Embed Size (px)

Citation preview

1

Covered Bonds Investor Presentation

March 2018

2

Index

01 EXECUTIVE SUMMARY

Bankia Results……………………………………………………………………. 3

Covered Bonds Ratings…………………………………………………….. 5

02 MORTGAGE COVER POOL

Cover Pool Metrics…………………………………………………………….. 6

Residential Sub-Pool……………………………………..…………………. 8

Commercial Sub-Pool……………………………………………………….. 9

03 WHOLESALE MATURITIES

Wholesale Maturities profile………………………………………..… 10

04 ANNEXES

Macroeconomic Indicators……………………………………………. 11

Spanish Real Estate Markets…………………………………………. 12

D isclaimer

This do cument has beenpreparedbyBankia, S .A. (“Bankia”) and is presented e xclus ive ly fo r in formation purposes. It is no ta prospectus and does no t constitu te an offero r re commendation to invest.

This do cument does not cons titu te a commitment to subs cribe, o r an offer to finance , or an o ffer to se ll, o r a so licitation o f offers to bu yse cu rities of Bankia, allo f whichare s ubject to internal approval by Bankia.

Bankia does no t gu arantee the accu racy or comple teness of the info rmation contained in th is document. The in formation contained here in has been obtained fromsources that Bankia cons ide rs re liab le , bu tBankia does no t represent o r warrant that the information is comple te or accu rate, in particu lar with respect to data pro videdby th ird parties . Th is document may contain ab ridged o r unaudited info rmation and re cip ients are invited to consu lt the pub licdo cuments and information submittedbyBankia to the financial marke t superviso ry au thorities . All o p in ions and es timates are g iven as o f the d ate stated in the document and so maybe sub ject to change.The value o f any investment may flu ctuate as a result o f changes in the marke t. The information in th is do cument is no t intended to pred ict fu tu re resu lts and nogu arantee is given in that respect.

D is tribu tion o f th is do cument in o ther ju risd ictions may be prohib ited, and there fore re cip ients o f th is do cumento r any persons who maye ventually ob tain a copy of itare responsible for being aware of and complying with said restrictions. By accepting this document you accept the foregoing restrictions and warnings.

This document does not re veal all the ris ks o r o ther material facto rs relating to inves tments in the secu rities / transactions of Bankia. Befo re entering into anytrans action, po tential investo rs mus tensu re that they fu lly unders tand the terms o f the secu rities / transactions and the ris ks inhe rent in them. This do cument is no t aprospectus fo r the secu rities described in it. Po tential investo rs should only subscribe for se curities o f Bankia on the bas is of the info rmation pub lished in the appropriateBankia prospectus, noton the basis of the information contained in this document.

3

1Q18 HIGHLIGHTS

NON-PERFORMING LOANS(1) 11.6€

11.0

NPL COVERAGE RATIO 55.1% 53.7%

NPL RATIO 8.7% 9.5%

ATRIBUTABLE PROFIT 229 3M18€

FULLY LOADED CET1 12.7% 13.6%

%

ASSET QUALITY MAR 2018 MAR 2107

PROFITABILITY & CAPITAL MAR 2018 MAR 2017

COST OF RISK(3) 23 3M18

bps

%

%

€bn

ROE

€mn

%

%

CURRENT ISSUER RATINGS

LONG TERM OUTLOOK SHORT TERM

S&P GLOBAL RATINGS

FITCH RATINGS

BBB Stable A-2

BBB- Positive F3

01. EXECUTIVE SUMMARY

Bankia Results

1 COMMERCIAL ACTIVITY

€635mnNew residential

mortgages 3M 18

65%Average LTV new

mortgages

2 EFFICIENCY & PROFITABLITY

51.7%

Cost toIncome

ratio M ar18

0.8%

Operating expenses

1Q18 vs 1Q17 proforma Bankia+BMN

3 LIQUIDITY

92.7%LTD ratio

M ar18

€33.6bnLiquid Assets

M ar18

4 CAPITAL

+533bps

CET1 Phase in Buffer vs SREP

2018 requirements

DBRS BBB (high) Stable R-1 (low)

