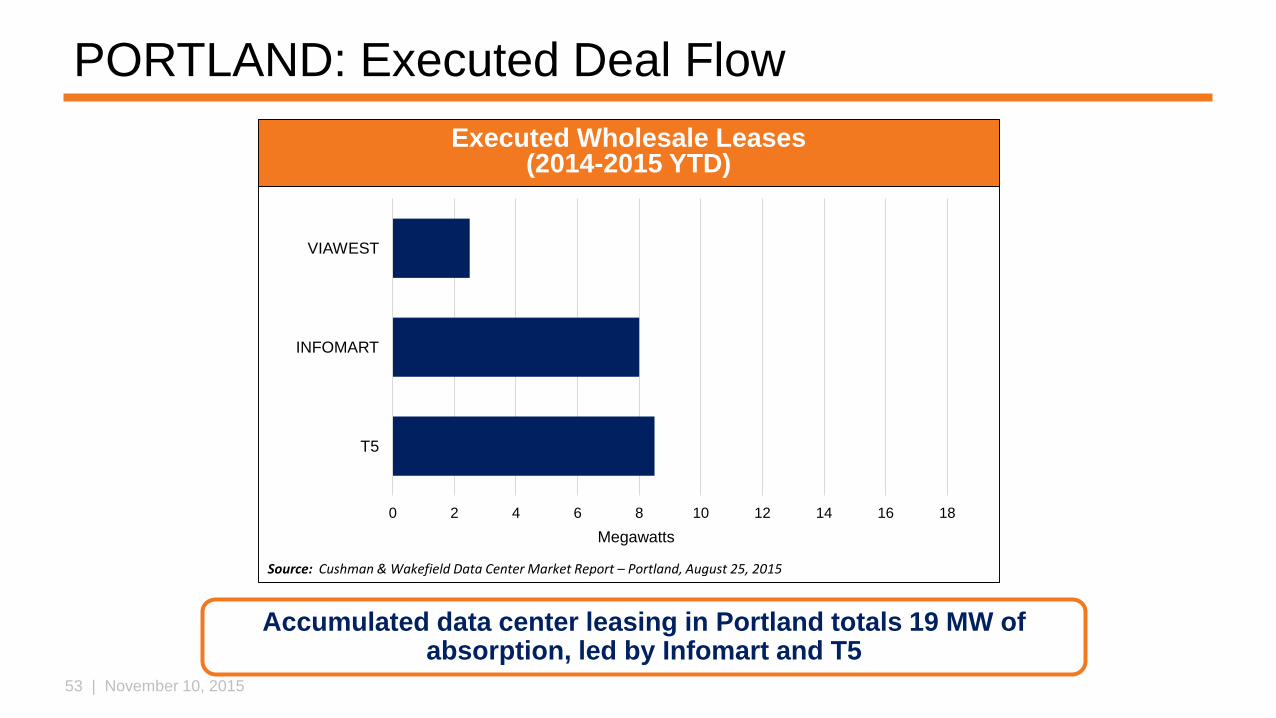

PORTLAND: Executed Deal Flow

0 2 4 6 8 10 12 14 16 18

T5

INFOMART

VIAWEST

Megawatts

Executed Wholesale Leases(2014-2015 YTD)

Source: Cushman & Wakefield Data Center Market Report – Portland, August 25, 2015

Accumulated data center leasing in Portland totals 19 MW of absorption, led by Infomart and T5

