Embed Size (px)

Citation preview

Concordia Bus Deutsche Bank HYB Conference

London – June 2002

2

Safe Harbour

The matters discussed in this presentation include

forward-looking statements that are subject to risks

and uncertainties including but not limited to

economic conditions, product demand, competitive

products and services, government regulation,

financial resources, certain litigation and other risks

indicated in filings with the US Securities and

Exchange commission

Frode Larsen - Chief Executive Officer

4

Corporate Purpose

TO BUILD A FOCUSSED, LEADING URBAN BUS

TRANSPORTATION COMPANY WITHIN EUROPE

THROUGH THE CREATION OF A PROFITABLE GROUP OF COMPANIES OPERATING UNDER

A STANDARD 'CONCORDIA CONCEPT' UNDER

THE VALUE BASED MANAGEMENT PHILOSOPHY FOR SUSTAINABLE VALUE GROWTH

FOR SHAREHOLDERS AND STAKEHOLDERS

5

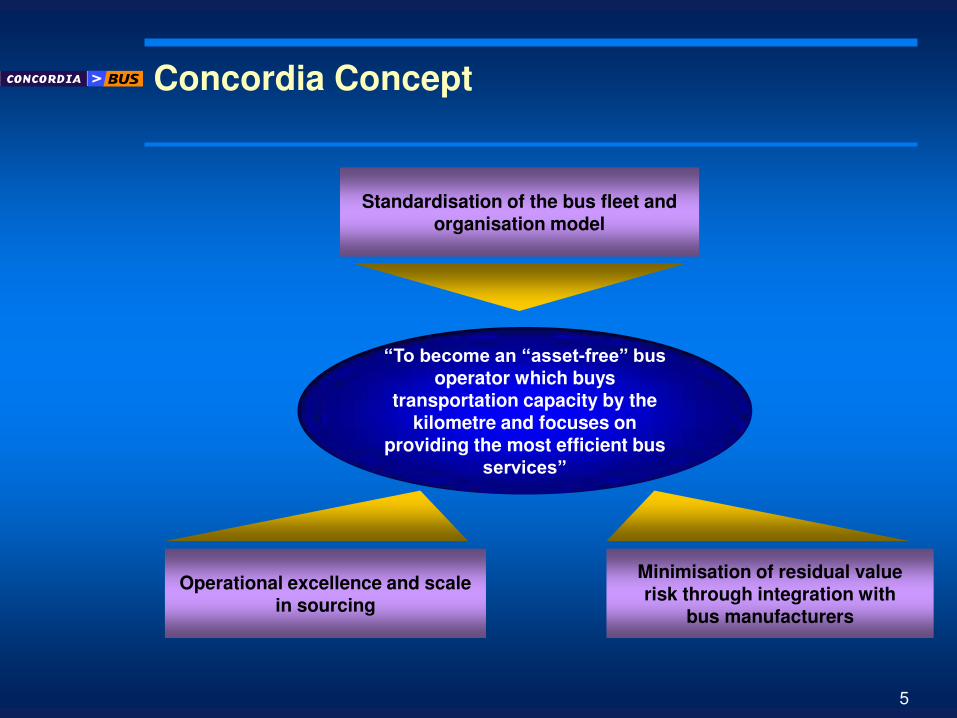

Concordia Concept

Standardisation of the bus fleet and organisation model

Minimisation of residual value risk through integration with

bus manufacturers

Operational excellence and scale in sourcing

“To become an “asset-free” bus operator which buys

transportation capacity by the kilometre and focuses on

providing the most efficient bus services”

