Embed Size (px)

Citation preview

CROWDFUNDINGMARKET REPORT

FACTS AND FIGURES - Q1 2014 BY CROWD VALLEY INC

IMPORTANT NOTICE

1

Please note that the provision of the information in this presentation does not create and is

not intended to create a relationship between Crowd Valley Inc. and any other person. You

are not and should not regard yourself as being a client or customer of Crowd Valley Inc. and

must not expect Crowd Valley Inc. to have any duties or responsibilities to you, act for you or

your clients, or be responsible for providing protections afforded to customers or yourselves

or be responsible for advising you in any respect. Please consult your own advisers as you

deem necessary.

The information provided herein is solely for informational purposes and should not

be construed as an attempt to solicit new clients or advertise our services for hire. The

information and opinions contained herein have been compiled or arrived at in good faith

from sources believed to be reliable; however, Crowd Valley cannot be held responsible for

its accuracy or completeness.

Crowd Valley does not engage in the offer, sale or transfer of securities. Securities may not

be offered or sold in the United States absent (i) registration under the U.S. Securities Act of

1933, as amended (the Securities Act) or (ii) an available exemption from registration under

the Securities Act. Please consult legal counsel in the appropriate jurisdiction before offering,

selling or buying securities as registration under the Securities Act or similar state legislation

may be required.

EXECUTIVE SUMMARY

2

Being an infrastructure provider for the international crowdfunding market, Crowd Valley

has gained a central position in this space. This gives the company a broad overview on

the sector’s most recent developments, with data collected on over 6,200 individuals and

companies to date. The present report differs from the previous ones, published with data

collected in Q3 and Q4 2013, as it is based on surveying a randomly-selected sample of more

than 100 individuals and companies out of the about 650 that have expressed an interest

in entering the crowdfunding market during the first quarter of 2014. Therefore, the analysis

provides probably the first data-driven insights on how the international crowdfunding sector

is developing in 2014.

The demand for crowdfunding technologies is still mainly based in the USA and it is above

all directed at equity investment models for startups. Nevertheless, during this quarter Crowd

Valley observed a steep increase in the demand for lending models and real estate platforms.

Other regions including Europe and Asia also play a major role in the crowdfunding sector,

representing significant proportions of the total demand for crowdfunding services.

In Q1 2014, the variety of organizations and professionals interested in entering this new

financial market is even more vast. In particular, many actors coming from the traditional

finance sector (i.e. broker dealers, asset managers, investment advisors, private equity funds,

etc) have shown an interest in crowdfunding. This seems to confirm what Crowd Valley

always believed: crowdfunding will bring about a paradigm shift, affecting not only the early

stage finance world, but the entire financial industry.

INTRODUCTION

3

Since the start of 2014, a few important milestones have been achieved by the crowdfunding

industry. In particular, in Europe, the UK and France have released their regulations for

securities crowdfunding, and the Spanish government has announced that it is also working

on regulatory activities. New Zealand has approved regulations for securities crowdfunding,

which are so far some of the most liberal. The European Commission has released a

communication on crowdfunding where it states that it will support the development of this

new financial source, as key for Europe’s long term growth. The UK has also allowed p2p

loans as part of Individual Savings Accounts (ISAs). All of these advances have stimulated

the attention of many actors, who are following closely the situation and are getting ready to

move the first steps into the market.

Crowd Valley has examined in this report a randomly-selected sample of more than 100

observations from across six continents, in order to unveil some of the most interesting trends

in the crowdfunding sector, which are presented in the following sections.

*Disclaimer on Data Collection

It should be taken into account that the sample used to analyze the market trends is

composed only of organizations and professionals who approached Crowd Valley due to

interest in one or more of the company’s services.