54 | November 10, 2015

STRATEGIC PRIORITIES: NEW MARKETSPHOENIX MARKET OPPORTUNITY

55 | November 10, 2015

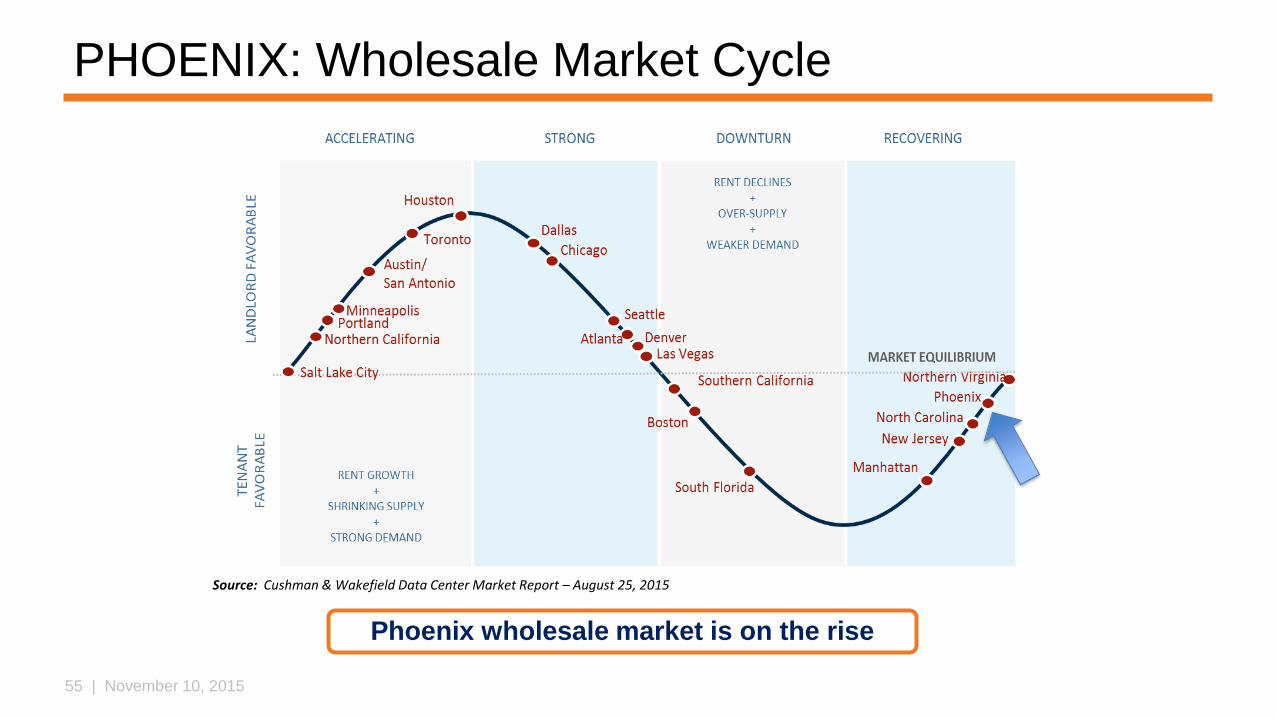

PHOENIX: Wholesale Market Cycle

Phoenix wholesale market is on the rise

Source: Cushman & Wakefield Data Center Market Report – August 25, 2015

56 | November 10, 2015

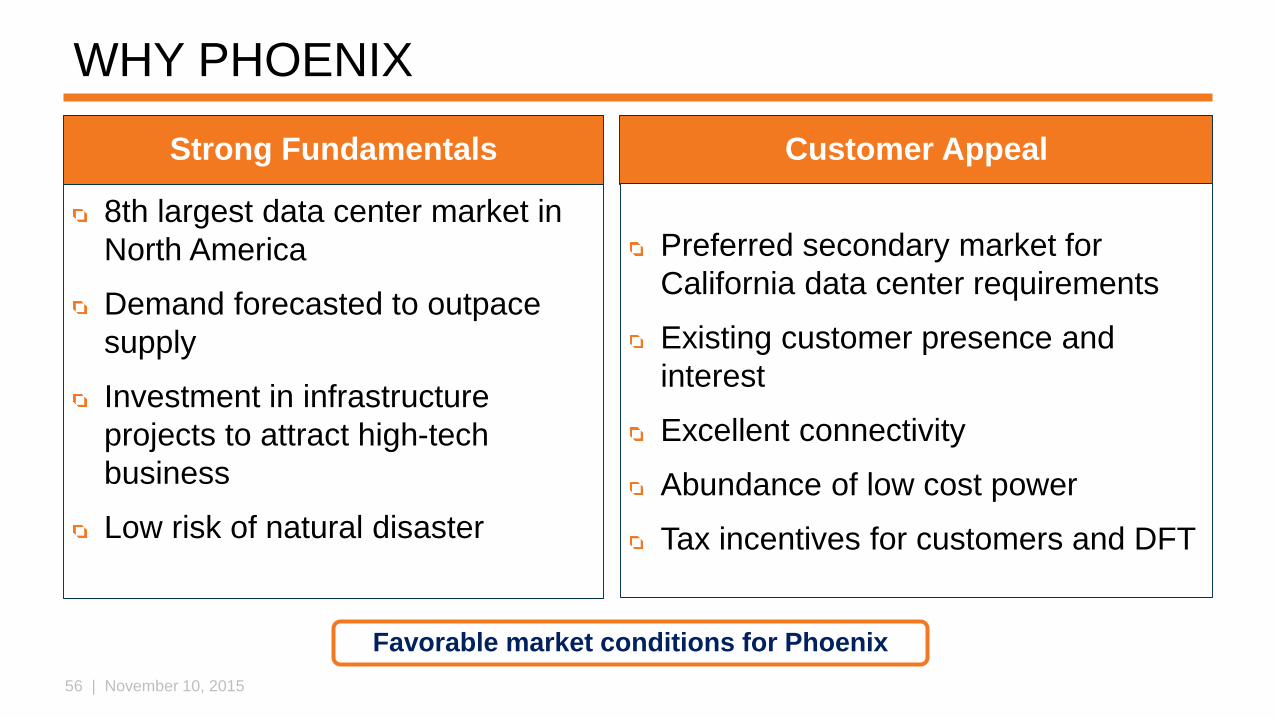

WHY PHOENIX

8th largest data center market in

North America

Demand forecasted to outpace

supply

Investment in infrastructure

projects to attract high-tech

business

Low risk of natural disaster

Favorable market conditions for Phoenix

Customer AppealStrong Fundamentals

Preferred secondary market for

California data center requirements

Existing customer presence and

interest

Excellent connectivity

Abundance of low cost power

Tax incentives for customers and DFT

57 | November 10, 2015

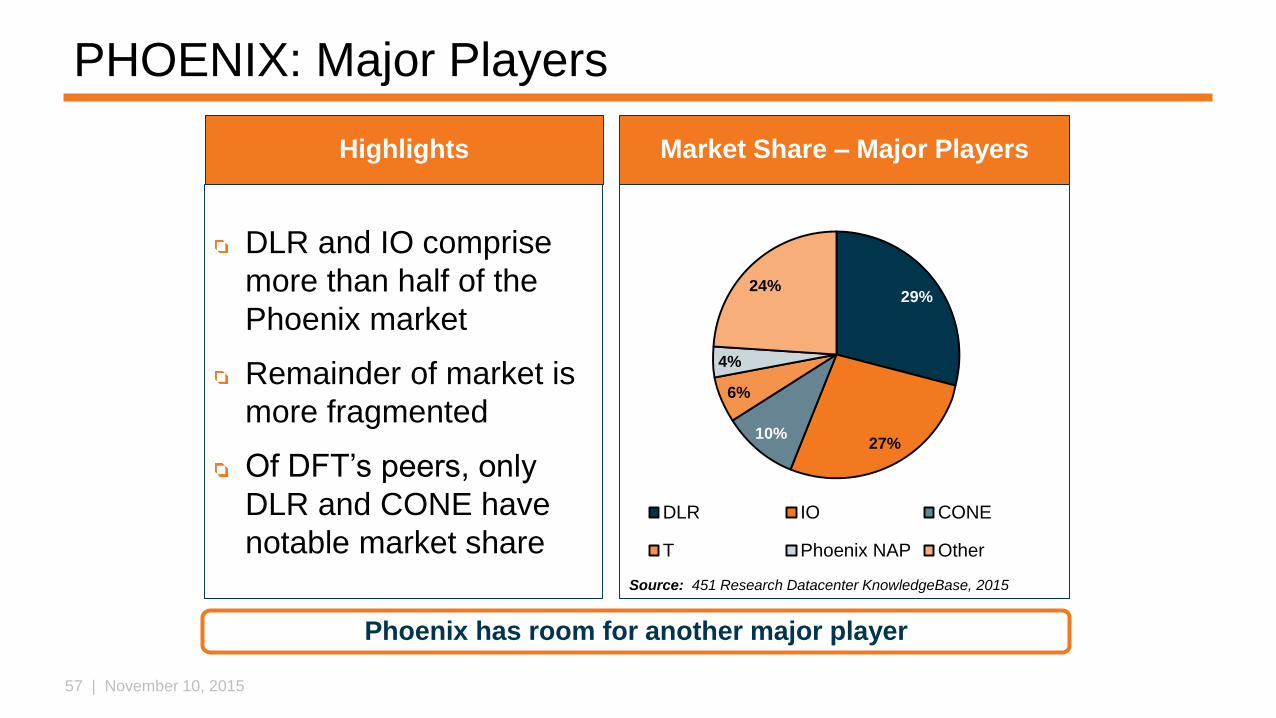

29%

27%10%

6%

4%

24%

DLR IO CONE

T Phoenix NAP Other

PHOENIX: Major Players

DLR and IO comprise

more than half of the

Phoenix market

Remainder of market is

more fragmented

Of DFT’s peers, only

DLR and CONE have

notable market share

Market Share – Major PlayersHighlights

Source: 451 Research Datacenter KnowledgeBase, 2015

Phoenix has room for another major player

58 | November 10, 2015

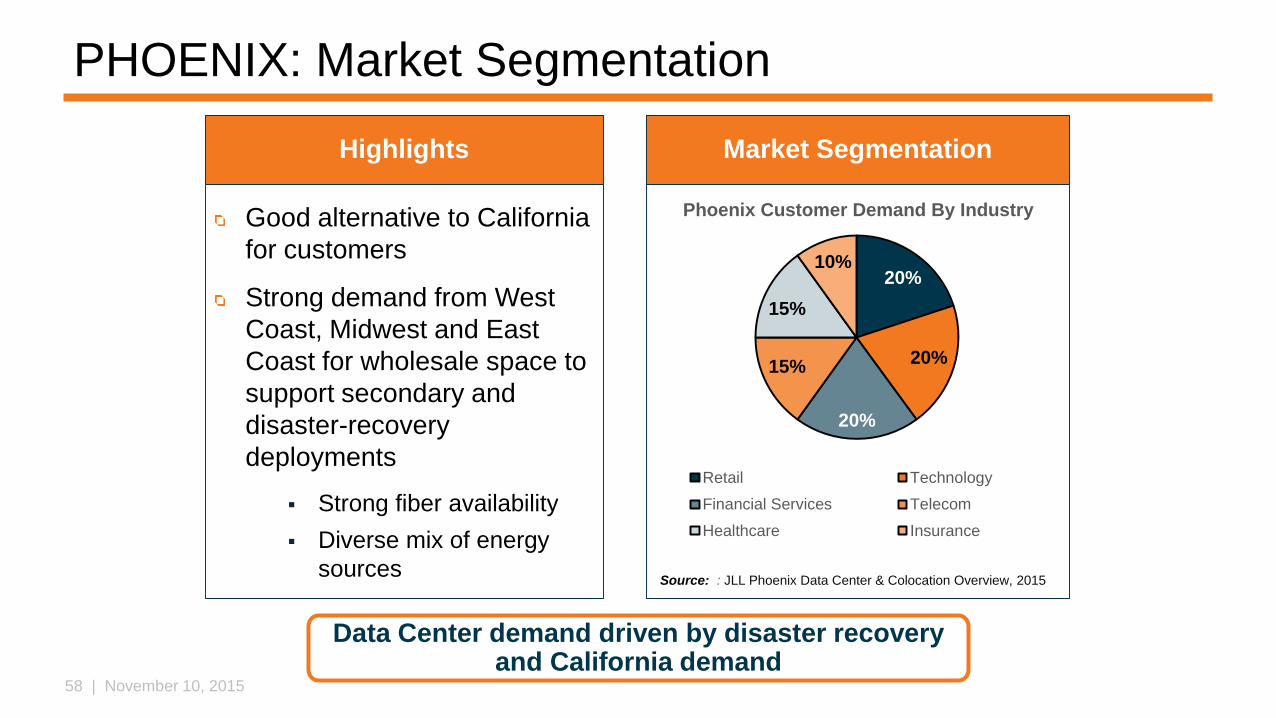

20%

20%

20%

15%

15%

10%

Phoenix Customer Demand By Industry

Retail Technology

Financial Services Telecom

Healthcare Insurance

PHOENIX: Market Segmentation

Market Segmentation

Source: : JLL Phoenix Data Center & Colocation Overview, 2015

Good alternative to California

for customers

Strong demand from West

Coast, Midwest and East

Coast for wholesale space to

support secondary and

disaster-recovery

deployments

Strong fiber availability

Diverse mix of energy

sources

Highlights

Data Center demand driven by disaster recovery and California demand

59 | November 10, 2015

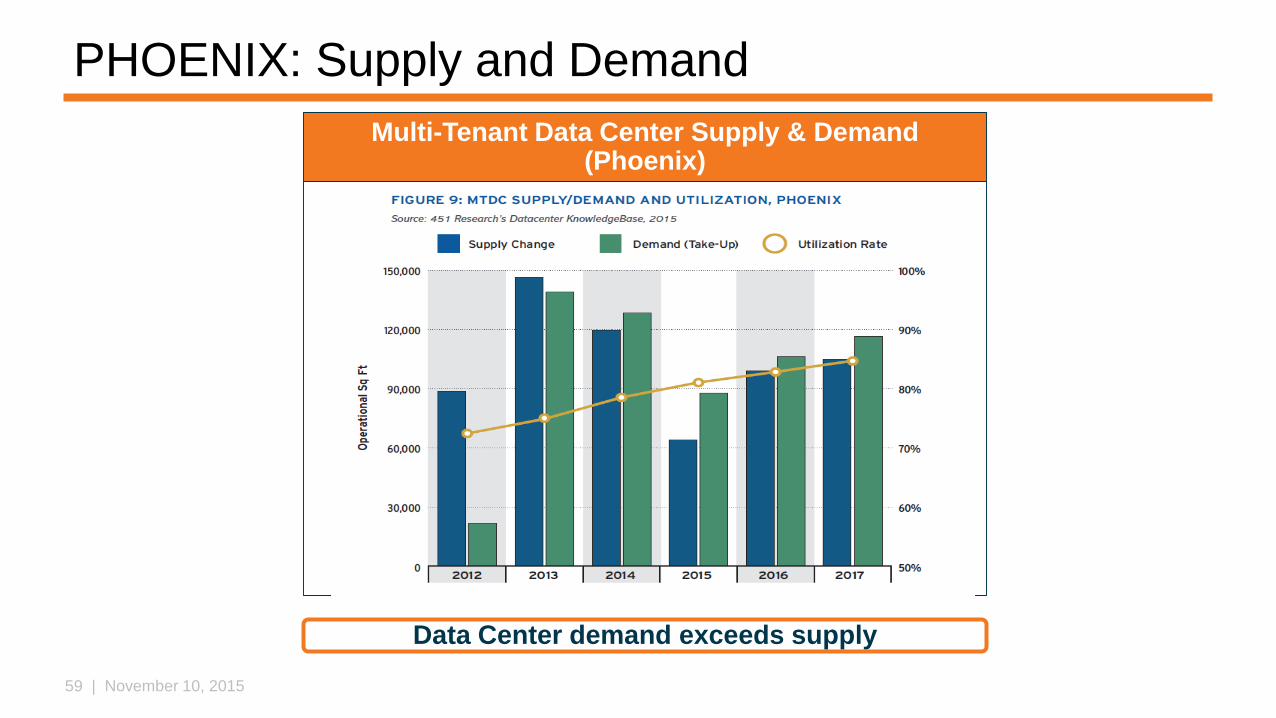

PHOENIX: Supply and Demand

Multi-Tenant Data Center Supply & Demand (Phoenix)

