Embed Size (px)

DESCRIPTION

enoy.

Citation preview

Session 07 © Furrer 2002-2008 1

Corporate StrategyFall 2008

Session 7 - Lecture 3

Corporate Governance

Dr. Olivier Furrer

Office: TvA 1-1-11, Phone: 361 30 79e-mail: [email protected]

Office Hours: only by appointment

Session 07 © Furrer 2002-2008 2

Corporate Governance

• Market, hierarchy, and the limits to the scope of the firm. => Transaction Costs Theory.(Williamson, 1975, 1985)

• Principals, agents, and the limits of the control mechanisms. => Agency Theory.(Fama and Jensen, 1983)

• Stakeholders, Stewards, and the limits of transaction and agency theories. (Carroll, 1979, 2003; Davis, Schoorman & Donaldson, 1997; Ghoshal, 2006)

Session 07 © Furrer 2002-2008 3

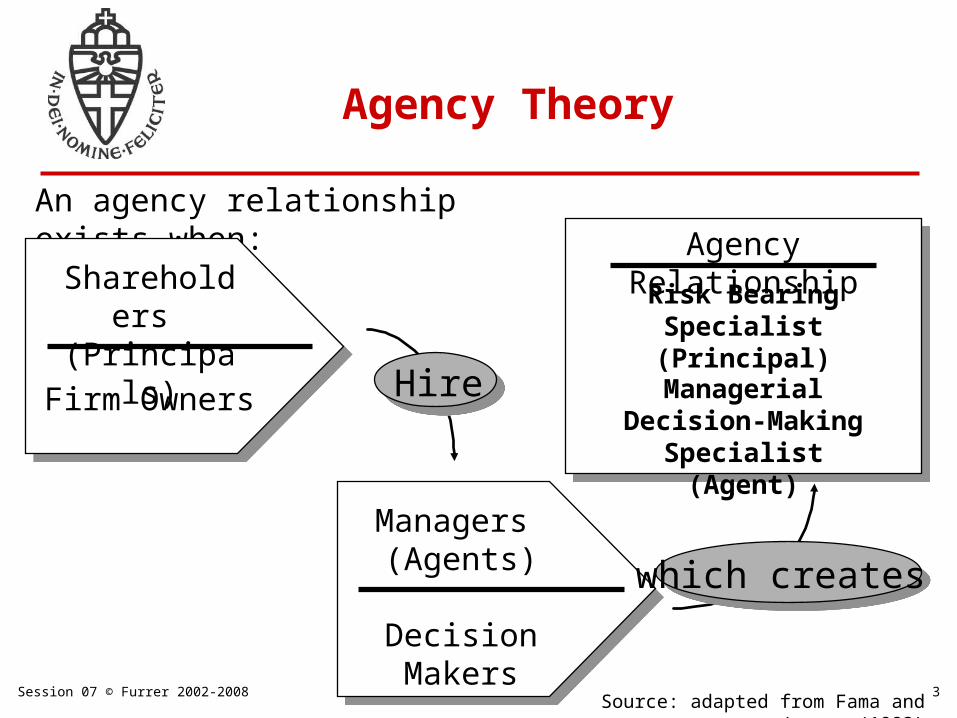

An agency relationship exists when:

Shareholders (Principals)

Firm Owners

Agency Relationship

Risk Bearing Specialist(Principal)

Managers (Agents)

DecisionMakers

which creates

Managerial Decision-Making Specialist

(Agent)

Hire

Agency Theory

Source: adapted from Fama and Jensen (1983)

