Embed Size (px)

Citation preview

Credit Rating of BH and Credit Rating of BH and Perspectives for its ImprovementPerspectives for its Improvement

Kemal Kozarić, Ph.D. and Željko Šain, Ph.D.

Dubrovnik, December 8 and 9, 2011

2

Macroeconomic indicators for BHMacroeconomic indicators for BH

.

2

2009 2010 2011Gross Domestic Product (GDP) KM 23.95 bill. KM 24.75 bill.GDP per capita KM 6.233 KM 6.440

Real Growth Rate -3.2% 0.7%2.2% (IMF proj.)

2.0% (other proj. and prognoses)

Growth Rate of Industrial Production

-3.3% 1.6% 4.5% (August 2011/2010)

Average Annual Inflation 0.0% 3.1% 3.9% (annual in August)Unemployment Rate in BH 24.1% 27.1% 27.6 %Average Wage at BH level KM 790 KM 798 KM 813 (August)

External DebtKM 5.2 bill.

(21.7% GDP) KM 6.25 bill.(25.4 % GDP)

KM 6.19 bill. (June)

Current Account DeficitKM 1.48 bill.

(6.2% GDP) KM 1.36 bill.

(5.5% GDP)KM 971 mill (first half of the

year)Coverage of Import by Export 44.8% 52.1% 54.3% (January – August)

DFI (estimate) KM 353 millions KM 340 millionsKM 193 mill. (first half of the

year) Foreign Exchange Reserves KM 6.212 bill. KM 6.457 bill. KM 6.265 bill. (August)

Macroeconomic indicators for BHMacroeconomic indicators for BH Rating of the macroeconomic situation in BH

““Better thBetter thaan might be expected”?n might be expected”? (evaluation by the part of academic and professional circles,

EC, IMF, and other international financial institutions)

Worrying... Worrying... ... Catastrophic? ... Catastrophic? (evaluation of the part of academic and professional circles,

NGO, ... data on the growth of indebtedness, foreign trade deficit, unemployment rate and overall economic activities in the real sector ...)

3

Macroeconomic indicators for BHMacroeconomic indicators for BH Rating of the macroeconomic situation in BH

Sovereign Credit Rating of BH as an indication of the macroeconomic situation?

Formal rating of two reputable rating agencies S&P: rating downgraded from B+ to B, on December 1, 2011,

rating status “on watch” Moody's: B2, rating changed from stable to negative since May

2011 Negative outlook this year (mainly political reasons) After recent changes the credit ratings of S&P and Moody’s are on

the same level

4

Credit RatingCredit Rating Credit Rating is an assessment of general creditworthiness

of a certain debtor or a debt instrument – Securities or other financial obligation, based on relevant risk factors

Rating of a certain client is an assessment of its creditworthiness, or “regular” servicing of obligations expressed with the appropriate label

Assessment/evaluation of Credit Rating: Internally developed quantitative models; Specialized rating agencies (Moody’s, Fitch, Standard & Poor’s…).

Financial institutions using both models of rating development

55

Credit RatingCredit Rating Credit Rating provides internationally harmonized and

recognized framework for assessment and comparation of credit quality of individual debtor and debt instruments (securities)

Credit Rating in any way does not give an oppinion on how some creditor (for example, a bank, a state) or investment is “good” or “bad”, profitable, successful etc., but only and exclusively the probability of return of “borrowed” funds within agreed time

For smaller banks and SMEs there is usually no external rating (not profitable)

66

Rating categories/labelsRating categories/labelsMoody’s S&P and Fitch Definitions Description

Aaa AAA

Investment grade

High investment grade

Assets of good quality, great diversification and established size, excellent market positioning, profiled management skills and very good capacity to cover the debt

Aa1 AA+ Good quality and liquidity of assests, promoted at various places in the market, good quality of management and a good capacity to cover the debt.