Data Center demand exceeds supply

60 | November 10, 2015

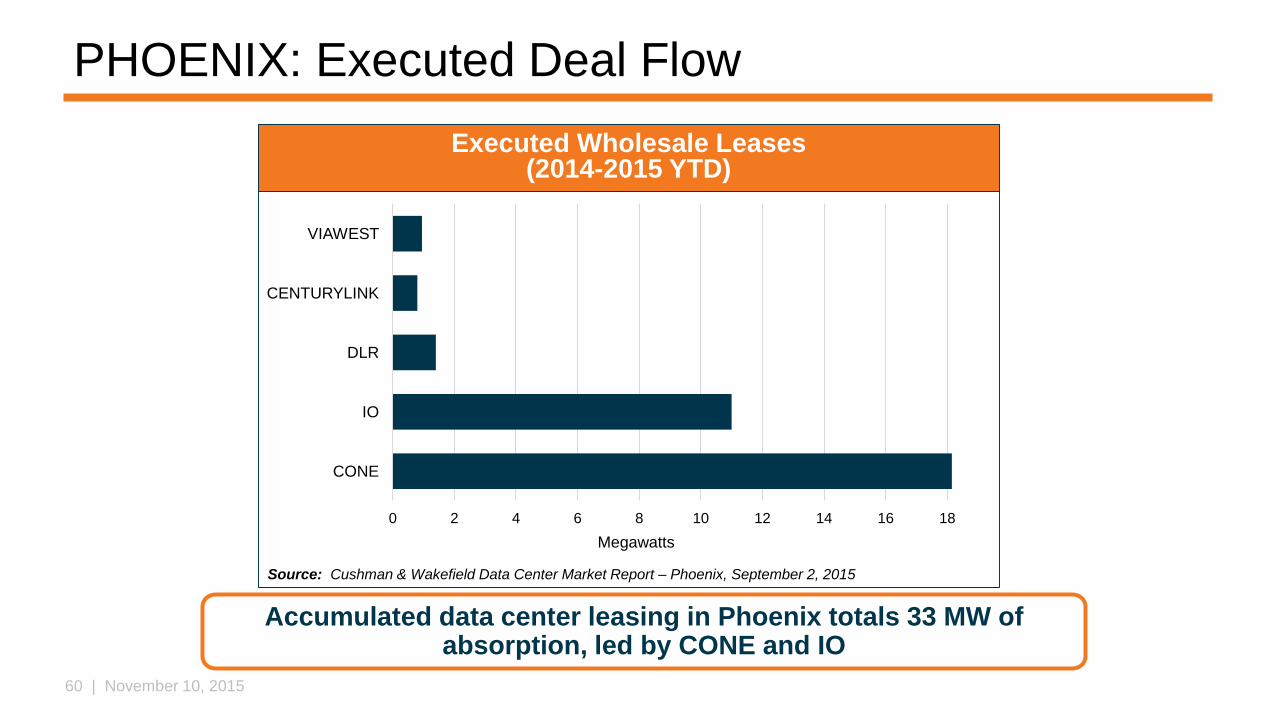

PHOENIX: Executed Deal Flow

0 2 4 6 8 10 12 14 16 18

CONE

IO

DLR

CENTURYLINK

VIAWEST

Megawatts

Executed Wholesale Leases(2014-2015 YTD)

Source: Cushman & Wakefield Data Center Market Report – Phoenix, September 2, 2015

Accumulated data center leasing in Phoenix totals 33 MW of absorption, led by CONE and IO

61 | November 10, 2015

STRATEGIC PRIORITIES: NEW MARKETSENTRY STRATEGY

62 | November 10, 2015

NEW MARKETS: Entry Strategy

Flexible design provides low and high density power, different levels of redundancy

Communicate a lower TCO by being in a multi-tenant data center

Existing customer base will serve as base of demand generation

Brand loyalty, and high quality service reputation

Targeted verticals: Cloud, Enterprise, Financial Services, Healthcare, Insurance, Retail, Technology, Content/Media

Partner with Systems Integrators (SI) and IT firms to drive opportunities

Flexible products adapted to each market will attract new customers

63 | November 10, 2015

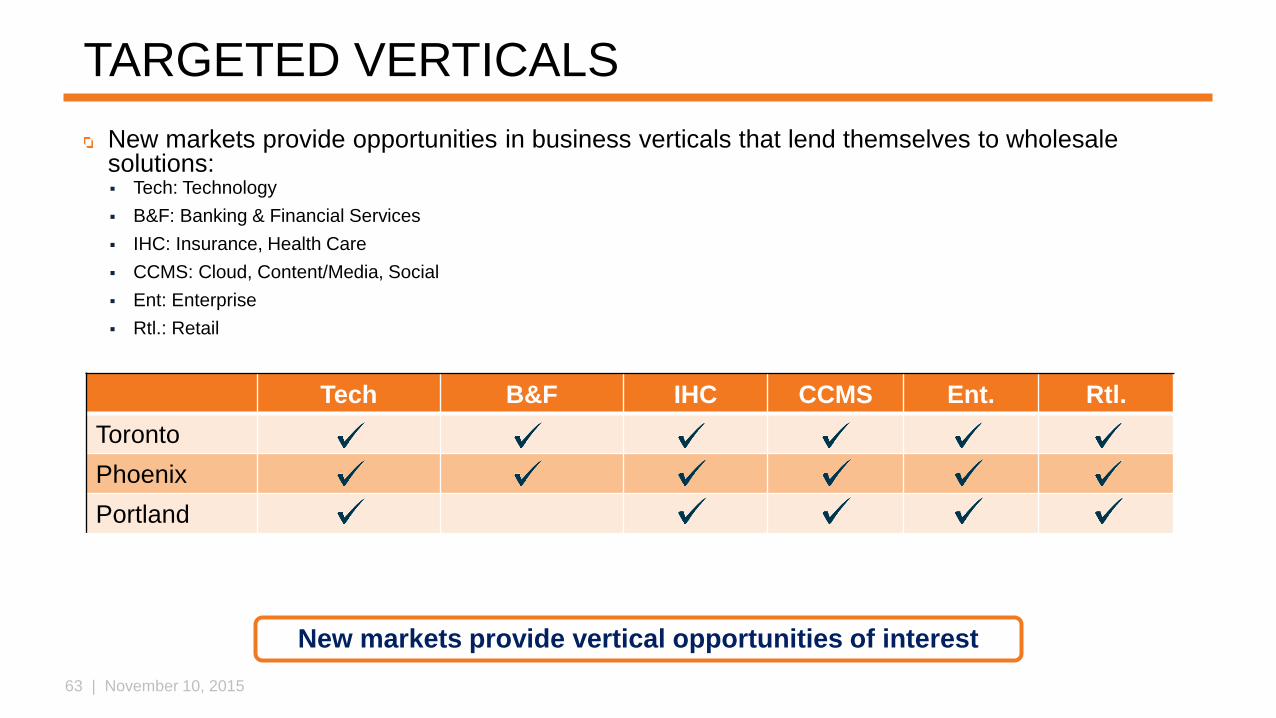

TARGETED VERTICALS

Tech B&F IHC CCMS Ent. Rtl.

Toronto

Phoenix

Portland

New markets provide vertical opportunities of interest

New markets provide opportunities in business verticals that lend themselves to wholesale solutions: Tech: Technology

B&F: Banking & Financial Services

IHC: Insurance, Health Care

CCMS: Cloud, Content/Media, Social

Ent: Enterprise

Rtl.: Retail

64 | November 10, 2015

STRATEGIC PRIORITIES: NEW PRODUCTS

65 | November 10, 2015

FINDINGS: Customers, Products & Services

Prospective customers in our target markets are buying a range of density and reliability

Analysis of existing and proposed data centers show range of N, N+1, N+2, 2N facilities

Helpful to segment customers based on their requirements for resilience and reliability

Allows us to tailor our products and services, and target marketing and sales approach more effectively

Multi-tenant data center is viable in new markets and geographies

Growing demand for multi-tenant data centers

Desire from both prospective and current customers to diversify their locations in addition to adding capacity

Requires different data center designs to suit specific market conditions

Understanding of customers’ needs is critical to properly align products and services

Multiple insights from customer analysis

66 | November 10, 2015

FINDINGS: Customers, Products & Services

New product and service offerings enhance existing products and help attract new customers

Varied customer requirements suggest need for flexibility and adaptability in our product and ways of working

Widening gap between low and high density customers

Hyper-scale segment may have lower resiliency requirements as new layer of redundancy is achieved via multiple data centers in diverse geographies

Desire to add computing power more rapidly favors shorter time to build rooms

Resiliency levels range from N to 2N with greatest concentration at N+1

Capital and operating cost remain important to both DFT and our customers

Smaller initial deployments to lower up front capital costs

Preference for fixed operating costs among some customer groups

Choice of product also impacts our operating and lease models

Manage customer and DFT risk

Assure appropriate pricing

Multiple products are viable in the market

67 | November 10, 2015

NEW PRODUCTS: Data Center

Flexibility Support a range of power densities (100-300 watts per SF)

Support a range of resiliencies (N to 2N)

Agility Create shell and backbone infrastructure that can support rapid deployment of

customized solutions for end users

Avoids stranded UPS/Cooling capacity in low density/low resiliency configurations

