Embed Size (px)

Citation preview

1 )

2l

3)

4l

5)

6)

Consultant Testimony/Presentation Points & Other Data On PPT lssues(through March 20, 2006)

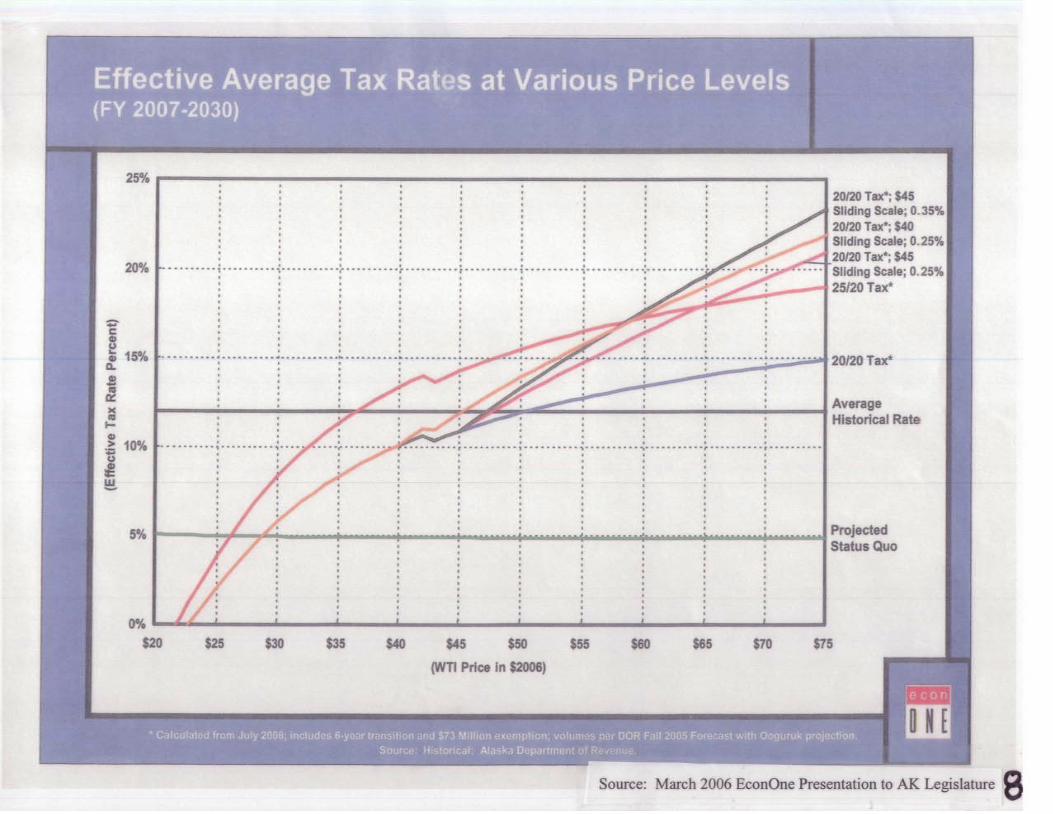

Statements that an oil tax rate of 25o/o, and greater at higher prices, would not deter longterm Investments, and would maximize long term state revenue. The differencebetween a 20% and 25o/o rate, at current prices, is roughly $0OO - $700 million in staterevenue. See attached testimony from consultants Daniel Johnston, Dr. Tony Finizza,and Barry Pulliam (p. 1-2). Also, Dr. Pedro Van Meurs February Testimony (p. 2).

A 20o/o and 25o/o PPT rate, and the Status Quo, all provide a tax rate lower (and atcertain prices much lower) than the world average goverment take of 670/o - 70%. Seeattached testimony from Johnston; Econ One Charts (p. 3-5).

lmplementing the bill as of January 1, 2006 (as originally proposed by the Governorand Van Meurs, and done with the 1989 ELF revisions) would not adversely impactinvestment decisions, and would raise significant additional revenue for the state. At a25% tax rate, moving the implementation date to July 1 will cost the state approximately$600 - $700 million. See attached testimony of Van Meurs (p.6).

A higher rate for more profitable, existing North Slope fields would be justified. Seeattached Johnston testimony (p.7).

Without a minimum tax, a 20% PPT would provide no production tax revenue at$23lbarrel, and less revenue than current law at $28lbarrel. A25o/o PPT would provideno production tax revenue at $2Zlbarrel, and less than current law at $26lbarrel. Seeattached Econ One projection (p.B). Johnston recommends the state consider imposinga minimum tax so the production tax does not fall to 0%. Johnston testimony attached(p.e).

Conoco has raised questions about its profitability in Alaska. According to ConocoAnnual Reports, the company's profits and profit margins in Alaska have been asfollows: 2005: $2.SS bill ion (43.1o/o);2004: $1.83 bill ion (41.3o/o);2003:1.45 biil ion(40.5o/o); 2002: $870 million (29o/o); and 2001; $866 million (28.7o/o). Conoco AnnualReport excerpts attached (p. 10-1 1).