Session 07 © Furrer 2002-2008 4

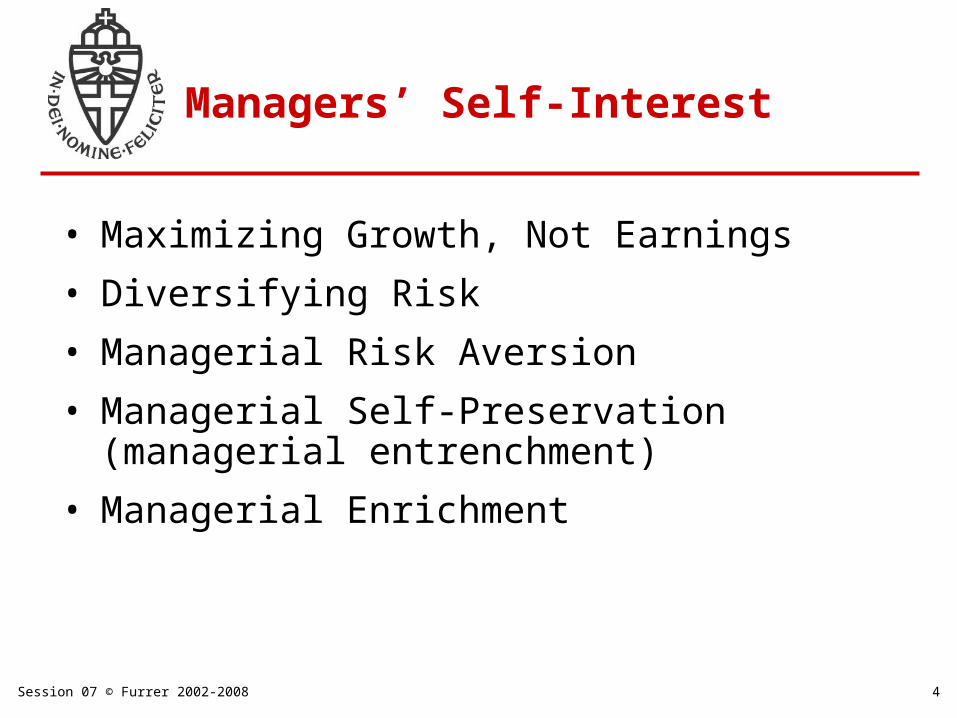

Managers’ Self-Interest

• Maximizing Growth, Not Earnings

• Diversifying Risk

• Managerial Risk Aversion

• Managerial Self-Preservation (managerial entrenchment)