6

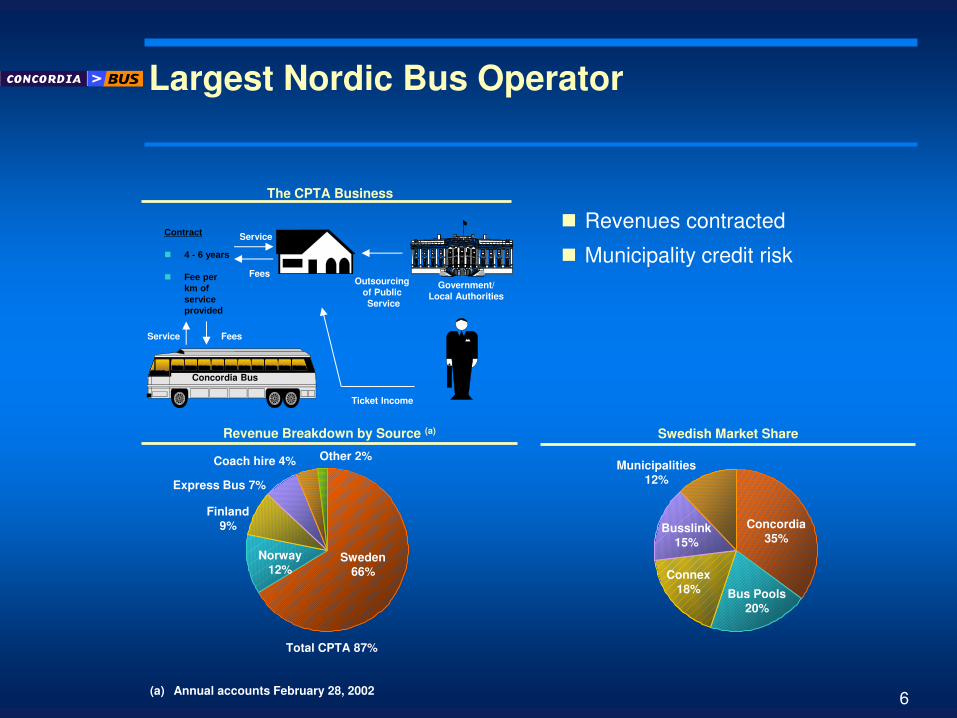

(a) Annual accounts February 28, 2002

Largest Nordic Bus Operator

Swedish Market Share

The CPTA Business

Service

Fees Outsourcing

of Public

Service

Government/

Local Authorities

Ticket Income

Concordia Bus

Contract

4 - 6 years

Fee per km of service provided

Service Fees

Concordia 35%

Bus Pools 20%

Connex 18%

Busslink 15%

Municipalities

12%

Revenue Breakdown by Source (a)

Sweden

66%

Norway

12%

Finland

9%

Express Bus 7%

Coach hire 4%

Total CPTA 87%

Other 2%

Revenues contracted

Municipality credit risk

7

Initial Underperformance

Dramatic increase in diesel prices

Increased oil prices and Swedish Krona depreciation

Sensitivity to oil price increase previously high. Hedging

strategy and indexation has significantly reduced sensitivity

Two new “mispriced” contracts inherited from the seller

Inflation compensation lower than realized cost inflation

CPI of 1.3% versus realized bus cost inflation of 2.4%; as at

February 2000, majority of revenue indexed to CPI

Cost savings more difficult to realize than originally anticipated

8

We have now “Turned the Corner”

Operating recovery underway in FY2003

New Contracts successfully operational without major issues and

started to contribute substantially

Restructuring programme announced in February has been

successfully implemented providing incremental benefits

Quarter 1 FY2003 Highlights:

Revenue up + 12.6%

EBITDAR up + 74.7%

EBITDA up + 86.6%

“External” factors remain positively in our favour Diesel prices stabilising

Swedish inflation acceptable

Performance of the business has turned and is improving:

new, profitable contracts, a better operating environment and incremental

cost savings

9

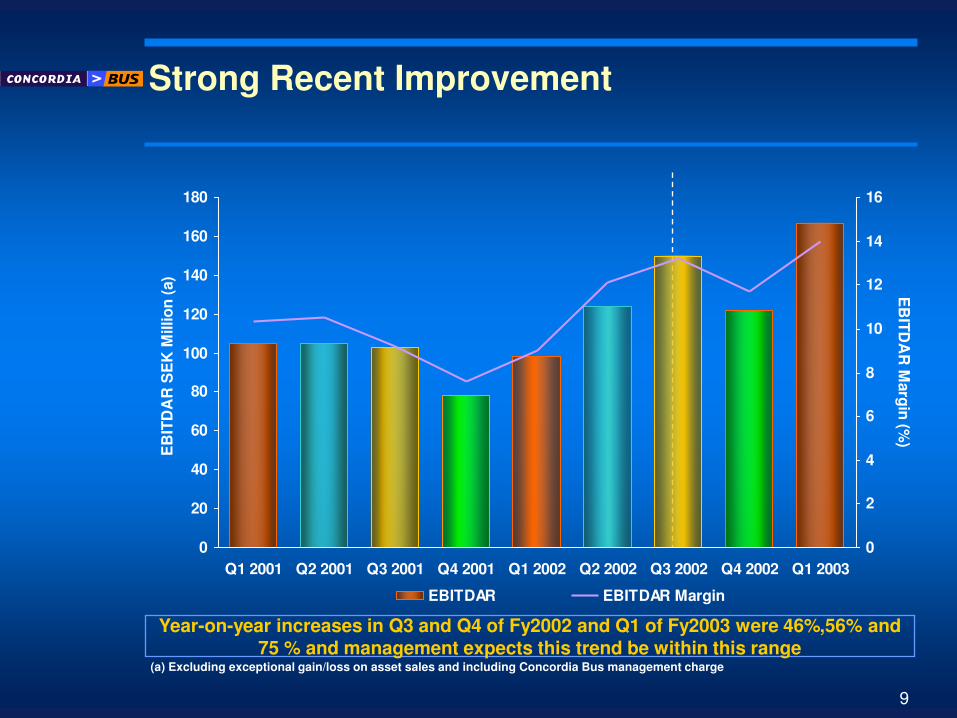

Strong Recent Improvement

Year-on-year increases in Q3 and Q4 of Fy2002 and Q1 of Fy2003 were 46%,56% and 75 % and management expects this trend be within this range

