Embed Size (px)

Citation preview

Country sheet: France 283

Country sheet: France

1.1 Summary

Market characteristics

(i) Very high domestic volumes (France has Europe’s second largest postal market, after

Germany);

(ii) An average population density, however, approximately 25% of the population live in rural

areas which are often sparsely populated and include hills and mountainous territory;

(iii) A reserved area covering all services related to items of domestic correspondence, direct mail

and incoming cross-border correspondence up to 50g and 2.5 times the basic tariff;

(iv) A broad universal service, including items of correspondence, newspapers, periodicals,

catalogues, printed matter weighing 2kg or less and parcels;

(v) A well-developed upstream market where various mail houses and mail consolidators are

active.

Regulatory developments

• Although in 1999 France implemented legislation setting out the limits of the

reserved area according to Directive 97/67/EC, a thorough transposition of Directives

97/67/EC and 2002/39/EC was only completed in 2005. Law no. 2005-516 on

regulation of postal activities reduced the reserved area to 50 grams and assigned

responsibility for regulating the postal sector in France to the regulator for

telecommunications (ART), which was renamed ARCEP. Full liberalisation is not

expected to take place before uniform European liberalisation in 2011. The law

defines four types of ‘means necessary to competitors’ (access rights).

Market developments

• In the cross-border mail, parcels and express segments, the degree of competition is

significant and several large (international) operators compete with La Poste. An

interesting trend is the increase in pick-up points for parcels, for example in tobacco

outlets. Within the unaddressed segment the concentration ratio is very high, with

Adrexo (merged with Kicible in 2006) and Mediapost (La Poste) competing with

each other. The upstream market for mail preparation is of considerable importance

in France, and this part of the value chain has been open to competition for many

years. Various mail houses and mail consolidators are active (around 250), although a

number of these consolidators are in the hands of La Poste and the others have

limited market power as they operate under subcontractor status. The markets for

direct mail preparation and administrative mail preparation are not very concentrated.

• In the addressed mail delivery segment, the results of competition are somewhat

limited and less than what was expected some years ago. With the introduction of

Main developments in the postal sector (2006-2008) 284

Adrexo Mail in 2006 a second delivery network seemed to have been generated.

However, Adrexo announced in February 2008 that it will withdraw from the

addressed mail market. One of the main reasons for this was the postponement of the

date of full liberalisation of the European postal market. Other reasons mentioned

were: barriers for alternative postal operators in Europe and the rules that could be

applied to alternative operators (e.g. financing of the universal service). With the

closing down of Adrexo’s addressed mail network the only alternative end-to-end

delivery network for addressed mail (besides La Poste) will disappear. The estimated

market share of La Poste in the delivery of addressed advertising mail and domestic

items of correspondence is close to 98-99%. It is not likely that this (semi-monopoly)

situation will change fundamentally before 2011.

• An interesting aspect is the international dimension of La Poste, especially in the

(international) parcel and express segments. La Poste owns (or participates in) more

than 200 subsidiaries in France, Europe and the non-European world. Strong brands

are GeoPost (Chronopost and DPD) and Sofipost.

Discussion point

• The development of competition in France in the addressed mail segment is lagging

behind. Since the closing down of Adrexo’s addressed mail network the only party

that could challenge La Poste on a national level (at least in theory) disappeared.

According to ECORYS, this withdrawal is a clear example of the effect of regulatory

uncertainty, and related to the implementation of European decision making. Adrexo

expected full market opening in December 2008, but after the postponement of full

market opening to 31 December 2010, Adrexo stopped (or paused) their investments

and cancelled their attempt to create a dedicated network for addressed mail. In

general, the postponement of European liberalisation seems to have caused a pause in

the initiatives and investments by alternative postal operators to become active in the

delivery of addressed letter mail.

Summary information on market developments:

Postal market

segment/aspect

Competition (market shares) Main competitors / remarks

Express Competitive TNT Express, Exapaq, GLS France

Parcel (main

players)

NPO (n.a.) Alveol, Adrexo/Distrihome, Kiala, Mondial-Relay, Sogep

Unaddressed NPO/Mediapost (50%) Adrexo (50%)

Cross-border mail NPO (80-85%) De Post/La Poste, DHL, DPWN, IMX, Royal Mail, Spring,

Swiss Post, Let France Routage

Addressed mail

(market share

CPOs)*

1-2% Adrexo stopped piloting a (local) dedicated addressed

mail network in 2008; in the upstream market La Poste

has a market share of only 10%

Population density

(inhabitants/km2)

111

Total addressed

mail market (items)

16.5 billion items (2006)

Addressed mail 270 (2006)

Country sheet: France 285

Postal market

segment/aspect

Competition (market shares) Main competitors / remarks

volume per capita

Status of NPO La Poste is a state enterprise Since 1991, La Poste’s legal status has been that of an

‘exploitant autonome de droit public’ – an autonomous

business firm which serves the general interest

Main divisions of

NPO

Mail, express, parcels, retail

outlets and financial services

Note: *The market share of CPOs refers to the combined market share of CPOs in domestic addressed mail

delivery, excluding magazines, periodicals and newspaper delivery. All figures refer to 2007, unless stated

otherwise. N.a. is not available.

Summary information on the implementation of the Postal Directive:

Aspect Implementation and remarks

Universal service and

its financing

The USO includes national and cross-border services for mail (including items of

correspondence, newspapers, periodicals, catalogues, printed matter) weighing 2kg or

less, parcels weighing up to 20kg, recorded delivery items and declared value items.

The USO is financed by the reserved area. It is possible to put a compensation fund in

place.

Reserved area From 1 January 2006 the reserved area covers all services related to items of domestic

correspondence and incoming cross-border correspondence up to 50g and 2.5 times

the basic tariff. Books, catalogues, newspapers and periodicals are explicitly excluded

from the reserved area. Direct (addressed) mail is seen as comprising domestic

correspondence and therefore (< 50g) part of the reserved area.

Licensing and network

access

Postal operators that provide non-reserved postal services relating to items of

correspondence (including cross-border items) should hold an authorisation, unless

their activity is limited to domestic correspondence and does not include delivery.

Some general requirements are linked to the authorisation. Authorisation holders have

access rights to (a part of) the La Poste network and to certain information kept by La

Poste. The CPCE (law) distinguishes four types of ‘means necessary to competitors’.

Tariff principles and

transparency of

accounts

The tariffs within the reserved area need approval by ARCEP, while for the services

that fall under the universal service but not under the reserved area, La Poste should

notify ARCEP before the changes will take effect. In June 2006, ARCEP introduced a

price cap system regarding the universal service provided by La Poste. In the period

2006-2008, tariffs in relation to the universal service could not rise more than a

determined yearly average of 2.1%.

Quality of service The QoS objectives are fixed by the Ministry, annually by a ministerial order. Up to

now, the (indicative) QoS levels to be attained have been defined in the contract

signed between La Poste and the state (e.g. ‘Le contrat de plan 2003-2007’). A new

contract will soon be signed between La Poste and the state specifying the ‘mission de

service public’ of La Poste for the period 2008-2012. In 2007, La Poste did not meet all

of the quality criteria; 82.5% of the mail was delivered the next day, whereas the

threshold was 85%, and the delivery of packages within two days was achieved in

85.8% of cases instead of 90%. For cross-border deliveries, performance was above

target (95.5%, with an 85% threshold).

National regulatory Since the end of 2005, ARCEP has been the independent postal regulator. Its activities

Main developments in the postal sector (2006-2008) 286

Aspect Implementation and remarks

authority (NRA) are mainly related to licensing, monitoring the universal service and accounting/price

control of the USP. Nine employees work full-time on postal affairs, and they receive

some support (2 full-time equivalents (FTEs)) from other services. Their regulatory

powers are broad, including for example regarding the collection of statistical

information.

1.2 General information

France is a large country with an average population density (111 inhabitants/km2

compared with the European average of 113 inhabitants/km2). However, around 25% of

the population live in rural areas that are often sparsely inhabited and include hills and

mountainous territory.1 Only 7% of the 61 million inhabitants live in the five largest

cities, of which Paris is the largest with 2.1 million inhabitants (see Table 0.1). If we take

into account Paris and its suburbs (Ile-de-France), the number of inhabitants is 11.4

million (circa 18% of the total population).2

Table 0.1 General country information (2007)

France

Population (in millions) 61.3*

Size of country (1,000 km2) 551.5*

Population density (inhabitants/km2) 111.2*

Degree of urbanisation 76.7**

Number (and %) of inhabitants in 5 largest cities 4.2 million (6.9%)***

Sources: *UPU (2006); **UN (2005); ***World Gazetteer (2008 estimate).

