Embed Size (px)

Citation preview

1

France is the largest member of the European Union (EU) by area. France or République Française refers to Metropolitan France

(the mainland in Western Europe), French Guiana in South America, Guadeloupe (the archipelago in the Caribbean Sea),

Martinique Island (north of Trinidad and Tobago), and Reunion (in the Indian Ocean).

Metropolitan France is bound by the Bay of Biscay and the Atlantic Ocean to the west, the English Channel and Strait of Dover

to the north-west, Belgium and Luxembourg to the north-east, Germany and Switzerland to the west, Italy and the Mediterranean

Sea to the south-east and Spain to the south-west. France is known for its stunning scenic beauty, the varied culture of the French

regions, the fiercely cultural loyalty, haute couture, radical thought and the scrumptious cuisine of the land.

French citizens enjoy a high standard of living and a high public education level. France has been listed as the world's "best overall

health care" provider by the World Health Organization. It is the most-visited country in the world, receiving 79.5 million foreign

tourists annually.

France is an active economic and political player among the European countries. France is a member of the United Nations, a

permanent member of the UN Security Council, and a member of the G8, G20, NATO, OECD, World Trade Organization, and

as well as the European Union.

GENERAL INFORMATION

Population 65,951,611 (July 2013 est.)

Capital Paris

Head of state Jean-Marc Ayrault

Chief of state Francois Hollande

Official language(s) French

Ethnic groups Celtic and Latin with Teutonic, Slavic, North African,

Indochinese, Basque minorities

Religions Roman Catholic 83%-88%, Protestant 2%, Jewish 1%,

Muslim 5%-10%, unaffiliated 4%

Life expectancy 81.56 years

Literacy rate 99%

HDI (2012) 0.893 (20th in the world)

Source: CIA World Factbook, 2013

1. Economic Overview

The French economy is diversified across all sectors. The government has partially or fully privatized many large companies,

including Air France, France Telecom, Renault, and Thales. However, the government maintains a strong presence in some sectors,

particularly power, public transport, and defense industries. With at least 79 million foreign tourists per year, France is the most

visited country in the world and maintains the third largest income in the world from tourism.

France is a developed country, possessing the worlds 5th-largest and Europe's 2nd-largest economy by nominal GDP. It is also the

world's 9th-largest by GDP at purchasing power parity. France is the wealthiest nation in Europe and the 4th-wealthiest in the

world in aggregate household wealth.

France had 39 of the 500 biggest companies of the world in 2010, France ranks 4th in the Fortune Global 500, behind the United

States, Japan and China. Paris is the second most important location in the world for the headquarters of the world's 500 largest

companies: there are more Fortune Global 500 company headquarters in Paris than in Beijing, New York, London or Munich,

but fewer than in Tokyo.

France Country Fact Sheet

2

France's real GDP contracted 2.6% in 2009, but recovered somewhat in 2010 and 2011, before stagnating in 2012. The

unemployment rate increased from 7.4% in 2008 to 10.3% in 2012. Youth unemployment shot up to 24.2% during the third

quarter of 2012 in metropolitan France. Lower-than-expected growth and high unemployment costs have strained France's public

finances. The budget deficit rose sharply from 3.4% of GDP in 2008 to 7.5% of GDP in 2009 before improving to 4.5% of GDP

in 2012, while France's public debt rose from 68% of GDP to 89% over the same period.

ECONOMIC INFORMATION

GDP (PPP) (2012 est.) USD2.291trn

GDP growth (2012 est.) 0%

GDP per capita (2012 est.) USD36,100

Inflation (2012 est.) 2.2%

Interest rate (31 December 2012) 1.5%

Unemployment rate (2012 est.) 10.3%

Exports (2012 est.) USD567.1bn

Imports (2012 est.) USD641.3bn

Trade balance USD3.2bn

Doing Business in… ranking (2013) 34

Source: Ease of Doing Business, 2013; CIA World Factbook, 2013

The graph below is a snapshot of the French GDP and growth from 2008 to 2017(forecast), it is evident that France was adversely

affected by the subprime crisis of 2008/9 as the country’s growth had receded into negative figures. Despite the recovery period

after 2008/9, however, the French economy and its fellow EU members are facing the European debt crisis, hence the depressed

growth figures from 2012 to 2014(forecast) are depressed. France is currently trying to improve its public finances through fiscal

consolidation. Growth is forecast to recover in 2015 and continue into the future.

Source: Business Monitor International, 2013

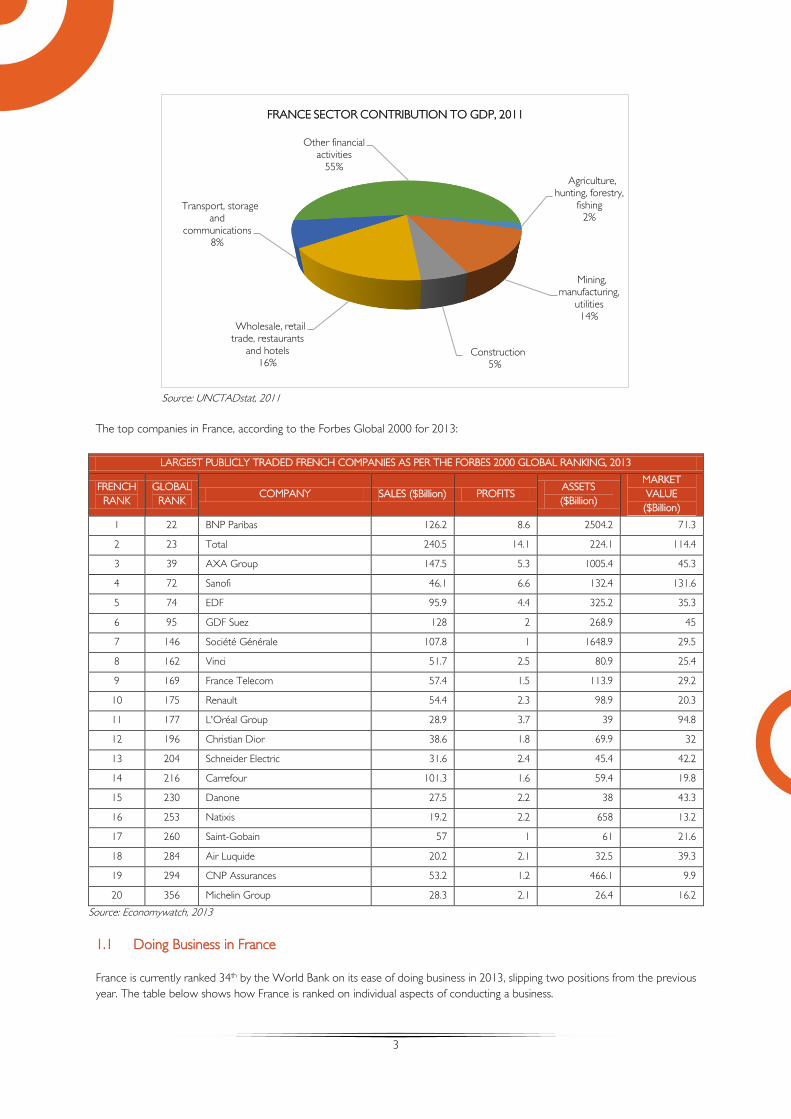

The contributions of the French economic sectors to GDP in 2011 are depicted in the graph below France has a highly developed

financial services sector and this makes up the most of its Gross Domestic Product (GDP) contribution. The second largest

contributor to GDP is wholesale, retail trade and hospitality followed by mining and manufacturing

2008 2009 2010 2011 2012 2013f 2014f 2015f 2016f 2017f

GDP(EURbn) 1799.2 1750.1 1776 1800.4 1801.9 1795.9 1804.3 1827.6 1857.2 1892.3

% Growth -0.08% -2.73% 1.48% 1.37% 0.08% -0.33% 0.47% 1.29% 1.62% 1.89%

-3%

-2%

-1%

0%

1%

2%

3%

1650

1700

1750

1800

1850

1900

1950

Val

ue (

EU

RD

bn)

FRANCE GDP & GROWTH, 2008-2017

3

Source: UNCTADstat, 2011

The top companies in France, according to the Forbes Global 2000 for 2013:

LARGEST PUBLICLY TRADED FRENCH COMPANIES AS PER THE FORBES 2000 GLOBAL RANKING, 2013

FRENCH

RANK

GLOBAL

RANK COMPANY SALES ($Billion) PROFITS

ASSETS

($Billion)

MARKET

VALUE

($Billion)

