Embed Size (px)

Citation preview

CUSTOMER AWARNESS AND ADOPTION OF

ISLAMIC BANKING PRODUCTS IN

MOGADISHU, SOMALIA.

BY

ALl ADAN SABRIYE

MBA-BANK1NG AND FINANCE (KIU, BBA- ACCOUNTING (SU)

MBA/39904/13 1/DF

A RESEARCH THESIS SUMMITED TO THE COLLEGE OF HIGHER

DEGREE AND RESAERCH [N PARTIAL FULFILMENT OF THE

REQUIREMENT FOR THE AWARD OF THE MBA-BANKING AND

FINANCE OF KAMPALA INTERNATIONAL UNIVERSITY

NOVEMBER 2014

TABLE OF CONTENTS

DECLARATION.

APPROVAL ii

DEDICATION Ii

ACKNOWLEDGEMENTS iv

ABSTRACT vii

CHAPTER ONE I

THE PROBLEM AND ITS SCOPE 1

1 .0 Introduction 1

1.1 Background 1

1.1.1 The Historical Background 1

1.1.2 Theoretical Background 3

1.1.3 Conceptual Background 3

1.1.4 Contextual Background 4

1.2 Statement of problem 5

1.3 purpose of the study 6

1.4 Specific objectives 6

1.5 Research Question 6

1.6 HYPOTHESIS 7

1.7 Significance of study 7

1.8 Scope of the study 7

1.8.1 Geographical scope 7

1.8.2 Content Scope 7

1.8.3 Theoretical scope 8

1.8.4 Time scope 8

1.9 Operational definitions of key terms 8

CHAPTER TWO 10

2.0 Introduction 10

2.1 THERETICAL REVIEW 10

2.2. CONCEPTUAL FRAMEWORK 12

2.3 Review the Related Literature 14

2.3.1 Concept of customer awareness 14

V

2.3.1 Concept of customer awareness 14

2.3.2 Concept of adoption on Islamic banking product 14

2.3.3 Contracts in Islamic Banking 16

2.3.4 Trading Contracts 16

2.3.5 Participation Contracts 18

2.3.6 Supporting Contracts 18

OBJECTIVES OF ISAMIC BANK 19

2.4 Related Studies 20

CHAPTER THREE: METHODOLOGY 24

3.0 Introduction 24

3.1 Research Design 24

3.2 Target Population 24

Table 3.1: Showing the target respondents to be used in the study 25

3.3 Sample size 24

3.4 Sampling procedure 25

3.5 Research Instruments (tools) 25

3.6 Validity and reliability of the instruments 26

3.7 Data Gathering Procedures 27

3.8 Data Analysis 28

3.9 Ethical Considerations 28

3.10 Limitations of the Study 29

CHAPTER FOUR: DATA PRESENTATION, ANALYSIS 30

4.0 Introduction 30

4.1 Demographic Information of the Respondents 30

4.3 Research Question one: level of awareness of Islamic banking product33

4.4 Research Question two: level of adoption of Islamic product 38

4.5 Research Question three: Hypothesis 41

Table 4.4 Relationship between the level awareness and adoption of 42

4.6 Regression between level of customer awareness and adoption of 43

CHAPTER FIVE: DISCUSSION, CONCLUSION AND 45

5.0 Introduction 45

5.1 Discussion of The Research Findings 45

CONCULUSION 51

vi

Recommendations. 51

REFRENCES 54

APPENDIX A 57

LIST OF TABLES AND FIGURES

Table 3.1: Sample size 26

Table 3.2: CVI Resualt 29

Table 4.1 Demographic Respondents 34

Table 4.2 Level of awareness 37

Table 4.3: Level of adoption 43

Table 4.3 Relationship between the level of awareness and adoption Islamic products 46

Table 4.4 Regression between level of awareness and adoption Islamic products 48Figure 2.1: Conceptual framework level of awareness and adoption Islamic products 13

VII

DECLARATION

I, All Adan Sabriye, declare that this dissertation is my own original work and has never been

submitted for the award of a Degree in any University Institution in and outside Somalia.

Name and Signature of Candidate

~-~a ApA-~ 5~~t

.4~_— ‘-- -

Date.4~. ~( 2~f-(

APPROVAL

This thesis entitled: customer awareness and adoption of Islamic banking products in

Mogadishu, Somalia, has been duly reviewed at each stage of its development by the

undersigned as the candidateTh supervisors.

Name and Signature

II

DEDICATION

I dedicated this thesis to my mather Mrs. Fadumo Yusuf wahliye, And all my Brothers and

sisters, friends And my entire relative.

HI

ACKNOWLEDGEMENTS

In the name of Allah, most merciful, most gracious, my thesis has been successfully

implemented by the assistance of various authorities. Therefore, I would like to grasp this

opportunity to express my appreciation to them who have involved directly or indirectly in

contributing towards my thesis.

First and foremost, I thank Allah the way he guided to me and the ability, knowledge and the

wealth he gave me to write this thesis, Without Allah I could not be able to success this

thesis.

Second, I would like to thank my supervisor, DR Ssendige Moharned. This work would not

be completed on time without his time, guidance, effort, support, and patience. I fervently

appreciate his contribution during the meeting as he has given me a lot of constructive

comments, sincere advice as well as steady guidance through the progression of this research

project to achieve my objectives.

I would like to express my gratitude to my beloved mother Mrs. Fadurna Yusuf Wehliye,

who made me the person I am today. She was a wonderful mother and I will always

appreciate the effort she invested into nurturing me and my siblings to greater heights. I

would like to thank my brother Mohamed Aden Sabriye for sponsoring my master degree and

his moral support through my study.

I would also like to acknowledge the lecturers of KIU, friends and classmates for their

opinions, encouragement and enthusiasm. I would like to thank the respondents of this study

as they have participated in our questionnaires surveys.

Once again, thank you and best regards to all of you!

iv

ABSTRACT

The study investigated the relationship between customer awareness and adoption of Islamic

banking products of 109 purposively and convenience selected customers from banks in

Mogadishu, Somalia, using descriptive, correlational research design. Data was collected

using both interview and self made questionnaire to answer three specific questions. Question

1; level of customer awareness on Islamic banking products in Mogadishu, Somalia; 2 level

of adoption on Islamic banking products; 3 relationship between customer awareness and

adoption of Islamic banking products. Data analysis using frequencies, percentages and means

revealed that the more male participated in the study (62.5%) most of them have certificates

(47.3%) majority are bellow 30 years, and 52.8% worked as private sectors.

Findings reveal that more than half of the respondents already aware of that there is Islamic

banking system in Somalia, but they do not aware of the kind of the products offered by

Islamic banks. The study also found out that the rate of Somali community using or

adopting on Islamic banking products is very low.

Finally the results indicated a positive and significant relationship between the level of

awareness and adoption and level of Islamic banking products, (r-value~,585 and sig.000),

Thus the null hypothesis is rejected and the alternative hypothesis is accepted. This implies

that the increase of customer awareness were able to lead the height rate adaption of Islamic

products

The study recommended to Islamic banks in Mogadishu, Somalia to conduct free seminars on

raising awareness of the customers to Islamic products in public places such as universities

and mosques. this ultimately may result increasing number of users.

Finally The study concluded that if Islamic banks wanted to attract and retain customers and

remain relevant in the Somalia context, they should have to develop relevant marketing

strategies to meet customers’ needs.

vi

CHAPTER ONE

THE PROBLEM AND ITS SCOPE

1.0 Introduction

In this study, the researcher investigated customer awareness and adoption of Islamic

banking products in Mogadishu, Somali. this chapter consisted of background, the

problem statement, objectives, significance, scope, assumptions. and the lastly

definition of the terms.

1.1 Background

1.1.1 The Historical Background

According to Khir, and Shanmugarn (2008), Islamic banking was an abstract concept

until the first half of the twentieth century. However, it has now become a full-

fledged system and discipline. Islamic banking first gained its appearance in Egypt

at Mit Ghamr Savings Bank which offered interest free banking, by El Najjar in

1963, Karim & Affif (2005).

In the seventies, many political changes have taken place in the Muslim countries

which helps to facilitate the establishment of Islamic financial institutions. During

this time, some Islamic banks came into existence in the Middle East. Examples are

The Islamic Development Bank (1DB), the Dubai Islamic Bank (1975), the Faisal

Islamic Bank of Sudan (1977). the Faisal Islamic Bank of Egypt (1977), the Bahrain

Islamic Bank (1979). and the Philippine Amanah Bank (PAB) was set up in 1973,

operates two windows for deposit transactions in commercial and Islamic. Later,

Islamic banks and financial houses were established in Qatar, Sudan, Bahrain,

Indonesia, Guinea, Denmark, Turkey, England, Jordan and Switzerland. Now, it is

estimated that there are more than 250 Islamic banks operating in over 75 countries.

Even in non-Muslim majority nations like the UK, Australia, United States of

America, they are attempting to set up Islamic Financial Institutions, HBZ and the

Habib Bank (Saidi, 2007).

Khir et al. (2008) stated Islamic banking made its debut in Malaysia in 1983 with the

establishment of Bank Islam Malaysia Berhad (BIMB). The increase in Muslim

populations and awareness of Islamic values has led to greater demand for Islamic

bank interest-free products. Bank Islam Malaysia was established to meet these

demands and challenges. BIMB introduced and marketed a variety of interest free

products such as Qard Hassan. Mudarabah, Musharakah Istisna Ijarah, Salam. and

others. BIMB business has expanded over the years. From the seed capital of only

RM8O million initially, Bank Islam’s shareholder funds rose up to RM2.5 billion as

at December 2010. Now, BIMB had 117 branches and more than 1000 self-service

terminals all over the Malaysia.

In Africa, Especially south Africa Muslims estimated currently about 1 million

Muslims. while in 1970 thcre were only about 270,000 (History of Muslims in South

Africa, 2007). Muslims of Malay origin are found mainly in the Western Cape, while

those of Indian origin are resident mainly in Kwazulu-Natal, Gauteng and

Mpurnalanga. Formalised Islamic banking, finance and investment products in South

Africa are in their infancy, having been established in 1989. islamic banks that offer

products according to Shariah law include the Albaraka Bank and Oasis Asset

Management (Said 2007).

On the other hand non-Islamic banks like Wesbank has established an Islamic

subsidiary known as the Islamic Finance Bank, while ABSA and the FNB have

opened Islamic banking departments. The fully-fledged Islamic banks operating in

South Africa are Albaraka bank, SRIVATSA (2008). The Albaraka Bank pioneered

Islamic banking and finance in South Africa in 1989 in response to the need for a

system of banking in line with Islamic economic principles. Albaraka offers only

Shariah compliant products and services. The head office is situated in Durban, with

branches in Durban, Cape Town, Johannesburg and Pretoria. Products and services

offered to Muslims and non-Muslims include residential property, motor vehicle,

trade, savings, investment accounts, equity participation accounts, equity share

portfolio funds and estate planning fInance, SAIDI (2007).

In addition, In 2004, WesBank, in partnership with Pure Capital, began offering a

Shariah-compliant vehicle finance product in response to consumers wishing to

finance vehicles in a manner which is compliant with Shariah Law SAIDI (2007).

1.1.2 Theoretical Background

Diffusion Innovation adoption theory was based on this study. This theory was

developed by Regrose (1973), cited from journal of information technology (2009).

This theory stated a certain percentage of the population will readily adopt the

innovation, while others will be less likely to adopt, through which an individual or

other decision making unit passes from knowledge of a innovation, to forming

attitude towards the innovation, to decision to adopt or reject, to implement the new

idea, and to conformation of this decision, Fliegel & Kivlin (1966).

1.1.3 Conceptual Background

According to Rogers (1962), innovation-adoption model defines that awareness is

the stage when an individual is exposed to innovation but lacks of complete

information about it, The individual is interested in the new idea and seeks more

information about it, Fliegel & Kivlin(1966), Customer awareness refers to the

strength of a product or services’ presence in the consumer’s mind, (Aaker 1996).

Zink (2006) defined customer awareness as a measure of the percentage that target

market aware of the product/service. Marketers can create awareness among their

target audience through repetitive advertising and publicity.

While, adoption is the acceptance and continued use of a product, service or idea.

Consumers go through “a process of knowledge, persuasion, and confirmation”

before they ready to adopt a product or service (Regress and Shoemaker 1971).

