Embed Size (px)

Citation preview

1Cooper Human Systems

CREDIT CARD MARKET SIMULATION: QUANTIFYING THE IMPACT OF CHANGE LEADS TO DRAMATIC STRATEGIC INNOVATIONTuesday, November 19, 2013

Presented by:

David Starr, Cooper Human Systems

Sharon Els, PA Consulting Group

Hosted by:

Steve Adler, IBM & Karim Chichakly, isee systems

Cooper Human Systems

2Cooper Human Systems

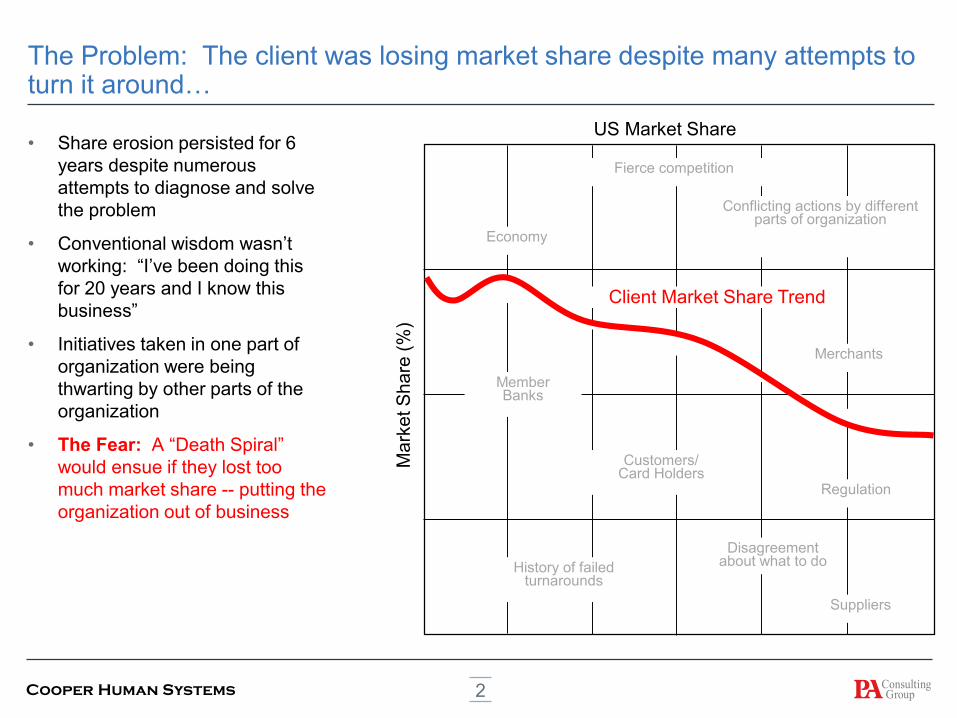

• Share erosion persisted for 6

years despite numerous

attempts to diagnose and solve

the problem

• Conventional wisdom wasn’t

working: “I’ve been doing this

for 20 years and I know this

business”

• Initiatives taken in one part of

organization were being

thwarting by other parts of the

organization

• The Fear: A “Death Spiral”

would ensue if they lost too

much market share -- putting the

organization out of business

The Problem: The client was losing market share despite many attempts to turn it around…

US Market Share

Ma

rke

t S

ha

re (

%)