0

20

40

60

80

100

120

140

160

180

Q1 2001 Q2 2001 Q3 2001 Q4 2001 Q1 2002 Q2 2002 Q3 2002 Q4 2002 Q1 2003

EB

ITD

AR

SE

K M

illio

n (

a)

0

2

4

6

8

10

12

14

16

EB

ITD

AR

Marg

in (%

)

EBITDAR EBITDAR Margin

(a) Excluding exceptional gain/loss on asset sales and including Concordia Bus management charge

10

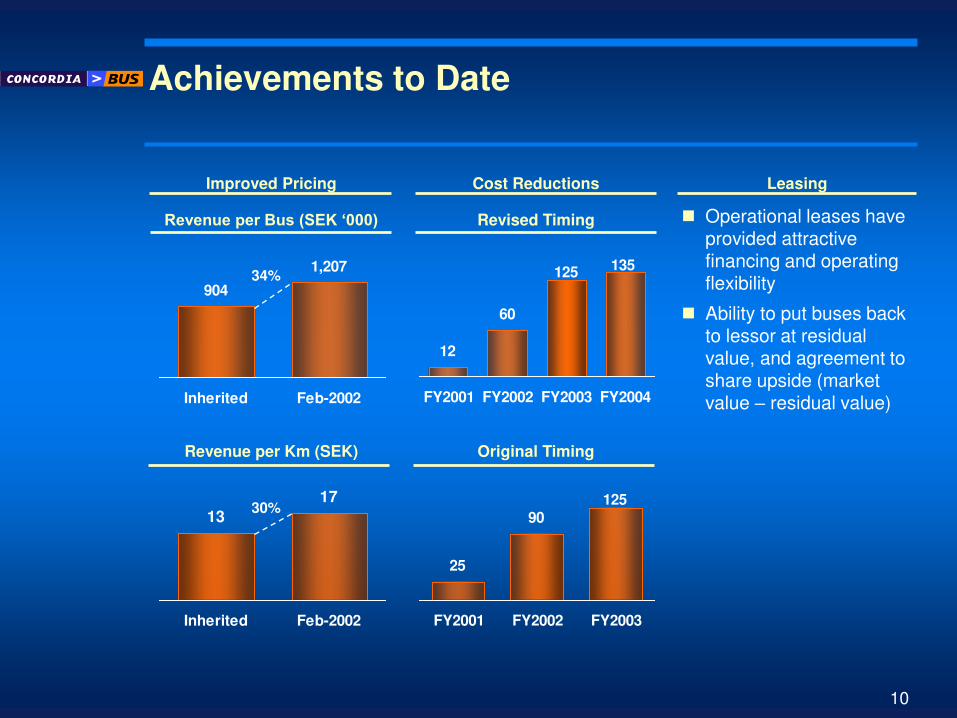

Achievements to Date

Leasing Cost Reductions

Operational leases have provided attractive financing and operating flexibility

Ability to put buses back to lessor at residual value, and agreement to share upside (market value – residual value)