Islamic banking is interest free asset backed banking governed by the principles of

Islamic shariah (Gerrard and Cunningham. 1997). According to Khan (20101)

islamic banking product is product that an Islamic bank offers like Murabaha,

Mudaraba, Musharika, Ijara. Istisna, salam, saving account, and wakalah. kafalah

and others.

1.1.4 Contextual Background

Islamic banks in Somalia are part Islamic banks Systems that operate in many other

part of the developed and developing country. The banking sector in Somalia

currently comprises of an active informal sector and virtually non-existent formal

sector. The private sector banks dominate the informal sector, whereas the formal

banking sector includes central banks in Mogadishu (southern Somalia), Hargeisa

(Somaliland) and Bosasso (Puntland).

Although these central banks are either dysfunctional (Bank of Somaliland and State

Bank of Puntland) or defunct (the central bank in Southern Somalia). Islamic banks

in Mogadishu, Somali, currently operate more than five years by offer different

moods of investment as Murabaha, Musharaka, mudaraba, Istisnaa, but it is a limited

scheme, Islamic bankers’ goal was to dominate in entirely market or in whole

country this finally result growth and development of Islamic banking system in

Somali.lo

therefore they employ managers who facilitate and implement a determine goals, in

order to achieve the growth and development of lBS. so it needed to create strong

awareness in Somalis communities about merits of Islamic banking system by

putting needed awareness in market or whole country, and fulfill expected or

targeted awareness towards using of Islamic banking products on Muslim society in

Mogadishu, Somalia.

1.2 Statement of problem

Statistically, there is research done that shows usage of Islamic banks are increasing

over the years, so the users are made up from Muslim and non- Muslims on the

world. However, the usage of conventional banks is still higher than Islamic banks’

usage by Saduman Okumus in (2005). From this statistic, it is very obvious that the

gap between conventional banks and Islamic banks arc very huge as the difference in

number of users. In Somalia. Islamic banks users still have not adopt or might not

even aware Islamic banking products.

This could be seen in the numerous indicators; most of customers were confuse

some concepts of Islamic banking products, were self-distrust with using Islamic

banking products, on anther hand individual customers has questioned about the

products of Islamic banking, moreover there is great misinform entirely population

regarding for Islamic banking products, these issues final result; Islamic Banking has

become stagnant because they have failed to offer their products to the public.

Lack of awareness on products could bring Islamic banking are still widely

unaccepted, its believed that customers are still not fully confident with using

Islamic products, in addition customer are afraid to use Islamic products through

investment because they think that any mistake or error could mean a loss of money.

Poor understanding or perception or awareness on Islamic banking products will

influence Islamic bank systems by decreasing or not improving number of usages,

this will be opportunity for interest based banks by introducing new conventional

bank.

In Somalia, people are 100% muslims and islam dosen,t allow using interst rate

while the conventional banks are almost based on using interest rates. However,

there are some Islamic banks in Somalia such as Salam Somali Bank and Dahabshiil

those claim in providing Islamic products. In the light of this. the study intends to

I:

investigate customer awareness and adaption of Islamic banking product and service

in Mogadishu Somalia.

1.3 Purpose of the study

The purpose of this study was to establish the relationship between consumer

awareness and adoption of Islamic banking products in Mogadishu Somalia.

1.4 Specific objectives

1) To determine the level awareness of Islamic banking products in term of:

1.1. Understanding

1.2. Perception

1.3. Attitude

2) To examine the level of adoption on Islamic Banking products in terms of:

1.1. Early adaptors

1.2. Late adopters

1.3. Laggard

3) To find out if there is a significant relationship between customer awareness

and adoption of Islamic banking product.

1 .5 Research Question

1) What is level of awareness on Islamic Bank’s products according to:

1.1. Understand?

1.2. Perception?

1.3. Attitude?

2) What is level of Adoption on Islamic bank’s products in term of:

1.4. Early adaptors

1.5. Late adopters

1.6. Laggard

Is there is a significant relationship between customer awareness and adoption of

Islamic banking product.

1.6 HYPOTHESIS

HO: There is no significant relationship between customer awareness and adoption

of Islamic banking products of in Mogadishu. Somalia.

1.7 Significance of study

The findings of this study were useful to the following groups of people:

Managers of Islamic bank: these managers will get to know the importance of

customer awareness to their products, and how to attract target customers by

positioning such offerings in their minds. So the study will help managers to take

good Islamic investment related decisions.

Small and medium enterprises: the study will benefit for SMEs in Mogadishu by

understand the importance of applying Islamic product in their business, and also

will be chance to getting different types of mode of financing on their business

offered by Islamic banking.

Researchers and students: the study provides future researchers with an

alternative summary measure. The result of this study also served as a data base for

further researchers and students in this field of research.

Readers: Either Muslims or non-Muslims will benefit from the study. They will get

baseline understanding of how Islamic banks make investments.

1.8 Scope of the study

1.8.1 Geographical scope

The conducted in some selected banks in Mogadishu, Somalia Especially two

districts namely Hamarweine and Howl-wadag. The area was selected because the

headquarters of Islamic Banks are built there, and also it is the central of economic

activities in south and central Somalia.

1.8.2 Content Scope

The variables to be examined in this study include customer awareness which was

broken in to customer understanding, perception, and attitude, of product. The other

variable (DV) adoption of Islamic banking product. which was broken in to early

adaptors, late adopter and laggards. Other variables to be included in the study are:

demographic characteristics of the respondents which included age. gender,

education level, and work experience.

1.8.3 Theoretical scope

This study was based innovation adoption theory. This theory was developed by

Rogers (1973), cited from journal of information technology (2011). This theory

states in general that successful adoption of a particular innovation should score

higher in terms of its relative advantage over existing practices, compatibility to

users’ needs, trialability and observability, and lower in its complexity to use, Fliegel

& Kivlin,(1966)

1.8.4 Time scope

The time bound of this study was six months starting from February 2014 up to

October 2014.

1.9 Operational definitions of key terms

Since the purpose of this study is to examine the awareness, and adoption of Islamic

banking products in Mogadishu, the following terms are defined as they are used in

the study:

Islamic baking: Islamic banking is banking based on Islamic law (Shariah). It

follows the Shariah, called fiqh muamalat (Islamic rules on transactions). The rules

and practices of fiqh muamalat came from the Quran and the Sunnah, and other

secondary sources of Islamic law such as opinions collectively agreed among

Shariah scholars (ijma’), analogy (qiyas) and personal reasoning (ijtihad).

Customer awareness: is refers to the strength of a product or services’ presence in

the consumer’s mind.

Islamic banking product: is product that an Islamic bank offers like Murabaha,

Mudaraba, Musharika, Ijara, Istisna, salam, saving account, and wakalah, kafalah

others.

Murabaha : is a contract wherein the Islamic bank, upon request by the customer,

purchases the asset from a third party supplier/vendor and resells it to the customer

either against immediate payment or on a deferred payment basis i.e. Cost plus

finance

Mudaraba : is a profit sharing partnership agreement in which the investor (the

Rab-ul-mal) provides the necessary finance, while the recipient of the funds(the

Mudarib or the manager) provides the professional, managerial and technical know-

how towards carrying out the venture, trade or service with an aim of earning profit.

musharika: This is a type of partnership between the Bank and the customer

whereby each party contributes to the capital of the partnership in equal or varying

proportions either to establish a new venture or share in an existing one

Ijarah (leasing): An arrangement in which bank purchases the equipment or

property selected by the customer and then leases it to the customer on

predetermined fixed rate , as agreed by both parties.

walkalah: Wakalah is the transfer of authority from one party (muwakkil) to other

party (wakil) in relation with transferable matters.

kafalah: Guarantee transaction provided by insurer (kafil) to a third party or insured

(makful lahu) to fulfill the obligation of the second party (rnakful ‘anhu/ashil).

CHAPTER TWO: LITERATURE REVIEW

2.0 Introduction

This chapter reviews the literature about the customer awareness and adoption of

Islamic banking product. The chapter was organized into three main sections. The

first section addresses relevant theory of study. while the second section discuss on

conceptual framework, The last section highlights literature review and prior studies

related to this study and gap of the study.

2.1 THERETICAL REVIEW

Sequence of events that people exceed from early level of knowledge regarding a

service. product. or innovation to achieve positive or unfavorable attitude about it to

make choice whether adopt or reject, Diffusion Innovation adoption theory will be

based on this study. This theory was eveloped by Regrose (1973), cited from journal

of information technology (2009). This theory is a popular model used in explaining

user adoption of new technology, product. service and idea. He defines diffusion as

“the process by which in innovation is communicated through certain channels over

time among the member of social society”. He also defines innovation broadly as

“an idea, practice, or object that is perceived as new by an individual or other unit of

adoption” Fliegel & Kivlin (1966).

therefore potential adopters can evaluate based on innovation attributes such as

Relative advantage (is the degree to which consumers perceive new product or

service as different from and better than substitutes); compatibility (is the extent to

which a new product or service is consistence with consumers’ need, beliefs, value,

experience); complexity (difficulty of understanding and use); observability( is the

extent to which an innovation is visible and communicable to consumers),

trialability( refers to the ability of consumers to experiment with new innovation and

evaluate its benefits). Burkrnan (1987).

Furthermore, In general, the adoption process has been defined as the process

through which individual adopters pass from awareness to full acceptance of a new

innovation (Rogers 1999; 2003). According to Roger there are two levels to

adoption. Initially, innovation must be purchased, acquired and adopted by

individuals or organizations. Subsequently, it must be either accepted or rejected by,

Burkman (1987).

The ultimate users in the society or community. The relative newness of these

innovations and the associated uncertainty is what differentiates innovation adoption

decisions from other types of decision making (Gerard et al., 2003).

Thus, the diffusion literature provides an ideal framework to be applied to the

present study which, seeks to extend the research area in a product innovation

context, the innovation being Islamic banking. The study would determine the

relationship between consumer awareness and adoption of Islamic banking products

in Mogadishu Somalia, Fliegel, & Kivlin, (1966).

Therefore the dependent and independent variable of this research is based the

theory of Diffusion of Innovation model (Rogers, 2003), Fliegel& Kivlin (1966).

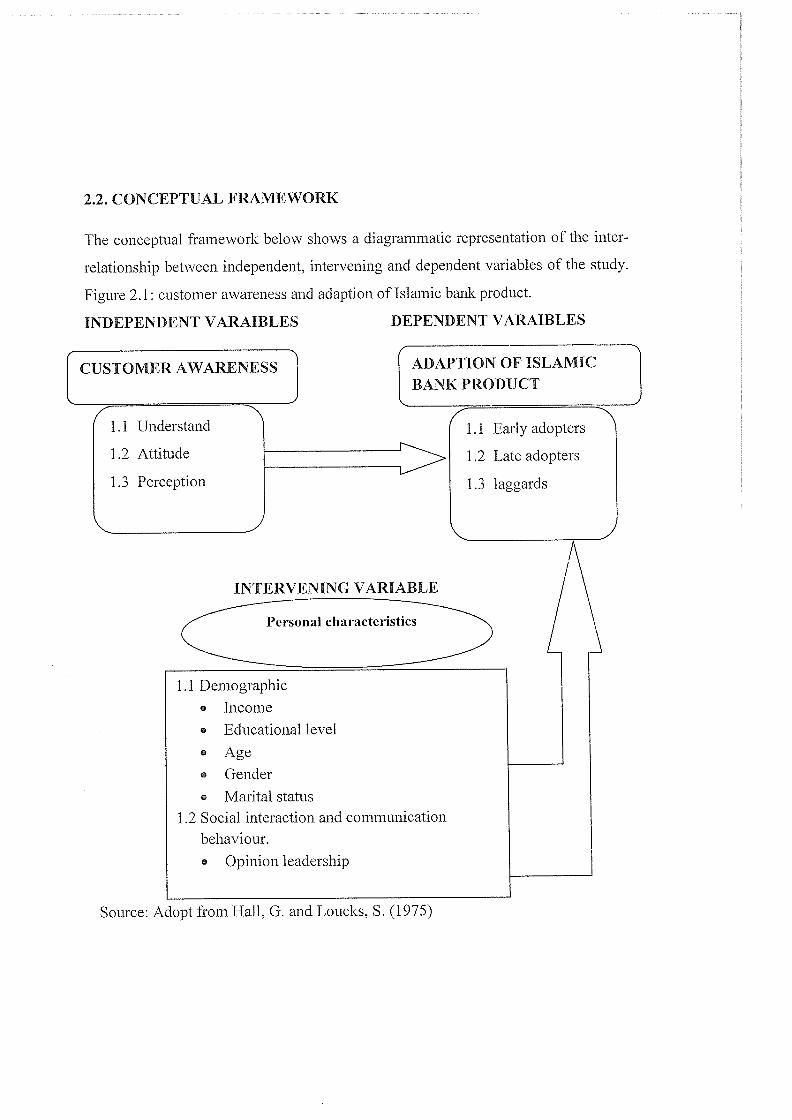

2.2. CONCEPTUAL FRAMEWORK

The conceptual framework below shows a diagrammatic representation of the inter

relationship between independent, intervening and dependent variables of the study.