• Managerial Enrichment

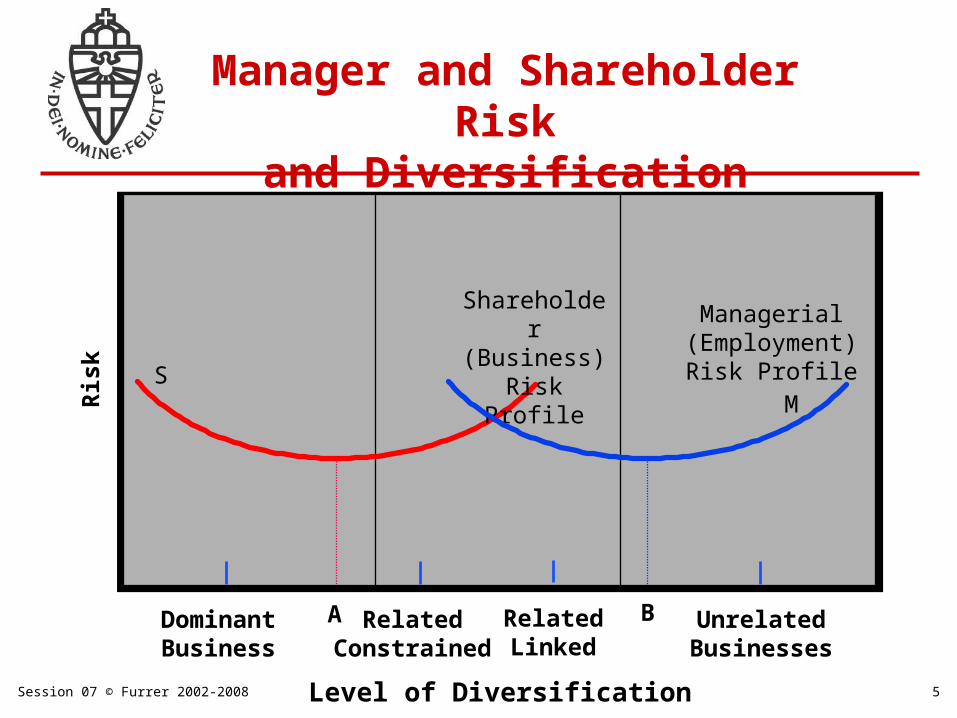

Session 07 © Furrer 2002-2008 5Level of Diversification

Manager and Shareholder Riskand Diversification

Ris

k

DominantBusiness

UnrelatedBusinesses

RelatedConstrained

RelatedLinked

Shareholder (Business) Risk

Profile

Managerial(Employment) Risk

ProfileSM

A B

Session 07 © Furrer 2002-2008 6

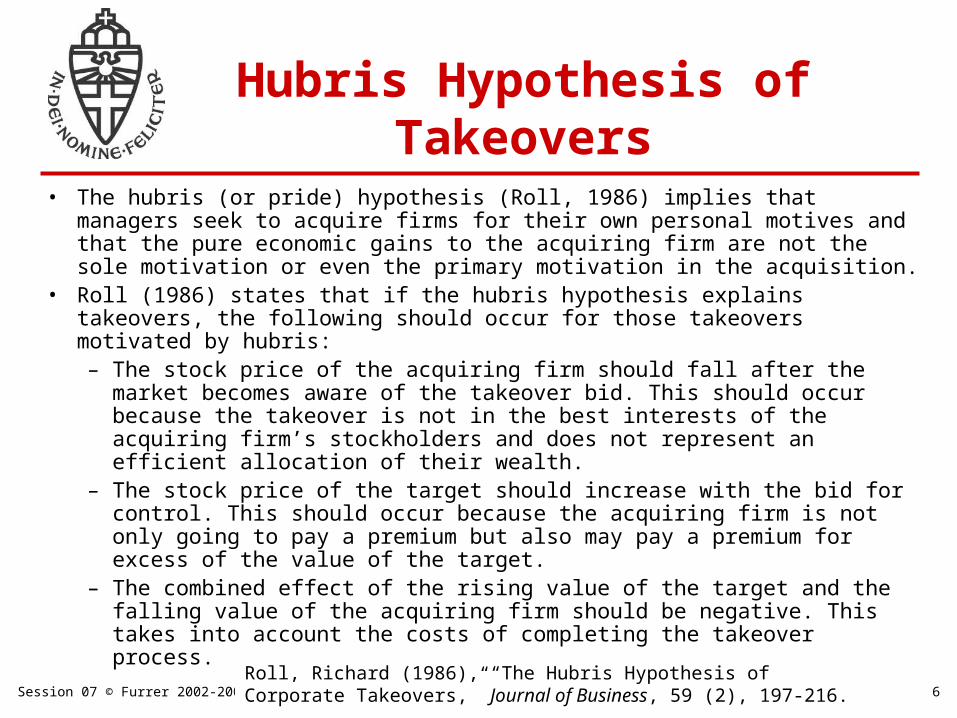

• The hubris (or pride) hypothesis (Roll, 1986) implies that managers seek to acquire firms for their own personal motives and that the pure economic gains to the acquiring firm are not the sole motivation or even the primary motivation in the acquisition.

• Roll (1986) states that if the hubris hypothesis explains takeovers, the following should occur for those takeovers motivated by hubris:– The stock price of the acquiring firm should fall after the market becomes

aware of the takeover bid. This should occur because the takeover is not in the best interests of the acquiring firm’s stockholders and does not represent an efficient allocation of their wealth.

– The stock price of the target should increase with the bid for control. This should occur because the acquiring firm is not only going to pay a premium but also may pay a premium for excess of the value of the target.

– The combined effect of the rising value of the target and the falling value of the acquiring firm should be negative. This takes into account the costs of completing the takeover process.

