Embed Size (px)

Citation preview

Copper-mining critical supplies market analysis

16/2016

Intellectual Property Registration N° 270140

Copper-mining critical supplies market analysis

1

Chilean Copper Commission

Executive Summary

Critical supplies are those whose supply situation could be crucial for a mining project or operation

in the mid and long term. The criticality is related to the supply shortage risk, the heavy dependence

on imports, the supply monopoly, and the relative burden of the supply on the cost structure.

This study originates from the application of the Cochilco-developed methodology for identifying

critical supplies in the mining industry. Six relevant supplies are analyzed in the second version of

this study: Quicklime, Grinding Balls, Extraction Trucks, Shovel-Loaders, Off Road Tires and

Flocculants. It must be noted that Cochilco also tracks other relevant mining supplies such as water,

electric power, sulfuric acid and manpower.

The objective of this study is to understand the critical supplies market and focus efforts on tracking

these supplies.

Quicklime

There are two companies manufacturing quicklime for Chile’s mining industry; Inacal comprises 92%

of the nationwide production capacity. The current quicklime stock offer is one million tons and it

could increase to 1.5 million tons depending on the consolidation of the Sopromin Project in

Tocopilla, the startup of the 165 ktpa plant in Atacama region, and the prospective operation of a

project planned for 2020, which is still in the initial stages and its capacity would be around 200,000

tons per year.

During 2015, quicklime imports were near 400 thousand tons, from which Sibelco and Cefas led the

introductions with a combined 72% of the imports.

A reduction is expected on quicklime consumption for the 2016-2025 period, compared to the

projections shown on this study’s first version (-2,060 thousand tons). Taking into account the

current quicklime import-levels and the domestic production capacity, the quicklime supply for

mining and other industries is guaranteed until year 2022. From then on, the supply will depend on

the development of mining projects and the strategy to meet the escalating demand (quicklime

domestic production increase and/or increase in quicklime imports).

The quicklime imports CIF1 value has been continuously increasing since 2009 (+63%).

Grinding Balls

There are three companies manufacturing grinding balls for the mining industry in Chile, Moly-Cop

comprises 80.4% of the installed capacity production. In addition, it is expected that an Aceros Chile

owned new plant will launch production of forged steel balls for mining in 2017 with a

1 Sales clause that includes the merchandise value in the country of origin, freight and insurance coverage up until destination point.

Copper-mining critical supplies market analysis

2

Chilean Copper Commission

manufacturing capability of 48 thousand tons, which would increase the local production capability

8% (586 to 634 ktpa)

Imports gained relevance from 2010 due to the establishment of a Joint Venture in Chinese by

Elecmetal for the production of grinding balls. In 2015, grinding balls imports reached 157 thousand

tons, 97% of them were the forged grinding ball type. Elecmetal and Codelco are the largest grinding

ball importers, with 66% and 20% of the total imported amounts, respectively.

The demand modeling shows that 466 thousand tons of grinding balls are consumed per year, this

consumption may reach 779 thousand tons by 2025, in the case that the entire mining project

portfolio is implemented. The current installed capacity of grinding balls comfortably meets their

demand in the mining industry. If the entire mining projects portfolio is implemented, the external

supply (imports) would be even more relevant.

The forged grinding balls imports CIF value (with the greatest demand in mining), has fallen from

2012, as well as the CIF value of the steel bars used to manufacture forged balls in Chile.

Extraction trucks

The extraction truck brands with the greatest presence in the Chilean copper mining operations are

Caterpillar, Komatsu and Liebherr.

With respect to the Large Scale Copper Mining, in the 2002-2015 period, 1,132 units of the most

used trucks were imported. The peak of imports was in 2012 (201 units), then it decreased and

reached 24 units in 2015.

Based on the modeling performed for the 2016-2025 period, the Large Scale Mining will require 554

new extraction trucks units and the Medium Scale Mining will require 101 units.

Since 2013 there is a dissimilar price behavior of the high tonnage trucks (some models prices rise

and others decrease). Regarding lower tonnage units, relatively stable prices are observed.

Mining Shovels

The most utilized mining shovels’ brands in Large Scale Copper Mining are P&H, Caterpillar and

Komatsu.

Analyzing a sample of mining operations (75% of the national production), it is observed that the

most utilized are rope shovels (73% of the shovel-loaders units). The average age of the rope shovel

units and hydraulic units samples are 15 and 9 years, respectively.

96 units of the studied shovel-loaders brands were imported in the 2002-2015 period, reaching a

peak in 2012 (18 shovel-loaders), then the imports decreased to just 4 units in 2015.

There is a sustained rise of the CIF value for the imported shovel-loaders until 2013, as after it

started falling.

Copper-mining critical supplies market analysis

3

Chilean Copper Commission

Off The Road Mining Tires (OTR)

The most important Off The Road tire, OTR, importers (of analyzed sizes) are Bridgestone and

Michellin, that together account for 85% of the imported value in 2015. Off road tires imported

directly by mining companies represent 14%, with Codelco leading and in previous years Minera

Escondida.

There was a constant rise in the OTR tires imports until 2013 (US $351 million CIF). Thenceforth, a

reduction in imports can be observed reaching US$ 209 CIF in 2015 as a result of the mining industry

slowdown.

The tire demand projection for tire-rings sizes 57” and 63”, which is associated only to extraction

trucks with at least a 150-ton capacity, shows that for the 2016-2025 period approximately 50,000

units will be required. This amount considers the tires needed for the current operating truck units

of the models studied in this investigation (Caterpillar 789, 793, 797 and Komatsu 730E, 830E, 930E)

and those projected acquisitions.

In relation to the price for the analyzed period (2005-2015), the larger the tire size, the bigger the

CIF value variation. It was observed a sustained price rise in large-size tires that stopped in 2013.

However, this situation is not as clear for smaller sized tires, where the CIF values present less

significant variations.

Flocculants

The main large copper mining companies use imported flocculants, different commercial brands are

available. The main manufacturers are SNF, Basf, Kemira and Orica.

The suitable flocculants are chosen based on lab test results, therefore, it is unlikely for an

immediate switch to a different brand.

The flocculants consumption for the 2016-2025 period is directly related with the projections of

sulfide ore processed in concentrator plants and could experience a 67% rise until 2025, growing

from the current 9 thousand tons to 15 thousand tons of flocculants per year.

While the analyzed brands differ in their CIF values, some of them obtained their maximum value in

2014, then their values began to drop; others showed a more steady behavior.

Final comment

Critical supplies are relevant to the cost structure in mining operations, and, as a result, their

commercialization produces significant income for the suppliers. In general, it was observed that

the studied markets tend to an oligopolistic structure, and in some cases there is clearly a

predominant supplier.

From the products origin standpoint, except the quicklime and grinding balls production, the rest of

the analyzed supplies (trucks, shovel-loaders, OTR tires and flocculants) are provided by

manufacturers that have their factories outside of Chile, that is to say, those supplies must be

imported. Moreover, in recent years the market share of locally produced goods has been

threatened by imports.

Copper-mining critical supplies market analysis

4

Chilean Copper Commission

Index

1. Introduction and objectives ...............................................................................................7 2. Quicklime ..........................................................................................................................8 2.1. Quicklime cycle ......................................................................................................................... 8 2.2. Quicklime uses .......................................................................................................................... 9 2.3. Quicklime supply .....................................................................................................................11 2.3.1. Domestic Production ..............................................................................................................11 2.3.2. Lime imports 13 2.4. Quicklime demand ..................................................................................................................14 2.4.1. Quicklime final use ..................................................................................................................14 2.4.2. Quicklime Consumption in the Copper Mining.......................................................................15 2.5. Quicklime offer and demand ..................................................................................................16 2.6. Quicklime price .......................................................................................................................17 3. Grinding balls .................................................................................................................. 19 3.1. Using grinding balls in copper mining .....................................................................................19 3.1.1. Grinding balls size and filling level ..........................................................................................20 3.2. Grinding balls supply ...............................................................................................................21 3.2.1. Domestic Production ..............................................................................................................21 3.2.2. Grinding balls imports and exports .........................................................................................22 3.3. Grinding balls consumption in the copper mining ..................................................................25 3.4. Grinding balls offer and demand ............................................................................................27 3.5. Grinding balls price .................................................................................................................28 4. Extraction Trucks ............................................................................................................. 30 4.1. Extraction trucks imports ........................................................................................................30 4.2. New trucks demand ................................................................................................................32 4.3. Extraction Trucks Price ............................................................................................................34 5. Mining Shovels ................................................................................................................ 36 5.1. Shovel-loaders supply .............................................................................................................36 5.2. Imported shovel-loaders .........................................................................................................37 5.3. Mining Shovels’ Price ..............................................................................................................38 6. Mining OTR Tires ............................................................................................................. 39 6.1. Tires imports ...........................................................................................................................39 6.2. Tires demand ..........................................................................................................................40 6.3. Tires Price ................................................................................................................................41 7. Flocculants used in the copper mining .............................................................................. 43 8. Bibliography .................................................................................................................... 47

Copper-mining critical supplies market analysis

5

Chilean Copper Commission

List of figures

Fig. 1: Quicklime cycle ......................................................................................................................... 9

Fig. 2: Imports distribution by lime type 2015 .................................................................................. 13

Fig. 3: Major importers of quicklime 2005-2015 ............................................................................... 14