Figure 2.1: customer awareness and adaption of Islamic bank product.

INDEPENDENT VARAIBLES DEPENDENT VARAIBLES

I CUSTOMER AWARENESS ADAPTION OF ISLAMIC

L J BANK PRODUCT

1.1 Understand 1.1 Early adopters

1.2 Attitude 1.2 Late adopters

1.3 Perception 1.3 laggards

INTERVENING VARIABLE

~~sona1cIiaracteiistics

1.1 Demographico Incomeo Educational levelo Ageo Gendero Marital status

1.2 Social interaction and communicationbehaviour.o Opinion leadership

Source: Adopt from Hall, G. and Loucks, S. (1975)

Figure 2.2 indicate

The conceptual framework above is derived from the views Fliegel & Kivlin (1966)

and attempts to explain the relationship that exists between the dependent,

independent, extraneous or intervening variables that all put together, create an

impact on adaption of Islamic bank products in any given Islamic banking industry.

Considering all the variables mentioned, it is the dependent variable (customer~

adaption of 1BPs) that was of the primary interest for this study.

The framework shows that three sub themes of independent variables (understand,

attitude, and perception) are used in an attempt to investigate deeply the extent to

which they can create an effect on customer~ adaption). In addition, these three sub

themes are used as a basis for the questionnaire. From the framework, the researcher

believes that customer~ adaption can be affected by the independent variables, which

can lead to either poor awareness or good awareness. It is important to note that

when rate of adaption on Islamic banking products dissatisfaction, he/she may

respond to the imbalance by opting for a number of actions that may lead to low

adaption and hence failure to achieve Islamic banks goals and objectives.

It is also indicated in the framework, that the extraneous variable had the potential to

influence custorners~ adaption. For instance, if customer may have high income

level, education level, in addition good opinion leadership, and social character to

him or her and hence a hope for better adaption. However, whenever one of the

extraneous variables intercept in between the independent an dependent variables (as

shown in the frame work), the custorner~ adaption is likely to be affected positively

or negatively.

2.3 Review the Related Literature

2.3.1 Concept of customer awarenessAccording to Zink (2006), defined Awareness as a prerequisite for action. Customer

awareness refers to the strength of a product or services’ presence in the consumer’s

mind. Aaker, (1996,) defined customer awareness as a measure of the percentage

that target market aware of the product/service. Marketers can create awareness

among their target audience through repetitive advertising and publicity. Stryfom

(1995) Customer awareness can provide a host of competitive advantage for

business organizations.

Aaker (1996).Customer awareness of the products and services is an asset that can

be durable and thus sustainable. Organizations can generate brand awareness by,

firstly having a broad sales base, and secondly becoming skilled at operating outside

the normal media channels. Customers first recognize the products or services

offered by the organization, and then they recall it back in their minds by seeing the

benefits of such products or services. Aaker (1996).

Customer awareness is also a challenge before the banks. Bank can market their

products and services by giving the proper knowledge about the product to

customers or by awarding the customer about the products. Bank should literate the

customers, (Sasanee, 20G4).

2.3.2 Concept of adoption on Islamic banking productIslamic banking is based upon the principle that the use of Riba (interest) is

prohibited. This prohibition is based upon Sharia ruling. Since Muslims cannot

receive or pay interest, they are unable to conduct business with conventional banks

(Gerrard and Cunningham, 1997). To service this niche market, Islamic financial

institutions have developed a range of halal3 interest-free financing instruments that

conform to Sharia ruling, and therefore are acceptable to their clients (Malaysian

Business, Dec. 16, 2001).

Despite the prohibition of interest by four of the world’s major religions (Judaism,

Christianity, Hinduism, and Islam), today’s international economic system is based

on interest. However efforts are going on to replace the conventional interest-based

banking system with the interest free banking and finance. Apart from religious

dimension, the case against interest has been examined by many researchers (Aziz.

2011).

It is estimated that there are about 1.8 billion Muslims in the world and, after

Christianity, Islam is the next largest religion. Islam is the predominant religion in

the Middle East and parts of Asia, Africa and in countries such as Turkey, Iran, Iraq,

Egypt, Nigeria, Indonesia, India, Pakistan and Bangladesh. In Iran, Pakistan and

Sudan. only Islamic banking is allowed (Chong & Liu, 2008).

Apart from these areas, there are migrant Muslims all over the world, including

South Africa and the United States of America. Owing to the presence of Muslims,

international banks such as Citibank have created wings to cater for Muslim clients,

offering diverse products, mainly financing businesses (Citibank, 2009). Bank offers

Islamic financing services which are Shariah compliant, and provides construction

and home loan financing following Murabuhaguidance (Devon Bank, 2009). Islamic

banks have enjoyed phenomenal growth, from an asset base of barely US$ 1 billion

in 1975 and fewer than 10 Islamic banks (Martin, 1997).

There are more than 180 Islamic banks and financial institutions operating more than

8000 branches in different countries in Asia, Africa, the Middle East, Europe and

North America. It is expected that by 2010 Islamic Banks and financial institutions

will comprise 50 per cent-60 per cent of the total private savings of Muslims

worldwide (Gainor, 1999).

Islamic banking has been defined as banking in consonance with the ethos and value

system of Islam and governed, in addition to the conventional good governance and

risk management rules, by the principles laid down by Islamic Shariah. Interest free

banking is a narrow concept denoting a number of banking instruments or

operations, which avoid interest. Islamic banking, the more general term is expected

not only to avoid interest-based transactions, prohibited in the Islamic Shariah, but

also to avoid unethical practices and participate actively in achieving the goals and

objectives of an Islamic economy (Khir et al, 2008).

While another author defined Islamic bank refers to banking system that is based on

the principles of Islamic law and guided by Islamic economics, which strives sharing

profits and interest-free business transactions, (Karim & Affif~ 2005).

2.3.3 Contracts in Islamic Banking

Islamic Banking Institutions are offering a wide range of shariah Compliant products

& services with objective of satisfying different types of financial and investment

needs of their individual and institutional customers by based on contracts. Contracts

can be classified into three board categories which are trading contracts,

participation contracts and supporting contracts (Khir et al, 2008).

2.3.4 Trading Contracts

Trading contract is a sale contract where it can be sale for goods, cash and debt.

These contracts are based on the principle of buying and selling of assets (Khir et al.,

2008). The most common trading contracts in the Islamic banks are following:

1. Murabahah (cost-plus sale): A sale on mutually agreed profit. Khan (2010)

stated that it is a sale contract in which client requests the bank to purchase an item

for his or her from third party. Bank resells it to the client on the cost plus profit

basis once bank receive it. Awareness of Islamic Banking Products and Services

among Non-Muslims in Malaysia

2. Bai Bithaman Ajil (deferred payment sale): Sale of goods on a deferred

payment basis at a price that includes a profit margin agreed upon by both buyer and

seller (Khir et al., 2008).

3. Bai Dayn (sale on debt): Refers to debt financing such as provision of financial

resources required for production, commerce and services It can be traded only the

documents have proven that the real debts arising from bona fide merchant

transactions (Khir et aL, 2008).

4. Bai Inah: According to Khan (2010) it is a contract of selling an asset by the bank

to the customer through deferred payment and repurchases the asset by the bank

from the customer on cash terms at a later date.

5. Ijarah (leasing): An arrangement in which bank purchases the equipment or

property selected by the customer and then leases it to the customer on

predetermined fixed rate , as agreed by both parties ~Nanava, 2007).

6. Ijarah Thumma Bai (leasing followed by purchase): A simple leasing for the

leasing period with an option for the leasee to purchase the property at the end of the

leasing period through a contract of purchase (Bley and Kuehn’s, 2004).

7. Bai Salam (future delivery): A contract where payment is made in advance for a

good to be delivered in the future (Khir et al., 2008).

8. Istina (sale by order): A buyer orders an item for the manufacture based on

period, criteria, terms and conditions earlier agreed. Buyer (customer) can make the

payment in installments to the seller (bank) when the goods have been received. At

the time of contract, the item does not exist (Khir ci’ al., 2008). Awareness of Islamic

Banking Products and Services among Non-Muslims in Malaysia

9. Sukuk (bond): As Nanava (2007) stated sukuk are new development Islamic

financial product on a market, there is increasingly high demand on an innovation.

Besides, Sukuk are asset-backed securities and comply with the Syariah principles.

They issued bonds to raise, funds and these funds are invested in a project. After

that, income from a project is distributed to the holder of the bonds.

2.3.5 Participation Contracts

Islam encourages equity based participation where focus is on profit and loss

sharing. Banks and lenders become partners in business instead of becoming

creditors by investing their money. The objective is the risky investments provide

motivation to the economy and encourages entrepreneurs to maximize their efforts.

The most common participation contracts in the Islamic banks are following (Khir el

al., 2008).

Musyarakah: Musyarakah is a contract of equity participation which used to

finance medium and long-term investment. Two or more parties entered into the

contract and form a joint venture. Each of the parties contributes capital and

participates in the management of project. Profit is shared according to the

proportion of shares or according to the agreement in fraction, ratio or percentage.

The loss should born by all partners according to proportion of shares. The profit and

loss are cannot be shared in absolute amount (Khir ci al., 2008).

Mudharabah: Mudharabah is a trustee finance contract or passive partnership and

providing only profit sharing. The profit does not have predetermined profit since

the deposit is guaranteed that there is no risk of loss. In this transaction, one party

(bank) provides capital and other party (entrepreneur) offers labour and expertise.

Profit from the project is shared between both parties on a pre-agreed basis. While,

the loss is borne by the owner(s) of capital only; the liability of entrepreneur is

limited to their time and effort (Khan, 2010).

2.3.6 Supporting Contracts

There are other contracts that support and facilitate trading and mobilisation of

deposits which compliance with the Syariah principles. The most common

supporting contracts in the Islamic banks are following:

1. Rahnu (mortgages): An agreement whereby a valuable asset is collateralized for

debt (Khir eta!., 2008).

2. Kafalah (guarantee): A contract of guarantee by the contracting parties. Third

party becomes the guarantor of the debtor for the payment of debt (Khir et a!., 2008).

Third party assures that the debtor will repay the debt to the creditor.

3. Wakalah (Agency): a person assigns someone else to carry out a certain task on

his or her behalf usually will charge certain fee ((Khir et a!., 2008).

4. Qardh Hassan (benevolent loan): Refers to a zero- interest loan in which there is

no interest charge for the loan (Khan, 2010). The borrower only required to repay the

principle amount borrowed from the lender.

5. Wadiah Yad Dhamanah (savings with guarantee): Refers to goods or deposits,

which have been deposited with another person, for safe-keeping (Khir el a!., 2008).

The custodian is permitted to use the deposited amount for trading and investment.

The profit derived from utilizing the deposits is distributed to the custodian only.

The five essential principles on which Islamic banking is based consist of:

~ Prohibition on Interest (nba)

D Prohibition of Uncertainty (gharar)

ü Prohibition on Speculation or gambling (maisir)

El Restriction on activities/commodities e.g. Alcohol, Arms and Ammunition and

Pork

El Profit and loss sharing mechanism

OBJECTIYES OF ISAMIC BANK

1) Maximizing profits (good percentage of return to investors): The objective of

Islamic banks is to maximize profits with safe investments. Most of the

participants agreed that as far as the profit is interest free, they want the

banks to earn them maximum profits but those profit should be nba free.

2) Helping in alleviating poverty (poverty eradication):49 % of sample agreed

that since Shariah based business will help in betterment of economy in long

run, but this will take some time.

3) Providing employment opportunities: 55% of the participants agreed that

new system has not only offered new products to customers, but also created

new jobs in labor market through new branches for Islamic banking.