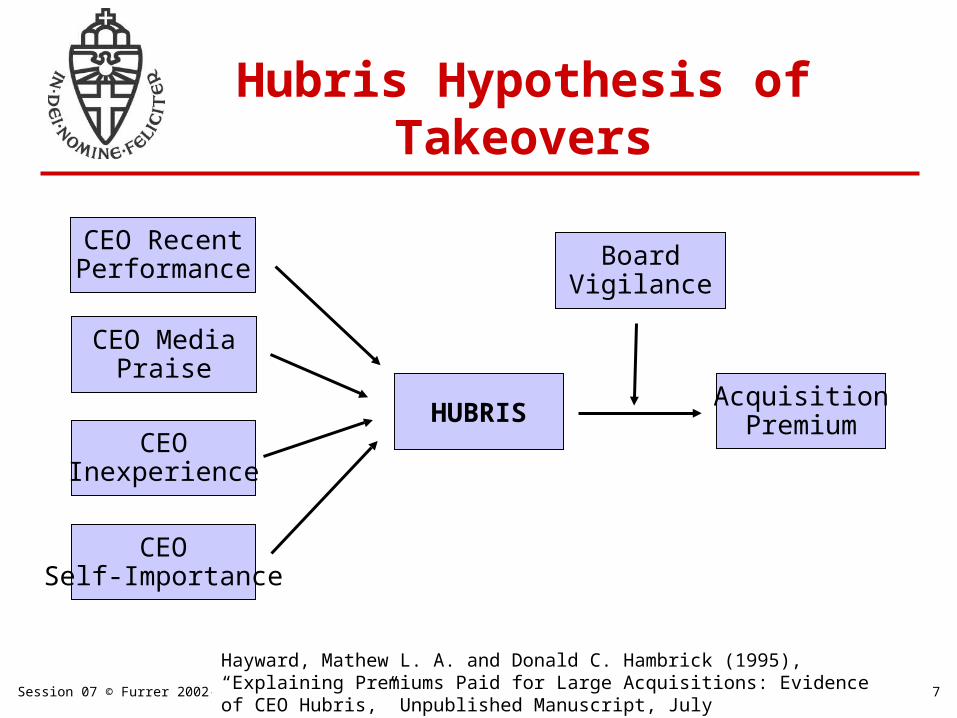

Hubris Hypothesis of Takeovers

Roll, Richard (1986), “The Hubris Hypothesis of Corporate Takeovers,” Journal of Business, 59 (2), 197-216.

Session 07 © Furrer 2002-2008 7

Hubris Hypothesis of Takeovers

Hayward, Mathew L. A. and Donald C. Hambrick (1995), “Explaining Premiums Paid for Large Acquisitions: Evidence of CEO Hubris,” Unpublished Manuscript, July

HUBRISAcquisition

Premium

BoardVigilance

CEO RecentPerformance

CEO MediaPraise

CEOInexperience

CEOSelf-Importance

Session 07 © Furrer 2002-2008 8

• The winner’s curse of takeovers states that bidders who overestimate the value of a target will most likely win a contest. This is due to the fact that they will be more inclined to overpay and outbid rivals who more accurately value the target.

• This result is not specific to takeovers but is the natural result of any bidding contest (Baserman and Samuelson, 1983).

• In a study of 800 acquisition from 1974 to 1983, Varaiya (1988) showed that on average the winning bid in takeover contests significantly overstated the capital market’s estimate of any takeover gains by as much as 67%.

• Varaiya (1988) measured overpayment as the difference between the winning bid premium and the highest bid possible before the market responded negatively to the bid. This study provides support for the existence of the winner’s curse, which in turn, also supports the hubris hypothesis.

The Winner’s Curse Hypothesis of Takeovers

Varaiya, Nikhil (1988), “The Winner’s Curse Hypothesis and Corporate Takeovers,” Managerial and Decision Economics, 9, 209-219.

Session 07 © Furrer 2002-2008 9

Contextual Factors thatExacerbate Agency Problems

• Antitrust Enforcement

• Life Cycle and Free Cash Flow

• Market Pressure (Quarterly Earnings)

• Executive Compensation

• Disengaged Shareholders

Session 07 © Furrer 2002-2008 10

Governance Mechanisms

Ownership Concentration

Boards of Directors

Executive Compensation

Market for Corporate Control

Multidivisional Organizational Structure

Session 07 © Furrer 2002-2008 11

Ownership Concentration

monitor management closely

time, effort and expense to monitor closely

- Large block shareholders have a strong incentive to

- Their large stakes make it worth their while to spend

- They may also obtain Board seats which enhances

their ability to monitor effectively (although financial institutions are legally forbidden from directly holding board seats)

Governance Mechanisms

Session 07 © Furrer 2002-2008 12

Boards of Directors

- Review and ratify important decisions

- Set compensation of CEO and decide when to

replace the CEO

- Lack contact with day to day operations

- Insiders- Related Outsiders- Outsiders

Governance Mechanisms

Session 07 © Furrer 2002-2008 13

Recommendations for more effective Board Governance

- Increase diversity of board members backgrounds

- Strengthen internal management and accounting

control systems

- Establish formal processes for evaluation of the board’s performance

Governance Mechanisms

Session 07 © Furrer 2002-2008 14

Salary, Bonuses, Long term incentive compensation

• Executive decisions are complex and non-routine

• Many factors intervene making it difficult to establish how managerial decisions are directly responsible for outcomes