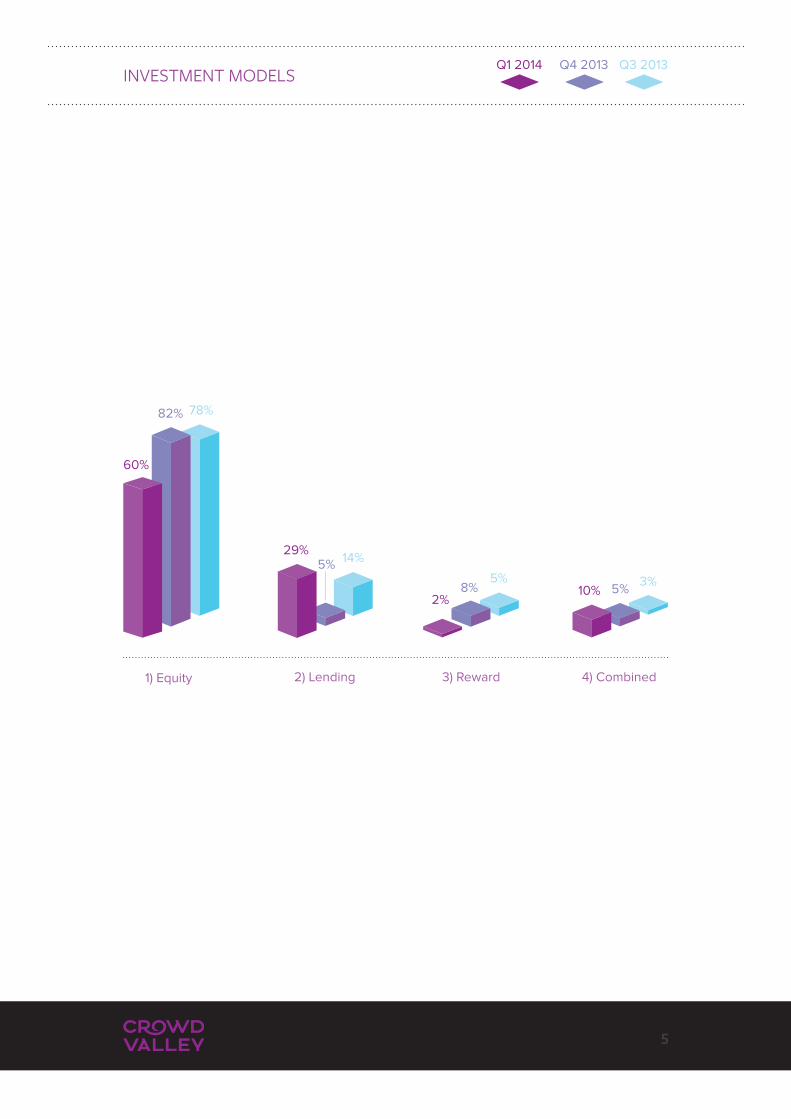

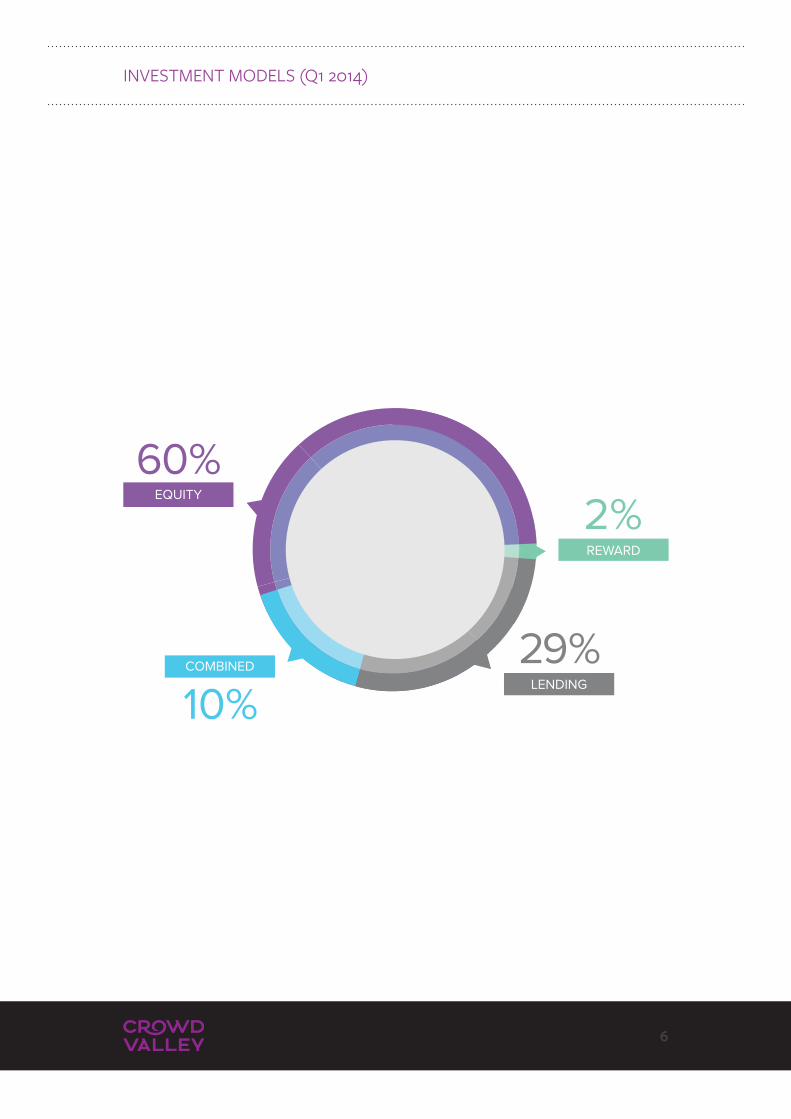

INVESTMENT MODELS

4

Being a provider of technologies, services and methodologies for securities professional

looking to get involved in this new financial market, Crowd Valley seeks to understand the

demand for the different investment models.

The company identified four main categories of investment models:

1) Equity-based crowdfunding;

2) Lending, which includes peer-to-peer lending, business loans and other forms of lending;

3) Reward-based crowdfunding;

4) Combined, which refers to those cases where two or more of the aforementioned models

are combined in one platform.

The charts below show the percentages each investment model held on the total demand for

crowdfunding operations during Q4 2013 and Q1 2014. Even though equity remains the most

demanded model, compared to the previous quarter, it has been undergone it has undergone

a decrease (from 82% in Q4 to 60% in Q1). This has been counterbalanced by a consistent

increase in the demand of lending models (from 5% in Q4 to 29% in Q1). The demand for

combined models keeps, instead, growing.

INVESTMENT MODELS

1) Equity

60%

29%5%

2%8% 10% 5%

Q1 2014 Q4 2013

82% 78%

14%

5% 3%

Q3 2013

2) Lending 3) Reward 4) Combined

5

INVESTMENT MODELS (Q1 2014)

