Embed Size (px)

Citation preview

![Page 1: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/1.jpg)

Consumption-led Growth

Markus Brunnermeier Pierre-Olivier [email protected] [email protected]

Oleg [email protected]

University of HelsinkiHelsinki, November 2018

1 / 31

![Page 2: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/2.jpg)

Introduction

![Page 3: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/3.jpg)

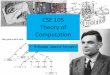

Motivation I

• Gourinchas and Jeanne (2013): the capital allocation puzzle

[15:40 3/10/2013 rdt004.tex] RESTUD: The Review of Economic Studies Page: 1485 1484–1515

GOURINCHAS & JEANNE THE ALLOCATION PUZZLE 1485

AGO

ARG

BEN

BGD

BOL

BRA

BWA

CHL

CHN

CIV

CMR

COG

COL

CRI CYPDOMECU

EGYETH

FJI

GAB

GHAGTM

HKG

HND

HTI

IDN IND

IRN

ISR

JAM

JOR KEN

LKA

MARMEX

MLI

MOZ

MUS

MWI

MYS

NER

NGA

NPL

PAKPAN

PER

PHLPNGPRYRWA

SEN

SGP

SLV

SYR

TGO

THA

TTO

TUN

TUR

TWN

TZA

UGA

URY

VEN

ZAF KOR

MDG

−10

−50

510

15C

apita

l Inf

low

s (p

erce

nt o

f GD

P)

−4 −2 0 2 4 6Productivity Growth (%)

Figure 1

Average productivity growth and average capital inflows between 1980 and 2000. 68 non-OECD countries

The allocation puzzle is illustrated by Figure 1, which plots the average growth rate of totalfactor productivity (TFP) against the average ratio of net capital inflows to GDP for 68 developingcountries over the period 1980–2000.2 Although the variables are averaged over two decades,there is substantial cross-country variation both in the direction and in the volume of net capitalinflows, with some countries receiving more than 10% of their GDP in capital inflows on average(Mozambique, Tanzania), whereas others export about 7% of their GDP in capital outflows(Taiwan). More strikingly, the correlation between the two variables is negative, the opposite ofthe theoretical prediction.3 To illustrate with two countries that are typical of this relationship (i.e.close to the regression line), Korea, a development success story with an average TFP growth of4.1% per year and an average annual investment rate of 34% between 1980 and 2000, receivedalmost no net capital inflows, whereas Madagascar, whose TFP fell by 1.5% a year and averageannual investment rate barely reached 3%, received 7% of its GDP in capital inflows each year,on average.

As we show in this article, the pattern observed in Figure 1 is just one illustration of arange of results that point in the same direction. Capital flows from rich to poor countries arenot only low (as argued by Lucas (1990)), but their allocation across developing countries isnegatively correlated or uncorrelated with the predictions of the standard textbook model. Thisis the “allocation puzzle”.

We provide a more detailed characterization of the allocation puzzle by looking at differentbreakdowns (decompositions) of capital flows. First, we delineate the respective roles ofinvestment and saving. We augment the neoclassical growth model with two “wedges”: onewedge that distorts investment decisions, and one wedge that distorts saving decisions. It is then

2. Net capital inflows are measured as the ratio of a country’s current account deficit over its GDP, averaged overthe period 1980–2000. The construction of the data is explained in more detail in Section 3.

3. The regression line on Figure 1 has a slope −0.72 (p-value of 0.1%).

at University of C

alifornia, Berkeley on D

ecember 9, 2013

http://restud.oxfordjournals.org/D

ownloaded from

Average productivity growth and capital inflows between 1980 and 2000 for 68 non-OECD countries.

• In this paper, we swap the axes of this plot: can international capital flows alterproductivity growth trajectories?

2 / 31

![Page 4: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/4.jpg)

Motivation I

• Gourinchas and Jeanne (2013): the capital allocation puzzle

[15:40 3/10/2013 rdt004.tex] RESTUD: The Review of Economic Studies Page: 1485 1484–1515

GOURINCHAS & JEANNE THE ALLOCATION PUZZLE 1485

AGO

ARG

BEN

BGD

BOL

BRA

BWA

CHL

CHN

CIV

CMR

COG

COL

CRI CYPDOMECU

EGYETH

FJI

GAB

GHAGTM

HKG

HND

HTI

IDN IND

IRN

ISR

JAM

JOR KEN

LKA

MARMEX

MLI

MOZ

MUS

MWI

MYS

NER

NGA

NPL

PAKPAN

PER

PHLPNGPRYRWA

SEN

SGP

SLV

SYR

TGO

THA

TTO

TUN

TUR

TWN

TZA

UGA

URY

VEN

ZAF KOR

MDG

−10

−50

510

15C

apita

l Inf

low

s (p

erce

nt o

f GD

P)

−4 −2 0 2 4 6Productivity Growth (%)

Figure 1

Average productivity growth and average capital inflows between 1980 and 2000. 68 non-OECD countries

The allocation puzzle is illustrated by Figure 1, which plots the average growth rate of totalfactor productivity (TFP) against the average ratio of net capital inflows to GDP for 68 developingcountries over the period 1980–2000.2 Although the variables are averaged over two decades,there is substantial cross-country variation both in the direction and in the volume of net capitalinflows, with some countries receiving more than 10% of their GDP in capital inflows on average(Mozambique, Tanzania), whereas others export about 7% of their GDP in capital outflows(Taiwan). More strikingly, the correlation between the two variables is negative, the opposite ofthe theoretical prediction.3 To illustrate with two countries that are typical of this relationship (i.e.close to the regression line), Korea, a development success story with an average TFP growth of4.1% per year and an average annual investment rate of 34% between 1980 and 2000, receivedalmost no net capital inflows, whereas Madagascar, whose TFP fell by 1.5% a year and averageannual investment rate barely reached 3%, received 7% of its GDP in capital inflows each year,on average.