Executive Compensation

• In addition, stock ownership (long-term incentive compensation) makes managers more susceptible to market changes which are partially beyond their control

Incentive systems do not guarantee that managers make the “right” decisions, but they do increase the likelihood that managers will do the things for which they are rewarded

Governance Mechanisms

Session 07 © Furrer 2002-2008 15

Designed to control managerial opportunism

- Corporate office and Board monitor managers’ strategic decisions

- Increased managerial interest in wealth maximization

Multidivisional Organizational Structure

Governance Mechanisms

M-form structure does not necessarily limit corporate- level managers’ self-serving actions

- May lead to greater rather than less diversification

Broadly diversified product lines makes it difficult for top-level managers to evaluate the strategic decisions of divisional managers

Session 07 © Furrer 2002-2008 16

Market for Corporate Control

Operates when firms face the risk of takeover when they are operated inefficiently

The market for corporate control acts as an important source of discipline over managerial incompetence and waste

• Changes in regulations have made hostile takeovers difficult

• Many firms began to operate more efficiently as a result of the “threat” of takeover, even though the actual incidence of hostile takeovers was relatively small

• The 1980s saw active market for corporate control, largely as a result of available pools of capital (junk bonds)

Governance Mechanisms

Session 07 © Furrer 2002-2008 17

LegislationBeginning in late 2001, several large American companies (Enron, Worldcom, etc.) experienced spectacular bankruptcies because of fraud on the part of their executives and less than optimal corporate governance practices on the part of their boards.

Sarbannes-Oxley Act- CEOs and CFOs of the largest corporations should personally sign off financial statements, certifying they are true and accurate (Penalty: up to 20-year prison sentence)- A new definition of “independent director,” also changed the rules as to how to audit firms.

Governance Mechanisms

Session 07 © Furrer 2002-2008 18

Shareholders Service Organizations and Corporate Governance Rating FirmsCompanies such as GovernanceMetrics, Moody’s, and Standard & Poor’s offer rating of corporate governance systems.

Alternative theories- Stewardship Theory (Davis, Schoorman & Donaldson, 1997)

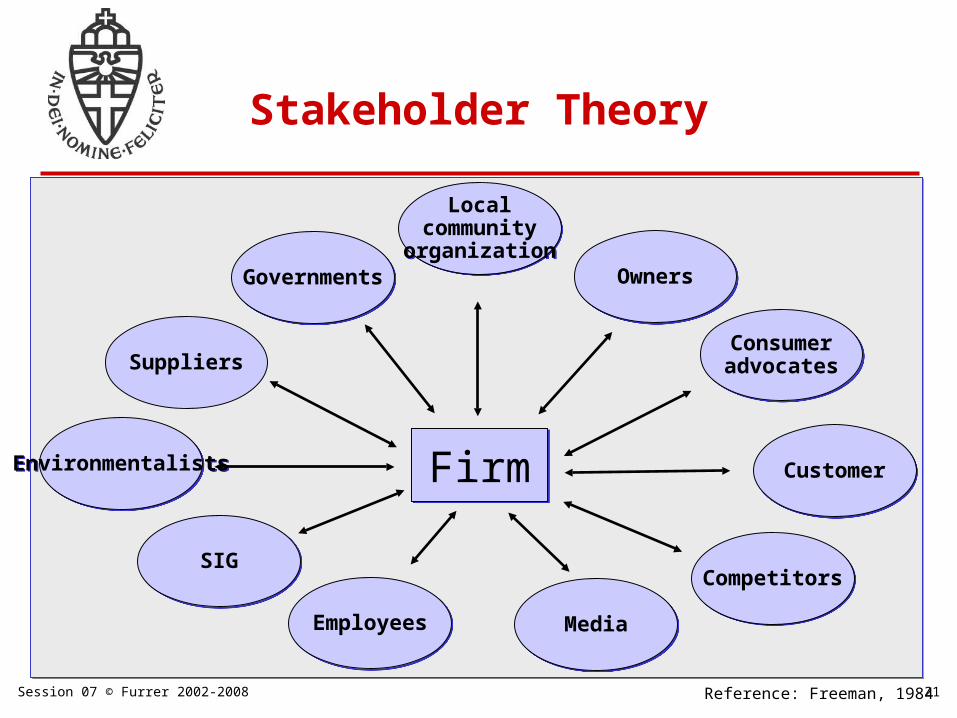

- Stakeholder Theory (Freeman, 1984)

