Embed Size (px)

Citation preview

Current bankruptcy trends Mortgage servicer challenges and solutions

Financial Services Risk Management

Current bankruptcy trends | 1

Executive summary

Shortcomings in bankruptcy operations and technology pose significant risks and increased costs to mortgage servicers in terms of operational and technological efficiency, as well as legal liability. This paper proposes solutions to a multitude of challenges in key focus areas in the end-to-end borrower bankruptcy process, including regulatory and compliance risks, data integrity problems, limited case tracking and monitoring, and incorrect payment application. EY has the deep industry knowledge, regulatory experience and technology solutions that are essential to supporting servicers’ efforts to enhance their programs, streamline their processes and better align their practices to regulatory expectations.

Background

As part of the broader regulatory focus on the mortgage servicing industry, servicers are facing increased scrutiny regarding their ability to properly handle the procedural requirements, quality control expectations and volume demands inherent to servicing loans while debtors are in bankruptcy. Concerns over mortgage servicers’ approaches to handling bankruptcy cases are apparent in regulatory guidelines, consent orders, recent settlements and mortgage servicing rules. The regulatory guidelines set forth in the 2011 Office of Comptroller of Currency (OCC)/Federal Reserve Bank (FRB) mortgage servicing consent orders, the National Mortgage Settlement servicing standards, and the Consumer Financial Protection Bureau (CFPB) mortgage servicing rules all include bankruptcy-related guidelines or requirements and emphasize the need for improvements around how servicers handle debtors’ loans while debtors are in bankruptcy. The subject of servicer mishandling of bankruptcy cases has also been repeatedly highlighted in speeches made by the Director of the Executive Office of the Department of Justice’s United States Trustee Program.

In addition to expressing concerns over the mishandling of bankruptcy cases in consent orders, and public speeches, there has been a significant settlement in March 2015, in excess of $50 million in penalties, affecting one of the nation’s largest mortgage servicers that was accused of robo-signing payment change notices, as well as failure to timely and accurately provide payment change notices and escrow statements to borrowers.

This combination of regulatory guidelines, public statements and enforcement actions, as well as a willingness among regulatory agencies to coordinate efforts across agencies and with the United States Trustee Program (USTP), indicates that mortgage servicers’ handling of bankruptcy matters will continue to be a prominent focal point in examinations and investigations. In order to withstand this increased scrutiny, servicers should consider how to best manage their bankruptcy departments in order to guard against the financial penalties and negative publicity that may stem from further regulatory actions in this area. The following challenges and proposed solutions describe and illustrate key areas of focus in bankruptcy operations and how EY can help servicers enhance their programs, streamline their processes and better align their practices to regulatory expectations.

Applicable requirements

In addition to an obligation to comply with the US Bankruptcy Code, along with jurisdictional and local rules, mortgage servicers must consider the bankruptcy-related servicing requirements and expectations included in the following settlements and regulations.

Office of Comptroller of Currency/Federal Reserve Board consent orders

The 2011 OCC/FRB mortgage servicing consent orders were issued in 2011 to the 13 largest mortgage servicers. Among other terms, these orders included requirements that servicers comply with specified time frames for

Current bankruptcy trends | 2

bankruptcy cases, including additional details in sworn statements such as bankruptcy Proofs of Claim (POCs) and Motions for Relief (MFRs) related to ownership of the debt and amounts claimed as due and owed.

Subsequent consent orders with other servicers reflected similar terms related to servicing loans when debtors have filed for bankruptcy.

Attorneys General National Mortgage Settlement servicing standards/Department of Justice metrics

As part of the Attorneys General and federal government National Mortgage Settlement (NMS), five of the largest mortgage servicers were bound to the settlement terms beginning in February 2012. In addition to requiring payments be made to mortgage refinance programs and debt relief be provided directly to borrowers, the NMS included new servicing standards that placed stricter guidelines on mortgage servicing, including a requirement for better communication with borrowers, a single point of contact, adequate staffing levels and training, and appropriate standards for executing documents in bankruptcy cases.

Consumer Financial Protection Bureau guidelines:

Consumer Financial Protection Bureau (CFPB) guidelines, effective January 2014, addressed bankruptcy-related loan documentation. In particular, the Real Estate Settlement Procedures Act (RESPA), implemented by Regulation X, and the Truth in Lending Act (TILA), implemented by Regulation Z included expanded requirements regarding the issuance of payment statements.