Fig. 4: Imports and domestic production capacity of quicklime 2015 .............................................. 14

Fig. 5: Participation (%) by final use of quicklime in Chile ................................................................ 15

Fig. 6: CaO estimated consumption vs 2015 scenario (thousand tons) ............................................ 16

Fig. 7: Offer – Demand of quicklime (2016-2025). Imports not included. ........................................ 17

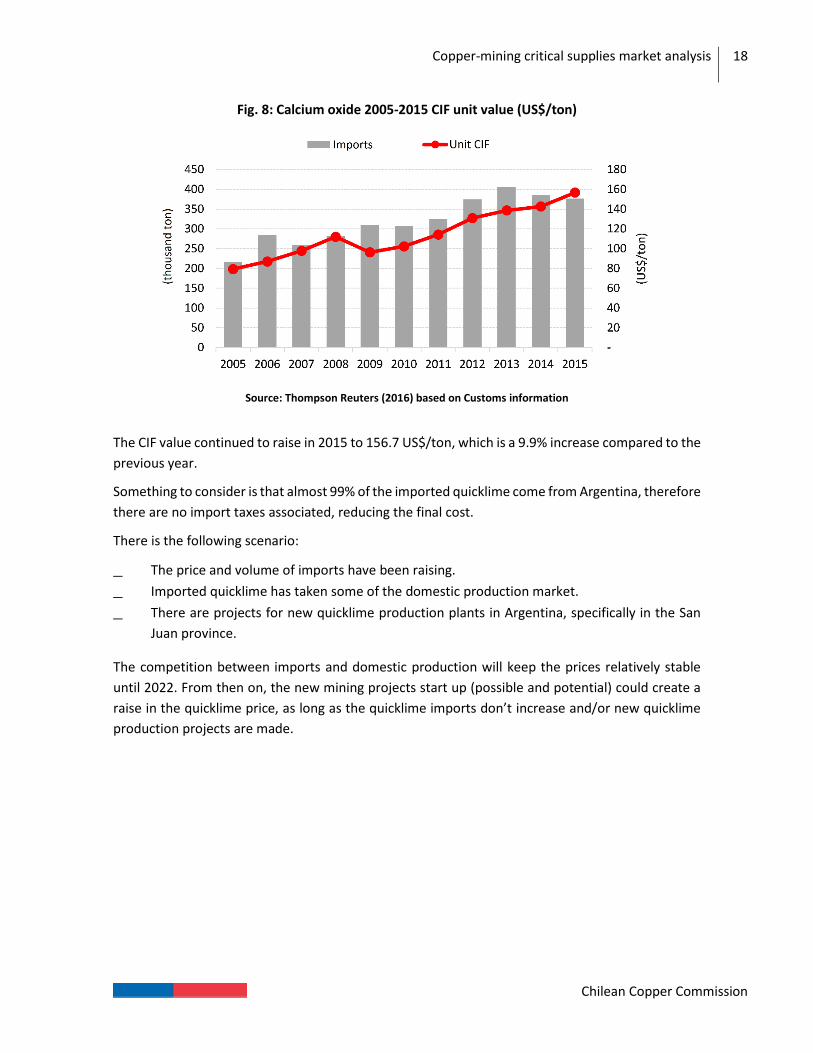

Fig. 8: Calcium oxide 2005-2015 CIF unit value (US$/ton) ................................................................ 18

Fig. 9: Types of crushing and grinding circuits .................................................................................. 19

Fig. 10: Grinding balls major importers (2005- Mar 2016) ............................................................... 23

Fig. 11: Country of origin of imported grinding balls (2005-2015) ................................................... 24

Fig. 12: Grinding balls imports and exports (thousand ton) ............................................................. 24

Fig. 13: 2016 vs 2015 processed ore Cu projections ......................................................................... 25

Fig. 14: Steel grinding balls consumption projections (2016-2025) .................................................. 26

Fig. 15: Steel grinding balls offer - demand (2016-2025). Imports not included. ............................. 27

Fig. 16: Valor CIF unitario bolas de molienda forjadas 2009-2016 (Mar) ......................................... 28

Fig. 17: Molten grinding balls CIF unit value 2009-2015 ................................................................... 29

Fig. 18: New mining trucks imports, by brand, 2002-2015 ............................................................... 31

Fig. 19: New mining trucks imports, by target market, 2002-2015 .................................................. 31

Fig. 20: New mining trucks imports for the large mining, 2002-2015 .............................................. 32

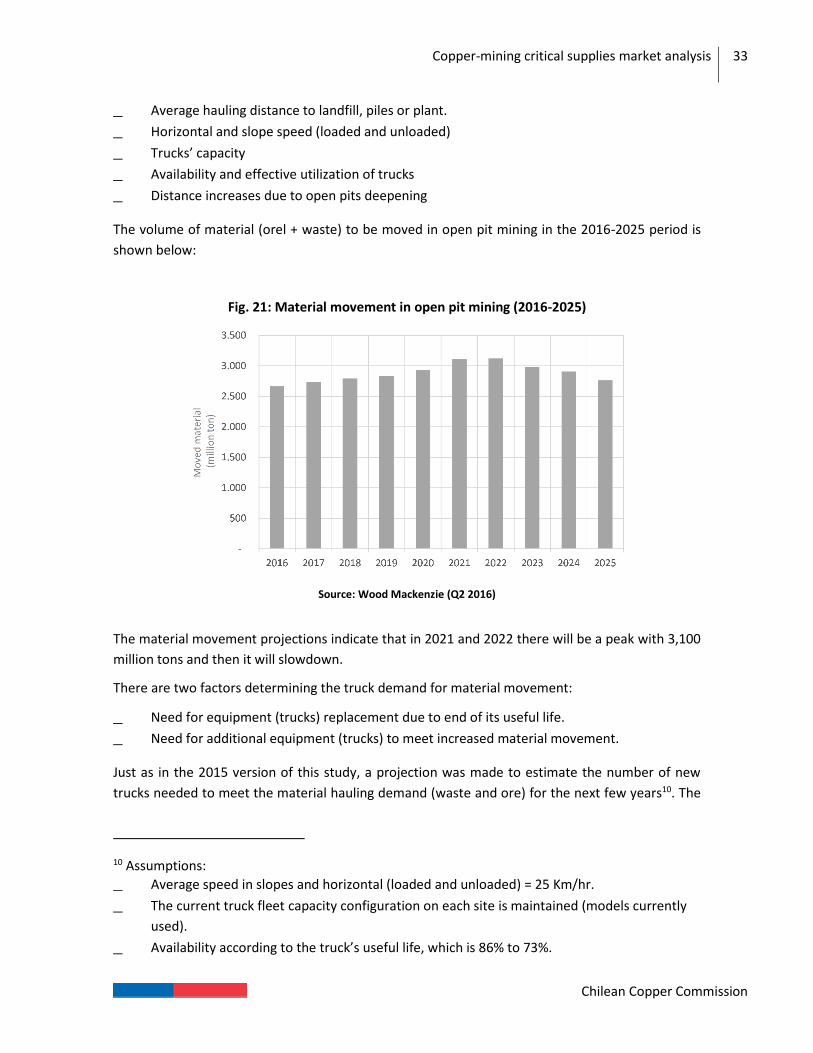

Fig. 21: Material movement in open pit mining (2016-2025) ........................................................... 33

Fig. 22: Need for new mining trucks (2016-2025) ............................................................................. 34

Fig. 23: CIF value (Million US$/unit) CAEX trucks .............................................................................. 35

Fig. 24: Imported mining shovels units (2005-2015) ........................................................................ 37

Fig. 25: CIF unit value mining shovels 2005-2015 ............................................................................. 38

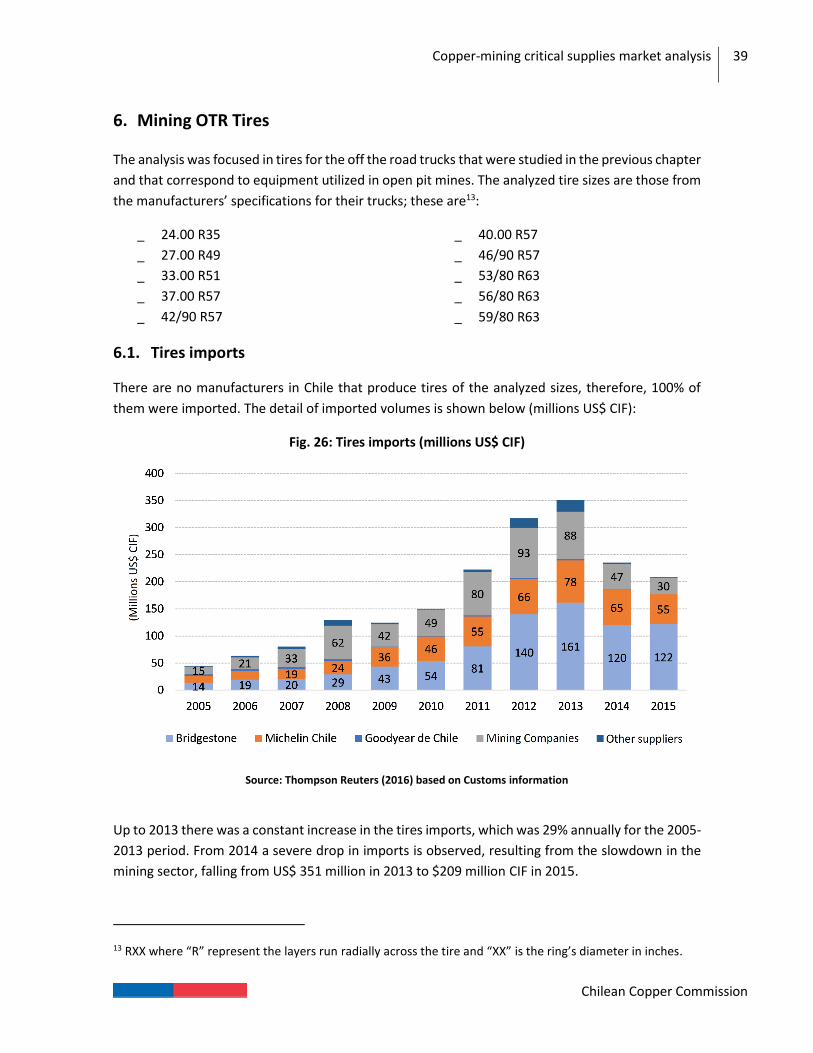

Fig. 26: Tires imports (millions US$ CIF) ............................................................................................ 39