6

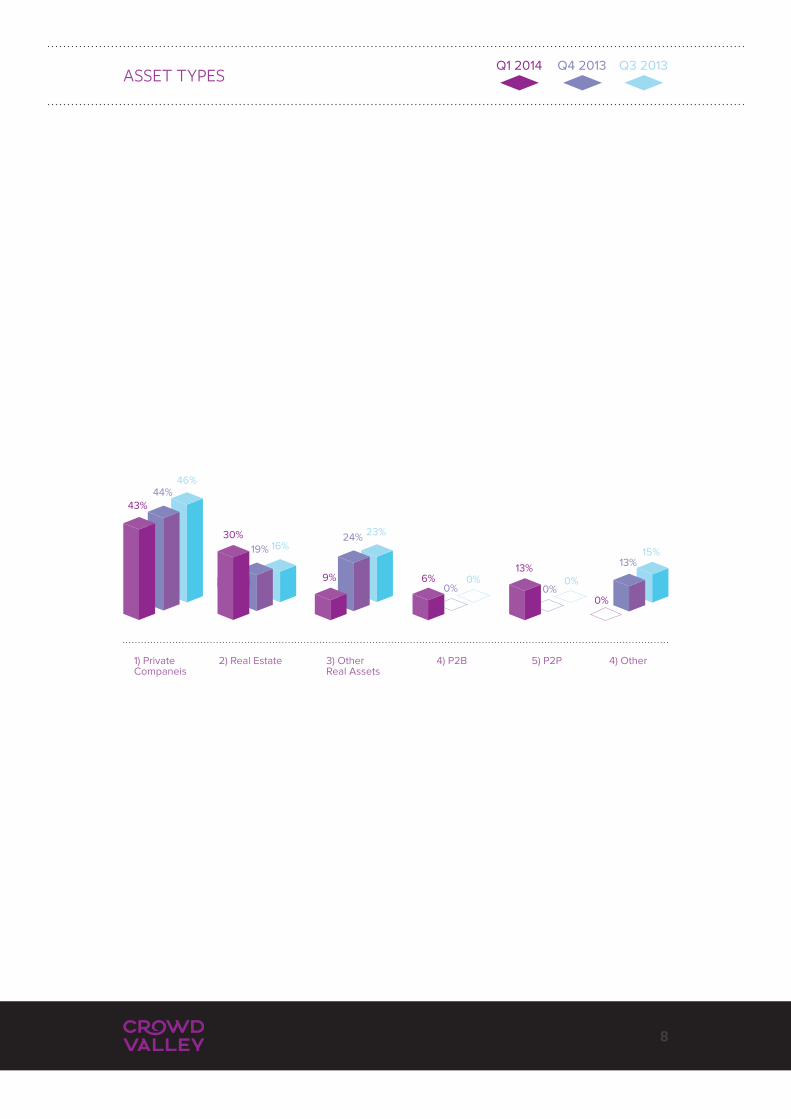

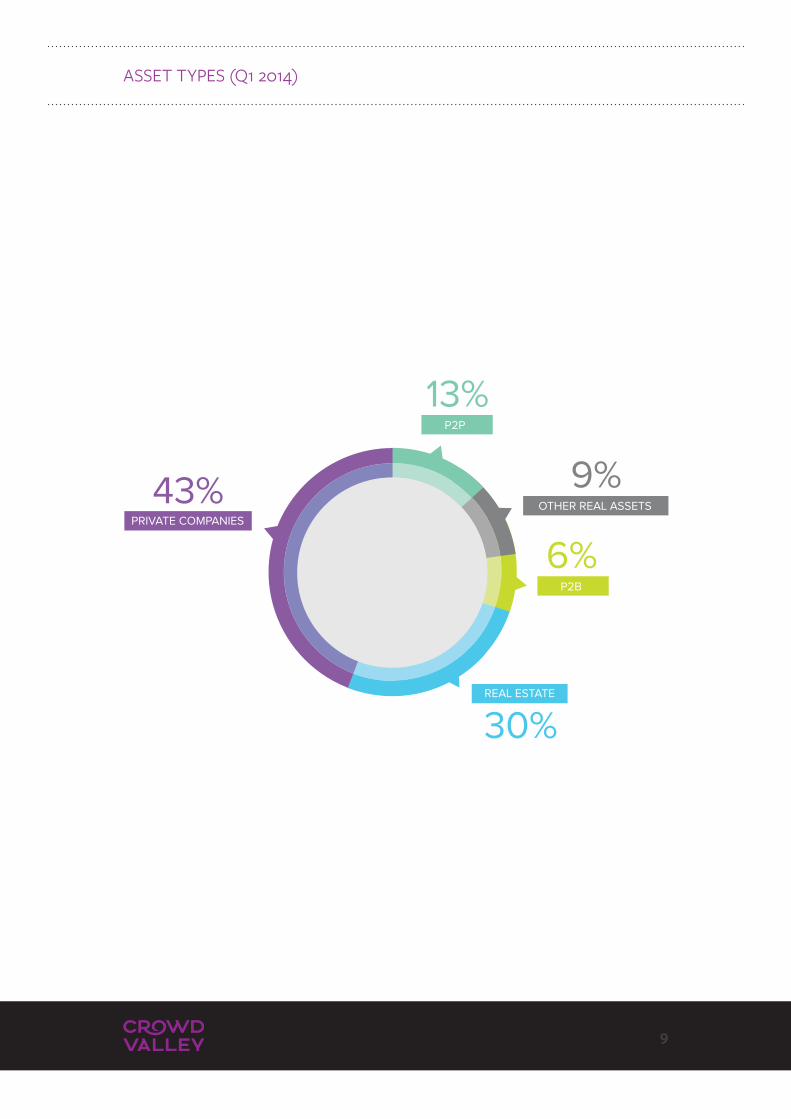

ASSET TYPES

7

Many people still associate crowdfunding with startups, even though during the past two

years, this new fundraising methodology has been used to enable investments in many

other assets than startups alone. Crowd Valley has directly witnessed a rising demand for

crowdfunding portals for other assets such as real estate, cleantech and energy among many

others. In particular the company identified four main categories of assets:

1) Private companies*;

2) Real Estate;

3) Other Real Assets, which include, among others, energy, cleantech and life science;

4) Other, which comprehends all other kinds of assets, that could not fit into the former

categories, for example education and intellectual property (IP).

The charts below represent the total demand for crowdfunding platforms or services divided

by asset type. In Q1 2014 Real Estate has experienced a steep increase: from 19% in Q4

to 30% in Q1. While the “Startups” category holds firmly its position, this quarter two new

categories made it into the chart: Peer-to-Peer (P2P) and Peer-to-Business (P2B), where P2P

refers to individuals supporting other individuals and P2B refers to individuals supporting

businesses or other entities. In fact, given the great increase in the demand of lending

models, as highlighted in the previous section, Crowd Valley decided to look more closely at

it, segmenting the asset types in P2P and P2B loans.

*In this edition Crowd Valley changed the category name from “Startups” to “Private

Companies”, since it observed that the demand is not just for startup portals, but for more

mature businesses platforms too.

1) Private Companeis

43%

44%

30%

19%

9% 6%13%

24%

0% 0%0%

13%

46%

16%

23%

0% 0%

15%

2) Real Estate 3) Other Real Assets

4) P2B 5) P2P 4) Other

ASSET TYPES

8

Q1 2014 Q4 2013 Q3 2013

ASSET TYPES (Q1 2014)