1 22 BNP Paribas 126.2 8.6 2504.2 71.3

2 23 Total 240.5 14.1 224.1 114.4

3 39 AXA Group 147.5 5.3 1005.4 45.3

4 72 Sanofi 46.1 6.6 132.4 131.6

5 74 EDF 95.9 4.4 325.2 35.3

6 95 GDF Suez 128 2 268.9 45

7 146 Société Générale 107.8 1 1648.9 29.5

8 162 Vinci 51.7 2.5 80.9 25.4

9 169 France Telecom 57.4 1.5 113.9 29.2

10 175 Renault 54.4 2.3 98.9 20.3

11 177 L'Oréal Group 28.9 3.7 39 94.8

12 196 Christian Dior 38.6 1.8 69.9 32

13 204 Schneider Electric 31.6 2.4 45.4 42.2

14 216 Carrefour 101.3 1.6 59.4 19.8

15 230 Danone 27.5 2.2 38 43.3

16 253 Natixis 19.2 2.2 658 13.2

17 260 Saint-Gobain 57 1 61 21.6

18 284 Air Luquide 20.2 2.1 32.5 39.3

19 294 CNP Assurances 53.2 1.2 466.1 9.9

20 356 Michelin Group 28.3 2.1 26.4 16.2

Source: Economywatch, 2013

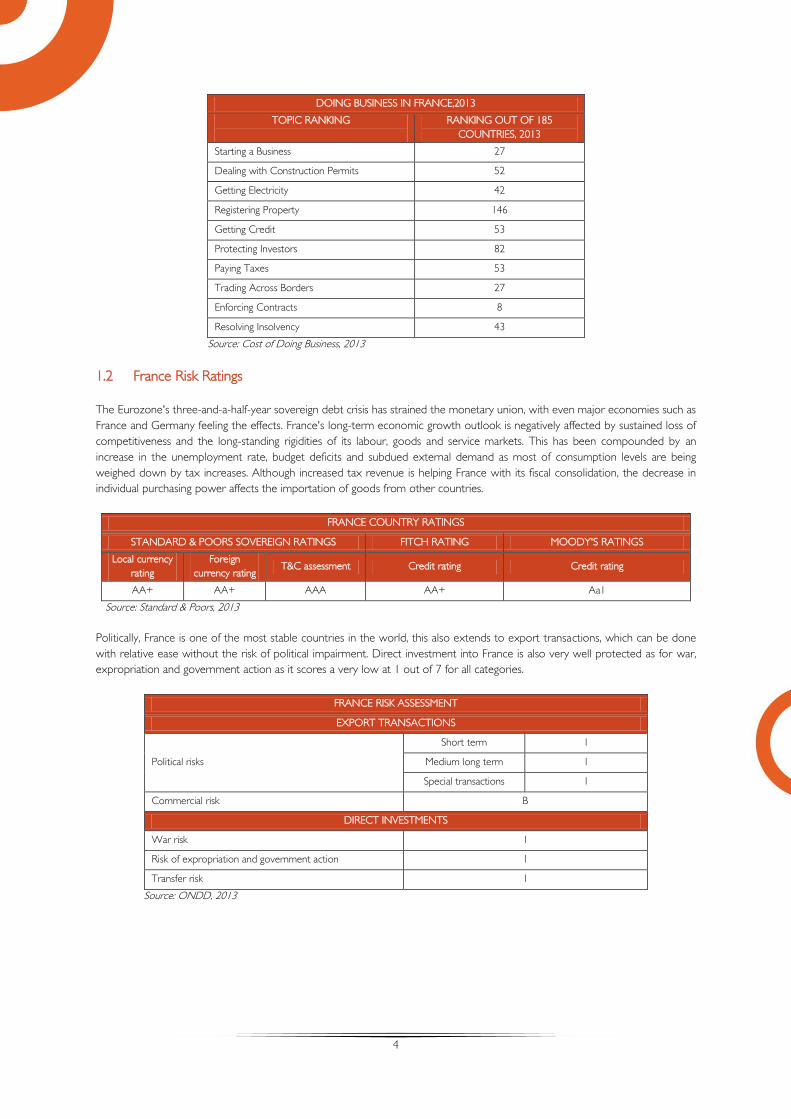

1.1 Doing Business in France

France is currently ranked 34th by the World Bank on its ease of doing business in 2013, slipping two positions from the previous

year. The table below shows how France is ranked on individual aspects of conducting a business.

Agriculture, hunting, forestry,

fishing2%

Mining, manufacturing,

utilities14%

Construction5%

Wholesale, retail trade, restaurants

and hotels16%

Transport, storage and

communications8%

Other financial activities

55%

FRANCE SECTOR CONTRIBUTION TO GDP, 2011

4

DOING BUSINESS IN FRANCE,2013

TOPIC RANKING

RANKING OUT OF 185

COUNTRIES, 2013

Starting a Business 27

Dealing with Construction Permits 52

Getting Electricity 42

Registering Property 146

Getting Credit 53

Protecting Investors 82

Paying Taxes 53

Trading Across Borders 27

Enforcing Contracts 8

Resolving Insolvency 43

Source: Cost of Doing Business, 2013

1.2 France Risk Ratings

The Eurozone's three-and-a-half-year sovereign debt crisis has strained the monetary union, with even major economies such as

France and Germany feeling the effects. France's long-term economic growth outlook is negatively affected by sustained loss of

competitiveness and the long-standing rigidities of its labour, goods and service markets. This has been compounded by an

increase in the unemployment rate, budget deficits and subdued external demand as most of consumption levels are being

weighed down by tax increases. Although increased tax revenue is helping France with its fiscal consolidation, the decrease in

individual purchasing power affects the importation of goods from other countries.

FRANCE COUNTRY RATINGS

STANDARD & POORS SOVEREIGN RATINGS FITCH RATING MOODY'S RATINGS

Local currency

rating

Foreign

currency rating T&C assessment Credit rating Credit rating

AA+ AA+ AAA AA+ Aa1

Source: Standard & Poors, 2013

Politically, France is one of the most stable countries in the world, this also extends to export transactions, which can be done

with relative ease without the risk of political impairment. Direct investment into France is also very well protected as for war,

expropriation and government action as it scores a very low at 1 out of 7 for all categories.

FRANCE RISK ASSESSMENT

EXPORT TRANSACTIONS

Political risks

Short term 1

Medium long term 1

Special transactions 1

Commercial risk B

DIRECT INVESTMENTS

War risk 1

Risk of expropriation and government action 1

Transfer risk 1

Source: ONDD, 2013

5

2. Trade

2.1 France Global Trade

France's global trade has continually increased over the last ten years, however imported goods have been increasing faster than

exports. Trade reached its highest point in 2008 however this level of imports and exports could not be achieved again until

2012 due to the decreased global demand as a result of the subprime crisis.

Source: TradeMap, 2013

As with most European nations, France conducts most of its trade with its EU partners, with 6 of its top ten export destinations

being EU member countries. Germany is the main importer of French goods and is also the fastest growing export market for

France. Africa is not a prominent trading partner with France, with less than 1% share of France’s global trade. South Africa

accounts for 0.4% of exports from France to the world and 0.2% of France’s imports from the world.

TOP 10 DESTINATION MARKETS FOR EXPORTS FROM FRANCE, 2012

RANK COUNTRY

VALUE

2012

(ZARbn)

%

GROWTH

2011-2012

%

SHARE

2012

1 Germany 748.7 8.29% 16.45%

2 Italy 335.9 -1.61% 7.38%

3 Belgium 333.3 10.75% 7.32%

4 Spain 307.2 1.05% 6.75%

5 United Kingdom 307.0 10.96% 6.74%

6 United States 279.0 19.51% 6.13%

7 Netherlands 192.8 7.73% 4.24%

8 China 158.6 17.82% 3.48%

9 Switzerland 144.4 10.13% 3.17%

10 Russian Federation 95.9 28.83% 2.11%

TOTAL EXPORTS 4552.1 8.86% 100.00%

Source:TradeMap, 2013

Following the export trend, France imports most of its goods from its EU counter parts, with Germany being the top source

market, followed by China (8%). The United States features on both top ten imports and export market lists and is the fastest

growing import market for the French at 21.71%.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Exports(ZARbn) 2,679.6 2,648.3 2,749.1 3,211.4 3,791.3 4,822.6 3,849.3 3,728.9 4,181.6 4,552.1

Imports(ZARbn 2,712.5 2,779.8 3,011.7 3,552.6 4,294.4 5,637.9 4,482.9 4,366.8 5,039.5 5,424.7

Trade Balance(ZARbn) -32.8 -131.4 -262.7 -341.2 -503.2 -815.2 -633.6 -637.8 -857.9 -872.6

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

Val

ue (

ZA

Rbn)

FRANCE GLOBAL TRADE, 2003 - 2012

6

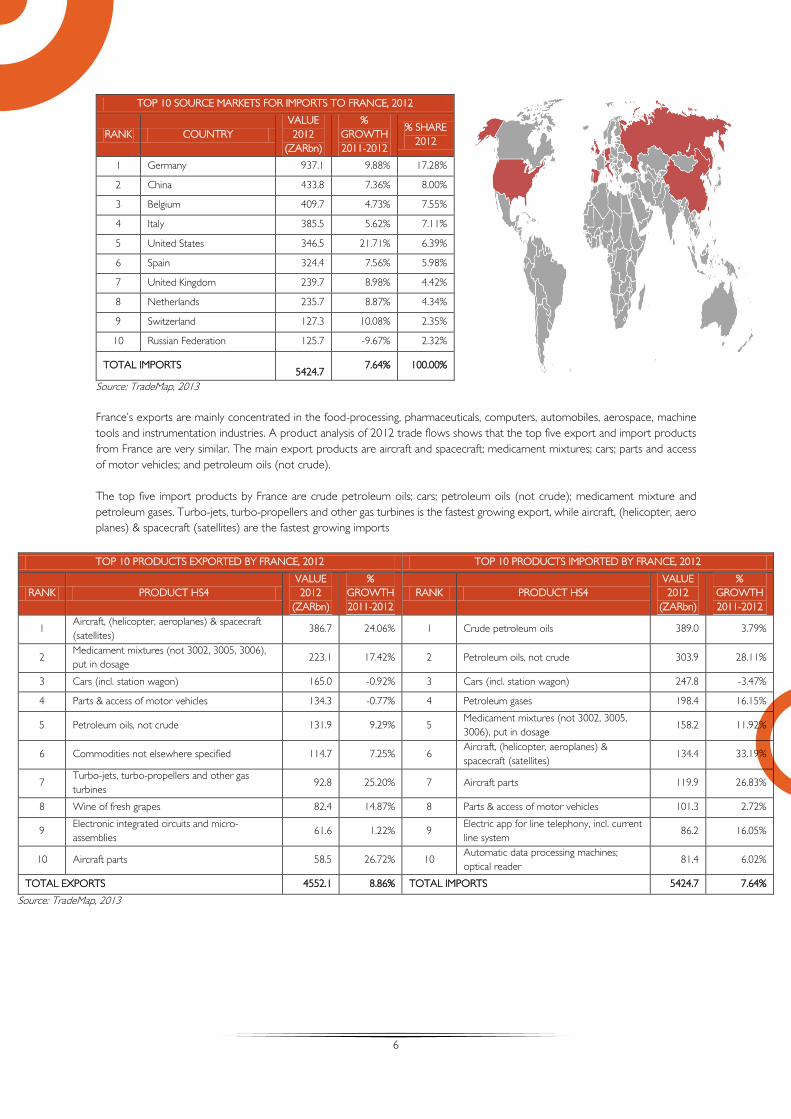

TOP 10 SOURCE MARKETS FOR IMPORTS TO FRANCE, 2012

RANK COUNTRY

VALUE

2012

(ZARbn)

%

GROWTH

2011-2012

% SHARE

2012

1 Germany 937.1 9.88% 17.28%

2 China 433.8 7.36% 8.00%

3 Belgium 409.7 4.73% 7.55%

4 Italy 385.5 5.62% 7.11%

5 United States 346.5 21.71% 6.39%

6 Spain 324.4 7.56% 5.98%

7 United Kingdom 239.7 8.98% 4.42%

8 Netherlands 235.7 8.87% 4.34%

9 Switzerland 127.3 10.08% 2.35%

10 Russian Federation 125.7 -9.67% 2.32%

TOTAL IMPORTS

5424.7 7.64% 100.00%

Source: TradeMap, 2013

France’s exports are mainly concentrated in the food-processing, pharmaceuticals, computers, automobiles, aerospace, machine

tools and instrumentation industries. A product analysis of 2012 trade flows shows that the top five export and import products

from France are very similar. The main export products are aircraft and spacecraft; medicament mixtures; cars; parts and access

of motor vehicles; and petroleum oils (not crude).

