Embed Size (px)

Citation preview

CTMA WEALTH MANAGEMENT

2018 Review

CTMA Wealth Management

Thank you for your business. We respect and appreciate the trust you have placed in us. We appreciate any and all questions. Please let us know what you are thinking….

the better you understand, the better we understand.

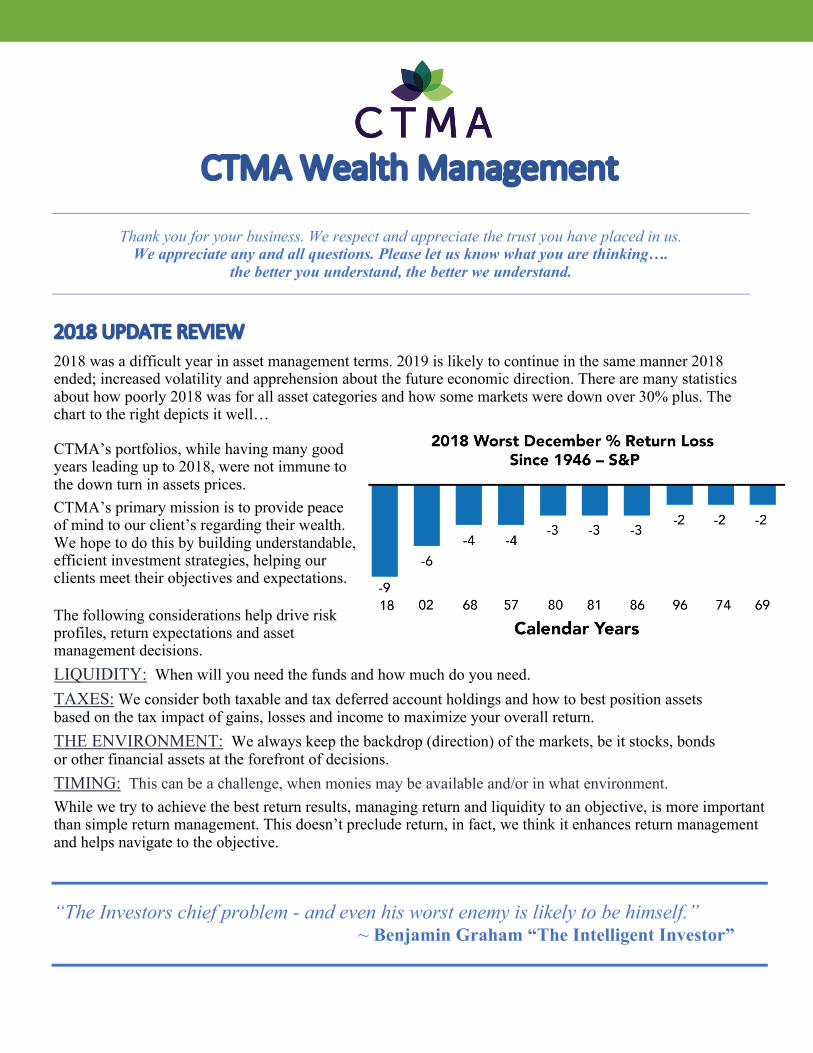

2018 UPDATE REVIEW 2018 was a difficult year in asset management terms. 2019 is likely to continue in the same manner 2018 ended; increased volatility and apprehension about the future economic direction. There are many statistics about how poorly 2018 was for all asset categories and how some markets were down over 30% plus. The chart to the right depicts it well…

CTMA’s portfolios, while having many good years leading up to 2018, were not immune to the down turn in assets prices. CTMA’s primary mission is to provide peace of mind to our client’s regarding their wealth. We hope to do this by building understandable, efficient investment strategies, helping our clients meet their objectives and expectations.

The following considerations help drive risk profiles, return expectations and asset management decisions. LIQUIDITY: When will you need the funds and how much do you need. TAXES: We consider both taxable and tax deferred account holdings and how to best position assets based on the tax impact of gains, losses and income to maximize your overall return. THE ENVIRONMENT: We always keep the backdrop (direction) of the markets, be it stocks, bonds or other financial assets at the forefront of decisions. TIMING: This can be a challenge, when monies may be available and/or in what environment. While we try to achieve the best return results, managing return and liquidity to an objective, is more important than simple return management. This doesn’t preclude return, in fact, we think it enhances return management and helps navigate to the objective.