Fig. 27: Imported tire units by type ................................................................................................... 40

Fig. 28: Large size tires demand (2016-2025) ................................................................................... 41

Fig. 29: CIF unit value tires (US$/unit) .............................................................................................. 42

Fig. 30: Mining flocculants major brands imports (MMUS$ CIF) ...................................................... 44

Fig. 31: Flocculants projected consumption (tons) ........................................................................... 45

Fig. 32: Average CIF unit value of conventional flocculants (US$ CIF/kg) ......................................... 45

Tables index

Table 1: Lime uses (Quicklime, slaked lime and hydraulic) ................................................................. 9

Table 2: Major quicklime producers for mining in Chile ................................................................... 12

Table 3: Filling level ........................................................................................................................... 20

Table 4: Grinding means uses ........................................................................................................... 20

Table 5: Grinding balls production companies .................................................................................. 22

Copper-mining critical supplies market analysis

6

Chilean Copper Commission

Table 6: Categorization of off road extraction trucks, by target market .......................................... 30

Table 7: Mining Shovels large copper mining ................................................................................... 36

Table 8: Number of loaders by make, model and type ..................................................................... 37

Table 9: Major brands of flocculants utilized in mining .................................................................... 43

Copper-mining critical supplies market analysis

7

Chilean Copper Commission

1. Introduction and objectives

The objectives of this study are:

1. Support the growth of mining activities and investments in our country through the

identification and understanding of the market of the supplies considered as critical.

2. Contribute to the monitoring of public policies aimed at sustainable development of mining

in Chile and consolidate its contribution to the country, by the development of studies that

track or perform a follow up on these critical supplies.

On the first version of the study, a methodology was formulated and applied with the purpose of

identifying in a reasonable manner most of the supplies that are considered critical in the Large

Copper Mining, in both, the operations (OPEX) and capital projects (CAPEX). As a result emerged

the need to follow up on those supplies that are critical for the mining, with the goal of identifying,

understanding and monitoring the main determinants of their markets. On this matter, from a time

ago, Cochilco permanently follows up the high impact critical supplies for the mining such as electric

power, water, sulfuric acid and manpower.

The market of 6 mining supplies were analyzed in the third version of the study:

Quicklime,

Grinding balls,

Flocculants,

Tires for off the road extraction trucks(OTR),

Extraction trucks (CAEX),

Mininig Shovels.

With the purpose of having an expert opinion about the contents of this report, some the

suppliers mentioned on this study were contacted. It is important to note that some of the local

offer values come from estimations based on the information provided by the same companies

and other interviewed sources; meanwhile, the imported offer was obtained from the customs

records. The demand projections are based in Cochilco own estimations.

Copper-mining critical supplies market analysis

8

Chilean Copper Commission

2. Quicklime

Quicklime2 is obtained by burning limestone (ore) to the calcium carbonate decomposition

temperature. At this stage it is called quicklime (calcium oxide) and then it is treated with water to

be called later slaked lime (calcium hydroxide). As explained later, the principal use of quicklime in

the mining industry is as a PH regulator in the sulfurized copper and copper auriferous ore flotation

processes.

2.1. Quicklime cycle

It is necessary to know the lime cycle in order to understand the concept of quicklime and slaked

lime.

Calcination

Quicklime is produced from high purity (CaCO3) calcium carbonate (limestone), which are subjected

to a calcination process in vertical or rotary furnace at temperatures ranging between 1.100°C and

1.300°C, allowing its decomposition. The chemical equation that determines the reaction is as

follows:

CaCO3 + heat = CaO (solid) + CO2(gas).

The CaO (solid) is commonly known as quicklime and its main characteristic is that it has high

alkalinity (pH 12) when solubilized with water, this is the reason it is utilized as PH regulator in mining

and industrial processes, where neutralizing, soften and clarifying water is required and for

stabilizing clay soils.

Hydration

Calcium oxide is chemically unstable and when in contact with water in any state (liquid, solid, gas)

the process known as hydration begins and it becomes in calcium hydroxide Ca(OH)2, typically called

slaked lime, air lime or hydrated lime. The hydration process is quick and it produces a lot of heat.

The chemical equation representing this reaction is as follows:

CaO + H2O = Ca(OH)2 + heat

Re carbonation

When slaked lime reacts with the CO2 from the air, process known as re carbonation, calcium

carbonate is formed again acquiring properties originally possessed as rock.

Ca(OH)2 + CO2 + time = CaCO3 + H2O

2 Calcium oxide, CaO.

Copper-mining critical supplies market analysis

9

Chilean Copper Commission

Fig. 1: Quicklime cycle

Source: Cochilco

2.2. Quicklime uses

The following table summarizes the countless uses of quicklime:

Table 1: Lime uses (Quicklime, slaked lime and hydraulic)

Trade Use Function

Industrial Organic and inorganic chemistry

Binding agent, collector or precipitant.

Water treatment Coagulant, depressant, purifier and pH regulator.

Water treatment through inverse osmosis

PH regulator.

Paper and pulp Binding agent y basifying.

Food and subproducts Nutrient, coagulant and stabilizer, among other uses.

Sugar production Binder and neutralizer of acidity.

Petroleum Thickener, sealant and pH regulator.

Thermal power stations Sulfur sorbent or detainer, depends on the process.

Construction Silicic and lightweight bricks

Binding agent.

Copper-mining critical supplies market analysis

10

Chilean Copper Commission

Trade Use Function

Lightweight concrete Reacting agent.

Mortar Plasticizer and displacer.

Asphalt paving Waterproofing, anti-disintegrant and stabilizer.

Estabilización de suelos Binder and displacer.

Protective coating Paint

Agriculture Soil improvements PH regulator.

Plant nutrient Accelerant

Fertilizer Deodorizer and nutrient.

Insecticide, fungicide Diluent

Diverse Uses Pigments Binder and pH regulator.

Varnish Neutralizer

Rubber Desiccant

Pollution control Absorbent

Mariculture Decontaminant

Farming Germicidal

Metal mining Smelter Acts as flux, binder. Absorbs smoke gases and chimney gases. Bar unmolding, nickel precipitation catalyst, wire production lubricant, and others.

Copper Smelters Flux and cast remover.

Neutralizes the acid effluents generated by the acid plants associated with these smelters.

Cyanidation of auriferous minerals (Au) and argentiferous (Ag)

Besides having a specific role in each cyanidation processes, prevents the generation of hydrocyanic acid in the cyanide hydrolysis. Alkalizing in cyanidation.

Alkaline flotation PH regulator, Pyrite depressant, calcium salts precipitant, linking of the active silica contained in clays, among others.

Leaching gravel Neutralizes the residual acidity and sticks the clays contained in the ore (stabilizer)

Non-metal mining Obtaining all salts and nitrates

PH regulator or precipitant, and others.

Obtaining synthetic colemanite

Linking agent (boric acid production).

Copper-mining critical supplies market analysis

11

Chilean Copper Commission

Trade Use Function

Obtaining granulated ulexite (fertilizer)

Binder

Obtaining granulated potassium nitrate

Binder

Obtaining lithium Linking agent and depressant of the magnesium present in the brines containing lithiumo.

Treatment of water or RILES

Neutralizer.

Source: Cochilco based on the book “Quicklime: is a chemical reactive!” (2008)

This investigation’s scope of work is to gain knowledge about the market of quicklime associated

with the copper mining, and related specifically with the flotation process.

2.3. Quicklime supply

2.3.1. Domestic Production

This work estimates the domestic supply of lime in Chile for the mining market, with special interest

in the Calcium Oxide (Cao) or quicklime offer that is used in copper flotation processes, smelters

and gold mining. It must be noted that the major domestic quicklime producers supplying to the

mining industry, don’t publish detailed information showing the bulk quantities for their lime

products. With the purpose of determining the percentage of quicklime production, data based on

the actual dispatched products was utilized, this information was provided by the companies

themselves and for the remaining ones it is assumed that 90% of their production is quicklime.

There are two companies, in the domestic market, leading the lime production (quicklime and slaked

lime) for the mining industry, their capabilities are detailed in the following table:

Copper-mining critical supplies market analysis

12

Chilean Copper Commission

Table 2: Major quicklime producers for mining in Chile

Empresa Controller Products Facility Target Market

Maximum Capability

(ktpa)

INACAL Cementos Bío Bío S.A.