Client Market Share Trend

Conflicting actions by different parts of organization

Economy

Disagreement about what to do

Fierce competition

History of failed turnarounds

MemberBanks

Regulation

Customers/Card Holders

Suppliers

Merchants

3Cooper Human SystemsCooper Human Systems

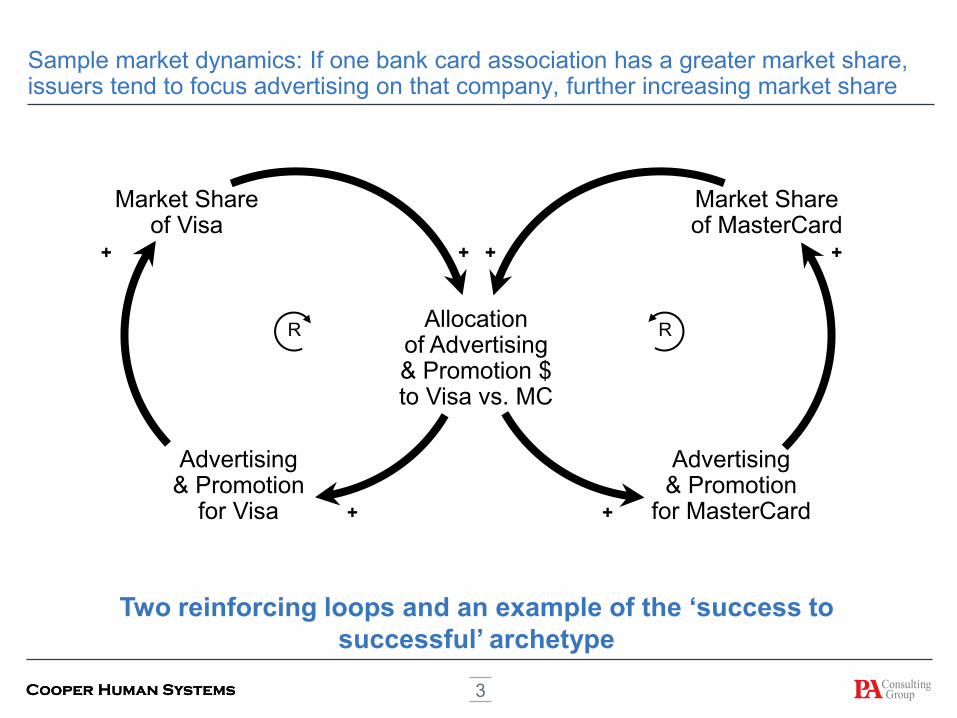

Sample market dynamics: If one bank card association has a greater market share, issuers tend to focus advertising on that company, further increasing market share

Allocationof Advertising& Promotion $to Visa vs. MC

Market Shareof MasterCard

Advertising& Promotion

for MasterCard

Advertising& Promotion

for Visa

Market Shareof Visa

Two reinforcing loops and an example of the ‘success to

successful’ archetype

RR

+ +

++

+ +

4Cooper Human SystemsCooper Human Systems

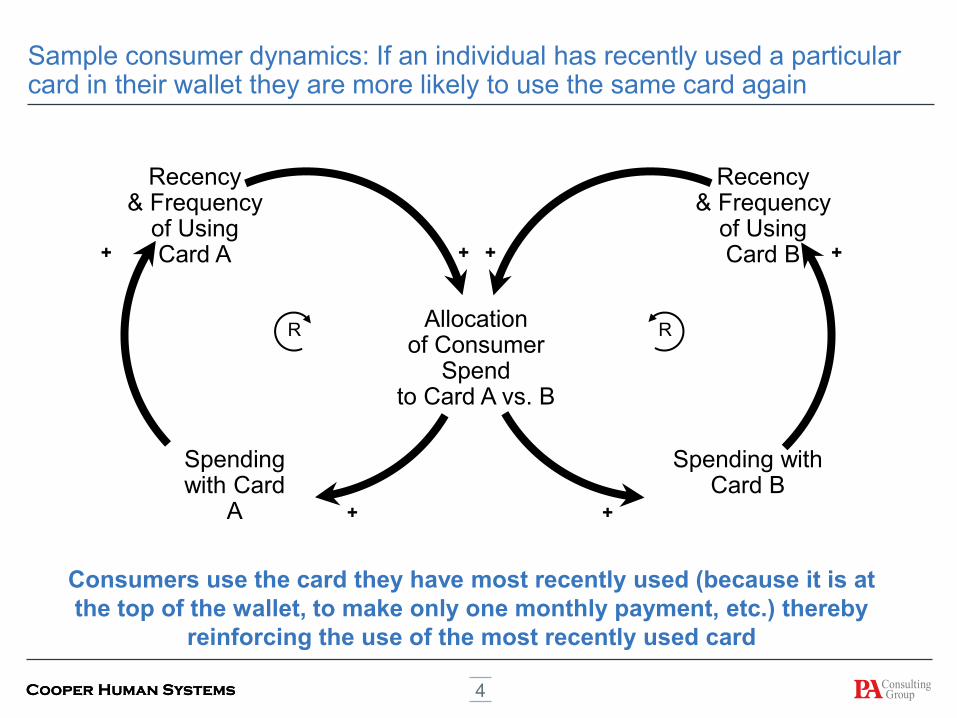

Sample consumer dynamics: If an individual has recently used a particular card in their wallet they are more likely to use the same card again