Improved Pricing

904

1,207

Inherited Feb-2002

13

17

Inherited Feb-2002

34%

30%

12

60

125 135

FY2001 FY2002 FY2003 FY2004

Revenue per Bus (SEK ‘000) Revised Timing

25

90

125

FY2001 FY2002 FY2003

Revenue per Km (SEK) Original Timing

Vasant Mistry - Chief Financial Officer

12

Risks

Coverage and Management..……

13

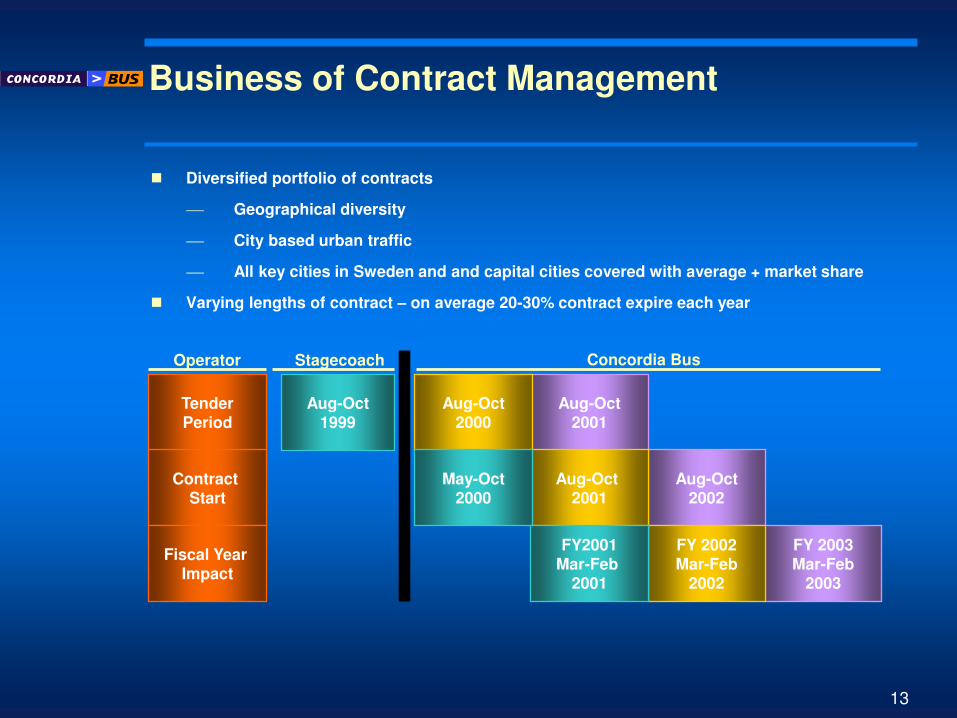

Business of Contract Management

Aug-Oct 2001

Aug-Oct 2000

Aug-Oct 1999

Tender Period

Aug-Oct 2002

Aug-Oct 2001

May-Oct 2000

Contract Start

FY 2003 Mar-Feb

2003

FY 2002 Mar-Feb

2002

FY2001 Mar-Feb

2001

Fiscal Year Impact

Operator Stagecoach Concordia Bus

Diversified portfolio of contracts

Geographical diversity

City based urban traffic

All key cities in Sweden and and capital cities covered with average + market share

Varying lengths of contract – on average 20-30% contract expire each year

14

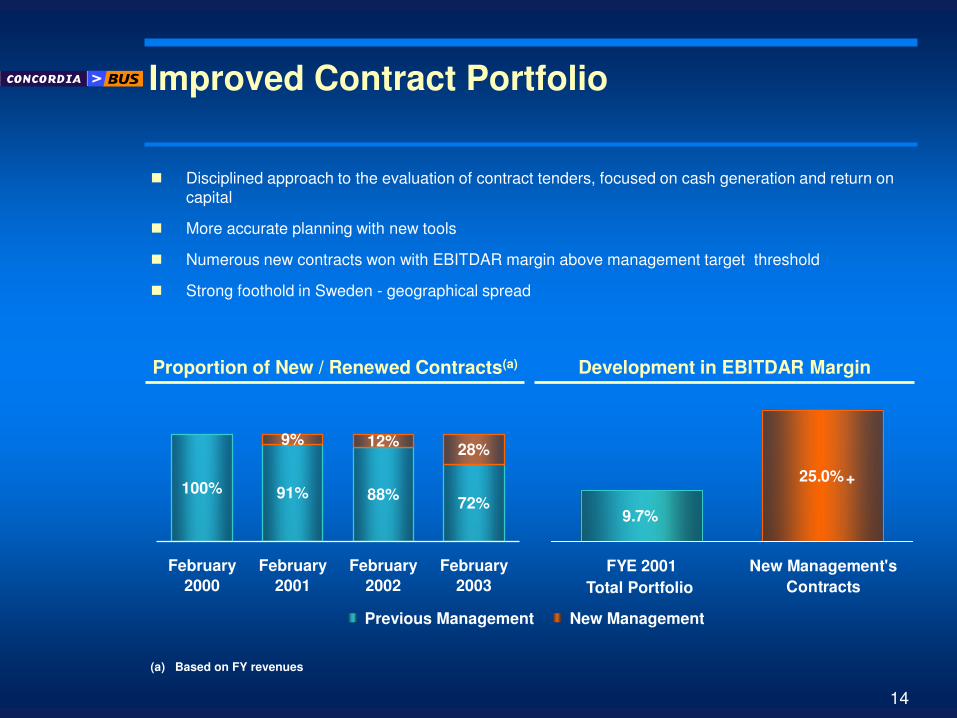

Improved Contract Portfolio

Disciplined approach to the evaluation of contract tenders, focused on cash generation and return on