4) Minimizing cost of operations: Participants established that Islamic banking

has to reduce the cost since they are offering products with profit and loss

basis making sure that they look for loopholes in their control systems.

2.4 Related Studies

‘Latch, and Arrifin (2009), Khattak and Rehman (2010), Okumus (2005), Khan and

Syahid (2008) have similar results in their studies. Latch et al. (2009) have

conducted a research in Thailand that examining the perception of the customers

towards the objectives, characteristics and criteria of Islamic bank. In their study, it

was found that most of the Thailand customers were aware of the special

characteristics of Islamic banking system and they are different from the

conventional banking system, and also, they have little awareness about the Islamic

banking products and services.

A study was conducted by Kamal, Ahmed and Al-Khatib in (1999). They tried to get

the degree of awareness of the customers towards the lBS products. They had taken

a sample of 90 respondents and come to the conclusion that most of the customers

have a little bit knowledge about the specific products such as Mudarabah and

Murabaha. But most of them do not use these products (Naser et al., 1999).

According to study conduct by Khattak and Reharnan (2010) and Okumus (2005)

where they investigated customer’ s awareness level towards Islamic banking

products in Pakistan and Turkey, they found out that there is good in some of the

general products like current accounts and time deposit account. However, for some

of the Islamic financial products such as Murabahah and I!arah. most of the

customers are unaware of them.

Another study was conducted in (2005) by Saduman on the platform of Turkey. This

study basically covered the theoretical and practical aspect of the Turkish Islamic

banking sector. With the sample of 110 respondents this study tried to know about

the awareness and satisfaction of the Islamic banking customers towards the Islamic

banking system. They came to the conclusion that numbers of customers are aware

with few specific products like Musharakah and Mudarabah. But most of them were

not enrolled in the dealing of these products (Saduman, 2005).

And also study carried in Bangladesh by Khan et al (2004). interested in examining

the awareness and usage of various Islamic bank products and services among

Islamic bank customers in Bangladesh. Their results show that there is a high level

of customer awareness of some general products such as current account and saving

account.

While a study was conducted by Gerrard and Cunningham (1997), where they

investigated the awareness of the Singapore customer towards the Islamic banking

products and its different services. They determined that there is a general lack of

awareness of the customer regarding the lBS (Gerrard and Cunningham, 1997).

In addition, According to Thambiah, and Arumugam (2011), conducted in Malaysia

stated as Islamic banking terms such as —Mudarabahll, —Bai’ Bithman AjilII, and

—Ba InahN are appeared to be less popular among the banking customers. The

reason for low awareness and Adoption for individual borrowing products might due

to Islamic banking products are named in Arabic terms.

On the other hand, Rammal and Zurbruegg (2006) intended to examine the

awareness of Muslim Australians of Islamic banking. especially the demand for

profit-and-loss sharing agreements. Their results show that generally there is a lack

of awareness in regards to the basic rules and principles of Islamic financing. The

results also indicate that a number of respondents would not take up halal financing

options if credit facilities were taken away.

Rammal and Zurbruegg’s (2006) results are supported by Thambiah el. al. (2011)

study which analyse the awareness on Islamic retail banking (IRB), between the

urban and rural banking customers in Malaysia and their findings also show that

generally there is a lack of awareness on IRB between the urban and rural banking

customers.

Furthermore, a study on Malaysia corporate customers revealed that providers of

Islamic banking products and services have not done enough in educating customers

and marketing their products. As an example, more than 65 percent of the

respondents indicated they had limited knowledge in Islamic banking system. Loo’s

(2010) study in Malaysia shows that the non Muslims still could not understand the

concept of Islamic banking even though there are a lot of advertising campaigns that

targeted at them. However, for Muslims, 82% of them agree that they understand the

concept of Islamic banking.

On the other hand view study like a study conducted by Latch et al. (2009) that

examining the perception of the customers towards the objectives, characteristics

and criteria of selecting Islamic bank, it was revealed that Thai customers perceived

that there are no differences between the Islamic bank and the conventional bank

products and services, except in the names used to highlight the Islamic Banking

products.

A study was conducted in (1989) by Erol and El-Bdour on Jordan customers. They

tried to find the attitude of Jordanian people towards interest free banking.

Ultimately they got that religion is not the main factor for the selection of financial

institution, but in fact there are some other factors too which are influencing the

decision criteria of the customers and in this regard the main factor is the level of

profitability, that is, returns on their investment ( Erol and E1-Bdour, 1989).

A study was conducted in (1998) by Metawa and Almossawi on the Bahrain

customers. They investigated the customer’s attitude by taking a sample of 90

customers. They got to the point that there were two main factors involved: “1.

Adherence to the Islamic principle, 2. and return rate” (Metawa and Almossawi,

1998). A study was conducted by Hegazy on the Egypt customer’s attitude in (1995).

He targeted the customersof Islamic bank. Finding of his study were that most

customers chose banks due to a combination of religious and better return, their

efficiency and speed of delivering banking services. (Hegazy, 1995).

However, based on these prior studies and arguments in many different countries,

they agreed mostly that Islamic banking product and service is very important issue

in society and economic.

although there are less prior studies carried out in Somalia that addresses the

customer awareness and adoption of Islamic banking product, so there is a need to

study upon this issue. So that this study will attempt to investigate customer

awareness and adoption of Islamic banking product.

CHAPTER THREE: METHODOLOGY

3.0 Introduction

This chapter consisted of design, population, sampling strategies, data collection

methods, data collection instruments, data quality control, procedure and data

analysis.

3.1 Research Design

Since the purpose of this study is to examine the relationship between customer

awareness and adoption of Islamic banking products in Mogadishu, Somalia,

therefore this study was employed descriptive design specifically descriptive

correlational. Both qualitative and quantitative data was collected by use of this

design.

3.2 Target Population

The target population employed in this study was included 150 customers from two

different Islamic banks in Mogadishu. SALAAM SOMALI BANK (SSB),

DAHABSHIIL INTERNATIONAL BANK (DTB). Since they are the basic banks

and practice Islamic banking system and offer Islamic banking products, therefore it

is considered appropriate for the focal point of this study.

The total population of the study was 150 customers, Computed (Using Slovens’

Formula) sample size are 109.

3.3 Sample size

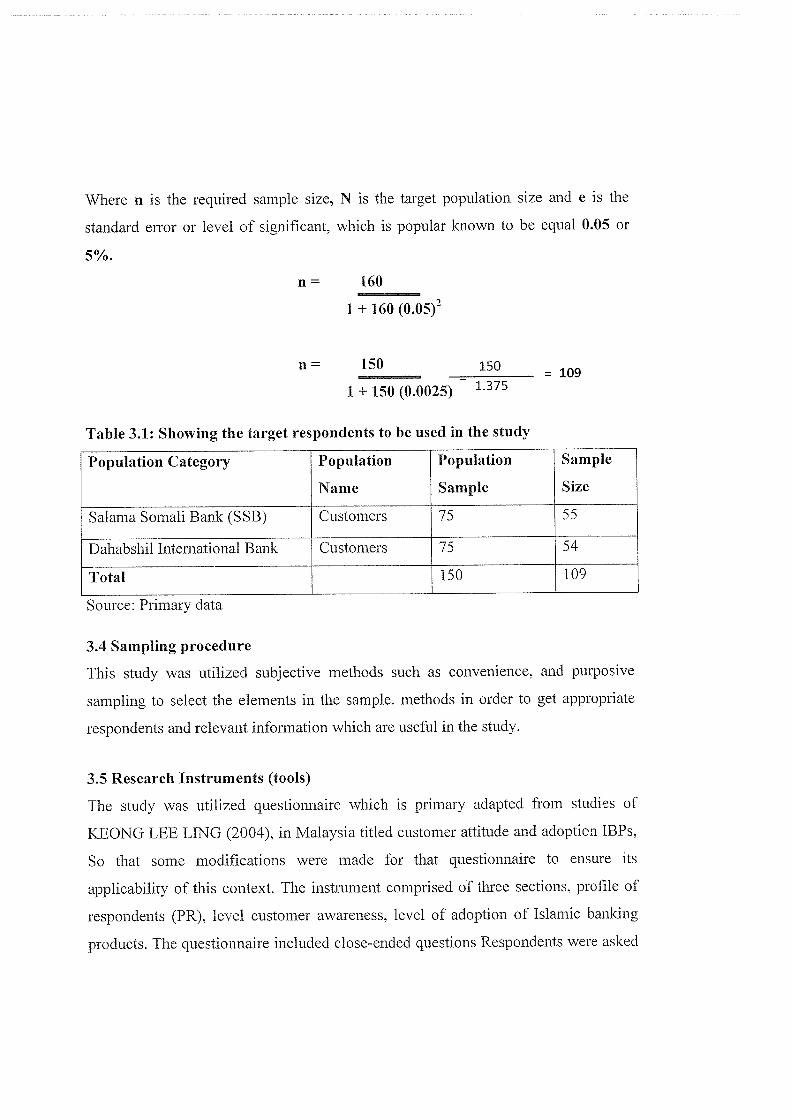

A total of 109 subjects were selected using The Sloven’s formula to determine the

minimum sample size. Table 1 above shows the respondents of the study with the

following categories.

n= N

1 + N (e2)

Where n is the required sample size, N is the target population size and e is the

standard error or level of significant, which is popular known to be equal 0.05 or

5%.

160

1 + 160 (0.05)2

n= 150 —_150 = 109

1 + 150 (0.0025) 1.375

Table 3.1: Showing the target respondents to be used in the study

Population Category Population Population Sample

Name Sample Size

Salarna Somali Bank (SSB) Customers 75 55

Dahabshil International Bank Customers 75 54

Total 150 109

Source: Primary data

3.4 Sampling procedure

This study was utilized subjective methods such as convenience, and purposive

sampling to select the elements in the sample. methods in order to get appropriate

respondents and relevant information which are useful in the study.

3.5 Research Instruments (tools)

The study was utilized questionnaire which is primary adapted from studies of

KEONG LEE LING (2004), in Malaysia titled customer attitude and adoption 1BPs.

So that some modifications were made for that questionnaire to ensure its

applicability of this context. The instrument comprised of three sections, profile of

respondents (PR), level customer awareness, level of adoption of Islamic banking

products. The questionnaire included close-ended questions Respondents were asked

if costumer awareness have relation to adoption of Islamic banking products. This

method was selected because it was easy to administer questionnaires, it saved time

and it was helped to collect information that is applicable to the study.

In addition the study used an interview. The interview guide was designed to obtain

in-depth information from key respondents. Interviewees were probed and

information obtained helped supplement data from questionnaires. Interviews helped

to test for areas hard to investigate by the use of the questionnaire approach.

Interviews further helped test for variations in responses as suggested by Amin

(2005).

3.6 Validity and reliability of the instruments

One important aspect that is worth to be considered when selecting research design

is validity and reliability. Thus the study should have to be aware of to threats of

reliability and validity of the result in this study. Easter-smith et al. (2002) defined

reliability as the extent to which data collection techniques will yield consistent

findings. To increase reliability, the study adapted relevant instruments which were

slightly modified. While Validity refers to the extent to which data collection

method accurately measures what it was intended to measure or to the extent to

which research findings are about what they are claimed to be about (Saunders et al.,

2009).

To ensure the validity of the instruments, the instruments approved by the

supervisor, Moreover, the questionnaire and interview was pre-tesied to two

individuals before being taken to the field in order to evaluate the relevance of each

item in the instruments to the purpose of this study. So the next section pointed out

the procedure of data collection. In validity content concerned with a test’s ability to

include or represent all of the content of a particular construct, is assessed by

overview of the items by trained individuals taking CVI above 0.70 as accepted for

social sciences (Amin, 2005).