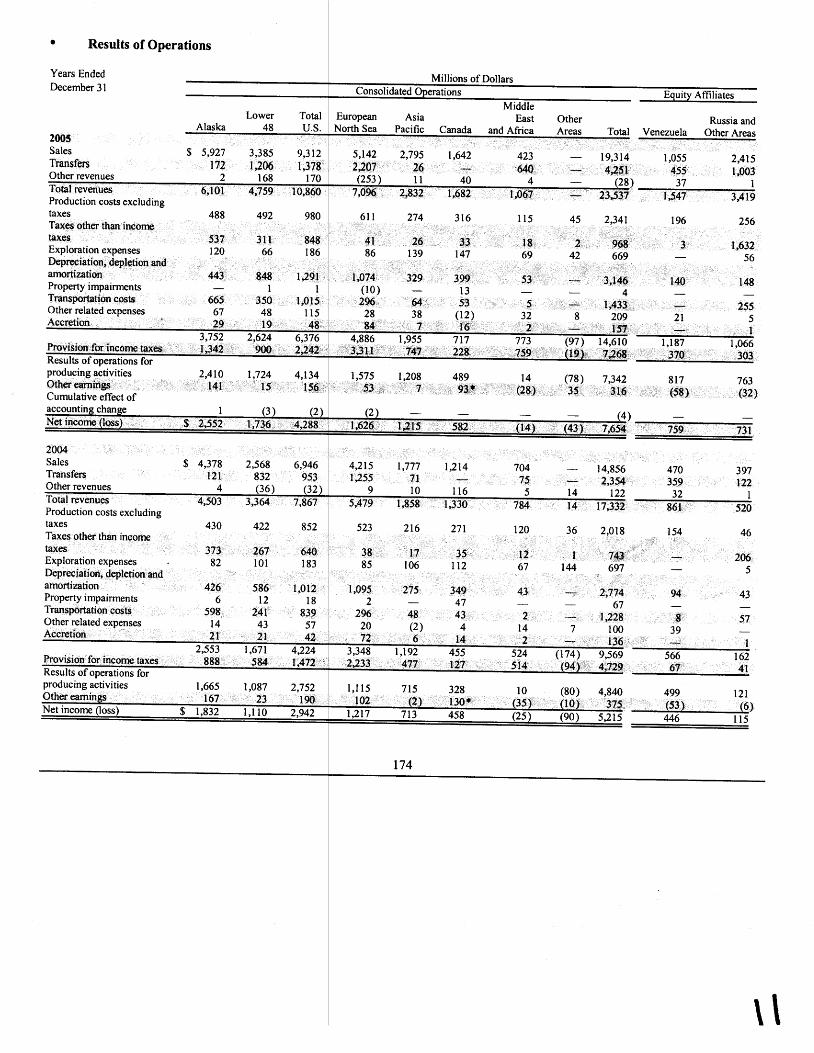

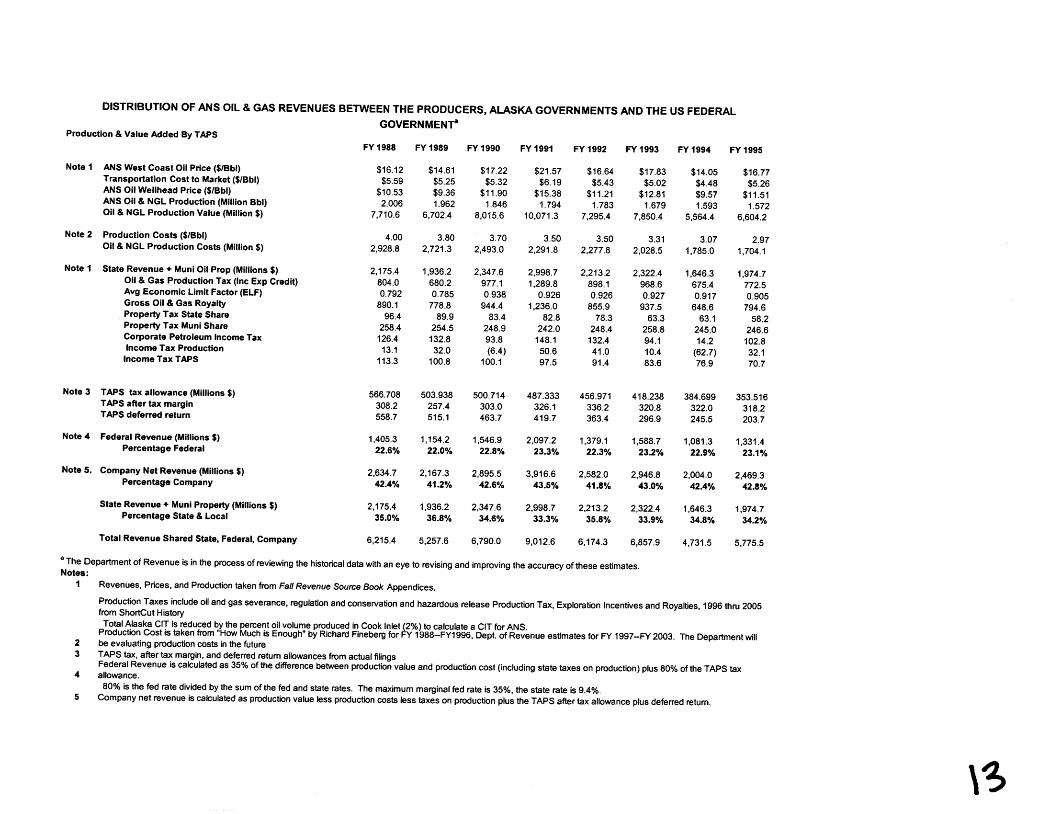

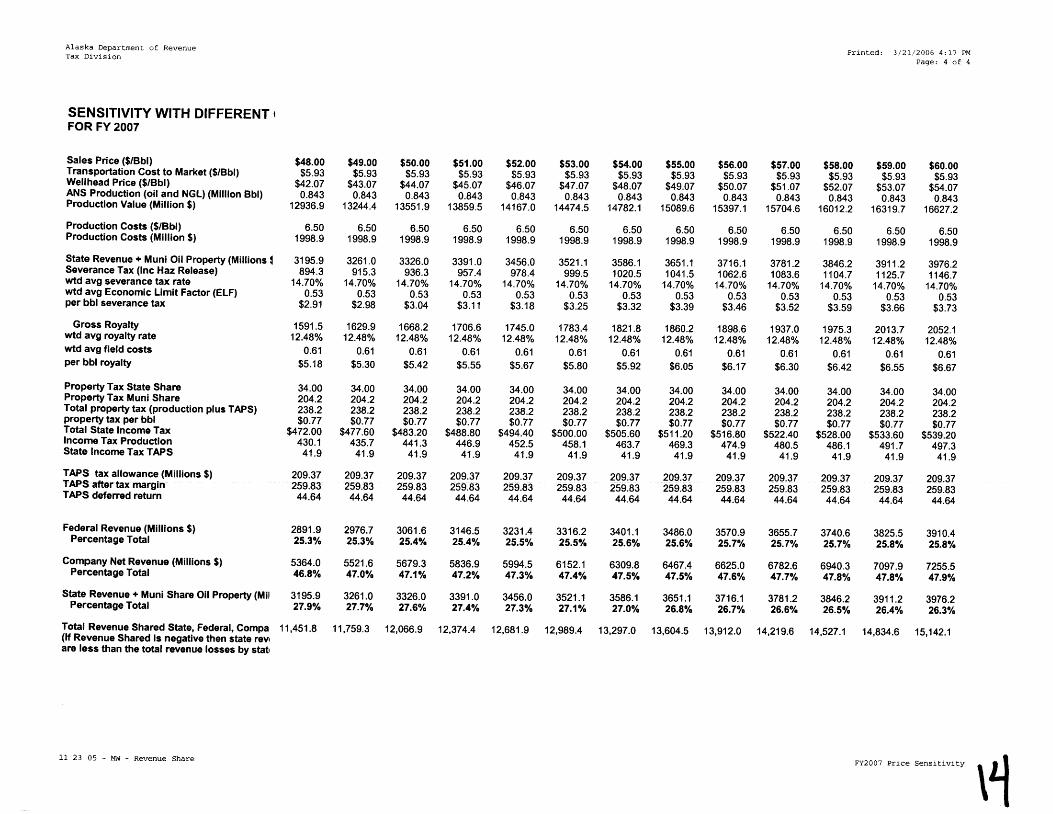

The Department of Revenue has calculated the state and corporate profit share on NorthSlope oil production. According to these figures, FY'05 state oil revenue totaled $3.22billion and estimated company profits totaled $5.25 billion. In FY'04 state revenuetotafed $2.41 billion and company profits were $3.47 billion. In FY'03 state revenuetotaled $2.095 billion and company profits were $2.926 billion. The Dept. of Revenuealso projects that at $59/bbl, company profits for this year wilt exceed $7 billion, while thestate's share will be approximately $4 billion. See attached November, 2005, DORRevenue estimates. (p. 12-14)

A more detailed transcript of consultant testimony (Finniza, Pulliam, Van Meurs, andJohnston) is provided here as well. See attached (p. 1 S-21).

7l

8)

onsultan N A ate PPT

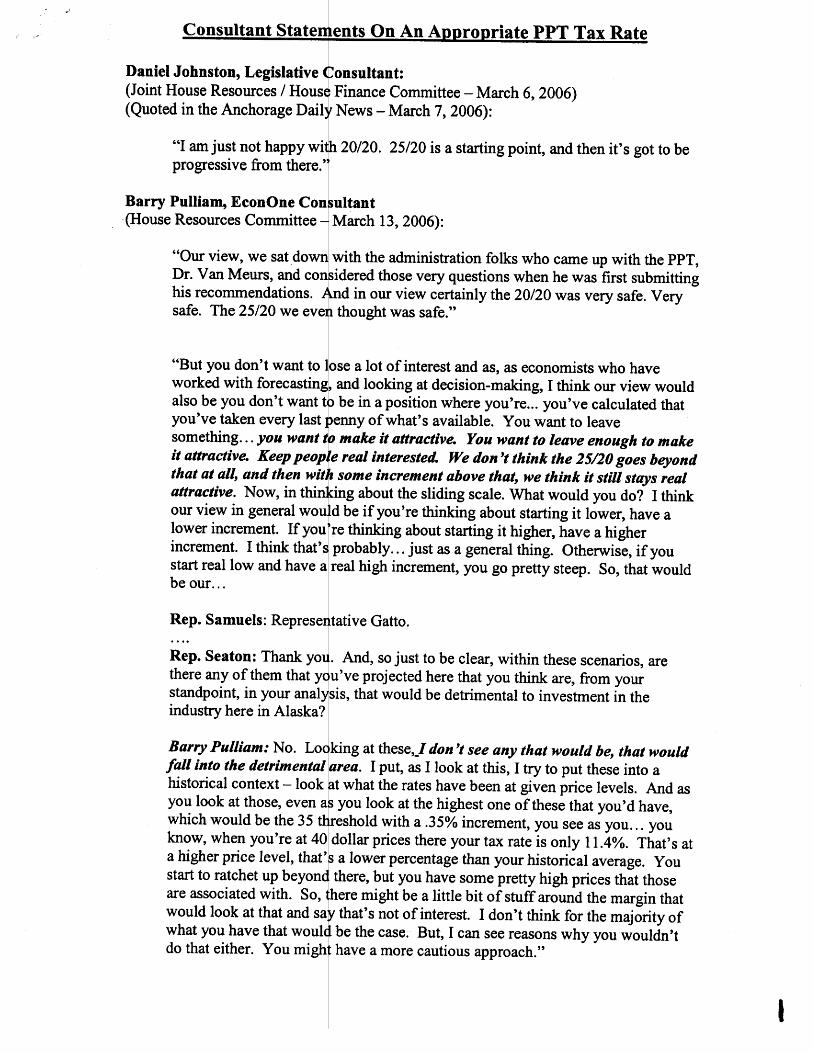

Daniel Johnston, Legislative onsultant:Finance Committee - March 6,2006)News - March 7,2006):

(Joint House Resources / Ho(Quoted in the fuichorage Dail

"I am just not happy 20/20. 25/20 is a starting point, ffid then it's got to beprogressive from there.

Barry Pulliam, EconOne Con Itant(House Resources Committee March 13, 2006):

"Our view, we sat with the administration folks who carne up with the ppr,Dr. Van Meurs, and idered those very questions when he was first submittinghis recommendations. in our view certainly the 20/20 was very safe. Verysafe. T\e 25/20 we thought was safe."

"But you don't want to a lot of interest and as, as economists who haveworked with forecasti

our view in general be if you're thinking about starting it lower, have alower increment. If you re thinking about starting it higher, have a higher

probably. . . just as a general thing. Otherwise, if youreal high increment, |ou go pretty steep. So, that would

increment. I think that'

ive Gatto.

also be you don't wantyou've taken every lastsomething... you wantit uttractive. Keepthat at all, and thenattractive. Now, in thi

start real low and havebe our.. .

would look at that andwhat you have that wo

and looking at decision-making, I think our view wouldbe in a position where you're... you've calculated that

y of what's available. You want to leavemake it attractive. You want to leave enough to makereal interested llte don't think the 25/20 goes beyondsome increment above that, we think it still stays realing about the sliding scale. what would you do? I think

ere might be a little bit of stuff around the margin thatthat's not of interest. I don't think for the majority ofbe the case. But, I can see reasons why you wouldn'thave a more cautious approach."

::o. Samuels: Repres

Rep. Seaton: Thank yo . And, so just to be clear, within these scenarios, areu've projected here that you think are, from yourthere any of them that

standpoint, in your anal is, that would be dekimental to investment in theindustry here in Alaska?