Future Proof Allow customers to expand in the same room as technologies evolve and power density

needs increase

Easily reconfigurable when lease expires and tenant occupancy changes

New product adds flexibility and agility for now and later

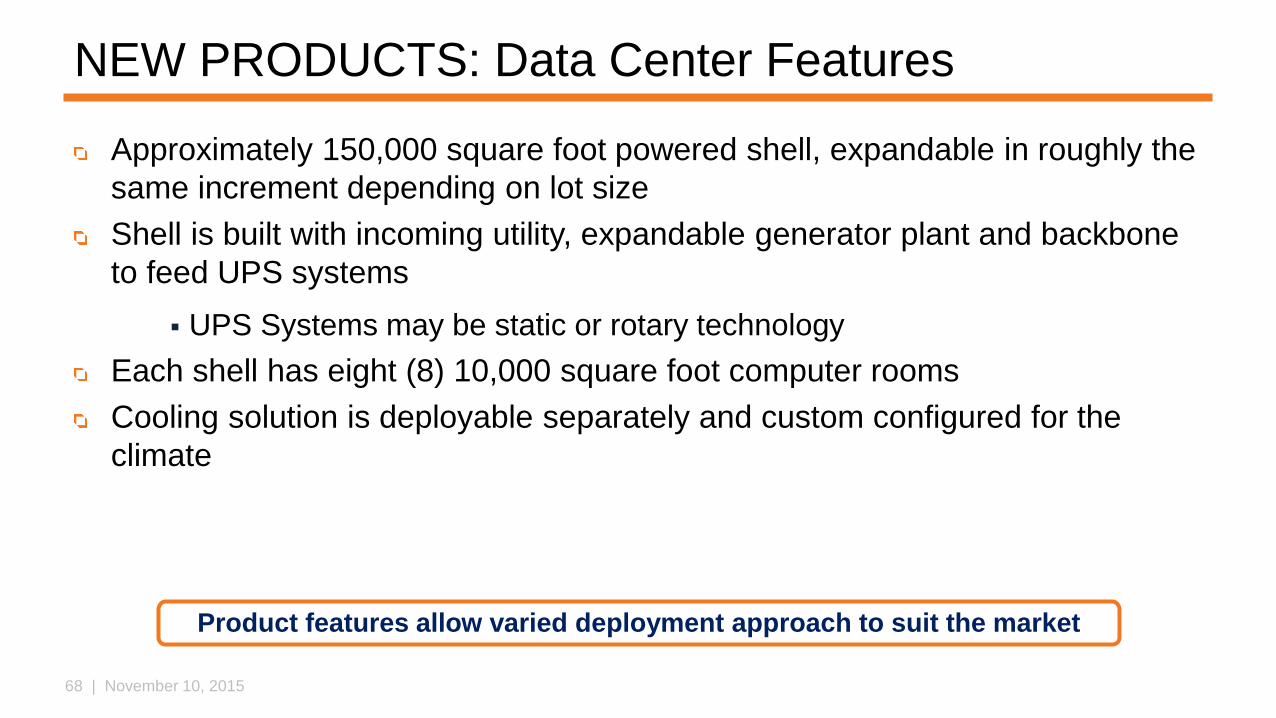

68 | November 10, 2015

NEW PRODUCTS: Data Center Features

Approximately 150,000 square foot powered shell, expandable in roughly the

same increment depending on lot size

Shell is built with incoming utility, expandable generator plant and backbone

to feed UPS systems

UPS Systems may be static or rotary technology

Each shell has eight (8) 10,000 square foot computer rooms

Cooling solution is deployable separately and custom configured for the

climate

Product features allow varied deployment approach to suit the market

69 | November 10, 2015

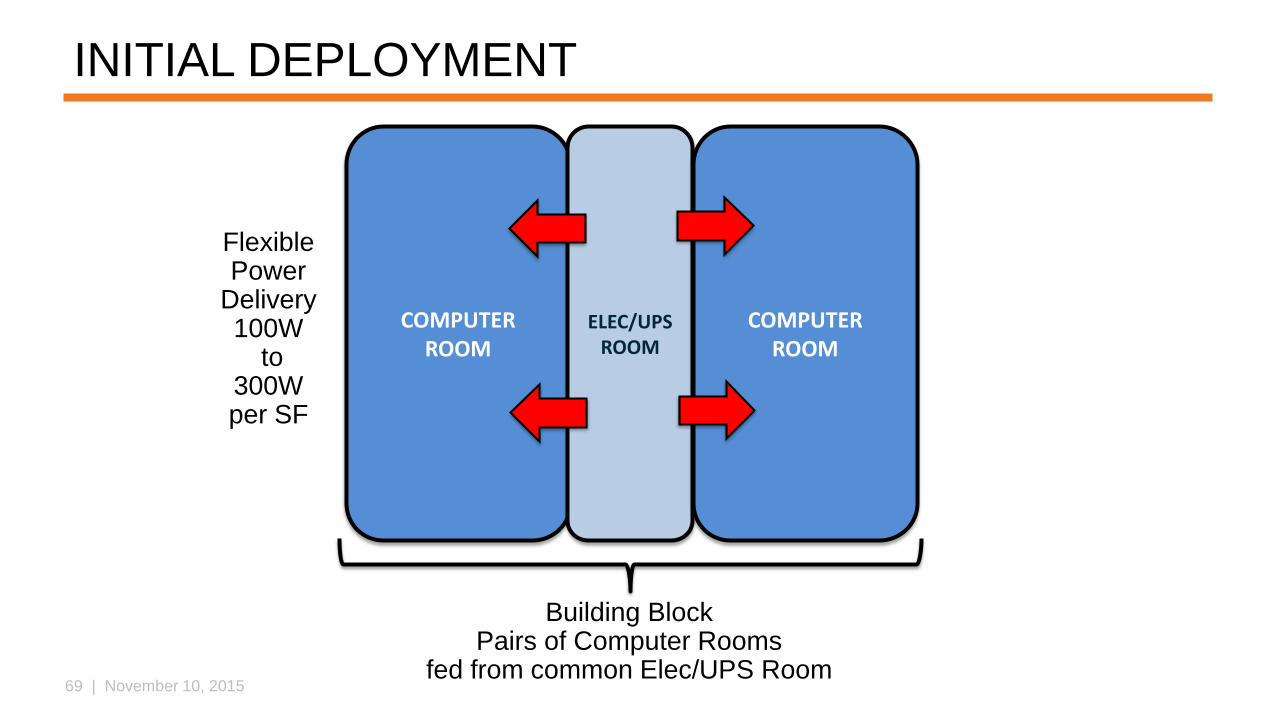

Building BlockPairs of Computer Rooms

fed from common Elec/UPS Room

COMPUTERROOM

ELEC/UPS ROOM

COMPUTERROOM

Flexible Power

Delivery100W

to 300W per SF

INITIAL DEPLOYMENT

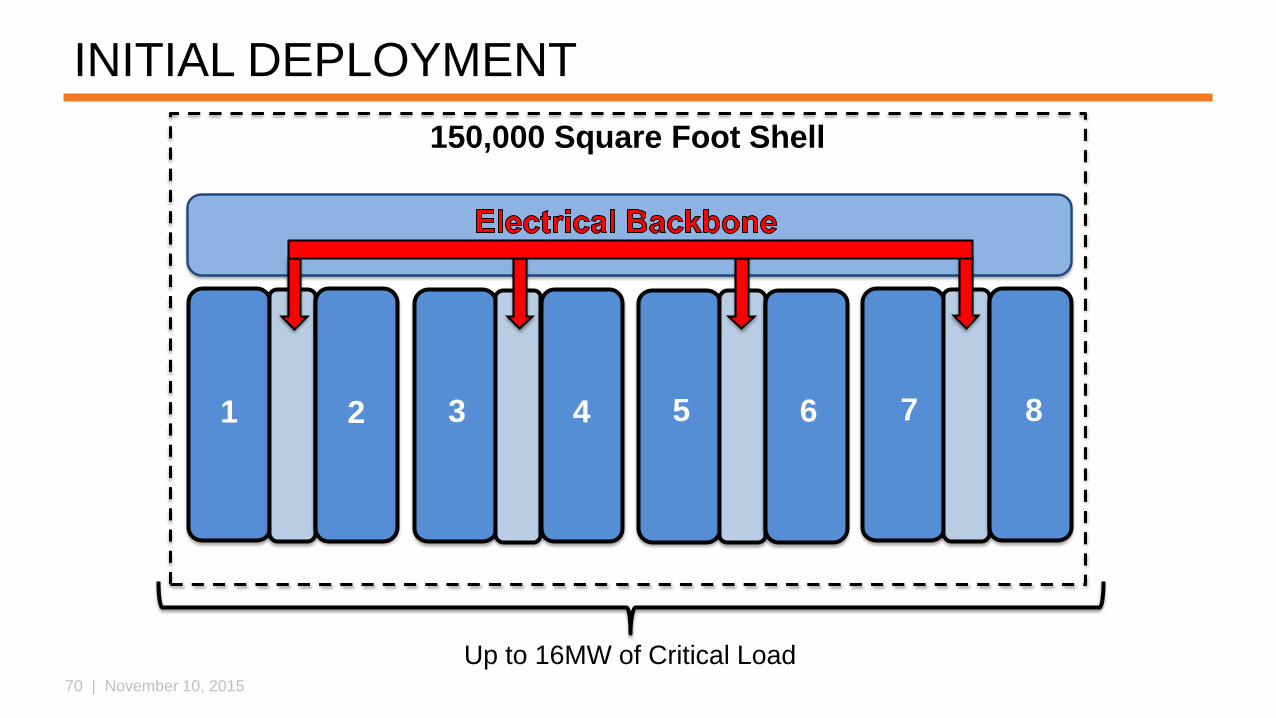

70 | November 10, 2015

1 2 3 4 5 6 7 8

150,000 Square Foot Shell

Up to 16MW of Critical Load

INITIAL DEPLOYMENT

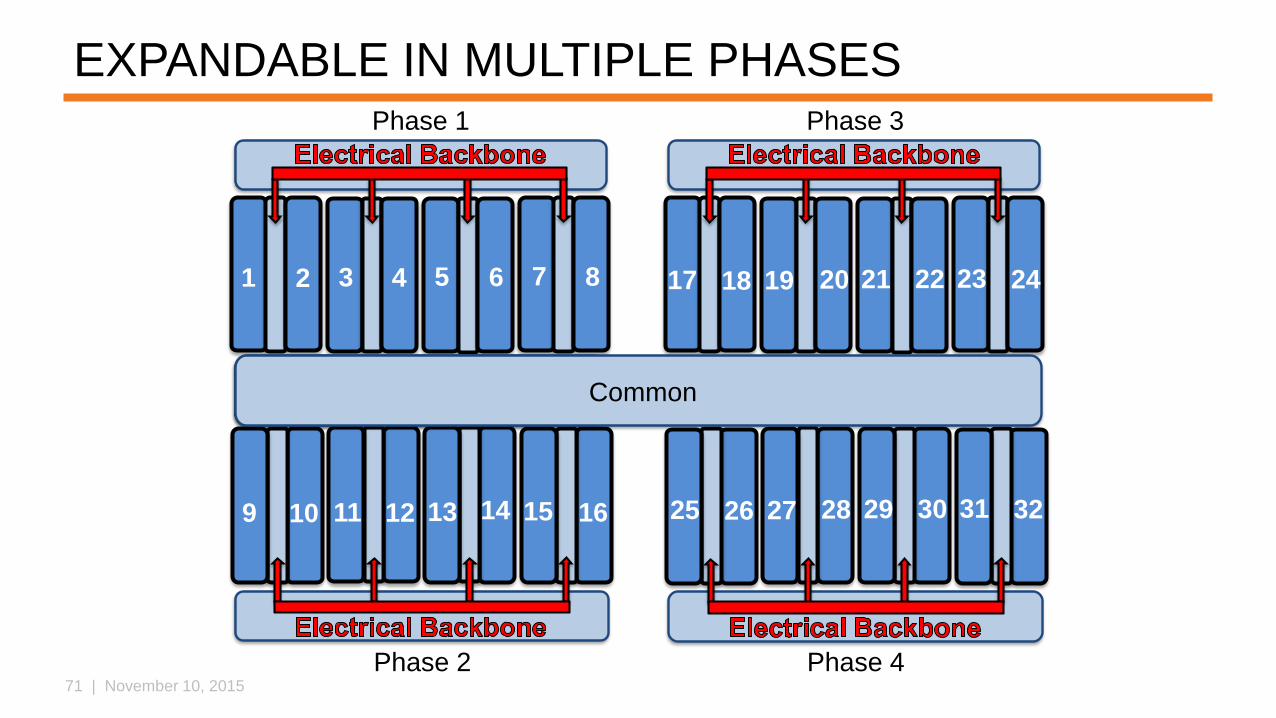

71 | November 10, 2015

1 2 3 4 5 6 7 8

Phase 1

Common

Phase 2

9 10 11 12 13 14 15 16

Phase 3

17 18 19 20 21 22 23 24

Phase 4

25 26 27 28 29 30 31 32

Common

EXPANDABLE IN MULTIPLE PHASES

72 | November 10, 2015

RAPID DEPLOYMENT

Determine a customer’s specific density and resiliency needs

Optimize time to deliver customized solution

Target 16-20 week build cycle

Compared to 6 to 9 months to build out a phase in our current model

Requires key elements to be in place

Pre-engineered design solutions

Inventory of component to reduce lead time

Standing agreements with contractors and suppliers

Rapid deployment speeds product delivery to customers

73 | November 10, 2015

NEW PRODUCTS: Flexible Lease Structure

Full Service lease structure is an important alternative to offer customers, particularly new customers