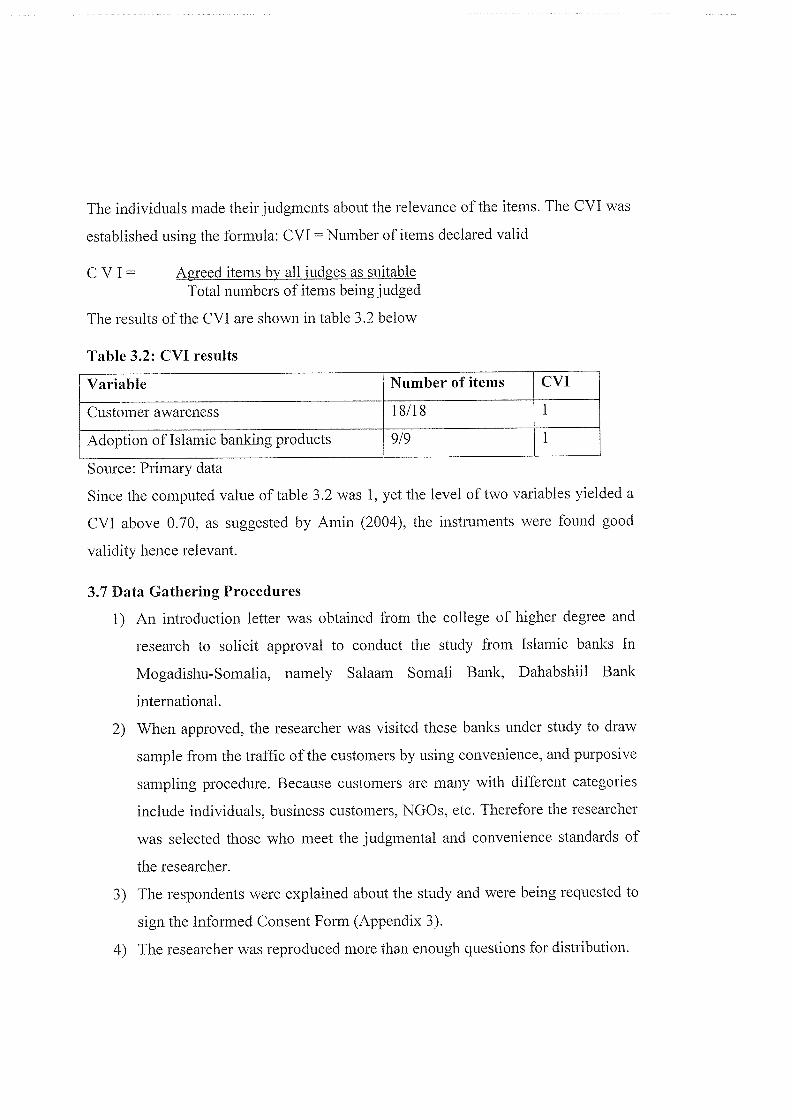

The individuals made their judgments about the relevance of the items. The CVI was

established using the formula: CVI = Number of items declared valid

C V I = Agreed items by all judges as suitableTotal numbers of items being judged

The results of the CVI are shown in table 3.2 below

Table 3.2: CVI results

Variable Number of items CVI

Customer awareness 1 8/18 1

Adoption of Islamic banking products 9/9 1

Source: Primary data

Since the computed value of table 3.2 was 1, yet the level of two variables yielded a

CVI above 0.70, as suggested by Amin (2004), the instruments were found good

validity hence relevant.

3.7 Data Gathering Procedures

1) An introduction letter was obtained from the college of higher degree and

research to solicit approval to conduct the study from Islamic banks In

Mogadishu-Somalia, namely Salaam Somali Bank, Dahabshiil Bank

international.

2) When approved, the researcher was visited these banks under study to draw

sample from the traffic of the customers by using convenience, and purposive

sampling procedure. Because customers are many with different categories

include individuals, business customers, NGOs, etc. Therefore the researcher

was selected those who meet the judgmental and convenience standards of

the researcher.

3) The respondents were explained about the study and were being requested to

sign the Informed Consent Form (Appendix 3).

4) The researcher was reproduced more than enough questions for distribution.

5) Research assistants were selected to assist the researcher in the data

collection; brief and orient them in order to be consistent in administering the

questionnaires and interview.

During the Administration of the Questionnaires

1) The respondents were being requested to answer completely and not to leave

any part of the questionnaires unanswered and interview.

2) The researcher and assistants was emphasized retrieval of the questionnaires

and interview within five days from the date of distribution.

3) On retrieval, all returned questionnaires and interview was checked if all are

answered.

After the Administration of the instruments

After the receiving the instruments back in a time, the researcher was checked the

completeness of all answers that whether the respondents answered the entire

questionnaire and interview. After checked the researcher was arranged the data and

edit the data for the errors and completeness of whether the respondents have left

unfulfihling questionnaires.

18 Data Analysis

After receiving the questionnaire back, the researcher was, encode the data into the

computer and statistically treated using the Statistical Package for Social Sciences

(SPSS), while Qualitative data was prepared by use of code sheets which captured

relative data on the study variables and after this, both inferential and descriptive

statistics helped the researcher to ascertain the level of deviation of variances of

opinions as such interpretations were addressed in chapter four.

3.9 Ethical Considerations

In this study, the researchers was considered the ethical issues related to the research

project, and was ensure the confidentiality of the respondents. To consider ethical

issue the following activities was implemented: Solicit permission through a written

request to the concerned officials of the Banks under study, information of the

respondents was used only for academic purpose, Secrecy, privacy and

confidentiality of the undisclosed information was the main concern of this study.

3.10 Limitations of the Study

The following are some of antitrade that out to the validity of the research

Extraneous variables which was beyond the researcher’s control such as

respondents’ honesty, personal biases and uncontrolled setting of the study.

Testing: The use of research assistants can bring about inconsistency in the

administration of the questionnaires in terms of time of administration,

understanding of the items in the questionnaires and explanations given to

the respondents. To minimize this threat, the research assistants will be

oriented and briefed on the procedures to be done in data collection.

Mortality: Not all questionnaires will be returned completely answered nor

even retrieved back due to circumstances on the part of the respondents such

as travels sickness, hospitalization and refusal/withdrawal to participate. In

anticipation to this, the researcher will reserve more respondents by

exceeding the minimum sample size. The respondents will also be reminded

not to leave any item in the questionnaires unanswered and will be closely

followed up as to the date of retrieval.

CHAPTER FOUR: DATA PRESENTATION, ANALYSIS,INTERPRETATION

4.0 Introduction

This chapter presents data analysis, presentation, and interpretation. The data

analysis and interpretation was based on the research questions as well as research

objectives, the presentation is divided in to two parts. The first part presents the

respondents profile or demographic information, while the second part deals with

presentation, interpretation, and analysis of the research questions and objectives.

Below are the data presentations and analysis of research findings.

4.1 Demographic Information of the Respondents

This part presents the background information of the respondents who participated in

the study. The purpose of this background information was to find out the

characteristics of the respondents and show the distribution of the population in the

study. Their distribution is established as it follows in table

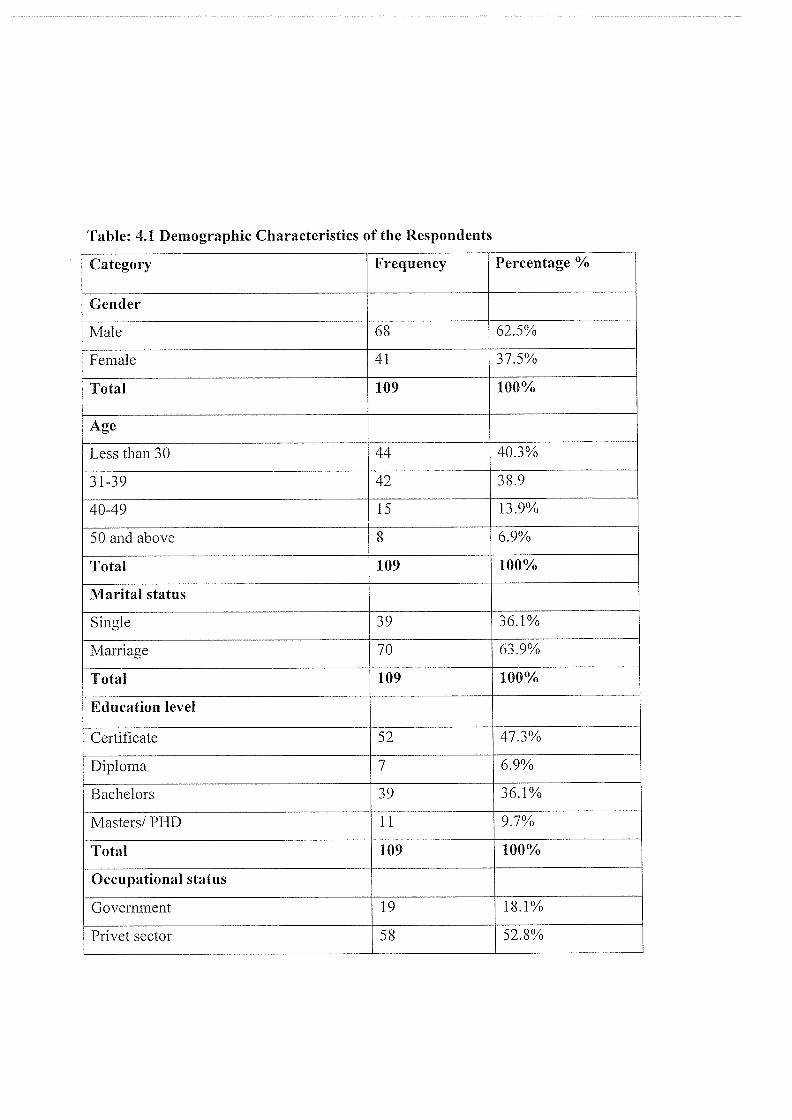

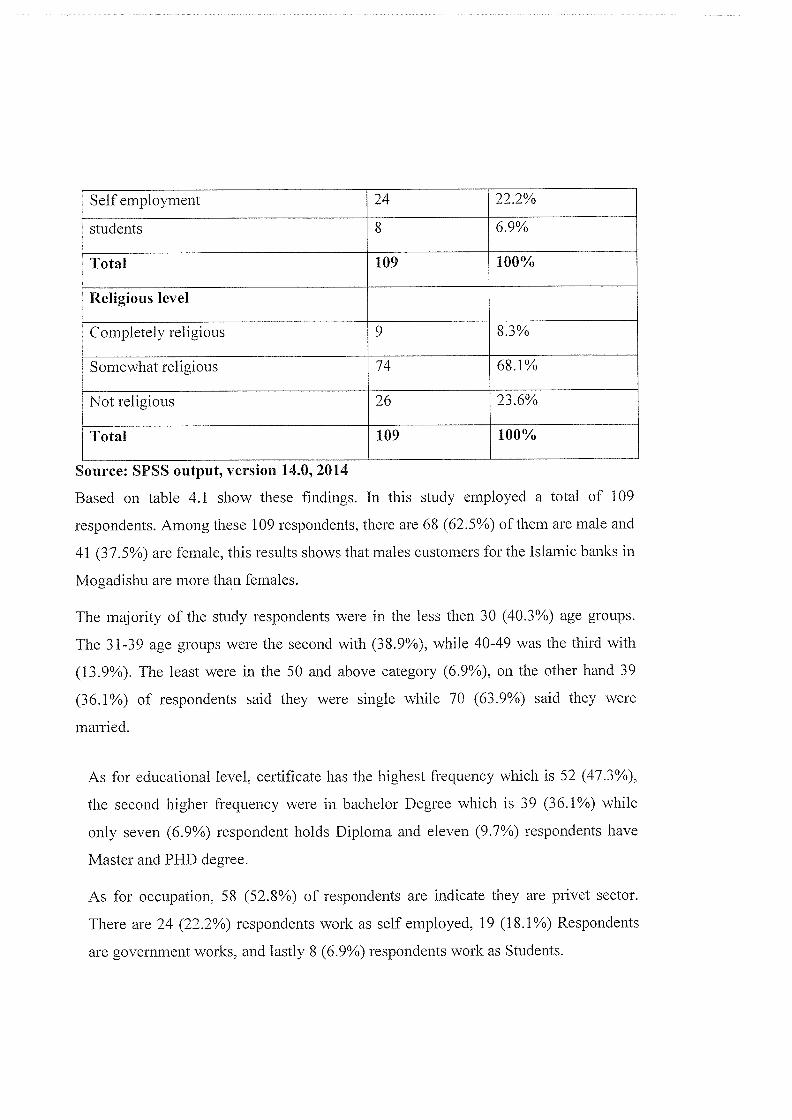

Table: 4.1 Demographic Characteristics of the Respondents

Category Frequency Percentage %

Gender

Male 68 62.5%

Female 41 37.5%

Total 109 100%

Age

Lessthan30 44 40.3%

31-39 42 38.9

40-49 15 13.9%

50 and above 8 6.9%

Total 109 100%

Marital status

Single 39 36.1%

Marriage 70 63.9%

Total 109 100%

Education level

Certificate 52 47.3%

Diploma 7 6.9%

Bachelors 39 36.1%

Masters! PHD 1 1 9.7%

Total 109 100%

Occupational status

Government 19 18.1%

Privet sector 58 52.8%

Self employment 24 22.2%

students 8 6.9%

Total 109 100%

Religious level

Completely religious 9 8.3%

Somewhat religious 74 68.1%

Not religious 26 23.6%

Total 109 100%

Source: SPSS output, version 14.0, 2014

Based on table 4.1 show these findings. In this study employed a total of 109

respondents. Among these 109 respondents, there are 68 (62.5%) of them are male and

41 (37.5%) are female, this results shows that males customers for the Islamic banks in

Mogadishu are more than females.