Barry Pulliam.. No. king at these, -I don't see any that would he, that woaldfaU intu the detrimentalhistorical context - look

. I put, as I look at this, I try to put these into awhat the rates have been at given price levels. And as

you look at those, evenwhich would be the 35

you look at the highest one of these that you'd have,

know, when you're atreshold with a .35Yo increment, you see as you... youdollar prices there your tax rate is only ll.4%. That's at

a higher price level, that' a lower percentage than your historical average. youthere, but you have some pretty high prices that thosestart to ratchet up

are associated with. So,

do that either. You migh

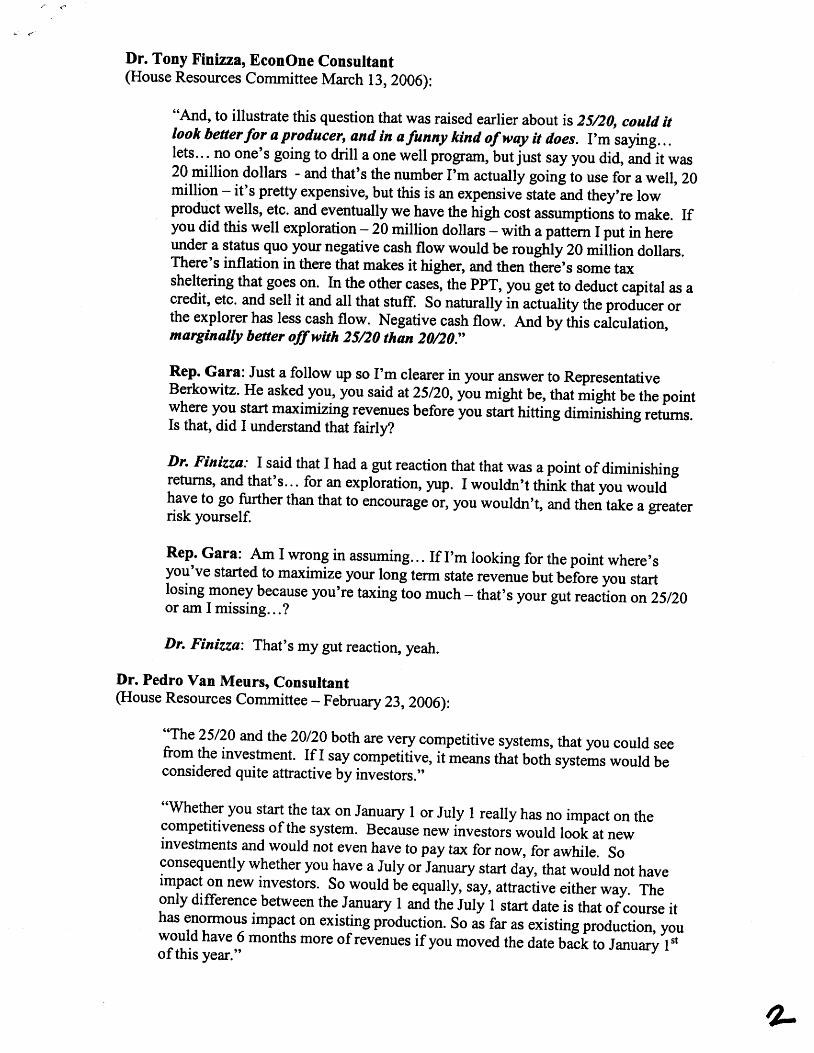

Dr. Tony Finizza, EconOne Consultant(House Resources Committee March 13, 2006):

"And, to illustrate this question that was raised earlier about is 25/20, could itIook better for a producer, and in a funny hind of way it does. I'm saying. . .lets-. - no one's going to drill a one well progrzm, but just say you did, and-it was20 million dollars - and that's the number I'm actually going io up for a well, 20million - it's pretty expensive, but this is an expensivi siate *a tn"y're lowproduct wells, etc. and evenfually we have tfre triglr cost assumptions to make. Ifyou did this well exploration - 20 million dollars - with a pattern I put in hereunder a status quo your negative cash flow would be roughly 21miition dollars.There's inflation in there that makes it higher, and then th"re', some t.,rsheltering that goes on. In the other cases, the PPT, you get to deduct capital as acredit, etc. and sell it and all that stuff. So naturally in "rtoutity the producer orthe explorer has less guth flow. Negative cash flow. And by tiris calculation,marginally better offwith 25/20 than 20/20.-

Rep. Gara: Just a follow up so I'm clearer in your answer to RepresentativeBerkowitz. He asked You, you said at 25/20, 1'ou might be, that titigtrt be the pointwhere you start maximizing revenues before you stan hitting diminishing rrti*r.Is that, did I understand that fairly?

Dn Finizza: I said th.at I had a gut reaction that that was a point of diminishingreturns, and that's... for an exploration, yup. I wouldn't thi-nk that you wouldhave to go further than that to encourage or, you wouldn't, and then take a greaterrisk yourself.

Rep. Gara: Am I *?nq in assuming. . . If I'm looking for the point where,syou've started to marimize your long term state revenue but before you startlosing money because you're taxing ioo much - that's your gut reaction on 25/20or am I missin g. . .?

Dn Finizza: That's my gut reaction, yeah.

Dr. Pedro Van Meurs, Consultant(House Resources committee - February 23,20a6):

"The 25/20 and the 20/20 both are very competitive systems, that you could seefrom the investment. If I say competitive, it'means ttr-at bottr syst#s would beconsidered quite attractive by investors."

"Whether you start the tax on January I or July I really has no impact on thecompetitiveness of the system. Because new investors would look at newinvestments and would not even have to pay tax for now, for awhile. Soconsequently whether you have a July orJanuary start d^y, that would not haveimpact on new investors. So would be equally, say, attractive either way. Theonly difference between the January t ani ilre lufy i start date is that of course ithas enormous impact on existing pioduction. So as far as existing production, youwould have 6 months more of revenues if you moved the date Uact to January lrrof this yefr."

Consultant Daniel Johnston on Average Worldwide Government Take

Joint House Resources / House Finance committeeMarch 6,2006 (2:45 - 2:48 pm)

Rep. Kerttula: That was my last question was... Are you aware of any other country thatallows that dollar for dollar kind of set off for the oil or, I mean, the gas against the oil orany other manner - one against the other like that. That confuses -.1o aiow that.

Daniel Johnston: Through the Chair, Representative Kerttula. I think I understand thequestion. . . dollar-for-dollar credits. . .

Rep. Kerttula: Right.

Daniel Johnston: But you're talking about dollar-for-dollar credits from oil expendituresagainst gas profits?

Rep. Kerttula: Right, or vice-versa, the gas against the oil.

Daniel Johnston: I'm sure that they do exist and specific examples of, you know, whereyou have the2 different types of production and the credits can'ocross the fence" as wesay. Many many countries apply and allow either credits or the cousin to credits that wecall "uplifts" - investment allowances and things like that. But when govemments havedifferent terms for gas as they often do - and quitr often they do - the statistics that Ishowed, and I know there were a lot of those, the world average government take evenright nou' is probably 67 or 70 depending upon how you calculate it. Wood Mackenzieaggregates their statistics a little bit differently too [inaudible] but in the WoodMackenzie world average govemment take statistiofrom theii study was I think 7l%.The world average statistic for gas take is maybe 61 . When you ha-ve a different taxsystem for one versus the other, then you've got problems.

Rep. Kerttula: Thank you.

F u) x d Fi o H F o o tal

F z t! z Fl

Fi X t5 / z U FJ

F o - F F FI z Ft

F 3 b,J e b.)

e z U \J UI

b.)

O Fg F o FE o 0 F 0

el*

I's lsE

E3

SF

3 3

ss

ss

lF

t3

tE

r8

ES

Eg

EE

slF

elgg

lle l

g -lF

|

:slil

l,l;

s lg F

l Ee l

g -lF

lel

gFl$

lel

$nll

1\'

s$

Fs

s3

ss

$$

$$

33

FF

3S

$s

ss

s$

p3

ps

s3

$*

$$

s$

FS

FS

SS

s3

I$

$S

3F

3S

F3

$s

$$

s$

PF

FF

Ss

$$

$F

$$

3p

sF

3s

:|

o}

Nq

r{

ss

*8

sa

F3

SF

33

{(

r(

oc

tt

cr

{*

A*

re

**

FF

SF

33

oo

D{

(r

{8

**

**

S

ls ls ll ls ls ls ll |t

sE

ss

sp

3

s$

*I

$I

s r

!r r r

3 a

E$

s $

s $

I

-e

ss

ss

ss

=3

ss

$I

i v

FF

F3

33

FN

@5

5C

r{

8*

**

tt

3F

F3

3s

a

s$

s$

$$

FF

FF

SS

e

$$

s$

$]

FF

Fs

ss

3

sg

i$

s]

s

PF

FF

FT

G

$$

S$

S*

FE

Fs

ss

A

ss

i$

si

!

-

C - FF

I

g H f! K B1

Fr

l HI $l rl HI

3l

hl

FI

ts. 1

fl

E Ft

(!

-=

p $E H

H=Or -'

F . 'P= 6E o? = .

il-l.ltI ll'l

E H'Pr l;'l

n l r

Eu s E $ * H x $T X b H € T b H- J - - t b 6 - { - { b c !

( n ( h ( n

:o .\ s-tor N l-,\ O \ a \ 3r\ c\ o\

(5 Ln Cn(c -J

!t,( L A o ) C )\o \o \oo - G o _

Crr Cn (-n

I 1r t-l

O ) J S- o o - ao\ o\

Or CF (h

9 F C Ncn N) (,

S ; € ; !