Simplicity - the Triple Net structure is less widely understood

Certainty - some customers want to be able to budget costs throughout the lease term with greater certainty than the Triple Net model allows

Rent includes all costs related to operating expenses

“Full” rent amount subject to annual escalation

Exceptions:

Metered Power including cooling uplift - passed through to customer at DFT cost

Property taxes and insurance – increased above annual escalation percentage passed through to customer

Amortized capital costs that result from change in law (e.g., environmental regulation requires additional scrubbers or ADA requires additional accommodations)

DFT will price full service leases so that it can recover its operating costs over the lease term and earn a risk premium

New lease structure attracts new customers

74 | November 10, 2015

STRATEGIC PRIORITIES: PROGRESS

75 | November 10, 2015

STRATEGIC PRIORITIES: Progress

Accelerate growth in our current business Defined new full-service lease model in addition to Triple Net

Expansions and lease-ups in existing markets

Target New Markets for Expansion Created short list of land in key locations (Toronto, Portland, Phoenix)

Negotiating land acquisition (Toronto, Portland, Phoenix)UNDERWAY

UNDERWAY

76 | November 10, 2015

STRATEGIC PRIORITIES: Progress

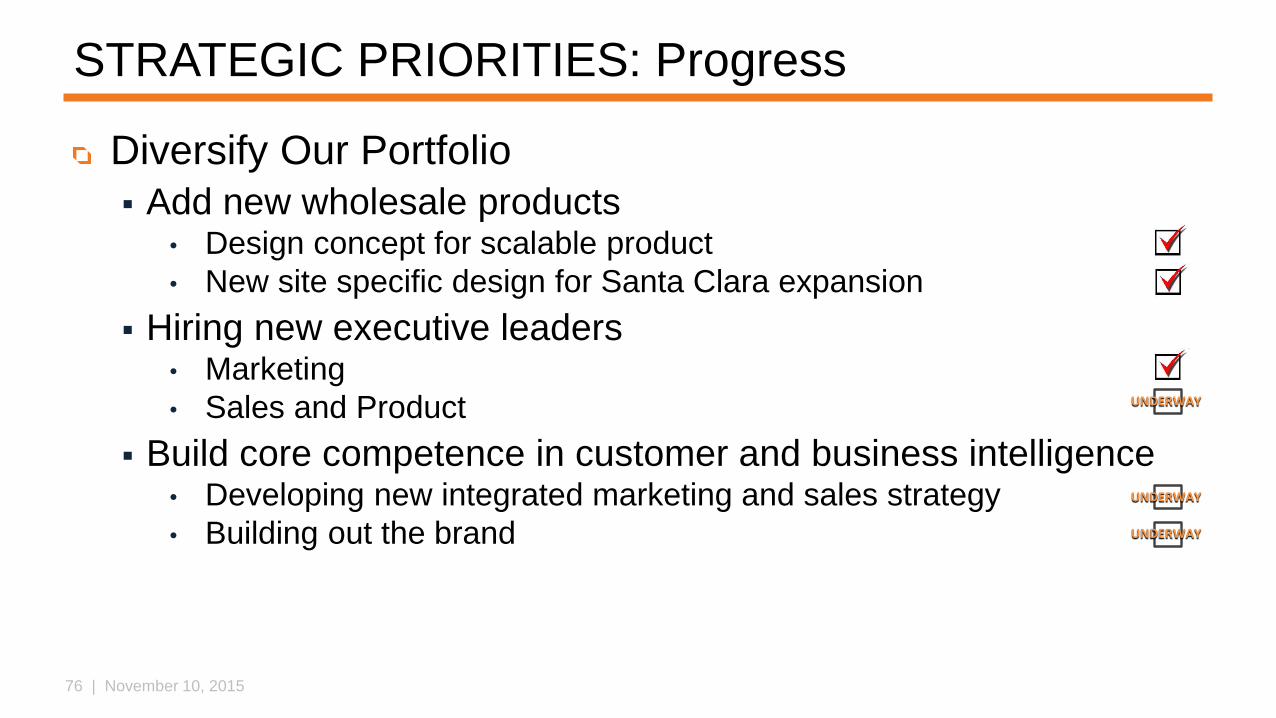

Diversify Our Portfolio

Add new wholesale products• Design concept for scalable product

• New site specific design for Santa Clara expansion

Hiring new executive leaders• Marketing

• Sales and Product

Build core competence in customer and business intelligence• Developing new integrated marketing and sales strategy

• Building out the brand

UNDERWAY

UNDERWAY

UNDERWAY

77 | November 10, 2015

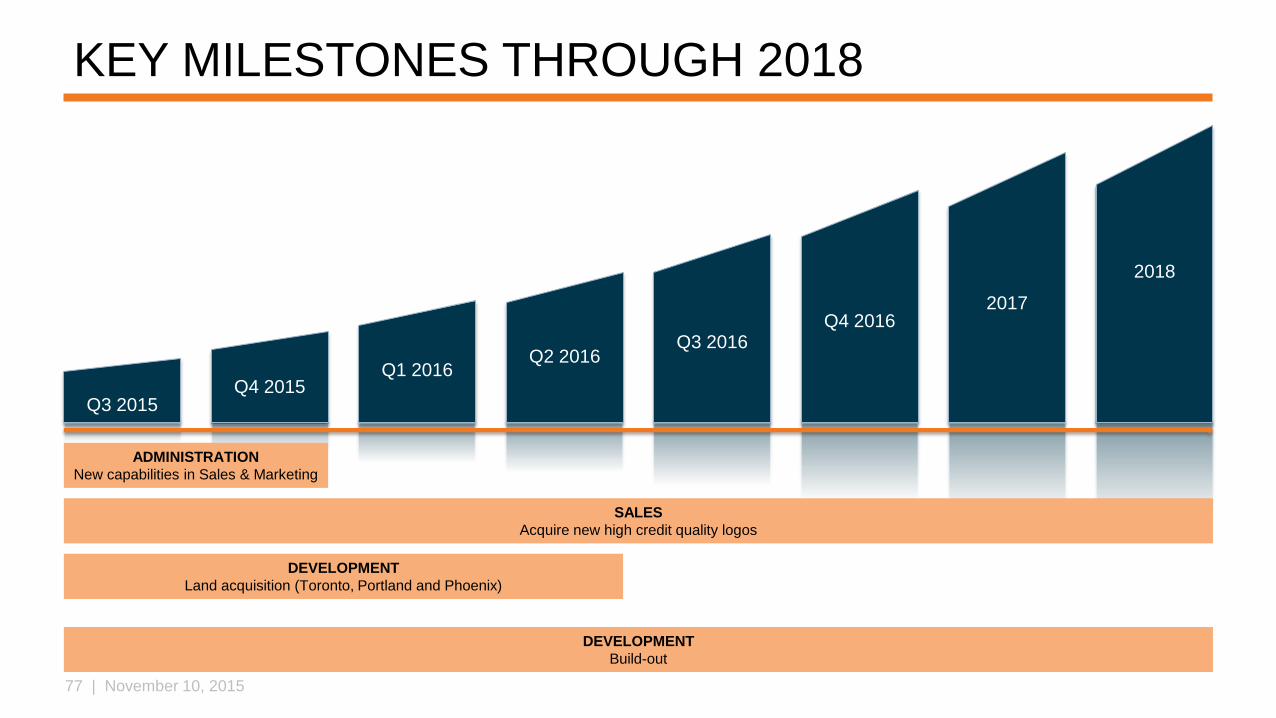

KEY MILESTONES THROUGH 2018

Q3 2015Q4 2015

Q1 2016Q2 2016

Q3 2016Q4 2016

2017

2018

ADMINISTRATION

New capabilities in Sales & Marketing

SALES

Acquire new high credit quality logos

DEVELOPMENT

Land acquisition (Toronto, Portland and Phoenix)