Quicklime (granulated and

ground) and hydrated lime

Antofagasta Arica-Parinacota, Tarapacá and Antofagasta regions

650

Copiapó Atacama and Coquimbo regions

550

SOPROCAL Rozas Rodríguez family through La

Tirana Ltda. Investments

Quicklime (granulated and

ground) and hydrated lime

Melipilla Mining operations at central zone

110 (*)

Source: Cochilco based on companies’ information, Annual Reports, Environmental Evaluation and Services

(*) The plant production capability is 165 ktpa. However, due to environmental restrictions it reduced its

production to 110 ktpa.

DIA approved Project and soon to start operations3:

In May 2014, SOPROMIN’s quicklime plant received a favorable rating for the project (RCA N°

0260/2014) that will replace 3 vertical furnaces for 2 horizontal ones. This replacement will increase

the plant’s project treatment capability from 87 to 216 ktpa. The renovation will require a US$ 25

million investment and the construction phase is estimated to last 18 months. Important

negotiations are currently taking place in an engineering, purchasing construction contract (EPC) for

the procurement of the plant out of Chile and that should initiate production in 2018. Owned

limestone reserves allow for a 25-year useful lifetime.

To determine the ability of lime producers to supply the domestic market, the following

assumptions were made:

_ Plant utilization: It is estimated that the effective utilization is 90% of the installed capacity.

_ Distribution of the offered products: The lime manufacturing plants generally produce

calcium oxide. However, some of that product becomes calcium hydroxide, and it is destined

to a different market. Similarly, a part of the calcium oxide produced is for other uses but

mining (between 10% and 20% of the CaO, depending on the company)

3 By the end of this study, there was no information about the conditions of the lime production plant located in the Atacama region (Caldera and Copiapó communes), which has a 165 ktpa quicklime production capacity (aimed at mining and environmental markets) and that was planned to begin operations during second half of 2015. For that reason, it was not considered in the previous table, but it was taken into account for the following years offer-demand balance.

Copper-mining critical supplies market analysis

13

Chilean Copper Commission

It is calculated that in 2016 the quicklime offer of domestic production would be around a million

tons. The quicklime offer would increase to 1.5 million tons per year if the Sopromin project is

complete by 2018 and the Atacama based (Caldera and Copiapó communes) quicklime production

plant starts operating, which has a 165 ktpa quicklime capacity.

2.3.2. Lime imports

Three types of lime are imported: Quicklime, Slaked lime and hydraulic lime4. 425.4 tons of lime

were imported during 2015, 90.6% of the total was quicklime

Fig. 2: Imports distribution by lime type 2015

Source: Thompson Reuters (2016) based on Customs information

In CIF terms, US $74.6 were imported, 79% of the imports was quicklime and 21% slaked lime. In

comparison, the hydraulic lime imports are marginal, representing less than 1% of the total.

Just as observed in previous years, in 2015 95% of the total volume of imported quicklime comes

from Argentina.

The largest quicklime imported volume was registered in 2013 with 406 thousand tons. A decreasing

tendency was maintained in 2015 with 376 thousand tons of imported quicklime, which is a 2.3%

reduction compared to the previous period.

SIBELCO Chile remains as the major quicklime importer with volumes representing 54% of the total

imports in 2015. Followed by CEFAS Chile, which has its production plants in Argentina and imported

18% of the total calcium oxide in 2015.

The imports leadership has changed in the last 10 years as it is show below:

4 The difference between hydraulic and hydrated lime is that the first one contains significant amounts of silicon and aluminum. As a reminder, hydraulic lime is used in construction only in hydrated state.

Copper-mining critical supplies market analysis

14

Chilean Copper Commission

Fig. 3: Major importers of quicklime 2005-2015

Fuente: Thompson Reuters (2016) based on Customs information

Minera LBE was acquired by Sibelco in Argentina in 2009.

Fig. 4: Imports and domestic production capacity of quicklime 2015

Source: Own collection

Considering the domestic installed quicklime production capacity and the exports for mining

utilization, the quicklime offer for 2015 is approximately 1,341 thousand tons.

2.4. Quicklime demand

2.4.1. Quicklime final use

There are many uses for lime, but there isn’t current public information of the amounts by final

utilization. However, Coloma (2008) provides the following breakdown showing the lime’s final

utilization percentages in the 2000-2010 period:

Copper-mining critical supplies market analysis

15

Chilean Copper Commission

Fig. 5: Participation (%) by final use of quicklime in Chile

Source: Cochilco based on the book “Quicklime: is a chemical reactive!” (2008)

80% of the quicklime used between 2007 and 2009 was in flotation processes (associated with the

copper mining). Cyanide by leaching and agitation is used in the gold extraction and it accounted for

13% of the total quicklime utilization nationwide.

2.4.2. Quicklime Consumption in the Copper Mining

The most common use of quicklime in the mining industry is the copper flotation process. In order

to estimate the quicklime demand is necessary to have a daily consumption indicator measured in

quicklime kilograms per ton of processed orel (quicklime Kg/ ore ton). Depending on the ore to be

treated, the quicklime unit consumption value presents significant variation. The quicklime unit

consumption values range from 1.5 to 1.7 kg/ton of processed ore. The first obtained value was the

result of a Cochilco study (2007)7 and it is similar to values of some engineering projects that were

consulted. The second value was estimated by the largest quicklime producer in Chile (INACAL). For

calculation purposes in the offer & demand estimation, the intermediate value of 1.6 kg/ton of

processed ore will be assumed.

When multiplying the quicklime unit consumption value by the copper sulphide ore projection for

2016-2025, the following estimates are obtained:

76%81% 84% 86% 86% 82% 78% 80% 79% 79% 80%

18% 10% 7% 7% 9%11% 15% 12% 13% 13% 13%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Smelter

Chemical

Effluent neutralization

Cyanide (leaching & agitation)

Flotation

Copper-mining critical supplies market analysis

16

Chilean Copper Commission

Fig. 6: CaO estimated consumption vs 2015 scenario (thousand tons)

Source: Cochilco

(*) From quicklime consumption estimates in 2015 version of this study, but utilizing the corrected

consumption rate of 1.6 kg of CaO/ton of treated Cu ore.

The “Base”, “Probable”, “Possible” and “Potential” scenarios consider the quicklime consumption

for different copper ore processing scenarios by flotation processes, which depend on the probable

realization of investments in the mining projects portfolio for 2025 (Cochilco). These estimates differ

from the 2015 report projections (dashed line), which demostrates the decrease of the quicklime

expected consumption due to some companies postponing and others cancelling their planned

investments as a result of the deteriorating marked conditions. The new projections, considering a

reduced volume of processed ore, entail the need of a lesser amount of quicklime for their copper

flotation processes for 2016-225 period and estimates -2,060 thousand tons (2015 estimate vs 2016

estimate).

The “CaO for other uses” item represents the estimated consumption of quicklime in smelters,

cyanide (silver extraction) and other applications, which accounts for 25% of the quicklime amount

used in copper flotation processes (Potential scenario consumption excluded).

2.5. Quicklime offer and demand

The following figure shows the domestic offer and demand balance:

Copper-mining critical supplies market analysis

17

Chilean Copper Commission

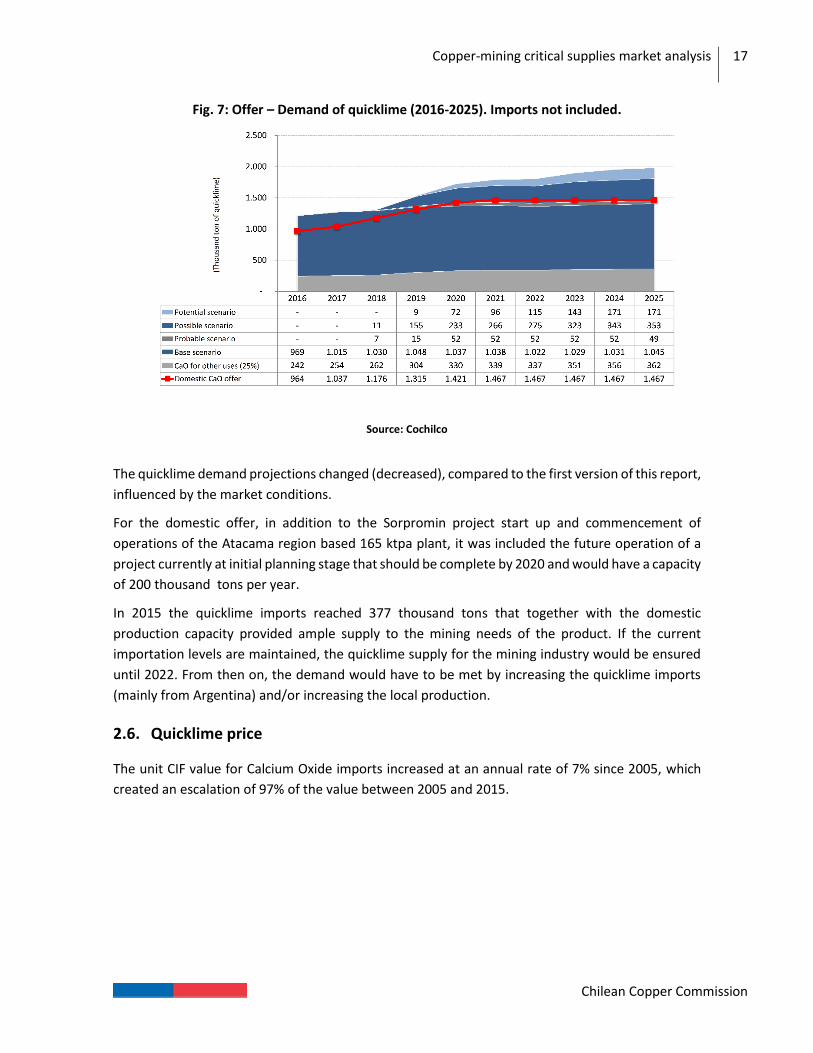

Fig. 7: Offer – Demand of quicklime (2016-2025). Imports not included.