L } L J N\ o { \(rt

'rO b"

)t "-t ;e

(,) Gr t\)5 C ) o )( n € r o

s s s

CjJ.$r ., c.l

cl O --J

S > e ; €

\J

\oo-

cr (t( h

- -

-r ch\o \o

q ( ' ( ' t

.(o I :\(., € (o\c \c \oo\ a\ o\

CN LN CX( c - - J s

c ^ ) r - . Js s s

Ln (n (t| . D C D C )(l) rc Gl\G \-o \oc -

CN LN CN(I:) --J (t

--J (r) --J

-o \o -.oo\ F\ o\

(^t lrt \)A, -r L,

io trr \)q .rq N

(, (^1 t\)

| ' c ) l(, 11]r l\)

S ; e ; e

(, (t N)q t J t J

I $ O ) O

s s s

9n!s

(/)5(D\o6-

U)oFl

o!t

|-rD'F.to

hJOoo\rrlooo(DFUFl

(Du,oFt

g)

o

o

Fl-(D

0aU,F)

Fto

v t

3i':

T7

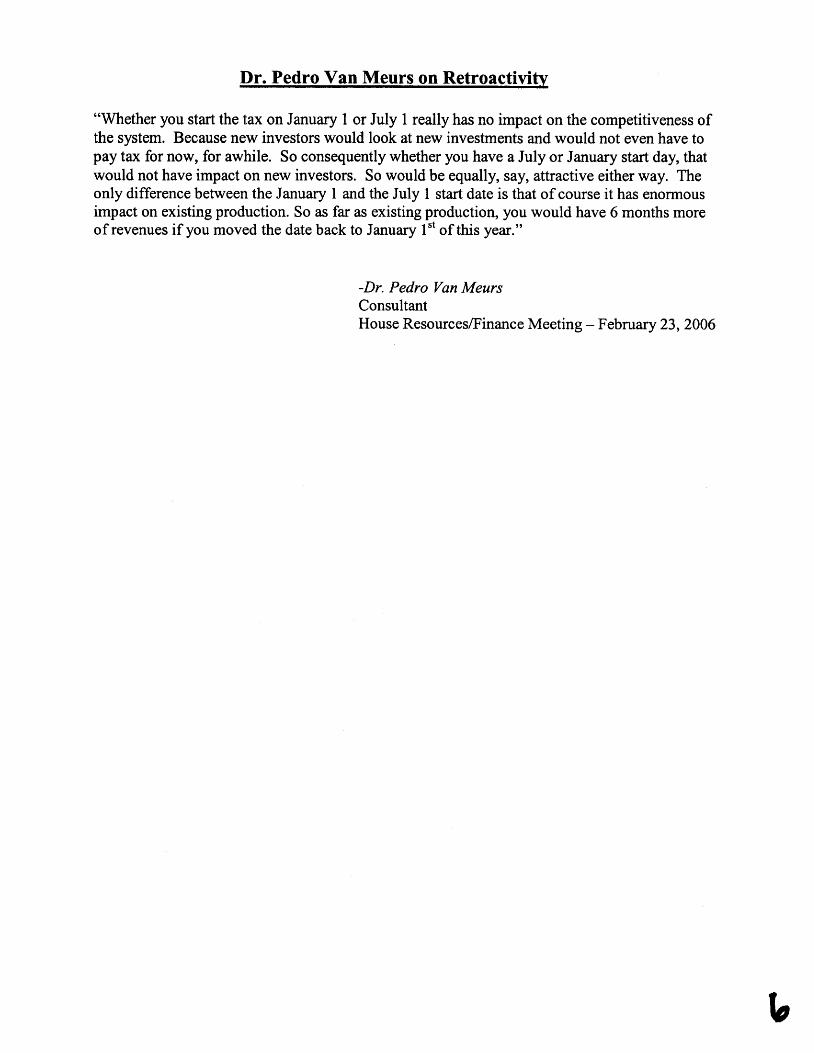

Dr. Pqdfo Van l4eurs on Retroactivitv

"Whether you start the tax on January 1 or July I really has no impact on the competitiveness ofthe system. Because new investors would look at new investments and would not even have topay tax for now, for awhile. So consequently whether you have a July or January start day, thatwould not have impact on new investors. So would be equally, say, attractive either way. Theonly difference between the January I and the July I start date is that of course it has enonnousimpact on existing production. So as far as existing production, you would have 6 months moreof revenues if you moved the date back to January l't of this year."

-Dr. Pedro Van MeursConsultantHouse ResourceslFinance Meeting - February 23,2006

ConsultaFt Daniel Johnston on Separate PPT Tax Rate J'or Leeacv Fields

Representative LeDoux :Well this is probably a little bit of a follow up on Representative Ramras's question but... ifthis were totally up to you. You were elected emperor as far as this thing was concerned, andyour only consideration is: what is going to bring the most money into the state of Alaskaover the next 25 or 30 years and also what is going to facilitate exploration, and your onlypolitical consideration is you don't want to do something to makelhe oil companies pack upand go home. What system would yoa recommend?,

Daniel Johnston:Through the Chair, Representative LeDoux, I'm glad you added that last part to that question. Iwould try as best I could. . . well you'd have to get rid of all the lawyers, br"u.r.. theri's a legalissue... if lcandowhatl'dliketodo, I'dliketojusttreatdifferentirovincesindifferentways,and many countries do. And we see the bigger fields, the older fietis in the lJnited Kingdomthat receive a highertax rate than the smaller, newerfields and stuff like that becausi thqt,reiust so dffirenl So I would stracture the system in such a way th;; we could just really tiutysegregate the dffirent classes of investor, because that would have to be betteiit seems to methan tqring to use that magic 73 dollar number because that is the thing that really makes thedifference.

-Daniel JohnstonLegislative ConsultantJoint House ResourceslFinance Meeting - March 6, zao6

g=g=

sfg

rA

=

{O

{

O

{

{fs

fsrs

.p--

8F

8.F

8O

Or

OO

o6

i\r

ir i,

s$

s

(Eftc

ffvc

Tar

Rab

Poc

cnt)

-.

a

3S

t? =o

E;I

:+G

t!

ob 3 I

$.9

oc

l gs

E ia

TC

'a 8 :t g

E-l

E

C - FF

T

ctI

o F - e !! 3 n It t..) a E o o F'

LJ t o t'd t 6 g d sl F}

H. g 6 t( r{ o E.

F E t g Ft o 6

ultant Daniel Johnston on a Minimum Alternative Tax

Rep. Kelly:Okay, and the, on the safety net. All of the families of curves that everyone shows, onthe progressive system, which I think is a slam dunk that we're going to certainly go forthe progressive system. But those curves, all on the bottom when they come below theELF line are diving for zero like a rock falling. Would you under gird this progressivesystem with either a left-in-place ELF or something else so that that hits a leveing pointbefore it goes right through the bottom.

Daniel Johnston:Through the chair, Representative Kelly. To quote a previous witness, "All the numbersare wrong." You... every one of the runs that people do, it seems, in all the differentanalyses show different crossover points - we talk a lot about crossover. It's my opinionthat with a fair share of the profits, the state of Alaska would be fairly dramaticuttyprotected, but that's not enough of a guarantee" Ifeet that you should druw a line in thesand so that yoa'd never be worse than what ELF woald huve yielded. And, so youmight contemplate something where you calculate the tax in 2 ways - you calculate ELFand you calculate the new PPT, whatever that might be, and take the higher of the 2.That's the way we did it in New Zeolund. That's the way it's done in Newfoundland.There's a few other places - Kazakstan has s calculations.

-Daniel JohnstonLegislative ConsultantJoint House Resources/Finance Meeting - March 6,2006(2:40 - 2:42 p.m.)

t Results of OperationsYears [r.ndedt)ece nr'e r. -j I l l ions of Dollars

Consol idated OperationsLower Total European Ari"

20r)3 "t

)a ies.nanst_ers $3,564 2,464 6,029 3,g72 g7g 225 677 I t,6gl 423103 54s 648 903 t42 g4t 77 2,61t 266 2,g77Other re ienues ( l l ) 93 g2 g 33 3l l0 t64 34-liltal revc-nuesl ( ) [ a | f c v c l l L | c 5 3 , 6 5 6 3 , l 0 2 6 , 7 5 8 4 , 7 8 3 1 , 0 5 4 \ a g �

Prorluc:tiorr costs l�g1- 657 1,449 645 l7S 271 170 2,710 l7gEx'loratior.r expcllses rnrl nrn.rrizrtinn

56 143 199 l2r 5l 94 127 sg2 zDcprcciatiorr, depletion and ar.r-rortizarion 436 S7l 1,00j gS4 163 326 4A 2,490 104l'r 'trpertv irrrpailnrents 65 65 160 S _ 230'lr-irrrsp.rt.t ior cosrs 666 rgg g54 266 40 q0 23 r,zz3 z0()rrre'r'elaterr experlscs 7 7g g5 29 13 gr 44 262 27\ c e f u t r o n 2 5 l g 4 3 S 0 5 l l 2 l l l Z

t,674 t,382 3,056 2,55g 607 zil)r-ovision fbl income raxes sgs 4g6 r,0gl r,srs 2zs s7 36? 3,264 g3l lcsults of operatio's

3]]::::llll',r: . 223 34 2s7 st 3 6R t tal.t ?a1 ,<,\",;; ;; j iil [it] ',ol 'ill 1ii,t&.t ',r.t "r""rtr.

2001Sa les'l'r'a

rr s t'crsOllrer reverrues

$2,997t02(2)

I , t 9 4r , 3 l 5

63

6 , t 7 07 l r s

I04

927 3,924401 503

3 l

400 5.990 | 802,053 62

l 4 9 2 t 2

347 t25235

' 7 a, t

Jiltal re'u,enues[ 'rociuct ion costsHxploration expensesDepreciat ion, deplet ion and amort izat ionProperty inrpairnrents' l ' r 'arrsportat i

on costsOthcr related experlses

3,0e7769l 0 l552

46 8 123

4,428| ,2 t3

209886t 2

76839

) s7 )34367

4804 l

125/ )

367i l832

r05

l 4

8 , r 3 5I,864

s84r,556

53908140

8,389t ,921

584I ,586

5 39 1 6152

25457

30

;t 2

4 t4l r 423126

5t l

354764559

l 0I

1,33 r444r08334

887l 6

3,030r,665

147( r 8 )

3 , 1 7 71 ,617

27t96

t ,441 t 63 98981 t9 49

1 , 3 0 1360

967 334294 66I)r t l is iorr l i r l i rrcorrre taxes

l lcsrrlrs ol' opcr.arions fbr proclucing activities( ) t h c r ' c l l f n i j t g s

673t97

268 941 460l 8 2 t 5 t 0

r ,365 165243 Q4,)

84(2)