The majority of the study respondents were in the less then 30 (40.3%) age groups.

The 3 1-39 age groups were the second with (38.9%), while 40-49 was the third with

(13.9%). The least were in the 50 and above category (6.9%), on the other hand 39

(36.1%) of respondents said they were single while 70 (63.9%) said they were

married.

As for educational level, certificate has the highest frequency which is 52 (47.3%),

the second higher frequency were in bachelor Degree which is 39 (36.1%) while

only seven (6.9%) respondent holds Diploma and eleven (9.7%) respondents have

Master and PHD degree.

As for occupation, 58 (52.8%) of respondents are indicate they are privet sector.

There are 24 (22.2%) respondents work as self employed, 19 (18.1%) Respondents

are government works, and lastly 8 (6.9%) respondents work as Students.

According to above table 4.1 for religion, 74 (68.1%) of them are somewhat

religious, 26 (23.1%) are not religious, 9 (8.3%) are complete religious. This also

shows that most of the respondents are somewhat religious.

4.3 Research Question one: level of awareness of Islamic banking product

Research question one was derived from the first objective of the study. The first

objective of this study was to determine the awareness level of Islamic banking

products. To achieve this objective Respondents were subjected to a number of

questions to provide answers to research question one mentioned above.

The questions administered to the respondents were aimed at investigating the

respondent’s responses towards the stated research objective. Keeping view of the

independent variable in this study was level awareness of Islamic banking. This

variable was broken into four dimensions namely understanding (with five

questions), Attitude (with three questions). perception (with two questions), and

other questions regarding to awareness (with eight questions). Each

questionlstatement was likert scaled (Likert 1932) ranging from strongly Agree,

Agree, Disagree and Strongly Disagree and their responses were analyzcd by using

SPSS and summarized means and rank as indicated the below table 4.2.

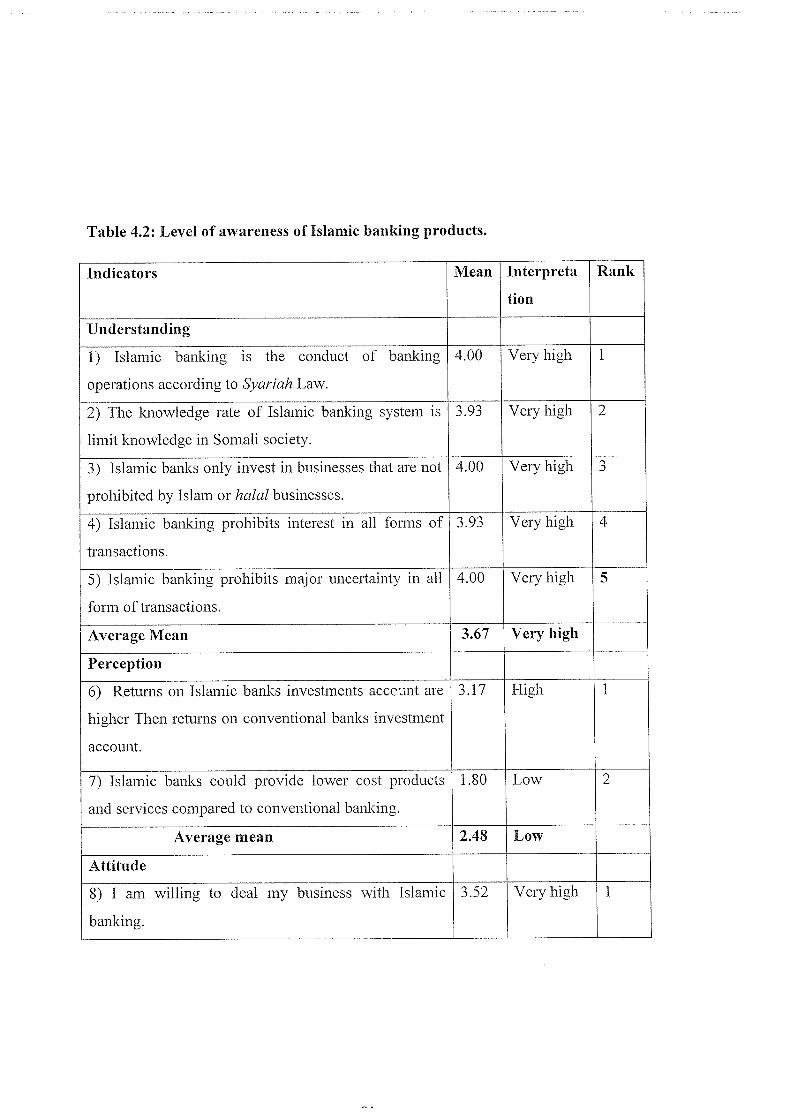

Table 4.2: Level of awareness of Islamic banking products.

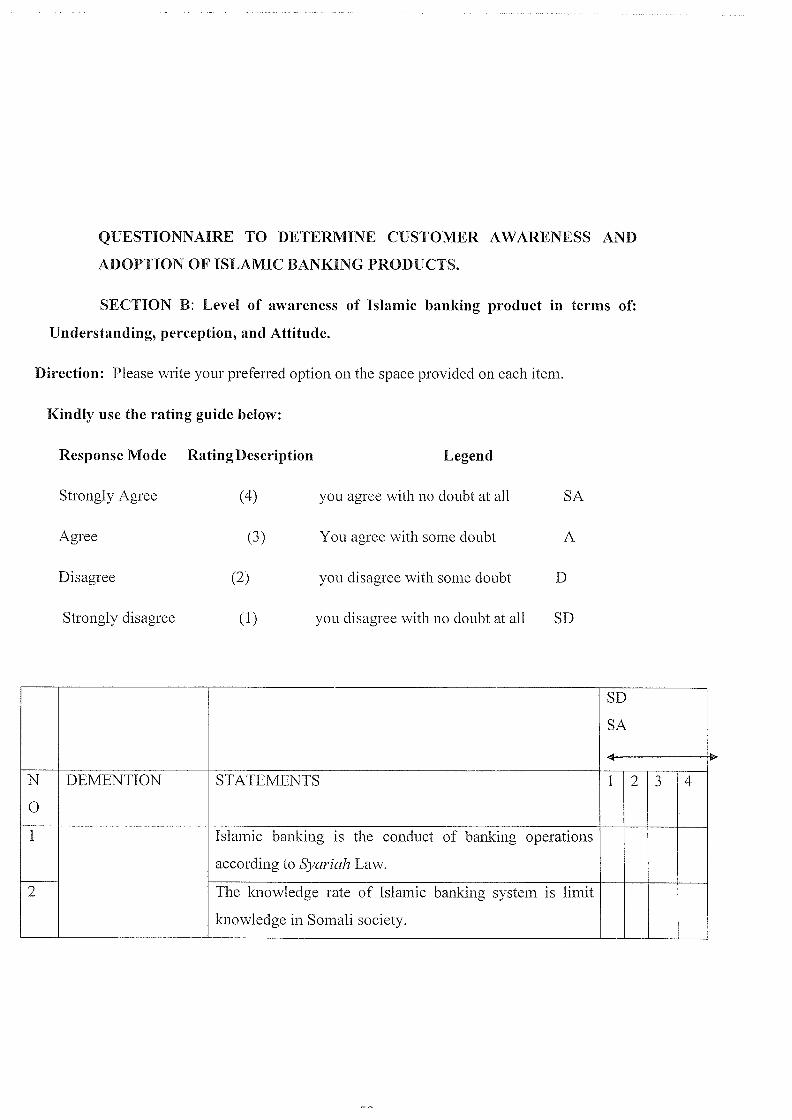

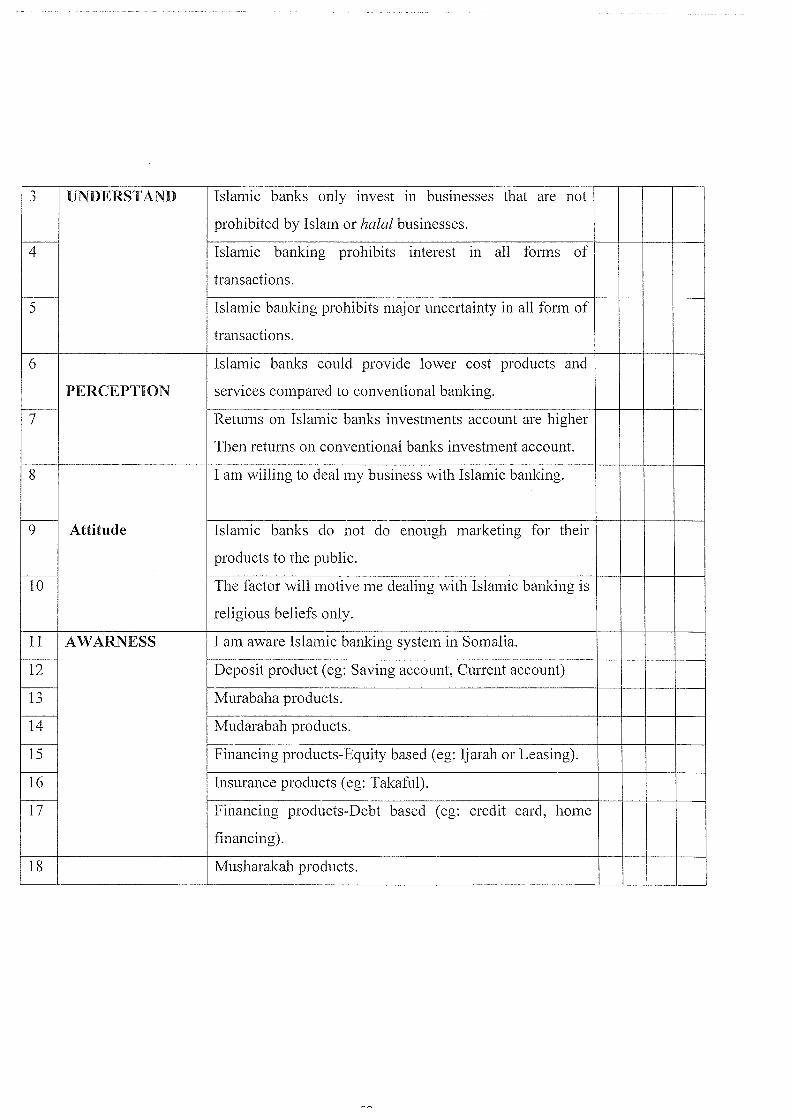

Indicators Mean I Interpreta Rank

tion

Understanding

1) Islamic banking is the conduct of banking 4.00 Very high 1

operations according to Syariah Law.

2) The knowledge rate of Islamic banking system is 3.93 Very high 2

limit knowledge in Somali society.

3) Islamic banks only invest in businesses that are not 4.00 Very high 3

prohibited by Islam or halal businesses.

4) Islamic banking prohibits interest in all forms of 3.93 Very high 4

transactions.

5) Islamic banking prohibits major uncertainty in all 4.00 Very high 5

form of transactions.

Average Mean 3.67 Very high

Perception

6) Returns on Islamic banks investments acceunt are 3.17 High 1

higher Then returns on conventional banks investment

account.

7) Islamic banks could provide lower cost products 1.80 Low 2

and services compared to conventional banking.

Average mean 2.48 Low

Attitude

8) I am willing to deal my business with Islamic 3.52 Very high 1

banking.