As we show in this article, the pattern observed in Figure 1 is just one illustration of arange of results that point in the same direction. Capital flows from rich to poor countries arenot only low (as argued by Lucas (1990)), but their allocation across developing countries isnegatively correlated or uncorrelated with the predictions of the standard textbook model. Thisis the “allocation puzzle”.

We provide a more detailed characterization of the allocation puzzle by looking at differentbreakdowns (decompositions) of capital flows. First, we delineate the respective roles ofinvestment and saving. We augment the neoclassical growth model with two “wedges”: onewedge that distorts investment decisions, and one wedge that distorts saving decisions. It is then

2. Net capital inflows are measured as the ratio of a country’s current account deficit over its GDP, averaged overthe period 1980–2000. The construction of the data is explained in more detail in Section 3.

3. The regression line on Figure 1 has a slope −0.72 (p-value of 0.1%).

at University of C

alifornia, Berkeley on D

ecember 9, 2013

http://restud.oxfordjournals.org/D

ownloaded from

Average productivity growth and capital inflows between 1980 and 2000 for 68 non-OECD countries.

• In this paper, we swap the axes of this plot: can international capital flows alterproductivity growth trajectories?

2 / 31

![Page 5: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/5.jpg)

Motivation II

1. What is the relationship between openness and growth?— trade openness— financial openness

2. Is it possible to borrow like Argentina or Spain and grow like China?

(i) What is wrong with Spanish-style (consumption-led) growth?(ii) What is special about Chinese-style (export-led) growth?

• A model of endogenous convergence growth— to open the blackbox of productivity evolution under different openness regimes— a “neoclassical” (DRS) environment with endogenous innovation decisions by entrepreneurs— emphasis on the feedback from international borrowing into the pace and composition (T

vs NT) of convergence

3 / 31

![Page 6: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/6.jpg)

Motivation II

1. What is the relationship between openness and growth?— trade openness— financial openness

2. Is it possible to borrow like Argentina or Spain and grow like China?

(i) What is wrong with Spanish-style (consumption-led) growth?(ii) What is special about Chinese-style (export-led) growth?

• A model of endogenous convergence growth— to open the blackbox of productivity evolution under different openness regimes— a “neoclassical” (DRS) environment with endogenous innovation decisions by entrepreneurs— emphasis on the feedback from international borrowing into the pace and composition (T

vs NT) of convergence

3 / 31

![Page 7: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/7.jpg)

Motivation II

1. What is the relationship between openness and growth?— trade openness— financial openness

2. Is it possible to borrow like Argentina or Spain and grow like China?

(i) What is wrong with Spanish-style (consumption-led) growth?(ii) What is special about Chinese-style (export-led) growth?

• A model of endogenous convergence growth— to open the blackbox of productivity evolution under different openness regimes— a “neoclassical” (DRS) environment with endogenous innovation decisions by entrepreneurs— emphasis on the feedback from international borrowing into the pace and composition (T

vs NT) of convergence

3 / 31

![Page 8: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/8.jpg)

Empirical Motivation I

I

Figure 1: CA imbalances in the Euro Zone

4 / 31

![Page 9: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/9.jpg)

Empirical Motivation II

Figure 1: Sectoral reallocation in the Euro Zone (Piton, 2017)

4 / 31

![Page 10: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/10.jpg)

Main Insights

• Openness has two effects (on incentives for innovation):(i) change in relative market size(ii) increase in foreign competition and domestic cost of production, a price effect

• With balanced trade, it’s a wash: trade openness does not affect the pace and directionof productivity growth

• Trade deficits (a) unambiguously favor non-tradable sector and (b) tend to reduce paceof innovation

— reduced-form relationship between NX and sectoral growth— furthermore, NX/Y is a sufficient statistic— trade surpluses promote GDP growth

• Sudden stops in financial flows followed by both recessions and fast tradableproductivity growth take off

• Laissez-faire productivity growth is in general suboptimal— capital controls may improve upon market allocation

5 / 31

![Page 11: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/11.jpg)

Main Insights

• Openness has two effects (on incentives for innovation):(i) change in relative market size(ii) increase in foreign competition and domestic cost of production, a price effect

• With balanced trade, it’s a wash: trade openness does not affect the pace and directionof productivity growth

• Trade deficits (a) unambiguously favor non-tradable sector and (b) tend to reduce paceof innovation

— reduced-form relationship between NX and sectoral growth— furthermore, NX/Y is a sufficient statistic— trade surpluses promote GDP growth

• Sudden stops in financial flows followed by both recessions and fast tradableproductivity growth take off

• Laissez-faire productivity growth is in general suboptimal— capital controls may improve upon market allocation

5 / 31

![Page 12: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/12.jpg)

Main Insights

• Openness has two effects (on incentives for innovation):(i) change in relative market size(ii) increase in foreign competition and domestic cost of production, a price effect

• With balanced trade, it’s a wash: trade openness does not affect the pace and directionof productivity growth

• Trade deficits (a) unambiguously favor non-tradable sector and (b) tend to reduce paceof innovation

— reduced-form relationship between NX and sectoral growth— furthermore, NX/Y is a sufficient statistic— trade surpluses promote GDP growth

• Sudden stops in financial flows followed by both recessions and fast tradableproductivity growth take off

• Laissez-faire productivity growth is in general suboptimal— capital controls may improve upon market allocation

5 / 31

![Page 13: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/13.jpg)