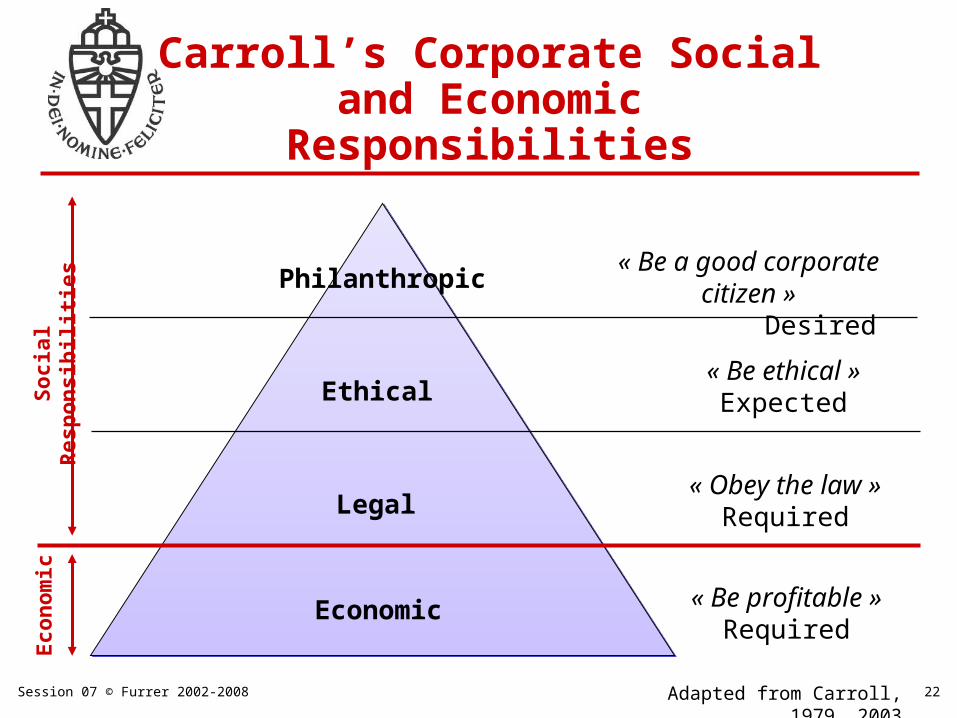

- Corporate Social Responsibility (Carroll, 1979, 2003)