The top five import products by France are crude petroleum oils; cars; petroleum oils (not crude); medicament mixture and

petroleum gases. Turbo-jets, turbo-propellers and other gas turbines is the fastest growing export, while aircraft, (helicopter, aero

planes) & spacecraft (satellites) are the fastest growing imports

TOP 10 PRODUCTS EXPORTED BY FRANCE, 2012 TOP 10 PRODUCTS IMPORTED BY FRANCE, 2012

RANK PRODUCT HS4

VALUE

2012

(ZARbn)

%

GROWTH

2011-2012

RANK PRODUCT HS4

VALUE

2012

(ZARbn)

%

GROWTH

2011-2012

1 Aircraft, (helicopter, aeroplanes) & spacecraft

(satellites) 386.7 24.06% 1 Crude petroleum oils 389.0 3.79%

2 Medicament mixtures (not 3002, 3005, 3006),

put in dosage 223.1 17.42% 2 Petroleum oils, not crude 303.9 28.11%

3 Cars (incl. station wagon) 165.0 -0.92% 3 Cars (incl. station wagon) 247.8 -3.47%

4 Parts & access of motor vehicles 134.3 -0.77% 4 Petroleum gases 198.4 16.15%

5 Petroleum oils, not crude 131.9 9.29% 5 Medicament mixtures (not 3002, 3005,

3006), put in dosage 158.2 11.92%

6 Commodities not elsewhere specified 114.7 7.25% 6 Aircraft, (helicopter, aeroplanes) &

spacecraft (satellites) 134.4 33.19%

7 Turbo-jets, turbo-propellers and other gas

turbines 92.8 25.20% 7 Aircraft parts 119.9 26.83%

8 Wine of fresh grapes 82.4 14.87% 8 Parts & access of motor vehicles 101.3 2.72%

9 Electronic integrated circuits and micro-

assemblies 61.6 1.22% 9

Electric app for line telephony, incl. current

line system 86.2 16.05%

10 Aircraft parts 58.5 26.72% 10 Automatic data processing machines;

optical reader 81.4 6.02%

TOTAL EXPORTS 4552.1 8.86% TOTAL IMPORTS 5424.7 7.64%

Source: TradeMap, 2013

7

France’s exports represent 3.1% of global exports and is the world’s 5th largest

exporter. France's imports represent 3.65% of global imports and the world’s 7th

largest importer.

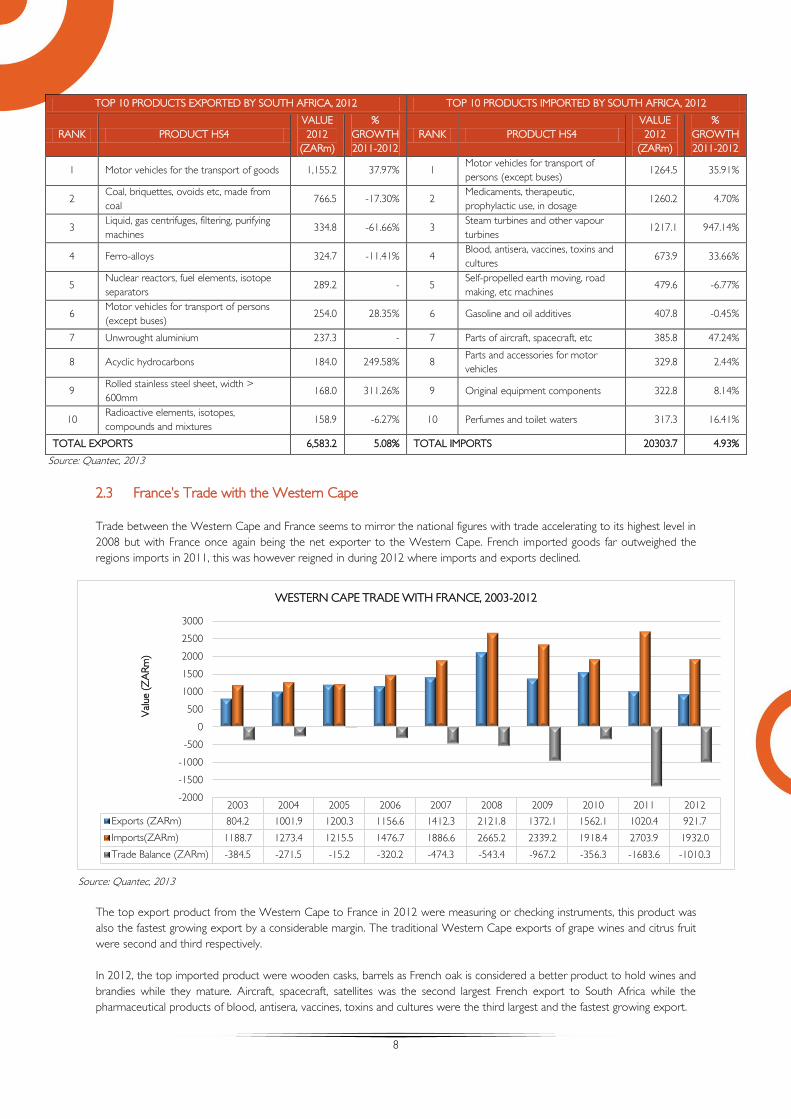

2.2 Trade with South Africa

South Africa’s trade with France has been increasing in the period shown below, with South Africa as net importer of French

made goods. Trade between the two countries accelerated from 2004 till 2008 with a boom period. However the aftermath of

the subprime crisis decreased trade levels. There has been a recovery in 2012, although South Africa’s trade deficit with France

has continued to increase.

Source: Quantec, 2013

The export baskets between South Africa and France consists mainly of metals, minerals and industrial and equipment. The

leading export form South Africa to France being motor vehicles for the transport of goods, coal and liquid, gas centrifuges, and

filtering, purifying machines. Although South Africa exports motor vehicles for transport of persons (except buses), France has

the comparative advantage in the export of this product, France is the largest exporter of pharmaceutical goods in the world and

this is exhibited by the this good being the second largest import from France to South Africa.

Top global exporter of

aircraft, spacecraft, and parts thereof

Top global exporter of beverages, spirits and

vinegar

Top global exporter for essential oils,

perfumes, cosmetics, toileteries

2nd largest global importer of explosives,

pyrotechnics, matches,

pyrophorics

Top global importer of

aircraft, spacecraft, and parts thereof

Top global importer of cork and articles of

cork

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Exports (ZARbn) 5,175.4 5,511.9 6,302.9 7,307.1 9,001.7 10,206.5 6,241.5 6,428.7 6,265.0 6,583.2

Imports(ZARbn) 15,456.7 18,596.6 15,407.7 16,938.6 18,841.6 20,872.7 16,921.9 17,111.1 19,349.5 20,303.7

Trade Balance(ZARbn) -10281.35 -13084.73 -9104.79 -9631.50 -9839.85 -10666.14 -10680.41 -10682.34 -13084.55 -13720.42

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

Val

ue (

ZA

Rm

)

SOUTH AFRICA'S TRADE WITH FRANCE, 2003-2012

8

TOP 10 PRODUCTS EXPORTED BY SOUTH AFRICA, 2012 TOP 10 PRODUCTS IMPORTED BY SOUTH AFRICA, 2012

RANK PRODUCT HS4

VALUE

2012

(ZARm)

%

GROWTH

2011-2012

RANK PRODUCT HS4

VALUE

2012

(ZARm)