Aa2 AA

Aa3 AA-

A1 A+Medium

investment grade

Satisfactory quality and liquidity of assets, the average market position and management quality, regular credit standards, the average capacity to cover the debt.

A2 A

A3 A-

Baa1 BBB+Lower investment

grade

Acceptable quality and liquidity of assets, but with a noticeable degree of risk, a weaker capacity to cover the debt.

Baa2 BBB

Baa3 BBB-

Ba1 BB+

Non-investment

grade

Below investment grade

Acceptable quality and liquidity of assets, although with a significant degree of risk, low business diversification, limited liquidity and limited margins of debt coverage .

Ba2 BB

Ba3 BB-

B1 B+

Speculative grade

The loan under review, assets quality is acceptable, but with temporary difficulties in liquidity level, the high financial “leverage”, some weaknesses in management, positioning and market positioning.

B2 B

B3 B-

Caa CCC

High risk High risk

As above, but with evident difficulties, and debt management is sometimes tense and hard. Uncertainty regarding the payment of the interest rates, but not of the principal debt.

Ca CC

77

Country riskCountry risk The possibility of non-compliance of obligations to the bank

as a result of actions of government or events in the debtors country

The determinants of country risk: Political risk Economic risk Risk of transfers Risk of default Risk of guarantee

Management of country risk: The adoption of formal policies for management of country risk Internal monitoring The mechanism of reporting to the bank management

The elements that determine country The elements that determine country riskrisk

Political elementsPolitical elements::

Political stability The attitude toward foreign investors The issue of privatization/nationalization Monetary inflation Balance of payments The behaviour of bureaucracy

Operating elementsOperating elements::

Economic growth Currency convertibility Legal effect of contracts Professional services and contractual relations Utility services (fax, phone) Labour/productivity costs Local management and partners

Financial elements:Financial elements:

Currency convertibility Short-term loans Long-term loans/capital risk Inflation Balance of payments Legal effect of contracts The behaviour of bureaucracy

Elements of nationalization:Elements of nationalization: The attitude toward foreign investors and profit Nationalization Currency convertibility Bureaucracy