capital

More accurate planning with new tools

Numerous new contracts won with EBITDAR margin above management target threshold

Strong foothold in Sweden - geographical spread

Proportion of New / Renewed Contracts(a) Development in EBITDAR Margin

Previous Management New Management

9.7%

25.0%

FYE 2001 New Management's

Contracts

100% 91% 88%72%

9% 12%28%

February

2000

February

2001

February

2002

February

2003

(a) Based on FY revenues

Total Portfolio

+

15

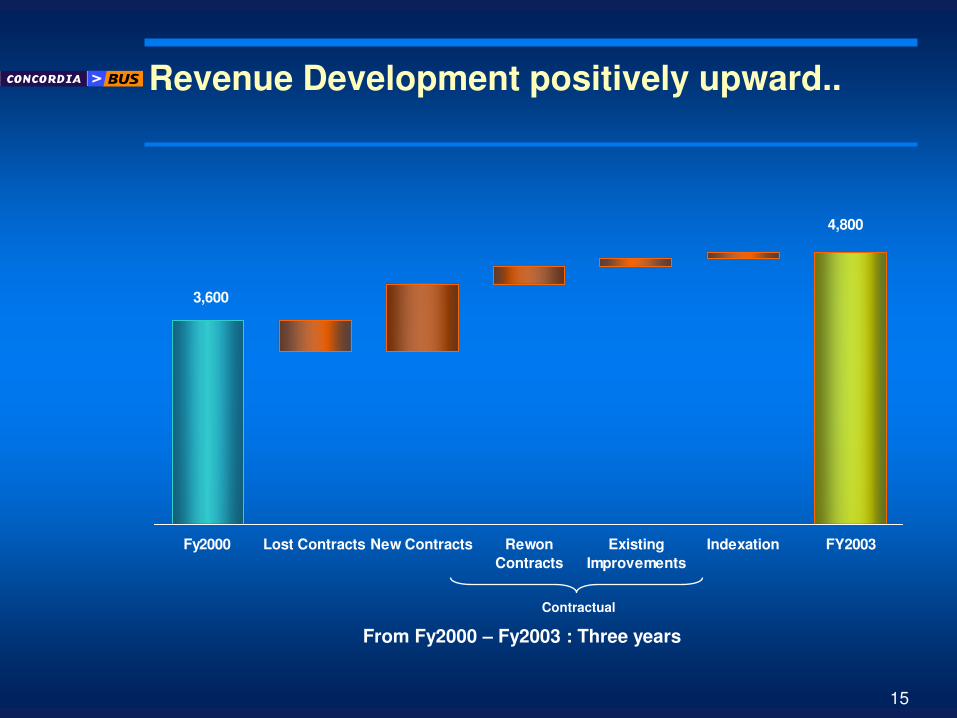

3,600

4,800

Fy2000 Lost Contracts New Contracts Rewon

Contracts

Existing

Improvements

Indexation FY2003

Revenue Development positively upward..

Contractual

From Fy2000 – Fy2003 : Three years

16

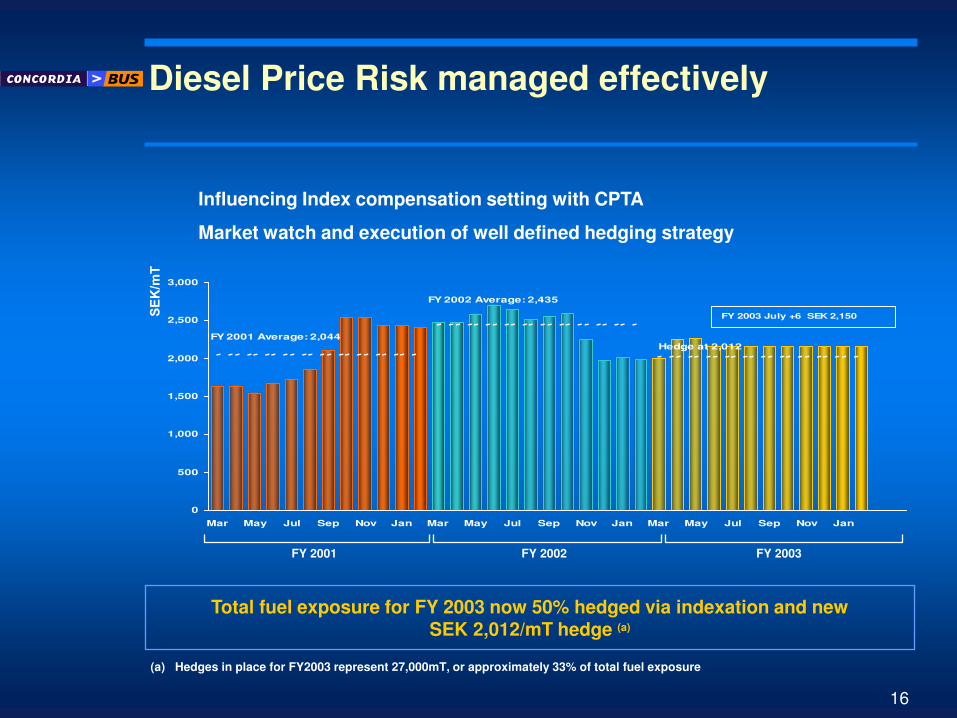

Diesel Price Risk managed effectively

FY 2001 Average: 2,044

FY 2002 Average: 2,435

Hedge at 2,012

0

500

1,000

1,500

2,000

2,500

3,000

Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan

FY 2003 July +6 SEK 2,150

FY 2001 FY 2002 FY 2003

Total fuel exposure for FY 2003 now 50% hedged via indexation and new SEK 2,012/mT hedge (a)

(a) Hedges in place for FY2003 represent 27,000mT, or approximately 33% of total fuel exposure