%

GROWTH

2011-2012

1 Motor vehicles for the transport of goods 1,155.2 37.97% 1 Motor vehicles for transport of

persons (except buses) 1264.5 35.91%

2 Coal, briquettes, ovoids etc, made from

coal 766.5 -17.30% 2

Medicaments, therapeutic,

prophylactic use, in dosage 1260.2 4.70%

3 Liquid, gas centrifuges, filtering, purifying

machines 334.8 -61.66% 3

Steam turbines and other vapour

turbines 1217.1 947.14%

4 Ferro-alloys 324.7 -11.41% 4 Blood, antisera, vaccines, toxins and

cultures 673.9 33.66%

5 Nuclear reactors, fuel elements, isotope

separators 289.2 - 5

Self-propelled earth moving, road

making, etc machines 479.6 -6.77%

6 Motor vehicles for transport of persons

(except buses) 254.0 28.35% 6 Gasoline and oil additives 407.8 -0.45%

7 Unwrought aluminium 237.3 - 7 Parts of aircraft, spacecraft, etc 385.8 47.24%

8 Acyclic hydrocarbons 184.0 249.58% 8 Parts and accessories for motor

vehicles 329.8 2.44%

9 Rolled stainless steel sheet, width >

600mm 168.0 311.26% 9 Original equipment components 322.8 8.14%

10 Radioactive elements, isotopes,

compounds and mixtures 158.9 -6.27% 10 Perfumes and toilet waters 317.3 16.41%

TOTAL EXPORTS 6,583.2 5.08% TOTAL IMPORTS 20303.7 4.93%

Source: Quantec, 2013

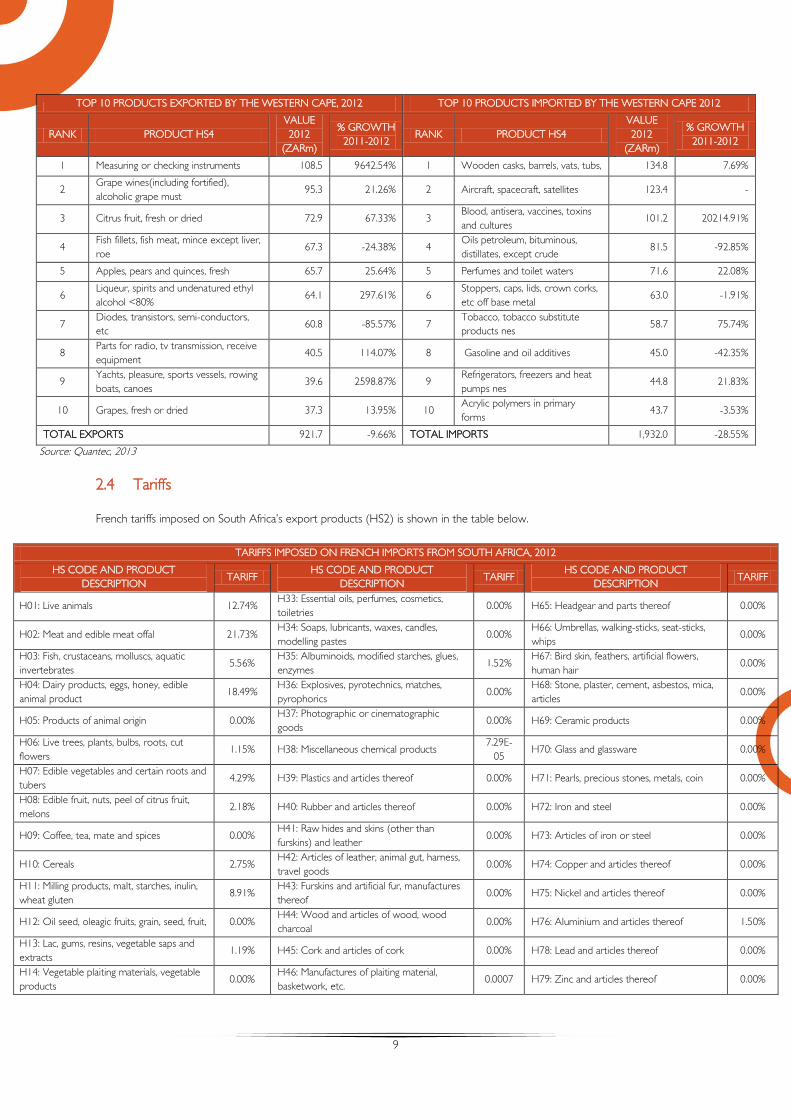

2.3 France’s Trade with the Western Cape

Trade between the Western Cape and France seems to mirror the national figures with trade accelerating to its highest level in

2008 but with France once again being the net exporter to the Western Cape. French imported goods far outweighed the

regions imports in 2011, this was however reigned in during 2012 where imports and exports declined.

Source: Quantec, 2013

The top export product from the Western Cape to France in 2012 were measuring or checking instruments, this product was

also the fastest growing export by a considerable margin. The traditional Western Cape exports of grape wines and citrus fruit

were second and third respectively.

In 2012, the top imported product were wooden casks, barrels as French oak is considered a better product to hold wines and

brandies while they mature. Aircraft, spacecraft, satellites was the second largest French export to South Africa while the

pharmaceutical products of blood, antisera, vaccines, toxins and cultures were the third largest and the fastest growing export.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Exports (ZARm) 804.2 1001.9 1200.3 1156.6 1412.3 2121.8 1372.1 1562.1 1020.4 921.7

Imports(ZARm) 1188.7 1273.4 1215.5 1476.7 1886.6 2665.2 2339.2 1918.4 2703.9 1932.0

Trade Balance (ZARm) -384.5 -271.5 -15.2 -320.2 -474.3 -543.4 -967.2 -356.3 -1683.6 -1010.3

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

Val

ue (

ZA

Rm

)

WESTERN CAPE TRADE WITH FRANCE, 2003-2012

9

TOP 10 PRODUCTS EXPORTED BY THE WESTERN CAPE, 2012 TOP 10 PRODUCTS IMPORTED BY THE WESTERN CAPE 2012

RANK PRODUCT HS4

VALUE

2012

(ZARm)

% GROWTH

2011-2012 RANK PRODUCT HS4

VALUE

2012

(ZARm)

% GROWTH

2011-2012

1 Measuring or checking instruments 108.5 9642.54% 1 Wooden casks, barrels, vats, tubs, 134.8 7.69%

2 Grape wines(including fortified),

alcoholic grape must 95.3 21.26% 2 Aircraft, spacecraft, satellites 123.4 -

3 Citrus fruit, fresh or dried 72.9 67.33% 3 Blood, antisera, vaccines, toxins

and cultures 101.2 20214.91%

4 Fish fillets, fish meat, mince except liver,

roe 67.3 -24.38% 4

Oils petroleum, bituminous,

distillates, except crude 81.5 -92.85%

5 Apples, pears and quinces, fresh 65.7 25.64% 5 Perfumes and toilet waters 71.6 22.08%

6 Liqueur, spirits and undenatured ethyl

alcohol <80% 64.1 297.61% 6

Stoppers, caps, lids, crown corks,

etc off base metal 63.0 -1.91%

7 Diodes, transistors, semi-conductors,

etc 60.8 -85.57% 7

Tobacco, tobacco substitute

products nes 58.7 75.74%

8 Parts for radio, tv transmission, receive

equipment 40.5 114.07% 8 Gasoline and oil additives 45.0 -42.35%

9 Yachts, pleasure, sports vessels, rowing

boats, canoes 39.6 2598.87% 9

Refrigerators, freezers and heat

pumps nes 44.8 21.83%

10 Grapes, fresh or dried 37.3 13.95% 10 Acrylic polymers in primary

forms 43.7 -3.53%

TOTAL EXPORTS 921.7 -9.66% TOTAL IMPORTS 1,932.0 -28.55%

Source: Quantec, 2013

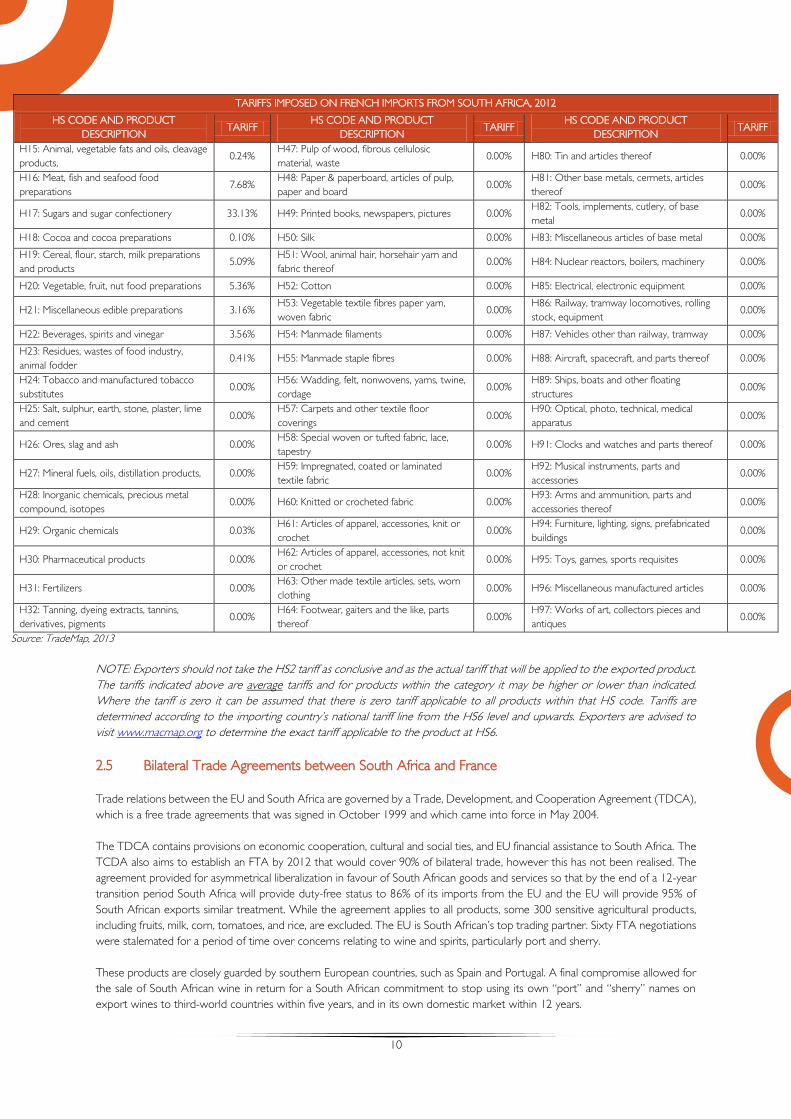

2.4 Tariffs

French tariffs imposed on South Africa’s export products (HS2) is shown in the table below.