9

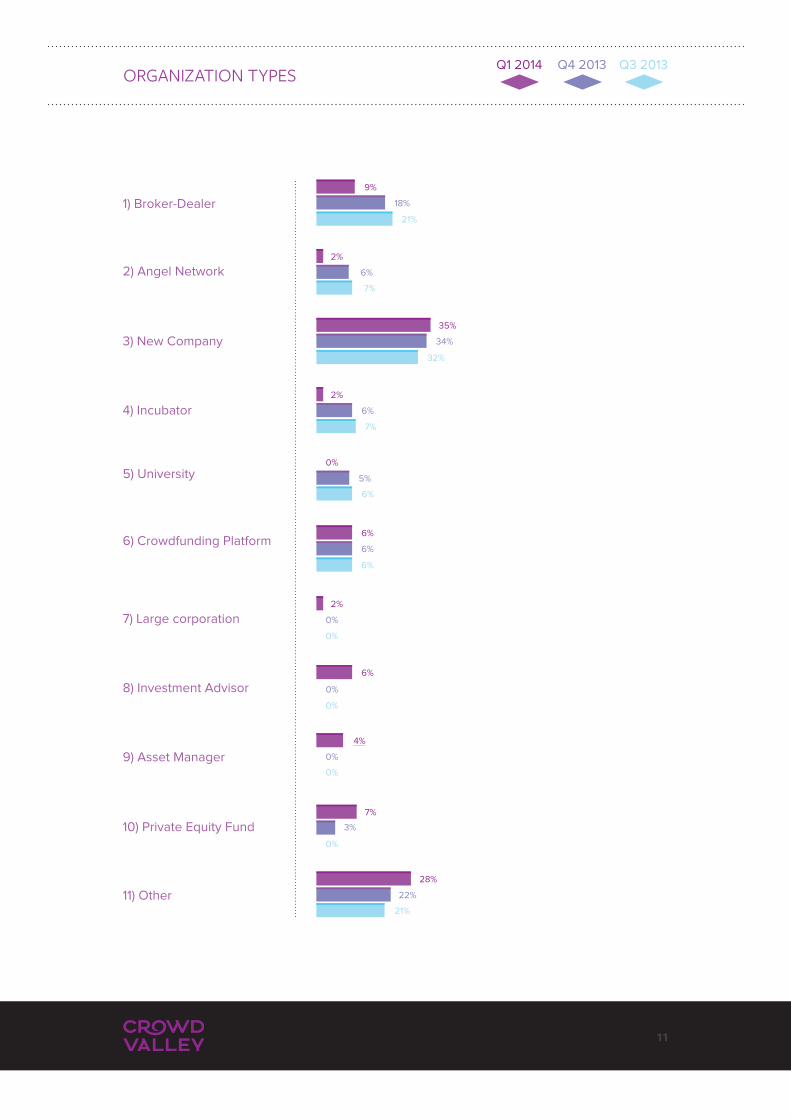

CLIENT PROFILE

10

In fifteen months of activity, Crowd Valley has been approached by many organizations and

professionals interested in its crowdfunding technologies or related services. The variety in

the potential clients’ profiles is particularly interesting. The company has identified several

types of organizations which were then grouped in the following categories:

1) Broker-Dealer representatives;

2) Angel Network;

3) New Company, which refers to potential clients who are going to create a new company

for the crowdfunding activity;

4) Incubator;

5) University;

6) Already existing Crowdfunding Platform;

7) Private Equity Fund;

8) Other, which includes already established companies that are planning to expand their

operations into crowdfunding.

In the present edition we changed the survey form, including three new categories: Large

Corporation, Investment Advisor and Asset Manager. These types of actors, who now display

an interesting percentage on the total demand, during the past data collection processes

were probably self-declaring “Broker-Dealer” or “Other”. Adding the three abovementioned

categories allowed the company to segment further the demand and frame in a more

accurate way the situation.