Global Convergence in Corporate Governance

Governance Mechanisms

Session 07 © Furrer 2002-2008 19

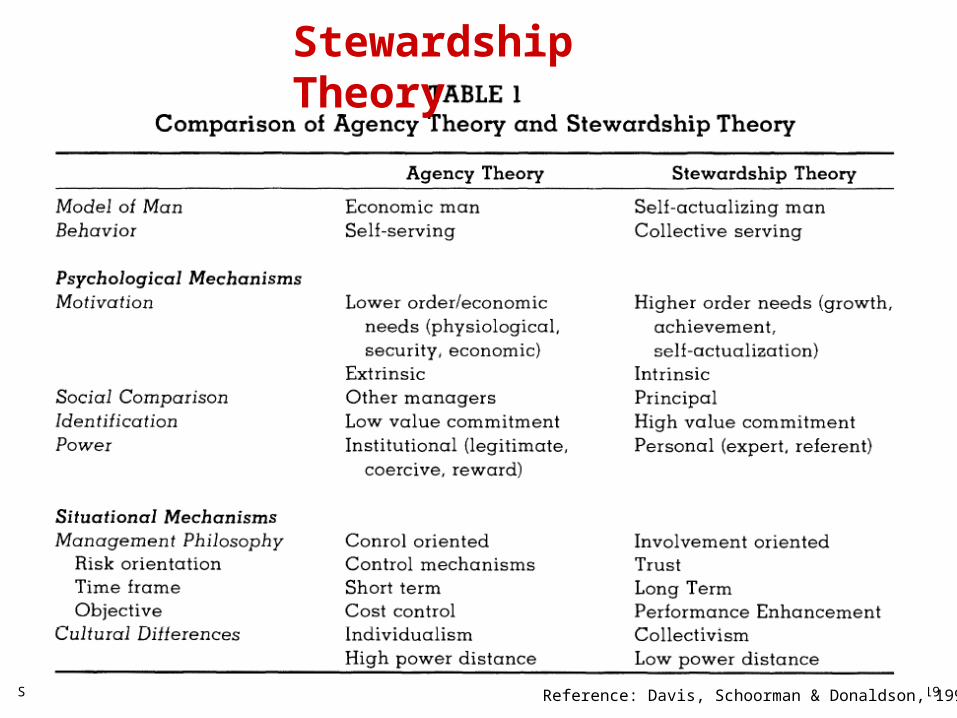

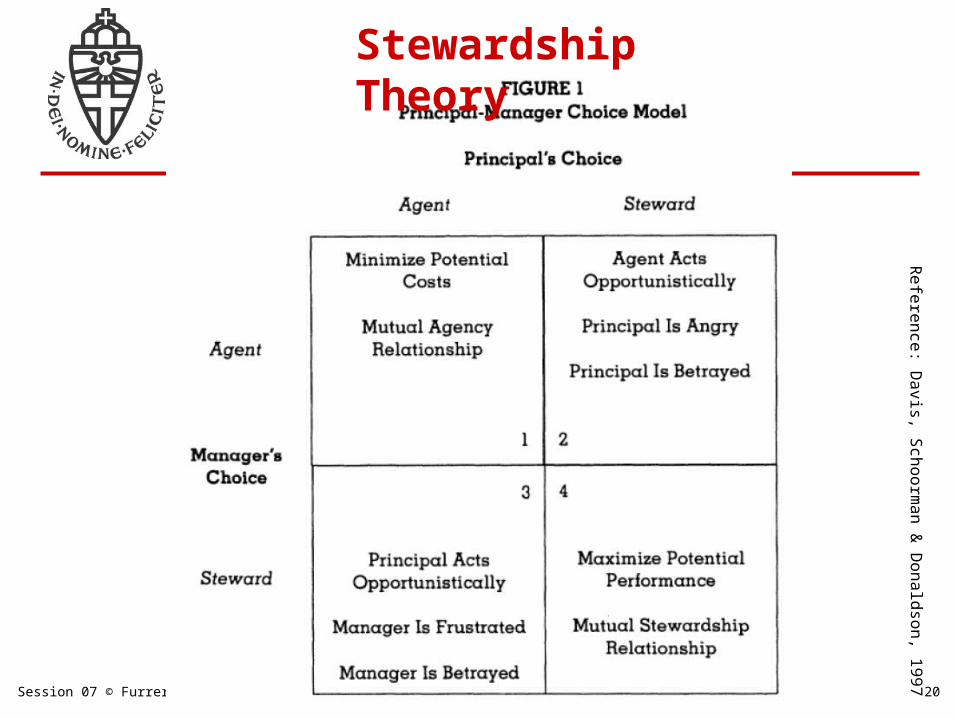

Stewardship Theory

Reference: Davis, Schoorman & Donaldson, 1997

Session 07 © Furrer 2002-2008 20

Stewardship Theory

Reference: D

avis, Schoorm

an & D

onaldson, 1997

Session 07 © Furrer 2002-2008 21

Stakeholder Theory

FirmFirm

Localcommunity

organization

Localcommunity

organizationOwnersOwners

ConsumeradvocatesConsumeradvocates

CustomerCustomer

MediaMedia

CompetitorsCompetitors

GovernmentsGovernments

Suppliers

EnvironmentalistsEnvironmentalists

SIGSIG

EmployeesEmployees

Reference: Freeman, 1984

Session 07 © Furrer 2002-2008 22

Carroll’s Corporate Social and Economic Responsibilities

Adapted from Carroll, 1979, 2003

Economic

Legal

Ethical

Philanthropic

« Be profitable »Required

« Obey the law »Required

« Be ethical »Expected

« Be a good corporate citizen »

Desired

Eco

nom

icS

ocia

l Res

pon

sib

ilit

ies