In December 2014, the CFPB proposed changes to the mortgage rules under RESPA (Regulation X) and TILA (Regulation Z). If adopted, the proposed changes include requiring periodic statements to be provided to borrowers in bankruptcy and narrowing the scope of exemption from the early intervention requirements for borrowers in bankruptcy.

Current bankruptcy trends | 3

Key challenges

The concerns highlighted by regulators are symptomatic of broader challenges in current bankruptcy operations and technology solutions that pose significant risks to mortgage servicers. Remediation of the end-to-end bankruptcy process, in order to reduce risks and satisfy regulator and court expectations, requires particular attention to the following key areas and their related challenges:

Key area Challenges

Case management Inadequate case management systems prevent transparency as cases move through the bankruptcy process and risk erroneous disclosures and account activities.

Payment application Inaccurate payment application due to system limitations and ineffective system controls creates data integrity issues.

Payment reconciliation Lack of controls around payment reconciliation creates data integrity issues, requires manual workaround and often leads to remediation efforts.

Proof of Claim (POC) and Motion for Relief (MFR) documentation

Process control gaps, inadequate training, system deficiencies, lack of comprehensive reporting and high attorney revision rates hinder accurate and timely filing of POCs and MFRs.

Payment Change Notification (PCN)

Uncontrollable PCNs and related system deficiencies lead to inaccurate notifications, filings after the required 21-day notification period, and failure to inform borrowers and trustees of payment changes.

Escrow Complex manual processes performed in an inadequately controlled environment lead to inaccurate escrow analyses that impact the accuracy and timeliness of downstream processes.

Use of third-party vendors Inadequate management and supervision of third-party vendors, including attorneys, lead to bankruptcy violations and case delays due to erroneous document drafting and inappropriate disclosure of sensitive borrower information.

Current bankruptcy trends | 4

How EY can help

EY’s Financial Services Advisory team provides insights into emerging industry trends, helps address new consumer compliance requirements and assists with deploying the right program to satisfy the increased regulatory demands. EY’s offerings include the following types of support:

Regulatory transformation, operational change management, preparation and response

To help mortgage services address the challenges of efficient bankruptcy compliance, EY can provide full service solutions with compliance, operations, customer experience and technology experience components. Recognizing the scope of challenges posed by bankruptcy requirements, EY is prepared to provide thorough support through assessments, operational change management, third-party vendor interaction and risk-management, evaluation and education, and process and technology solution mapping. EY’s ability to identify potential regulatory gaps allows us to deliver defined, actionable recommendations for closing gaps, supporting training and remediation efforts, and documenting end-to-end compliance.

Look-back file reviews, quality assurance testing, assessments and operational change management

EY has the extensive knowledge and industry insights necessary to perform extensive look-back file reviews and ongoing quality assurance testing of file processing. We can also rapidly assess the current state, in order to identify compliance gaps and key areas of inefficiency. Based on these identified areas needing improvement, EY can quickly develop and help execute implementation plans to support operational change management, streamline processes, and close compliance shortcomings.

Third-party vendor oversight and risk management

In addition to shoring up internal processes, improving efficiency within bankruptcy operations and closing compliance gaps, EY can also help enhance third-party vendor practices as an additional approach to improving the timeliness and quality of bankruptcy filings. We have significant experience developing and implementing third party vendor oversight programs and risk management.

Process and technology solution mapping

EY can provide key solutions that enhance bankruptcy operations by identifying gaps in current bankruptcy processes and systems, reviewing account errors, planning and executing remediation efforts, and implementing technology solutions to improve automation and accuracy. These solutions include current state assessment and remediation of bankruptcy processes, account look-back and remediation, third-party vendor process assessment and review process remediation, account reconciliation, and business transformation solutions.

EY can also provide solutions from a technology standpoint to enhance automation, accuracy and stakeholder engagement in bankruptcy processes. These solutions include the development of a customized case management tool, technology infrastructure assessments, data integrity evaluations and clean-up, an attorney scoring tool, online workflow guide, and enhanced reporting.

Current bankruptcy trends | 5

Case management

Inadequate case management models may prevent transparency as loans move through the bankruptcy process. Financial institutions should establish end-to-end case management models with automated event-driven notification that move loans efficiently and accurately through the bankruptcy process.