1) Broker-Dealer

2) Angel Network

3) New Company

4) Incubator

5) University

6) Crowdfunding Platform

8) Investment Advisor

9) Asset Manager

10) Private Equity Fund

11) Other

7) Large corporation

ORGANIZATION TYPES

11

21%

18%

9%

7%

6%

2%

32%

34%

35%

7%

6%

2%

6%

5%

0%

6%

6%

6%

0%

3%

7%

0%

0%

4%

21%

22%

28%

6%

0%

0%

0%

0%

2%

Q1 2014 Q4 2013 Q3 2013

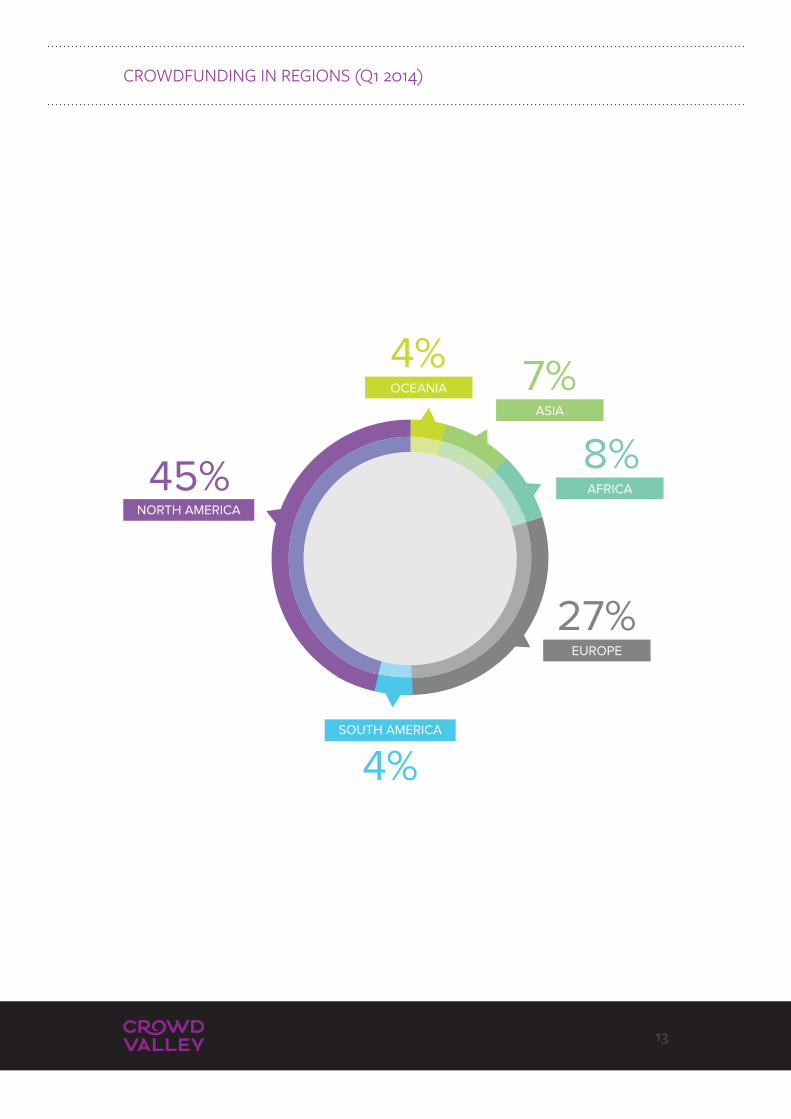

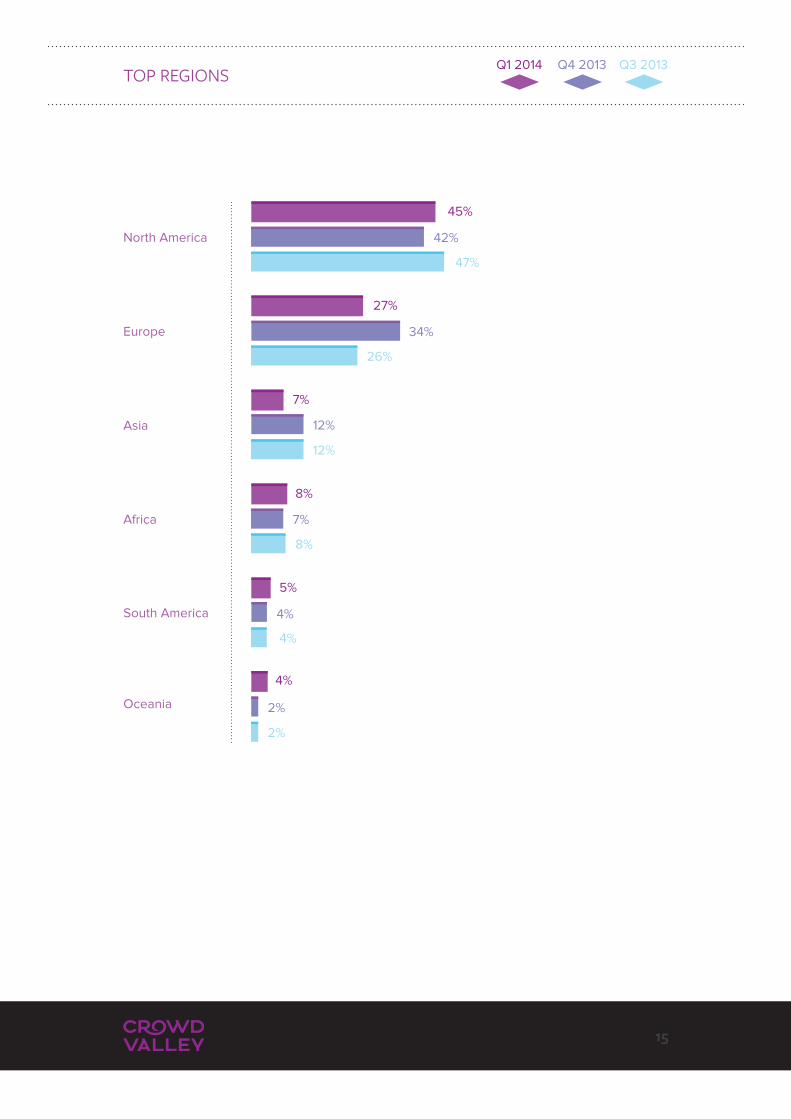

THE GEOGRAPHY OF CROWDFUNDING PLATFORMS

12

The demand for crowdfunding services is global. In fact, as shown by the following chart, the

organizations and the professionals who approached Crowd Valley since its start are from six

different continents. North America, driven by the US, which is still the main market, improves

its position, with its percentage increasing from 42% in Q4 to 45% in Q1. In Q1 2014 the

demand from Europe went back to the level of Q3 2013 (from 34% to 27%). In particular, the

UK, Italy and France remain the biggest markets in the region.

The new entrant of this quarter is Australia, which is among the top six locations with 4% of

the total demand. Africa and South America maintain more or less the same percentage as

the previous quarters, while Asia experiences a decrease.

CROWDFUNDING IN REGIONS (Q1 2014)