DEVELOPMENT

Build-out

78 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

79 | November 10, 2015

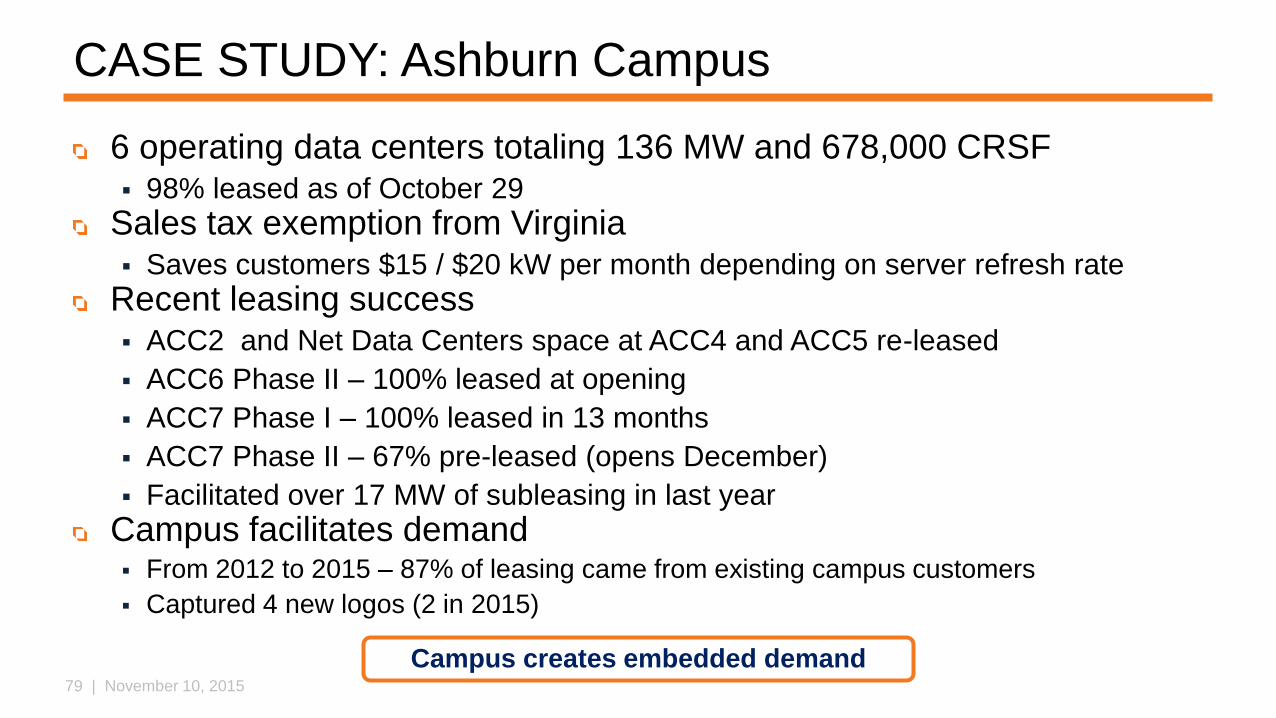

CASE STUDY: Ashburn Campus

6 operating data centers totaling 136 MW and 678,000 CRSF 98% leased as of October 29

Sales tax exemption from Virginia Saves customers $15 / $20 kW per month depending on server refresh rate

Recent leasing success ACC2 and Net Data Centers space at ACC4 and ACC5 re-leased

ACC6 Phase II – 100% leased at opening

ACC7 Phase I – 100% leased in 13 months

ACC7 Phase II – 67% pre-leased (opens December)

Facilitated over 17 MW of subleasing in last year

Campus facilitates demand From 2012 to 2015 – 87% of leasing came from existing campus customers

Captured 4 new logos (2 in 2015)

Campus creates embedded demand

80 | November 10, 2015

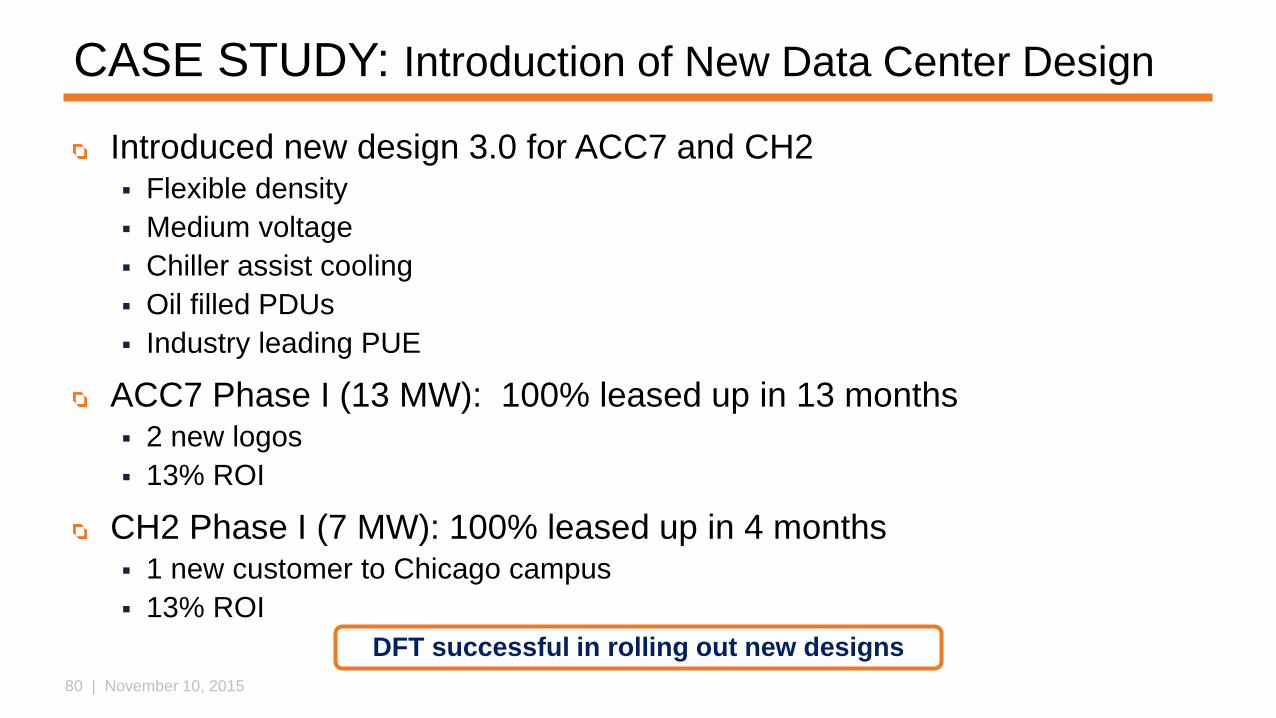

CASE STUDY: Introduction of New Data Center Design

Introduced new design 3.0 for ACC7 and CH2 Flexible density

Medium voltage

Chiller assist cooling

Oil filled PDUs

Industry leading PUE

ACC7 Phase I (13 MW): 100% leased up in 13 months 2 new logos

13% ROI

CH2 Phase I (7 MW): 100% leased up in 4 months 1 new customer to Chicago campus

13% ROI

DFT successful in rolling out new designs

81 | November 10, 2015

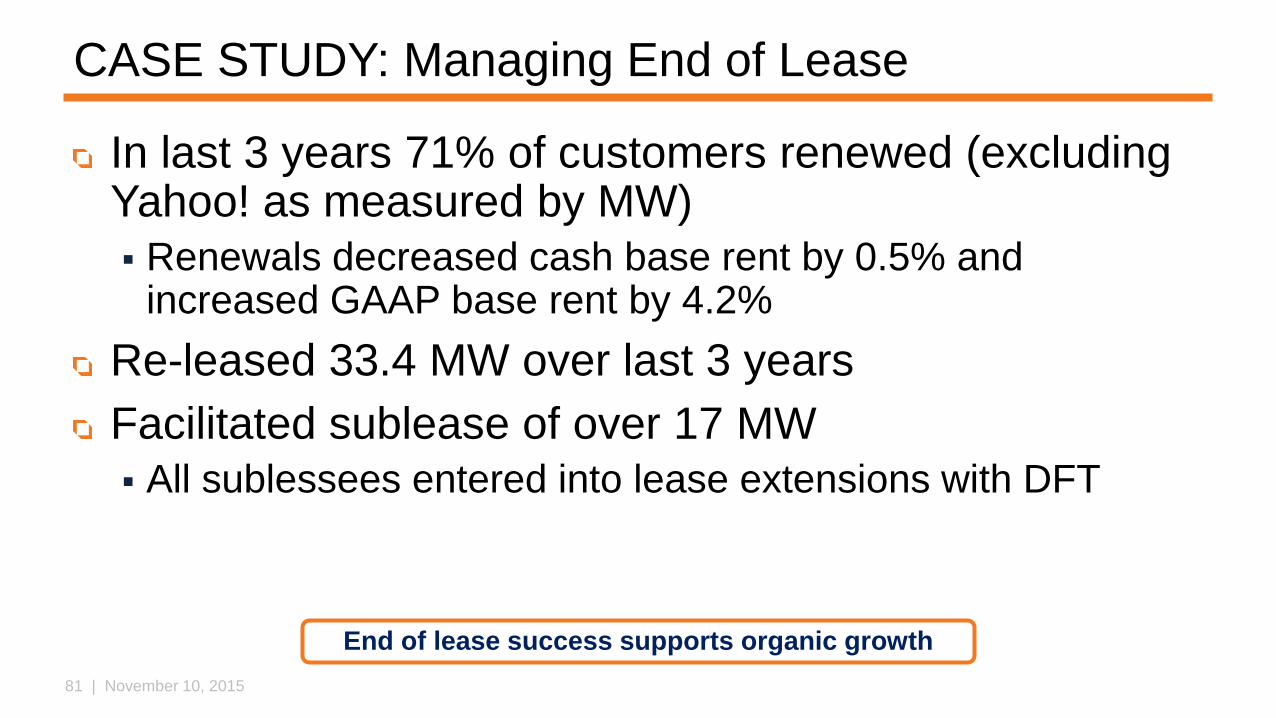

CASE STUDY: Managing End of Lease

In last 3 years 71% of customers renewed (excluding Yahoo! as measured by MW)