49) A *

( r 6 e )(4)

l . -5102 t9E& [' rrcr irrconre (loss) $ 870

I J ( 1 7 3 ) 1 . 7 4 9200 rSl l cs-n .ans t . ! . rs $3 '020 I '178 4 ,198 546 I54 31 321 5 ,2s3 8r ) f l i . . * - . , . . ^ . - . . . . l l g I lg 23g 1 ,039 1 - )1 .1o t l t c ' re 'e r rues ;^

' ;2 LJo r rv rT 1 ,27734 26 60 23_(4) 5 _ 84 r 85' folal reverruet

' f . Ia l revetr t res

\ ' / d t t I

l)r 'rrcl 'crio' c'sts 3'173 l '323 4'496

,.$*:::J;i:ti:i ,21 '23 ',113 'fi :1 j li; iil: 2a t . _ . \ / IL"\ l ' r l r rdtr t ' r r c ' (psl lsss

ar td anrorf izat ior-r 61 69 130 31 3i n l 315Dcpleciation. depletion and anrorrization 531 203 :/34 233 22 4 27 1,020 zJ ' r ( r l )c t ' l ) r r r rpairnrcnts

n TT'r'rrrisp<rrration cosls 726 77 g03 60 3 6 gjzOt l rcrre laredcxpenses 2 5 7 (g) 5 I n Zg z

470 r ,608

1 ,069 641 1,7 t0 t , t27 53 zz2 2 7 _ , 7 1 , 4 9 0R c s u | t s o f < l p e r a t i o n s f b r p r o < l u c i n g a c t i v i t i e s 6 7 7 4 6 8 �

, r , r r ) 1 ,6s6 l

r Rc:sults of operations for producing activi t ies consist of al l theacti ' i t ies "vithin the E&p organization, except for pipel ine and'rarine operatio's. liquefied natural gas operations, a canadianSy'.crude operation, and crucle oil and gas marketing activities,which are i 'c luded in other earnings. Also excluded ar-e non-l:&P lct ivi t ies, inch.rding our Midstream segment, downstreampetroleum and chenrical activities, as well as general corporareadnrinistrative expenses and interest.

r Tralrsfers are valued at prices that approximate market.

r other revenues include gai^s and l.sses from asset sales,including net gains of approximatery $r65 rnii l ion in 2003;certain amounts resurting from the purchase and sare ofhydrocarbons; and other miscellaneous income.

r Production costs consist of costs incurred to operate andmaintain wells and related equipment and faciiities usecl in theproduction of petroleum liquids and natural gas. These cosrsalso include taxes other than income taxes, depreciation ofsupport equipment and administrative expenses related to the

l 0 l

to

o Results of Operations

Years EndedDecember 3l

2005SalesTransfenOther revenues

Consolidated

European AsiaNorth Sea Pacific

Millions of Dollars

MiddleEast

Canada and Africa

Equirv Affiliates

Russia andVenezuela Other Areas-

1,0554ss37

r.,54V,

196

' 3

r,40

3,419

256

1,.6g256

817(5*)

763(37)

Alaska

6,101 4,759 l0,g@,

488 492 980

3,752 2,624,, 900

Lower48

1,724:r..15

TotalU.S.

OtherAreas

5,927 3,395 9,312172, , IaM, 1,379,

2 168 r70

2,795 1,64226,', ;;l l 4 0

5,14222,A1Qs3

1r86

848t86

,2:6 ''139' , , i

. , , . '3 7 9 , ,

,.64.,,,,38

:, : l - , , : . ; :

r2:91I

1,015l l 54g

53? 3l Ir20 66

, . . ' l t , . ' ,

.

443. 848I

665', : 35067 4829, ', , '"19.

2r6' 1 7

106

523

3885

1,095,2

296,2072:

37382

4266

598t 4

,2 t '

423040,

4

Total

19,314425.1

28)

2Ar51,003

ITotal revenuesProduction costs excludingtaxesTaxes other than incometaxesExploration expensesDepreciation, depletion andamortizationProperty impairmentsTransportation costsOther related expensesAccretion.

Provision for income taxes IResults of operations forproducing activitiesOther earningsCumulative effect of

6,376 4,886l 1

7,09d , 2;g:32

6il 274

23#7T

2,341. ' . : : t , , : , : : ,:: ,,.;::.: :'968

669. , , 1 ' , : , :

3,1',4

r,41.3,209

,,.,tiTj14,610

:.rilr.t,.,,, 'i7 .,',,,',:,rlt ,, .,303

7,342.TTf i

t)16$ 759,

43

57

.I

499 r21' '

,,', ,(53.), ,'' . '(6)446 ll5

2,410',,,'l+t

I

s 4,379' t } l

4

1,665, t6v

4,134, ' 156

37.16 42s:8

2,568832

7,86;7,

8s2

640.183

: l

1,0121 8

. 8395742,

1,671 4,224, 584, ,," I',4:12

I,097 2,752, 2 3 , ' ' 1 9 0

l, l l0 2,942

1,575.ji,.s

4,215 1,777l2s;'5 '7r

9 1 0

(78),,35i:

397r22

I

47035932

946953(32

6,

7U

t20 36

: i It44

t6241

566.67'

55

1,074,(10)

,29fi,t,28

: 8

I

1,955',,14i1,

399j1 353'(r2)1 :.r

489$,q

773i59.

148

2555

r , 1 .

45: - :2

42

+

(e7) l , l 87 I,066I 7

2 l

l l 5,,: ',rE69

, a.:,a,;

53.,5 . , .

32' , '.2

3 1 6

'3,3.

r47

717zre

520

46

2W5

861,

154

94

,,839' :

l 4QS:I

accountlNet income

2W4SalesTransfersOther revenuesTotal revenues

Provision for income taxesResults of operations forproducing activitiesOther eamirNet income

Production costs excludingtaxesTaxes other than incometaxes ' lExploration expensesDepreciation, depletion andamortizationProperty impairmentsTransportation costsOther related expensesAccretion

36 )4;503 , 3,364

430 422

267l 0 l

586t 2

74t'432t

2,553888

7,3r582

1,214-

l l 61,330

271, . .

35tt2

17,732'.

2 ,019, l i

,',,,7*3i;697

. , , a : r , , , . , , , , ,

2;71467

,lazt'100:I36..:

704755

J267, l ' ,

43

2I42

24T4

l0

14,956-- 2354t4 t22

275, 3,49147

48. ,(2> 4

' . f ' ' : , , ' . 1 4 7

455tfi

3,348223t

7t5I , l l 5

713

|,192,,'41V:V

t74

328130!.

(r74) 9,5694

(80)t0

4,840, t375

\ t

c, U' { 7 @ c J o z o 'n 2 @ o 9! o @ v m m z c m C

N@ m { € m

^m

u:

z>

1

$fi

za

?n

fio

29

-{

c"

o m 7 ln |. o x o o nt n 2 3 m z { U' z c, { I m c @ 'n m tr,

m n l-

?z

z!

FA

E-

g'

.N

r[

q

o!

o

>>

{>

3

F

=^

=

zz

='

os

lv

o TL

.tl

$d

Ex

*fiE

l:

"$,"

'3

i3s

3 il

b,L

b3

u\t

i,-

, t"

g

6Ia

tr

ol

rr

$A

oI

$$

Hx

Fs

.$

E,

Fi3

s8

EL

:-in

illi

"N

iril

iq

i,

'FA

gS

{

Ao

ri

*dq

;tn

slt

*r

*x

;fi*

B

J-.

s

g.r

l-

'1

'@

i

sd

;NtF

i3*

Fr

$lp

r3 B

io-

-;

iLR

ib

r$

a

'giX

;

'o

H€

srn

se

sn

l:

rn

ss

q

EN

N.

.

'lp

-t

N

o

i

Fs

Hi*

:sn

i $

s S

ep

gt

H

;:$

sr$

sg

; H

r fie

sg

; H

g+

rsF

ai $g

B g

zg

9

;=

qs

i$ $

H

eg

f $ F

EF

q F

fi ;T

F g

AE

$ F

; g

g =

6 e

ss

e:

eB

. * g

ga

* B

g il

5, f

i & t

..

,, ,

$

,!

.,i:

E

= .

*e d

_ s

=

.E H

3 s

s

tsE

ae

$B

l :6

-qe

q

s :

S

Fi

s;.

-3 iY

gf :

F

is

A

5 E

H,E

g

rF

$f

g'l

F

'fi F

"F pc

*H

Fg

q n

+

F F

H

; s

3 s

i s

d s

BF

g$

q

"lF

F

i .5

J

J+

fr a E

e I

E :

rE rB

ill a

HI

E$

i

a3

t

;'

bo

F\

Fb

s

r o

i.,S

b""

- g

a

P

c.

*F

tr

+

3'e

I

f,

r$

r r

tf E

fi i

l

; $

s Fg

$g

:$f;

TF

. F

T

$

E

g.

g

I i

g

N

*r

ie6

sb

:'

i'rs

dt

€i

ts

-c

DN

N_

-N

9

3

i 3

O

E

H

S

IB

N

S

",

NF

F

B

i i

x 5

r s

-t sH

lnH

$$

$$

$$

Hd

e

+

# F

i

s'$

pi

is o

HF

5

3

E

; 3

s;

$i

sx

nlQ

iE

Ei'

g

i

:E =

H rH

ut

*uH

3

3 s

3 s

S s

; li

l]

-{

NO

tr

tv

i 3

5 t

t

Ns

*E

Fa

f

N

bri

$

5i

g)(

jJ@

or

3q

co

$

rr

S'c

o

iri"

N

J

(r

)O

rN

)N

-u x

s s

N u

s *

HF

fi g

fi s

d s

J

sB

H

AN

N)

-l

:u8

sr$

fis

g

$*

iafi

ss

HL

ilio

;;b

.dL

rb

.,

\t

-q

\S.,

, s

'

rt

\)

N)

@1

a$

Hs

*H

fi$

3

'$*

Sa

Ss

E

Hb

or

Db

;i

l-

N-

,'-

r

g

aE

;S

f

l

r.