The structure of strategic riskThe structure of strategic risk

culture of risk

corporate management

business

market

clients

competition

regulation

people

STRATEGIC RISK OF THE

COMPONENT

Risk

Time

Risk

Risk

Risk

Risk

Risk

Risk

Risk

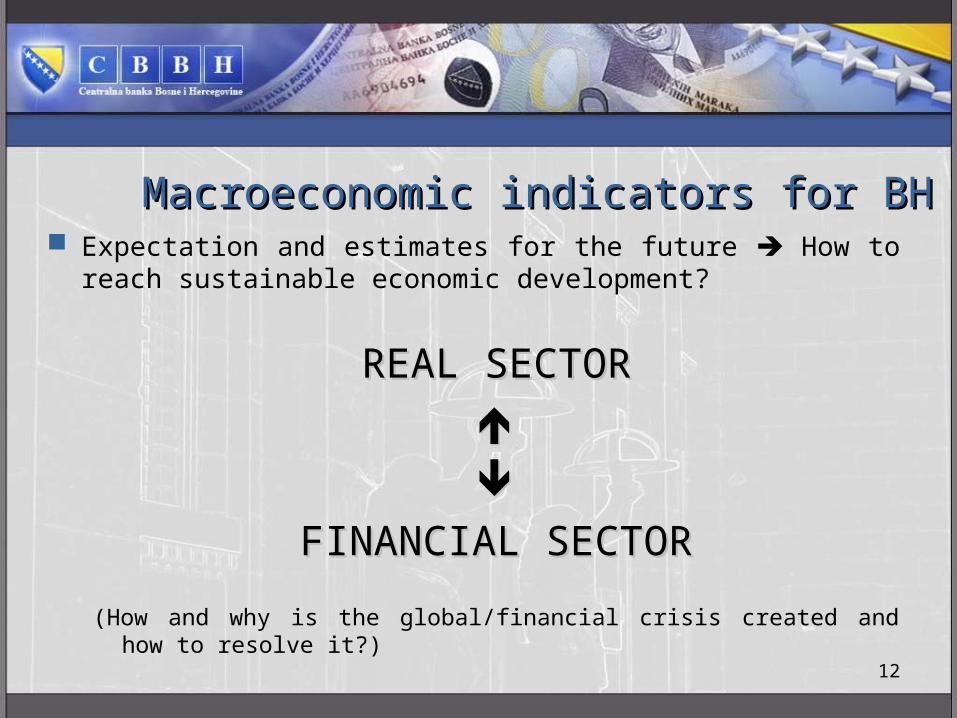

Macroeconomic indicators for BHMacroeconomic indicators for BH

Expectation and estimates for the future How to reach sustainable economic development ?

2012 and short term 2012 and short term debt crisis in the EU and slowdown in economic growth

(recession or crisis with a double bottom) and implications for SE Europe, Western Balkans, Bosnia and Herzegovina

““Long” term Long” term Is there potential for healthy growth of the real sector

based on growth of employment, domestic demand and export? Is it (only) the capital/money that is missing?

11

Macroeconomic indicators for BHMacroeconomic indicators for BH Expectation and estimates for the future How to reach

sustainable economic development?

REAL SECTORREAL SECTOR

FINANCIAL SECTORFINANCIAL SECTOR

(How and why is the global/financial crisis created and how to resolve it?) 12

The structure of the financial sector in The structure of the financial sector in BHBH Banking sector dominates the financial sector in BH

main source and channel for financing the real sector (and people)

High percentage of foreign ownership is a potential risk because strategic decisions are made out of reach of monetary authorities of BH

Relatively small share of other financial intermediaries Table: The value of the assets of financial intermediaries

1313

2007 2008 2009 2010

Value, KM millions

Share, %Value, KM millions

Share, %Value, KM millions

Share, %Value, KM millions

Share, %

Banks 19.570 79,8 20.815 80,8 20.604 82,7 20.416 84,3

Investments funds 1.762 7,2 1.225 4,8 871 3,5 888 3,7

Leasing companies 1.378 5,6 1.607 6,2 1.416 5,7 1.108 4,6

Insurance and reinsurance companies 853 3,5 890 3,5 940 3,8 941 3,9

Microcredit organisations 946 3,9 1.213 4,7 1.087 4,4 856 3,5

Total 24.510 25.749 24.919 24.210

Banking sector in BHBanking sector in BH The financial sector “bank The financial sector “bank dominateddominated” : ” :

84% of total assets of the financial sector (at the end of 2010)

The dominance of foreign banking groups:The dominance of foreign banking groups: 95% of total assets and 82% of action/equity capital is

concentrated in banks with majority foreign ownership The significance of “Vienna Initiative” (external debt of the

banking sector – 29.5% of total liabilities)

High liquidityHigh liquidity Good capital adequacy (16Good capital adequacy (16..11% in % in 2010, 152010, 15.5% in Q1, .5% in Q1, 2011)2011) Endangered profitabilityEndangered profitability

Loss in 2010 NPL (non-performing loans) – growth

1414

Profitability and level of NPLsProfitability and level of NPLs.