Risks Potential solutions/industry practices • Lack of transparent end-to-end view of loans as

servicer bankruptcy operations teams are siloed based on bankruptcy event (e.g., pre-confirmation vs. post-confirmation) and chapter (e.g., Ch. 9, Ch. 11, Ch. 13) often leads to system backlogs and data integrity issues.

• Ineffective and inconsistent coding and documentation of loan status throughout bankruptcy case causes significant downstream inefficiencies and redundant processes.

• Lack of transparency in certain areas, such as loan modifications and stipulated agreements, leads to impediments in downstream processes and timely research needed to resolve case impediments.

• Untimely or insufficient alerts of upcoming bankruptcy events cause backlogs in timely handling of event-specific processes and downstream case management progress.

• Lack of knowledge sharing across bankruptcy units leads to redundant efforts and inconsistent application of practices.

• Inadequate monitoring and control points around book-loss decisioning lead to unnecessary corporate losses.

• Insufficient control points around onboarding new accounts and rejections leads to delays in downstream processes such as document preparation and timely filing, case progress to new event points, and untimely responses to debtor, judicial or internal inquiries.

• Operations:

• Establish single point-of-contact with end-to-end oversight of a loan

• Enhance case management processes and controls to send automated event notifications and proactively alert downstream processes of upcoming events, delays and issues with accounts

• Standardize and document methods for loan status updates to eliminate timely research and enable single point-of-contact to access and rapidly understand case history and status

• Encourage knowledge sharing across bankruptcy units to avoid redundant processes and leverage leading practices

• Increase accountability within setup, case management and closing teams through established performance metrics and quality assurance (QA)/quality control (QC) processes

• Technology:

• Integrate case management functions, including automated event-driven notifications, to enable end-to-end case governance throughout the entire bankruptcy process, regardless of loan type or bankruptcy event, and to allow loans to flow seamlessly through bankruptcy processes and diminish likelihood of missed handoffs, data integrity issues across systems, untimely processing and redundant research

• Focus case management functionality on accuracy of system coding and status, handoff management to complement functional specialization, enhanced data sourcing, and mapping and integrity