Main Insights

• Openness has two effects (on incentives for innovation):(i) change in relative market size(ii) increase in foreign competition and domestic cost of production, a price effect

• With balanced trade, it’s a wash: trade openness does not affect the pace and directionof productivity growth

• Trade deficits (a) unambiguously favor non-tradable sector and (b) tend to reduce paceof innovation

— reduced-form relationship between NX and sectoral growth— furthermore, NX/Y is a sufficient statistic— trade surpluses promote GDP growth

• Sudden stops in financial flows followed by both recessions and fast tradableproductivity growth take off

• Laissez-faire productivity growth is in general suboptimal— capital controls may improve upon market allocation

5 / 31

![Page 14: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/14.jpg)

Main Insights

• Openness has two effects (on incentives for innovation):(i) change in relative market size(ii) increase in foreign competition and domestic cost of production, a price effect

• With balanced trade, it’s a wash: trade openness does not affect the pace and directionof productivity growth

• Trade deficits (a) unambiguously favor non-tradable sector and (b) tend to reduce paceof innovation

— reduced-form relationship between NX and sectoral growth— furthermore, NX/Y is a sufficient statistic— trade surpluses promote GDP growth

• Sudden stops in financial flows followed by both recessions and fast tradableproductivity growth take off

• Laissez-faire productivity growth is in general suboptimal— capital controls may improve upon market allocation

5 / 31

![Page 15: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/15.jpg)

Literature

• Neoclassical investment theory: Barro, Mankiw & Sala-i-Martin (1995)

• Learning-by-doing and dutch disease— Corden and Neary (1982), Krugman (1987), Young (1991), Benigno and Fornaro (2012, 2014)— Export-led growth: Rajan and Subramanian (2005), Rodrik (2008)

• Trade and growth— Rivera-Batiz and Romer (1991), Grossman and Helpman (1993), Ventura (1997), Acemoglu and Ventura

(2002), Parente and Prescott (2002)— Empirics: Frankel and Romer (1999), Ben-David (1993), Dollar and Kraay (2003)

• Financial flows and growth:— Aioke, Benigno and Kiyotaki (2009), Alfaro, Kalemli-Ozcan, and Volosovych (2008), Gopinath et al

(2017)

• Trade and growth with Frechet distributions and beyond— Kortum (1997), EK (2001, 2002), Klette and Kortum (2004)— Alvarez, Buera and Lucas (2017), Perla, Tonetti and Waugh (2015) . . .

6 / 31

![Page 16: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/16.jpg)

Model Setup

![Page 17: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/17.jpg)

Model Setup

• Real small open economy in continuous time— exogenous world interest rate r∗ in terms of world good

• Two sector economy:— γ tradable (exportable) and— 1− γ non-tradable (non-exportable)

and symmetric in all other respects

• Rest of the world (ROW) in steady state:

W ∗ = A∗T = A∗N = A∗ and P∗F = P∗N = P∗ = 1

• We study convergence growth trajectories:

AT (0),AN(0) < A ≤ A∗

• Growth results from new product creation by profit-maximizing entrepreneurs

7 / 31

![Page 18: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/18.jpg)

Model Setup

• Real small open economy in continuous time— exogenous world interest rate r∗ in terms of world good

• Two sector economy:— γ tradable (exportable) and— 1− γ non-tradable (non-exportable)

and symmetric in all other respects

• Rest of the world (ROW) in steady state:

W ∗ = A∗T = A∗N = A∗ and P∗F = P∗N = P∗ = 1

• We study convergence growth trajectories:

AT (0),AN(0) < A ≤ A∗

• Growth results from new product creation by profit-maximizing entrepreneurs7 / 31

![Page 19: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/19.jpg)

Households

• Representative household:

max{C(t),L(t)}

∫ ∞0

e−ϑtU(t)dt, U = 11−σC

1−σ − 11+ϕL

1+ϕ

s.t. B = r∗B + WL + Π︸ ︷︷ ︸=GDP

− PC︸︷︷︸=Y

• Static market clearing (goods and labor):

WL = Y + NX ,

CσLϕ = W /P

8 / 31

![Page 20: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/20.jpg)

Households

• Representative household:

max{C(t),L(t)}

∫ ∞0

e−ϑtU(t)dt, U = 11−σC

1−σ − 11+ϕL

1+ϕ

s.t. B = r∗B + WL + Π︸ ︷︷ ︸=GDP

− PC︸︷︷︸=Y

• Static market clearing (goods and labor):

WL = Y + NX ,

CσLϕ = W /P

8 / 31

![Page 21: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/21.jpg)

Demand

• Two sectors:Y = PC = γPTCT + (1− γ)PNCN

where

C = CγTC

1−γN and CT =

[κ

1ρC

ρ−1ρ

F + (1−κ)1ρC

ρ−1ρ

H

] ρρ−1

, ρ > 1

• Aggregators of individual varieties:

CH =

[1

γ

∫ ΛT

0

CH(i)ρ−1ρ di

] ρρ−1

and CN =

[1

1− γ

∫ ΛN

0

CN(i)ρ−1ρ di

] ρρ−1

9 / 31

![Page 22: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/22.jpg)

Exports and Imports

• Tradable expenditure:

γPTCT =

∫ ΛT

0

PH(i)CH(i)di + γPFCF

• Aggregate imports:

X ∗ = γPFCF = γκ

(PF

PT

)1−ρ

Y , PF = τP∗F = τ

• Aggregate exports:X = γP∗HC

∗H = γκ(τPH)1−ρY ∗

• Net exports:

NX = X − X ∗ = γκτ 1−ρ[P1−ρH Y ∗ − Pρ−1

T Y]

10 / 31

![Page 23: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/23.jpg)