Influencing Index compensation setting with CPTA

Market watch and execution of well defined hedging strategy

17

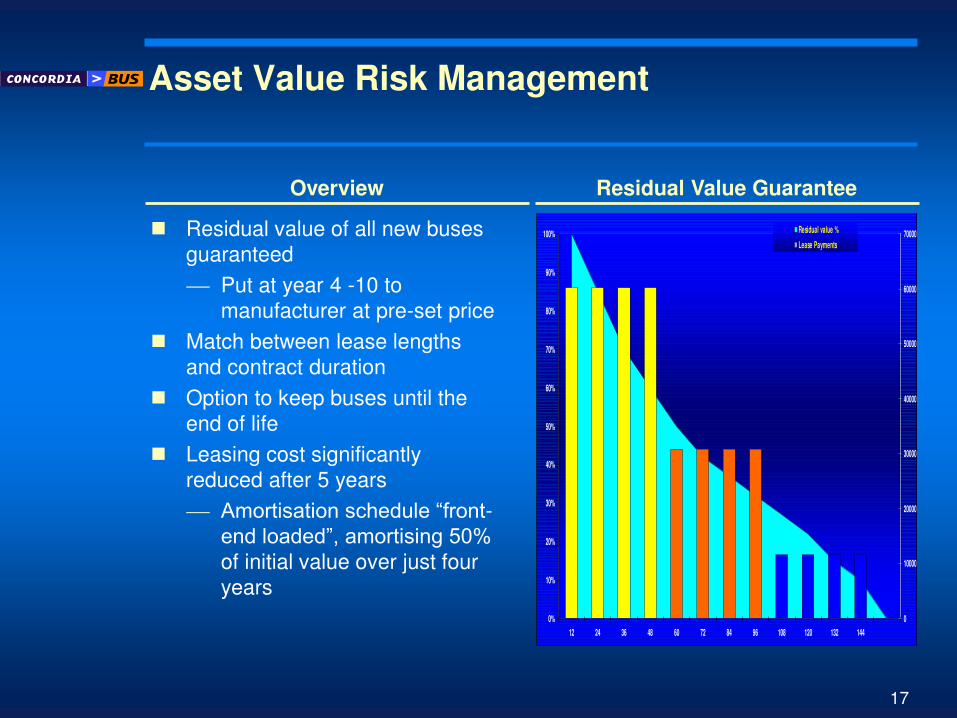

Asset Value Risk Management

Residual value of all new buses

guaranteed

Put at year 4 -10 to

manufacturer at pre-set price

Match between lease lengths

and contract duration

Option to keep buses until the

end of life

Leasing cost significantly

reduced after 5 years

Amortisation schedule “front-end loaded”, amortising 50% of initial value over just four

years

Overview Residual Value Guarantee

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

12 24 36 48 60 72 84 96 108 120 132 144

0

10000

20000

30000

40000

50000

60000

70000Residual value %

Lease Payments

18

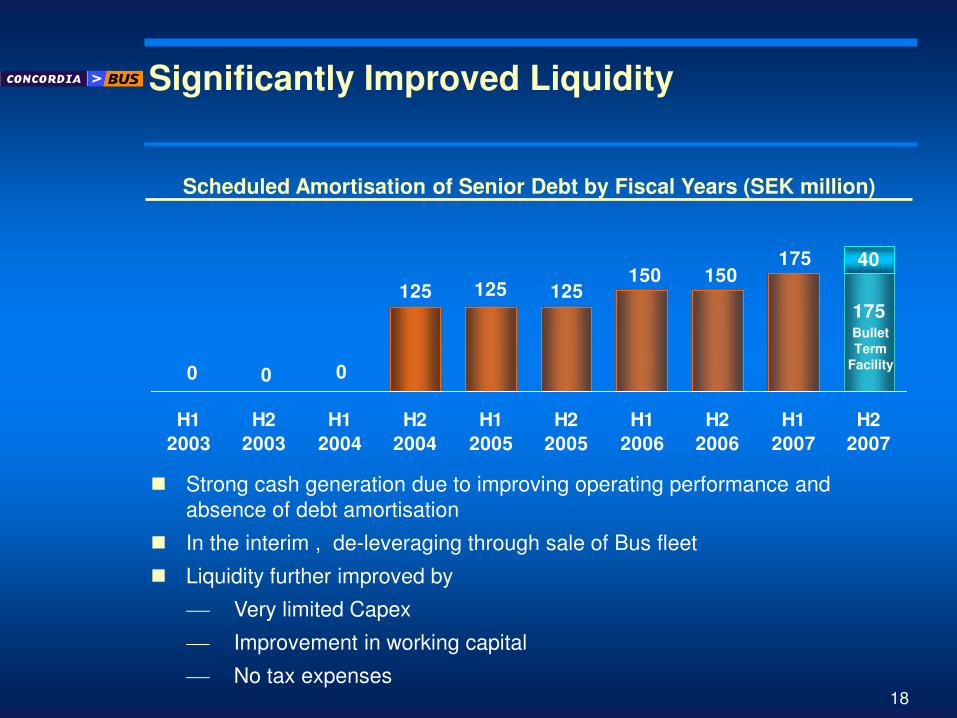

Significantly Improved Liquidity

Scheduled Amortisation of Senior Debt by Fiscal Years (SEK million)

175

175150150

125125

0 0 0

125

40

H1

2003

H2

2003

H1

2004

H2

2004

H1

2005

H2

2005

H1

2006

H2

2006

H1

2007

H2

2007

Strong cash generation due to improving operating performance and

absence of debt amortisation

In the interim , de-leveraging through sale of Bus fleet

Liquidity further improved by

Very limited Capex

Improvement in working capital

No tax expenses

Bullet

Term

Facility

19

State of the Art Technology and

applications…improved management systems…..