)r

\r

di

-

O)

s.

.

-t

^-

r.

x

sld

Is$

;sx

H*

FA

FrE

H.,

)(

oN

iui'

oB

-c

r,

[3

XiS

gI

sr

tt- f

o 6 { v o c I o 2 o 'n z an I F o @ v m m z c m U'

@ m { € m^

nt

xz

=J

$ft

za

€z

fr

oz

o-

{c

D(

) m 7 sn r 6 x o o m v z = nr z { U' z 0 { T m c 6 'n m o m n

lz

z!

i t

i

3 gtr

:t T

rziz

iil

r83

i33

ed

;E

e9

3€

F E

59

88

8s

;t

i

isiii

tiflF

Fss

FiIi

!rR

:a8

!8f *

; 3

r!A

e E

'$ F r $g iiE

E' E

EE

Ei

#;

*ec

=

Fg

Q=

$

5S

FA

3g

eo

3r

av

o 3

**e

rrq

tsI

xa

;eA

gs

;

NN

{i

I:$

rx$

$fc

iu

rti

gF

€N

t\

t{

i

frif

*n*E

$x

x

t H

giE

; B'

-r

('

li

ds

rEq

*€d

$

eq

r$q

S$

F

-r

o)

i-

,-

3'-

r,

.-

dp

IS

d

.

g-

3q

"3

A

e]

r,

!v

BS

Fp

NF

F

ry

F

c,

,i9

o,

t

o\-

bD

5;i

lb'A

rn

\ '.

S

i"il

gB

l s

t

--

N-

Or

j

ss

$s

s*x

H$

;a

Fg

8g

t Br

ur

$@

t

da

sH

*F

:S$

H

, 3

;3a

i E

rg

b"

;ilr

S:^

a,

a;

61

5S

SS

o

--

:J

u1

.,

AI

ss

$H

nH

BH

H

H,"

3if

fas

EL

nb

,-

UU

bS

6d

b

og

tl,

€g

ag

I

Fg

ft

$a

gg

frfl

E$

uE

g

s z

$$

$g

,Flf

iig

gs

93

gB

:5

E 6

' il

F$

id ;E

a H

s:i

i f,

g qF

5 s

dP

!' i

x

;5

g B

$

a#

g

fl

ds

d i

I, I

.o

, N

N

A

o

,ti

?

a=

3_

1 d *

=

\

Hi

rE

N5

ss

$6

=-

s,

qE

9g

:

f

Sf

ti

$t

t*

;r:

F i

s 1

g E

f€ 3

F

f, $

n g

"$

s'i

oi

^,.r

?u

Fg

4 e

iF

g'

!: t

$n

$*

SS

$ig

E$

F H

tB

3t*

;

Ei

fi

f d

Fe

FiH

px

nH

s;

se

iiH

:-

Bs

;s

ss

st

si

#f

FE

g

a

$.

f .@

r$

..

, re

s

Fr E

I i

$ *

fr€

$* F

s tu

n+

* $

t

g

; c

$S

q

i *

d

-l o

f *f

f n

"i s

a$

*f

p

3

e

*

i S

F i

F

[d

fu-.

X

g

i 3

4

(

"

sN

S

o

sr

s

i"f

;E

ds

ig

g

i

fr

f,

3

.,f

of

,.,-

i n

o

V

E

i g

{

f$ B

H H

$ H

$*

$

ft

H

* i,

i $

:n, F

b

S\

l.;5

Hd

F!

'�

.3

g

r g

F

l $

R sH

p"d

xs

H=

;

f;

B

; s

r $

5 s

i ti

gd

+3

g

I i

-q

.-l

-1.,

--

o

)s

H

il$

i$g

ltr

r$

-t? \ts

0o

c{

6

C

PF

0n

do

i€3

5;+

Sig

iEll

*=

$.

39

f;

$H

*o

55

=s

-$

d

I=

eE

P"

3

Ct

:

tc

l<

i#ii

qil

:,3

4g

rsiE

E*=

*"E

Fq

gg

igii

i ii

igE

s=

E

=

s6

=@

O

+

O^

fr*$

ai a

$ d+

gEi lH

; liit

- B B* [+

[fl i*

iEE

l= = =

arL

oH

. p

. E

EE

u

tr F

g =

:iH

ss

$tr

tr

il*F

?s

sg

*-i

=

i3

ib e

; !,

;

qfl

€\'

-q

d

s

.fi

g$

J

3

t c

ee

E

Q

rg

[a E

*

s E

ls

fr

'<d

e

€

cn

q

g

2

fig

i E

'L

=

f

l '+ r

q3

rH

l u

H

+d

H

-*S

laN

Dp

qp

o

^F

a

cr-

i*3

d

$

oB

*E

3 il

s sH

n;

Fg

E

;qg

5$

sa

:a

*; u

as

sg

g

g gE

tgg

cD

:€

ilr

Sb

N u B € o o o (a o ry o

@N

N

6

A

+6

tr

+F

@N

liq

p

f€-

f:-

ta

-lo

8

d

8o

B*

8f

@@

a

+@

o<

rre

s

crl

o

+o

<

^to

:66

_

6o

r <

r,X

<rr

a,i

fR

Er d

8e

lSts

ag

Sg

rF

Fi-

fE

3$

as

Eq

rr

r$r$

5

+ri

€

+6

€N

Nq

e

s"

P

i t"

- i

-H

6

ioK

ta8

A(o

(o

s(r

]so

r+:9

5

('|

o

{\s

d

.jo

riQ

r 6

or

orI

S6

iij

RE

q d

tslS

Ss

qs

Sg

b*

Ffg

fE

iS

{sE

Nr'

l E

r

a

A

+q

Itr

sS

raN

Diq

e

s"

P

i tr

- l

.E

d

tof*

fi5

(o(o

s

oro

oG

)ol\

(J

r o

sq

i <

.ro

:6N

j _

6o

r :;

!tf

ah

or

iP

b\P

lb

bb

,gg

ij

rn

gF

=

FL

; -

Ao

(o

oA

o)\

| (o

Jo

NN

Ne

o

r;

<a

i)

di;

XL

nr

irc

6

<.n

<,r

i66

5g

$ H

H IR

It

FH

H *a

$e

uu

r s -

fQ a

-I=

H E

- 4

:ffa

Er

$3

S3

S3

s

rq ;

1E

iS5

s S

ES

r EE

SIn

r5 [

$q

EH

in

,,

-os

p!*

rX

p

ld

^r.

,r_

$

.,i

$U

e

e F

:A

d

d.'

g*g

I F

S

IE

qfi

F

SF

+

E8

8N

Bf

8o

q-

o)o

)rrg

: (o

o,

a;-

(^,o

r(o

5 s

i s

d s

s

RB

r tie

rs*s

s{s

3 H

ER

$i xE

ts{b

Ed

@r

A

n **

in p

F t$

8 :*

gi$

sa

E

a*$

s

a$

{d

ss

tsii

lE

e-i

l i$ I

$ H

H F

FH

r*S

pH

FF

F

= S

* p=

Ss

$

€*

$s

ErF

; $

a S

; S

i e

F{

d{e

.{*5

8 sI$

g

sIS

t:

6s

f,&

q8

rF

@"E

Xfi

l$ F

A F

HH

or*

iFu

ps

a

"*d

a--

{s€

d-

$:F

aE

6 s

B s

s s

; s

*t d

iEii

rsE

s

{Ffi

F5

F*B

H

s ;$

QH

E

@

*H

H

-^

Hp

N?

Nq

p

*^

Fa

u

"_

iaH

d

IoK

*B

s@

(o

$o

)<lt

oG

)os

(n

o

Atu

c

.ro

:N6

6

o:

*6

FF

FR

tsq

dte

\SS

s s

E$

d s

ilR

3l

BE

iS

qs

ra

+H

H

^ A

q?

NN

qp

* _

$a

e

F

aa

.o

E

of*

ga

(o

(o

s

or

Ao

G)

os

o

o

s

6

aD

o:J

E6

_

6o

r

F;F

f;ir

iR

E$

dS

slS

Ss

ae

SS

ail

S;r

Es

SS

ss

r@

A

rH

H

-"

IaN

Na

*

-$

6

*-

iaq

-

S

o8

.'8

f (o

@

5:.

loo

qr)

95

s

r o

+

<o

<

^io

*.t

6 j

6

or

Fil

{ ;a

E\*

59

iu$

H S

ilS

xi E

E i$

Qil

g6

r

tHH

,s$

BB

BB

e -

F$

o^

$a

s d

^ $

pa

*EF

H{ ;s

Es

sS

B

EE

$3

fi

fi$

fr3

E

g S

$A

$d

T n o * N

rEt

N

0r

or

qo

Oo

*P

EJ

N E 5 o <n

o o f P' rr

N F N

H S

$ H

Ha

5

A

Nq

' 5

0'

+

Sb

S

io

Si.

n

i E N

H ig

F$

cto

) a

rs

(Jtr

(o

.�b

S

Lt'

S

b

N ii !

$ s

3 F

8-

r

a

|N

o

to

)5

S

:'

iQr

Si.

r

d u N

$ ig

Ft

a

>q

i b

qb

o

S:-

G) p d

H s

S u

$I

GO

j (n

{ o

)o,

c'r

b

sr

Sb

S

b

d .: F

3 S

ft.d

q:_

- {o

) c

D(,

t {o

o

iQ:-

:€

b

Sio

i ;X H

S 3

3 F

Hi

cD

d

{N

{

('1

(')

Si\

r S

b,

S\

J--D

F-

The transcript that follows includes the excerpted statements on the preceding pages, on(Q more complete transcription of the testimony before and after those excerptedstatements.