Technology and Revenues

• Technology of product i ∈ [0,ΛJ ] in sector J ∈ {T ,N}:

YJ(i) = AJ(i)LJ(i)

• Marginal cost pricing if technology is non-excludable:

PH = W /AT where AT =[

1γ

∫ ΛT

0AT (i)ρ−1di

] 1ρ−1

• Revenues:

RN(i) = PN(i)CN(i) =

(PN(i)

PN

)1−ρ

RN ,

RT (i) = PH(i)CH(i) + P∗H(i)C∗H(i) =

(PH(i)

PH

)1−ρ

RT

where RN = Y and

RT = (1− κ)

(PH

PT

)1−ρ

Y + κ(τPH)1−ρY ∗ = Y

[1 +

NX

γY

]

11 / 31

![Page 24: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/24.jpg)

Technology and Revenues

• Technology of product i ∈ [0,ΛJ ] in sector J ∈ {T ,N}:

YJ(i) = AJ(i)LJ(i)

• Marginal cost pricing if technology is non-excludable:

PH = W /AT where AT =[

1γ

∫ ΛT

0AT (i)ρ−1di

] 1ρ−1

• Revenues:

RN(i) = PN(i)CN(i) =

(PN(i)

PN

)1−ρ

RN ,

RT (i) = PH(i)CH(i) + P∗H(i)C∗H(i) =

(PH(i)

PH

)1−ρ

RT

where RN = Y and

RT = (1− κ)

(PH

PT

)1−ρ

Y + κ(τPH)1−ρY ∗ = Y

[1 +

NX

γY

]

11 / 31

![Page 25: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/25.jpg)

Technology and Revenues

• Technology of product i ∈ [0,ΛJ ] in sector J ∈ {T ,N}:

YJ(i) = AJ(i)LJ(i)

• Marginal cost pricing if technology is non-excludable:

PH = W /AT where AT =[

1γ

∫ ΛT

0AT (i)ρ−1di

] 1ρ−1

• Revenues:

RN(i) = PN(i)CN(i) =

(PN(i)

PN

)1−ρ

RN ,

RT (i) = PH(i)CH(i) + P∗H(i)C∗H(i) =

(PH(i)

PH

)1−ρ

RT

where RN = Y and

RT = (1− κ)

(PH

PT

)1−ρ

Y + κ(τPH)1−ρY ∗ = Y

[1 +

NX

γY

]11 / 31

![Page 26: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/26.jpg)

Technology Draws

• An entrepreneur has n� 1 possible ideas (projects):

ZJ(`)(`)iid∼ Frechet(z , θ), ` = 1..n, θ > ρ− 1

• A fraction γ of ideas are tradable, J(`) = T

• An entrepreneur can adopt only one project

• The technology is privately owned for one period

• Period profits:

ΠT (`) =1

ρ

(ρ

ρ− 1

W

ZT (`)

1

PH

)1−ρ

RT

= %RT

Aρ−1T

ZT (`)ρ−1

ΠN(`) =1

ρ

(ρ

ρ− 1

W

ZN(`)

1

PN

)1−ρ

RN

= %RN

Aρ−1N

ZN(`)ρ−1

12 / 31

![Page 27: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/27.jpg)

Technology Draws

• An entrepreneur has n� 1 possible ideas (projects):

ZJ(`)(`)iid∼ Frechet(z , θ), ` = 1..n, θ > ρ− 1

• A fraction γ of ideas are tradable, J(`) = T

• An entrepreneur can adopt only one project

• The technology is privately owned for one period

• Period profits:

ΠT (`) =1

ρ

(ρ

ρ− 1

W

ZT (`)

1

PH

)1−ρ

RT

= %RT

Aρ−1T

ZT (`)ρ−1

ΠN(`) =1

ρ

(ρ

ρ− 1

W

ZN(`)

1

PN

)1−ρ

RN

= %RN

Aρ−1N

ZN(`)ρ−1

12 / 31

![Page 28: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/28.jpg)

Technology Draws

• An entrepreneur has n� 1 possible ideas (projects):

ZJ(`)(`)iid∼ Frechet(z , θ), ` = 1..n, θ > ρ− 1

• A fraction γ of ideas are tradable, J(`) = T

• An entrepreneur can adopt only one project

• The technology is privately owned for one period

• Period profits:

ΠT (`) =1

ρ

(ρ

ρ− 1

W

ZT (`)

1

PH

)1−ρ

RT

= %RT

Aρ−1T

ZT (`)ρ−1

ΠN(`) =1

ρ

(ρ

ρ− 1

W

ZN(`)

1

PN

)1−ρ

RN

= %RN

Aρ−1N

ZN(`)ρ−1

12 / 31

![Page 29: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/29.jpg)

Technology Draws

• An entrepreneur has n� 1 possible ideas (projects):

ZJ(`)(`)iid∼ Frechet(z , θ), ` = 1..n, θ > ρ− 1

• A fraction γ of ideas are tradable, J(`) = T

• An entrepreneur can adopt only one project

• The technology is privately owned for one period

• Period profits:

ΠT (`) =1

ρ

(ρ

ρ− 1

W

ZT (`)

1

PH

)1−ρ

RT = %RT

Aρ−1T

ZT (`)ρ−1

ΠN(`) =1

ρ

(ρ

ρ− 1

W

ZN(`)

1

PN

)1−ρ

RN = %RN

Aρ−1N

ZN(`)ρ−1

12 / 31

![Page 30: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/30.jpg)

Technology Adoption

• Project choice:ˆ = arg max

`=1..nΠJ(`)(`)

and we define (ZT , ZN , Z ) and (ΠT , ΠN , Π)

• Lemma 1 (i) The probability to adopt a tradable project:

πT ≡ P{ΠT ≥ ΠN} =γ · χ

θρ−1

γ · χθρ−1 + 1− γ

, χ ≡ ()ρ−1 RT

RN.