1.3 Regulatory developments

1.3.1 Postal law and regulation

The law of 25 June 1999 on spatial planning and sustainable development transposed the

main obligations of Directive 97/67/EC of 15 December 1997 defining the universal

service with its principles and the guarantees given to users, as well as the reserved area

for the universal service provider, and designating La Poste as the postal universal service

provider in France. A thorough transposition of Directives 97/67/EC and 2002/39/EC was

only completed in 2005.

Law no. 2005-516 on the regulation of postal activities (Postal Act 2005) reduced the

reserved area to 50 grams (in accordance with the Directives) and assigned the

1 ECORYS 2005a.

2 INSEE (Institut National de la Statistique et des Etudes Economiques), facts and figures No 112, January 2006 (figures

based on 2005).

Country sheet: France 287

responsibility for regulating the postal sector in France to the regulator for

telecommunications (ART), which was renamed ARCEP (Autorité de Régulation des

Communications Electroniques et des Postes). ARCEP was granted full authority for

regulating the postal sector, e.g. granting of licences, tariff control, supervision of the

universal service provision and its sustainability, access rules and settlement of disputes

between operators.

The French Post and Electronic Communications Code (CPCE) was amended by the

Postal Act 2005 and also by some secondary legislation. For example, the scope and

nature of the universal service were defined in the Decree of 5 January 2007 on the USP,

and Decree no. 2006-507 of 3 May 2006 detailed the licensing procedures and settlement

of disputes (see Table 0.2).

Table 0.2 Postal law and regulation

Postal law and

regulation

Date of introduction Date of latest

amendment

Remarks

Post and Electronic

Communications Code

27 February 1952 20 May 2005 (Law no.

2005-516 on regulation

of postal activities)

Decree no. 2007-310

on the national postal

fund for geographical

equalisation

5 March 2007

Order enacted in

application of article

R.2-1 of the CPCE and

setting out the terms

and conditions for

posting and delivery of

postal shipments

7 February 2007 Applies to all postal operators

Decree no. 2007-29 on

the universal postal

service and the rights

and obligations of La

Poste and amending

the CPCE

5 January 2007 Defines the universal service and

the rights and obligations of La

Poste regarding its postal public

service missions

Decree no. 2006-1239

on La Poste’s

contribution

to regional planning

11 October 2006 Defines La Poste’s contribution

to regional planning

Decree no. 2006-1020

concerning postal

service operators’

liability

11 August 2006 Applies to all postal service

operators

Order of 3 May 2006

implementing article

R.1-2-6 of the CPCE

3 May 2006 Applies to the licensees

Main developments in the postal sector (2006-2008) 288

Postal law and

regulation

Date of introduction Date of latest

amendment

Remarks

relating to the

obligations of licensed

postal service

providers

Decree no. 2006-507

on regulation of postal

activities, amending

the CPCE

3 May 2006 Applies to the licensees

Law no. 2005-516 on

regulation of postal

activities

20 May 2005 Reduces the reserved area to 50

grams. Introduction of an

independent regulator (ARCEP,

previously ART)

Law no. 90-568

concerning

organisation of the

postal public service in

France and France

Telecom

2 July 1990 20 May 2005 Applies to the operating rules for

La Poste. Amended by Law no.

2005-216 of 20 May 2005

Source: ECORYS desk research, ECORYS questionnaire – ARCEP, La Poste and Ministry of Economics,

Industry and Employment.

1.3.2 Universal service obligation

La Poste was officially designated as the universal service provider in France in 1999;

this was also registered in article L.2 of the CPCE. Regarding the universal postal service,

the CPCE states that La Poste shall provide all users across the whole of the national

territory with permanent postal services that meet established quality standards and that

these services shall be offered at affordable prices for all users.

Scope of the universal service

The universal postal service includes national and cross-border services for mail weighing

2 kilograms or less, parcels weighing up to 20 kilograms, recorded delivery items and

declared value items. The particular features of the universal service are laid down in

Decree 2007-29 of 5 January 2007, which states that the universal postal service shall

cover provision of domestic and cross-border postal services for the following (article

R.1):

• items of correspondence weighing up to 2kg, including:

o ordinary individual and bulk mail, where individual domestic mail shall include

both priority and non-priority items;

o registered items with or without acknowledgement of receipt.

• newspapers and periodicals weighing up to 2kg;

• catalogues and other printed matter weighing up to 2kg;

Country sheet: France 289

• postal packages weighing up to 20kg, sent singly to the public as ordinary or

registered items and excluding postal services provided to businesses under contracts

covering multiple items;

• insured items of a value below the limit determined by a decree of the Minister for

Postal Services;

• redirection of the postal items (under the USO);

• literature for blind people in the form of ordinary or registered items.

Books, catalogues, newspapers and periodicals are not seen as items of correspondence.

Direct mail however forms part of items of correspondence (article R.1).

The postal items covered by the universal service shall, except in special circumstances,

be duly approved by the national regulator and be collected and delivered on every

working day (so six times, Saturday is seen as a working day) throughout metropolitan

France (articles R.1-1 and R.1-1-1).

In accordance with article R.1-1-10 and taking into account the categories above, La

Poste as the universal service provider defined a catalogue of universal service products.

La Poste shall simultaneously forward to the Minister for Postal Services and ARCEP

any proposals for substantive changes (other than tariff changes) to the catalogue

affecting services relating to individual mail covered by the universal service. ARCEP

shall have one month from receipt of the document to issue its opinion and forward it to

the Minister for Postal Services. If no objection has been notified by the Minister for

Postal Services within two months of the document’s receipt, the changes shall be

deemed to be approved. La Poste shall also inform the Minister for Postal Services and

ARCEP of any changes to the catalogue affecting bulk mail services.3

Scope of the network

The universal service shall be provided permanently to all users throughout metropolitan

France. Article R.1-1 determines that the services covered by the universal service shall

be within reach of users. Post-office branches providing public access to services covered

by the universal service, must be so located that at least 99% of the national population

and at least 95% of the population of each département is less than10 kilometres from a

post-office branch and all communes with over 10,000 inhabitants have at least one post-

office branch per 20,000 inhabitants.

Compensation fund

Considering USO financing, article L.2-2 of the CPCE provides for the possibility of

putting a compensation fund in place at the request of the universal service provider.

Regarding the costs of providing the universal service (and related to that, the sources of

financing it), ARCEP reported that the costs of the universal service have not been

appraised (or communicated by La Poste) so far.4

3 ECORYS questionnaire – Ministry.

4 ECORYS questionnaire – ARCEP and La Poste.

Main developments in the postal sector (2006-2008) 290

Provision for blind and partially sighted people

The universal service also contains provisions for blind and partially sighted people.

Article R.1 states that literature for blind people – in the form of ordinary or registered

items – is free of charge when subject to the conditions laid down by an order of the

Minister for Postal Services.

1.3.3 Reserved area

From 1 January 2006 the reserved area comprises all services covering items of domestic

correspondence and incoming cross-border correspondence, including those sent by

priority mail, weighing less than 50 grams and whose price is under 2.5 times the basic

tariff (article L.2 CPCE). Books, catalogues, newspapers and periodicals are explicitly

excluded from the reserved area. Direct (addressed) mail is seen as domestic

correspondence and therefore (partially) within the scope of the reserved area (article L.1

CPCE).

For segments like parcels, express, mail preparation and consolidation no regulatory

framework has ever been implemented.5

Table 0.3 shows the scope of the reserved area.

Table 0.3 Liberalisation of postal services and the reserved area (2008)

Postal product Within reserved area

(yes, no, partially or unclear)

Remarks

Bulk mail and consolidation

B2B non-bulk mail*

Individual item mail

Partially Items of domestic correspondence up

to 50g and 2.5 times the public tariff

are still within the reserved area.

Books, catalogues, newspapers and

periodicals are not items of

correspondence. Direct mail forms

part of items of correspondence.

Consolidation (upstream) is not part

of the reserved area.

Items of correspondence

Cross-border mail Partially Outgoing cross-border mail is

liberalised. Inbound cross-border mail

up to 50g and 2.5 times the public

tariff is still within the reserved area.