Source: Cochilco

The quicklime demand projections changed (decreased), compared to the first version of this report,

influenced by the market conditions.

For the domestic offer, in addition to the Sorpromin project start up and commencement of

operations of the Atacama region based 165 ktpa plant, it was included the future operation of a

project currently at initial planning stage that should be complete by 2020 and would have a capacity

of 200 thousand tons per year.

In 2015 the quicklime imports reached 377 thousand tons that together with the domestic

production capacity provided ample supply to the mining needs of the product. If the current

importation levels are maintained, the quicklime supply for the mining industry would be ensured

until 2022. From then on, the demand would have to be met by increasing the quicklime imports

(mainly from Argentina) and/or increasing the local production.

2.6. Quicklime price

The unit CIF value for Calcium Oxide imports increased at an annual rate of 7% since 2005, which

created an escalation of 97% of the value between 2005 and 2015.

Copper-mining critical supplies market analysis

18

Chilean Copper Commission

Fig. 8: Calcium oxide 2005-2015 CIF unit value (US$/ton)

Source: Thompson Reuters (2016) based on Customs information

The CIF value continued to raise in 2015 to 156.7 US$/ton, which is a 9.9% increase compared to the

previous year.

Something to consider is that almost 99% of the imported quicklime come from Argentina, therefore

there are no import taxes associated, reducing the final cost.

There is the following scenario:

_ The price and volume of imports have been raising.

_ Imported quicklime has taken some of the domestic production market.

_ There are projects for new quicklime production plants in Argentina, specifically in the San

Juan province.

The competition between imports and domestic production will keep the prices relatively stable

until 2022. From then on, the new mining projects start up (possible and potential) could create a

raise in the quicklime price, as long as the quicklime imports don’t increase and/or new quicklime

production projects are made.

Copper-mining critical supplies market analysis

19

Chilean Copper Commission

3. Grinding balls

In addition to the copper mining, grinding balls are also utilized in other industries such as cement

and energy generation.

3.1. Using grinding balls in copper mining5

Grinding balls are utilized in all of the mineral grinding processes: conventional, unitary, SAG and

regrinding. Grinding is the procedure that follows the ore crushing and in which the particle

reduction is continued to a maximum size of 180 micron, allowing the separation of the copper

particles.

The grinding process is performed in three different ways: conventional grinding, unitary (with and

without HPGR) and SAG grinding.

Fig. 9: Types of crushing and grinding circuits

Source: Cochilco

Conventional Grinding: Contains two phases, the first one is with rod mills and the second one with

ball mills.

Unitary Grinding (with and without HPGR): This type of grinding utilizes ball mills and may

incorporate unitary grinding with high pressure grinding rolls (HPGR).

5 www.codelcoeduca.cl

Copper-mining critical supplies market analysis

20

Chilean Copper Commission

Around 40 to 45% of their interior volume is occupied by 1”-4” diameter steel balls, which are the

grinding media. In a 20-minute long process for each ore particle that has to be ground, 80% of the

mineral is reduced to size of 180 microns or smaller.

SAG Grinding: Utilizes a high capacity mill where the material is deposited right after the primary

crusher and contains steel balls inside; when the mill rotates, the material falls and gets ground by

the impact effect between the balls and the material itself. Most of the material released by this

mill go to the flotation phase where the copper concentrate is obtained. A smaller amount of

material returns to the ball mill for grinding until the required size for the following phase is

achieved.

3.1.1. Grinding balls size and filling level

The filling level depends on the percentage fraction of the total internal volume of the mill loaded

with grinding media (rods, balls).

Table 3: Filling level

Mill type Filling Level

Rods 30-40%

Balls 40-45%

Balls (regrinding) 25-30%

SAG 10-15% Fuente: Cochilco.

The grinding balls size depend on the grinding type as shown on the following table:

Table 4: Grinding means uses

Grinding Type

Balls Size (inches)

SAG 4" - 6"

Balls 1" - 4"

Vertical 0,5" - 1,5"

Ultra fine (ISA) < 0,1" Source: Cochilco based on the presentation Moly-Cop, 2012

Two types of balls are produced in Chile. Forged steel and molten steel.

Despite of their higher price, forged steel balls are 10-15% more efficient than molten steel balls

because they wear less.

Forged steel balls production is limited to a maximum diameter of 4” because they cannot withstand

the strong impacts that are characteristic in Semi Autogenous Grinding (SAG), where larger diameter

balls are required.

Copper-mining critical supplies market analysis

21

Chilean Copper Commission

A modern grinding circuit consumes approximately between 30 and 40% large balls (>4”), between

40 and 50% mid-size balls (2” - 3.5”) and the rest small balls (<2”).

3.2. Grinding balls supply

3.2.1. Domestic Production

The Chilean most important manufacturers of grinding balls are Moly-Cop Chile S.A., SK Sabo S.A.

and Proacer S.A.

Moly-Cop Chile S.A. manufactures and distributes Steel balls for grinding; these are utilized in the

extraction of copper, gold and iron. Founded in 1959, their Talcahuano and Mejillones, company

owned plants, have a grinding means rated capacity of 471,000 tons. Moly-Cop is 100% controlled

by Arrium, an Australian firm that acquired Moly-Cop from Anglo American Plc in 2011.

SK Sabo S.A. is a company 99.99% controlled by Magotteaux, a Belgian Enterprise leading in

development, fabrication and commercialization of grinding balls and wear parts (casting). At the

same time, Sigdo Koppers controlls 95% of Magotteaux. SK Sabo S.A. has a plant in Antofagasta,

Chile with a capacity of 55,000 ton/year of forged grinding balls. The major businesses where their

products are commercialized are the mining and cement industries.

Proacer S.A. is another company controlled 100% by Magotteaux, which is at the same time

controlled by Sigdo Koppers S.A. The company has an installed capacity of 60,000 tons of low-

chrome balls.

Copper-mining critical supplies market analysis

22

Chilean Copper Commission

Table 5: Grinding balls production companies

Company Plant

Location

Rated Production (ton/ year)

Balls Market

Moly-Cop

Talcahuano 202,000

1" to 6" forged steel grinding balls

The main Chilean clients are the large concentrators like Minera Collahuasi, Codelco, Los Pelambres, Minera Candelaria, Anglo Chile and Alumbrera in Argentina

Mejillones 269,000

SK Sabo S.A. Antofagasta 55,000 Forged steel grinding balls. Clients in Northern Chile

and Peru

Proacer Ltda. Santiago (Til Til)

60,000 2" to 4" molten low-chrome

grinding balls Mining market

Fuente: Cochilco Based on companies’ information, institutional websites and memoires.

When analyzing the three major grinding balls suppliers, it can be observed that Moly-Cop has 80.4%

of the installed capacity and Sigdo Koppers 19.6% through its subsidiaries SK Sabo S.A. and Proacer.

By March 2016, the three major manufacturers’ combined steel balls production installed-capacity

for mining is 586 ktpa.

Approved RCA

_ In October 2014 a R.C.A. (527/2014) was issued approving the construction and operation of

a forged balls manufacturing plant for the large mining. This plant, owned by Aceros Chile S.A.

will be located in the Puente Alto commune. The project’s phase 1, with a 48,000 ton capacity,

started construction in February 2016 and will be in commercial-production conditions in

January 2017. The execution of phases 2 and 3 of the project are subjected to the market’s

demand evolution. The target market is the large mining in Chile, Peru and Argentina, the

same markets where Aceros Chile currently offers molten steel liners for grinding equipment

and crushers.

_ In May 2013 a R.C.A. (54/2013) was issued approving the construction and operation of a

steel forged balls manufacturing plant aimed mainly for the comminution processes (size

reduction) of mining materials. This SK Sabo owned plant will be installed in the Coquimbo

commune with a total rating of 150,000 tons. However, the project’s implementation was not

materialized.

With the Aceros Chile S.A. plant startup, the domestic installed capacity would reach 634 ktpa.

3.2.2. Grinding balls imports and exports

The major grinding balls importers are companies that manufacture and/or supply grinding balls,

mining enterprises, and cement producers.

Copper-mining critical supplies market analysis

23

Chilean Copper Commission

Elecmetal induced a powerful effect on the forged balls imports since 2010 as a result of the creation

of “ME Long Teng Grinding Media (Changshu) Co. Ltd.”, a Joint Venture 50/50 established in China

for the fabrication of grinding balls.

In 2015, 97% of grinding balls imported volume for mining were of forged type, the remaining were

molten.