House Resources Committee - March 13, 2006

(l I:03 a.m.)Tony Finizza: And, to illustrate this question that was raised earlier about is 25120, could it loofor a producer, and in a funny kind of way it does. Itm sayi[g... lets... no onets going to drilt:program, but just say you did, and it was 20 million dollars - and that's the number I'm actuause for a well, 20 million - it's pretty expensive, but this is an expensive state and they're low pwells, etc. and eventually we have the high cost assumptions to make. If you did this well explrmillion dollars - with a pattern I put in here under a status quo your negative cash flow would20 million dollars. There's inflation in there that makes it higher, and then there's some tax shthat goes on. In the other cases, the PPT, you get to deduct capital as a credit, etc. and sell it arstuff. So naturally in actuality the producer or the explorer has less cash flow. Negative cash Iby this calculation, marginally better off with 25120 than 20120.

Rep. Samuels: Representative Berkowitz.

Rep. Berkowitz: Two questions with that. First of all could you walk us through those numbers, hrthere, just so I make sure I understand it, and secondly did you analyze at different rates than 20120,you do 30120, or anything in the spread between?

Tony Finizza: Through the Chair, Representative Berkowitz, I personally didn't do anything but thrcases. They could be done ffid, we didn't think that was the boundaries we were allowed, we were pthose possibilities. This is just to, the most likely PPTs that were being contemplated, I think is whaI looked at it. So, if in this, the way this is calculated by, first of all you have to imagine the pattern rwhich I unfortunately haven't a picture of it. You put in the exploration capital over this time periodit's like that picture I showed earlier. Like this. It's something like that, 1lou put in...so the cterc.rr,near the end of the 4 year period. You, in the 4'h year, and then you take off oi that, the. . . and you cathe capital expenditures being made, and then there's atax credit for those expenditures being given.those all alter the cash flow there.

Rep. Samuels: Representative Gara.

Rep. Gara: Thank you. Doctor, just going from 20120 to 25120, and showing a slightly better cashexplorer at25120, can we assume if we went to 30120 or what Johnston recommended - 25120 and th,a higher price, that the cash flow result would be maybe similar to 25/20 or.

Tony Finizzaz Yes, what's working here is the factthatyou're actually giving allowing capex expenbe in a sense deducted, someone else is helping pay for it, rather than in the status quo. So the higherate, you actually can shelter more of those expenditures. Now, the idea is not that this would be theproject, that this would bear fruit and you'd have with some probability development capital and pro,program' so you actually would find out if you looked at a total program that this pattern might not p

Rep. samuels: I'm assuming that 100 would create a problem?

Tony Finizza: I'm sorry?

Rep. samuels: I'm assuming that 100 would create a problem.

l5

Tony Finizza: 100 and any credit would be a problem probably.

(1 1:II a.m.)

Rep. Ramras: Representative Seaton?

Rep' Seaton: Yeah, trying to comprehend this. Is the factor that exploration is a negative loss all themean, you're never going to make money on exploration. When you're going to make money is if ycsomething, and then you go into productiont. So if you want to stimulate exploration, exploration is rgoing to be a negative cash flow, so the mofe you subsidize that from the state, the more positive beris. Although taxes aren't going to be paid until something gets into the development stage. Is that bawhat we're talking about?

Tony Finizza: That's pretty accurate, yos.

Rep. Berkowitz: Mr. Chairman?

Rep. Ramras: Representative Berkowitz.

Rep. Berkowitz: Thank you very much. On that point then, where is it . . .. You've already establish100% tax rate is not effective. But at what point have we reached diminishing returns? Is it at 25,isit at 35? Where is that point?

Tony Finizza: Through the Chair, Representative Berkowitz. I. . . that is the question, what are dimirreturns. I...honestly, we don't think that any of these schemes, these programs would be onerous, buyou have to... personally I would say is yorl have to err on the side of making sure you're not oneroucan't go too far here. I think this might becpme a little more clearer when we put the whole programrather than just the complete loss phase. And what you put in here has to be for other parts of the systwell.

Rep. Berkowitz:I understand, but if we're seeking that point that's, we need to know where diminisreturns is before we determine whether its Onerous. And it seems to me, knowing where diminishingexists is a number that we ought to have.

Tony Finizza: Representative Berkowitz,that is the 24 dollar, 64 dollar question. I don't think anyocan answer that. There is no diminishing returns - no analysis that can be done in my opinion.

Rep. Berkowitz: But you could run a3\/2Qnumber, you could run a35135 number, and we'd be ablcompare based on this hypothetical.

Tony Finizna: I think this is what you'd be missing, and I think this might be clearer when we put tlthing together. If you encourage too much exploration, you subsidize too much exploration, it may reconomic. You'd be losing money. The state bears a risk here too. If you encourage more exploratirprices don't warrant that as commercial exploration, you would be, you would have wasted --on.y.the measure we're trying to do here, it's not how much exploration you're gonna get but how muchcommercially economic exploration and I don't think I can help on that answer. I think it's more, buI think the diminishing returns probably Br€r.. If I had a gut feel on this, I can't do it analytically, I tftprobably at it with this 25120. I think it might be there, but that's gut feel.

Rep. Samuels: Representative Crawford, Kerttula and then Gatto.

rb

Rep. Crawford: Thank you Mr. Chairman. My question for you is way more basic. And that's the egoing to a profits based tax. It seems to me that when you change from a production based tax to a ptax that you're leaving it open to manipulation of what a profit is, and what your opinion of what, yorthis a right thing to do, to go to a profits based tax rather than a severance tax based on production.

(I I :17 a.m.)Rep. Samuels: Representative Kerttula.

Rep. Kerttula: I'm not sure I'm going to be even able to understand it, but I wanted to ask the quesback to the 25120 or higher, is it because you're going to be able to get the deduction from the creditrhigher number. Is that what it is?

Tony Finizzaz Yup.

Rep. Kerttula: What if you went then, to 35/30. What if you're giving even more deductions and ciwouldn't that also commensurately make it so that the higher tax rate was acceptable?

Tony Finuza: Well, the arithmetic would show that in this particular example. The question is theryou be willing, as a state, to run the risk of running a big loss at that level. In a failed exploration prrthink when I put this together, it might be clear, and we may not get to that tlpe of clarity, but I'll tr1

Rep. Samuels: We'll try to keep moving on here because you might get to answer some of these qurRepresentative Gatto.

Rep. Gatto: I'll pass.

Rep. Samuels: Thank you. Representative Gara.

Rep. Gara: Thank you. Just a follow up so I'm clearer in your answer to Representative Berkoasked You, you said at 25120, You might be, that might be the point where you start maximizingbefore you start hitting diminishing returns. Is that, did I understand that fairly?

Tony Finizza: I said that I had a gut reaction that that was a point of diminishing returns, andfor an explorationo yup. I wouldnot think that you would have to go further than that to encou.you wouldnot, and then take a greater risk yourself.

Rep. Gara: Am I wrong in assuming... ff f'm looking for the point where's you've started to nyour long term state revenue but before you start losing money because you're taxing too muclyour gut reaction on 25120 or am I missing?

Tony Finizza: That's my gut reaction, yeah.

Rep. Gara: Thank you.

(1 2:5 5 p.m.)Rep. Samuels: Representative Ramras.

Rep. Ramras: Thank you Mr. Chairman. Let me back it offjust a little bit from, in, [indiscernible] rchart. Somewhere between... your suggestion is that at 20120 and at 25/20 you don't disturb industrevaluation of whether investment in Alaska is economic or not. And, that was at the beginning whenthe models were at a 30 dollar stress price, 40 dollar base price... I asked you about 50, you said wel

l7

model's not necessarily symmetric in that way and that it's against that forecasters have been burnerSo we're.... What this suggests is that if you clear the hurdle of the economic decisions of industry-a25 million barrel or a 500 million barrel field are economic or not - if you clear that hurdle, then ifthis progressivity, whether it's .2, or .25 or .3 or .35, then you're sharing in the windfall profits afteryou have kinda cleared the space of where the oil companies in their board rooms are making their dwhether or not it's economic to invest in Alaska.

Barry Pulliam: Yeah, I mean, you're doing... any tax system you put into place they will evaluate 'that in mind. Having something like this, is a different one they would have to evaluate. But what itthat they would know, at lower levels, whatever level below this threshold you put in here, whether40 or 45, whatever, that the rate would be... there would be no increase in the marginal rate.

Rep. Ramras: Alright , again, an IRA. If any of us at this table had an IRA, , our retirement, that wrto project... You know they say that atage 20 you can be aggressive and go all in stocks. And atagmix of stocks and bonds and at age 60, you better be real careful with your nest egg because you gotout" So if we're selecting a place on this spectrum of prices per barrel and this is our nest egg,we cejeopardizeitatall. The whole point of PPT is to incentivize exploration and more investment dollarAlaska to keep the pipe full. Where along that spectrum are we safe? 30 as a stress price? 40 as a baSomeofyourmodelswentashighas45. What 'sthesafenumberwherewe'rebehavingl ike a60yprotecting the nest egg of their IRA. Where's that number along the spectrum?

Barry Pulliam: Our view, we sat down with the administration folks who came up with the PPMeurs, and considered those very questions when he was first submitting his recommendationourview certainly the 20120 was very safe. Very safe. The 25120 we even thoughtwas safe.

Rep. Ramras: I'm solry, Mr. Chair, I meant a price per barrel of oil, for economics...

Barry Pulliam: Oh, I'm sorry...