Unaddressed mail No

Parcel mail No

Express mail No

Source: ECORYS desk research.

Note: *La Poste refers to this category as ‘individual items sent by firms’ (to businesses or consumers).

5 Gallet-Ryback, Moreno, Nadal and Toledano (2008).

Country sheet: France 291

As far as we know, no plans have been made to liberalise any further before the European

liberalisation date of 31 December 2010.

1.3.4 NRA

Since 2005, ARCEP (Autorité de Régulation des Communications Electroniques et des

Postes) has been the independent postal regulator. As mentioned above, ARCEP was

granted full authority for regulating the postal sector.

The main ARCEP activities are threefold (ARCEP website):

• Issuing licences and implementing the rights and obligations attached to them. In the

CPCE a licensing system is introduced for domestic mail delivery and cross-border

correspondence (article L.5-1);

• Monitoring La Poste’s universal service mission and in particular its performance in

terms of quality of service (articles L.5-2, 4° and R.1-1-8). These quality

requirements will be issued by the minister in charge of the postal sector, after giving

the universal service provider an opportunity to make its submissions and obtaining

the opinions of ARCEP and the Commission for the Public Service of Postal and

Electronic Communications;

• Accounting and price control of the universal service provider (article L.5-2). In order

to implement the principles of separate, transparent accounts, and in particular to

guarantee the universal service’s financing conditions, ARCEP shall define the cost-

accounting principles, establish the accounting system specifications and ensure

compliance by the universal service provider with the cost-accounting obligations

laid down in the decree on universal service (article R.1-1-15). In 2007, ARCEP

published a decision (no. 07-443) on the specification of the format and content of the

regulatory accounts. After a public consultation process, ARCEP adopted a decision

concerning the accounting rules on 12 February 2008.6

Further, ARCEP has the power to impose penalties on the universal service provider or

other operators authorised under article L.3 if they violate the obligations regarding the

universal service (article L.5-3). Table 1.4 summarises the NRA’s regulatory powers.

Regarding ARCEP’s involvement in issues relating to competition, there is the possibility

that ARCEP will inform the national competition authority (Conseil de la concurrence)

about forbidden cartel agreements and abuse of dominant position. ARCEP has already

asked for the opinion of the French competition council on La Poste’s rebate policy

(Conseil de la concurrence, avis no. 07-A-17).7 Furthermore, it is possible that the

national competition authority will ask ARCEP for more information on its view on

competition issues in the postal sector (article L.5-8).

6 ECORYS questionnaire – ARCEP, La Poste.

7 ECORYS questionnaire – La Poste.

Main developments in the postal sector (2006-2008) 292

Capacity of the NRA

At the end of 2006, ARCEP’s total staff capacity was 163 people.8 Nine employees work

full-time on postal affairs. In addition, the postal regulation department receives legal and

economic support from other services (approximately equivalent to 2 FTEs).9

Complaints and redress procedures

Another of ARCEP’s tasks is the settlement of disputes between postal actors (postal

operators, consolidators or clients) regarding contracts. These range from disputes

concerning the (normal) conditions of the universal service (article L.5-4) to those

relating to (third-party) access to certain facilities of the incumbent (article L.5-5).10

To date, ARCEP has only settled one dispute between La Poste and a consolidator. The

consolidator challenged the regulator’s decision before the Court of Appeal of Paris,

which confirmed the absence of discriminatory practice by La Poste (decision no. 2007-

0635).11

In recent years, ARCEP has taken steps to establish contacts with customers’ associations

and, when applicable, they will be consulted.12

Table 0.4 Regulatory powers of the NRA

Powers Yes/no/unclear Remarks

Require data from USP – can the NRA

require the USP to disclose existing

records?

Yes La Poste shall supply any information requested

by ARCEP for the purpose of carrying out its

duties and supervising the universal postal

service (article R.1-1-16, decree on universal

service)

Require accounting system – can the

NRA require the USP to maintain

regulatory accounts in the manner

determined by the NRA?

Yes The accountancy obligations are set out in

secondary legislation.13

ARCEP shall define the cost-accounting

principles, establish the accounting system

specifications, and ensure compliance with the

cost-accounting obligations (article L.5-2)

Require new data studies – can the NRA

require the USP to collect new data,

possibly at substantial expense to the

USP?

Yes La Poste shall supply any information requested

by ARCEP for the purpose of carrying out its

duties and supervising the universal postal

service (article R.1-1-16, decree on universal

service)

Cancel unlawful rates – authority to

cancel unlawful tariffs

No ARCEP approves tariffs within the reserved

area and may give reasoned public opinion on

tariffs within the universal service open to

competition (article L.5-2). ARCEP may impose

8 ARCEP (2007a).

9 ECORYS questionnaire – ARCEP.

10 ECORYS questionnaire – La Poste.

11 ECORYS questionnaire – La Poste; see also Gallet-Ryback, Moreno, Nadal and Toledano (2008), p. 21.

12 ECORYS questionnaire – ARCEP.

13 ECORYS questionnaire – La Poste.

Country sheet: France 293

Powers Yes/no/unclear Remarks

penalties (article L.5-3)

Levy fines – impose fines in case of

unlawful activity

Yes ARCEP has the power to impose penalties

under certain circumstances (article L.5-3)

Seek judicial order – to seek judicial

enforcement of regulatory orders

Uncertain

Set new rates for USP – authority to set

lawful tariffs even if the USP does not

propose them

No

Require downstream access – authority

to require the USP to provide

downstream access even if it does not

wish to do so

Uncertain/no According to ARCEP – very uncertain.

La Poste – no, in accordance with article L.2-1

La Poste can conclude access to network

contracts based on special tariffs (negotiated

access) with large customers, consolidators and

competitors. These tariffs must not be

discriminatory.

Require data from non-USPs – authority

to require information from postal

operators other than the USP

Yes Licence holders shall provide ARCEP annually

with statistical information on the use, coverage

area and access arrangements of their services

(article R.1-2-7)

Source: ECORYS desk research, questionnaire.

1.3.5 Licences

Postal operators which provide non-reserved postal services relating to items of

correspondence (including cross-border items) should hold an authorisation, unless their

activity is limited to domestic correspondence and does not include delivery (article L.3).

Authorisations are valid for 10 years.

Authorisation holders should meet the following general requirements (Decree no. 2006-

507):

• guaranteeing safety of users, staff and service provider’s equipment;

• guaranteeing confidentiality of items of correspondence and the integrity of their

contents;

• providing users with access to a free, simple and transparent complaints procedure;

• protecting personal data and privacy;

• ensuring that the technical requirements for service provision are environmentally

friendly;

• identifying the postal items they deliver with a distinctive sign.

Further, Decree no. 2006-507 demands that licence holders shall provide ARCEP with

annual statistical information on the use, coverage area and access arrangements of their

services, including data on the nature and volume of the various mail services covered by

their authorised activity.

Main developments in the postal sector (2006-2008) 294

The request for an authorisation needs to be drawn up in French and needs to contain all

manner of information: (i) information about the requestor, (ii) technical data, (iii)

commercial data, (iv) information on technical capacity, and (v) information on financial

capacity.

The CPCE states that ARCEP can refuse an authorisation only through a considered

decision on grounds based on the applicant’s financial, economic or technical inability to

comply on a long-term basis with the obligations attached to its postal activity (article

L.5-1). Getting an authorisation is free of charge.

Table 0.5 Entry regulations

Instrument Services allowed under

the licence

Conditions for obtaining

the licence

Number of licences

approved (2007)

Authorisation Services relating to items

of correspondence

(including cross-border

items) that are not part of

the reserved area

Requirements regarding

(i) safety, (ii)

confidentiality, (iii)

transparent access, (iv)

privacy, and (v) the

environment

20

Source: ECORYS desk research, ARCEP website.

ARCEP has granted 20 licenses. 12 licenses (including La Poste) are granted to postal

operators for domestic mail delivery (letters > 50g) and nine (including La Poste) to

operators for outgoing cross-border mail.14

These domestic operators focus on local

markets (e.g. a city) and only Adrexo focused on the whole country.