Grinding balls imports evolution is shown on the following figure6 (in thousand tons), but without

considering companies that are not related to the grinding for copper mining such as cement

manufacturers, energy and others.

Fig. 10: Grinding balls major importers (2005- Mar 2016)

Source: Thompson Reuters (2016) based on Customs information

From 2010, Elecmetal became the major grinding balls importer for the mining industry, reaching

66% of 2015 imports. Acording to Elecmetal’s annual report, business areas, the company is

oriented to meet domestic and international demand for grinding balls for SAG and secondary

grinding. Elecmetal imports exclusively forged balls.

Codelco, the second largest importer of grinding balls, accounted for 20% of imports in 2015.

Magotteaux imported only molten balls until 2012. However, in 2015 forged balls represented 67%

of its total imports. An opposite scenario occurs with SK Sabo, which until 2013 imported only forged

grinding balls, and then changed in 2014 when molten grinding balls were 68% of the total imports.

SK Sabo didn’t register any imports of grinding balls in 2015.

Based on the grinding balls country of origin, the following is observed:

6 Considered tariff codes for molten balls: 73259900 and 73259110; Forged balls: 73261110 and 73261190.

Copper-mining critical supplies market analysis

24

Chilean Copper Commission

Fig. 11: Country of origin of imported grinding balls (2005-2015)

Fuente: Thompson Reuters (2016) based on Customs information

Chinese forged grinding balls represented 96% of the imported volume in 2015. Followed by

Peruvian with a marginal 3% share.

On the other hand, molten grinding balls imports are led by Peru and China with a 12% and 30%

shares respectively.

In 2015, the imported volume of grinding balls for mining (forged and molten) was approximately

157 thousand tons, which is 27% of the current domestic grinding balls production capacity (for

mining).

Regarding grinding balls exports, 84% of the 142 thousand tons of exports in 2015 were forged balls.

The main destination of exported forged balls in 2015 were Brazil, Argentina and Peru with 53%,

20% and 16% of the totals respectively. At the same time, Moly-Cop’s exports were 89% of the

exported balls in 2015. Proacer was responsible for 99.7% of the molten balls exports in 2015, with

Brazil as the major destination.

The evolution of exports and imports by grinding balls types, in thousand tons is shown below:

Fig. 12: Grinding balls imports and exports (thousand ton)

Source: Thompson Reuters (2016) based on Customs information

Copper-mining critical supplies market analysis

25

Chilean Copper Commission

From 2014, the forged grinding balls imports exceeded the exports. The molten grinding balls have

an opposite case scenario.

3.3. Grinding balls consumption in the copper mining

The grinding balls demand in the copper mining is related to the amount of processed ore in the

concentrating plants (the leached ore is not subjected to milling processes).

The contrast between the current and last year’s report (2015) projections for ore processing is

shown on the following figure. These projections are based on the mining companies’ decisions

regarding the realization, delay, restructuration or termination of their investment projects.

Fig. 13: 2016 vs 2015 processed ore Cu projections

Source: Cochilco

The processes ore projections fall (sulfide line) is due to the companies’ decisions for delaying and

in some cases cancelling their investment plans, as a result of the adverse economic scenario that

generated the drop in commodities prices.

A 770 gr/ton of ore unit consumption rate was utilized, this value was obtained from a 2007

Cochilco7 study and it is within the median value range of a succession of analyzed values. The

estimate for industry consumption of grinding balls was calculated with the previously mentioned

unit consumption rate.

7 “Business Opportunities for Providers of Goods, Supplies and Mining Services in Chile”, Cochilco, November 2007.

Copper-mining critical supplies market analysis

26

Chilean Copper Commission

Considering the processed copper ore 2016-2025 projections from the latest Mining Projects

Cadastre, the following estimate was obtained for consumption of steel grinding balls, grouped by

probable, possible and potential projects.

Fig. 14: Steel grinding balls consumption projections (2016-2025)

Fuente: Cochilco

According to the estimate, the current yearly consumption is 466,000 tons of grinding balls, with a

possible increase to 779,000 tons in 2025 given the case that all projects in the Cadastre are

implemented (probable, possible and potential mining projects).

Copper-mining critical supplies market analysis

27

Chilean Copper Commission

3.4. Grinding balls offer and demand

The following scenario is estimated for the grinding balls offer and demand to 2025:

Fig. 15: Steel grinding balls offer - demand (2016-2025). Imports not included.

Source: Cochilco

For the domestic offer estimate, it was assumed the utilization of 90% of the production plants and

the Aceros Chile S.A. plant startup in 2017.

The current installed capacity of production of grinding balls comfortably meets the demand for

grinding balls in mining. If the investments that have the highest level of uncertainty in their

execution are implemented (possible and potential scenarios), then the domestic production

capacity would be overcome from 2019.

However, the market balance changes when considering the grinding balls imports (mainly forged)

that reached 157 thousand tons in 2015. The grinding balls imports would have more relevance

from 2019 if most of the mining projects portfolio get implemented.

Copper-mining critical supplies market analysis

28

Chilean Copper Commission

3.5. Grinding balls price

Forged Balls

The following figure shows the CIF unit prices (US$/ton) from a sample of imported forged grinding

balls for mining uses, and which volume is 79% of the total imported tonnage for this industry in the

2009-2015 period. The considered diameters were: 6.25”, 5.5", 5", 3", 2” 1.5", 1” and 40mm. These

prices were compared with the CIF prices of imported Steel bars utilized for the fabrication of balls8.

Fig. 16: Valor CIF unitario bolas de molienda forjadas 2009-2016 (Mar)

Source: Thompson Reuters (2016) based on Customs information

Molten Balls

A sample was taken from imported molten balls for mining uses, which represent 78% of the total

imported tonnage for the industry in the 2009-2015 period. The following diameters were

considered: 2”, 3”, 40 mm, 30 mm and 50 mm. The prices are compared against the steel spot price

at the London Metal Stock Exchange.

8 Tariff code: 72283000.

Copper-mining critical supplies market analysis

29

Chilean Copper Commission

Fig. 17: Molten grinding balls CIF unit value 2009-2015

Source: Thompson Reuters (2016) based on Customs information

There is an evident price drop in the forged grinding balls from 2012, similar to the price of imported

steel bars utilized for balls fabrication.

Copper-mining critical supplies market analysis

30

Chilean Copper Commission

4. Extraction Trucks

The analysis was performed on the off the road trucks market, for transportation of extracted

material in copper open pit mining operations, emphasizing on the large scale copper mining.

Extraction trucks mission is to transport the extracted material to a destination point that is defined

by the mining plan. They are the most commonly utilized transportation units in mining and are

specially designed to haul mining heavy loads.

Material transportation is one of the most important aspects in an open pit mining operation, it

signifies around 50% of the operations cost, and in some cases up to 60%.

4.1. Extraction trucks imports

The following analysis is focused in the importation of off the road trucks of the brands with the

most presence in the extraction operations of the Large Scale copper mining: Caterpillar, Komatsu

y Liebherr. The studied models and their target markets are shown below:

Table 6: Categorization of off road extraction trucks, by target market

Target Market Brand Model

Large Mining

Caterpillar 793- 795- 797

Komatsu 830E- 930E- 960E

Liebherr T282

Medium-scale mining Caterpillar 789

Komatsu H785

Small Mining Caterpillar 773-775-777-785

Komatsu HD465- HD605- 730E

Source: Cochilco

In the 2002-2015 period were imported 2,107 brand new truck units. The following figure shown

the trucks imports grouped by brand.

Copper-mining critical supplies market analysis

31

Chilean Copper Commission

Fig. 18: New mining trucks imports, by brand, 2002-2015

Source: Thompson Reuters (2016) based on Customs information

84% of the units’ importation was performed by the companies representing the manufacturers in

Chile and 6% was imported directly by the Large Scale copper mining users led by Codelco, Barrick

and Anglo American.

On the other hand, each model has determined commercialization target market (small, median

and large scale mining). When grouping the imported trucks according to their target market, the

following scenario is observed:

Fig. 19: New mining trucks imports, by target market, 2002-2015

Copper-mining critical supplies market analysis

32

Chilean Copper Commission

Source: Thompson Reuters (2016) based on Customs information

In the 2002-2015 period 1,132 trucks were imported for the large scale copper mining. However,

due to the global market recession, the truck imports began decreasing in 2012, reaching in 2015

levels observed in 2004. It must be noted that the imports analysis is focused only in those models

of the most utilized brands in the large mining (Komatsu, Caterpillar y Liebherr). Therefore, the

previously shown graphic doesn’t include the imported trucks of other brands that are mainly

destined to the mid-scale and small mining.

Fig. 20: New mining trucks imports for the large mining, 2002-2015

Source: Thompson Reuters (2016) based on Customs information

Komatsu, Caterpillar y Liebherr are the most common brands in the open pit copper large mining.

In the analyzed period 1,132 trucks were imported with a peak in 2012 (201 units).

Komatsu trucks importations raised from 2012 (specifically the 930E model) and on the other hand,

no imports were registered for Liebherr trucks, model T282 since 2013.

4.2. New trucks demand

The demand for trucks is given by the movement of material needs at the operating open pits and

future mining projects. Based on the estimated material movement9 for the 2016-2025 period, it

was obtained an estimate of the truck demand for the following years focused in the large copper

mining operations. The calculation of the number of trucks considers variables such as:

9 Wood Mackenzie, Q2 2016.

Copper-mining critical supplies market analysis

33

Chilean Copper Commission

_ Average hauling distance to landfill, piles or plant.