Allocationof Consumer

Spendto Card A vs. B

Recency& Frequency

of UsingCard B

Spending with Card B

Spending with Card

A

Recency& Frequency

of UsingCard A

Consumers use the card they have most recently used (because it is at

the top of the wallet, to make only one monthly payment, etc.) thereby

reinforcing the use of the most recently used card

RR

+ +

++

+ +

5Cooper Human SystemsCooper Human Systems

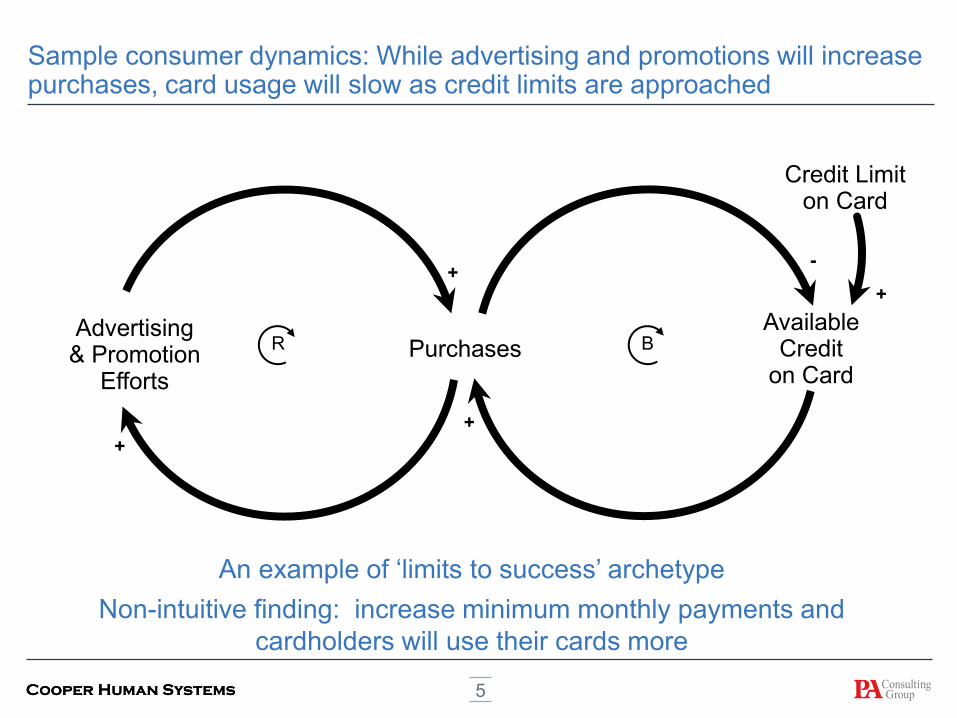

Sample consumer dynamics: While advertising and promotions will increase purchases, card usage will slow as credit limits are approached