Current bankruptcy trends | 6

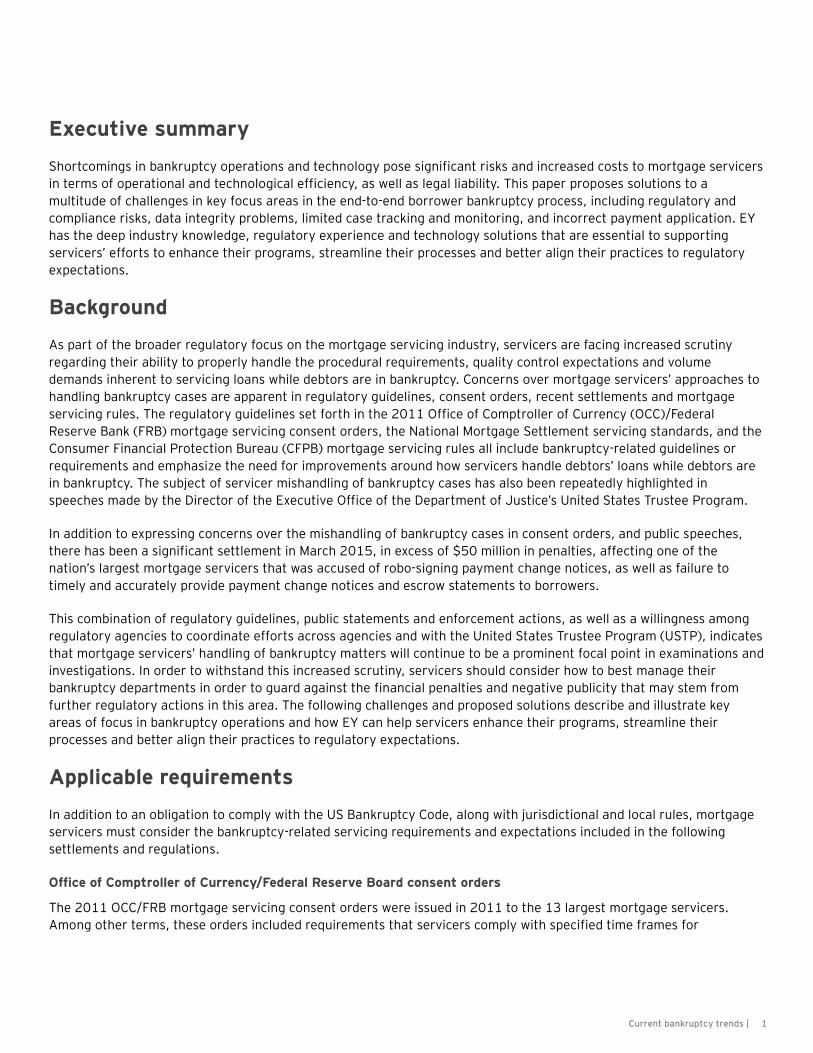

Case management solution

An effective case management solution could be an overall solution for the inefficiencies in processes such as bankruptcy, foreclosures, and other QA/QC process management

The case management solution should ideally have the following modules:

• A case manager to track different cases

• A metrics reporting module to report on the various bankruptcy and other metrics

• A checklist file tracker to track all the files required for each case

• A parameters function to automatically create the dates servicer needs to comply with

• Show supporting data from source systems (e.g., charge-off systems, transaction systems) to help facilitate effective QA/QC process

• An analytics function to help management track the various activities and identify stress points to make necessary adjustments

Parameters

Case data

Case manager

Metrics reports

Analytics

Analytics and parameters

Case management

Transaction systems, customer tables, charge-off

systems, mortgage/loans database

Source data

ETL

Checklist file tracker

Supporting data

Current bankruptcy trends | 7

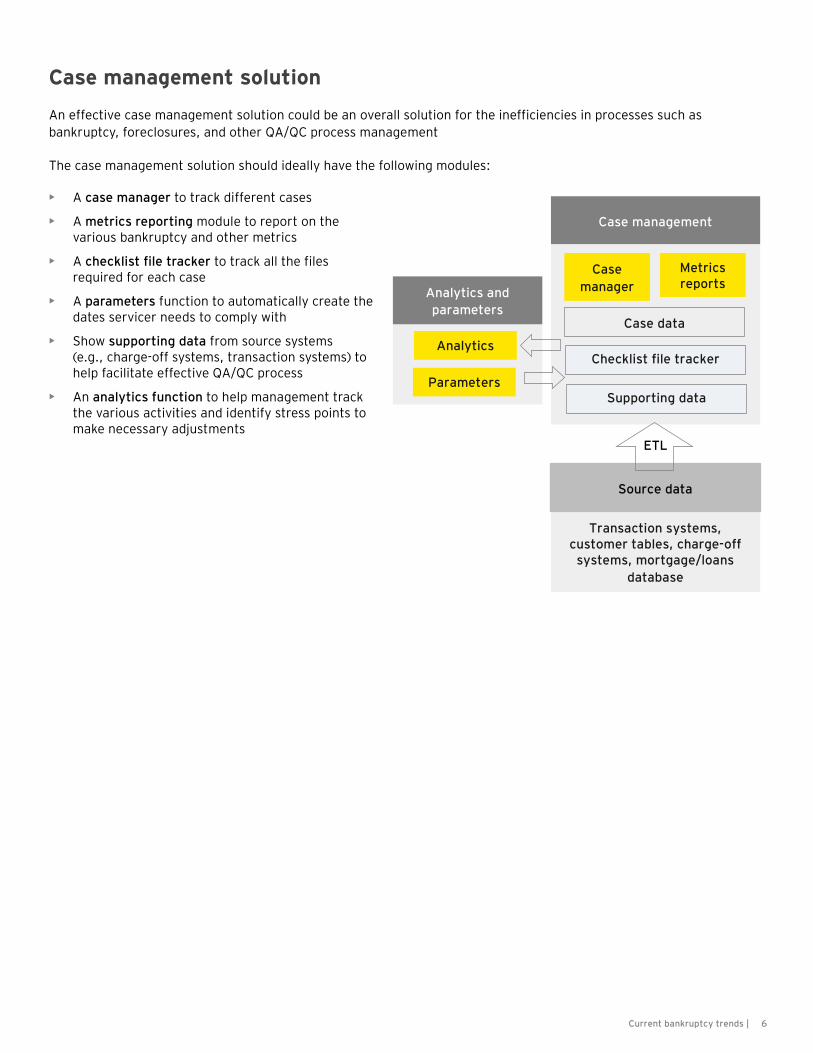

Payment application

Inaccurate application of payments due to system limitations and ineffective system controls create data integrity issues. Financial institutions can also refine pay application operations and automate where appropriate to make the payment application process more efficient.