3043M17

7.5% 3M18

10.2% 3M17

15.67%

Total Solvency Ratio Fully Loaded

M ar18

SCOPE RATINGS BBB+ Stable S-2

31 3M17

(1) As of 31/12/2017 was €9.7bn before effect of consolidating BMN. Post BMN the amount as of 31/12/2017 was €12.1bn

4

ATTRIBUTABLE PROFIT (2)

€816mnNET INTEREST INCOME

€1,968mn

PHASE IN CET1

14.15%FULLY LOADED CET1(4)

12.46%

01. EXECUTIVE SUMMARY

Bankia Results

€

CUSTOMER FUNDS (3)

+22.8%€

BRANCHES

> 2,400CUSTOMER FUNDS

€175,960mnGROSS CUSTOMER LOANS

€128,782mn€

2017 HIGHLIGHTS (1)

UNIVERSAL BANKING MODEL, based on multi-channelmanagement, with a presence throughout Spain and highmarket shares in historical core regions, strengthened withthe merger of Banca Mare Nostrum (BMN).

BEST IN CLASS CORPORATE GOVERNANCE, optimalorganizational structure and highly respected managementteam.

SOLVENT, EFFICIENT AND PROFITABLE INSTITUTION, theGroup ended 2017 with an ROE of 6.6%.

CLEAN BALANCE SHEET, with continuing asset qualitydynamics post merger with BMN, with a reduction of €0.5bn in NPLs in 1Q18.

SUSTAINABLE CAPITAL AND LIQUIDITY GENERATION.Comfortable solvency levels with a Phase In CET1 ratio of14.15% and Fully Loaded CET1 ratio of 12.46%, as ofDecember 2017.

POSITIVE COMMERCIAL DYNAMICS, reflected in thegrowth of fee and commission income (+3.2% year-on-yearat Dec17 and +2.4% year-on-year at Mar18 vs proformaBankia+BMN), offsetting part of the pressure that theeuribor continues to exert on net interest income.

(1) Dec.17 data post merger between Bankia and BMN.

(2) The “Profit/(loss) attributable to the group asreported” amounts to €505mn after includingintegration cost with BMN for €312mn. The BankiaGroup reported income statement, includes BMN’scontribution to the results for the month of Decemberonly.

(3) Includes the off-balance sheet products marketedby BMN, which as from 2018 will be managed byBankia.