PurchasesAvailable

Crediton Card

Credit Limiton Card

Advertising& Promotion

Efforts

An example of ‘limits to success’ archetype

Non-intuitive finding: increase minimum monthly payments and

cardholders will use their cards more

BR

+

+

-

+

+

6Cooper Human SystemsCooper Human Systems

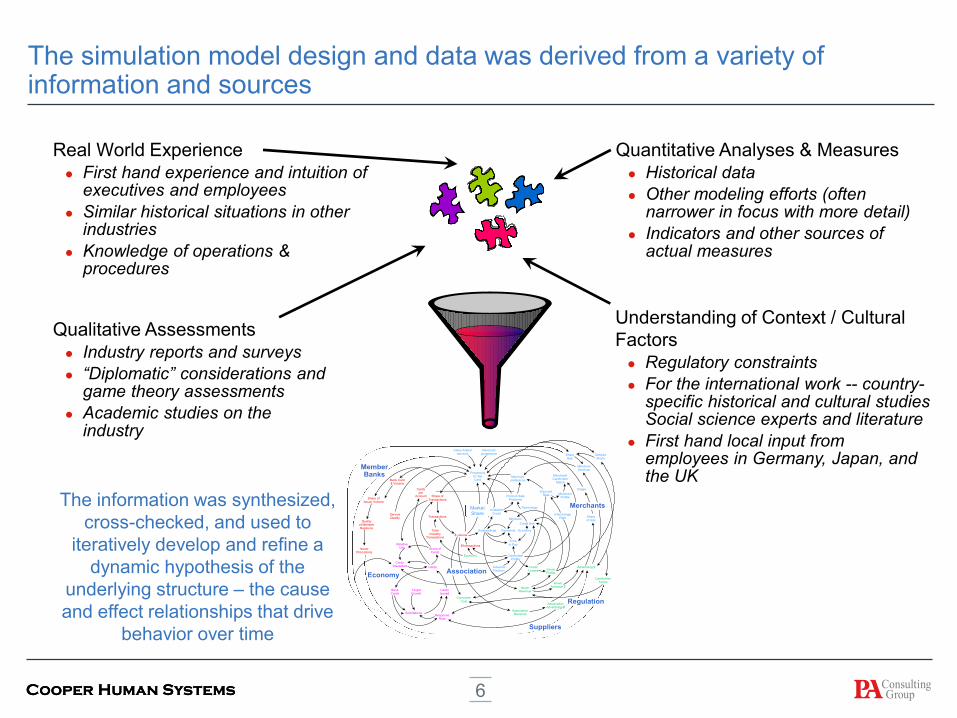

The simulation model design and data was derived from a variety of information and sources

The information was synthesized,

cross-checked, and used to

iteratively develop and refine a

dynamic hypothesis of the

underlying structure – the cause

and effect relationships that drive

behavior over time

Real World Experience

First hand experience and intuition of executives and employees

Similar historical situations in other industries

Knowledge of operations & procedures

Quantitative Analyses & Measures

Historical data

Other modeling efforts (often narrower in focus with more detail)

Indicators and other sources of actual measures

Qualitative Assessments

Industry reports and surveys

“Diplomatic” considerations and game theory assessments

Academic studies on the industry

Understanding of Context / Cultural

Factors

Regulatory constraints

For the international work -- country-specific historical and cultural studies Social science experts and literature