_ Horizontal and slope speed (loaded and unloaded)

_ Trucks’ capacity

_ Availability and effective utilization of trucks

_ Distance increases due to open pits deepening

The volume of material (orel + waste) to be moved in open pit mining in the 2016-2025 period is

shown below:

Fig. 21: Material movement in open pit mining (2016-2025)

Source: Wood Mackenzie (Q2 2016)

The material movement projections indicate that in 2021 and 2022 there will be a peak with 3,100

million tons and then it will slowdown.

There are two factors determining the truck demand for material movement:

_ Need for equipment (trucks) replacement due to end of its useful life.

_ Need for additional equipment (trucks) to meet increased material movement.

Just as in the 2015 version of this study, a projection was made to estimate the number of new

trucks needed to meet the material hauling demand (waste and ore) for the next few years10. The

10 Assumptions:

_ Average speed in slopes and horizontal (loaded and unloaded) = 25 Km/hr.

_ The current truck fleet capacity configuration on each site is maintained (models currently

used).

_ Availability according to the truck’s useful life, which is 86% to 73%.

Copper-mining critical supplies market analysis

34

Chilean Copper Commission

graphic below shows the estimated truck demand for the 2015-2025 period, for a group of

operations that represent over 90% of the material movement in open pit mining. The estimated

value corresponds to the average of the projections for scenarios where trucks have different useful

life ranging from 10 years to a maximum of 15 years.

Fig. 22: Need for new mining trucks (2016-2025)

Fuente: Own collection

The estimate assumes that the fleet replacements will take place in 3 years in trucks grouped in two

capacity varieties:

_ Large Mining (Trucks similar to Caterpillar 793-9797 and Komatsu 830E – 930E).

_ Mid-scale mining (Trucks similar to Caterpillar 789).

In the 2016-2025 period, the large-scale mining will require 554 new extraction trucks and the mid-

scale mining 101 trucks.

The demand projection for new trucks considers the replacement of existing equipment fleets as a

result of the end of their useful lives and assumes that the current hauling configurations are

maintained (truck models). The same assumptions were applied for the quantification of the

additional trucks required to meet the increase of material movement in mining operations.

4.3. Extraction Trucks Price

All the extraction trucks are imports. The subsequent figure shows the evolution of the imports CIF

value for the models of trucks with the highest demand of the following brands: Komatsu, Caterpillar

and Liebherr.

_ Trucks’ effective utilization BD (76%)

Copper-mining critical supplies market analysis

35

Chilean Copper Commission

Fig. 23: CIF value (Million US$/unit) CAEX trucks

Fuente: Thompson Reuters (2016) based on Customs information

Considering the manufacturer’s load ratings, resemblances in in the prices are found between

models 930E (Komatsu) and 797 (Caterpillar), as well as between models 830E (Komatsu) and

789/793 (Caterpillar).

Copper-mining critical supplies market analysis

36

Chilean Copper Commission

5. Mining Shovels

Surface mining couldn’t be feasible without large mining shovel equipment, which are an essential

part of the mining process. Hydraulic and cable (rope) shovels are the most utilized loading

equipment in the copper large-scale open pit mining.

The mining shovels are large pieces of equipment with low unit costs and good maintenance and

support availability. Among their differences between the cable (rope) shovels and the hydraulic

ones is that the first ones have higher load capacity.

5.1. Shovel-loaders supply

The shovel-loaders analysis is focused in the most utilized models in the large-scale copper mining

in Chile, which are:

Table 7: Mining Shovels large copper mining

Brand Series Tipo Capacity11

(yd3)

Caterpillar 7495 (Bucyrus 495 series) Cable 53-73

P&H 4100 Cable 54-76

P&H 2800 Cable 34-46

Komatsu PC 8000 Hydraulic 55

Komatsu PC 5500 Hydraulic 32-37

Source: Cochilco

According to Editec. S.A. (2014)12 publication, in a group of 18 large-scale copper mining operations

that represent 75% of the annual production, the following was observed:

_ 73% of a total of 128 equipment units are electric cable (rope) shovels and the remaining

(27%) are hydraulic shovels. Due to the extraction companies tendency of moving larger

amounts of material (ore and waste), the cable (rope) shovel is the most utilized in open pit

mining thanks to their loading productivity.

_ The average age of the operating cable (rope) shovels and hydraulic shovels of the sample

is approximately 15 and 9 years respective (as of 2015).

_ The shovel-loaders distribution by type and Brand is shown below:

11 The capacity range was obtained from “Mining Equipment Cadastre 2014/2013”, Editec S.A. 12 “Mining Equipment Cadastre 2014/2013”.

Copper-mining critical supplies market analysis

37

Chilean Copper Commission

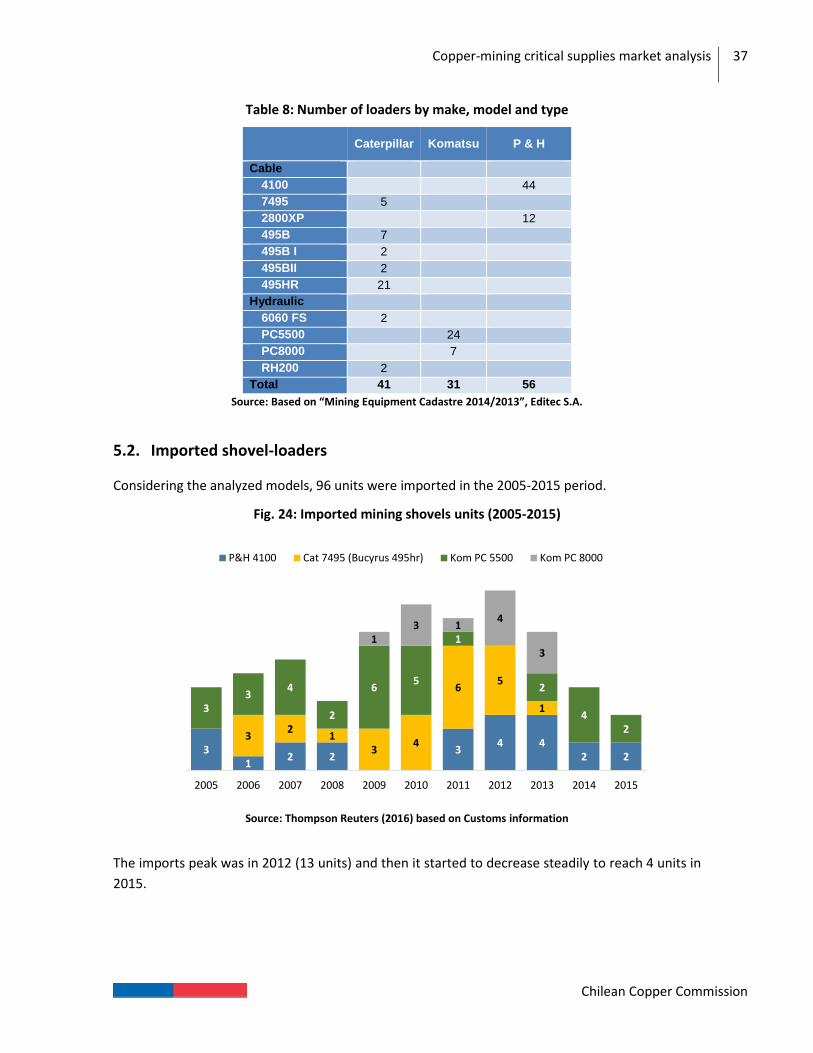

Table 8: Number of loaders by make, model and type

Caterpillar Komatsu P & H

Cable

4100 44

7495 5

2800XP 12

495B 7

495B I 2

495BII 2

495HR 21

Hydraulic

6060 FS 2

PC5500 24

PC8000 7

RH200 2

Total 41 31 56

Source: Based on “Mining Equipment Cadastre 2014/2013”, Editec S.A.

5.2. Imported shovel-loaders

Considering the analyzed models, 96 units were imported in the 2005-2015 period.

Fig. 24: Imported mining shovels units (2005-2015)

Source: Thompson Reuters (2016) based on Customs information

The imports peak was in 2012 (13 units) and then it started to decrease steadily to reach 4 units in

2015.

31

2 23

4 42 2

32

13

4

65

133

4

2

65

1

2

42

13 1

4

3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

P&H 4100 Cat 7495 (Bucyrus 495hr) Kom PC 5500 Kom PC 8000

Copper-mining critical supplies market analysis

38

Chilean Copper Commission

48 units of the bigger models (cable/rope shovels P&H 4100 XPB-XPC and Caterpillar 7495 (Bucyrus

495hr)) were imported on the 2005-2015 period. Almost 100% of the units were imported directly

by the mining companies, the buyers.

A different scenario is observed with Komatsu models PC8000 and PC5500 since only 18% of the

units was imported directly by mining companies. The vast majority (64%), of the imports were

made by the distributor of the brand in Chile

5.3. Mining Shovels’ Price

Likewise to the extraction trucks, 100% of the analyzed brands of mining shovels were imported.

The following figure shows the CIF value evolution of the analyzed mining shovels models.

Fig. 25: CIF unit value mining shovels 2005-2015

Source: Thompson Reuters (2016) based on Customs information

Apparently 2013 marked the end of the shovel-loaders’ price rise. During the last 2 years the models

4100 and PC 5500 present CIF values decline.