TARIFFS IMPOSED ON FRENCH IMPORTS FROM SOUTH AFRICA, 2012

HS CODE AND PRODUCT

DESCRIPTION TARIFF

HS CODE AND PRODUCT

DESCRIPTION TARIFF

HS CODE AND PRODUCT

DESCRIPTION TARIFF

H01: Live animals 12.74% H33: Essential oils, perfumes, cosmetics,

toiletries 0.00% H65: Headgear and parts thereof 0.00%

H02: Meat and edible meat offal 21.73% H34: Soaps, lubricants, waxes, candles,

modelling pastes 0.00%

H66: Umbrellas, walking-sticks, seat-sticks,

whips 0.00%

H03: Fish, crustaceans, molluscs, aquatic

invertebrates 5.56%

H35: Albuminoids, modified starches, glues,

enzymes 1.52%

H67: Bird skin, feathers, artificial flowers,

human hair 0.00%

H04: Dairy products, eggs, honey, edible

animal product 18.49%

H36: Explosives, pyrotechnics, matches,

pyrophorics 0.00%

H68: Stone, plaster, cement, asbestos, mica,

articles 0.00%

H05: Products of animal origin 0.00% H37: Photographic or cinematographic

goods 0.00% H69: Ceramic products 0.00%

H06: Live trees, plants, bulbs, roots, cut

flowers 1.15% H38: Miscellaneous chemical products

7.29E-

05 H70: Glass and glassware 0.00%

H07: Edible vegetables and certain roots and

tubers 4.29% H39: Plastics and articles thereof 0.00% H71: Pearls, precious stones, metals, coin 0.00%

H08: Edible fruit, nuts, peel of citrus fruit,

melons 2.18% H40: Rubber and articles thereof 0.00% H72: Iron and steel 0.00%

H09: Coffee, tea, mate and spices 0.00% H41: Raw hides and skins (other than

furskins) and leather 0.00% H73: Articles of iron or steel 0.00%

H10: Cereals 2.75% H42: Articles of leather, animal gut, harness,

travel goods 0.00% H74: Copper and articles thereof 0.00%

H11: Milling products, malt, starches, inulin,

wheat gluten 8.91%

H43: Furskins and artificial fur, manufactures

thereof 0.00% H75: Nickel and articles thereof 0.00%

H12: Oil seed, oleagic fruits, grain, seed, fruit, 0.00% H44: Wood and articles of wood, wood

charcoal 0.00% H76: Aluminium and articles thereof 1.50%

H13: Lac, gums, resins, vegetable saps and

extracts 1.19% H45: Cork and articles of cork 0.00% H78: Lead and articles thereof 0.00%

H14: Vegetable plaiting materials, vegetable

products 0.00%

H46: Manufactures of plaiting material,

basketwork, etc. 0.0007 H79: Zinc and articles thereof 0.00%

10

TARIFFS IMPOSED ON FRENCH IMPORTS FROM SOUTH AFRICA, 2012

HS CODE AND PRODUCT

DESCRIPTION TARIFF

HS CODE AND PRODUCT

DESCRIPTION TARIFF

HS CODE AND PRODUCT

DESCRIPTION TARIFF

H15: Animal, vegetable fats and oils, cleavage

products, 0.24%

H47: Pulp of wood, fibrous cellulosic

material, waste 0.00% H80: Tin and articles thereof 0.00%

H16: Meat, fish and seafood food

preparations 7.68%

H48: Paper & paperboard, articles of pulp,

paper and board 0.00%

H81: Other base metals, cermets, articles

thereof 0.00%

H17: Sugars and sugar confectionery 33.13% H49: Printed books, newspapers, pictures 0.00% H82: Tools, implements, cutlery, of base

metal 0.00%

H18: Cocoa and cocoa preparations 0.10% H50: Silk 0.00% H83: Miscellaneous articles of base metal 0.00%

H19: Cereal, flour, starch, milk preparations

and products 5.09%

H51: Wool, animal hair, horsehair yarn and

fabric thereof 0.00% H84: Nuclear reactors, boilers, machinery 0.00%

H20: Vegetable, fruit, nut food preparations 5.36% H52: Cotton 0.00% H85: Electrical, electronic equipment 0.00%

H21: Miscellaneous edible preparations 3.16% H53: Vegetable textile fibres paper yarn,

woven fabric 0.00%

H86: Railway, tramway locomotives, rolling

stock, equipment 0.00%

H22: Beverages, spirits and vinegar 3.56% H54: Manmade filaments 0.00% H87: Vehicles other than railway, tramway 0.00%

H23: Residues, wastes of food industry,

animal fodder 0.41% H55: Manmade staple fibres 0.00% H88: Aircraft, spacecraft, and parts thereof 0.00%

H24: Tobacco and manufactured tobacco

substitutes 0.00%

H56: Wadding, felt, nonwovens, yarns, twine,

cordage 0.00%

H89: Ships, boats and other floating

structures 0.00%

H25: Salt, sulphur, earth, stone, plaster, lime

and cement 0.00%

H57: Carpets and other textile floor

coverings 0.00%

H90: Optical, photo, technical, medical

apparatus 0.00%

H26: Ores, slag and ash 0.00% H58: Special woven or tufted fabric, lace,

tapestry 0.00% H91: Clocks and watches and parts thereof 0.00%

H27: Mineral fuels, oils, distillation products, 0.00% H59: Impregnated, coated or laminated

textile fabric 0.00%

H92: Musical instruments, parts and

accessories 0.00%

H28: Inorganic chemicals, precious metal

compound, isotopes 0.00% H60: Knitted or crocheted fabric 0.00%

H93: Arms and ammunition, parts and

accessories thereof 0.00%

H29: Organic chemicals 0.03% H61: Articles of apparel, accessories, knit or

crochet 0.00%

H94: Furniture, lighting, signs, prefabricated

buildings 0.00%

H30: Pharmaceutical products 0.00% H62: Articles of apparel, accessories, not knit

or crochet 0.00% H95: Toys, games, sports requisites 0.00%

H31: Fertilizers 0.00% H63: Other made textile articles, sets, worn

clothing 0.00% H96: Miscellaneous manufactured articles 0.00%

H32: Tanning, dyeing extracts, tannins,

derivatives, pigments 0.00%

H64: Footwear, gaiters and the like, parts

thereof 0.00%

H97: Works of art, collectors pieces and

antiques 0.00%

Source: TradeMap, 2013

NOTE: Exporters should not take the HS2 tariff as conclusive and as the actual tariff that will be applied to the exported product.

The tariffs indicated above are average tariffs and for products within the category it may be higher or lower than indicated.

Where the tariff is zero it can be assumed that there is zero tariff applicable to all products within that HS code. Tariffs are

determined according to the importing country’s national tariff line from the HS6 level and upwards. Exporters are advised to

visit www.macmap.org to determine the exact tariff applicable to the product at HS6.

2.5 Bilateral Trade Agreements between South Africa and France

Trade relations between the EU and South Africa are governed by a Trade, Development, and Cooperation Agreement (TDCA),

which is a free trade agreements that was signed in October 1999 and which came into force in May 2004.

The TDCA contains provisions on economic cooperation, cultural and social ties, and EU financial assistance to South Africa. The

TCDA also aims to establish an FTA by 2012 that would cover 90% of bilateral trade, however this has not been realised. The

agreement provided for asymmetrical liberalization in favour of South African goods and services so that by the end of a 12-year

transition period South Africa will provide duty-free status to 86% of its imports from the EU and the EU will provide 95% of

South African exports similar treatment. While the agreement applies to all products, some 300 sensitive agricultural products,

including fruits, milk, corn, tomatoes, and rice, are excluded. The EU is South African’s top trading partner. Sixty FTA negotiations

were stalemated for a period of time over concerns relating to wine and spirits, particularly port and sherry.

These products are closely guarded by southern European countries, such as Spain and Portugal. A final compromise allowed for

the sale of South African wine in return for a South African commitment to stop using its own “port” and “sherry” names on

export wines to third-world countries within five years, and in its own domestic market within 12 years.

11

2.6 Port to Port

France is blessed with numerous ports on it northern and Mediterranean coasts through a long history of maritime trade. The

main ports are shown in the table below.

CAPE TOWN PORT TERMINAL TO FRENCH MAIN SEA PORTS

FRENCH PORTS DISTANCE TRANSIT TIME

Port of Bordeaux 10801km(5832.3M) 35 days 9 hrs.