Rep. Ramras: ...not the tax program, but the price per barrel of oil. 30 as a stress, 40 as a base, whclear the hurdle on the other side where we're inside of all the board room projections, along theirbe

Barry Pulliam: Well, I think in that 35-40 range, is about right. But, you also need, I think, to.... I :a long term average, within that you're going to have prices lower, and prices higher. So, the notionkind of system that people have talked about, the progressivity, is that when prices are higher, you slAnd when they're lower you share in that as well. So, I think as far as an average, what people 3ro, rFtnrzza has indicated, that people are looking at today, to make this investment decisionJ - jS-+0, thhurdle for investment decisions. Now, do they think that that's... they're hoping for some upside, rilthat's one of the reasons they do it. As part of that analysis, they're looking at the upside. They ma1that the upside's there with I00% certainty and certainly they, it's... they discount it... but they makthere is a potential for upside, there is a pretty good chance they think at 40I'm going to do well on tdown at 30 I'm not going to lose my shirt. But boy I'd sure like that upside. We all would like the uthat's what we're talking about here. And how do you balance that between the state getting apart oland investors getting apart of the upside? And, it's a, it is abalance, if you make it too steep, ihen irwill look atthat, they'll plug that into their formulas, and they'll say, okay, what am I going to wantaway with... if oil goes to $80 dollars a barrel. Because that's part of my decision *ukitrg, and therechance it's going to go to 80 - what's it going to look like for me? Well, if you're goinglo take everaway from me abov e 40 dollars a barrel, you're not that attractive. If you're going to take a little bitfrom me as price goes up... that's okay. That's pretty consistent with what happens around the worl,take too much away from me, you get less attractive. So, it's striking that balance, and again, if youin light of the work that was done by Dr. Van Meurs and our review of it, we certainly thought that tlwould not result in rates, in tax rates or government take that would be discouraging at price levels tt

t0

might see, and even as you get on the upsimuch of the upside. And, consistent withtaking away... having a higher incrementtoo high. I would say, and then [indiscerniFrnrzza and I are not fiscal system papproach this with a... approach it cautiothat's the key. You are out there as a statevalue of this resource for the state ofhigh enough to keep people interestedof interest may not be bad, depending on winterest and as, as economists who haveour view would also be vou don't want ttaken every last penny of what's availablattractive. You want to leave enough tothe 25120 goes beyond that at all, and theattractive. Now, in thinking about the slwould be if you're thinking about startinstarting it higher, have a higher increif you start real low and have a real high

Rep. Samuels: Representative Gatto.

Rep. Gatto: Just looking at the maximum80, 100, let's just say... Does your chartdollar?

Barry Pulliam: Our charts stop at 80, the

Rep. Gatto: I'm looking for your suggesti

Barry Pulliam: Yes.

Rep. Gatto: Or did you mean it to say, be

Barry Pulliam: Extend it like this... youit, and say we're just not gonna. . . we couldprices, that's you're looking, if you have 8a barrel so... it's a... this allows for some p

Rep. Samuels: Representative Seaton.

Rep. Seaton: Thank you. Ando so just toyou've projected here that you think are,detrimental to investment in the industrv

Barry Pulliam: No. Looking at theseo I darea. I puto as I look at this, I try to put tat given price levels. And as you look athave, which would be the 35 threshold wiat 40 dollar prices there your tax rate ispercentage than your historical average.high prices that those are associated with so, there might be a little bit of stuff around the margin that

lq

certainly wouldn't be discouraging. You're not taking away toohat Mr. Johnston has said, even as you get into the very high prices,that, is not going to be discouraging either. Just don't wanna get

le] in general to the extent, again, and give a big caveat here, Dr.and as you've heard from some, we are mere economists and so,y. Higher taxes, in general, are... you have to find the balance,

ing to... your goal, I think, is and should be, to maximize the. And that involves finding a balance between having arate that isnot so high that you start to lose a lot of interest. Losing a little bit

the total revenue pie is... But you don't want to lose a lot ofked with forecasting, and looking at decision-making, I think

be in a position where you're... youtve calculated that you'veYou want to leave something... you want to make itke it attractive. Keep people real interested. We don't think

with some increment above that, we think it still stays realing scale. What would you do? I think our view in generalit lower, have a lower increment. If you're thinking about

t. I think that's probably... just as a general thing. Otherwise,crement, you go pretty steep. So, that would be our...

rices you have here... If we explode this view and sayoil is aboveially stop at 80 and say we no longer incrementalitize (sic) at x

lculations can easily be extended beyond 80...

Because these are your charts. Did you mean it to stop at 80?

80, count every 5 dollars and extend it. ..

ght... you know, there could become a level where you would capave some cap out there. But at over 80 dollars here, these are real

dollars real prices, you know, out 20 years, you're over 100 dollarshealthy pricing in here.

clear, within these scenarios, are there any of them thatfrom your standpointo in your analysis , that would behere in Alaska?

't see any that would be, that would fall into the detrimentalese into a historical context - look at what the rates have beenose, even as you look at the highest one of these that youod

a .35o/o increment, you see as you... you know, when youtrely ll.4o/o. That's at a higher price levelo that's a lowerou start to ratchet up beyond there, but you have some pretty

would look atthat and say that's not of interest. I don't think for the majorify of what you halwould be the case. But, I can see reasons why you wouldn't do that either. You might have a ncautious approach.

(1 : I0 p.m.)Barry Pulliam: If I could answer, Chairman Ramras, also... the... we are assuming here that, as witsystems, you try and anticipate the future, and tailor your system as best you can. But if the future tube different than what you expect, you can alter it. And should alter it to make sure you strike the rigIf you told me, however, that I cannot change this tax in the future, this decision is one that I have tofor a long time, then... or, at least this is one.. . this is taxes. Once you make a decision you're not grable to raise them. You may be able to lower them, but if you're constrained against raising them, I tshould enter into your calculation of where along this you go to the less aggressive end or the more aend. If you can't raise them realistically in the future. . . if you find out that you were wrong, then yobetter off to have. . . to be on the more aggressive side, knowing that you could come back and lowerthat's not a constraint, then if you've been too conservative at the outset, you can revisit it and look ait again. But I am mindful of the fact that just as a... it is hard as legislators, I know, to raise taxes. lto lower them than it is to raise them.

House Resources Committee - February 23, 2006

(2: 10 p.m.)Rep. Gara: I want to assess the difference between the 25 percent tax plan that you had presented tome and others, and the 20 percent tax plan that is before us now. Two of the main differences wasthe 20 percent creditl}S percent tax and the other was the effective date of January 1". And when wrspoke, you said with those provisions, with the25120 and Jan 1't effective date that would put us in astrong position competitively and provide a fair return to the state. With a Jan I't effective date doyou still think that that would be a fair assumption with the 25120 plan, in your mind?

Dr. Pedro Van Meurs: The 25120 and the 20120 both are very competitive systems, that youcould see from the investment. If I say competitive, it means that both systems would beconsidered quite attractive by investors. Consequently that is an important factor. What is ofcourse the concept is when would the tax actually start. Obviously an early start date, a retroactivestart date starting in January . . ... would be an extra year of income for the state. T1,pically aroundthe world, taxes start after they have been approved, but sometimes you can backdate them. Thecurrent law kind of contemplates that it starts on the first of July, so consequently that is what the bilcontains.

Rep. Gara: When we discussed it last week or the week before, I think your position was that theJanuary. I start date wouldn't really impact the competitiveness. Still be appropriate from thecompetitiveness and revenue standpoint. Is that still a fair assumption if we decided to go back andamend the bill to go back to that [to the Jan I't start date]

Dr. Pedro Van Meurs: That is absolutely true. Whether you start the tax on Jan I or Juty Ireally has no impact on the competitiveness of the system. Because new investors would lookat new investments and would not even have to pay tax for now, for awhile. So consequentlywhether you have a July or Jan start d"y, that would not have impact on new investors. Sowould be equally, say, attractive either way. The only difference between the Jan 1 and theJuly I start date is that of course it has enormous impact on existing production. So as far asexisting production, you would have 6 months more of revenues if you moved the date back toJan l't of this year.

LO

Joint House Resources / House Finance Committee - March 6, 2006(2:45 - 2:48 pm)

Rep. Kerttula: If we can allow incentives, and we've got aUS Supreme Court case right now, sothat's going to be a good question. But if we can. .. are allowed to break them apart, then your

recommendation is that we break apart the legacy versus the newer fields that we want toincentivize?

Daniel Johnston: Through the Chair, Representative Kerttula. Yes, that's got its problems too, nodoubt about that. But in my mind at least, I've got a lot of experience and a lot of comfort withcountries that do things that way. Quiet a few. And Pakistan has onshore terms, and then they haveto pay Pakistan 1, Pakist an 2 and Pakistan 3 terms for different types of areas. Algeria has Zono A,Zone B and Zone C as I recall. And then you have offshore terms and you have onshore terms andsome countries have some special and different terms for gas than for oil. That's what I'mcomfortable with and that's what I've seen.

Rep. Kerttula: That was my last question \ryas... Are you aware of any other country thatallows that dollar for dollar kind of set off for the oil or, I mean, the gas against the oil or anyother manner - one against the other like that. That confuses me to allow that.

Daniel Johnston: Through the Chair, Representative Kerttula. I think I understand thequestion... dollar-for-dollar credits...

Rep. Kerttula: Right.

Daniel Johnston: But you're talking about dollar-for-dollar credits from oil expendituresagainst gas profits?

Rep. Kerttula: Righto or vice-versa, the gas against the oil.

Daniel Johnston: Iom sure that they do exist and specific examples of, you know, where youhave the 2 different types of production and the credits can oocross the fence" as we say. Manymany countries apply and allow either credits or the cousin to credits that we call "uplifts" -

investment allowances and things like that. But when governments have different terms forgas as they often do - and quite often they do - the statistics that I showed, and I know therewere a lot of those, the world average government take even right now is probably 67 or 70depending upon how you calculate it. Wood Mackenzie aggregates their statistics a little bitdifferently too [inaudible] but in the Wood Mackenzie world average government take statistirfrom their study was I think 7lo . The world average statistic for gas take is maybe 6L. Wheryou have a different tax system for one versus the other, then youtve got problems.

Rep. Kerttula: Thank you.

L I