First hand local input from employees in Germany, Japan, and the UK

Outstandings Payments

Transactions

$ volume

Available

Credit

$/transactions

TotalIndustry

Transactions

Economy CardholderProfile

Timeto Pay

Merchantpreference

Propensityto UseCard

MerchantProfile

Technology

Minimum

Credit limit

Economy

Merchant/Cardholder

Match

Share ofCards

CreditLosses

AdvancePosition Issuer

Profits

InterchangeRate

IssuerRevenue

CardsDiscarded

RelativeUse

Cards

CardsIssued

TargetGrowth

BankCards

ResponseRate

AssociationRevenueSolicitations

IssuerAdvance $

Advertising $

CardholderTerms

ShareGap

DesiredShare

MerchantServices

Merchantacceptance

Value-Addedservices

Image

Shareof Ads

Bank Card$ Volume

Share ofIssuer Volume

Qualityof MemberRelations

ServiceQuality

IssuerPromotions

Cardsper

Account Share of

Transactions

Point-of-SaleProblems

DiscountRate

Market

Share

AssociationAdvertising &

Consumer

Cost

Economy

MemberBanks

Regulation

Suppliers

Merchants

Association

7Cooper Human SystemsCooper Human Systems

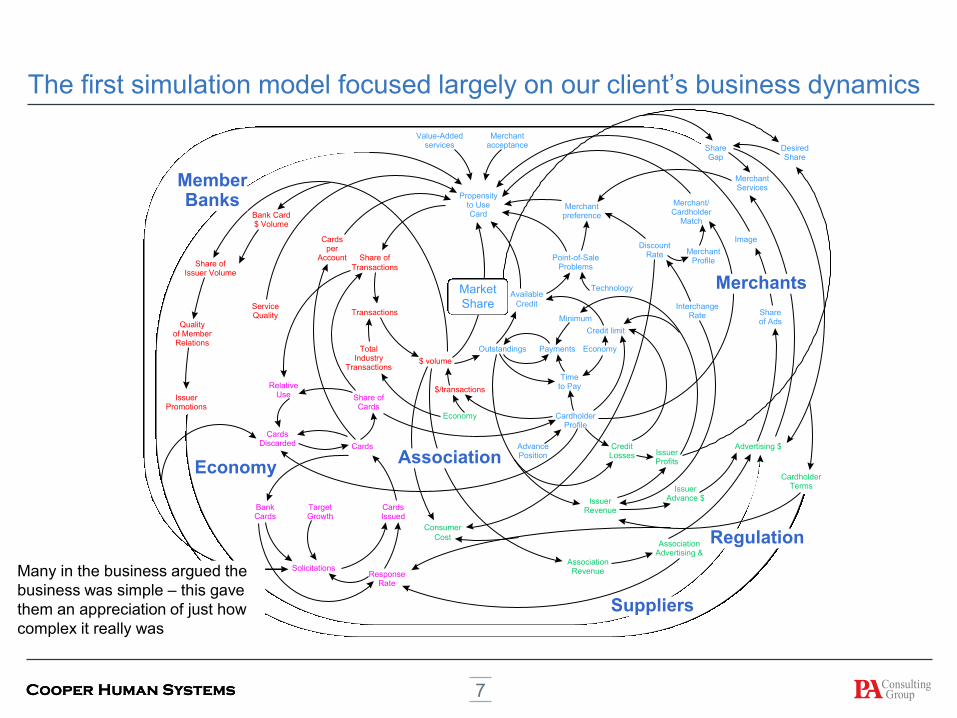

The first simulation model focused largely on our client’s business dynamics

Outstandings Payments

Transactions

$ volume

Available

Credit

$/transactions

TotalIndustry

Transactions

Economy CardholderProfile

Timeto Pay

Merchantpreference

Propensityto UseCard

MerchantProfile

Technology

Minimum

Credit limit

Economy

Merchant/Cardholder

Match

Share ofCards

CreditLosses

AdvancePosition Issuer

Profits

InterchangeRate

IssuerRevenue

CardsDiscarded

RelativeUse

Cards

CardsIssued

TargetGrowth

BankCards

ResponseRate

AssociationRevenueSolicitations

IssuerAdvance $

Advertising $

CardholderTerms

ShareGap

DesiredShare

MerchantServices

Merchantacceptance

Value-Addedservices

Image

Shareof Ads

Bank Card$ Volume

Share ofIssuer Volume

Qualityof MemberRelations

ServiceQuality

IssuerPromotions

Cardsper

Account Share of

Transactions

Point-of-SaleProblems

DiscountRate

Market

Share

AssociationAdvertising &

Consumer

Cost

Economy

MemberBanks

Regulation

Suppliers

Merchants

Association

Many in the business argued the

business was simple – this gave

them an appreciation of just how

complex it really was

8Cooper Human SystemsCooper Human Systems

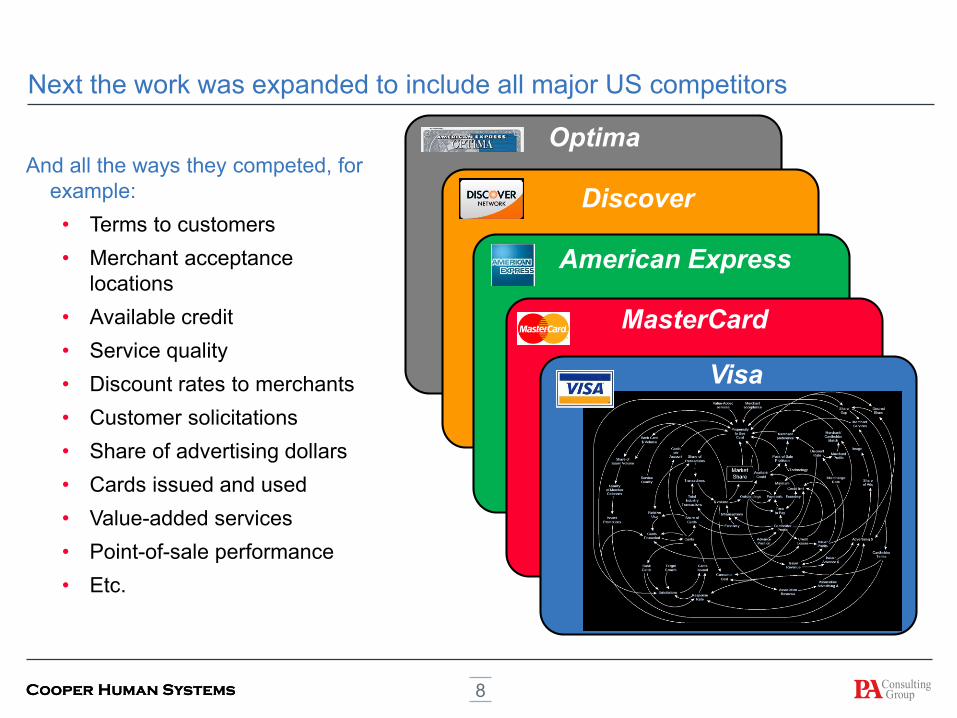

Next the work was expanded to include all major US competitors

And all the ways they competed, for

example:

• Terms to customers

• Merchant acceptance

locations

• Available credit

• Service quality

• Discount rates to merchants

• Customer solicitations

• Share of advertising dollars

• Cards issued and used

• Value-added services

• Point-of-sale performance

• Etc.