(ii) The productivity conditional on adoption:

E{Zρ−1T

∣∣ ΠT ≥ ΠN

}=

(πTγ

)ν−1

A∗ρ−1,

where A∗ ≡ EZ = (nz)1/θΓ(ν)1ρ−1 and ν ≡ 1− ρ−1

θ ∈ (0, 1).

13 / 31

![Page 31: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/31.jpg)

Technology Adoption

• Project choice:ˆ = arg max

`=1..nΠJ(`)(`)

and we define (ZT , ZN , Z ) and (ΠT , ΠN , Π)

• Lemma 1 (i) The probability to adopt a tradable project:

πT ≡ P{ΠT ≥ ΠN} =γ · χ

θρ−1

γ · χθρ−1 + 1− γ

, χ ≡(PH

PN

)ρ−1RT

RN.

(ii) The productivity conditional on adoption:

E{Zρ−1T

∣∣ ΠT ≥ ΠN

}=

(πTγ

)ν−1

A∗ρ−1,

where A∗ ≡ EZ = (nz)1/θΓ(ν)1ρ−1 and ν ≡ 1− ρ−1

θ ∈ (0, 1).

13 / 31

![Page 32: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/32.jpg)

Technology Adoption

• Project choice:ˆ = arg max

`=1..nΠJ(`)(`)

and we define (ZT , ZN , Z ) and (ΠT , ΠN , Π)

• Lemma 1 (i) The probability to adopt a tradable project:

πT ≡ P{ΠT ≥ ΠN} =γ · χ

θρ−1

γ · χθρ−1 + 1− γ

, χ ≡(AN

AT

)ρ−1RT

RN.

(ii) The productivity conditional on adoption:

E{Zρ−1T

∣∣ ΠT ≥ ΠN

}=

(πTγ

)ν−1

A∗ρ−1,

where A∗ ≡ EZ = (nz)1/θΓ(ν)1ρ−1 and ν ≡ 1− ρ−1

θ ∈ (0, 1).

13 / 31

![Page 33: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/33.jpg)

Technology Adoption

• Project choice:ˆ = arg max

`=1..nΠJ(`)(`)

and we define (ZT , ZN , Z ) and (ΠT , ΠN , Π)

• Lemma 1 (i) The probability to adopt a tradable project:

πT ≡ P{ΠT ≥ ΠN} =γ · χ

θρ−1

γ · χθρ−1 + 1− γ

, χ ≡(AN

AT

)ρ−1RT

RN.

(ii) The productivity conditional on adoption:

E{Zρ−1T

∣∣ ΠT ≥ ΠN

}=

(πTγ

)ν−1

A∗ρ−1,

where A∗ ≡ EZ = (nz)1/θΓ(ν)1ρ−1 and ν ≡ 1− ρ−1

θ ∈ (0, 1).13 / 31

![Page 34: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/34.jpg)

Productivity Dynamics

• λ is the innovation rate and δ is the rate at which technologies become obsolete:

ΛT = λπT − δΛT

• Assume λ is country-specific and λ ≤ δ

• Lemma 2 The sectoral productivity dynamics is given by:

AT

AT=

δ

ρ− 1

[(A

AT

)ρ−1(πTγ

)ν− 1

]where A ≡ A∗

(λ

δ

) 1ρ−1

.

14 / 31

![Page 35: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/35.jpg)

Productivity Dynamics

• λ is the innovation rate and δ is the rate at which technologies become obsolete:

ΛT = λπT − δΛT

• Assume λ is country-specific and λ ≤ δ

• Lemma 2 The sectoral productivity dynamics is given by:

AT

AT=

δ

ρ− 1

[(A

AT

)ρ−1(πTγ

)ν− 1

]where A ≡ A∗

(λ

δ

) 1ρ−1

.

14 / 31

![Page 36: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/36.jpg)

Summary

AT (t)

AT (t)=

1

ρ− 1

[λ

(A∗

AT (t)

)ρ−1(πT (t)

γ

)ν− δ

],

πT (t)

1− πT (t)=

γ

1− γχ(t)

θρ−1 ,

χ =

(PH

PN

)ρ−1RT

RN=

(AN

AT

)ρ−1 [1 +

NX

γY

],

B(0) +

∫ ∞0

e−rtNX (t) = 0.

15 / 31

![Page 37: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/37.jpg)

Closed Economy

![Page 38: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/38.jpg)

Closed Economy, κ ≡ 0

• In closed economy RT = RN = Y , and therefore:

χ =

(PH

PN

)ρ−1

=

(AN

AT

)ρ−1

• The project choice is, thus:

πT (t)

1− πT (t)=

γ

1− γ

(AN(t)

AT (t)

)θ

• Proposition 1 (i) Starting from AT (0) = AN(0), equilibrium project choice in the closedeconomy is πT (t) ≡ γ,

AT (t) =[e−δtAT (0)ρ−1 +

(1−e−δt

)Aρ−1

] 1ρ−1 and ΛT = γ

λ

δ.

(ii) Equilibrium allocation C = w1+ϕσ+ϕ , L = w

1−σσ+ϕ , w = A.

(iii) Efficiency: . . .