Port of Brest 10656.7km(5754.2M) 35 days 3 hrs

Port of Fos Sur Mer 10767.7km(5814.1M) 35 days 7hrs

Marsaille 10781km(5821.2M) 35 days 8hrs

Sete Terminal 10722.3km(5878.6M) 35 days 5 hrs

Port of La Pallice 10716.4km(5786.4M) 35 days 5 hrs

Port of Rouen 11188.3(6041M) 35 days 23hrs

Port of Le Harve 11075.3(5890.2M) 35 days 19hrs

Source: Sea-Rates, 2013

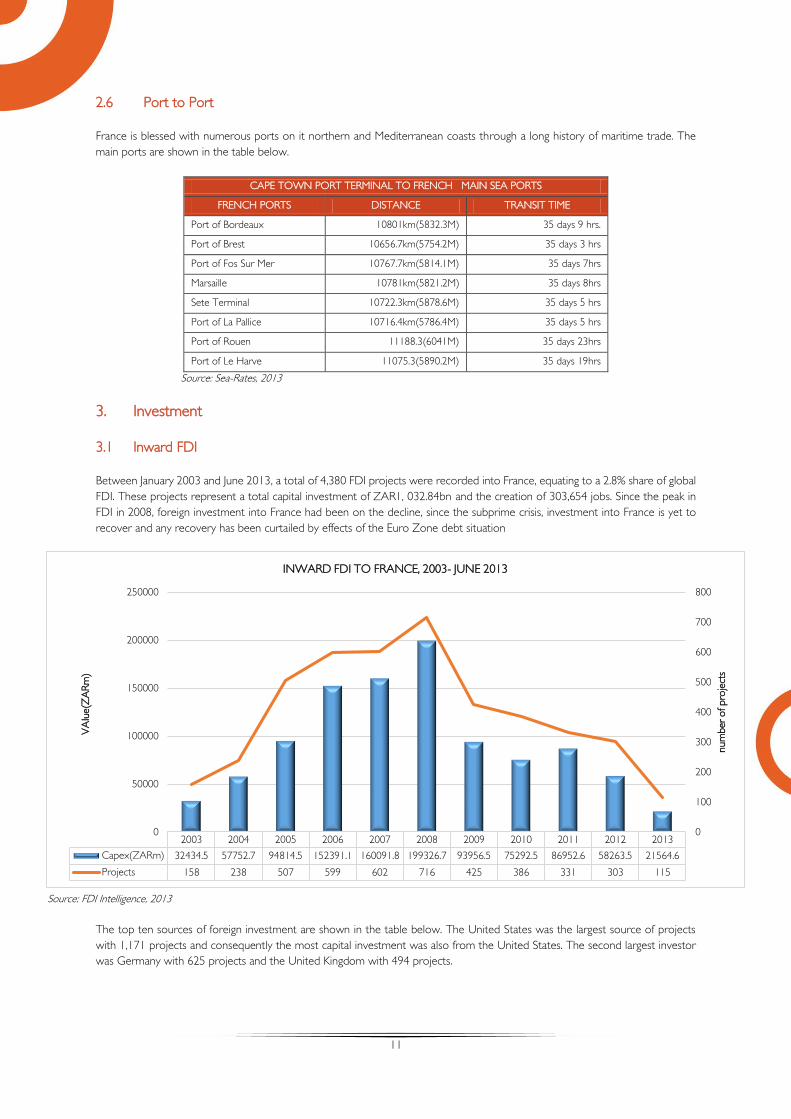

3. Investment

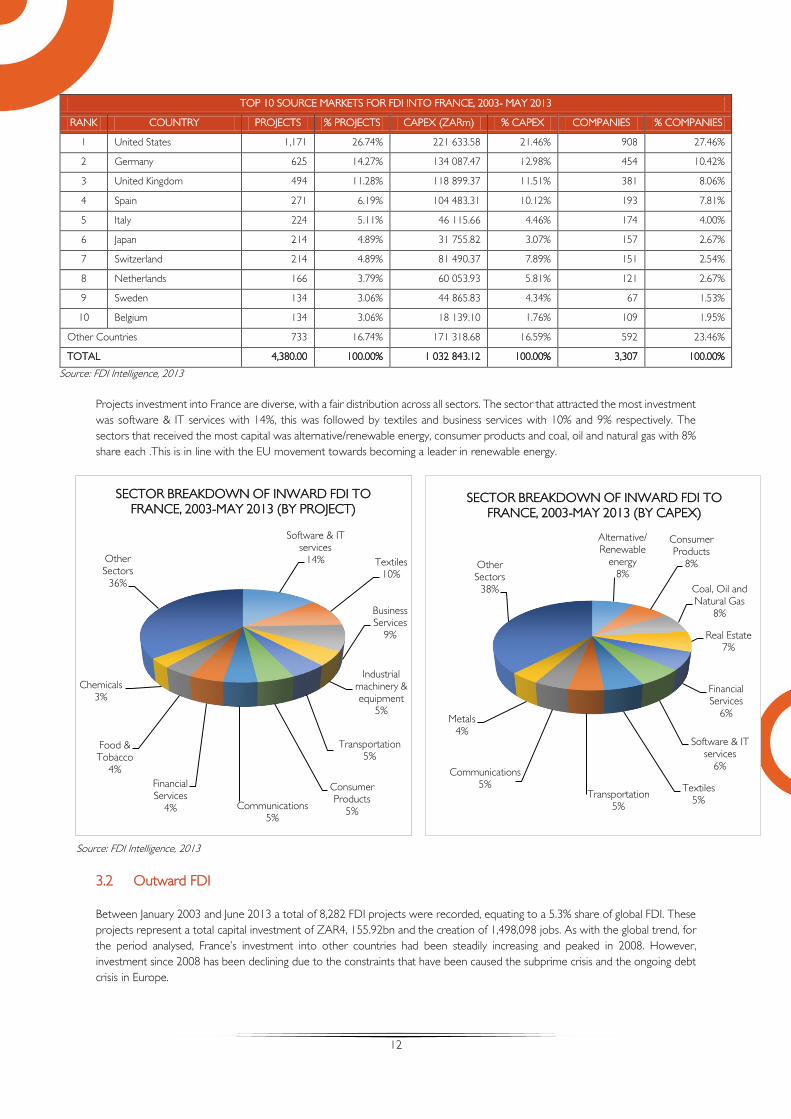

3.1 Inward FDI

Between January 2003 and June 2013, a total of 4,380 FDI projects were recorded into France, equating to a 2.8% share of global

FDI. These projects represent a total capital investment of ZAR1, 032.84bn and the creation of 303,654 jobs. Since the peak in

FDI in 2008, foreign investment into France had been on the decline, since the subprime crisis, investment into France is yet to

recover and any recovery has been curtailed by effects of the Euro Zone debt situation

Source: FDI Intelligence, 2013

The top ten sources of foreign investment are shown in the table below. The United States was the largest source of projects

with 1,171 projects and consequently the most capital investment was also from the United States. The second largest investor

was Germany with 625 projects and the United Kingdom with 494 projects.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Capex(ZARm) 32434.5 57752.7 94814.5 152391.1 160091.8 199326.7 93956.5 75292.5 86952.6 58263.5 21564.6

Projects 158 238 507 599 602 716 425 386 331 303 115

0

100

200

300

400

500

600

700

800

0

50000

100000

150000

200000

250000

num

ber

of pro

ject

s

VA

lue(Z

AR

m)

INWARD FDI TO FRANCE, 2003- JUNE 2013

12

TOP 10 SOURCE MARKETS FOR FDI INTO FRANCE, 2003- MAY 2013

RANK COUNTRY PROJECTS % PROJECTS CAPEX (ZARm) % CAPEX COMPANIES % COMPANIES

1 United States 1,171 26.74% 221 633.58 21.46% 908 27.46%

2 Germany 625 14.27% 134 087.47 12.98% 454 10.42%

3 United Kingdom 494 11.28% 118 899.37 11.51% 381 8.06%

4 Spain 271 6.19% 104 483.31 10.12% 193 7.81%

5 Italy 224 5.11% 46 115.66 4.46% 174 4.00%

6 Japan 214 4.89% 31 755.82 3.07% 157 2.67%

7 Switzerland 214 4.89% 81 490.37 7.89% 151 2.54%

8 Netherlands 166 3.79% 60 053.93 5.81% 121 2.67%

9 Sweden 134 3.06% 44 865.83 4.34% 67 1.53%

10 Belgium 134 3.06% 18 139.10 1.76% 109 1.95%

Other Countries 733 16.74% 171 318.68 16.59% 592 23.46%

TOTAL 4,380.00 100.00% 1 032 843.12 100.00% 3,307 100.00%

Source: FDI Intelligence, 2013

Projects investment into France are diverse, with a fair distribution across all sectors. The sector that attracted the most investment

was software & IT services with 14%, this was followed by textiles and business services with 10% and 9% respectively. The

sectors that received the most capital was alternative/renewable energy, consumer products and coal, oil and natural gas with 8%

share each .This is in line with the EU movement towards becoming a leader in renewable energy.

Source: FDI Intelligence, 2013

3.2 Outward FDI

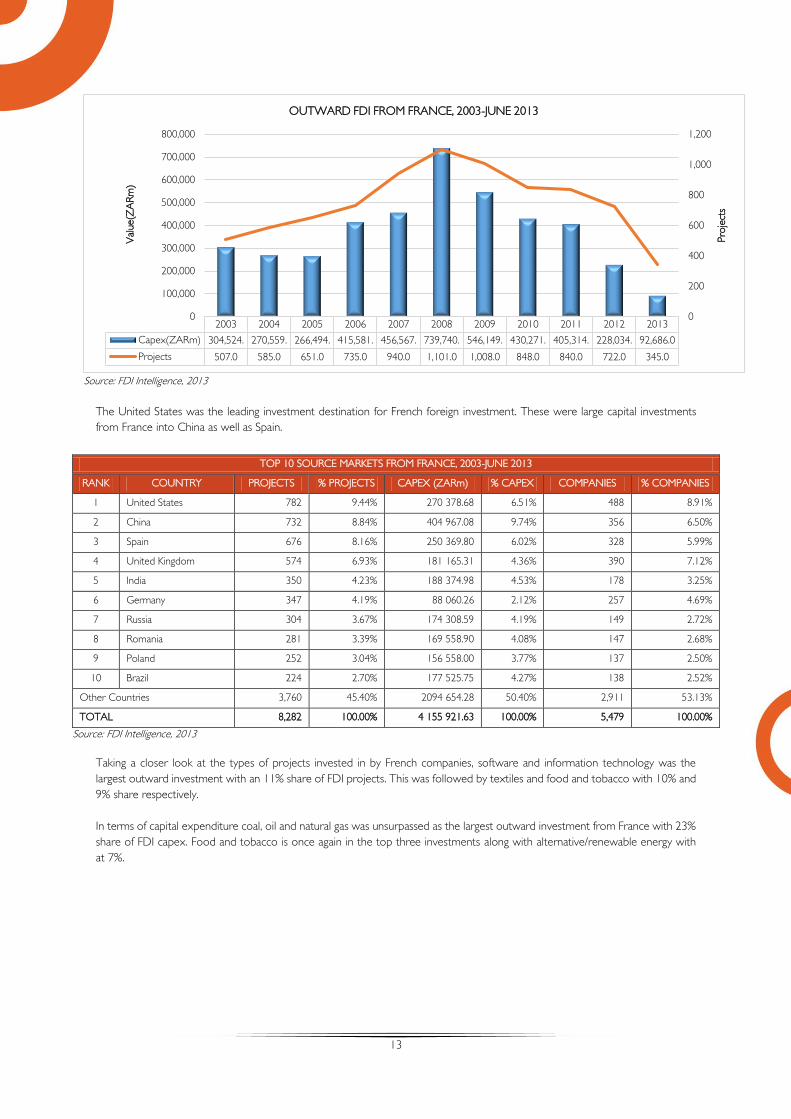

Between January 2003 and June 2013 a total of 8,282 FDI projects were recorded, equating to a 5.3% share of global FDI. These

projects represent a total capital investment of ZAR4, 155.92bn and the creation of 1,498,098 jobs. As with the global trend, for

the period analysed, France’s investment into other countries had been steadily increasing and peaked in 2008. However,

investment since 2008 has been declining due to the constraints that have been caused the subprime crisis and the ongoing debt

crisis in Europe.