“The Investors chief problem - and even his worst enemy is likely to be himself.” ~ Benjamin Graham “The Intelligent Investor”

CTMA WEALTH MANAGEMENT

2018 Review

2018…. THE YEAR OF “MAGICAL THINKING” We came into January with euphoria and all-time market highs. Then there was an announcement by the U.S. Government about the Budget and the ever-increasing large projected deficits. This in a close to full employment environment. It surprised the markets and they sold off; 10% in just 10 trading days. Spring came and U.S. companies, due to the new 2017 tax laws, started to repatriate funds and began buying large amounts of their own stock (e.g. Apple, Cisco, Intel, etc...) sending the market higher. July and early August may have seen the market’s most euphoric time, sending some stocks with no earnings to hit all-time highs (circa 2000 and the dotcom bubble). Not to be outdone, in October with the markets at all-time highs, The Federal Reserve policies that were announced in 2017 to shrink their Balance Sheet and raise interest rates, began to bite. The market felt the liquidity drain and started its roller-coaster ride down.

The news on Brexit, The China “Trade War” and the Mid Term Elections all helped create uncertainty. We can’t forget Bitcoin; it entered 2018 as “the alternative asset” of choice; only to have it lose close to 70% of its value in 2018. During the course of the year we reallocated from higher risk assets into cash and treasuries. For the first time in many years you could own Treasuries both for return and to balance risk. Over the past 5 years we had been mostly fully invested in growth. The shifting of assets helped. However, this didn’t stop most remaining positions from having difficulty and overall account

returns from suffering. We believe the move away from the higher risk growth, into cash, treasuries and some hedging (primarily in taxable accounts) helped to mitigate the volatility and lessen the overall losses.

“It’s a hell of a start knowing what makes you happy.” ~ Lucille Ball

2018…BRINGS A SMILE

CTMA WEALTH MANAGEMENT

2018 Review

2019 – WHAT HAPPENS NEXT? No one knows for sure how the future will play out. The biology of systems and economies shifts as they flow. The flow of economies and by extension money shifts and changes value over time. You have to base things on reason and probabilities, understanding the need to be flexible as things change.

We’ve attached an article from the October issue of the Economist. It shows how the economics of the world have and are shifting. Demographics, systems and the laws of nature do not change because of who holds the microphone. Although the changes may be slowed and or disrupted, life is invariably tied to rules. People by and large, want to do better wherever they may live.

Reflecting back to late 2017, the overall slowdown in the world started in China and not because of a trade war. Over the past 40 years the Chinese have done amazing things. They took close to a billion people out of abject poverty building cities, roads and systems to support a long-term sustainable society.

Some perspective, in 2018 approximately 17.2 million passenger vehicles were sold in the U.S.A., in China they sold approximately 23.8 million.

China and the rest of the world is paying the price for its rapid growth. The debts incurred were significant and like with most debt cycles, some of the debts are bad and will need to be written off. It will take time.

Will the excess leverage change the course of history? Most likely not. Just slow it down. How long will depend on policy making decisions.

The Eastern World, China, India and the other Asian economies will continue to grow and prosper. We have, in some portfolios HDB & DBBS, and will continue to take positions in theses area, mostly through well run banks, and Indexes designed to capture the expected growth.

As we ended 2018, the U.S. markets were catching up with the rest of the world, which has been repricing risk and selling markets. We believe the set-up of the new Congress and the Federal Reserve’s positioning of money and interest rates, as well as other central banks, will put pressure on fund flows and volatility will continue.

We continue to hold increased cash and treasury positions to help offset volatility, taking advantage of changing interest rates and to take advantage of other markets when the business cycle stabilizes. Holding stable businesses, paying (see yield) you to own them is a key strategy entering 2019.

However, the cycle will change, and funds will flow to the places where growth is occurring – Domestically and Internationally.

“It is not the strongest of the species that survives. Nor the most intelligent – but the one that is the most responsive to change.” ~ Charles Darwin

CTMA WEALTH MANAGEMENT

2018 Review

“Talent wins games, but teamwork and intelligence wins championships.” ~ Michael Jordan

Exchange Traded Funds (ETFs) We utilize these investments to provide broad exposure to a market and include SPY, QQQ, VBK, INDA, CWI and others. They are designed to capture the risk and return of a market and are an effective risk return strategy. AT&T (T) The stock was down. The company is absorbing the transition in its business from telephone to media and from wireline to 5G. Its dividend yield is appx 7% and although it has increased its debt to restructure itself for the future, most of its debt maturities are years away. They are core holding for income and value. Gas Log Partners (GLOP) This is a Liquefied Natural Gas Shipping Company paying an appx 11% dividend yield. Natural Gas is now the fuel of choice and will continue to see worldwide growth as many Countries (China, India, Europe, Egypt etc...) continue to grow the market. It’s a volatile position due to its smaller market capitalization or size. However, it’s extremely well run and since we began owning it (2014), the company has delivered on what it said it was going to do. It’s an MLP or Master Limited Partnership. Gas Log Ltd (GLOG) The largest publicly traded Independent Liquefied Natural Gas Shipping Company in the world. GLOG is the General Partner of GLOP. Through the affiliation it operates GLOPs ships. They are in a growing market and have a track record of success. It has an appx dividend yield of 3.5%. Paychex (PAYX) The Company has an exceptional track record; no long-term debt, has an appx. 3.4% dividend yield and is in the employment and staffing business. CVS Since 2014 when it announced it would stop selling cigarettes, the company has been transforming into a health & wellness company. CVS acquired Aetna in 2018. The company will be absorbing the business and should now be focused on growing its core wellness model. It has an appx dividend yield of 3%. Verizon (VZ) After purchasing AOL & Yahoo they recognized this was a mistake and are now all about 5G or the next generation of communication. It has an appx dividend yield of 4.4%.