1.3.6 Access

Upstream activities have been liberalised in France for a long time.15

Large customers,

mailing houses and mail consolidators can deliver their mail at different levels of La

Poste sorting centres (at national level, department level (ca. 100), and postal code level

(ca. 40,000)) at discounted prices. The terms of delivery are negotiated and non-

discriminatory (article L.2-1).16

Authorisation holders have access rights to (a part of) the La Poste network and to certain

information kept by La Poste (based on article L.3-1). The CPCE distinguishes four types

of ‘means necessary to competitors’:

• Delivery service to PO boxes installed in post offices for customers opting for this

particular type of delivery;

• The postcode directory, supplemented by the link between these codes and the

geographical information about streets and addresses. It is important for a reference

14

Gallet-Ryback, Moreno, Nadal and Toledano (2008). 15

Gallet-Ryback, Moreno, Nadal and Toledano (2008) have described the historical background of mail preparation in

France. 16

ECORYS (2005a).

Country sheet: France 295

work like the postcode directory, or any other geographical reference work used for

addressing mail, to be transparent;

• Information collected by La Poste about addressees’ changes of address. In the past,

this information was of course notified to the operator holding the postal monopoly.

Its retransmission to new postal market entrants, in accordance with economic

procedures yet to be specified, is an obvious prerequisite for balanced competition;

• A redirection service in the event of change of address. This type of service cannot be

taken on by an authorised operator when the addressee’s new address is outside the

geographical area covered by that operator. In such cases, La Poste will perform this

service on behalf of the authorised operator.

Access to the delivery network and PO boxes is mandatory. Terms and conditions should

be negotiated between access seeker and La Poste. If a dispute arises, ARCEP has to

settle the dispute and may set the terms and conditions.17

ARCEP mentions that access to letterboxes has raised several legal and technical issues

(building security, law on private property). However, the CPCE stipulates that the USP

and authorisation holders are entitled to access letterboxes in order to deliver postal items.

Article L.5-10 demands that the USP and authorisation holders have access on the same

terms.

ARCEP has conducted a public consultation, resulting in a compromise solution by

which all licensees will be given access to the access codes (managed by La Poste) in

order to reach letterboxes.18

Table 0.6 Network access

Upstream/downstream Form of access Regulated?

(yes, no, unclear)

Upstream Access to street letter boxes No

Access to outward sorting centres

Downstream Access to inward sorting centres

Access to delivery offices

No. Large customers, consolidators

and competitors have access to La

Poste network based on special

tariffs (negotiated access). These

tariffs must not be discriminatory.19

Access to PO boxes Yes

Source: ECORYS (2005a), ECORYS questionnaire – La Poste.

1.3.7 Price regulation

ARCEP determines (based on La Poste’s proposal or own research) ‘the particular

features of the multi-annual tariff framework for universal service provision’, and can

17

ECORYS – private contact with ARCEP. 18

ECORYS questionnaire – La Poste. 19

ECORYS questionnaire – La Poste.

Main developments in the postal sector (2006-2008) 296

distinguish between individual and bulk mail (article L.5-2 CPCE). Relating to this,

ARCEP introduced in June 2006 a price cap system regarding the universal service

provided by La Poste. In the period 2006-2008 tariffs in relation to the universal service

could not rise more than the yearly average of 2.1% (ARCEP, decision no. 06-0576, La

Poste press release 13 June 2006).

The tariffs within the reserved area need approval by ARCEP. For the services that fall

under the universal service but not under the reserved area, La Poste should notify

ARCEP before the changes will take effect. In such cases, ARCEP may give a reasoned

public opinion (article L.5-2 CPCE).

The Postal Act 2005 allows La Poste to negotiate with bulk mailers, consolidators of mail

from different customers and licence holders about specific contracts that deviate from

the standard terms and conditions of universal service provision, including special tariffs

for business services. However, these tariffs and conditions have to be objective and non-

discriminatory and should take into account the avoided costs (article L.2-1 CPCE).

1.3.8 Quality of service

As mentioned above, one of ARCEP’s tasks is to monitor La Poste’s quality performance

relating to the universal service obligation. The objectives of service quality are fixed by

the Ministry, annually by a ministerial order. The contract signed between La Poste and

the state (e.g. ‘Le contrat de plan 2003-2007’) also defines the level of quality of services

to be reached (see Table 0.7).20

According to article L.5-2 of the CPCE, ARCEP

commissions an independent body to carry out a study on quality of service on an annual

basis and publishes the results.21

A new contract will soon be signed between La Poste and the state specifying the

‘mission de service public’ of La Poste for the period 2008-2012.22

ARCEP has undertaken some steps to increase the transparency of the universal service

by involving various stakeholders.23

In particular, postal service users were consulted

about their needs and expectations regarding information on the quality of the universal

postal service. On the basis of this consultation, ARCEP and La Poste have examined the

possibility of carrying out reliable measurement when it appears to be useful and

publishing the information needed most by postal service users. La Poste carries out the

measurements and publishes the results. ARCEP makes sure that the measurements are

reliable and that the information made public fits the needs of postal users.

In 2005 and 2006, information concerning the transit time of the main universal service

postal products was published (domestic single piece priority mail, parcels, cross-border

mail). On the basis of the consultation results, the (categories of) information measured

20

ECORYS questionnaire – Ministry of Economy, Industry and Employment. 21

ECORYS questionnaire – La Poste. 22

ECORYS questionaire – Ministry of Economy, Industry and Employment. 23

ECORYS questionnaire – ARCEP.

Country sheet: France 297

and made public will increase year on year. For instance, the number of collection points

regarding latest collection time and the satisfaction rate for the handling of complaints

were published for the first time this year. In 2009 (based on 2008 data), this should result

in the publication of information on: (i) parcels – substantial delays, (ii) transit time of

registered mail, and (iii) registered mail – substantial delays. ARCEP and La Poste are

also working on the possibility of publishing information on the transit time of delivery

advices.

Table 1.7 shows that La Poste has not met all of the quality criteria. In 2007, 82.5% of the

mail was delivered the next day, while the threshold was 85%. The delivery of packages

within two days was met in 85.8% of cases instead of 90%. For cross-border deliveries,

performance was above target. La Poste indicated that these results must be analysed

taking into account the specificities of French territory (low density and many districts to

deliver to across the whole territory: 36,000).24

Table 0.7 Quality of service by USP (2006 and 2007)

Standard Threshold Performance of USP Remarks

Delivery D+1 (prior)

Delivery D+2 (prior)

85%

95%

2006: 81.2%

2007: 82.5%

2006: 96.2%

2007: 96.3%

In 2002, only 67% of the

priority mail was delivered

the next day

% of lost mail n.a. 0.09%* Rough estimation of

ARCEP/TNS Sofres

(2006). The % of lost mail

for received items (by

households) is 0.03%,

and 0.09% for sent items.

Delivery of cross-border

mail D+3 (inbound)

Delivery of cross-border

mail D+3 (outbound)

Delivery of cross-border

mail D+5 (inbound)

Delivery of cross-border

mail D+5 (outbound)

85%

85%

97%

2006: 95.9%

2007: 95.5%

2006: 94%

2007: 94.8%

2006: 99.3%

2007: 99.1%

98.7%

98.8%

Delivery D+2 of packages

Delivery D+3 of packages

Delivery D+4 of packages

90%

95%

-

2006: 84.1%

2007: 85.8%

2006: 95.5%

2007: 96%

2006: 98.5%

24

ECORYS questionnaire – La Poste.

Main developments in the postal sector (2006-2008) 298

Standard Threshold Performance of USP Remarks

2007: 98.7%

Source: La Poste (2008b).

*La Poste (ECORYS questionnaire) indicated that the percentage of lost mail and the total ‘loss rate’ are based

on the perceptions of users (panel of 1,022 clients). This estimation cannot be compared with the results of the

statistical analysis of the quality performance of the USP.

Note: n.a. is not available.

Random check on quality

Regarding the percentage of lost mail, 78% of French households (and 69% of

companies) declared that during the 12 months before the random check they received all

the letters or parcels they expected, or received them without any damage.25

Some 9% of

households (and 18% of companies) declared that they had not received an expected letter

(for parcels the figure was 4% for both households and companies). ARCEP estimates the

total ‘loss rate’ for letters not received as three in 10,000 (0.03%) for households and one

in 10,000 for companies (0.01%).

The ‘loss rate’ for items sent by households was higher: probably nine in 10,000 (0.09%)

(and one in 10,000 for companies). Some 6% of households (and 17% of companies)

declared that a sent letter was never received. For parcels this figure was 2% for

households and 5% for companies. Overall, 89% of households (and 775 of the

companies) did not experience the loss of any sent items.26

Monitoring compliance with CEN standards

Measuring the quality of the universal service, the number of complaints and how they

have been handled calls for reliable methods and supervision of their correct application.