Risks Potential solutions/industry practices • Lack of centralized data source across bankruptcy

teams leads to inconsistent cash/ledger amounts and confusion as to condition of account data.

• System integration issues due to multiple systems of record impede bankruptcy processes and lead to financial impacts, customer complaints and intensified regulatory scrutiny.

• Inadequate automated processes that cannot distinguish between pre-petition and post-petition payments require timely manual processing and remediation.

• Inefficient lockbox processing adds significant time to payment application processes.

• Lack of understanding of system functionality, including full technology stack and leverageable capabilities, results in underused technology systems that do not align to business needs and are not readily flexible to accommodate future technology enhancements.

• Limited architecture and data dependency mapping hinder success of system enhancement efforts.

• Operations:

• Consolidate lockbox processes in order to streamline initial stages of payment application and reduce processing time

• Use sophisticated quality review to confirm payments are correctly applied up-front and avoid downstream rework, potential missed service-level agreements (SLAs) and inaccurate filings

• Streamline system technology decisioning and loan classification to align with business priorities and compliance with regulatory mandates

• Outsource core payment application functions to allow internal resources to act as center of excellence, focusing on value-added work and complex queries

• Technology:

• Automate processing of trustee payments and enable seamless alignment between trustee databases, debt collectors and bankruptcy attorney systems

• Enhance system capabilities that automatically allocate funds to pre-petition and post-petition payment applications

• Centralize data sources that provide accurate account information to teams across bankruptcy unit

• Define clear target-state architectural blueprint paying out business capabilities, target technology stack and interim stages to avoid increases in technology costs without realizing benefits to the business

Current bankruptcy trends | 8

Payment reconciliation

Lack of controls and consistency around payment reconciliation processes can lead to data integrity issues and require time-consuming manual workarounds and remediation efforts. Financial institutions would benefit from streamlined payment reconciliation processes, assisted by a centralized data source that has natural control points throughout the bankruptcy life cycle.

Risks Potential solutions/industry practices • Limited functionality in legacy systems regarding

nonconforming loan amortization products and optional products creates the need for manual ledgers.

• Ineffective communication/documentation across bankruptcy leads to redundant downstream processes (e.g., reconciliation of payment history) and inability to update systems following bankruptcy events (e.g., chapter conversion).

• Insufficient control points prevent bankruptcy ledgers from being balanced prior to critical processes in an efficient manner.

• Inability to accurately assess and code fees throughout the bankruptcy life cycle poses financial risks to both the borrower and financial institution.

• Limited quality controls over manual adjustments create a high-risk environment with significant impacts to the integrity of the system of record and decrease success of downstream processes.

• System limitations prevent ledgers from accurately tracking payment history after certain bankruptcy events, such as agreed orders, loan modifications or stipulated agreements.

• Operations:

• Increase transparency and management oversight, including formal quality assurance programs as well as documented performance metrics/SLAs, increase accountability and improve performance management

• Use control points to verify accurate payment history prior to critical stages in the bankruptcy life cycle

• Increase communication and knowledge sharing with other bankruptcy teams to encourage account coding and documentation in appropriate and standardized manners in order to facilitate downstream process execution

• Integrate data governance model to provide standards and policies to promote consistency in resolving data integrity issues in ledgers

• Technology:

• Increase system functionality to monitor and track specific loan types, such as Home Equity Line of Credit (HELOC) and Daily Simple Interest (DSI) loans

• Enhance systems to enable automated bankruptcy plan ledgers and contractual ledgers after bankruptcy events, such as loan modifications, agreed orders and stipulated agreements, and to reduce reliance on wrapper tools to update systems of record

Current bankruptcy trends | 9

Proof of Claim/Amended Proof of Claim/Motion for Relief

Control gaps, inadequate training, system deficiencies, lack of comprehensive management reporting and high attorney revision rates hinder accurate and timely POCs, Amended Proofs of Claim (APOCs) and MFRs. Financial institutions are required to follow POC/APOC and MFR filing requirements set forth by the OCC and NMS guidelines, as well as the US Bankruptcy Code, in order to avoid fines and other consequences. Furthermore, filing accurate and timely POC/APOCs and MFRs limits negative financial impacts to the institution and delays in collection, foreclosure or eviction activities.