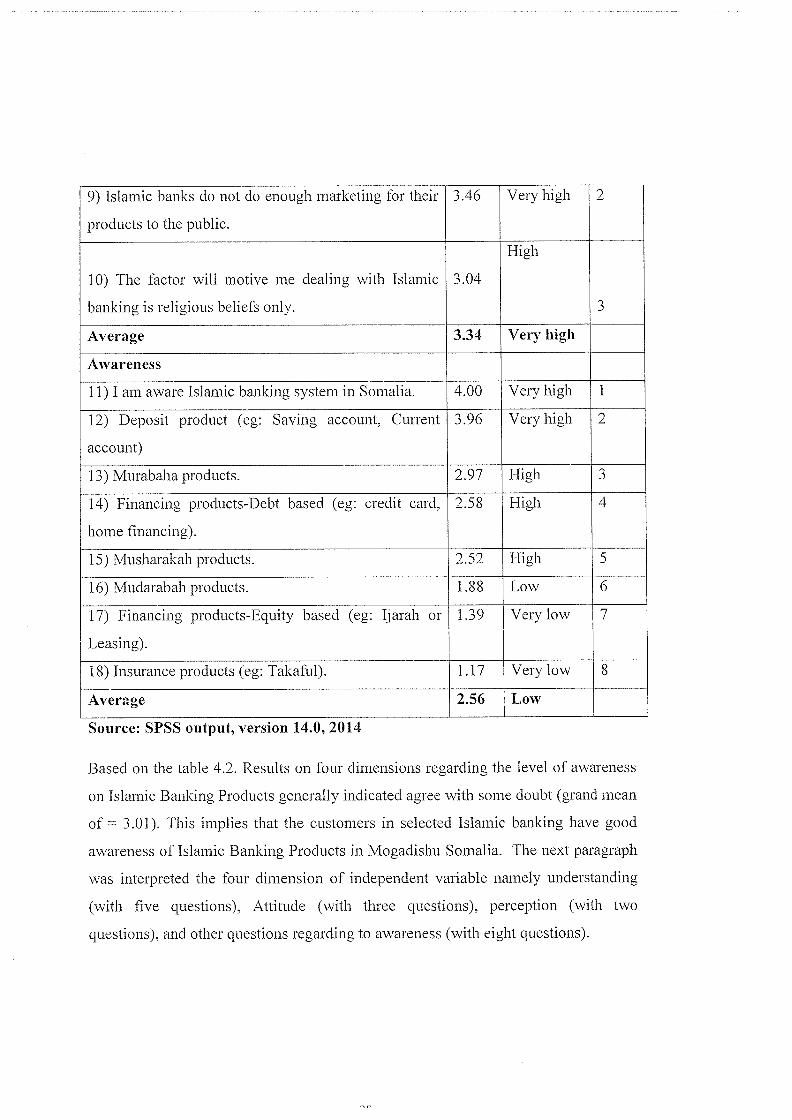

9) Islamic banks do not do enough marketing for their 3.46 Very high 2

products to the public.

High

10) The factor will motive me dealing with Islamic 3.04

banking is religious beliefs oniy. 3

Average 3.34 Very high

Awareness

1 1) I am aware Islamic banking system in Somalia. 4.00 Very high I

12) Deposit product (eg: Saving account, Current 3.96 Very high 2

account)

13) Murabaha products. 2.97 High 3

14) Financing products-Debt based (eg: credit card, 2.58 High 4

home financing).

15) Musharakah products. 2.52 High 5

16) Mudarabah products. 1.88 Low 6

17) Financing products-Equity based (eg: Ijarah or 1.39 ~ Very low 7

Leasing).

18) Insurance products (eg: Takaful). 1.17 Very low 8

Average 2.56 Low

Source: SPSS output, version 14.0, 2014

Based on the table 4.2. Results on four dimensions regarding the level of awareness

on Islamic Banking Products generally indicated agree with some doubt (grand mean

of = 3.01). This implies that the customers in selected Islamic banking have good

awareness of Islamic Banking Products in Mogadishu Somalia. The next paragraph

was interpreted the four dimension of independent variable namely understanding

(with five questions), Attitude (with three questions), perception (with two

questions). and other questions regarding to awareness (with eight questions).

UNDRESTNDING: The first dimension of independent variable (awareness level)

understood (with five questions). it shows that majority of the respondents strongly

agree with no doubt that Islamic Banking is the conducts of banking operation

according to Syariah Law, that Islamic banking prohibits interest in all form of

transactions, that Islamic banks only invest in businesses that are not prohibited by

Islam or halal businesses, in addition the respondents strongly agree with no doubt

that The knowledge rate of Islamic banking system is limit knowledge in Somali

society, while the majority of deponents are agree with some doubt that Islamic

banking prohibits major uncertainty in all form of transactions.

Therefore, on average first dimension of independent variable was indicated strongly

agree with no doubt (average mean~3.67), this implying that understanding the

concept of Islamic banking is above the average level. For some basic concept such

as Interest, Halal, syriah low, this might due to most of the respondents are

graduated students and they have learnt Islamic studies in their informal study. Thus,

they have certain basic knowledge about the concept of Halal, syriah low, and

interest.

Perception: The second dimension was perception (with two questions) towards

Islamic banking products, as above table indicated that the respondents are agree

with some doubt that Returns on Islamic banks investments account are higher Then

returns on conventional banks investment account, on the other hand, the

respondents are disagree with some doubt that Islamic banks could provide lower

cost products and services compared to conventional banking.

Therefore the mean this dimension was (average mean ~2.48) disagree with some

doubt, this implies that customers of Islamic banks have bad perception of Islamic

banking products. Because they believed that the return of Islamic banking is more

than the return of conventional, this might due to most of the customers does not

deal interest based bank, in addition that they believe the charged Islamic bank was

near the same charge conventional bank and the deference was name of that cost

charged to product or service.

Attitude: Third dimension of above independent variable was attitude, based on

table 4.2. respondents are strongly agreed with no doubt that Islamic banks do not do

enough marketing for their products to the public, that they are willing to deal with

their business with Islamic banking, on the other hand respondents are agree with

some doubt that The factor will motive dealing with Islamic banking is religious

beliefs only.

Therefore the mean this dimension was (average mean ~3.34) strongly agree with no

doubt, this implies that the customers of Islamic banks have good attitude towards

Islamic banks, which may result in to adopt products and services on their business

in the future.

Awareness: The lastly dimension of independent variable (awareness level) was

reveal other a statements/questions regarding overall awareness Islamic products.

According to the above table 4.2 The results showed that the most of the respondents

are aware of Islamic banking in Somalia, also it shows that among the seven

products offered by Islamic Banks, Deposit products (eg: Saving account, Current

account) have the highest awareness level as the above mean indicate which is

strongly agree, The following product that has the second highest level of awareness

is Murabaha products and Musharakah products, Financing products-Debt based (eg:

credit card, home financing). Mudarabah products have low awareness. And lastly

the product that has lowest level of awareness from the respondents was Insurance

products (eg: Takaful), and Financing products-Equity based (eg: Ijarah or Leasing).

Therefore the mean of lastly dimension in table 4.6 indicated that respondents rated

averagely on statements of awareness as represented by (average mean ~2.56), this

implies that the customers of Islamic banks have good awareness in some of the

general products such as Deposit product (eg: Saving account, Current account),

Murabaha products.

4.4 Research Question two: level of adoption of Islamic product

Research question two was derived from the second objective of the study. The

second obj~ctive of this study was to examine the level of adoption of Islamic

banking product. To achieve this objective Respondents were subjected to a number

of questions to provide answers to research question mentioned above.

The questions administered to the respondents were aimed at investigating the

respondent’s response towards the stated research objective. Keeping view of the

dependent variable in this study was level adoption of Islamic banking. This variable

was broken into four dimensions namely early adaptors (with three questions), late

adaptors (with three questions), laggards (with three questions). Each

questionlstatement was likert scaled (Likert 1932) ranging from strongly Agree,

Agree, Disagree and Strongly Disagree and their responses were analyzed by using

SPSS and summarized means and rank presented below table 4.3.

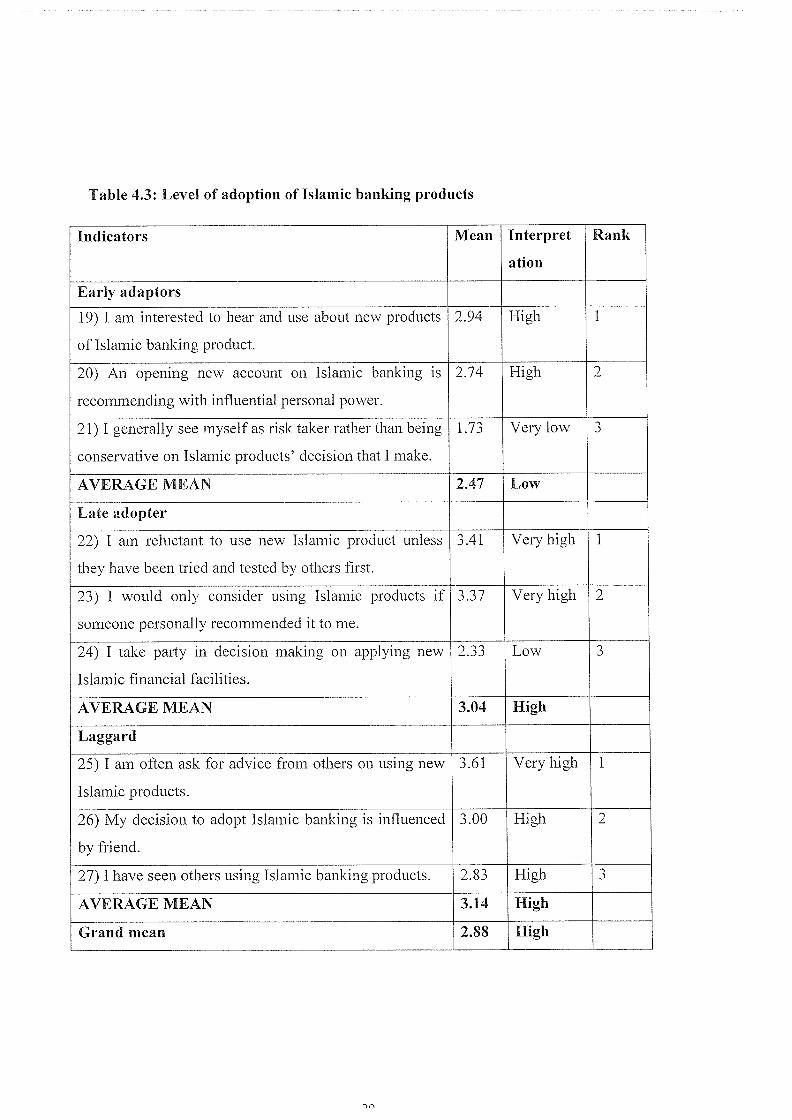

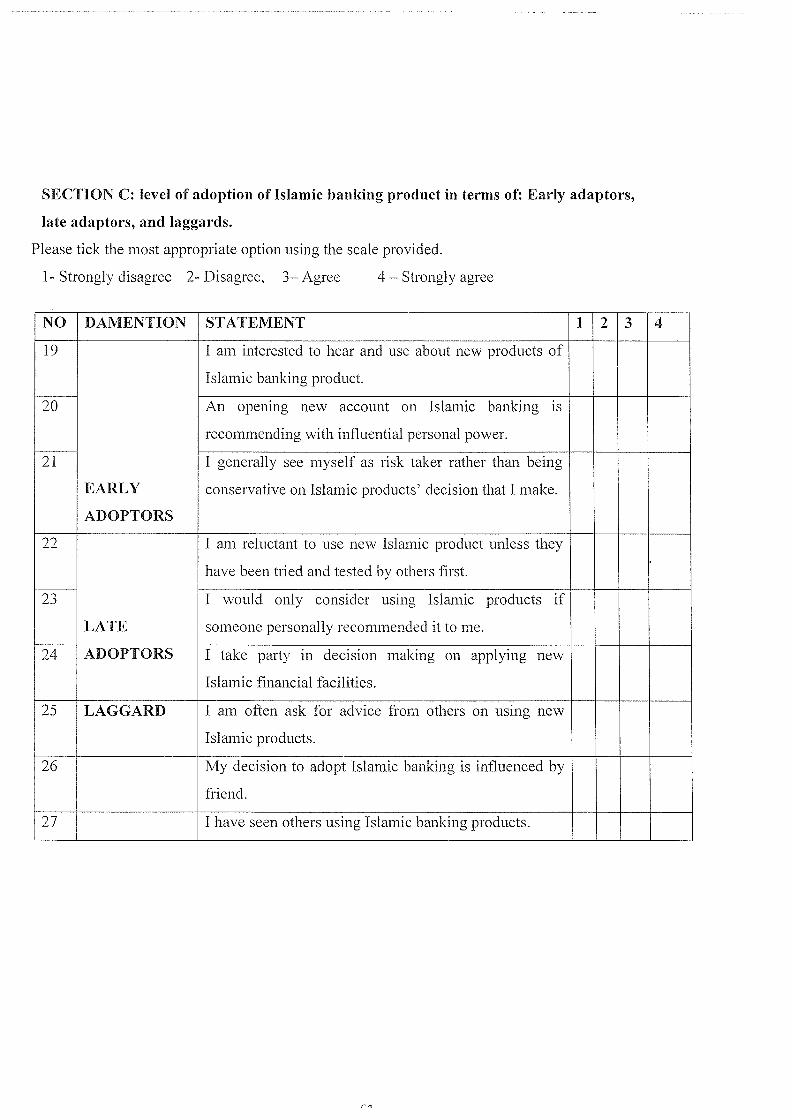

Table 4.3: Level of adoption of Islamic banking products

Indicators Mean Interpret Rank

ation

Early adaptors

19) I am interested to hear and use about new products 2.94 — High 1

of Islamic banking product.