The transit time of single piece priority mail and the number of complaints are measured

according to the specifications of EN 13850 and EN 14012 respectively. The other

quality of service indicators will have to be made more and more auditable. The standard

EN 13850 provides for an end-to-end measurement system encompassing all postal

operator responsibilities, starting from the point where the item is collected or accepted

up to its final delivery. Quality of service is evaluated using the findings of a survey

based on test letters exchanged between panellists.27

In 2006, ARCEP commissioned an audit of the service quality for ordinary letters from

the consultancy firm of Ernst and Young. The purpose of this audit was to check whether

La Poste’s measurement complies with the standard EN 13850, which was made

mandatory under European and national regulations. The auditor identified the need for a

number of improvements to ensure better compliance with EN 13850. ARCEP and La

Poste are working on implementing these recommendations.28

25

ARCEP (2006d). 26

ARCEP (2006d). 27

ECORYS questionnaire – ARCEP. 28

ECORYS questionnaire – ARCEP.

Country sheet: France 299

1.4 The mail market

ARCEP has reported that in 2006 the volume of the French postal market was circa 39.3

billion items (2005 figure: 39.6 billion items), with a turnover of circa € 15.2 billion

(2005 figure: € 15 billion). Thus total volume decreased in 2006 while revenues

increased. Most market segments lost volume of turnover, except for registered letters

and parcels and domestic and cross-border parcel delivery. The market for unaddressed

items did not change in volume, but generated 4.5% more revenue.29

Mail volumes are expected to decline further, for example because of rationalisation

(such as less frequent mailings, putting two bills in one envelope, ensuring that close to

35 grams of mail is put in an envelope for that weight category) and substitution

(electronic billing in the B2B area, internet for consumer mail).30

1.4.1 Mail market overall

In 2006, the overall volume of the postal market was approximately 39.3 billion items,

representing a value of € 15.2 billion (see unnumbered table below). Unaddressed (direct)

mail was the largest submarket in volume (47%), but the value was only 4.3% of the total

turnover, which confirms that these are low value-added activities. Turnover in 2006

increased by 4.4% compared with 2005. ARCEP (2007a) noted that this rise in volume

was related to increased prices because of the introduction of an environmental tax

(January 2005) and the application of a new (minimum salary) agreement (June 2005).

Table 0.8 Overview of the postal market in 2005 and 2006 (in million items and million €)

Volume (2005) Volume (2006) Turnover (2005) Turnover (2006)

Items of

correspondence

16,806 16,540 8,470 8,435

Registered letters and

parcels

276 279 1,302 1,382

Parcels

o/w ordinary parcels

o/w express light

parcels

638

o/w 358

o/w 280

665

o/w 365

o/w 300

3,464

o/w 1,464

o/w 2,000

3,698

o/w 1,598

o/w 2,100

Paid press delivery 2,789 2,710 492 484

Total addressed items

delivered in France

20,509 20,194 13,728 13,999

Items of

correspondence

(export)

523 480 500 422

Ordinary parcels

(export)

7 8 74 85

Press (export) 28 27 31 29

29

ARCEP (2007b). 30

ECORYS (2005a).

Main developments in the postal sector (2006-2008) 300

Volume (2005) Volume (2006) Turnover (2005) Turnover (2006)

Total addressed items

exported

558 516 605 536

Unaddressed

advertising

18,570 18,568 630 658

Total 39,637 39,278 14,963 15,193

Source: ARCEP (2007b).

Note: imports are included in the overall figure for items of correspondence, registered items, parcels, press

items and unaddressed advertising; paid press delivery does not include revenue from non-postal delivery of

press.

The second largest submarket – items of correspondence (individual item mail, bulk mail

and B2B non-bulk mail) – generated € 8.4 million in 2006 (55% of the total) and

represented 16.5 billion items (42%). In 2006, the reserved area (up to 50g) encompassed

only 35% of the volume of the total market, but nearly 84% (in volume, 73% in terms of

revenue) of the market for items of correspondence. In 2005, the corresponding figures

were 39% of the total market and 92% of the market for items of correspondence (in 2005

the reserve area was still up to 100g).31

The (domestic) market for delivery of parcels is growing (up 2% in 2006 compared with

2005), while the export of parcels (8 million items) increased by 18% compared with

2005. Turnover increased by 9.1% for domestic parcel delivery and 14.6% for cross-

border delivery. The volumes and turnover of the express market stayed nearly the same.

Regarding cross-border mail (items of correspondence), the volume decreased to 480

million items (-8.1%) and turnover fell by € 422 million (-15.5%).

Table 0.9 Size of the mail market in turnover (million €)

Postal product 2005 2006

Bulk mail and consolidation n.a. n.a.

B2B non-bulk mail n.a. n.a.

Individual item mail n.a. n.a.

Items of correspondence 8,470 8,435

Cross-border mail 500 422

Unaddressed mail 630 658

Parcel mail < 30 kg 1,464 1,598

Express mail 2,000* 2,100*

Total 14,963 15,193

Source: ARCEP (2007b); *estimated by the Ministry of Transport.

Note: Not shown in the table: registered letters and parcels (2005: 1,302; 2006: 1,382), domestic press items

(2005: 492; 2006: 484) and exported press (2005: 31; 2006: 29). Parcel mail: excluding export (2005: 74; 2006:

85). Cross-border mail: only export. Import traffic could not be isolated: € 251 million in 2006, including items of

correspondence, registered mail, press items and ordinary parcels. Express mail: this estimation by the Ministry

of Transport does not include the activities of all operators. It includes domestic and outgoing transborder items.

Note: n.a. is not available.

31

ARCEP (2007b).

Country sheet: France 301

Table 0.10 Size of the mail market in physical terms (million items)

Postal product 2005 2006

Bulk mail and consolidation 9,873 9,571

B2B non-bulk mail* 3,673 3,824

Individual item mail 3,260 3,144

Items of correspondence 16,806 16,540

Cross-border mail** 523 480

Unaddressed mail 18,570 18,568

Parcel mail 358 365

Express mail*** 280 300

Total 39,637 39,278

Source: ARCEP (2007b); *items of correspondence sent by firms; **items of correspondence (export);

***estimated by the Ministry of Transport.

Note: Not shown in the table: registered letters and parcels (2005: 276; 2006: 279), domestic press items (2005:

2,789; 2006: 2,710) and exported press (2005: 28; 2006: 27). Parcel mail: export excluded (2005: 7; 2006: 8).

Cross-border mail: only export. Import traffic could not be isolated: 390 million items in 2006, including items of

correspondence, registered mail, press items and ordinary parcels. Express mail: this estimation by the Ministry

of Transport does not include the activities of all operators. It includes domestic and outgoing transborder items.