Risks Potential solutions/industry practices • Lack of resource capacity to support volume, as well

as limited subject-matter knowledge, limits the ability to resolve issues.

• Inadequate training on complex scenarios as well as new bankruptcy forms that went into effect December 2015 causes high volume of escalations, and limited cross-training leads to imbalance of resources across the team.

• Process and control deficiencies lead to inaccurate and untimely filings, disclosure of non-public personal information (NPPI), and unsustainable processes.

• System deficiencies due to data integrity issues among internal systems result in lack of visibility around status of POC/APOC and MFR populations and inaccurate/untimely filings.

• Inadequate law firm oversight resulting from servicers failing to monitor adherence to bankruptcy legal requirements (i.e. timeliness and accuracy of POCs/APOCs and MFRs).

• High attorney error rates cause process bottlenecks, as files are sent back-and-forth for correction, and delay filings.

• Insufficient management of attorney legal filing credentials increases risk of filings with incorrect attorney information.

• Operations:

• Realign management teams and executive leadership to increase oversight, align expertise, and allow flexibility in response to volume increases

• Use cross-training opportunities to promote staff flexibility and hold regular management-led trainings to bridge gaps between problems associates face and issues identified by leadership

• Contract third-party vendors to support volume and help reduce out-of-standard populations

• Implement 100% in-line quality assurance of referrals and validations, as accuracy controls checks prior to filing, to enable adherence to current US Bankruptcy Code and NPPI redaction

• Develop enhanced management controls to improve accuracy and efficiency, meet referral requirements, and satisfy regulatory and investor guidelines

• Enhance attorney scorecards to better measure performance and hold legal partners accountable for adherence to timelines and document accuracy

• Centralize tracking of attorney filing credentials, including review of credential controls as part of vendor/attorney reviews

• Technology:

• Consolidate and enhance key reports to manage referral timelines set forth by NMS, Fannie Mae, Freddie Mac and bankruptcy courts and track referral population process, defects, productivity and risk/issues

• Consolidate data/tasking/timelines through a centralized workflow portal

Current bankruptcy trends | 10

Payment Change Notification

Uncontrollable PCNs and system deficiencies may lead to filings after the required 21-day notification period. Financial institutions are required to file a PCN 21 days before the payment change goes into effect. However, due to the number of uncontrollable factors that may contribute to a PCN trigger within the 21-day window, it is crucial to have the right system triggers established and to have extensive reporting around controllable and uncontrollable PCNs.

Risks Potential solutions/industry practices • Uncontrollable PCNs, which are payment changes

that occur less than 25 days to the effective date (e.g., HELOC, interest only, loan modifications), are generated within the 21-day advance notice window and are automatically late.

• Limited operational reporting to identify controllable and non-controllable populations and to track timely PCN filings results in lack of transparency into volume progress and timeliness.

• System deficiencies cause transmission and processing errors, which result in missed PCNs. Additionally, limited available historical data fails to give associates a full view into the loan history.

• Limited visibility into PCN exceptions/impediments can lead to increased out-of-standard inventory.

• Lack of transparency into removed PCNs can cause lack of traceability into which PCNs are removed automatically by the system, or manually by an associate, without proper validation.

• Inadequate law firm oversight resulting from servicers failing to monitor adherence to bankruptcy legal requirements (i.e. timeliness and accuracy of PCNs).

• Insufficient management of attorney legal filing credentials increases the risk of filings with incorrect attorney information.