MasterCard

American Express

Discover

Optima

Visa

9Cooper Human SystemsCooper Human Systems

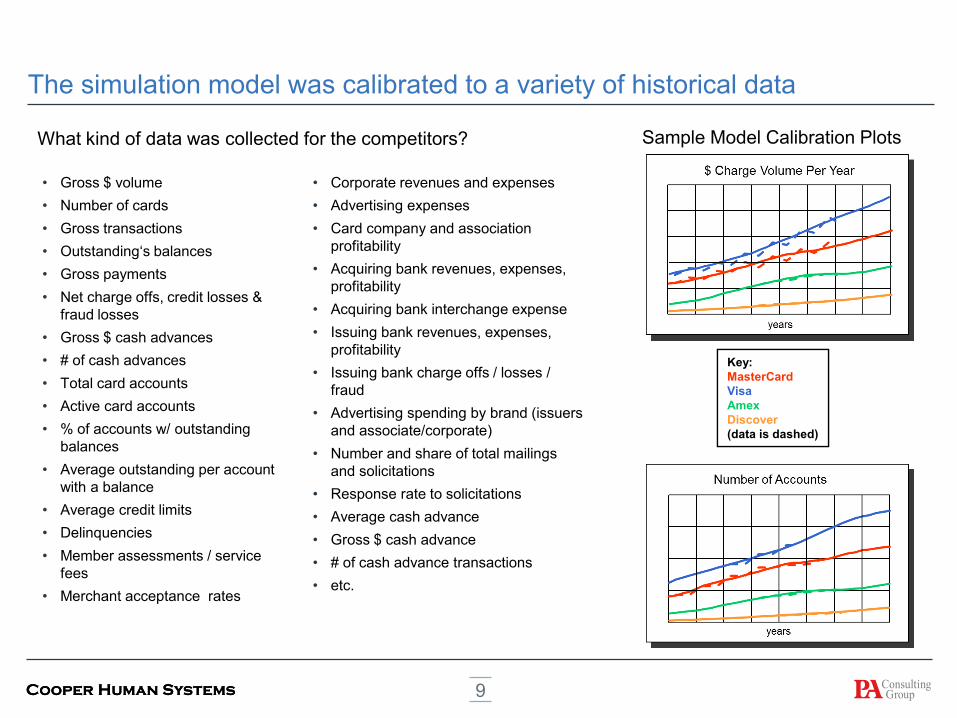

The simulation model was calibrated to a variety of historical data

Key:

MasterCard

Visa

Amex

Discover

(data is dashed)

Key:

MasterCard

Visa

Amex

Discover

(data is dashed)

• Gross $ volume

• Number of cards

• Gross transactions

• Outstanding‘s balances

• Gross payments

• Net charge offs, credit losses &

fraud losses

• Gross $ cash advances

• # of cash advances

• Total card accounts

• Active card accounts

• % of accounts w/ outstanding

balances

• Average outstanding per account

with a balance

• Average credit limits

• Delinquencies

• Member assessments / service

fees

• Merchant acceptance rates

Sample Model Calibration Plots

• Corporate revenues and expenses

• Advertising expenses

• Card company and association

profitability

• Acquiring bank revenues, expenses,

profitability

• Acquiring bank interchange expense

• Issuing bank revenues, expenses,

profitability

• Issuing bank charge offs / losses /

fraud

• Advertising spending by brand (issuers

and associate/corporate)

• Number and share of total mailings

and solicitations

• Response rate to solicitations

• Average cash advance

• Gross $ cash advance

• # of cash advance transactions

• etc.

What kind of data was collected for the competitors?

10Cooper Human Systems

The “Business As Usual” simulation showed that without major intervention our client’s share would continue to fall

US Market Share (all competitors)

Historical share trend

“Business as usual” Simulation

Market Share

Conflicting actions by different parts of organizationEconomy

Disagreement about what to do

Fierce competition

History of failed turnarounds

MemberBanks

Regulation

Customers/Card Holders

Suppliers

Merchants

11Cooper Human SystemsCooper Human Systems

First we tested the initiatives the organization had recently undertaken, or was considering. None of these reversed the loss of share.