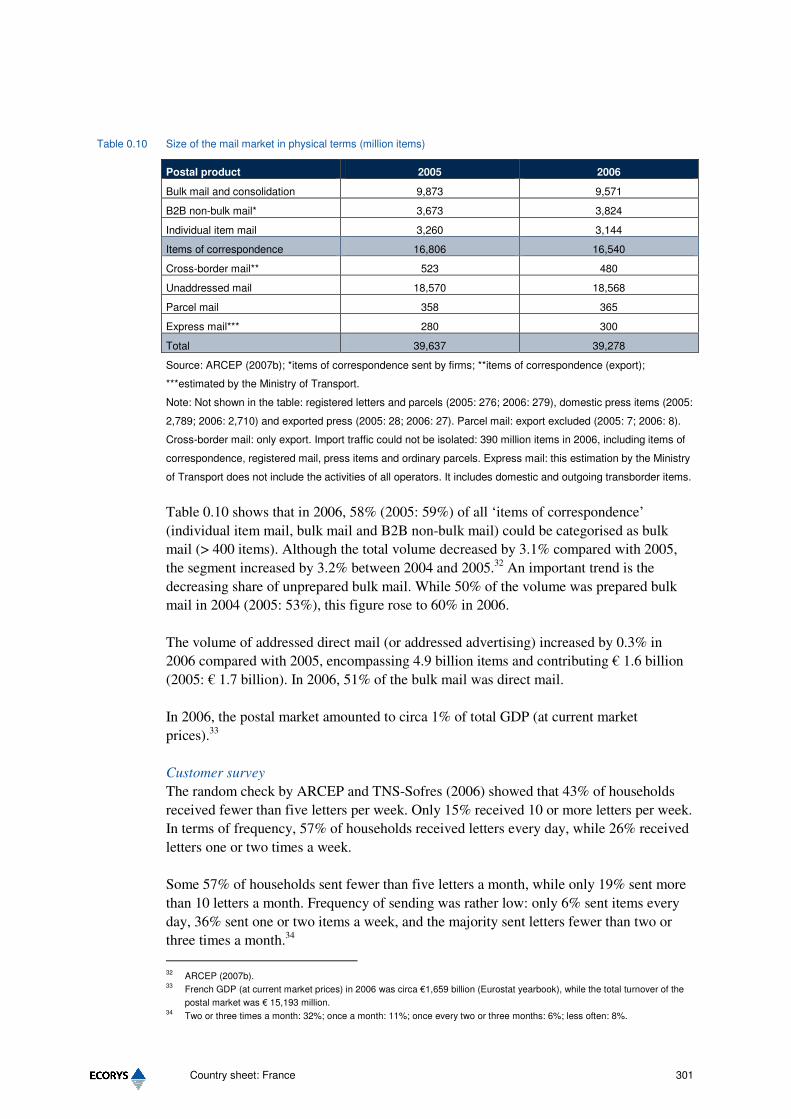

Table 0.10 shows that in 2006, 58% (2005: 59%) of all ‘items of correspondence’

(individual item mail, bulk mail and B2B non-bulk mail) could be categorised as bulk

mail (> 400 items). Although the total volume decreased by 3.1% compared with 2005,

the segment increased by 3.2% between 2004 and 2005.32

An important trend is the

decreasing share of unprepared bulk mail. While 50% of the volume was prepared bulk

mail in 2004 (2005: 53%), this figure rose to 60% in 2006.

The volume of addressed direct mail (or addressed advertising) increased by 0.3% in

2006 compared with 2005, encompassing 4.9 billion items and contributing € 1.6 billion

(2005: € 1.7 billion). In 2006, 51% of the bulk mail was direct mail.

In 2006, the postal market amounted to circa 1% of total GDP (at current market

prices).33

Customer survey

The random check by ARCEP and TNS-Sofres (2006) showed that 43% of households

received fewer than five letters per week. Only 15% received 10 or more letters per week.

In terms of frequency, 57% of households received letters every day, while 26% received

letters one or two times a week.

Some 57% of households sent fewer than five letters a month, while only 19% sent more

than 10 letters a month. Frequency of sending was rather low: only 6% sent items every

day, 36% sent one or two items a week, and the majority sent letters fewer than two or

three times a month.34

32

ARCEP (2007b). 33

French GDP (at current market prices) in 2006 was circa €1,659 billion (Eurostat yearbook), while the total turnover of the

postal market was € 15,193 million. 34

Two or three times a month: 32%; once a month: 11%; once every two or three months: 6%; less often: 8%.

Main developments in the postal sector (2006-2008) 302

Ordinary letters were received by 94% of companies every day, while 68% sent ordinary

letters every day. In terms of volumes, ARCEP reported that 37% of companies received

fewer than 20 letters every day, while 315 received more than 50 letters; 24% of

companies sent more than 50 ordinary letters per week, while the majority (52%) sent

fewer than 20 letters per week.

1.4.2 B vs C

ARCEP has reported on the physical postal streams in the market for ‘items of

correspondence’ (individual item mail and bulk mail).35

The largest stream (64%) is the

B2C stream, with more than 10 billion items, while the volume of the B2B and B2C

streams are more or less the same size (17%). Correspondence between individual

consumers constituted only 3%.

Table 0.11 Postal streams in the market for addressed mail in turnover (million €)

Postal stream 2006

B2B n.a.

B2C n.a.

C2B n.a.

C2C n.a.

8,435

Source: ARCEP (2007b), p.15.

Note: n.a. is not available.

Table 0.12 Postal streams in the market for addressed mail in physical terms (million items)

Postal stream 2006

B2B 2,866 (17%)

B2C 10,530 (64%)

C2B 2,646 (16%)

C2C 496 (3%)

16,540

Source: ARCEP (2007b), p.15, based on ‘items of correspondence’

Note: La Poste indicated that: (i) the objective of the percentages given by ARCEP is to present a rough

overview of the market, and (ii) furthermore, these percentages relate to La Poste’s activity and not to the whole

market. The results are not in line with market structure, according to La Poste.36

1.4.3 Market opening

Most postal services are de jure liberalised – for example, export, domestic parcels,

domestic express items, press items for subscribers and unaddressed mail. Only items of

35

ARCEP (2007b). La Poste indicated that: (i) the objective of the percentages given by ARCEP is to present a rough

overview of the market, and (ii) furthermore, these data relate to La Poste’s activity and not to the whole market. The results

of the table are not in line with market structure. 36

ECORYS questionnaire – La Poste.

Country sheet: France 303

correspondence (including inward cross-border mail) up to 50 gram (until 2005, 100g) are

part of the reserved area. La Poste faces competition in most of the de jure liberalised

markets, especially those for outgoing cross-border mail, parcel mail and express mail.

In 2006, revenue from the reserved area was € 6.2 billion (13.8 billion items), while in

2005 (reserved area still up to 100g) it was € 7.0 billion (15.4 billion items). In terms of

total volume of the postal market, the reserved area comprised 41% in 2006 (2005: 47%),

and 35% of total turnover (2005: 39%). Focusing on ‘items of correspondence’

(individual item mail, bulk mail and B2B non-bulk mail), the reserved area comprised

83.5% of market volumes and 73% of market revenues. In 2005 (reserved area up to

100g), the volume was 92%.37

ARCEP estimated that in the liberalised domestic market (correspondence above 50g),

the market share of La Poste is de facto above 98%.38

La Poste reported that in 2006, 70% of the La Poste Group’s activities were open to

competition. In 2005, this figure was 64.5% according to La Poste.39

Gallet-Ryback, Moreno, Nadal and Toledano state that in practise market opening only

affects advertising mail and (in less extent) business transaction mail. They observe that

in the segment for addressed (advertising) mail only delivery in urban areas is a serious

option. They estimate the (theoretically) contestable market at 25% of the total market for

letter mail delivery (€ 500-700 million per year).40

1.4.4 Cross-border mail

Inbound cross-border mail up to 50 gram and 2.5 times the public tariff is still within the

reserved area. In 2006, the volume of the total cross-border postal market (inbound and

outbound items of correspondence, registered mail, parcel and press) was circa 906

million items, representing € 787 million. That was – according to ARCEP – circa 8% of

the world market.41

The export traffic comprised 516 million items in 2006 (2005: 558 million), generating €

536 million (2005: 605 million), a decrease of 7.5% in volume and 11.4% in turnover.

This decrease was mainly caused by lower letter volumes (-8.2% and -15.6% in

turnover), while the volume of outgoing press declined by 3.6%. The volume and

turnover of outgoing parcels increased by more than 14% compared with 2005.

ARCEP has reported that in 2006, ABC-postal streams (with France as country B)

comprised 16% of the volume of the outbound cross-border postal market and 11% of the

turnover. In 2005, the volume share was only 6%.42

37

ARCEP (2007b). 38

ECORYS questionnaire – ARCEP. 39

La Poste, press release 12 April 2007. 40

Gallet-Ryback, Moreno, Nadal and Toledano (2008). 41

ARCEP (2007b). 42

ARCEP (2007b).

Main developments in the postal sector (2006-2008) 304

The outgoing cross-border market is liberalised since the end of the 1990s43

and rather

competitive, with the main players all (related to) large international players: Deutsche

Post, Swiss Post, G3/Spring (joint venture between TNT, Royal Mail and Singapore

Post), Belgian Post and Royal Mail. IMX France is the only operator not related to a

foreign incumbent. Gallet-Ryback, Moreno, Nadal and Toledano estimate the market

share of La Poste at 80-85%.44

1.4.5 Impact of innovation

Facing the rationalisation of large clients’ purchasing behaviour and the development of

e-communications, La Poste is investing € 3.4 billion in a vast industrial programme

(CQC). Modernisation of the production tools will be completed by new services, a real

social project for all the mail postal workers (new jobs, training) and new organisations

for deliverers. La Poste’s mail activity and its subsidiaries have built innovative offers

such as electronic registered mail and mail solutions that mix sending electronic mail with

‘re-materialisation’ before delivery.45

Substitution

The precise impact on each mail sub-segment is not known (see Table 0.13). The

development of e-communications is significant for bills, transactional information and

advertising. For example, the ‘carte vitale’ (medical reimbursement electronic forms)

represented a loss of 945 million mail items in 2006. In 2007, 7.4 million people used e-

declarations for their revenue declaration to the tax authorities. This figure was 30%

higher than the preceding year.46

Table 0.13 Impact of electronic substitution

Postal product % change in total market volume (avg/year)

Bulk mail and consolidation n.a.