• Operations:

• Develop manager and team lead procedures to monitor and track PCN production, escalation and removals

• Deploy new control routines to review, assess and resolve QA and QC findings

• Enhance attorney scorecards to better measure performance and hold legal partners accountable for adhering to timelines and document accuracy

• Centralized tracking of attorney filing credentials, including review of credential controls as part of vendor/attorney reviews

• Technology:

• Enhanced reporting to highlight uncontrollable vs. controllable loan populations, reconcile PCNs that are triggered against PCNS received in workflow tools, and receive additional insight into coming-due, filed late or not-filed PCNs

• Enhance PCN systems by implementing a PCN exception queue for actively tracking and monitoring PCN objections and out-of-standard filings, expanding historical PCN activity to show details throughout the life of the loan, and modifying system logic to prevent false triggers due to initial escrow analysis

Current bankruptcy trends | 11

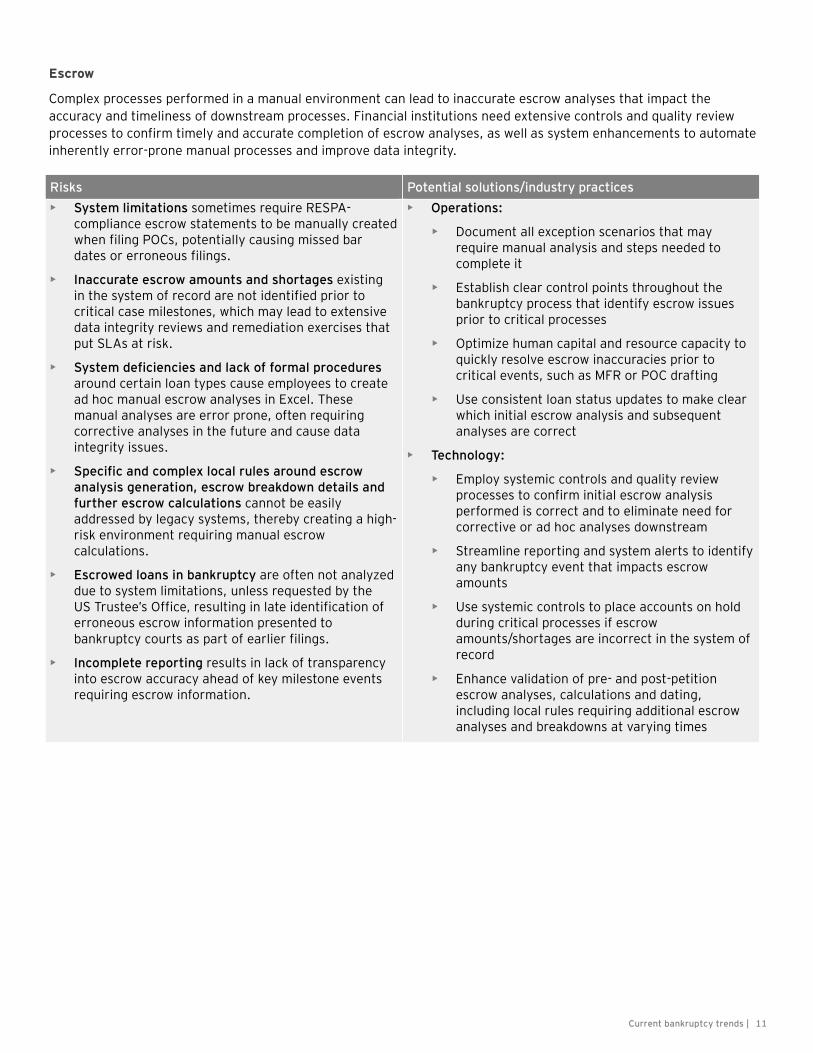

Escrow

Complex processes performed in a manual environment can lead to inaccurate escrow analyses that impact the accuracy and timeliness of downstream processes. Financial institutions need extensive controls and quality review processes to confirm timely and accurate completion of escrow analyses, as well as system enhancements to automate inherently error-prone manual processes and improve data integrity.

Risks Potential solutions/industry practices • System limitations sometimes require RESPA-

compliance escrow statements to be manually created when filing POCs, potentially causing missed bar dates or erroneous filings.

• Inaccurate escrow amounts and shortages existing in the system of record are not identified prior to critical case milestones, which may lead to extensive data integrity reviews and remediation exercises that put SLAs at risk.

• System deficiencies and lack of formal procedures around certain loan types cause employees to create ad hoc manual escrow analyses in Excel. These manual analyses are error prone, often requiring corrective analyses in the future and cause data integrity issues.

• Specific and complex local rules around escrow analysis generation, escrow breakdown details and further escrow calculations cannot be easily addressed by legacy systems, thereby creating a high-risk environment requiring manual escrow calculations.