Software & IT services

14% Textiles10%

Business Services

9%

Industrial machinery &

equipment5%

Transportation5%

Consumer Products

5%Communications

5%

Financial Services

4%

Food & Tobacco

4%

Chemicals3%

Other Sectors

36%

SECTOR BREAKDOWN OF INWARD FDI TO

FRANCE, 2003-MAY 2013 (BY PROJECT)

Alternative/ Renewable

energy8%

Consumer Products

8%

Coal, Oil and Natural Gas

8%

Real Estate7%

Financial Services

6%

Software & IT services

6%

Textiles5%

Transportation5%

Communications5%

Metals4%

Other Sectors

38%

SECTOR BREAKDOWN OF INWARD FDI TO

FRANCE, 2003-MAY 2013 (BY CAPEX)

13

Source: FDI Intelligence, 2013

The United States was the leading investment destination for French foreign investment. These were large capital investments

from France into China as well as Spain.

Source: FDI Intelligence, 2013

Taking a closer look at the types of projects invested in by French companies, software and information technology was the

largest outward investment with an 11% share of FDI projects. This was followed by textiles and food and tobacco with 10% and

9% share respectively.

In terms of capital expenditure coal, oil and natural gas was unsurpassed as the largest outward investment from France with 23%

share of FDI capex. Food and tobacco is once again in the top three investments along with alternative/renewable energy with

at 7%.

TOP 10 SOURCE MARKETS FROM FRANCE, 2003-JUNE 2013

RANK COUNTRY PROJECTS % PROJECTS CAPEX (ZARm) % CAPEX COMPANIES % COMPANIES

1 United States 782 9.44% 270 378.68 6.51% 488 8.91%

2 China 732 8.84% 404 967.08 9.74% 356 6.50%

3 Spain 676 8.16% 250 369.80 6.02% 328 5.99%

4 United Kingdom 574 6.93% 181 165.31 4.36% 390 7.12%

5 India 350 4.23% 188 374.98 4.53% 178 3.25%

6 Germany 347 4.19% 88 060.26 2.12% 257 4.69%

7 Russia 304 3.67% 174 308.59 4.19% 149 2.72%

8 Romania 281 3.39% 169 558.90 4.08% 147 2.68%

9 Poland 252 3.04% 156 558.00 3.77% 137 2.50%

10 Brazil 224 2.70% 177 525.75 4.27% 138 2.52%

Other Countries 3,760 45.40% 2094 654.28 50.40% 2,911 53.13%

TOTAL 8,282 100.00% 4 155 921.63 100.00% 5,479 100.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Capex(ZARm) 304,524. 270,559. 266,494. 415,581. 456,567. 739,740. 546,149. 430,271. 405,314. 228,034. 92,686.0

Projects 507.0 585.0 651.0 735.0 940.0 1,101.0 1,008.0 848.0 840.0 722.0 345.0

0

200

400

600

800

1,000

1,200

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Pro

ject

s

Val

ue(Z

AR

m)

OUTWARD FDI FROM FRANCE, 2003-JUNE 2013

14

Source: FDI Intelligence, 2013

3.3 FDI Flows between South Africa & France

Between January 2003 and June 2013 a total of 36 FDI projects were recorded amounting to ZAR15.58bn and creating 2,894

jobs. When looking closer at French investment into South Africa it is varied with no definitive trend. In 2010, there was a large

inflow of capital intensive FDI and in 2011 a large number of FDI projects were recorded.

Source: FDI Intelligence, 2013

In terms of the types of projects French companies invested in, it is mostly service based investments with a small percentage in

manufacturing. Business services attracted the largest share with 17%, followed by financial services (14%) and software and IT

services (11%). In analyzing the investment expenditure, although alternative and renewable energy attracted 3 projects, these

projects amounted to 35% of the investment value. Communications accounted for 19% and chemical projects accounted for

15%.

Software & IT services

11%

Textiles10%

Food & Tobacco

9%

Business Services

8%

Consumer Products

7%Financial Services

6%

Communications4%

Transportation4%

Chemicals4%

Hotels & Tourism

4%

Other Sectors

33%

SECTOR BREAKDOWN OF OUTWARD FDI

FROM FRANCE, 2003-JUNE 2013 (PROJECTS)

Coal, Oil and Natural Gas

23%

Food & Tobacco

7%

Alternative/ Renewable

energy7%

Automotive OEM

6%Chemicals6%

Hotels & Tourism

6%Communications5%

Consumer Products

4%

Building & Construction

4%

Transportation3%

Other Sectors

29%

SECTOR BREAKDOWN OF OUTWARD FDI

FROM FRANCE, 2003-JUNE2013

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Capex(ZARm 2,153.3 750.6 1,172.1 69.4 225.7 515.8 8,673.6 1,428.4 460.4 135.6

Projects 2 3 3 1 4 7 5 7 3 1

0

1

2

3

4

5

6

7

8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Pro

ject

s

Val

ue(Z

AR

m)

FDI FROM FRANCE TO SOUTH AFRICA, 2004-JUNE 2013

15

Source: FDI Intelligence, 2013

Listed below are the top 10 French companies investing in South Africa

TOP 10 COMPANIES INVESTING INTO SOUTH AFRICA, 2003-JUNE 2013

RANK INVESTING COMPANY PROJECTS CAPEX(ZARm)

1 BNP Paribas 3 233.1

2 Concentrix Solar 2 5,333.28

3 Diana Group 2 339.74

4 Teleperformance 2 76.05

5 Lafarge 2 524.9

6 Air Liquide 1 2,036.76

7 SCOR 1 100.85

8 Accor 1 996.06

9 CMA CGM 1 187.64

10 Elonex 1 15.71

Other companies 20 5740.29

Total 36 15584.38

Source: FDI Intelligence, 2013

3.4 FDI from South Africa to France

Between January 2003 and June 2013, a total of 6 FDI projects were recorded amounting to ZAR499.27m and creating 223 jobs.

In this period there was one investment from the Western Cape by Bridge People and Technology worth, ZAR66m

Business Services

17%

Financial Services

14%

Software & IT services

11%

Electronic Components

11%

Transportation8%

Chemicals8%

Alternative/ Renewable

energy8%

Biotechnology3%

Building & Construction

3%

Business Machines &

Equipments3%

Other Sectors

14%

SECTOR BREAKDOWN OF FDI FROM

FRANCE TO SOUTH AFRICA, 2003-JUNE

2013 (PROJECTS)

Alternative/ Renewable

energy35%

Communications19%

Chemicals15%

Hotels & Tourism

6%

Software & IT services

6%

Transportation5%

Business Services

4%

Building & Construction

3%

Financial Services

3%

Electronic Components

2%

Other Sectors

2%

SECTOR BREAKDOWN OF FDI FROM

FRANCE TO SOUTH AFRICA, 2003-JUNE

2013 (CAPEX)

16

FDI FROM SOUTH AFRICA TO FRANCE, 2003 - JUNE 2013

PROJECT

DATE INVESTING COMPANY

PARENT

COMPANY

SOURCE

STATE

INDUSTRY

SECTOR SUB-SECTOR

INDUSTRY

ACTIVITY

CAPEX

(ZARm) JOBS

Oct-12 HL Hall International HL Hall &

Sons Mpumalanga Food & Tobacco

Fruits & vegetables &

specialist foods

Logistics, Distribution

& Transportation 218.2 94

May-12 Barloworld Supply Chain

Software Barloworld Gauteng

Software & IT

services

Software publishers, except

video games

Sales, Marketing &

Support 67.0 23

Jan-10 HL Hall International HL Hall &

Sons Mpumalanga Food & Tobacco

Fruits & vegetables &

specialist foods

Sales, Marketing &

Support 28.9 27

Apr-07 Crane

Telecommunications Datatec Gauteng Communications

Wired telecommunication

carriers

Sales, Marketing &

Support 36.4 19

May-06 Dimension Data Europe

Dimension

Data Holdings

(DiData)

Gauteng Software & IT

services

Computer facilities

management services

Sales, Marketing &

Support 81.8 35

Dec-03 Bridge People and

Technology

Bridge People

and

Technology

Western Cape Software & IT

services

Custom computer

programming services

Sales, Marketing &

Support 67.0 25

TOTAL 499.3 223.0

Source: FDI Intelligence, 2013

3.5 FDI from France to Western Cape

Between January 2003 and June 2013 a total of 9 FDI projects were recorded from France into the Western Cape. These projects

represent a total capital investment of ZAR5.76bn and a total of 1,044 jobs were created. Sales, marketing and support received

attracted the largest amount of projects, while electivity projects received the largest capital expenditure.

FDI FROM FRANCE TO THE WESTERN CAPE, 2003 – JUNE 2013

PROJECT

DATE

INVESTING

COMPANY

DESTINATION

CITY INDUSTRY SECTOR SUB-SECTOR INDUSTRY ACTIVITY

CAPEX

(ZARm) JOBS

Sep-10 Concentrix Solar Not Specified Alternative/Renewable energy Solar electric power Electricity 2666.6 95

Sep-10 Concentrix Solar Not Specified Alternative/Renewable energy Solar electric power Electricity 2666.6 95

Mar-10 Tenesol Cape Town Electronic Components All other electrical

equipment & components Manufacturing 98.4 135

Nov-09 Teleperformance Cape Town Business Services Business support services Customer Contact Centre 38.0 297

Nov-09 Teleperformance Cape Town Business Services Business support services Customer Contact Centre 38.0 297

Sep-09 AD Software Cape Town Software & IT services Software publishers,

except video games Sales, Marketing & Support 63.6 14

Jun-09 Trusted Logic Cape Town Software & IT services Software publishers,

except video games Sales, Marketing & Support 63.6 14

Mar-09 Solaire Direct Cape Town Electronic Components All other electrical

equipment & components Manufacturing 58.7 70

Jan-09 Diana Group (Groupe

Diana) Cape Town Chemicals

Paints, coatings, additives &

adhesives Sales, Marketing & Support 66.1 27

Total 5759.8 1044.0

Source: FDI Intelligence, 2013

4. Tourism

4.1 Overview of the Tourism Offerings in France

According to the annual report on tourism from France's international competitiveness agency, the DGCIS. France was the

world’s top tourist destination again last year, maintaining this status that it has held since the 1990s, with 83 million foreigners

visiting in 2012. The new figure beat the previous record of 81.4 million foreign visitors in 2011.