B2B non-bulk mail n.a.

Individual item mail n.a.

Items of correspondence n.a.

Cross-border mail n.a.

Unaddressed mail n.a.

Parcel mail n.a.

Express mail n.a.

Total n.a.

Source: n.a.

Note: n.a. is not available.

43

Gallet-Ryback, Moreno, Nadal and Toledano (2008). 44

Gallet-Ryback, Moreno, Nadal and Toledano (2008). 45

ECORYS questionnaire – La Poste. 46

ECORYS questionnaire – La Poste.

Country sheet: France 305

1.5 Market structure and competition

1.5.1 National postal operator/universal service provider

Since 1991, La Poste’s legal status has been that of an ‘exploitant autonome de droit

public’. This means that it operates as an autonomous business firm, while remaining

within the public sector and serving the general interest (Act no. 598-568). La Poste is a

100% state-owned enterprise in charge of services of general interest such as the

universal postal service, the transportation of press, the rural network presence and the

banking basic service.47

‘Le contrat de plan 2003-2007’ (the contract between La Poste and the French

government defining the main objectives of the public enterprise during that period)

stated that La Poste’s activity was divided into four business lines: mail, parcels and

express, financial services and network services.48

A new contract will soon be signed

between La Poste and the state specifying the ‘mission de service public’ of La Poste for

the period 2008-2012.49

Since 2003, the handling of mail has been in an ongoing process of reorganisation (‘cap

qualité courrier’), the aim of which is to rationalise the production process and reduce

average costs per mail item processed.50

In recent years, La Poste has expanded its activities in other (EU) countries. It has a large

number of business alliances and majority as well as minority positions in various

subsidiaries, among others in the USA and UK. La Poste has established a European

network for parcel and express delivery, particularly via GeoPost.

Most of the markets where La Poste is active are opened to competition. In 2006, roughly

70% of La Poste’s income was generated in competitive markets.51

After losses in 2001 and 2002, La Poste is back on track and reported profits for the

period 2003-2006. In 2006, its net profit was € 789 million – a 41.7% increase over the

2005 profit. For 2007, the net profit target was € 850 million.

La Poste’s postal network

In 2006, La Poste expanded its national network to more than 17,000 outlets. Its customer

relations project resulted in the renovation of 1,100 post offices and the opening of 1,499

public and private partner outlets. Another 1,000 post offices were to be renovated in

2007.

47

ECORYS questionnaire – La Poste. 48

ECORYS questionnaire – La Poste. 49

ECORYS questionnaire – Ministry. 50

ECORYS questionnaire – La Poste. 51

ECORYS questionnaire – La Poste.

Main developments in the postal sector (2006-2008) 306

Table 0.14 Postal network of the national postal operator

La Poste 2007

Number of post offices 12,522 (1 January 2007)

Number of postal agencies 4,523

Number of street post boxes 140,500 (2005)

Robin and Zarifian (Eurofound, 2007) reported that reduction of the number of post

offices is being discussed intensively: ‘Currently, La Poste has officially committed itself

to keeping the 17,000 contact points, mainly as a result of political pressure and at the

request of the state. However, in fact, the number of ‘real’ post offices with staff paid for

by La Poste is gradually decreasing. The aim is to drop to about 9,500 post offices and

annexes. Other contact points are gradually being created, either by “postal relays” in

cafés or supermarkets, or by postal agencies, which sell La Poste’s products and services,

but whose staff is paid for by local authorities’.52

La Poste stresses firmly that these assumptions made by Robin and Zarifian are not based

on any economic or legal analysis. La Poste points out that the number of post offices

(17, 000) is not the result of political pressure, but is defined by law and secondary

legislation. Further, La Poste stresses that concerning the number of post offices, it has no

such objective of reducing (to 9,500) the number of ‘real’ post offices.53

Breakdown per segment

Postal activities (mail, express, parcels) in 2006 generated nearly € 15.5 billion (Table

1.15), which was more than 75% of the total turnover of the La Poste Group. Postal bank

activities yielded another € 5 billion.

Table 0.15 Division of the national postal operator’s turnover per market segment

Postal product 2006

(in million €)

%

Bulk mail and consolidation n.a.

B2B non-bulk mail n.a.

Individual item mail 2,113 14%

Items of correspondence 9,540 62%

Cross-border activities 705 5%

Unaddressed mail 339 (Mediapost) 2%

Parcel mail 1,238 8%

Express mail 2,932 19%

Total postal activities 15,486

Source: La Poste (2007).

Note: The percentages are taken from the turnover of postal activities. The total turnover of the La Poste Group

was € 20,069. N.a. is not available. Items of correspondence includes direct mail.

52

Eurofound (2007). 53

ECORYS questionnaire – La Poste.

Country sheet: France 307

Within its postal activities, La Poste distinguishes between mail (bulk, individual, cross-

border, unaddressed), parcels and express. Parcels and express yielded respectively € 1.2

and € 2.9 billion (mainly GeoPost) in 2006, together making up 27% of total postal

revenues.

Regarding revenues and profit from letter mail and more specifically from the reserved

area, ARCEP reported that in volume terms, 83% of the market for items of

correspondence in 2006 was part of the reserved area (2005: 92%). In 2006, the turnover

of services within the reserved area was € 6.2 billion, while the turnover of La Poste’s

mail activities (excluding press and services) was € 10.2 billion, resulting in a 61% share

of services within the reserved area. In 2005, this share was 68% (€ 7.0 billion out of €

10.3 billion).54

Vertical and horizontal integration

The La Poste Group is active in four main areas: mail, parcel/express, La Poste retail

outlets and financial services (La Banque Postale). La Banque Postale (Postal Bank) is a

100% subsidiary of the La Poste Group and together with La Poste uses the network of

more than 17,000 outlets (post offices and post agencies).

In France, Europe and the non-European world, La Poste owns (or participates in) more

than 200 subsidiaries, mainly in the express delivery sector and (to a lesser extent) the

mail sector (USA, Great Britain) (see overview in Table 1.16).55

Table 0.16 Overview of alliances and partnerships of the national postal operator

La Poste Mail Express Logistics

Austria DPD Austria

Nahte Quehenberger

Belgium Chronopost International

Belgium

DPD

GeoPost Benelux

Jet Worldwide Belgique

DPD

Bulgaria GeoPost Bulgaria

Czech Republic DPD CZ DPD

Denmark Chronopost International Denmark

Jet Worldwide

Germany GeoPost

Chronopost International Germany

DPD (various subsidiaries)

Jet Worldwide

Tat Express

Armadillo

GeoPost

DPD (various

subsidiaries)

Denkhaus Versand

Logistik

Tat Express

Greece Interattica Grèce

Hungary DPD Hungary

54

ARCEP (2007b). 55

ECORYS questionnaire – La Poste; annual reports 2005-2007.

Main developments in the postal sector (2006-2008) 308

La Poste Mail Express Logistics

Ireland GeoPost

Interlink

GeoPost

Interlink

Italy Chronopost International

Tat Express

Latvia Baltic Logistic System

Lithuania Baltic Logistic System

Luxembourg DPD SARL DPD SARL

Netherlands Insa BV

(upstream)

Sofipost BV

Chronopost International Nederland

GeoPost

DPD Nederland

DPD Nederland

Poland Masterlink ACP Air Cargo Poland

Masterlink

Portugal Chronopost International Portugal

Jet Worldwide Portugal

Slovakia DPD DPD

Slovenia DPD Slovenia

Spain GeoPost

Seur (several subsidiaries)

Menexpres

ILSA

STU

Zium Mensajeros

Tat Express

Chronopost Expresse Espana

Sweden GeoPost Nordic and Eastern Europe

UK IBC UK

GeoPost (various subsidiaries)

UK Letter

DPD UK

Interlink Express

Parceline

Mail Plus

Interlink Express Parcels

GeoPost

Parceline

DPD

Source: ECORYS (2005b); La Poste (2007).