(4) Includes IFRS9 impact of -20 bps

5

01. EXECUTIVE SUMMARY

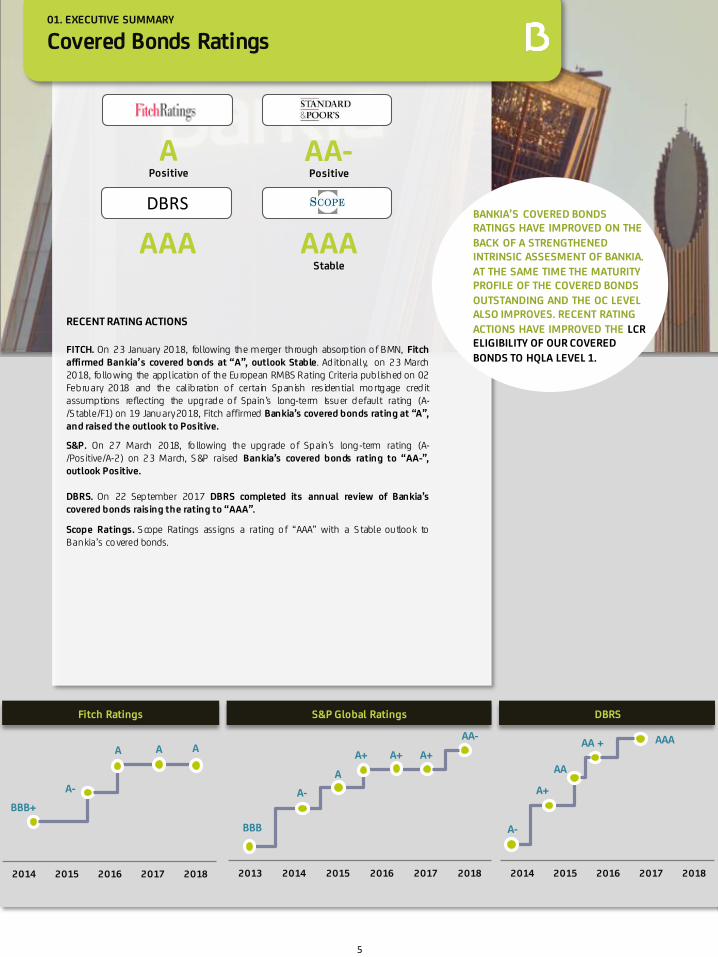

Covered Bonds Ratings

2013 2014 2015 2016 2017 2018

BBB

A-

A

S&P Global Ratings DBRS

2014 2015 2016 2017 2018

A-

A+

A+AA

A+AA +

AA-Positive

AAA

DBRS

APositive

AAAStable

Fitch Ratings

A-

BBB+

A

BANKIA’S COVERED BONDS RATINGS HAVE IMPROVED ON THE

BACK OF A STRENGTHENED INTRINSIC ASSESMENT OF BANKIA.

AT THE SAME TIME THE MATURITY PROFILE OF THE COVERED BONDS

OUTSTANDING AND THE OC LEVEL ALSO IMPROVES. RECENT RATING

ACTIONS HAVE IMPROVED THE LCR ELIGIBILITY OF OUR COVERED

BONDS TO HQLA LEVEL 1.

A+

AAA

2014 2015 2016 2017 2018

A AAA-

RECENT RATING ACTIONS

FITCH. On 23 January 2018, following the merger through absorption o f BMN, Fitchaffirmed Bankia’s covered bonds at “A”, outlook Stable. Ad itionally, on 23 March2018, fo llo wing the application of the European RMBS Rating Criteria published on 02February 2018 and the calibration o f certain Spanish res idential mo rtgage cred itassumptions reflecting the upgrade o f Spain’s long-term Issuer default rating (A-/S table/F1) on 19 January2018, Fitch affirmed Bankia’s covered bonds rating at “A”,and raised the outlook to Positive.

S&P. On 27 March 2018, fo llowing the upgrade o f Spain’s long-term rating (A-/Positive/A-2) on 23 March, S &P raised Bankia’s covered bonds rating to “AA-”,outlook Positive.

DBRS. On 22 September 2017 DBRS completed its annual review of Bankia’scovered bonds raising the rating to “AAA”.

Scope Ratings. S cope Ratings assigns a rating o f “AAA” with a S table outloo k toBankia’s co vered bonds.

6

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Cartera Base Total Cédulas emitidas

85,368

73,680

56,019

44,815

30,162

14,654

Total Collateral Elegible Legal Issuance Issued

02. MORTGAGE COVER POOL

Cover Pool Metrics (1)

AMPLE ISSUANCE CAPACITY

HIGHOC

LEVEL

STRONG ELEGIBLE COVER POOL

COLLATERAL AND CB’s OUTSTANDING

88%Res idential

12%Commercial

76% o f the co verpo ol elig ible € 14,654

millio n IssuanceCapacity

X 80%

2014 2015 2016 2017 2018

X 2,44 o ver-co llateralized

Co llateral CB’s Outstanding

ACTIVE OC MANAGEMENT

(1) Includes BMN`s cover pool.

7

02. MORTGAGE COVER POOL

Cover Pool Metrics (1)

Q1 2018 Q1 2017

Collateral Eligible Collateral Eligible

Outstanding (million €) 73,680 56,019 60,079 45,969

Number of loans 876,653 735,468 673,226 574,803

Number of debtors 795,549 674.367 605,719 529,085

Average S easoning (months) 102 110 94 104

Time to maturity (months) 239 224 244 233

Average LTV 59% 47% 58% 48%

Q1 2018 Q1 2017

Collateral Eligible Collateral Eligible

Residential 63,174 50,514 52.024 42.462

Co mmercial 10,506 5,505 8,055 3,507

COLLATERAL LTV DISTRIBUTION

NPL RATIO

83% OF THE COVER POOL

HAS A LTV RATIO BELOW

80%

NPL’S DECLINING TREND ALTERED BY THE MERGER WITH

BMN

2016 2017 2018

0

5.000

10.000

15.000

20.000

25.000

30.000

0-40% 40%-60% 60%-80% 80%-100% >100%

5,61% 5,48% 5,41% 5,35% 5,31%5,82%

Q4 Q1 Q2 Q3 Q4 Q1

(1) Includes BMN`s cover pool.