17

4.2 French Trends and Travel Patterns

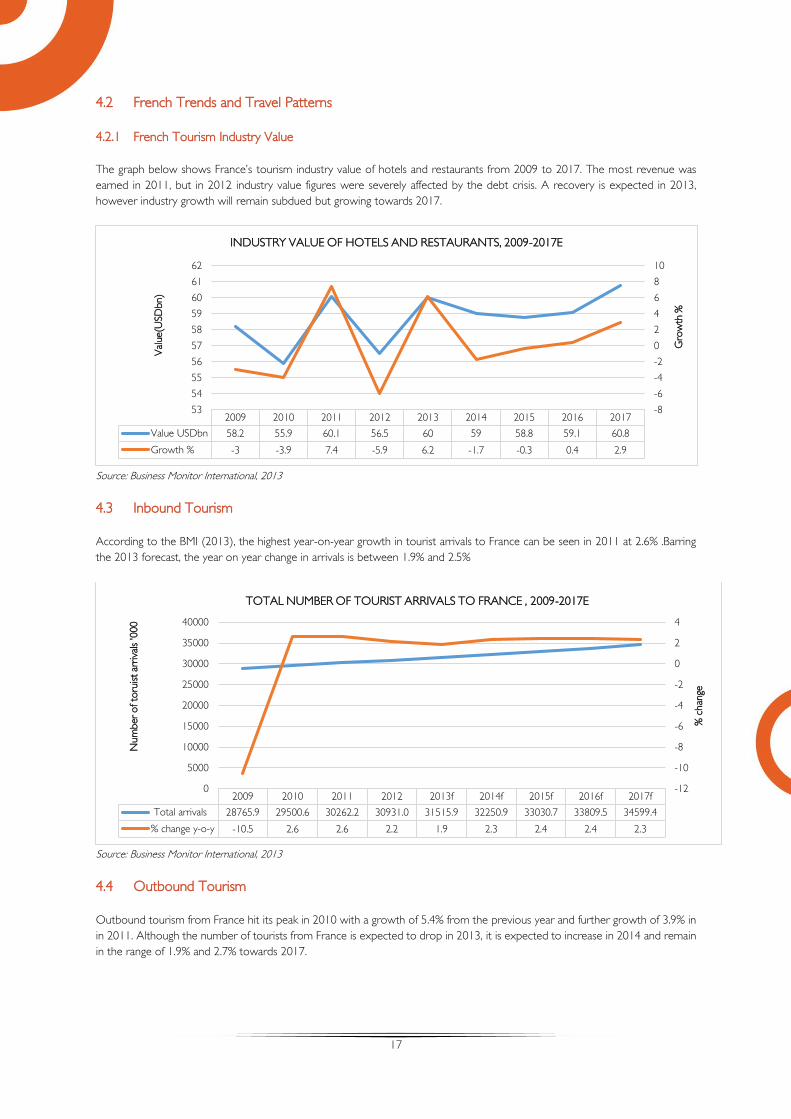

4.2.1 French Tourism Industry Value

The graph below shows France’s tourism industry value of hotels and restaurants from 2009 to 2017. The most revenue was

earned in 2011, but in 2012 industry value figures were severely affected by the debt crisis. A recovery is expected in 2013,

however industry growth will remain subdued but growing towards 2017.

Source: Business Monitor International, 2013

4.3 Inbound Tourism

According to the BMI (2013), the highest year-on-year growth in tourist arrivals to France can be seen in 2011 at 2.6% .Barring

the 2013 forecast, the year on year change in arrivals is between 1.9% and 2.5%

Source: Business Monitor International, 2013

4.4 Outbound Tourism

Outbound tourism from France hit its peak in 2010 with a growth of 5.4% from the previous year and further growth of 3.9% in

in 2011. Although the number of tourists from France is expected to drop in 2013, it is expected to increase in 2014 and remain

in the range of 1.9% and 2.7% towards 2017.

2009 2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Total arrivals 28765.9 29500.6 30262.2 30931.0 31515.9 32250.9 33030.7 33809.5 34599.4

% change y-o-y -10.5 2.6 2.6 2.2 1.9 2.3 2.4 2.4 2.3

-12

-10

-8

-6

-4

-2

0

2

4

0

5000

10000

15000

20000

25000

30000

35000

40000

% c

han

ge

Num

ber

of to

ruist ar

riva

ls '000

TOTAL NUMBER OF TOURIST ARRIVALS TO FRANCE , 2009-2017E

2009 2010 2011 2012 2013 2014 2015 2016 2017

Value USDbn 58.2 55.9 60.1 56.5 60 59 58.8 59.1 60.8

Growth % -3 -3.9 7.4 -5.9 6.2 -1.7 -0.3 0.4 2.9

-8

-6

-4

-2

0

2

4

6

8

10

53

54

55

56

57

58

59

60

61

62

Gro

wth

%

Val

ue(U

SD

bn)

INDUSTRY VALUE OF HOTELS AND RESTAURANTS, 2009-2017E

18

Source: Business Monitor International, 2013

4.5 French Tourist Arrivals into South Africa

The graph below illustrates the total number of tourist arrivals from France into South Africa for the period 2009 to 2012.

Tourists from France has been on the relative increase since 2009, with the stand out years being the FIFA Soccer World Cup

induced visitors and 2012.

Source: SATourism, 2013

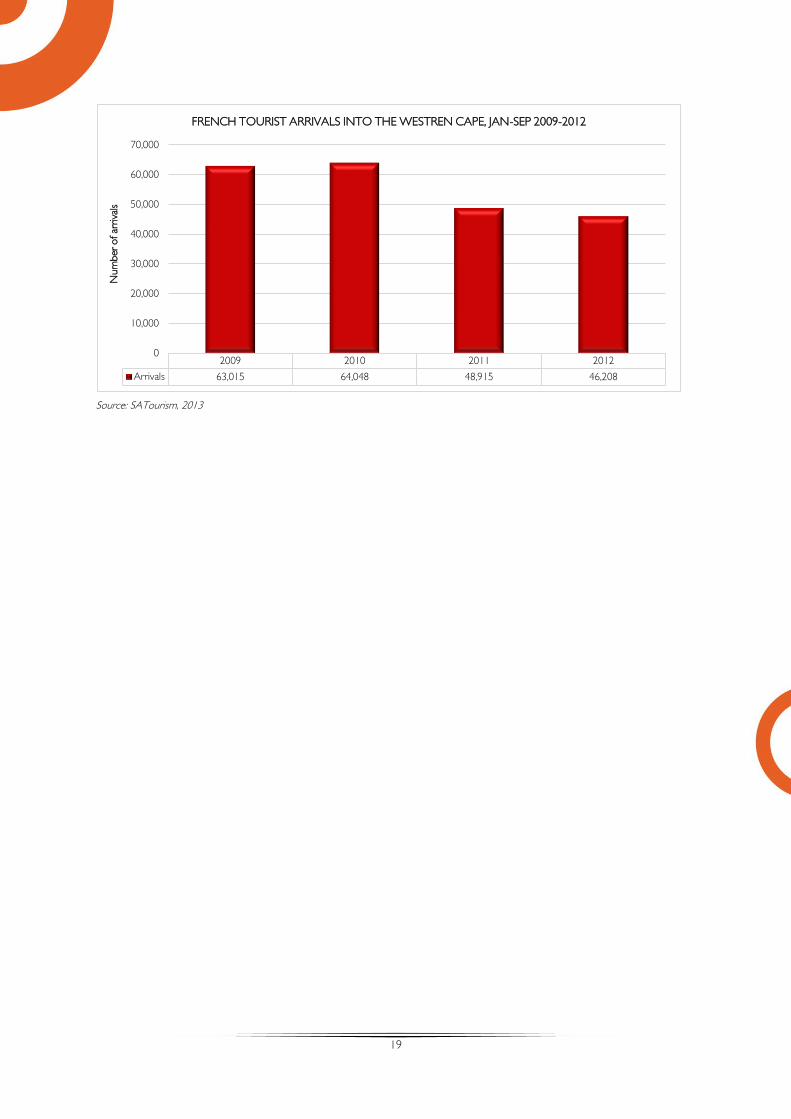

4.5.1 French Tourist Arrivals into the Western Cape

The figure below illustrates the total number of tourist arrivals from France to the Western Cape between January and September,

across the period 2009 to 2012. The largest share of tourists from France were received in 2010 with 64,048 arrivals, this has

however tapered off in subsequent years with 46,208 arrivals in 2012.

2009 2010 2011 2012 2013 2014 2015 2016 2017

Total departures 41196.4 43440.9 45124.3 45684.5 45910.8 47163.5 48144.5 49146.5 50075.1

% chaneg y-o-y 0.10 5.40 3.90 1.20 0.50 2.70 2.10 2.10 1.90

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0.0

10000.0

20000.0

30000.0

40000.0

50000.0

60000.0

% c

han

ge

Tota

l num

ber

of outb

ound toru

ist '0

00

TOTAL NUMBER OF OUTBOUND TOURISTS FROM FRANCE, 2009-2017E

2009 2010 2011 2012

Arrivals 103,985 115,401 105,420 122,244

90,000

95,000

100,000

105,000

110,000

115,000

120,000

125,000

Num

ber

of ar

riva

ls

FRENCH TOURIST ARRIVALS INTO SOUTH AFRICA, 2009-2012

19

Source: SATourism, 2013

2009 2010 2011 2012

Arrivals 63,015 64,048 48,915 46,208

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Num

ber

of ar

riva

lsFRENCH TOURIST ARRIVALS INTO THE WESTREN CAPE, JAN-SEP 2009-2012