1515

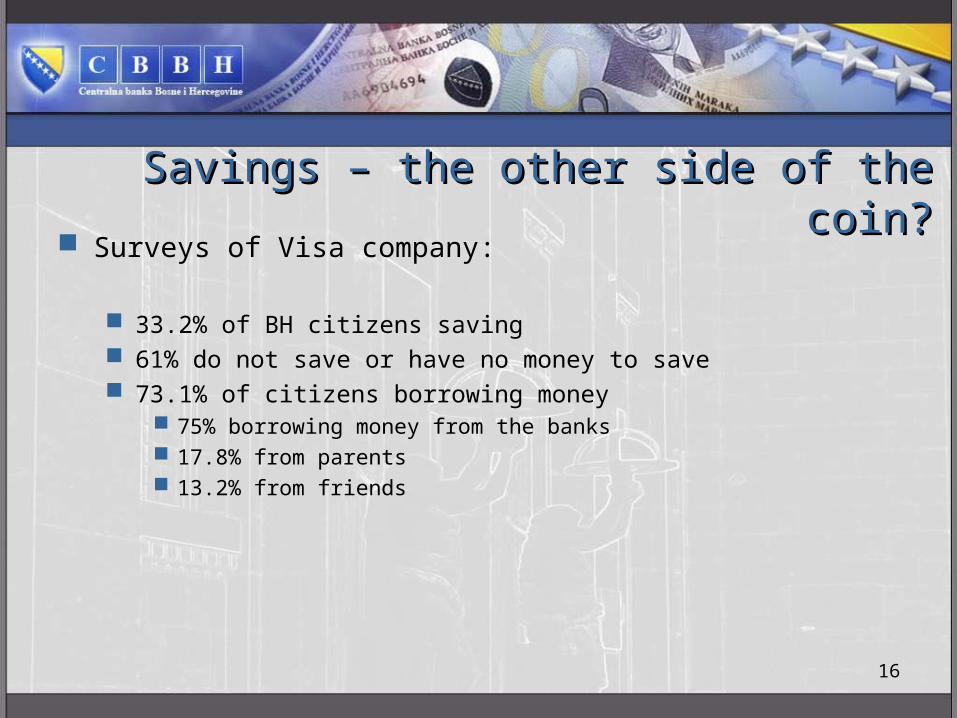

Savings – the other side of the coin?Savings – the other side of the coin? Surveys of Visa company:

33.2% of BH citizens saving 61% do not save or have no money to save 73.1% of citizens borrowing money

75% borrowing money from the banks 17.8% from parents 13.2% from friends

16

LoansLoans

The loans to private companies increased by KM 354 millions or 5%, the loans to households increased by KM 98 millions or 1.5%, total loans increased by KM 471 millions or 3.4%.

1717

In KM millions

31. 12. 2008.Amount Share

31. 12. 2009. Amount Share

31. 12. 2010. Amount Share

30. 06. 2011.Amount Share

TOTAL LOANS 14.040 100 % 13.496 100 % 13.936 100 % 14.407 100 %

Out of these:-Private companies

6.633 47 % 6.474 48 % 6.732 48 % 7.086 49 %

-Public companies 222 2 % 237 2 % 309 2 % 350 2 %

-Government institutions 231 1 % 343 2 % 436 3 % 445 3 %

-Households 6.687 48 % 6.292 47 % 6.314 46 % 6.412 45 %

-Other sectors 267 2 % 150 1 % 145 1 % 114 1 %

The debt crisis in the Euro Zone – a risk of The debt crisis in the Euro Zone – a risk of new recession and/or the crisis with a double new recession and/or the crisis with a double

bottombottom?? Started and culminated in Greece threat of bankruptcy, leaving the Euro Zone...

Continued in Ireland and Portugal (Countries: “PIGS” – the members of the Euro Zone)

Endangered Spain, Italy...?

IndicatorIndicator share of public debt in GDP, the level of budget deficit, unemployment rate

ConsequenceConsequence decline in sovereign credit rating, growth of the loans price, inability in public debt servicing, help from the IMF and the EU, the domino effect, the survival of the euro and the Euro Zone..., 18

The debt crisis in the Euro Zone – a risk of The debt crisis in the Euro Zone – a risk of new recession and/or the crisis with a double new recession and/or the crisis with a double

bottombottom??RANKING OF SELECTED COUNTRIES BY THE PARTICIPATION OF PUBLIC DEBT IN GDP

Source: ST invest, 24.10.2011, weekly newsletter, 34/2011

S. nr. Country GDP in USD billions

Public debt as % in GDP Note/comment (SB)