8

RESIDENTIAL PORTFOLIO

02. MORTGAGE COVER POOL

Residential Sub-Pool

RESIDENCIAL PORTFOLIO ELIGIBILITY

STANDS AT 79%

AVERAGE LTV OF THE

ELIGIBLE PORTFOLIO IS

49%

Q1 2018 Q1 2017

Collateral Eligible Collateral Eligible

O utstanding (million €) 63,174 50,514 52,024 42,462

Number of loans 821,432 699,232 634,688 548,106

Number of debtors 756,987 647,735 579,995 510,424

Average S easoning (months) 106 113 98 105

Time to maturity (months) 256 235 262 241

Average LTV 58.4% 48.7% 56.4% 49.2%

MATURITY DISTRIBUTION

GEOGRAPHIC DISTRIBUTION Collateral (€mn) Q1 2018

Madrid 17,240

C. Valenciana 9,798

Andalucía 8,840

Catalunya 7,773

Castilla La Mancha 2,736

Canarias 2,615

Castilla y León 2,105

Rest 12,067

87% LOANS FOR PRIMARY RESIDENCE

98% FIRST RANKED MORTGAGES

0

5.000

10.000

15.000

20.000

25.000

30.000

1-5 5-10 10-20 20-30 >30

27%

12%

16%4%

3%

4%

1%

1% 1%1%

1%1%

1%

14%

6%

7%

9

COMMERCIAL PORTFOLIO

RESTRICTIONS TO REAL ESTATE

LENDING IN RECENT YEARS

AVERAGE LTV OF THE ELIGIBLE COMMERCIAL

PORTFOLIO STANDS AT 36%

Q1 2018 Q1 2017

Collateral Eligible Collateral Eligible

O utstanding 10,507 5,506 8.055 3.508

Number of loans 55,221 36,236 38.538 26.697

Number of debtors 38,562 26,632 25.724 18.661

Average S easoning (months) 76 80 67 83

Time to maturity (months) 133 125 132 134

Average LTV 63,6 36,3 68,1% 36,7%

SPLIT BY INDUSTRY CODE

MATURITY DISTRIBUTION

02. MORTGAGE COVER POOL

Commercial Sub-Pool

Real Estate Building&

Materials

Business Services

Retail Food / Beverage/ Tobacco

Lodging/ Restaurants

ConsumerProducts

Healthcare Leisure / Entertainment

Utilities Farming/ Agricultural

Services

Others

21%

18%

12%9%

6%4% 3% 3% 3% 3% 3%

15%

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

1-5 5-10 10-20 20-30 >30

10

2.501 2.764 418

2.025

12.381

260 983

35

101

1.000

175

1.250

2018 2019 2020 2021 >2021

03. WHOLESALE MATURITIES

Wholesale Maturities Amortizing Profile

2,761 4,747 418 2,235 13,731

Amount Outstanding (€mn) 23,892

Covered Bonds (1) 20,088

Senior Debt 1,379

Subordinated debt 2,425

(1) No t including re ta ined covered bonds

11

04. ANNEXES

Macroeconomic Indicators

SPAIN SOVEREIGN DEBT RATING

LONG TERM OUTLOOK DATE

STANDARD & POOR’S

FITCH RATINGS

A- Positive Mar18

A- Stable Jan18

MOODY’S

DBRS

Baa1 Stable Apr18

A Stable Apr18

“GROWTH

CONSOLIDATION

”

“FAVOURABLE

EMPLOYMENT

TREND”

“HOUSEHOLD

SPENDING, MAIN

DRIVER OF THE

ECONOMY”

€

Sales (deflated and seasonally adjusted)

RETAIL TRADE INDEX (Annual Rate %)

UNEMPLOYMENT RATE IN SPAIN

QUARTERLY SERIES GDP. PREVIOUS QUARTER RATE (%)