The La Poste Group is present in the all-value chain of mail in France. In the field of

document management (paper and electronic), it offers a complete set of services from

consulting to outsourcing of the whole document process. La Poste owns (or participates

in) several actors, such as: Orsid, Maileva, Aspheria (mailing houses), Certinomis and

Seres (electronic services).56

All the mail subsidiaries are grouped together in the holding company Sofipost.57

56

ECORYS questionnaire – La Poste. 57

ECORYS questionnaire – La Poste.

Country sheet: France 309

1.5.2 Competitor postal operators

The main competitor of La Poste (and its subsidiary Mediapost58

) is Adrexo, which was

originally mainly active in unaddressed mail delivery and direct mail. Adrexo competes

with La Poste in the B2C parcel market, the unaddressed mail market and until February

2008 in the addressed mail market (bulk direct mail).59

Adrexo is part of the SPIR

Communication Group and delivers its own products, but also collects volume from other

sources. In February 2008, Adrexo announced the shutdown of its addressed mail

network. As well as La Poste and Adrexo, several local companies are active in this

market segment. Regarding outgoing international mail, several foreign companies

(mainly incumbents) are active in the French market.

Parties like Stamper’s (Fox), Athus/Solgeco and Let France Services are all small local

niche players. Their business plan focuses on business mailers, professionals, SMEs and

banks. Gallet-Ryback, Moreno, Nadal and Toledano observe that the delivery of letter

mail above 50g in fact is a complement to their other local activities and can not be seen

as separate autonomous services. These operators claim that it is currently not

profitable.60

Table 1.17 provides an overview of the main competitors.

Table 0.17 Overview of main competitors in the postal market (2007)

Postal

operator

Market Volume and

turnover of

No. of

employees

Service level

(no. of

deliveries per

week)

Coverage

Adrexo Letters > 50g

(direct mail),

unaddressed

mail, parcels

Unaddressed/

addressed:

8.2 billion/39

million items

€ 245 million/€

59 million

1,450

employees and

23,500

deliverers

At least three

times per

week in urban

areas, one to

two times per

week in rural

areas

National coverage,

delivery to around

25.1 million

letterboxes

Mediapost (La

Poste)

Unaddressed

10 billion items 13,500

employees,

12,000

deliverers

n.a. 98%

Althus/Solgeco Letters > 50g

(direct mail)

n.a. n.a. n.a. Regional

Stamper’s (Fox) Letters > 50g

(direct mail)

n.a. n.a. n.a. Regional

IMX France Outbound cross- n.a. 19 employees n.a. Not applicable

58

Mediapost, the largest operator of unaddressed mail in France, is 76% owned by La Poste. Mediapost delivers 10 billion

items a year, which was 54% of the total volume of 18.6 billion items in 2005 and 2006. The Mediapost network covers

nearly the whole of France (98%), with 13,500 employees and 12,000 deliverers. 59

ECORYS questionnaire – Adrexo. 60

See for more information: Gallet-Ryback, Moreno, Nadal and Toledano (2008), p. 14-16.

Main developments in the postal sector (2006-2008) 310

Postal

operator

Market Volume and

turnover of

No. of

employees

Service level

(no. of

deliveries per

week)

Coverage

border mail

Deutsche Post

AG

Outbound cross-

border mail

n.a. n.a. n.a. Not applicable

Swiss Post

International

France

Outbound cross-

border mail

n.a. n.a. n.a. Not applicable

La Poste Belge Outbound cross-

border mail

n.a. n.a. n.a. Not applicable

G3 Worldwide

(Spring)

Outbound cross-

border mail

n.a. n.a. n.a. Not applicable

DHL Global Mail Outbound cross-

border mail

n.a. n.a. n.a. Not applicable

Royal Mail

Group

Outbound cross-

border mail

n.a. n.a. n.a. Not applicable

Let France

Routage

Letters > 50g,

outbound cross-

border mail

n.a. n.a. n.a. Regional, cross-

border: not

applicable

Distrihome

(Adrexo)

Parcels > 500,000 items

a year

160 deliverers n.a. National coverage

Mondial Relay Parcels n.a. n.a. n.a. National coverage

Alvéol Parcels n.a. n.a. n.a. National coverage

Kiala Parcels n.a. n.a. n.a. National coverage

Sogep Parcels n.a. n.a. n.a. National coverage

Coliposte Parcels n.a. n.a. n.a. National coverage

TNT Express Express n.a. n.a. n.a. National coverage

Exapaq Express n.a. n.a. n.a. National coverage

GLS France Express n.a. n.a. n.a. National coverage

Chronopost

International

Express n.a. n.a. n.a. National coverage

Note: n.a. is not available.

In June 2006, ARCEP granted a (non-reserved) domestic mail delivery authorisation to

Adrexo, the only operator in addition to La Poste with a nationwide licence. In September

2006, Adrexo started its new postal service Adrexo Mail, using its new delivery network

for addressed correspondence. However, Adrexo announced in February 2008 that it will

shut down its addressed mail network.

Adrexo Mail delivered 39.1 million items in 2007 and realised a turnover of € 59.1, an

increase of nearly 260% compared with 2006 (€ 16.5 million). However, its operational

results for 2006 and 2007 were negative: € -1.4 million and € -16.4 million respectively.

Three reasons were noted for the decision to shut down the addressed mail network: (i)

the date of full liberalisation of the French postal market set at 1 January 2011, while the

Country sheet: France 311

European Commission called for completion of this liberalisation in January 2009; (ii)

barriers for alternative postal operators in Europe, especially in the German and Dutch

markets; and (iii) the rules that could be applied to alternative operators (financing of the

universal service, social costs inherent in the future collective bargaining agreement).

Some other postal operators have been granted a licence for (non-reserved) domestic mail

delivery at a local scale: Stamper’s (around Pau), Solgeco 26 (around Romans, Valence),

Alternative Post (around Lyon), JS Activ’ (around Perpignan), Press’Tissimo (around

Paris), ProCourrier (around Montpellier), Courier Service 03 (around Vichy), Courrier

Plus (around Lille, Roubaix, Tourcoing, Villeneuve d’Ascq), Let France Routage (around

Alsace and Lorraine) and Althus (Aix les Bains, Anneçy et Chambery).

Unaddressed mail

Two competitors are active in the unaddressed mail segment: Mediapost (a subsidiary of

La Poste) and Adrexo. In addition, 100 local operators are active in this market.

Traditionally, Adrexo delivered mainly unaddressed mail, catalogues, magazines, etc. and

is the main competitor of Mediapost, the La Poste subsidiary, with a market share of

approximately 45%.61

Adrexo focuses on last-mile delivery and has almost complete

territorial coverage, with delivery to around 25.1 million letterboxes in France in 2007. It

has around 1,450 employees and 23,500 deliverers, and delivers an annual volume of 8.2

billion items. In 2007, Adrexo realised a turnover of € 244.5 million (2006: € 229.5

million), with an operating profit of € 25 million (2006: € 23.8 million). Delivery takes

place at least three times per week in urban areas and one to two times per week in rural

areas. Customers bring their mail to one of Adrexo’s distribution centres, of which there

are currently 244.

In February 2006, Adrexo merged with Kicible, previously one of the largest competitors.

Kicible was mainly active in delivering unaddressed items published by publisher S3G,

but also delivered unaddressed mail for other publishers. Kicible was mainly active in the

south-east of France.

Cross-border mail

Regarding the transportation of (outgoing) cross-border mail, ARCEP has granted eight

licences. Besides La Poste, these licences were assigned to IMX France, Deutsche Post,

Swiss Post, Spring, De Post/La Poste, DHL, Royal Mail and Let France Routage. This

market is competitive.

Parcels and express

Coliposte, the parcel delivery line of La Poste, is one of the main players in the parcel

segment and carries out the universal service obligations for parcels up to 20kg. In the

B2C parcel market, La Poste, several mail order companies with their own delivery

network (such as Mondial Relay) and Adrexo (Distrihome) are active.

In addition, some operators (such as Alvéol, Kiala and Sogep) provide pick-up points.

Sogep is a subsidiary of mail order company La Redoute, and Kiala uses the network of

61

ECORYS questionnaire – La Poste.

Main developments in the postal sector (2006-2008) 312

Mondial Relay, the subsidiary of another mail order company, Les 3 Suisses. Together,

Sogep and Mondial Relay have more than 7,500 pick-up points throughout France.

The express mail market (letters and parcels up to 30kg) is judged to be competitive. In