20) An opening new account on Islamic banking is 2.74 High 2

recommending with influential personal power.

21) I generally see myself as risk taker rather than being 1.73 Very low 3

conservative on Islamic products~ decision that I make.

AVERAGE MEAN 2.47 Low

Late adopter

22) 1 am reluctant to use new Islamic product unless 3.41 Very high I

they have been tried and tested by others first.

23) I would only consider using Islamic products if 3.37 Very high 2

someone personally recommended it to me.

24) I take party in decision making on applying new 2.33 Low 3

Islamic financial facilities.

AVERAGE MEAN 3.04 High

Laggard

25) I am often ask for advice from others on using new 3.61 Very high 1

Islamic products.

26) My decision to adopt Islamic banking is influenced 3.00 High 2

by friend.

27) I have seen others using Islamic banking products. 2.83 High 3

AVERAGE MEAN 3.14 High

Grand mean 2.88 High

Source: SPSS output, version 14.0, 2014

Based on the table 4.4. Results on three dimensions regarding the level of adoption

on Islamic Banking Products generally indicated agree with some doubt (grand mean

of = 2.88). This implies that level of the usage or adaption on Islamic banking

products’ rate is low. The next paragraph was interpreted the three dimension of

dependent variable namely early adopter (with three questions), late adopters (with

three questions), and laggards (with three questions).

Early Adopters: The first dimension of dependent variable (adaption level) was

early adaptors (with three questions). it shows that majority of the respondents are

agree with some doubt that they interested to hear and use about new products of

Islamic banking product, An opening new account on Islamic banking is

recommending with influential personal power. While the majority of deponents are

strongly disagree that they generally see themselves as risk taker rather than being

conservative on Islamic products’ decision that they make. Therefore, on average

first dimension of dependent variable was indicated disagree with some doubt

(average mean =2.47), this implies that the one-third of customers are low to be early

adopt or use of new or exist products.

Late adopter: The second dimension was late adaptors (with three questions)

towards adaption of Islamic banking products, as above table indicated that the

respondents are agree with some doubt that costumers are take party in decision

making on applying new Islamic financial facilities, on the other hand. the

respondents are strongly agree that they would only consider using Islamic products

if someone personally recommended it to me, I am reluctant to use new Islamic

product unless they have been tried and tested by others first. Therefore the mean

this dimension was (average mean =2.47) disagree with some doubt, this implies that

two-third of customers are highly willing to adopt or use (Islamic products) after the

average member of a social system are accept

Laggards: Third dimension of above dependent variable was laggard, based on table

4.4 respondents are agreed with some doubt that their decision to adopt Islamic

banking was influenced by friend, they have seen others using Islamic banking

products respectively, on the other hand respondents are strongly agree with no

doubt that they am often ask for advice from others on using new Islamic products.

Therefore the mean this dimension was (average mean =3.14) agree with some

doubt, this implies that customers are low willing to adopt or use (Islamic products)

this means that half one-third customers decide after looking at whether the

innovation is successfully adopted by other members of the social system in the past.

4.5 Research Question three: Hypothesis

Research question four was derived from the fourth objective of the study. The

fourth objective of this study was to establish the relationship between costumer

awareness and adaption of Islamic banking products in Mogadishu, Somali, to

achieve this objective, the researcher correlate 27 questionnaire statements for both

independent and dependent variable to provide answers to research question three.

The results are presented in the following table.

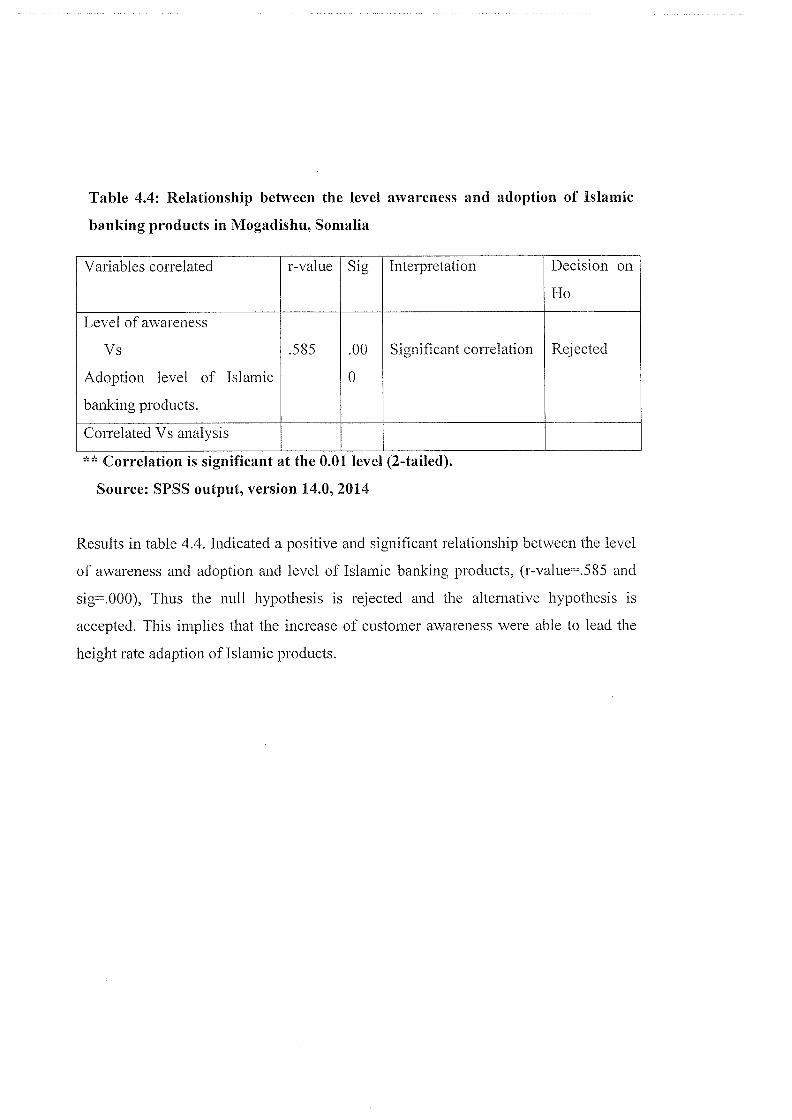

Table 4.4: Relationship between the level awareness and adoption of Islamic

banking products in Mogadishu, Somalia

Variables correlated r-value Sig Interpretation Decision on

Ho

Level of awareness

Vs .585 .00 Significant correlation Rejected

Adoption level of Islamic 0

banking products.

Correlated Vs analysis

** Correlation is significant at the 0.01 level (2-tailed).

Source: SPSS output, version 14.0, 2014

Results in table 4.4. Indicated a positive and significant relationship between the level

of awareness and adoption and level of Islamic banking products, (r-value.585 and

sig.000), Thus the null hypothesis is rejected and the alternative hypothesis is

accepted. This implies that the increase of customer awareness were able to lead the

height rate adaption of Islamic products.

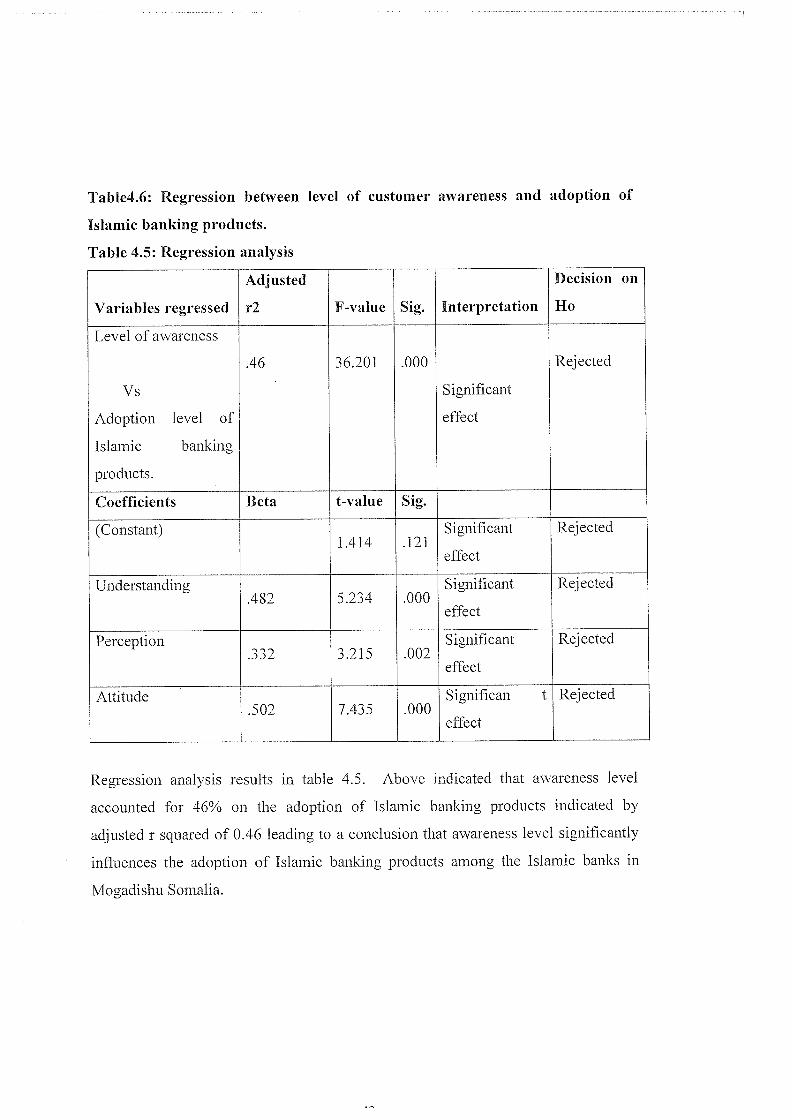

Table4.6: Regression between level of customer awareness and adoption of

Islamic banking products.

Table 4.5: Regression analysis

Adjusted Decision on

Variables regressed r2 F~value Sig. Interpretation Ho

Level of awareness

.46 36.201 .000 Rejected

Vs Significant

Adoption level of effect

Islamic banking

products.

Coefficients Beta t-value Sig.

(Constant) Significant Rejected1.414 .121

effect

Understanding Significant Rejected.482 5.234 .000

effect

Perception Significant Rejected.332 3.215 .002

effect

Attitude Significan t Rejected.502 7.435 .000

effect

Regression analysis results in table 4.5. Above indicated that awareness level

accounted for 46% on the adoption of Islamic banking products indicated by

adjusted r squared of 0.46 leading to a conclusion that awareness level significantly

influences the adoption of Islamic banking products among the Islamic banks in

Mogadishu Somalia.

CHAPTER FIVE:

DISCUSSION, CONCLUSION AND IMPLICATIONS

5.0 Introduction

This is the last chapter of the study. Due on the analysis of previous chapter, the

summary of statistical analysis and discussion of major finding will be identified for

further improvement for Islamic banking and services. This chapter will be ended