13

United States

United Kingdom

Italy

Australia

Canada

France

Other

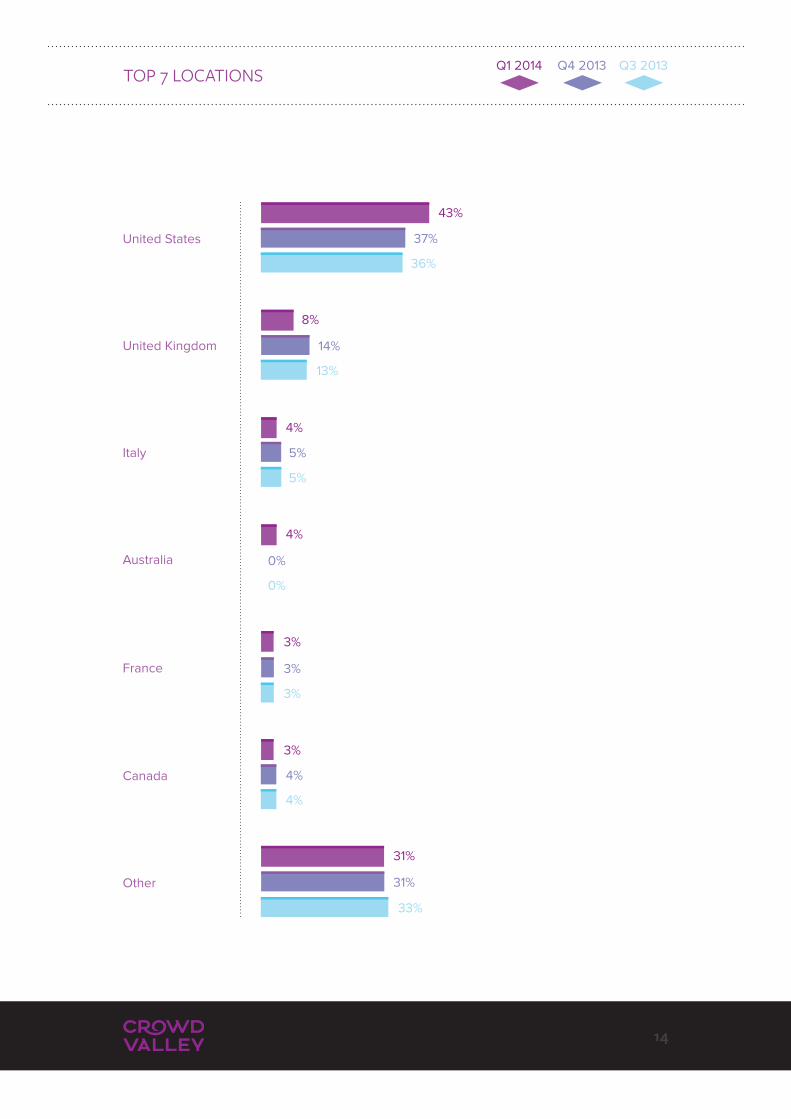

TOP 7 LOCATIONS

14

Q1 2014 Q4 2013 Q3 2013

36%

37%

43%

8%

13%

14%

4%

5%

5%

4%

0%

0%

3%

3%

3%

3%

4%

4%

31%

33%

31%

TOP REGIONS

North America

Europe

Asia

Africa

South America

Oceania

15

47%

42%

45%

26%

34%

27%

12%

12%

7%

8%

7%

8%

4%

4%

5%

2%

2%

4%

Q1 2014 Q4 2013 Q3 2013

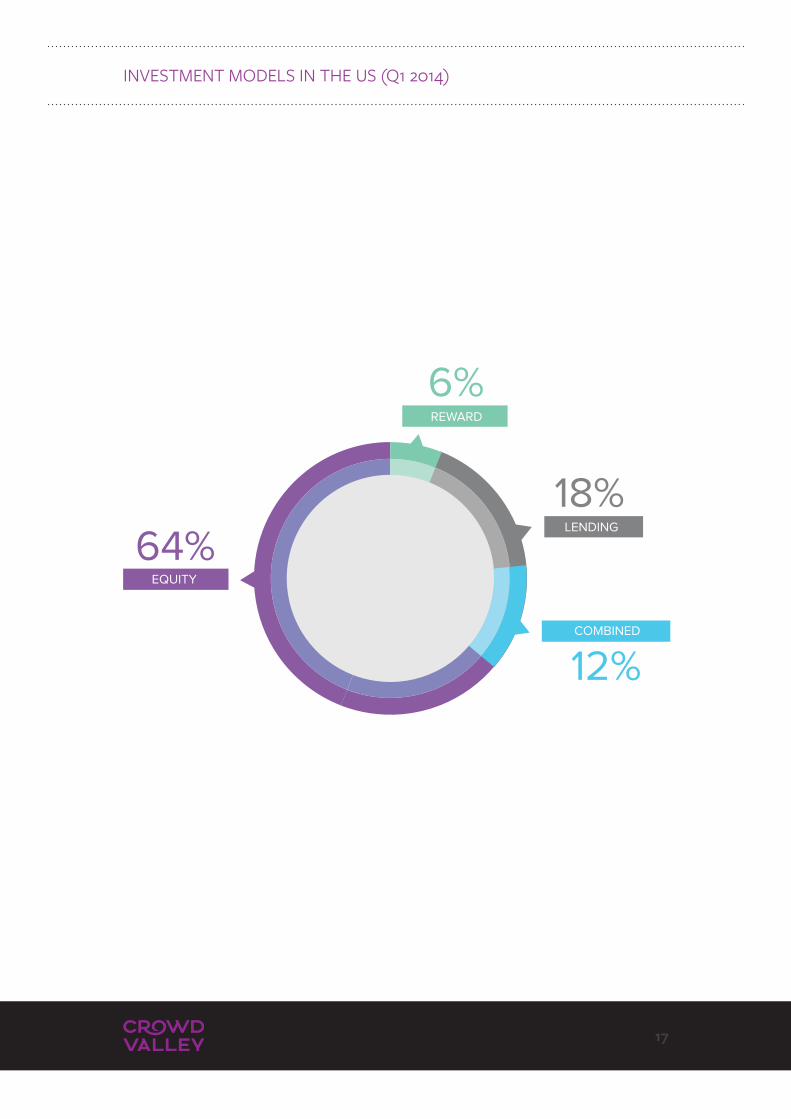

FOCUS ON THE US (Q1 2014)

16

Even if the demand for Crowd Valley’s crowdfunding services and technologies is global,

the biggest market remains the USA (37% in Q4 2013 and 43% in Q1 2014), where the

crowdfunding sector is more established than elsewhere*. Thus, this section presents

facts and figures focusing only on the US market. It is particularly interesting to notice that,

although “New Company” is the main category, the actors from the traditional finance sector

(i.e. Broker-Dealers, Private Equity Funds, Asset Managers and Investment Advisors) play a

relevant role.

*Massolutions, 2012. Crowdfunding Industry Report.

INVESTMENT MODELS IN THE US (Q1 2014)