Position Updates in Brief Below is a brief synopsis of positions. You may own some and /or all of these positions. It largely depends on your liquidity needs, risk profile and timing on when you have funds available. Some of the largest holdings, we believe can be held through the market cycle with the dividends invested into other areas as the market cycles in 2019 and beyond.

CTMA WEALTH MANAGEMENT

2018 Review

Royal Bank of Canada (RY) One of, if not the best run bank in Canada. It has an appx dividend yield of 4.2%.

J.P Morgan (JPM) One of, if not the best run bank in the U.S.A. It has an appx dividend yield of 3.3%. British Petroleum (BP) This worldwide oil company managed through the spill in the gulf and is now positioned to generate the cash required to meet its long-term capital needs to grow and has an appx dividend yield of 6.45%. Pfizer, Merck & Johnson & Johnson (PFE, MRK, JNJ) All of these drug companies pay dividends, are well capitalized and are well positioned in their respective market places.

General Motors & Ford (GM, F) These two have been tough to own. The narrative of the China story, self-driving cars, electric “will rule the world soon” and remember “the industry went bankrupt” has frightened many investors. However, each understands the problems they are facing and are actively dealing with the real economics of the industry (to fully understand you may want to check out their respective websites and listen to the investor conference calls). They each have an appx dividend yield of 4.5% (GM) and 7.3% (F) respectively and are income and value-based investments. HDFC Bank (HDB) The second largest bank in India. Zoetis (ZTS) Large provider of animal drugs medicines. Other positions, REITS & MLPs Long dated assets with debt were repriced down. Even though they have cash flow to meet the debt service and assets to support the underlying businesses. Sanchez Energy A small oil company we owned was extremely disappointing. If you want to learn more, please let us know.

YIELD…WHAT DOES IT MEAN? We’re often asked what does yield mean; be it interest, distributions or dividends and how do I understand or calculate it. Yield is the amount of $$$’s paid to the owner of an asset. It could be interest paid from owning Cash, Bonds, and Treasuries, Dividends from Stocks, Distributions from Master Limited Partnerships (MLPs) or Real Estate Investment Trusts (REIT). The amount paid is based on the type of security and is almost always expressed as an annual percentage. By way of example: A stock pays a $1 dividend on a quarterly basis and the stock on the day of the payment is worth $80. The dividend yield would be 5% based on ($1 x 4 payments) = $4/$80 or 5%. If the price of the stock goes up or down during the next quarter and the dividend stays at $1 then the yield will change. By way of example: A stock pays a $1 dividend on a quarterly basis and the stock on the day of the payment is now worth $100. The dividend yield would be 4 % based on ($1 x 4 payments) = $4/$100 or 4%.