We then executed a thorough set of sensitivity

tests, varying most of the parameters in the

model by plus or minus 25%

12Cooper Human SystemsCooper Human Systems

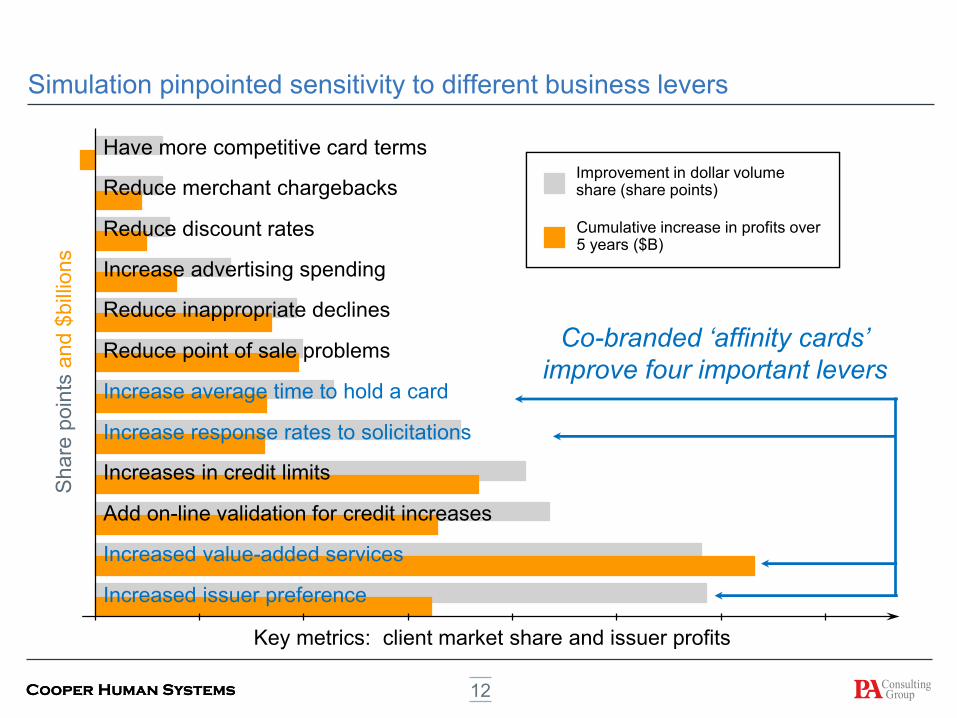

Simulation pinpointed sensitivity to different business levers

Key metrics: client market share and issuer profits

Improvement in dollar volume share (share points)

Cumulative increase in profits over 5 years ($B)

Share

poin

tsa

nd

$bill

ions

Have more competitive card terms

Reduce merchant chargebacks

Reduce discount rates

Increase advertising spending

Reduce inappropriate declines

Reduce point of sale problems

Increase average time to hold a card

Increase response rates to solicitations

Increases in credit limits

Add on-line validation for credit increases

Increased value-added services

Increased issuer preference

Co-branded ‘affinity cards’

improve four important levers

13Cooper Human SystemsCooper Human Systems

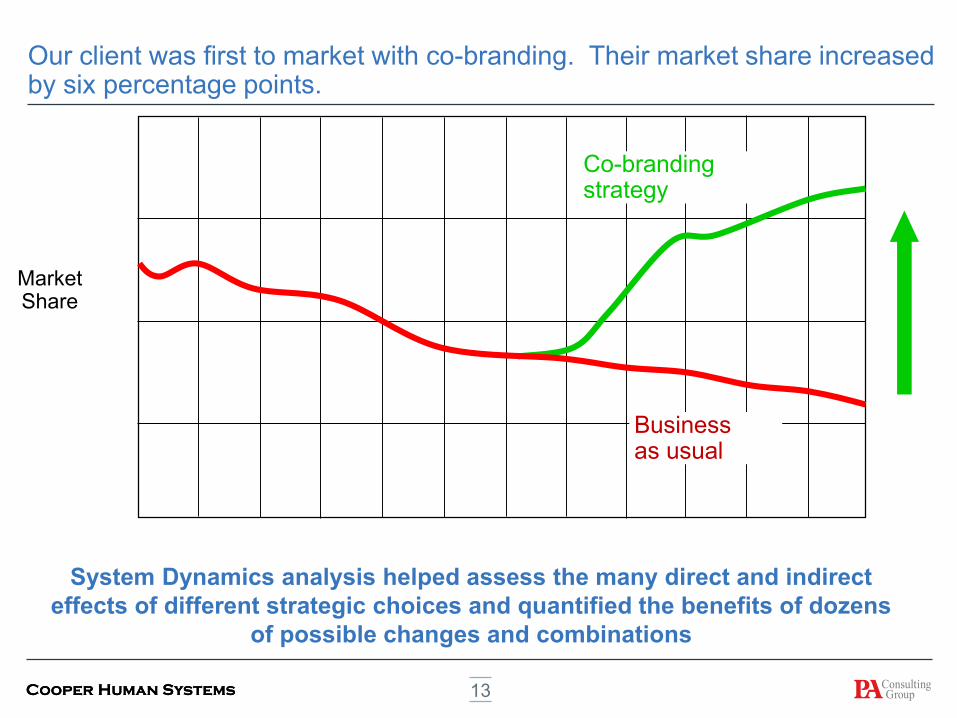

Our client was first to market with co-branding. Their market share increased by six percentage points.