17

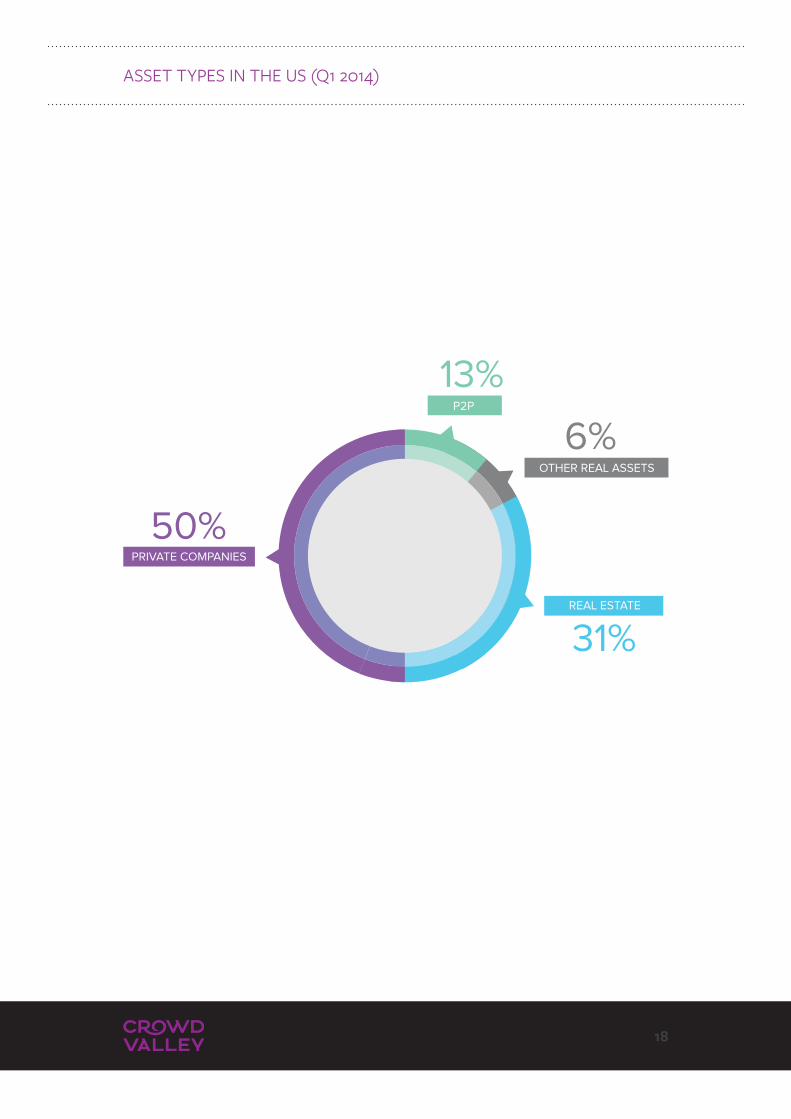

ASSET TYPES IN THE US (Q1 2014)

18

1) Broker-Dealer

2) New Company

3) Private Equity Funds

4) Investment Advisor

5) Asset Manager

6) Other

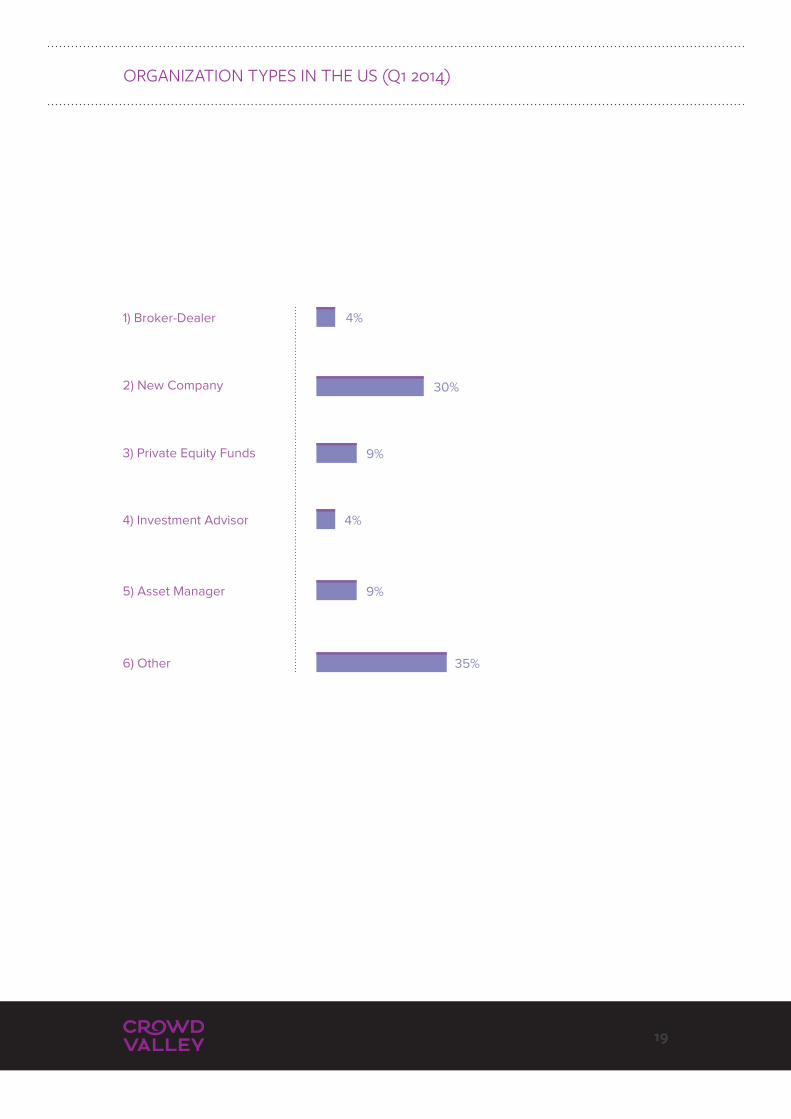

ORGANIZATION TYPES IN THE US (Q1 2014)