0,2

0,5

1,1

1,7

2,3

1,7

0,7 0,61

-0,4

1,3

0,6

2,22 1,9

JAN17 FEB17 MAR17 APR17 MAY17 JUN17 JUL17 AUG17 SEP17 OCT17 NOV17 DIC17 ENE18 FEB18 MAR18

0,70,7

0,9

0,8

0,70,7

0,8

0,7

0,9

4T 20173T 20172T 20171T 20174T 20163T 20162T 20161T 20164T 2015

0%

5%

10%

15%

20%

25%

30%

1T 20184T 20173T 20172T 20171T 20174T 20163T 20162T 20161T 20164T 20153T 20152T 20151T 2015

12

04. ANNEX

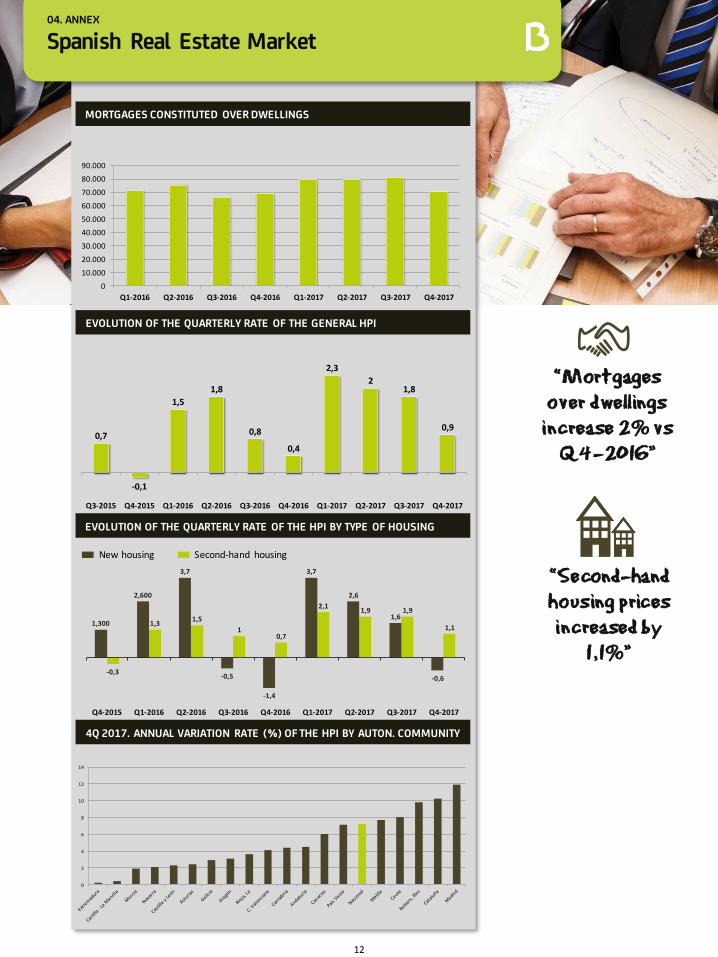

Spanish Real Estate Market

MORTGAGES CONSTITUTED OVER DWELLINGS

EVOLUTION OF THE QUARTERLY RATE OF THE GENERAL HPI

“Mortgages

over dwellings

increase 2% vs

Q4-2016”

“Second-hand

housing prices

increased by

1,1%”

EVOLUTION OF THE QUARTERLY RATE OF THE HPI BY TYPE OF HOUSING

1,1

1,91,92,1

0,71

1,51,3

-0,3-0,6

1,6

2,6

3,7

-1,4

-0,5

3,7

2,600

1,300

Q4-2017Q3-2017Q2-2017Q1-2017Q4-2016Q3-2016Q2-2016Q1-2016Q4-2015

0

2

4

6

8

10

12

14

4Q 2017. ANNUAL VARIATION RATE (%) OF THE HPI BY AUTON. COMMUNITY

New housing Second-hand housing

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017 Q3-2017 Q4-2017

0,9

1,82

2,3

0,4

0,8

1,8

1,5

-0,1

0,7

Q4-2017Q3-2017Q2-2017Q1-2017Q4-2016Q3-2016Q2-2016Q1-2016Q4-2015Q3-2015

13