CTMA WEALTH MANAGEMENT

2018 Review

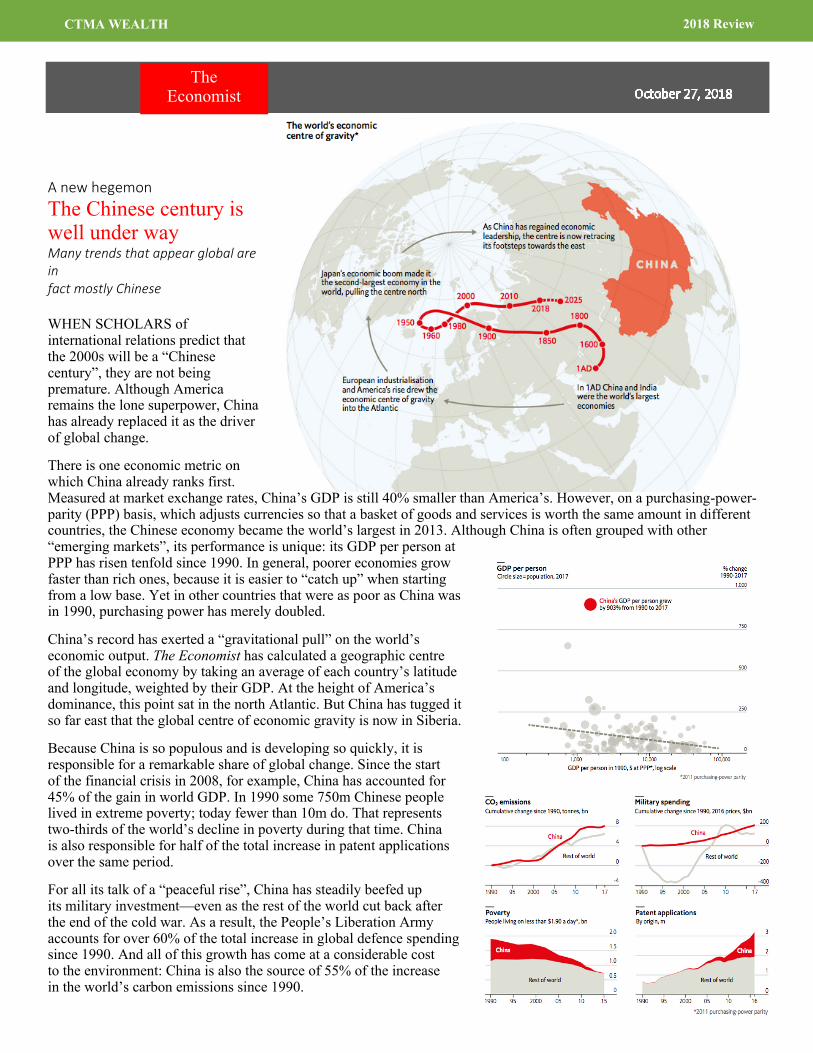

A new hegemon The Chinese century is well under way Many trends that appear global are in fact mostly Chinese

WHEN SCHOLARS of international relations predict that the 2000s will be a “Chinese century”, they are not being premature. Although America remains the lone superpower, China has already replaced it as the driver of global change. There is one economic metric on which China already ranks first. Measured at market exchange rates, China’s GDP is still 40% smaller than America’s. However, on a purchasing-power-parity (PPP) basis, which adjusts currencies so that a basket of goods and services is worth the same amount in different countries, the Chinese economy became the world’s largest in 2013. Although China is often grouped with other “emerging markets”, its performance is unique: its GDP per person at PPP has risen tenfold since 1990. In general, poorer economies grow faster than rich ones, because it is easier to “catch up” when starting from a low base. Yet in other countries that were as poor as China was in 1990, purchasing power has merely doubled. China’s record has exerted a “gravitational pull” on the world’s economic output. The Economist has calculated a geographic centre of the global economy by taking an average of each country’s latitude and longitude, weighted by their GDP. At the height of America’s dominance, this point sat in the north Atlantic. But China has tugged it so far east that the global centre of economic gravity is now in Siberia. Because China is so populous and is developing so quickly, it is responsible for a remarkable share of global change. Since the start of the financial crisis in 2008, for example, China has accounted for 45% of the gain in world GDP. In 1990 some 750m Chinese people lived in extreme poverty; today fewer than 10m do. That represents two-thirds of the world’s decline in poverty during that time. China is also responsible for half of the total increase in patent applications over the same period. For all its talk of a “peaceful rise”, China has steadily beefed up its military investment—even as the rest of the world cut back after the end of the cold war. As a result, the People’s Liberation Army accounts for over 60% of the total increase in global defence spending since 1990. And all of this growth has come at a considerable cost to the environment: China is also the source of 55% of the increase in the world’s carbon emissions since 1990.

The Economist

CTMA WEALTH MANAGEMENT

2018 Review

Want to know more? Ask Melinda

CTMA UPDATES

“And in the end, it’s not the years in your life that count. It’s the life in your years.” ~ Abraham Lincoln

Retirement Asset Management Program “RAMP”: Over the past few years we’ve made an effort to build a product which delivers a valuable opportunity to our small and mid-size accounts. It’s a Smart Simple Solution to retirement needs (IRAs, 401ks & Simple Plans) using low cost Exchange Traded Funds. There are 4 portfolios (Conservative, Balanced, Growth & Aggressive) and each is allocated to an objective. They are rebalanced monthly, helping with volatility and are designed to be flexible while meeting the return objective.

Website We’ve recently updated our website to provide more information to our clients on our philosophy, products and services. Our site provides further understanding of CTMA’s focus to provide Smart Simple Solutions. Please take a moment to explore it. You’ll find more life quotes there.

Please visit the site by following the link below and make sure you check out our newest team member/mascot Harley Rose on the Insights page.

www.ctmawealth.com/meet-harley Referrals:

We truly appreciate our clients telling others how we work and the trust you show! THANK YOU!

Melinda Torgerson Investment Advisor [email protected]

![Common Wealth Final[1]](https://img.pdfslide.us/doc/110x75/577d255a1a28ab4e1e9e9791/common-wealth-final1.jpg)