19

4%

30%

9%

9%

35%

4%

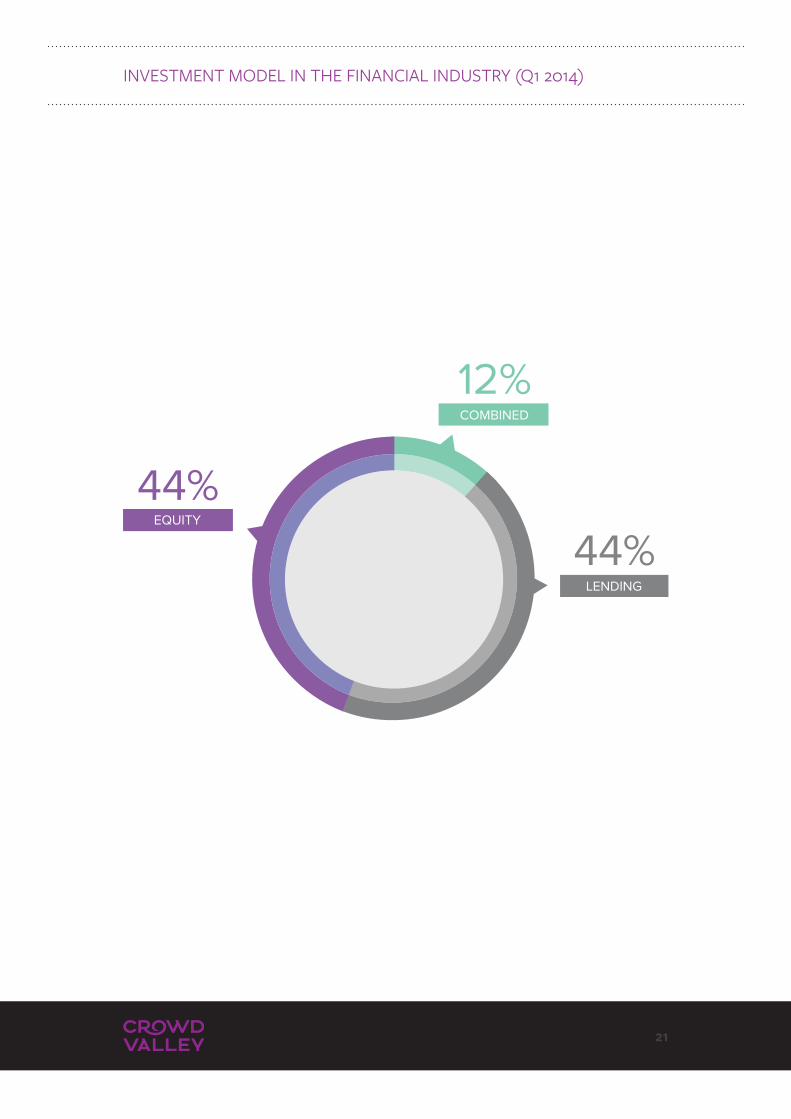

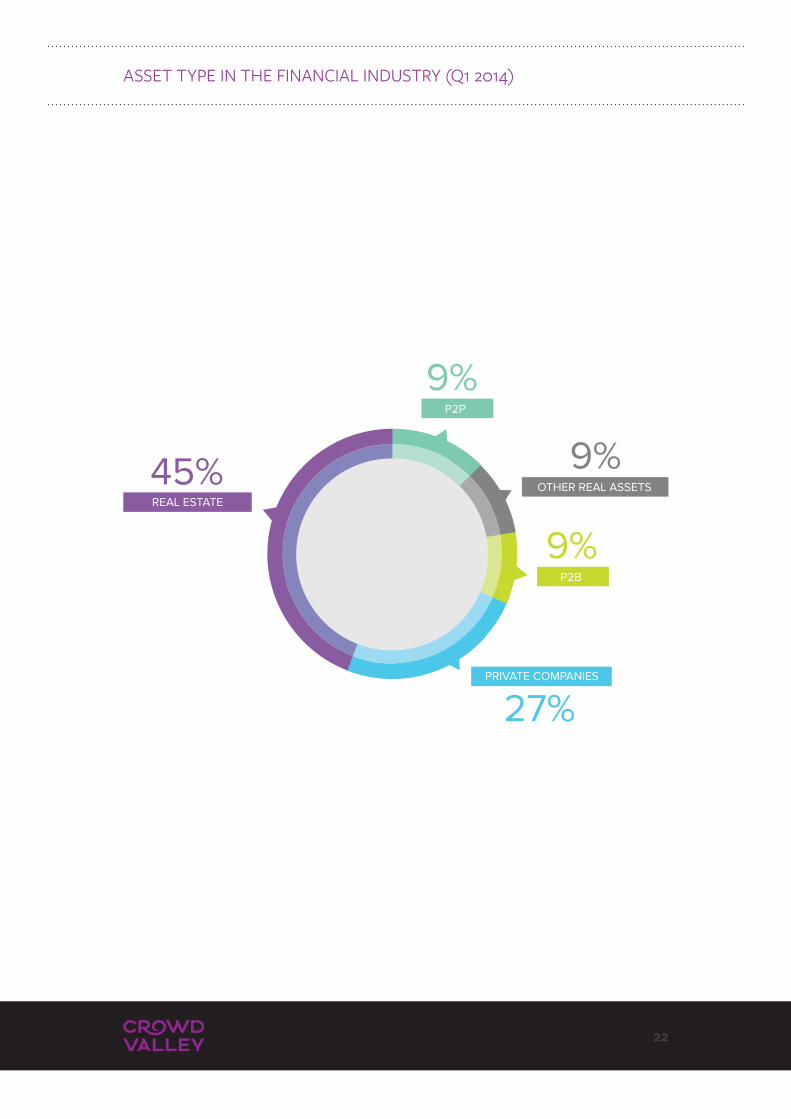

FOCUS ON THE FINANCIAL INDUSTRY

20

Given that in Q1 2014 the demand from traditional financial industry actors represents a

significant part of the total demand for crowdfunding services , Crowd Valley decided to focus

on these types of actors in the present section. The charts below highlight the investment

models and the asset types most required by the financial industry actors. As it was easy to

predict, the demand for reward crowdfunding platforms is null. More interestingly, real estate

is the most requested asset type.

INVESTMENT MODEL IN THE FINANCIAL INDUSTRY (Q1 2014)

21

ASSET TYPE IN THE FINANCIAL INDUSTRY (Q1 2014)

22

CONCLUSION

23

The present report presents facts and figures obtained analysing the data the company

collected during Q1 2014. The results contained in this report are probably the first data-

driven trends of the international crowdfunding market to be published in 2014. In particular,

since the start of 2014, the organization observed the following new trends:

1) The demand for lending models has increased significantly;

2) Real estate is the asset category where demand has increased the most;

3) New relevant actors from the traditional finance world, such as private equity funds and

asset managers, are looking to enter the crowdfunding ecosystem;

4) USA still remains the main market, but other countries, for example Australia, are

strengthening their position.

5) Traditional finance world actors are especially interested in Real Estate crowdfunding.

By publishing this information Crowd Valley aims to expand the current knowledge about this

new, transparent financial sector and to support regulators and other relevant stakeholders in

the global ecosystem in evaluating the market’s evolution. The company will continue publish

similar reports on a regular basis.

CROWD VALLEY CONTACTS

24

Main Contacts

Report Authors

MARKUS LAMPINEN - CROWD VALLEY CEO [email protected]

(646) 801 4054

PAUL HIGGINS - CROWD VALLEY COO [email protected]

(415) 580 0087

ALESSANDRO RAVANETTI - CROWD VALLEY CMO [email protected]

REX KEMPCKE - ENERGY EXPERT [email protected]

IRENE TORDERA - MARKETING & COMMUNICATIONS COORDINATION [email protected]

Don’t miss the opportunity to work with ChangeLab23, contact:

THIS REPORT WAS DESIGNED BY OUR TRUSTED PARTNER:

a leading design & development company in financial technologywith a strong focus on good user experience

and measurable results

![[Crowd15] Crowd Motivation & The Impact of Technology: The Economics of Crowdsourcing and Crowdfunding](https://img.pdfslide.us/doc/110x75/55a67c481a28ab41568b4638/crowd15-crowd-motivation-the-impact-of-technology-the-economics-of-crowdsourcing-and-crowdfunding.jpg)