16 / 31

![Page 39: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/39.jpg)

Closed Economy, κ ≡ 0

• In closed economy RT = RN = Y , and therefore:

χ =

(PH

PN

)ρ−1

=

(AN

AT

)ρ−1

• The project choice is, thus:

πT (t)

1− πT (t)=

γ

1− γ

(AN(t)

AT (t)

)θ

• Proposition 1 (i) Starting from AT (0) = AN(0), equilibrium project choice in the closedeconomy is πT (t) ≡ γ,

AT (t) =[e−δtAT (0)ρ−1 +

(1−e−δt

)Aρ−1

] 1ρ−1 and ΛT = γ

λ

δ.

(ii) Equilibrium allocation C = w1+ϕσ+ϕ , L = w

1−σσ+ϕ , w = A.

(iii) Efficiency: . . .

16 / 31

![Page 40: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/40.jpg)

Balanced Trade

![Page 41: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/41.jpg)

Balanced Trade

• Consider open economy with κ > 0 and τ ≥ 1

• Lemma 3 (i) The relative revenue shifter is given by:

RT

RN= (1− κ)

(PH

PT

)1−ρ

+ κ(τPH)1−ρY∗

Y= 1 +

NX

γY.

(ii) Under balanced trade, χ = (AN/AT )ρ−1, and hence πT (t) and (AT (t),AN(t)) followthe same path as in autarky.

• Equilibrium allocation is nonetheless different from autarkic:

w = C = A ·(

1

τ 2ρ−1

A∗

AT

) κγ1+(2−κ)(ρ−1)

• Laisser-faire productivity dynamics is suboptimal.The planner would choose πT (t) < γ for all t ≥ 0.

17 / 31

![Page 42: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/42.jpg)

Balanced Trade

• Consider open economy with κ > 0 and τ ≥ 1

• Lemma 3 (i) The relative revenue shifter is given by:

RT

RN= (1− κ)

(PH

PT

)1−ρ

+ κ(τPH)1−ρY∗

Y= 1 +

NX

γY.

(ii) Under balanced trade, χ = (AN/AT )ρ−1, and hence πT (t) and (AT (t),AN(t)) followthe same path as in autarky.

• Equilibrium allocation is nonetheless different from autarkic:

w = C = A ·(

1

τ 2ρ−1

A∗

AT

) κγ1+(2−κ)(ρ−1)

• Laisser-faire productivity dynamics is suboptimal.The planner would choose πT (t) < γ for all t ≥ 0.

17 / 31

![Page 43: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/43.jpg)

Balanced Trade

• Consider open economy with κ > 0 and τ ≥ 1

• Lemma 3 (i) The relative revenue shifter is given by:

RT

RN= (1− κ)

(PH

PT

)1−ρ

+ κ(τPH)1−ρY∗

Y= 1 +

NX

γY.

(ii) Under balanced trade, χ = (AN/AT )ρ−1, and hence πT (t) and (AT (t),AN(t)) followthe same path as in autarky.

• Equilibrium allocation is nonetheless different from autarkic:

w = C = A ·(

1

τ 2ρ−1

A∗

AT

) κγ1+(2−κ)(ρ−1)

• Laisser-faire productivity dynamics is suboptimal.The planner would choose πT (t) < γ for all t ≥ 0.

17 / 31

![Page 44: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/44.jpg)

Open Economy

![Page 45: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/45.jpg)

Financial Openness

• With open current account:

πT1− πT

=γ

1− γ

(AN

AT

)θ [1 +

NX

γY

] θρ−1

• Lemma 4 NX (t)<0 and AT (t)≥AN(t) ⇒ AT (t)< AN(t).

• Proposition 5 In st.st. with NX =−r∗B > 0: AT > A > AN .

• Proposition 6 Starting from AT (0) = AN(0) < A, there exist two cutoffs 0 < t1 < t2 <∞:• NX (t) < 0 for t ∈ [0, t1) and NX (t) > 0 for t > t1, and• AT (t) < AN(t) for t ∈ (0, t2) and AT (t) > AN(t) for t > t2.

At t = t2, AT (t) = AN(t) = A(t) < Aa(t).

18 / 31

![Page 46: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/46.jpg)

Financial Openness

• With open current account:

πT1− πT

=γ

1− γ

(AN

AT

)θ [1 +

NX

γY

] θρ−1

• Lemma 4 NX (t)<0 and AT (t)≥AN(t) ⇒ AT (t)< AN(t).

• Proposition 5 In st.st. with NX =−r∗B > 0: AT > A > AN .

• Proposition 6 Starting from AT (0) = AN(0) < A, there exist two cutoffs 0 < t1 < t2 <∞:• NX (t) < 0 for t ∈ [0, t1) and NX (t) > 0 for t > t1, and• AT (t) < AN(t) for t ∈ (0, t2) and AT (t) > AN(t) for t > t2.

At t = t2, AT (t) = AN(t) = A(t) < Aa(t).

18 / 31

![Page 47: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/47.jpg)

Convergence Path

0 50 100 150 200 250 300

0

0.3

0.7

1

Figure 2: Productivity convergence in closed and open economies

19 / 31

![Page 48: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/48.jpg)

Impact of Openness

0 50 100 150

-1

-0.5

0

0.5

0 50 100 150

0

0.2

0.4

0.6

0.8

• Two effects of openness:1. Relative size of the market: Y /Y ∗

2. Competition: PT/PH < 1

1 +NX

γY=

(PH

PT

)1−ρ

·

[(1− κ) + κ

(τ

PH

)1−ρ

=X/X∗︷ ︸︸ ︷P1−ρH Y ∗

Pρ−1T Y

]20 / 31

![Page 49: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/49.jpg)

Endogenous Innovation

![Page 50: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/50.jpg)

Endogenous Innovation Rate

• Entrepreneurship decision as in Lucas (1978) if EΠ ≥ φW :

λ = Φ

(EΠ

W

)and EΠ

W=%RN/W

Aρ−1N

Emax{χZρ−1

T , Zρ−1N

}

• Lemma 5 EΠ

W= % ·

(A∗

A· A

Aθ

)ρ−1

·Ψ(

1 +NX

Y

)

• Proposition 8 (i) λ is increasing in A∗/A and in A/Aθ ≥ 1 .(ii) λ increases with trade openness iff σ < 1 and ϕ <∞.