Market Share

Co-brandingstrategy

Businessas usual

System Dynamics analysis helped assess the many direct and indirect

effects of different strategic choices and quantified the benefits of dozens

of possible changes and combinations

14Cooper Human SystemsCooper Human Systems

Co-branded cards transformed the US credit card industry. Sample co-branded credit cards

15Cooper Human Systems

Why System Dynamics was helpful in this case

The model represented the way whole

business works:

Interaction among internal functions

Competitor actions and reactions

Economic and demographic impacts

Built on existing work

Used results of other company models as inputs

Used a wide range of industry data

Represented cause and effect relationships,

employing all forms of information:

Linkages between parts of the system

Soft factors such as brand awareness, reputation, etc.

Decisions rules rather than specific decisions

Quickly simulated how the entire business

and market performed under a wide range of

“What-if...?” questions:

• Less input-intensive once developed

• Fast simulation time

• Built-in analysis and comparison capability

Provided more robust mid-to-long-term

predictive accuracy:

• Dynamic feedback

• Decision rules

• Breadth of model

Helped to build confidence in, and

commitment to, change:

• A mechanism for management participation

• Stimulates discussion of strategic issues

System Dynamics helped the client understand the causes of the problem

and determine the consequences of alternative courses of action

16Cooper Human Systems

APPENDIX

17Cooper Human Systems

David Starr: Dave has been the CIO of three Fortune Five Hundred

companies, advisor to two U.S. Presidents, rated #1 CIO in the country twice,

and is a former member of the Board of Directors of Best Buy Corporation. He

is currently working with Cooper Human Systems using System Dynamics to

build life science models. David has a bachelor in Physics from Florida State,

and has studied at Harvard Business School and Duke University.

Sharon Els: Sharon has specialized in business modelling and simulation for

over twenty years. Her client work has included: assessing emerging strategic

issues and options, optimizing corporate resource allocation, delivering projects

on time and on budget, and resolving large contract disputes and predicting

market changes and evolution. She has consulted to a number of financial,

technology, and defense firms in the U.S. and Europe including Pfizer, 3Com,

Boeing, Raytheon, AT&T, Pepsi, the US Navy and the US Marine Corps.

Sharon holds a bachelor’s degree in Civil Engineering from MIT, and an MBA

from MIT's Sloan School.

Speaker Bios

18Cooper Human SystemsCooper Human Systems

JapanJapan

Stage 3:

Analyzing Strategies in Different

Countries (e.g., UK, Germany, Japan)

GermanyGermany

Later the work was expand to evaluate international markets

UKUK

Outstandings Payments

Transactions

$ volume

Available

Credit

$/transactions

TotalIndustry

Transactions

Economy CardholderProfile

Timeto Pay

Merchantpreference

Propensityto UseCard

MerchantProfile

Technology

Minimum

Credit limit

Economy

Merchant/Cardholder

Match

Share ofCards

CreditLosses

AdvancePosition Issuer

Profits

InterchangeRate

IssuerRevenue

CardsDiscarded

RelativeUse

Cards

CardsIssued

TargetGrowth

BankCards

ResponseRate

AssociationRevenueSolicitations

IssuerAdvance $

Advertising $

CardholderTerms

ShareGap

DesiredShare

MerchantServices

Merchantacceptance

Value-Addedservices

Image

Shareof Ads

Bank Card$ Volume

Share ofIssuer Volume

Qualityof MemberRelations

ServiceQuality

IssuerPromotions

Cardsper

Account Share of

Transactions

Point-of-SaleProblems

DiscountRate

Market

Share

AssociationAdvertising &

Consumer

Cost

Economy

MemberBanks

Regulation

Suppliers

Merchants

Association

Macro-Economy Debit

Stage 1:

Understanding Key

Client Dynamics

Stage 2:

Analyzing US Market Strategy

Options

Client Executive: “We are

often investing in initiatives

that are thwarted by other

actions the organization is

pursuing”Client Executives: “How can

we better compete in this

market place?” Client Executives: “What should we be doing

differently overseas?”