Standardisation Common Applications

Traffic planning

Fleet Maintenance

Financial Applications

Business Planning –DSS

New Operations Management system (under development)

Internal Systems focus leading to Proactive Management of risks and

improved profitability…

Web based Distribution of management information

Web based location/Depot level dissemination of operating and

financial information

Culture change and introduction of results driven culture

20

Concordia’s Capitalisation (SEK m)

May 31, 2002 February 2002

High Yield Bond 1,454 1,454

Other Debt 1,060 1,021

Total Debt 2,514 2,475

Cash 422 207

Net Debt 2,092 2,268

Equity 444 400

NBV of Assets 2,016 2,096

Net Debt+ Leases / EBITDAR 5.78 5.39(a)

(a) – Based on last 12 months EBITDAR

21

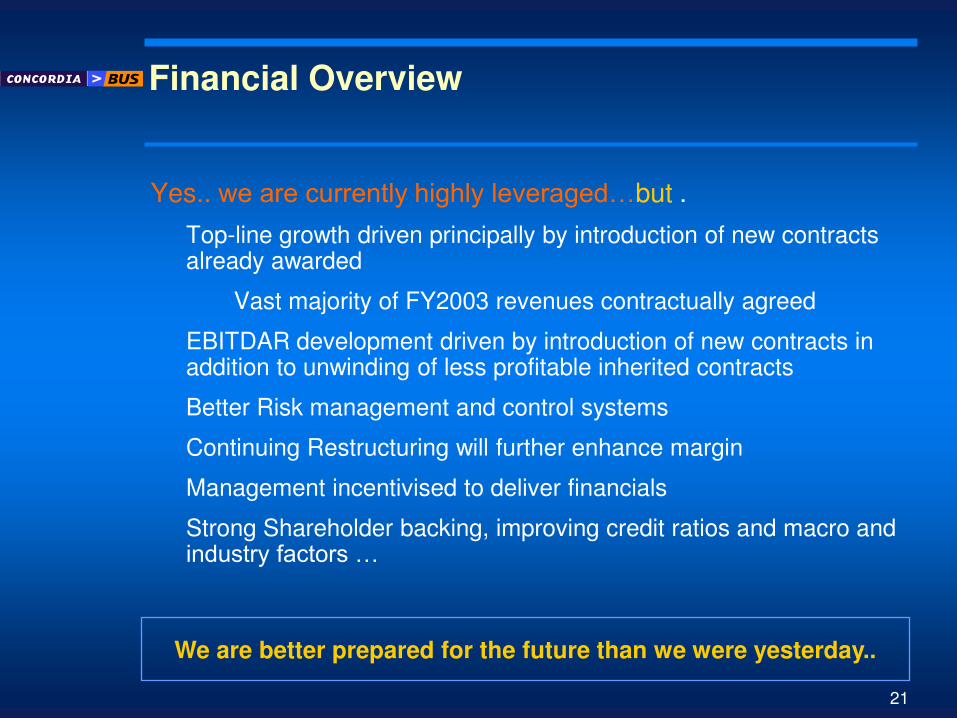

Financial Overview

Yes.. we are currently highly leveraged…but .

Top-line growth driven principally by introduction of new contracts already awarded

Vast majority of FY2003 revenues contractually agreed

EBITDAR development driven by introduction of new contracts in addition to unwinding of less profitable inherited contracts

Better Risk management and control systems

Continuing Restructuring will further enhance margin

Management incentivised to deliver financials

Strong Shareholder backing, improving credit ratios and macro and industry factors …

We are better prepared for the future than we were yesterday..