• Escrowed loans in bankruptcy are often not analyzed due to system limitations, unless requested by the US Trustee’s Office, resulting in late identification of erroneous escrow information presented to bankruptcy courts as part of earlier filings.

• Incomplete reporting results in lack of transparency into escrow accuracy ahead of key milestone events requiring escrow information.

• Operations:

• Document all exception scenarios that may require manual analysis and steps needed to complete it

• Establish clear control points throughout the bankruptcy process that identify escrow issues prior to critical processes

• Optimize human capital and resource capacity to quickly resolve escrow inaccuracies prior to critical events, such as MFR or POC drafting

• Use consistent loan status updates to make clear which initial escrow analysis and subsequent analyses are correct

• Technology:

• Employ systemic controls and quality review processes to confirm initial escrow analysis performed is correct and to eliminate need for corrective or ad hoc analyses downstream

• Streamline reporting and system alerts to identify any bankruptcy event that impacts escrow amounts

• Use systemic controls to place accounts on hold during critical processes if escrow amounts/shortages are incorrect in the system of record

• Enhance validation of pre- and post-petition escrow analyses, calculations and dating, including local rules requiring additional escrow analyses and breakdowns at varying times

Current bankruptcy trends | 12

Use of third-party vendors

Inadequate management and supervision of third-party vendors, including attorneys, may lead to US Bankruptcy Code violations and case delays due to erroneous document drafting and inappropriate disclosure of sensitive borrower information. Third-party vendors are often retained to assist with increased volume, draft legal filings, or outsource inefficient processes. When using third parties, financial institutions must maintain proper oversight and security measures to protect borrower information from exposure and reduce likelihood of erroneous filings.

Risks Potential solutions/industry practices • Security concerns and difficulty obtaining access for

third-party vendors dealing with sensitive information often require financial institutions to transmit data outside of their firewalls.

• Working outside the system of record can cause audit issues if data is not property transmitted back to original system.

• Lack of experience among contracted third-party vendors in handling complex loans may result in increased errors and impede case progress.

• Limited reporting on progress and accomplishments can make updating executive leadership and key stakeholders difficult.

• Insufficient quality control processes result in failure to prevent and detect third-party vendor data integrity and erroneous document preparation trends.

• Inadequate law firm oversight resulting from servicers failing to monitor adherence to bankruptcy legal requirements (i.e. timeliness and accuracy of bankruptcy legal documents).

• High error rates cause process bottlenecks as files are sent back-and-forth for corrections, resulting in untimely filings.

• Insufficient management of attorney legal filing credentials increases risk of filings with incorrect attorney information.

• Operations:

• Work in system of record whenever possible in order to verify that third-party vendor work is captured in the original system and to avoid problems with transmitting and obtaining data outside established firewalls

• Increase training prior to beginning projects and leverage internal associates to train third-party vendor counterparts

• Use subject-matter resources from third-party vendors to assist with complex projects and avoid mishandling complex loans

• Establish robust QC processes to enable early detection of error trends and allow for escalation and remediation of training gaps, system problems, and automated and manual errors

• Enhance attorney scorecards to better measure performance and hold legal partners accountable for adhering to timelines and document accuracy

• Centralize tracking of attorney filing credentials, including review of credential controls as part of vendor/attorney reviews

• Technology:

• Establish reporting requirements for third-party vendors to develop and distribute on regular basis in order to show progress through production volume and identify risks and issues

• Integrate third-party feeds to tie bankruptcy alerts, trustee information and time-stamped court filings into the system of record

Current bankruptcy trends | 13

Ernst & Young LLP contacts Maureen Day Partner, Advisory Financial Services +1 212 773 2783 [email protected]

Paul Nagai Principal, Advisory Financial Services +1 212 773 9337 [email protected]

Todd Rosenkranz Executive Director, Advisory Financial Services +1 214 969 8479 [email protected]

Amy Gennarini Principal, Advisory Financial Services Financial Services +1 212 773 2696 [email protected]

Chris Pedersen Senior Manager, Advisory Financial Services +1 312 879 2550 [email protected]

Naga Tumuluri Senior Manager, Advisory Financial Services +1 212 773 3675 [email protected]

To learn more about our services and how we can help, please visit www.ey.com/us/financialservices

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP. All Rights Reserved.

BSC No. 1601-1808772 SCORE no. CK1046 ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com