1. Japan 5,5 233 Most of the debt is in the hands of local creditors

2. Greece 0,3 166 Bankruptcy avoided so far

3. Italy 2,1 121 Credit rating downgraded

4. Ireland 0,2 109 Rating downgraded, uses a package of assistance

5 USA 14,5 100 "Technical" bankruptcy avoided during summer, for first time credit rating downgraded

6. France 2,6 87 Rating AAA, „on watch“

7. Germany 3,3 83 Rating AAA

8. G. Britain 2,3 81 Rating AAA

9. Spain 1,4 56 Rating downgraded

10. Portugal 0,2 39 (only Sp. banks) Rating downgraded, uses a package of assistance

11. China 5,9 ? Foreign exchange reserves more than billion 3,2

19

Public debt as % in GDP in the Public debt as % in GDP in the countries of the regioncountries of the region

RANKING OF SELECTED COUNTRIES BY THE PARTICIPATION OF PUBLIC DEBT IN GDP

Source: IMF, World Economic Outlook 10.2011

R.No. Country Public debt as

% in GDP 1. Albania 59.4 2. Bosnia and Herzegovina 39.6 3. Croatia 47.5 4. Macedonia 26.3 5 Montenegro 43.1 6. Serbia 44.1

20

The debt crisis in the Euro Zone – a risk of The debt crisis in the Euro Zone – a risk of new recession and/or the crisis with a double new recession and/or the crisis with a double

bottom?bottom?

Projections of economic growth (original/corected) in %

Region/country 2011 2012 World 4.0 4.3 4.0 4.5 Euro Zona 1.6 2.0 1.1 1.7 USA 1.5 2.5 1.8 2.7 Japan -0.5 -0.7 2.3 2.9

Source: IMF, World Economic Outlook, September 2011

21

The debt crisis in the Euro Zone – a risk of The debt crisis in the Euro Zone – a risk of new recession and/or the crisis with a double new recession and/or the crisis with a double

bottom?bottom?

Projections of economic growth (original/corrected) in %

Region/country 2011. 2012. 2013. World 3.1 2.6 3.4 2.7 3.4 3.1 Euro Zona 1.7 1.6 1.8 0.8 2.1 1.5 USA 2.6 1.5 2.8 1.8 2.9 2.6 UK 1.4 1.0 1.7 1.2 - 2.1

Source: Fitch Rating Agency– Global Economic Outlook, October 2011

22

The debt crisis in the Euro Zone – a risk of The debt crisis in the Euro Zone – a risk of new recession and/or the crisis with a double new recession and/or the crisis with a double

bottom?bottom? The escalation of debt crisis (hesitation and mismatching The escalation of debt crisis (hesitation and mismatching

attitude of the EU?)attitude of the EU?)

despite agreed and received assistance, the bankruptcy is threatening to Greece (Portugal and Ireland slightly better condition)

more and more serious situation in Spain and italy (Franch rating “on watch”)

The exposure of european banks “trigger” of the banking crisis?

Quarterly data Quarterly data generally slowdown of economic growth and export, threatening inflation, “high unemployment”

Nouriel Rubini Nouriel Rubini The chances for new recession bigger than

50% !

23

How to ensure a better credit rating in the How to ensure a better credit rating in the future?future?

For better credit rating in the future, we should:

Provide political stability; Create a better macroeconomic environment; Raise awareness of responsibility for credit rating

(governments, ministries, regulators, the CBBH, the real sector);

Assure budget discipline (reduce the budget deficit and adopt budgets for all levels in time, particularly for BH);

Remove the administrative barriers for corporate sector and, the most important, remember that the above items are

not one- shot measures, but a continuous process.24

2525

Thank you for your attentionThank you for your attentionhttp://www.cbbh.bahttp://www.cbbh.ba

25