Renewals decreased cash base rent by 0.5% and increased GAAP base rent by 4.2%

Re-leased 33.4 MW over last 3 years

Facilitated sublease of over 17 MW

All sublessees entered into lease extensions with DFT

End of lease success supports organic growth

82 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

83 | November 10, 2015

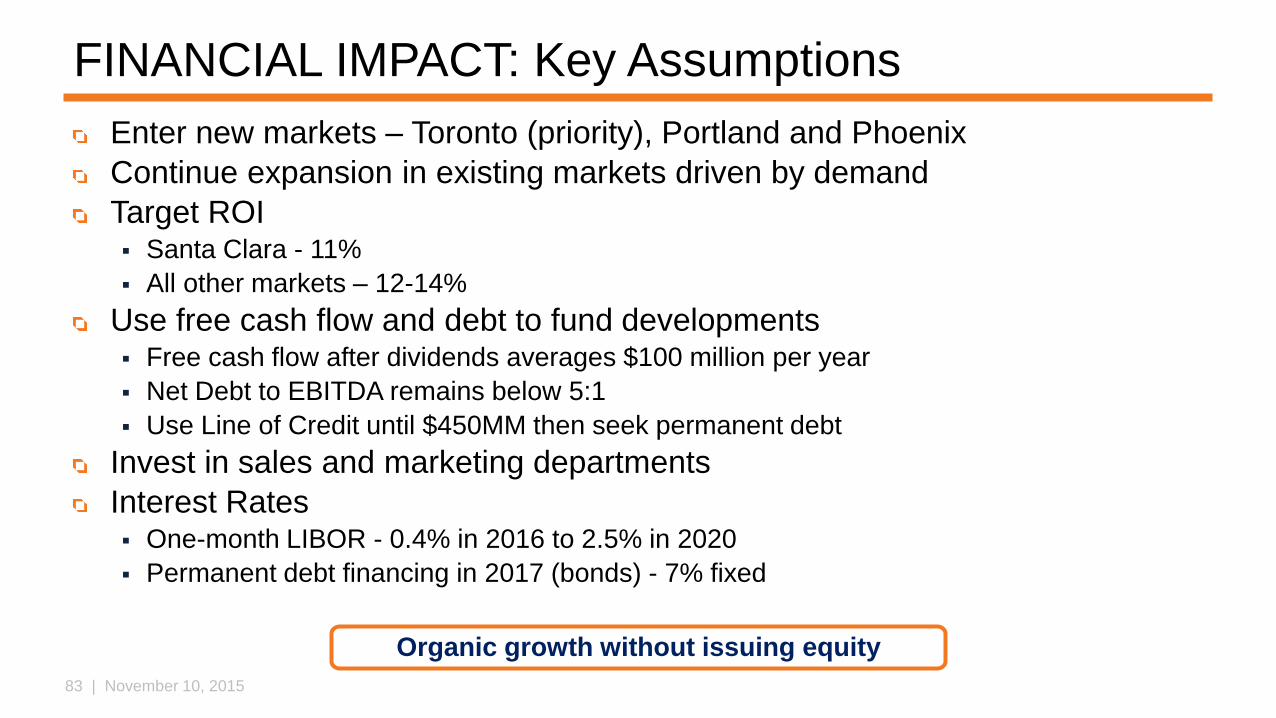

FINANCIAL IMPACT: Key Assumptions

Enter new markets – Toronto (priority), Portland and Phoenix

Continue expansion in existing markets driven by demand

Target ROI Santa Clara - 11%

All other markets – 12-14%

Use free cash flow and debt to fund developments Free cash flow after dividends averages $100 million per year