(iii) When σ = 1, Ψ ≈ 1 +[ (

AN

AT

)1−γ− ϕ

1+ϕ

]NXY ,

and λ increases with NX when AN ≥ AT .

• Endogenous non-tradable tilt reinforces the negative effect of trade deficits oninnovation rate

• Induced NX > 0 with policy if the goal is max growth rate

21 / 31

![Page 51: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/51.jpg)

Endogenous Innovation Rate

• Entrepreneurship decision as in Lucas (1978) if EΠ ≥ φW :

λ = Φ

(EΠ

W

)and EΠ

W=%RN/W

Aρ−1N

Emax{χZρ−1

T , Zρ−1N

}

• Lemma 5 EΠ

W= % ·

(A∗

A· A

Aθ

)ρ−1

·Ψ(

1 +NX

Y

)• Proposition 8 (i) λ is increasing in A∗/A and in A/Aθ ≥ 1 .

(ii) λ increases with trade openness iff σ < 1 and ϕ <∞.

(iii) When σ = 1, Ψ ≈ 1 +[ (

AN

AT

)1−γ− ϕ

1+ϕ

]NXY ,

and λ increases with NX when AN ≥ AT .

• Endogenous non-tradable tilt reinforces the negative effect of trade deficits oninnovation rate

• Induced NX > 0 with policy if the goal is max growth rate

21 / 31

![Page 52: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/52.jpg)

Endogenous Innovation Rate

• Entrepreneurship decision as in Lucas (1978) if EΠ ≥ φW :

λ = Φ

(EΠ

W

)and EΠ

W=%RN/W

Aρ−1N

Emax{χZρ−1

T , Zρ−1N

}

• Lemma 5 EΠ

W= % ·

(A∗

A· A

Aθ

)ρ−1

·Ψ(

1 +NX

Y

)• Proposition 8 (i) λ is increasing in A∗/A and in A/Aθ ≥ 1 .

(ii) λ increases with trade openness iff σ < 1 and ϕ <∞.

(iii) When σ = 1, Ψ ≈ 1 +[ (

AN

AT

)1−γ− ϕ

1+ϕ

]NXY ,

and λ increases with NX when AN ≥ AT .

• Endogenous non-tradable tilt reinforces the negative effect of trade deficits oninnovation rate

• Induced NX > 0 with policy if the goal is max growth rate21 / 31

![Page 53: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/53.jpg)

Empirical Implications

![Page 54: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/54.jpg)

Empirical Implications

• Reduced-form relationship between NX and sectoral growth:

AT (t)

AT (t)− AN(t)

AN(t)= g0

[−(ρ− 1) (1 + µ) log

AT (t)

AN(t)+µ

γ

NX (t)

Y (0)

],

with g0 ≡ δρ−1

(λδA∗

A0

)ρ−1

, which is also the base growth rate

— holds whether NX 6= 0 are market outcomes or policy-induced— i.e., applies equally for NX < 0 in Spain and NX > 0 in China

• NX/Y is a sufficient statistic for the feedback effect from equilibrium allocation tosectoral productivity growth

22 / 31

![Page 55: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/55.jpg)

Preliminary empirical results

• KLEMS panel of sector-country productivity growth(17 OECD countries, 33 ∼3-digit sectors, 2001–2007 change)

• Empirical specification:∆ logAks = dk + ds + b · logA0

ks + c · Λs · nxk + εks

— ∆ logAks is productivity growth in sector s , country k

— Λs is median sector-level home share across countries

Dep. var: VA/L RVA/L KLEMS VA/L RVA/L∆ logAks (1) (2) (3) (4) (5)

Λs · nxk−0.36∗∗∗ −0.41∗∗ 0.07 −0.20 −0.00

(0.10) (0.15) (0.20) (0.14) (0.14)

logA0ks

−4.75∗∗ −4.43∗∗∗ −0.74 −2.17∗∗ −3.40∗∗∗

(1.76) (0.98) (0.72) (0.73) (0.56)

R2 0.68 0.57 0.33 0.54 0.59Observations 532 530 399 399 399— 6% trade deficit reduces relative sectoral productivity growth by 1% across tradability quartiles (25th–75th)

23 / 31

![Page 56: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/56.jpg)

Preliminary empirical results

• KLEMS panel of sector-country productivity growth(17 OECD countries, 33 ∼3-digit sectors, 2001–2007 change)

• Empirical specification:∆ logAks = dk + ds + b · logA0

ks + c · Λs · nxk + εks

Dep. var: VA/L RVA/L KLEMS VA/L RVA/L∆ logAks (1) (2) (3) (4) (5)

Λs · nxk−0.36∗∗∗ −0.41∗∗ 0.07 −0.20 −0.00

(0.10) (0.15) (0.20) (0.14) (0.14)

logA0ks

−4.75∗∗ −4.43∗∗∗ −0.74 −2.17∗∗ −3.40∗∗∗

(1.76) (0.98) (0.72) (0.73) (0.56)

R2 0.68 0.57 0.33 0.54 0.59Observations 532 530 399 399 399— 6% trade deficit reduces relative sectoral productivity growth by 1% across tradability quartiles (25th–75th)

23 / 31

![Page 57: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/57.jpg)

Unit Labor Costs

• Two ULC measures: w/A and W /AT

— move together holding τ constant

• Autarky (assume σ = 1):w a(t) = C a(t) = A(t)