Copper-mining critical supplies market analysis

39

Chilean Copper Commission

6. Mining OTR Tires

The analysis was focused in tires for the off the road trucks that were studied in the previous chapter

and that correspond to equipment utilized in open pit mines. The analyzed tire sizes are those from

the manufacturers’ specifications for their trucks; these are13:

_ 24.00 R35

_ 27.00 R49

_ 33.00 R51

_ 37.00 R57

_ 42/90 R57

_ 40.00 R57

_ 46/90 R57

_ 53/80 R63

_ 56/80 R63

_ 59/80 R63

6.1. Tires imports

There are no manufacturers in Chile that produce tires of the analyzed sizes, therefore, 100% of

them were imported. The detail of imported volumes is shown below (millions US$ CIF):

Fig. 26: Tires imports (millions US$ CIF)

Source: Thompson Reuters (2016) based on Customs information

Up to 2013 there was a constant increase in the tires imports, which was 29% annually for the 2005-

2013 period. From 2014 a severe drop in imports is observed, resulting from the slowdown in the

mining sector, falling from US$ 351 million in 2013 to $209 million CIF in 2015.

13 RXX where “R” represent the layers run radially across the tire and “XX” is the ring’s diameter in inches.

Copper-mining critical supplies market analysis

40

Chilean Copper Commission

Bridgestone and Michelin are the major manufacturers of tires for heavy duty trucks occupied in

open pit mining.

Direct imports of tires managed by the large-scale copper mining companies (operational) account

for 29% of the total imports in the 2005-2015 period, being Minera Escondida and Codelco the most

prominent (24% of the imported volume in the analyzed period). Unlike the rest of the mining

operations, these two companies register steadiness in the tires imports during the last 9 years.

The following figure shows the imported units arranged by their size:

Fig. 27: Imported tire units by type

Source: Thompson Reuters (2016) based on Customs information

Tires importation reached its peak in 2013 and then began declining to the present.

6.2. Tires demand

The analysis considered only sizes 57” and 63”, that correspond to trucks with loading capacity over

150 tons. Therefore, this demand is related to the trucks’ fleet size in operation during the 2016-

202514 period.

14It was assumed the average duration of a tire as 5,000 hours.

Copper-mining critical supplies market analysis

41

Chilean Copper Commission

Fig. 28: Large size tires demand (2016-2025)

Source: Own collection

The analyzed tires are those required by trucks of the following models: Caterpillar 789, 793, 797

and Komatsu 730E, 830E, 930E. Tires of these types that are used in other equipment were not

considered in the projection.

6.3. Tires Price

As it has been observed in the rest of the mining supplies, during the last few years, the tires for

mining show a fall in their prices.

Copper-mining critical supplies market analysis

42

Chilean Copper Commission

Fig. 29: CIF unit value tires (US$/unit)

Source: Thompson Reuters (2016) based on Customs information

The larger the size of the tire, the higher is the price variation for the analyzed period. Stated

otherwise, the slowdown of mining hit stronger to the prices of larger size tires, especially tires sizes

57” and 63”. Prices started to decrease in 2012. For tires of smaller sizes, perhaps the existence of

a greater number of suppliers / providers explain the lower price variability.

Copper-mining critical supplies market analysis

43

Chilean Copper Commission

7. Flocculants used in the copper mining

Conventional flocculants are polymers used in the process of concentration, specifically in the areas

of:

Concentrate thickening (it is a physical, chemical process that allows for the separation of

copper sulfide ore and other elements such as molybdenum from other minerals that make

up most of the original rock) and

Filtration/thickening of tailings (it allows the partial recovery of water used in the grinding and

flotation operations).

Because it is not possible to predict theoretically what is the suitable synthetic flocculants for a

particular suspension, the selection is made based on lab tests and considers factors like the settling

velocity of different polymers having different ionic characteristics, molecular weights, chain

structures, etc. on a representative sample of the material to settle.

According to sources, conventional flocculants occupied by the major large scale copper mining

companies are imported and they are available under different trademarks. Below is a list of some

flocculants used in mining, the information was obtained from the records of imports:

Table 9: Major brands of flocculants utilized in mining 15

Manufacturer Brand

Aguasin Praestol 2620

Basf Magnafloc-1011

Magnafloc-333

Magnafloc-2025

Magnafloc-155

Magnafloc-338

Kemira A-110

Orica AP-2020

NP-9910

Snf TEC-2050

913 SH

SNF923 SH

TEC-228

SNF-103

SNF-670

Source: Cochilco

15 Considered tariff codes: 39089000, 38249099, 39069000, 38089329 and 36069000.

Copper-mining critical supplies market analysis

44

Chilean Copper Commission

Note that there may be other imported flocculants’ brands for mining use, however specifications

describing the product does not provide information about their end use.

The imports evolution, in CIF Million Dollars (MM US$), of the most utilized flocculants in mining

processes is:

Fig. 30: Mining flocculants major brands imports (MMUS$ CIF)

Source: Thompson Reuters (2016) based on Customs information

The previous figure considers the imported volumes (MM US$ CIF) by the flocculants manufacturers

of the brands indicated in table 9, and other flocculants’ brands manufactured by BASF, Kemira and

SNF.

In the 2010-2015 period, the market’s percentage share according to the flocculants’ imported

volumes are SNF (63%), Orica (15%), BASF (6%) and Kemira (6%). These shares consider only the

flocculants’ brands shown in table N°9.

Using a unit consumption rate of 15gr/ton of utilized flocculants per tons of processed sulfide ore

(expert’s criteria) the consumption estimate for the next 10 years is obtained.

Copper-mining critical supplies market analysis

45

Chilean Copper Commission

Fig. 31: Flocculants projected consumption (tons)

Source: Cochilco

The expected flocculants consumption could significantly increase depending on the

implementation of those projects categorized as “possible” in the mining investments portfolio,

which are those mining investments less likely to materialize in the terms defined by their owners

and the most likely to be affected by changes in market conditions.

Fig. 32: Average CIF unit value of conventional flocculants (US$ CIF/kg)

Source: Thompson Reuters (2016) based on Customs information

Copper-mining critical supplies market analysis

46

Chilean Copper Commission

During the last two years the flocculants CIF value16 show a decreasing tendency, this situation

continues today.

On the other hand, in the last few years, mining companies are moving toward the increasing of ore

processing, this implies increasing the thickeners utilized for water recycling. Sometimes

conventional flocculants are not the able to maintain their efficiency and cause operational

problems occur (torque increase at raking arms) and transportation of thickened paste. To solve

these problems, a line of polymers have been created, “rheology modifier flocculants” with the goal

of increasing the thickeners’ efficiency.

16 The average unit value considers the flocculants’ brands with continuity and relevance in the

imported volumes in the 2010-2015 period. (Praestol 2620 (Aguasin), Magnafloc 155 (Basf), Magnafloc

2025 (Basf), Magnafloc 333 (Basf), Superfloc A-110 (Kemira), Orifloc AP 2020 (Orica), Orifloc NP 9910 (Orica),

913 SH (Basf) and 923 SH (Basf)).

Copper-mining critical supplies market analysis

47

Chilean Copper Commission

8. Bibliography

Aceros Chile S.A. (s.f.). Servicio de Evaluación Ambiental. Obtenido de

http://seia.sea.gob.cl/expediente/ficha/fichaPrincipal.php?modo=ficha&id_expediente=2

128479692

(s.f.). Brochure Camiones Caterpillar (773 -775 -777-785-789-793-795-797) (56 ton); Komatsu

(730E- 830E -930E -960E- HD465 - HD605- HD785); Liebherr (T282).

(s.f.). Brochure Palas Mod. Caterpillar (7495); P&H (2800-4100); Komatsu (PC 8000 - PC 5500).

Cementos Bio Bio S.A. (s.f.). Memorias 2010-2015.

Cochilco. (2007). Opotunidades de Negocios para Proveedores de Bienes, Insumos y Servicios

Mineros en Chile.

Cochilco. (2016). Actualizacion de la inversion en la mineria chilena -cartera de proyectos 2016 -

2025.

Coloma Álvarez, G. (2008). La Cal: ¡Es un reactivo químico! Santiago.

Compañía Electro Metaqlúrgica S.A. (s.f.). Memorias Anuales 2010-2015.

Editec S.A. (2014). Catastro de Equipamiento Minero 2013-2014. Santiago: Editec. S.A.

Moly_Cop. (Marzo de 2012). Presentación OneSteel Mining Consumables.

Sigdo Koppers S.A. (s.f.). Memorias 2014-2015.

Soprocal. (s.f.). Memorias 2010-2015.

Sopromin Tocopilla Ltda. (s.f.). Modificación DIA Planta de Cal. Obtenido de Servicio de Evaluación

Ambiental:

http://seia.sea.gob.cl/expediente/ficha/fichaPrincipal.php?modo=ficha&id_expediente=8

332747

Thompson Reuters. (2016). CheckPoint. Base de Datos Exportaciones e Importaciones.

Copper-mining critical supplies market analysis

48

Chilean Copper Commission

This work was developed in the

Research and Policy Planning Department (Dirección de Estudios y Políticas Públicas) by:

Ronald Monsalve

Mining Market Analyst

Jorge Cantallopts

Director of Research and Policy Planning (Estudios y Políticas Públicas)

August / 2016