Net Debt to EBITDA remains below 5:1

Use Line of Credit until $450MM then seek permanent debt

Invest in sales and marketing departments

Interest Rates One-month LIBOR - 0.4% in 2016 to 2.5% in 2020

Permanent debt financing in 2017 (bonds) - 7% fixed

Organic growth without issuing equity

84 | November 10, 2015

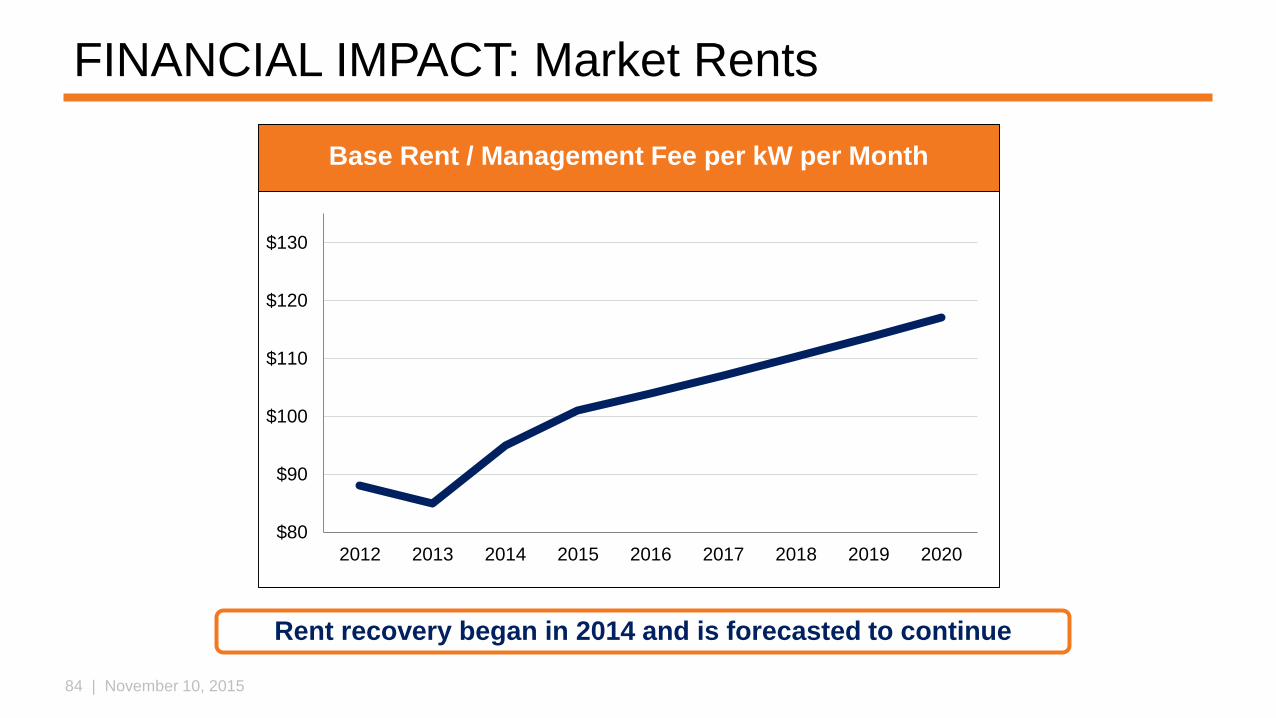

FINANCIAL IMPACT: Market Rents

Base Rent / Management Fee per kW per Month

Rent recovery began in 2014 and is forecasted to continue

$80

$90

$100

$110

$120

$130

2012 2013 2014 2015 2016 2017 2018 2019 2020

85 | November 10, 2015

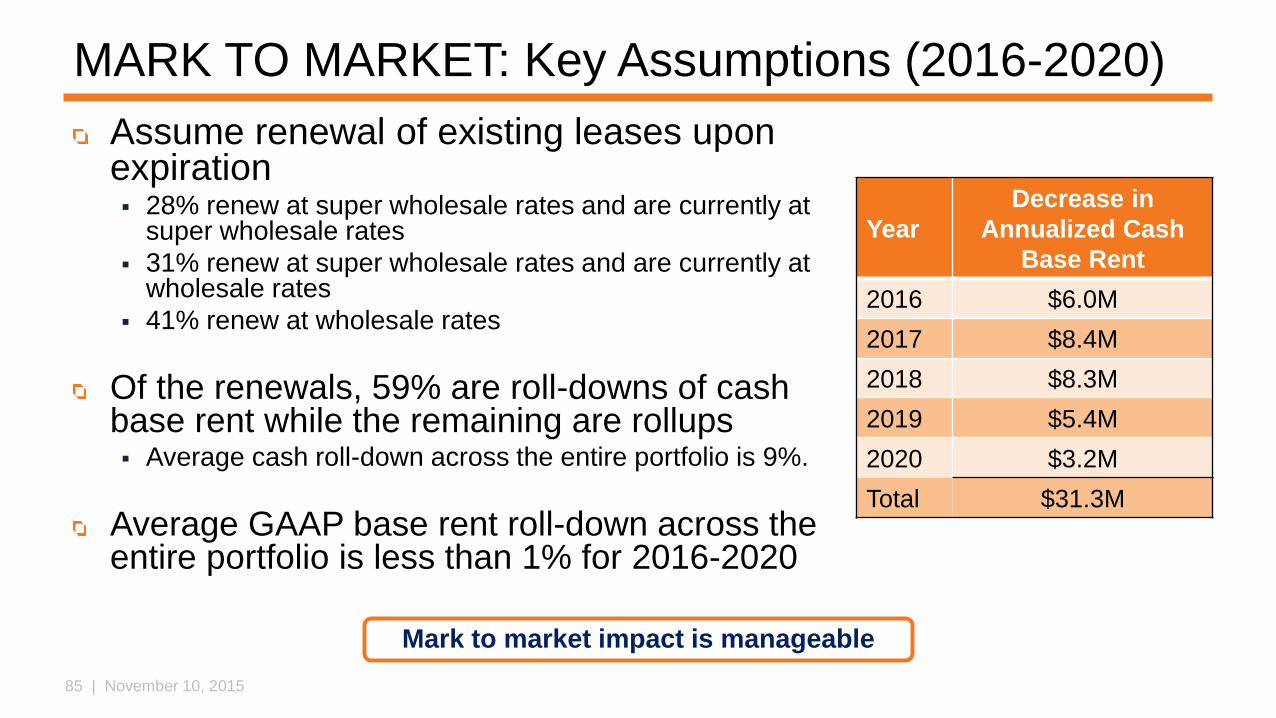

Assume renewal of existing leases upon expiration 28% renew at super wholesale rates and are currently at

super wholesale rates

31% renew at super wholesale rates and are currently at wholesale rates

41% renew at wholesale rates

Of the renewals, 59% are roll-downs of cash base rent while the remaining are rollups Average cash roll-down across the entire portfolio is 9%.

Average GAAP base rent roll-down across the entire portfolio is less than 1% for 2016-2020

Mark to market impact is manageable

MARK TO MARKET: Key Assumptions (2016-2020)

Year

Decrease in

Annualized Cash

Base Rent

2016 $6.0M

2017 $8.4M

2018 $8.3M

2019 $5.4M

2020 $3.2M

Total $31.3M

86 | November 10, 2015

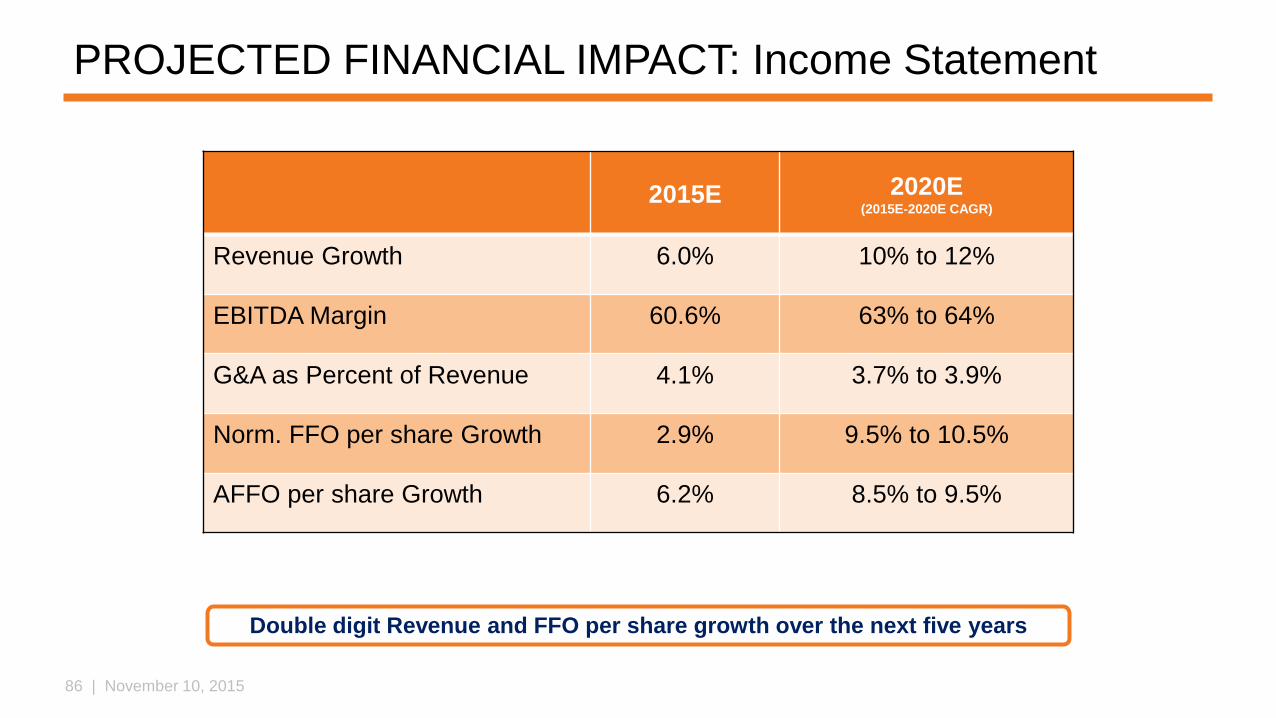

PROJECTED FINANCIAL IMPACT: Income Statement

2015E 2020E (2015E-2020E CAGR)

Revenue Growth 6.0% 10% to 12%

EBITDA Margin 60.6% 63% to 64%

G&A as Percent of Revenue 4.1% 3.7% to 3.9%

Norm. FFO per share Growth 2.9% 9.5% to 10.5%

AFFO per share Growth 6.2% 8.5% to 9.5%

Double digit Revenue and FFO per share growth over the next five years

87 | November 10, 2015

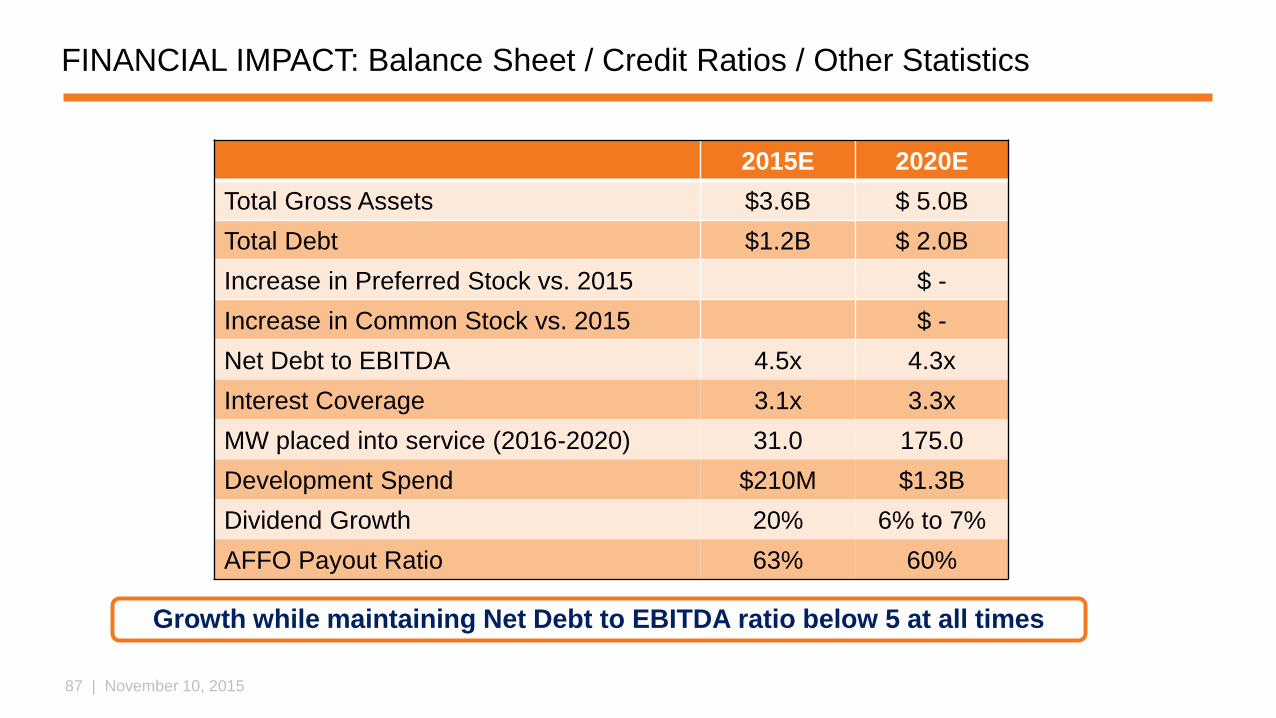

FINANCIAL IMPACT: Balance Sheet / Credit Ratios / Other Statistics

2015E 2020E

Total Gross Assets $3.6B $ 5.0B

Total Debt $1.2B $ 2.0B

Increase in Preferred Stock vs. 2015 $ -

Increase in Common Stock vs. 2015 $ -

Net Debt to EBITDA 4.5x 4.3x

Interest Coverage 3.1x 3.3x

MW placed into service (2016-2020) 31.0 175.0

Development Spend $210M $1.3B

Dividend Growth 20% 6% to 7%

AFFO Payout Ratio 63% 60%

Growth while maintaining Net Debt to EBITDA ratio below 5 at all times

88 | November 10, 2015

CONTENTS

Mission and Vision

Strategy Summary

Current Situation

Opportunities

Strategic Priorities

New Markets

New Products

Progress

Execution – Case Studies

Financial Impact

Closing

89 | November 10, 2015

CLOSING

We will:

Offer more flexibility to serve the needs of both new and existing customers

Diversify geographic footprint

Increase number of high quality logos

We will deliver increased revenue growth and profitability without new equity

90 | November 10, 2015 WWW.DFT.COM

91 | November 10, 2015

RECONCILIATIONS OF NET INCOME TO NAREIT FFO, NORMALIZED FFO AND AFFO (1)