• Balanced trade:

wb(t) = C b(t) = A(t)

(A∗

AT (t)

) κγ1+(2−κ)(ρ−1)

> A(t)

• Open financial account:wb(0) < w(0) < C (0)

• ULC increase on impact and gradually fall along the convergence path

24 / 31

![Page 58: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/58.jpg)

Applications

![Page 59: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/59.jpg)

Application

1. Physical capital and financial frictions

2. Misallocation and growth policy

3. Rollover crisis

• Sudden stop in capital flows during transition triggers a reversal in trade deficits and arecession in non-tradable sector

• Rapid take off in tradable productivity growth, provided labor market can flexibly adjust bya sharp decline in wages

25 / 31

![Page 60: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/60.jpg)

Rollover Crisis

0 5 10 15 20 25 30 35 40 45 50

0

0.2

0.4

0.6

0.8

1

1.2

26 / 31

![Page 61: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/61.jpg)

Conclusion

![Page 62: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/62.jpg)

Conclusion

• Standard endogenous growth forces have a robust implication for the relationshipbetween trade deficits and:

1. non-tradable tilt of innovation2. overall lower speed of convergence growth

• Countries that borrow along the convergence growth trajectory are likely toexperience asymmetric and slower convergence

— lagging tradable productivity— high unit labor costs and depressed innovation rate— particularly vulnerable to rollover crisis along such trajectories

• Countries that are concerned with GDP growth rather than welfare might find itoptimal to subsidize exports

27 / 31

![Page 63: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/63.jpg)

Appendix

![Page 64: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/64.jpg)

Price Indexes

• Average sectoral prices:

PH =

[1

γ

∫ ΛT

0

PH(i)1−ρdi

] 11−ρ

and PN =

[1

1− γ

∫ ΛN

0

PN(i)1−ρdi

] 11−ρ

• Aggregate price indexes:

P = PγTP1−γN where PT =

[κP1−ρ

F + (1− κ)P1−ρH

] 11−ρ

• Equilibrium sectoral prices:

PH =W

AT, PN =

W

ANand PF = τ

• Real wage rate:

w =W

P= A

[1− κ+ κ

(WτAT

)ρ−1] γρ−1

, A ≡ AγTA1−γN

28 / 31

![Page 65: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/65.jpg)

Solution for NX

• Equilibrium system:

C = w1+ϕσ+ϕ

[1 +

NX

Y

]− ϕσ+ϕ

where w = A

(W

τAT

)κγand

NX

Y=

γκ(WτAT

)ρ−κγ[τ 1−2ρA

∗ 1+ϕσ+ϕ

C

A

AT−(

W

τAT

)(1−κγ)+(2−κ)(ρ−1)]

29 / 31

![Page 66: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/66.jpg)

Efficiency in Closed Economy

• Proposition (i) If AT (0) = AN(0), then π∗T (t) = γ and AT (t) = AN(t) for all t maximizes A(t) for all t . (ii) If

AN(t) > AT (t) at some t , then π∗T (t) ∈

(γ, πT (t)

), and laissez-faire dynamics with πT (t) is suboptimal.

• Optimal policy satisfies (for J ∈ {T ,N}):(π∗T

1− π∗T

1− γγ

)1−ν

=ξT

ξN

(AN

AT

)ρ−1

,

where bJ(t)ξT (t)− ξJ(t) = aJ(t),

and aJ(t) ≡(AJ(t)

A(t)

)η−1

A(t)ζ , bJ(t) ≡ ϑ+ δ

(A

AJ(t)

)ρ−1 (πJ(t)

γJ

)ν

• bJ(t) plays the role of discount rate and aJ(t) is the flow benefit

• ξT /ξN = RT /RN in the limit of ϑ→∞ (perfect impatience)Otherwise, ξT /ξT ∈ (1,RT /RN)

• Patents with finite time-varying duration can decentralize π∗T (t) back to slides

30 / 31

![Page 67: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/67.jpg)

Comparison with Learning-by-Doing

• General learning-by-doing formulation:

YT (t) = F(AT (t), LT (t)

),

AT (t) = G(AT (t),AN(t), LT (t), LN(t)

)

• Mapping of the baseline model into learning-by-doing:

F (AT , LT ) = AL,

G (AT ,AN , LT , LN) = G(AT , πT (AT ,AN , LT , LN)

),

G (AT , πT ) =δ

ρ− 1

[(A

AT

)ρ−1(πTγ

)ν− 1

],

πT1− πT

1− γγ

=

(AN

AT

)θ (RT

RN

) θρ−1

and RT

RN=

LTLN

31 / 31

![Page 68: Consumption-led Growth - Princeton University · Motivation I Gourinchas and Jeanne (2013): the capital allocation puzzle [15:40 3/10/2013 rdt004.tex] RESTUD:The Review of Economic](https://reader035.pdfslide.us/reader035/viewer/2022070723/5f01eca77e708231d401b554/html5/thumbnails/68.jpg)

Comparison with Learning-by-Doing

• General learning-by-doing formulation:

YT (t) = F(AT (t), LT (t)

),

AT (t) = G(AT (t),AN(t), LT (t), LN(t)

)

• Mapping of the baseline model into learning-by-doing:

F (AT , LT ) = AL,

G (AT ,AN , LT , LN) = G(AT , πT (AT ,AN , LT , LN)

),

G (AT , πT ) =δ

ρ− 1

[(A

AT

)ρ−1(πTγ

)ν− 1

],

πT1− πT

1− γγ

=

(AN

AT

)θ (RT

RN

) θρ−1

and RT

RN=

LTLN

31 / 31