23

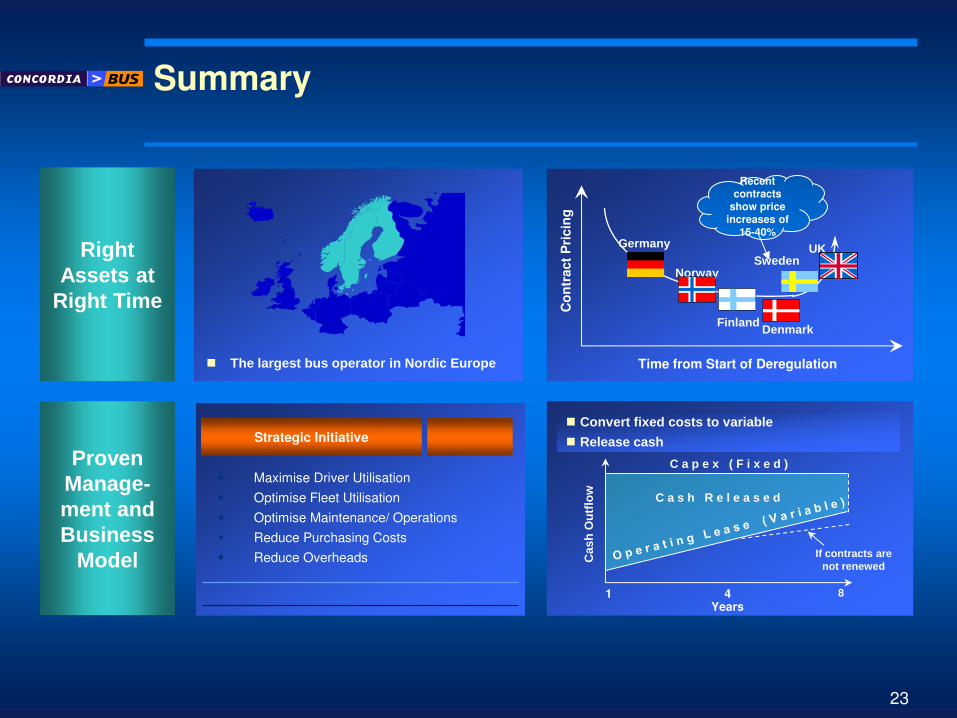

Summary

Right Assets at

Right Time

Proven Manage-ment and Business

Model

The largest bus operator in Nordic Europe

Maximise Driver Utilisation

Optimise Fleet Utilisation

Optimise Maintenance/ Operations

Reduce Purchasing Costs

Reduce Overheads

Strategic Initiative

Cas

h O

utf

low

4

If contracts are not renewed

C a s h R e l e a s e d

C a p e x ( F i x e d )

Convert fixed costs to variable

Release cash

1 8

Co

ntr

act

Pri

cin

g

Time from Start of Deregulation

Germany

Norway Sweden

Finland

UK

Recent contracts

show price increases of

15-40%

Denmark

Years

24

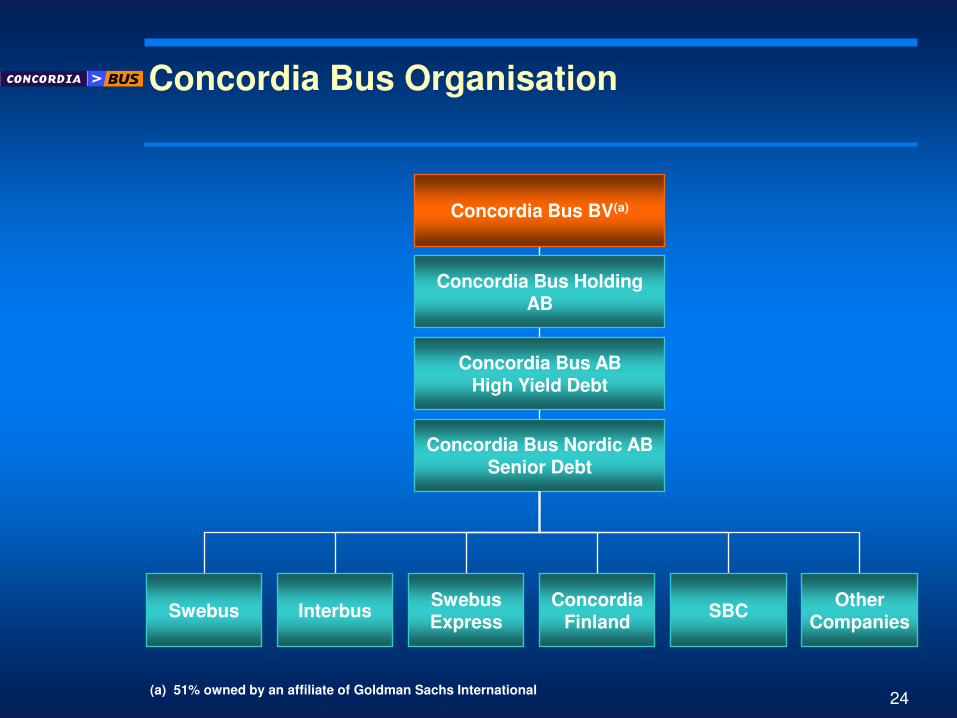

Concordia Bus Organisation

Concordia Bus AB High Yield Debt

Concordia Bus BV(a)

Concordia Bus Holding AB

Concordia Bus Nordic AB Senior Debt

Swebus SBC Interbus Concordia

Finland Swebus Express

Other Companies

(a) 51% owned by an affiliate of Goldman Sachs International